Javier Sanz-Cañada

Javier Sanz-Cañada Carolina Yacamán-Ochoa

Carolina Yacamán-Ochoa Rocío Pérez-Campaña

Rocío Pérez-Campaña- 1Research Group on Agro-Food Systems and Territorial Development, Institute of Economics, Geography and Demography (IEGD/CSIC), Madrid, Spain

- 2Research Group Ecological Humanities (GHECO), Department of Geography, Autonomous University of Madrid, Madrid, Spain

- 3Department of Geography, Complutense University of Madrid, Madrid, Spain

The paper attempts to investigate the capacity of agroecological cooperative supermarkets in Spain to promote scaling of food products by means of a double perspective. We first employ a vertical scaling approach to analyze the issues affecting the governance and collective organization of the Cooperative Supermarket Network (CSN), set up in May 2022 and comprising eleven Spanish supermarkets. Secondly, we employ a perspective of horizontal scaling to investigate the potential for increased numbers of members, as well as the geographic and sociodemographic variables at play which limit the abovementioned scaling: to this end we use the case study of the cooperative supermarket La Osa, opened in Madrid in December 2020. We adopt a methodology based on participatory action research throughout the years 2022 and 2023, in which the research team was involved in the real processes of creation and development of the CSN or of La Osa. The study confirms the hypothesis that agroecological cooperative supermarkets constitute a formula for efficient retail distribution for scaling sustainable food in Spain. As opposed to the first-generation options for responsible consumption, these supermarkets appear to contribute to generating significant economies of scale and scope. In terms of vertical scaling, joint provision of services, as well as the gaining of political influence in society, constitute the main advantages in relation to the functioning of the CSN. While the recruitment of new members has heretofore been considered a priority in horizontal scaling, particular emphasis should also be placed on loyalty strategies targeting existing members.

1 Introduction

According to Sage et al. (2021), in the last few years a second generation of alternative food networks (AFNs) has been appearing. These attempt to address the shortcomings of the first generation of AFNs (consumer groups, producers' markets or community supported agriculture) with regard to scaling. The fact that these small-sized initiatives generally do not suffice to completely fill families' shopping baskets undermines the respective initiatives aimed at increasing consumption of agroecological food products and, in general terms, of sustainably produced and distributed foodstuffs. Consequently, the real impact of first-generation initiatives has been slight in relation to the ecological transition or to social change.

The initiatives integrating the second generation of AFNs are much more complex with regard to their socio-productive model, number of references, the infrastructure they require and their structure of governance (Rocas-Royo, 2021). Producers' cooperatives dedicated to logistics and wholesale distribution (food hubs), as well as consumers' co-ops involved in retail distribution in the shape of cooperative and participatory supermarkets, constitute two of the principal formulae of the new institutionality (Sanz-Cañada et al., 2023). They have arisen in an attempt to overcome the barriers facing the scaling of sustainable food production and consumption.

The international literature addresses the different systems of scaling of agroecology and sustainable food (Moore et al., 2015; Rosset and Altieri, 2017; Mier y Terán et al., 2018; Nicholls and Altieri, 2018; Ferguson et al., 2019). Hence, vertical scaling (or scaling up) refers to the radius of action of agroecology reaching the institutions in the broader sense of the term, as well as influencing public policies, as compared with a situation involving dispersed small initiatives wielding no institutional or political influence. This modality seeks to promote systemic transformations at the policy level, involving the introduction of urban food policies aiming at developing sustainable food systems or a ban on the greenwashing tactics used by major supermarket chains; it also attempts to establish governmental incentives for non-profit grocery outlets.

In second place, agroecology's horizontal scaling (scaling out) refers to an increase in the number of producers and consumers in a group, cooperative or territory, or to the spatial dissemination of the model. Strategies related to scaling out are characterized as the capability of an organization to replicate a given social innovation across diverse communities, thereby broadening its impact and involving a tendency toward massification. This strategy underscores the importance of increasing the geographic or demographic scale, for example, related to the propagation of agro-food networks within various city districts or the augmentation of their membership base.

In their examination of systemic social innovation, Moore et al. (2015) propose three pivotal strategies for scaling, adding to these the concept of scaling deep, such as the strategies aimed at promoting shifts in societal values and cultural norms, and improving interpersonal relationships. These strategies constitute an attempt to create a significant cultural and behavioral shift, and to encourage consumers to adopt a more conscientious stance on the consumption of local, fresh, seasonal, and ecological products; they also strive to make society aware of the importance of advocating food democracy at both local and regional scale.

The objective of this second generation of AFNs is to push sustainable food beyond a segment of activist consumers, reaching a significant percentage of total agro-food production and consumption. Scaling deep strategies become especially pertinent within a context in which attributes based upon appreciation of local produce, territorial rootedness, health or respect for the environment play a role in the eating habits of increasingly bigger segments of the population (Forssell and Lankoski, 2015; Aufrère et al., 2019). One indicator of the emergence of sustainable food involves the growing tendency in Spain to consume food bearing ecological certification from 2012 to 2022: expenditure on organic food showed an increase of 187%, compared with an 8.9% growth of total spending on food (household and extra-domestic) (MAPA, 2021, 2023). Nonetheless, in 2022 in Spain ecological consumption only accounted for 2.4% of food consumption volume and 3.4% of its value.

This growing tendency, however, of people to consume food products presenting attributes linked to the environment or to the local context is being exploited by the Big Retailers, who are increasingly employing greenwashing commercial techniques: currently, 45.3% of organic food products are increasingly being marketed through self-service establishments belonging to the Big Retail Sector (MAPA, 2023). Conversely, the absence of capillary and professionalized logistics and distribution networks within the scope of AFNs hinders accessibility by consumers to these outlets.

Sanz-Cañada and Yacamán-Ochoa (2022) point out that one of the principal stumbling blocks hindering scaling of agroecology in Spain involves the total lack of commercial logistics or distribution specific to AFNs, because producers generally address logistics and distribution in an atomized and non-professionalized manner. Cooperative action is the only option with regard to collectively dealing with physical (logistics) and commercial distribution issues (Yacamán-Ochoa et al., 2020); this is a vital task with regard to generating collective action synergies and to reaching a certain degree of economies of scale and scope of these activities (De Roest et al., 2018).

The present paper makes particular reference to agroecological cooperative supermarkets, in relation to which the literature is lacking1, from a vision that analyses them as formulae for the new institutionalization of sustainable food. These are associative consumer initiatives in which the members of the cooperative, dedicated to the retailing of agroecological and sustainable foodstuffs, avail of a physical shop with long opening hours and days; moreover, they dedicate all or a large part of the business to the sale of organic products, which are as local as is possible. These supermarkets are characterized by adopting a participatory and ascending model of governance in which many decisions are taken in assemblies and in thematic commissions.

The paper attempts to investigate the capacity of cooperative supermarkets in Spain to promote scaling-up of food products by means of a double perspective of vertical and horizontal scaling. The research question is whether agroecological cooperative supermarkets constitute a formula for efficient retail distribution for scaling sustainable food in Spain, optimizing the economies of scale and scope at the commercial level.

Firstly, we analyze, from a perspective of vertical scaling, the issues affecting the governance and collective organization of the Network of Cooperative Supermarkets (Red de Supermercados Cooperativos, Section 4.1), set up in May 2022 and currently comprising eleven supermarkets. Secondly, we will employ a perspective of horizontal scaling to investigate the potential for increased numbers of members, as well as the geographic and sociodemographic variables at play which limit the abovementioned scaling; to this end we will employ the case study of the cooperative supermarket La Osa, opened in Madrid in December 2020 (Section 4.2). Lastly, Sections 5 and 6, related to discussion of results and conclusions, provide a debate on the impact of agroecological cooperative supermarkets and their organizations in the vertical and horizontal scaling of sustainable food.

2 Theorical framework: agroecological cooperative supermarkets and scaling of sustainable food

The scientific literature has analyzed and debated the characteristics of the dominant model of food production and marketing at global scale, known as the Big Retail model (Moati, 2001; Sanz-Cañada, 2002; Daumas, 2006). The economic and contractual predominance of the global distribution chains defines a competitive strategy that subjects the prices and commercial profit margins of the different phases of the agro-food chain to strong downward pressure. Although it might seem paradoxical, this also indirectly affects the food chains, which precisely are characterized by representing an alternative to the conventional model.

The alternative food sector therefore needs to adapt strategies that provide a sufficient volume of different food references which are intended to attain economies of scale and scope in order to ensure fair prices and a range of products that can fill the shopping basket in one single establishment. Accessibility to outlets and consumer prices are the two main factors hindering the growth of sustainable food consumer segments. Consequently, there is a need to promote cooperative strategies aimed at optimizing logistics and marketing costs, on one hand, and on the other, to facilitate accessibility both of producers to the exchange or sale centers and of consumers to the retail outlets.

Creating agroecological cooperative supermarkets can help to mitigate these limiting factors. They are not profit-making organizations, and their principal objective is to make quality agroecological food as accessible as possible. One must be a member in order to obtain products in these centers, or at least in some, to pay lower prices. Members contribute small amounts of money to the company capital of the cooperative (in some of them, only at the start, but in others, a monthly fee is paid) and monthly work (a small number of hours per member).

This kind of supermarket, specifically known as “participatory”, obliges members to put in a certain number of hours of work per month in the shop. Although these supermarkets also hire full-time professionals, payroll costs are considerably reduced as a result of these hours worked by the members in tasks such as storage, inventory, cash desk, weighing fruit and vegetables or cleaning, among others.

A common element to be found in the bibliography on agroecological cooperative supermarkets involves the existence of an ascending governance in the taking of the cooperatives' strategic decisions (Hingley et al., 2011; Aufrère et al., 2019; Giacchè and Retière, 2019), a fact that fits well in the mindset of the agroecological movements. In this sense, the aim is to forge close ties between members, thus promoting the sense of belonging to a community, which is further reinforced by the work done by the members in the participatory supermarkets. Hingley et al. (2011) point out that the goal of these cooperative supermarkets should entail linking business networks with social networks, by means of both political participation and community networks.

Grassart (2023) identifies the origin of agroecological cooperative supermarkets as a contemporary adaptation of the two conventional models of food consumption that predominated at different times of the XX century: consumption cooperatives in which there was no real shop opening on a daily basis and with limited opening hours, and self-service shops belonging to the Big Retail model. Unlike the latter ones, second-generation cooperative supermarkets incorporate the political, transformational dimension characterizing agroecological initiatives; additionally, they are becoming consolidated as an alternative, in relation both to the conventional supermarkets and to other types of first-generation alternative food networks (Giacchè and Retière, 2019).

Economies of scale are vital with regard to supplying cooperative supermarkets, compared with the first-generation options: optimizing transaction costs and concentrating the point of sale make sustainable food to be more accessible and affordable to a larger number of people. Cooperative supermarkets constitute an efficient formula for establishing a “fair price” (Aufrère et al., 2019) through strategies aimed at increasing both the number of members and the unitary expenditure per member.

Furthermore, from the perspective of the economies of scope, cooperative supermarkets constitute a realistic option with regard to providing food products presenting values (Lusk and Briggeman, 2009; Lamarque et al., 2023). Thus, compared with the first-generation AFNs, such as consumer groups, these supermarkets enable families to do all their weekly shopping in the same shop, rather than just some of it, due to the large number and diversity of references of food, personal hygiene and household cleaning products on sale. Availing of a wide range of ecological and local products in one single establishment at fair prices enables a family to significantly increase its consumption of value-based food. This is particularly important at the present time, because the lack of time and accessibility is commonplace amongst many responsible consumers, especially in the big cities.

In a context of growing awareness of sustainable food and the consumption thereof, self-service shops should become the future of the scaling of commercial distribution formulae chosen mainly by consumers from the alternative food sector, as currently occurs within the scope of the conventional food system. According to Spain's Food Consumption Panel in 2022, supermarkets, hypermarkets and discount shops represented 76% of the total volume of food purchases in households (MAPA, 2023).

The pioneering reference of this model of consumer and participatory cooperativism is the supermarket Park Slope Food Coop, which opened in 1973 in Brooklyn (New York), closely linked to consumer-based political activism and as a hub for activist engagement (Jochnowitz, 2001; Gauthier et al., 2019; Dee Povitz, 2020). More recently, the model started to reach Europe. In 2016 La Louve opened up in París and in 2018, Bees Coop in Brussels and Camilla in Bologna. In recent years, new cooperative supermarkets have appeared in many cities in France, Switzerland, Belgium and Italy (Giacchè and Retière, 2019), among other countries. In Spain, several establishments have been created since the end of the 2010s. Previously, there had existed some agroecological cooperative supermarkets, which date back, in some cases, to the end of the 1990s (see Section 4).

3 Materials and methods

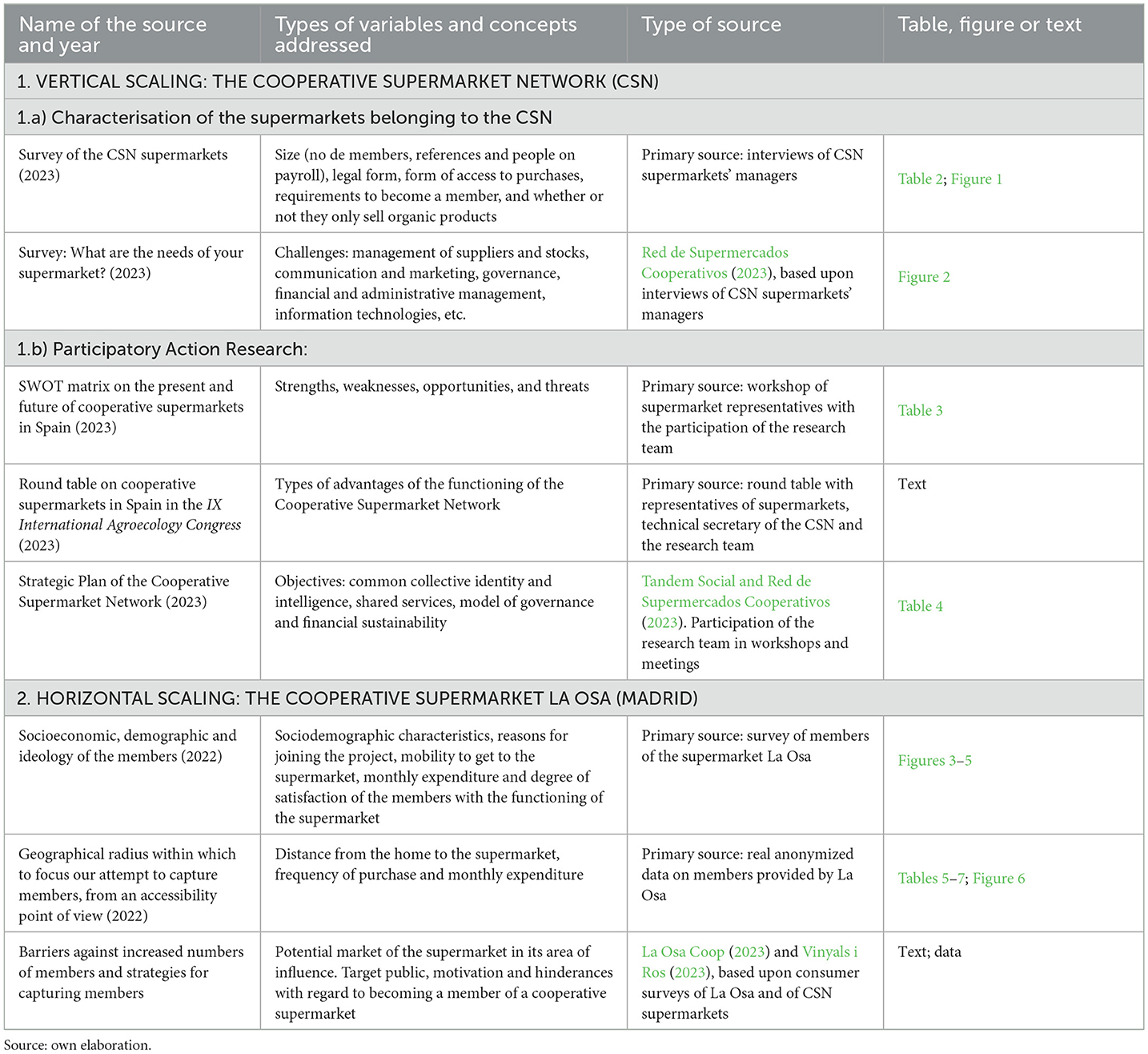

The methodological approach of this article appraises the two variants of sustainable food scaling: vertical scaling, relating to the Cooperative Supermarket Network (CSN) in Spain, and horizontal scaling, corresponding to the case study of a cooperative supermarket in Madrid, La Osa2. We adopted a method based on participatory action research, in which the research team was involved in the processes of creation, promotion or development of the CSN or of La Osa. Throughout 2022 and 2023, we combined primary data gathered from direct observations and participatory events (work groups, workshops, meetings and assemblies) with secondary sources from surveys and reports commissioned by the CSN or by La Osa. Methodological details, including variables and primary or secondary data are outlined in Table 1.

Table 1. Diagram of the methodology employed in the research paper.

3.1 Vertical scaling: the Cooperative Supermarket Network

The CSN facilitates resource sharing and collective strategies among Spain's cooperative supermarkets to promote agroecological consumption and a sustainable, equitable and democratic food model. As of 2023, the CSN comprised 11 supermarkets with 17 shops across 14 municipalities, serving over 11,000 consumers in different regions of the country, and generating over 10 million € in revenue3.

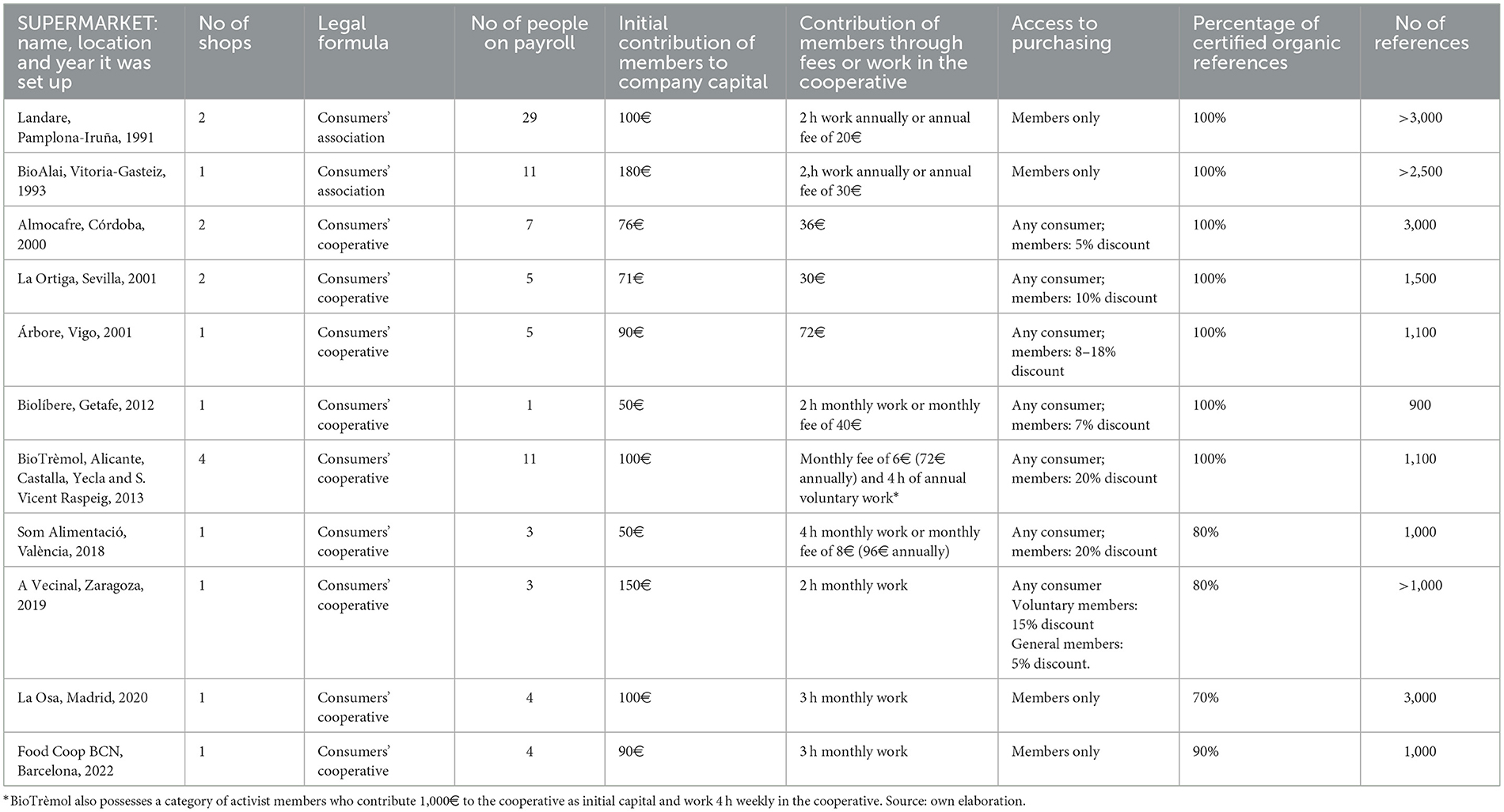

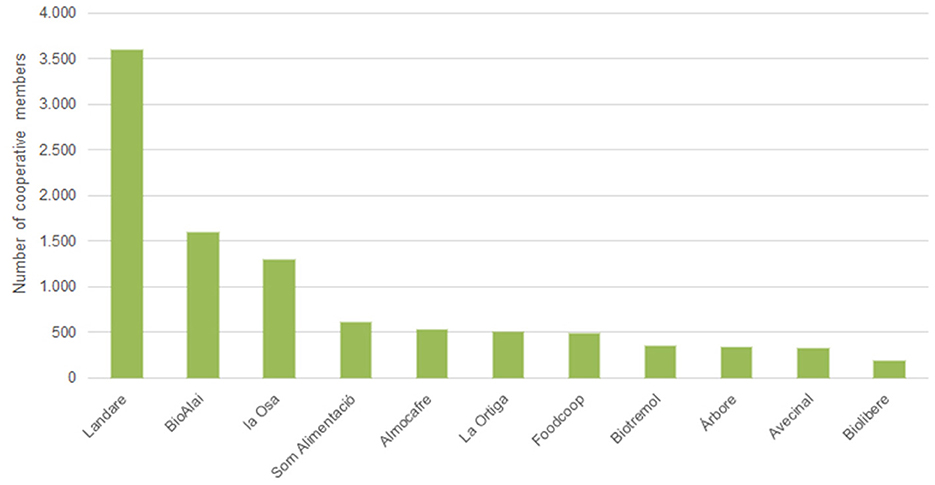

In 2023 we conducted interviews with the managers of the 11 supermarkets4 (Table 1), who answered questions about the main variables characterizing the cooperatives (Table 2; Figure 1, Section 4.1). At the same time, the CSN itself interviewed the managers (Red de Supermercados Cooperativos, 2023), in order to define and prioritize the main challenges facing cooperative supermarkets (Figure 2, Section 4.1).

Table 2. Differential characteristics of the CSN cooperative supermarkets.

Figure 1. Number of members of the CSN cooperative supermarkets (2023). Source: own elaboration.

Figure 2. What are currently the main challenges facing your supermarket? Source: Red de Supermercados Cooperativos (2023).

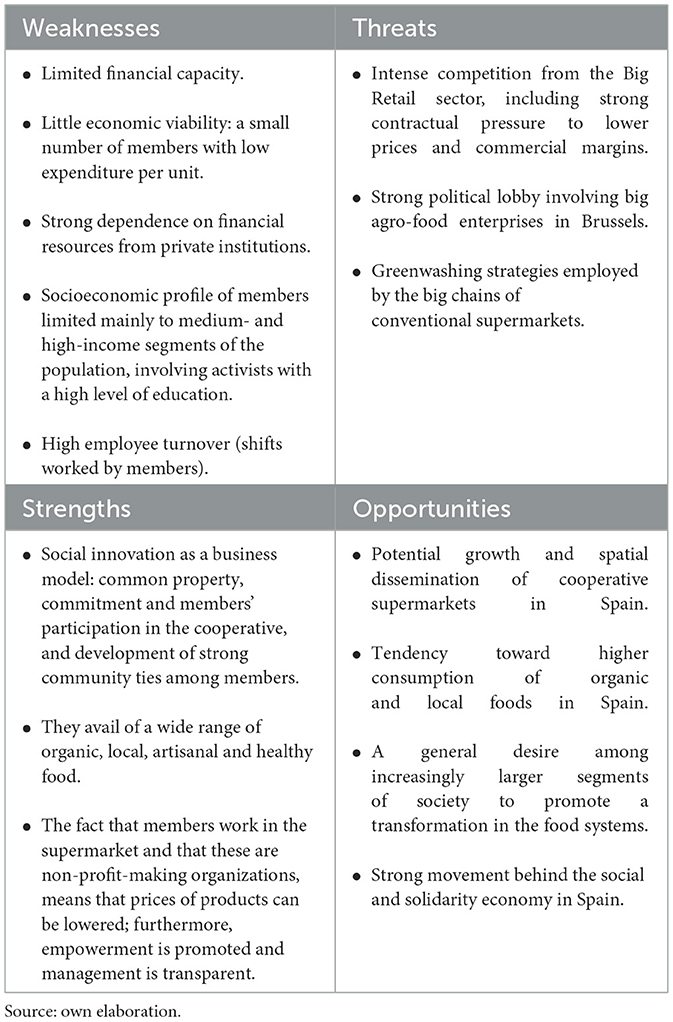

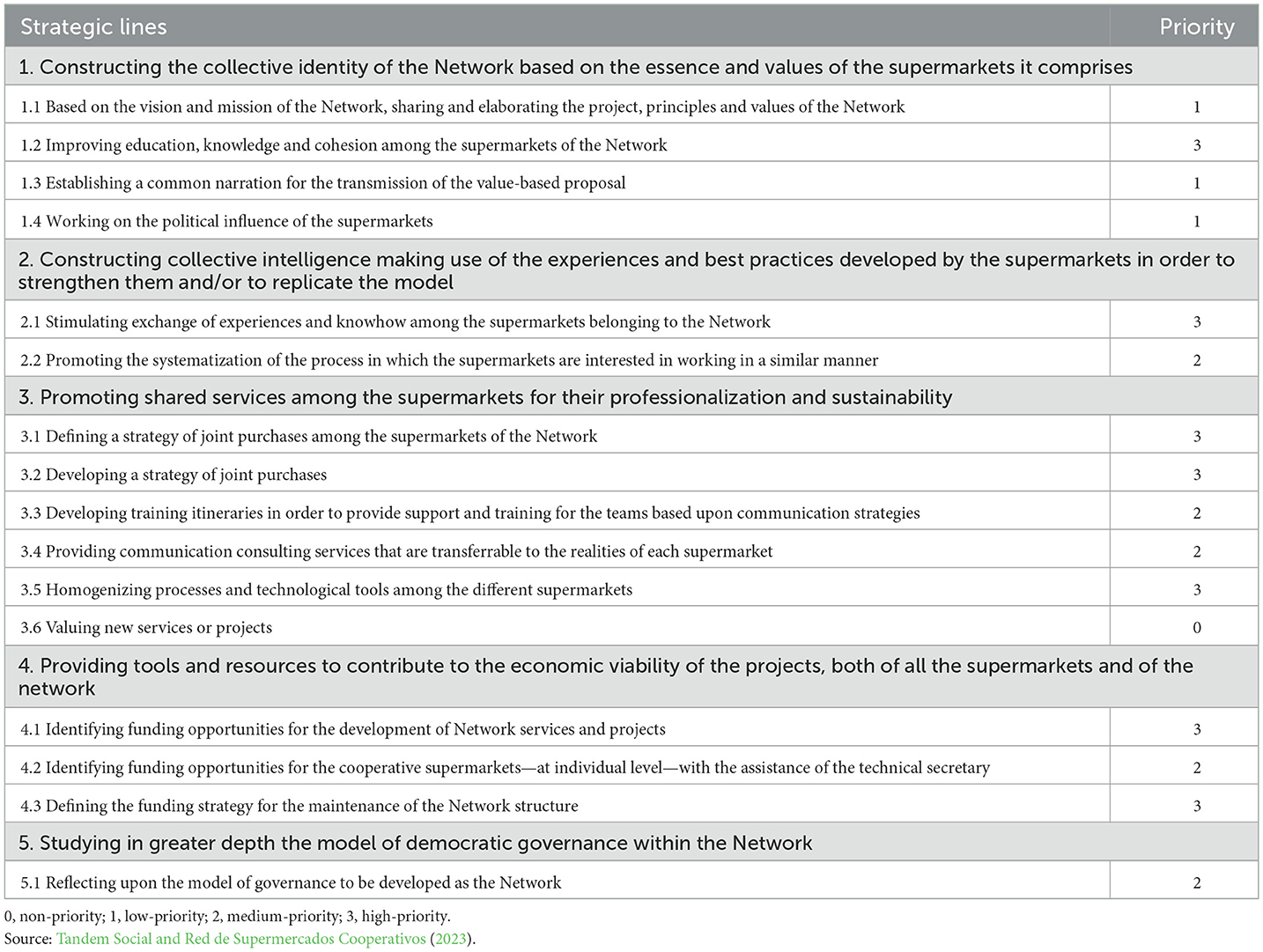

The creation process of the CSN began in the first half of 2022. The foundational assembly (I Congress) took place in Zaragoza in May 2022. The nine participating supermarkets discussed the legal formulae, the mission and vision, the values, the statutes and the internal regulations. Among the results of this first stage, we have selected the SWOT matrix presented in Table 3 (Section 4.1.1.1). In the following months, the CSN focused on launching thematic working groups, which constitute a key axis of the network's functioning. The CSN participated in numerous dissemination and training events, as well as in scientific congresses. For this paper we selected the results of a round table coordinated by the research team in the IX International Agroecology Congress, held in Seville in January 2023. The CSN Strategic Plan was drawn up from April until the end of 2023 (Tandem Social and Red de Supermercados Cooperativos, 2023). A diagnosis was first made of the situation (April–June) by means of individualized interviews with the supermarkets and several virtual collective meetings. The II State CSN Congress, held in Madrid in 2023, was dedicated to defining the strategic lines of the Plan. The consultancy company Tandem Social drew up a draft of the Plan in which five objectives were defined and subdivided into sixteen strategic lines. Finally, the supermarkets categorized these lines as being high, medium or low, or not a priority (Table 4, Section 4.1.1.3)5.

Table 3. SWOT analysis of the activity of cooperative supermarkets in Spain (2022).

Table 4. Prioritization of strategic lines of the Cooperative Supermarket Network.

3.2 Horizontal scaling: the cooperative supermarket La Osa

La Osa, opened in December 2020, is Madrid city's sole agroecological cooperative supermarket. A total surface area of 800 m2 (400 m2 for the sales area) is operated by its members, who must work 3-h shifts every 4 weeks. Only members and people associated with these (five per member) can purchase products, which include food (70% organic), but also household cleaning and personal hygiene products.

Horizontal scaling of La Osa would not only increase the number of members, but also the monthly spending of the current ones. The cooperative currently has high fixed costs intended to finance the debt incurred (700,000€) due to the investments in fixed capital for setting up the supermarket (cameras, shelves, dispensers, lifts, furniture, etc.). The active members (who work shifts and can purchase) total around 710, although the estimates were a lot higher prior to the opening of the supermarket Furthermore, the average expenditure per member in 2022 was 99.30€ a month, which is quite low in relation to an optimal situation in which all members of La Osa did their weekly shopping therein.

There are much fewer active members than total members (1,400). Some of the reasons for this large difference between total and active members are the following: some shareholders join out of empathy and solidarity with the project, but live far away, even in other regions; others are relatives of an active member; in other cases, they have stopped working the obligatory shifts and their status as buyers is therefore withdrawn.

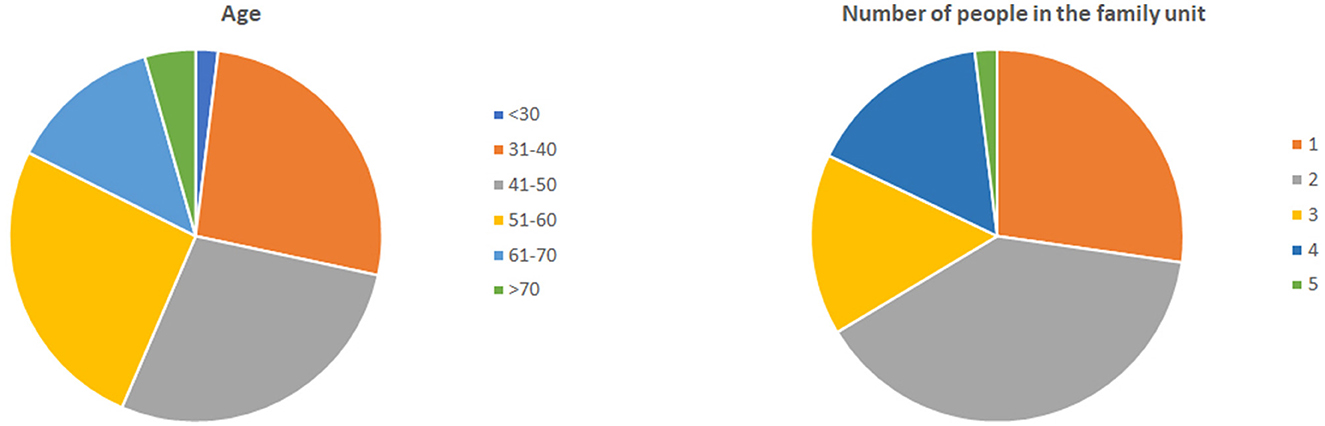

Our objective involves identifying the geographic and sociodemographic variables limiting the recruitment of new members, in a context of horizontal scaling. To this end, we employed two primary sources. In the first place, we examined the sociodemographic, economic and ideological profile of the members in an attempt to define the segments of consumers to whom the communication strategy should be addressed. The research team conducted an on-line survey in 2022 with the supermarket members; of a statistical population of 710 people, 363 members answered. The questions were mostly closed-interval ones (Figures 3–5, Section 4.2.1).

Figure 3. Distribution of members of La Osa supermarket according to age groups and number of people in the family unit. Source: Survey of members of the cooperative supermarket La Osa (2022).

Secondly, we attempted to establish the radius of action to focus our efforts to recruit from a perspective of urban accessibility. We obtained anonymized information on members' households, spending and purchasing frequency (year 2022). In order to ensure members' anonymity, the data on location were spatially aggregated on a continuous mesh of regular hexagons with a 300 m diameter (Figure 6, Section 4.2.2). This tessellation proves to be a better solution than using administrative units, because it helps to mitigate the problem of the modifiable spatial unit (Condeço-Melhorado et al., 2020).

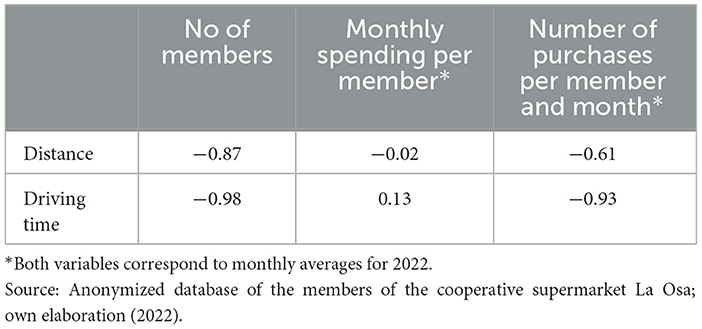

We analyzed the spatial distribution of members within the municipality of Madrid, and calculated the distances and times from members' homes to supermarket, attempting to establish correlations between these variables, on one hand, and purchasing frequencies and monthly spending, on the other. To this end we performed an exploratory analysis, establishing a series of distance intervals (0.5 km) and driving time (5 min), based upon an analysis of the supermarket's commercial area. The network employed for this calculation was the one available for the ArcGIS Pro Network Analyst (Tables 5–7, Section 4.2.2).

Table 5. Correlation coefficient between distance from the home to the supermarket and the variables spatial distribution of the home, expenditure and frequency of members' purchases.

Additionally, to perform a comparative analysis of the results obtained through the primary sources, we employed two studies of particular relevance based on surveys to analyze the reasons why consumers join a cooperative supermarket or the barriers existing in this regard: a survey commissioned by La Osa conducted with 393 people (members and non-members) intended to establish the potential market of the shop (La Osa Coop, 2023); and a study conducted by Vinyals i Ros (2023) on a group of 1,142 consumers belonging to eight supermarkets of the CSN, intended to establish the most effective campaign to increase the number of cooperative' members.

4 Results

4.1 The Cooperative Supermarket Network

One of the CSN's priority objectives involves representing the collective interests of the supermarkets, increasing their visibility at different geographical scales and disseminating this model in society. Moreover, the CSN promotes inter-cooperation among the member supermarkets, enhancing their degree of professionalism, particularly in terms of management and of adopting information technologies. Its governance structure comprises a Governing Body, an assembly (which meets at least once a year), a technical secretary, and several work groups that meet on a fairly regular basis: purchases, communication, information technologies for supermarket management, subsidies (for obtaining financial resources), and a coordination group.

As for the mindsets of cooperative supermarket owners, they can all be said to be clearly committed to promoting sustainable food, agroecology and food sovereignty. Supermarkets websites reflect the following values: links between producers and consumers, the principles of a social and solidarity-based economy, prioritizing local products, reducing the ecological footprint, fair food prices, democratic decision making, or ensuring the economic viability of farming and artisanal agro-industries.

Table 2 and Figure 1 present a series of differential characteristics of the supermarkets belonging to the CSN. The dates on which these were set up in Spain vary from 1991 to 2022. The latest wave, corresponding to those set up as from 2018, is based upon the Park Slope Food Coop (New York) model of participatory supermarket and on that of La Louve (Paris), where members are obliged to participate in work shifts in the supermarket. These cooperative supermarkets are dispersed through the country, but they are all situated in different-sized cities. All these supermarkets require an initial contribution from the members to the company capital as a condition for joining: this ranges from 50 to 180€. A feature differentiating these supermarkets from conventional ones is that all or most of the references are certified as organic: the minimum percentage corresponds to La Osa (70%), but most of these supermarkets only sell organic food.

There is a high degree of variability in the number of members in the supermarkets and in the people on the payroll: Landare stands out due to possessing two shops, 3,600 members and 29 people on the payroll; BioAlai has 1,600 members, 11 people on the payroll and one shop; at the other end of the spectrum is Biolíbere, with only 180 members, one shop and one worker on the payroll. The figures concerning Landare and BioAlai are explained by the fact that they are pioneer in Spain (1991 and 1993, respectively) and because they are located in regions (Navarra and Basque Country) presenting strong rootedness in the social and solidarity economy.

The number of references of these supermarkets ranges from 900 to over 3,000: four of them (Landare, Almocafre, La Osa and BioAlai) have over 2,500, a figure that indicates considerable variety, compared to consumer groups or other alternative food networks; however, a conventional supermarket offers between 5,000 and 10,000 references.

The predominant legal formula is the consumer cooperative, but only two supermarkets are consumers' associations (similar to cooperatives, but with fewer legal requirements). These supermarkets are non-profit-making companies whose business model prioritizes participation, democratic decision making, transparency and social responsibility. They all avail of a Governing Body, which serves to manage the cooperative, and a general assembly, which is the organ taking strategic decisions and which is accountable to the members. The participatory work is also specified in the commissions and work groups that address themes such as purchases, communication, economy, governance, gender, information technologies or measures for reducing environmental impact (sale of products in bulk, reducing the plastic used in packaging, etc.).

Transparency in gross margin policy is a crucial feature that characterizes the model of CSN supermarkets: they have only one or a very small number of fixed margins (2–3) on all products, which is around 20–25%. The supermarkets opened in 2018, which broadly follow the model of the La Louve supermarket in Paris, are particularly committed to this strategy, which aims for a single margin. They reject the margin compensation policy used by the large-scale retail sector for reasons of fairness in the value chain.

Other characteristics that best differentiate the model of organization of the cooperative supermarkets belonging to the CSN are: (i) the modality of access to purchases in the supermarket; (ii) the existence (or not) of compulsory work shifts each month; (iii) the existence (or not) of monthly or annual fees to be paid by members. In the first place, in four of the supermarkets, only the members and the people associated with these can purchase, whereas in the seven remaining ones, everyone can buy products, whether a member or not: members can shop at lower prices, which ranges from a 5 to a 20% discount. In the second place, the shifts are obligatory in three supermarkets and not in seven of them, but the members pay a fee in the latter ones; finally, one supermarket (Som Alimentaciò) permits members to choose whether they pay a fee or work a shift.

Figure 2 analyses current challenges of cooperative supermarkets. Most of them highlight the need for more members, in order to scale, due to the need to address the high fixed costs through a bigger sales volume: “achieving financial sustainability” and “increasing the number of members” provided seven positive answers. It should also be pointed out that six supermarkets responded positively to the challenge “increasing the amount of work done by members in the cooperative (both voluntary and obligatory)”, in order to reach organizational sustainability.

On a second plane, the cooperative supermarkets prioritize the challenges relating to professionalization, above all with regard to the management of references and to ERP (enterprise resource planning) by means of information technologies: “improving management with ERP,” “improving management of purchases and sales,” “improving accounts and administration management,” and “improving training of hired staff” elicit five positive answers. It should be kept in mind that the cooperative supermarkets are burdened with huge transaction costs in relation to suppliers, stocks and references. Scaling through a strategy of joint purchasing by the CSN supermarkets could help to address this issue.

Other challenges, such as setting up an on-line shop or increasing the number of staff hired, might appear to be a priority, but the supermarkets do not highlight them. It is also worth mentioning that although social justice is an objective of cooperative supermarkets, it is so difficult to achieve profitability that, in the absence of high impact public policies, there is little chance of implementing initiatives aimed at bringing disadvantaged social groups into supermarkets.

4.1.1 Participatory action research

4.1.1.1 SWOT analysis

Table 3, based upon the results of a workshop held at the CSN foundational Congress, provides the following results relating to a SWOT analysis of the cooperative supermarkets in Spain. The cooperative supermarkets indicate that they suffer numerous weaknesses in terms of economies of scale and scope in relation to supply (De Roest et al., 2018). This contrast with the Big Retail Sector, which optimally manages a huge number of references, merging cutting edge information technologies with a highly advanced logistics structure. The limited financial capacity and poor economic viability of these supermarkets means that they have serious problems with regard to running communication campaigns, implementing other marketing strategies and adopting information technologies in a truly professionalized manner. To this end they necessarily must increase their volume of billing, whether through increased numbers of members or greater expenditure per unit of current members. The lack of real support from public policies, especially certain regional governments, also constitutes a weakness in the initial stages following the creation of the supermarket. Participants in the workshop also considered as a weakness the fact that the socioeconomic profile of potential members mainly involves segments of the population with a high level of education and an activist profile, because this limits the potential social base and hinders recruitment of new members. It was also pointed out that the voluntary and compulsory shifts worked by the members implies a high job turnover, which can sometimes jeopardize efficiency.

Secondly, the fierce competition in prices and costs from the Big Retailers poses a serious threat, because this gives rise to a clearly unequal competitiveness, due to the fact that the big commercial chains represent an oligopoly, and therefore have a strong influence on regulations and policies. On the contrary, cooperative supermarkets attempt to obtain fair prices for their producers; they accept the pricing established by the sovereign decisions of producers, and they apply profit margins that reward their commercial function. Additionally, greenwashing and localwashing strategies by the big conventional supermarket chains can coopt a large part of the increased demand for organic and local food products that have helped to create the alternative networks.

The main strength of the model of cooperative supermarkets is precisely the fact that they constitute a social innovation based upon principles of the social and solidarity economy, on bottom up governance and on the development of strong community ties among members. The criteria influencing producers supplying the supermarkets depend upon certain values framed within the scope of Agroecology: values-based food should constitute the main axis of cooperative supermarkets' strategies for differentiation and marketing mix. Furthermore, compared to other options such as consumer groups, the shops avail of a wide range of organic, local, seasonal, artisanal and healthy food products. Other strengths that offset the unequal competitiveness in prices and costs of the cooperative supermarkets in relation to the Big Retailers are, on one hand, the voluntary and compulsory shifts worked by cooperative members and, on the other, the fact that the cooperatives are non-profit organizations. In addition, members' participation in the cooperative generate empowerment of them.

As for opportunities, these cooperative supermarkets have a good potential for billing and geographic expansion, due to the continuously growing demand for organic foodstuffs in Spain in the last decade and to the increasing taste of consumers for local produce. Likewise, increasing numbers of consumers are criticizing the predominant conventional food model. All these factors constitute a necessary condition for scaling the sustainable food system, provided that the Big Retail sector does not absorb the lion's share of the increased demand for organic and local food. Additionally, we also consider as an opportunity the strong support for model of cooperative supermarkets in Spain by REAS, which is the network of networks of the social and solidarity economy.

4.1.1.2 Advantages of networking for cooperative supermarkets

During the IX International Agroecology Congress in Seville in January 2023, the research team organized a round table featuring the CSN's technical secretary and representatives from four network supermarkets. The discussion focused on two main questions: (i) the primary challenges for the survival of cooperative supermarket models; (ii) the benefits of supermarkets functioning as a network, especially within the CSN. Below is a summary of the debate.

Firstly, cooperative supermarkets need political influence to shape legislation in order to support their model, focusing on bulk product sales, reusable packaging management, and other aspects of the circular economy. This is crucial to counteract the greenwashing conducted by Big Retailers.

Secondly, the round table agreed on the vital importance of establishing alliances with agroecological suppliers' logistic centers to boost supply capabilities. Collaborating with food hubs not only secures a more efficient supply of fresh local products, but also strengthens network relationships with key suppliers, improving economies of scale and scope in the supply of supermarkets.

Thirdly, adopting and sharing technological tools, such as the Odoo management system, was proposed as a way to enhance collective purchasing, stock and information management, accounting and business activities and online sales This leads to more efficient management and cost reductions.

In fourth place, there is a need to increase the economies of scale in the supply system by enabling collective buying by the CSN. Although geographic dispersion of supermarkets limits the advantages that might exist, these joint purchases have already started with non-local products like tropical fruits, bananas from the Canary Isles, cleaning products and cosmetics, etc. Creating a common supplier database is crucial for this initiative.

In addition, a proposal was made for the development of a collective brand involving producers and supermarkets to certify that the shared agroecology-based values had been respected regarding product origin and socio-environmental commitment in production processes. Campaigns focusing on these values through communication and marketing content were also recommended. Additionally, proposals included actions to develop specialized training programmes in sustainable food trade, a cloud-based virtual space with training resources, and an incubator for cooperative supermarkets providing integral support during the establishment and initial stages.

4.1.1.3 Strategic Plan of the Cooperative Supermarket Network

The Strategic Plan represents a significant milestone in our participatory research. Within the dynamization process of the consultancy company Tandem Social, five objectives were defined and subdivided into sixteen strategic lines. The supermarkets classified each of these lines into four categories (Table 4): seven high-priority ones, five medium-priority, three low-priority, and one considered to be non-priority.

A key limitation for advancing strategic lines involves the workload of the technical secretariat. In the short term, high-priority lines will be promoted, followed by medium-priority ones in the medium term. Joint provision of services drives the CSN's creation and its commissions and work groups. Thus, supermarkets prioritize defining and developing a joint purchasing strategy, as well as incorporating management information technologies (3.1, 3.2 and 3.5). Surprisingly, the adoption of joint communication strategies is seen as a medium-level priority (3.3 and 3.4). Given the significance of financial sustainability for the continuity of CSN, funding strategies (4.1 and 4.3) constitute a high-priority. Creating a collective identity based upon mutual supermarket is also deemed to be crucial (1.2 and 2.1).

4.2 La Osa cooperative supermarket

4.2.1 Sociodemographic profile, purchases, and motivations of the members

To implement horizontal scaling strategies focusing on increasing the number of members, the supermarket's target public is crucial, as this influences the potential demand for value-based food products. Analysis of the survey reveals that the majority of the interviewees possess quite a high educational level, with 90% possessing a university degree and 10% having completed secondary education. Moreover, 60% are women and 40% are men. Most members are mainly in their thirties, forties or fifties (Figure 3), comprising 80.9% of the total. Family units with one or two members are predominant, making up 62.8% of the cooperative members.

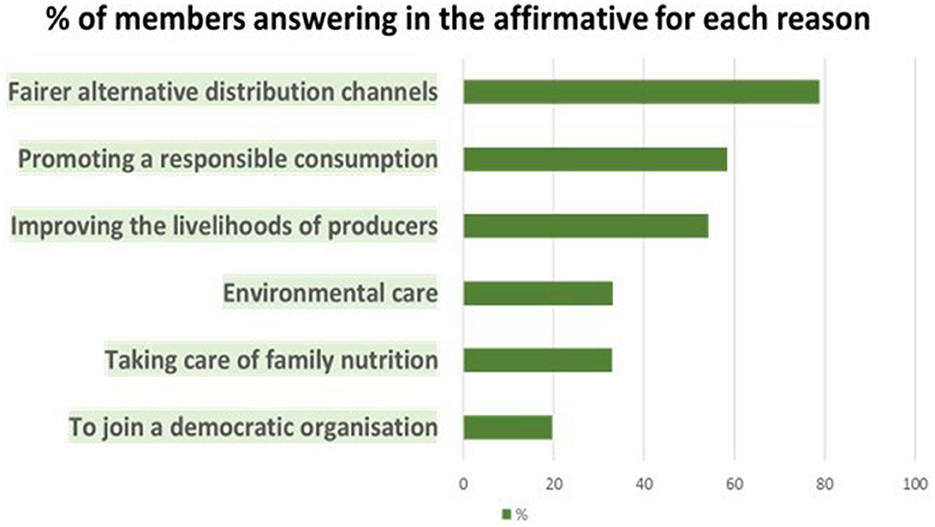

Figure 4 shows that La Osa cooperative members are highly aware of sociopolitical aspects in the agro-food chain, prioritizing fair distribution channels and responsible consumption; they prioritize these aspects above any generic questions referring to the environment or health-related ones. Specifically, 78.9% participate in order to strengthen fairer distribution channels, 58.4% to promote responsible consumption, and 54.3% to improve producers' livelihoods. Moreover, 58.1% are involved in other agroecology-related organizations or associations.

Figure 4. Reasons for becoming members of the cooperative The interviewees were requested to choose, through non-exclusive answers, three of the preselected reasons. Source: Survey of members of the cooperative supermarket La Osa (2022).

These results reflect an activist profile and basically coincide with those obtained by Sanz-Cañada et al. (2018), in a study on consumer groups in the Lavapiés neighborhood in Madrid, and by the La Osa Coop (2023), in a study on a very large sample of the supermarket's consumers.

The latter source reveals that 78% of interviewees joined La Osa to align their purchases with their values. Over 60% of the members were motivated both by buying organic and local products and by the goal of social transformation of the agro-food system. Members present fit a consumer profile of empowered activists, “involving social awareness, and seeking and valuing quality and products that generate a low level of environmental impact”.

Vinyals i Ros (2023), on interviewing a sample consisting of members of eight supermarkets belonging to the CSN, also identified a strong demand for value-based food products. High percentages of interviewees cited reasons for participation such as the sale of organic products (74.6%), of local food (63.9%), promoting social transformation (60%), responsible consumption (62.3%), or healthy food products (57.5%). Of less importance for these activist consumers were price (14.6%) or variety of products (13.9%).

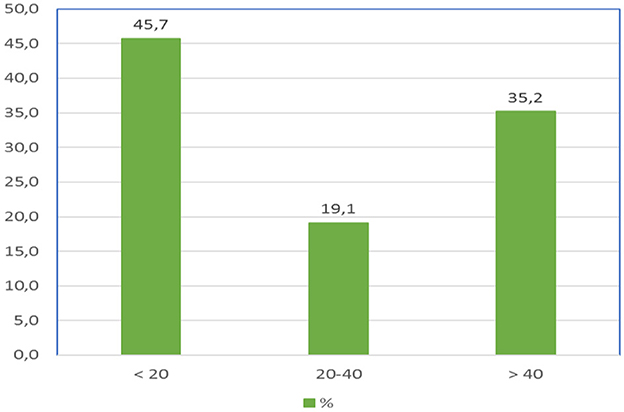

When analyzing the distribution of the interviewees into three groups, according to total expenditure on food (Figure 5), 45.7% spend <20% of their family budget in the supermarket, a figure that rises to 64.8% if expenditure is below 40%. Despite a high degree of satisfaction with the supermarket's functioning and product quality, most members do not spend a significant proportion of their family budget to La Osa.

Figure 5. Percentage of members according to proportion of family expenditure on food in the La Osa supermarket. Source: Survey of members of the cooperative supermarket La Osa (2022).

We detected a high degree of satisfaction among interviewees regarding purchases and supermarket functioning. Using a scale from 1 to 7 (7 being the highest), 92.6% expressed a high degree of satisfaction (categories 5–7), 90.3% were satisfied with rapport and kindness among members, and 83.5% were content with the treatment provided by the consumer office. Additionally, 74.9% rated La Osa's variety and quality as being high or very high (5–7).

Members were also asked about their means of transport to do the shopping: 25.6% walk, 42.2% go by car, 21.9% by public transport, and a minority of consumers go by bicycle or motorcycle. That is to say, one fourth of the consumers do their shopping within the commercial area of influence that is equivalent to 15 min walking distance.

Lastly, the interviewees were asked about their satisfaction with the compulsory work shifts. Initially viewed as an empowerment tool and an element for project identification, 71.1% said they enjoyed the shifts (very much or quite a lot) on a scale from 1 to 5, whereas only 5.8% dislike them a little, or really dislike them. Moreover, regarding the regulations facilitating participation and ensuring commitment in the shifts, 64.1% answer positively, whilst 2.2% had a negative opinion.

4.2.2 Barriers to horizontal scaling: distance from members' homes to the supermarket

Both Vinyals i Ros (2023) and La Osa Coop (2023) surveyed consumers regarding the main obstacles to joining a cooperative supermarket: the first source surveyed consumers from the all of the CSN supermarkets, whereas the latter one asked people belonging or close to the supermarket La Osa (both members and non-members). Distance from the home to the supermarket emerged as a significant factor in both studies, with 64 and 81% of respondents citing it as an impediment, respectively. Furthermore, both studies coincide in identifying other important barriers: higher food prices (70 and 63%, respectively), lack of project awareness (64 and 57%), and specifically for La Osa, a lack of time to work the shifts (55%).

Analyzing the distance from the home to the supermarket as the principal barrier to increasing membership, there is a need to establish the supermarket's commercial influence area and the profile of potential consumers, in order to plan a suitable campaign to recruit members. Using data from La Osa's 2022 membership, we created a tessellation and aggregated data on numbers of members, total number of annual purchases, and total annual expenditure (Figure 6). The graph reveals a general decrease in the all three variables on increasing the distance from the home. One spatial exception to this pattern can be observed: an area to the south of the supermarket, in the vicinity of the Malasaña and Chueca neighborhoods, shows higher values for these variables. This area corresponds to the previous location of the shop selling organic food product (named 2decológico), which preceded and led the creation of La Osa in 2020.

Figure 6. Spatial distribution of the homes of the supermarket members, of their purchasing frequency and of their annual expenditure in La Osa. Source: Anonymized database of the members of the cooperative supermarket La Osa; own elaboration (2022).

We also analyzed the degree of correlation between the distance from the home to La Osa, in real distance and driving time, and, respectively, number of members, monthly spending and purchasing frequency (Table 5). Results show that the further away the home is from the shop, logically, there will be fewer members, with regard both to distance (r = −0.87) and in particular, to time (r = −0.98). The purchasing frequency of members is greater when they reside closer to the supermarket, which can clearly be seen when expressed in driving time (r = −0.93). Monthly spending, however, is relatively independent from distance from the home (r = −0.02 in distance and 0.13 in time): although it might seem paradoxical, the monthly spending per member is statistically independent from the distance variable: the predominant behavior of the activist consumer of La Osa indicates that members who live further away from the shop purchase less frequently than those living closer, but they spend more per visit.

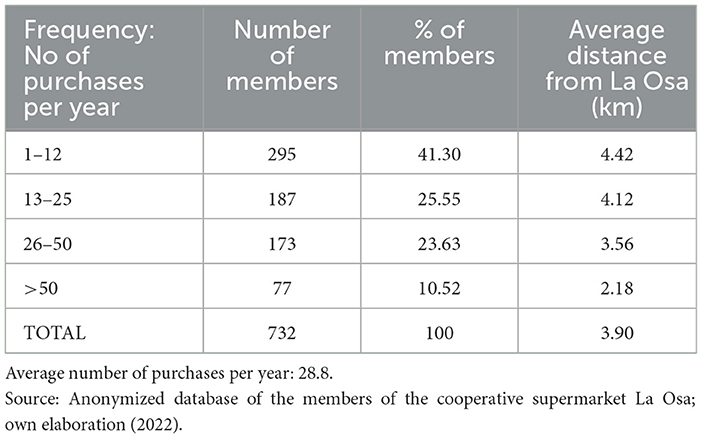

Additionally, we analyzed per purchase frequency intervals the number of members and average distance from the supermarket (Table 6). We observed that the lower the purchase frequency interval, the shorter is the average distance from members' houses to La Osa. Nonetheless, the lowest interval (1–12 purchases) corresponds to a frequency of fewer than 13 purchases, which reflects the number of compulsory shifts worked each year by the members of the cooperative: 41% purchasing with this frequency. This infrequent shopping pattern has negative economic implications for the cooperative's viability. Moreover, only 11% of members shop at least once a week, which corresponds to the interval of over 50 yearly purchases.

Table 6. Number of members and distance from the supermarket according to intervals of annual purchasing frequency.

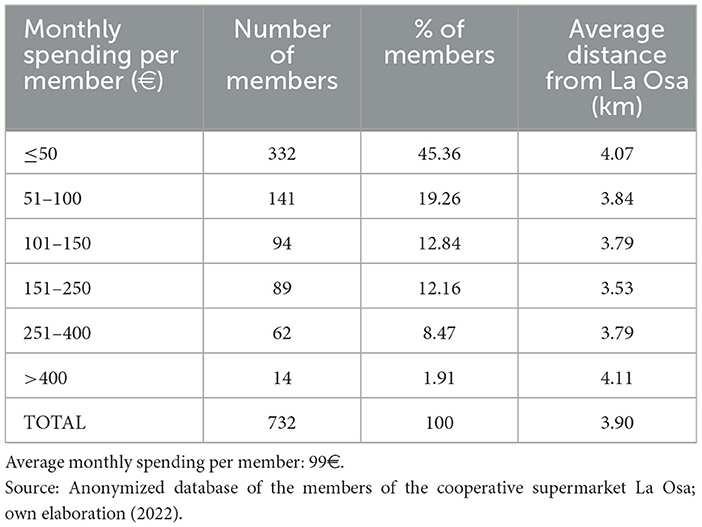

Finally, we studied the number of members and distance from the supermarket according to intervals of monthly expenditure in the supermarket (Table 7). Interestingly, we found no significant differences in average distances across different expenditure intervals, suggesting a statistical independence between monthly spending and distance. However, only 22.5% of members spend over 150 euros a month in La Osa: this is an amount deemed necessary to cover operational and financial costs. The average monthly spending per member is 99€, with 45% of the members spending 50€ or less every month. Many members' spending falls short of covering operational costs, a fact that jeopardizes the profitability of the project.

Table 7. Number of members and distance from the supermarket according to monthly expenditure intervals.

5 Discussion

The present research reveals that cooperative supermarkets face various challenges associated with vertical scaling within the CSN. The joint provision of services emerges as a key advantage in the operation of the CSN. In particular, we highlight the importance of transitioning toward a common central purchasing office, sharing and developing technological tools, and enhancing collective promotion and communication efforts. Another priority goal of the CSN is to gain political influence in society for both promoting responsible consumption and engaging public administrations in order to develop policies that reward public goods inherent to this kind of consumption.

Our study has shown that a consumer segment based upon the values associated with responsible consumption predominates in the Spain's agroecological cooperative supermarkets. As for horizontal scaling, one of the main aims of the cooperative supermarkets set up during the last decade in Spain involves recruiting a greater number of members in order to achieve economies of scale in supply and marketing. In our case study of La Osa supermarket, one of the most pressing issues involves paying off the debt resulting from investments in fixed capital in order to set up the supermarket6.

In addition, we analyzed the socio-economic profile of La Osa's potential members in order to profile target consumers for these supermarkets and to identify the barriers preventing new members from joining: it falls within the segments of the population with medium and high-level incomes, a high level of education, and an activist profile, all of which limits the potential social base. These consumers prioritize attenuating environmental impacts, improving animal welfare and promoting social justice. According to Piracci et al. (2023), they are known as sustainability-focused consumers: they demonstrate a profound understanding of the sustainability-related challenges agro-food systems are facing, from a political and holistic point of view, and are often engaged in volunteerism within social, ecological, and political organizations.

The empowered activist consumers can generally be said to prevail in La Osa. Empirical research has revealed that this typology of consumer presents high levels of satisfaction with the work shifts, with the functioning of the supermarket and with the personal relationships with other members of the cooperative La Osa. We have verified that, once activist members join the cooperative, they do not necessarily spend less due to being further away from the shop; rather, although they shop less frequently, they tend to spend more on each visit.

Thus, a shop is better situated when it is closer to city center neighborhoods, as these predominantly present the abovementioned profile. These areas of Madrid, however, are usually undergoing gentrification, which raises land prices, and consequently, rents are usually sky-high, beyond the reach of the cooperative supermarkets: this required locating the supermarket in a working-class neighborhood (La Ventilla) in the city's expansion area, where becoming a member of a cooperative is not always commonplace. It is therefore difficult to find more activist consumers within the commercial area of influence—a 15-min walk from the supermarket. This typology of consumer should be sought in a wider area of the city, albeit in an isochronic area—up to a 20-min drive from the supermarket.

A second type of consumer segment, which Piracci et al. (2023) classify as naturalness and health driven consumers, corresponds to non-activist consumers7, basically concerned with their health and exhibit environmental awareness in a less political or social version than the sustainability-focused consumers: in their consumption they prioritize values such as those relating to naturalness, healthiness and seasonality. For them, the distance from home to the supermarket, the perception of prices and the compulsory work shifts necessary for the functioning of these participatory supermarkets can constitute a barrier to joining the cooperatives. In the investigation conducted on La Osa, a distance over than 1–1.5 km from home to the shop becomes an impediment to shopping. This is reinforced by the following facts: on the one hand, consumer preference for proximity shopping is very high in Spain, due to the dense distribution of commercial outlets, and, on the other hand, because large retailers increasingly market organic and local products. The aforementioned circumstances could dissuade non-activist consumers from walking over 15 min from their home to the shop.

In other matters, we have discovered that a significant number of members make a monthly purchase that is far below the necessary threshold of 150€ a month. Consequently, although recruitment of new members has heretofore been considered a priority, particular emphasis should also be placed on loyalty strategies directed toward current members. Of the many strategies existing in this sense, we can highlight the need to continue promoting and improving internal communications, a more visually attractive shop, emphasis on the emotional factors linking consumers with producers and with agricultural landscapes, or showing the lower prices of specific products both on the networks and in the shop.

6 Conclusions

Firstly, we verify the hypothesis put forward in the Introduction. The different strategies for achieving horizontal scaling (increasing the number of members) and vertical scaling (networking) used by the agroecological cooperative supermarkets constitute valid tools, as well as an efficient retail formula with regard to scaling sustainable food products in Spain. As opposed to the first-generation options for responsible consumption, these second-generation alternative food networks (Sage et al., 2021) appear to contribute to generating significant economies of scale and scope. This is a result of concentrating a large number of consumers in one sales point where they can do all their shopping for value-based products at affordable prices.

Secondly, the implementation of strategies for improving the vertical scaling of agroecological cooperative supermarkets through the development of a national network, such as the CSN, constitutes a social innovation based on the principles of agroecology and of the social and solidarity economy. The goal of the CSN does not only involve consolidating the networking of existing agroecological cooperative supermarkets, but also intends to replicate the model in other territories, municipalities and neighborhoods. We have observed that, in turn, most CSN supermarkets claim that their principal challenge involves promoting horizontal scaling in order to achieve financial sustainability by offsetting distributing costs by means of a higher sales turnover. Due to the limited financial capacity and the difficult economic viability of the supermarkets, other challenges, such as the professionalization of management or the adoption of information technologies, also very much depend upon a sufficient scale in sales turnover.

Considering the typology of potential consumers who can adhere a cooperative supermarket, combined strategies aiming at attracting not only sustainable-focused consumers but also those driven by naturalness and health-related issues. Once the segment of empowered activist consumers residing in an isochronous zone (up to 20 min drive) from the supermarket La Osa has become relatively saturated, it is necessary to focus on strategies for attracting the segment of naturalness and health-driven consumers. Nonetheless, the sociodemographic characteristics of the neighborhood where the supermarket is located make it difficult to attract the latter typology of consumers as new members in the commercial area of influence (a 15-min walk).

Consequently, there is a need to consolidate the emerging process of developing the CSN, which is only just starting out, in order to obtain significant synergies deriving from the vertical scaling process. However, development and consolidation of these agroecological cooperative supermarkets in Spain involve embryonic horizontal scaling strategies; these highlight the need not only to recruit new members, but also to focus specifically on loyalty strategies among existing members.

Whatever may be the case, the essence of these recruitment and loyalty campaigns should place especial emphasis on scaling deep strategies (Moore et al., 2015) based upon the transmission of positive emotions associated with the values of sustainable food products, which differ from the organic and local products sold in conventional supermarkets. Several distinctive features of the cooperative supermarket model merit emphasis, notably its foundational values: community engagement, member empowerment, a sense of belonging to the cooperative, fair prices, establishment of emotional connections with producers, and the contribution this model makes to the ecological and social transition of the agro-food system.

Finally, the limitation of our study involves its exclusive focus on cooperative members and agroecological supermarkets, which may cause bias in relation to broader consumer engagement and horizontal scaling strategies. Future research involving the perspectives of non-members will likely enhance our understanding and help to develop more inclusive scaling strategies.

Data availability statement

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

Author contributions

JS-C: Conceptualization, Formal analysis, Funding acquisition, Investigation, Methodology, Project administration, Resources, Supervision, Validation, Visualization, Writing – original draft, Writing – review & editing. CY-O: Conceptualization, Investigation, Methodology, Visualization, Writing – original draft. RP-C: Conceptualization, Formal analysis, Methodology, Visualization, Writing – original draft.

Funding

The author(s) declare financial support was received for the research, authorship, and/or publication of this article. This publication is framed within the research grant “Sustainable food networks as chains of values for agroecological and food transition. Implications for territorial public policies” (PID2020-112980GB-C22; 2021-2025), funded by the Spanish Scientific, Technical and Innovation Research Plan: MCIN/AEI/10.13039/501100011033.

Acknowledgments

The authors would like to thank to the Technical Secretary and to our colleagues in the Red de Supermercados Cooperativos (Cooperative Supermarket Network) for all their collaboration. We are also indebted to the Governing Body, to the staff, and to our colleagues from La Osa cooperative supermarket.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

The author(s) declared that they were an editorial board member of Frontiers, at the time of submission. This had no impact on the peer review process and the final decision.

Publisher's note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Footnotes

1. ^An extensive search provided the following results: Jochnowitz, 2001; Hingley et al., 2011; Aufrère et al., 2019; Gauthier et al., 2019; Giacchè and Retière, 2019; Dee Povitz, 2020; Hispacoop, 2020; Rocas-Royo, 2021; Grassart, 2023.

3. ^Funding, both from the Carasso Foundation and the Spanish government's EU-funded Recovery, Transformation and Resilience Plan (PERTE), proved to be crucial to finance the CSN, as it covered, among other expenses, two years' salary for the technical secretary.

4. ^After the CSN had been set up with new supermarkets, these were joined in the Network by BioAlai, de Vitoria and Som Alimentaciò, from Valencia, in 2023.

5. ^This Strategic Plan also contemplates deploying the lines with their respective schedules and funding plan, a whole series of recommendations and a contingency plan.

6. ^A new strategy was recently introduced by La Osa in an attempt to increase their sales turnover: this allows each member to have up to five associates who are not required to work shifts or pay any amount to the cooperative's company capital.

7. ^The third and last typology of consumers characterized by Piracci et al. (2023) is the so-called private benefit seekers, referring to the consumer who shows few ethical or environmental values, choosing products for their price, quality or appearance or for health-related reasons. This type of consumer would be the least likely to join an agroecological cooperative supermarket.

References

Aufrère, L., Eynaud, P., Gauthier, O., and Vercher, C. (2019). Entreprendre en commun(s). Une étude du processus de création d'un supermarché coopératif et participatif. Revue française Gestion 279, 83–96. doi: 10.3166/rfg.2019.00332

Condeço-Melhorado, A., Mohino, I., Moya-Gómez, B., and García-Palomares, J. C. (2020). The Rio Olympic Games: a look into city dynamics through the lens of Twitter data. Sustainability12:7003. doi: 10.3390/su12177003

Daumas, J. C. (2006). Consommation de masse et grande distribution: une révolution permanente (1957-2005). Vingtième siècle Revue d'Histoire 91, 57–76. doi: 10.3917/ving.091.76

De Roest, K., Ferrari, P., and Knickel, K. (2018). Specialisation and economies of scale or diversification and economies of scope? Assessing different agricultural development pathways. J. Rural Stud. 59, 222–231. doi: 10.1016/j.jrurstud.2017.04.013

Dee Povitz, L. (2020). Nourishing progressive ideals in dark ages: boycotts at the Park Slope Food Coop in the 1970s. Soc. Hist. 53, 373–398. doi: 10.1353/his.2020.0018

Ferguson, B. F., Aldasoro Maya, M., Giraldo, O., Mier, M., Giménez Cacho, T., Morales, H., et al. (2019). Special issue editorial: what do you mean by agroecological scaling? Agroecol. Sustain. Food Syst. 43, 722–723. doi: 10.1080/21683565.2019.1630908

Forssell, S., and Lankoski, L. (2015). The sustainability promise of alternative food networks: an examination through “alternative” characteristics. Agric. Hum. Values 32, 63–75. doi: 10.1007/s10460-014-9516-4

Gauthier, O., Léglise, L., Ouahab, A., Lanciano, É., and Dufays, F. (2019). Food Coop 2016 - Tom Boothe, Vol. 22. M@n@gement, 671–702. Available online at: https://management-aims.com/index.php/mgmt/article/view/4261 (accessed March 26, 2024).

Giacchè, G., and Retière, M. (2019). The “promise of difference” of cooperative supermarkets: making quality products accessible through democratic sustainable food chains. Rev. Desenvolvimento Regional 24, 35–48. doi: 10.17058/redes.v24i3.14002

Grassart, C. (2023). Les supermarchés coopératifs et participatifs, un modèle socio-productif émergeant? Revue Régul. 34:22518. doi: 10.4000/regulation.22518

Hingley, M., Mikkola, M., Canavari, M., and Asioli, D. (2011). Local and sustainable food supply: the role of European retail consumer co-operatives. Int. J. Food Syst. Dyn. 2, 340–356. doi: 10.22004/ag.econ.121953

Hispacoop, AAVV. (2020). Un nuevo modelo de cooperativismo de consumo. Cuadernos de las cooperativas de consumidores. Madrid: Hispacoop, 29. Available online at: https://hispacoop.es/wp-content/uploads/2021/04/Cuadernos-29-comprimido.pdf (accessed January 15, 2024).

Jochnowitz, E. (2001). Edible activism: food, commerce, and the moral order at the Park Slope Food Coop. Gastronomica 1, 56–63. doi: 10.1525/gfc.2001.1.4.56

Lamarque, M., Tomé-Martín, P., and Moro-Gutiérrez, L. (2023). Personal and community values behind sustainable food consumption: a meta-ethnography. Front. Sustain. Food Syst. 7:12192887. doi: 10.3389/fsufs.2023.1292887

Lusk, J. L., and Briggeman, B. C. (2009). Food values. Am. J. Agric. Econ. 91, 184–196. doi: 10.1111/j.1467-8276.2008.01175.x

MAPA (2021). Análisis de la caracterización y proyección de la producción ecológica en España en 2020. Madrid: Ministerio de Agricultura, Pesca y Alimentación. Available online at: https://www.mapa.gob.es/es/alimentacion/temas/produccion-eco/informecaracterizacionecologicos2020-nipodef_tcm30-583131.PDF (accessed February 05, 2024).

MAPA (2023). Informe del Consumo Alimentario en España 2022. Madrid: Ministerio de Agricultura, Pesca y Alimentación. Available online at: https://www.mapa.gob.es/es/alimentacion/temas/consumo-tendencias/informe-consumo-2022-baja-res_tcm30-655390.pdf (accessed February 5, 2024).

Mier y Terán, M., Giraldo, O. F., Aldasoroa, M., Morales, H., Ferguson, B. G., Rosset, P., et al. (2018). Bringing agroecology to scale: key drivers and emblematic cases. Agroecol. Sustain. Food Syst. 42, 637–665. doi: 10.1080/21683565.2018.1443313

Moore, M. L., Riddell, D., and Vocisano, D. (2015). Scaling out, scaling up, scaling deep: strategies of non-profits in advancing systemic social innovation. J. Corp. Citizenship 58, 67–84. doi: 10.9774/GLEAF.4700.2015.ju.00009

Nicholls, C. I., and Altieri, M. A. (2018). Pathways for the amplification of agroecology. Agroecol. Sustain. Food Syst. 42, 1170–1193. doi: 10.1080/21683565.2018.1499578

Piracci, G., Casini, L., Contini, C., Stancu, C. M., and Lähteenmäki, L. (2023). Identifying key attributes in sustainable food choices: an analysis using the food values framework. J. Clean. Prod. 416:137924. doi: 10.1016/j.jclepro.2023.137924

Rocas-Royo, M. (2021). The Blockchain was not: the case of four cooperative agroecological supermarkets. Front. Blockchain 4:624810. doi: 10.3389/fbloc.2021.624810

Rosset, P. M., and Altieri, M. A. (2017). Agroecology: Science and Politics. Rugby: Practical Action Publishing.

Sage, C., Kropp, C., and Antoni-Komar, I. (2021). “Grassroots initiatives in food system transformation: the role of food movements in the second ‘Great Transformation',” in Food System Transformations. Social Movements, Local Economies, Collaborative Networks, ed. C. Kropp, I. Antoni-Komar, and C. Sage (London; New York, NY: Routledge), 1–19.

Sanz-Cañada, J. (2002). “El Sistema Agroalimentario Español. Estrategias competitivas frente a un modelo de demanda en un contexto de mercados imperfectos,” in Agricultura y sociedad en el cambio de siglo, eds. C. Gómez Benito, and J. J. González Rodríguez (Madrid: Mc Graw Hill), 143–179.

Sanz-Cañada, J., Belletti, G., and Lagoma, C. (2018). Politics and territorial governance of food consumer groups in the district of Lavapiés, Madrid. AGER J. Depopul. Rural Dev. Stud. 25, 65–97. doi: 10.4422/ager.2018.16

Sanz-Cañada, J., Sánchez-Hernández, J. L., and López-García, D. (2023). Reflecting on the concept of local agroecological food systems. Land 12:1147. doi: 10.3390/land12061147

Sanz-Cañada, J., and Yacamán-Ochoa, C. (2022). “Innovación y alimentación sostenible. Políticas y modelos cooperativos de logística y comercialización,” in La España rural: retos y oportunidades de futuro, ed. E. Moyano Estrada (Almería: Fundación Cajamar, serie Mediterráneo Económico), 333–346. Availabe online at: https://publicacionescajamar.es/wp-content/uploads/2022/03/me-35-innovacion-y-alimentacion-sostenible.pdf (accessed January 10, 2024).

Tandem Social and Red de Supermercados Cooperativos (2023). Plan Estratégico de la Red de Supermercados Cooperativos 2024-2026. Mimeo: Red de Supermercados Cooperativos.

Keywords: cooperative supermarkets, scaling, sustainable food, agroecology, participatory action research, alternative food networks

Citation: Sanz-Cañada J, Yacamán-Ochoa C and Pérez-Campaña R (2024) Are agroecological cooperative supermarkets an alternative for scaling sustainable food? Front. Sustain. Food Syst. 8:1395819. doi: 10.3389/fsufs.2024.1395819

Received: 04 March 2024; Accepted: 30 April 2024;

Published: 23 May 2024.

Edited by:

Luigi Mastronardi, University of Molise, ItalyReviewed by:

Grégori Akermann, INRAE Occitanie Montpellier, FranceAurora Cavallo, Mercatorum University, Italy

Copyright © 2024 Sanz-Cañada, Yacamán-Ochoa and Pérez-Campaña. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Javier Sanz-Cañada, amF2aWVyLnNhbnpAY2Nocy5jc2ljLmVz