Verena Otter

Verena Otter Douglas M. Robinson

Douglas M. Robinson

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Sustain. Food Syst., 18 December 2024

Sec. Agricultural and Food Economics

Volume 8 - 2024 | https://doi.org/10.3389/fsufs.2024.1449684

This article is part of the Research TopicStrategies Of Digitalization And Sustainability In Agrifood Value ChainsView all 23 articles

Society and policy demand greater sustainability of food systems, driving practitioners to improve the transparency of supply chain networks through digital innovation. Uncertainties regarding the structuring of relationships with primary and secondary stakeholders for sharing intangible data and information diminishes the potential for exploitation of digital transparency. While businesses are accustomed to organizing efficient flows of tangible goods, management research integrating digital transparency considerations to investigate and conceptualize structural changes in agri-food supply chain networks (AFSCNs) is scarce. This gap motivates the following four questions of this study: (1) Who are the primary and secondary stakeholders in the AFSCNs of the digital era? (2) What are their transparency interests? (3) How do AFSCN structures change with the emergence of digital innovations that can facilitate sustainability transition through greater transparency? (4) How to conceptualize those structural changes to AFSCNs? The netchain approach and respective transparency concept are integrated with classical stakeholder theory. Data was collected via a series of 21 semi-structured pilot interviews with technology providers in the EU agri-food sector and analyzed using structured content analysis. Results paint a complex picture of contemporary primary and secondary stakeholders of AFSCNs and their interests. Primary stakeholder interests lead to coopetition in vertical and horizontal relationships of the netchain and low transparency efforts by intermediaries. Both hamper the dissemination of digital innovations and the exploitation of their potential to improve AFSCN sustainability. Among secondary stakeholders, policymakers and governments, NGOs, and technology providers excel in being drivers of digital transparency for sustainability, with social media as a strong direct communication tool to reach netchain stakeholders, consumers, and research institutes/universities as collaborators and customers. The emergence of “information AFSCN” and “digital AFSCN” increases the complexity of the whole supply chain network through intermediation, reconfiguration, and emergence modes of change to underlying structures. Agri-food business managers, scientists, and policymakers should innovate in private and public governance to facilitate collaborative advantage and sustainability in a combination aligned with innovative digital transparency solutions.

Agri-food systems worldwide are coming under ever-increasing pressure to address contemporary sustainability challenges of the 21st century (Béné, 2020; Hellegers, 2022; Jaiswal and Agrawal, 2020; Meuwissen et al., 2019; Pingali, 2015). In the European Union (EU), the Farm to Fork strategy is a key plank in the European Green Deal with the objectives of making agri-food systems fair, healthy, and environmentally friendly. The European Green Deal necessitates significant change and furnishes the EU agri-food sector with a foundation to flourish in a dynamic business environment that embraces new ideas and technologies (European Commission, 2022). To facilitate achieving the goal of making agri-food systems more sustainable, agri-food supply chain networks (AFSCNs) must become more transparent. Through greater transparency, sustainability efforts can be controlled across stages of even complex global supply chains, and common market failures mitigated. Still, practitioners often counter transparency with caution, given the uncertainties about the usage of their information and data (Gardner et al., 2019). Bad data governance, power imbalances, competitive disadvantages, diverse transparency interests of supply chain network stakeholders, and technical and structural incompatibilities are typical barriers in sharing information and data of the own business. Digital innovations emerging over the past two decades are effective tools to overcome those barriers when managed well in collaboration with various other stakeholders, including competitors, and for shared transparency benefits (Gardner et al., 2019; Carmela Annosi et al., 2020). Although one of the five thematic clusters of social science literature linked to agriculture 4.0 is the “economics and management of digitalized agricultural production systems and value chains” (Klerkx et al., 2019, p. 1), management decision-making to form and maintain multistakeholder relationships in supply chains and networks remains challenging across strategic, tactical, and operational levels, given the limited guidance that exists on the “collaboration-battlefield” of the two agri-food business megatrends “digitalization-sustainability” (Lichtenthaler, 2021).

Much of the contemporary social science literature on agri-food focuses either on the development and adoption of digital innovation to increase transparency, efficiency, and sustainability (e.g., Silvestri et al., 2023; Benyam et al., 2021), the creation of digital innovation ecosystems (Wolfert et al., 2023), or on the sustainability transition of the food system through innovation in general (e.g., Herrero et al., 2020; Barrett et al., 2022). Of the latter studies, only a few investigate the role of supply chain transparency in-depth and mainly as a catalyst rather than part of the transition process (Gardner et al., 2019); although digital innovations can modify which data and information business decision-makers consider relevant, complete and correct, and thus reshape their transparency interests (Flyverbom, 2016). Research that links the topics of “digitalization” and “sustainability” in the agri-food sector is still in its infancy; it focuses on identifying new research pathways (Klerkx et al., 2019) and developing a first integrative conceptual framework (Lichtenthaler, 2021). This similarly holds true for management studies considering the digitalizing transparency of AFSCNs toward sustainability transitions in the food system in particular. In their qualitative study, Carmela Annosi et al. (2020) implicitly open critical pathways for supply chain governance research to overcome the digitalization barrier of difficulties in collaboration and coordination between partners, especially those of diverging goals and size, and support the respective drivers of striving for higher competitiveness and eco-friendliness in food supply chains. Gardner et al. (2019) started walking the pathway by developing 10 initial propositions toward conceptualizing the role of transformative AFSCN transparency to generate knowledge for sustainability from a supply chain perspective, which assigns central importance to trust and cooperation among stakeholders sharing information. Their request for deeper investigations of the induced changes in collaborations between actors across sectors and supply chain levels underlines that in the context of sustainability transitions, existing literature falls short of a multistakeholder perspective on structural changes in digitalizing AFSCNs that evolve equally around transparency from the flow of intangible data and information and the flow of tangible goods and services.

To close this gap in the literature, we ask the following four questions: (1) Who are the primary and secondary stakeholders in the AFSCNs of the digital era? (2) What are their transparency interests? (3) How do AFSCN structures change with the emergence of digital innovations that can facilitate sustainability transition through greater transparency? (4) How to conceptualize those structural changes to AFSCNs? To answer these questions, we integrate the netchain approach and respective transparency concept (Lazzarini et al., 2001; Hofstede, 2003; Nijhoff-Savvaki et al., 2008; Otter et al., 2014; Adetoyinbo et al., 2023) with classical stakeholder theory (Freeman 1984) to identify and conceptualize stakeholders and their relationships in the context of digital transparency for sustainability in modern AFSCNs. Data was collected via a series of 21 semi-structured interviews with technology providers in the EU agri-food sector and analyzed using structured content analysis.

This research follows an abductive approach as described by Timmermans and Tavory (2012) in two steps. In the first step we deduce from existing literature on supply chain networks and stakeholder analysis in agri-food systems conceptual insights on primary and secondary stakeholders, their relationships and interests, the understanding of transparency in governance structures, as well as the changes induced by digital innovations and their providers to agri-food supply chain organization in the context of the two megatrends “digitalization” and “sustainability.” In the second step, we draw new empirical insights on those themes from qualitative interview data to extend the state-of-the-art and further develop our literature-based propositions.

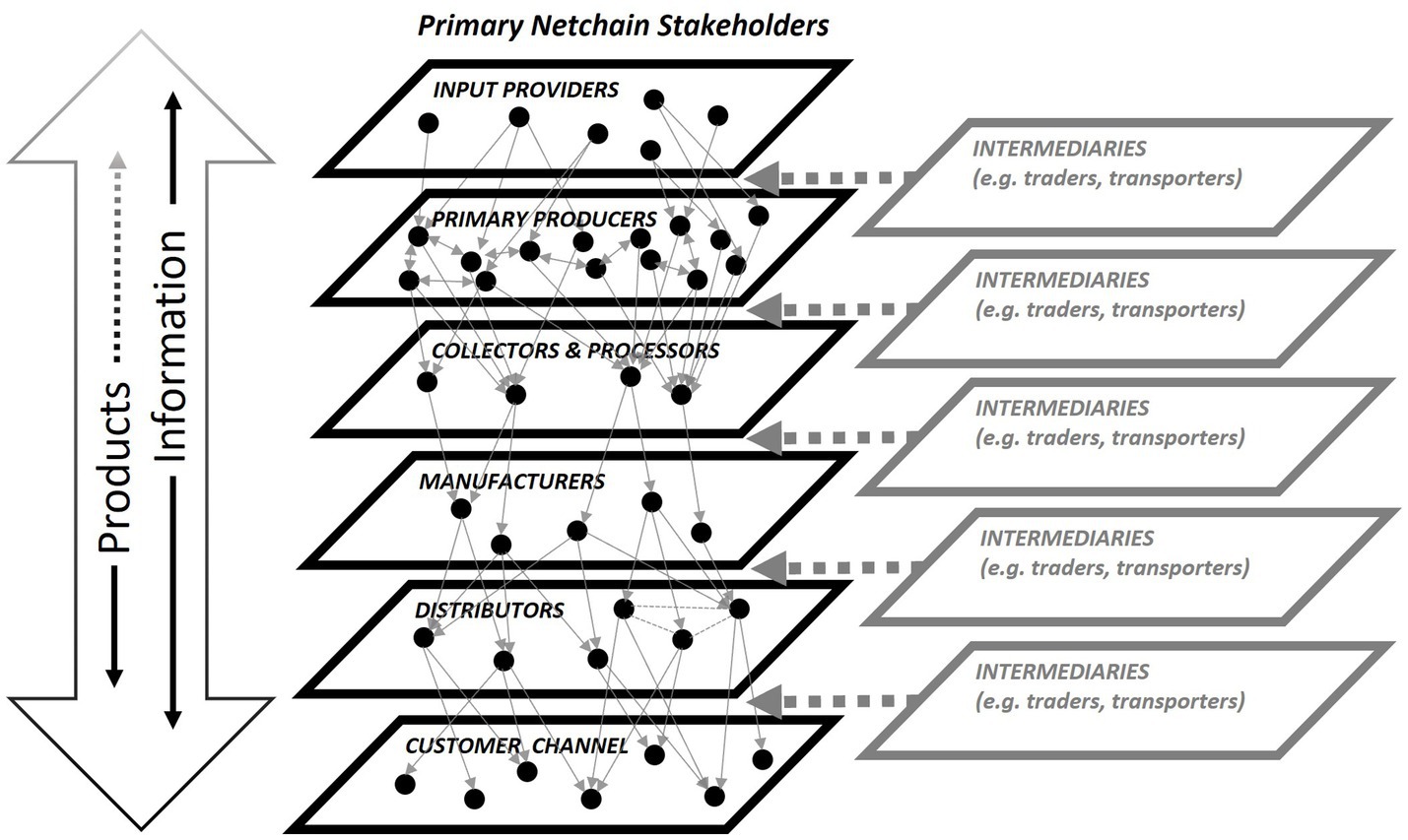

Netchain analysis is a concept that integrates both supply chain and network analyses and considers inter-organizational collaboration based on different types of interdependencies (sequential, pooled, and reciprocal) between firms within particular industries or groups. As such, the original concept focused on the value creation and coordination mechanisms in vertical and horizontal relationships between members of different stakeholder groups (Althoff et al., 2005; Lazzarini et al., 2001; Otter et al., 2014). Empirical applications of the netchain concept in AFSCNs paint a complex picture of the organizations involved and their relationships (see Figure 1). Those organizations pursue their business activities on the supply chain stages of input provision, primary production, collection and processing, manufacturing, and distribution into customer channels. Between the firms that are producing agri-food products by adding and creating value across various tiers, intermediaries trade or transport the products further downstream. The complexity of netchains correlates with their geographical scope ranging from local, regional, and national to global (Nijhoff-Savvaki et al., 2008; Otter et al., 2014; Adetoyinbo et al., 2023). Past empirical studies on agri-food supply chains typically describe information as product(ion)-related and “accompanying” the product flows to reciprocal interdependencies in vertical and horizontal relationships (Nijhoff-Savvaki et al., 2008; Theuvsen, 2004).

Figure 1. Classical netchain of an agri-food product. [Source: Authors’ own creation based on Lazzarini et al. (2001) and Djekic et al., 2021].

The digital era has shifted society and business toward being more information-driven (Flyverbom, 2016). Digital solutions, such as blockchain technology, artificial intelligence (AI), data platforms, and online marketplaces, intermediate the product markets underlying the netchain relationships (Carmela Annosi et al., 2020) and beyond. Netchain structure, comprising supply chain actors and their relationships, is one of three decision components of the business ecosystems digital innovation ecosystems are embedded into. While some organizations, like digital technology provider Google, position themselves as “open by default” to create and capture value from information and data, for example, knowledge, the emergence of digital innovation ecosystems comes with platforms to join developers with users in the agri-food netchain for collective value creation and capture from the technology and information flowing between them (Wolfert et al., 2023; Flyverbom, 2016). Consequently, digital technologies may facilitate the formation of new sequential, reciprocal, and pooled relationships between agri-food netchain organizations that are based on information and data exchange to single-firm and/or collective benefits from following a joined digital innovation strategy.

Proposition 1: With ongoing digitalization, the flow of intangible information and data in netchains increasingly detangles from the flow of tangible products.

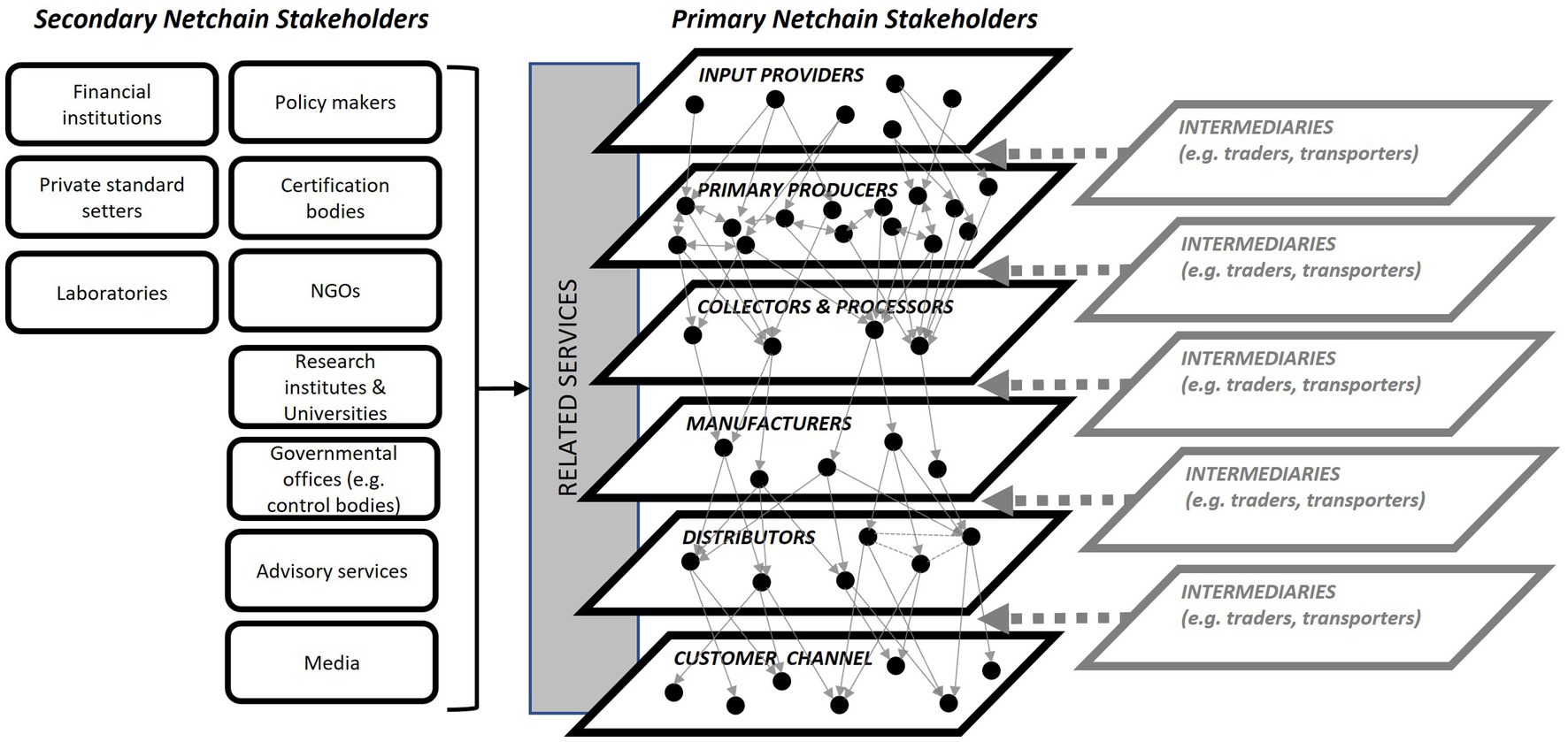

Subsequent research on agri-food products has developed the netchain concept of Lazzarini et al. (2001) further by extending it toward external/lateral relationships (Althoff et al., 2005; Otter et al., 2014; Nijhoff-Savvaki et al., 2008; Adetoyinbo et al., 2023), considering that netchain firms can interact with a vast variety of other “non-chain” organizations, but not necessarily economically (Nijhoff-Savvaki et al., 2008) as depicted in Figure 2. Such relationships were first defined by Althoff et al. (2005, p. 28) as related services that are “(...) responsible for supportive activities. They have a major influence on the core processes. These include input providers and by-product users, consulting/advisory and veterinary services, quality programs and their certifiers and public bodies responsible for inspection activities”. Later studies agglomerate the organizations to which external/lateral supply chain network relationships are maintained in a broader sense as simply “stakeholders” that do not belong to any supply chain stage, also including, for example, NGOs, research institutes/universities, and providers of (digital) technologies that develop innovative tools, and/or collect, store, process, and disseminate data and information (Nijhoff-Savvaki et al., 2008; Otter et al., 2014; Adetoyinbo et al., 2023).

Figure 2. Supply chain network of an agri-food product. [Source: Authors’ own creation based on Lazzarini et al. (2001), Nijhoff-Savvaki et al. (2008), Otter et al. (2014), Adetoyinbo et al. (2023), and Djekic et al. (2021)].

Stakeholders are broadly defined as a set of individuals who either affect or are affected by the operations of an organization (Clarkson, 1995; Freeman 1984; Mitchell et al., 1997). From a value creation perspective, the collective endeavors of stakeholders are key, while the withdrawal of their support can threaten the viability of a business to operate as a going concern (Freudenreich et al., 2020). Stakeholders can be either primary when they have an economic interest in a transaction or secondary when they exert influence or are influenced by an organization but are not transacting with it directly (Freeman 1984). That conceptual framing defines organizations that pursue economic interests while transacting a particular agri-food product and related data within vertical and horizontal netchain relationships as primary stakeholders. Organizations are defined as secondary stakeholders if they are involved in providing or co-creating institutional environment and related services that are unspecific to a particular agri-food product within lateral relationships to primary stakeholders (see Figure 2). The generic four main stages of agri-food supply chains—producers, processors, traders (including retailers), and consumers—(Bellemare et al., 2017; Carmela Annosi et al., 2020) are in the stakeholder literature considered primary stakeholders (Djekic et al., 2021), while policymakers, governmental offices (e.g., control bodies), NGOs, media, private standard setters, certification bodies, laboratories, research institutes, universities, financial services and advisory services (Nijhoff-Savvaki et al., 2008; Otter et al., 2014; Adetoyinbo et al., 2023) are considered as secondary stakeholders (Djekic et al., 2021). Primary and secondary stakeholders and their relationships with each other constitute AFSCNs1.

Secondary stakeholder roles and interests in agri-food supply chains developed toward being sustainability focused over the past three decades. Policymakers manifest sustainability focus toward the achievement of the United Nations’ (UN’s) Sustainable Development Goals (SDGs) in their agendas, such as the EU Green Deal, and legislation on EU-, national, and federal levels (Djekic et al., 2021; European Commission, 2022). Private standard setters complement public sustainability standards, and certification and control bodies, together with laboratories, to assure compliance, often communicated through food labels (Djekic et al., 2021). Media and NGOs have power over the generation of agri-food sustainability knowledge in the society at large by mediating the process through decisions over which information is shared and when. Particularly the rise of social media in the digital era, leads to different forms of imperfect information beyond incompleteness. Being a playing field of communication for various AFSCN primary and secondary stakeholders, hypes are created about some sustainability topics over others (Djekic et al., 2021; Stevens et al., 2016). Research institutes and universities generate new findings from data and disseminate them to students and other stakeholders of the AFSCN, as do advisory services (Djekic et al., 2021). Financial institutes influence through credit approvals which investments into sustainable innovation are being made in agri-food and technology companies. Particularly startups depend on external funding to scale up. To make informed decisions about sustainability-focused investment, investors depend on access to reliable indicators and data (Negra et al., 2020). Agri-food technology providers contributed to the emergence of the digital era by shifting their focus from hardware to software innovations to create and capture value. Software innovations are tools that help collecting, storing, processing, and disseminating data and information. Technology providers offer those tools themselves and/or services related to the use of these tools (Kosior, 2018; Poppe et al., 2013).

Proposition 2: In the digital era, secondary stakeholders’ value creation and capture from intangible sustainability information and data proliferates in AFSCN.

“Technology providers” is a term used in science and practice that groups organizations of different scales and product/service portfolios. Some technology providers increasingly equip their traditional machinery and hardware products with software (e.g., tractor manufacturers like Deutz Fahr, John Deer, and CLAAS), while others develop innovative machinery that depends in its functioning inevitably on the complementary digital tool (software) and data (e.g., manufacturers of robotics for production and processing). Those firms are considered input suppliers and thus primary stakeholders of the AFSCN, as machinery constitutes a classical input to agricultural production and food processing. A third type of technology providers in agri-food focuses its activities on digital tools in the form of software and related services. Contemporary examples are blockchain technology, the Internet of Things (IoT), AI, cloud computing, big data platforms and decision support systems. Some of these digital tools go beyond the pure collection, processing, storing, and distribution of data and information by contributing to the generation of new knowledge (e.g., decision support systems). The grouping of an organization with the latter portfolio to the primary or the secondary AFSCN stakeholders depends on the concrete tool and service provided and whether it constitutes an input or a related service to facilitate the value creation of agri-food products (Wolfert et al., 2023; Lezoche et al., 2020). What unites all the different technology companies is the joined interest in digital transparency, which can be achieved only through the interconnectivity of tools and systems (Carmela Annosi et al., 2020).

Proposition 3: Technology providers can be either primary or secondary stakeholders to the digital AFSCN depending on their value creation and coordination function.

In the EU, transparency of agri-food supply chains became a hot topic with the bovine spongiform encephalopathy (BSE) crisis at the end of the 1990s and was responded by politics with integrating the agri-food business obligation of tracking and tracing products “one step forward and one step back” the chain into to EU General Food Law (European Commission, 2007). Since then, the understanding of agri-food transparency in science and practice has often been reduced to traceability, and the two terms used interchangeably in studies (Patelli and Mandrioli, 2020; Gardner et al., 2019). The term traceability is legally defined in the EU General Food Law as “the ability to trace and follow a food, feed, food-producing animal or substance intended to be, or expected to be incorporated into a food or feed, through all stages of production, processing and distribution” (European Parliament 2002, 8). Researchers like Gardner et al. (2019, p. 164) often view “transparency broadly as a state in which information is made apparent and readily available to certain actors.” Hofstede (2003, 18) provides with “the extent to which all the netchain’s stakeholders have a shared understanding of and access to, the product-related information that they request, without loss, noise, delay, and distortion” a more comprehensive, while concrete definition beyond the purely vertical and linear supply chain perspective and on the edge of business and information science. In that view, tracking and tracing (history transparency) is a subset of overall transparency, next to information exchange that helps coordinate processes and procedures (operations transparency) and exchange of strategic information (strategy transparency), for example, on the development of product innovations. Particularly strategy transparency is relevant in the context of digital innovation ecosystems and today’s demands of society at large for sustainability in AFSCN, as innovation development is accelerated by co-creation between developer/provider and users, and interoperability of digital tools can only be achieved in collaboration (Wolfert et al., 2023). Interoperability helps AFSCN’s primary stakeholders in obtaining a competitive advantage by assuring sustainability through history transparency and greater efficiency from operations transparency based on data and information from digital tools.

Proposition 4: Transparency for sustainability constitutes the game-changing interest of technology providers in AFSCN relationships.

Coopetition, meaning “a situation where competitors simultaneously cooperate and compete with each other” (Bengtsson and Kock, 2003, p. 38) to enhance the collective outcome, in turn leading to greater individual outcomes from competitive advantage. Different forms of coopetition have a long history in EU agri-food supply chains. Farmer cooperatives, machine rings, and food retailers’ category management systems are only a few examples (Walley and Custance, 2010). Both, the digitalization and the sustainability megatrends share that individual firms can capture more value from collaborative advantage rather than competitive advantage (Wolfert et al., 2023; Gardner et al., 2019). With the emergence of initiatives such as digital platforms for digital innovation ecosystem building (Wolfert et al., 2023; Kosior, 2018) and sustainability alliances to create greater transparency (e.g., Tropical Forest Alliance) (Gardner et al., 2019), AFSCNs show tendencies toward supply chain integration and collaborative value co-creation instead of exchange to individual benefits, also including secondary stakeholders (Carmela Annosi et al., 2020). The development and creation of innovative organizational structures in AFSCN are fueled by the need for clear governance of business relationships between stakeholders to define ownership rights over the intangibles, particularly strategic information and intellectual property over innovations (Wolfert et al., 2023; Flyverbom, 2016; Kosior, 2018). The social media opportunities agri-food stakeholders have today contributed to AFSCN integration and collaboration tendencies by creating hypes on sustainability topics, bypassing larger food companies and institutional structures by establishing a direct communication channel between producers and consumers, strengthening horizontal relationships in the netchain, and creating new data relevant for agri-food businesses (Stevens et al., 2016).

Proposition 5: Digital transparency for sustainability changes the organizational structures of AFSCN radically.

Results are generated via qualitative data from a series of semi-structured expert interviews conducted with providers of innovative technology solutions for EU agri-food supply chains. All technology providers had an identified aim of improving sustainability at single or multiple tiers of agri-food supply chains through transparency. Interview participants were prescreened based on their roles in their respective enterprises, with business professionals, supply chain managers, company directors, and operating officers targeted as key informants. Individuals in such organizational positions were deemed the most knowledgeable to provide insights into stakeholders, their transparency interests, and the organization within respective AFSCNs. All the participants were asked to provide consent for the interviews, and the research received ethical clearance prior to implementation.

In total, 21 interviews were conducted between November 2022 and January 2023, and between March and June 2024. The interviewees represented 20 agri-food technology startups located in the EU. The interviews themselves lasted between 45 min and 2.5 h in duration, taking an average of 1 h and 7 min. Topics for the interviews included basic demographic questions about participants and their companies and covered the issues of stakeholder identification, supply chain governance, network organization, and transparency perspectives. To ensure the understanding of participants around stakeholder concepts, interviewees were provided preparatory material, which included the stakeholder definition by Freeman (1984), and were presented with a verbatim definition during the interviews to help ensure consistent comprehension. All interviews were conducted in English.

The interviews were all performed online due to the geographic dispersion of participants and researchers, and transcribed through Microsoft (MS) Teams recording software, with associated video recordings captured to verify the transcripts later. After cleaning the interview transcripts, structured content analysis was performed using the software Atlas.ti. Interviews were coded, first, to ascertain which digital services the technology providers were offering; second, to identify both primary and secondary stakeholders in various EU AFSCNs; and third, to see how the digital services were offered in terms of the relationships between the various stakeholders identified in the AFSCNs.

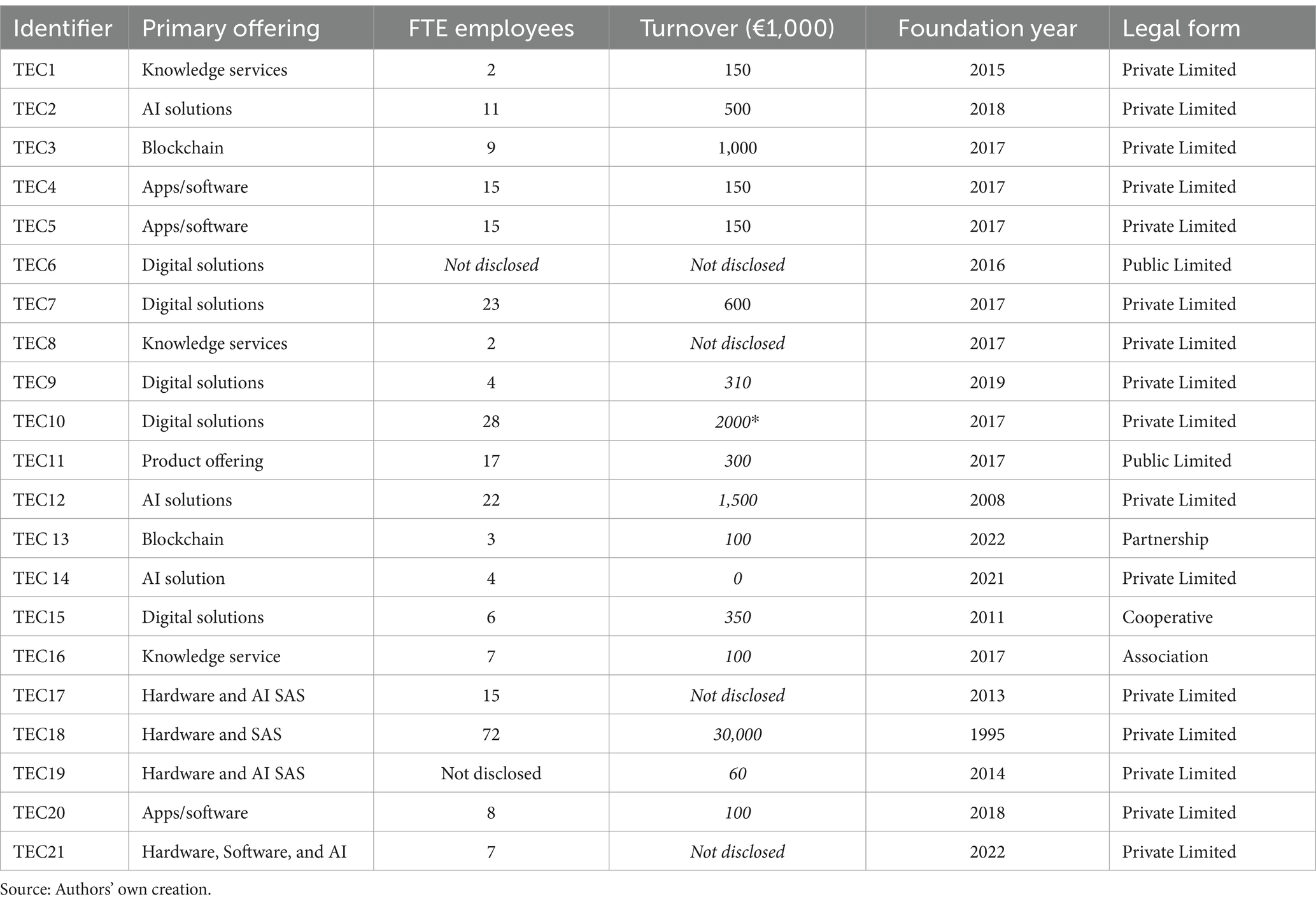

The interviewed technology providers offer a variety of potential digital transparency solutions in the agri-food industry, ranging from knowledge services, specific solutions such as AI, blockchain, or specific web platforms and app interfaces, mixtures of technologies partially including hardware, or even consumer products with specific transparency characteristics. The technology providers themselves are primarily small enterprises comprising between 2–28 full-time equivalent (FTE) employees, with turnover ranging from approximately €0 to €2 million (⌀ €535,000). One technology provider can be classified as medium-sized with above 70 FTE and a €30 million turnover. That company offers a technology relevant to this research as a novel and smaller part of its business portfolio.

The primary offering of the technology providers interviewed is outlined in Table 1. To protect participant confidentiality, data has been aggregated under broad categories. TEC1 offers knowledge consultancy services to a spectrum of stakeholders across their relevant agri-food supply chain, with the aim of connecting the actors together. This differs from the knowledge services offered by TEC8, which are customized to specific primary stakeholders in the netchain on a case-by-case basis. TEC2, TEC12, and TEC14 are looking at generating data-driven AI solutions targeted at specific individual actors in the netchain, while TEC6 and TEC7 both offer digital platforms that look to coordinate activities between netchain tiers, though not necessarily sequential ones. The start-up, interviewees TEC4 and TEC5 work for, developed a software/app solution to optimize the internal processes of agri-food businesses. TEC10 offers a digital platform linked with intelligent farming solutions. Digital traceability, underpinned with blockchain technology and targeted at producers and retail/catering, is in the focus of TEC9 and TEC13. TEC3 follows a different strategy with their blockchain solution, namely to link together multiple actors of the supply chain to facilitate transparency in information exchange. TEC15 offers IoT-based decision support systems to single firms. TEC17, TEC18, and TEC19 provide a combination of hardware and SaaS or AI SaaS. TEC20 focuses on smart packing and related software, and TEC21 on hardware together with its own software and AI solution for the agri-food industry.

Table 1. Organizational characteristics of participating technology providers.

The individuals representing those companies during the interviews are balanced in terms of gender, with 10 men and 9 women participants, and have an average age of 44 years. They are from 10 different countries, with all but one interviewee being from the EU. Nineteen of the 21 interviewees reside in their home countries. All participants have completed school with A-levels. Five of them finished bachelor’s level studies as the highest professional qualification, while 12 possess MSc, MBA, or diploma degrees, and three have completed doctoral-level studies. One interviewee reported practical training as a professional qualification. The specialization of the professional qualifications is mixed between natural sciences and business/economic studies, and despite the nature of their businesses as technology providers, only a few possess information technology or equivalent qualifications in a digitalization space. However, this may also be a direct result of the purposeful sampling technique of prescreening for individuals that could provide insights into stakeholder roles and organizations within their respective AFSCNs.

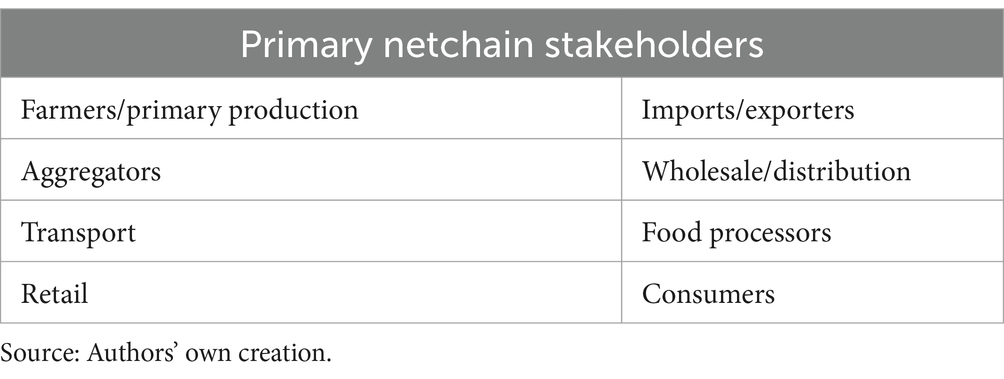

First, considering identified primary netchain stakeholders (Table 2); input suppliers were only mentioned very few times (TEC15 and TEC17), while upstream in the supply chain, farmers and primary production were recognized with a significant role. They are interlinked in the products and services provided by 10 of the 20 startups and were often mentioned by participants in the interviews. Regardless of the length of the supply chain, inevitably, they all involve one actor:

Table 2. Primary netchain stakeholders as identified by technology providers.

“So obviously there is....() the supply chains that we are focusing on are very short. So there is not a lot of actors, for example, obviously there is the farmer... the farmer is also the one that basically labels and sells the product.” (TEC9; 6:37)

This underlines the fact that primary production is critical to most agri-food supply chains. Some technology providers even deem it necessary to give financial incentives to participate:

“... we have the idea to give to the farmer money to use the platform. Why? Because if we don’t do this phase, the farmers () don’t use the platform to insert data.” (TEC10; 6:55)

The central role primary production plays for many of the technology providers leads to considerations of how to incentivize them to engage in transparency measures. Additionally, many technology providers also identified agricultural cooperatives as partners.

Other primary stakeholders present, depending on the length of the chain and level of integration, are importers and exporters. This is largely due to the EU single market, where even though agricultural products may move cross-border, they do not require customs checks. However, for agri-food chains that originate or overlap outside the EU customs union, importers and exporters were identified by interviewees TEC1 and TEC7. Another primary stakeholder mentioned but not always present were aggregators or intermediaries (TEC1, TEC6, TEC7, TEC15, TEC17, TEC18, and TEC19). Their role in some chains is significant, depending on the country the chain is located in. When speaking in the context of older farmers in southern Europe, one interviewee made the comment:

“Right now what they do is the brokers, the traders, the buyers, they visit the farmers and they tried to deal with them and to close the deal with them.” (TC6; 38:33)

This illustrates the potential for these supply chains to change business models and reorganize, particularly as the younger generation takes over farming operations and is more comfortable with digital tools, a point reinforced by TEC6.

Primary stakeholders such as distribution and wholesalers exist inside agri-food supply chains (TEC6, TEC7, TEC9, TEC13, TEC14, TEC15, TEC17, and TEC18). However, their role is not prominent to the majority of the interviewees. Another primary stakeholder that several of the participants touched upon (TEC1, TEC3, TEC9, TEC13, TEC20) but that only two actively engaged with (TEC6, TEC16) was the role of transportation in the different stages of the supply chain. It seemed to be just outside the current scope of most interviewees while integrated into the netchain for others:

“Because for example, as is currently, we don’t have transportation involved anywhere … because there’s no need for the type of claims that you make.” (TEC3; 16:26)

“So it’s another member of our board who is a farmer who has a warehouse and actually he’s kind of web and he has the relationship to all this transport companies. So we don’t have trucks for our own. We do actually work with existing truck companies that drive food around.” (TEC16; 11:52)

Further downstream in agri-food supply chains, many interviewees identified other intermediate steps depending on the specific chain. Another primary stakeholder is consistently identified as food processors, even when short supply chains are targeted (TEC13). What a processor actually entails can be very different depending on the supply chain. It could be a large actor such as Heineken (TEC6), a manufacturer of ready meals (TEC20), or more specific actors such as one that assists in processing for TEC11. It may also be a food company such as Milka (TEC7), or a company that processes some sort of raw agricultural product into a different form for further use or consumption, such as juice (TEC3), the milling of grain (TEC8), olives (TEC9) or washed ready-to-eat fruit and vegetables (TEC21). Regardless of the exact nature and how they are processed, they are present in almost every supply chain, and some interviewees identified that they can occur multiple times within the same supply chain (TEC1 and TEC8). However, an overarching theme that can be drawn is that processing in some agri-food chains is complex and can occur in multiple tiers in the chain, involving both horizontal and vertical relationships.

The retail stage of the chain was mentioned by all the interviewees, and represents the last step before the consumer. To underline this, at least two of the technology providers have products in their portfolio where it appears that the target market of their product offerings is the retail end of the chain. The significance of retail and its role in driving transparency solutions was underlined by TEC1 and TEC14:

“… because usually when supermarkets are doing the right thing of asking tough questions to their suppliers …. they’re not going to communicate on the fact that they’re asked to be sure there's no forced labor and no slavery. Because you can’t put a sticker, no slavery on a product (because that means products without the sticker have slavery).” (TEC1; 9:25)

“… we have strategies via our channels we have, we built our relations with all some kind of groups that have these biodiversity in their background and behind that all these big retailers are very interested …” (TEC14; 10:28)

Retail actors of various natures may be enticed by transparency, insofar that it adds value to their product, more so than simply fulfilling regulatory requirements. Furthermore, the retail end of agri-food supply chains is not just confined to supermarkets but also identified to include other avenues such as restaurants and hotels, and even hospitals, kindergartens, and catering at larger events (TEC1, TEC4, TEC5, TEC13, TEC16, TEC17, and TEC20).

Some interviewees identified the consumer as a primary stakeholder downstream in the chain. Whether the technology providers identified them directly is correlated with their service offering. If companies had a solution that spanned large parts of the chain (TEC6, TEC7, TEC9, and TEC14), or had consumers in focus (TEC2, TEC11, and TEC17), they were mentioned more often:

“… I guess the other main stakeholder is the consumer.” (TEC9; 7:28)

“… we take into consideration the end consumers.” (TEC14; 19:57)

“It’s something [the application] that could protect the consumer from buying something or eating something that is not completely fresh.” (TEC17; 10:10)

Although their stakeholder role may be more implicit to some organizations, for some technology providers consumers were identified indirectly as being an essential driver of their business, but not explicitly mentioned as a stakeholder.

“We support them (food processors) with communication to the media, but also communication to the customers.” (TEC8; 3:21)

Overall, many technology providers perceive the transparency interests of primary stakeholders as mostly economic in nature and their view on information as product-related and a possibility to obtain competitive advantage (TEC13 and TEC14).

“… lot of it is purely based on the fact that they can sell their product for a higher price if they can prove that.” (TEC13; 40:57)

Particularly retailers were often identified by the technology providers as being significant drivers of digital transparency for sustainability in agri-food supply chains to keep their license to operate in front of societal expectations and legal frameworks:

“... big retailers are very interested, very interested because they have all to show their carbon footprint and do something for all this environment...” (TEC14; 10:30)

However, organizations such as supermarkets and the retail side all depend on upstream information flowing down the chain. This means that they can drive transparency measures (TEC1, TEC3, and TEC9), but are still dependent on others to provide the needed information. The most crucial downstream actor in this context is the producer (TEC1, TEC6, TEC9, and TEC10):

“Exactly. It’s all information that is involved from the city, the chemistry, the agriculture, the soil, the compositions of the soil, that you know the water used.... So everything that is involved and around the production.” (TEC7; 11:32)

For primary producers, it may not be easy to extract the financial benefits from transparency incentives (TEC6). As discussed above, without financial incentives, they may have no incentive to engage in transparency measures (TEC9 and TEC10). At the same time, there are uncertainties about data protection.

“They [the companies] ask a lot about data protection.” (TEC18; 26:09).

Financial resistance to transparency measures can also take other forms. It could be that information asymmetry is playing a role in why some primary stakeholders do not want to engage in transparency (TEC1, TEC6, TEC9, and TEC20). If they do, it may diminish competitive advantages. It could also be that companies do not have the resources to process big data and provide it to other stakeholders (TEC20). One potential transparency disruptor in the intermediate steps in agri-food chains was identified—aggregators—who would essentially profit from information asymmetry in products.

“… those traders and those brokers …. sometimes they are part of the solution … sometimes they are part of the problem because they don’t want to provide the source of the products they are buying and what they want is to mix them up in order to protect the information where the product is coming in, is coming from.” (TEC6; 36:55).

This was not limited to small-scale aggregators; large-scale ones were also not inclined to play, as oligopoly power in the chain may increase the chances of collusion and excess rents these actors are able to extract from a lack of transparency (TEC1 and TEC6).

As alluded to earlier, transport either was not being actively considered by many interviewees (TEC3) or simply put into the too hard basket (TEC1). The following perception may have summed up why:

“Those companies never take ownership of the product. So at this stage we’ve not ruled them out, but we've set them aside because it's another world, and if we have to start to talk to Maersk, to CMA CGM, it's going to be a nightmare.” (TEC1; 9:46)

The discussion with TEC1 opened up to consider aspects such as freight handlers themselves also having no interest in actually knowing what is in the cargo they are carrying—the following description was provided as their impression into how far the interest for the transportation companies extends:

“They almost don’t care what’s inside except if it explodes because that is technically—that is the only thing they need to know if your stuff is exploding or not in order to know where to put it on their pile. Because exploding boxes are basically at the edge on top the first one to be dropped if there is a fire on board. The rest, if it’s freezing. They just need to know if it needs to be powered.” (TEC1; 9:81)

When considering secondary stakeholders, it was probably unsurprising that policymakers were one of the most commonly named actors. Interviewees were all briefed that they were participating in an interview funded through a Horizon EU research and innovation project, so this alone may have brought this stakeholder to the forefront of their minds. Policymakers identified varied from EU level, such as the Commission and Parliament (or simply the EU in general), to national governments (inside and outside the EU), but also sometimes dropped down to the regional and local level (TEC1, TEC4, TEC15, TEC16, TEC17, TEC18, TEC19, and TEC21), and even border control agencies (TEC8), public bodies that work in environmental and health monitoring (TEC15) and tourism boards were identified (TEC9). To underline the significance of the government:

“I mean, policymakers are usually key in any activity that you find in Europe and then in some of the other countries... the government is beyond the regulation.” (TEC8, 24:26)

“So farmers, this kind of associations, agronomists that work with them and also local authorities that deal with innovation and support in agriculture.” (TEC15; 11:53)

In addition to their sustainability interest manifested in green agendas and their data protection and market regulations, TEC12 particularly emphasized the importance of data that they possess, either directly or that can be scraped from their websites.

The other group of secondary stakeholders identified at a rate perhaps equally to or even higher than governmental actors for some technology providers (e.g., TEC1 and TEC18) was the role of NGOs due to their sustainability interests. One participant (TEC1) had a hefty focus on them in terms of how their organization interacted with NGOs and in that they were highly active in the agri-food chain this organization was engaged in. However, that participant was able to provide a lot of insights. One of such was addressing the potential dual roles that NGOs play:

“So you have two type of NGOs. So you have the NGOs that are scrutinizing the supply chains and are advising supermarkets to buy this or that product... and (the) other ones are second stakeholders in the sense they are shaping the way people are working in the supply chain.” (TEC1; 49:48).

The organization another interviewee worked for had actually received funding for developing a digital solution from an NGO (TEC3). Closely related to NGOs could also be bodies such as industry associations (TEC8).

A second group closely aligned with NGOs, because they may be NGOs themselves, such as the MSC, that was also prominent were certification and labeling organizations. In the case of the technology providers, the perceived role of certification bodies was more indirect and at arm’s length. The focus is on the information they provide rather than being directly connected to their networks:

“Not directly, but indirectly yes. So for example, in our platform, if you state that a certain crop has a certain specific certification. You can say all the certifications in quality you have, but you have to prove that with uploading the certifications you have to the platform so we can be sure.” (TEC6; 39:33)

Although that was not always the case, some companies were interested in binding them in tighter:

“...you work with the Global Gap certification. So Global Gap, UN, United Nations to FAO, which is an international government. So basically we’re trying to collaborate with them.” (TEC7; 25:29)

Again, directly related to certification bodies are agencies and organizations tasked with monitoring or taking responsibility for issued certifications along with auditing and compliance. Some technology providers partnered with specific companies responsible for issuing quality certifications (TEC6). How integrated such services are can depend on the relationship between partners. If they have long-term relationships built on trust, auditing and compliance may be managed in-house, with spot markets relying more on external testing (TEC8). Linking to the monitoring of certification and compliance, stakeholders such as laboratories were also identified as secondary stakeholders (TEC7 and TEC8).

As with the multitude of processing actors on the primary stakeholder side, there is also a wide variation of different supporting services. This can include organizations producing products such as bottles (TEC3 and TEC9), bottle caps (TEC2), packaging and labelling (TEC3, TEC9, and TEC19), satellite and imaging services (TEC3 and TEC12) and financial institutes and insurances (TEC4, TEC6, TEC14, TEC15, TEC16, and TEC17). It can even extend as far as business incubators (TEC4). The fact that research institutes could play a role was not lost on every participant, considering they were participating in a research interview, with several mentioning universities and labs also as their direct collaborators or customers (TEC4, TEC7, TEC9, TEC16, TEC17, TEC18, TEC19, and TEC21). On the information dissemination side, while traditional media was not highlighted, consultancies and social media were (TEC3 and TEC14).

“… Especially social media, so we use as well transformers at this and through social media concerning perhaps the cocktail tomato, because then we can estimate that there is a higher perhaps use or is more recipes or whatever, and that will affect as well trends, and weather data or whether people are on holidays or not. So as well to take all these consumer related information into consideration for using them for the predictive models of any pricing.” (TEC14; 20:01)

Although technology providers perceive the transparency interests of primary stakeholders as mainly economic in nature, they themselves are considering many sustainability aspects as part of their transparency solutions.

“And so our API will pull certain points like so we focus on CO2, water use, land use, social environmental claims, where it comes from and out of the block our API can pull and fill in a product passport which will show exactly where the product came from.” TEC13 (28:39)

Some technology providers see the role of their services more as intermediating the markets, for example, by diminishing information asymmetries in the negotiation processes underlying vertical netchain relationships between primary stakeholders while they form collaborations with them to offer their services (TEC14).

“… in this way (we) look whether we have to adapt as well the algorithms and what kind of structure affects the market.” (TEC14; 19:08)

“…So you need a special sort of farmer as well to cooperate.” (TEC14; 21:38).

Other technology providers compete with traditional service providers (e.g., consultancies and traders) and have the goal to reorganize the chain for greater transparency.

“What we're trying to do and certainly what we've already started to do is to cut out the middleman.” TEC13 (19:47)

A third type of technology provider builds economic transactions and serves as input suppliers, sometimes even including tangibles (e.g., hardware), to other secondary stakeholders of AFSCN, which provide information and data services, such as research institutes and universities.

“If a university typically buys a sensor from us, the university probably has data scientists or chemometricians to build those calibrations.” (TEC17; 11:9)

Overall, the results of this research uncover substantial complexity and diversity in stakeholders and their interests and relationships in EU agri-food netchains, more than past literature from before the digital era conceptualized and observed (Lazzarini et al., 2001; Nijhoff-Savvaki et al., 2008; Otter et al., 2014; Carmela Annosi et al., 2020; Adetoyinbo et al., 2023), and even for regional and national chains. These organizations can be grouped along the following supply chain stages: input supply, primary productions, distribution and wholesale, processing, aggregation and trading (including brokers), and retail targeted toward the final consumer. Overall tendencies of businesses becoming more and more information driven (Flyverbom, 2016) are observed in agri-food netchains, too, although interests may diverge strongly among the groups. While firms in downstream stages close to the consumer are interested in information sharing to obtain competitive advantage by assuring sustainability, aggregators and traders, and primary producers show limited interest or even disinterest as they do not benefit (enough) from transparency relatively to the amount of data and information they need to supply and process. This indicates that value created collectively from technology and information is captured unevenly across the netchain stages (Wolfert et al., 2023; Flyverbom, 2016). Farmers show particular hesitance to share their data due to data protection and ownership concerns. Different from past empirical studies on agri-food netchains, which typically describe information as product(ion)-related and “accompanying” the product flows to reciprocal interdependencies in vertical and horizontal relationships (Nijhoff-Savvaki et al., 2008; Theuvsen, 2004. This study shows that information shared is becoming proportionally less related to a specific product, than related to the firm (e.g., on practices and strategies), the business ecosystem, or the natural environment (e.g., weather and biodiversity data). This supports our initial proposition 1 and allows for the following extension.

Proposition 1.1: With ongoing digitalization the flow of intangible information and data in netchains increasingly detangle from the flow of tangible products.

Proposition 1.2: With ongoing digitalization, agri-food netchains become dyadic in relationships for either product transactions or data and information transactions.

Even more diversity and complexity are observed with respect to secondary stakeholders compared to past AFSCN and stakeholder literature (Djekic et al., 2021; Nijhoff-Savvaki et al., 2008; Otter et al., 2014; Adetoyinbo et al., 2023). Still in line with the literature, the following secondary stakeholder groups of AFSCN are identified in this study: policymakers and governments of various geographical scopes, NGOs, private certification and labeling organizations (setting private standards), auditing and control bodies (assuring compliance with private and public standards), financial institutes, business incubators and assurance companies, research institutes/universities and laboratories, consultancies, social media and technology providers (hardware and software). Policymakers and governments are identified by the technology providers as one of the secondary stakeholder groups with the greatest interest in establishing digital transparency for sustainable AFSCN, due to their sustainability and digitalization agendas, along with growing publicly maintained (sustainability) data platforms and their facilitation of digital innovation ecosystems (Djekic et al., 2021; European Commission, 2022; Wolfert et al., 2023). Similarly, technology providers recognize the vital transparency and sustainability claims NGOs lobby for in AFSCN, particularly in the fishery sector. Research institutes and universities are identified by some technology providers as collaborators and customers beyond their role of generating new findings from data and disseminating them to students and other stakeholders of the AFSCN (Djekic et al., 2021). Social media stand out when it comes to communication and the formation of opinions and perceptions, while technology providers are ascendants to digitalization. Private certification and labeling organizations are often identified by technology providers as belonging to secondary stakeholders, who are perceived as related at arm’s length, although it is their primary goal to create greater transparency through higher standards and better labeling. Overall, the activities of secondary stakeholders to the AFSCN have opened up new opportunities for value creation and capture from sustainability information and data; however, the salience of the particular groups seems to differ significantly.

Proposition 2.1: In the digital era, secondary stakeholders’ value creation and capture from intangible sustainability information and data proliferates in AFSCN.

Proposition 2.2: The salience of AFSCN secondary stakeholders differs greatly depending on their digital transparency claims.

Providers of digital technologies and services have expanded their activities to the extent that some of their offerings can be considered an input rather than a related service to facilitate the value creation to agri-food products, particularly when this involves the supply of hardware to primary stakeholders of the AFSCN (Wolfert et al., 2023; Lezoche et al., 2020). The grouping of an organization with the latter portfolio to the primary or the secondary AFSCN stakeholders depends on the concrete tool and service provided (Carmela Annosi et al., 2020). However, results from the expert interviews indicate that technology providers may even present challenges to defining related services from the conceptual background. Some of the interviewed companies now offer digital services connecting actors at multiple levels of the netchain. While some provide services in the form of various digital platforms and technologies directly to one or more core actors in the netchain in the sense of traditional related services, some facilitate the flows of goods between two or more of the core actors at the heart of the netchain, without ever taking possession of the goods themselves. This is often beyond simple blockchains for traceability that were promoted as an initial transparency solution in agri-food chains.

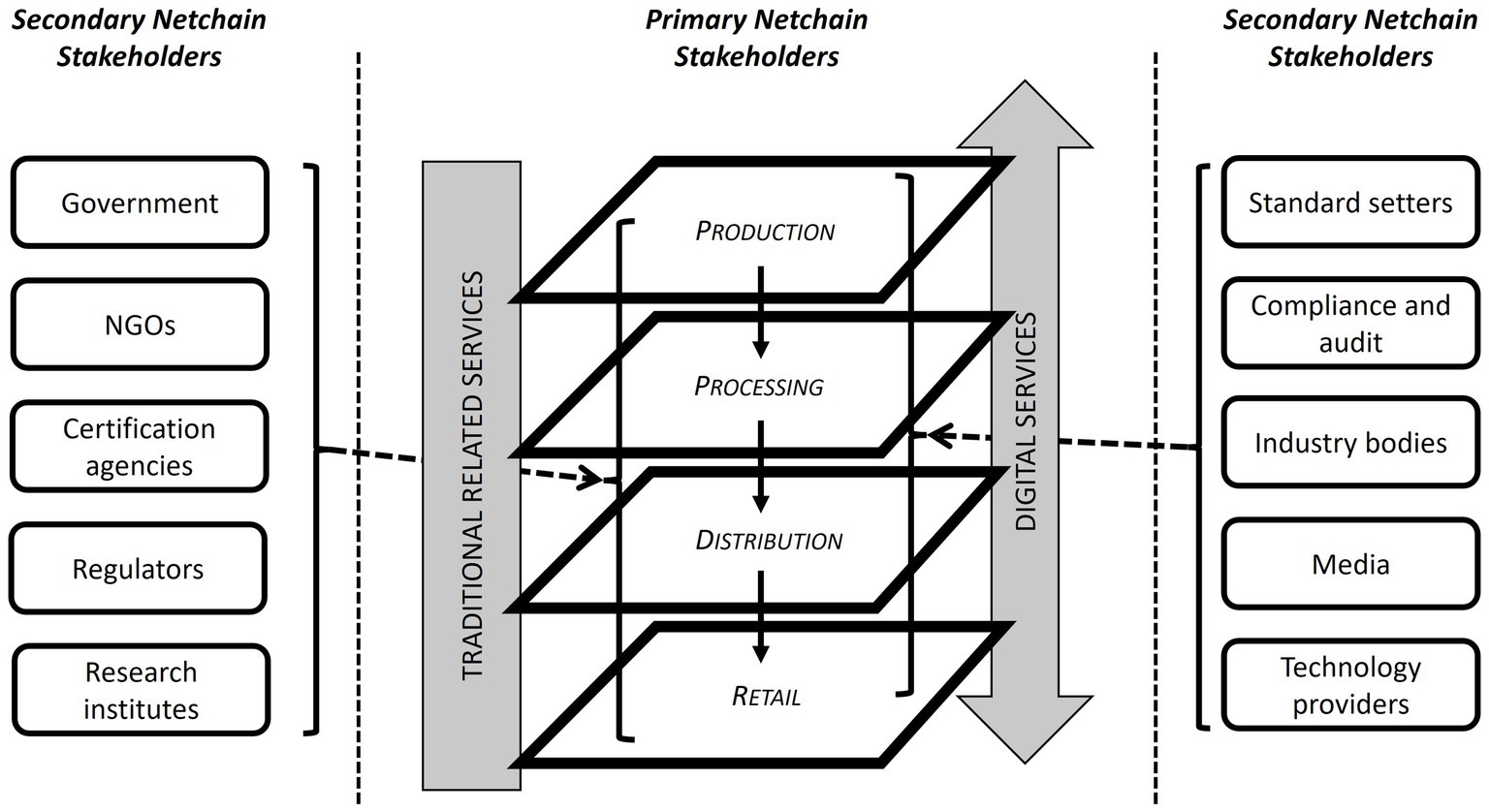

Some of the novel digital solutions generated by the technology providers are now being offered directly to netchain actors, from producers to retailers and distributors, where either the entire or partial exchange process is coordinated by the digital service provider in a digital AFSCN approach (see Figure 3). Solutions such as cloud computing, quick response (QR) codes, and web-based platforms are not necessarily innovative from a technological perspective, but novelty lies in implementation for transparency purposes and the supply chain governance implications they entail. These exchanges cover data such as production information and product characteristics, which contain the desired transparency details, potentially accompanied by an exchange of a physical product facilitated through a digital platform. This is also a clear demarcation from the data exchange warehouse concept (Althoff et al., 2005), where the purpose of data exchange was to more strictly coordinate supply chain actors, aid organizational decision-making, and deliver traceability in agrifood supply chains (Banterle and Stranieri, 2008; Hobbs Jill, 2006; Patelli and Mandrioli, 2020). When paring this back to a stakeholder perspective, providing such services by technology providers may fulfill the classical definition of a primary stakeholder based on economic exchange between two or more actors in the chain (Clarkson, 1995; Freeman, 1984). However, how well they can engage their solutions for transparency may depend first on practical considerations, such as the ability to implement interoperable technological solutions between partners, but second on the engagement of stakeholders for transparency.

Figure 3. Digital agri-food supply chain network (Source: Authors’ own creation).

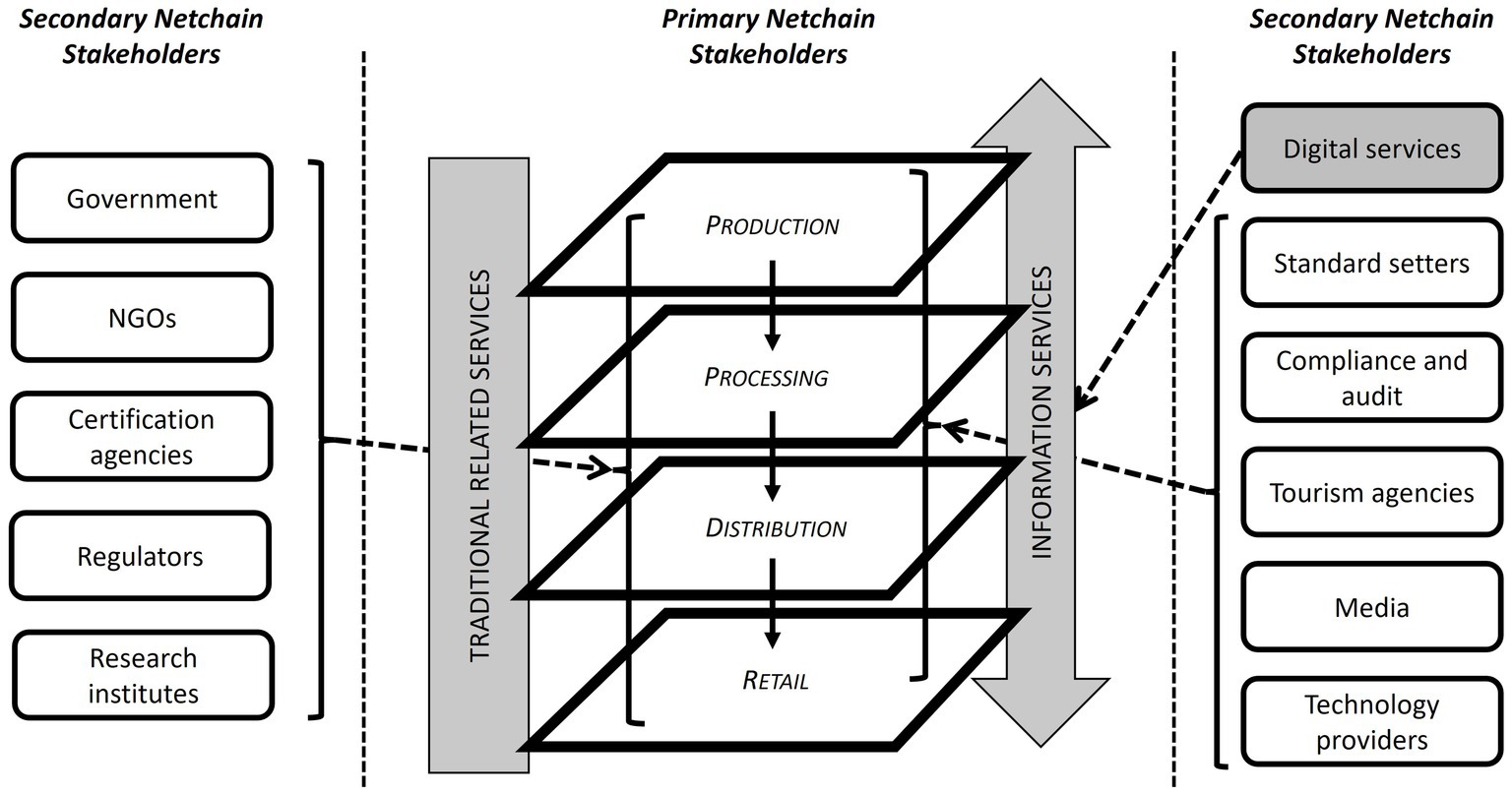

Another variation of the proposed structure in modern netchains is the information AFSCN approach (see Figure 4). Here, digital services, such as some of the interviewed technology providers, deliver information and IT systems that enable data and information exchanges. These data exchanges occur potentially between multiple actors in both horizontal and vertical relationships of the netchain. Solutions such as blockchain are innovative from a technological perspective, and the key is integrating their operational implementation with the conceptual way of implementation for transparency purposes. However, a critical element is ownership. Digital services do not own these information services nor necessarily possess a service contract or other ongoing contractual or formal relationships with the platform. The information service platforms themselves can be owned by actors such as industry groups or non-profit organizations. The digital service providers are responsible for establishing what information service platforms are designed to collect, how they will collect it, and what interoperability they have with other systems. Thus, their role in the process is also significant.

Figure 4. Information agri-food supply chain network (Source: Authors’ own creation).

Organizations such as digital services offering information service solutions would, by the strict stakeholder definition of Freeman (1984), not be included as primary stakeholders of AFSCNs, as long as they do not offer any hardware (Djekic et al., 2021). This is due to them not being involved in economic transactions regarding food products. At the same time, they have critical roles in modern digitalized netchains due to their influence over property rights and the exchange of information and data. Such information and data are needed to serve increasing demands for transparency related to sustainability transitions. It will result in even more prominence for digital services in agri-food supply chains and their increasing relevance as stakeholders. Coupled with this trend is the growing value of data in all forms and the significance of stakeholders involved with data exchange, storage, and validation in the chains. However, based on existing stakeholder definitions that rely on the concept of economic exchange and tangible goods (Freeman, 1984; Freudenreich et al., 2020; Kaler, 2002; Miles, 2017), we find that many digital service companies would only be considered as secondary stakeholders as they are not involved in such exchanges, but in those of intangible assets.

Proposition 3.1: Digital technology providers can be either primary or secondary stakeholders to the digital AFSCN, depending on their value creation in hardware and/or software.

Proposition 3.2: As secondary stakeholders, digital technology providers differ greatly in the type and scope of services they offer to primary stakeholders of the AFSCN.

Proposition 3.3: Either digital AFSCN or information AFSCN arises from the introduction of digital innovations for sustainability.

As the information shared is getting proportionally less related to a specific product only, than related to the firm (e.g., on practices and strategies), the business ecosystem, or the natural environment (e.g., weather and biodiversity data), the findings of this study challenge the actuality of limiting transparency to “product related-information.” Technology providers face many demands of society for greater environmental and social sustainability in agri-food, lobbied and sometimes even co-financed by NGOs, and respond to them by developing their digital solutions beyond traceability functions in structure and content. During the process of digital innovation development, providers work with many other secondary and primary stakeholders across agri-food supply chain stages, share business networks, and create strategy transparency with co-creation partners, as described by Wolfert et al. (2023). Hence the breadth of which digital solutions offer scope to transparency for sustainability beyond traceability (history transparency) toward operations and strategy transparency shapes their disruptive potential, and we refine the original proposition 4 into:

Proposition 4.1: A broader scope of transparency for sustainability constitutes the game-changing interest of technology providers in AFSCN relationships.

The results of this study imply three modes of change digital transparency solutions for sustainability can induce in the relationships underlying organizational structures in AFSCN—intermediation, reconfiguration, and emergence. In confirmation of Carmela Annosi et al. (2020), the intermediation mode technology providers’ software services intermediate agri-food netchain relationships and markets by lowering information asymmetries while at the same time collaborating with the parties themselves. Reorganization is the mode in which competition is as much part of its nature as it comes with governance challenges. Many innovative digital tools, such as online market platforms and blockchain, can bypass supply chain steps or rule out some services of stakeholders, such as consultancies and input suppliers. Stakeholders that govern such data platforms, for example, research institutes and universities, are gaining more importance for practitioners as gatekeepers to information. In the emergence mode, technology providers build economic transactions between other stakeholders and serve as input suppliers, even of tangibles (e.g., hardware), to other secondary stakeholders of AFSCN, who provide information and data services such as research institutes and universities. The intermediation mode aligns with what has been described as “information AFSCN” above, whereas the reorganization and emergence mode aligns with the “digital AFSCN.”

Proposition 5.1: Digital transparency for sustainability changes the organizational structures of AFSCN radically.

Proposition 5.2: As secondary stakeholders, digital technology providers either intermediate, reorganize, or emerge agri-food netchain relationships.

This study initially raised the following four research questions: (1) Who are the primary and secondary stakeholders in the AFSCNs of the digital era? (2) What are their transparency interests? (3) How do AFSCN structures change with the emergence of digital innovations that can facilitate sustainability transition through greater transparency? (4) How to conceptualize those structural changes to AFSCNs?

Results of research questions (1) and (2) reveal input supply, primary production, distribution and wholesale, processing, aggregation and trading (including brokers), and retail toward the final consumer as main groups of primary stakeholders with vertical and horizontal relationships to exchange products and information. Along the agri-food netchain, primary producers are the main suppliers of data and information, while large processors and retailers are demanders to satisfy both their customers and final consumers. Too often, value capture upstream in the netchain remains low due to power imbalances in both the markets for agri-food products and the markets for data and information. Such competition and uncertainties regarding data protection and ownership make farmers and fishers reluctant to share data and information via innovative digital tools. The long-overlooked role of the intermediaries, transporters, and aggregators/traders and their low economic interest in transparency in agri-food netchains further complicate the diffusion of digital tools and their potential for sustainability acceleration. Primary stakeholders should move their relationship practices from competition to collaboration among all actors of agri-food netchains to incentivize digital transparency. This implication targets particularly large, powerful businesses downstream.

Secondary stakeholders in lateral relationships to the netchain organizations are policymakers and governments of various geographical scopes, NGOs, private certification and labeling organizations (setting private standards), auditing and control bodies (assuring compliance with private and public standards), financial institutes, business incubators and assurance companies, research institutes/universities and laboratories, consultancies, social media, and technology providers (hardware and software). Particularly, policymakers and governments, NGOs, and technology providers excel in being drivers of digital transparency for sustainability in AFSCN, with social media as a strong direct communication tool at hand to reach netchain stakeholders and consumers. Sustainability and digitalization policy agendas facilitate the rapid rise of technology providers, developing and offering information and knowledge services. These “new kids on the block” drive structural changes to AFSCN and detangle information flows from the product flows in AFSCN to create value by developing and implementing innovative digital tools. Not seldom do technology providers collaborate with research institutes/universities during the development of digital innovations. The latter organizations may also serve as early adopters of innovative digital products and services. Digital technology providers should continue building intense, long-term collaboration with a broader base of private agri-food netchain businesses as potential end-users to co-create the digital innovation ecosystem’s development of digital tools and related governance structures. With well-defined stakeholder engagement strategies digital innovations can be customized to the interests and needs of the different end-users and prevented from failure.

In answering the research question (3), we conclude that with the emergence of digital and information services to increase transparency for sustainability, the original netchains, consisting of relationships to exchange agri-food products, may decrease in complexity due to bypassing of stages and integration. Due to the detangling of data and information relationships from the product relationships, innovative digital transparency solutions induce three modes of change to the relationships underlying organizational structures in AFSCN—intermediation, reconfiguration, and emergence. These modes create a transparency paradox as they facilitate the co-creation of value from data and information on the one hand and new AFSCN complexities on the other hand. In the” information AFSCN,” technology providers do not fuse with netchain relationships (intermediation mode), while in ‘Digital AFSCN’ they do (reconfiguration and emergence modes). Thus, digital innovation for transparency and sustainability comes with the challenge of developing and implementing innovative forms of fitting supply chain network structures and public and private governance to regulate ownership over intangibles and to assure fair capture of the digital transparency value created collaboratively among primary and secondary stakeholders. The current predominant coopetition does not only task agri-food business managers and scientists to innovate in private governance but also policymakers to establish public governance, specifically for business-related data and information beyond the GDPR regulation. The best combination of innovative governance and technology to sociotechnical innovation bundles can facilitate value capture to collaborative advantage in favor of overall food system sustainability (Barett et al. 2022).

The research question (4) is answered with the following 10 propositions to be further developed into hypotheses and tested quantitatively by researchers in follow-up studies:

Proposition 1.1: With ongoing digitalization, the flow of intangible information and data in netchains increasingly detangles from the flow of tangible products.

Proposition 1.2: With ongoing digitalization agri-food netchains become dyadic in relationships for either product transactions or data and information transactions.

Proposition 2.1: In the digital era, secondary stakeholders’ value creation and capture from intangible sustainability information and data proliferates in AFSCN.

Proposition 2.2: The salience of AFSCN secondary stakeholders differs greatly depending on their digital transparency claims.

Proposition 3.1: Digital technology providers can be either primary or secondary stakeholders to the digital AFSCN, depending on their value creation in hardware and/or software.

Proposition 3.2: As secondary stakeholders, digital technology providers differ greatly in the type and scope of services they offer to primary stakeholders of the AFSCN.

Proposition 3.3: Either digital AFSCN or information AFSCN arises from the introduction of digital innovations for sustainability.

Proposition 4.1: A broader scope of transparency for sustainability constitutes the game-changing interest of technology providers in AFSCN relationships.

Proposition 5.1: Digital transparency for sustainability changes the organizational structures of AFSCN radically.

Proposition 5.2: As secondary stakeholders, digital technology providers either intermediate, reorganize, or emerge agri-food netchain relationships.

While this study provides new insights regarding the perspective of technology providers on AFSCN structures in the digital era, it may be subject to self-selection and response bias, even when mitigated appropriately. Future research should develop the propositions further to testable hypotheses using an interactive multistakeholder approach to consider the views of particularly the primary stakeholders of AFSCN. Special attention should be paid to evaluating the stakeholders’ importance and interests identified in this study. The propositions and their advancements can be used as a basis for modeling complex AFSCN systems quantitatively, for example, using a system engineering approach (Gaudio et al., 2023) or agent-based modeling. Finally, the transparency definition by Hofstede (2003) underlying this research deserves reflection because it does not yet consider the value creation and capture from intangible data. Future research should revise this definition to the new realities of the digital era.

The datasets presented in this article are not readily available because the datasets used for this study are based on qualitative semi-structured interviews which contain sensitive personal and/or commercial information. In order to protect the confidentiality of participants, these datasets cannot be disclosed. Requests to access the datasets should be directed to dmVyZW5hLm90dGVyQHd1ci5ubA==.

The studies involving humans were approved by Social Sciences Ethics Committee (SEC) of Wageningen University & Research. The studies were conducted in accordance with the local legislation and institutional requirements. The participants provided their written informed consent to participate in this study.

VO: Conceptualization, Data curation, Formal analysis, Funding acquisition, Investigation, Methodology, Project administration, Supervision, Validation, Visualization, Writing – original draft, Writing – review & editing. DR: Data curation, Formal analysis, Investigation, Validation, Visualization, Writing – original draft, Writing – review & editing.

The author(s) declare that financial support was received for the research, authorship, and/or publication of this article. Funded by the EU under Grant Agreement No. 101060739.

The authors would like to thank Christopher Bear from Cardiff University, Esra Zora from Delft University of Technology, and Andrea Colafranceschi from ILSI Europe for their collaboration on the data collection, and all interviewees for participating in the interviews.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Views and opinions expressed are, however, those of the author(s) only and do not necessarily reflect those of the EU or of the Research Executive Agency. Neither the EU nor the granting authority can be held responsible for them.

1. ^While earlier studies building on the netchain approach (e.g., Otter et al., 2014; Adetoyinbo et al., 2023) used the terms “netchain” and “supply chain network” rather interchangeably, we introduce a sharper demarcation under consideration of stakeholder theory. While “netchain” comprises only the actors along the supply chain (primary stakeholders) and their relationships, “supply chain network” includes both primary and secondary stakeholders with their linkages amongst each other.

Adetoyinbo, A., Trienekens, J., and Otter, V. (2023). Contingent resource-based view of food netchain organization and firm performance: a comprehensive quantitative framework. Supply Chain Manag. 28, 957–974. doi: 10.1108/SCM-11-2022-0448

Althoff, G., Ellebrecht, A., and Petersen, B. (2005). Chain quality information management: development of a reference model for quality information requirements in pork chains. J. Chain Network Sci. 5, 27–38. doi: 10.3920/JCNS2005.x052

Banterle, A., and Stranieri, S. (2008). The consequences of voluntary traceability system for supply chain relationships. an application of transaction cost economics. Food Policy 33, 560–569. doi: 10.1016/j.foodpol.2008.06.002

Bellemare, M. F., Metin, Ç., Peterson, H. H., Novak, L., and Rudi, J. (2017). On the measurement of food waste. Am. J. Agric. Econ. 99, 1148–1158. doi: 10.1093/ajae/aax034

Barrett, C. B., Benton, T., Fanzo, J., Herrero, M., and Nelson, R. J. (2022): Socio-technical innovation bundles for agri-food systems transformation. Sustainable Development Goals Series. Springer Nature.

Béné, C. (2020). Resilience of local food systems and links to food security – a review of some important concepts in the context of COVID-19 and other shocks. Food Secur. 12, 805–822. doi: 10.1007/s12571-020-01076-1

Benyam, A., Soma, T., and Fraser, E. (2021). Digital agricultural technologies for food loss and waste prevention and reduction: Global trends, adoption opportunities and barriers. J. Clean. Prod. 323, 1–16. doi: 10.1016/j.jclepro.2021.129099

Carmela Annosi, M., Brunetta, F., Capo, F., and Heideveld, L. (2020). Digitalization in the agri-food industry: the relationship between technology and sustainable development. Manag. Decis. 58, 1737–1757. doi: 10.1108/MD-09-2019-1328

Clarkson, M. B. E. (1995). A stakeholder framework for analyzing and evaluating corporate social performance. Acad. Manag. Rev. 20, 92–117. doi: 10.2307/258888

Djekic, I., Batlle-Bayer, L., Bala, A., Fullana-i-Palmer, P., and Jambrak, A. R. (2021). Role of the food supply chain stakeholders in achieving UN SDGs. Sustain. For. 13, 1–16. doi: 10.3390/su13169095

European Commission (2007). Food Traceability - Tracing food through the production and distribution chain to identify and address risks and protect public health. Available at: https://food.ec.europa.eu/system/files/2016-10/gfl_req_factsheet_traceability_2007_en.pdf (Accessed May 06, 2024).

European Commission. (2022). A European Green Deal. Available at: https://commission.europa.eu/strategy-and-policy/priorities-2019-2024/european-green-deal_en (Accessed December 08, 2022).

European Parliament (2002). Regulation (EC) No 178/2002 of the European Parliament and of the Council. Available at: http://data.europa.eu/eli/reg/2002/178/2022-07-01 (Accessed May 06, 2024).

Flyverbom, M. (2016). Transparency: mediation and the management of visibilities. Int. J. Commun. 10, 110–122.

Freudenreich, B., Lüdeke-Freund, F., and Schaltegger, S. (2020). A stakeholder theory perspective on business models: value creation for sustainability. J. Bus. Ethics 166, 3–18. doi: 10.1007/s10551-019-04112-z

Gardner, T. A., Benzie, M., Börner, J., Dawkins, E., Fick, S., Garrett, R., et al. (2019). Transparency and sustainability in global commodity supply chains. World Dev. 121, 163–177. doi: 10.1016/j.worlddev.2018.05.025

Gaudio, M. T., Chakraborty, S., and Curcio, S. (2023). The systems engineering approach as a modelling paradigm of the agri-food supply-chain. Chem. Eng. Trans. 102, 67–72. doi: 10.3303/CET23102012

Hellegers, P. (2022). Food security vulnerability due to trade dependencies on Russia and Ukraine. Food Security. doi: 10.1007/s12571-022-01306-8

Herrero, M., Thornton, P. K., Mason-D’Croz, D., Palmer, J., Benton, T. G., Bodirsky, B. L., et al. (2020). Innovation can accelerate the transition towards a sustainable food system. Nat. Food 1, 266–272. doi: 10.1038/s43016-020-0074-1

Hobbs, J. E. Liability and traceability in agri-food supply chains. In: Quantifying the agri-food supply chain, Eds. C. J. M. Ondersteijn, J. H. M. Wijnands, R. B. M. Huirne, and O. van Kooten 85–100.