Jingru Wang

Jingru Wang Tinghua Liu

Tinghua Liu Qi Liu1

Qi Liu1 Xiao Liu

Xiao Liu

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Sustain. Food Syst. , 05 June 2024

Sec. Agricultural and Food Economics

Volume 8 - 2024 | https://doi.org/10.3389/fsufs.2024.1396739

This article is part of the Research Topic Towards Sustainable Development Goal of Zero Hunger: Exploring the Dynamic Relationships between Food Pricing, Agriculture, and Food Security View all 29 articles

Agriculture is crucial for the economy and individuals, and there is a pressing need to improve its quality, efficiency, and competitiveness in emerging countries. This study uses data from Chinese-listed companies to investigate the effect of trade credit on agricultural firms’ total factor productivity. The results demonstrate that trade credit access and provision can increase agribusinesses’ total factor productivity. Heterogeneity analysis reveals that access to business credit has a higher contribution to total factor productivity for agribusinesses in the primary sector, for firms in the versus maturity stage, and with low or medium supplier concentration. The provision of trade credit has a more pronounced positive impact on agribusinesses in the maturing stage and enterprises with low or medium customer concentration. This paper further validates the channels of action through which trade credit affects a firm’s high-quality development. This research makes a valuable contribution to enhancing the quality and productivity of China’s agricultural sector.

Agriculture and its associated sectors play a crucial role in China’s national economic progress, serving as a significant source of livelihood and influencing societal peace and stability. China has embarked on a new phase of actively encouraging the revival of rural areas and expediting the modernization of agricultural and rural regions. Agricultural transformation and upgrading are both urgent and long-term strategies for China’s agricultural development (Wang et al., 2022). According to available data, China’s contemporary agriculture-related sectors are developing rapidly. Nevertheless, China’s agriculture-related industries continue to face issues and obstacles, including an irrational industrial structure, low technological advancement, and challenges to achieving sustainable development. Promoting high-quality development in the contemporary agriculture sector is a crucial problem in the context of China’s economy.

Enhancing the organization of the agriculture sector and improving its technical proficiency necessitate financial backing (Sokolova and Litvinenko, 2020). However, the scale of China’s agriculture-related industries is small, the industrial structure is not complete, and financing is difficult (Ren et al., 2019). Some agricultural enterprises find it difficult to meet bank requirements in terms of business scale, asset quality, collateral, and so on, as well as to obtain bank credit support (Yi et al., 2021). Informal finance is essential for supporting the growth of companies facing challenges in obtaining funding from traditional banking institutions (Ayyagari et al., 2010).

Trade credit is a significant element of informal financing (Cull et al., 2009). It pertains to the commercial practice of businesses providing items to clients and granting them the option to delay payment (Ding et al., 2023). Agricultural businesses typically have extensive production, supply, and marketing chains at the enterprise level. The production process, from agricultural products to transporting raw materials, processing, and sales, involves a lengthy time cycle. Trade credit may efficiently reduce capital risks and borrowing costs during the manufacturing and marketing phases (Deshmukh, 2022). With the development of supply chain finance, agribusinesses usually choose trade credit such as prepaid accounts for financing at the production and procurement stages, and by publicizing the design of commodity production, manufacturers with the intention of purchasing will provide a portion of the funds as support (Gashayie and Singh, 2015). Monetary financing through prepayment prevents firms from facing obstacles in obtaining total operating funds from banks owing to other issues in the traditional business process. Utilizing trade credit ensures the seamless continuation of company production (Wang et al., 2013). The core enterprise can finance agribusiness during the sales stage by providing accounts receivable financing. Accounts receivable from product sales can serve as collateral for financing, with the expectation of a return of funds upon completion of the sale (Wang, 2014).

This article is highly relevant to the studies of Grau and Reig (2018) and Detthamrong and Chansanam (2023). The study conducted by Detthamrong and Chansanam (2023) examines the correlation between trade credit and the performance of agribusinesses in Thailand. The research focuses on Thai-listed agricultural firms from 2001 to 2020. The findings reveal that agribusinesses that invest in trade credit experience a substantial enhancement in their business performance. However, failing to recover the trade credit can adversely impact the firm’s cash flow, impeding business growth. Using European agri-food business panel data, Grau and Reig (2018) examined how trade credit affected corporate profitability throughout the European crisis. Grau and Reig (2018) indicated that boosting trade credit to the business during this period can boost market visibility and profitability. Furthermore, as noted by Grau and Reig (2018), the influence of trade credit on corporate profitability may vary depending on factors including company size and nation.

This research examines how trade credit affects agricultural enterprises’ high-quality growth. It concludes that trade credit availability and supply boost Chinese agricultural enterprises’ TFP (Total Factor Productivity). Heterogeneity demonstrates that obtaining trade credit is conducive to increasing the productivity of all elements in traditional agricultural companies, growing enterprises and enterprises with low concentration of suppliers. Trade credit supply has a more pronounced stimulating impact on mature enterprises and enterprises with low customer concentration. By conducting a mechanism test, it has been shown that the availability of trade credit for firms can alleviate financial limitations and substantially enhance their level of innovation. And offering trade credit reduces inefficient investment, encourages innovation, and boosts firm factor productivity. The paper concludes by applying the entropy weight method to quantify the composite index of high-quality development of agribusiness.

This research makes a marginal contribution, evident in the following features.: Firstly, it enriches the related research on the role of trade credit, and the existing study focuses on a single perspective to assess the influence of trade credit financing on agricultural firms’ profitability and neglects the impact of trade credit provision on high-quality development (Detthamrong and Chansanam, 2023). This article examines both the acquisition and supply of trade credit. It is a beneficial addition to the current research.

Second, we approach the analysis from a unique, “comprehensive” agribusiness perspective. The current studies have only examined a limited range of agribusiness activities, focusing on a narrow subset. Additionally, the research database in China contains a relatively small number of enterprises in agriculture, forestry, animal husbandry, and fishery-related industries. This limited scope may introduce bias in the findings if it solely concentrates on the narrow agricultural sector.

Third, it enhances the research aspect of high-quality development and broadens the understanding and assessment approach to high-quality development in the agricultural sector. The concept of high-quality development is well-structured, but there is no consistent definition for measuring it at the micro-enterprise level. Most studies have used the total factor productivity of the enterprise as a primary indicator of high-quality development (Huang et al., 2022). This is because the total factor productivity comprehensively considers the enterprise’s labor, capital, and factor inputs. Furthermore, the related study on the high-quality growth of agricultural firms lacks a systematic assessment index system and measurement technique. This study thoroughly investigates the high-quality advancement of agribusiness by analyzing total factor productivity and comprehensive indicators. It broadens the research framework and system for high-quality agribusiness growth while ensuring the results’ rigor and trustworthiness.

Fourth, Prior research has primarily focused on studying the influence of trade credit on the industrial sector, with less emphasis on its role in agricultural enterprises. This paper examines trade credit’s role in agribusiness operations and financing costs. It analyzes how trade credit affects agricultural enterprises’ financing costs, technological innovation, and investment efficiency. These findings are valuable for utilizing trade credit funds in agricultural enterprises to foster enterprise development and for the government’s management of supply-chain finance funds.

This article is structured as follows: Section 2 introduces the theoretical framework and establishes the research hypotheses. Section 3 provides an overview of the research design, encompassing the sources of data, model specifications, and a description of the statistical analysis. Section 4 addresses the regression analysis, elaborating on the foundational regression, tests for robustness, and analysis of heterogeneity. Section 5 provides a deeper exploration of the mechanism analysis. Section 6 discusses the creation and detailed examination of the composite index for high-quality development. Finally, Section 7 presents the conclusions and policy implications derived from the study.

The assessment of high-quality development primarily involves two approaches: establishing a comprehensive set of indicators and choosing proxy variables (Zhang et al., 2023). As per researchers’ interpretation of the meaning of high-quality enterprise growth, the crucial aspect is enhancing the overall factor productivity of firms. The existing literature on the investigation of factors that affect total factor productivity primarily concentrates on resource allocation efficiency (Yang, 2015; Wen, 2019; Cao et al., 2022), enterprise innovation (Bartelsman et al., 2013; Liu, 2021; Wu et al., 2021), and limitations in obtaining financial resources (Sheng and Liu, 2021; Zhang and Pang, 2023). Furthermore, several academics have analyzed the influence of the three variables, namely financial environment, policy system, and taxes, on firms’ productivity.

Capital plays a vital role in driving economic growth, and optimizing the allocation of resources is a crucial way to increase the economy’s overall productivity (Yang, 2015). On a macro level, Banerjee and Duflo discover that the inefficient distribution of resources across different companies decreases overall societal TFP. Hsieh and Klenow (2009) suggest that resource allocation distortions are the primary cause of declining total factor productivity in China, estimating that its productivity could improve by 30–50 percent if it were to match the resource allocation efficiency of the United States. At the microenterprise research level, firms facing capital constraints, market failures, or other issues that cause resources to flow toward inefficient firms or sectors can lead to distortions in factor inputs. This, in turn, harms firms’ overall productivity (Restuccia and Rogerson, 2017). Almeida and Wolfenzon (2006) assert that the efficient allocation of capital by businesses influences their effectiveness. In his study, Ryzhenkov (2016) discovered a considerable misallocation of resources within the Ukrainian manufacturing sector, and improving the efficiency of resource allocation across enterprises would result in substantial productivity development for manufacturing companies.

Firms’ total factor productivity also closely relates to financing constraints. It has been shown that the level of productivity and the likelihood of innovation through invention or adoption depend on the availability of finance. Ferrando et al. have empirically demonstrated that funding limitations exert a substantial inhibitory impact on the total factor productivity of enterprises in countries within the euro area. Ayyagari et al. (2010) validated the negative impact of funding limitations on the overall efficiency of enterprises. Krishnan et al. (2015) demonstrated that increasing financing channels can improve enterprises’ total factor productivity in a natural experiment framework. Based on Chinese firm statistics, Dong et al. (2022) have identified that alleviating financial restrictions is a crucial pathway for enhancing investor confidence and boosting the overall productivity of corporations. This indicates that funding limitations continue to be a significant barrier limiting the high-quality growth of Chinese firms. Nevertheless, several academics contend that limitations on funding exert a beneficial influence on the overall efficiency of enterprises. Wang (2022) argues that financial limitations can decrease the risks associated with corporate innovation, enhance the quality and effectiveness of innovation, and ultimately contribute to the advancement of overall corporate productivity.

An enterprise’s innovation significantly influences the enhancement of total factor productivity within a business. The academic community has long been concerned with the theoretical and practical challenge of improving total factor productivity through innovation. According to Schumpeter’s theory of economic growth, corporate innovation can transfer production factors from low-productivity firms to high-productivity firms, causing less productive companies to exit the market. This process ultimately enhances the industry’s overall productivity (Bartelsman et al., 2013). Dabla-Norris et al. (2012) found that innovation is critical to firm performance as it can directly increase productivity and that the impact of innovation on productivity is more significant in less developed countries. Sandvik and Sandvik (2003) noted that innovation is an essential means of enhancing firms’ competitiveness, is often regarded as a core developmental competency of firms, and is also considered an effective way of increasing firm productivity (Lumpkin and Dess, 1996).

Trade credit finance helps alleviate the financial limitations faced by businesses. Trade credit is a kind of collaborative financing that plays a crucial role in informal finance. It is commonly employed in corporate transactions, including the buying and selling of goods and services. It is a significant means of obtaining corporations’ funding and possesses little risk and accessibility. When enterprises have limitations in obtaining funds, they may choose trade credit as an alternative form of funding (Petersen and Rajan, 1997; Seifert et al., 2013). Rajan and Zingales (1996) highlighted that, apart from formal financial channels, trade credit serves as a crucial means of financing for firms operating in regions with an undeveloped formal financial system. Molina and Preve (2012) discovered that enterprises facing financial challenges use trade credit as a substitute for cash obtained through bank loans. In times of economic hardship, firms may seek financing from suppliers when traditional financial institutions are reluctant to provide loans.

Trade credit financing alleviates the financial limitations faced by businesses and motivates them to expand their investments in inventories, fixed assets, and other resources. In their respective studies, Abuhommous and Almanaseer (2021) and Karakoç (2023) discovered that managers might employ trade credit financing as a beneficial means to augment corporation worth and attain elevated growth objectives. Fisman and Love (2003) discovered that industries that relied more heavily on trade credit financing had elevated growth rates in regions with limited progress in finance.

Nevertheless, acquiring trade credit can sometimes entail adverse repercussions for enterprises. Molina and Preve (2012) research demonstrated that the utilization of trade credit by enterprises during periods of financial limitations leads to a decline in sales income. Opler and Titman (1994) further verified that when a company has limitations in obtaining funds, its operational performance would substantially fall if it heavily relies on trade credit. Białek-Jaworska and Nehrebecka (2016) indicated that trade credit had a detrimental effect on firm value, decreasing its overall worth.

Trade credit supply is when a firm provides short-term financing to its customers, enabling them to delay payment while buying the service and commodity. Existing literature has put out three primary theoretical arguments to elucidate the motives behind corporations offering trade credit to their clients.

First, competition theory elucidates the underlying drive of firms to offer trade credit. Firms in the same industry may engage in interest rivalry. These companies would strategically enhance their pricing advantages by offering trade credit to increase consumer loyalty and promote their products. This helps them maintain or extend their market competitiveness (Schwartz, 1974). Wilson and Summers (2002) stated that trade credit is a significant business marketing tool. Businesses that achieve higher product profits are inclined to offer trade credit as a means of increasing sales (Petersen and Rajan, 1997). Furthermore, firms may use trade credit to engage in price discrimination against customers (Meltzer, 1960), increasing sales and profits.

Second, according to information theory, trade credit provision is a strategic tool to mitigate information asymmetry. This allows consumers to determine product quality and helps suppliers appropriately evaluate customers’ default risk. Smith (1987) posited trade credit functions as a means of quality assurance. Suppliers offer trade credit to client companies when there is a lack of information symmetry between businesses.

Third, providing trade credit reduces inventory management costs and ensures stability throughout the supply chain. By offering trade credit to both upstream and downstream enterprises, financing support is provided to customers, resulting in reduced search costs for suppliers and customers (Petersen and Rajan, 1997; Wang, 2014).

Offering trade credit for commercial transactions can also have a negative impact on firms. Białek-Jaworska and Nehrebecka (2016) suggests that providing trade credit can influence a firm’s profitability and liquidity. Furthermore, firms that offer trade credit are vulnerable to the danger of client default and incur additional costs associated with credit management (Mian and Smith, 1992).

Trade credit is important in the informal financial system because it helps address the limitations and inefficiencies of the official financial system (Ju et al., 2013). The concepts of “comparative advantage theory” and “credit rationing theory” (Petersen and Rajan, 1997) provided evidence of the function of trade credit in financing. During a moment of monetary tightening, when banks limit lending to agriculture and the cost of corporate finance increases significantly, trade credit will serve as an alternative funding source to official financial channels. Agricultural firms get trade credit, which also serves as an indirect signal to banks and financial institutions regarding their sound business operations. As a result, they can secure credit from these traditional financial institutions, mitigating the financing limitations. Alleviating financing constraints contributes to high-quality enterprise development.

The innovation of an enterprise has a substantial impact on improving the overall productivity of a corporation. By mitigating the limitations on financial resources that companies face, obtaining trade credit might empower major agribusinesses to augment their investments in innovation, enhance their innovative efforts, and boost their overall efficiency. Studies indicate that depending solely on internal funding to support innovative inputs and sustainability is challenging. Consequently, many organizations shifted toward external financing to facilitate innovation endeavors. Liu et al. (2022a) concluded that using trade credit finance is beneficial for promoting innovation within organizations, particularly substantial innovation.

H1a: Obtaining trade credit is conducive to improving TFP and promoting high-quality development of agricultural enterprises.

Trade credit also has a negative effect on the high quality of business development. On the one hand, firms may not invest short-term funds such as trade credit in R&D, and thus it will not have a substantial impact on the high quality of their development. On the other hand, trade credit increases the short-term debt-servicing pressure of enterprises, and the willingness of enterprises to innovate may decline with the rise of debt-servicing pressure (Shao and Wang, 2023), which is not conducive to high-quality development of enterprises.

H1b: Obtaining trade credit is not conducive to improving TFP and has a negative effect on the high-quality development of agricultural enterprises.

The market competition hypothesis suggests that, in a competitive market, an agribusiness offering trade credit to its clients can enhance its price advantage and increase customer loyalty (Wilson and Summers, 2002). Likewise, a gain in market share may have a favorable incentive impact on the enterprise’s total factor productivity. (Summers and Wilson, 2003). On the one hand, to maintain their existing market position, agribusinesses will take the initiative to enhance the technological content of their products, which will promote the total factor productivity of the enterprise. On the other hand, a high market share implies steady growth in sales, and the enterprise has sufficient cash flow to provide stable financial support for R&D and innovation. Therefore, the provision of trade credit by enterprises can enhance their productivity by exerting the effect of market competition (Liu et al., 2022b). In addition, during the sales stage, if an agricultural enterprise is unable to obtain timely replenishment of funds to be invested in the next cycle of production activities, it can apply for financing by using the accounts receivable derived from the sale of goods as a condition for payment of credit funds to commercial banks, which ensures the continuity of cash flow and is conducive to the enhancement of the enterprise’s production efficiency (Białek-Jaworska and Nehrebecka, 2016).

Trade credit possesses a distinct advantage in obtaining information (Pepur et al., 2020), which agribusinesses can effectively monitor through commodity trading. This advantage enables trade credit to partially mitigate information asymmetry. Enterprises are motivated to innovate their goods proactively and enhance their TFP to maintain a steady supply-and-demand connection with their consumers and preserve their market position (Summers and Wilson, 2003).

H2a: Providing trade credit has a positive impact on corporate TFP and is conducive to the high-quality development of agricultural enterprises.

However, a large number of customers confront financial crises due to poor management. In that case, the trade credit funds provided by the company are difficult to recover, resulting in the company lacking funds for ongoing operations (Martínez-Sola et al., 2014), which will have a negative impact on the company’s total factor productivity. Therefore, the trade credit provided by the seller’s company due to the coercive effect may cause involuntary losses to the company due to the buyer’s default event. The breakdown of the capital chain will significantly reduce the size of the company’s available funds and increase financing costs, thereby inhibiting the company’s total factor productivity.

H2b: Providing trade credit is not conducive to improving TFP and inhibits the high-quality development of agricultural enterprises.

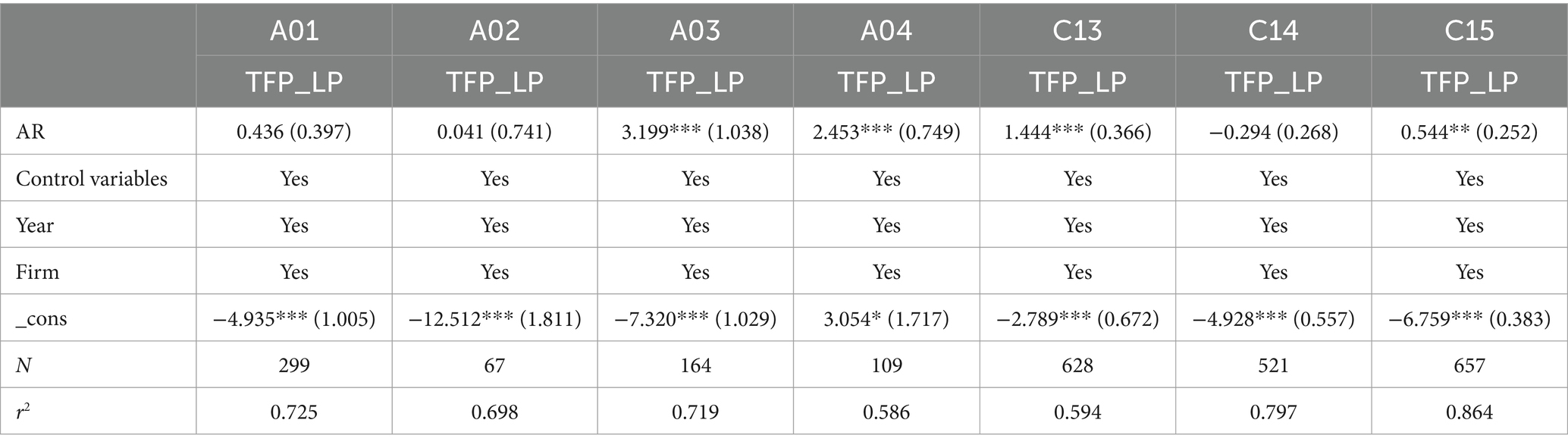

This study’s sample comprises agricultural enterprises publicly traded on the Shanghai and Shenzhen Stock Exchanges in China from 2002 to 2022. According to Cao et al.’s (2022) examination, the mentioned agricultural companies include agriculture (A01), forestry (A02), animal husbandry (A03), and fishery (A04) within the primary sector; agro-food processing (C13), food manufacturing (C14), and wine, beverage, and refined tea manufacturing (C15) within the secondary sector; and agriculture, forestry, animal husbandry, and fishery services (A05) within the tertiary sector. The sample was refined by (1) excluding companies classified as ST, *ST, and PT; and (2) eliminating outliers and missing values. We applied a shrinkage method to continuous variables within the 1st and 99th percentiles of the sample to ensure the reliability of the regression results and account for extreme values. The screening process resulted in a total of 2,480 valid firm-year observations.

In order to delve into the role of trade credit on the high-quality development of enterprises, this paper uses model (1) to measure the effect of obtaining trade credit on the high-quality development of agricultural enterprises, and model (2) to measure the impact of trade credit provided by agricultural enterprises on the high-quality development of enterprises.

Explained variable (TFP), the current measurement methods of high-quality development are mainly divided into two categories: using a single or comprehensive indicator measurement method. In recent years, total factor productivity (TFP) has emerged as a crucial metric for researchers to assess the development of companies. TFP contains a wealth of information about the company, such as product quality, enterprise business development, and enterprise innovation. In light of this, the study employs total factor productivity as a benchmark for appraising the high-quality development of agricultural enterprises. Nevertheless, the study devises a comprehensive, integrated evaluation system to gage the high-quality development of agricultural enterprises, taking into account the potential bias and constraints associated with relying solely on one indicator of total factor productivity.

Based on Levinsohn and Petrin’s (2003), the LP method to calculate TFP better overcomes the endogeneity problem in the OLS estimation of total factor productivity. Therefore, this article uses the LP method in benchmark regression to calculate the total factor productivity of agricultural enterprises. To make the result more reliable, this article also conducts robustness testing using various enterprise total factor productivity measurement methods, such as the OP and GMM methods.

Explanatory variables are mainly categorized into obtaining trade credit (AP) and providing trade credit (AR), and AP is defined as (accounts receivable + notes receivable + prepayment)/total assets, and AR is defined as (accounts payable + notes payable + prepayment)/total assets.

This paper utilizes control variables to account for various factors that influence the total factor productivity of enterprises, including bank loans (Bank), enterprise scale (Size), cash flow ratio (Cashflow), financial leverage (Lev), return on total assets (Roa), proportion of fixed assets (Fixed), revenue growth rate (Growth), and company listed age (ListAge). The specific calculation method of control variables is in Table 1. Furthermore, the variable in the model denotes the specific fixed effects of each unique business, represents the fixed effect of time, and stands for the random disturbance term.

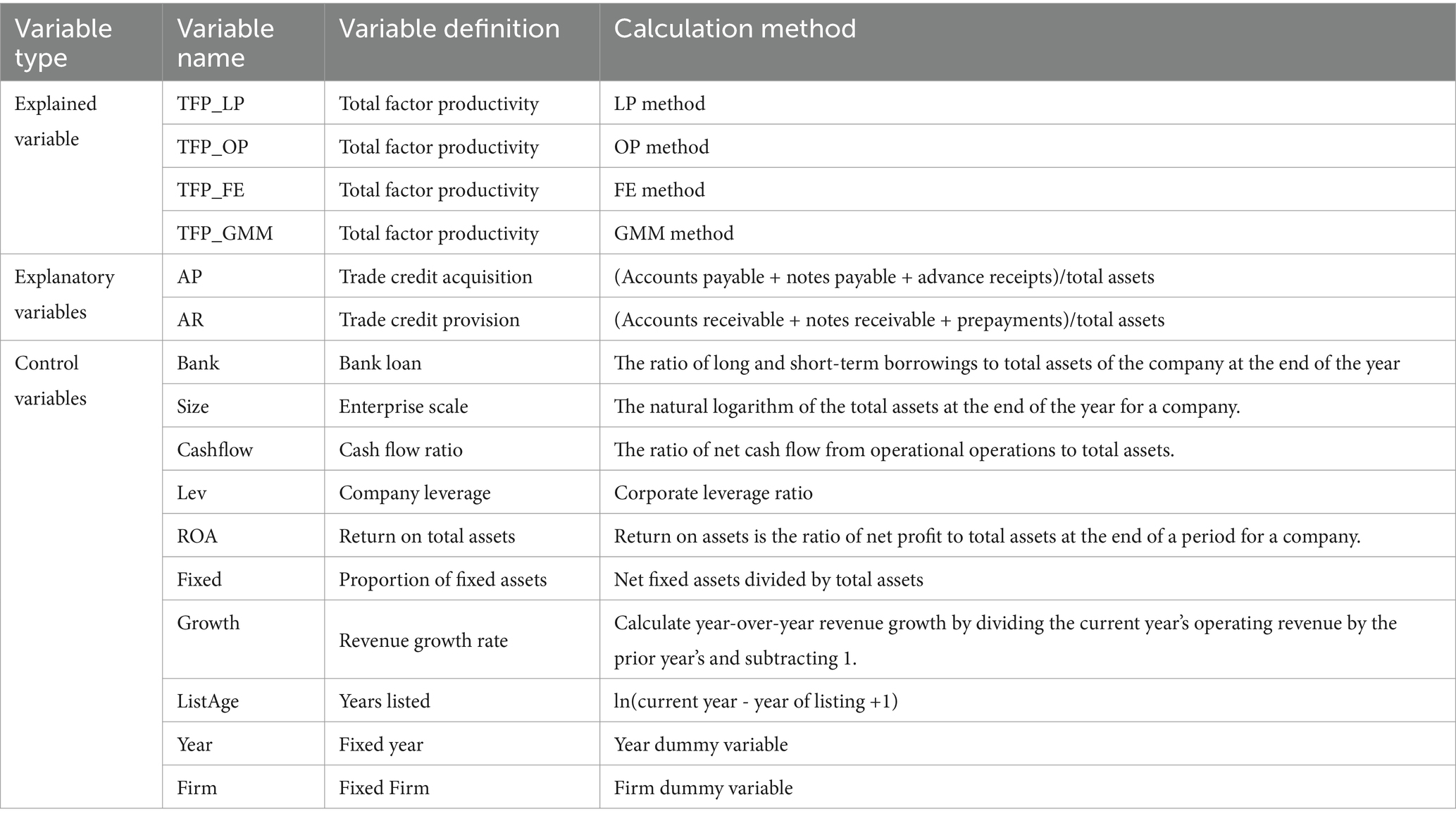

Table 1. Definitions of variables.

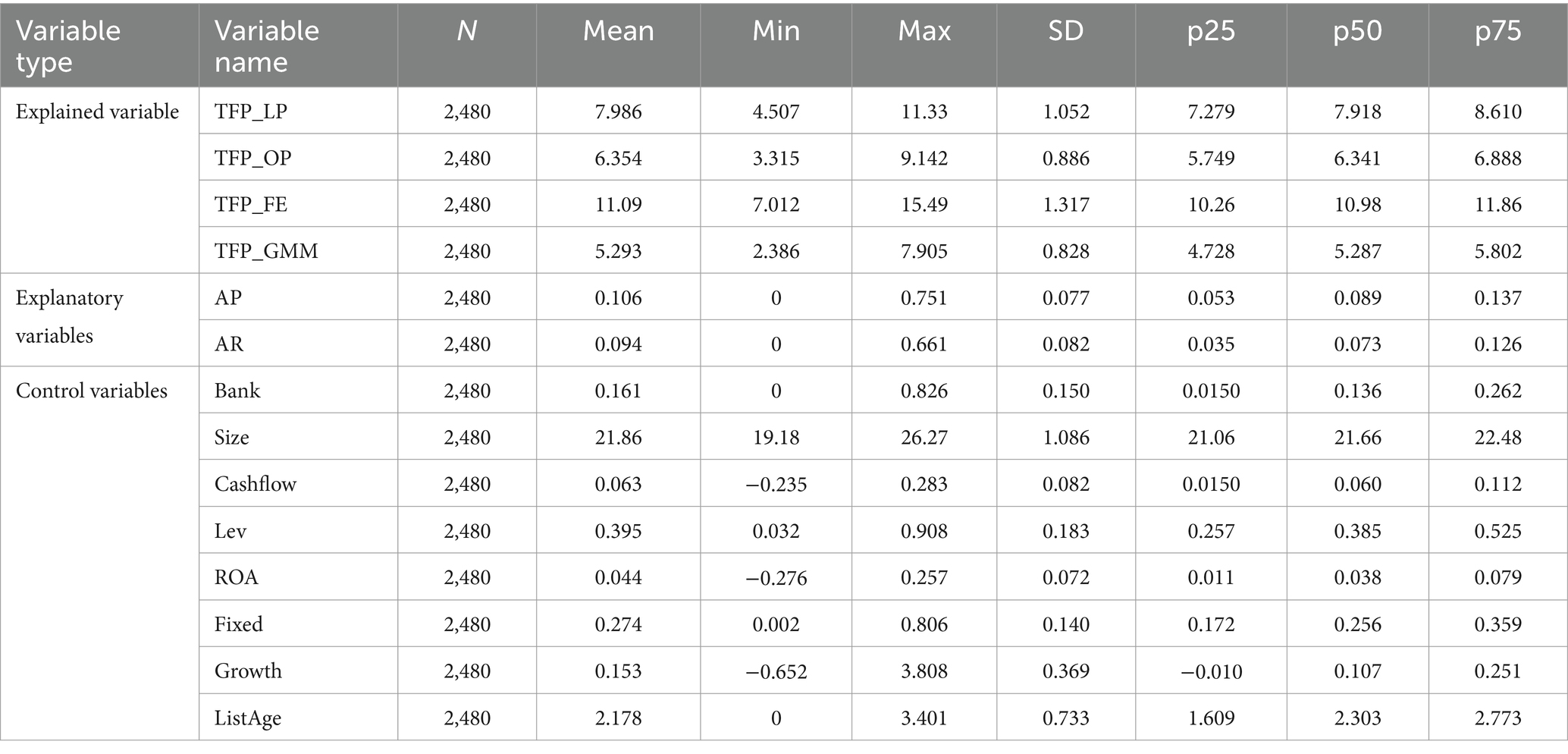

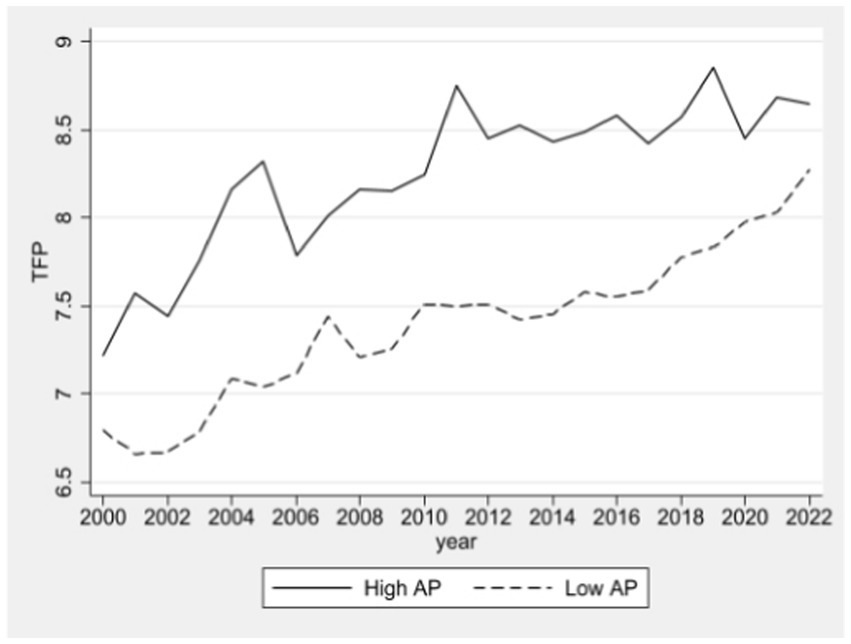

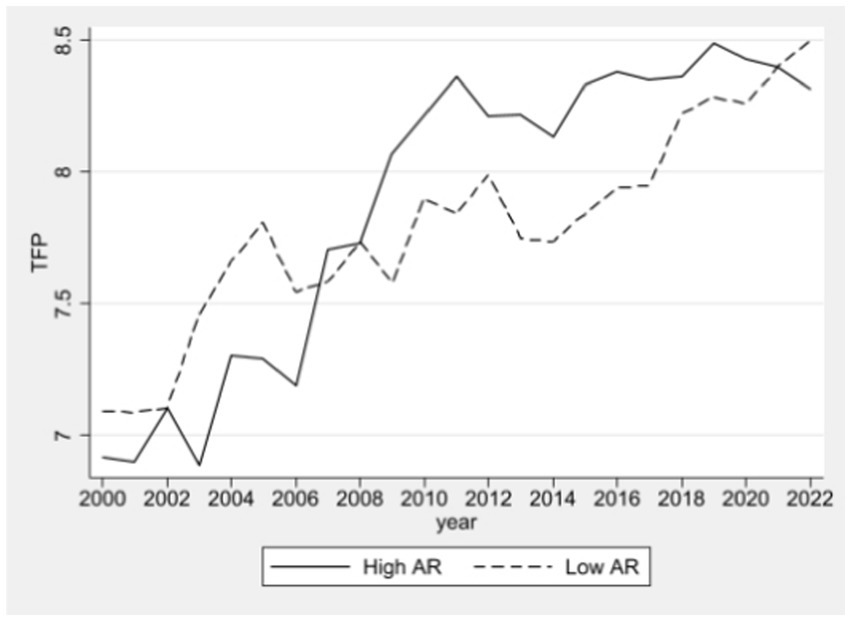

This article employs a descriptive statistical analysis to examine each variable within the overall sample (Table 2). The findings indicate that the mean TFP_LP for all enterprises is 7.986, with a maximum of 11.33 and a minimum of 4.507. This indicates a significant difference in the TFP_LP among agricultural businesses. On average, these companies get trade credit of 10.6% of their total assets and extend trade credit of 9.4%. Chinese agricultural firms typically have a Cashflow of 6.3%, Lev of 39.5%, ROA of 4.4%, and a proportion of fixed assets of 27.4%. In this study, we have categorized the data into three sets based on the levels of trade credit acquisition and supply. Subsequently, we have compared the group with the highest degree of trade credit acquisition to the group with the lowest level. Figure 1 shows that the former group, with a considerable level of trade credit acquisition, exhibited a substantially higher average TFP than the lower group. Our preliminary statistical analysis results have shown that the affirmative impact of trade credit on businesses’ overall productivity. Within this context, it is noteworthy that in Figure 2, the TFP of the group with a higher provision of trade credit was significantly lower before 2008 than that of the group with a lower provision. This discrepancy can be attributed to the Chinese government’s implementation of the People’s Republic of China on Property Rights in 2007, which offered a certain level of safeguarding for the provision of trade credit by enterprises. Building upon this critical finding, the paper later undertakes a policy analysis utilizing the double-difference methodology, delving deeper into the effects and implications of this specific policy and occurrence.

Table 2. Descriptive statistics of variables.

Figure 1. TFP group statistical chart (trade credit acquisition).

Figure 2. TFP group statistical chart (trade credit supply).

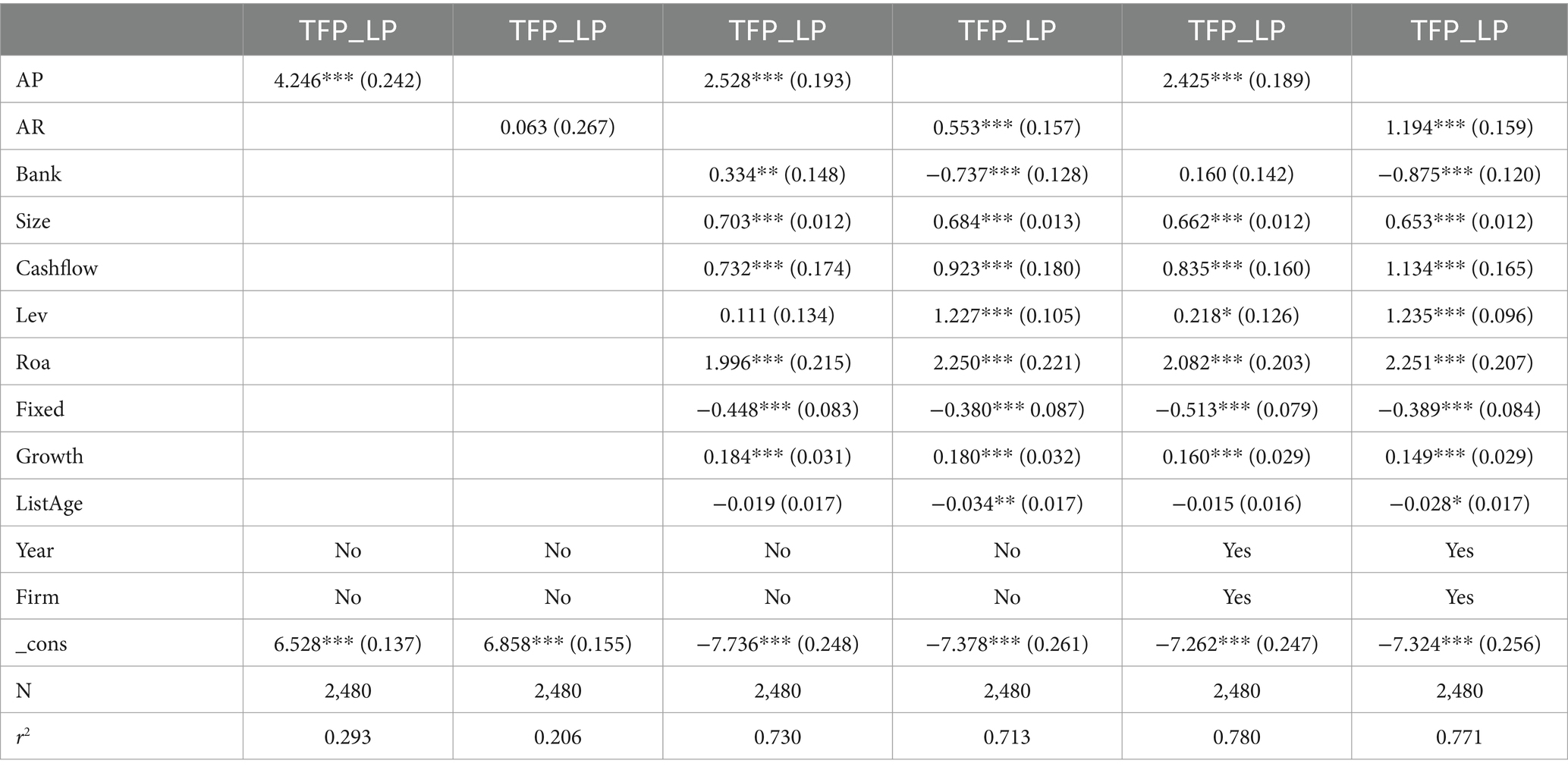

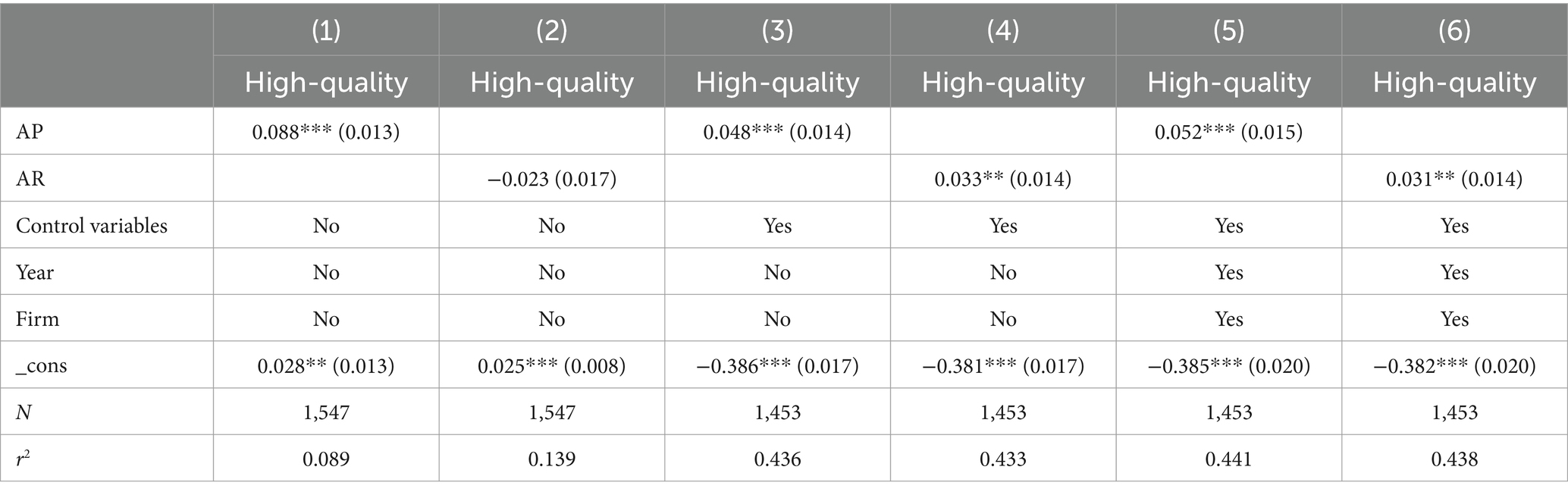

According to Table 3, the 1 and 2 columns present results without factoring in control variables, while the 3 and 4 columns consider control variables but neglect to consider the year and individual fixed factors. The 5 and 6 columns incorporate both control variables and fixed factors. Table 3 results show that the acquisition and provision of trade credit significantly enhance businesses’ overall productivity. At the 1% level, the majority of the calculated coefficients are significantly positive. Furthermore, the model results indicate that obtaining trade credit has a more significant positive impact on total factor productivity than the supply of trade credit. The initial regression findings provide evidence that supports H1 and H2a, suggesting that trade credit beneficially influences improving the overall efficiency of businesses (Table 4).

Table 3. Results of the baseline regression.

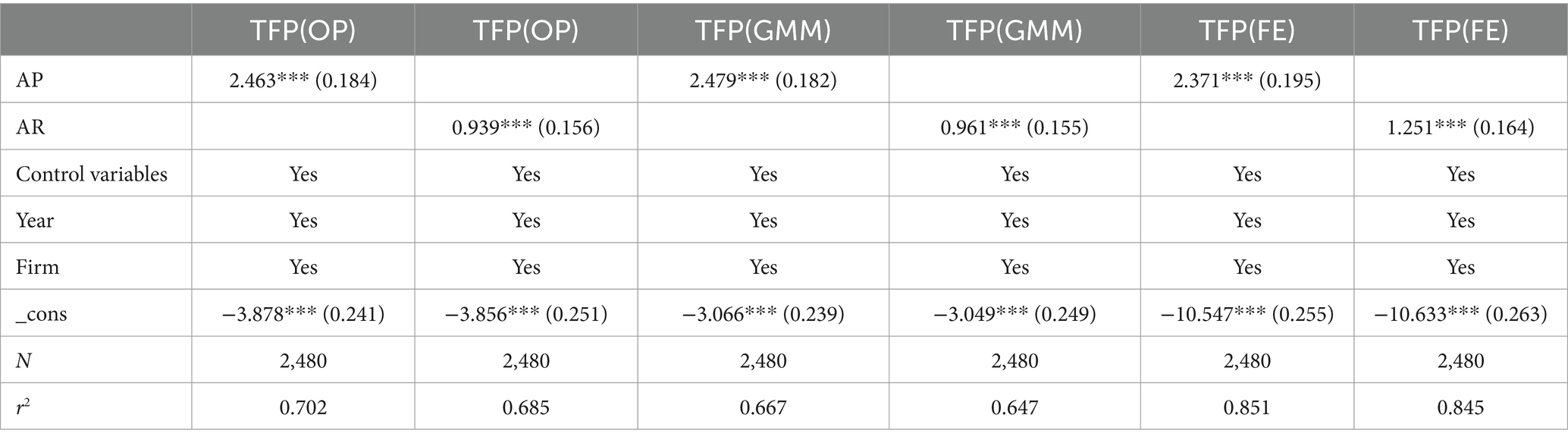

Table 4. Substituting Variables.

This study replaces the TFP measure and, following Li and Li (2020), employs the OP, GMM, and FE methods. This method also produces comparable results, in Table 4, with trade credit accessibility and availability showing significant beneficial effects on enterprises’ total factor productivity at the 1% level. This supports the earlier findings of the benchmark regression conducted in this study.

While the research has controlled the crucial aspects that might impact the overall productivity of firms, it is still possible that the model may overlook essential variables. In addition, the development of enterprises will expand their access to finance from banks, increasing the trade credit supply. Thus, trade credit may reversely affect enterprises’ total factor productivity.

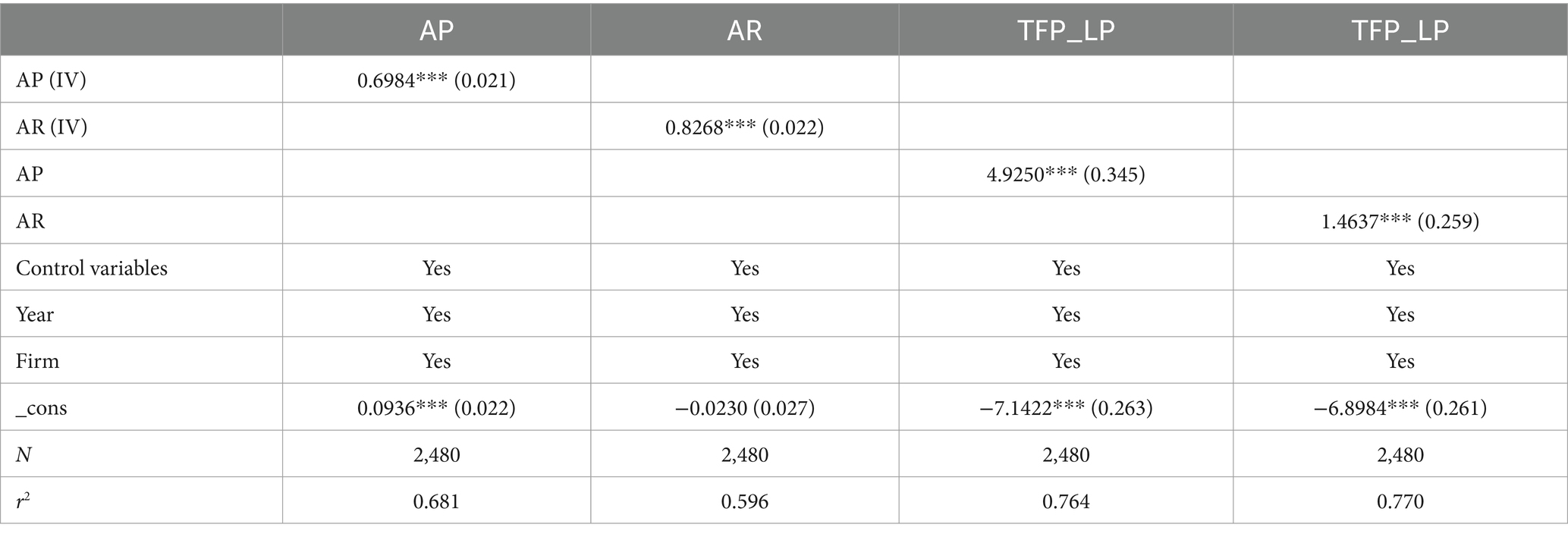

This study incorporates an instrumental variable, AP/AR Industry, which derives from the average of past trade credit acquisition and provision within the firm’s industry, to mitigate the impact of endogeneity on the study findings. Mei and Cheng (2021) suggest re-evaluating the model regression results using the two-stage least squares (2SLS) technique. Regarding correlation, enterprises’ business and operating features are comparable, implying that their supply and obtaining of trade credit are similar to those of other enterprises in the same sector. Regarding exogeneity, the industry mean refers to a variable at the industry level. The industry average of company credit has less association with the firm’s micro-level factors, thereby fulfilling the exogeneity principle.

During the preliminary phase, we observed that the estimated coefficients of the instrumental and corresponding explanatory variables have a remarkable significance level, with a p-value lower than 0.01. This serves as evidence that the instrumental variables effectively elucidate the endogenous variables. The F-value exceeds 10, indicating that the instrumental variables fulfill the necessary criteria and that there are no weak instrumental variables. The research results in Table 5 show that providing and obtaining trade credit has a positive impact on the total factor productivity of enterprises, which is consistent with the results of the baseline regression of this study.

Table 5. Results of the least squares method.

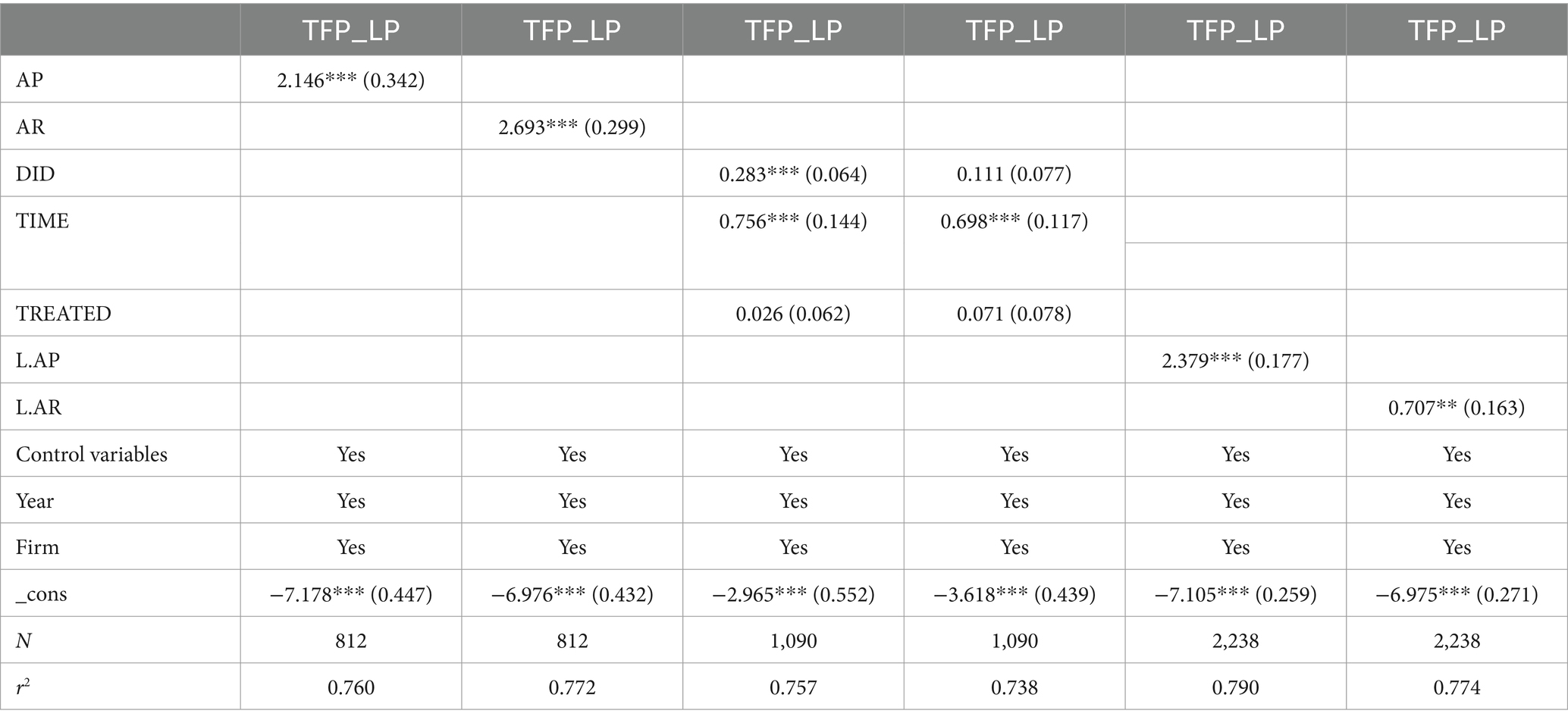

Amidst the widespread economic upheaval of 2008, businesses across the globe were reeling from the ramifications of the financial crisis. The adverse effects of this crisis were profound, manifesting in reduced investments and depleted production rates (Shuai et al., 2023). As such, our study exclusively focuses on post-2010 data. Notably, our empirical findings reveal that even during periods free of financial crises, trade credit remains a crucial catalyst for enhanced total factor productivity in firms.

As a growing market nation, China has implemented and revised several regulations to enhance firms’ external business environment. Specifically, the Property Law was officially announced in March 2007. China’s Law on Property Rights has established comprehensive regulations on security rights, mortgages, and pledges, resulting in a well-structured and comprehensive property rights framework. As seen in Figure 2 above, the group with a higher provision of trade credit had a lower TFP than the group with a lower provision of trade credit before 2007, which may be mainly because the reform of security rights marked by the enactment of the Property Law in 2007 has taken measures to protect the funds provided by enterprises for trade credit. The Chinese law clearly states that inventory (Article 108) and accounts receivable (Article 223) can be mortgaged and pledged. The law explicitly states inventories (Article 108) and receivables (Article 223) can be mortgaged and pledged. According to research by Jun et al. (2017), the Property Law provides appropriate safeguards for creditors and encourages firms to enhance their innovative capabilities. This article employs the Property Law for quasi-natural experiment analysis to investigate the alterations in firms’ total factor productivity level. By using the difference-in-differences model and analyzing the disparities between the experimental and control groups, it is possible to mitigate the endogeneity problem to some degree and obtain a more accurate measurement of the causal link between the two. The results from applying the double differencing method in column 3 of Table 5 demonstrate that the productivity level is more significant in the group with a higher provision of trade credit. Additionally, this paper conducts a placebo test on the policy time in advance, and the results in the 4th column of Table 6 are not statistically significant, which confirms the reliability of the outcomes. Adopting the difference-in-differences model also further overcomes the interference of endogeneity concerns, confirming the robustness of the benchmark regression results.

Table 6. Difference-in-difference test results and lagged test results.

Firms’ innovation achievements are strongly linked to the enhancement of overall efficiency. However, there is a delay between the inputs made toward innovation and the actual outcomes of innovation. Notably, the production of high-quality innovations requires a longer duration. As a result, there might be a temporal mismatch between the availability of trade credit funding and the firms’ overall efficiency. Consequently, we conduct a regression analysis on the whole factor productivity of businesses using a one-period lag. The results in rows 5 and 6 of Table 6 show that trade credit still positively affects enterprises’ total factor productivity. This reinforces the robustness and dependability of the study’s findings.

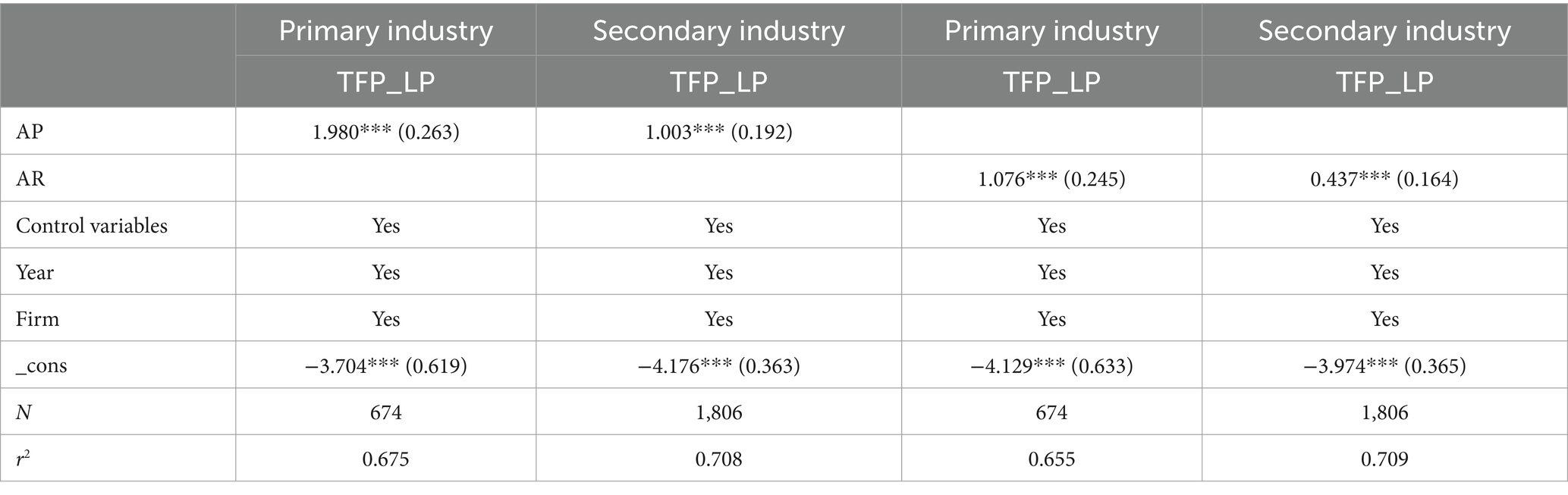

Large publicly traded companies in the agricultural industry encompass various businesses, including agriculture, forestry, animal husbandry, and fishery operations. These include secondary industries such as food manufacturing, agricultural food processing, wine production, beverage production, and refined tea production. In addition, there are service companies related to agriculture, forestry, animal husbandry, and fishery in the tertiary industry. However, due to the limited size of the tertiary sector sample, this article primarily focuses on categorizing primary and secondary industrial divisions. According to Table 7, access to trade credit facilitates TFP in the fisheries, agriculture, and agricultural food processing sectors. However, its influence on the food manufacturing industry is less significant, and it even has a negative effect on the animal husbandry sector. On the other hand, the result in Table 8 shows that trade credit provision positively impacts TFP in the fisheries and animal husbandry sectors but has no significant influence on the agricultural, forestry, and food manufacturing industries. The results in Table 9 reveal that trade credit significantly impacts TFP in the primary industry. This paper posits that the low earnings and elevated business risks of conventional agricultural businesses primarily hinder their ability to secure funding from banks and financial institutions. Therefore, these enterprises often rely on inter-enterprise trade credit funds for development. Additionally, companies in the primary sector tend to offer similar goods, leading to increased competition and a stronger incentive to offer trade credit to stabilize sales or gain a larger market share.

Table 7. Segmentation - trade credit acquisition.

Table 8. Segmentation - trade credit provision.

Table 9. Segmentation industries.

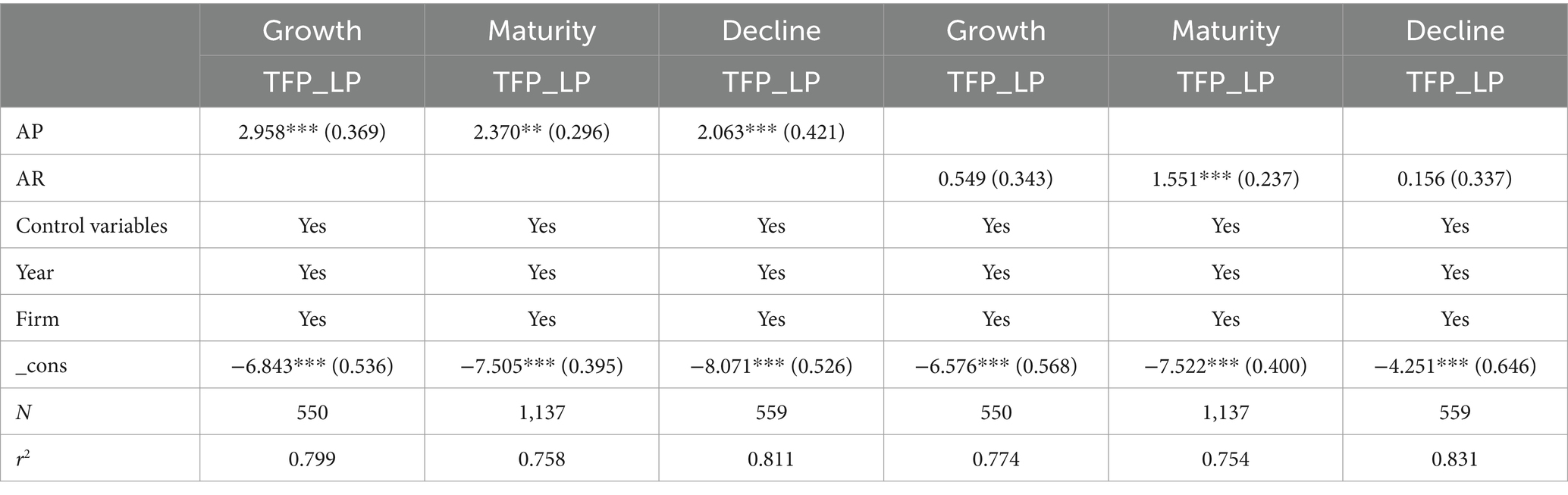

The enterprise life cycle hypothesis pertains to the dynamic trajectory of a business’s development and expansion, encompassing three distinct stages: growth, maturity, and decline. According to the hypothesis, firms at different phases have distinct financial demands and resource usage rates. The effect of trade credit on company growth may differ based on the business’s life cycle stage.

For firms in the growth stage, the findings indicate that having access to commercial finance significantly impacts productivity. From the standpoint of obtaining trade credit, businesses in the growth phase face limited access to external financial resources. Using trade credit financing may effectively reduce funding limits and provide “incentive effects” that promote high-quality firm development. From the perspective of providing trade credit, enterprises face a shortage of funds during the growth stage. To quickly expand their market, they tend to offer more trade credit to clients. However, this practice hampers the allocation of funds toward research and development (R&D), thereby hindering the overall improvement of the enterprises’ total factor productivity.

For mature firms, both obtaining and supplying trade credit significantly increase their TFP, and mature firms have a relatively stable market share and substantial profits relative to growth-phase firms. On the one hand, acquiring trade credit provides mature firms with funds for innovation. On the other hand, mature firms are more capable of lowering transaction costs based on stable markets and sales channels, making the provision of trade credit more stable and profitable, and promoting firms’ high-quality development.

For declining firms, formal financing is relatively difficult. It relies more on trade credit funding from business transactions, so that trade credit financing funds for declining firms may support firms in innovation and improve their total factor productivity. In addition, declining firms’ provision of trade credit further deteriorates firms’ financial flows, which is not conducive to high-quality growth.

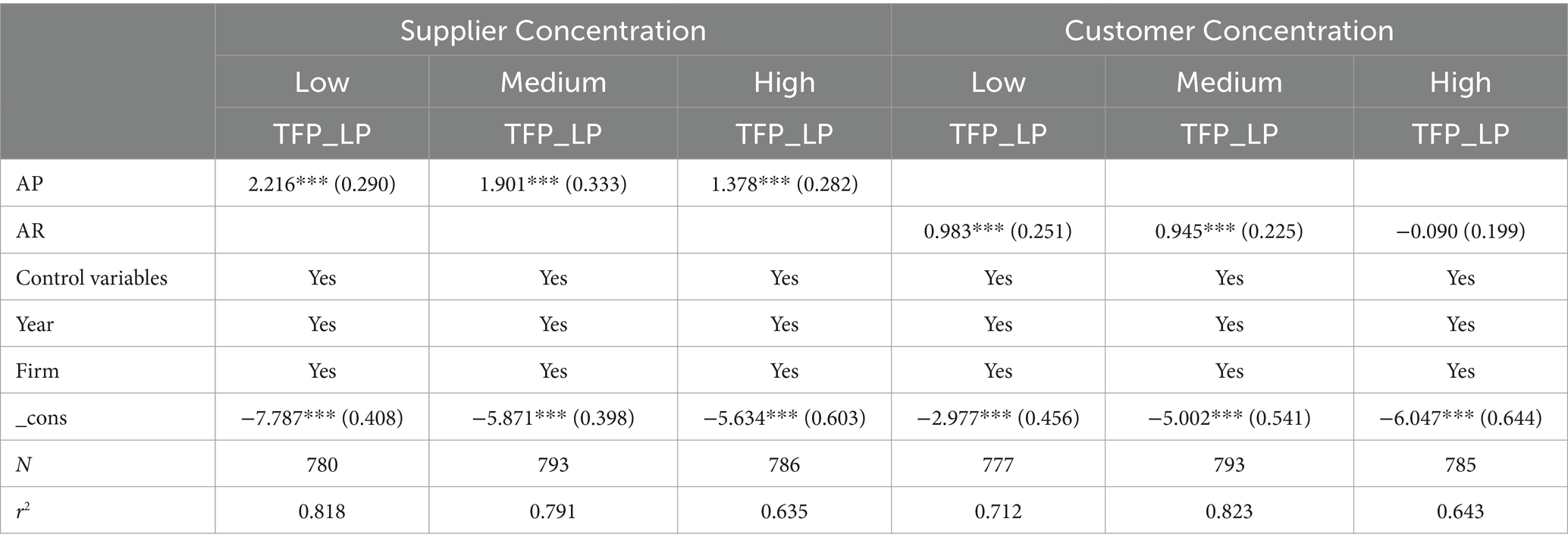

Supplier concentration can significantly affect the availability of trade credit. Supplier groups are the controllers of raw materials for enterprises and usually have strong negotiating power. When supplier concentration is low, agricultural enterprises have a stronger bargaining position and can acquire more advantageous trading terms, such as more extended payment periods and higher accounts payable. This allows them to obtain more trade credit than they provide. As the concentration of suppliers increases, the voice of enterprises gradually decreases when suppliers tend to occupy a dominant position, and the trade credit that enterprises obtain from suppliers decreases. High supplier concentration might lead to suppliers demanding early payment, worsening the enterprise’s financial restrictions and hindering its high-quality growth.

Thus, this article argues that the function of trade credit financing may vary among enterprises with varying levels of supplier concentration. Columns 1–3 of Table 10 demonstrate that trade credit financing has the most substantial impact on enterprises with low customer concentration, and this impact is statistically significant at the 1% level.

Table 10. Distinguishing business life cycles.

Customer concentration refers to allocating an enterprise’s revenue among its various client groups over a specific time frame. We commonly measure it by calculating the proportion of the enterprise’s total revenue that its top five customers generate during that period. Customer concentration can have both advantageous and perilous implications for trade credit. Positively, higher customer concentration allows for better information sharing between the company and the customer, reducing information asymmetry. This is beneficial for ensuring fund recovery, effectively allocating funds for the company’s development, and improving TFP. However, the customer concentration also has detrimental impacts; a high customer concentration can increase the client’s negotiating power.

The findings from Table 11 indicate that the provision of trade credit has a substantial role in fostering the high-quality growth of companies with low and medium customer concentration levels. This result is consistent with the study of Dong et al. (2021), where firms with high customer concentration face the problem of blackmail from their primary customers, which leads to financial difficulties and higher financing costs, thus weakening the incentives for firms to innovate and is not conducive to the improvement of their total factor productivity.

Table 11. Distinguish between supplier concentration and customer concentration.

Stable and adequate funding is crucial for the growth of an enterprise in China, as the formal finance sector is not well developed. The small scale of agricultural enterprises makes it challenging to obtain sufficient financial support, leading to financing constraints for many agricultural enterprises. Enterprise innovation requires consistent financial backing. Insufficient financing can lead to interruptions in innovation, increase sunk costs for businesses, diminish their passion for innovation, and perhaps disrupt routine operations. Guo (2023) revealed that financial restrictions hinder the enhancement of total factor productivity in Chinese fishing firms.

This research utilizes the methods developed by Petersen and Rajan (1997) to create a thorough index. The KZ index gages the degree of financing constraints faced by agribusiness. Several factors, such as net cash flow from operations, payout level, dividend holdings, degree of indebtedness, and growth index, contribute to its calculation. We adjust these factors for normalization based on the total assets at the start of the period. A higher KZ index indicates more significant financing constraints. The data presented in Table 12 demonstrates a negative correlation between trade credit financing and the KZ index. This suggests that access to trade credit offers alternative financing options for agribusinesses, which contributes to easing agribusiness financing constraints. Previous studies by Allen et al. (2005) and Cull et al. (2009) support this finding.

Table 12. Mechanism test.

The distortion of capital allocation is a fundamental issue that restricts the high-quality development of companies. Neoclassical economic theory emphasizes that the demand for factors of production by a firm is determined by the marginal cost and marginal benefit associated with their use. However, in practice, the marginal cost and marginal benefit of using factors of production often differ, leading to inefficient investments that significantly hinder the enterprise’s pursuit of high-quality development. In their study, Xing et al. (2023) discovered that enhancing the effectiveness of resource allocation can boost firms’ overall factor productivity. Efficiently addressing the issue of inadequate investment in agricultural firms holds significant practical importance in enhancing their innovative capacity, improving TFP, and achieving high-quality development.

In this paper, we refer to Richardson (2006) and Li and Huang (2020) to measure the investment efficiency of the company to build the model (3).

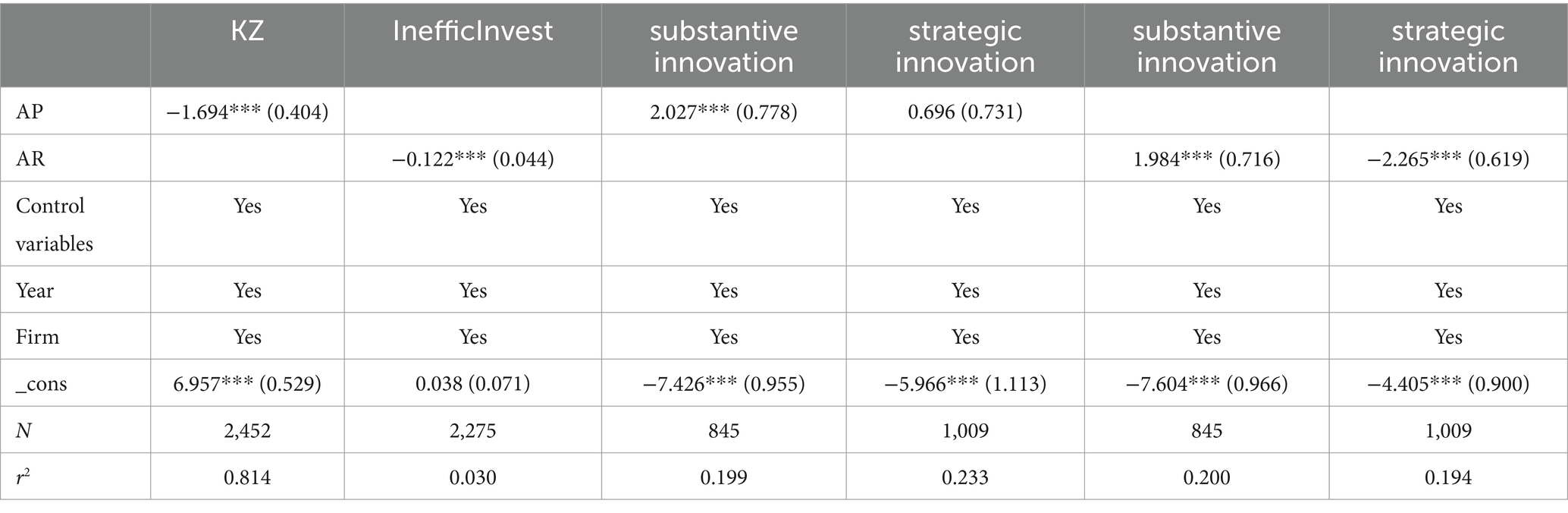

where is the firm’s actual new investment expenditures in year t; denotes the firm’s growth capacity in year t-1, as measured by Tobin’s Q; stands for denotes the age of the firm at year t-1; denotes the firm’s financial leverage in year t-1, as measured by gearing; denotes the firm’s cash flow in year t-1; denotes the size of the firm’s assets in year t-1; denotes the firm’s stock return in year t-1; denotes t − 1 year’s new investment expenditures; denotes the industry dummy variable; and denotes the year dummy variable. Further, perform OLS regression on the model (3) to get the model’s residuals. As estimated by the model, the magnitude of these residuals represents the extent of the company’s inefficiency investment. A higher absolute value of the residuals indicates more significant inefficiency in the investment. Results in Table 12, column 2, show that the provision of trade credit can curb inefficient investment, which is conducive to increased efficiency in the use of funds and the promotion of TFP by enterprises.

Total factor productivity (TFP) refers to the portion of economic growth that cannot be accounted for by the increase in inputs from production factors. Technological innovation has a crucial role in enhancing the overall productivity of organizations. Schumpeter’s theory of economic growth posits that firms’ innovations can result in transferring factors of production from less productive companies to more productive companies. This process compels less productive firms to exit the market, ultimately enhancing the industry’s overall productivity (Bartelsman et al., 2013). Karafillis and Papanagiotou (2011) examined the correlation between innovation and organic agriculture. In a study conducted by Karafillis and Papanagiotou (2011), the connection between innovation and total factor productivity in organic agriculture was examined. Their research revealed a positive correlation between innovation and TFP in this field.

This research delves deeper into the influence of the supply and acquisition of trade credit on corporate innovation. This study measures innovation using company patent applications as a proxy variable. We can classify the patents granted to Chinese enterprises into three categories: innovation, utility model, and design. Invention patents are considered significant inventions aimed at advancing a company’s technical development and obtaining a competitive edge. Enterprises seeking to prioritize “quantity” and “speed” of invention may employ strategic innovation by obtaining design and utility model patents, which are comparatively less challenging.

The findings in Table 12 demonstrate that acquiring trade credit has a significant impact on promoting firms’ substantive innovation. In contrast, it does not significantly influence enterprises’ strategic innovation. Trade credit supply fosters substantial company innovation and significantly impeding strategic innovation. When combined with the prior theoretical research, it is further validated that businesses that get trade credit may mitigate financial limitations, enhance investment in innovation, enhance the quality of enterprise innovation, and foster high-quality business development.

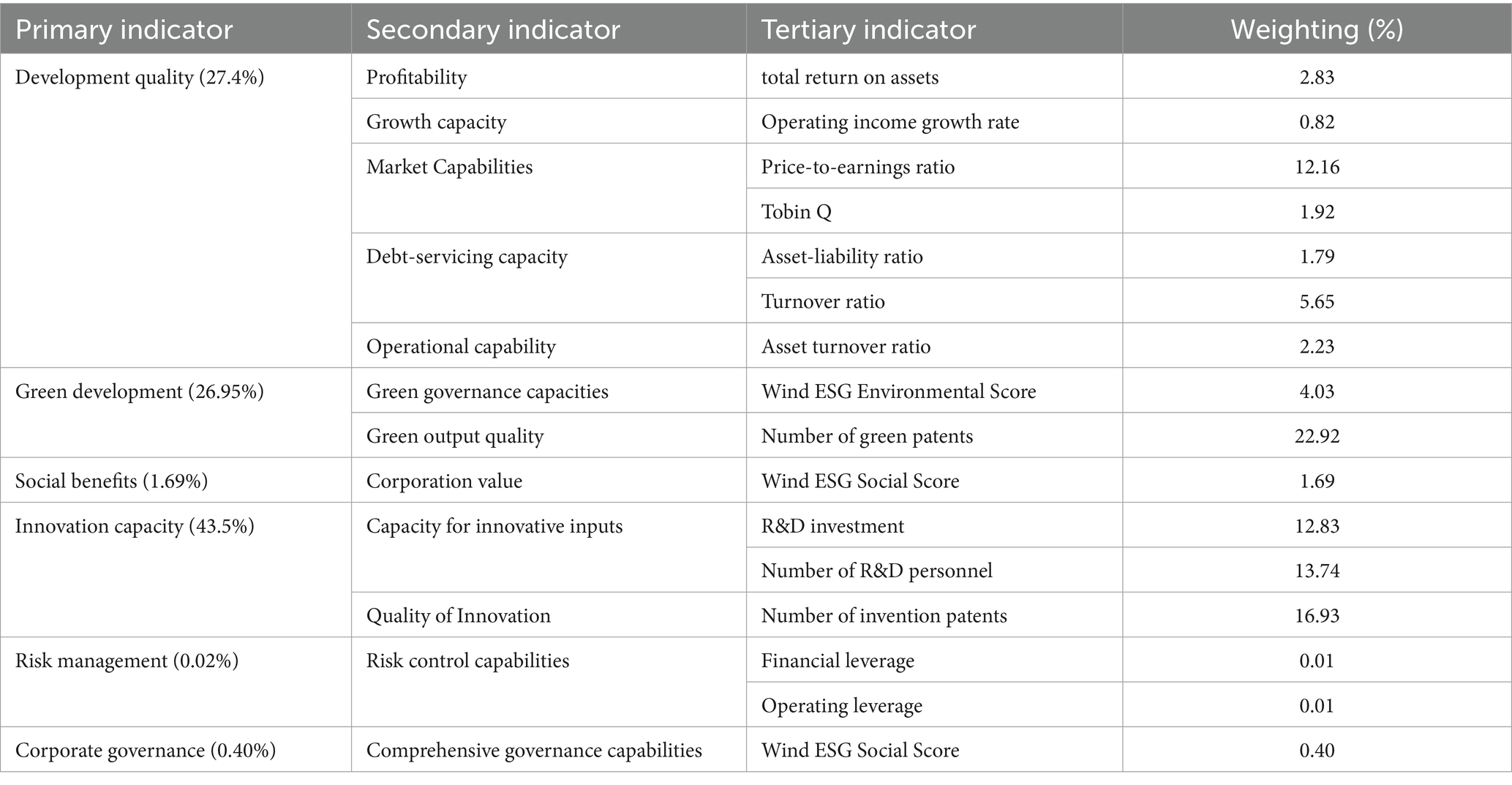

To address the limitations of using a single indicator to measure high-quality enterprise development. This study further creates a thorough index that evaluates the high-quality growth of businesses while accounting for their goals and processes. This paper refers to the enterprise high-quality development index proposed by Tian and Ding (2023) and analyzes the high-quality development index system of agricultural enterprises from the two aspects of the goal and internal process, which mainly include six first-level indexes: development quality, green development, social efficiency, innovation ability, risk management, and corporate governance. As well as 12 secondary indicators and 16 tertiary indicators to measure the high-quality development index of big agriculture, from Table 13, the high-quality development index weight ratio shows that each element of the impact of the size of the enterprise’s high-quality development index in which the enterprise’s innovation capacity accounted for the more significant proportion of the high-quality development index of agribusiness is the same as the theoretical analysis of the previous analysis.

Table 13. Construction of high-quality indicator system.

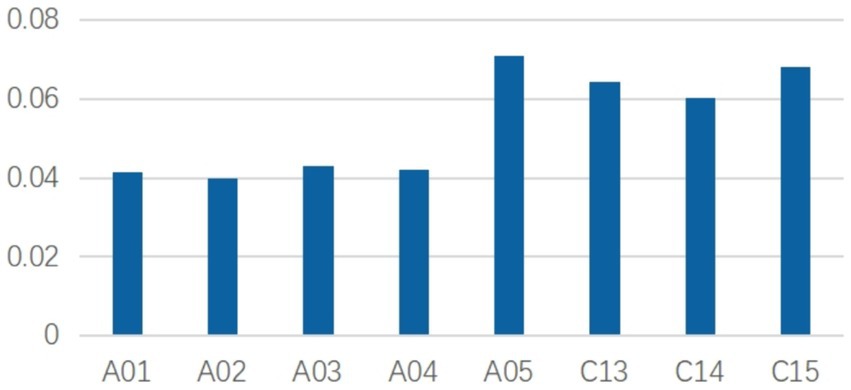

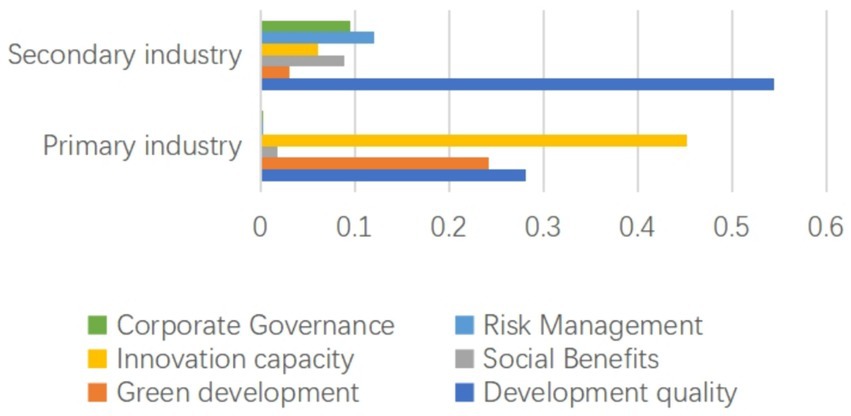

According to Figure 3, the industry-standard data for high-quality development indicators in agriculture reveals that the secondary and fishery service industries dominate. At the same time, the traditional agricultural primary sector lags in terms of high-quality development. Figure 4 demonstrates that the ability to innovate plays a crucial role in promoting high-quality development for primary sector agribusiness. In contrast, the quality of development profoundly impacts secondary agribusiness.

Figure 3. High-quality development industry average.

Figure 4. Statistics on various indicators by industry.

This study does a regression analysis to examine the impact of trade credit on the composite index of high-quality company development. The results in Table 14 indicate that obtaining and providing trade credit significantly promotes the high-quality growth of enterprises.

Table 14. High-quality indicator regression results.

The study performed a benchmark test and discovered that trade credit notably influences the overall factor productivity of agricultural businesses. To address the endogeneity issue in the model, the study replaced the variables and conducted a further robustness test using the least squares method. The study’s ultimate conclusion underscores the potential of trade credit accessibility and supply to boost enterprises’ TFP significantly. These results align with those of the benchmark regression and are consistent with the conclusions drawn by Detthamrong and Chansanam (2023).

Furthermore, this paper aims to examine the mechanism through how trade credit impacts businesses’ high-quality growth, using theoretical and empirical perspectives.

We further investigate the impact of trade credit on enterprise financing constraints, inefficient investment, and innovation. Research has shown that trade-credit financing can help companies overcome financial constraints. Additionally, offering trade credit can prevent companies from making inefficient investments (Karakoç, 2023), stimulate innovation, and improve TFP.

There is a deficiency in the current state of affairs regarding evaluating companies’ high-quality development, as there is a lack of a comprehensive index system and measuring procedures. Additionally, utilizing a single indicator to gage the quality of enterprise development has its limitations, as it may not accurately depict the influence of each contributing factor. To address this issue, this article employs the entropy value technique to appraise the high-quality growth of agricultural firms. This method, distinguished by six primary and 13 innovative indicators, has proven efficient in empirical testing. Moreover, the study has revealed that trade credit plays a significant role in enhancing firms’ high-quality development index. This finding further solidifies the credibility and robustness of the conclusions presented in this research.

Government policies should be strengthened to support agribusinesses and mitigate their long production cycles and financing constraints. Implementing the Property Law has significantly improved productivity and corporate profits. At the same time, a well-functioning financial system can help alleviate financing constraints and improve corporate governance, leading to increased agricultural productivity and modernization. The reform of the domestic financial market should also be promoted, including improving the informal financial market and establishing an enterprise information disclosure system. Supply chain finance should be actively developed to enhance financial service levels for the agricultural industry.

At the enterprise level, businesses should leverage bank and trade credit to attract talent and promote technological progress, resulting in improved productivity. Additionally, internal governance mechanisms, such as improving information disclosure, should be enhanced to obtain more financial support and increase competitiveness. The utilization of supply chain finance is also encouraged to improve overall financial services for agricultural enterprises.

China’s agricultural development faces challenges such as overconsumption of resources, reliance on inputs, and poor management. This has hindered sustainable development and led to a lack of competitiveness. To improve, China must adopt a new model, enhance sustainability, and promote transformation and upgrading for long-term growth. The concept of extensive agriculture sees the sector as an interconnected system and argues that trade credit can boost high-quality growth by addressing financing constraints, curbing inefficient investments, and promoting innovation.

Data are available from the corresponding author upon reasonable request.

JW: Conceptualization, Data curation, Writing – original draft. TL: Resources, Writing – review & editing, Project administration. QL: Writing – review & editing, Validation, Visualization. XL: Funding acquisition, Writing – review & editing.

The author(s) declare that financial support was received for the research, authorship, and/or publication of this article. This research was supported by the National Social Science Foundation of China (Project Title: Research on the micro-mechanism of trade credit affecting the high-quality development of the real economy under the digital economy, Grant No. 21BJL035).

The authors declare that the research was conducted without any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Abuhommous, A. A. A., and Almanaseer, M. (2021). The impact of financial and trade credit on firms market value. J. Asian Finan. Econ. Bus. 8, 1241–1248. doi: 10.13106/JAFEB.2021.VOL8.NO3.1241

Allen, F., Qian, J., and Qian, M. (2005). Law, finance, and economic growth in China. J. Financ. Econ. 77, 57–116. doi: 10.1016/j.jfineco.2004.06.010

Almeida, H., and Wolfenzon, D. (2006). Should business groups be dismantled? The equilibrium costs of efficient internal capital markets. J. Financ. Econ. 79, 99–144. doi: 10.1016/j.jfineco.2005.02.001

Ayyagari, M., Demirgüç-Kunt, A., and Maksimovic, V. (2010). Formal versus informal finance: evidence from China. Rev. Financ. Stud. 23, 3048–3097. doi: 10.1093/rfs/hhq030

Bartelsman, E., Haltiwanger, J., and Scarpetta, S. (2013). Cross-country differences in productivity: the role of allocation and selection. Am. Econ. Rev. 103, 305–334. doi: 10.1257/aer.103.1.305

Białek-Jaworska, A., and Nehrebecka, N. (2016). The role of trade credit in business operations. Argum. Oecon. 37, 189–231.doi: 10.15611/aoe.2016.2.08

Cao, W., Feng, Y., Yu, C., and Wan, D. (2022). RMB exchange rate changes, corporate innovation and manufacturing total factor productivity. Econ. Res. 57, 65–82.

Cull, R., Xu, L. C., and Zhu, T. (2009). Formal finance and trade credit during China's transition. J. Financ. Intermed. 18, 173–192. doi: 10.1016/j.jfi.2008.08.004

Dabla-Norris, E., Kersting, E. K., and Verdier, G. (2012). Firm productivity, innovation, and financial development. South. Econ. J. 79, 422–449. doi: 10.4284/0038-4038-2011.201

Deshmukh, J. (2022). “Informal trade credit guarantee networks” in Persistent and emerging challenges to development: Insights for policy-making in India (Singapore: Springer Nature Singapore), pp. 371–384.

Detthamrong, U., and Chansanam, W. (2023). Do the trade credit influence firm performance in agro-industry? Evidence from Thailand. Heliyon 9:e14561. doi: 10.1016/j.heliyon.2023.e14561

Ding, F., Liu, Q., Shi, H., Wang, W., and Wu, S. (2023). Firms' access to informal financing: the role of shared managers in trade credit access. J. Corp. Finan. 79:102388. doi: 10.1016/j.jcorpfin.2023.102388

Dong, L., Chen, J., and Guo, H. (2022). The impact of investor sentiment on corporate total factor productivity. J. Zhongnan Univ. Econom. Law 2, 78–90. doi: 10.19639/j.cnki.issn1003-5230.2022.0018.%W.CNKI

Dong, Y., Li, C., and Li, H. (2021). Customer concentration and M&A performance. J. Corp. Finan. 69:102021. doi: 10.1016/j.jcorpfin.2021.102021

Fisman, R., and Love, I. (2003). Trade credit, financial intermediary development, and industry growth. J. Financ. 58, 353–374. doi: 10.1111/1540-6261.00527

Gashayie, A., and Singh, M. (2015). Agricultural finance constraints and innovative models experience for Ethiopia: empirical evidence from developing countries. Res. J. Finan. Account. 6, 39–49.

Grau, A. J., and Reig, A. (2018). Trade credit and determinants of profitability in Europe. The case of the Agri-food industry. Int. Bus. Rev. 27, 947–957. doi: 10.1016/j.ibusrev.2018.02.005

Guo, X. (2023). The impact of financial openness on total factor productivity of fishery enterprises—from the perspective of alleviating financing constraints. China's Fish. Econ. 41, 82–91.

Hsieh, C.-T., and Klenow, P. J. (2009). Misallocation and manufacturing TFP in China and India. Q. J. Econ. 124, 1403–1448. doi: 10.1162/qjec.2009.124.4.1403

Huang, H., Qi, B., and Chen, L. (2022). Innovation and high-quality development of enterprises—also on the effect of innovation driving the transformation of China’s economic development model. Sustain. For. 14:8440. doi: 10.3390/su14148440

Ju, X., Lu, D., and Yu, Y. (2013). Financing constraints, working capital management and corporate innovation sustainability techniques. Econ. Res.

Jun, J., Danlin, S., Xuanyu, J., and Zhihong, Y. (2017). Creditor protection and corporate innovation. Finan. Res. 11, 128–142.

Karafillis, C., and Papanagiotou, E. (2011). Innovation and total factor productivity in organic farming. Appl. Econ. 43, 3075–3087. doi: 10.1080/00036840903427240

Karakoç, B. (2023). Trade credit and corporate investment: enhancing value creation. J. Asia Pac. Econ., 1–30. doi: 10.1080/13547860.2023.2266271

Krishnan, K., Nandy, D. K., and Puri, M. (2015). Does financing spur small business productivity? Evidence from a natural experiment. Rev. Financ. Stud. 28, 1768–1809. doi: 10.1093/rfs/hhu087

Levinsohn, J., and Petrin, A. (2003). Estimating production functions using inputs to control for unobservables. Rev. Econ. Stud. 70, 317–341. doi: 10.1111/1467-937X.00246

Li, W., and Huang, S. (2020). Relational shareholders and financing constraints—empirical evidence based on family groups. Account. Res. 2, 74–89.

Li, D., and Li, D. (2020). Comparison and analysis of measurement methods of Total factor productivity. Int. J. Front. Eng. Technol 2, 18–30. doi: 10.25236/IJFET.2020.020102

Liu, T. (2021). Study on the influence of commercial credit on technological innovation of enterprises. China Social Sciences Press: Beijing, China.

Liu, T., Liu, W., Elahi, E., and Liu, X. (2022a). Supply chain finance and the sustainable growth of Chinese firms: the moderating effect of digital finance. Front. Environ. Sci. 10:182. doi: 10.3389/fenvs.2022.922182

Liu, T., Wang, J., Rathnayake, D. N., and Louembé, P. A. (2022b). The impact of trade credit on firm innovation: evidence from Chinese A-share listed companies. Sustain. For. 14:1481. doi: 10.3390/su14031481

Lumpkin, G. T., and Dess, G. G. (1996). Clarifying the entrepreneurial orientation construct and linking it to performance. Acad. Manag. Rev. 21, 135–172. doi: 10.2307/258632

Martínez-Sola, C., García-Teruel, P. J., and Martínez-Solano, P. (2014). Trade credit and SME profitability. Small Bus. Econ. 42, 561–577. doi: 10.1007/s11187-013-9491-y

Mei, D., and Cheng, M. (2021). Trade credit financing, customer concentration and corporate R&D investment. Econ. Manag. Rev. 37, 139–149. doi: 10.13962/j.cnki.37-1486/f.2021.05.012.%W.CNKI

Meltzer, A. H. (1960). Mercantile credit, monetary policy, and size of firms. Rev. Econ. Stat. 42, 429–437. doi: 10.2307/1925692

Mian, S. L., and Smith, C. W. Jr. (1992). Accounts receivable management policy: theory and evidence. J. Financ. 47, 169–200. doi: 10.1111/j.1540-6261.1992.tb03982.x

Molina, C. A., and Preve, L. A. (2012). An empirical analysis of the effect of financial distress on trade credit. Financ. Manag. 41, 187–205. doi: 10.1111/j.1755-053X.2012.01182.x

Opler, T. C., and Titman, S. (1994). Financial distress and corporate performance. J. Financ. 49, 1015–1040. doi: 10.1111/j.1540-6261.1994.tb00086.x

Pepur, S., Kovač, D., and Ćurak, M. (2020). Factors behind trade credit financing of SMEs in Croatia. Zbornik Veleučilišta u Rijeci 8, 59–76. doi: 10.31784/zvr.8.1.11

Petersen, M. A., and Rajan, R. G. (1997). Trade credit: theories and evidence. Rev. Financ. Stud. 10, 661–691. doi: 10.1093/rfs/10.3.661

Rajan, R., and Zingales, L. (1996). Financial dependence and growth. Mass: National bureau of economic research Cambridge. doi: 10.3386/w5758

Ren, C., Liu, S., Van Grinsven, H., Reis, S., Jin, S., Liu, H., et al. (2019). The impact of farm size on agricultural sustainability. J. Clean. Prod. 220, 357–367. doi: 10.1016/j.jclepro.2019.02.151

Restuccia, D., and Rogerson, R. (2017). The causes and costs of misallocation. J. Econ. Perspect. 31, 151–174. doi: 10.1257/jep.31.3.151

Richardson, S. (2006). Over-investment of free cash flow. Rev. Acc. Stud. 11, 159–189. doi: 10.1007/s11142-006-9012-1

Ryzhenkov, M. (2016). Resource misallocation and manufacturing productivity: the case of Ukraine. J. Comp. Econ. 44, 41–55. doi: 10.1016/j.jce.2015.12.003

Sandvik, I. L., and Sandvik, K. (2003). The impact of market orientation on product innovativeness and business performance. Int. J. Res. Mark. 20, 355–376. doi: 10.1016/j.ijresmar.2003.02.002

Schwartz, R. A. (1974). An economic model of trade credit. J. Financ. Quant. Anal. 9, 643–657. doi: 10.2307/2329765

Seifert, D., Seifert, R. W., and Protopappa-Sieke, M. (2013). A review of trade credit literature: opportunities for research in operations. Eur. J. Oper. Res. 231, 245–256. doi: 10.1016/j.ejor.2013.03.016

Shao, K., and Wang, X. (2023). Do government subsidies promote enterprise innovation?——Evidence from Chinese listed companies. J. Innov. Knowl. [J]. 8:100436.

Sheng, M., and Liu, Y. (2021). How does foreign direct investment affect total factor productivity of enterprises? Discuss. Mod. Econ. 6, 84–93. doi: 10.13891/j.cnki.mer.2021.06.011.%W.CNKI

Shuai, H., Li, Q., Liu, C., and Luo, D. (2023). How can investment in innovation enhance a company's competitive advantage? ——based on the perspective of supply chain intermediary. J. Xinjiang Univ. (Philosophy and Social Sciences Edition) 51, 9–25. doi: 10.13568/j.cnki.issn1000-2820.2023.06.002

Smith, J. K. (1987). Trade Credit and Informational Asymmetry. J. Finance. 42, 863–872. doi: 10.1111/j.1540-6261.1987.tb03916.x

Sokolova, A., and Litvinenko, G. (2020). "Innovation as a source of agribusiness development", in: IOP Conference Series: Earth and Environmental Science. Vol. 421, No. 2, p. 022053 IOP Publishing.

Summers, B., and Wilson, N. (2003). Trade credit and customer relationships. Manag. Decis. Econ. 24, 439–455. doi: 10.1002/mde.1041

Tian, D., and Ding, B. (2023). Research on the measurement and mechanism of high-quality enterprise development: based on the perspective of organizational resilience. Chin. Soft Sci. 9, 154–170.

Wang, Y. (2014). Financial restraint and trade credit secondary allocation function. Econ. Res. 49, 86–99.

Wang, D. (2022). Technological innovation, financing constraints and enterprise total factor productivity. Financ. Theory Res. 5, 105–112. doi: 10.13894/j.cnki.jfet.2022.05.003.%W.CNKI

Wang, T., Lan, Q., and Chu, Y. (2013). Supply chain financing model: based on China's agricultural products supply chain. Appl. Mech. Mater. 380-384, 4417–4421. doi: 10.4028/www.scientific.net/AMM.380-384.4417

Wang, G., Mi, L., Hu, J., and Qian, Z. (2022). Spatial analysis of agricultural eco-efficiency and high-quality development in China. Front. Environ. Science 10. doi: 10.3389/fenvs.2022.847719

Wen, D. (2019). Resource misallocation, total factor productivity and the growth potential of China’s manufacturing industry. Economics(Quarterly) 18, 617–638. doi: 10.13821/j.cnki.ceq.2019.01.10

Wilson, N., and Summers, B. (2002). Trade credit terms offered by small firms: survey evidence and empirical analysis. J. Bus. Financ. Acc. 29, 317–351. doi: 10.1111/1468-5957.00434

Wu, L., Chen, W., Lin, L., and Feng, Q. (2021). Research on the impact of innovation and green technology innovation on enterprise total factor productivity. Math. Statis. Manag. 40, 319–333. doi: 10.13860/j.cnki.sltj.20200818-007.%W.CNKI

Xing, E., Deng, Y., Yuan, L., and Dai, P. (2023). Information disclosure quality and corporate total factor productivity. Chin. Soft Sci. 7, 114–126.

Yang, R. (2015). Research on total factor productivity of Chinese manufacturing enterprises. Econ. Res. 50, 61–74.

Yi, Z., Wang, Y., and Chen, Y. J. (2021). Financing an agricultural supply chain with a capital-constrained smallholder farmer in developing economies. Prod. Oper. Manag. 30, 2102–2121. doi: 10.1111/poms.13357

Zhang, L., and Pang, C. (2023). The impact of financing constraints on enterprise total factor productivity - based on data from GEM listed companies. Soc. Sci. 7, 69–75.

Keywords: trade credit, agribusiness, total factor productivity, high-quality development system, entropy approach

Citation: Wang J, Liu T, Liu Q and Liu X (2024) Does trade credit facilitate high-quality development in agricultural enterprises? – Insights from Chinese enterprises. Front. Sustain. Food Syst. 8:1396739. doi: 10.3389/fsufs.2024.1396739

Edited by:

Ruishi Si, Xi'an University of Architecture and Technology, ChinaCopyright © 2024 Wang, Liu, Liu and Liu. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Tinghua Liu, aGFkZHkxMDA5QDE2My5jb20=; Xiao Liu, eF9saXV4aWFvQDEyNi5jb20=

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.