Mário B. Ferreira1

Mário B. Ferreira1 Filipa de Almeida2,3*

Filipa de Almeida2,3* Jerônimo C. Soro1

Jerônimo C. Soro1 Márcia Maurer Herter4

Márcia Maurer Herter4 Diego Costa Pinto5

Diego Costa Pinto5 Carla Sofia Silva1

Carla Sofia Silva1- 1CICPSI, Faculdade de Psicologia, Universidade de Lisboa, Lisbon, Portugal

- 2Faculdade de Psicologia, Universidade de Lisboa, Lisbon, Portugal

- 3Católica Lisbon School of Business and Economics, Universidade Católica Portuguesa, Lisbon, Portugal

- 4Business and Law Research Unit, Universidade Europeia, Lisbon, Portugal

- 5NOVA Information Management School (NOVA IMS), Universidade Nova de Lisboa, Lisbon, Portugal

This paper aims to explore the association between over-indebtedness and two facets of well-being – life satisfaction and emotional well-being. Although prior research has associated over-indebtedness with lower life satisfaction, this study contributes to the extant literature by revealing its effects on emotional well-being, which is a crucial component of well-being that has received less attention. Besides subjective well-being (SWB), reported health, and sleep quality were also assessed. The findings suggest that over-indebted (compared to non-over-indebted) consumers have lower life satisfaction and emotional well-being, as well as poorer (reported) health and sleep quality. Furthermore, over-indebtedness impacts life satisfaction and emotional well-being through different mechanisms. Consumers decreased perceived control accounts for the impact of over-indebtedness on both facets of well-being (as well as on reported health and sleep). Financial well-being (a specific component of life satisfaction), partly mediates the impact of indebtedness status on overall life satisfaction. The current study contributes to research focusing on the relationship between indebtedness, well-being, health, and sleep quality, and provides relevant theoretical and practical implications.

Introduction

Being indebted at certain stages of life may be a means of consumption smoothing across the lifecycle, improving households’ economic welfare (e.g., Hall, 1978; Lombardi et al., 2017). However, debt becomes most problematic when it leads to over-indebtedness, that is, when it exceeds household resources leading to the inability to meet all payment obligations and to cover living expenses over long time periods. Indeed, the burden of over-indebtedness has been shown to have a negative impact on several indicators of psychological and physical health.

This study seeks to contribute to the extant literature by focusing on the relationship between debt and subjective well-being (SWB). Specifically, we explore how being over-indebted (vs. not being over-indebted) affects two different facets of SWB: life satisfaction and emotional well-being. In addition, the current study also compares over-indebted and non-over-indebted consumers on measures of reported health and sleep quality.

Finally, the mediating role of (a) consumers’ financial well-being (a specific component of life satisfaction); (b) financial anxiety; and (c) perceived sense of control, is explored in order to look for empirical evidence on the underlying processes of the relationship between debt and SWB as well as the relationship between debt and measures of health and sleep quality.

In what follows, we begin by briefly reviewing different concepts of over-indebtedness. We then notice that while there is a substantial amount of literature on the detrimental effects of over-indebtedness, there is a relative shortage of studies on the impact of over-indebtedness on SWB. Finally, the goals and hypotheses of the study here reported are presented.

Several different definitions of over-indebtedness and consequently different ways on how to measure it have been proposed in the literature (Berthoud and Kempson, 1992; Bridges and Disney, 2004; Kempson et al., 2004; European commission, 2008; D’Alessio and Iezzi, 2013; Angel, 2016). Nevertheless, research has been converging on a shared set of indicators (Keese, 2009; BIS–Department for Business, Innovation and Skill, 2010) that broadly refer to four features of over-indebtedness: making high repayments relative to income (e.g., households spending more than 30% of their gross monthly income on unsecured repayments), having a high number of credit commitments (e.g., four or more credit loans), being in arrears, and the subjective perception of debt as a burden (D’Alessio and Iezzi, 2013).

All of these indicators of debt difficulties provide potentially valuable information but suffer from some drawbacks. The first two set fixed limits – of repayment-to-income ratios and of number of credit commitments – to define and measure over-indebtedness. However, such limits depend on income level and household assets. For instance, debt (relative to income) and number of credits can increase above defined limits for households with high levels of income, without this necessarily making debt management problems more acute.

By using information on household arrears in making payments, the third feature is less vulnerable to the problem of setting arbitrary limits. However, the definition of the point where over-indebtedness begins based on arrears depends on the judged seriousness of the arrears, which, in turn, is likely to be dependent on the financial circumstances of the household, among other variables.

Given these limitations associated with the first three indicators, D’Alessio and Iezzi (2013) argued that a better way to identify over-indebtedness may be to enquire households on whether or not they are facing debt repayment difficulties. The downside of this type of subjective indicator is that the interpretation of terms such as “heavy repayment difficulties” is likely to vary among households (Drentea and Lavrakas, 2000) and to be sensitive to consumer’s individual differences.

Finally, other objective indicators of over-indebtedness, such as judicial decisions declaring personal bankruptcy (or other court arranged solutions for resolution), are likely to be too narrow in the identification of over-indebted households failing to capture several, if not most, circumstances of over-indebtedness (D’Alessio and Iezzi, 2013).

One way to attenuate this problem is to check for the existence of more than one indicator when looking into potential cases of over-indebtedness (Białowolski, 2019). In the study, here presented, over-indebted households are consumers who voluntary looked for the help of debt advise experts, reporting an inability to meet recurrent expenses, and who in general spent more than 30% of their gross monthly income on total borrowing repayments (secured and unsecured).

The reviewed indicators of over-indebtedness mostly refer to the process of becoming over-indebted, rather than the outcomes associated with having problems with debts. However, being over-indebted has considerable negative impacts on households. From an economical perspective, over-indebted households often face liquidity constrains (Attanasio, 1995; Crook, 2003) as they become unable to borrow against future earnings, making it increasingly challenging to accommodate their financial needs.

From a socio-psychological perspective, individuals with unmet loan payments have been shown to display more suicidal ideation and are at a higher risk of depression than those without such financial difficulties (e.g., Hintikka et al., 1998; Gathergood, 2012; Turunen and Hiilamo, 2014). Unpaid financial obligations have also been associated with poorer subjective health, deterioration of health-related behavior, and physical illness (Lenton and Mosley, 2008; Bridges and Disney, 2010; Chmelar, 2013; Guiso and Sodini, 2013; Sweet et al., 2013; Turunen and Hiilamo, 2014; Clayton et al., 2015). Confirming this pattern, a recent longitudinal study of Finnish adults found an association between over-indebtedness and an increased incidence of various chronic diseases (Blomgren et al., 2016). More recently, Warth et al. (2019) found a negative relationship between over-indebtedness and sleep quality. Notably, poor sleep plays a major role in a variety of health problems, from hypertension (Gangwisch et al., 2006; Buxton and Marcelli, 2010; Meng et al., 2013) to diabetes (Buxton and Marcelli, 2010; Morselli et al., 2012; Zizi et al., 2012; Grandner et al., 2014) and mortality (Gallicchio and Kalesan, 2009; Grandner and Patel, 2009; Cappuccio et al., 2010; Grandner et al., 2010).

Taken together, such detrimental consequences are worrisome given the increasing number of over-indebted households across Europe and around the world (e.g., Betti et al., 2007; Barba and Pivetti, 2009; Harvey, 2011; Kempson, 2015), and serve to highlight the importance of further research to better understand the relationship between over-indebtedness and different indicators of well-being and health.

While there is a large body of literature on the risk factors, remedies, and detrimental effects of over-indebtedness, there is a relative lack of research on the impact of debt on SWB. This is surprising given the longstanding research interest in the relationship between finances and SWB (e.g., Diener and Biswas-Diener, 2002; Howell and Howell, 2008). Recently, Tay et al. (2017) conducted a systematic review and meta-analysis of the literature on debt and different aspects of SWB, including overall well-being (e.g., life satisfaction), domain-specific (e.g., financial well-being), and emotional well-being (i.e., positive and negative feelings). Although only a relatively small number of empirical studies were found, results suggest a negative, but somewhat weak association between debt and SWB (but see Białowolski et al., 2019). Several reasons may contribute to this. First, only seven studies of the 19 identified by Tay et al. (2017) met their criteria for meta-analysis. Second, according to the hedonic treadmill hypothesis (Brickman and Campbell, 1971), people rapidly adapt to change. This suggests that the deteriorated life circumstances associated with indebtedness could have an attenuated effect on life satisfaction with the passage of time. Indeed, prior research indicates that most life circumstances quickly cease to influence global reports of SWB (Easterlin, 1995; Kahneman et al., 2004).

Third, Tay et al. (2017) did not distinguish between being the holder of manageable debt and being over-indebted (although their meta-analysis showed that variables, such as level of debt and overall financial resources, play a critical role as moderators of the relationship between debt and SWB).

In line with other research (Angel, 2016; Białowolski et al., 2019), the present study considers this crucial distinction, as being over-indebted is not merely a function of debt but it may involve, as aforementioned, several other features. Moreover, since over-indebtedness is often associated with careless consumer behavior and financial imprudence (Disney et al., 2008; Anderloni and Vandone, 2010), being over-indebted is often a source of social stigma and prejudice, which puts additional pressure on these consumers’ already difficult living conditions.

Furthermore, although prior research (e.g., O’Neill et al., 2005; Zhang and Kemp, 2009; Drentea and Reynolds, 2012; Hogan et al., 2013; Olson-Garriott et al., 2015; see Tay et al., 2017, for a review) has used different measures of well-being to understand how people think and feel about their lives, it has not clearly distinguished between the impact of over-indebtedness on two qualitatively different facets of SWB: life satisfaction (based on a global evaluation by the individual of his/her life) and emotional well-being (the affect experienced by an individual on a more day-to-day basis; Pavot and Diener, 1993; Kahneman and Riis, 2005). Nonetheless, life satisfaction and emotional well-being are different constructs with moderate to high discriminant validity (Lucas et al., 1996; see also Dolan et al., 2017). For instance, United States consumers who earn above $75,000 annually are increasingly more satisfied with their lives (life satisfaction) but they do not have higher emotional well-being (based on experienced feelings; Kahneman and Deaton, 2010).

In this paper, the effect of being over-indebted (vs. not being over-indebted) on life satisfaction and emotional well-being is explored. In addition, the current study also includes measures of global subjective health and sleep quality in which over-indebted and non-over-indebted consumers are also compared. The goal is to ascertain whether over-indebted consumers show lower levels of SWB (both life satisfaction and emotional well-being) than non-over-indebted consumers. Based on prior cited research, over-indebted consumers are further expected to have poorer reported health and sleep quality, in addition to increased sleep-related disturbances, than their non-over-indebted counterparts.

Furthermore, two possible but not mutually exclusive accounts are considered for why over-indebted consumers might show lower SWB (as well as lower quality of health and sleep) than non-over-indebted consumers. First, given that financial well-being is one of the key life domains that inform SWB (Diener et al., 1999; Kahneman, 1999), becoming over-indebted may adversely affect financial well-being, and thus contribute to decreasing SWB. However, since financial well-being is defined as personal satisfaction with one’s financial status (i.e., a specific component of life satisfaction), the mediating role of financial well-being is expected to occur for life satisfaction but not for emotional well-being.

Second, being indebted greatly limits the extent to which consumers may attain their life goals, calling into question the fulfillment of fundamental needs of autonomy and self-control, which are crucial for promoting SWB (Sheldon et al., 2010; Tay and Diener, 2011). Hence, by leading to the depletion of financial resources, over-indebtedness may not only create financial anxiety but also reduce consumers’ perceived self-control over their own lives. Both aspects (financial anxiety and reduced self-control) could be expected to lower SWB.

Since financial anxiety and perceived self-control are likely to affect not only the global attainment of one’s life goals but also consumers’ daily emotional experience, these factors are expected to mediate both life satisfaction and SWB.

We further expect to find that financial satisfaction, perceived control, and financial anxiety mediate the relationship between over-indebtedness and both health and sleep. Such expectation is in line with previous literature. Indeed, financial satisfaction has been found to be associated to both health (Kostelecky, 1994; Hsieh, 2001; Hansen et al., 2008) and sleep quality (Summers and Gutierrez, 2018). Perceived control has also been shown to have a significant impact on health and sleep (Bobak et al., 1998; Bosma et al., 1999; Gerstorf et al., 2011; Adachi et al., 2013; Gould et al., 2016). Finally, stress (Keller et al., 2012) and anxiety (Gould et al., 2016) both have a negative impact on one’s health and sleep.

Materials and Methods

Participants

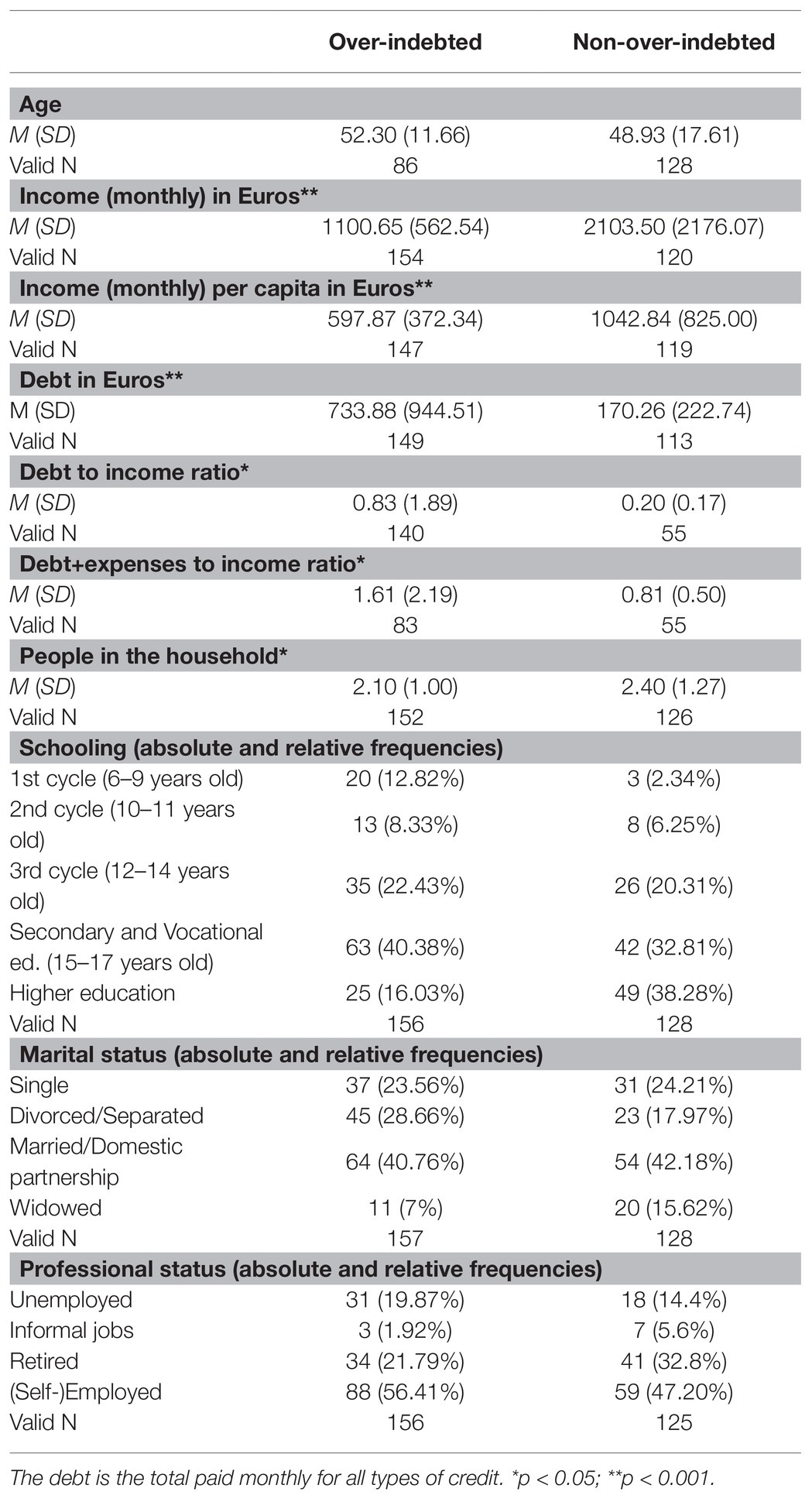

Three hundred and sixty-five Portuguese consumers responded to the study questionnaire, of which 236 were over-indebted and 129 were non-over-indebted. The questionnaire was created and applied in the context of a research project on over-indebtedness funded by the Portuguese science foundation with the collaboration of the debt advice department of an NGO for the Consumer Defense (DECO). DECO’s debt advice experts offer counseling to over-indebted households who contact them free of charge. Households may contact DECO online (by email or through their website) or directly in their offices. Over-indebted consumers (i.e., consumers reporting an inability to meet recurrent expenses, and who in general spent more than 30% of their gross monthly income on total borrowing repayments – secured and unsecured) who contacted DECO between 2017 and 2018 were invited to voluntarily participate in the study by filling the questionnaire. Data from non-over-indebted consumers were collected during the same time period through convenience sampling from different sources (e.g., part-time courses on different areas of education and development promoted by the city governments and other NGO platforms of social action). Six participants of this sample reported being over-indebted and their data were included in the sample of over-indebted consumers. A summary of the socio-demographic measures of both over-indebted and non-over-indebted groups are displayed in Table 1. Apart from variables pertaining to debt, which were expected to differ between the groups, income, and education also differed significantly between the over-indebted and the non-over-indebted groups.

Table 1. Socio-demographic characteristics of over-indebted and non-over-indebted samples of participants.

Materials

The questionnaire included (a) socio-demographic items (e.g., marital status, schooling, professional status, and number of people in the household); (b) questions on financial aspects of the respondent’s life (e.g., income, monthly expenses, and monthly installments of loans); and (c) the main dependent measures of the current study: life satisfaction, emotional well-being, sleep quality, and reported health. Perceived control, financial anxiety, and financial well-being were also assessed as potential mediators. Finally, the questionnaire included other measures collected for different research purposes, which will not be addressed herein.

Life Satisfaction

Life Satisfaction was assessed using the Cantril Self-Anchoring Striving Scale (Cantril, 1965). Participants were asked to imagine a ladder with steps from 0 to 10, where 0 was the worst possible life for them and 10 the best possible life for them. They were then asked to indicate the step on which they saw their lives at that particular time and the step on which they envisaged their lives 5 years from then.

Emotional Well-Being

Emotional well-being was assessed using a simplified version of the Day Reconstruction Method (DRM – Kahneman et al., 2004), in which participants were required to indicate on a five-point rating scale (1 – not at all, 5 – extremely) how intensely they had felt a set of negative and positive emotions (used in the original DRM questionnaire) during the morning, afternoon, and evening of the previous day. The negative emotions included: frustrated, angry, depressed, hassled, and criticized. The positive emotions included: happy and competent. Mean responses for positive and negative emotions were obtained for each moment of the day and in total. Four scores of net affect (composed of the subtraction of the mean negative emotions from the mean positive ones) were computed, one for each part of the day (morning, afternoon, and evening) and one global score (entire day). Positive values represent positive net affect, and negative values represent negative net affect (Kahneman et al., 2004).

Reported Health

Health was evaluated by means of two questions: “Globally, how do you evaluate your health?” and “How do you evaluate your health compared to other people of your age?” based on the same rating scale (1 – Excellent, 2 – Good, 3 – Fair, 4 – Poor, and 5 – Very poor). Individual responses to these questions were averaged in a composite measure of self-reported health (Cronbach’s alpha = 0.91).

Sleep Quality

Subjective quality of sleep and sleep-related disturbances were measured using four questions from the Pittsburgh Sleep Quality Index (PSQI – Buysse et al., 1989). Three components of the PSQI were assessed: subjective sleep quality (“During the past month, how would you rate your sleep quality overall?,” using a four-point rating scale: 1 – Very good, 2 – Fairly good, 3 – Fairly bad, and 4 – Very bad); sleep duration (“During the past month how many hours of actual sleep have you managed to get at night? – This may differ to the number of hours you have spent in bed,” by means of the following four-point rating scale: (>7 h, 6–7 h, 5–6 h, and <5 h – where >7 = 1, 6–7 = 2, 5–6 = 3, and <5 = 4); and daytime dysfunction (“During the past month, how often have you had trouble staying awake while driving, eating meals, or engaging in social activity?,” measured with the following rating scale: 1 – Not at all during the past month; 2 – Less than once a week; 3 – Once or twice a week; and 4 – Three or more times a week and “During the past month, how much of a problem has it been for you to keep up enough enthusiasm to get things done?,” measured with the following scale: 1 – No problem at all; 2 – Only a slight problem; 3 – Somewhat of a problem; and 4 – A very big problem). A confirmatory factor analysis was performed to evaluate how well these four items defined an underlying sleep quality factor. Results of this analysis revealed a good model fit, χ2(2) = 9.18, p = 0.01; CFI = 0.98; TLI = 0.94; SRMR = 0.03). All factor loadings were highly significant (i.e., p < 0.001) and higher than 0.50. We then used the standardized factor loadings to calculate the composite reliability or coefficient omega (Ω), which was above the 0.70 benchmark for acceptable reliability (Ω = 0.78; Nunnally and Bernstein, 1994).

Perceived Control

Perceived control was measured with two questions adapted from the perceived stress scale of Cohen et al. (1983): “How often have you been feeling you do not have control over the important things in your life?” and “How often have you been feeling you are not able to deal with everything you have to do?” (Both using the following rating scale: 1 – Never, 2 – Hardly ever, 3 – Sometimes, 4 – Frequently, and 5 – Very frequently). Individual responses to these questions were averaged in a composite measure of perceived control (Cronbach’s alpha = 0.82).

Financial Anxiety

Financial anxiety was assessed using nine items from the Financial Anxiety Scale (FAS; Shapiro and Burchell, 2012, Study 1). Participants responded to the statements on a five-point rating scale from 1 (Totally disagree) to 5 (Totally agree). Examples of the FAS are: “Thinking about my personal finances can make me feel guilty,” “Thinking about my personal finances can make me feel anxious,” and “Discussing my finances can make my heart race or make me feel stressed” (Cronbach’s alpha = 0.86).

Financial Well-Being

Financial well-being was assessed by questioning participants on how satisfied they were with their financial status compared to their friends. Participants answered using a rating scale from 0 (Not satisfied at all) to 10 (Very satisfied).

Procedure

Over-indebted consumers responded to the questionnaire either in a paper form (while waiting for their individual appointment with DECO experts) or in an editable computer file sent to them by email (those who contacted the consumer defense association through its website or by email). Non-over-indebted consumers responded to the questionnaire on paper. Participants did not always respond to all the questions. As a consequence, there is some variation in the number of participants for each analysis. The questionnaire was approved by the ethics committee of the Faculdade de Psicologia of Universidade de Lisboa. Data from consumers were used with their informed consent and always anonymously.

Results

Comparing Between Over-Indebted and Non-over-Indebted Consumers

The following analyses tested for differences between over-indebted and non-over-indebted consumers in the measures of interest (life satisfaction, emotional well-being, sleep, and health). As the two samples were not fully matched in terms of education, monthly income, employment status, and marital status (Table 1), we controlled for the effect of these variables by creating a propensity score indicating the predicted probability of being over-indebted vs. non-over-indebted, given these four potentially confounding variables.

Life Satisfaction

Using the valid data from 219 participants (104 over-indebted and 115 non-over-indebted), a repeated measures ANCOVA was conducted with Indebtedness Status (over-indebted, non-over-indebted) as a between-participants factor; Time of life satisfaction (current life satisfaction; predicted future life satisfaction) as a within-participants factor; and the propensity score as a covariate. The dependent variable was participant’s assessment of their own life satisfaction using ladder of Cantril (1965).

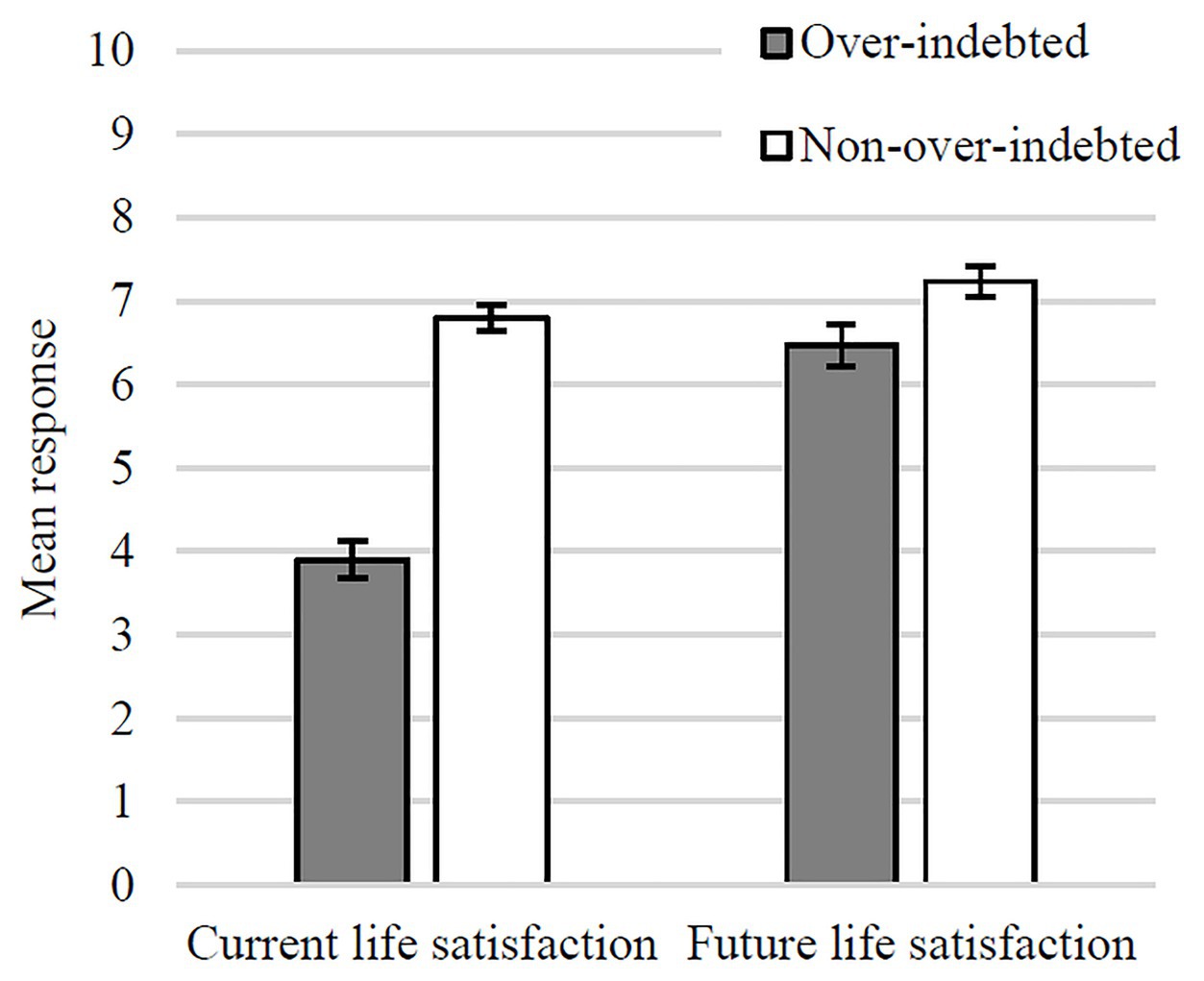

The ANCOVA yielded two main effects and one interaction (Figure 1). A main effect of Indebtedness Status, F(1, 216) = 47.64, p < 0.001, ηp2 = 0.18, such that over-indebted participants reported poorer overall life satisfaction [M = 5.18, SE = 0.19, 95% CI (4.81, 5.55)] than their non-over-indebted counterparts [M = 7.00, SE = 0.18, 95% CI (6.68, 7.37)]. A main effect of Time of life satisfaction, F(1, 216) = 4.46, p = 0.04, ηp2 = 0.02, such that all participants reported higher predicted future life satisfaction [M = 6.85, SE = 0.16, 95% CI (6.55, 7.16)] than current life satisfaction [M = 5.35, SE = 0.13, 95% CI (5.10, 5.61)]. An interaction between Indebtedness Status and Time of life satisfaction, F(1, 216) = 35.35, p < 0.001, ηp2 = 0.14, indicating that although non-over-indebted consumers reported an increase from current [M = 6.77, SE = 0.19, 95% CI (6.40, 7.14)] to predicted future life satisfaction [M = 7.28, SE = 0.22, 95% CI (6.81, 7.72)], F(1, 216) = 5.43, p = 0.021, ηp2 = 0.02, for their over-indebted counterparts, this increase between current [M = 3.94, SE = 0.20, 95% CI (3.55, 4.33)] and predicted future life satisfaction [M = 6.43, SE = 0.24, 95% CI (5.96, 6.89)] was considerably steeper, F(1, 218) = 115.69, p < 001, ηp2 = 0.35.

Figure 1. Mean evaluations of current and future life satisfaction (with SEs) in over-indebted and non-over-indebted groups.

As expected, over-indebted consumers clearly presented overall lower levels of life satisfaction (i.e., across current and predicted future measures of life satisfaction) compared to non-over-indebted consumers. The current life satisfaction of over-indebted consumers is particularly low (below the midpoint of Cantril’s ladder). Interestingly, the reported interaction between current vs. predicted future life satisfaction and over-indebted vs. non-over-indebted consumers suggests that regardless of their difficult financial conditions, over-indebted consumers appear to believe in a better (financial) future as they anticipate a steeper increase in their predicted future life satisfaction.

Emotional Well-Being

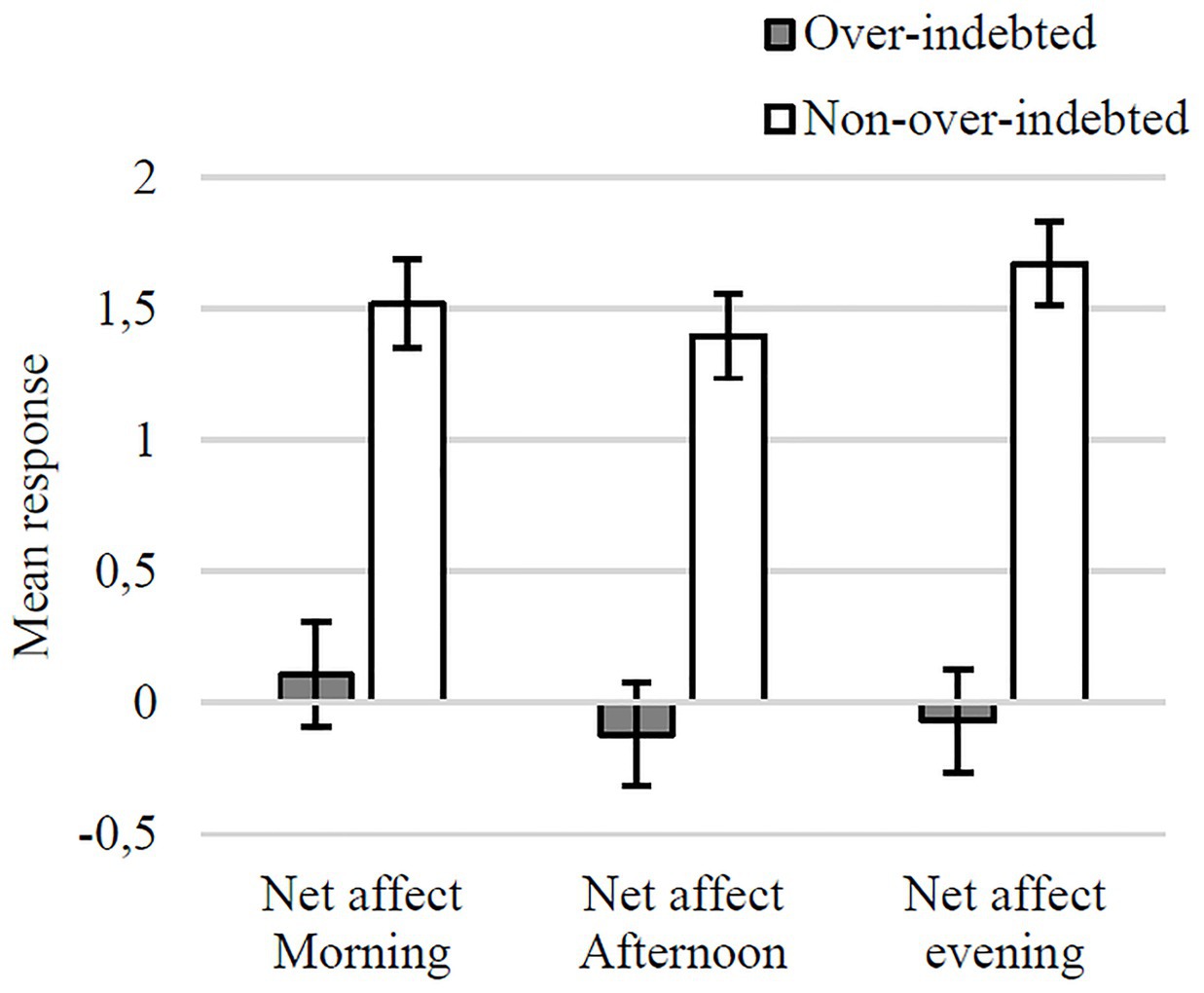

Using the valid data from 209 participants (96 over-indebted and 113 non-over-indebted), a repeated measures ANCOVA was conducted with Time of the day (morning, afternoon, and evening) as a within-participants factor, Indebtedness Status (over-indebted, non-over-indebted) as a between-participants factor, and the propensity score as a covariate. The dependent variable was the net affect (composed of the subtraction of the mean negative emotions from the mean positive ones).

The ANCOVA yielded one main effect of Indebtedness Status, F(1, 206) = 29.91, p < 0.001, ηp2 = 0.13, such that over-indebted consumers reported lower emotional well-being [M = −0.29, SE = 0.134 95% CI (−0.95, 0.37)] than their non-over-indebted counterparts [M = 1.15, SE = 0.43, 95% CI (0.30, 2.00)]. The interaction between indebtedness status and net affect suggests that the net affect of over-indebted consumers tended to deteriorate from morning to evening, while the net affect for non-over-indebted consumers tended to improve. However, this interaction did not reach statistical significance F(2, 412) = 2.39, p = 0.093, ηp2 = 0.01 (Figure 2).

Figure 2. Mean evaluations of net affect on the previous day (with SEs) in over-indebted and non-over-indebted groups.

As expected, emotional well-being (operationalized in terms of net affect), was lower for over-indebted consumers compared to non-over-indebted consumers. Furthermore, over-indebted consumers experienced more negative emotions (relative to positive emotions) than non-over-indebted consumers, and this difference tends to become more pronounced from morning to evening.

Sleep

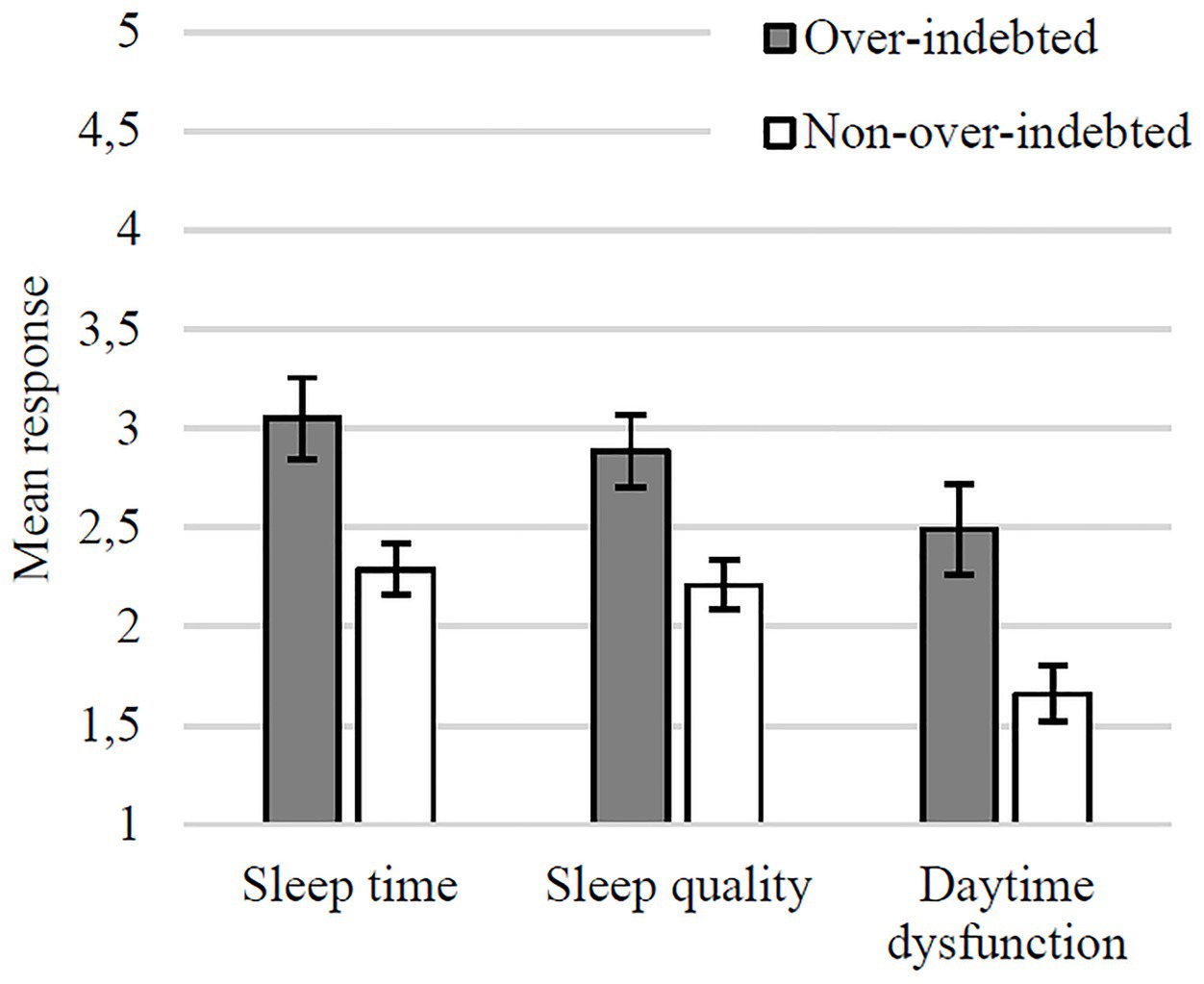

Using the valid data from 211 participants (100 over-indebted and 111 non-over-indebted), a repeated measures ANCOVA was conducted with Indebtedness Status (over-indebted, non-over-indebted) as a between-participants factor, Sleep (sleep time, sleep quality, and daytime dysfunction) as a within-participants factor, and with the propensity score as a covariate.

The ANCOVA yielded a main effect of Indebtedness Status, F(1, 208) = 54.60, p < 0.001, ηp2 = 0.21, indicating that over-indebted consumers report worse sleep overall [M = 2.87, SE = 0.13, 95% CI (2.61, 3.11)] than non-over-indebted consumers [M = 2.13, SE = 0.16, 95% CI (1.81, 2.45)]. There was also a main effect of Sleep, F(2, 416) = 6.15, p = 0.002, ηp2 = 0.03 [MSleep Time(ST) = 2.73, SEST = 0.14, 95% CI (2.45, 3.01), MSleep Quality(SQ) = 2.61, SESQ = 0.14, 95% CI (2.33, 2.89), and MDaytime Dysfunction(DD) = 2.14, SEDD = 0.14, 95% CI (1.86, 2.42)], suggesting lower levels of day time dysfunction compared to the sleep time and sleep quality components (Figure 3).

Figure 3. Mean evaluations of sleep time and quality and daytime dysfunction (with SEs) in over-indebted and non-over-indebted groups.

In short, over-indebtedness appears to have substantial negative effects on different aspects of sleep. Over-indebted consumers sleep less and worse than non-over-indebted consumers and have poorer daytime functioning.

Reported Health

Using the valid data from 226 participants (110 over-indebted and 116 non-over-indebted), a one-way ANCOVA was conducted with Indebtedness Status (over-indebted, non-over-indebted) as a between-participants variable and with the propensity score as covariate. The dependent variable was participants reported health.

The ANCOVA yielded a main effect of Indebtedness Status, F(1, 223) = 34.32, p < 0.001, ηp2 = 0.13, such that over-indebted consumers reported poorer health [M = 3.00, SE = 0.08, 95% CI (2.85, 3.16)] than their non-over-indebted counterparts [M = 2.33, SE = 0.08, 95% CI (2.18, 2.48)].

Over-indebted consumers’ reported health was close to the rating scale point “fair” and significantly worse than non-over-indebted consumers’ health (which was closer to the point “good”).

Mediation Analysis

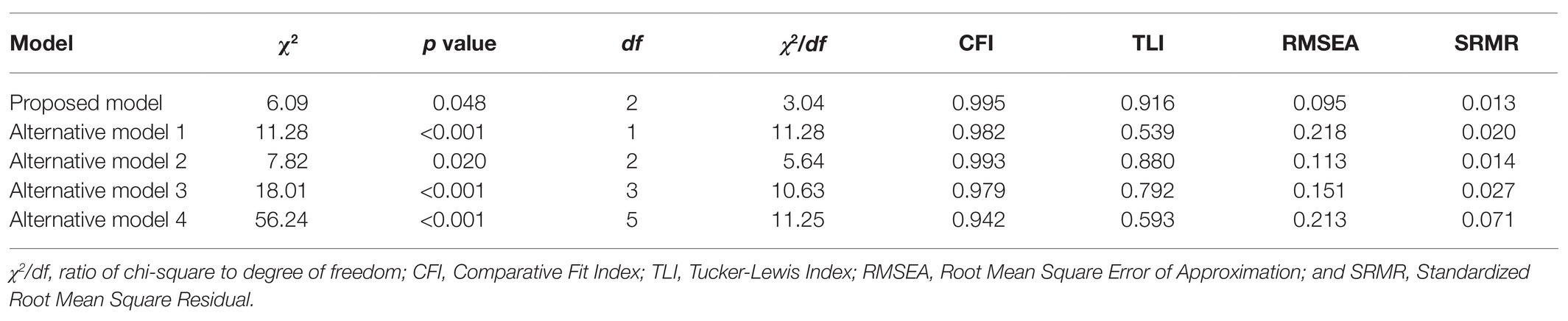

In this section, the results of the mediation analysis between indebtedness status (over-indebted and non-over-indebted) and the dependent variables, such as life satisfaction (current), global score of emotional well-being (aggregating for the morning, afternoon, and evening), and health and sleep (aggregating sleep time, sleep quality, and daytime dysfunction) are presented. We controlled for education, income, marital status, and employment status, via the propensity score created. Perceived control, financial anxiety, and financial well-being were included as possible mediators. The following analyses were performed using MPlus 7.2 (Muthén and Muthén, 1998–2012). Based on theoretical assumptions, significant correlations among mediators and among criterion variables were included in the model. To test the mediation hypotheses, bootstrap estimation was used with 5,000 subsamples to derive the 95% CI for the indirect effects (Preacher and Selig, 2012). The following fit indexes and criteria were used as indicative of a good model fit: the comparative fit index (CFI) and the Tucker-Lewis Index (TLI) higher than 0.95, the root mean square error of approximation (RMSEA) and standardized root mean residual (SRMR) lower than 0.08 (Hu and Bentler, 1999; Kline, 2011).

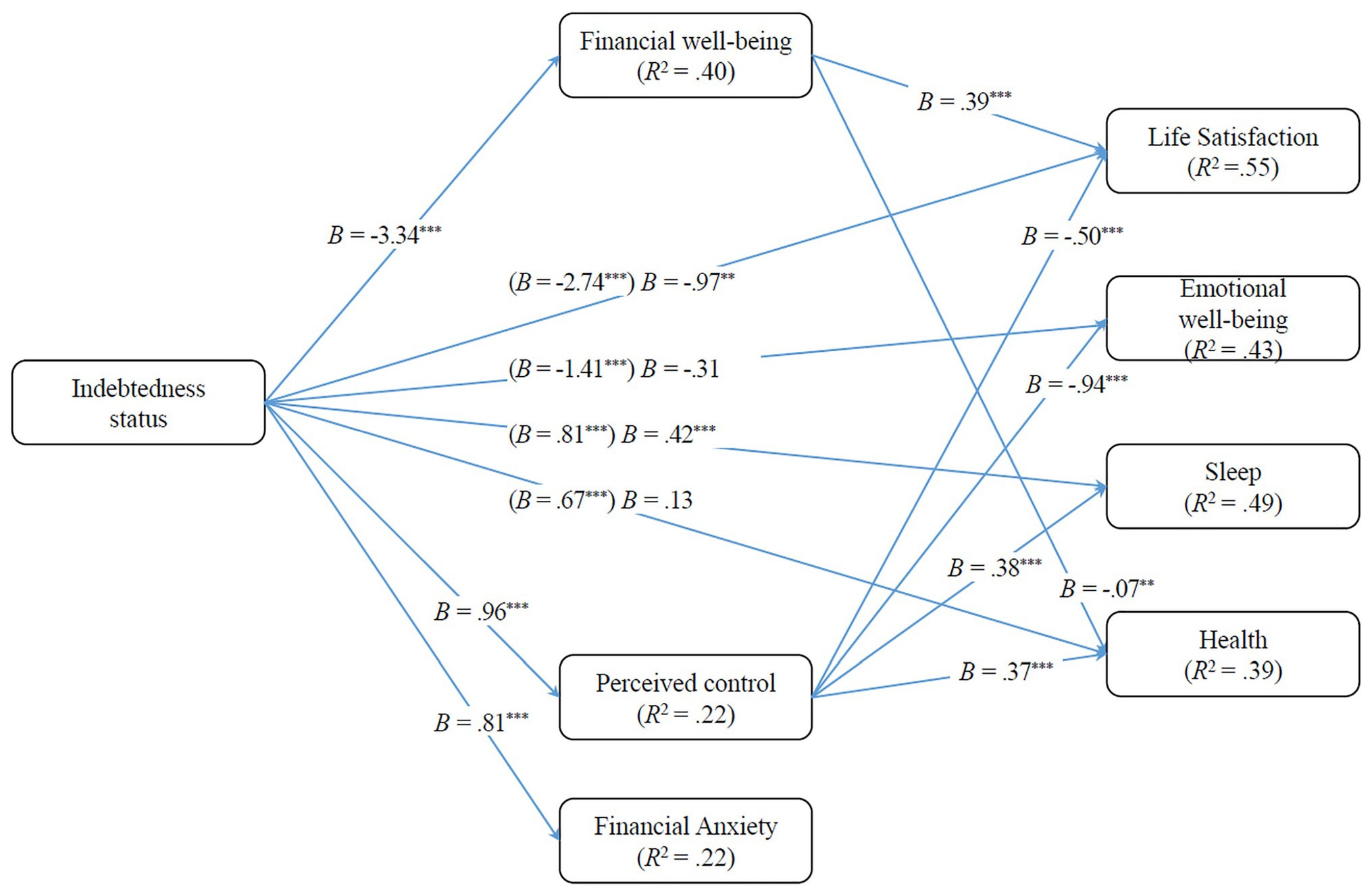

The multi-mediator path analysis model examining the indirect effects of indebtedness on life satisfaction, emotional well-being, health, and sleep, through perceived control, financial anxiety, and financial well-being, controlling for level of education, income, marital status, and employment status (through the propensity score) presented a good fit to the data: χ2(2) = 6.09, p = 0.048; CFI = 0.995; RMSEA = 0.095, 90% CI: (0.008, 0.185); SRMR = 0.013. The RMSEA index is slightly above the cutoff value of 0.08, but still under the 0.10 cutoff value for acceptable fit (Chen et al., 2008). Mode results are depicted in Figure 4.

Figure 4. Mediation model for the effect of indebtedness status on life satisfaction, emotional well-being, sleep, and health via perceived control, financial well-being, and financial anxiety.

Results revealed significant indirect effects of indebtedness on: (1) life satisfaction, through financial well-being, B = −1.30, SE = 0.30, p < 0.001, 95% CI: (−1.90, −0.76) and perceived control, B = −0.48, SE = 0.16, p = 0.002, 95% CI: (−1.61, −0.24); (2) emotional well-being, through perceived control, B = −0.91, SE = 0.17, p < 0.001, 95% CI: (−1.27, −0.60); (3) sleep quality, also through perceived control, B = 0.36, SE = 0.07, p < 0.001, 95% CI: (0.24, 0.49); and (4) reported health, through financial well-being, B = 0.22, SE = 0.08, p = 0.010, 95% CI: (0.05, 0.38) and perceived control, B = 0.36, SE = 0.08, p < 0.001, 95% CI: (0.21, 0.53).

More specifically, over-indebtedness was associated with: (1) lower levels of perceived control, which in turn predicted lower levels of life satisfaction, emotional well-being, sleep quality, and reported health; and (2) lower levels of financial well-being, which in turn predicted lower levels of life satisfaction and reported health. Although higher levels of financial anxiety were also predicted by over-indebtedness, financial anxiety did not emerge as a significant mediator in the model.

As shown in Figure 4, both total and direct effects of indebtedness on life satisfaction and sleep quality were significant, although the direct effects were lower than the total effect. In contrast, the direct effect of indebtedness on emotional well-being and on reported health was not significant. Thus, perceived control and financial well-being partially mediated the association between indebtedness status and life satisfaction, and fully mediated the association between indebtedness status and reported health. Finally, perceived control also fully mediated the association between indebtedness status and emotional well-being and partially mediated the association between indebtedness status and sleep quality. The propensity score did not predict any of the mediating or criterion variables.

Given the cross-sectional nature of the data, we tested four alternative models to exclude the possibility of other plausible pathways: (1) a model that was the “reverse” of our hypothesized model, examining the proposed criterion variables (i.e., life satisfaction, emotional well-being, sleep, and health) as predictors of indebtedness status, via the proposed mediators (i.e., perceived control, financial anxiety, and financial well-being; Alternative model 1); (2) a model examining indebtedness status as predictor, the proposed criterion variables as mediators, and the proposed mediators as criterion variables (Alternative model 2); and (3) a model examining the proposed mediators as predictors of the proposed criterion variables, via indebtedness status (Alternative model 3); and (4) a model examining perceived control as predictor of the proposed criterion variables, via indebtedness status, financial well-being, and financial anxiety (Alternative model 4). We then compared the fit of all models against one another to see which best fit the data. As shown in Table 2, the comparison of the fit indices of all models showed that the hypothesized model fit the data better than all four alternative models. In the next section, we thus focus on this model when discussing the mediational analysis results.

Table 2. Model fit comparison between the proposed model and the alternative models.

Discussion

This paper sought to assess and further explore the association of over-indebtedness to SWB, examining two of its components – life satisfaction and emotional well-being. This is an important issue for several reasons. First, although recent research has confirmed the negative outcomes of over-indebtedness in terms of mental and physical health (e.g., Emami, 2010; Gathergood, 2012; Angel, 2016), there is less research on the impact of debt on SWB. Second, although meta-analysis of Tay et al. (2017) found a negative association between debt and well-being, they did not distinguish between the two facets of well-being here considered. Furthermore, some prior research on well-being suggested that individuals rapidly adapt to life changing events and that most life circumstances have little influence on measures of SWB (Easterlin, 1995; Kahneman et al., 2004). Thus, the extent to which deteriorated life circumstances associated with over-indebtedness lead to decreased life satisfaction and/or emotional well-being is still an important research issue.

In our study, over-indebtedness was associated with lower life satisfaction, adding to the findings of Tay et al. (2017), but also with lower emotional well-being, a crucial component of SWB which has received less attention. Furthermore, the over-indebted consumers in our study were, for the most part, medium to long-term cases of over-indebtedness, who requested the assistance of a consumer defense NGO (DECO) following a lengthy period of financial hardship, and often as a last resort. This suggests that, in contrast with other life changing circumstances, the detrimental effects of over-indebtedness on life satisfaction and emotional well-being do not fade away, as proposed by the hedonic treadmill hypothesis (Brickman and Campbell, 1971). These results are in line with other findings that point to circumstantial changes that have more than just transitory effects. Among these changes are, for example, the effects of unemployment (often a main cause of indebtedness) and chronic pain (Lucas et al., 2004).

Our study further considered three potential mediators of the relationship between indebtedness status and the two facets of SWB: perceived control, financial anxiety, and financial well-being. The relationship between indebtedness status and life satisfaction was partly mediated by perceived control and financial well-being, that is, over-indebted consumers’ lower levels of perceived control and financial well-being partly explained their lower life satisfaction when compared to non-over-indebted consumers. As for emotional well-being, perceived control over one’s life fully explained the relationship between over-indebtedness and emotional well-being.

The partial mediation of financial well-being of the relationship between indebtedness and life satisfaction is in line with previous research (Diener et al., 1999; Kahneman, 1999; Tay et al., 2017) and provides some support for the first explanatory mechanism presented in the introduction, according to which life satisfaction is influenced by smaller life domains, one of them being financial well-being. Moreover, finding that financial well-being matters for life satisfaction but not for emotional well-being reaffirms the importance of considering separate measures of these two facets of well-being by confirming that they are different constructs with distinct determinants and consequences (Kahneman and Krueger, 2006).

The second explanation advanced in the introduction argues that a lack of financial resources limits the extent to which consumers may attain their goals, calling into question autonomy and self-control, which are crucial for well-being. The current results provide some support for this account by showing that over-indebtedness reduces consumers’ perceived self-control over their own lives. Reduced self-control then lowers both life satisfaction and emotional well-being.

This study also investigated whether indebtedness status predicted health and sleep quality. Confirming previous findings (e.g., Summers and Gutierrez, 2018), over-indebted consumers reported poorer overall health, worse sleep, and more sleep-related disturbances. These are important risk factors to consider. Self-ratings of health, for instance, have been found to be a strong predictor of mortality over the years (Mossey and Shapiro, 1982; Idler and Benyamini, 1997).

The mediating role of the same three variables (perceived control, financial anxiety, and financial well-being) on the impact of over-indebtedness on health and sleep were also explored. Perceived control and financial well-being emerged as the only significant mediators, with both fully mediating the relationship between indebtedness status and health, and perceived control partially mediating the relationship between indebtedness status and sleep quality.

It is noteworthy that perceived control emerged as a consistent mediator of the relationship between over-indebtedness and all dependent variables (life satisfaction, emotional well-being, health, and sleep). In other words, a lack of control over one’s life not only contributes to fully explaining the relationship between over-indebtedness and emotional well-being, but also partially explained the relationship between indebtedness status and life satisfaction. Furthermore, perceived control was also found to partially explain sleep quality and to fully explain reported overall health. These results are in line with recent findings by Białowolski et al. (2021), which show that financial control has a substantial impact on well-being (which is greater than being in a financially fragile situation). The authors found that financial control has a protective role on well-being through the promotion of (positive) emotional well-being outcomes and a protective one against emotional ill-being outcomes, which in turn translates into improved physical health and sleep.

Perceived control is a central motivator of individuals’ decision-making and behavior (e.g., Miller, 1979; Leotti et al., 2010; Higgins, 2012). It has been defined as “the belief that one can determine one’s own internal states and behavior, influence one’s environment, and/or bring about desired outcomes” (Wallston et al., 1987, p. 5). Individuals are highly motivated to believe they have control over their lives (e.g., Kelly, 1955; Burger and Cooper, 1979; Rothbaum et al., 1982) and to re-establish it in various ways. Thus, interventions aimed at promoting over-indebted consumers’ perceived control may be of relevance to improve their SWB.

Helzer and Jayawickreme (2015) explored the relationship between primary and secondary control strategies and the same two facets of well-being assessed in the present work. They defined primary control as the tendency to achieve mastery over circumstances via goal striving, and secondary control as the tendency to achieve mastery over circumstances via sense-making. Their findings indicated that primary control was more consistently associated with emotional well-being, whereas secondary control was associated with life satisfaction.

Taken together, the present findings and Helzer and Jayawickreme (2015) results suggest that the different strategies over-indebted consumers may use to re-establish control over their lives will differentially affect well-being. Thus, guidelines for interventions and the provision of support for over-indebted consumers should focus not only on primary control strategies, via measures that facilitate consumers’ efforts to recover from their severe financial difficulties (e.g., renegotiation of debt payment conditions), but also on secondary control strategies. In the latter case, this would involve helping over-indebted consumers to make sense of their challenging and complex social and financial situation (e.g., facing social discrimination, changing consumer habits) in order to better deal with it. This is particularly relevant for the cases in which increasing primary control might not be immediately feasible.

Finally, identifying over-indebtedness as a long-lasting threat to one’s SWB should be taken as a cautionary note for policymakers and practitioners alike. We suggest that the assessment of policies to fight over-indebtedness and empower consumers could include measures of life-satisfaction and emotional well-being. In other words, Government and NGO’s educational programs of financial guidance (e.g., financial literacy and financial decision-making courses) as well as specific legislation to protect and empower over-indebted consumers could include the improvement of consumers’ SWB among their standard goals.

Limitations

Although our results unveil the stark consequences that over-indebtedness brings to one’s life, this study has several limitations that need to be considered.

First, a cross-sectional design was used, which prevents us from drawing strong conclusions that the individual differences in SWB (sleep quality and health) are due to over-indebtedness status. Nevertheless, the comparison of the proposed model with the alternative ones supported the hypothesized direction of effects over the other possible causal directions. Despite this, it is always possible that other variables (besides those we controlled for) also have predictive value over SWB.

Second, our measure of financial well-being was composed of a single item. Although single item measures have been used before (e.g., Johnson and Krueger, 2006; Switek, 2013), they fail to capture the multi-dimensional nature of financial well-being (Iannello et al., 2020). Future research should thus rely on multiple-item instruments that account for the different dimensions (cognitive, behavioral, materialistic, and relational) of financial well-being (e.g., Sorgente and Lanz, 2019; Iannello et al., 2020).

Third, our procedure classified all cases of over-indebted participants under the same conceptual umbrella, which is likely to be an oversimplification. In other words, not all over-indebted households should be considered equal (Ferreira et al., 2020). The diversity of risk factors of over-indebtedness strongly suggests that there are different over-indebted profiles associated to distinguishable causes (e.g., work loss, disease, low financial literacy, poor decision-making, and financial imprudence). A more fine-grained analysis of the impact of over-indebtedness on well-being should thus distinguish among these causes.

Fourth, although the present research acknowledged the multifaceted nature of well-being by measuring both life satisfaction and emotional well-being, a multidimensional perspective of well-being (Keyes et al., 2002; Iannello et al., 2020) further considers the concept of psychological well-being, which entails the perception of engagement with existential life challenges (Keyes et al., 2002) and is often assessed through the concept of flourishing (Diener et al., 2010). Hence, in order to better evaluate the impact of over-indebtedness on the multiple dimensions of well-being, future research should also include operationalizations of psychological well-being (Ryff and Keyes, 1995).

Future research should ideally replicate these findings using better and more comprehensive measures of well-being and using new matched samples of over-indebted and non-over-indebted households. Furthermore, longitudinal designs with at least two waves of data collection are crucial to clarify causal links and more clearly disentangle alternative mediating directions.

Conclusion

In sum, the reported findings (and their limitations) should not be evaluated in isolation but rather as another research effort, contributing to a literature concerning the effects of debt on consumers’ well-being. Our results are well-aligned with prior research on the psychological and physical implications of over-indebtedness (replicating several previous findings) and provide some new insights in terms of the underlying mechanisms that link indebtedness to well-being. Moreover, to our knowledge, these are among the first findings specifically focusing on over-indebtedness and different facets of well-being (but see also Angel, 2016; Białowolski et al., 2019) and the first within the Portuguese context. Hopefully, they will contribute to set the stage for further research on these mechanisms and their boundary conditions.

Data Availability Statement

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

Ethics Statement

The studies involving human participants were reviewed and approved by Ethics committee of the Faculty of Psychology, University of Lisbon. The participants provided their written informed consent to participate in this study.

Author Contributions

MF, FA, and JS contributed equally to the conceptualization, data collection and analysis, manuscript writing, and thus sharing first co-authorship. DP, MH, and CS provided the indispensable analysis and inputs on results and discussion. All authors contributed to the article and approved the submitted version.

Funding

This research was supported by grants from the Foundation for Science and Technology attributed to MF (PTDC/MHCPAP/1556/2014) and to MF and DP (DSAIPA/DS/0113/2019).

Conflict of Interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

References

Adachi, M., Staisiunas, P. G., Knutson, K. L., Beveridge, C., Meltzer, D. O., and Arora, V. M. (2013). Perceived control and sleep in hospitalized older adults: a sound hypothesis? J. Hosp. Med. 8, 184–190. doi: 10.1002/jhm.2027

Anderloni, L., and Vandone, D. (2010). The profitability of the consumer credit industry: evidence from Europe. SSRN Elec. J. doi: 10.2139/ssrn.1653517

Angel, S. (2016). The effect of over-indebtedness on health: comparative analyses for Europe. Kyklos 69, 208–227. doi: 10.1111/kykl.12109

Attanasio, O. P. (1995). “The intertemporal allocation of consumption: theory and evidence” in Carnegie-Rochester conference series on public policy, Vol. 42. North-Holland, 39–89.

Barba, A., and Pivetti, M. (2009). Rising household debt: its causes and macroeconomic implications—a long-period analysis. Camb. J. Econ. 33, 113–137. doi: 10.1093/cje/ben030

Berthoud, R., and Kempson, E. (1992). Credit and debt: The PSI report (No. 728). Policy Studies Institute.

Betti, G., Dourmashkin, N., Rossi, M., and Yin, Y. P. (2007). Consumer over-indebtedness in the EU: measurement and characteristics. J. Econ. Stud. 34, 136–156. doi: 10.1108/01443580710745371

Białowolski, P. (2019). Patterns and evolution of consumer debt: evidence from latent transition models. Qual. Quant. 53, 389–415. doi: 10.1007/s11135-018-0759-9

Białowolski, P., Węziak-Białowolska, D., and McNeely, E. (2021). The role of financial fragility and financial control for well-being. Soc. Indic. Res. 15, 1–21. doi: 10.1007/s11205-021-02627-5

Białowolski, P., Węziak-Białowolska, D., and VanderWeele, T. J. (2019). The impact of savings and credit on health and health behaviours: an outcome-wide longitudinal approach. Int. J. Public Health 64, 573–584. doi: 10.1007/s00038-019-01214-3

BIS–Department for Business, Innovation and Skill (2010). Over-indebtedness in Britain: Second follow-up report.

Blomgren, J., Maunula, N., and Hiilamo, H. (2016). Over-indebtedness and chronic disease: a linked register-based study of Finnish men and women during 1995–2010. Int. J. Public Health 61, 535–544. doi: 10.1007/s00038-015-0778-4

Bobak, M., Pikhart, H., Hertzman, C., Rose, R., and Marmot, M. (1998). Socioeconomic factors, perceived control and self-reported health in Russia. A cross-sectional survey. Soc. Sci. Med. 47, 269–279. doi: 10.1016/S0277-9536(98)00095-1

Bosma, H., Schrijvers, C., and Mackenbach, J. P. (1999). Socioeconomic inequalities in mortality and importance of perceived control: cohort study. BMJ 319, 1469–1470. doi: 10.1136/bmj.319.7223.1469

Brickman, P., and Campbell, D. T. (1971). “Hedonic relativism and planning the good society” in Adaptation-level theory. ed. M. H. Appley (New York: Academic Press), 287–305.

Bridges, S., and Disney, R. (2004). Use of credit and arrears on debt among low-income families in the United Kingdom. Fisc. Stud. 25, 1–25. doi: 10.1111/j.1475-5890.2004.tb00094.x

Bridges, S., and Disney, R. (2010). Debt and depression. J. Health Econ. 29, 388–403. doi: 10.1016/j.jhealeco.2010.02.003

Burger, J. M., and Cooper, H. M. (1979). The desirability of control. Motiv. Emot. 3, 381–393. doi: 10.1007/BF00994052

Buxton, O. M., and Marcelli, E. (2010). Short and long sleep are positively associated with obesity, diabetes, hypertension, and cardiovascular disease among adults in the United States. Soc. Sci. Med. 71, 1027–1036. doi: 10.1016/j.socscimed.2010.05.041

Buysse, D. J., Reynolds, C. F., Monk, T. H., Berman, S. R., and Kupfer, D. J. (1989). The Pittsburgh sleep quality index: a new instrument for psychiatric practice and research. Psychiatry Res. 28, 193–213. doi: 10.1016/0165-1781(89)90047-4

Cantril, H. (1965). The pattern of human concerns. New Brunswick, NJ: Rutgers University Press, 1965.

Cappuccio, F. P., D’Elia, L., Strazzullo, P., and Miller, M. A. (2010). Sleep duration and all-cause mortality: a systematic review and meta-analysis of prospective studies. Sleep 33, 585–592. doi: 10.1093/sleep/33.5.585

Chen, F., Curran, P. J., Bollen, K. A., Kirby, J., and Paxton, P. (2008). An empirical evaluation of the use of fixed cutoff points in RMSEA test statistic in structural equation models. Sociol. Methods Res. 36, 462–494. doi: 10.1177/0049124108314720

Chmelar, A., (2013). Household debt and the European crisis (Report n° 13). Brussels: Centre for European Policy Studies. Available at: https://www.ceps.eu/wp-content/uploads/2013/07/Household%20Debt%20and%20the%20European%20Crisis.pdf (Accessed March 29, 2021).

Clayton, M., Liñares-Zegarra, J., and Wilson, J. O. (2015). Does debt affect health? Cross country evidence on the debt-health nexus. Soc. Sci. Med. 130, 51–58. doi: 10.1016/j.socscimed.2015.02.002

Cohen, S., Kamarck, T., and Mermelstein, R. (1983). A global measure of perceived stress. J. Health Soc. Behav. 24, 386–396. doi: 10.2307/2136404

Crook, J. (2003). The Demand and Supply for Household Debt: A Cross Country Comparison, Credit Research Centre (No. 03/01). University of Edinburgh Working Paper Series.

D’Alessio, G., and Iezzi, S. (2013). Household over-indebtedness: definition and measurement with Italian data. Questioni di Economia e Finanza (Occasional Paper) 149, 1–26. doi: 10.2139/ssrn.2243578

Diener, E., and Biswas-Diener, R. (2002). Will money increase subjective well-being? Soc. Indic. Res. 57, 119–169. doi: 10.1023/A:1014411319119

Diener, E., Suh, E. M., Lucas, R. E., and Smith, H. L. (1999). Subjective well-being: three decades of progress. Psychol. Bull. 125, 276–302. doi: 10.1037/0033-2909.125.2.276

Diener, E., Wirtz, D., Tov, W., Kim-Prieto, C., Choi, D., Oishi, S., et al. (2010). New measures of well-being: flourishing and positive and negative feelings. Soc. Indic. Res. 39, 247–266. doi: 10.1007/s11205-009-9493-y

Disney, R., Bridges, S., and Gathergood, J. (2008). Drivers of Over-indebtedness. Report to the UK Department for Business. Available at: https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.514.9586&rep=rep1&type=pdf (Accessed March 29, 2021).

Dolan, P., Kudrna, L., and Stone, A. (2017). The measure matters: an investigation of evaluative and experience-based measures of well-being in time use data. Soc. Indic. Res. 134, 57–73. doi: 10.1007/s11205-016-1429-8

Drentea, P., and Lavrakas, P. J. (2000). Over the limit: the association among health, race and debt. Soc. Sci. Med. 50, 517–529. doi: 10.1016/S0277-9536(99)00298-1

Drentea, P., and Reynolds, J. R. (2012). Neither a borrower nor a lender be: the relative importance of debt and SES for mental health among older adults. J. Aging Health 24, 673–695. doi: 10.1177/0898264311431304

Easterlin, R. A. (1995). Will raising the incomes of all increase the happiness of all? J. Econ. Behav. Organ. 27, 35–47. doi: 10.1016/0167-2681(95)00003-B

Emami, S. (2010). Consumer overindebtedness and health care costs: how to approach the question from a global perspective. World Health Report (2010) Background paper, 3. World Health Organization, Geneva. Available at: http://www.who.int/healthsystems/topics/financing/healthreport/3BackgroundPaperMedBankruptcy.pdf (Accessed March 29, 2021).

European Commission (2008). Towards a common operational European definition of over-indebtedness. European Commission. Brussels. Available at: http://www.oee.fr/files/study_overindebtedness_en.pdf (Accessed March 29, 2021).

Ferreira, M. B., Pinto, D. C., Herter, M. M., Soro, J., Vanneschi, L., Castelli, M., et al. (2020). Using artificial intelligence to overcome over-indebtedness and fight poverty. J. Bus. Res. doi: 10.1016/j.jbusres.2020.10.035 (in press).

Gallicchio, L., and Kalesan, B. (2009). Sleep duration and mortality: a systematic review and meta-analysis. J. Sleep Res. 18, 148–158. doi: 10.1111/j.1365-2869.2008.00732.x

Gangwisch, J. E., Heymsfield, S. B., Boden-Albala, B., Buijs, R. M., Kreier, F., Pickering, T. G., et al. (2006). Short sleep duration as a risk factor for hypertension: analyses of the first National Health and nutrition examination survey. Hypertension 47, 833–839. doi: 10.1161/01.HYP.0000217362.34748.e0

Gathergood, J. (2012). Self-control, financial literacy and consumer over-indebtedness. J. Econ. Psychol. 33, 590–602. doi: 10.1016/j.joep.2011.11.006

Gerstorf, D., Röcke, C., and Lachman, M. E. (2011). Antecedent–consequent relations of perceived control to health and social support: longitudinal evidence for between-domain associations across adulthood. J. Gerontol. B Psychol. Sci. Soc. Sci. 66, 61–71. doi: 10.1093/geronb/gbq077

Gould, C. E., Beaudreau, S. A., O’Hara, R., and Edelstein, B. A. (2016). Perceived anxiety control is associated with sleep disturbance in young and older adults. Aging Ment. Health 20, 856–860. doi: 10.1080/13607863.2015.1043617

Grandner, M. A., Chakravorty, S., Perlis, M. L., Oliver, L., and Gurubhagavatula, I. (2014). Habitual sleep duration associated with self-reported and objectively determined cardiometabolic risk factors. Sleep Med. 15, 42–50. doi: 10.1016/j.sleep.2013.09.012

Grandner, M. A., Hale, L., Moore, M., and Patel, N. P. (2010). Mortality associated with short sleep duration: the evidence, the possible mechanisms, and the future. Sleep Med. Rev. 14, 191–203. doi: 10.1016/j.smrv.2009.07.006

Grandner, M. A., and Patel, N. P. (2009). From sleep duration to mortality: implications of meta-analysis and future directions. J. Sleep Res. 18, 145–147. doi: 10.1111/j.1365-2869.2009.00753.x

Guiso, L., and Sodini, P. (2013). “Household finance: an emerging field” in Handbook of the economics of finance. Vol. 2, eds. G. M. Constantinides, M. Harris, and R. M. Stulz (Amsterdam: Elsevier), 1397–1532.

Hall, R. E. (1978). Stochastic implications of the life cycle-permanent income hypothesis: theory and evidence. J. Polit. Econ. 86, 971–987. doi: 10.1086/260724

Hansen, T., Slagsvold, B., and Moum, T. (2008). Financial satisfaction in old age: a satisfaction paradox or a result of accumulated wealth? Soc. Indic. Res. 89, 323–347. doi: 10.1007/s11205-007-9234-z

Harvey, D. (2011). “The enigma of capital and the crisis this time” in Business as usual: The roots of the global financial meltdown. eds. C. Calhoun and G. Derluguian (NY: NYU Press), 89–112.

Helzer, E. G., and Jayawickreme, E. (2015). Control and the “good life” primary and secondary control as distinct indicators of well-being. Soc. Psychol. Personal. Sci. 6, 653–660. doi: 10.1177/1948550615576210

Hintikka, J., Viinamäki, H., Tanskanen, A., Kontula, O., and Koskela, K. (1998). Suicidal ideation and parasuicide in the Finnish general population. Acta Psychiatr. Scand. 98, 23–27. doi: 10.1111/j.1600-0447.1998.tb10037.x

Hogan, E., Bryant, S., and Overymyer-Day, L. (2013). Relationships between college students’ credit card debt, undesirable academic behaviors and cognitions, and academic performance. Coll. Stud. J. 47, 102–112.

Howell, R. T., and Howell, C. J. (2008). The relation of economic status to subjective well-being in developing countries: a meta-analysis. Psychol. Bull. 134, 536–560. doi: 10.1037/0033-2909.134.4.536

Hsieh, C. M. (2001). Correlates of financial satisfaction. Int. J. Aging Hum. Dev. 52, 135–153. doi: 10.2190/9YDE-46PA-MV9C-2JRB

Hu, L. T., and Bentler, P. M. (1999). Cutoff criteria for fit indexes in covariance structure analysis: conventional criteria versus new alternatives. Struct. Equ. Model. 6, 1–55. doi: 10.1080/10705519909540118

Iannello, P., Sorgente, A., Lanz, M., and Antonietti, A. (2020). Financial well-being and its relationship with subjective and psychological well-being among emerging adults: testing the moderating effect of individual differences. J. Happiness Stud. 22, 1–27. doi: 10.1007/s10902-020-00277-x

Idler, E. L., and Benyamini, Y. (1997). Self-rated health and mortality: a review of twenty-seven community studies. J. Health Soc. Behav. 38, 21–37.

Johnson, W., and Krueger, R. F. (2006). How money buys happiness: genetic and environmental processes linking finances and life satisfaction. J. Pers. Soc. Psychol. 90:680. doi: 10.1037/0022-3514.90.4.680

Kahneman, D. (1999). “Objective happiness” in Well-being: The foundations of hedonic psychology. eds. D. Kahneman, E. Diener, and N. Schwarz (Russell Sage Foundation), 3–25.

Kahneman, D., and Deaton, A. (2010). High income improves evaluation of life but not emotional well-being. Proc. Natl. Acad. Sci. U. S. A. 107, 16489–16493. doi: 10.1073/pnas.1011492107

Kahneman, D., and Krueger, A. B. (2006). Developments in the measurement of subjective well-being. J. Econ. Perspect. 20, 3–24. doi: 10.1257/089533006776526030

Kahneman, D., Krueger, A. B., Schkade, D. A., Schwarz, N., and Stone, A. A. (2004). A survey method for characterizing daily life experience: the day reconstruction method. Science 306, 1776–1780. doi: 10.1126/science.1103572

Kahneman, D., and Riis, J. (2005). “Living, and thinking about it: two perspectives on life” in The science of well-being. eds. F. A. Huppert, N. Baylis, and B. Keverne (New York: Oxford University Press), 285–304.

Keese, M. (2009). Triggers and determinants of severe household indebtedness in Germany. Ruhr Economic Paper, (150). Available at: http://repec.rwi-essen.de/files/REP_09_150.pdf (Accessed March 29, 2021).

Keller, A., Litzelman, K., Wisk, L. E., Maddox, T., Cheng, E. R., Creswell, P. D., et al. (2012). Does the perception that stress affects health matter? The association with health and mortality. Health Psychol. 31, 677–684. doi: 10.1037/a0026743

Kelly, E. L. (1955). Consistency of the adult personality. Am. Psychol. 10, 659–681. doi: 10.1037/h0040747

Kempson, E. (2015). “Over-indebtedness and its causes across European countries” in Consumer debt and social exclusion in Europe. eds. H. W. Micklitz and I. Domurath (London: Routledge), 137–153.

Kempson, E., McKay, S., and Willitts, M. (2004). Characteristics of families in debt and the nature of indebtedness (No. 211). Leeds: Corporate Document Services. Available at: http://www.pfrc.bris.ac.uk/Reports/Characteristics.pdf (Accessed March 29, 2021).

Keyes, C. L., Shmotkin, D., and Ryff, C. D. (2002). Optimizing well-being: the empirical encounter of two traditions. J. Pers. Soc. Psychol. 82:1007. doi: 10.1037/0022-3514.82.6.1007

Kline, R. (2011). Principles and practice of structural equation modelling. 3rd Edn. New York, NY: Guilford Press.

Kostelecky, K. (1994). A family resource management approach to satisfaction with personal life and financial situation in retirement. Unpublished. Master of Science, Iowa State University.

Lenton, P., and Mosley, P. (2008). Debt and health (Working paper 2008004). Avaialable at: http://eprints.whiterose.ac.uk/9978/1/SERP2008004.pdf (Accessed March 29, 2021).

Leotti, L. A., Iyengar, S. S., and Ochsner, K. N. (2010). Born to choose: the origins and value of the need for control. Trends Cogn. Sci. 14, 457–463. doi: 10.1016/j.tics.2010.08.001

Lombardi, M. J., Mohanty, M. S., and Shim, I. (2017). The real effects of household debt in the short and long run (Working paper 607). Available at: https://www.bis.org/publ/work607.pdf (Accessed March 29, 2021).

Lucas, R. E., Clark, A. E., Georgellis, Y., and Diener, E. (2004). Unemployment alters the set point for life satisfaction. Psychol. Sci. 15, 8–13. doi: 10.1111/j.0963-7214.2004.01501002.x

Lucas, R. E., Diener, E., and Suh, E. (1996). Discriminant validity of well-being measures. J. Pers. Soc. Psychol. 71, 616–628. doi: 10.1037/0022-3514.71.3.616

Meng, L., Zheng, Y., and Hui, R. (2013). The relationship of sleep duration and insomnia to risk of hypertension incidence: a meta-analysis of prospective cohort studies. Hypertens. Res. 36, 985–995. doi: 10.1038/hr.2013.70

Miller, S. M. (1979). Controllability and human stress: method, evidence and theory. Behav. Res. Ther. 17, 287–304. doi: 10.1016/0005-7967(79)90001-9

Morselli, L. L., Guyon, A., and Spiegel, K. (2012). Sleep and metabolic function. Pflügers Archiv–Euro. J. Physiol. 463, 139–160. doi: 10.1007/s00424-011-1053-z

Mossey, J. M., and Shapiro, E. (1982). Self-rated health: a predictor of mortality among the elderly. Am. J. Public Health 72, 800–808. doi: 10.2105/AJPH.72.8.800

Muthén, L. K., and Muthén, B. O. (1998-2012). Mplus User’s Guide. 7th Edn. Los Angeles, CA: Muthén & Muthén.

Olson-Garriott, A. N., Garriott, P. O., Rigali-Oiler, M., and Chao, R. C. L. (2015). Counseling psychology trainees’ experiences with debt stress: a mixed methods examination. J. Couns. Psychol. 62, 202–215. doi: 10.1037/cou0000051

O’Neill, B., Sorhaindo, B., Xiao, J. J., and Garman, E. T. (2005). Financially distressed consumers: their financial practices, financial well-being, and health. J. Financ. Couns. Plan. 16, 73–87. Available at: https://digitalcommons.uri.edu/cgi/viewcontent.cgi?article=1007&context=hdf_facpubs (Accessed March 20, 2021).

Pavot, W., and Diener, E. (1993). Review of the satisfaction with life scale. Psychol. Assess. 5, 164–172. doi: 10.1037/1040-3590.5.2.164

Preacher, K. J., and Selig, J. P. (2012). Advantages of Monte Carlo confidence intervals for indirect effects. Commun. Methods Meas. 6, 77–98. doi: 10.1080/19312458.2012.679848

Rothbaum, F., Weisz, J. R., and Snyder, S. S. (1982). Changing the world and changing the self: a two-process model of perceived control. J. Pers. Soc. Psychol. 42, 5–37. doi: 10.1037/0022-3514.42.1.5

Ryff, C. D., and Keyes, C. L. M. (1995). The structure of psychological well-being revisited. J. Pers. Soc. Psychol. 69:719. doi: 10.1037/0022-3514.69.4.719

Shapiro, G. K., and Burchell, B. J. (2012). Measuring financial anxiety. J. Neurosci. Psychol. Econ. 5, 92–103. doi: 10.1037/a0027647

Sheldon, K. M., Abad, N., Ferguson, Y., Gunz, A., Houser-Marko, L., Nichols, C. P., et al. (2010). Persistent pursuit of need-satisfying goals leads to increased happiness: a 6-month experimental longitudinal study. Motiv. Emot. 34, 39–48. doi: 10.1007/s11031-009-9153-1

Sorgente, A., and Lanz, M. (2019). The multidimensional subjective financial well-being scale for emerging adults: development and validation studies. Int. J. Behav. Dev. 43, 466–478. doi: 10.1177/0165025419851859

Summers, L., and Gutierrez, D. (2018). Assessing and treating financial anxiety: the counselor as a resource, rather than referrer. J. Individ. Psychol. 74, 437–447. doi: 10.1353/jip.2018.0032

Sweet, E., Nandi, A., Adam, E. K., and McDade, T. W. (2013). The high price of debt: household financial debt and its impact on mental and physical health. Soc. Sci. Med. 91, 94–100. doi: 10.1016/j.socscimed.2013.05.009

Switek, M. (2013). Explaining well-being over the life cycle: A look at life transitions during young adulthood. IZA Discussion Paper No. 7877. Available at: http://ssrn.com/abstract=2377613 (Accessed March 29, 2021).

Tay, L., Batz, C., Parrigon, S., and Kuykendall, L. (2017). Debt and subjective well-being: the other side of the income-happiness coin. J. Happiness Stud. 18, 903–937. doi: 10.1007/s10902-016-9758-5

Tay, L., and Diener, E. (2011). Needs and subjective well-being around the world. J. Pers. Soc. Psychol. 101, 354–365. doi: 10.1037/a0023779

Turunen, E., and Hiilamo, H. (2014). Health effects of indebtedness: a systematic review. BMC Public Health 14:489. doi: 10.1186/1471-2458-14-489

Wallston, K. A., Wallston, B. S., Smith, S., and Dobbins, C. J. (1987). Perceived control and health. Curr. Psychol. 6, 5–25. doi: 10.1007/BF02686633

Warth, J., Puth, M. T., Tillmann, J., Porz, J., Zier, U., Weckbecker, K., et al. (2019). Over-indebtedness and its association with sleep and sleep medication use. BMC Public Health 19:957. doi: 10.1186/s12889-019-7231-1

Zhang, J., and Kemp, S. (2009). The relationships between student debt and motivation, happiness, and academic achievement. N. Z. J. Psychol. 38, 24–29. Available at: https://www.psychology.org.nz/journal-archive/NZJP-Vol382-2009-3-Zhang.pdf (Accessed March 29, 2021).

Keywords: debt, over-indebtedness, subjective well-being, life satisfaction, net affect

Citation: Ferreira MB, de Almeida F, Soro JC, Herter MM, Pinto DC and Silva CS (2021) On the Relation Between Over-Indebtedness and Well-Being: An Analysis of the Mechanisms Influencing Health, Sleep, Life Satisfaction, and Emotional Well-Being. Front. Psychol. 12:591875. doi: 10.3389/fpsyg.2021.591875

Edited by:

Kamlesh Singh, Indian Institute of Technology, IndiaReviewed by:

Piotr Bialowolski, Harvard University, United StatesPaola Iannello, Catholic University of the Sacred Heart, Italy

Copyright © 2021 Ferreira, de Almeida, Soro, Herter, Pinto and Silva. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Filipa de Almeida, ZmlsaXBhZGVhbG1laWRhQHVjcC5wdA==