Sidi Chen1

Sidi Chen1 Min Fan

Min Fan Yaojun Fan

Yaojun Fan

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 20 March 2023

Sec. Environmental Economics and Management

Volume 11 - 2023 | https://doi.org/10.3389/fenvs.2023.1074159

This article is part of the Research TopicAssessment of Nuclear and Renewable Energy Utilization for Sustainable Economic GrowthView all 9 articles

Enterprise managers play a decisive role in management decisions. With the emergence of managerial ability measurement methods, the influence of managerial ability on enterprise development has received wide attention. Taking Chinese A-share listed companies from 2007 to 2019 as samples, this paper uses a fixed-effect model to examine the impact of management abilities on corporate performance and studies the moderating effect of compensation incentives on this impact. It is found that managerial ability has a significant positive correlation with the performance of listed companies, and this positive correlation is more obvious when the management has higher compensation incentives. Further research shows that higher ability management helps improve the performance of firms with low financing constraints but has no significant effect on the performance of firms with high financing constraints. In addition, compared with state-owned enterprises, the managerial ability of non-state-owned enterprises can promote the improvement of enterprise performance. This paper studies the impact of managerial ability on firm performance from the perspective of compensation incentives, enriching the related literature on managerial ability and firm performance.

In recent years, many financial crises, such as Enron, Worldcom and the 2008 financial crisis in the United States, have shown the importance of the company’s management. As a result, academicians and practitioners have explored the management of agitation and, at the same time, investigated the promotion and implementation of corporate governance mechanisms. Corporate governance has always been an important research topic in the field of accounting. Ownership and management are separated in an enterprise, so it is necessary for the management of the company to exert their own abilities and not deviate from the path suitable for the development of the company. As the leader of enterprise decision-making, management’s ability will certainly affect the business performance of enterprises (Yung and Chen, 2018; Yujie, 2021). A management team with strong ability can obtain, distinguish, and use information, which is helpful to reduce the information asymmetry and principal–agent problem faced by enterprises in mergers and acquisitions. “Upper echelons theory” shows that, due to the complexity of the internal and external environments, the management cannot have a comprehensive understanding of all aspects of the enterprise. The cognitive ability and values of the management determine their ability to obtain relevant information and then affect their strategic choices and corporate performance (HAMBRICK and MASON, 1984).

Previous studies have shown that finance, asset allocation behavior, R&D, and innovation are important factors affecting business performance. Finance is the booster of enterprise development. The development and perfection of finance have driven the development of financial intermediaries and financial markets, which is conducive to improving the capital structure of enterprises and improving enterprise performance (Liu et al., 2020). Especially during the COVID-19 pandemic, due to travel restrictions, electronic payments showed prominent advantages in the development of digital finance and digitalization (Li et al., 2022; Zheng Hui et al., 2022) compared with traditional cash-based payments, which provides great convenience for enterprise development. In addition, the research of Jawad (2021) also shows that liquidity costs must be adjusted due to the uncertainty related to the pandemic. R&D and innovation are important factors in improving business performance (Wang et al., 2022). In previous studies (Liu et al., 2022; Tinghui et al., 2022; Liu et al., 2022), researchers found that the financialization and digital transformation of enterprises and the development of digital finance of cities can effectively improve the efficiency of technological innovation and the innovation and entrepreneurship of cities, so as to promote the high-quality development of enterprises and cities. Environmental regulations and corporate social responsibility are also important factors affecting corporate value. The research of Liu et al. (2022b) has proved that scientific environmental policies can promote energy efficiency by influencing industrial structure and R&D innovation investment. Corporate social responsibility is another important carrier of non-financial information disclosure of enterprises, which is closely related to the production efficiency and performance of enterprises (Li et al., 2021).

Management’s ability significantly affects the company’s earnings quality (Demerjian et al., 2013; Choi et al., 2015), investment efficiency (Lijie et al., 2020), enterprise innovation strategy selection (Li et al., 2022), and new market entry strategy (Goldfarb and Xiao, 2011), and these effects will ultimately be revealed in the company’s performance. Many studies have explored the relationship between corporate governance mechanisms and corporate performance, the consideration of the company governance mechanism of the shareholders, the board of directors function, the function of the independent directors, stakeholders, information transparency, and corporate governance mechanisms. These studies have largely found that the operating performance of a better company is significantly superior to that of a company with poor corporate governance mechanisms (Huiqin, 2018). The more competent the management, the better the corporate governance. Human capital is reflected in the form of ability. The stronger the managerial ability, the easier it is to build high-quality internal control mechanisms and improve the level of corporate governance (Xiaonan and Panpan, 2021). Strong management ability can identify defects in internal controls and give timely corrections and guarantee the quality of the internal controls. Internal control is the most important part of an enterprise’s internal management; managerial ability can, through internal controls, have a positive promoting effect on corporate governance (ning-ning xu, 2017). Therefore, the stronger the managerial ability, the higher the company’s operating performance.

According to the principal–agent theory, the goals pursued by the principal and the agent are often different. In the principal–agent relationship, both parties expect to maximize their own interests. As the actual owner of the residual value of the enterprise, the client’s goal is to maximize the value of the enterprise and create more wealth for themselves. However, the agents (management) aim to pursue their own interests, such as higher salary and more in-service benefits, and may make some decisions contrary to the wishes of the principal when managing the enterprise (Huaijian and Xiaohan, 2021). Therefore, the information asymmetry between owners and management and the resulting principal–agent problem will prevent management from functioning effectively. In this case, compensation incentive or equity incentive for management can promote management to make strategic decisions that are more beneficial to the long-term development of enterprises, reduce the principal agent problem, and prevent management from taking short-term behaviors that are not conducive to enterprise innovation in order to avoid risks (Jensen and Meckling, 1976). Close alignment of the personal interests of managers and the interests of enterprises can provide a strong guarantee for promoting the improvement of enterprise performance, the effective allocation of enterprise resources, and the sustainable development of enterprises.

This paper investigates the impact of managerial ability on enterprise performance from the perspective of managerial ability and discusses the impact of managerial ability on enterprise performance under the context of salary incentives to provide a theoretical and practical basis for the design of managerial compensation incentives. The innovation of this paper is mainly in two aspects: first, the influence of managerial ability on enterprise performance is investigated, which enriches the related research on enterprise performance. Second, from the perspective of salary incentives, this paper discusses how the executive compensation incentive can impact business performance through managerial ability. The paper provides theoretical and empirical evidence for enterprises to evaluate the effect of a salary incentive mechanism and strengthen the construction of compensation incentives, giving a role for a salary incentive mechanism in the promotion of enterprise performance. Third, the paper explores whether different financing constraints will change the impact of management abilities on enterprise performance to provide evidence for enterprises to further promote the mitigation of financing constraints.

The management of an enterprise, as the “first worker,” plays an important role in major decisions such as mergers and reorganizations. With the application of high-level echelon theory, signal theory, and principal–agent theory in management theory, the influence of management characteristics on enterprises has gradually become the focus of scholars’ research (Kailan, 2021). Corporate financial performance can be regarded as the performance of managers in the past to implement policies to earn compensation for the company, and managerial ability is closely related to corporate performance. Since Demerjian et al. used the DEA-Tobit two-stage model to extract the measurement index of managerial ability, the difficult problem of measuring this index has been solved, and many scholars have conducted empirical analysis on the relationship between managerial ability and enterprise performance. Zhang Dunli et al. (2015) believe that the personal characteristics of senior executives have a significant impact on the strategy, structure, decision-making methods, and performance of the organization. Personal characteristics, such as educational background, age, and education level of senior executives, have a positive impact on enterprise performance. The financial performance of a company will be significantly improved by leaders with excellent management talents, and the shareholding of management with professional backgrounds can improve the enterprise value (He Huiqin, 2018).

The more competent the management is, the more likely it is to communicate its operation and management results to the outside world through high-quality accounting information disclosure (Li Xianan and Zhu Panpan, 2021). Improving managerial ability can further alleviate the financing constraints faced by the enterprise, bring sufficient funds to the enterprise, better support the investment plan, and continuously improve enterprise performance. There are many ways in which managerial ability can promote enterprise performance. On one hand, managerial ability plays a signaling role. Companies with higher managerial ability have lower information asymmetry and higher efficiency of asset utilization and resource allocation, thus promoting the improvement of enterprise total factor productivity (Hong and Juan, 2019), and thus, enterprise performance will also be improved. On the other hand, existing studies have also proved that managerial ability will impact the innovation level and efficiency of enterprises and then the innovation performance of enterprises (Li et al., 2022).

Based on the aforementioned analysis, this paper puts forward the research hypothesis H1:

H1. Competent management helps improve enterprise performance.

According to the principal–agent theory, compensation incentives for management can bundle the interests of enterprise owners and management so that the management can make decisions that can bring long-term benefits to the enterprise (Jianhua et al., 2021). Mingquan and Xin (2016) took Chinese A-share listed companies from 2008 to 2014 as the target and found through regression that the management after compensation incentives could promote performance improvement more. Xu Min et al. (2017) conducted a study based on data from 527 listed manufacturing companies in China and found that the compensation incentives of senior executives could promote the technological innovation input of enterprises. Because the earnings of the management are mostly related to the future performance of the enterprise (Su, 2015) and the enterprise value is related to the fluctuation of the stock price, the high-level management with higher compensation incentives is more motivated to improve the performance of the company by giving play to their ability and avoiding the loss of their own interests caused by a decline of the stock price.

Previous studies have shown that compensation incentives can promote management risk taking by associating the manager’s income with the volatility of the company’s stock price (Armstrong and Vashishtha, 2012). Balkin et al. (2000) tested the relationship between executive compensation and R&D investment in high-tech companies, and the results showed a positive correlation. Compensation incentives enable management to have the residual claim on the company’s net assets, which, to a certain extent, improves the beneficial synergy between executives and shareholders, strengthens the mutual benefit mechanism of benefit sharing and risk sharing, reduces agency problems, and enhances the enthusiasm of executives to serve shareholders (Rui et al., 2011). Chuntao and Min, 2010 studied the impact of executive compensation incentives on innovation input under different ownership structures in China and reported that compensation incentives could promote enterprise R&D. Therefore, in the context of high salary incentives, the stronger the managerial ability, the better the enterprise development and performance.

Based on the aforementioned analysis, this paper puts forward the research hypothesis H2:

H2. Highly competent management with more compensation incentives can significantly improve enterprise performance.

This paper selects Chinese A-share non-financial listed companies from 2007 to 2019 as samples and draws on existing studies to conduct the following screening: first, the missing observations of the main research variables are eliminated. Second, the financial sector sample was removed. Third, ST shares were excluded, as were companies with abnormal trading. Fourth, to control for the effects of extreme values, we shrink the tail of continuous variables. We ended up with 28,054 sample observations. Data were collected from the CSMRA database, and data processing was performed using STATA 16.0.

Managerial ability refers to the ability of managers to create output using existing company resources. At present, the widely accepted measurement method is the two-stage data envelopment analysis method proposed by Demerjian et al. (2012).

In the first stage, data envelopment analysis (DEA) is used to measure the enterprise’s production efficiency (θ). Operating revenue (SALES) is considered as the output variable, and operating costs (COGS), net fixed assets (PPE), amount of R&D investment (RD), selling and administrative expenses (SGA), and net intangible assets (TAN) are considered as input variables. The specific model is as follows:

In the second stage, because production efficiency is jointly affected by factors at both the enterprise level and the management level, the influence of factors at the management level can be determined after removing the influence of enterprise-level factors on the enterprise’s production efficiency. The firm’s production efficiency is taken as the dependent variable. Free cash flow (CFO), environmental uncertainty (EU), diversification (HHI), firm SIZE (SIZE), AGE of establishment (AGE), and market share (MS) are taken as independent variables, as shown in Model (2).

In this paper, a Tobit regression model is used to estimate model (2), and the regression residuals are management ability (MA).

Drawing on the research of Zhang Lin and Liqiu (2021), this paper uses the ratio of operating profit to total assets to measure enterprise performance (ROA).

According to the existing related literature (Yiting, 2017; Wang et al., 2022), this paper selects firm-level factors, such as firm size (SIZE), firm growth (GROWTH), free cash flow (CFO), gearing ratio (LEV), percentage of independent directors (BOARD), and the shareholding ratio of the largest shareholder (FIRST) as the main regression model’s control variables to remove the impact of heterogeneous factors on firm performance in terms of firm characteristics.

Referring to previous studies, considering that industry, company, and year factors may affect the regression results, this paper constructs the following model (3) to test the relationship between managerial ability and enterprise performance.

In Eq. 3, the subscript I is enterprise, C is city, and t is year. The explained variable ROA is enterprise performance, the core explanatory variable MA is enterprise managerial ability, and X is the control variable. φ is the firm-fixed effect, γ is the industry-fixed effect, and ω is the time-fixed effect.

To test the moderating effect of compensation incentives on the relationship between managerial ability and enterprise performance, MA and EC [the cross multiplication of the natural logarithm of executive compensation (MA*EC)] are added on the basis of model (4), and the explained variables and control variables are the same as mentioned previously. The specific model is as follows:

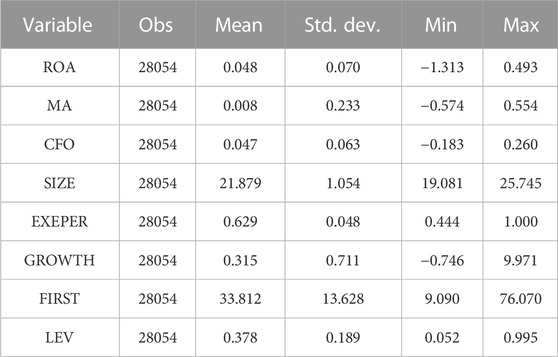

The descriptive statistical results of this paper are shown in Table 1. The mean values of management ability (MA) and enterprise performance (ROA) are 0.008 and 0.048, respectively. The standard deviations of managerial ability (MA) and enterprise performance (ROA) are 0.233 and 0.070, respectively, indicating that managerial ability varies greatly among different types of companies.

TABLE 1. Descriptive statistics.

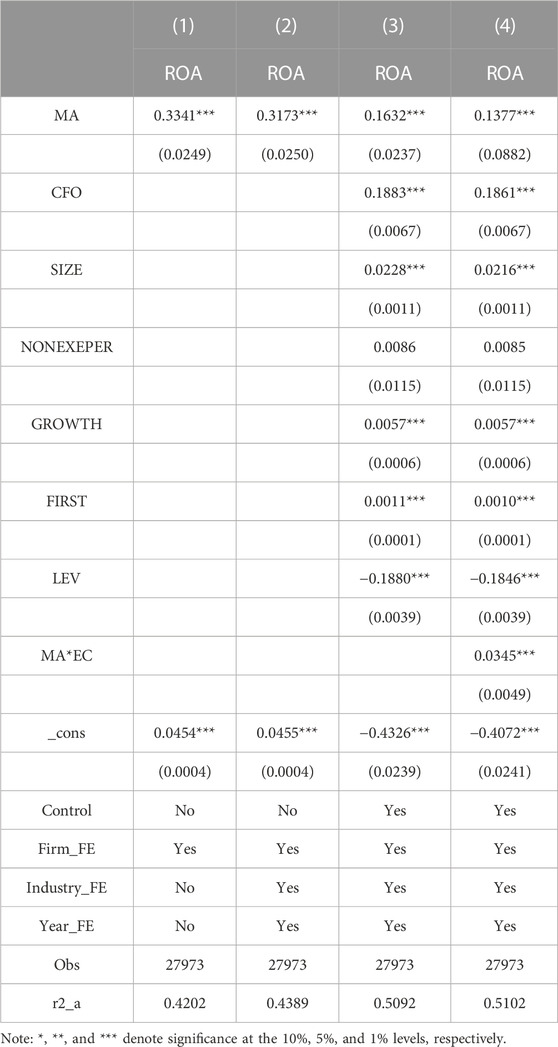

Table 2 shows the impact of management abilities on enterprise performance. Column (1) shows the results without adding control variables when controlling for firm-fixed effects, and the coefficient of MA is 0.3341, which is significant at the 1% level. Column (2) further adds industry- and year-fixed effects, and the coefficient of MA is 0.3173, which is significant at the 1% level. Column (3) adds control variables and all fixed effects, and the coefficient of MA is 0.1632, which is significant at the 1% level. The results show that the coefficient of MA is significantly positive from column (1) to column (3), indicating that highly capable management can improve the performance level of China’s A-share listed companies, and research hypothesis H1 has been verified. The economic significance behind this is that the higher the ability of the management, the lower the degree of enterprise information asymmetry, the higher the efficiency of asset utilization and resource allocation, and the higher the enterprise performance.

TABLE 2. Benchmark regression.

Table 2 (4) shows the results of the impact of managerial ability on enterprise performance after considering compensation incentives. The results show that the coefficient of managerial ability and compensation incentive (MA*EC) is 0.0345, which is significant at the 1% level. The economic significance behind this is that the higher level of salary incentive, to a certain extent, improves the benefit synergy between executives and shareholders, strengthens the mutually beneficial mechanism of benefit sharing and risk sharing, reduces the agency problem, and helps management play its role. In conclusion, under the incentive of a higher level of compensation, the promotion effect of managerial ability on enterprise performance is enhanced, and research hypothesis H2 is verified.

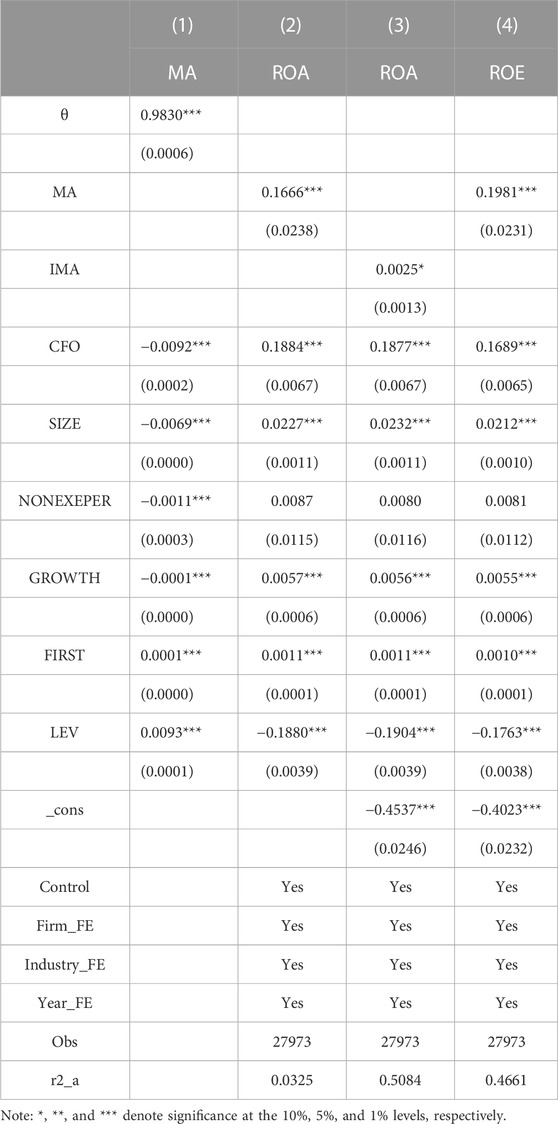

To reduce the endogeneity problem between management ability and enterprise performance, this paper uses the two-stage least square method to regress the model (2). Enterprise efficiency (θ) is used as an instrumental variable, and the regression results are shown in columns (1) and (2) of Table 3. (1) is the regression result of the first stage, and (2) is the regression result of the second stage. The results show that the coefficient of θ in the first stage is 0.9830, which is positive and significant at the 1% level. The coefficient of the regression between MA and ROA in the second stage is 0.1666, which is still significant at the 1% level. The basic results of this paper are still valid.

TABLE 3. Robustness test 1.

Following Liu Jianhua et al. (2021), the management ability index was divided into nine equal fractions to construct the discrete variable IMA to measure the management capability, and MA was replaced to conduct the regression again. A higher IMA indicates more competent management. Column (3) of Table 3 shows that the coefficient of IMA is 0.0025, which is significant at the 10% level, consistent with the previous conclusion.

Return on equity (ROE) is used as an alternative indicator of ROA to conduct a new regression. The regression results are shown in column (4) of Table 3. The coefficient of MA is 0.1981, which is significant at the 1% level, consistent with the previous conclusion.

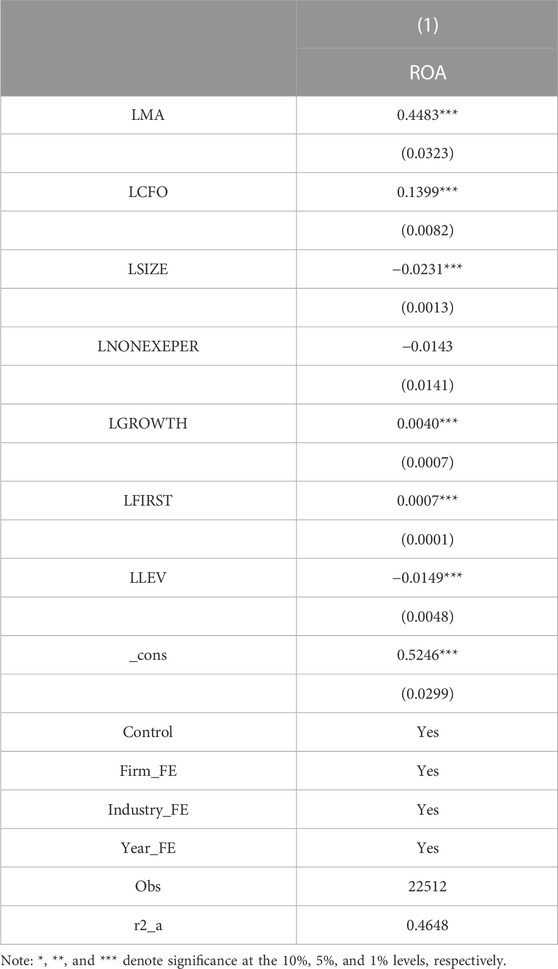

Considering that there may be a time lag in the promotion effect of management ability improvement on enterprise performance, this paper regressed the explanatory and control variables in model (3) after a lag of one period. The regression results are shown in Table 4. The coefficient of LMA is 0.4483, which is significant at the 1% level. This indicates that the conclusion of this paper still holds after considering the possible lag effect of management ability on enterprise performance.

TABLE 4. Robustness test 2.

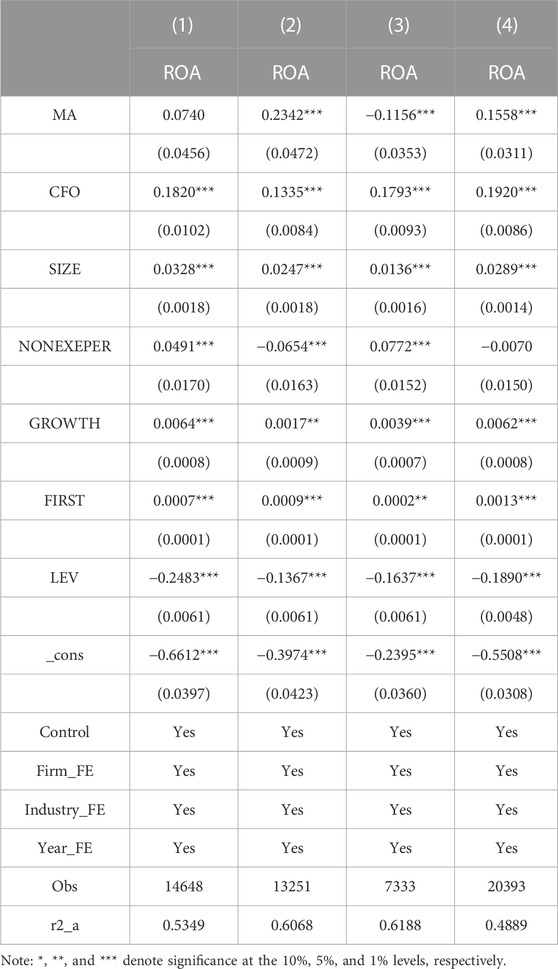

To further test whether the influence of managerial ability on firm performance still exists under different circumstances, this paper first performs group regression on firms with different financing constraints. Referring to the research of Ju Xiaosheng et al. (2013), the SA index is adopted as the measurement index of the financing constraint, where SA = −0.737 × SI + 0.043 × SI2−0.040 × A, and SI is the natural logarithm of the total assets of the enterprise, A is the listed years of the enterprise, and SA is negative. If the absolute value of SA is larger, the financing constraint is larger. In this paper, enterprises with financing constraints greater than the industry median are regarded as having high financing constraints, enterprises with financing constraints less than the industry median are regarded as having low financing constraints, and grouped regression is conducted. The regression results are shown in columns (1) and (2) of Table 5. It can be seen that the influence coefficient of managerial ability on enterprise performance is 0.2342 in enterprises with lower financing constraints, which is significant at the 1% level. The influence coefficient of managerial ability on enterprise performance is 0.0740 in enterprises with higher financing constraints, but it is not significant. The economic significance behind this is that the development of enterprises will be affected by the enterprise environment, and the financing constraint problem represents the bad financing environment of enterprises, which is not conducive to enterprise development and will naturally hinder the ability of management to play its role and reduce its impact on enterprise performance.

TABLE 5. Further analysis.

The differences in business objectives and risk control between state-owned enterprises and non-state-owned enterprises will have an impact on enterprise activities, and the management of state-owned enterprises is more prone to inaction. Therefore, it is necessary to distinguish samples according to the nature of property rights before conducting research. In this paper, the sample of state-owned enterprises and the sample of non-state-owned enterprises are respectively regressed, and the regression results are shown in columns (3) and (4) of Table 5. It can be seen that the influence coefficient of managerial ability on enterprise performance is 0.1558 in non-state-owned enterprises and −0.1156 in state-owned enterprises, both of which are significant at the 1% level. The economic significance behind this is that in non-state-owned enterprises, improving management’s ability can effectively improve the performance of enterprises. In state-owned enterprises, the goal of management is to promote the overall progress and development of society in addition to promoting performance improvement and, sometimes, even to sacrifice the interests of enterprises to serve society. Therefore, the higher the management’s ability, the lower the performance may occur.

In the context of China’s economic transformation, the high-quality development of enterprises is often greatly influenced by management. As a standard to measure the cognitive level of the management and the ability to deal with affairs, managerial ability is bound to have an important impact on the development of enterprises. Competent management has richer working experience and professional knowledge and can integrate enterprise resources to improve business performance. This paper takes the A-share listed companies in China from 2007 to 2019 as the analysis sample and empirically studies the impact of management ability on enterprise performance and the role of compensation incentives in that performance. The study found that the stronger the ability of the management, the better the performance of the enterprise. This conclusion is still valid after the endogenous test and robustness test. In addition, the compensation incentive means of enterprises can significantly change the impact of management on enterprise performance. The more powerful the compensation incentive, the more capably can management promote enterprise performance. In a further study, we found that in companies with a low degree of financing constraints and in non-state-owned enterprises, management ability has a more obvious role in promoting enterprise performance.

First, because the improvement of management ability has an important impact on the growth of enterprise performance, enterprises should pay attention to the role of management when carrying out innovation activities. For example, in management recruitment, attention should be paid to the quality or ability of the management in the level of innovation. In the work, we should strengthen the management assessment, establish an assessment system, and urge the management to invest in high-quality and profitable activities. Second, a reasonable and effective compensation incentive mechanism should be formulated to encourage management to better exert its ability to implement and deliver investment projects conducive to improving company performance. Third, investors, the board of directors, and regulators should strengthen their understanding of the importance of the management team of listed companies and jointly promote corporate governance reform by improving the performance ability of senior executives, optimizing the allocation of power, improving corporate performance, and effectively protecting the interests of investors. In addition, it is also necessary to strengthen the training of management and expand their vision so they can understand the frontier of technology and guide enterprises on the right path of innovation and development.

The study is not without limitations. This article only focuses on China. In addition, this article does not conduct a specific empirical analysis of how managerial ability affects enterprise performance. If it can provide practical experience of the influence of managerial ability on enterprise performance, it will provide more support for the development of managerial ability theory. In the future, researchers should also consider the long-term impact of managerial ability on firm performance and bring more ways to measure managerial ability. They can also study related developments in other countries.

The original contributions presented in the study are included inthe article/Supplementary Material, further inquiries can be directed to the corresponding authors.

SC: software, validation, investigation, data curation, manuscript revision, and financial support. MF: methodology, writing—original draft, resources, supervision, software, manuscript revision, and software. XW: conceptualization, supervision, financial support, and manuscript revision. YF: methodology, writing—original draft, resources, supervision, and financial support. S-TC: proofreading and literature review. SR: proofreading and literature review.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors, and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Armstrong, C. S., and Vashishtha, R. (2012). .Executive stock options, differential risk-taking incentives, and firm value. J. Financial Econ. 104 (1), 70–88. doi:10.1016/j.jfineco.2011.11.005

Balkin, D. B., Markman, G. D., and GOMEZ-Mejia, L. R. (2000). Is CEO pay in high-technology firms related to innovation? Acad. Manag. J. lancet 6: 1118–1129. doi:10.5465/1556340

Choi, W., Han, S., Jung, S. H., and Kang, T. (2015). .CEO's operating ability and the association between accruals and future cash flows. J. Bus. Finance Account. 42 (5-6), 619–634. doi:10.1111/jbfa.12118

Chuntao, Li, and Min, Song (2010). Innovation activities of Chinese manufacturing firms: The role of ownership and CEO incentive. Econ. Res. J. 5, 135–137.

Demerjian, P. R., Fay, L. M., Itamar, L. B., and Mcvay, S. E. (2013). .Managerial ability and earnings quality. Account. Rev. 88 (2), 463–498. doi:10.2308/accr-50318

Goldfarb, A., and Xiao, M. (2011). Who thinks about the competition? Managerial ability and strategic entry in US local telephone markets. Am. Econ. Rev., 101, 3130–3161. doi:10.1257/aer.101.7.3130

Hambrick, D. C., and Mason, P. A. (1984). Upper echelons:the organization as a reflection of its top managers. Acad. Manag. Rev. 2, 193–206. doi:10.5465/amr.1984.4277628

Hong, L., and Juan, W. (2019). Management competence, corporate culture and corporate social responsibility information disclosure. East China Econ. Manag. 33 (10), 138–146.

Huaijian, L., and Xiaohan, G. (2021). Research and Development investment, executive incentive and corporate performance: An empirical study based on Chinese listed companies. J. Harbin Univ. Commer. Soc. Sci. Ed. 6, 36–48.

Huiqin, H. (2018). Corporate governance, managerial ability and corporate performance. Finance Account. Commun., 15, 52–55.

Jawad, S. (2021). COVID-19 and liquidity risk, exploring the relationship dynamics between liquidity cost and stock market returns. Natl. Account. Rev. 3 (2), 218–236. doi:10.3934/nar.2021011

Jensen, M. C., and Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Agency Costs Ownersh. Struct. 3 (4), 305–360. doi:10.1016/0304-405x(76)90026-x

Jianhua, L., Tingting, X., and Zhenyi, Y. (2021). Management competence, long-term incentives and goodwill impairment. Account. Res. 5, 41–54.

Kailan, T. (2021). Research on the role of management characteristics on M&A performance. Finance Account. Commun., 19, 44–46.

Li, Z., Chen, H., and Mo, B. (2022). Can digital finance promote urban innovation? Evidence from China. Borsa Istanb. Rev. 2022, 10. doi:10.1016/j.bir.2022.10.006

Li, Z., Liao, G., and Albitar, K. (2020). Does corporate environmental responsibility engagement affect firm value? The mediating role of corporate innovation. Bus. Strategy Environ. 29 (3), 1045–1055. doi:10.1002/bse.2416

Li, Z., Yang, C., and Huang, Z. (2022). How does the fintech sector react to signals from central bank digital currencies? Finance Res. Lett. 50, 103308. doi:10.1016/j.frl.2022.103308

Li, Z., Zou, F., and Mo, B. (2021). Does mandatory CSR disclosure affect enterprise total factor productivity? Econ. Research-Ekonomska Istraživanja 35, 4902–4921. doi:10.1080/1331677x.2021.2019596

Lijie, Y., Xueying, C., Ying, Z., and Xiaojun, C. (2020). Management capability and investment efficiency. Account. Res. 4, 100–118.

Liu, Y., Failler, P., and Liu, Z. (2022b). Impact of environmental regulations on energy efficiency: A case study of China’s air pollution prevention and control action plan. Sustainability 14 (6), 3168. doi:10.3390/su14063168

Liu, Y., Failler, P., and Ding, Y. (2022a) Enterprise financialization and technological innovation: Mechanism and heterogeneity. PLoS ONE 17(12): e0275461. doi:10.1371/journal.pone.0275461

Liu, Y., Li, Z., and Xu, M. (2020). The influential factors of financial cycle spillover: Evidence from China. Emerg. Mark. Finance Trade 56 (6), 1336–1350. doi:10.1080/1540496x.2019.1658076

Rui, L., Jianhua, L., and Ning, X. (2011) Internal control, property rights and Performance Sensitivity of executive compensation. Accounting Research, 10:42–48.

Mingquan, S., and Xin, C. (2016). Management power, executive compensation and corporate performance. J. Central Univ. Finance Econ., 5, 97–104.

Ningning, X. (2017). Management competence and internal control: Empirical evidence from Chinese listed companies. Audit Res. 2, 80–88.

Su, K. (2015). Managerial equity incentive, risk taking and capital allocation efficiency. Manag. Sci. 3, 14.

Tinghui, L., Jieying, W., Danwei, Z., and Ke, L. (2022). Has enterprise digital transformation improved the efficiency of enterprise technological innovation? A case study on Chinese listed companies. Math. Biosci. Eng. 19 (12), 12632–12654. doi:10.3934/mbe.2022590

Wang, X., Fan, M., Fan, Y., Li, Y., and Tang, X. (2022). R&D investment, financing constraints and corporate financial performance: Empirical evidence from China. Front. Environ. Sci. 10, 2022. doi:10.3389/fenvs.2022.1056672

Xiaonan, L., and Panpan, Z. (2021). Management capability, debt heterogeneity and corporate governance. Finance Account. Commun. 4, 46–49.

Xiaosheng, J., Di, L., and Yihua, Y. (2013). Financing constraints, working capital management and sustainability of enterprise innovation. Econ. Res. J. 1, 4–16.

Min, X., Lingli, Z., and Zhen, F. (2017) Financial constraints, R&D investment and performance of smes. Journal of finance and accounting, (30):37–43.

Yangzi, L. (2022). Managerial ability, executive incentive and enterprise innovation strategy choice. J. Zhongnan Univ. Econ. Law, 2, 41–51.

Yiting, H., and Danxia, L. (2017). Corporate governance, government subsidies and corporate performance. Finance Account. Commun. 33, 70–73.

Yujie, L. (2021). Management capacity and enterprise risk bearing. Beijing: Beijing Jiaotong University. doi:10.26944/d.cnki.gbfju.2021.002792

Yung, K., and Chen, C. (2018). .Managerial ability and firm risk-taking behavior. Rev. Quantitative Finance Account. 51 (4), 1005–1032. doi:10.1007/s11156-017-0695-0

Lin, Z., and Liqiu, F. (2021) Research and development investment, audit opinion and corporate performance. China Certif. Public Accountants, 02:47–53.

Keywords: managerial ability, corporate performance, compensation incentives, moderating effect, financing constraints

Citation: Chen S, Fan M, Wang X, Fan Y, Chen S-T and Ren S (2023) Managerial ability, compensation incentives, and corporate performance. Front. Environ. Sci. 11:1074159. doi: 10.3389/fenvs.2023.1074159

Received: 19 October 2022; Accepted: 20 February 2023;

Published: 20 March 2023.

Edited by:

Mihaela Simionescu, Romanian Academy, RomaniaCopyright © 2023 Chen, Fan, Wang, Fan, Chen and Ren. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Min Fan, MTE2MDUyOTg4MUBxcS5jb20=; Yaojun Fan, eWFvanVuZmFuOTk2QGdtYWlsLmNvbQ==; Shichi Ren, cmVuc2hpY2hpQHN3dWZlLmVkdS5jbg==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.