Bianca Wutzler

Bianca Wutzler Paul Hudson1,2

Paul Hudson1,2- 1Institute of Environmental Science and Geography, University of Potsdam, Potsdam, Germany

- 2Department of Environment and Geography, University of York, York, United Kingdom

Flood risk management in Germany follows an integrative approach in which both private households and businesses can make an important contribution to reducing flood damage by implementing property-level adaptation measures. While the flood adaptation behavior of private households has already been widely researched, comparatively less attention has been paid to the adaptation strategies of businesses. However, their ability to cope with flood risk plays an important role in the social and economic development of a flood-prone region. Therefore, using quantitative survey data, this study aims to identify different strategies and adaptation drivers of 557 businesses damaged by a riverine flood in 2013 and 104 businesses damaged by pluvial or flash floods between 2014 and 2017. Our results indicate that a low perceived self-efficacy may be an important factor that can reduce the motivation of businesses to adapt to flood risk. Furthermore, property-owners tended to act more proactively than tenants. In addition, high experience with previous flood events and low perceived response costs could strengthen proactive adaptation behavior. These findings should be considered in business-tailored risk communication.

Introduction

Flooding is a significant threat for human well being, via impacts on health and economic activity. According to Munich Re (2018), floods have accounted for 40% of disasters worldwide since 1980. Additionally, the European Environment Agency (2019) states that floods accounted for a total loss of EUR 162 billion across the EEA member states over the same period. Just recently, i.e., in July 2021, Belgium, Germany, Luxembourg, and the Netherlands were hit by devastating floods that occurred because of heavy and continuous rainfall. More than 180 people lost their lives in Germany, while 38 individuals lost their lives in Belgium (Kreienkamp et al., 2021). In some towns, e.g., in Bad Münstereifel or Euskirchen, the inner cities and main shopping streets were severely damaged and forced the commercial sector out of business. In total, 30 billion euros are provided for recovery and reconstruction in Germany alone (Federal Ministry of the Interior and Community, 2021).

Flood risks can be summarized as the interaction between hazard, exposure, and vulnerability (Kron, 2005; IPCC, 2022). Hazard is the combination of the probability of a flood occurring and its potential magnitude. Exposure is the quantity and value of people or assets located in flood-prone areas, while vulnerability captures how susceptible affected objects are to suffering damage during a flood (Kron, 2005; IPCC, 2022). One main avenue for limiting flood damage is through regional flood protection (e.g., levees) that aims to prevent inundation of land up to the design value of the structures, often up to a 100-year flood. However, flood damage cannot be completely prevented by such structural measures owing to physical limitations or because such investments are not cost-beneficial (Bos and Zwaneveld, 2017). Residents and businesses in floodplains can lower their level of vulnerability via employing protective or preparatory measures at their properties, which lower potential flood impacts. For example, such property-level measures are flood-adapted building use (e.g., avoiding expensive assets in the flood-prone parts of the building), flood-proof interior fitting (e.g., by water resistant materials) or having a water pump available helps to restore flooded properties. Even during extreme events like the catastrophic flood in August 2002 in Central Europe, these measures were highly effective (Kreibich et al., 2005). The observation that a multitude of such adaptation measures exist, is important because it is expected that damage from floods will increase in the future (IPCC, 2022). That is mainly because the threatened areas on rivers and coasts become more populated, while climate change potentially alters the frequency and intensity of extreme precipitation in some regions (Merz et al., 2007; IPCC, 2022). Therefore, flood risk management strategies need to be expanded and improved (Kreibich et al., 2015). For this reason, there is a growing focus on integrated flood risk management concepts in which all the actors who contribute toward flood risk generation should take actions to reduce flood risk (Merz et al., 2010; Bubeck et al., 2016; Kuhlicke et al., 2020a). For example, since 2005 property-owners in flood-prone areas in Germany are obliged to reduce flood damage to the best of their ability [§5(2) in the German Federal Water Act].

In line with this movement, there is a growing understanding of how and why private households adapt to floods and which factors influence their decision whether they implement property-level adaptation measures (e.g., Grothmann and Reusswig, 2006; Bubeck et al., 2012; Koerth et al., 2013). For example, prior experience with floods and perceived effectiveness of property-level measures seem to be important drivers for private adaptation (Grothmann and Reusswig, 2006). On the other hand, there is relatively less research on adaptation strategies of businesses (Kreibich et al., 2007) although they also suffer greatly from flood events (DKKV (German Committee for Disaster Prevention), 2015; Jehmlich et al., 2020). Direct damage in the corporate sector after the disastrous event in 2013 were estimated to be around EUR 1.32 billion (Federal Ministry of the Interior Building Community, 2013).

There have been some studies lately that gave insights into the flood management of businesses. Neise and Revilla Diez (2019) revealed that adaptation strategies are related to the business size using the cities Jakarta and Semerang (Indonesia) as case studies. Small businesses can less effectively adapt to flood risk than large or medium-sized businesses due to lower financial resources and competitiveness (Neise and Revilla Diez, 2019). Moreover, there were shortcomings in business continuity planning among small and medium-sized businesses in Thailand (Kato and Charoenrat, 2017). Experience with previous flooding was found to be an important driver for precautionary behavior of businesses according to Herbane (2015), Jehmlich et al. (2020), and Kuhlicke et al. (2020b). Similarities in flood preparedness, adaptive behavior and recovery of small businesses and private households in Can Tho city (Vietnam) were found by Chinh et al. (2016) and in Germany by Hudson et al. (2022). Furthermore, Sieg et al. (2017) stated that damage processes and therefore needs for adaptation differ between business sectors. Bhattacharya-Mis et al. (2018) found that professionals in the construction sector who could act as flood protection advisors to businesses are not sufficiently educated about flood risk.

More research is still needed to detect the adaptation patterns of businesses to serve as entry points for tailored risk communication and to further investigate drivers for their actions within the sphere of climate change adaptation and disaster risk reduction (Forino and von Meding, 2021). Therefore, this study focuses on the following two questions to provide a wider baseline of inferences from our exploratory analysis: (a) Which strategies do businesses in Germany choose to adapt to floods? and (b) Which factors influence the choice of a specific adaptation strategy? Two data sets are compared that relate to different flood events and flood types in Germany. For the first dataset, businesses were surveyed that were damaged by a riverine flood event in 2013 and the second data set surveyed businesses that were damaged by pluvial floods (also known as urban floods or sometimes flash floods in hilly regions) between 2014 and 2017. Since responses and coping options were found to be different in private households affected by fluvial flooding in 2013 from those affected by pluvial flooding in 2016 (Thieken et al., 2022), this paper explores adaptation strategies of businesses for these flood types, too.

The findings of this research contribute to a better understanding of adaptation of businesses in flood-prone areas. On this foundation, measures can be derived to better support businesses in the future. Additionally, this study intends to provide indications for later studies on how businesses adapt to flood risk and what could influence their capabilities to reduce flood damage. In part we achieve this by using questions and theoretical frameworks designed for private households and individuals and apply them to businesses. An outcome of this approach is to better link the disparate strands of research.

Character and impacts of the flood events studied

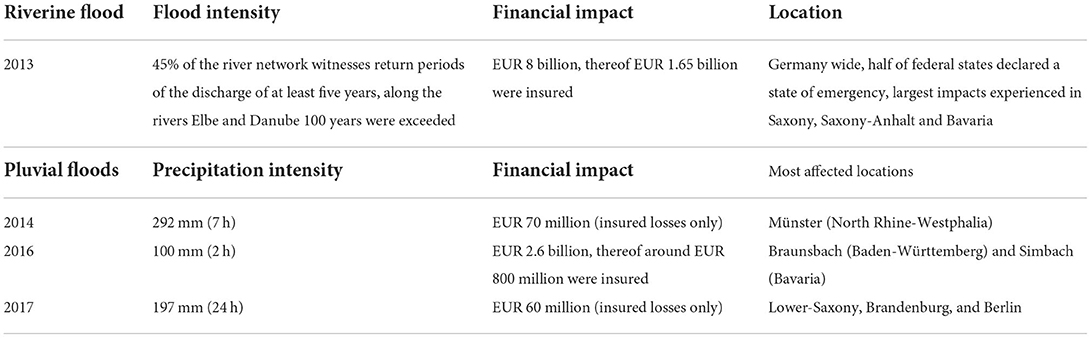

For this study, the extensive river flood that hit Central Europe, particularly Germany, in June 2013 was taken as case study for a fluvial flood. Already in May of 2013, monthly rainfall amounts were above average and led to record-breaking soil moisture in large areas (DWD – Deutscher Wetterdienst, 2013) and high streamflows (Thieken et al., 2016a). Torrential rain from 31 May to 2 June 2013 then resulted in high shares of surface runoff and consequently flood peaks and inundations along the rivers Upper Rhine, Weser as well as Danube and Elbe in particular (Merz et al., 2014; Schröter et al., 2015; Thieken et al., 2016a). Flood frequency analyses revealed that this event was Germany's most severe fluvial flood since 1950 (Merz et al., 2014) affecting 45% of the German river network (Schröter et al., 2015). As a result, eight out of the 16 German federal states declared a state of emergency (BMI, 2013 as cited in Thieken et al., 2016a,b). As direct impacts, 14 people were reported dead and direct losses summed up to EUR 8 billion, from which around 19% were allocated to industry and commerce (Thieken et al., 2016b). In addition, business interruptions and traffic disruption caused further (indirect) impacts (Thieken et al., 2016b).

After 2013, heavy pluvial and flash floods occurred at different places across Germany causing considerable damage. On 28 July 2014, the city of Münster in North Rhine-Westphalia witnessed torrential rainfall of up to 292 mm in 7 h due to incoming hot and humid air that collided with a cold front. The event flooded almost the whole city with 310,000 inhabitants and caused insured losses of more than EUR 70 million (Spekkers et al., 2017); two people died. While this event was mainly localized around Münster, a series of severe and just slowly moving convective storms hit several places in Germany, particularly Braunsbach in Baden-Württemberg and Simbach in Bavaria, from 26 May to 9 June 2016 (Piper et al., 2016). Intense rainfall of more than 100 mm within 24 h (Piper et al., 2016) or even within just 2 h in Braunsbach (Bronstert et al., 2017) caused devastating flash floods with overall losses of EUR 2.6 billion (Munich Re, 2017); 11 people lost their lives. In 2017, heavy rain events again caused considerable damage in Lower-Saxony, Brandenburg, and Berlin (Dillenardt et al., 2022).

An overview of the hydrological and financial impacts of the studied floods is provided in Table 1. The material and methods section below builds on a survey dataset based on experiences in relation to these flood events.

Table 1. Overview of the hydrological and financial impacts of large floods in Germany between 2013 and 2017.

Materials and methods

Between 12 May and 17 July 2014, businesses that had suffered (financial) flood damage from the 2013-event were surveyed on their impacts, adaptation strategies and further topics, i.e., around one year after the flood. Potentially affected premises were called by a sub-contracted pollster and were guided through a standardized questionnaire (also called computer-aided telephone interviews—CATI). To retrieve the phone numbers, lists of affected streets and zip codes were compiled based on information from affected municipalities and flood reports as well as by an intersection of street maps with inundation areas. Big businesses that were explicitly reported affected in flood documentations were added to the sample. The questionnaire had been adapted from former surveys (see Kreibich et al., 2007; Thieken et al., 2017) and contained around 90 questions on the following topics:

- Business characteristics (sector, number of employees, number of buildings, assets, perceived vulnerability with regard to flooding, etc.,);

- Hydraulic characteristics of the flood at the business premise;

- Flood warnings and response (emergency measures);

- Contamination and clean-up work;

- (Financial) flood damage (to buildings, operational facilities, merchandise, products, and warehouse inventory, motor vehicle inventory; due to interruptions of operations);

- Reconstruction, compensation, plans to relocate;

- Previously experienced floods;

- Long-term preventive or protective measures at the site of the premise.

In total, 557 interviews across nine federal states were completed (see Thieken et al., 2016b). 35% (n = 197) of the surveyed businesses were located in Saxony, 24% (n = 133) in Saxony-Anhalt, 21% (n = 119) in Thuringia, and 16% (n = 88) in Bavaria. This pattern reflects the severity and extent of the flood.

Companies affected by pluvial or flash floods between 2014 and 2017 were surveyed from 17 October to 21 November 2017 using the same questionnaire; questions were partly rephrased to better address the different flood type. Since flooding was more localized, it was challenging to identify affected businesses. Despite huge efforts, just 103 cases were gathered, of which 12 businesses were affected in 2014, 7 in 2015, 75 in 2016, and another 9 in 2017.

Classifications of adaptation strategies

All surveyed businesses were assigned to different adaptation strategies based on the following six groups of strategies that were originally proposed by Neise and Revilla Diez (2019): proactive adaptation, reactive adaptation, relocation, surrendering, depending, and collaboration (see below). This classification directly addresses flood risk and therefore it stands out from other typologies that rather focus on impacts of climate change in general (Neise and Revilla Diez, 2019). In adapting this group classification to our study, we assume that each group is mutually exclusive, i.e., a business can be allocated to one group based on the dominate activity they employ. In doing so, we find the following modified classification groups best fit our dataset: proactive, reactive, reactive and proactive, relocation and passive. These strategies will be further characterized below; an overview of each group's characteristics is provided in Table 2.

Table 2. Overview of the adaptation strategies.

Neise and Revilla Diez (2019) define the proactive adaptation strategy as corresponding to businesses that are well-informed and active regarding flood risk and their options to limit flood damage. These businesses lower their vulnerability by implementing long-term adaptation measures, e.g., water barriers in and around the building or a flood adapted building use. In this study all businesses were assigned to the proactive strategy that implemented at least one of (and only) the listed long-term measures (Table 2) before the flood that we find best fits to the definition of Neise and Revilla Diez (2019).

The reactive group is less flexible with respect to changing flood patterns and relies on short-term emergency measures (e.g., pumps) and established routines (Neise and Revilla Diez, 2019). Undertaking emergency measures before or during the flood, but no precautionary action, therefore was the decisive factor for a business to be assigned to the reactive strategy.

It is also possible that these two strategies co-exist. Therefore, the group reactive and proactive was formed by businesses that use both proactive and reactive adaptation strategies.

The relocation group includes all businesses that already moved at the time of the interview from the place where they had been hit by the flood or that planned to do so within the next six months.

Furthermore, there are businesses that do not undertake adaptive measures themselves. Neise and Revilla Diez (2019) distinguish “depending” from “surrendering” businesses. The businesses that fall into the “depending” group rely on regional flood protection, aid from external stakeholders (e.g., insurance) or financial aid from public institutions after a flood event (Neise and Revilla Diez, 2019). Businesses in the “depending” group confirmed the employment of at least one of these factors in the interview and did not implement any damage-reducing measures. If a business did not fit into any of the before mentioned groups it was assigned to the surrendering strategy, also called the “wait-and-see”-strategy (Neise and Revilla Diez, 2019). These businesses have neither implemented any of the investigated measures to limit flood risk, nor have they indicated that they feel protected by other structures such as regional flood protection. After allocating businesses of our data sets to these groups (depending, and surrendering), their sample sizes were small. Therefore, both groups were merged for data analysis and form the passive strategy because both strategies indicate that the businesses do not actively reduce their flood risk though slightly different in focus.

Finally, Neise and Revilla Diez (2019) define the collaboration strategy, which is characterized by the fact that these firms prefer to use their resources to support joint protection measures with other businesses or public institutions, rather than adapting individually to protect everyone effectively. For example, neighboring businesses could collect money to build a flood barrier for the whole street (Neise and Revilla Diez, 2019). Since the questionnaire did not address collaborative flood protection measures, this strategy was left out of the analysis.

Data analysis

Theoretical basis for explanatory variable selection

There are several influencing factors that have already been identified to explain flood preparedness of private households or individual adaptation strategies against flood hazard. In the context of this work, the most important of these factors are analyzed in relation to the adaptive behavior of businesses.

The Protection Motivation Theory (PMT) from Rogers (1975) has been used in the context of flood protection in various studies (e.g., Grothmann and Reusswig, 2006; Bubeck et al., 2012, 2018). Two main components that influence the response to a hazard were identified: threat appraisal and coping appraisal. Several studies (Takao et al., 2004; Kreibich et al., 2005; Siegrist and Gutscher, 2006; Thieken et al., 2006, 2007; Lindell and Hwang, 2008; Dillenardt et al., 2022) found that threat appraisal, which includes the perceived flood probability and the perceived severity of a flood, is unreliable to predict whether adaptive measures are carried out or not. This is primarily the result of cross-sectional survey design, in which a respondent is asked for their risk perceptions after having potentially implemented adaptive behaviors, which alter their risk perceptions from their pre-adaptive levels (Bubeck et al., 2020). Additionally, the threat appraisal factor was not fully covered by the survey (i.e., only the perceived probability component and not the perceived impact element). Therefore, while threat appraisal is part of PMT, we have elected to omit threat appraisal as a consideration in the following data analysis. This is due to the potential measurement error that the two aforementioned problems could introduce into our analysis. Instead, perceived self-efficacy, perceived response efficacy and perceived response costs were considered as three factors of coping appraisal. According to Grothmann and Reusswig (2006) these variables have significantly higher explanatory power for private adaptive behavior than perceived risk of flooding when using cross-sectional data.

Furthermore, PMT can be extended by additional variables that help explain adaptive behavior. Former studies found that experience with floods is a significant driver to lower flood risk (e.g., Grothmann and Reusswig, 2006; Botzen et al., 2019; Kuhlicke et al., 2020a). Similarly important is the ownership of the building. For private households tenants are less motivated to implement adaptive measures than owners because the financial consequences are lower for them and they do not have the authority to implement changes to the building (Kreibich et al., 2005; Thieken et al., 2007; Bubeck et al., 2012; Dillenardt et al., 2022). Moreover, for businesses Neise and Revilla Diez (2019) found connections between business size and adaptation strategies. Large businesses are more likely to adopt a proactive strategy or move to another region, whereas smaller businesses tend to adopt a reactive strategy or surrender. These three variables are hence included in our data analyses.

Correlation and regression analyses

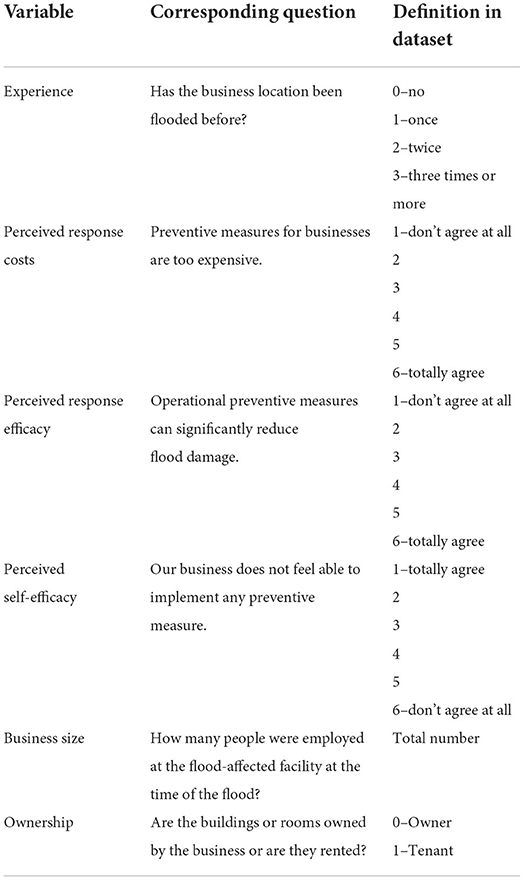

To investigate connections between the choice of an adaptation strategy and possible factors influencing that choice, correlation analyses were carried out for all five adaptation strategies in combination with the core PMT variables that were described above (perceived response costs, response efficacy, self-efficacy) and the variables previous flood experience, business size (in terms of the number of employees) and property ownership. Table 3 summarizes how these variables were defined in the dataset.

Table 3. Overview of the analyzed variables.

The correlation of the variables experience, perceived response costs, response efficacy, and self-efficacy with the adaptation strategies of the businesses was calculated after Spearman-Rho. Furthermore, the variable ownership was analyzed with a contingency table and the Phi-correlation-coefficient. In this study the number of employees was used as an indicator for business size and correlations were tested with Pearson correlation coefficients.

For a closer examination of possible influences on adaptive behavior, a binary logistic regression analysis was carried out for each adaptation strategy in addition to the correlation analyses. The selected adaptation strategies are the dependent variable in each case. The same factors as in the correlation analysis, namely experience, perceived response costs, perceived response efficacy, perceived self-efficacy, business size and property ownership were examined as independent variables.

Results and discussion

Distribution of adaptation strategies

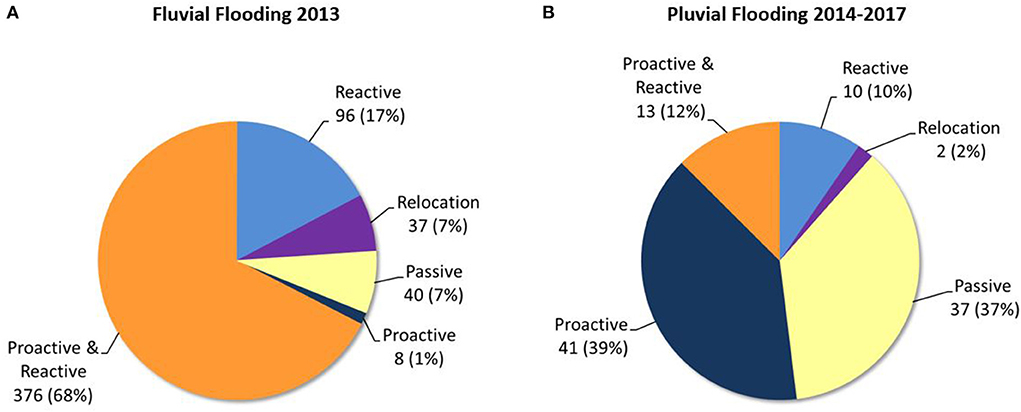

Figure 1 provides an overview of adaptation strategies that the surveyed businesses choose to protect themselves against flood damage.

Figure 1. Absolute and relative frequencies of the adaptation strategies chosen by the businesses damaged by the flood (A) 2013 (n = 557, source: survey 2014), (B) 2014–2017 (n = 103, source: survey 2017).

Regarding Figure 1A by far the largest share of the businesses (376; 68%) belongs to the group proactive and reactive. Accordingly, most businesses pursue a mixed form of a proactive and a reactive strategy. They have already limited possible damage before the flood with structural precautionary measures or with adapted building use. However, they still had to become active during the flood and conduct further emergency measures to reduce the damage. Only very few businesses (8; 1%), on the other hand, could be assigned to the exclusively proactive strategy (Figure 1A), in which the businesses no longer acted during the flood event. The two aforementioned groups have reduced their vulnerability and took long-term precautionary measures before the flood. In comparison, most businesses (41; 39%) pursue a proactive strategy in Figure 1B whereas only 12% of the businesses are in the proactive and reactive group. This could be explained by assuming that there is generally less time for a spontaneous response in a pluvial or flash flood than in a riverine flood due to differences in warning lead times. In addition, the difference in the share of businesses that were assigned to the proactive group in both data sets may be accounted by conducting the second survey again at a later date and different locations.

Furthermore, the reactive strategy represents the second largest group (96; 17%) in the distribution of adaptation strategies in Figure 1A (2013-flood). In Figure 1B the share of businesses within this group (pluvial/flash floods) is slightly smaller (10; 10%). These businesses did not act in advance, but only during the flood using emergency measures. They try to protect their building from flood damage, but they could take further steps to be more prepared by also employing more proactive adaptation strategies as well if they have the authority to do so.

A further 40 businesses (7%) were grouped as passive (Figure 1A) and did not actively try to reduce flood damage. The share of this group is significantly larger (38; 37%) in Figure 1B. This supports the assumption that in case of pluvial or flash floods businesses might not have had enough time to react and therefore most businesses either proactively implemented protective measures in advance or did not protect themselves at all. Maybe this result also indicated that risk awareness regarding pluvial flooding is less developed. Another explanation for differences between the data sets might potentially be the business sector, which is not included in this study, and which should therefore be explored in further studies.

In both data sets a relatively small share of businesses (7% in Figure 1A and 2% in Figure 1B) had already relocated or planned to do so within the next six months after the survey. The small sample size in the relocation group might be due to a problem with the data collection. If the businesses had already moved to another region to limit flood risk before the time of the survey, it is difficult to locate them for a survey afterwards. According to Neise and Revilla Diez (2019), one reason for businesses to stay in the flood-prone area could be the regional network with customers and business partners that the businesses do not want to leave. Jehmlich et al. (2020) found similar indications based on semi-structured interviews and survey data. Since the influence of the social and economic environment on the adaptation strategies of the businesses could not be illuminated in this study, there is a starting point for further research to investigate this aspect. For this purpose, it could be specifically analyzed which reasons are decisive for businesses to maintain their business location in a flood-prone area.

Drivers for adaptive behavior of the businesses

Correlation results

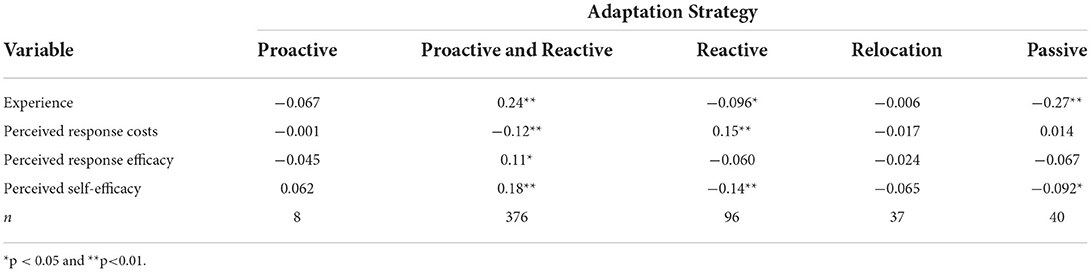

To gain first insights into drivers behind adaptation strategies among the businesses, correlation analysis was carried out. Tables 4, 5 show the results of the rank correlation analysis used for the factors experience, perceived response costs, perceived response efficacy, and perceived self-efficacy.

Table 4. Spearman-Rho-coefficients for possible drivers of precautionary behavior and adaptation strategies (n = 557, data: businesses in Germany damaged by the 2013 flood).

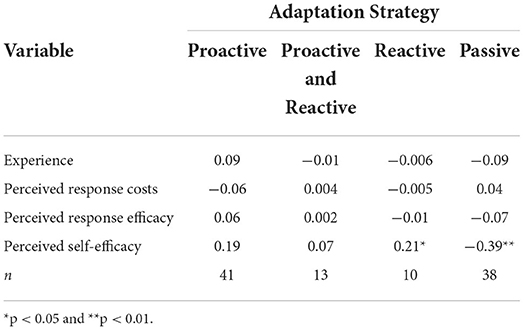

Table 5. Spearman-Rho-coefficients for possible drivers of precautionary behavior and adaptation strategies (n = 102, data: businesses in Germany damaged by pluvial floods 2014-2017).

In case of the 2013 flood no statistically significant results could be found for the exclusively proactive strategy due to small sample size (n = 8); the same holds for the relocation strategy (Table 4).

For the variable flood experience, there is a significant positive correlation with the proactive and reactive group and a negative correlation with the groups reactive and passive. This means that businesses with more flood experience tended to better protect themselves proactively. In the groups proactive and reactive and passive, the correlation with previously experienced floods is the strongest of all factors. Accordingly, the motivation for a more proactive adaptation behavior increases with increasing flood experience. Due to the relatively small sample size in the passive strategy the results for this group must be viewed with caution and cannot be unconditionally transferred to other businesses or affected regions.

A positive correlation with the variable perceived response costs means that businesses perceive costs of mitigation measures against flood damage to be too high. Accordingly, such an investment tends to be seen as too expensive by businesses with a reactive adaptation strategy. This can be seen in the positive correlation, which is the strongest among all factors in this strategy (Table 4). Businesses in the proactive and reactive group on the other hand are more likely to perceive precautionary measures as affordable, which is shown by a negative correlation with the cost variable. For the passive strategy there is no significant correlation with this item.

Regarding the variable perceived response efficacy, there is only a significant positive correlation with the adaptation strategy proactive and reactive (Table 4). Accordingly, the businesses in this group rate the effectiveness of property-level adaptation measures against flood damage higher than businesses that choose a different strategy.

The groups reactive and passive perceive their self-efficacy to be lower than the proactive and reactive group (Table 4). This means that the former feel less able to carry out precautionary measures, which can be seen in the negative correlation with this item. Businesses with a more proactive strategy, on the other hand, tend to see their ability to protect themselves against floods as higher.

The results for the 2014–2017 flash flood data set (Table 5) show only two significant correlations between the variable perceived self-efficacy and the strategies reactive (positive correlation) and passive (negative correlation). Businesses that are in the reactive group tend to rate their self-efficacy higher than businesses in the passive group. Combining this with the result of the 2013 data set it can be assumed that the perceived self-efficacy is an important driver for businesses to become active and at least try to protect the business from flooding in case of an event.

Due to the small sample size of the strategy relocation in this data set no correlation analysis was carried out for this group.

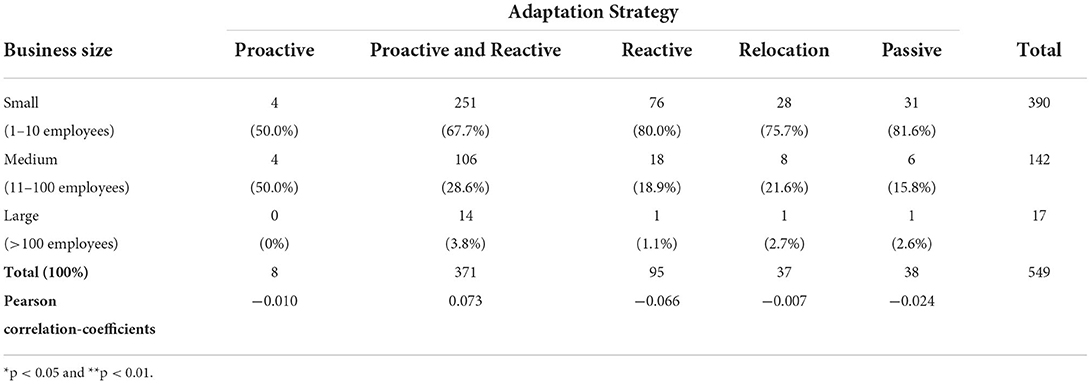

Tables 6, 7 show the absolute and relative frequencies of the adaptation strategies, divided into three classes of business size. In addition, the tables also contain the Pearson correlation coefficients, which were calculated without the class division of the business size. The class division was not retained for the correlation analysis because the number of large businesses is very small.

Table 6. Distribution of business size with class division of the number of employees and Pearson correlation coefficient without class division of the number of employees (n = 549, data: businesses in Germany damaged by the 2013 flood).

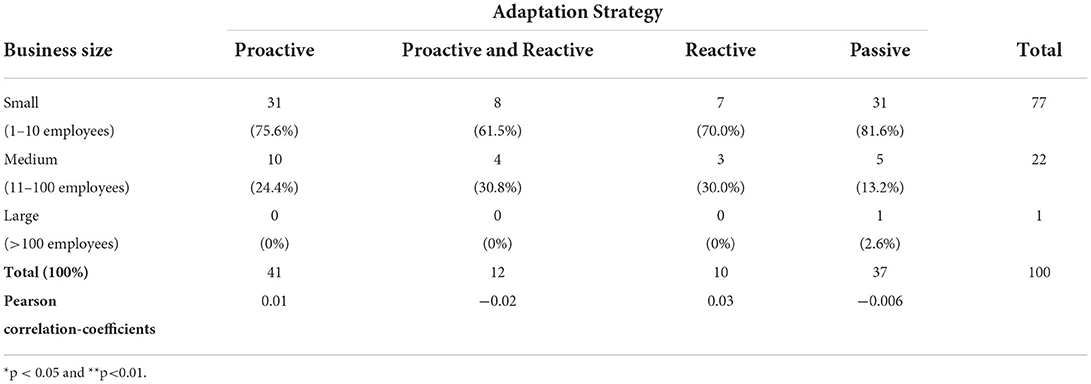

Table 7. Distribution of business size with class division of the number of employees and Pearson correlation coefficient without class division of the number of employees (n = 100, data: businesses in Germany damaged by pluvial floods 2014-2017).

No significant correlation could be found between the size of the business and the various adaptation strategies based on a Pearson correlation analysis in both data sets (Tables 6, 7).

Most of the businesses surveyed are smaller businesses with a maximum of 10 employees. Less than half of the businesses are medium-sized and very few are large. A positive or negative effect of business size on flood risk adaptation cannot be observed. This might be due to the unequal distribution of small and larger businesses. Furthermore, the results must be viewed with caution due to the relatively small sample size and cannot be unconditionally transferred to other businesses or flood regions.

Tables 8, 9 show the contingency table with Phi-correlation-coefficients of the adaptation strategies and the variable ownership. The percentage of owners and tenants is given per adaptation strategy (per column).

Table 8. Contingency table for ownership of the building and the chosen adaptation strategy of the businesses with phi correlation coefficients (n = 542, data: businesses in Germany damaged by the 2013 flood).

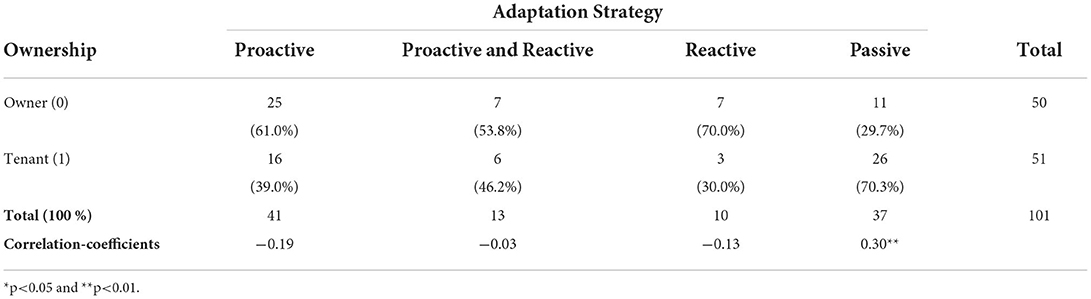

Table 9. Contingency table for ownership of the building and the chosen adaptation strategy of the businesses with phi correlation coefficients (n = 101, data: businesses in Germany damaged by pluvial floods 2014-2017).

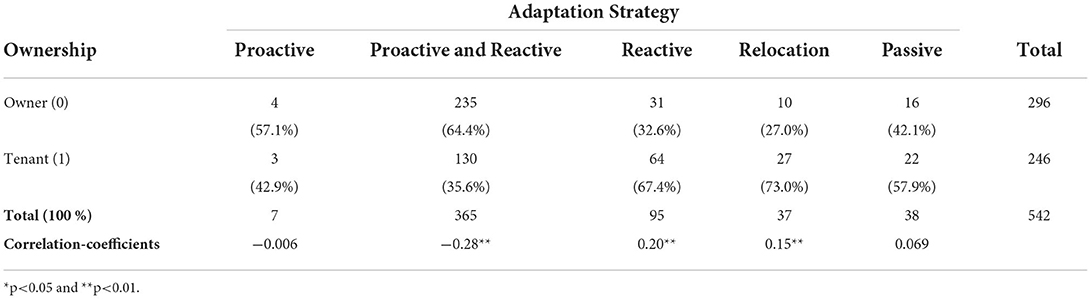

The binary variable of ownership is coded 0 for owner and 1 for tenant. In total, 296 surveyed businesses in the 2013 data set are owners, and 246 businesses are tenants. Due to missing information, only 542 of the 557 businesses surveyed were considered (Table 8).

Within the strategies proactive and passive, the shares of owners and tenants differ only slightly. Within the proactive group the share of owners is slightly higher whereas the share of tenants is higher within the passive group. In the correlation analysis, no statistically significant result could be found for either group (Table 8).

The shares of the two groups (tenants and owners) differ more clearly for the strategies proactive and reactive, reactive and relocation. Within the reactive adaptation strategy and the relocation strategy, about one third of the businesses are owners and two thirds of the businesses are tenants. For both strategies there is a significant positive correlation (Table 8), which illustrates that tenants are more likely to choose reactive adaptive behavior or relocation than owners. In contrast, in the group proactive and reactive about one third of the businesses are tenants and two thirds are owners. This is reflected in the significant negative correlation (Table 8).

In the 2014–2017 data set, 50 businesses are owners and 51 are tenants (Table 9). In the proactive group and the reactive group there are more owners than tenants. Within the proactive and reactive strategy the distribution is almost equal (Table 9). In contrast, the share of tenants in the passive group is higher than the share of owners. Furthermore, the passive strategy is the only one in Table 9 that shows a significant positive correlation. This means that in this case tenants show passive behavior more often than owners.

Regression results

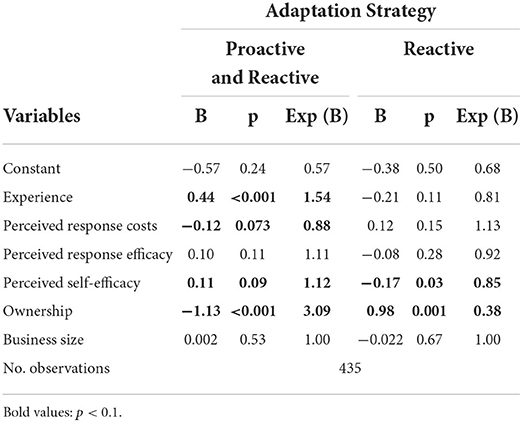

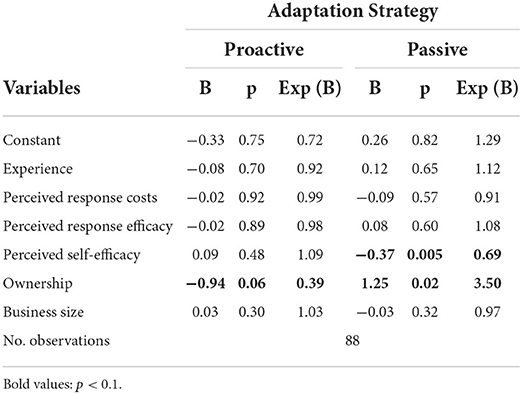

Due to the low sample size it is unlikely that reliable correlations could be observed for the strategies proactive, relocation and passive in case of the 2013 flood data set. Regarding the data set of the 2014–2017 flash floods, the same holds for the strategies proactive and reactive, reactive, and relocation. Therefore, we focus the regression analysis of the 2013 data on the strategies proactive and reactive, and reactive and the regression analysis of the 2014–2017 data on the strategies proactive and passive. Tables 10, 11 show the regression coefficients (B), the odds ratio [Exp (B)] and the corresponding probability values (p) of the binary logistic regression models for the adaptation strategies.

Table 10. Influence of various factors on adaptation behavior (data: businesses in Germany damaged by the 2013 flood).

Table 11. Influence of various factors on adaptation behavior (data: businesses in Germany damaged by pluvial floods 2014-2017).

In Table 10 there is a clear difference between the proactive and reactive group and the exclusively reactive group regarding the variable “flood experience.” As already shown in the correlation analysis, experience with previous flood events has a positive effect on more proactive behavior. With increased experience, the probability also increases that a business can be assigned to the proactive and reactive group and thus protects itself against flood damage in the long term. The effect that more experience increases the motivation to mitigate flood exposure has been observed similarly for private households by Thieken et al. (2007) with regard to the 2002 flood in Germany. On the other hand, no significant correlation can be observed for flood experience in the case of the reactive strategy (Table 10) and in the case of the strategies proactive and passive (Table 11).

The variable ownership plays a potentially major role in all regression models. Owners tend toward a more proactive strategy (Tables 10, 11). As was mentioned before, this can be explained by tenants having lower financial risks and limited scope to act compared to owners (Kreibich et al., 2005; Thieken et al., 2007; Bubeck et al., 2012).

Smaller effects (p < 0.1) are also recognizable in the regression model for the strategy proactive and reactive (Table 10) regarding the factors perceived response costs and perceived self-efficacy (cf. Table 10). Businesses assigned to the proactive and reactive group are more likely to see precautionary measures against flood damage as affordable. In addition, Neise and Revilla Diez (2019) found that most businesses that pursue a reactive strategy have a lower financial capacity than businesses within the proactive group and therefore fear a reduction in competitiveness if they invest into flood protection. Furthermore, businesses within the proactive and reactive group tend to rate their own self-efficacy higher. In the reactive group (Table 10), the relationship to perceived self-efficacy is reversed. When businesses pursue this strategy, they rate their abilities to protect themselves against floods lower. This effect is even stronger regarding the passive strategy (Table 11). This result indicates similarities with the flood adaptation behavior of private households. Bubeck et al. (2012) report that coping appraisal is a very important and decisive variable in determining whether a private household implements adaptation measures against floods. To support businesses in flood preparedness, more attention should therefore be paid to promoting their own competencies to better protect themselves. Financial support from the government for the purchase of flood protection measures could also be a motivation for businesses to act more proactively. This conclusion was also reached by Kreibich et al. (2011) in their investigation of the cost-effectiveness of preventive measures taken by private households against flood damage. Regarding perceived response efficacy, no significant effect is observable in either regression model.

When looking at business size, Neise and Revilla Diez (2019) observation that larger businesses act more proactively, whereas smaller businesses tend to adapt reactively or to capitulate could neither be proven with statistically significant correlations nor with the regression models. This could be due to the nature of the sample, as only very few large businesses were surveyed. Further research is needed to investigate this relationship in more depth to find out whether supporting offers to reduce flood risk should be tailored differently to small and large businesses. This would require including larger flood-affected businesses in the survey to be able to make reliable statements about their adaptation choices.

Overall, the results reflect behavioral patterns that are known from research on flood adaptation of private households. Experience with previous floods, and a positive assessment of coping capacity and costs increase the motivation of businesses to act more proactively. However, just as with private households, being a tenant and not an owner of the property reduces the ability to implement proactive measures.

Conclusion

This work supports the assumption that businesses pursue different strategies to adapt to flood risk in their region. The classification of adaptation strategies by Neise and Revilla Diez (2019) proves to be applicable. It could largely be applied to the businesses surveyed after floods in Germany and revealed different dominant strategies for different flood types (Figure 1). However, it is noticeable that the strategies cannot always be clearly distinguished from each other. Regarding the question which strategies businesses in Germany that had been damaged by different flood events between 2013 and 2017 chose to adapt to flood risk we found that in addition to businesses opting for an exclusively proactive or an exclusively reactive strategy, many businesses make a compromise between these two strategies. Furthermore, the main strategies in both data sets are different. While the proactive and reactive group predominates within the 2013 flood data set, the 2014–2017 flood data set is dominated by the proactive and the passive strategy.

In both cases, many businesses have lowered their vulnerability with long-term, proactive measures on the building. Nevertheless, especially regarding extreme events, there is still great potential to optimize and expand existing precautions and routines. This is especially true as they receive relatively less focus as compared to private households and individuals. However, businesses play an important role for the recovery and long-term wealth of a flood-affected region. Therefore, strengthening their adaptation capabilities should deserve more attention.

In this context, experience with floods has emerged as an important factor influencing the motivation to adapt. Thus, it is recommended to support especially inexperienced businesses more strongly in implementing precautionary measures. Communicating costs, efficiencies, and “how-to-implement”-guidelines could foster adaptation, since it was also found that perceived response costs play a role in the choice of adaptation strategy. Accordingly, the willingness of businesses to invest into long-term protection could be increased by making public funds available to subsidize such measures. However, appropriate preparedness for potential flood impacts is not only a question of experience and perceived response costs, but also of the business's capabilities. These capabilities should be strengthened so that more businesses feel able to act with foresight in the future. Businesses should be offered individual advice on what they can do (even with limited resources) to make their business location more flood-proof and what specific steps they need to take to do so. A free or low-cost consultancy service with experts who come to the business location and draw up an individual precautionary plan could be helpful for this. This is like suggestions for private households and individuals, potentially leading to positive synergies with a single effort. Furthermore, the perceived self-efficacy of businesses could be increased by sharing success stories of comparable businesses that already adapted. This would likely encourage many businesses to adapt more proactively.

In addition to individual adaptation, building communities of businesses that support each other regarding flood risk management might help to protect everyone more effectively. For example, see Winkler et al. (2022) who suggest that mentorships between SMEs with differing flood experiences could prove a fruitful avenue for reducing the vulnerability of SMEs to flooding. This is an example of one type of collective activity that businesses could undertake, another is the collective investment in flood defenses that go beyond the means of a single actor (e.g., see Neise and Revilla Diez, 2018). However, further research is needed to investigate the influence of the social environment and interactions with other businesses or chambers, as well as business size, on adaptation behavior. For this, more large businesses need to be surveyed about their adaptation. Additionally, the survey should include specific questions on cooperation with other businesses or public institutions in matters of flood risk reduction as well as the wider social context and expectations a company acts in.

This work is an initial exploratory analysis and can be seen as a starting point for similar, larger, studies that can focus more intense on these aspects. It provides indications of how businesses that were damaged by different flood events in Germany have adapted to flood risk and identifies which out of a commonly perceived set of important factors might have the stronger influence on adaptation strategies of businesses.

Data availability statement

The raw data supporting the conclusions of this article will be made available by the authors upon request, without undue reservation.

Ethics statement

Ethics review and approval/written informed consent was not required as per local legislation and institutional requirements.

Author contributions

BW carried out the data analysis. AT and PH supervised the findings of this work. BW and AT wrote the manuscript with input from PH. All authors discussed the results and approved the final manuscript.

Funding

The presented work was developed within the framework of the Research Training Group Natural Hazards and Risks in a Changing World (NatRiskChange) funded by the Deutsche Forschungsgemeinschaft (DFG; GRK 2043/2). The two data sets were collected within the BMBF-project Hochwasser 2013 (FKZ: 13N13017) and the DFG Research Training Group NatRiskChange (GRK 2043/1), respectively.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher's note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Bhattacharya-Mis, N., Lamond, J., Montz, B., Kreibich, H., Wilkinson, S., Chan, F., et al. (2018). Flood risk to commercial property: training and education needs of built environment professionals. Int. J. Disaster Resilience Built Environ. 9, 385–401. doi: 10.1108/IJDRBE-03-2017-0024

Bos, F., and Zwaneveld, P. (2017). Cost-benefit Analysis for Flood Risk Management and Water Governance in the Netherlands: An Overview of One Century. The Hague, CPB Netherlands: Bureau for Economic Policy Analysis. doi: 10.2139/ssrn.3023983

Botzen, W. J. W., Kunreuther, H., Czajkowski, J., and De Moel, H. (2019). Adoption of individual flood damage mitigation measures in New York city: an extension of protection motivation theory. Risk Anal. 39, 2143–2159. doi: 10.1111/risa.13318

Bronstert, A., Agarwal, A., Boessenkool, B., Fischer, M., Heistermann, M., Köhn-Reich, L., et al. (2017). The Braunsbach flash flood of Mai 29th, 2016—origin, pathways and impacts of an extreme hydro-meteorological event. Part 1: meteorological and hydrological analysis. Hydrol. Wasserbewirtsch. 61, 150–162 (in German).

Bubeck, P., Aerts, J. C. J. H., de Moel, H., and Kreibich, H. (2016). Preface: flood-risk analysis and integrated management. Nat. Hazards Earth Syst. Sci. 16, 1005–1010. doi: 10.5194/nhess-16-1005-2016

Bubeck, P., Berghäuser, L., Hudson, P., and Thieken, A. H. (2020). Using panel data to understand the dynamics of human behavior in response to flooding. Risk Anal. 40, 2340–2359. doi: 10.1111/risa.13548

Bubeck, P., Botzen, W. J. W., and Aerts, J. C. J. H. (2012). A review of risk perceptions and other factors that influence flood mitigation behaviour. Risk Anal. 32, 1481–1495. doi: 10.1111/j.1539-6924.2011.01783.x

Bubeck, P., Botzen, W. J. W., Laudan, J., Aerts, J. C. J. H., and Thieken, A. H. (2018). Insights into flood-coping appraisals of protection motivation theory: empirical evidence from Germany and France. Risk Anal. 38, 1239–1257. doi: 10.1111/risa.12938

Chinh, D. T., Dung, N. V., Kreibich, H., and Bubeck, P. (2016). The 2011 flood event in the mekong delta: preparedness, response, damage and recovery of private households and small businesses. Disasters 40, 753–788. doi: 10.1111/disa.12171

Dillenardt, L., Hudson, P., and Thieken, A. H. (2022). Urban pluvial flood adaptation: results of a household survey across four German municipalities. J. Flood Risk. Manag. 15, e12748. doi: 10.1111/jfr3.12748

DKKV (German Committee for Disaster Prevention). (2015). Das Hochwasser im Juni 2013: Bewährungsprobe für das Hochwasserrisikomanagement in Deutschland. DKKV-Report 53, Bonn, Germany.

DWD – Deutscher Wetterdienst (Ed.). (2013). Das Hochwasser an Elbe und Donau im Juni 2013, Berichte des Deutschen Wetterdienstes 242, Offenbach, Germany.

European Environment Agency. (2019). Economic Losses from Climate-related Extremes. EuropeanEnvironment Agency, Copenhagen, Denmark.

Federal Ministry of the Interior Building and Community. (2013). Bericht zur Flutkatastrophe 2013 - Katastrophenhilfe, Entschädigung, Wiederaufbau. Federal Ministry of the Interior, Building and Community, Berlin, Germany. Available online at: https://www.bmi.bund.de/SharedDocs/downloads/DE/veroeffentlichungen/themen/bevoelkerungsschutz/kabinettsbericht-fluthilfe.pdf (accessed March 01, 2022).

Federal Ministry of the Interior and Community. (2021). Aufbauhilfe 2021: Bund und Länder greifen den vom Hochwasser betroffenen Regionen unter die Arme. Press release of August 18, 2021, Available online at: https://www.bmi.bund.de/SharedDocs/pressemitteilungen/DE/2021/08/aufbauhilfe-2021.html (Last accessed April 22, 2022).

Forino, G., and von Meding, J. (2021). Climate change adaptation across businesses in Australia: interpretations, implementations and interactions. Environ Dev Sustain. 23, 18540–18555. doi: 10.1007/s10668-021-01468-z

Grothmann, T., and Reusswig, F. (2006). People at risk of flooding - why some residents take precautionary action while others do not. Nat. Hazards 38, 101–120. doi: 10.1007/s11069-005-8604-6

Herbane, B. (2015). Threat orientation in small and medium-sized enterprises. Disaster Prev. Manag. 24, 583–595. doi: 10.1108/DPM-12-2014-0272

Hudson, P., Thieken, A. H., and Bubeck, P. (2022). A comparison of flood protective decision-making between German households and businesses. Mitig. Adapt. Strateg. Glob. Change 27:5. doi: 10.1007/s11027-021-09982-1

IPCC (2022). Climate Change 2022: Impacts, Adaptation and Vulnerability. In Press, Cambridge University Press.

Jehmlich, C., Hudson, P., and Thieken, A. H. (2020). Short contribution on adaptive behaviour of flood-prone businesses: a pilot study of Dresden-Laubegast, Germany. J. Flood Risk Manag. 13:e12653. doi: 10.1111/jfr3.12653

Kato, M., and Charoenrat, T. (2017). Business continuity management of small and medium sized enterprises: evidence from Thailand. Int. J. Disaster Risk Reduct. 27, 577–587. doi: 10.1016/j.ijdrr.2017.10.002

Koerth, J., Jones, N., Vafeidis, A. T., Dimitrakopoulos, P. G., Melliou, A., Chatzidimitriou, E., et al. (2013). Household adaptation and intention to adapt to coastal flooding in the Axios - Loudias - Aliakmonas National Park, Greece. Ocean Coast. Manag. 82, 43–50. doi: 10.1016/j.ocecoaman.2013.05.008

Kreibich, H., Bubeck, P., Van Vliet, M., and De Moel, H. (2015). A review of damage-reducing measures to manage fluvial flood risks in a changing climate. Mitig. Adapt. Strateg. Glob. Change 20, 967–989. doi: 10.1007/s11027-014-9629-5

Kreibich, H., Christenberger, S., and Schwarze, R. (2011). Economic motivation of households to undertake private precautionary measures against floods. Nat. Hazards Earth Syst. Sci. 11, 309–321. doi: 10.5194/nhess-11-309-2011

Kreibich, H., Muller, M., Thieken, A. H., and Merz, B. (2007). Flood precaution of businesses and their ability to cope with the flood in August 2002 in Saxony, Germany. Water Resour. Res. 43:W03408. doi: 10.1029/2005WR004691

Kreibich, H., Thieken, A. H., Petrow, T., Müller, M., and Merz, B. (2005). Flood loss reduction of private households due to building precautionary measures: lessons learned from the Elbe flood in August 2002. Nat. Hazards Earth Syst. Sci. 5, 117–126. doi: 10.5194/nhess-5-117-2005

Kreienkamp, F., Philip, S. Y., Tradowsky, J. S., Kew, S. F., Lorenz, P., Arrighi, J., et al. (2021). Rapid Attribution of Heavy Rainfall Events Leading to the Severe Flooding in Western Europe during July 2021. World Weather Attribution. Available online at: https://www.worldweatherattribution.org/wp-content/uploads/Scientific-report-Western-Europe-floods-2021-attribution.pdf (accessed March 01, 2022).

Kron, W. (2005). Flood Risk = Hazard • Values • Vulnerability. Water Int. 30, 58–68. doi: 10.1080/02508060508691837

Kuhlicke, C., Masson, T., Kienzler, S., Sieg, T., Thieken, A. H., and Kreibich, H. (2020b). Multiple flood experiences and social resilience: findings from three surveys on households and businesses exposed to the 2013 flood in Germany. Weather Clim. Soc. 12, 63–88. doi: 10.1175/WCAS-D-18-0069.1

Kuhlicke, C., Seebauer, S., Hudson, P., Begg, C., Bubeck, P., Dittmer, C., et al. (2020a). The behavioural turn in flood disaster risk management and its implication for future research and policy. WIREs Water 7:e1418. doi: 10.1002/wat2.1418

Lindell, M. K., and Hwang, S. N. (2008). Household's perceived personal risk and responses in a multihazard environment. Risk Anal. 28, 539–556. doi: 10.1111/j.1539-6924.2008.01032.x

Merz, B., Didszun, J., and Ziemke, B. (2007). RIMAX Risikomanagement Extremer Hochwasserereignisse, 2nd Edn. GeoForschungsZentrum Potsdam (GFZ), Potsdam, Germany.

Merz, B., Elmer, F., Kunz, M., Mühr, B., Schröter, K., and Uhlemann-Elmer, S. (2014). The extreme flood in June 2013 in Germany. Houille Blanche 1, 5–10. doi: 10.1051/lhb/2014001

Merz, B., Hall, J., Disse, M., and Schumann, A. (2010). Fluvial flood risk management in a changing world. Nat. Hazards Earth Syst. Sci. 10, 509–527. doi: 10.5194/nhess-10-509-2010

Munich Re. (2018). “A stormy year,” in TOPICS Geo Natural Catastrophes 2017, Munich, Germany. Available online at: https://www.munichre.com/content/dam/munichre/global/content-pieces/documents/302-09092_en.pdf (accessed March 01, 2022).

Neise, T., and Revilla Diez, J. (2018). Firms' contribution to flood risk reduction – scenario-based experiments from Jakarta and Semarang, Indonesia. Procedia Eng. 212, 567–574. doi: 10.1016/j.proeng.2018.01.073

Neise, T., and Revilla Diez, J. (2019). Adapt, move or surrender? Manufacturing firms' routines and dynamic capabilities on flood risk reduction in coastal cities of Indonesia. Int. J. Disaster Risk Reduct. 33, 332–342. doi: 10.1016/j.ijdrr.2018.10.018

Piper, D., Kunz, M., Ehmele, F., Mohr, S., Mühr, B., Kron, A., et al. (2016). Exceptional sequence of severe thunderstomrs and related flash floods in May and June 2016 in Germany. Part 1: Meteorological background. Nat. Hazards Earth Syst. Sci. 16, 2835–2850. doi: 10.5194/nhess-16-2835-2016

Rogers, R. W. (1975). A protection motivation theory of fear appeals and attitude change. J. Psychol. 91, 93–114. doi: 10.1080/00223980.1975.9915803

Schröter, K., Kunz, M., Elmer, F., Mühr, B., and Merz, B. (2015). What made the June 2013 flood in Germany an exceptional event? A hydro-meteorological evaluation. Hydrol. Earth Syst. Sci. 19, 309–327. doi: 10.5194/hess-19-309-2015

Sieg, T., Vogel, K., Merz, B., and Kreibich, H. (2017). Tree-based flood damage modelling of businesses: damage processes and model performance. Water Resour. Res. 53, 6050–6068. doi: 10.1002/2017WR020784

Siegrist, M., and Gutscher, H. (2006). Flooding risks: a comparison of lay people's perceptions and expert's assessments in Switzerland. Risk Anal. 26, 971–979. doi: 10.1111/j.1539-6924.2006.00792.x

Spekkers, M., Rözer, V., Thieken, A., ten Veldhuis, M.-C., and Kreibich, H. (2017). A comparative survey of the impacts of extreme rainfall in two international case studies. Nat. Hazards Earth Syst. Sci. 17, 1337–1355. doi: 10.5194/nhess-17-1337-2017

Takao, K., Motoyoshi, T., Sato, T., and Fukuzono, T. (2004). Factors determining residents' preparedness for floods in modern megalopolises: The case of the Tokai flood disaster in Japan. J. Risk Res. 7, 775–787. doi: 10.1080/1366987031000075996

Thieken, A., Kreibich, H., Müller, M., and Lamond, J. (2017). “Data collection for a better understanding of what causes flood damage—experiences with telephone surveys,” in Flood Damage Survey and Assessment: New Insights from Research and Practice, Chapter 7, eds D. Molinari, S. Menoni, and F. Ballio (AGU, Wiley), 95–106. doi: 10.1002/9781119217930.ch7

Thieken, A. H., Bessel, T., Kienzler, S., Kreibich, H., Müller, M., Pisi, S., et al. (2016b). The floods of June 2013 in Germany. How much do we know about its impacts? Nat. Hazards Earth Syst. Sci. 16, 1519–1540. doi: 10.5194/nhess-16-1519-2016

Thieken, A. H., Kienzler, S., Kreibich, H., Kuhlicke, C., Kunz, M., Mühr, B., et al. (2016a). Review of the flood risk management system in Germany after the major flood in 2013. Ecol. Soc. 21:51. doi: 10.5751/ES-08547-210251

Thieken, A. H., Kreibich, H., Müller, M., and Merz, B. (2007). Coping with floods: preparedness, response and recovery of flood-affected residents in Germany in 2002. Hydrol. Sci. J. 52, 1016–1037. doi: 10.1623/hysj.52.5.1016

Thieken, A. H., Petrow, T., Kreibich, H., and Merz, B. (2006). Insurability and mitigation of flood losses in private households in Germany. Risk Anal. 26, 383–395. doi: 10.1111/j.1539-6924.2006.00741.x

Thieken, A. H., Samprogna Mohor, G., Kreibich, H., and Müller, M. (2022). Compound inland flood events: different pathways, different impacts and different coping options. Nat. Hazards Earth Syst. Sci. 22, 165–185. doi: 10.5194/nhess-22-165-2022

Keywords: risk management, climate change adaptation, floods, disaster risk reduction, Germany, precaution, emergency management

Citation: Wutzler B, Hudson P and Thieken AH (2022) Adaptation strategies of flood-damaged businesses in Germany. Front. Water 4:932061. doi: 10.3389/frwa.2022.932061

Received: 29 April 2022; Accepted: 05 September 2022;

Published: 26 September 2022.

Edited by:

Heidi Kreibich, GFZ German Research Center for Geosciences, GermanyReviewed by:

Kulkarni Shashikanth, Osmania University, IndiaPaola Salvati, Istituto di Ricerca per la Protezione idrogeologica IRPI-CNR, Italy

Matthijs Kok, HKV Consultants, Lelystad, Netherlands

Copyright © 2022 Wutzler, Hudson and Thieken. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Bianca Wutzler, Ynd1dHpsZXJAdW5pLXBvdHNkYW0uZGU=