95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

PERSPECTIVE article

Front. Comput. Sci. , 17 April 2023

Sec. Networks and Communications

Volume 5 - 2023 | https://doi.org/10.3389/fcomp.2023.1099582

This article is part of the Research Topic Infrastructure Sharing in Broadband Networks: Impact on Telecommunications Operators and Consumers View all 5 articles

William Lehr1*

William Lehr1* Volker Stocker2

Volker Stocker2Resource sharing is fundamental to the design of telecommunication networks. The technology, economic and policy forces shaping the transition to next-generation digital networking infrastructure—characterized here as “5G+” (for 5G and beyond)—make new and evolved forms of edge sharing a necessity. Despite this necessity, most of the economic and policy research on Network Sharing Agreements (NSAs) has focused on sharing among service providers offering retail services via networks owned and operated by legacy fixed and mobile network operators (MNOs). In this essay, we make the case for why increased and more dynamic options for sharing, in particular of end-user owned network infrastructure, should be embraced for the future of NSAs. Furthermore, we explain how such a novel sharing paradigm must be matched by appropriate regulatory policies.

Sharing has always been fundamental to the design of telecommunication networks. Statistical multiplexing of the traffic from multiple end-users makes it economically feasible to provide end-user services with capabilities and performance that would not be affordable if end-users had to be provisioned with dedicated facilities1. From an engineering perspective, the history of networking is one of evolving from purpose-built silo networks to general-purpose digital networks offering an evolving range of services with diverse bandwidth and other Quality of Service (QoS)2performance needs. Historically, the sharing was managed on behalf of end-users by legacy telecommunication service providers who mostly owned and operated the networks over which the shared services were provided3. The centrality of these service providers was also reflected in the roaming agreements and sharing via wholesale service offerings that facilitated the accelerated build-out of fixed and mobile coverage and allowed operators to make use of the excess capacity that networks typically have available4. From an economics perspective, regulators have sought to balance the dual goals of minimizing total costs and promoting competition, which is arguably most intense when the service providers own and operate separate facilities-networks. Consequently, regulatory policies have often sought to restrict network sharing, or when necessary, viewed it as a last-choice option.

With the transition to next-generation networks, in the following referred to as 5G+5, the need to deploy many more small cell sites and the significant increase in capital costs required to provision 5G+ networks makes it increasingly important that network resources be shared, in particular, if national (or supranational as in the EU) 5G service goals are to be realized in a timely fashion and at reasonable cost6. For example, BEREC concluded that there are significant benefits to both passive and active sharing7, with the potential to reduce total operator OPEX and CAPEX by 20–40%8. Those cost savings are a direct result of reducing the need for redundant infrastructure investment and the potential to realize higher asset utilization when resources are shared. Capacity sharing also makes it feasible to realize economies of scale and scope9. Additionally, the evolution of networking technology toward 5G+ implies a transition toward more modular, flexible, software-controllable networks supporting much expanded and dynamic customization capabilities on a more fine-grained or granular basis10. These capabilities contribute to reducing overall network costs while also making it possible to provision customized services with different QoS on a more granular basis in the face of more dynamic and heterogeneous demand. Essentially, 5G+ networks are predicated on novel resource sharing approaches (aka “next-generation resource sharing”) that allow multiplexed sharing in multiple dimensions (time, QoS, control, etc.) of an expanded range of digital (bandwidth, computing, storage, etc.) and non-digital (local antenna sites, power supply, conduit, etc.) resources11.

In this essay, we explore the necessity for dynamic edge sharing in 5G+ next-generation networks. We make the case for why increased options for sharing of end-user owned network infrastructure ought to be more actively considered and embraced by policymakers. We explain why converging policy, business economics, and technical forces are expected to make local end-user provided edge network infrastructure an increasingly important feature for 5G+ networking and thus our digital future12. In this context, we contextualize the discussion within the existing technical and economics literature on Network Sharing Agreements (NSAs) and explain how the need for increased edge-resource sharing is a technical and market driven imperative requiring appropriate regulatory policy consideration and responses. The remainder of this essay is structured as follows. Section 2 lays out some key considerations related to the technical aspects of migrating toward next-generation infrastructures and resource sharing and emphasizes its implications. Section 3 then discusses the ensuing policy challenges and outlines key features of and a path toward next-generation regulatory policies capable of facilitating and matching changing industry structures. Section 4 distills major insights and discusses the case for edge sharing. Section 5 concludes.

Next-generation 5G+ networks are transformative, giving rise to new ownership and value chain constellations. More specifically, respective infrastructure resources will be provided by an array of entities and lead to ownership and value chain constellations that deviate from those that characterized the legacy world. To the extent that ownership of capital intensive 5G+ resources (mostly passive, but also including active) is shifted to end-user owned edge networks, the economic tension between minimizing total network costs while enabling facilities-based competition among service providers can be reduced13. On the continuum of strategies for addressing the challenges posed by the increasing need to provision for shared edge networks while addressing the difficulty of sustaining facilities-based competition among service providers, the rise of TowerCos is an important example14. Other examples include community or municipal networks, neutral hosts, and a variety of other novel business models that seek to solve the edge-network provisioning challenge of 5G15. Additionally, from a technical and business perspective, there are growing strategic reasons why end-users with edge networks may wish to assume control (including ownership) of relevant network resources16.

Options for dynamic provisioning and cooperative sharing among end-users already exist. However, the basic software and network support is expected to improve significantly in the next few years to enable the provisioning of end-user local clouds as an alternative and complement to private and public connectivity and cloud service providers. The implementation of active and more efficient sharing of existing, complementary communications and computing resources owned by different/competing entities both located at the edge and in core networks, however, is predicated on enhanced contractual flexibility and evolved forms of coordination between and among diverse entities. Whereas, those business models are evolving, the precise form they may take remains uncertain17.

At the same time that edge-cloud technical capabilities and demand for edge-based control and investment in edge-based (local) digital infrastructure and capabilities (including intelligence, computing, storage, and connectivity) is increasing, national and international cloud and digital infrastructure providers are expanding their capabilities to dynamically reconfigure their resources and push their services closer to the edge18. Some of the motivation for this expansion is in response to the growing threat to legacy ISP business models posed by edge providers that are adding capabilities to provide value-added capabilities that compete with ISP services. Downstream, providers of end-user devices and applications that are part of the Apple iOS and Android ecosystems offer ways to enable services that augment ISP resources and capabilities. Upstream, digital platform service providers like Google, Amazon, and Microsoft offer cloud and higher-level content and application services that both compete with ISP services and increase the need for additional downstream capacity19.

The nature and pace of changes associated with these developments will impact how the ecosystem for 5G+ networks and services evolves. Importantly, 5G+ networks may act as “enabling platforms” (e.g., Bauer and Bohlin, 2022). They may nurture and facilitate innovation processes among networks, the services they provide, and their interactions with the other digital and non-digital resources that they depend on. Additionally, newly emerging edge network providers with (asset-heavy and) locally focused business models may disrupt incumbent legacy operators and service landscapes (e.g., Knieps and Bauer, 2022).

Earlier, we noted how passive and active sharing among network operators can lead to significant—large double digit—reductions in total costs by avoiding duplicative excess investment in multiple network elements20. Avoiding such excess investment reduces operator investment costs, and in the face of bottleneck constraints on finances and other operator resources, may allow industry investment to be better targeted to provide expanded access to improved network services sooner, thereby realizing additional total welfare benefits and assisting in the realization of national connectivity targets as specified, for example, via universal service goals.

Shifting the cost of network elements from operators to end-users, however, will have less obvious implications on aggregate investment requirements and costs. Whereas, the cost shift will not eliminate the costs, it may actually sacrifice scale and/or scope economies and sharing opportunities if end-user owned/managed network assets (e.g., computing resources, site power, and other elements) are utilized less efficiently than edge computing or edge network assets owned by an operator, which has an incentive to share operator owned assets by multiplexing the demand of multiple end-users. Additionally, integrating end-user resources into the fabric of the Internet infrastructure will add novel complexities that may add to coordination and interoperability costs, at least in the short-term. Offsetting such potentially lost cost-economies, however, is the potential to make use of significantly under-utilized existing computing and network resources that end-users already own or are in a better position to deploy or expand21.

The rise of new models for 5G+ cost sharing among new types of edge and legacy core network providers has the potential to reorganize and restructure ownership and value chains. It may thus generate more liquid technical and business relationships and render the associated contractual fabric more flexible. This will, in turn, yield an ecosystem that is inherently not only dynamic and complex, but also diverse along multiple dimensions (e.g., control, space, time, etc.). This increased complexity will challenge traditional notions of industry structures or market definition that seek to classify and categorize the interactions between service providers on the basis of vertical or horizontal interactions.

The forces propelling the vision of 5G+ infrastructure are part of the global digital economy transformation underway. This transformation reflects the expanded integration and application of digital technologies to all aspects of social and economic activity, which presents the ultimate demand driver for investment in 5G+ infrastructure: to enable increased access to networked, on-demand, high-performance ICT resources—for communication, computation, and storage. These resources constitute the infrastructural basis needed to enable Smart-X capabilities where X is any task that may benefit from automation or augmentation with information and communication technology (ICT)22. Examples of the most ambitious ICT applications that 5G+ infrastructure is expected to support include Virtual/Augmented/Mixed/Extended Reality (VR/AR/MR/XR) use cases, Autonomous Vehicles (AV)/Unmanned Aerial Vehicles (UAV), and Robotic Process Automation (RPA). Some of these applications will be edge-native, for example, because of stringent latency requirements or edge-device limitations23.

5G+ infrastructure constitutes an enabler of our digital future. At its core, its bottom-line technical implication is that respective 5G+ networks will include interfaces (by design) to facilitate dramatically expanded mix-and-match opportunities among the various components needed to assemble an end-to-end service24. From an end-user's perspective, a key economic driver for these expanded mix-and-match capabilities is to allow the digital infrastructure to simultaneously and seamlessly support diverse and increasingly demanding services, which potentially may be offered by multiple entities. The applications and end-users may have widely different requirements along one or more dimensions related to connectivity (e.g., bandwidth and other QoS performance metrics), computation and storage, time, cost of service, and other factors. A key aspect and “byproduct” of the associated technical changes and expanded capabilities that are motivated by the desire to meet end-user requirements for more capable services efficiently (i.e., at lower total cost) is that it is increasingly feasible to consider many more technical network sharing options. As the technical design space of sharing options expands, so too does the business design space for sharing options (so long as economically viable options are not precluded by regulatory policies).

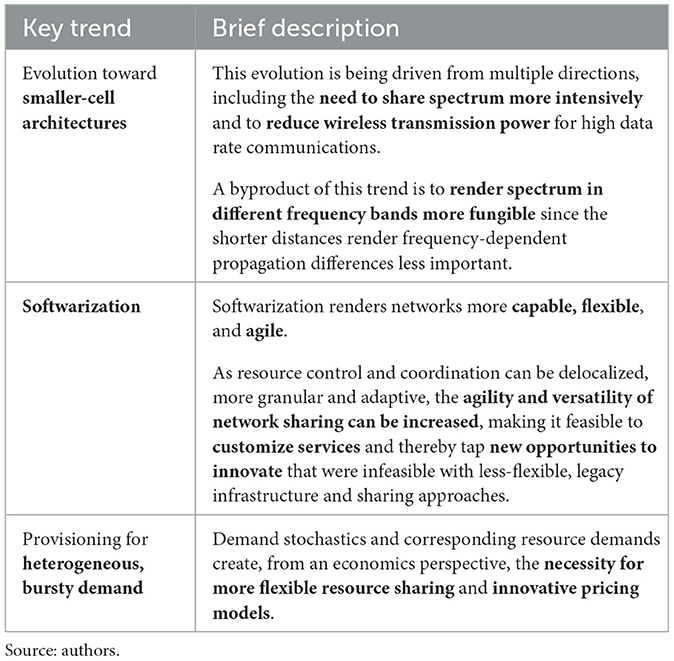

In Table 1, we identify three key technical/market trends that exemplify the forces making it technically and economically feasible to adopt more dynamic sharing approaches.

Table 1. Key trends that facilitate or drive more dynamic sharing approaches.

Expanded technical capabilities give rise to potential demand growth. This is because lower costs and increased capabilities make it economically viable to expand services to previously uneconomic sources of demand and also foster innovation and new services. When coupled to the expanded mix-and-match capabilities, the increased demand creates potential opportunities for expanded competition via entry using legacy or novel business models in both component or system markets, if new models for network resource sharing are embraced.

Historically, when the last-mile networks were provided by integrated providers over separate, service-provider owned and managed facilities-based networks, policymakers viewed NSAs as threats to competition. As a consequence, they often severely restricted such agreements. In light of the increased difficulties of promoting facilities-based competition and industry consolidation at multiple service provider levels (among MNOs, digital platform providers, and device/ancillary service providers)25, the necessity for policymakers to embrace a richer perspective on NSAs among service providers has increased. This necessity has been emphasized by a growing body of economic research investigating these NSAs among service providers; it has shown that under most conditions and those that have prevailed in practice, NSAs have tended to be efficiency and welfare-enhancing (e.g., Maier-Rigaud et al., 2020; Pápai et al., 2020; Koutroumpis et al., 2021).

In the case of MNOs, the most common and least worrisome type of sharing for policymakers is passive, but technologists and economists who have considered 5G, anticipate a greater need for active network sharing in the future. Many have noted that active NSAs are preferrable from a competition perspective to mergers as a mechanism for realizing cost economies (Afraz et al., 2019; Motta and Tarantino, 2021; Oughton et al., 2022).

An implicit assumption of the technical and economics literature that has examined network sharing has taken the perspective that the networks are provided by (legacy) service providers that own/manage the networks to deliver services to increasingly demanding and heterogeneous end-users. With this perspective, industry structures are framed in a particular and rather static way and the sharing of resources is assumed to remain among a specific set of service providers. Occasionally, however, it has been recognized that more efficient sharing calls for the restructuring of asset ownership and control to enable the NSAs. A key example is the sharing of towers by MNOs that helped promote the emergence of independent tower companies as significant players in the industry. Economics research on NSAs has identified the importance of TowerCos, while acknowledging that more research is needed to understand how they should fit into the industry economics and policy challenges associated with managing the transition to 5G (Mölleryd et al., 2014; Koutroumpis et al., 2021).

As we explained above, enabling the more local digital infrastructure needed to support 5G+ going forward (i.e., smaller cells, edge computing, etc.) will increase opportunities for entry by additional novel participants in the 5G+ landscape; it will also require accessing and sharing resources that are controlled and owned by end-users. Those may mostly include non-digital assets such as antenna-sites, final-hop access wiring, and end-user owned servers and network terminal equipment for running hosted software applications that may be provided by other service providers.

In this context, embracing end-user sharing as a potentially efficient solution will help reorient regulatory attention away from policies inappropriately anchored in models of legacy industry structures that focus attention on imposing performance and coverage requirements based on the identity of the provider. Moving beyond a focus on NSAs between legacy telecommunication service providers, or only slightly better, between legacy telecommunication service providers and other large-scale service providers such as digital platform service providers, TowerCos or others, should help in enabling regulatory policies to be more responsive to the changing needs and potential for 5G+ digital infrastructures. Establishing guardrails and frameworks that facilitate market entry and edge sharing at different levels (at the component or system-level) should increase the ecosystem's capabilities to adapt to newly emerging demands and technical innovations.

Embracing a richer perspective on NSAs that includes end-users also acknowledges the potential need for changes in ownership structures and reorganized industry value chains that can assist in paving the way for achieving 5G service goals in a timely fashion while promoting competition (contestability) and enabling market forces to direct ecosystem participants toward cost-minimizing and welfare maximizing deployment and sharing options. Significantly, regulatory attention can then be directed toward wherever problems may actually arise, rather than on where problems were perceived to be most likely to arise based on legacy industry value chains.

Adopting and “triangulating” different but complementary perspectives reveals that end-user sharing offers a range of important benefits, yields more sharing capabilities, and enhances market opportunities and end-user choice as well as competition.

The shift to small cells implies that the need for new investment and access to resources that are inherently local (site, power supply, etc.) increases26. This, in turn, means that end-users are closer to where investment is needed and less likely foreclosed by the economics of distance. In legacy settings, a service provider has a clear advantage over individual end-users when it comes to investments in assets that provide services over a large area. For example, a central computer has a lot of capacity that provides a service to many end-users that are distributed over a large area. The necessity or role of any single end-user (“bargaining position”) is reduced and does not shape the design of respective investments and assets. Small cells are fundamentally different and subject to a different investment paradigm. They are inherently local infrastructure, and each individual end-user (depending on how small the cell is) represents a bigger share of the end-users for which that investment is co-specialized and localized27.

Moreover, assets that must be shared by large numbers of end-users (e.g., a large-scale data center) are typically too expensive in terms of upfront cost (fixed, potentially even sunk) and realize too much in the way of scale economies to be competitive with end-user-deployed infrastructure. Put another way, individual end-users would never deploy a Class 5 switch but may very well-deploy a Private Branch eXchange (PBX) or local router—and as the modularity and costs of technology decline, the PBX/local router becomes a more affordable and capable competitor for delivering functionality that previously required the Class 5 switch.

In recent years, the trend toward more modular28 , smaller ICT components that are more capable has driven a move toward more embedded CPUs and lowered the costs for deploying more capable CPUs and other ICT devices at all levels. This trend drives changing cost economies, expanding opportunities for more distributed and local infrastructure deployments, including those located close to end-users or on end-user premises29. As a consequence, these trends pave the way for change—in terms of how networks are designed and provisioned, where they are deployed, by whom they are owned, and how they are shared.

The expanded technical capabilities explained above expand markets and market opportunities. They imply a digital future that is both more heterogeneous and unpredictable. For example, in a world where AR/VR did not exist, no one would have it. In a world where AR/VR can exist, different users will use AR/VR differently, depending on the applications used and the configuration of the end-user's in-home or on-device networking capabilities30. Just as we see increased fragmentation of digital markets with extremely long tails and unstable concentration of Top 100 websites, media properties, etc., we should expect to see fragmentation of digital resource demands31.

End-users' heterogeneous preferences are not limited to the selection of applications used, but also includes the range of options for satisfying end-user demand. That includes the ability of end-users to select among different suppliers and contracting terms32. As there is no unique industry structure that maximizes end-user choice across these multiple dimensions, there are benefits of enabling expanded options for end-user self-provisioning33.

However, many end-users—indeed, most—may prefer not to self-provision. Relying on a service provider that is able to aggregate the traffic and demands of many users to realize scale and scope economies in many cases may offer lower costs, and service providers even may know better than many end-users (e.g., mass market consumers) how to match products and services to maximize consumer welfare34. In a world of uncertain demand and supply trajectories and where information is asymmetric and imperfect (i.e., there are fundamental unknowns and unknowables), the allocation of decision-making control (choice) among end-users and service providers so as to maximize total or individual welfare is indeterminant. In many cases, service providers may be better (or worse) situated to manage the risk associated with uncertainty—but which is the case will depend on the context.

Nevertheless, and despite these considerations, one can think of scenarios in which even when end-user deployed infrastructure and sharing among end-users and among end-users with service providers is less efficient (i.e., costs are not lower or networks not more capable), enabling end-user deployed infrastructure can still deliver benefits in terms of competition (due to increased contestability) and resiliency (due to non-correlated failure modes).

In view of the points made above, we identify several substantial reasons that make a compelling case for closer consideration of edge sharing. In many cases, end-users either own relevant resources, control access to them (e.g., access to a small cell site or power) or can provide them most efficiently (e.g., basic maintenance—plugging a resource in or other actions that would otherwise require a truck-role since they cannot be accomplished solely by software-initiated remote action). In those situations, which we anticipate to increase in a world of 5G+ networks, options for end-user involvement must be ensured.

Edge sharing has many benefits but comes in different shapes and forms. First, edge sharing will need to be among end-users. For example, edge sharing may take place within the same household across multiple individuals, devices, and apps that are likely to share a single or multiple connectivity options with the larger world35. This might also be the case in multi-tenant occupancy situations where the edge network is shared as in a mall, apartment building (or gated community), or campus (anchor institution like a school, library, or industrial campus). Second, another relevant form of edge sharing may be between end-users and established service providers (e.g., legacy service providers like access ISPs, digital platforms, and cloud service providers) as well as alternative/novel service providers (e.g., neutral hosts, next-generation antenna or ancillary resource enterprises36).

One strategy for reducing the service provider costs of deploying 5G+ infrastructure is to shift the costs of certain elements from service providers to end-users. For example, the broadband modems provided by fixed-broadband providers and the small-cell hotspots provided by MNOs are typically leased to subscribers, but make use of subscriber-provided site-access and power37. The control of these assets is divided between service providers and end-users. For example, the service provider may install the devices on end-user premises and have significant capabilities to remotely monitor and control the functioning of the devices. However, the end-users also have control power associated with the device configuration and service options they elect to enable (including their rights to terminate or modify their service agreement). Distributing ownership and control of key assets to end-users restructures the bargaining and contracting relationship between service providers and their customers. On one hand, it shifts parts of the total costs off the books of service providers onto the books of end-users. This reduces the investment burden for service providers, which may make additional facilities-based competition more likely or improve the return on the investment that remains on service provider books. On the other hand, it may shift, to a certain extent, bargaining power to end-users (but that need not necessarily follow38), or if it enables additional facilities-based entry, may intensify competition39. With this in mind, small cell portability and open architecture options should be protected to support and safeguard edge sharing, competition, and end-user choice.

An unavoidable consequence of where the trajectory of digitalization is taking us technically and from an economic-access-to-critical-resources perspective is that end-users will need to be more involved in enabling next-generation networks and services. Recognizing and understanding that point is critical for designing marketplaces and suitable guardrails and regulatory policies for network sharing.

Network sharing of local 5G+ infrastructure that is owned by end-users has the potential to yield significant benefits. First, cost savings can be achieved by taking advantage of existing ICT resources that otherwise need to be duplicated to provide services. Moreover, end-users may be in a better position to deploy or expand relevant local resources. Second, strategic flexibility to adapt industry value chains to respond to and enable more robust innovation in technical architectures and business models can be enhanced by expanding the realm of NSAs to new types of edge-networks, up to and including NSAs involving end-user digital and non-digital resources. Third, competition for last-mile infrastructure can be intensified by embracing the option for end-users' self-provisioning, even if many end-users may quite appropriately opt for service provider provisioning. It expands the options for mix-and-match competition (contestability) among technical and business model alternatives for provisioning the resources, components, and systems needed at the edge to support 5G+ services and applications. Embracing end-user NSAs expands mix-and-match opportunities.

Existing regulatory models are too predicated on legacy models of industry structure. Those legacy models anticipate and thereby reinforce barriers to entry that presume particular architectures and provisioning approaches. Those are burdened by the legacy of silo-based telecommunication services where the critical service was the bit-level transport connectivity provided by access service providers to edge content and application service providers.

That industry value chain model is under assault as fixed and wireless, terrestrial and non-terrestrial technical alternatives for providing last-mile connectivity are simultaneously competing and being integrated into a richer connectivity fabric for providing mobile and fixed services. Moreover, the digital infrastructure required to support 5G+ services and applications requires that edge-based networks provide dynamic access to computing and storage resources in addition to just the traditional telecommunication “bit-transport” services, especially if the more demanding applications such as AR/VR and AI-driven automation are to be realizable. Precisely how best to provide and integrate those computing and storage capabilities with broadband connectivity capabilities is uncertain.

Although there is broad support from policymakers, industry, and academics of the long-term vision of what sorts of capabilities we want and expect our global digital infrastructure to provide, there is no general agreement as to what the best industry structure and path for realizing those capabilities should follow. There is also significant variance with respect to forecasts of how the future will evolve.

In light of this uncertainty and in recognition of the fact that public investment will comprise at most only a small share of the total investment needed to build next-generation digital infrastructure, a key goal of policymakers will be to promote a healthy market ecosystem which will imply continuing with a light-handed regulatory approach. The Internet ecosystem is too complex and geographically diverse to be amenable to command-and-control, public utility-style regulation, even if one were to imagine that that were desirable. In such an environment, policymakers should embrace more expansive NSAs to realize the efficiency benefits that expanded active as well as passive sharing of network resources can enable. Introducing such flexibility is necessary but hardly sufficient to also enable expanded sharing with end-users. It will also be necessary to make sure that regulatory rules are not biased against end-user provided network elements. For example, regulatory rules that block community-based networks (or community franchises that discriminate against competition from other service providers) both risk distorting costs and erecting inefficient barriers to competition. Next-generation regulatory policy should recognize and embrace the opportunities end-user participation offers, not preclude them.

Additionally, to protect against the many ways that NSAs might be abused to harm competition, policymakers will need to encourage an inclusive and dynamic ecosystem for network performance measurement. Part of that will include active government monitoring and measurement programs and transparency and disclosure mandates. However, the latter, while important, are hardly a panacea and are difficult to craft appropriately40. Finally, as network edges and end-users (in gated communities, shared tenant dwellings, industrial and academic campuses and other edge-private networks) assume a greater role in providing key elements comprising the fabric of our global digital computing and communications infrastructure, regulators will need to adapt how regulatory rules are targeted. Instead of targeting regulatory obligations to actors with specific business models (e.g., differentiating between access ISPs and edge providers), regulators will need to focus on whichever actor is engaging in the harmful behavior. Enabling this shift will be difficult since expanding the scope of businesses that may attract regulatory attention will make it difficult to enable sufficiently flexible regulatory oversight without risking regulatory abuse of its discretionary authority41.

Recognizing the unavoidable and expanded role that end-users (and by extension, new types of service provider business models) will be required to play in more efficiently provisioning essential resources and edge-network components for the 5G+ future should motivate policy-makers to embrace expanded notions for regulating NSAs. As explained herein, embracing end-user/edge-based sharing is compatible with the capabilities of today's technologies and their potential to enable growth in demand, reduce network costs, and expand end-user choice. Failure to do so risks biasing regulatory policies that may preclude efficient restructuring of edge networks and the emergence of novel business models and efficient sharing arrangements. Blocking such emergence may limit competition that might otherwise add an important source of competitive discipline to the 5G+ ecosystem.

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

WL and VS collaborated in co-authoring the contribution and are jointly responsible for the analysis and opinions offered. All authors contributed to the article and approved the submitted version.

Funding for publication provided by MIT Open Access publication support.

WL would like to acknowledge the support of NSF Grant #2228470. VS would like to acknowledge funding by the Federal Ministry of Education and Research of Germany (BMBF) under grant no. 16DII131 (Weizenbaum-Institut für die vernetzte Gesellschaft—Das Deutsche Internet-Institut).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

1. ^By end-users we refer the mass market consumers and business customers who are the source of the final demand for the network services provided by the various types of service providers. The latter include Internet Service Providers (ISPs) who provide the basic access services, digital platform service providers that provide various cloud services and complementary services, and edge service providers of content and application services.

2. ^In this essay, we adopt a broad understanding of QoS as it is often defined in terms of technical performance metrics such as latency, packet loss ratios, availability, or other metrics such as (peak) data rates. Compositing link-level QoS measurements or guarantees, which may be instantiated in Service Level Agreements (SLAs), is non-trivial and often subject to contention. Moreover, QoS is often distinguished from Quality of Experience (QoE) which brings in subjective but more holistic end-user perceptions in the consumption of applications or services. See, for example, Stocker (2020).

3. ^The legacy telecommunication service providers include legacy telephone (sometimes referred to as TelCos) and cable TV network operators (sometimes referred to as CableCos) and Mobile Network Operators (MNOs) that have evolved into today's broadband ISPs of wired and wireless, fixed and mobile networks. Much of the regulatory focus on these operators is directed at their networks and the provision of last-mile access services to mass-market consumers and businesses. Much of the popular attention is directed toward the retail Broadband Internet Access Services (BIAS) that for most end-users provide the on-ramps to wide-area network services and the global Internet (e.g., Stocker et al., 2020). Much of the focus on network sharing among these providers has been directed at their provision of connectivity (or data transmission) services, although many of these telecommunication service providers provide other services as well. Those include higher-layer application and content services (e.g., video entertainment, telephony, gaming, home security, etc.), as well as lower-layer basic infrastructure services (e.g., collocation facilities and other resources needed for the deployment of local and wide-area digital infrastructures). The latter are sold to both larger enterprises and other service providers as business telecommunication services, and include private lines in multiple configurations, Virtual Private Network (VPN) services, and other telecommunication services that are basic building blocks used to construct private and public networks.

4. ^Networks typically have excess capacity available (at least in parts of their networks) because they need to provision for expected peak capacity demands and because capacity investments are lumpy and designed to accommodate future traffic growth. Because traffic loads across locations and operators are subject to stochastic variation and are imperfectly correlated, sharing capacity among operators can reduce aggregate peak capacity provisioning costs, especially in edge networks. By edge networks, we mean the computing resources and network connections that are close to the end-users, but defining where the Internet's or a last-hop service provider's core network ends and the provider's or an end-user's edge network begins is not always obvious (Lehr et al., 2019). To understand why a bright-line definition of what constitutes the edge network is inappropriate in the context of this paper, consider the following question: Is an Internet of Things (IoT) device that is located on an end-user's premises (and belongs to the end-user and is not part of any service provider's network) that supports Internet connections and may be reachable from locations on the public Internet part of the Internet? The question we focus on in this essay relates directly to how end-users are likely to play a greater role in the control, ownership, and provisioning of edge network resources.

5. ^When used herein, 5G+ is shorthand for next-generation networks offering the capabilities articulated in ITU-R (2015) for 5G networks and beyond. This should not be equated or limited to the networks provided by traditional MNOs or the set of 5G standards defined by 3GPP. See Lehr (2022) and Lehr et al. (2021) for further discussion of this more expansive use of the 5G terminology. More recently, and because providers are already offering services touted as “5G,” some researchers are now referring to “6G” to identify next-generation networks, or in the case of IEEE P802 standards-based networks, to differentiate their offerings from the 3GPP cellular-based 5G technologies. All of these standards-based technology roadmaps are encompassed in our use of 5G+.

6. ^For example, EU recommendations for 5G rollouts emphasize the need to embrace infrastructure sharing to reduce the cost of deploying high-speed electronic communication networks (see Weissberger, 2020). Accommodating continued exponential data traffic growth as more users are using more demanding and interactive applications is driving network operators to densify their networks, adding more smaller cell sites which increases operator Capital Expenditures (CAPEX) and Operating Expenses (OPEX). For example, McKinsey projected that the transition to 5G could increase the total cost of ownership (CAPEX plus OPEX) by between 60% and 300% based on differing growth scenarios for the speed of transition to 5G and the projected growth in data traffic (see Grijpink et al., 2018). At the same time, changes such as the introduction of Software Defined Networking (SDN) and Network Function Virtualization (NFV) which are part of the softwarization of networks and are also part of the transition to 5G are helping to reduce costs, while also providing the basic functionality to enhance active network sharing, for example, via network slicing. For example, Bouras et al. (2016) propose a network architecture for softwarized 5G networks and develop a cost model based on which they compare the costs of their proposed architecture to the cost of a traditional architecture. Their experimental results show that the deployment of small cell base stations and the use of network softwarization and virtualization can help network operators realize a 63% reduction in OPEX and a 68% reduction in CAPEX (Bouras et al., 2016, p. 61; see also Oughton and Frias, 2018). Network operators are under significant pressure to adopt technologies and business strategies that will reduce costs in the face of continued exponential data growth unmatched by comparable revenue growth. For example, according to American Tower, mobile data traffic in the U.S. grew at 79% Compound Annual Growth Rate (CAGR) from 2006 to 2019, while tower revenue per GB fell from $76.93 to $0.31 (or at 34% CAGR) (see American Tower, 2020). GSMA (2023) provides a recent and comprehensive overview of the state and future of the mobile industry, including insights into the growth in mobile traffic, the number of licensed IoT devices, and mobile revenues. Moreover, additional studies estimating the cost savings from expanded NSAs include Rendon Schneir et al. (2020, pp. 65 and 68) and Koratagere Anantha Kumar and Oughton (2022). The latter examine 5G infrastructure sharing in rural areas. They report cost savings from advanced network sharing scenarios (or “business model options”) compared to a baseline scenario (no sharing; minimum average data rates of 30 Mbps and monthly data use of 50GB per user) of 10-20% for passive sharing, 20-35% for active sharing, and 35-50% for shared 5G neutral host networks (Koratagere Anantha Kumar and Oughton, 2022, pp. 14–15).

7. ^Modern networks require a wide range of both active and passive resources. Active resources are comprised of the active digital hardware and software elements, whereas passive resources include the antenna sites, masts, conduit and other non-electronic elements that are needed to support the operation of the active hardware and software elements. Body of European Regulators for Electronic Communications (BEREC) (2019) defines passive elements as “those which are not able to process or convert telecommunication signals in any way and which are not integrated parts of the system dedicated specifically to the conveyance of signals” and active elements as “those which are able to generate, process, amplify and control signals” [Body of European Regulators for Electronic Communications (BEREC), 2019, p. 12]. However, the distinction is not always clear. For example, passive elements are usually non-powered elements, but cooling equipment is generally considered passive infrastructure even though it is powered; and antennas were typically regarded as passive elements, but advanced smart antennas may be active. There are many different types of sharing agreements, including sharing of different active or passive elements, as well as higher-level services or resources. Dynamic sharing of spectrum resources is a form of active sharing, as well as roaming agreements among mobile operators. Radio Access Network (RAN) sharing is another form of active sharing in which operators agree to share RAN resources. There are also various core network and backhaul sharing agreements. Most of the active sharing agreements also include the sharing of passive elements. Historically, regulators have viewed passive sharing agreements as posing a lesser threat to competition than active sharing, but the benefits of expanding sharing agreements into active sharing are seen as offering even greater efficiency benefits [see, e.g., Body of European Regulators for Electronic Communications (BEREC), 2018, 2020, 2021].

8. ^Body of European Regulators for Electronic Communications (BEREC) (2018, p. 116) reported that cost-savings from different types of sharing agreements yielded reductions in CAPEX of 16–45%, and OPEX of 16–35%. These cost savings refer to reductions in total costs from sharing among operators.

9. ^For example, NFV (see Footnote 6) allows for consolidation of network functions, resulting in cost savings since it avoids the per-unit costs of supporting functions from multiple locations, and supports more scalable capacity expansion to more easily match capacity to aggregate demand which varies less than per-operator demands which fluctuate with market shares as well as aggregate demand.

10. ^Network softwarization and the shift to smaller cells makes it feasible to customize services on a more granular basis in multiple dimensions (space, time, and context). Services can vary by location, change over time, and vary by type of user or usage as software-controlled services adapt to changing demand and supply dynamics. For example, advanced radio base stations can dynamically allocate spectrum resources to flexibly support dynamically changing application demands.

11. ^Legacy statistical multiplexing exploited the fact that user traffic demand was asynchronous in time. Multi-service networks can support multiple types of traffic with different QoS requirements, allowing, for example, the same shared network to efficiently deliver latency tolerant and intolerant services. With NFV and network programmability (e.g., based on SDN or P4), capabilities for virtualization, customization, and delocalization of control and where an action takes place greatly expand the technical sharing options. This may include network slicing approaches. See, for example, Shukla and Stocker (2019).

12. ^These edge networks may be provided by the ultimate end-users or by new types of edge-network infrastructure providers. For example, addressing these challenges has already prompted expanded and changing roles for service providers like Tower Companies (TowerCos) and other novel forms of edge-network service provider business models that may operate at local, regional, or national scale and may take a number of forms. For example, American Tower and Crown Castle—two of the largest TowerCos—are separately exploring options for expanding the wholesale services they provide to MNOs and others to support the demands of newer small cell 5G+ networking (see https://americantower.com/ and https://www.crowncastle.com/). Although these are both service providers and there are other service provider models feasible (e.g., Real Estate Investment Trusts (REITs), etc.), these approaches are closer to what we are talking about than the traditional business models of legacy last-mile access providers like MNOs, TelCos and CableCos. Another example are municipal networks which are networks that also deviate from traditional networks and business models (e.g., Sirbu et al., 2006).

13. ^In fact, end-user owned edge networks not only expand the scope of service providers but also change the traditional trade-off between minimizing total network costs while enabling facilities-based competition among service providers based on which many current regulatory policies are designed. As noted earlier, when the principal architecture for providing last-mile network services depends on tightly integrated silo-networks (where the “silo” nature is reflected both in the technology used to provide the service and its service definition), facilities-based competition requires competing silos. In such a world, limited retail-level service-based competition can still occur if non-facilities-based resellers are able to acquire the requisite wholesale network services needed at suitable cost. The provision of such options can be enabled by regulatory mandates (e.g., local loop unbundling or total service resale requirements imposed on facilities-based networks) or market forces (e.g., when oligopoly competition among facilities-based providers is characterized by excess capacity as was the case in the U.S. in long-distance telephony services). Typically, however, such retail-level competition is viewed by policymakers as less intense and more costly from the perspective of the regulatory oversight required to ensure that the providers of potential bottleneck facilities do not abuse their market power. If the network costs associated with providing the service can be reduced by shifting some of the “silo” costs to end-users, then the total costs of silo-based competition are reduced. Moreover, to the extent the requisite resources that are shifted to the end-users can be shared among the facilities-based providers of other services, options for facilities-based or other types of intermodal competition are intensified, potentially further reducing the total costs and increasing the potential for service-level competition. By analogy, when legacy cable TV and telephone network providers morphed into IP-based providers of broadband network services that enabled them to enter each other's retail markets, what had been independent silo-based competition for last-mile network services became intermodal, duopoly competition in across most of the US, where most communities were served by overlapping cable TV and telephone last-mile networks.

14. ^TowerCos provide the cell towers used by MNOs to locate the MNOs' base station radios and associated hardware that provides the network connection to their customer's handsets. TowerCos like American Tower and Crown Castle which emerged in the mid-1990s, established themselves as providers of macrocell towers that allowed MNOs to reduce their infrastructure capital costs by outsourcing their need for tower space to separate businesses that shared those towers among multiple MNOs.

15. ^For a discussion of implications of 5G+ for the industry ecosystem, see Lehr et al. (2021) and Oughton et al. (2021).

16. ^That is, as we become more dependent on digital (AI-driven) automation that dependence renders decisions about and control of the digital automation more strategically important. With the next generation of networked IT services, we will find digital technology embedded ever-deeper into the fabric of our social and economic lives and in all aspects of business operations. This will expand the realm of business decision-making that will need to consider IT automation options (from Human Resources to operations, from Finance to sales). Additionally, as the IT resource requirements for local digital infrastructure (computing, storage, networking) increase the potential for excess dedicated capacity (and excess costs), it will increase cost-based incentives for sharing those resources within the business and with others (both customers and others)—if the costs of sharing are sufficiently low. In the case of business computing, we have seen the rise of general-purpose computing platforms (personal computers and other fat-client devices) compete with specialized (IT appliances that may be expected to proliferate with the growth of the IoT) and thin-client devices (e.g., Chromebooks that supplement their general-purpose computing capabilities with network-based resources). Put another way, the make-vs.-buy, self-source-vs.-outsource options are greater and the importance of those decisions have greater strategic relevance as the share of business operations that are digitally-augmented (or equivalently, automated) increases.

17. ^For example, with the move to smaller cell architectures (which requires the construction of many more cells) and the need for increased computing resources close to the network edge, TowerCos are expanding their footprint and business models to include data centers and small antenna infrastructures. Real estate developers of shared residential and business spaces (malls, office complexes, gated communities, etc.) are investing in passive infrastructure (wiring, server enclosures, power, distributed antenna, conduit, etc.) and active infrastructure (servers, WiFi connectivity, etc.) that may be shared with end-user tenants and wide-area service providers. The range of potential “end-users” that may be deploying equipment and control resources that are necessary for or can contribute to supporting 5G+ networks and services is incredibly diverse; their motivations for investing in the digital and non-digital resources are equally diverse. In the case of many consumers and business end-users, the motivation for investing in and controlling the relevant resources may be for private ends, whereas for others (e.g., antenna companies, neutral hosts, or real estate developers) the investments may be intended to support an IT service provider business. In either case, however, these entities represent non-traditional last-mile infrastructure resource providers.

18. ^The evolution toward programmable networks (e.g., via SDN and NFV; see also Footnote 11)—enabled by the shift from hardware to software-based functionality—has helped facilitate the reconfiguration of service provider core networks to allow those networks to reduce total costs (e.g., by realizing scale economies when a single software control platform can replace multiple distributed control platforms) and increase their ability to offer end-user customization services.

19. ^This pressure threatens the last-mile providers with losing control of value-added services and being reduced to commodity-service “dumb” connectivity pipes with most of the value-capture shifting to edge service providers of networks and higher-level content and application services. On the other hand, shifting a portion of the investment burden to end-users reduces the service provider costs and may facilitate additional service provider entry and/or improve the rate of return on the remaining service provider assets.

20. ^See Footnote 8.

21. ^That is, duplicative network investment is (partly) avoided by using under-utilized end-user owned equipment that exists or will exist regardless of whether the overall network ecosystem invests in operator owned or operator shared equipment.

22. ^The X may include energy grids, transportation systems, healthcare, supply chains, manufacturing, cities, etc.

23. ^For example, highly-interactive VR/AR applications for machine control (e.g., UAV navigation) or to enable acceptable end-user QoE (for seamless virtual-real world interactivity) may require applications capable of supporting millisecond latency that is impossible to deliver unless computing resources are locally available. Alternatively, thin-client IoT or Graphical User Interface (GUI) devices (e.g., Chromebooks) may need in-network computing resources locally available to support functionality that cannot be provided on-device because of device size, power, or other technical considerations. Such needs are drivers for the provision of Mobile Edge Computing (MEC; also: Multi-access Edge Computing) resources in future 5G small-cell base stations.

24. ^For example, the 5G standards being developed by 3GPP embrace service and network architectures that may make use of a wide range of wireless technologies, spanning many frequency bands (low, mid, and high-band spectrum), networking architectures (terrestrial and non-terrestrial networks, including UAV, High Altitude Platform Systems (HAPS), and satellite platforms), and spectrum resource management models (unlicensed to licensed spectrum).

25. ^Industry consolidation through mergers and acquisitions offer an alternative approach for service providers to realize the economic benefits of network sharing.

26. ^In the expanded world of 5G+ applications and use modalities, most of the last-hop connections will be wireless, using a wide array of wireless technologies operating over a wide array of distances. Increasingly, those last-hop wireless connections will be provided via base stations that are close to the end-user in physical space. The need to reuse scarce spectrum, respect tight electrical power budgets, and the expanded ability (and lower costs) of managing small-cell terrestrial networks are powerful techno-economic drivers for adopting these small cell (reduced coverage area per cell or base station) architectures. As the physical coverage area of the base station shrinks, the spectrum resources and number of end-users that need to be simultaneously supported by that base station shrinks also—meaning that the share of non-wireless (e.g., power, backhaul, etc.) and non-digital (e.g., site access) resources in cell provisioning costs increases. As these other resources rise in importance, so does the need to embrace novel resource sharing options for bundling and provisioning such resources to facilitate the efficient delivery of end-to-end services.

27. ^Co-specialization in this context means that the small cell and local infrastructure design and resource provision reflect the demands of a rather small number of end-users—single end-users make a difference. This stands in stark contrast to large area assets that provide services to large numbers of end-users and where aggregation leads to a situation in which a marginal user does not impact on network design or resource provision. Moreover, note that the end-user/owner of a cell could be a hotel operator or local business and so does not have to actually be the end-user who could be a residential homeowner, hotel guest, or employee.

28. ^The growth of softwarization and open standards-based, layered architectures has facilitated modularization.

29. ^See, for example, Paschos et al. (2018), Peterson et al. (2019), Satyanarayanan et al. (2019), or Gigis et al. (2021).

30. ^For example, different applications have very different traffic characteristics. Moreover, the use of those applications may differ across adjacent households, and even within a single household, over time at all time scales. For example, TV watching generates a lot of downstream traffic, video monitoring (e.g., for security or healthcare) generates a lot of upstream traffic, while video-conferencing or gaming is much more interactive and may generate a lot of traffic in both directions. For application responsiveness or other application-dependent requirements (e.g., affordability, availability, reliability, etc.), different (performance) requirements may be relevant.

31. ^However, this may not be the case if one particular application like Over-The-Top (OTT) video takes off, swamping the loads and shares of other types of traffic – what that might be is unknowable at this point. Ericsson (2022, p. 25) reports how video traffic is dominating global mobile data traffic (with a share of more than 70% of mobile traffic in 2022) and is expected to do so even more in the future. However, it needs to be noted that if such an application resembles a next-generation OTT entertainment application, it may be less worthy of public subsidy and protection than a Smart-X application. Examples of Smart-X applications that have the potential to deliver significant economic benefits may be realized across many sectors. For example, IHS (2017) estimated that the deployment of 5G could deliver upwards of $12 Trillion in global economic activity by 2035, spread across sectors as diverse as Agriculture to Manufacturing to Finance and Insurance (see IHS, 2017). For example, VR/AR applications could enable the creation of “digital twin” models of complex systems (factories, supply chains, hospitals, etc.) that could be used to support simulations to allow faster-than-real-time experimentation and pre-deployment testing (e.g., of software upgrades) that could reduce the likelihood of costly outages and accelerate the deployment of system improvements. IoT asset tracking applications could enhance the quality and reliability of global supply chains and network support for remote collaboration could facilitate better resource management and specialization. In another study, TMG-GSMA (2018) estimated that 5G applications using millimeter wave spectrum could add $565 billion to global GDP by 2034, with use cases ranging from VR and collaboration software tools, remote object manipulation, industrial automation, next generation transport connectivity, and ubiquitous high-speed broadband connectivity (TMG-GSMA, 2018, p. 8).

32. ^When selecting among products, end-users exercise their ability to choose whether (or not) to purchase a product, and in the event that they elect to purchase, they evaluate their product choices across multiple dimensions. Those dimensions include product features, price, and transaction terms. For example, an end-user may select a more (less) capable version of a product if the price difference justifies the trade-off. Other transaction terms like whether the transaction is for à la carte or bundled services, represents a short-term or long-term contract, and depending on the level of trust for the seller, may all factor into the end-user's choice considerations.

33. ^Economic theory is indeterminant as to what industry structure maximizes end-user choice. A monopolist may (or may not) provide a wider selection of products than a competitive industry, but offer less attractive pricing or other contracting terms.

34. ^For example, in selecting what programs to watch or news to read, many end-users prefer to rely on curation by service providers (e.g., broadcast channels or newspapers) or by end-user recommendations (aggregated by service providers) rather than their own individualized selection (e.g., on-demand selection).

35. ^A typical US household has four people; each of those may have multiple devices that may be differently connected or share connections to wider-area networks outside the home. To exemplify the sharing challenge, consider the following scenario: user#1 is engaged in a p2p multiplayer gaming application; user#2 is using a VR business app, and user#3 is a 3rd party roamer (e.g., taking advantage of Xfinity WiFi access provided by the homeowner and other local services).

36. ^For example, with the expansion of infrastructure for fueling electric vehicles (EVs), it is unclear how the underlying ICT infrastructure and power delivery infrastructure may be efficiently provided from a business perspective. The current model is for EVs to use existing Internet/telecoms infrastructure to communicate and control charging stations, but challenges of integrating EVs and electrification more generally with the integration of (locally generated) renewable energy may alter that balance. An example is the trend toward smart homes and smart energy grids (including prosumage in the context of microgrids).

37. ^The extent to which the customer may own or lease customer premise equipment from the provider varies. Modems are usually leased (although customers may sometimes provide their own modem, but often that is incapable of being used with another provider's network). Many times the modems include integrated WiFi access points, and in the case of some providers, both a WiFi access point that is dedicated for the subscriber's in-home private network and a second WiFi radio to support the service provider's roaming WiFi radio service (e.g., Comcast's Xfinity service). End-users may also self-provision other WiFi-related devices, PCs, and other devices (e.g., tablets or smartphones) which they use to access service provider services (e.g., broadband access, telephone, content, and applications).

38. ^It may depend on how co-specialized the assets are that end-users are required to invest in and the strength of complementarities this causes. One may purchase a razor and can only use the blades from the razor handle manufacturer. For that business model, razor/blade companies sell razors for much less than the cost, subsidizing the purchase of the handle, to lock in future blade purchases. But, whether or how much of a subsidy is provided, depends on the intensity of competition at the system level. When considering small cells, base stations that are not open, but are tied to a specific service provider's network may shift costs but restrict end-user choice. Small cells that are based on open source software with well-defined and open interfaces that are capable of supporting connectivity to multiple wireless networks and which may be switched between networks can facilitate both cost reallocation while preserving end-user choice (i.e., help minimize switching costs). Enabling such small-cell “portability” will help sustain competitive pressure in edge-networks, analogous to how eSIMs enable smartphone portability across service providers and number portability facilitates switching among service providers.

39. ^Lowering the investment cost burden for individual service providers reduces one source of an entry barrier.

40. ^See Lehr et al. (2015) for a discussion of the challenges of implementing effective disclosure and transparency rules in the Internet ecosystem, and Lehr (2012) regarding the measurement challenge that network measurement poses for policymakers.

41. ^Additionally, end-user organized edge networks are likely to be smaller than the service providers that are the usual focus of regulatory attention. The design of appropriate regulations should recognize that end-user networks may be less able to bear regulatory compliance obligations, and so burdensome disclosure, transparency reporting, licensing, or other costly obligations may pose significant entry barriers that would asymmetrically harm end-user participation.

Afraz, N., Slyne, F., Gill, H., and Ruffini, M. (2019). Evolution of access network sharing and its role in 5g networks. Appl. Sci. 9, 4566. doi: 10.3390/app9214566

American Tower (2020). U.S. Technology and 5G Update: Q2 2020. American Tower Investor Presentation.

Bauer, J. M., and Bohlin, E. (2022). Regulation and innovation in 5G markets. Telecommun. Policy 46, 102260. doi: 10.1016/j.telpol.2021.102260

Body of European Regulators for Electronic Communications (BEREC) (2018). BEREC Report on Infrastructure Sharing (BoR (18) 116). Available online at: https://www.berec.europa.eu/en/document-categories/berec/reports/berec-report-on-infrastructure-sharing (accessed March 28, 2023).

Body of European Regulators for Electronic Communications (BEREC) (2019). BEREC Common Position on Infrastructure Sharing (BoR (19) 110). Available online at: https://www.berec.europa.eu/en/document-categories/berec/regulatory-best-practices/common-approachespositions/berec-common-position-on-infrastructure-sharing (accessed March 28, 2023).

Body of European Regulators for Electronic Communications (BEREC) (2020). Summary Report on the Outcomes of Mobile Infrastructure Sharing Workshop (BoR (20) 240). Available online at: https://www.berec.europa.eu/en/document-categories/berec/reports/summary-report-on-the-outcomes-of-mobile-infrastructure-sharing-workshop (accessed March 28, 2023).

Body of European Regulators for Electronic Communications (BEREC) (2021). Report on the Diversification of the 5G Ecosystem (BoR (21) 160). Available online at: https://www.berec.europa.eu/en/document-categories/berec/reports/report-on-the-diversification-of-the-5g-ecosystem (accessed March 28, 2023).

Bouras, C., Ntarzanos, P., and Papazois, A. (2016). “Cost modeling for SDN/NFV based mobile 5G networks,” in 2016 8th International Congress on Ultra Modern Telecommunications and Control Systems and Workshops (ICUMT) (IEEE), 56–61. doi: 10.1109/ICUMT.2016.7765232

Ericsson (2022). Ericsson Mobility Report. Available online at: https://www.ericsson.com/4ae28d/assets/local/reports-papers/mobility-report/documents/2022/ericsson-mobility-report-november-2022.pdf (accessed March 28, 2023).

Gigis, P., Calder, M., Manassakis, L., Nomikos, G., Kotronis, V., Dimitropoulos, X., et al. (2021). Seven years in the life of Hypergiants' off-nets,” in Proceedings of the 2021 ACM SIGCOMM 2021 Conference (New York, NY: Association for Computing Machinery (ACM)), 516–533. doi: 10.1145/3452296.3472928

Grijpink, F., Ménard, A., Sigurdsson, H., and Vucevic, N. (2018). The Road to 5G: The Inevitable Growth of Infrastructure Cost (2018). The Road to 5G: The Inevitable Growth of Infrastructure cost. McKinsey Global Institute (MGI). Available online at: https://www.mckinsey.com/industries/technology-media-and-telecommunications/our-insights/the-road-to-5g-the-inevitable-growth-of-infrastructure-cost (accessed March 28, 2023).

GSMA (2023). The Mobile Economy 2023. Available online at: https://www.gsma.com/mobileeconomy/wp-content/uploads/2023/02/270223-The-Mobile-Economy-2023.pdf (accessed March 28, 2023).

IHS (2017). The 5G Economy: How 5G Technology Will Contribute to the Global Economy. IHS Economics and IHS Technology. Available online at: https://cdn.ihs.com/www/pdf/IHS-Technology-5G-Economic-Impact-Study.pdf (accessed March 28, 2023).

ITU-R (2015). IMT Vision–Framework and Overall Objectives of the Future Development of IMT for 2020 and Beyond. Rec. ITU-R M.2083-0; M Series: Mobile, Radiodetermination, Amateur and Related Satellite Services. International Telecommunications Union. Available online at: https://www.itu.int/dms_pubrec/itu-r/rec/m/R-REC-M.2083-0-201509-I!!PDF-E.pdf (accessed March 28, 2023).

Knieps, G., and Bauer, J. M. (2022). Internet of things and the economics of 5G-based local industrial networks. Telecommun. Policy 46, 102261. doi: 10.1016/j.telpol.2021.102261

Koratagere Anantha Kumar, S., and Oughton, E. (2022). Techno-economic assessment of 5G infrastructure sharing business models in rural areas (version 2). TechRxiv. [preprint]. doi: 10.36227/techrxiv.21258531.v1

Koutroumpis, P., Castells, P., and Bahia, K. (2021). To Share or Not to Share? The Impact of Mobile Network Sharing for Consumers and Operators (Working Paper No. 2021-9). Oxford Martin School. Available online at: https://www.oxfordmartin.ox.ac.uk/downloads/Network-Sharing.pdf (accessed March 28, 2023).

Lehr, W. (2012). Measuring the Internet: the data challenge (Digital Economy Working Paper 184). Organization for Economic Cooperation and Development (OECD).

Lehr, W. (2022). “5G and AI convergence, and the challenge of regulating smart contracts,” in Europe's Future Connected: Policies and Challenges for 5G and 6G Networks, eds E. Bohlin and F. Cappelletti [European Liberal Forum (ELF)], 72–80. Available online at: https://liberalforum.eu/publication/europes-future-connected-policies-and-challenges-for-5g-and-6g-networks/ (accessed March 28, 2023).

Lehr, W. E, Kenneally, and Bauer, S. (2015). “The road to an open internet is paved with pragmatic disclosure and transparency policies,” in TPRC 43: The 43rd Research Conference on Communication, Information and Internet Policy. doi: 10.2139/ssrn.2587718

Lehr, W. H., Clark, D. D., Bauer, S., Berger, A., and Richter, P. (2019). Whither the public internet? J. Inform. Policy 9, 1–42. doi: 10.5325/jinfopoli.9.2019.0001

Lehr, W. H., Queder, F., and Haucap, J. (2021). 5G: a new future for mobile network operators, or not? Telecommun. Policy 45, 102086. doi: 10.1016/j.telpol.2020.102086

Maier-Rigaud, F. P., Ivaldi, M., and Heller, C.-P. (2020). Cooperation Among Competitors: Network Sharing Can Increase Consumer Welfare. Available online at: https://ssrn.com/abstract=3571354 (accessed March 28, 2023).

Mölleryd, B. G., Markendahl, J., and Sundquist, M. (2014). “Is network sharing changing the role of mobile network operators?” in 25th European Regional Conference of the International Telecommunications Society (ITS). Available online at: http://hdl.handle.net/10419/101392 (accessed March 28, 2023).

Motta, M., and Tarantino, E. (2021). The effect of horizontal mergers, when firms compete in prices and investments. Int. J. Indus. Organiz. 78, 102774. doi: 10.1016/j.ijindorg.2021.102774

Oughton, E., and Frias, Z. (2018). The cost, coverage and rollout implications of 5g infrastructure in Britain. Telecommun. Policy 42, 636–652. doi: 10.1016/j.telpol.2017.07.009

Oughton, E., Lehr, W., Katsaros, K., Selinis, I., Bubley, D., and Kusuma, J. (2021). Revisiting wireless internet connectivity: 5g Vs Wi-Fi 6. Telecommun. Policy 45, 102127. doi: 10.1016/j.telpol.2021.102127

Oughton, E. J., Comini, N., Foster, V., and Hall, J. W. (2022). Policy choices can help keep 4G and 5G universal broadband affordable. Technol. Forecast. Soc. Change 176, 121409. doi: 10.1016/j.techfore.2021.121409

Pápai, Z., Csorba, G., Nagy, P., and McLean, A. (2020). Competition policy issues in mobile network sharing: a European perspective. J. Eur. Competit. Law Pract. 11, 346–359. doi: 10.1093/jeclap/lpaa018

Paschos, G. S., Iosifidis, G., Tao, M., Towsley, D., and Caire, G. (2018). The role of caching in future communication systems and networks. IEEE J. Select. Areas Commun. 36, 1111–1125. doi: 10.1109/JSAC.2018.2844939

Peterson, L., Anderson, T., Katti, S., McKeown, N., Parulkar, G., Rexford, J., et al. (2019). Democratizing the network edge. ACM SIGCOMM Comput. Commun. Rev. 49, 31–36. doi: 10.1145/3336937.3336942

Rendon Schneir, J., Konstantinou, K., Bradford, J., Zimmermann, G., Droste, H., Canto Palancar, R., et al. (2020). Cost assessment of multi-tenancy for a 5G broadband network in a dense urban area. Digital Policy Regul. Govern. 22, 53–70. doi: 10.1108/DPRG-10-2019-0086

Satyanarayanan, M., Gao, W., and Lucia, B. (2019). “The computing landscape of the 21st century,” in HotMobile' 19: Proceedings of the 20th International Workshop on Mobile Computing Systems and Applications [Association for Computing Machinery (ACM)], 45–50. doi: 10.1145/3301293.3302357

Shukla, A., and Stocker, V. (2019). “Navigating the landscape of programmable networks: looking beyond the regulatory status quo,” in TPRC47: The 47th Research Conference on Communication, Information and Internet Policy 2019. doi: 10.2139/ssrn.3427455

Sirbu, M., Lehr, W., and Gillett, S. (2006). Evolving wireless access technologies for municipal broadband. Govern. Inform. Quart. 23, 480–502. doi: 10.1016/j.giq.2006.09.003

Stocker, V. (2020). Innovative capacity allocations for All-IP networks: a network economic analysis of evolution and competition in the internet ecosystem. Nomos. doi: 10.5771/9783748902607

Stocker, V., Smaragdakis, G., and Lehr, W. (2020). The state of network neutrality regulation. ACM SIGCOMM Comput. Commun. Rev. 50, 45–59. doi: 10.1145/3390251.3390258

TMG-GSMA (2018). Study on Socio-Economic Benefits of 5G Services Provided in mmWave Bands [Study prepared by TMG Telecom January 2019 on behalf of GSMA]. GSMA. Available online at: https://www.gsma.com/spectrum/wp-content/uploads/2019/10/mmWave-5G-benefits.pdf (accessed March 28, 2023).

Weissberger, A. (2020). “EU Recommendations on very high capacity broadband network infrastructure and a joint approach to 5G rollouts,” in IEEE ComSoc Technology Blog. Available online at: https://techblog.comsoc.org/2020/09/21/eu-recommendations-on-very-high-capacity-broadband-network-infrastructure-joint-approach-to-5g-rollouts/ (accessed March 28, 2023).

Keywords: 5G, broadband, network sharing, next-generation networks, telecommunications, Internet, regulatory economics, policy

Citation: Lehr W and Stocker V (2023) Next-generation networks: Necessity of edge sharing. Front. Comput. Sci. 5:1099582. doi: 10.3389/fcomp.2023.1099582

Received: 15 November 2022; Accepted: 17 March 2023;

Published: 17 April 2023.

Edited by:

Pantelis Koutroumpis, University of Oxford, United KingdomReviewed by:

Toshiya Jitsuzumi, Chuo University, JapanCopyright © 2023 Lehr and Stocker. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: William Lehr, d2xlaHJAbWl0LmVkdQ==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.