95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

BRIEF RESEARCH REPORT article

Front. Phys. , 12 November 2020

Sec. Social Physics

Volume 8 - 2020 | https://doi.org/10.3389/fphy.2020.590623

This article is part of the Research Topic From Physics to Econophysics and Back: Methods and Insights View all 31 articles

Ajit Mahata

Ajit Mahata Md. Nurujjaman*

Md. Nurujjaman*Investors adopt varied investment strategies depending on the time scales (τ) of short-term and long-term investment time horizons (ITH). The nature of the market is very different in various investment τ. Empirical mode decomposition (EMD) based Hurst exponents (H) and normalized variance (NV) techniques have been applied to identify the τ and characteristics of the market in different time horizons. The values of H and NV have been estimated for the decomposed intrinsic mode functions (IMF) of the stock price. We obtained

The stock market is a complex dynamical system where the evolution of the dynamics depends on the participation of different types of investors or traders [1–3]. Investors/traders participate in the stock market to gain profit implementing different investment and trading strategies depending on investment time horizons (ITH) [45]. The participation of diversified investors, reaction to the information, and short-term and long-term investment approaches play crucial roles in the movement of stock prices [4].

In the stock markets, there are mainly two types of investors: short-term investors who invest for short-term gain and long-term investors who invest for long-term gain [67]. Studies show that the

As the market is mean reversing in short-term

In the short-term

In this article, we estimated the τ of the stock price in the short-term and long-term

The remaining part of this paper is organized as follows: In Section 2, we introduce the method of analysis, while Section 3 presents the data analyzed. Results and discussion and conclusion are delineated in Sections 4 and 5, respectively.

A nonlinear two-step technique—EMD followed by Hilbert–Huang Transform (

The

The

a. Lower envelope

b. Mean value of the envelope

c. Repeat the processes (a) and (b) by considering h as a new data set until the

Once the conditions are satisfied, the process terminates, and h is stored as the first

where

where P is the Cauchy principle value, and

Rescaled-range (R/S) analysis is a technique to estimate the correlation present in a time series by calculating H [26–28]. Details of the R/S technique are described below. Let us consider a time series of length L and divided into p subseries of length l. Each subseries is denoted as

and

respectively. Mean adjusted series is calculated as

for j = 1, 2, 3, …, l. Cumulative time series is given by

for j = 1, 2, 3, …, l.

Range of the series has been calculated as

Individual subseries range can be rescaled or normalized by dividing the standard deviation. So, R/S is written as

The ratio of each subseries of length l is expressed as

Normalized variance (

where q is the total number of

We have analyzed the stock indices and stock prices of a few companies of different countries from December 1995 to July 2018, namely, 1) S&P 500 (USA), 2) Nikkei 225 (Japan), 3) CAC 40 (France), 4) IBEX 35 (Spain) 5) HSI (Hong Kong), 6) SSE (China), 7) BSE SENSEX (India), 8) IBOVESPA (Brazil), 9) BEL 20 (Euro-Next Brussels), 10) IPC (Mexico), 11) Russell 2000 (USA), and 12) TA125 (Israel), and stock prices of the companies 1) IBM (USA), 2) Microsoft (USA), 3) Tata Motors (India), 4) Reliance Communication (RCOM) (India), 5) Apple Inc. (USA), and 6) Reliance Industries Limited (RIL) (India). Stock indices and price data were downloaded from yahoo finance, and the analysis was carried out using MATLAB software.

The stock market shows different behavior in different investment horizon.

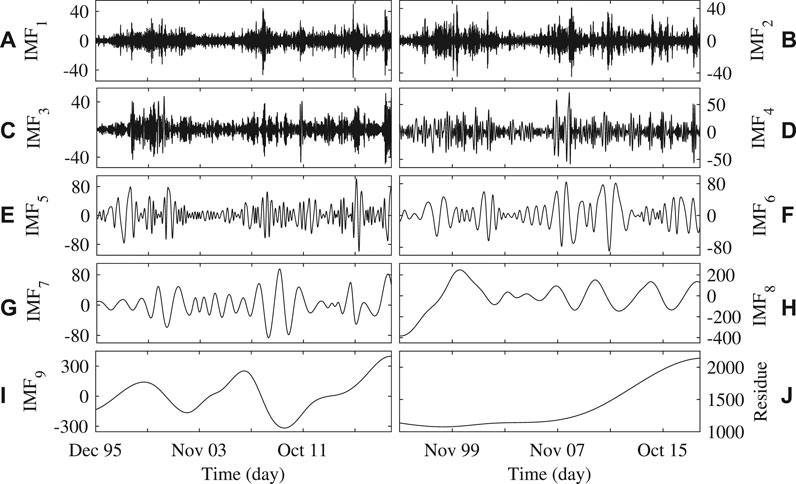

Figures 1A–J show the

FIGURE 1. The plots (A)–(I) represent the

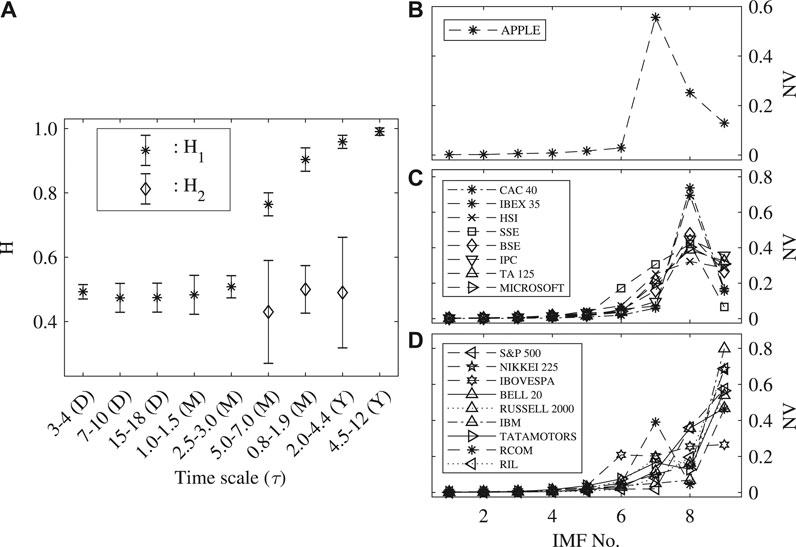

H has been calculated for all the

FIGURE 2. (A) shows the Hurst exponents (

To further validate the robustness of the proposed method, analysis of the decomposed time series has been carried out using

In order to analyze the market dynamics in short-term

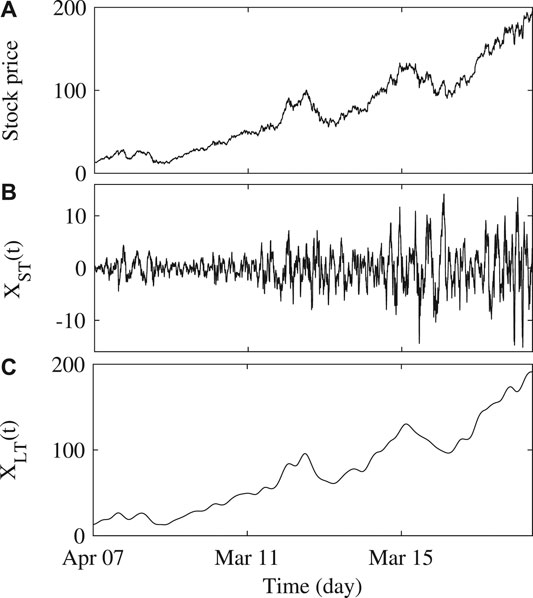

We have reconstructed a time series

FIGURE 3. (A) represents the daily price movement of Apple Inc. from April 2007 to March 2018. (B),(C) represent the reconstructed short-term time series

Higher-order

Table 1 shows that the correlation coefficient (J) between

TABLE 1. Correlation coefficient

In this paper, we have studied the stock market using the empirical mode decomposition (

The analysis yielded a value of

A detailed study of the market in the long-term

Publicly available datasets were analyzed in this study. These data can be found here: https://in.finance.yahoo.com, https://www.screener.in, https://www.macrotrends.net

All the authors have equally contributed to preparing the manuscript.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

The authors acknowledge the help of Taraknath Kundu and suggestions of the anonymous reviewers in preparing and improving the manuscript.

1. Mantegna RN, Stanley HE. Introduction to econophysics: correlations and complexity in finance.. Cambridge, United Kingdom: Cambridge University Press (1999).

2. Bouchaud J-P, Potters M. Theory of financial risk and derivative pricing: from statistical physics to risk management.. Cambridge, United Kingdom: Cambridge University Press (1999).

3. Huang NE, Wu M-L, Qu W, Long SR, Shen SS. Applications of Hilbert–Huang transform to non-stationary financial time series analysis. Appl Stoch Model Bus Ind (2003). 19:245–68. doi:10.1002/asmb.501

4. Peters EE, Peters ER, Peters D. Fractal market analysis: applying chaos theory to investment and economics., Vol. 24. Hoboken, NJ: John Wiley & Sons (1994).

5. Jegadeesh N, Titman S. Returns to buying winners and selling losers: implications for stock market efficiency. J Finance (1993). 48:65–91. doi:10.1111/j.1540-6261.1993.tb04702.x

6. Campbell JY, Viceira LM, Viceira LM. Strategic asset allocation: portfolio choice for long-term investors (Clarendon lectures in economic). Oxford, United Kingdom: Oxford University Press (2002).

7. Cremers M, Pareek A, Sautner Z. Short-term investors, long-term investments, and firm value. Recuperado el (2017). 15:39.

8. Menkhoff L. The use of technical analysis by fund managers: international evidence. J Bank Finance (2010). 34:2573–86. doi:10.1016/j.jbankfin.2010.04.014

9. Mahata A, Bal DP, Nurujjaman M. Identification of short-term and long-term time scales in stock markets and effect of structural break. Phys Stat Mech Appl (2019). 12:123612. doi:10.1016/j.physa.2019.123612

10. Lui Y-H, Mole D. The use of fundamental and technical analyses by foreign exchange dealers: Hong Kong evidence. J Int Money Finance (1998). 17:535–45. doi:10.1016/s0261-5606(98)00011-4

11. Levy RA. The predictive significance of five-point chart patterns. J Bus (1971). :316–23. doi:10.1086/295382

12. Samaras GD, Matsatsinis NF, Zopounidis C. A multicriteria dss for stock evaluation using fundamental analysis. Eur J Oper Res (2008). 187:1380–401. doi:10.1016/j.ejor.2006.09.020

13. Fama EF, French KR. Size and book-to-market factors in earnings and returns. J Finance (1995). 50:131–55. doi:10.2139/ssrn.498243

14. Lakonishok J, Shleifer A, Vishny RW. Contrarian investment, extrapolation, and risk. J Finance (1994). 49:1541–78. doi:10.3386/w4360

15. Basu S. Investment performance of common stocks in relation to their price-earnings ratios: a test of the efficient market hypothesis. J Finance (1977). 32, 663–82. doi:10.1111/j.1540-6261.1977.tb01979.x

16. Sloan RG. Do stock prices fully reflect information in accruals and cash flows about future earnings? Acc Rev (1996). 71:289–315.

17. Fama EF, French KR. The cross-section of expected stock returns. J Finance (1992). 47:427–65. doi:10.1108/03074350510770026

18. Barbee WC, Mukherji S, Raines GA. Do sales–price and debt–equity explain stock returns better than book–market and firm size? Financ Anal J (1996). 52:56–60. doi:10.2469/faj.v52.n2.1980

19. Mukherji S, Dhatt MS, Kim YH. A fundamental analysis of Korean stock returns. Finance Anal J (1997). 53:75–80. doi:10.2469/faj.v53.n3.2086

20. Bhandari LC. Debt/equity ratio and expected common stock returns: empirical evidence. J Finance (1988). 43:507–28. doi:10.1111/j.1540-6261.1988.tb03952.x

21. Hasanov M. Is South Korea’s stock market efficient? Evidence from a nonlinear unit root test. Appl Econ Lett (2009). 16:163–7. doi:10.1080/13504850601018270

22. Hartman D, Hlinka J. Nonlinearity in stock networks. Chaos Interdiscipl J Nonlinear Sci (2018). 28:083127. doi:10.1063/1.5023309

23. Huang NE, Shen Z, Long SR, Wu MC, Shih HH, Zheng Q, et al. The empirical mode decomposition and the hilbert spectrum for nonlinear and non-stationary time series analysis. Proc R Soc Lond A Math Phys Eng Sci (1998). 454:903–95. doi:rspa.1998.0193

24. Huang W, Shen Z, Huang NE, Fung YC. Engineering analysis of biological variables: an example of blood pressure over 1 day. Proc Natl Acad Sci USA (1998). 95:4816–21. doi:10.1073/pnas.95.9.4816

25. Chowdhury S, Deb A, Nurujjaman M, Barman C. Identification of pre-seismic anomalies of soil radon-222 signal using Hilbert–Huang transform. Nat Hazards (2017). 87:1587–606. doi:10.1007/s11069-017-2835-1

27. Nurujjaman M, Iyengar AS. Realization of SOC behavior in a dc glow discharge plasma. Phys Lett (2007). 360:717–21. doi:10.1016/j.physleta.2006.09.005

28. Carreras B, Van Milligen BP, Pedrosa M, Balbın R, Hidalgo C, Newman D, et al. Self-similarity of the plasma edge fluctuations. Phys Plasmas (1998). 5:3632–43. doi:10.1063/1.873081

29. Chatlani N, Soraghan JJ. EMD-based filtering (EMDF) of low-frequency noise for speech enhancement. IEEE Trans Audio Speech Lang Process (2012). 20:1158–66. doi:10.1109/tasl.2011.2172428

Keywords: empirical mode decomposition, Hurst exponent, short-term investment time horizon, long-term investment time horizon, time scale, normalized variance

Citation: Mahata A and Nurujjaman M (2020) Time Scales and Characteristics of Stock Markets in Different Investment Horizons. Front. Phys. 8:590623. doi: 10.3389/fphy.2020.590623

Received: 02 August 2020; Accepted: 29 September 2020;

Published: 12 November 2020.

Edited by:

Anirban Chakraborti, Jawaharlal Nehru University, IndiaReviewed by:

Suchetana Sadhukhan, National Autonomous University of Mexico, MexicoCopyright © 2020 Nurujjaman and Mahata. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Md. Nurujjaman, amFtYW5fbm9ubGluZWFyQHlhaG9vLmNvLmlu

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.