Karla Bayly-Castaneda1†

Karla Bayly-Castaneda1† María Soledad Ramírez-Montoya2*†

María Soledad Ramírez-Montoya2*† Arturo Erdély-Ruiz3†

Arturo Erdély-Ruiz3† Miguel Angel Montoya-Bayardo4†

Miguel Angel Montoya-Bayardo4†- 1School of Business, Tecnológico de Monterrey, Monterrey, Mexico

- 2EGADE Business School, and Institute for the Future of Education, Tecnologico de Monterrey, Monterrey, Mexico

- 3Actuary Program, FES Acatlán, Nacional Autonomus University of Mexico, Estado de Mexico, Mexico

- 4Hub Europe (Spain), Tecnológico de Monterrey, Monterrey, Mexico

The objective of the study was to validate the construction of a financial literacy measurement instrument aligned with complex thinking competencies in Mexican women entrepreneurs. By means of the construct validation method, the content was validated by expert judgment, validation by exploratory and confirmatory factor analysis, as well as internal consistency by means of a pilot test applied to a sample of 189 participants. A highly valid and reliable version was obtained, organized in four dimensions with a total of 23 items. This study examines and estimates the determinants of financial literacy for the first time under the light of complex reasoning.

Introduction

Entrepreneurship, as the mainstay of the economy in a complex and constantly changing environment, deserves to be studied not only about the threats it faces or the identification of opportunities and their viability analysis, but also about the characteristics and decision-making skills of those who undertake them, especially women, one of the economically vulnerable sectors of the population. Financial literacy is an essential skill in modern life in both developed and emerging economies (García-Mata, 2021b) because, with the increasing complexity of the financial world, the ability to understand and properly manage money has become a pressing need directly related to the success of female entrepreneurship (Baporikar and Akino, 2020). Through the acquisition of knowledge, skills and positive attitudes regarding money management, the female entrepreneur will be better prepared to face recurrent economic crises that threaten the survival of her business (Niwaha et al., 2016; Rachapaettayakom et al., 2020). However, few efforts are directed at addressing the need for financial literacy of adult women who are on the path of entrepreneurship.

Beyond theoretical knowledge about financial instruments and services, women entrepreneurs require support for the development of competencies aimed at putting this knowledge into practice in contexts such as scenario analysis, risk assessment, the search for solutions, as well as informed decision making. The promotion of financial literacy initiatives under the scheme of complex thinking can give the entrepreneur the ability to improve her decision-making process for an effective, innovative and efficient management of her business resources (Dzwigol et al., 2020; Ramos et al., 2021). The objective of this research is the design and validation of the construction of an instrument to measure the complex thinking sub-competencies of Mexican women entrepreneurs aligned to their level of financial literacy, presenting an original approach as it is the first of its kind. The result has demonstrated that it is possible to evaluate the level of financial literacy of women entrepreneurs in the context of complex thinking, so that future initiatives in this field can be developed.

Financial literacy

Financial literacy, as a discipline of study, awakened interest only at the beginning of the 21st century as a result of the financial crises that have characterized it up to now, resulting in questions about the influence of attitudes, behaviors and knowledge on individuals' decision making with respect to the management of their money and the impact of these decisions on their general wellbeing. Starting with the work of Lusardi (2001), who was a pioneer in questioning the reasons for the factors underlying the lack of a savings culture and its impact on long-term financial planning, and the subsequent posing of a first set of questions aimed at measuring financial literacy (Lusardi, 2008, 2011; Lusardi and Mitchell, 2009), as well as the work of different governments and institutions, among which the effort of the Organization for Economic Cooperation and Development (OECD) in the development of measurement instruments such as the PISA test (Programme for International Student Assessment), which includes the measurement of basic knowledge on money management among young people (OECD, 2018), stands out, it was in 2012 when the Mexican Government launched a first measurement initiative, the National Survey on Financial Inclusion (ENIF) (CNBV, 2012). The results of these measurements consistently point to the existence of a significant gender gap where women not only show lower rates of financial literacy but also of access to useful and affordable financial products and services (UNESCO, 2020; UN Women, 2021). Now, beyond the impact that financial literacy has on women's individual wellbeing, it is time to focus on the influence of this level of financial literacy on the success of female entrepreneurship, especially in micro and small businesses where planning, management and financing decisions are usually made by a single person.

A first approach to the object of study is to establish what is understood as financial literacy, both individually and in the management of the enterprise or business. Although there is diverse literature on the subject, the definition of the construct is heterogeneous and there is no agreement (Anshika and Mallik, 2021). This represents an important challenge when trying to propose a model for its measurement. According to the OECD, financial literacy is defined as the process by which financial consumers improve their understanding of financial products, related concepts, as well as the underlying risks and, through information, instruction and/or objective advice, develop the skills and confidence to become more aware of financial risks and opportunities, make informed decisions, know where to go for help and take any effective action to improve their economic wellbeing (Raccanello and Guzmán, 2014). Another more technical approach establishes the financial literacy of the entrepreneur as the ability to understand the functioning of the business in terms of possessing knowledge about recording income and expenses, separation between personal and business money, as well as financial planning (Ali et al., 2018). Given the above, we can add that, in a business context, this definition can be complemented with the execution of actions aimed at the stable growth and financial viability of the business over time. It is important to note the importance of the ability to make timely and informed decisions according to individual circumstances.

Women and entrepreneurship

Globally, there is an unequal race for business survival. In Latin America, and especially in the case of Mexico, this inequality is extremely marked by the proportion distributed between large and small companies. According to the 2019 Economic Censuses, 99.8% of the country's establishments are micro, small or medium-sized (INEGI, 2020). These micro and small enterprises (MSMEs) are the pillar of economic growth for developing countries in addition to allowing the generation of employment and self-employment for women, one of the vulnerable groups recognized by both the OECD and UNESCO, which in the framework of the 2030 Agenda points out the need for the integration of women not only in productive processes, but also in social and economic ones (UNESCO, 2017), inequality in terms of financial inclusion in Mexico prevents women from accessing savings and investment mechanisms to ensure a decent standard of living in retirement (INEGI, 2021; INMUJERES, 2022). Entrepreneurship allows women not only to contribute to the economic wellbeing of the country, but also to guarantee the generation of income for their personal and family wellbeing while facilitating compatibility with care and household tasks.

Despite this, this sector faces enormous barriers in accessing funding and financing sources, as well as financial products and services through formal institutions, in addition to the lack of ability of entrepreneurs for financial management and long-term business planning. Without the understanding of basic financial concepts, people lack the equipment to make decisions related to the management of their resources (Vanegas et al., 2020; Anshika and Mallik, 2021) which is reflected in low performance rates and a high mortality rate of MSMEs in Mexico, which until before the COVID-19 pandemic, resulted in an average life time for this sector of 7.8 years (INEGI, 2020). Empowering women entrepreneurs by developing competencies to improve financial decision-making through innovative financial literacy initiatives can translate, over time, into a determining factor for an improvement in the population's wellbeing indexes.

Complex thinking

Decision making is a reflective process that involves analyzing and discerning between different alternatives, a decision implies knowledge, understanding and analysis of a problem in order to generate the right decision. Some authors suggest that correct decision making is linked to greater cognitive capacity, and this is a requirement for financial literacy, also establishing that the greater the cognitive capacity, the greater the gender gap in financial inclusion (Muñoz-Murillo et al., 2020). In addition to the above, studies have shown that financial literacy is neither stable nor constant, nor can it be assumed that once acquired it will affect people's decision making, since it changes according to time and circumstances, being related to the experiences, contexts and skills of the individual or the social situations that surround him/her (Bay and Catasús, 2014). It becomes, then, a personal process in which the individual needs to take responsibility for his or her self-training in order to prepare him or herself for changing economic environments (Vanegas et al., 2020). Technological evolution and the speed with which large volumes of information are transferred have evolved the business world, demanding from its managers the ability to make decisions quickly, to be self-taught, capable of interpreting reality, systematizing their decisions and learning from their own mistakes (Pacheco-Velázquez et al., 2023). In other words, the entrepreneur must not only acquire knowledge related so far to financial literacy, but simultaneously requires the development of complex thinking skills.

Unlike simple reasoning, which focuses on solving problems with a single correct answer, complex reasoning involves the consideration of multiple perspectives and the integration of multiple sources of information to find effective solutions. Complex thinking is defined as the competence acquired by individuals that allows them to develop a holistic view of the world, enabling them to carry out cognitive activities, analysis and synthesis to face challenges and solve problems (Vázquez-Parra et al., 2022a,b). According to the complex thinking competency it integrates four sub-competencies:

a) Systemic: allows the identification of the elements and interconnections that make up an environmental problem or situation.

b) Critical: analyzes and evaluates the reasoning considering its validity and its differentiation with existing knowledge and structures.

c) Scientific: provides methodologies that allow the construction of objective reasoning to make decisions.

d) Innovative: provides creative and novel elements to evaluate the environment and the problems faced by the individual.

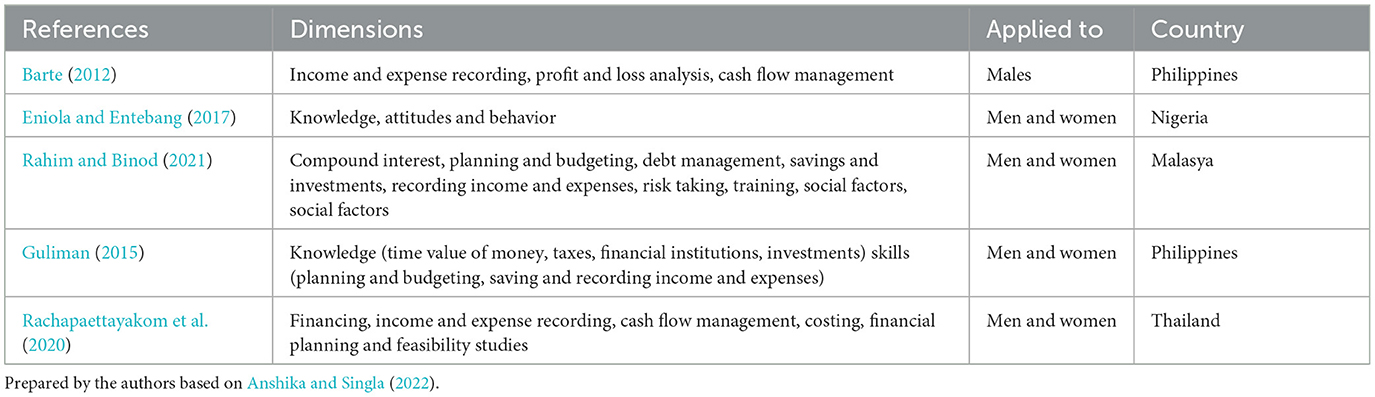

These sub-competencies are related to financial literacy in that they frame the knowledge of theoretical concepts and the skills to generate behaviors and attitudes for their application based on the experience and understanding of the environment as a consequence of business activities (Manzanera-Román and Brändle, 2016; García-González et al., 2020; Oggero et al., 2020; Cruz-Sandoval et al., 2023). From the literature review it is clear that, although there are measurement instruments regarding the application of financial literacy aimed at micro and small business management, there is no evidence of the existence of measurement instruments that relate the field of financial literacy in the female sector to the subcompetencies of complex thinking. Table 1 summarizes some studies on financial literacy in entrepreneurs that have addressed the operationalization of financial literacy related to entrepreneurship, which have served as the basis for the development of the instrument that we present in the framework of this research.

Table 1. Previous studies.

Method

The method of the study was the construct validation through the convergent and discriminant validity of a measurement instrument by means of a three-stage process. In the first stage, a literature review was carried out in order to construct the operationalization of variables based on previous research on financial literacy and its relationship with complex thinking competencies. Derived from the review, and given the non-existence of instruments that addressed both constructs, it was decided to proceed with the adaptation of the instrument: “OECD/INFE Survey Instrument to Measure the Financial Literacy of MSMEs” (Escobar-Pérez and Martínez, 2008; OECD, 2019) by reformulating items based on four sub-competencies of complex thinking: critical thinking, systems thinking, innovative thinking and scientific thinking according to the framework proposed by Vázquez-Parra et al. (2023), as well as translation and cultural adaptation ensuring the use of language oriented to favor women's financial inclusion (Agnew et al., 2018; Whitehouse, 2018; Osei-Tutu and Weill, 2021; Bertrand and Osei-Tutu, 2022). Next, a content validation process was carried out by expert judgment followed by the application of Aiken's V concordance test and a qualitative review of observations made by the experts. Finally, once the corrections derived from the previous process were attended to, progress was made toward the piloting of the instrument and its validation by means of exploratory factor analysis, confirmatory factor analysis and, finally, the internal consistency test by calculating Cronbach's Alpha coefficient.

Content validity through expert judgment

A group of seven expert judges was formed with proven experience in the field of financial literacy, as well as professional experience in direct contact with women entrepreneurs. As part of the experience of this group of experts we can highlight that three of them are authors of two or more books of international circulation on the subject of personal finance, three occupy management positions in financial institutions where they actively participate in the development of financial products and training aimed at women, and finally, one expert directs, at a national level, an initiative dedicated to the area of support for entrepreneurs in the post-acceleration stage of their business. The average number of years of experience in the area of personal finance and/or female entrepreneurship in this group is 11.3 years.

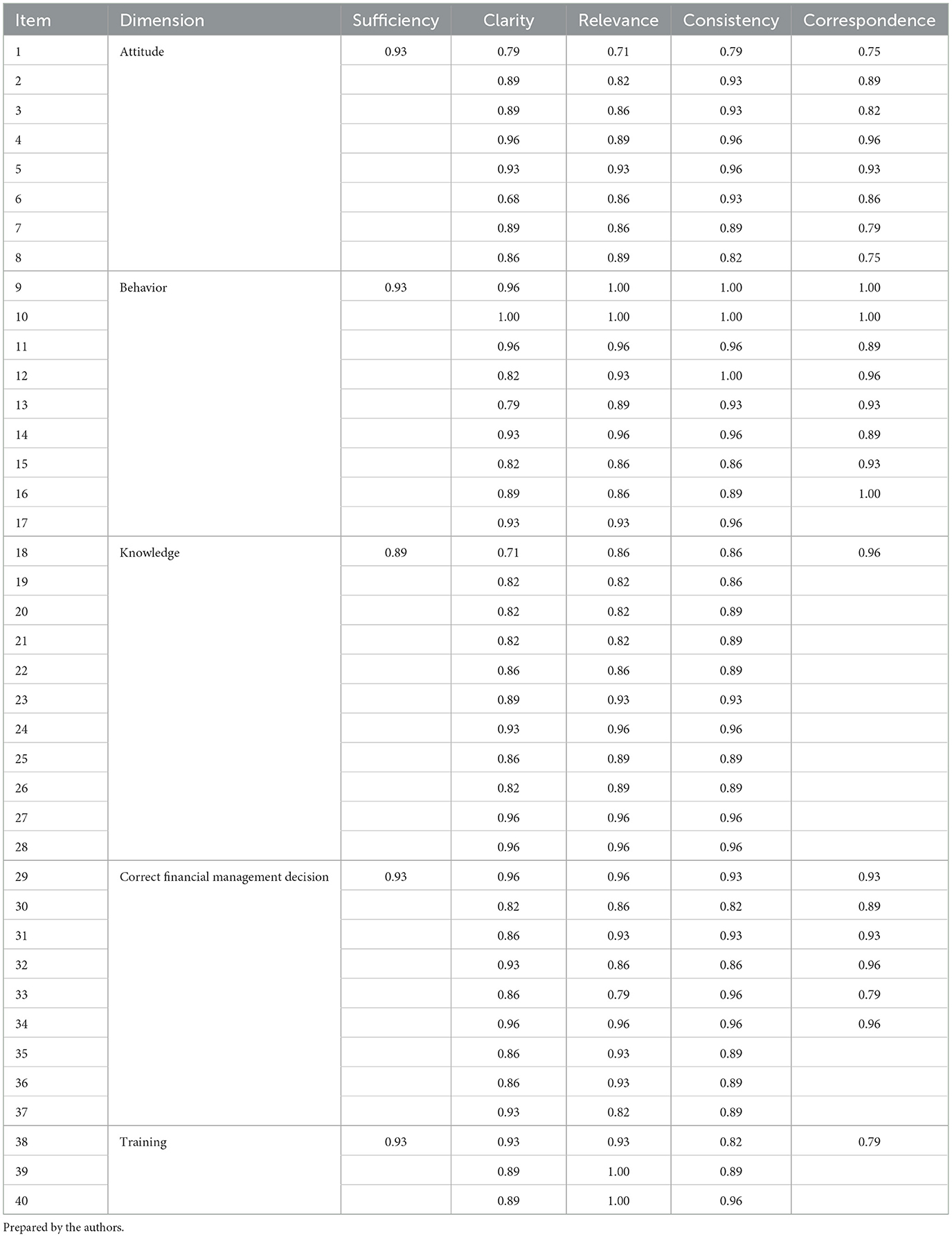

This group received the first version of the questionnaire with 40 items grouped into five domains of interest: Attitude, Behavior, Knowledge, correct financial management decision and Training, and four subdomains corresponding to the sub-competencies of Complex Thinking: systemic, innovative, critical and scientific. The experts received the questionnaire via the Google Forms tool, and were asked to evaluate each item based on clarity (the item is understood, correctly worded), coherence (the item is related to the dimension it measures), relevance (the item is important and should be included) and sufficiency (items belonging to the same dimension and sufficient to measure it) (Matsumoto-Royo et al., 2021; Ramírez-Montoya et al., 2022; OECD, (n/d)) using a Likert-type polytomous scale from 1 to 5, as well as the inclusion of qualitative comments on the items. The criterion for the acceptance of items as valid was defined as those with a concordance index >0.71 according to the estimate using Alkien's V coefficient test (Escurra, 1988; Penfield and Giacobbi, 2004), as well as the content analysis of the comments made by the group of experts.

Construct validity

Participants

The questionnaire received responses during February and March 2023 using a convenience sampling of women entrepreneurs between 18 and 69 years of age (n = 189). From the total number of observations, those where the participant stated that she was not directly involved in the financial decisions of the business or did not own the business (88) were eliminated, thus reducing the sample to 101 women entrepreneurs distributed as follows: 18–19 years (n = 9), 20–29 years (n = 37), 30–39 years (n = 13), 40–49 years (n = 20), 50–59 years (n = 14), and 60–69 years (n = 8), with businesses employing one person (n = 42) and employing between 2 and 50 people (n = 59). All of them agreed to participate in the sample collection by expressing their consent for data collection (Valenzuela and Flores Fahara, 2013), declaring to be involved in making both investment and financing decisions for their business.

Procedure

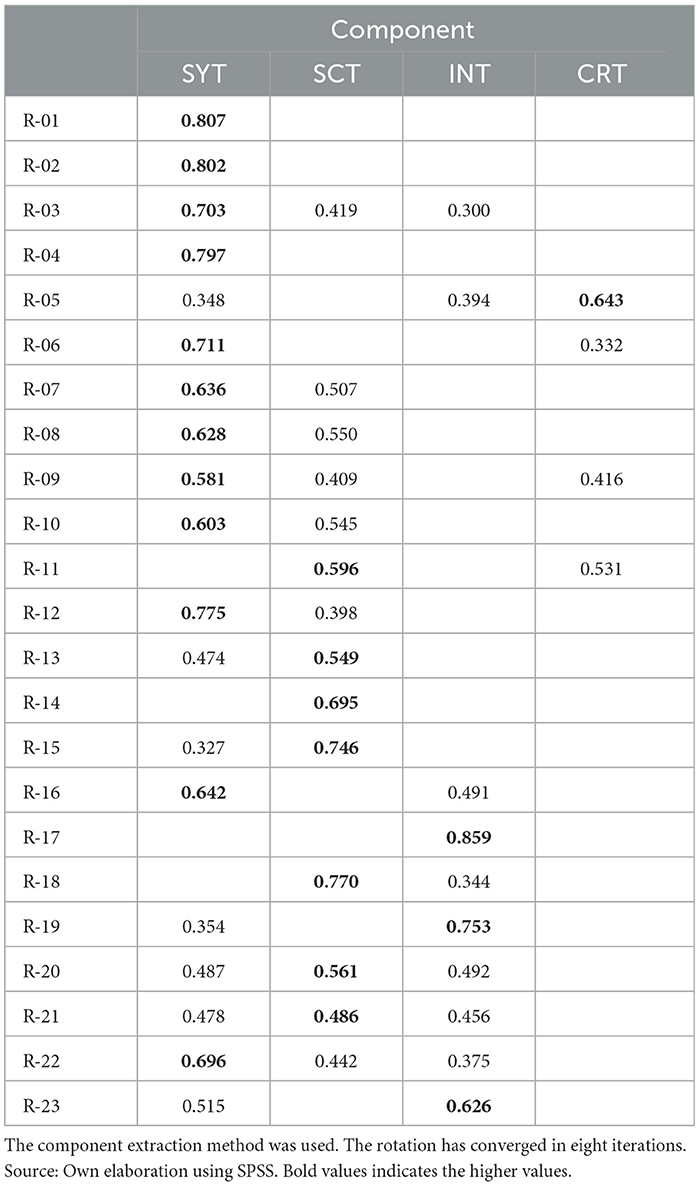

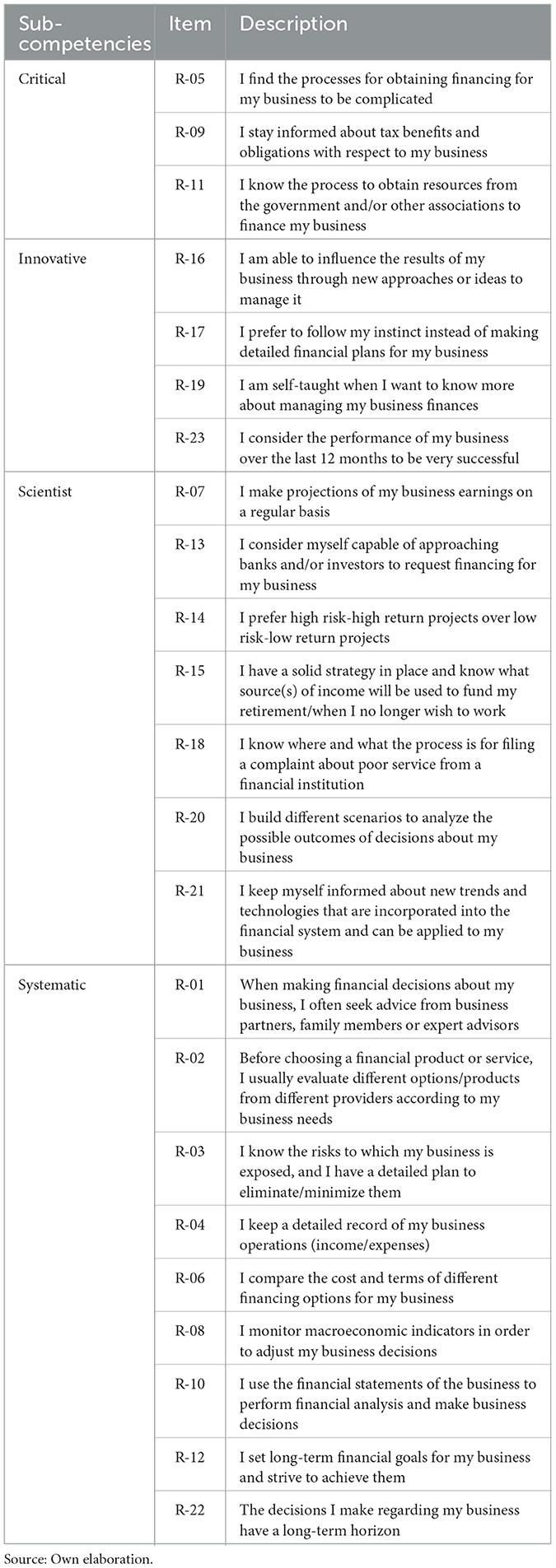

Once the results obtained during the validation process by expert judgment were integrated, a new version of the questionnaire was integrated with 23 items grouped into four dimensions associated with the sub-competences of complex thinking: (1) Scientific Thinking (SCT) with items R-01, R-02, R-05 and R-10, (2) Critical Thinking (CRT) with items R-06, R-12, R-13 and R15, (3) Innovative Thinking (INT) with items R-09, R-14, R-16, R-17, R-19 and R-23, and finally (4) Systematic Thinking (SYT) with items R-03, R-04, R-07, R-08, R-11, R-18, R-20, R-21 and R-22.

The questionnaire was applied online using the Google Forms tool. The results validation process consisted of performing an exploratory factor analysis in order to identify the relationships between the variables of interest and group them into latent factors or underlying constructs, as well as confirmatory factor analysis to confirm the underlying structure identified in a previous exploratory factor analysis (García and Caro, 2009; García-González et al., 2020). This statistical technique was performed using the SSPS tool in order to validate the dimensionality of the data set and its latent factors. The Kaiser–Meyer–Olkin (KMO) test was also performed as a measure of sampling adequacy used as a prior evaluation of data in terms of their adequacy to perform a factor analysis with an expected value between 0 and 1. The reliability of the instrument was calculated using Cronbach's alpha as a measure of reliability or internal consistency of the set of items included in the questionnaire. Cronbach's alpha ranges from 0 to 1, with values >0.7 being considered acceptable for most research purposes (González and Pazmiño, 2015). The data collection and analysis process took care of ethical aspects such as the confidentiality of the participants, their individual responses and the care of the personal data provided. The methodological quality, data management and interpretations of the results were taken care of throughout the research process.

Results

Content validity

Through the calculation of Aiken's V coefficient (Aiken, 1985), the relevance of the items with respect to a content domain was quantified based on the evaluations of the seven expert judges, with a result of total agreement among the judges for 39 of the 40 items evaluated, that is, they obtained a score higher than 0.71 in terms of clarity, relevance, coherence and correspondence. The content analysis of the qualitative observations made by the expert judges was also carried out, finding that all the observations corresponded to the Clarity dimension in nine of the items. In this sense, the observations were grouped in terms of suggestions for modification or elimination. As a result of this analysis, a second version of the questionnaire was constructed with the 23 items best evaluated by the group of expert judges, the results of which are shown in Table 2, which summarizes the value of Aiken's V coefficient calculated for each item and moves toward the reliability validity stage by piloting the instrument.

Table 2. Result of the calculation of the Aiken V coefficient.

Construct validity

The suitability of the data for factor analysis was verified by obtaining a KMO value equal to 0.928, whose reading indicates having an excellent sample to perform the factor analysis of the data. The results obtained from Bartlett's test of sphericity indicate that the value of the chi-square test statistic is 2,129.689 with 253 degrees of freedom and a significance level of <0.001, which allows rejecting the null hypothesis that the observed correlation matrix is equal to the expected correlation matrix for independent and uncorrelated variables and indicates that there is sufficient evidence to conclude that the variables are correlated. These statistical indicators reinforce that the sample size is adequate for the methodological objective of the study, in addition to what MacCallum et al. (1999) establish as a recommendation to ensure the validity and reliability of the results obtained, where sample sizes of between 100 and 200 participants are considered adequate for factor analyses in instrument validation studies.

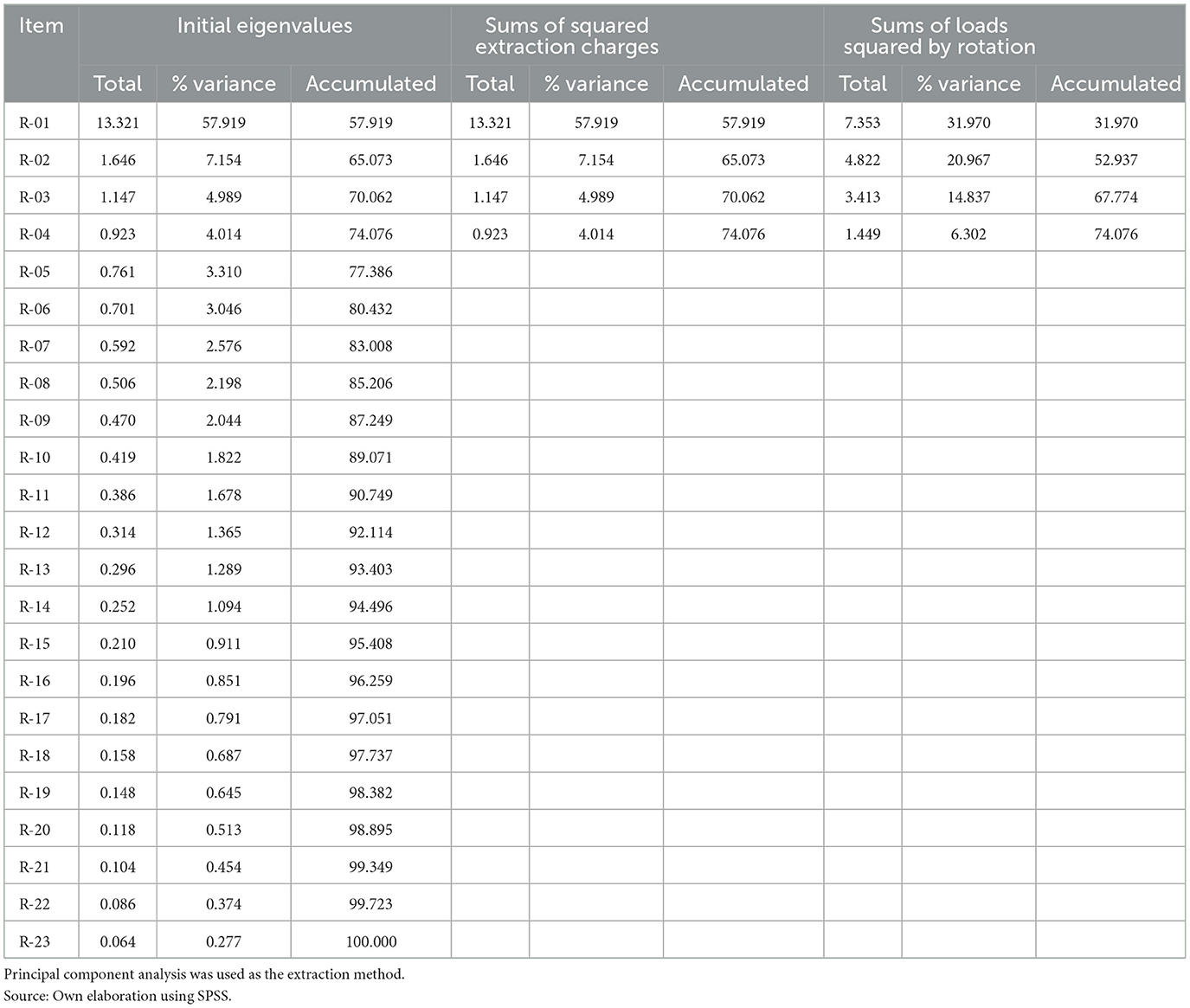

In the next stage of the factor analysis, the principal components table was analyzed with Kaiser normalization rotation and Varimax rotation, which seeks to maximize the variance explained by each component and minimize the variance shared among the components. Table 3 shows that it is possible to group four common factors that explain 74.076% of the accumulated variance.

Table 3. Total variance explained.

The extraction of four principal components shows in Table 4 the variables that are significantly associated with each of them when having loadings ≥0.3.

Table 4. Rotated component matrix.

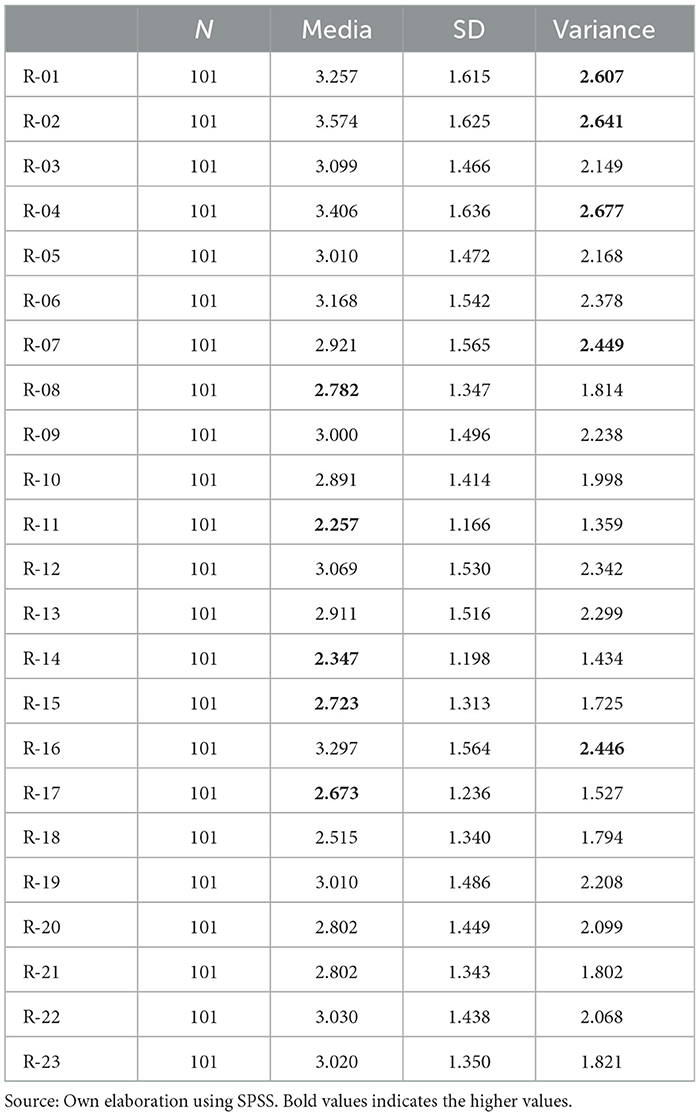

With respect to the data obtained during the piloting of the instrument, descriptive statistics were calculated for each item. Table 5 shows that the highest mean was 3.754 for item R-02, while the lowest mean was 2.257 for R-11.

Table 5. Descriptive statistics of the pilot test.

The confirmatory factor analysis establishes a model of relationships that empirically confirms the modeled structure of the instrument after the reclassification of the items as a result of the rotated component matrix analysis. The model fit indices are as follows:

• Comparative Fit Index (CFI): CFI value is 0.839. A CFI >0.90 generally indicates a good model fit, while values >0.80 can be considered acceptable.

• Tucker-Lewis Index (TLI): The TLI value is 0.818. Similar to CFI, a TLI >0.90 is indicative of a good model fit, while values >0.80 may be considered acceptable.

• Root Mean Square Error of Approximation (RMSEA): The RMSEA value is 0.122. An RMSEA ≤ 0.05 indicates a good model fit, while values between 0.05 and 0.08 indicate an acceptable fit. In this case, the RMSEA value suggests an acceptable model fit.

• Chi-square by degrees of freedom (X2/df): The X2 value is 558.472 and there are 224 degrees of freedom, resulting in an X2/df of ~2.49. An X2/df value close to 2 or less indicates a good model fit.

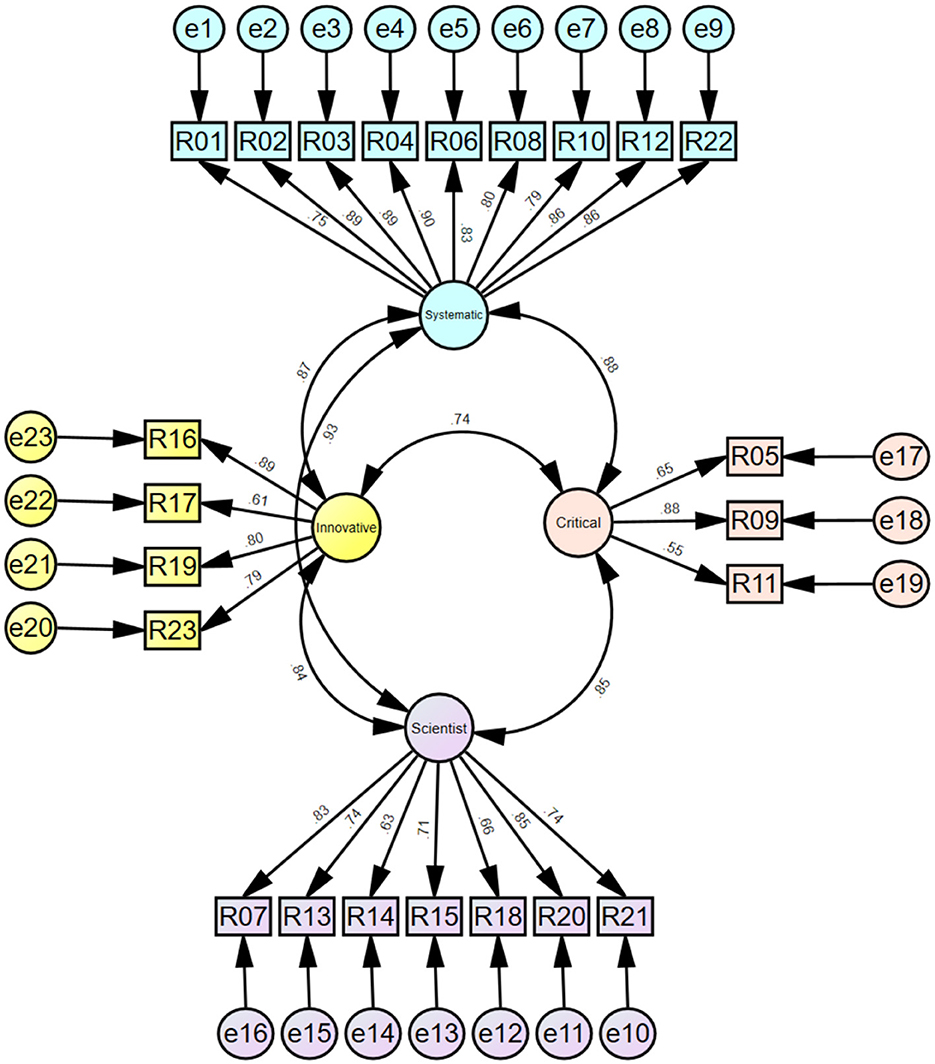

In summary, the fit indices suggest an acceptable overall model fit. Figure 1 presents the model generated, while Table 6 shows the reclassification of the items for the development of the final version of the measurement instrument.

Figure 1. Results of the confirmatory factor analysis after item reclassification. Source: Own elaboration using SPSS Amos.

Table 6. Reclassified reagents.

Finally, to measure the reliability of the instrument, the internal consistency of the instrument was estimated through the calculation of Cronbach's Alpha coefficient, obtaining a measurement precision of 0.966. According to the scale established for this measurement, the result is considered excellent.

Discussion and conclusions

The final version of the instrument allows measuring the level of financial literacy of women entrepreneurs in terms of attitudes, knowledge, behaviors and decision making aligned to the sub-competencies of complex thinking according to the results of the confirmatory factor analysis as shown in Figure 1, given the need to promote female entrepreneurship not only as a form of self-support but also as a source of employment generation and economic growth (UNESCO, 2017, 2020; INEGI, 2020; UN Women, 2021) through financial inclusion initiatives that offer an increase in financial literacy levels allowing women entrepreneurs to face and weather the ups and downs of the economy (Raccanello and Guzmán, 2014; Ali et al., 2018; Oggero et al., 2020; García-Mata, 2021a) but also help them to enable complex reasoning competencies needed in a constantly evolving business environment (Bay and Catasús, 2014; Dzwigol et al., 2020; Vanegas et al., 2020; Ramos et al., 2021). Knowing the level of financial literacy aligned to complex thinking competencies through the designed instrument allows the design and generation of effective financial literacy programs.

Content validity through expert judgment, as shown in Table 2, allowed establishing the relevance of the items designed (Escurra, 1988; Padilla García and Benítez, 2014; Sireci and Padilla, 2014; Matsumoto-Royo et al., 2021), while the exploratory and confirmatory factor analysis established the construct validity and its high relationship with the dimension assigned to them, as well as the reliability and internal consistency of the data validated by calculating Cronbach's Alpha (García and Caro, 2009; González and Pazmiño, 2015; García-González et al., 2020). The information collected through the instrument can be used in financial literacy programs with emphasis on complex thinking sub-competencies for financial decision making in business.

The analyses carried out show that the instrument designed is a valid and reliable measure of financial literacy aligned with complex thinking competencies in Mexican women entrepreneurs. In conclusion, this study has generated an innovative instrument that can be used to measure the mastery not only of attitudes, knowledge, behaviors and financial decision-making of women entrepreneurs in Mexico, but also their interrelation with the sub-competencies of complex thinking that are necessary in the daily practice of entrepreneurship in the country.

A possible limitation of this study is related to the participants, since it was applied to women with some initiative to support entrepreneurship and who also have access to the internet through a mobile device, which leaves out those with lower socioeconomic status and/or limited use of electronic devices or digital media or who do not belong to any network to promote entrepreneurship. The validation of this instrument through its application to a population sample that includes women entrepreneurs who do not have the support of business development initiatives and in areas with limited access to internet or mobile devices is recommended to cover this limitation. Another future line of research is the design of longitudinal research to measure the effects over time of a personalized financial literacy initiative and its impact not only on the lengthening of the life of the business but also on its growth and performance levels, on the other hand, the possibility of studying in depth the impact of the empowerment in complex thinking skills for the empowerment of female entrepreneurship is generated.

Data availability statement

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

Ethics statement

Ethical approval was not required for the study involving human participants in accordance with the local legislation and institutional requirements. Written informed consent to participate in this study was not required from the participants in accordance with the national legislation and the institutional requirements.

Author contributions

KB-C: Conceptualization, Data curation, Formal analysis, Investigation, Methodology, Project administration, Validation, Writing – original draft, Writing – review & editing. MR-M: Funding acquisition, Methodology, Supervision, Writing – review & editing. AE-R: Writing – review & editing. MM-B: Writing – review & editing.

Funding

The author(s) declare that financial support was received for the research, authorship, and/or publication of this article. The authors acknowledge the financial support of Tecnologico de Monterrey through the “Challenge-Based Research Funding Program 2022”. Project ID # I005 - IFE001 - C2-T3 - T also academic support from Writing Lab, Institute for the Future of Education.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

The author(s) declared that they were an editorial board member of Frontiers, at the time of submission. This had no impact on the peer review process and the final decision.

Publisher's note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Agnew, S., Maras, P., and Moon, A. (2018). Gender differences in financial socialization in the home-an exploratory study. Int. J. Consum. Stud. 42, 275–282. doi: 10.1111/ijcs.12415

Aiken, L. R. (1985). Three coefficients for analyzing the reliability and validity of ratings. Educ. Psychol. Meas. 45, 131–142. doi: 10.1177/0013164485451012

Ali, H., Omar, E. N., and Nasir, H. A. (2018). “Financial literacy of entrepreneurs in the small and medium enterprises,” in Proceedings of the 2nd Advances in Business Research International Conference, eds. F. Noordin, A. K. Othman, and E. S. Kassim (New York, NY: Springer), 31–38. doi: 10.1007/978-981-10-6053-3_4

Anshika and Singla, A.. (2022). Financial literacy of entrepreneurs: a systematic review. Manag. Financ. 48, 1352–1371. doi: 10.1108/MF-06-2021-0260

Anshika, Singla, A., and Mallik, G. (2021). Determinants of financial literacy: empirical evidence from micro and small enterprises in India. Asia Pac. Manag. Rev. 26, 248–255. doi: 10.1016/j.apmrv.2021.03.001

Baporikar, N., and Akino, S. (2020). Financial literacy imperative for success of women entrepreneurship. Int. J. Innov. Digit. Econ. 11, 1–21. doi: 10.4018/IJIDE.2020070101

Barte, R. (2012). Financial Literacy in MicroEnterprises: The Case of Cebu Fish Vendors. Philippine Management Review. Available online at:https://www.semanticscholar.org/paper/Financial-Literacy-in-Micro%C2%ADEnterprises%3A-The-Case-Barte/30d8488d3afac1532fb69377e5e00990e2c0527e (accesed November 4, 2023).

Bay, C., and Catasús, B. (2014). Situating financial literacy. Crit. Perspect. Account. 25, 36–45. doi: 10.1016/j.cpa.2012.11.011

Bertrand, J., and Osei-Tutu, F. (2022). Language gender-marking and borrower discouragement. Econ. Lett. 212:110298. doi: 10.1016/j.econlet.2022.110298

CNBV, I. (2012). National Financial Inclusion Survey (ENIF). Comisión Nacional Bancaria y de Valores, 85. Available onlie at: https://www.cnbv.gob.mx/Inclusi%C3%B3n/Paginas/Encuestas.aspx (accesed November 4, 2023).

Cruz-Sandoval, M., Vázquez-Parra, J. C., and Carlos-Arroyo, M. (2023). Complex thinking and social entrepreneurship. an approach from the methodology of compositional data analysis. Heliyon 9:e13415. doi: 10.1016/j.heliyon.2023.e13415

Dzwigol, H., Dzwigol-Barosz, M., Miśkiewicz, R., and Kwilinski, A. (2020). Manager competency assessment model in the conditions of industry 4.0. Entrep. Sustain. Iss. 7, 2630–2644. doi: 10.9770/jesi.2020.7.4(5)

Eniola, A. A., and Entebang, H. (2017). SME managers and financial literacy. Glob. Bus. Rev. 18, 559–576. doi: 10.1177/0972150917692063

Escobar-Pérez, J., and Martínez, A. (2008). Content validity and expert judgment: an approach to their use. Av. Medición 6, 27–36. doi: 10.32870/ap.v9n2.993

Escurra, L. M. (1988). Quantification of content validity by criterion judges. J. Psychol. 6, 103–111.

García, J. A. M., and Caro, L. M. (2009). Confirmatory factor analysis and the validity of scales in causal models. Ann. Psychol. 25:2. doi: 10.6018/analesps

García-González, A., Ramírez-Montoya, M. S., and León, G. D. (2020). Social entrepreneurship as a transversal competence: construction and validation of an assessment instrument in the university context. REVESCO J. Coop. Stud. 136:e71862. doi: 10.5209/reve.71862

García-Mata, O. (2021a). The effect of financial literacy and gender on retirement planning among young adults. Int. J. Bank Market. 39, 1068–1090. doi: 10.1108/IJBM-10-2020-0518

García-Mata, O. (2021b). Financial literacy among millennials in Ciudad Victoria, Tamaulipas, Mexico. Estud. Gerenciales 37, 399–412. doi: 10.18046/j.estger.2021.160.4021

González, J. A., and Pazmiño, M. R. (2015). Calculation and interpretation of Cronbach's Alpha for the case of validation of the internal consistency of a questionnaire, with two possible Likert-type scales. Rev. Publ. 2, 62–77. Available online at: https://nbn-resolving.org/urn:nbn:de:0168-ssoar-423821

Guliman, S. D. (2015). An evaluation of financial literacy of micro and small enterprise owners in Iligan city: knowledge and skills. J. Glob. Bus. 4, 17−23.

INEGI (2020). Economic Censuses 2019. Available online at: https://www.inegi.org.mx/programas/ce/2019/ (accesed November 4, 2023).

INEGI (2021). Encuesta Nacional de Inclusión Financiera (ENIF) 2021 (p. 30). Available online at: https://www.inegi.org.mx/programas/enif/2021/#Documentacion (accesed November 4, 2023).

INMUJERES (2022). Inequality in figures (Bulletin No. 5). National Institute of Women, 2. Available online at: http://estadistica-sig.inmujeres.gob.mx/formas/temas.php (accesed November 4, 2023).

Lusardi, A. (2001). Explaining Why so Many People Do Not Save (SSRN Scholarly Paper No. 285978). Rochester, NY. doi: 10.2139/ssrn.285978

Lusardi, A. (2008). Planning and financial literacy: how do women fare? American Econ. Rev. 98, 413–417. doi: 10.1257/aer.98.2.413

Lusardi, A. (2011). Financial literacy around the world: an overview. J. Pension Econ. Finan. 10, 497–508. doi: 10.1017/S1474747211000448

Lusardi, A., and Mitchell, O. (2009). How Ordinary Consumers Make Complex Economic Decisions: Financial Literacy and Retirement Readiness (No. w15350; p. w15350). Cambridge, MA: National Bureau of Economic Research. doi: 10.3386/w15350

MacCallum, R., Widaman, K., Zhang, S., and Hong, S. (1999). Sample size in factor analysis. Psychol. Methods 4, 84–99. doi: 10.1037/1082-989X.4.1.84

Manzanera-Román, S., and Brändle, G. (2016). Abilities and skills as factors explaining the differences in women entrepreneurship. Suma Neg. 7, 38–46. doi: 10.1016/j.sumneg.2016.02.001

Matsumoto-Royo, K., Ramírez-Montoya, M.-S., and Conget, P. (2021). Design and validation of a questionnaire to assess opportunities for pedagogical practice, metacognition and lifelong learning provided by initial teacher education programs. Stud. Educ. 41, 131–161.

Muñoz-Murillo, M., Álvarez-Franco, P. B., and Restrepo-Tobón, D. A. (2020). The role of cognitive abilities on financial literacy: new experimental evidence. J. Behav. Exp. Econ. 84:101482. doi: 10.1016/j.socec.2019.101482

Niwaha, M., Tibihikirra, P., and Tumuramye, P. (2016). Entrepreneurship and financial literacy: an insight into financial practices of rural small and micro business owners in the Rwenzori region.

OECD (2018). Pisa results (Volume IV): Are students smart about money? Available online at: https://www.oecd.org/education/pisa-2018-results-volume-iv-48ebd1ba-en.htm (accesed November 4, 2023).

OECD (2019). OECD/INFE survey instrument to measure the financial literacy of MSMEs, 42. Available online at: https://www.oecd.org/financial/education/2020-survey-to-measure-msme-financial-literacy.pdf (accesed November 4, 2023).

OECD (n/d). Financial Literacy test-PISA. Available online at: https://www.oecd.org/pisa/test/financialliteracytest/ (accessed March 12 2023).

Oggero, N., Rossi, M. C., and Ughetto, E. (2020). Entrepreneurial spirits in women and men. The role of financial literacy and digital skills. Small Bus. Econ. 55, 313–327. doi: 10.1007/s11187-019-00299-7

Osei-Tutu, F., and Weill, L. (2021). Sex, language and financial inclusion*. Econ. Trans. Inst. Change 29, 369–403. doi: 10.1111/ecot.12262

Pacheco-Velázquez, E. A., Vázquez-Parra, J. C., Cruz-Sandoval, M., Salinas-Navarro, D. E., and Carlos-Arroyo, M. (2023). Business decision-making and complex thinking: a bibliometric study. MDPI 13:80. doi: 10.3390/admsci13030080

Padilla García, J. L., and Benítez, I. (2014). Validity Evidence Based on Response Processes. Granada.

Penfield, R. D., and Giacobbi, P. R. Jr. (2004). Applying a score confidence interval to aiken's item content-relevance index. Meas. Phys. Educ. Exerc. Sci. 8, 213–225. doi: 10.1207/s15327841mpee0804_3

Raccanello, K., and Guzmán, E. H. (2014). Education and financial inclusion. Rev. Latinoam. Estud. Educativos 44:2. doi: 10.48102/rlee.2014.44.2.250

Rachapaettayakom, P., Wiriyapinit, M., Cooharojananone, N., Tanthanongsakkun, S., and Charoenruk, N. (2020). The need for financial knowledge acquisition tools and technology by small business entrepreneurs. J. Innov. Entrep. 9. doi: 10.1186/s13731-020-00136-2

Rahim, S., and Binod, R. B. (2021). Financial literacy: the impact on the profitability of the SMEs in kuching. Int. J. Bus. Soc. 21, 1172–1191. doi: 10.33736/ijbs.3333.2020

Ramírez-Montoya, M. S., Castillo-Martínez, I. M., Sanabria-Zepeda, J., and Miranda, J. (2022). Complex thinking in the framework of education 4.0 and open innovation: a systematic literature review. J. Open Innov. Technol. Mark. Complex. 8. doi: 10.3390/joitmc8010004

Ramos, E. V. R., Otero, C. A., and Heredia, F. D. (2021). Competency-based training of the management professional: from a contingency approach. Rev. Cienc. Soc. 451–466. doi: 10.31876/rcs.v27i2.35933

Sireci, S., and Padilla, J. L. (2014). Validating assessments: introduction to the special section. Psicothema 26, 97–99. doi: 10.7334/psicothema2013.255

UN Women (2021). Win-Win: Gender Equality is Good Business. UN Women. Available online at: https://lac.unwomen.org/es/digiteca/publicaciones/2021/09/ganar-ganar-la-igualdad-de-genero-es-un-buen-negocio (accesed November 4, 2023).

UNESCO (2017). UNESCO Moves Forward. The 2030 Agenda for Sustainable Development. United Nations Educational, Scientific and Cultural Organization. Available online at: https://es.unesco.org/creativity/files/unesco-avanza-agenda-2030-para-desarrollo-sostenible (accesed November 4, 2023).

UNESCO (2020). Summary of the Global Education Monitoring Report, 2020: Inclusion and Education: All without Exception. Available online at: https://unesdoc.unesco.org/ark:/48223/pf0000373721_spa (accesed November 4, 2023).

Valenzuela, J. R., and Flores Fahara, J. R. (2013). Fundamentos de Investigación Educativa, Vol. 2, 1st Edn. Monterrey: Editorial Digital Tecnológico de Monterrey.

Vanegas, J. G., Mesa, M. A. A., and Gómez-Betancur, L. (2020). Financial education in women: a study in the López de Mesa neighborhood of Medellín1. Rev. Fac. Cienc. Econ. 28, 121–141. doi: 10.18359/rfce.4929

Vázquez-Parra, J. C., Castillo-Martínez, I. M., and Ramírez-Montoya, M. S. (2022a). Development of the perception of achievement of complex thinking: a disciplinary approach in a Latin American student population. Educ. Sci. 12:5. doi: 10.3390/educsci12050289

Vázquez-Parra, J. C., Castillo-Martínez, I. M., Ramírez-Montoya, M. S., and Amézquita-Zamora, J. A. (2023). Gender gap in the perceived mastery of reasoning-for-complexity competency: an approach in Latin America. J. Appl. Res. High. Educ. 12. doi: 10.1108/JARHE-11-2022-0355

Vázquez-Parra, J. C., Cruz-Sandoval, M., and Carlos-Arroyo, M. (2022b). Social Entrepreneurship and complex thinking: a bibliometric study. Sustainability 14:20. doi: 10.3390/su142013187

Keywords: financial literacy, complex thinking, measurement instrument, higher education, educational innovation

Citation: Bayly-Castaneda K, Ramírez-Montoya MS, Erdély-Ruiz A and Montoya-Bayardo MA (2024) Financial literacy to develop complex thinking skills: quantitative measurement in Mexican women entrepreneurs. Front. Educ. 9:1331866. doi: 10.3389/feduc.2024.1331866

Received: 01 November 2023; Accepted: 29 May 2024;

Published: 03 July 2024.

Edited by:

Muhammad Kristiawan, University of Bengkulu, IndonesiaReviewed by:

María Teresa De La Garza Carranza, Tecnológico Nacional de México, MexicoSílvio Manuel da Rocha Brito, Polytechnic Institute of Tomar (IPT), Portugal

Copyright © 2024 Bayly-Castaneda, Ramírez-Montoya, Erdély-Ruiz and Montoya-Bayardo. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: María Soledad Ramírez-Montoya, c29scmFtaXJleiYjeDAwMDQwO3RlYy5teA==

†ORCID: Karla Bayly-Castaneda orcid.org/0000-0002-4170-6072

María Soledad Ramírez-Montoya orcid.org/0000-0002-1274-706X

Arturo Erdély-Ruiz orcid.org/0000-0003-1653-8342

Miguel Angel Montoya-Bayardo orcid.org/0000-0002-5545-6334