Qingrong Liu

Qingrong Liu Bilal

Bilal Bushra Komal3

Bushra Komal3

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Psychol. , 22 April 2022

Sec. Psychology of Language

Volume 13 - 2022 | https://doi.org/10.3389/fpsyg.2022.851405

This study presents a corpus-based comparison of the Chief Executive Officer (CEO) statements between annual reports and corporate social responsibility (CSR) reports. Using a corpus of 209 CEO statements from annual reports and CSR reports of Chinese companies, this study employs the Discourse-Historical Approach of critical discourse analysis to investigate the nomination strategies and key topics in these two related reports. The results showed that corporate leaders tend to have different priorities in annual reports and CSR reports. In annual reports, corporate leaders highlight the economic and pragmatic concerns of stakeholders to create a professionally capable and objective corporate image. In CSR reports, corporate leaders highlight the ethical concerns of stakeholders to create a socially responsible corporate image and adopt a more engaging and affiliative voice through the use of first-person pronouns. This study has significance in understanding the differences in the related genres of annual reports and CSR reports for the stakeholders.

Corporate communication plays a crucial role in establishing favorable relationships with stakeholders. In corporate communication, Chairman’s or the Chief Executive Officer (CEO) statement serves as an important means to project the image of the corporation and can reflect “the tone at the top” (Amernic et al., 2010). A plethora of studies have explored impression management in the CEO statements to project a positive corporate image (Conaway and Wardrope, 2010; Barkemeyer et al., 2014; Aerts and Yan, 2017; Boudt and Thewissen, 2019; Yan et al., 2019; Na et al., 2020). As a separate section placed at the beginning of annual reports and corporate social responsibility (CSR) reports, the CEO statements embody the major performance, plans, and missions of a company. Due to its great importance, the CEO statement has been an area of great interest in a wide range of fields, including accounting and applied linguistics.

Previous studies of the CEO statements are mainly taken from annual reports (Hyland, 1998; Bhatia, 2008; Amernic et al., 2010; Conaway and Wardrope, 2010; Patelli and Pedrini, 2014; Boudt and Thewissen, 2019; Yan et al., 2019). So far, only a few studies have investigated the CEO statements in CSR reports (Barkemeyer et al., 2014; Rajandran and Taib, 2014b; De-Miguel-Molina et al., 2019; Na et al., 2020). As the CEOs make statements in both the annual reports and CSR reports, it is of great value to explore how the CEOs adapt their discursive strategies and content in these two related genres. The motivation for this study came from our observation that some companies had the same or very similar CEO statements in annual reports and CSR reports. For instance, the CEO statements of Sinotrans Limited in 2018 were identical except for the introductory sentence.

In fact, annual reports and CSR reports can be seen as two related genres that address different stakeholders and convey different communicative purposes (Fuoli, 2018). In annual reports, the main stakeholders are investors and shareholders. By contrast, the stakeholders in CSR reports are more diverse and less focused. As different stakeholders have different expectations and interests, Pirson and Malhotra (2011) advised organization leaders to adjust information disclosure to the needs of different stakeholders, so as to build a trustworthy image effectively. To facilitate effective communication, the CEOs need to have genre knowledge and adjust their discourse to present an identity that best suits the needs of the audience and communicative purpose. Genre knowledge includes not only the right form of language, but also the awareness of choosing appropriate content “to a particular purpose in a particular situation” (Berkenkotter and Huckin, 1995). As the CEO statements are voluntary and unaudited, the CEOs have great freedom in the choice of content (Boudt and Thewissen, 2019). Therefore, the identification of recurrent themes in the CEO statements is important because it reflects the attention of corporate leaders (Amernic et al., 2010). This study aims to identify the interpersonal and ideational differences when CEOs address different stakeholders.

This study used a corpus of the CEO statements made by 87 Chinese companies covering a wide range of sectors to compare how companies adjust corporate messages in different contexts. We employed the Discourse-Historical Approach (DHA) developed by Reisigl and Wodak (2009) as the analytical framework, which integrates nomination strategies and key topics. This study also makes a methodological contribution. While previous studies in accounting have generally conducted thematic analysis manually through repeated close reading (Smith and Taffler, 2000; Amernic et al., 2010; Conaway and Wardrope, 2010; Marais, 2012), this study identifies recurrent themes in the CEO statements by using an automatic software Wmatrix (Rayson, 2008). There is now an increasing trend of using corpus linguistic methods in the analysis of corporate discourses (El-Haj et al., 2019). Compared with traditional manual coding through close reading, corpus-based approach is more efficient and can also avoid potential subjectivity in manual coding (Breeze, 2018). So far, computer-assisted analysis of accounting has been mainly conducted through the concordances of specific words, such as first-person pronouns (Lischinsky, 2011), modality markers (Aiezza, 2015), or through sentiment analysis (Barkemeyer et al., 2014; Boudt and Thewissen, 2019; Na et al., 2020). With a corpus of CEO statements from annual reports and CSR reports from Chinese listed companies, this study addresses the following research questions:

1. What are the nomination strategies in annual report and CSR report CEO statements?

2. What are the key topics in annual report and CSR report CEO statements?

The remainder of this article is organized as follows. After a general review of related literature, the methodology of the research will be presented followed by the presentation of results and discussion. The article ends with implications and recommendation for future research.

The extant research has studied companies’ legitimization of CSR activities from the perspective of firm performance (Bin et al., 2020; Saha et al., 2020; Suler et al., 2021), stakeholder engagement for green products (Ionescu, 2021; May et al., 2021; Vãtãmãnescu et al., 2021), financial behavior of retail investors (Crişan-Mitra et al., 2020; Priem, 2021; Bin, 2022), and corporate communication in the recent years. Specifically, corporation communication has gained an immense attention in academia regarding how a company portrays its financial and sustainable performance and activities to various stakeholders (Bedford et al., 2022; Jiang and Park, 2022). As the snapshot of corporate communication in a year, the CEO statements in CSR reports have received less attention compared with their counterparts in annual reports.

Previous studies have consistently revealed the significance of the CEO statements to users of corporate annual reports (Bournois and Point, 2006; Amernic et al., 2010; Mäkelä and Laine, 2011; Barkemeyer et al., 2014). Till now, many studies have investigated the influence of financial performance on the CEO statements in terms of linguistic structures (Clatworthy and Jones, 2006; Cen and Cai, 2013; Moreno et al., 2019) and readability (Bayerlein and Davidson, 2011; Wang et al., 2018).

Thematic analysis of the CEO statements is also an important area that has drawn immense attention. Prior studies have generally conducted content analysis to identify the prominent themes of the CEO statements. For instance, Bournois and Point (2006) analyzed 28 French CEO statements to explore the main themes (e.g., market, growth, and strategic plans, etc.) and provided recommendations to the CEOs for improving their statements to stakeholders. Amernic et al. (2010) conducted a close reading of the nine CEO statements from a British Petroleum company and identified some prominent themes, including the heroic theme to emphasize achievement and leadership, the theme of difficult business environment and future risk, business strategy, business philosophy, and the theme of trust. Jonäll and Rimmel (2010) synthesized three major themes, i.e., the company’s strength, strategies, and future plans in the CEO statements of three Swedish companies via the close reading method. Ngai and Singh (2014) analyzed the CEO messages of 234 companies from China and identified the themes of environmental factors, growth, operating philosophy, product/market mix, unfavorable financial reference, and favorable financial reference. In another study based on 32 CEO statements, Ngai and Singh (2018) identified company development, operating philosophy, company profile, business environment, corporate performance, and product and service as key themes.

While these studies explore the common themes of the CEO statements, some studies have considered the influence of different factors on the themes of the CEO statements. One of the factors considered is culture. For instance, Conaway and Wardrope (2010) compared annual report CEO statements between United States and Latin American companies and identified eight key themes, namely, financial reporting, expansion, external environment, customer relations, corporate governance, leadership, social responsibility, and mission or outlook. Despite similar themes, this study found that the Latin American CEOs displayed richer topics such as gratitude and regional political issues, which reflect their high-context culture. In addition to culture, another factor that is found to influence the theme of the CEO statements is financial performance. For instance, Smith and Taffler (2000) compared the themes in the CEO statements of low- and high-performance companies using a sample of British manufacturing firms. They noted that firms with poor performance disclosed more bad news such as losses, closures, and resignations, whereas firms with better performance portrayed more good news such as profits, dividends, and growth. Similarly, Clatworthy and Jones (2001) showed that profitable companies tended to discuss results and acquisitions, whereas unprofitable companies were inclined to discuss board changes. Bhana (2009) found that companies with improving performance highlighted good news, whereas companies with declining performance downplayed bad news. Geppert and Lawrence (2008) conducted a content analysis of the CEO statements in companies of high and low reputation and found that high repute companies concentrated more on realism using more concert words and present tense than companies with low reputation. These studies provide evidence to the view that corporate leaders are selective and strategic in their narrative reporting (Clatworthy and Jones, 2006).

With growing concern for environmental and social responsibility, it has become a common practice for companies to make CSR reports (Aiezza, 2015; Conte et al., 2020; Lin, 2020). Studies have shown that CSR reports play an increasingly essential role in evaluating corporate reputation (Goodman et al., 2011; Hetze, 2016; Pérez-Cornejo et al., 2020). Despite the importance of CSR reports, the CEO statements in CSR reports are under-researched and deserve more attention.

Among the scant literature on the CEO statements in CSR reports, Grantham and Vieira (2018) conducted a case study of the CEO statements of ExxonMobil company in CSR reports from 2002 to 2013 and found that profit and planet themes varied over time due to external factors. Specifically, the CEOs’ focus on profit declined following the 2007 financial crisis and the theme of planet gained more attention following the 2010 BP oil spill.

Some studies have employed critical discourse analysis (CDA) to examine the rhetorical strategies that the CEOs use to portray corporations as agents of positive change to different stakeholders of the companies (Rajandran and Taib, 2014a,b). For example, Rajandran and Taib (2014b) used a sample of 27 CEO statements in CSR reports of Malaysian companies and identified six themes, i.e., achievement, identification, aspiration, disclosure, recognition, and appreciation. Using the same sample of Malaysian companies, Rajandran and Taib (2014a) investigated the language strategies of CEO statements in disclosing CSR performance. This study proposed three strategies in portraying corporations as compliant and responsible agents, namely, the categorization of participants in CSR events, types of evaluation, and temporal representation of CSR performance. Rajandran (2018) identified the main stakeholders in the Malaysian CEO statements from CSR reports and examined CEOs’ communicative strategies through language and image in interacting with these stakeholders.

So far, prior literature suggests the influence of cultural and economic context on CEO statements’ language and content. In fact, other contextual factors such as audience and communicative purposes also deserve consideration.

Till now, only a few studies have compared the CEO statements between annual reports and CSR reports, the two related genres with different stakeholders in mind, especially from the perspective of content. Among the few pertinent studies, Marais (2012) compared the types of rhetoric in 90 French companies’ CEO discourses related to CSR performance, including the CEO statements from annual reports and CSR reports. This study shows that instrumental rhetoric is mainly used by the CEOs in annual reports, whereas values rhetoric is mainly employed in CSR reports. In other words, the CEOs employ different rhetoric strategies to communicate and legitimize their actions through the CEO statements. Mäkelä and Laine (2011) examined the content of two Finnish companies’ CEO statements in annual reports and sustainability reports. Their study showed that the CEO statements in the two genres reflected different types of discourse, i.e., economic growth discourse in annual reports and well-being discourse in sustainability reports. Despite its insightful contribution to the understanding of the CEO statements in annual reports and CSR reports, this study only investigated two Finnish companies through qualitative studies. A corpus-based analysis with a larger sample can test if the finding can be generalized and can also provide quantitative information concerning the distribution of specific topics. Barkemeyer et al. (2014) conducted a corpus-based study to compare the CEO statements’ sentiment in sustainability reports and annual reports from 34 companies in 10 years. The results indicate that the CEO statements in sustainability reports are more optimistic and certain than those in annual reports. This study highlights the value of using corpora in comparing the two related genres of annual report and CSR report CEO statements. This study will extend the corpus-based comparison between these two genres from sentiment analysis to thematic analysis.

This study was based on a corpus of the CEO statements made by Chinese companies listed in the Hong Kong Stock Exchange1 concerning their performance in the annual year of 2018. The companies listed in the Hong Kong Stock Exchange were chosen because they were required to provide detailed disclosures of CSR reports since January 2016 under new listing rules (HKEX, 2015, 2019). The year 2018 was chosen because it was the latest time of conducting this study. In addition, 2018 marks the 40th anniversary of the reform and opening-up policy in China. It is also the first year to implement the guiding principles of the 19th National People’s Congress of the Communist Party of China, which officially launched a new era in sustainable development and environmental protection. The historical context highlights the integration of economic development and sustainable development.

As this study aimed at comparing the CEO statements in annual and CSR reports, the companies that issued both the annual reports and stand-alone CSR/environmental, social and governance (ESG) reports were selected. Reports with CSR and ESG titles were merged into the same CSR reports genre because of their similar communicative purpose of reporting social responsibility. The companies that integrated CSR reports in annual reports were excluded from analysis. Among the 261 listed companies, 171 companies issued stand-alone CSR reports concerning their performance in 2018. The English versions of the CSR reports and annual reports of these companies were downloaded from their disclosure documents2 in PDF format. The companies that did not issue the CEO statements in either annual reports or CSR reports were excluded from the data. Among the companies that presented stand-alone CSR reports, 87 companies issued the CEO statements in both the annual reports and CSR reports. In the cases that companies issued both the Chairman’s and President’s statements, both the statements were collected. Altogether, 209 CEO statements by 87 Chinese companies were compiled, with 109 CEO statements from annual reports and 100 from CSR reports.3 Appendix 1 shows the list of the selected companies and their industry distribution based on the China Stock Market and Accounting Research (CSMAR) database classification. It can be seen that the companies cover a wide range of sectors.

The CEO statements in annual and CSR reports were extracted from the downloaded PDF texts and pasted to word files for checking and cleaning. The words that were unidentified or made separate due to formatting were fixed by checking the original documents. Chinese characters that occurred in the files were deleted. After checking, the CEO statements were saved as TXT files.

Table 1 shows the general information of the CEO statements corpus. The statistics indicate that the CEO statements in annual reports tend to be longer than their counterparts in CSR reports.

Table 1. The general statistics of the Chief Executive Officer (CEO) statements corpus.

For the analysis of the data, the DHA developed by Reisigl and Wodak (2009) was adopted as the analytical framework. The DHA belongs to the broad school of CDA. In CDA, discourse is regarded as a system of linguistic choices from which authors make decisions about inclusion and exclusion (Benwell and Stokoe, 2006). Language not only represents reality, but also constitutes social reality. The selection and highlighting of certain aspects of reality is referred to as “framing” (Entman, 1993). In discourse, framing is reflected by the inclusion of certain keywords, key topics, and phrases that are salient, which can be identified through corpus tools.

The DHA analytical framework consists of five main discursive strategies, namely, nomination, predication, argumentation, perspectivization, and intensification/mitigation. For this study, we focused on the discursive strategies of nomination and argumentation. Nomination refers to the naming of social actors. As annual reports and CSR reports present major achievements of the company to different stakeholders, we investigated how companies referred to themselves and what main stakeholders were referred to. According to stakeholder theory, the top management of a company is responsible to all the parties that have direct and indirect stakes in the company including investors, suppliers, creditors, customers, community, and environment, etc. (Freeman, 1984; Freeman et al., 2006). The CEOs put their utmost efforts to fulfill the needs to these stakeholders and provide them with information concerning their CSR activities, priorities, challenges, and achievements in a particular year through the CEO statements in annual and CSR reports (Barkemeyer et al., 2014; Ngai and Singh, 2014; Fehre and Weber, 2016; Rajandran, 2018). Argumentation strategies are realized through key topics and macrotopics consist of many specific subtopics.

Among the common corpus tools available, Murphy (2013) compared three types of representative software in the extraction of themes. Based on the comparative results together with close textual analysis of the concordances, Murphy (2013) argued that keyword analysis software (WordSmith) and key semantic domain analysis software (Wmatrix) displayed more robustness in “discerning dominant messages in a text” than sentiment analysis software (DICTION) (p. 77). Compared with keyword method, key semantic domain analysis such as Wmatrix (Rayson, 2008) is more synthetic and robust in that it has the advantage of grouping words that are similar in meaning into a single category. Therefore, we employed the corpus tool Wmatrix developed by Rayson (2008) to identify the CEO statements’ key topics in annual and CSR reports.

Wmatrix employed UCREL semantic analysis system (USAS), an automatic semantic tagging system, to assign a semantic domain tag to each word in a given text (see Rayson et al., 2004 for a detailed introduction to USAS). USAS is a multitier semantic tagging system that classifies words into 21 major semantic categories and 232 specific semantic fields (the full tag set and prototypical examples of each semantic field can be downloaded in the website: http://ucrel.lancs.ac.uk/usas/). Wmatrix allows users to either choose the reference corpus already provided by the software or upload their own reference corpus to perform analysis. In this study, the two corpora of the CEO statements were both uploaded to Wmatrix and chosen as each other’s reference corpus when making key semantic domain analysis. The total frequency of each semantic domain of a given corpus is calculated and compared with that in the reference corpus using log-likelihood (LL), which is a statistical test widely employed in corpus linguistics to measure if there is significant difference in item frequencies between two corpora (Rayson, 2003). The semantic domains that have a significantly higher frequency in the selected corpus than the compared reference corpus are key semantic domains, which are a good indicator of the prominent topics of the corpus under investigation. Those with LL value larger than 10.83 is considered to be significant at the level of 0.1% or p < 0.001.4

As corpus linguists suggest the investigation of word lists and key topics in combination with their concordances, so as to present a better picture of the context of the words and provide the nuances of a message (Rayson, 2008; Murphy, 2013), we used Wmatrix to generate the concordances and collocates of a search term. The analysis of the concordances and collocates of the keywords can help to identify their typical uses and patterns.

This section compares the CEO statements in annual reports and CSR reports in nomination strategies and key topics and discusses their differences.

Nomination refers to the naming of social actors (Reisigl and Wodak, 2009). In this study, we focused on self-reference and main stakeholders.

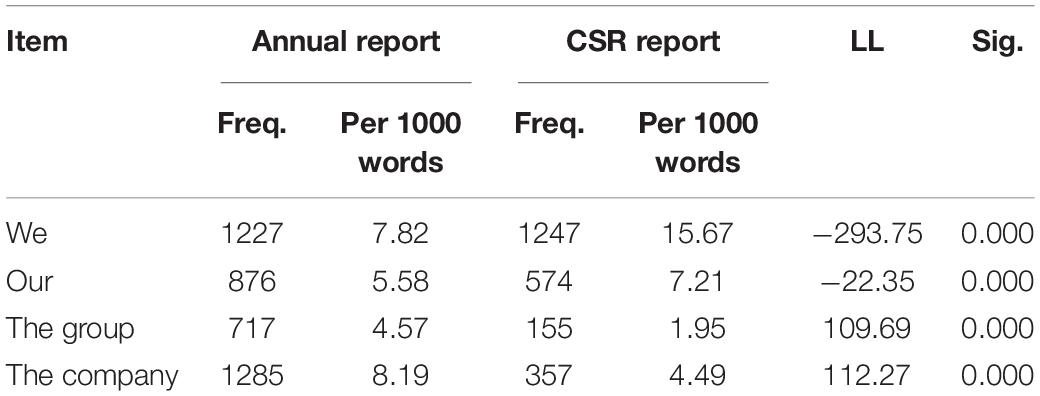

The choice of self-reference forms serves as a powerful strategy for identity construction (Blitvich, 2010). They can project different identities of the in-groups and out-groups (Tajfel, 1981). In self-reference, the CEO statements in both the annual reports and CSR reports used the first-person plural pronoun and third-person self-reference. However, as seen from Table 2, there is a significantly higher frequency of third-person self-reference in the form of the company and the group in the annual reports, whereas there is a significantly higher frequency of the first-person plural pronouns we and our in CSR reports. When referring to the companies, the CEOs prefer the more detached form represented by the company or the group in the annual reports. The use of the third-person self-reference form is considered to be a more inanimate reference (Thomas, 1997) and delivers an institutional voice. It can project a more detached and objective “out-group” identity (Tajfel, 1981). By contrast, the CEOs tend to project a more inclusive and affiliative voice in CSR reports through the use of we and our. Compared with the company or the group, the plural form of the first person is more inclusive and engaging, which can “maximize the affective impact” by involving all the members of the organization (Lischinsky, 2011). Such use projects an “in-group” identity (Tajfel, 1981) and can build solidarity and affiliation with the audience (Aiezza, 2015). Some of the most frequent content words that collocate with we include served, adhere(d), continue(d), actively, always, improved, supported, enhanced, promoted, committed, and developed. Most of these collocates have a positive connotation, which project an optimistic, committed, and caring corporate image.

Table 2. Statistics of self-reference in annual report and corporate social responsibility (CSR) report CEO statements.

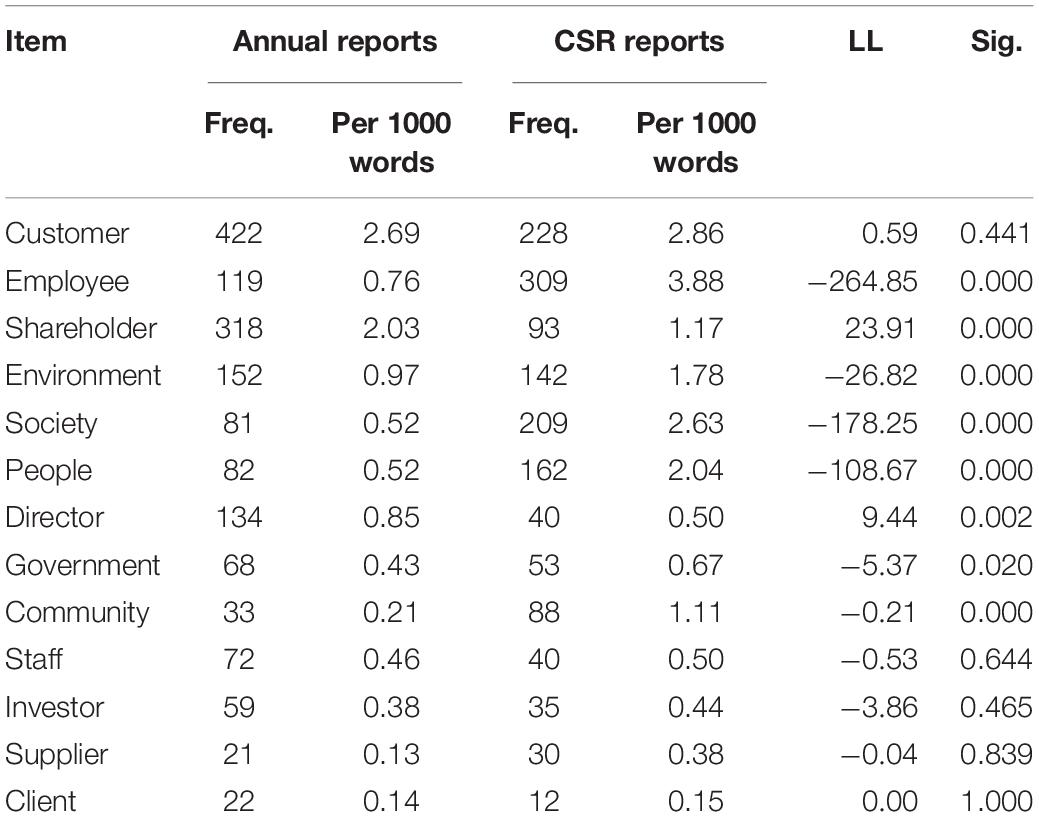

The nomination difference between the CEO from annual and CSR reports is also reflected in the communication regarding stakeholders. To identify specific stakeholders, this study drew related research (Rajandran, 2018) and the concordances of some main stakeholders. The words referring to stakeholders were searched in the corpus in both their singular and plural forms. Table 3 presents the main stakeholders in annual and CSR report CEO statements.

Table 3. Statistics of words referring to stakeholders in annual report and CSR report CEO statements.

The four major stakeholders identified in Rajandran’s (2018) study, namely, the community, customer, employee, and environment, all had a high frequency in this corpus, despite some slight differences in the ranking. While community was found to rank first in Rajandran’s (2018) study of the Malaysia CEO statements, it had a lower rank in this corpus. One of the reasons may be attributed to the fact that community was one of the designated sections in CSR reports in Malaysia (Rayson et al., 2004), but it was sometimes subsumed in the broader category of society in Chinese CSR reports. In the CEO statements in Chinese companies, there was a high frequency of referring to society and the public, which express a similar meaning to community. Another reason may be due to the different size in sampling. In Rajandran’s (2018) study, only 32 CEO statements from 15 companies were included. With a much larger and wider sample of 209 CEO statements from 87 companies, this study identified a wider range of highly frequent stakeholders.

The comparison indicates that there is a significantly higher frequency of shareholder in the CEO statements from annual reports. This finding consistent with prior research suggests that the CEOs tend to highlight the main stakeholders in annual reports, especially the stakeholders with economic interests and decision power (Goodman et al., 2011). As Bartlett and Chandler (1997) rightly maintain, the general-purpose nature of annual reports makes it unlikely to “satisfy the widely differing information needs of a large body of shareholders.” In contrast, the CEO statements in CSR reports have a significantly higher frequency of employee, environment, society, people, and community. In CSR reports, the CEOs try to connect with a wider network of stakeholders, showing care and concern to internal employees and external stakeholders (Brennan et al., 2013; Ngai and Singh, 2014; Cooren, 2020). Thus, the comparative results suggest that the CEO statements in annual reports are more pragmatic oriented, whereas CSR reports are more value oriented and people oriented.

The key topics were identified through the software Wmatrix, which can generate key semantic domains in a given corpus.

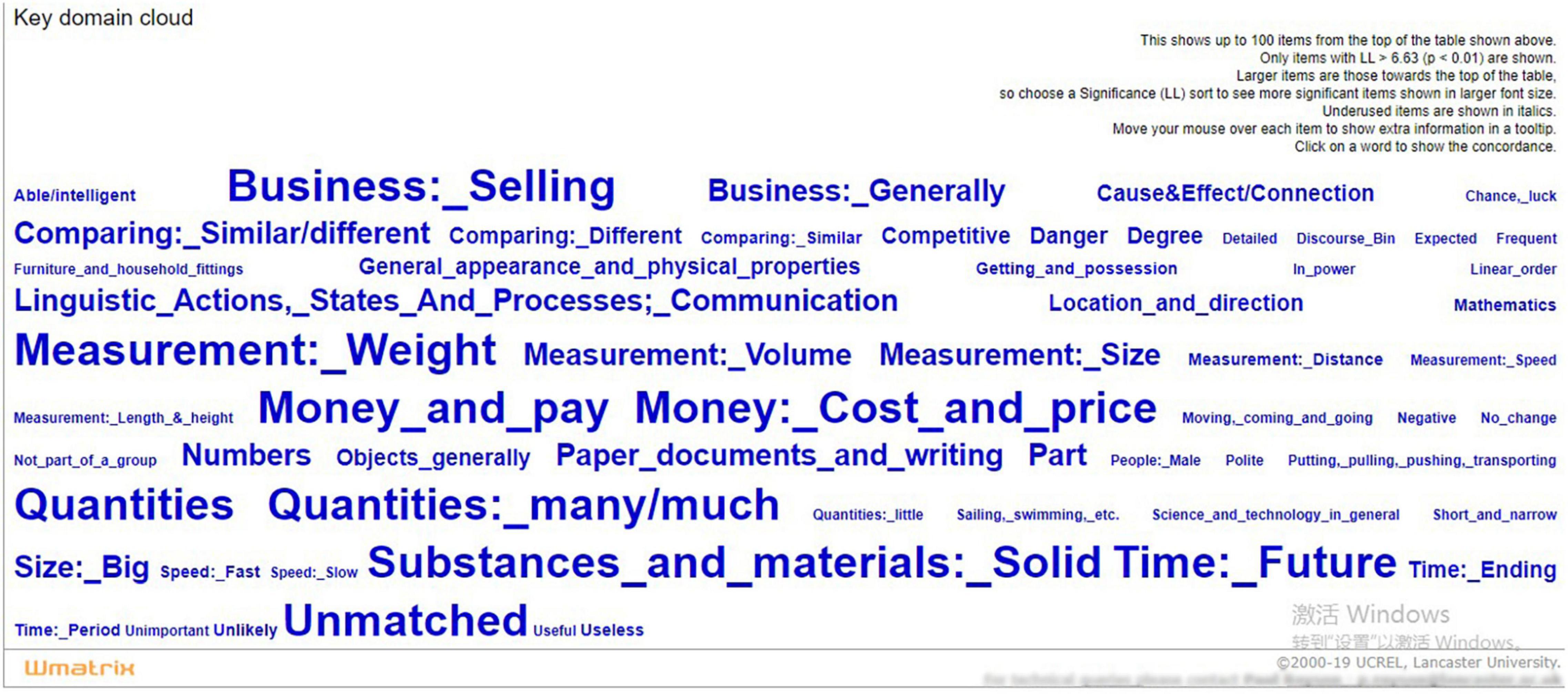

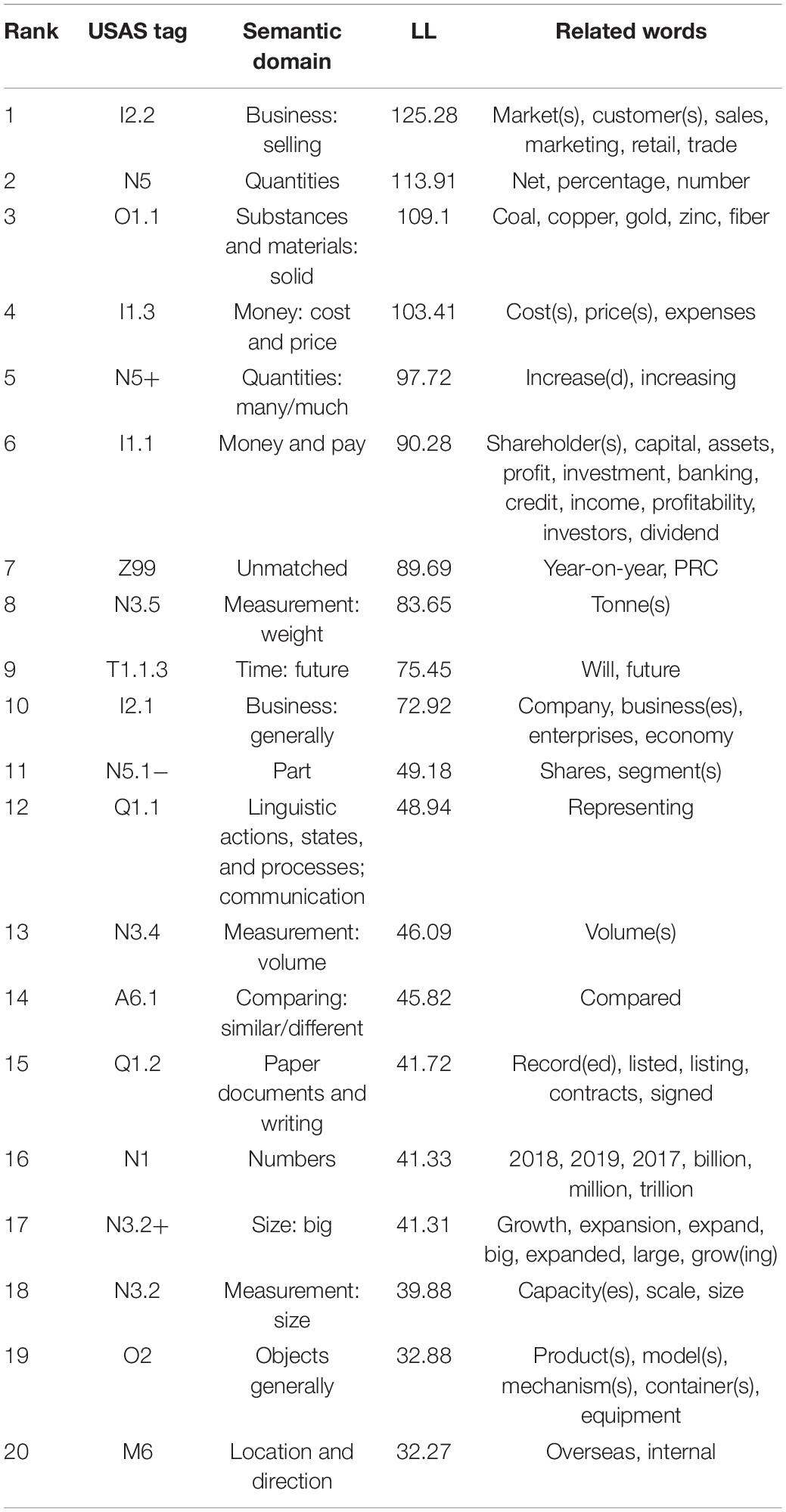

Figure 1 shows the key semantic domain cloud of the CEO statements in annual reports. Following Rayson (2008) who listed the top 20 items when comparing the semantic domains of two related documents, we presented the top 20 key semantic domains in the descending order of LL value in Table 4.

Figure 1. Key semantic domain cloud of the annual report Chief Executive Officer (CEO) statements.

Table 4. Top 20 key semantic domains in the annual report CEO statements.

Semantic domains that share the same higher-level semantic category or have similar meanings are merged and discussed together. The top key semantic domains can be classified into the following main categories.

The first main semantic category includes business: selling (I 2.2), business: generally (I 2.1), money: cost and price (I 1.3), and money and pay (I 1.1). They share the same USAS tag I, which means money and commerce in industry (see http://ucrel.lancs.ac.uk/usas/usas_guide.pdf for the specific introduction to the USAS semantic tags). In the semantic domain cost and price, the representative word cost often occurs in phrases such as cost reduction, cost-to-income ratio, low cost, and cost control:

(1) The group earnestly promoted operation and management as well as cost reduction and efficiency improvement.

In the semantic domain money and pay, it is interesting to note that shareholders and investors are also included. The frequent occurrence of these two words suggests that the CEOs in annual reports are keenly aware of stakeholders that have financial relations with the companies.

The second key semantic category is about numbers and measurement represented by the semantic tag of N, including quantities (N5), quantities: many/much (N5+), numbers (N1), measurement: weight (N3.5), measurement: volume (N3.4), measurement: size (N3.2), size: big (N3.2+), and part (N5.1−). While quantities, numbers, and measurement show objective reports of numbers and measures, two other semantic domains in this main semantic category show positive evaluation, i.e., quantities: many/much (N5+) represented by increase(d), increasing, and size: big (N3.2+) represented by growth and expand(ed):

(2) In 2018, the bank achieved coordinated growth in quality and efficiency.

The frequent use of such words is consistent with previous studies’ finding that growth and expansion are a common theme in the annual report CEO statements (Bournois and Point, 2006; Amernic et al., 2010; Conaway and Wardrope, 2010; Mäkelä and Laine, 2011; Ngai and Singh, 2014).

The third main category includes substances and materials: solid (O 1.1) and objects generally (O2). The representative words in substances and materials are closely related to the specific industries of the companies. A study of the concordances of some representative words of objects generally shows that they typically occur in positive contexts, as can be seen in the following example:

(3) These products have boosted the optimization of the company’s product structure and the layout of strategic new products and new special products. The company has expedited the transformation and upgrading of high value-added products represented by canned beer and craft beer.

The fourth key semantic domain is future, represented by will and future. The most frequent right collocates of will is continue as shown in the following example:

(4) In the coming year, the bank will continue to follow the path of high-quality development.

The fifth key category includes linguistic actions, states, and processes: communication (Q 1.1) and paper documents and writing (Q 1.2), which share the semantic tag of Q, representing language and communication. In the semantic domain of linguistic actions, the most related word representing typically occurs in the context of representing an increase of and representing a year-on-year increase of:

(5) The healthcare service business’s revenue amounted to RMB 2555 million, representing an increase of 22.42% compared to 2017.

In the semantic domain of paper documents and writing, the representative word recorded often collocates with revenue, Renminbi (RMB), million, billion, and growth, which are also about financial performance.

Other semantic domains in the top 20 include unmatched, comparison, location, and direction. The unmatched domain includes words that cannot be classified into specific semantic domains. The most frequent word in the semantic domains of comparison was compared. It is interesting to note that compared often occurs in contexts to compare financial performance with the previous year as seen in example 5. The frequent use of such specific financial performance is consistent with previous finding that financial reporting is a common theme in the CEO statements from annual reports (Mäkelä and Laine, 2011). In the semantic domain of location and direction, the most frequent words are overseas and internal. Typical collocates of overseas include market(s), business(es), and projects. Typical phrases containing internal are internal control, internal management, and compliance. Such uses indicate that the CEOs are concerned not only about internal corporate governance, but also about international markets.

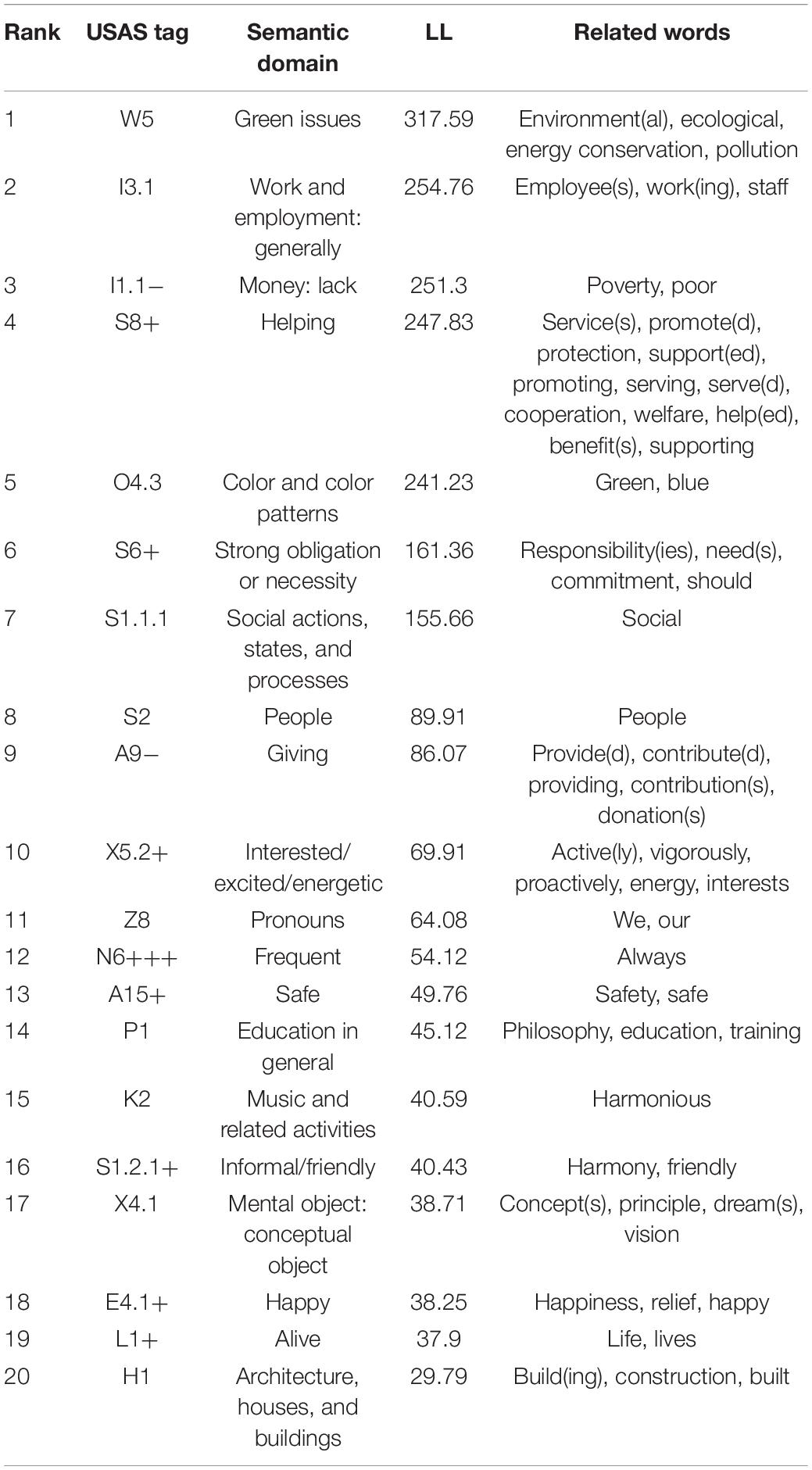

Figure 2 shows the key semantic domain cloud of CSR report CEO statements. The specific statistics of the top 20 key semantic domains are shown in Table 5.

Figure 2. Key semantic domain cloud of the corporate social responsibility (CSR) report CEO statements.

Table 5. Top 20 key semantic domains in the CSR report CEO statements.

These top key semantic domains in CSR report CEO statements can be classified into the following major categories.

The first main category concerns environment, including green issues as well as color and color patterns represented by green, which is also related to green issues, as can be seen in the following example:

(6) We made innovation in green insurance and financing services to facilitate pollution prevention.

The second main category is work and employment. The following example reflects the importance attached to employees in CSR report CEO statements:

(7) We are committed to creating a happy home for employee growth. We see employees as the key to achieving exceptional results and strive to create an enabling environment for employees by putting them first.

The third key category is related to lack of money, represented by poverty and poor. A detailed examination shows that the most common collocate of poverty is alleviation, which actually shows corporations’ concern for society (see example 8).

The fourth key category covers a wide range of semantic domains, including helping (S8+), strong obligation or necessity (S6+), social actions, states, and processes (S1.1.1), people (S2), and informal/friendly (S1.2.1+), which all share the semantic tag of S, meaning social actions, states, and processes. A typical example is provided below:

(8) In this year, we vigorously fulfilled our social responsibility by strengthening targeted poverty alleviation and actively engaging in rescue and relief work, instilling among the people a deep-rooted image of an enterprise with firm commitment.

The frequent use of such words is consistent with previous research finding that social responsibility is a common theme in the CEO statements from CSR reports (Marais, 2012). The frequent occurrence of the semantic domain of people also supports evidence from previous research that the CEO statements from CSR reports are people oriented (Grantham and Vieira, 2018).

Three other semantic domains are also related to corporations’ engagement with social responsibility. One is the semantic domain of giving, which shows corporates’ contribution to the society, as illustrated in the following example:

(9) The Bank donated more than RMB 300,000 to remote primary schools, villages, and towns, donated RMB 2 million to Zhengzhou Charity Federation, and provided financial assistance to poor university students for 3 consecutive years.

Another semantic domain related to social issues is architecture, houses, and buildings, represented by build(ing), construction, and built. Typical phrases containing construction include infrastructure construction and construction of ecological civilization and typical words that follow building include society and China. This semantic domain is used metaphorically by comparing the construction of society to the building of a house:

(10) The year 2019 will be an important year in advancing the 13th Five-Year Plan and instrumental for securing a decisive victory in building a moderately prosperous society in all the respects.

The semantic domain of alive, represented by life and lives, is also related to social issues. A detailed study of the collocates and concordances shows that the most common phrase containing life is a better life, reflecting corporations’ concern for improving people’s living standards.

The fifth key category is interested/excited/energetic. This category is mainly about positive stance, represented by active(ly), vigorously, and proactively. Two other keywords in this semantic domain are energy and interests. But, it should be noted that the common collocates of energy are conservation, saving, reduction, emission, clean, and consumption, which show concerns for environmental protection. As for the word interests, common phrases include rights and interests and employees’ interests. Thus, energy and interests in this category show corporations’ responsibility for the environment and employees.

The sixth category is mental object, especially conceptual object, represented by concept(s), principle, dream(s), and vision:

(11) We always adhere to the concept of green development.

Closely related to this semantic domain is education in general, represented by philosophy, education, and training. Typical phrases of philosophy include new development philosophy, people-oriented philosophy, and philosophy of sustainable development, similar to that of concept and principle in expressing the values and missions of the company. A study of the concordances of education shows that it mainly refers to the specific field that the company contributes to or the training of employees.

Several other semantic domains are related to the mental concepts of values and missions. One is the semantic domain of safe, represented by safety and safe. Common phrases include safety production, safety management, safe production, and safe working environment. Another semantic domain is music and related activities, represented by the word harmonious. A close examination shows that the word harmonious is used metaphorically to indicate agreeable relationship, as can be seen in the following example:

(12) We share the benefits with stakeholders and are dedicated to promoting healthy, sustainable, and harmonious development of the economy, society, and environment.

Another semantic domain related to mental objects and missions is the semantic domain of happy, represented by happiness, relief, and happy.

The semantic domain of pronouns represented by we and our is discussed in the nomination strategies in section “Key Topics in the Annual Report Chief Executive Officer Statements.” The identification of words with a wide range of word classes shows the robustness of Wmatrix in identifying different priorities in two corpora. The semantic domain of frequent, represented by the adverb always, concerns interpersonal meanings, which will be explained in detail in the following section.

The comparison of the CEO statements between annual reports and CSR reports shows substantial differences in their key topics. The results corroborate Mäkelä and Laine’s (2011) findings that the CEO statements in annual reports tend to represent economic discourse of growth and profitability, whereas the CEO statements in CSR reports are more about social and well-being discourse. The differences also corroborate Fuoli’s (2018) argument that the CEOs in annual and CSR reports tend to portray different aspects of corporate identity.

In annual reports, there is a tendency to highlight business outcomes such as market expansion, sales revenue, market shares, and cost reduction. Such rhetoric based on rational arguments with a focus on economic benefits to stakeholders appeals to readers’ logos to achieve pragmatic legitimacy (Marais, 2012). Using specific numbers and measurement to present growth and improvement over the previous year can enhance investors’ confidence and portray a competent and pragmatic corporate image. As Clatworthy and Jones (2006) point out, successful companies are more likely to present their comparative results. It is interesting to note that despite the overall pattern of showing goods news through specific numbers and comparison, some companies also reported decreased profits or sales compared with the previous year. Although reports about financial loss or decline may influence shareholders or investors’ confidence about the company’s financial performance (Lin, 2020), factual reports can nevertheless project a credible and trustworthy corporate image (Lamond et al., 2010).

By contrast, the CEOs in CSR reports tend to highlight green issues, social responsibility, and people’s well-being. They demonstrate adherence and commitment to the concept of green development, people-oriented development, and sustainable development. Such rhetoric of values appeals to readers’ pathos to achieve moral legitimacy (Marais, 2012). By highlighting the issues that are based on moral values, the CEOs project an ethical, caring, and responsible corporate image (Ozdora-Aksak and Atakan-Duman, 2015; Nwagbara and Belal, 2019). In addition, the frequent occurrence of harmonious and harmony in CSR report CEO statements echoes corporate responses to the Chinese government’s initiation in 2006 of the idea of building a harmonious society (Marquis and Qian, 2014). The use of these intertextual links to government discourse reflects Chinese corporations’ effort to attain political legitimacy (Marquis et al., 2017; Tang et al., 2018). Aside from verbal statements, the CEOs also list specific social responsibility initiatives, including their concrete efforts in pollution prevention, strengthening employee training and development, creating a safe working environment, participating in poverty alleviation activities, and making donations. The presentation of concrete CSR initiatives can help corporations project a trustworthy corporate image.

In addition to the distinct differences at the level of ideational meaning, the comparison between the CEO statements from annual and CSR reports also reveals differences at the level of interpersonal meaning, particularly in the use of always and will. The word always occurs more frequently in CSR report CEO statements, but the word will occurs more frequently in the annual report CEO statements. The word always can be seen as a booster in the field of metadiscourse, which highlights the writer’s certainty (Hyland, 2005) and can reflect the company’s “constant commitment” (Aiezza, 2015). The more frequent use of this word in CSR report CEO statements is consistent with Barkemeyer et al.’s (2014) finding that the CEOs displayed more certainty in CSR reports than in annual reports. Compared with past facts, future-looking statements are considered to be less reliable (Aiezza, 2015). Quite a few studies suggest that less profitable companies tended to use more future references as impression management strategies (Clatworthy and Jones, 2006; Cen and Cai, 2013). Although this study did not consider the company’s profitability, their frequent occurrence indicates that future outlooks are still an important move in the CEO statements from annual reports. They can also convey the determination and good intention of the company. In addition, the common phrase will continue to implicitly expresses the company’s successful past and constant commitment.

This study compared the nomination strategies and key topics of the CEO statements in annual reports and CSR reports made by Chinese companies using the DHA of CDA. The results show that corporate leaders try to project a positive corporate image in both the genres, but tend to have different priorities. In annual reports, the CEOs aim to highlight the economic and pragmatic concerns of stakeholders to create a professionally capable and objective corporate image. In CSR reports, the CEOs tend to highlight the ethical concerns of stakeholders to project a socially responsible corporate image and adopt a more engaging and affiliative voice through the use of first-person pronouns to construct a caring corporate image.

This study has significance in understanding the differences in the related genres of annual report and CSR report CEO statements and can shed light on projecting positive corporate images to different audiences. In annual reports, the CEOs portray shareholders’ wealth maximization objective by putting more stress on money, quantities, and growth discourse to the current and prospective investors of the company. In contrast, the CEOs in CSR reports emphasize green issues, people, service, and values to show their social care. The findings of this study have implications for top management in considering the aspects covered in the CEO statements delivered to different audiences as well as their weight of priorities. This study also has methodological implications. We admit that we have identified some similar basic themes such as business growth in annual reports and green issues in CSR reports to prior studies, which adopted manual coding (Mäkelä and Laine, 2011; Marais, 2012). This consistence in general findings highlights the advantages and robustness of corpus-based automatic analysis over manual coding. This approach can, thus, be extended to the analysis of other accounting discourse. The automatic semantic analysis provides new avenues for future research of accounting narratives, which can help to identify the key themes or key topics of given texts (Bostan et al., 2020). In this study, we have focused on two discursive strategies of the DHA, namely, the nomination strategies and the key topics. As a comprehensive and powerful analytical framework, the DHA has been mainly applied in political discourse (Reisigl and Wodak, 2009). Other discursive strategies of the DHA can be investigated in accounting discourse.

Through detailed analysis of the keywords in each semantic domain together with their concordances and collocates, we have identified some fine-grained topics, which can have implications to the CEOs as to what to include in their statements. In addition, we have also identified some unique themes and keywords, such as poverty alleviation and harmonious development with Chinese characteristics as compared to prior studies in Western context (Mäkelä and Laine, 2011; Bostan et al., 2020).

Admittedly, a few limitations in this study should be noted. First, despite the robust function of automatic semantic tagging, it should be pointed out that USAS has a precision rate of about 91% and there are still instances of inaccuracy mainly due to word sense disambiguation, which is a great challenge for semantic coding (Rayson et al., 2004). For some polysemous words, they may be assigned a semantic field tag based on frequency-based dictionaries and past tagging experience, which do not exactly match the meaning in the context. For instance, the word “building” is classified into the semantic category of “houses and architecture” based on its prototypical meaning. But, in example (10), it means “develop” in the specific context, which is used in its associative meaning derived from the prototypical meaning. Similarly, the word “harmony” is classified into the semantic category of “music and related activities” because harmony also has the meaning of “notes of music combined together in a pleasant way.” But, in example (12), it means “a state of peaceful existence.” That is to say, the automatic semantic tagging system may not recognize the metaphorical meaning or fine-grained meaning of certain words that are polysemous. This is also one of the reasons why this study investigates the context of keywords through concordance and collocates to better interpret their meanings in contexts. Second, our findings are limited to a cross-sectional analysis of the CEO statements in annual and CSR reports of Chinese companies in a single year. Future studies can be extended to multiple years and other countries as the CEOs’ preferences for communicating with stakeholders might vary with changes in the external environment. Finally, it should also be pointed out that this study is based on textual analysis of the CEOs’ communication with stakeholders in annual reports and CSR reports, without considering their effectiveness. Thus, we urge upcoming studies to conduct qualitative research by interviewing different stakeholders to explore their perceptions and opinions of the effective CEO statements.

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author/s.

QL and Bilal contributed to conception and design of the study. BK organized the database. QL performed the statistical analysis. QL, Bilal, and BK wrote the first draft of the manuscript. All authors contributed to the manuscript and approved the submitted version.

We acknowledge the financial support of Hubei University of Economics to support the open access of this manuscript through its excellent Ph.D. program-wide grant number XJ18BS06. This manuscript was also supported by a project (19G002) by Hubei Provincial Department of Education, China.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Aerts, W., and Yan, B. (2017). Rhetorical impression management in the letter to shareholders and institutional setting. Account. Audit. Account. J. 30, 404–432. doi: 10.1108/aaaj-01-2015-1916

Aiezza, M. C. (2015). “We may face the risks”…“risks that could adversely affect our face.” A corpus-assisted discourse analysis of modality markers in CSR reports. Stud. Commun. Sci. 15, 68–76. doi: 10.1016/j.scoms.2015.03.005

Amernic, J., Craig, R., and Tourish, D. (2010). Measuring and Assessing Tone at the Top Using Annual Report CEO Letters. Edinburgh: The Institute of Chartered Accountants of Scotland.

Barkemeyer, R., Comyns, B., Figge, F., and Napolitano, G. (2014). CEO statements in sustainability reports: Substantive information or background noise? Account. Forum. 38, 241–257. doi: 10.1016/j.accfor.2014.07.002

Bartlett, S. A., and Chandler, R. A. (1997). The corporate report and the private shareholder: Lee and Tweedie twenty years on. Br. Account. Rev. 29, 245–261. doi: 10.1006/bare.1996.0044

Bayerlein, L., and Davidson, P. (2011). The influence of connotation on readability and obfuscation in Australian chairman addresses. Man. Aud. J. 27, 175–198. doi: 10.1108/02686901211189853

Bedford, D., Chalphin, I., Dietz, K., and Phlypo, K. (2022). The Shifting Landscape of Organizational Communication. Bingley: Emerald Publishing Limited.

Berkenkotter, C., and Huckin, T. N. (1995). Genre Knowledge in Disciplinary Communication: Cognition/Culture/Power. Hillsdale, NJ: Erlbaum.

Bhana, N. (2009). The chairman’s statements and annual reports: Are they reporting the same company performance to investors? Invest. Analy. J. 38, 32–46. doi: 10.1080/10293523.2009.11082513

Bhatia, V. K. (2008). Towards critical genre analysis. Advan. Dis. Stud. 2008:166. doi: 10.21832/9781845414283-012

Bin, L. (2022). Goods tariff vs digital services tax: Transatlantic financial market reactions. Econ. Manag. Financ. Mark. 17, 9–30. doi: 10.22381/emfm17120221

Bin, L., Chen, J., and Ngo, A. X. (2020). Revisiting executive pay, firm performance, and corporate governance in China. Econ. Manag. Financ. Mark. 15, 9–32. doi: 10.22381/emfm15120201

Blitvich, P. G.-C. (2010). Who “we” are: The construction of American corporate identity in the Corporate Values Statement genre. English Profes. Acad. Purp. 2010, 123–139. doi: 10.1163/9789042029569_010

Bostan, I., Chersan, I.-C., Danileţ, M., Ifrim, M., and Chirilã, V. (2020). Investigations regarding the linguistic register used by managers to convey to stakeholders a positive view of their company, in the context of the business sustainability desideratum. Sustainability 12:6867. doi: 10.3390/su12176867

Boudt, K., and Thewissen, J. (2019). Jockeying for position in CEO letters: Impression management and sentiment analytics. Finan. Manage. 48, 77–115. doi: 10.1111/fima.12219

Bournois, F., and Point, S. (2006). A letter from the president: seduction, charm and obfuscation in French CEO letters. J. Bus. Strategy 27, 46–55. doi: 10.1108/02756660610710355

Breeze, R. (2018). Researching evaluative discourse in Annual Reports using semantic tagging. AELFE 2018, 41–66.

Brennan, N. M., Merkl-Davies, D. M., and Beelitz, A. (2013). Dialogism in corporate social responsibility communications: conceptualising verbal interaction between organisations and their audiences. J. Bus. Ethics 115, 665–679. doi: 10.1007/s10551-013-1825-9

Cen, Z., and Cai, R. (2013). ‘Impression management’in Chinese corporations: a study of chairperson’s statements from the most and least profitable Chinese companies. Asia Pac. Bus. Rev. 19, 490–505. doi: 10.1080/13602381.2013.811825

Clatworthy, M. A., and Jones, M. J. (2001). The effect of thematic structure on the variability of annual report readability. Account. Audit. Account. J. 14, 311–326. doi: 10.1108/09513570110399890

Clatworthy, M. A., and Jones, M. J. (2006). Differential patterns of textual characteristics and company performance in the chairman’s statement. Account. Audit. Account. J. 19, 493–511. doi: 10.1108/09513570610679100

Conaway, R. N., and Wardrope, W. J. (2010). Do their words really matter? Thematic analysis of US and Latin American CEO letters. J. Busi. Communi. 47, 141–168. doi: 10.1177/0021943610364523

Conte, F., Vollero, A., Covucci, C., and Siano, A. (2020). Corporate social responsibility penetration, explicitness, and symbolic communication practices in Asia: A national business system exploration of leading firms in sustainability. Corp. Soc. Responsib. Environ. 27, 1425–1435. doi: 10.1002/csr.1895

Cooren, F. (2020). A communicative constitutive perspective on corporate social responsibility: Ventriloquism, undecidability, and surprisability. Bus. Soc. 59, 175–197. doi: 10.1177/0007650318791780

Crişan-Mitra, C. S., Stanca, L., and Dabija, D.-C. (2020). Corporate social performance: An assessment model on an emerging market. Sustainability 12:4077. doi: 10.3390/su12104077

De-Miguel-Molina, B., Chirivella-González, V., and García-Ortega, B. (2019). CEO letters: Social license to operate and community involvement in the mining industry. Bus. Ethics Eur. Rev. 28, 36–55. doi: 10.1111/beer.12205

El-Haj, M., Rayson, P., Walker, M., Young, S., and Simaki, V. (2019). In search of meaning: Lessons, resources and next steps for computational analysis of financial discourse. J. Bus. Finance Account 46, 265–306. doi: 10.1111/jbfa.12378

Entman, R. M. (1993). Framing: Towards clarification of a fractured paradigm. McQuail’s Reader Mass Commun. Theory 1993, 390–397.

Fehre, K., and Weber, F. (2016). Challenging corporate commitment to CSR: Do CEOs keep talking about corporate social responsibility (CSR) issues in times of the global financial crisis? Manag. Res. Rev. 39, 1410–1430. doi: 10.1108/mrr-03-2015-0063

Freeman, R. E. (1984). Strategic Management: A Stakeholder Approach. Boston, MA: Pitman Publishing Agreement.

Freeman, R. E., Velamuri, S. R., and Moriarty, B. (2006). Company stakeholder responsibility: A new approach to CSR. Bus. Roundtable Instit. Corpor. Ethics 2006:19. doi: 10.5588/ijtld.19.0600

Fuoli, M. (2018). Building a trustworthy corporate identity: A corpus-based analysis of stance in annual and corporate social responsibility reports. Appl. Linguist. 39, 846–885. doi: 10.1093/applin/amw058

Geppert, J., and Lawrence, J. E. (2008). Predicting firm reputation through content analysis of shareholders’ letter. Corp. Reput. Rev. 11, 285–307. doi: 10.1057/crr.2008.32

Goodman, M. B., Johansen, T. S., and Nielsen, A. E. (2011). Strategic stakeholder dialogues: a discursive perspective on relationship building. Corp. Commun. 16, 204–217. doi: 10.1108/13563281111156871

Grantham, S., and Vieira, E. T. (2018). Exxonmobil’s social responsibility messaging – 2002–2013 CEO letters. Appl. Environ. Educ. Commun. 17, 266–279. doi: 10.1080/1533015x.2017.1411216

Hetze, K. (2016). Effects on the (CSR) reputation: CSR reporting discussed in the light of signalling and stakeholder perception theories. Corp. Reput. Rev. 19, 281–296. doi: 10.1057/s41299-016-0002-3

HKEX (2015). Hong Kong Stock Exchange Appendix 27 Environmental, Social, and Governance Reporting Guide Introduction. Available online at: https://www.hkex.com.hk/-/media/hkex-market/listing/rules-and-guidance/listing-rules-contingency/main-board-listing-rules/appendices/appendix_27 (accessed December 18)

HKEX (2019). Hong Kong Stock Exchange Consultation Paper on Review of the Environmental, Social and Governance Reporting Guide and Related Listing Rules. Available online at: https://www.hkex.com.hk/News/Market-Consultations/2016-to-Present/May-2019-Review-of-ESG-Guide?sc_lang=en (accessed Janurary 20, 2019)

Hyland, K. (1998). Exploring corporate rhetoric: Metadiscourse in the CEO’s letter. J. Bus. Commun. 35, 224–244. doi: 10.1177/002194369803500203

Hyland, K. (2005). Stance and engagement: A model of interaction in academic discourse. Dis. Stud. 7, 173–192. doi: 10.1177/1461445605050365

Ionescu, L. (2021). Corporate environmental performance, climate change mitigation, and green innovation behavior in sustainable finance. Econ. Manag. Financ. Mark. 16, 94–106. doi: 10.22381/emfm16320216

Jiang, Y. N., and Park, H. (2022). Mapping networks in corporate social responsibility communication on social media: A new approach to exploring the influence of communication tactics on public responses. Public Relat. Rev. 48:102143. doi: 10.1016/j.pubrev.2021.102143

Jonäll, K., and Rimmel, G. (2010). CEO letters as legitimacy builders: coupling text to numbers. J. Hum. Res. Cost. Account 14, 307–328. doi: 10.1108/14013381011105975

Lamond, D., Dwyer, R., Arendt, S., and Brettel, M. (2010). Understanding the influence of corporate social responsibility on corporate identity, image, and firm performance. Manage. Dec. 48, 1469–1492. doi: 10.1108/00251741011090289

Lin, Y. (2020). Communicating bad news in corporate social responsibility reporting: A genre-based analysis of Chinese companies. Discourse Commun. 14, 22–43. doi: 10.1177/1750481319876770

Lischinsky, A. (2011). “The discursive construction of a responsible corporate self,” in Tracking Discourses: Politics, Identity and Social Change, ed. J. G. P. Annika Egan Sjölander (Sweden: Nordic Academic Press), 257–286.

Mäkelä, H., and Laine, M. (2011). A CEO with many messages: Comparing the ideological representations provided by different corporate reports. Account. Forum 35, 217–231. doi: 10.1016/j.accfor.2011.06.008

Marais, M. (2012). CEO rhetorical strategies for corporate social responsibility (CSR). Bus. Soc. Rev. 7, 223–243. doi: 10.1108/17465681211271314

Marquis, C., and Qian, C. (2014). Corporate social responsibility reporting in China: Symbol or substance? Organ. Sci. 25, 127–148. doi: 10.1287/orsc.2013.0837

Marquis, C., Yin, J., and Yang, D. (2017). State-mediated globalization processes and the adoption of corporate social responsibility reporting in China. Manage. Org. Rev. 13, 167–191. doi: 10.1017/mor.2016.55

May, A. Y. C., Hao, G. S., and Carter, S. (2021). Intertwining corporate social responsibility, employee green behavior, and environmental sustainability: The Mediation Effect of Organizational Trust and Organizational Identity. Econ. Manag. Financ. Mark. 16, 32–61. doi: 10.22381/emfm16220212

Moreno, A., Jones, M. J., and Quinn, M. (2019). A longitudinal study of the textual characteristics in the chairman’s statements of Guinness. Account. Audit. Account. J. 32, 1714–1741. doi: 10.1108/aaaj-01-2018-3308

Murphy, A. C. (2013). On “true” portraits of Letters to Shareholders–and the importance of phraseological analysis. Int. J. Corpus Linguist. 18, 57–82. doi: 10.1075/bct.74.04mur

Na, H. J., Lee, K. C., Choi, S. U., Kim, S. T., and Exploring, C. E. O. (2020). messages in sustainability management reports: Applying sentiment mining and sustainability balanced scorecard methods. Sustainability 12:590. doi: 10.3390/su12020590

Ngai, C. S.-B., and Singh, R. G. (2014). Communication with stakeholders through corporate web sites: An exploratory study on the CEO messages of major corporations in Greater China. J. Bus. Tech. Commun. 28, 352–394. doi: 10.1177/1050651914524779

Ngai, C. S.-B., and Singh, R. G. (2018). Reading beyond the lines: themes and cultural values in corporate leaders’ communication. J. Commun. Manag. 22, 212–232. doi: 10.1108/jcom-01-2017-0005

Nwagbara, U., and Belal, A. (2019). Persuasive language of responsible organisation? A critical discourse analysis of corporate social responsibility (CSR) reports of Nigerian oil companies. Account. Audit. Account. J. 32, 2395–2420. doi: 10.1108/aaaj-03-2016-2485

Ozdora-Aksak, E., and Atakan-Duman, S. (2015). The online presence of Turkish banks: Communicating the softer side of corporate identity. Public Relat. Rev. 41, 119–128. doi: 10.1016/j.pubrev.2014.10.004

Patelli, L., and Pedrini, M. (2014). Is the optimism in CEO’s letters to shareholders sincere? Impression management versus communicative action during the economic crisis. J. Bus. Ethics 124, 19–34. doi: 10.1007/s10551-013-1855-3

Pérez-Cornejo, C., de Quevedo-Puente, E., and Delgado-García, J. B. (2020). Reporting as a booster of the corporate social performance effect on corporate reputation. Corp. Soc. Responsib. Environ. 27, 1252–1263. doi: 10.1002/csr.1881

Pirson, M., and Malhotra, D. (2011). Foundations of organizational trust: What matters to different stakeholders? Organ. Sci. 22, 1087–1104. doi: 10.1287/orsc.1100.0581

Priem, R. (2021). An exploratory study on the impact of the COVID-19 confinement on the financial behavior of individual investors. Econ. Manag. Financ. Mark. 16, 9–40. doi: 10.22381/emfm16320211

Rajandran, K. (2018). Multisemiotic interaction: The CEO and stakeholders in Malaysian CEO Statements. Corp. Commun. 23, 392–404.

Rajandran, K., and Taib, F. (2014a). Disclosing compliant and responsible corporations: CSR performance in Malaysian CEO statements. GEMA Online J. Lang. Stud. 14, 143–155. doi: 10.17576/gema-2014-1403-09

Rajandran, K., and Taib, F. (2014b). The representation of CSR in Malaysian CEO statements: A critical discourse analysis. Corp. Commun. 19, 303–317. doi: 10.1108/ccij-02-2013-0011

Rayson, P. (2008). From key words to key semantic domains. Int. J. Corpus Linguist. 13, 519–549. doi: 10.1075/ijcl.13.4.06ray

Rayson, P. E. (2003). Matrix: A Statistical Method and Software Tool for Linguistic Analysis Through Corpus Comparison. Lancaster: Lancaster University.

Rayson, P., Archer, D., Piao, S., and McEnery, A. M. (2004). The UCREL semantic analysis system. Working Pap. 2004, 1–6. doi: 10.2307/j.ctv1h7zms9.6

Reisigl, M., and Wodak, R. (2009). “The discourse-historical approach,” in Methods of critical discourse analysis, 2nd Edn, eds R. Wodak and M. Meyer (London, UK: Sage), 87–121.

Saha, R., Cerchione, R., Singh, R., and Dahiya, R. (2020). Effect of ethical leadership and corporate social responsibility on firm performance: A systematic review. Corp. Soc. Responsib. Environ. 27, 409–429. doi: 10.1002/csr.1824

Smith, M., and Taffler, R. (2000). The chairman’s statement-A content analysis of discretionary narrative disclosures. Account. Audit. Account. J. 13, 624–647. doi: 10.1108/09513570010353738

Suler, P., Palmer, L., and Bilan, S. (2021). Internet of Things sensing networks, digitized mass production, and sustainable organizational performance in cyber-physical system-based smart factories. J. Self Gov. Manag. Econ. 9, 42–51.

Tajfel, H. (1981). Human Groups and Social Categories: Studies in Social Psychology. Cambridge: Cup Archive.

Tang, Y., Ma, Y., Wong, C. W., and Miao, X. (2018). Evolution of government policies on guiding corporate social responsibility in China. Sustainability 10, 741. doi: 10.3390/su10030741

Thomas, J. (1997). Discourse in the marketplace: The making of meaning in annual reports. J. Bus. Commun. 34, 47–66. doi: 10.1177/002194369703400103

Vãtãmãnescu, E.-M., Dabija, D.-C., Gazzola, P., Cegarro-Navarro, J. G., and Buzzi, T. (2021). Before and after the outbreak of covid-19: Linking fashion companies’ corporate social responsibility approach to consumers’ demand for sustainable products. J. Clean. Prod. 321:128945. doi: 10.1016/j.jclepro.2021.128945

Wang, Z., Hsieh, T. S., and Sarkis, J. (2018). CSR performance and the readability of CSR reports: Too good to be true? Corp. Soc. Responsib. Environ. 25, 66–79. doi: 10.1002/csr.1440

Yan, B., Aerts, W., and Thewissen, J. (2019). The informativeness of impression management- financial analysts and rhetorical style of CEO letters. Pacif. Account. Rev. 31, 462–496. doi: 10.1108/par-09-2017-0063

Appendix Table 1. List of the selected companies.

Keywords: CSR reports, annual reports, CEO statements, semantic domains, corpus

Citation: Liu Q, Bilal and Komal B (2022) A Corpus-Based Comparison of the Chief Executive Officer Statements in Annual Reports and Corporate Social Responsibility Reports. Front. Psychol. 13:851405. doi: 10.3389/fpsyg.2022.851405

Received: 09 January 2022; Accepted: 21 February 2022;

Published: 22 April 2022.

Edited by:

Xiaofei Lu, The Pennsylvania State University (PSU), United StatesReviewed by:

Chaowang Ren, Guangdong University of Technology, ChinaCopyright © 2022 Liu, Bilal and Komal. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Bilal, YmlsYWxAaGJ1ZS5lZHUuY24=, orcid.org/0000-0001-6599-6687

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.