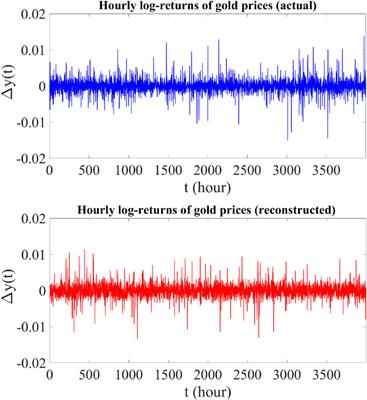

ORIGINAL RESEARCHPublished on 18 Jul 2024Introducing a new approach for modeling stock market prices using the combination of jump-drift processesAli Asghar MovahedHoushyar Noshaddoi 10.3389/fphy.2024.14025931,026 views

Published inFrontiers in Physics Statistical and Computational PhysicsSoft Matter PhysicsComplex Physical Systems2.1 impact factor4.6 citescore