Muhammad Awais

Muhammad Awais Naeem Ullah2

Naeem Ullah2

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Psychol. , 29 June 2022

Sec. Organizational Psychology

Volume 13 - 2022 | https://doi.org/10.3389/fpsyg.2022.884532

Corporate governance is a set of rules, regulations, procedures, processes, and practices through which an organization is controlled and directed. The present study aimed to examine the monitoring methods used in Islamic banking, including standardized measures for better performance, an individual’s aptitude towards Islamic financial markets, risk propensity, and the level of efficiency of the Islamic banking industry in Pakistan and Malaysia. There is room to improve monitoring systems for Islamic banking operations and standardized measures could improve efficiency, leading to more sustainable performance. The study uses a self-developed semi-structured scale based on literature and expert interviews, after content and context validity to gain a wide range of diverse information. In Pakistan and Malaysia, individuals’ perceptions are different because of differences in the banking environment and preferences. Eventually, the Islamic banking growth rate may differ in Pakistan and Malaysia. Thus, there should be regular monitoring to improve banking performance. Similarly, standardized measures for Islamic banking operations and governance performance in Pakistan and Malaysia will result in more sustainable performance. The antecedents of Islamic corporate governance could be improved to enhance banking performance, which helps individuals make decisions based on available product information. The business growth of the banking industry is based on convenient monitoring policies, standardized performance measures, and, most importantly, excellent corporate governance mechanisms. Improved monitoring measures will further enhance these business operations.

Private monitoring consists of two types, the first is external, which opines that monitoring is mainly a task of institutional investors (Mubeen et al., 2021a; Ge et al., 2022; Liu et al., 2022). The second is internal monitoring mechanisms, comprised of CEO and chairman separation of designation, independent board members, and an audit committee (Aqeel et al., 2021, 2022; Aman et al., 2022; Rahmat et al., 2022; Yao et al., 2022). The chief is on the Board of Directors (BOD) for the provision of the monitoring, controlling, and advisory commitments of the firm (Abbas et al., 2020; Mamirkulova et al., 2020; Mubeen et al., 2021b; Liu et al., 2022). They can build or deteriorate corporate governance (Balachandran and Williams, 2018). When BOD planning goes unexpectedly the company might enter into a state of bankruptcy (Mubeen et al., 2020; Wang et al., 2021; Fu, 2022). The BOD has the authority to fire a CEO if they do not comply with desires and expectations. Usually, the BOD fires an incompetent CEO based on soft information (Laux, 2008), which ideally results in the better performance of the firm (Khazaie et al., 2021; Paulson et al., 2021; Yoosefi Lebni et al., 2021; Li et al., 2022; Mamirkulova and Mi, 2022). BODs typically have two differing views: (1) Board capture means that the CEO can exert pressure on inside directors based on self-interest, which only maximizes the CEO’s well-being. (2) Conversely, the CEO might select internal directors based on maximizing the shareholders’ wealth because they are astute and connoisseurs of the internal affairs of a firm (Malik and Majeed, 2017; Irfan and Ali, 2019; Naveed et al., 2019; Shahzad and Malik, 2019; Ashraf et al., 2020).

As per Mollah and Zaman (2015), conventional banks (CBs) hire more internal CEOs than Islamic Banks (IBs; Abbas et al., 2019a, 2019b). The board of IBs takes more independent decisions than CBs. In non-Islamic boards, members tend to be more concerned with profit generation. Contrary to this, the independent directors of IBs are linked with a decline in the performance of the firm (Badar and Irfan, 2018; Ali, 2020; Ali et al., 2021; Zhu et al., 2021). The presence of multi-layer corporate governance in Islamic banks helps them to perform better than conventional banks (Elgattani and Hussainey, 2020). This also assists in the protection of shareholders. Board structure and CEO power also affect the performance of the firm (NeJhaddadgar et al., 2020; Azizi et al., 2021; Maqsood et al., 2021).

Banks with high individualism tend to have higher incentives but banks with high power hold less leverage (Zhang et al., 2012; Asad et al., 2017; Ahmad et al., 2021). As per Kutubi et al. (2018), board busyness has a U-shaped relationship with a bank’s risk and performance. The Brobdingnagian amount of losses reported are indicative of the performance of conventional banks and Islamic banks, and need to be analyzed, classified, reckoned, and identified for them to be managed effectively and efficiently.

As mentioned above, the better the audit committee the better the corporate governance (Abbas et al., 2019c, 2020; Asad et al., 2020). The BOD and management usually nominate audit committees with external directors to provide impartial and unbiased decisions to better the company (Haldar and Raithatha, 2017). Their main function is to oversee issues and help the BOD with financial management. One of its chief functions is to act as a bridge between the external auditor and company matters.

Since the inauguration of the Sarbanes Oxley Act (2002), there has been an enormous amount of external directors appointed to ensure transparency. External directors have more material effects than internal ones. Intense monitoring forces the CEO to share necessary information with the BOD. External directors do not face lawsuits when the company requires accounting restatements but there is a labor market penalty. Directors who play a vital role in different companies are busy and might attenuate governance to enhance CEO compensation, which is outright exploitation of a firm’s performance. On the other hand, busy directors are positively associated with new public firms.

CEO compensation plays a very important role in driving CSR (Peng, 2020) and controlling earning management (Park, 2017). Additionally, higher analyst coverage in terms of financial statements results in higher firm transparency and lower earnings management. Some authors (Winecoff, 2017; Thiemann et al., 2018; Tchamyou, 2021) outline that present data on bank governance is not sufficient to articulate a link between governance and global financial crises. Banks with shareholder-friendly boards face declining performance in global financial crises. Culture also plays a role in risk-taking and creates measurement complexities (Dubey et al., 2017). Shareholder wealth maximizes when in the terms of banks have higher inside shareholders, i.e., CEO and lesser franchise values.

This paper specifically targets Pakistan as a research medium and analyses to what extent Islamic finance interlinks with corporate governance. To find evidence of the links between Islamic laws and corporate governance, we examined examples from the banking and finance industries.

Although all the factors mentioned above have already been studied, they have not been considered in relation to the context of Pakistan and Pakistani culture. In the same way, there are similarities in performing operations, actions, and approaches to mitigating problems between conventional boards and Shariah Supervisory Boards (SSBs). Islamic banks perform their actions within the Islamic framework (Ahmed, 2011), but in Pakistan, banks tend to follow non-Islamic corporate governance regulations instead of the Islamic perspective. This does not signify that one of these structures is better than the other, as it depends upon culture, context, and religious beliefs. This paper substantiates that the “Anglo-Saxon model” (a capitalist model) of economics implements the stakeholder theory (a theory of organizational management and business ethics that accounts for numerous communities wedged by commercial entities like workers, dealers, native groups, creditors, and others) whilst considering how this theory is inherent and built into the framework of Islam. According to the Islamic framework, a company is culpable and accountable to society and stakeholders.

To critically analyze the organization of economic cooperation and development (OECD) within the Islamic context we found that there are similarities between conventional boards and SSB. When considering corporate governance in Pakistan it is unjust to compare it with the Anglo-Saxon model or structures in developed countries as, even though it is present in the constitution, corporate governance in Pakistan, is still in its initial stages. Differences, therefore, exist due to the novel structure of Pakistan and the old structures used in developed countries like the UK. For example, concepts of ownership structure, laws, and regulations, etc. To date, few codes have been extended in Pakistan regarding corporate governance, and the few that have tend to abide by the Anglo-Saxon model structure rather than Islamic.

This research is necessary to galvanize better corporate governance structures in Pakistan where, to date, there has been a lack of disclosure, transparency, and accountability, and alternative structures of corporate governance are needed. The present study explores the interlinking between Islamic laws and corporate governance in Pakistan, using examples from the banking and finance industries in both Pakistan and Malaysia.

The qualities and adeptness of corporate governance and audit committees along with previous literature inform this paper’s exploration of corporate governance and the roles and responsibilities of audit committees. Better corporate governance means that performance is also better because with better corporate governance shareholders and stakeholders are more satisfied. This eventually helps the firm to maximize its profits (Ramli and Ramli, 2016).

Discrepancies between actual and desired corporate governance are a vast issue (Mahrani and Soewarno, 2018; Jia et al., 2019). For instance, from the disclosure of financial reporting to audit committee oversight, there have been colossal discrepancies in economic downturns (Rahim et al., 2015). To scrutinize this we garnered facts about the composition and communication of audit committees.

Non-financial companies typically have high amounts of debt to pay and their corporate governance is also impaired (Mubeen et al., 2020; Nawaz et al., 2020). Maximum ownership usually resides within families, meaning the decisions of the firm serve their personal interests (Abbas et al., 2019d; Aman et al., 2019; Zhou et al., 2022), ultimately this can undermine the interests of minority shareholders. In contrast, the sole purpose of Shariah-compliant firms (SCFs) is that they are governed by the sovereign power of “Allah.” This is a driving force for SCFs to act ethically and as per the stipulated and articulated Islamic principles (Imamah et al., 2019). This requires self-monitoring because, at the end of the day, managers are solely accountable to the power of accountable to Allah (SWT).

The effect of religion on economy and decision-making has been thoroughly researched by Max Weber. This research compared two branches of Christianity, exploring Protestant beliefs and Catholicism. According to this research, the preaching of Catholics is associated with the growth of the economy. In the same way, some studies (Bello and Bello, 2017; Elnahas et al., 2017; Belligni, 2019) show a direct and positive relationship between religion and economic boom. A number of studies (Li et al., 2019; Davis and Renzetti, 2021) have asserted that companies founded by religious people take less risk. In the same way, companies that reside in religious areas tend to take fewer risks. Nevertheless, companies established in areas where activities such as gambling take place tended to be innovative (Jang et al., 2017). In the same way, religious employees tend to disallow and have a strong anathema to manipulating accounts, value-destroying behavior, and aggressive accruals.

Islamic finance has been in accretion ever since the UK announced that it would provide Islamic bonds. These bonds were floated in places such as Singapore and Hong Kong. These assets doubled between 2003 to 2013. This colossal increase in Islamic finance warrants further academic research, which is chiefly possible due to data availability. The availability of data, however, can result in a blinkered perspective, as one cannot see the full picture of Islamic finance beyond banking.

A study of 21 Gulf countries shows that Shariah Supervisory Boards (SSBs) disclosed more social activities than annual reports (Mallin et al., 2014). Social and ethical activity creates goodwill and is as significant as the financial performance of the firm. Nonetheless, empirical findings assert that there is a neutral relationship between these two. This is due to profit and loss sharing, as banks may pay zakat on behalf of their customers and Qard Hassan may also be provided to benefit society. According to slack resource theory, the relationship between CSR-FP is the inverse of “FP-CSR.” This is substantiated by firms that have higher financial performance, which tend to spend a higher amount of slack resources on CSR activities. This will assist in enabling better social performance management.

Based on this social performance management, Islamic banks have expanded their assets to around US$1.3 trillion, indicating that it is a fast-growing industry (Neifar and Jarboui, 2018). This shows its importance in the international financial system. Islamic banks have a domineering effect on the entire Islamic financial industry due to their high amount of assets. Thus, the disclosure of operational risk is cardinal to Islamic banking operations. This also assists in ameliorating the information asymmetry in the firm.

Alhammadi et al. (2020) state that the biggest risk for Islamic Financial Institutions (IFI) is margin risk, followed by operational risk. The former risk is instigated due to poor human resource strategies and poor systematic legislation.

Comprehensive tests were undertaken to explore how Islamic finance is being proliferated all around the globe. In particular, we explored how it has been used by international governments and firms, especially in second-world countries (Alzahrani, 2019). Even though Islamic (academic) research is often skeptical about following and accepting Islamic finance as a subject matter of empirical and theoretical analysis, the establishment of a journal of corporate finance will certainly highlight practicalities for corporate managers and demonstrate the functioning and well-developed state of Islamic finance.

Islamic banks are 4 percentage points better off than conventional banks in terms of being cost-efficient. However, they are 17 percent less profit efficient (Safiullah and Shamsuddin, 2019). Studies have shown that the comparison of conventional and Islamic banks has been a topic under discussion in recent years. Ali and Azmi (2016) argue that conventional banks should be supplanted by Islamic banks outright because conventional banks show no more or less recuperation in financial crises, whilst Islamic banks exhibit more resilience during the interim. However, religion is the sole catalyst of innovation and risk-taking decisions (Torlak et al., 2021). Financial statements are a judgmental elements (based on which you can take investment decisions) as religious people sometimes morally object to the account’s manipulation (window dressing).

Socially responsible investment (SRI) is an important aspect of Islamic banking. SRI has become important in the last few years and these types of investments have certainly increased by 9% (Azmi et al., 2019). Islamic finance has increased during these years but is also gradually decreased in some respects. This happened because Islamic fund managers had an advantage by screening Shariah-compliant equity funds. SRI disallows un-Islamic investments, for instance, investment in weapons and gambling, etc. This puts limitations on Shariah-compliant assets.

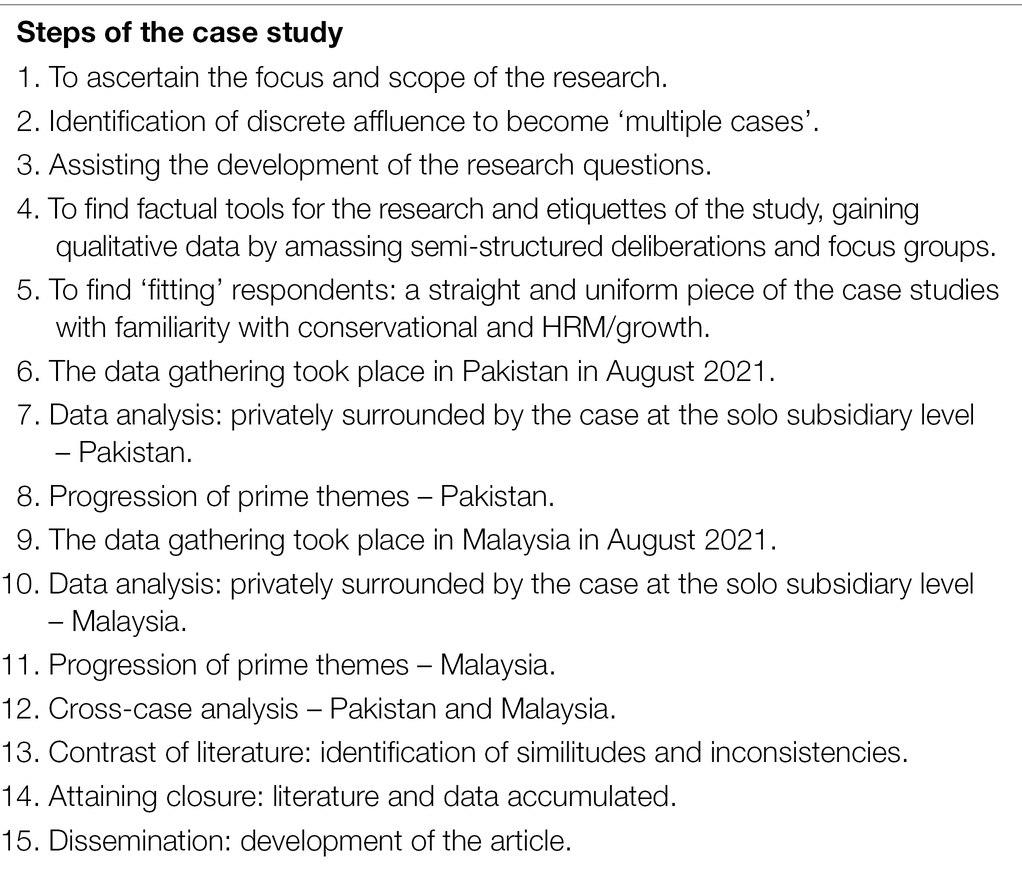

This study used an interview-based multi-case study technique (Eisenhardt, 1989; Eisenhardt and Graebner, 2007), in which shreds of evidence were collected via semi-structured deliberations to gain information and statistics apropos the sustainability and efficiency of the governance system of banks. In this paper, a qualitative technique was used to receive answers from interviewees. No quantifiable information was provided before the study and no evaluation of prospective responses was shared (Aqeel et al., 2021; Farzadfar et al., 2022). The numerous cases offer insights into central businesses through the close inspection of themes and proof. The case study decorum (Haddock-Millar et al., 2016) is outlined in Table 1.

Table 1. Case study protocol.

The discussions related to the theme of the study – the monitoring and efficiency in governance systems – and measure sustainability in the banking sector. This study uncovered diverse angles that were situation-specific, allowing for a proportional analysis of approaches to and the practice of Islamic Capitalism towards enhancing the growth of Islamic Finance.

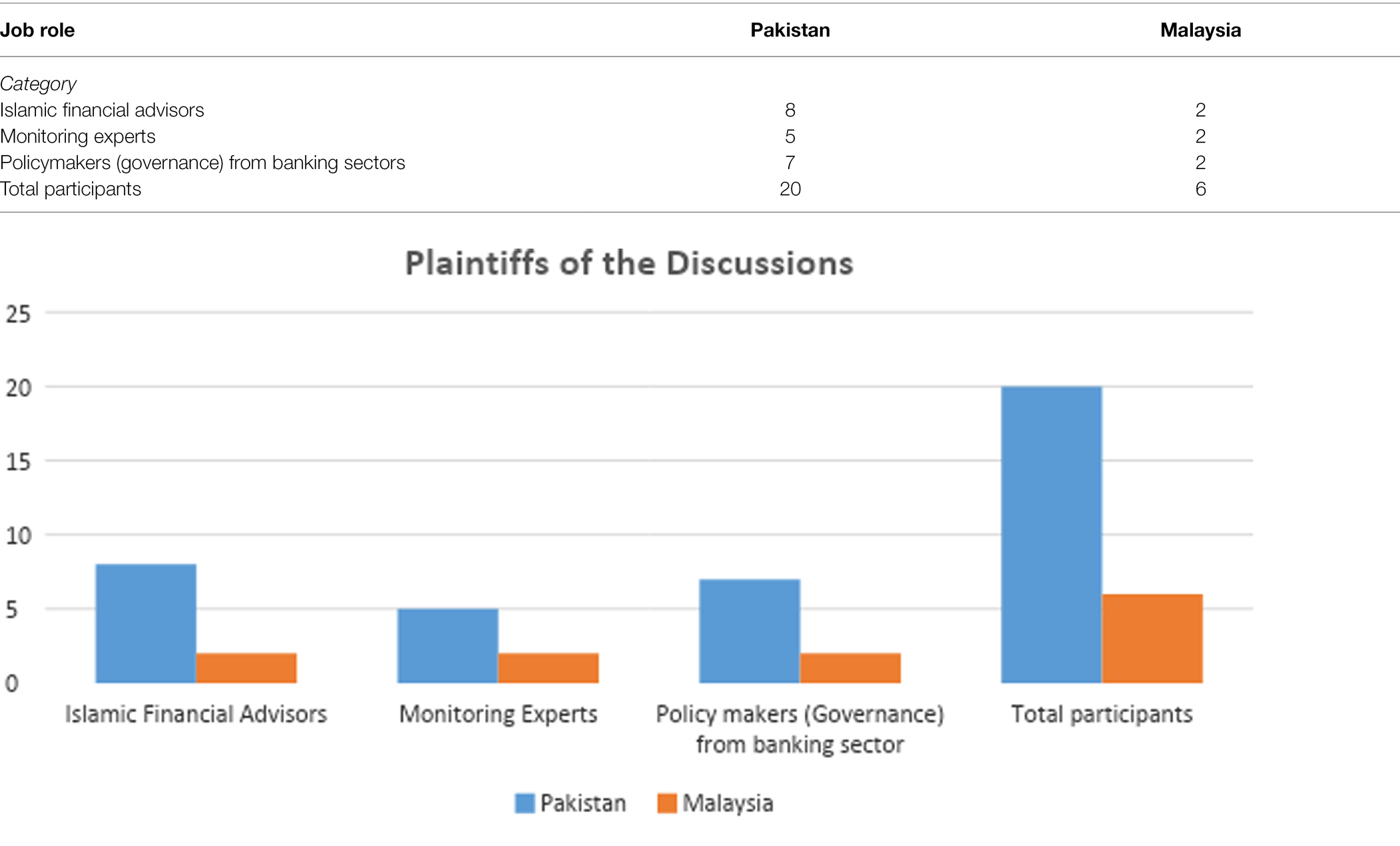

Interviewees included Islamic financial advisors, monitoring experts, and policymakers (governance) from the banking sectors of Pakistan and Malaysia. Semi-structured meetings were used to direct discussions and gain in-depth information. In total, the study arranged 26 interviews – 18 frontal and 8 through an open-ended scale (Table 2), however, only 21 participants provided all-inclusive and sound replies as per the prerequisite of the study.

Table 2. Plaintiffs of the discussions.

Table 2: Job Roles. This table speculates that whole contributors have excessive data concerning Shariah-based speculation and tradeoff practices and processes, and the wide-ranging ups and downs of the market.

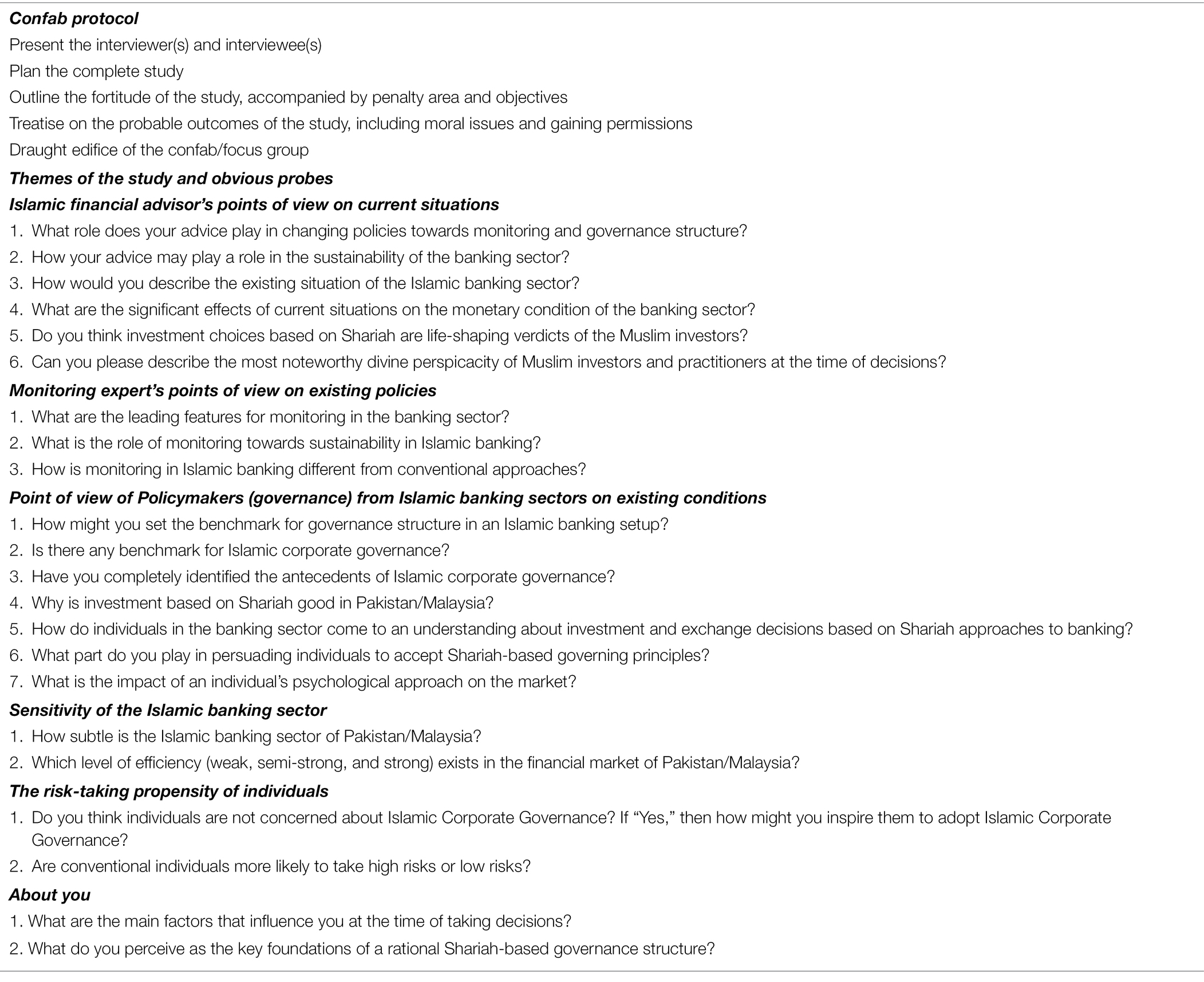

The focal confab questions (questions asked during an interview) were taken from literature on the extent of Islamic monitoring and governance systems and the sustainability of the Islamic banking sector. The confab questions are provided in Table 3.

Table 3. Confab protocol and probes.

The confab involved a dialogue on the Islamic monitoring system in the market, the life-shaping decisions of Muslim investors through Shariah-based governance practices, executives and practitioner psychosomatic intuitions, the sensitivity of the banking sector, and the daring propensity of persons in the marketplace. The confabs then explored the areas discussed in the literature, on the practice of Shariah-based approaches to monitoring and governance. The frontal confabs (forward discussions) lasted between 30 and 50 min and up to 60 min for each individual.

Corporate governance is a set of rules that an organization follows to mitigate fraudulent activities. These are the internal and external affairs of an organization and environmental factors that influence the decisions of an enterprise. To assimilate corporate governance in terms of financial performance, we first need to shed light upon the strengths of corporate governance (Liu et al., 2022). Corporate governance strength is underscored by corporate governance disclosure, and the present study provides advice for policy setting as per these standards.

Individuals and investors have different individual perceptions of the existing situation in the banking sector. The implementation of corporate governance varies across borders. This means that corporate governance needs to be implemented differently in different regions.

Despite the six principles of the Organization of Economic Cooperation and Development (OECD) there are still differences in perception across different countries, for example in the USA and Saudi Arabia. The establishment of corporate governance was initiated in the USA and then it shifted to the United Kingdom. It was initially an Anglo-American process. The exact definition of corporate governance had not been previously formulated. Therefore, researchers usually related agency cost theory with corporate governance and consider Anglo-American and continental European corporate governance comparable. The use of various models may give diverse returns in various circumstances. Moreover, most Muslims invest as per the religious teachings on investment because they want to secure their life after death, and people often think that investment as per Shariah principles will efficiently change their life.

Corporate governance gains new dimensions when based on the Islamic rules of the sovereignty of Allah Almighty and with the belief that Prophet Muhammad S.A.W is the last messenger. Islam creates a context of reference and rules from the perspective of the teachings of the Quran and Sunnah. The amalgamation started after the Sarbanes Oxley act when Tyco international showed its dark colors with fraudulent activities. In the conventional banking sector, interest rates, yield curves, and net interest margins for the state of the economy are gaged by GDP growth, employment growth, inflation, and currency fluctuations, which are considered the main aspects in terms of monitoring. By contrast, in Islamic banking, employment growth, inflation, and currency fluctuations are commonly monitored.

Islam and corporate governance are two distinct areas. The former is related to religious perspective and the latter is related to organizational orientation. This provides a new dimension to the corporate world. Although there has been a preponderance of studies that show agency costs are mitigated with better corporate governance, according to the Islamic perspective, the agency cost seems to diminish. This is theoretical and has not been empirically proven to date. Although the presence of corporate governance is supposed to benefit shareholders through procedural rules and principles, the companies still faced a huge disaster in the 1990s and early 2000s due to the high salaries of strategic managers (Erturk et al., 2004). It is important that monitoring is undertaken on a timely and regular basis, meaning the controlling authority can track planning and the use of the resources. It offers decision-makers an approach to sustainably planning for ventures and future actions. Moreover, monitoring criteria are usually based on the operational activities of the organization, but most of the determinants are common in all the subjects.

Corporate governance exists on two levels; it is either poor or good. Traditional wisdom is associated with corporate governance. It is engendered in such a way that explains the cause and effect of corporate governance with competition in firms and different industries operating under a single economy.

As per the governance methods, corporate governance has different definitions according to different authors. However, we can define corporate governance as an outright set of responsibilities that are shared among a board of directors to shield the rights of shareholders and stakeholders (Robertson et al., 2013). With its definition come the ties of Islam within Islamic institutions. For example, Islamic principles-based banks. Their operationalizing is different from conventional banks because of the addition of one religious element, EG Islam in terms of the Sunnah, Shariah, Quran, and teachings of the Prophet Muhammad (S.A.W). Moreover, it is extremely difficult to explore the complete antecedents of Islamic corporate governance.

In response to the many determinants of corporate governance, let us lucubrate the amalgamation of Islam with corporate governance and its determinants. Keeping corporate governance under, Islamic laws, principles, Shariah, Quran, and Sunnah are beneficial for a firm, enabling it to have a better grip on decision making. Islam has its rulings, which are further divided into worshipping (Allah is the only sovereign power) and Muamlaat, also known as mutual dealings between two parties. This helps to mitigate agency costs that are solely based upon agent and principal self-interests. Muamlaat has further polythetic characteristics known as the “Doctrine of Universal Permissibility,” which means that the two parties can enter a contract without having to sacrifice the Shariah principles. Furthermore, the implementation of ICG means that the views of traditionalists and the views of modernists have to be taken into account for the sake of implementation of ICG. Traditionalists have antithetical views concerning modernists. Traditionalists make use of Ijtihad to interpret the teachings of the Quran and Sunnah in the best way possible. The collaboration of Islamic scholars and financial secular experts would push technical advancements in banking.

Western models of capitalism are vastly different from Islamic capitalism because Islamic capitalism is based upon Islamic finance and the rulings of the Quran and Sunnah. As soon as Islamic finance emerged, there was a need for Islamic corporate governance to follow the rules as per Islamic principles. Corporate governance means to “check and balance a firm’s operations.” It helps to mitigate principal-agent theory, which has long been discussed under corporate governance as it determines the antecedents and compliance with ICG as per the policies set forth by the directors (agents).

Every individual in the market may affect the movements and returns of the market in the least manner. It is beneficial for investors to invest as per the rules of Shariah, because the biggest advantage is risk-sharing, which may lead to the mitigation of losses in most cases.

Islamic banking is less sensitive compared to conventional banking, because conventional banking faces the risks of interest rates, whereas, there is no concept of interest rate risk in Islamic banking. Conventional banking has credit risk usually in cash form; on the other hand, Islamic banking has credit risk in the form of assets/products.

Like all other sectors, Islamic banking is not fully efficient in Pakistan, as it is in the growth phase. By contrast, in Malaysia, Islamic banking is efficient as its growth rate is higher than conventional banking. It is significant that non-Muslims also prefer to be part of Islamic banking instead of conventional banking, as they know about the benefit of risk-sharing in any sort of investment.

Most of the individuals in Pakistan who are aware of Islamic banking must know about the governance mechanism of that place. Those who are unaware, want to learn about it. In Malaysia, almost all the individuals are keen to know about the governance mechanism, as they are open to investing after knowing more about it.

Many individuals in the Islamic banking sector also think they are in a safe position compared to people who are attached to conventional banking, as they are in a position of risk-sharing instead of risk gain or loss on an individual basis.

According to this study, we can infer that a dearth of independent audit committees and an inefficient corporate governance structure enable fraudulent companies to operate without monitoring activities. For example, if audit committees are dependent and influenced by internal auditors then all the decisions taken create a predilection for self-interest and fraudulent activities.

Keeping the literature in mind we can accept the fact that the gap exists. The process of creating financial instruments means that they should be inimitable and they should not be simply copied from conventional products. They ought to have a competitive edge over conventional finance. The gap also exists in that there is no standardized Islamic finance across borders as there are no sharia standards in national legislation. Some Muslim countries follow Islamic corporate governance models and some of them do not. Take as an example Malaysia, which follows it, and a country such as Saudi Arabia, which is under huge debt and does not abide by the laws of Islam.

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

All authors contributed to this study as per their area of expertise.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Abbas, J., Aman, J., Nurunnabi, M., and Bano, S. (2019a). The impact of social media on learning behavior for sustainable education: evidence of students from selected universities in Pakistan. Sustainability 11:1683. doi: 10.3390/su11061683

Abbas, J., Hussain, I., Hussain, S., Akram, S., Shaheen, I., and Niu, B. (2019b). The impact of knowledge sharing and innovation upon sustainable performance in Islamic banks: a mediation analysis through an SEM approach. Sustainability 11:4049. doi: 10.3390/su11154049

Abbas, J., Mahmood, S., Ali, H., Ali Raza, M., Ali, G., Aman, J., et al. (2019c). The effects of corporate social responsibility practices and environmental factors through a moderating role of social media marketing on sustainable performance of business firms. Sustainability 11:3434. doi: 10.3390/su11123434

Abbas, J., Raza, S., Nurunnabi, M., Minai, M. S., and Bano, S. (2019d). The impact of entrepreneurial business networks on firms’ performance through a mediating role of dynamic capabilities. Sustainability 11:3006. doi: 10.3390/su11113006

Abbas, J., Zhang, Q., Hussain, I., Akram, S., Afaq, A., and Shad, M. A. (2020). Sustainable innovation in small medium enterprises: the impact of knowledge management on organizational innovation through a mediation analysis by using SEM approach. Sustainability 12:2407. doi: 10.3390/su12062407

Ahmad, N., Naveed, R. T., Scholz, M., Usman, M., and Ahmad, I. (2021). CSR communication through social media: A litmus test for banking consumers’ loyalty. Sustainability 13:2319. doi: 10.3390/su13042319

Ahmed, A. S. (2011). An examination of the principles of corporate governance from an Islamic perspective: evidence from Pakistan. Arab Law Q. 25, 27–50. doi: 10.1163/157302511X540826

Alhammadi, S., Archer, S., and Asutay, M. (2020). Risk management and corporate governance failures in Islamic banks: a case study. J. Islam. Account. Bus. Res. 11, 1921–1939. doi: 10.1108/JIABR-03-2020-0064

Ali, M. H., Irfan, M., and Zafar, S. (2021). Effect of leadership styles on education quality in public universities with the interaction of organizational politics: using the partial Least Square algorithm. J. Soc. Sci. Humanities 1, 1–13. doi: 10.53057/josh/2021.1.2.1

Ali, M., and Azmi, W. (2016). Religion in the boardroom and its impact on Islamic banks’ performance. Rev. Financ. Econ. 31, 83–88. doi: 10.1016/j.rfe.2016.08.001

Ali, R. A. (2020). The impact of corporate governance, fundamental and macroeconomic factors on stock prices: an evidence from sugar and allied industry of Pakistan. Int. J. Enterp. Inf. Syst. 40, 1329–1341.

Alzahrani, M. (2019). Islamic corporate finance, financial markets, and institutions: an overview. J. Corp. Finan. 55, 1–5. doi: 10.1016/j.jcorpfin.2018.11.008

Aman, J., Mahmood, S., Nurunnabi, M., and Bano, S. (2019). The influence of Islamic religiosity on the perceived socio-cultural impact of sustainable tourism development in Pakistan: a structural equation modeling approach. Sustainability 11:3039. doi: 10.3390/su11113039

Aman, J., Shi, G., Ain, N. U., and Gu, L. (2022). Community wellbeing Under China-Pakistan economic corridor: role of social, economic, cultural, and educational factors in improving residents’ quality of. Life. 12:816592. doi: 10.3389/fpsyg.2021.816592

Aqeel, M., Abbas, J., Raza, S., and Aman, J. (2021). Portraying the multifaceted interplay between sexual harassment, job stress, social support and employees turnover intension amid COVID-19: a multilevel moderating model. Found. Univ. J. Bus. Econ. 6, 1–17.

Aqeel, M., Rehna, T., and Shuja, K. H. (2022). Comparison of students' mental wellbeing, anxiety, depression, and quality of life during COVID-19's full and partial (smart) lockdowns: a follow-up study at a five-month interval. Front. Psych. 13:828040. doi: 10.3389/fpsyg.2022.828040

Aqeel, M., Shuja, K. H., Rehna, T., Ziapour, A., Yousaf, I., and Karamat, T. (2021). The influence of illness perception, anxiety and depression disorders on students mental health during COVID-19 outbreak in Pakistan: a web-based cross-sectional survey. Int. J. Hum. Rights in Healthcare 15, 17–30. doi: 10.1108/ijhrh-10-2020-0095

Asad, A., Abbas, J., Irfan, M., and Raza, H. M. A. (2017). The impact of HPWS in organizational performance: a mediating role of servant leadership. J. Manag. Sci. 11, 25–48.

Asad, A., Basheer, M. F., Jiang, J., and Tahir, R. (2020). Open-innovation and knowledge management in small and medium-sized enterprises (SMEs): The role of external knowledge and internal innovation. Rev. Argentina Clín. Psicol. 29, 80–90.

Ashraf, M. S., Akhtar, N., Ashraf, R. U., Hou, F., Junaid, M., and Kirmani, S. A. A. (2020). Traveling responsibly to ecofriendly destinations: an individual-level cross-cultural comparison between the United Kingdom and China. Sustainability 12:3248. doi: 10.3390/su12083248

Azizi, M. R., Atlasi, R., Ziapour, A., and Naemi, R. (2021). Innovative human resource management strategies during the COVID-19 pandemic: a systematic narrative review approach. Heliyon 7:e07233. doi: 10.1016/j.heliyon.2021.e07233

Azmi, W., Ng, A., Dewandaru, G., and Nagayev, R. (2019). Doing well while doing good: The case of Islamic and sustainability equity investing. Borsa Istanbul Rev. 19, 207–218. doi: 10.1016/j.bir.2019.02.002

Badar, M. S., and Irfan, M. (2018). Shopping mall services and customer purchase intention along with demographics. J. Mark. Focus. Manag.

Balachandran, B., and Williams, B. (2018). Effective governance, financial markets, financial institutions & crises. Pac. Basin Financ. J. 50, 1–15. doi: 10.1016/j.pacfin.2018.07.006

Belligni, E. (2019). Between Religion and Economics: Towards A Shift of Paradigm In Early Modern Economic Literature. CINECA IRIS Institutional Research Information System - Universita Degli Studi Di Torino.

Bello, Y. O., and Bello, M. P. (2017). Exploring the relationship between religion tourism and economic development of a host community. Int. J. Bus. Manag. Invent. 6, 41–51.

Davis, R. E., and Renzetti, C. M. (2021). Is religious self-regulation a risk or protective factor for men’s intimate partner violence perpetration? J. Interpers. Violence. doi: 10.1177/0886260520985497

Dubey, R., Gunasekaran, A., Childe, S. J., Papadopoulos, T., Hazen, B., Giannakis, M., et al. (2017). Examining the effect of external pressures and organizational culture on shaping performance measurement systems (PMS) for sustainability benchmarking: Some empirical findings. Int. J. Prod. Econ. 193, 63–76. doi: 10.1016/j.ijpe.2017.06.029

Eisenhardt, K. M. (1989). Making fast strategic decisions in high-velocity environments. Acad. Manag. J. 32, 543–576.

Eisenhardt, K. M., and Graebner, M. E. (2007). Theory building from cases: opportunities and challenges. Acad. Manag. J. 50, 25–32. doi: 10.5465/amj.2007.24160888

Elgattani, T., and Hussainey, K. (2020). The impact of AAOIFI governance disclosure on Islamic banks performance. J. Financ. Report. Account. 18, 1–18. doi: 10.1108/JFRA-03-2019-0040

Elnahas, A. M., Hassan, M. K., and Ismail, G. M. (2017). Religion and ratio analysis: towards an Islamic corporate liquidity measure. Emerg. Mark. Rev. 30, 42–65. doi: 10.1016/j.ememar.2016.09.001

Erturk, I., Froud, J., Johal, S., and Williams, K. (2004). Corporate governance and disappointment. Rev. Int. Polit. Econ. 11, 677–713. doi: 10.1080/0969229042000279766

Farzadfar, F., Naghavi, M., Sepanlou, S. G., Saeedi Moghaddam, S., Dangel, W. J., Davis Weaver, N., et al. (2022). Health system performance in Iran: a systematic analysis for the global burden of disease study 2019. Lancet 399, 1625–1645. doi: 10.1016/s0140-6736(21)02751-3

Fu, Q. (2022). Reset the industry redux through corporate social responsibility: The COVID-19 tourism impact on hospitality firms through business model innovation. Front. Psychol. 12:795345. doi: 10.3389/fpsyg.2021.795345

Ge, T., Ullah, R., Abbas, A., Sadiq, I., and Zhang, R. (2022). Women’s entrepreneurial contribution to family income: innovative technologies promote females’ entrepreneurship Amid COVID-19 crisis. Front. Psychol. 13. doi: 10.3389/fpsyg.2022.828040

Haddock-Millar, J., Sanyal, C., and Müller-Camen, M. (2016). Green human resource management: a comparative qualitative case study of a United States multinational corporation. Int. J. Hum. Resour. Manag. 27, 192–211. doi: 10.1080/09585192.2015.1052087

Haldar, A., and Raithatha, M. (2017). Do compositions of board and audit committee improve financial disclosures? Int. J. Organ. Anal. 25, 251–269. doi: 10.1108/IJOA-05-2016-1030

Imamah, N., Lin, T. J., Handayani, S. R., and Hung, J. H. (2019). Islamic law, corporate governance, growth opportunities and dividend policy in Indonesia stock market. Pac. Basin Financ. J. 55, 110–126. doi: 10.1016/j.pacfin.2019.03.008

Irfan, M., and Ali, M. H. (2019). Attitude of customers towards adopting of mobile banking (M-Banking an empirical study from Pakistan). Innovative Syst. Des. Eng. 10, 30–33.

Jang, S., Kim, J., and von Zedtwitz, M. (2017). The importance of spatial agglomeration in product innovation: a microgeography perspective. J. Bus. Res. 78, 143–154. doi: 10.1016/j.jbusres.2017.05.017

Jia, N., Huang, K. G., and Man Zhang, C. (2019). Public governance, corporate governance, and firm innovation: an examination of state-owned enterprises. Acad. Manag. J. 62, 220–247. doi: 10.5465/amj.2016.0543

Khazaie, H., Lebni, J. Y., Mahaki, B., Chaboksavar, F., Kianipour, N., and Ziapour, A. (2021). Internet addiction status and related factors among medical students: a cross-sectional study in Western Iran. Int. Q. Community Health Educ. :272684X211025438. doi: 10.1177/0272684X211025438

Kutubi, S. S., Ahmed, K., and Khan, H. (2018). Bank performance and risk-taking—does directors' busyness matter? Pac. Basin Financ. J. 50, 184–199. doi: 10.1016/j.pacfin.2017.02.002

Laux, V. (2008). Board independence and CEO turnover. J. Account. Res. 46, 137–171. doi: 10.1111/j.1475-679X.2008.00269.x

Li, C., Xu, Y., Gill, A., Haider, Z. A., and Wang, Y. (2019). Religious beliefs, socially responsible investment, and cost of debt: evidence from entrepreneurial firms in India. Emerg. Mark. Rev. 38, 102–114. doi: 10.1016/j.ememar.2018.12.001

Li, Z., Wang, D., Hassan, S., and Mubeen, R. (2022). Tourists’ health risk threats amid COVID-19 era: role of technology innovation, transformation, and recovery implications for sustainable tourism. Front. Psychol. 12:769175. doi: 10.3389/fpsyg.2021.769175

Liu, Q., Qu, X., Wang, D., and Mubeen, R. (2022). Product market competition and firm performance: business survival Through innovation and entrepreneurial orientation Amid COVID-19 financial. Crisis 12:790923. doi: 10.3389/fpsyg.2021.790923

Mahrani, M., and Soewarno, N. (2018). The effect of good corporate governance mechanism and corporate social responsibility on financial performance with earnings management as mediating variable. Asian. J. Account. Res. 3, 41–60. doi: 10.1108/AJAR-06-2018-0008

Malik, M. S., and Majeed, S. M. (2017). Impact of IT investment on productivity of manufacturing organizations: evidence from textile sector of Pakistan. South Asian J. Banking Soc. Sci. 2, 75–87.

Mallin, C., Farag, H., and Ow-Yong, K. (2014). Corporate social responsibility and financial performance in Islamic banks. J. Econ. Behav. Organ. 103, S21–S38. doi: 10.1016/j.jebo.2014.03.001

Mamirkulova, G., and Mi, J. (2022). Economic corridor and tourism sustainability amid unpredictable COVID-19 challenges: assessing community well-being in the world heritage sites. Front. Psychol. 12:797568. doi: 10.3389/fpsyg.2022.797568

Mamirkulova, G., Mi, J., Mahmood, S., Mubeen, R., and Ziapour, A. (2020). New silk road infrastructure opportunities in developing tourism environment for residents better quality of life. Global Ecol. Conserv. 24:e01194. doi: 10.1016/j.gecco.2020.e01194

Maqsood, A., Rehman, G., and Mubeen, R. (2021). The paradigm shift for educational system continuance in the advent of COVID-19 pandemic: mental health challenges and reflections. Curr. Res. Behav. Sci. 2:100011. doi: 10.1016/j.crbeha.2020.100011

Mollah, S., and Zaman, M. (2015). Shari’ah supervision, corporate governance and performance: conventional vs. Islamic banks. J. Bank. Financ. 58, 418–435. doi: 10.1016/j.jbankfin.2015.04.030

Mubeen, R., Han, D., and Hussain, I. (2020). The effects of market competition, capital structure, and CEO duality on firm performance: a mediation analysis by incorporating the GMM model technique. Sustainability 12:3480. doi: 10.3390/su12083480

Mubeen, R., Han, D., and Raza, S. (2021a). Examining the relationship between product market competition and Chinese firms performance: the mediating impact of capital structure and moderating influence of firm size. Front. Psychol. 12. doi: 10.3389/fpsyg.2021.709678

Mubeen, R., Han, D., Alvarez-Otero, S., and Sial, M. S. (2021b). The relationship Between CEO duality and business Firms' performance: the moderating role of firm size and corporate social responsibility. Front. Psychol. 12:669715. doi: 10.3389/fpsyg.2021.669715

Naveed, R. T., Aslam, H. D., Anwar, B., and Ayub, A. (2019). The effect of general banking information technology system on customers’ satisfaction with the moderating effect of customer trust: an empirical study from Pakistani commercial (Islamic) banks. Al-Qalam, 387–401.

Nawaz, K., Jan, F. A., and Shah, S. K. (2020). The role of managerial ability in firm investment opportunities and performance of non–financial firms, a mediating role of corporate governance. Global Econ. Rev. V, 309–324. doi: 10.31703/ger.2020(V-I).26

Neifar, S., and Jarboui, A. (2018). Corporate governance and operational risk voluntary disclosure: evidence from Islamic banks. Res. Int. Bus. Financ. 46, 43–54. doi: 10.1016/j.ribaf.2017.09.006

NeJhaddadgar, N., Ziapour, A., Zakkipour, G., Abolfathi, M., and Shabani, M. (2020). Effectiveness of telephone-based screening and triage during COVID-19 outbreak in the promoted primary healthcare system: a case study in Ardabil province. Iran. Z Gesundh Wiss 29, 1301–1306. doi: 10.1007/s10389-020-01407-8

Park, K. (2017). Pay disparities within top management teams and earning management. J. Account. Public Policy 36, 59–81. doi: 10.1016/j.jaccpubpol.2016.11.002

Paulson, K. R., Kamath, A. M., Alam, T., Bienhoff, K., Abady, G. G., and Kassebaum, N. J. (2021). Global, regional, and national progress towards sustainable development goal 3.2 for neonatal and child health: all-cause and cause-specific mortality findings from the global burden of disease study 2019. Lancet 398, 870–905. doi: 10.1016/s0140-6736(21)01207-1

Peng, C. W. (2020). The role of business strategy and CEO compensation structure in driving corporate social responsibility: linkage towards a sustainable development perspective. Corp. Soc. Responsib. Environ. Manag. 27, 1028–1039. doi: 10.1002/csr.1863

Rahim, M. F. A., Johari, R. J., and Takril, N. F. (2015). Revisited note on corporate governance and quality of audit committee: Malaysian perspective. Procedia Econ. Fin. 28, 213–221. doi: 10.1016/S2212-5671(15)01102-8

Rahmat, T. E., Raza, S., Zahid, H., Mohd Sobri, F., and Sidiki, S. (2022). Nexus between integrating technology readiness 2.0 index and students’ e-library services adoption amid the COVID-19 challenges: implications based on the theory of planned behavior. J. Educ. Health Promot. 11:50. doi: 10.4103/jehp.jehp_508_21

Ramli, J. A., and Ramli, M. I. (2016). Corporate governance and corporate performance of Malaysian companies: examining from an Islamic perspective. Procedia Econ. Fin. 35, 146–155. doi: 10.1016/S2212-5671(16)00019-8

Robertson, C. J., Diyab, A. A., and Al-Kahtani, A. (2013). A cross-national analysis of perceptions of corporate governance principles. Int. Bus. Rev. 22, 315–325. doi: 10.1016/j.ibusrev.2012.04.007

Safiullah, M., and Shamsuddin, A. (2019). Risk-adjusted efficiency and corporate governance: evidence from Islamic and conventional banks. J. Corp. Finan. 55, 105–140. doi: 10.1016/j.jcorpfin.2018.08.009

Shahzad, M., and Malik, M. S. (2019). Quality and customer loyalty in Islamic banks: religiosity as a moderator by using Andrew Hayes model. Int. J. Enterp. Inf. Syst. 7, 379–396.

Tchamyou, V. S. (2021). Financial access, governance and the persistence of inequality in Africa: mechanisms and policy instruments. J. Public Aff. 21:e2201. doi: 10.1002/pa.2201

Thiemann, M., Birk, M., and Friedrich, J. (2018). Much ado about nothing? Macro-prudential ideas and the post-crisis regulation of shadow banking. Kölner Z. Soz. Sozialpsychol. 70, 259–286. doi: 10.1007/s11577-018-0546-6

Torlak, N. G., Demir, A., and Budur, T. (2021). Decision-making, leadership and performance links in private education institutes. Rajagiri Manag. J.

Wang, C., Wang, D., Duan, K., and Mubeen, R. (2021). Global financial crisis, smart lockdown strategies, and the COVID-19 spillover impacts: a global perspective implications From Southeast Asia. Front. Psych. 12:643783. doi: 10.3389/fpsyt.2021.643783

Winecoff, W. K. (2017). Global finance as a politicized habitat. Bus. Polit. 19, 267–297. doi: 10.1017/bap.2017.7

Yao, J., Ziapour, A., Toraji, R., and NeJhaddadgar, N. (2022). Assessing puberty-related health needs among 10–15-year-old boys: a cross-sectional study approach. Arch. Pediatr. 29, 307–311. doi: 10.1016/j.arcped.2021.11.018

Yoosefi Lebni, J., Moradi, F., Salahshoor, M. R., Chaboksavar, F., Irandoost, S. F., Ziapour, A., et al. (2021). How the COVID-19 pandemic effected economic, social, political, and cultural factors: a lesson from Iran. Int. J. Soc. Psychiatry 67, 298–300. doi: 10.1177/0020764020939984

Zhang, Q., Khattak, M. A. O., Zhu, X., and Shah, M. S. (2012). Critical success factors for successful lean six sigma implementation in Pakistan. Interdiscip. J. Contemp. Res. Bus. 4, 117–124.

Zhou, Y., Draghici, A., Mubeen, R., Boatca, M. E., and Salam, M. A. (2022). Social media efficacy in crisis management: effectiveness of non-pharmaceutical interventions to manage COVID-19 challenges [conceptual analysis]. Front Psychiatry 12:626134. doi: 10.3389/fpsyt.2021.626134

Keywords: governance, sustainability, Islamic banking, Pakistan, Malaysia

Citation: Awais M, Ullah N, Sulehri NA, Thas Thaker MM and Mohsin M (2022) Monitoring and Efficiency in Governance: A Measure for Sustainability in the Islamic Banking Industry. Front. Psychol. 13:884532. doi: 10.3389/fpsyg.2022.884532

Edited by:

Muhammad Irfan, Bahauddin Zakariya University, PakistanReviewed by:

S. Bano, Shanghai University of Sport, ChinaCopyright © 2022 Awais, Ullah, Sulehri, Thas Thaker and Mohsin. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Muhammad Awais, bS5hd2Fpc0BmdWkuZWR1LnBr

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.