Chiara Oppi

Chiara Oppi- Centre for Socio-Economic Dynamics and Co-operation, University of Bergamo, Bergamo, Italy

Sustainability reporting (SR) practices at higher education institutions (HEIs) appear fragmented and underutilized. Research is needed to persuade HEIs to adopt SR standards, explaining the SR advantages of achieving sustainability objectives and realizing organizational change. Only a few research studies have investigated how HEIs employees can be trained on SR and how this can affect SR implementation. This research explores SR training for HEIs employees, focusing on gender reporting (GR) training as a means to achieve sustainability objectives and realize organizational change. Among the United Nations' Sustainable and Development Goals (SDGs), gender equality (GE) emerges as a relevant topic to investigate, also in the HEIs context, with current research being limited. Through a survey among Italian HEIs employees who attended a GR training course, this study investigates the effects of learning outcomes of respondents' expected achievement of GR objectives and organizational change after GR implementation. The research also studies whether the perceived organizational barriers to GR affect the expected realization of organizational change. The results support the impact of learning outcomes on the expected achievement of GR objectives and organizational change. Conversely, the perceived organizational barriers to GR do not affect the expected realization of organizational change. The study enters the debate about GR at HEIs and contributes to literature on sustainability training for HEIs employees, providing practical implications for organizations that intend to implement such training and showing their advantages.

Introduction

Sustainability reporting (SR) is intended to measure, disclose, and be accountable to internal and external stakeholders about the organizational performance toward sustainability development (SD) (GRI, 2011). Its role SR is related to assessing and improving SD, to benchmark, facilitate transparency and auditing, and report interrelations with stakeholders (Daub, 2007; Adams and Frost, 2008; Burritt and Schaltegger, 2010). Sustainability reporting allows institutions to measure progress against targets, foster organizational awareness on sustainability issues, increase reputation, improve credibility based on transparency, and identify space for cost savings (Kolk, 2010). Sustainability reporting has been traditionally built on economic and environmental issues, while the emphasis on social issues appears to be less developed (Salzmann et al., 2005).

Now sustainability is no longer considered as having solely an environmental meaning, but also has economic and social dimensions (Dempsey et al., 2011). In particular, the relevance of social sustainability in pursuing SD emerges (Hopwood et al., 2005): SD aims to satisfy existing needs in the long term, where such needs do not only refer to the primary (basic) ones but extend to others such as education, social relationships, self-fulfillment, driving the space for action and opportunities (Littig and Griessler, 2005). Social sustainability is therefore directed at creating opportunities to meet people's needs and plays a major role in contributing to developing communities' sustainability (Dempsey et al., 2011).

In the public sector, higher education institutions (HEIs) fulfill a preferred role in delivering SD principles to a wide audience by developing new mental paradigms on sustainability (Leal Filho, 2010) and by creating a more sustainable society (Disterheft et al., 2012). Higher education institutions play a relevant role in promoting SD and they should act as examples in this regard (Amaral et al., 2015). According to Stephens et al. (2008), HEIs can support the societal transition toward sustainability: their role is crucial to promote proactive exchanges between institutions, individuals, and the community (Aleixo et al., 2020). They can act as catalysts in engaging society with sustainability (Lehmann et al., 2009), and assume social responsibility for sustainability (Aleixo et al., 2018). Education and training provided through such institutions are key to fulfilling the aims related to the social dimension of SD (Littig and Griessler, 2005; Dempsey et al., 2011; Aleixo et al., 2020). As reported by Alonso-Almeida et al. (2015) based on Lozano (2006) and Lozano (2013), HEIs can promote SD by redefining their mission and revising study programs, activities, research programs, and campus life through a reiterated process of stakeholder engagement and outreach, also based on assessing and reporting activities. Indeed, society requires HEIs to manage and be accountable for their environmental and social impacts (Hayter and Cahoy, 2016). Higher education institutions can legitimize their SD actions through reporting activities directed at assessing the achievement of sustainability goals (Alonso-Almeida et al., 2014), and making visible their impacts outside academic boundaries (Findler et al., 2018). In this regard, there is a need for universities to implement SR, aiming to assess the progress toward SD, communicating the efforts to stakeholders, and disclosing information about sustainability to the public (Lozano, 2011; Findler et al., 2018). Sustainability reporting can contribute by not only acting as a tool to communicate sustainability practices and engage stakeholders, but also by supporting improved management practices concerning SD integration (Adams and Frost, 2008).

Higher education institutions underwent pressure for the disclosure of more detailed information on sustainability issues (Del Sordo et al., 2016) and implemented SR to satisfy stakeholders' demands and legitimize their actions (Sassen and Azizi, 2018a). However, Lozano et al. (2015a) pointed out the need for HEIs to better engage in reporting and assessing their sustainability efforts. Indeed, SR production is limited in HEIs (Ferrero-Ferrero et al., 2018), despite HEIs orientation toward public sector objectives, such as social and non-profit ones, which should support a greater commitment to SD (Jongbloed et al., 2008). Sustainability reporting is a voluntary activity and appears to be scarcely integrated in HEI system (Ferrero-Ferrero et al., 2018; Aleixo et al., 2020) and at an early stage in the HEI context (Ceulemans et al., 2015a; Del Sordo et al., 2016; Huber and Bassen, 2018; Sassen and Azizi, 2018a). Sustainability reporting practices at HEIs are fragmented and organizations frequently fail to optimize the opportunities for benchmarking and comparisons to determine best practice and maximize mutual learning (Beringer, 2007; Del Sordo et al., 2016; Sassen and Azizi, 2018a).

In the last few years, several authors called for action to persuade HEIs to adopt SR standards and for HEIs that already implemented SR to share relevant information to increase SR strength and diffusion (see for example Ceulemans et al., 2015b's literature review on the topic). Findler et al. (2018) reported that HEIs have increasingly been integrating SD, but SR mainly contributes to the assessment of sustainability activities inside the organization and provide information limited to their internal engagement with SD; conversely, HEIs tend to neglect their impacts on the society. Alonso-Almeida et al. (2015) suggested that future studies should focus on sustainability practices at HEIs and assess their impact on organizations and society. This would shed light on the need for further research to promote SD and the adoption of SR (Lozano, 2011), also aiming at supporting the fulfillment of sustainability objectives (Alonso-Almeida et al., 2015).

In turn, Daub (2007) emphasized the importance of studies that highlight the advantages of developing SR at HEIs and suggested that further research could demonstrate its usefulness. Sustainability reporting can then accomplish its full potential when it is considered to be a vehicle to drive organizational change instead of only being a communication tool. In this regard, the importance of research that deepens the link between SR and organizational change emerges, as most studies are focused on SR tools and standards rather than how HEIs can change their processes to facilitate SD in organizations (Ceulemans et al., 2015b). There is however still only scant research on SR and organizational change management at HEIs (Ceulemans et al., 2015b), and, in particular, on the potential for organizational change of SR in HEIs (Larrán Jorge et al., 2019). Literature has emphasized the importance of exploring the link between SR, sustainability objectives, and organizational change, but also deepened the emergence of organizational barriers to limit such change (Lozano, 2006, 2013; Barth, 2013). Organizational barriers are caused by individual, group, or organizational processes and might affect the extent to which organizations change as a result of SR implementation (Lozano, 2006; Blanco-Portela et al., 2017). Literature suggests that it is essential to take organizational barriers into account while planning organizational change in order to determine strategies to overcome the barriers and realize the desired change. Future studies should then explore this relationship based on larger samples (Lozano, 2013).

The sustainability-related challenges discussed here require new perspectives and a transformed society and individuals (Tassone and Wals, 2014). Wals (2014) explored the HEI context and detected signs of learning approaches directed at helping people to understand and engage with sustainability. These are accompanied by an increased consciousness to develop multi-stakeholder interaction in such processes, directed at professional development, competencies, monitoring, evaluation, and assessment. However, a lack of training in sustainability emerged in HEIs, especially among employees and faculty members, who frequently have never been trained on the topic (Verhulst and Lambrechts, 2015). While literature has extensively investigated the integration of sustainability issues and related education concerning student curricula (see for example Shephard, 2008; Hill and Wang, 2018), research that deepens the patterns of HEI employees' education and training on SR, and its meaning for SR implementation, is lacking. Yet, sustainability education and training in universities is key to meet future challenges (Aleixo et al., 2018).

Based on those premises and on the gaps identified in the literature, this study aims to investigate how learning outcomes related to SR training can affect participants' perceptions of achieving sustainability objectives and realizing organizational change at HEIs. The study also explores the likelihood that the perceived organizational barriers participants experience at their institutions may hinder the perception of organizational change related to the implementation of SR practices.

The study pursues its aims by focusing on gender equality (GE) and gender reporting (GR). Gender equality is a topical social responsibility issues for HEIs, and is also listed as Goal 5 on the UN's Sustainable and Development Goals (SDGs) agenda (Hopper, 2019). Many international institutions have published guidelines and recommendations directed at promoting GE, such as the EU Gender Action Plan 2016–2020, which argues that “women's participation in the economy is essential for sustainable development and economic growth and is intrinsically linked to the global goal of eradicating poverty” (Ioannides, 2017, p. 33). Addressing GE, institutions can advance sustainable development agenda (Botlhale, 2011) and help to achieve other SDGs. In this sense, Razavi (2016) pointed out that GE is complemented by other SGDs and claims “complementing the target on unpaid domestic and care work is a target for achieving universal and equitable access to safe and affordable drinking water under Goal 6 (6.1). Other strategic elements such as full and productive employment/decent work for all women and men, and equal pay for work of equal value appear under Goal 8 (8.5), while access to social protection ‘for all' appears under Goal 1 (1.3).” (Razavi, 2016, p. 30). Other researches pointed out that women are more sensitive than men to environmental issues, so they can positively affect environmental policies; however, women face difficulties in reaching leadership positions and green jobs and this can threaten the achievement of sustainability objectives (Stevens, 2010). The Organization for Economic Cooperation and Development (OECD) has emphasized the relevance of GR, as a means for female economic and social empowerment. It highlights the importance of addressing this topic and is also aimed at ensuring accountability for policy commitments to GE (OECD, 2017). Reporting on GE issues is recognized as a way for organizations to be open about their efforts to legitimate their position and to adapt to social goals (Adams and Harte, 1998). The importance of integrating a gender perspective in SR was emphasized by literature (Miles, 2011), and studies deepening the different media adopted by HEIs to report for sustainability took GR into consideration (Del Sordo et al., 2016). Furthermore, the Global Reporting Initiative (GRI) includes the gender perspective in its SR guidelines (GRI, 2011). This suggests that GR can act as an agent of change for sustainability, as SR does (Ceulemans et al., 2015a).

The research is based on the Italian HEI context. Although the topic is becoming more relevant, literature still lacks of studies with a specific focus on academia (Broadbent, 2016; Galizzi and Siboni, 2016). Italy has been selected as a suitable study context because GR at HEIs is being discussed and is undergoing significant change following the publication of national regulations and guidelines. To increase the adoption of GR and make it more relevant as a decision-making tool at HEIs, specific recommendations have been published in the last few years by both the Italian central government (e.g., the Ministry of Education, University and Research—MIUR, 2018) and other national institutions (e.g., the National Agency for the Evaluation of the University and Research System—ANVUR, 2019). Among those, the Association of Italian University Rectors (CRUI), which represents the biggest association of HEIs in Italy as it involves 84 out of the 971 Italian institutions, developed specific guidelines for GR at HEIs (CRUI, 2019). Through these guidelines, the CRUI attempted to drive organizational change through GR, to support the diffusion and implementation of the tool at organizational level and to incentivize benchmarking among HEIs. To achieve this aim, the CRUI published the aforementioned guidelines in 2019 and in 2020 provided open source training about the development of GR, directed at professionals employed in various capacities at HEIs (e.g., academics and researchers, technical, and administrative staff, as well as senior managers) who are involved in GR implementation.

Through a survey directed at course delegates, this research aims to contribute to the literature by emphasizing the role of sustainability training concerning the development of SR (with specific attention to GR) in achieving intended sustainability objectives and organizational change, from the perspective of those who are involved in the courses and their learning outcomes. Literature emphasized the importance of fostering higher levels of empowerment to internal stakeholders (i.e., academics and non-academics) “to open-up critical issues and make conflict visible in an early stage of the decision-making process” of SR implementation and create a common culture of sustainability (Ferrero-Ferrero et al., 2018, p. 332). In particular, Ferrero-Ferrero et al. (2018) recommended developing training programs for academics and non-academics about the importance of the social sustainability dimension for HEIs. In fact, the absence of internal stakeholder engagement processes might hamper the implementation of SR (Blanco-Portela et al., 2017). Consistent to this, exploring stakeholders' perception of HEI sustainability in Portugal, Aleixo et al. (2018) pointed out that HEI stakeholders still mainly associate SD with financial and environmental dimensions, rather than social aspects such as GE. The paper therefore enters a field that is underexplored in the interplay between GE issues and HEIs, as the role of gender training in organizational change has not been investigated in-depth in the literature (Callerstig, 2016). The study also contributes to the investigation of the perceived organizational barriers to GR at HEIs and the extent to which such barriers hinder the realization of organizational change, adding knowledge with specific reference to the HEI context.

The manuscript is organized as follows: the next section focuses on hypothesis development; the third section provides an overview of GR at Italian HEIs and presents the contents of the gender training; the fourth section presents the design of the study and the methods applied; the fifth section presents the results of the analysis; the last section discusses the results and derives conclusions.

Hypothesis Development

Consistent with the study aims, in this research four main variables are considered: learning outcomes, expected achievement of GR objectives after GR implementation, expected organizational change after GR implementation, and perceived barriers to GR implementation. These variables are described in this section, and three main relationships among them are hypothesized.

Learning Outcomes

Learning outcomes refer to what participants in a course should know, understand or be able to do at the end of the course as far as knowledge, skills, abilities, or experience are concerned (Svanström et al., 2008). Adult learning has a critical role in transforming assumptions and beliefs that define people's tacit perspectives and influence thinking, attitudes, and actions (Mezirow, 1978). In this sense, learning can support critical awareness and a different way of interpreting the world, others, and ourselves. At an individual level, workers appear to be motivated to learn whether they are willing to do that and when they are in a context that incentivizes learning (Argyris, 1991). People are motivated to adopt new tools and technologies when they are empowered through the right knowledge, techniques, and aligned skills (Appelbaum et al., 1998). Courses have the potential to encourage learners to reflect, empower, and equip them to act on issues they consider important (Tassone and Wals, 2014). They can transfer expert knowledge, providing standard and relatively fixed solutions aiming at changing learners' behaviors in a specific direction (Wals and Jickling, 2002).

Concerning sustainability, courses support the revision of individual and group beliefs and provide practical insights on SD (Tassone and Wals, 2014). The importance of such training is also emphasized with regard to GE training, as GE issues are often not prioritized in organizations, lacking adequate managerial support with few individuals strongly committed to the topic and driving the work (Callerstig, 2016). In this sense, gender training is important, especially for non-gender experts, supporting them to conduct gender impact analyses and suggesting measures for gender mainstreaming (Council of Europe, 1998). In the case studied here, the gender training provided a tool for implementing GR at HEIs. Gender training aimed to increase learners' understanding of gender issues, but also focused on acknowledging, challenging, and changing inequalities through GR. Following the course, and according to the course aims, learners could change their understanding of GE issues through a wider perspective about the features of the GR to be developed at HEIs.

Expected Achievement of GR Objectives

Sustainability reporting is a voluntary process directed at communicating with the stakeholders about SD, being accountable for it, and assessing sustainable performance (Adams and Frost, 2008). Ceulemans et al. (2015a) explored SR objectives in organizations and surveyed those who seem to be addressed most frequently (whether intended or achieved). Sustainability reporting objectives are connected with performance assessment, benchmarking with other organizations, transparency and communication, and stakeholder relations (Schaltegger and Wagner, 2006; Daub, 2007; Ceulemans et al., 2015a; Domingues et al., 2017). The latter appear to be particularly relevant among SR objectives, in terms of their involvement (regarding both internal and external actors), exploiting dissemination and communication, as well as reinforcing organizational legitimacy (Daub, 2007; Blanco-Portela et al., 2017; Ferrero-Ferrero et al., 2018).

Discussing the factors that can affect the SR development and achieving its objectives, Schaltegger and Wagner (2006) focused on publishing guidelines or standards documents (e.g., GRI or IRRC) based on a multi-stakeholder consultation process and driven by general societal and political elements. The guidelines could have positive aspects, such as standardization and transparency, which benefit organizations that adopt them as they can also be aligned with goal definition and performance management systems (Morhardt et al., 2002; Siboni et al., 2013; Sassen and Azizi, 2018b). These positive elements might however be counteracted by information asymmetries, for instance between actors involved in guideline development and those who implement the guidelines at an organizational level (Schaltegger and Wagner, 2006), which may negatively impact the SR objectives. Training courses directed at reducing those asymmetries therefore offer positive contribution and incentivise sustainability consciousness (Mintz and Tal, 2014). Gender training is also considered key in supporting the implementation of GE policies (Halford, 1991), particularly when experts act as educators and can properly transfer knowledge to participants (Callerstig, 2016). Gender training are most effective when GE experts are able to transfer insight and ownership of the topics that are being studied, shedding light on the link between training concepts and reporting activities, and on the actions that should be taken in the organization to reach the reporting aims (Callerstig, 2016).

In the course under study, the training focuses on specific GR guidelines to be implemented by HEIs, and the educators are also those who developed the guidelines. Whether course participants increase their understanding of GR features, their learning outcomes can contribute to the diffusion of gender practices and can foster participants' expectations around achieving GR objectives. The first hypothesis is therefore formulated as:

H1: Learning outcomes positively affect the expected achievement of SR (GR) objectives at HEIs after SR (GR) implementation.

Expected Organizational Change After GR Implementation

Organizational change is aimed at moving organizations from the current state to a more desirable one (Ragsdell, 2000). Considering sustainability, organizational change refers to fostering values that integrate social and environmental aspects in strategic and managerial processes (Lovins et al., 2000; Lozano, 2013). A stable change toward sustainability is accompanied by a change in mental models, in the organizational structure, in operations, and in management, and it changes the vision for the future (Doppelt, 2000; Dunphy et al., 2003).

According to Freeman (1984), two main types of change focused on stakeholder involvement may occur: internal change, which involves internal stakeholders, and external change, which is linked to external stakeholders.

Aligned to this, Lozano and Garcia (2020) reported that sustainability changes have been mainly top-down, but external stakeholders as well as internal ones can drive change and innovation. Organizations tend to have more control over internal changes, and through this they can act proactively, while external changes, which are frequently unforeseen, tend to reduce their ability to seize opportunities. Sustainability literature investigated the development patterns of organizational change management for sustainability, aimed at making organizations more sustainable through a focus on soft issues (e.g., culture, behaviors, leadership style, stakeholder engagement) as well as managerial technologies and systems (Lozano, 2013; Lozano et al., 2015a).

In this vein, Ceulemans et al. (2015a) deepened the effects of SR reporting on organizational change management for sustainability at HEIs and explored the main changes emerging from those practices. In particular, and consistent with Albrecht et al. (2007), SR can mobilize stakeholders and allow organizational and individual learning. More in-depth and considering stakeholder relations, SR allows incremental changes in increasing awareness and improved communication, especially with internal stakeholders that perceive higher awareness and a sense of responsibility connected with sustainability processes. This is also related to a better understanding of the meaning of sustainability. Sustainability reporting is seen as a driver for organizational change, as it makes data more visible and accessible and can increase performance. This can foster a bottom-up approach in the integration of sustainability perspectives in HEIs and enhance the potential of SR for organizational change (Farinha et al., 2019).

Sustainability reporting as a vehicle for organizational change can be supported by the learning outcomes connected to SR training. In this regard, the model proposed by Appelbaum et al. (1998) foresees a relationship between learning outcomes and organizational change. Concerning GE, training has also been considered as a method to achieve organizational change, even if associated with a top-down approach to optimize its potential. For instance, Callerstig (2016) presented the results of a study conducted at a Swedish municipality where gender training was adopted as a major instrument for change, focusing on the outcomes for individuals, policies, and organizations. The research explored the role of gender training in affecting individuals' behavior and consequently driving change in institutional policies and practices. In the case studied here, attending the course and implementing GR properly, participants might see the possibility of achieving internal organizational change. We therefore hypothesize that HEI employees' learning outcomes make the achievement of organizational change associated with GR more visible and attainable.

H2: Learning outcomes positively affect the expected realization of organizational change at HEIs after SR (GR) implementation.

Organizational Barriers to GR

Although sustainability is likely to drive organizational change, incorporating sustainability in organizations could increase resistance and barriers to such change (Lozano, 2006, 2013; Barth, 2013; Blanco-Portela et al., 2017). At HEIs sustainability is seen as innovative and literature about how organizations responded to it as well as the consequent resistance has become more in-depth. Internal resistance is linked to individual barriers related to people's needs, emotional attitudes, denial and an unwillingness to change. Internal barriers may then relate to the whole organization, becoming organizational barriers.

In general, there are four categories of organizational barriers (Atkinson, 2000; Doppelt, 2000; Dunphy et al., 2003; Lozano, 2006, 2013; Hoover and Harder, 2015; Aleixo et al., 2018): managerial attitudes (e.g., leadership, strategy, planning), organizational aspects (such as structure, measurement, and assessment processes), patterns of support for employees, and organizational history (such as financial factors, human resources, time availability). Among organizational barriers, the investigation by Ceulemans et al. (2015a) about SR implementation at HEIs found organizational change to be hampered by the limited institutionalization of the process. Institutionalization processes can be a barrier per se, but may also be affected by internal organizational barriers, therefore overcoming such barriers may be beneficial to this process (DeSimone and Popoff, 2000).

Consistent with this, the literature suggests that HEIs should assess and report their SD activities in order to institutionalize SR and gain management support (also in terms of time and resources) (Ceulemans et al., 2015b; Lozano and Garcia, 2020). In the same vein, and referring to the implementation of GE practices, Callerstig (2016) underlined how a lack of support at managerial level can prevent gender practices from reaching their full potential.

Additional organizational barriers can refer to the impact of external factors (i.e., external barriers) and refer, for example, to the normative framework in which organizations operate, and their relationship with external stakeholders (DeSimone and Popoff, 2000). Organizations may be able to cope with internal organizational barriers while having a limited ability to overcome external barriers to change. Dealing with addressing the barriers, Lozano (2006) highlighted the need for organizational leaders to be aware of and understand the barriers to change in their organization, and to act in order to prevent or solve them.

Based on this, the effect of internal organizational barriers on organizational change is investigated in this study. Given that organizational barriers might prevent or slow down organizational change, we hypothesize that the perceived internal organizational barriers to GR implementation are negatively associated with the expected realization of organizational change after GR implementation at HEIs. The third hypothesis is therefore:

H3: The perception of organizational barriers to SR (GR) negatively affects the expected realization of organizational change at HEIs after SR (GR) implementation.

GR at Italian HEIs

In Italy's public sector, GR development does not follow a specific normative framework, but is included in a series of laws that affirm its importance. In 2006, the Code of Equal Opportunity for Women and Men (Italian Parliament, 2005) advised of the need for institutions to develop a positive action plan to implement GE strategically. The following year, the Ministry of Public Administration (Ministry of Public Administration, 2007) indicated the need for public administrations to implement GR processes. Two years later, the Legislative Decree 150/2009 recalled GR as an essential part of the performance cycle (Italian Parliament, 2009). These regulatory provisions were not followed by specific indications about GR characteristics.

Despite this, public administrations started developing such practices, especially among local entities. For example, 2 years later the enactment of the Legislative Decree 150/2009, Galizzi (2011) investigated the diffusion of GR practices in public administrations and reported an increasing trend of GR implementation in different local entities such as regions, provinces, and municipalities. The central government subsequently promoted projects to further incentivize GR development, aiming to enhance the integration of this perspective in governance processes—see for example the GerPA project developed by the Department of Equal Opportunities and the Presidency of the Council of Ministries with the University of Ferrara, Italy (Fioravanti et al., 2015). Further GR experiences at central level attempted to integrate gender in economic and financial perspectives, with a strong focus on gender budgeting (MEF—Ministry of Economics Finance, 2018). In this vein, the adoption of a gender perspective was explicitly related to the need of integrating the economic and financial dimension with indicators that can contribute to the redefinition and relocation of resources to pursue a sustainable development of the community. These regards, GE has been enclosed among the “Fair and Sustainable Wellbeing” indicators elaborated by the Italian National Institute of Statistics (ISTAT) with the aim to evaluate the progresses of society from economic, social, and environmental perspectives (Ministry of Economics Finance, 2018).

Because of this trend, an increasing number of Italian HEIs slowly started developing GR. For instance, some HEIs first integrated the gender perspective within different reporting activities (e.g., the Social report), then developed standalone GR (Del Sordo et al., 2016). Of the 97 Italian HEIs, only one had implemented GR in 2011, and by 2018 this number increased to 13 (Aversano et al., 2020). Those attempts resulted in a heterogeneous approach to GR: a great number of HEIs limited the GR function to a gender-sensitive analysis of the organizational context, while others deepened the results of the GE strategies that were implemented based on the identified gender needs identified and implemented performance measurement techniques around GE objectives. Higher education institutions have however often intended GR primarily as a reporting tool in stakeholder communication. While GR is becoming more relevant, its use is still lower than expected (OECD, 2017). In the Italian context, the topic has not been investigated in-depth by literature. Galizzi and Siboni (2016) investigated the tendency of Italian HEIs to promote GE strategies and Mazzotta et al. (2020) explored the interplay between HEIs' board composition and their gender-sensitive approach, but to the best of our knowledge GR-focused research has been lacking.

More recently, Italy's central government and other national institutions have published additional recommendations that also apply to HEIs. For instance, the Ministry of Education, University and Research (MIUR, 2018) released recommendations to develop positive actions aimed at pursuing GE, while Directive 2/2019 of the Ministry of Public Administration (Ministry of Public Administration, 2019) strengthened the relevance of the positive action plan as a strategic document to be included in performance cycles and listed GR among the requirements in all public administration. Both the aforementioned documents aimed to define an institutional framework to support the effective implementation, coordination, and sustainability of GE strategies in public organizations, consistent with the SDG agenda that is recalled in their premises. Furthermore, the ANVUR guidelines published in 2019 (ANVUR, 2019) were directed at supporting the integration of GR in performance and budget cycles.

Consistent with this pattern, the CRUI established a commission concerning GE issues at HEIs in 2018. Literature highlighted the support and benefits that single universities can gain in participating to a HEIs network for sustainability and the advantages related to knowledge sharing among and within HEIs (Farinha et al., 2019; Larrán Jorge et al., 2019). Collaboration and support among HEIs is considered a key success factor for those HEIs that have not implemented sustainability and SR, and to ensure homogeneity in this sense. Other studies emphasized the role of university rectors' associations or councils (for example, the role of the Portuguese University Rectors Council in Farinha et al., 2019) as mediating and coordinating the HEIs network toward sustainability.

The commission concerning GE issues consists of representatives of the 84 Italian HEIs that adhere to the CRUI. Commission members are appointed by each institution and involve rectors' deputies on equal opportunities, officials who are responsible for gender diversity committees or scholars with experience on equal opportunities. The commission addresses several topics related to GE, such as horizontal segregation in study and research areas (for example female participation in STEM courses), work-life balance, gender-inclusive language, positive actions directed at GE, and GR. A work group in each area has been created, consisting of a small number of HEI representatives with topical knowledge. The GR work group consisted of representatives of 10 Italian HEIs that have already implemented GR. The group aimed to create a standardized tool to assess and report performance in HEIs and to facilitate comparisons among them, as required by sustainability literature (Larrán Jorge et al., 2019).

Based on their work, the CRUI published the Guidelines for Gender Reporting at Italian Universities in September 2019 (CRUI, 2019). The guidelines call for a GR process integrated with HEIs' planning and control systems based on three main steps (Bettio and Rosselli, 2018): (i) a context analysis, which calculates the demographic, social, and economic indicators of GE; (ii) an analysis of local GE practices, which refers to work-life balance, procurement policies, gender empowerment, and considers expenditure to tackle gender disparities; and (iii) a gender impact analysis of expenditure, as well as the assessment of budget impacts in terms of improvements to reach GE. The potential of GR is therefore directed at achieving the objectives of gender mainstreaming and at supporting the development of gender-responsive logic as well as practices (Steccolini, 2019). Furthermore, as reported in the introduction of the guidelines, GR is intended as a mean for HEIs to contribute to the achievement of the SD goals that are recalled their strategic plans.

The publication of the aforementioned guidelines was followed by a training course. Given the attention HEIs paid to the guidelines and the number of clarification requests the authors received from those who attempted to implement GR at their institutions, the members of the work group decided to create an online training course on the topic 6 months after the guidelines were published.

The course consisted of four modules, following the structure of the guidelines: (A) Introduction to the course and to GR at HEIs; (B) GR as a governance tool (the integration of GR in strategic documents); (C) The integration of GR in HEI budgets; (D) Tools for context analysis (i.e., students, academic staff, technical, and administrative staff, and governance statistics) and for assessing the results of positive actions and impact assessment. For each module, the guideline authors recorded two to five short videos (5 min to half an hour each), supplemented by slides. The course also featured Excel tutorials to assist with context, the results of positive actions, and impact analysis (i.e., metrics calculation and graph plotting).

The course was registered between March and May 2020 and published in early June 2020. After publication, the CRUI invited all 84 HEIs that form part of the association to participate. The administrative office sent an email in June 2020 to HEI rectors and general directors, asking them to share the initiative among employees who might be interested in participating (e.g., HEIs' top management, researchers and academic staff, technical and administrative staff, Ph.D. students). Participation was free of charge, with open timelines.

Methodology

In late October 2020, 4 months after the publication of the training course, a questionnaire was distributed to all 247 participants (who came from 44 of the 84 invited HEIs).

The questionnaire was tested in two phases before it was distributed to the sample (Ricci et al., 2019): first with academic staff to ensure the validity of the measures, then with three GR experts to verify that the questions were aligned with the questionnaire's aims. The questionnaire was modified based on the feedback.

The questionnaire consisted of 42 questions on a seven-point Likert scale where respondents had to indicate their level of agreement (1 = “not at all”; 7 = “completely”). Three closed-answers questions were also included: the number of training modules attended, organizational role, and the extent to which course participation was directed to GR development.

The questionnaire was administered online, using the Qualtrics2 package. A total of 183 questionnaires were returned, which meant the overall response rate was 74.1%. There were however only 125 usable questionnaires, which lowered the actual response rate to 50.6% but is still considered acceptable based on the literature (Baruch, 1999).

The respondents represented employees at 37 HEIs. They were mainly women (n = 103; 82.4%). The respondents were mainly technical and administrative staff (n = 79; 63.2%), followed by academics (n = 34; 27.2%). A residual amount of respondents were other professionals, such as Ph.D. students (n = 10; 8.0%), and the remaining 1.6% were managers. The majority of respondents were to some extent involved in GR implementation (n = 83; 66.4%), while n = 41 (32.8%) attended the course regardless of their involvement in GR implementation; one participant did not respond. Among those involved in GR implementation, n = 30 have specific responsibilities: n = 9 are Deputy Rectors (on specific areas such as GE issues, well-being, social, and environmental performances), n = 4 chair the Single Guarantee Committee, a body that promotes equal opportunities for the whole university community and n = 17 are members of this body.

Concerning the training modules, 22 respondents (17.6%) participated in only one module, while 13.6% of the sample (n = 17) did two modules and seven respondents (5.6%) took part in three modules. More than half of the participants (n = 64; 51.2%) completed all four modules. At the time of the survey, 15 respondents (12.0%) had not yet started any modules; this group was not involved in the questions about the learning outcomes, which were limited to respondents who had done at least one module.

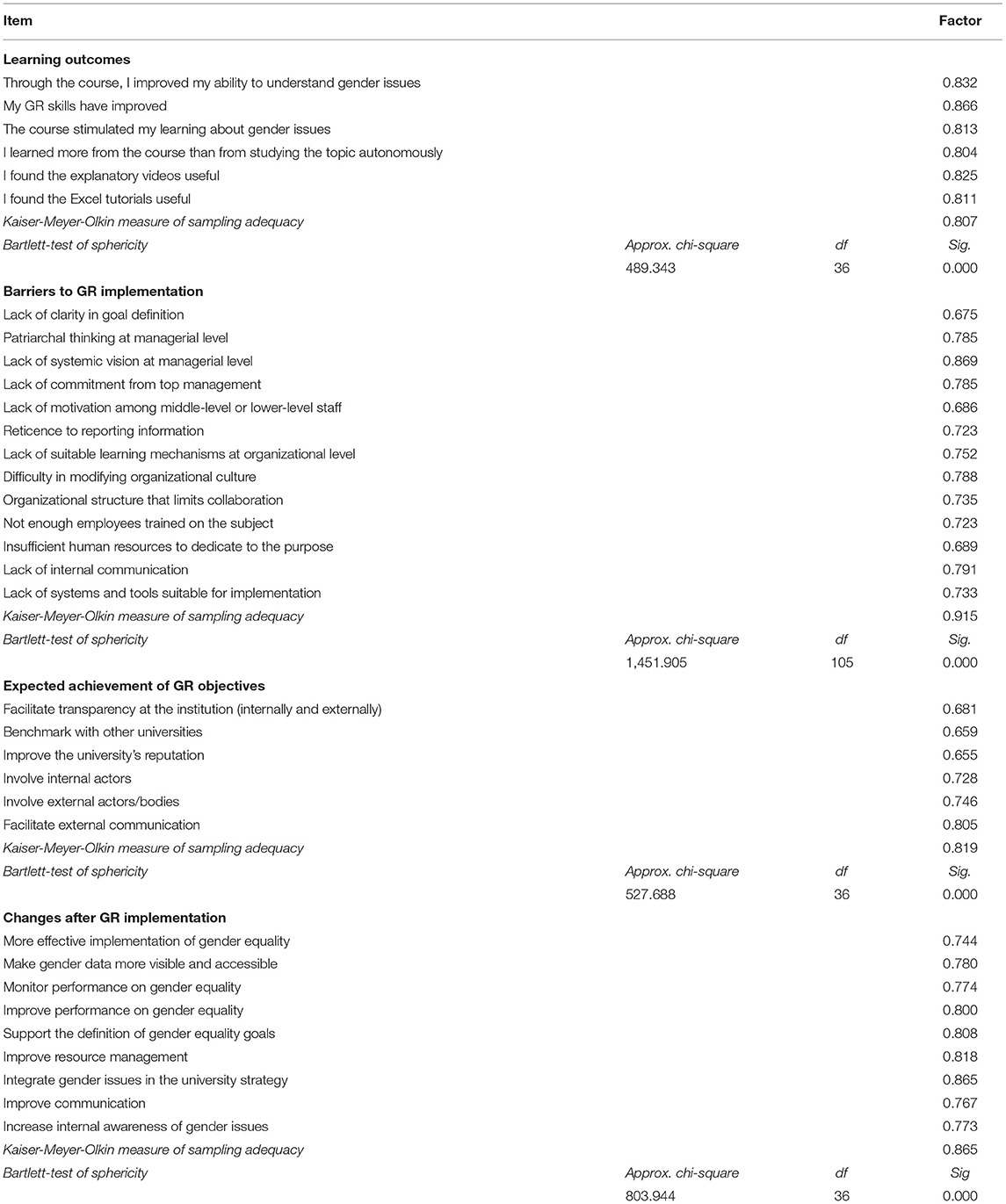

A statistical analysis using the IBM SPSS Statistics 22 software package was performed. The questions and their association with the study variables were analyzed. Each variable was scrutinized to verify the unidimensionality of the construct and the elements that did not pertain to the specific construct were eliminated where necessary. To assess the quality of the dataset, the Kaiser-Meyer-Olkin (KMO) test was performed, as it indicates the proportion of variance in the variables that could possibly have been caused by underlying factors. The Bartlett-test of sphericity was also used to ensure that the null hypothesis suggesting that the variables are related and not suitable for analysis could be rejected (Bartlett, 1950). The reliability of the constructs was evaluated on the basis of the Cronbach (1951) α coefficients. The variables are discussed below, and Table A1 in Appendix A illustrates the rotated component matrix of factor loadings concerning the variables.

Independent Variables

Learning Outcomes

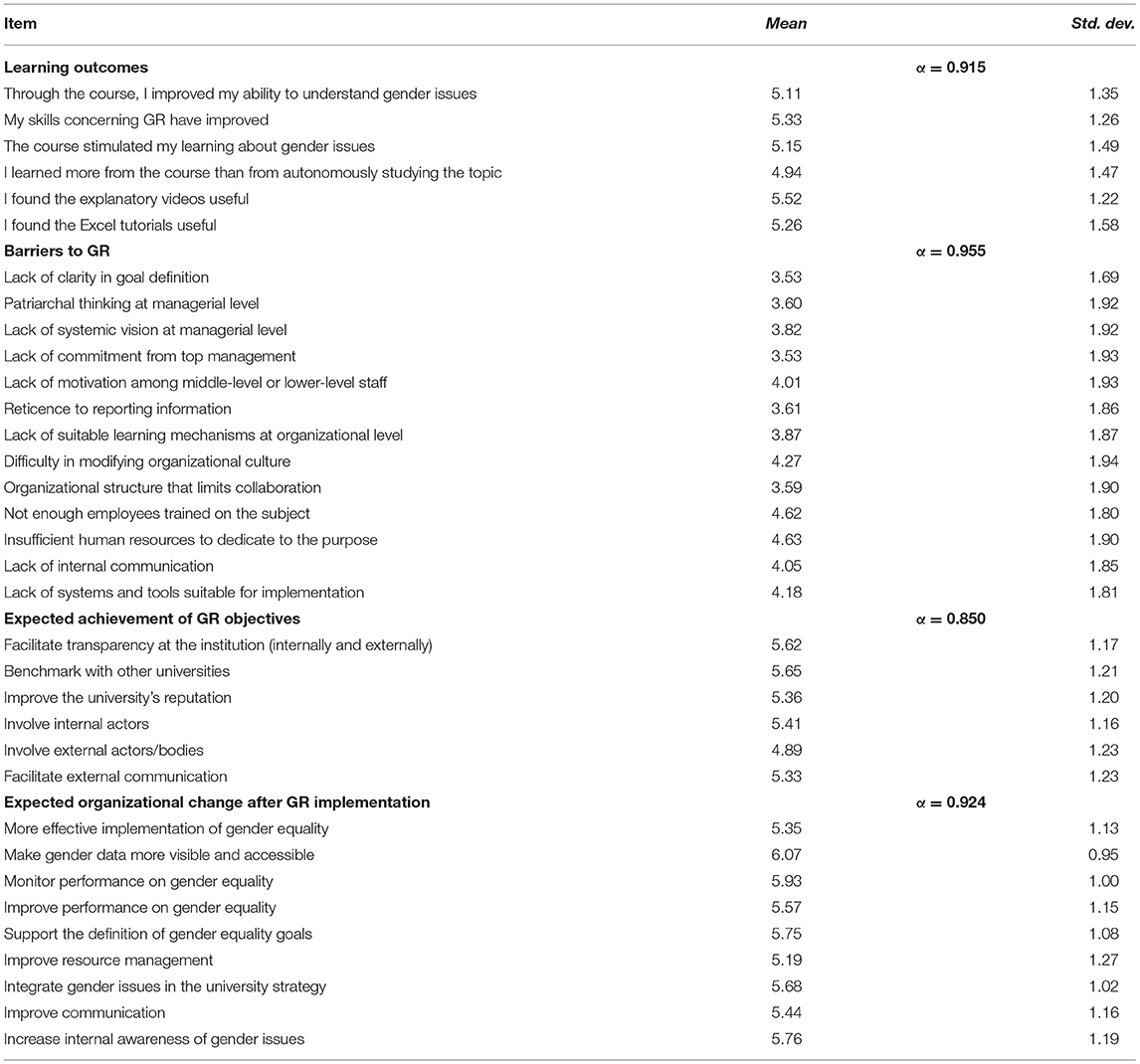

The first independent variable of the study refers to learning outcomes. Training for sustainability management had been addressed by literature (Hesselbarth and Schaltegger, 2014; Lozano et al., 2015b) aiming to determine its contents. Crucial components that emerged in this sense are knowledge (about sustainability concepts), skills (in terms of communication, critical analysis, and management), and attitudes (e.g., encouraging learners to question their point of view and develop reflective thinking). The items included in the questionnaire have been adapted by Wyness and Dalton (2018)'s questionnaire concerning the outcomes of sustainability degree courses. Wyness and Dalton (2018) conducted a survey on students' perceptions of their learning outcomes of a sustainability training, through an instrument that included questions on a five-point Likert scale. Consistent with this research purposes, such questions have been adapted to focus on GE and gender training. In this regard, the respondents who declared that they had participated in at least one module were asked to which extent they agreed (with 1 indicating “not at all” and 7 indicating “completely”) with the following items concerning the gender training course:

• Through the course, I improved my ability to understand gender issues

• My GR skills have improved

• The course stimulated my learning about gender issues

• I learned more from the course than from studying the topic autonomously

• I found the explanatory videos useful

• I found the Excel tutorials useful

• At the beginning of the course, I had a clear idea of what GR was

• By the end of the course, my views on GR had changed

• The course questioned my opinion on the role of GR.

The quality of the dataset was satisfactory, according to both the KMO test (sample adequacy = 0.807) and the Bartlett-test (p = 0.000). However, the factor analysis showed that the measurement was not unidimensional. The elements that did not refer to the construct (items 7, 8, and 9) were therefore removed. The reliability analysis through Cronbach's α coefficient for the remaining nine elements was satisfactory (α = 0.915).

Organizational barriers to GR

The second independent variable is based on Lozano's (2013) work on internal barriers to SR in organizations, adapted with regards to the topic under investigation. The construct is based on the integration of internal organizational barriers to SR: managerial (items 1–6), organizational (items 7, 10, 11) supportive (items 12–15), and historical (items 8–9). Respondents were asked to rate the extent to which they recognized a series of barriers connected with GR implementation in their organizations using a seven-point Likert scale (1 = “not at all”; 7 = “completely”). The items were the following:

• Lack of clarity in goal definition

• Patriarchal thinking at managerial level

• Lack of systemic vision at managerial level

• Lack of commitment from top management

• Lack of motivation among middle-level or lower-level staff

• Reticence to reporting information

• Lack of suitable learning mechanisms at organizational level

• Failure of previous attempts to implement GR

• Failure of previous attempts of another type (e.g., drafting a SR)

• Difficulty in modifying the organizational culture

• Organizational structure that limits collaboration

• Not enough employees trained on the subject

• Insufficient human resources to dedicate to the purpose

• Lack of internal communication

• Lack of systems and tools suitable for implementation.

The results of the KMO test (sample adequacy = 0.915) and the Bartlett-test (p = 0.000) confirmed the good quality of the dataset. The factor analysis reported that the scale was not unidimensional, therefore items 8 and 9 were deleted. Cronbach's α-test (α = 0.955) also confirmed the reliability of the results.

Dependent Variables

Expected Achievement of GR Objectives

The questions given to the sample were obtained from Ceulemans et al. (2015a), who explored the intended and achieved objectives of HEIs developing SR, having derived their items from sustainability literature (Schaltegger and Wagner, 2006; Daub, 2007; see for example Adams and Frost, 2008). Other researches (e.g., Domingues et al., 2017) adopted this construct and administered a survey based on a five-point Likert scale. The variable was constructed through nine items with respect to which respondents were asked to express their level of agreement about HEIs' ability to reach a series of intended objectives after GR implementation, on a scale from 1 (“not at all”) to 7 (“completely”):

• Evaluate the efforts made for GE

• Promote change

• Improve the university's performance with respect to GE

• Facilitate transparency at the institution (internally and externally)

• Benchmark with other universities

• Improve the university's reputation

• Involve internal actors

• Involve external actors/bodies

• Facilitate external communication.

The quality of the dataset was satisfactory, according to both the KMO test (sample adequacy = 0.819) and the Bartlett-test (p = 0.000). From the factor analysis it was clear that the construct was not unidimensional, therefore items 1–3 were excluded. Cronbach's α coefficient for the remaining elements was satisfactory (α = 0.850).

Expected Organizational Change After GR Implementation

The construct used was adapted from the work of Ceulemans et al. (2015a) about the detection of organizational changes associated with SR practices. Ceulemans et al. (2015a) surveyed a sample of HEIs that have published SR, and explored the organizational changes after SR implementation. The construct is based on the results of their research. It focused on cultural, behavioral, and leadership issues, stakeholder engagement, as well as changes in technology and the management system (see for example Lozano, 2013; Lozano et al., 2015a). The construct therefore comprises nine items about changes that HEIs could accomplish after GR implementation:

• More effective implementation of GE

• Make gender data more visible and accessible

• Monitor performance regarding GE

• Improve performance on GE

• Support the definition of GE goals

• Improve resource management

• Integrate gender issues in the university strategy

• Improve communication

• Increase internal awareness of gender issues.

The HEI employees involved in the study were asked to indicate their level of agreement with the above statements on a seven-point Likert scale where 1 indicated “not at all” and 7 “completely.” The validity of the data was assessed using both the KMO test (sample adequacy = 0.865) and the Bartlett-test (p = 0.000). The factor analysis indicated that the measurement was unidimensional and that the Cronbach coefficient α for the seven elements was meritorious (α = 0.924).

Control Variables

We included the following control variables in the model: the number of training modules done, participants' role in the organization, and the extent to which their course participation was directed to the development of GR. The first control variable refers to the number of course modules completed. We might expect that those who completed the whole course and might have achieved higher learning outcomes, would have different awareness levels concerning the expected achievement of GR objectives and organizational change after GR implementation compared to those who only partially completed the training. In this sense, a categorical variable ranging from 1 (only one module attended) to 4 (four modules attended) was included.

Concerning the second control variable, we supposed that respondents' role in the organization could affect the extent to which they perceived the two dependent variables. This might apply in particular to those in managerial positions or academic staff (and who might be to some extent involved in GR from a scientific point of view), vs. lower-level employees or people who studied the topic from external positions (such as Ph.D. students). This is because the first group may have a more complex organizational view and might be more aware of HEIs' ability to reach GR objectives and implement organizational change. Also, literature pointed out that HEIs with more proactive senior managers have a stronger commitment to SR (Adams, 2013) and that they can have a pivotal role in supporting the integration of sustainability discourses at all organizational levels (Blanco-Portela et al., 2017). This variable is represented by a categorical variable referring to managers, technical and administrative staff, academic staff, and others.

Last, we expected that participants' involvement in GR implementation at their institution could affect their perceptions about the dependent variables, as they might be differently committed to GR objectives and organizational change. This variable was represented by a dummy variable (yes/no).

Results

Descriptive statistics were computed for all variables and are presented in Table 1, which reports the mean and standard deviation statistics for the items. The mean for learning outcomes items ranged from 4.94 to 5.52, indicating a perceived level of learning from the course above the scale mean. Concerning GR barriers, mean values ranged from 3.53 to 4.63, being close to or slightly above the scale mean. The mean for the expected achievement of GR objectives variable ranged from 4.89 to 5.65, while higher degrees of expected organizational change after GR implementation emerged: the response mean ranged from 5.19 to 6.07.

Table 1. Mean and standard deviation statistics for the items, and Cronbach's Alpha coefficients for the variables.

Having assessed the average values concerning items of the questionnaire related to each variable, regressions were computed. We tested our hypotheses through three regressions, the results of which are reported in the following tables.

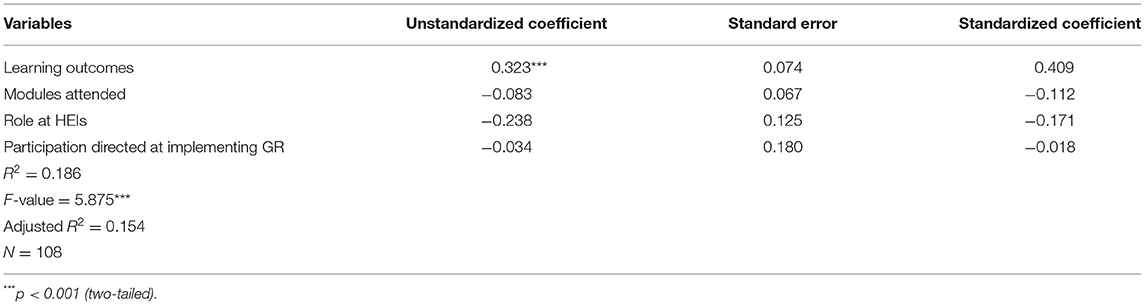

Hypothesis 1 states that learning outcomes affect respondents' expected achievement of intended GR objectives after GR implementation. As can be seen in Table 2, the analysis confirmed the expectations. The hypothesis that learning outcomes influence the expected achievement of the intended GR objectives was therefore grounded. More specifically, a positive and significant relationship (r = 0.323, p < 0.001) between the two variables emerged, as greater learning outcomes predicted higher expected achievement of GR objectives. Conversely, the control variables did not impact the dependent variable, although the role at HEIs was marginally significant (r = −0.238; p = 0.059). The influence of respondents' role at HEIs had a limited effect on the dependent variable: managers had a lower expected achievement of GR objectives compared to the other participants. The number of training modules completed and the extent to which participation is directed at GR implementation did not have an effect on the expected achievement of GR objectives.

Table 2. Results of regression analysis for learning outcomes on expected achievement of GR objectives after GR implementation.

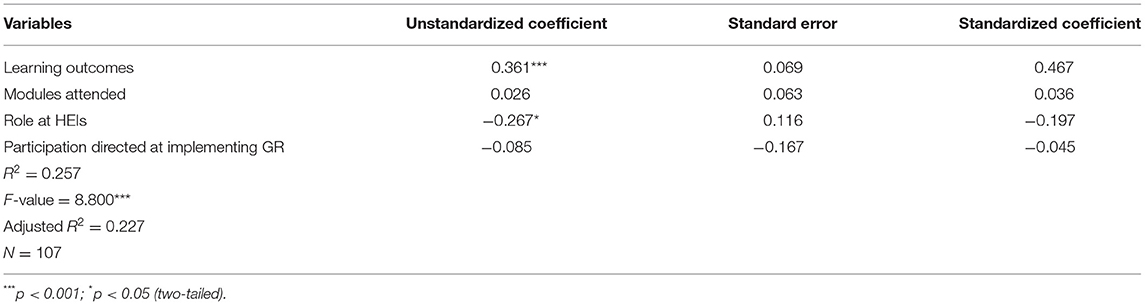

Hypothesis 2 stated that learning outcomes affect participants' perceptions of change after GR implementation. This relationship found support in the data (r = 0.361, p < 0.001), as reported in Table 3. In this sense, higher learning outcomes supported a higher perception of expected organizational change after GR implementation. Regarding control variables, participants' role at HEIs had an effect on the dependent variable (r = −0.267; p = 0.024). In particular, managers had a lower expected achievement of organizational change compared to the other groups. Conversely, the responses on expected organizational change were not affected by the number of modules completed and their involvement in GR implementation. Although low, the R2-values in both models can be considered acceptable based on literature focusing on explanatory power of regressions in social sciences (Moksony and Heged, 1990).

Table 3. Results of regression analysis for learning outcomes on expected organizational change after GR implementation.

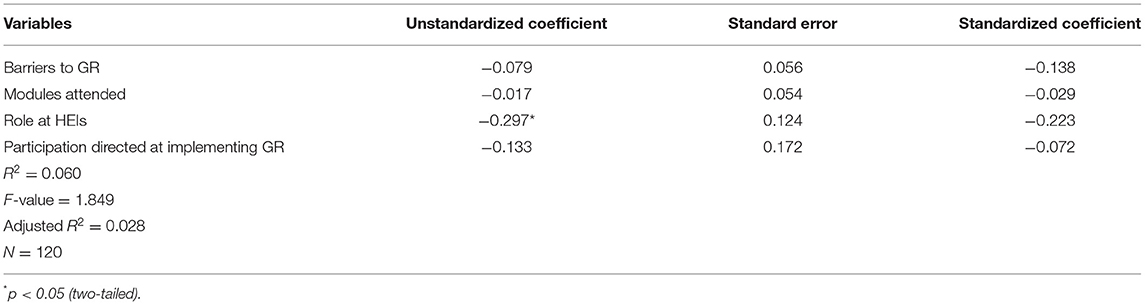

Hypothesis 3 stated that barriers to GR implementation negatively affect participants' perception of change after GR implementation. However, Table 4 shows that the interaction between the two variables was not statistically significant, therefore the hypothesis found no confirmation from the analysis (r = −0.079, p = 0.159).

Table 4. Results of regression analysis for barriers to GR on expected organizational change after GR implementation.

Discussion and Conclusions

The regression results partially support the assumptions. For Hypothesis 1, the results support the sustainability literature about the impact of learning outcomes on the expected achievement of SR objectives after implementation (Mintz and Tal, 2014; Wals, 2014; Daub et al., 2020) regarding GR and highlight the relevance of gender training in achieving the aims related to social sustainability (Aleixo et al., 2020). Attending gender training based on guidelines can therefore mold participants' perceptions of organizational benefits (as suggested by Morhardt et al., 2002). In the case, the training is structured around contributions by people who developed the guidelines, and this can limit the information misalignment between the guideline developers and HEI implementers that are highlighted in the literature (Schaltegger and Wagner, 2006). In this sense, knowledge transfer to participants might have improved (Callerstig, 2016) and this might have positively affected respondents' perceptions about the ability to reach GR goals after GR implementation. Also, participants in the course are employed in HEIs that are member of the CRUI, so the advantage related to knowledge sharing in national networks and the role of CRUI in mediating and coordinating HEIs toward GE are made clear (Aleixo et al., 2018; Farinha et al., 2019; Larrán Jorge et al., 2019).

The results relating to Hypothesis 2 support previous research on the subject that assessed the extent to which SR can become a driver for organizational change (Albrecht et al., 2007; Ceulemans et al., 2015a; Domingues et al., 2017; Larrán Jorge et al., 2019), in particular that learning outcomes can support such change (Verhulst and Lambrechts, 2015). This has also been reported with reference to gender issues and GR practices (Callerstig, 2016) and is confirmed in the case studied here. In fact, in this study learning outcomes derived from GR training positively influence respondents' expectations about realizing organizational change after GR implementation. However, stakeholders' function at HEIs play a role, with those in managerial positions perceiving lower levels of organizational change as a consequence of GR implementation, which could be explained by them having a more complex view of their organization. This confirms the importance of involving senior managers in sustainability discourses and promoting their commitment to SR to ensure the integration of sustainability at all organizational level (as suggested by Adams, 2013 and Blanco-Portela et al., 2017), and the holistic implementation of SD in HEIs (Lozano et al., 2015a).

Conversely, the results related to Hypothesis 3 differ from previous literature that explored the consequences of low support linked to SR and GR implementation as an organizational barrier to sustainability, and a factor that can prevent the practices from reaching their full potential (Ceulemans et al., 2015b; Callerstig, 2016; Blanco-Portela et al., 2017; Aleixo et al., 2018). We would have expected organizational barriers to GR to have an effect on respondents' expectations of organizational change after GR implementation, but this is not the case. Reasons for these results can be found in the extent to which respondents perceive organizational barriers to GR. From the items' mean it is clear that organizational barriers, although perceived, do not exert a major influence according to the participants, as the mean values are close to or slightly above the scale mean. This might explain the limited effect of such barriers. In these regards, also Aleixo et al. (2018) and Blanco-Portela et al. (2017) found out that HEIs engaged in sustainability can generate strategies for the effective institutionalization of sustainability practices, in terms of initiatives in education, research, and operations. Furthermore, the need to keep reinforcing the training of internal actors on sustainability issue emerges, so they become more involved in the process of change (Blanco-Portela et al., 2017). In this sense, gender training could assist to overcome barriers to GR implementation and to explain the importance of the social dimension of sustainability for the success of the HEIs (Ferrero-Ferrero et al., 2018).

The study reports the case of GR training provided to HEI employees in Italy, focusing on the effects of learning outcomes on their expectations of the achievement of GR objectives and organizational change after GR implementation. It also explores the extent to which perceived organizational barriers to GR hamper employees' expectations of organizational change.

Gender equality is frequently not prioritized at HEIs and the literature has highlighted the need to address the topic, calling for “a gender agenda” in academia (Broadbent, 2016; Galizzi and Siboni, 2016). The institutional context recommends the implementation of GR in HEIs, but normative pressures are missing in this sense. However, HEIs could be willing to report on GE to improve their credibility and reputation (Larrán Jorge et al., 2019), to benchmark with other institutions and to achieve SR objectives and organizational change. In this context, training can become a vehicle for knowledge transfer and may enhance learners' motivation and their ability to deal with GE issues. Through education, learners can acknowledge the contribution of sustainability practices to accomplishing sustainability (and particularly GE) objectives, as well as their impact on organizational change.

The research contributes to the stream of literature that links SR and the expected achievement of sustainability-related objectives and organizational change with a perspective on GE, which seems to be underinvestigated, especially in the Italian HEI context. It also contributes to management accounting literature that explores the value of sustainability training, and GR training in particular, to achieving organizational change, supporting the relevance of learning outcomes in molding learners' perceptions in this context. The study furthermore contributes to the literature investigating organizational barriers to SR and their possible consequences, shedding light on the relevance of perceived organizational change after GR training on respondents' opinion on organizational barriers to GR, which differs from the existing literature on the topic (Ceulemans et al., 2015b). In this sense, the study emphasized the importance of involving internal stakeholders in engagement processes to support the implementation of SR (Blanco-Portela et al., 2017; Ferrero-Ferrero et al., 2018).

Given these contributions, this research has implications for HEI managers, showing the impact of training in molding learners' perceptions about the extent to which organizations can address sustainability objectives and organizational change. Sustainability training provided to HEI employees can increase participants' awareness, without differences related to their involvement in reporting practices. When the developers themselves are course educators, this practice is likely to lower information misalignment between guideline developers and implementers. This suggest implications for educators organizing the training. In a broader context, sustainability training may potentially contribute to HEIs' role in incentivizing social sustainability (Del Sordo et al., 2016). When implemented adequately, GR practices are key in developing an inclusive environment and in increasing the quality of life at institutions, through training that aims to advance social sustainability. In addition, due to the relationship between HEIs and their local context, reaching GR aims also have an impact on creating more sustainable communities, fully realizing their potential to contribute to SD (Alonso-Almeida et al., 2015; Findler et al., 2018). This should happen when sustainability practices implemented at HEIs are shared with local institutions and their advantages are acknowledged by local policymakers who might decide to adopt them.

As far as study limitations are concerned, the sample is not representative of the entire HEI population, which reduces its generalizability. Also, the constructs considered in the survey are adapted from researches that adopted mix-method approaches. However, the results create avenues for further research on the topic, for instance about the factors that may enhance organizational change. As the study adopts a quantitative approach, future studies might replicate the research in different contexts, to support the quality of the survey instrument. Additional research in HEI context is also needed to investigate participants' attitudes to GE through qualitative analyses and to explore the actual implementation of GR after gender training. Although training can increase the attention to GE at HEIs and mold perceptions about achieving organizational change after GR implementation, it might not be sufficient. A more in-depth look at standards and solutions during the training may change learners' behavior, encouraging them to question their point of view and develop reflective thinking. Training can reach its full potential in organizations when it has institutional support. As Callerstig (2016) suggested, organizational change after training could be better achieved when organizations adopt a top-down approach and employees perceive a supporting environment. Future research could therefore explore differences in respondents' expected achievement of organizational change after GR implementation according to the level of top-management support.

Concerning organizational barriers, this study considered respondents' perceptions of barriers to GR, based on a sample of professionals from a context in which GR issues have hardly been investigated and in which GR implementation is at a very preliminary stage. In this sense, future research could use qualitative approaches to explore the development patterns of such barriers at HEIs and take an in-depth look at factors that could exacerbate or hinder their emergence.

Focusing on participants and their approach to SD after doing the course modules, additional research might investigate the role of learners as change agents for sustainability, and as individuals who can drive organizational change at HEIs. In this sense, research could explore the role of change agents' knowledge in implementing change, and the importance of the training.

Data Availability Statement

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

Ethics Statement

Ethical review and approval was not required for the study on human participants in accordance with the local legislation and institutional requirements. The patients/participants provided their written informed consent to participate in this study.

Author Contributions

The author confirms sole responsibility for study conception and design, data collection, analysis and interpretation of results, and manuscript preparation.

Conflict of Interest

The author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

The handling editor EV declared a past co-authorship with the author CO.

Acknowledgments

The author wishes to thank Emidia Vagnoni, Topic Editor of the Journal, and the Reviewers for their insightful suggestions. Acknowledgment goes also to the colleagues of the CRUI group who developed the GR training and supported data collection, and to all those who took part in the survey.

Footnotes

1. ^http://ustat.miur.it/dati/didattica/italia/atenei, accessed 28 November 2020. The Italian HEIs include 67 state universities and 19 legally recognized non-state universities, as well as 11 legally recognized non-state universities that offer distance learning.

2. ^Qualtrics (2020). Available online at: https://www.qualtrics.com.

References

Adams, C. (2013). Sustainability reporting and performance management in universities: challenges and benefits. Sustain. Account. Manag. Policy J. 4, 384–392. doi: 10.1108/SAMPJ-12-2012-0044

Adams, C. A., and Frost, G. R. (2008). Integrating sustainability reporting into management practices. Account. Forum. 32, 288–302. doi: 10.1016/j.accfor.2008.05.002

Adams, C. A., and Harte, G. (1998). The changing portrayal of the employment of women in British banks' and retail companies' corporate annual reports. Account. Org. Soc. 23, 781–812. doi: 10.1016/S0361-3682(98)00028-2

Albrecht, P., Burandt, S., and Schaltegger, S. (2007). Do sustainability projects stimulate organizational learning in universities? Int. J. Sustain. High. Educ. 8, 403–415. doi: 10.1108/14676370710823573

Aleixo, A. M., Azeiteiro, U. M., and Leal, S. (2020). Are the sustainable development goals being implemented in the Portuguese higher education formative offer? Int. J. Sustain. High. Educ. 21, 336–352. doi: 10.1108/IJSHE-04-2019-0150

Aleixo, A. M., Leal, S., and Azeiteiro, U. M. (2018). Conceptualization of sustainable higher education institutions, roles, barriers, and challenges for sustainability: an exploratory study in Portugal. J. Clean. Prod. 172, 1664–1673. doi: 10.1016/j.jclepro.2016.11.010

Alonso-Almeida, M. D. M., Llach, J., and Marimon, F. (2014). A closer look at the “Global Reporting Initiative” sustainability reporting as a tool to implement environmental and social policies: a worldwide sector analysis. Corp. Soc. Resp. Env. Ma. 21, 318–335. doi: 10.1002/csr.1318

Alonso-Almeida, M. D. M., Marimon, F., Casani, F., and Rodriguez-Pomeda, J. (2015). Diffusion of sustainability reporting in universities: current situation and future perspectives. J. Clean. Prod. 106, 144–154. doi: 10.1016/j.jclepro.2014.02.008

Amaral, L. P., Martins, N., and Gouveia, J. B. (2015). Quest for a sustainable university: a review. Int. J. Sustain. High. Educ. 16, 155–172. doi: 10.1108/IJSHE-02-2013-0017

ANVUR. (2019). Linee Guida per la Gestione Integrata dei Cicli di Performance e di Bilancio Delle Università Statali Italiane. Available online at: https://www.anvur.it/wp-content/uploads/2019/01/Linee-Guida-per-la-gestione-integrata-del-ciclo-della-performance-e-del-bilancio.pdf (accessed December 15, 2020).

Appelbaum, S. H., St-Pierre, N., and Glavas, W. (1998). Strategic organizational change: the role of leadership, learning, motivation and productivity. Manag. Decis. 36, 289–301.

Atkinson, G. (2000). Measuring corporate sustainability. J. Environ. Plan. Manag. 43, 235–252. doi: 10.1080/09640560010694

Aversano, N., Di Carlo, F., Lucchese, M., Sannino, G., and Tartaglia Polcini, P. (2020). “Linee guida per il Bilancio di Genere negli Atenei italiani: quali differenze rispetto alla prassi?,” Paper presented at SIDREA National Congress, University of Bari, 20th November 2020 (Bari).

Barth, M. (2013). Many roads lead to sustainability: a process-oriented analysis of change in higher education. Int. J. Sustain. High. Educ. 14, 160–175. doi: 10.1108/14676371311312879

Baruch, Y. (1999). Response rate in academic studies-a comparative analysis. Hum. Relat. 52, 421–438.

Beringer, A. (2007). The Lüneburg Sustainable Project in international comparison. An assessment against North American peers. Int. J. Sustain. High. Educ. 8, 446–461. doi: 10.1108/14676370710823609

Bettio, F., and Rosselli, A. (2018). “Gender budgeting in Italy: a laboratory for alternative methodologies?” in Gender Budgeting in Europe, eds A. O'Hagan and E. Klatzer (Cham: Palgrave Macmillan), 199–220.

Blanco-Portela, N., Benayas, J., Pertierra, L. R., and Lozano, R. (2017). Towards the integration of sustainability in Higher Education Institutions: a review of drivers of and barriers to organisational change and their comparison against those found of companies. J. Clean. Prod. 166, 563–578. doi: 10.1016/j.jclepro.2017.07.252

Botlhale, E. (2011). Gender-responsive budgeting: the case for Botswana. Dev. South. Afr. 28, 61–74. doi: 10.1080/0376835X.2011.545170

Broadbent, J. (2016). A gender agenda. Meditari Account. Res. 24, 169–181. doi: 10.1108/MEDAR-07-2015-0046

Burritt, R. L., and Schaltegger, S. (2010). Sustainability accounting and reporting: fad or trend? Account. Audit. Account. J. 23, 829–846. doi: 10.1108/09513571011080144

Callerstig, A. C. (2016). “Gender training as a tool for transformative gender mainstreaming: evidence from Sweden”, in The Politics of Feminist Knowledge Transfer: Gender Training and Gender Expertise, eds M. Bustelo, L. Ferguson, and M. Forest (London, UK: Palgrave Macmillan),118–138.

Ceulemans, K., Lozano, R., and Alonso-Almeida, M. D. M. (2015a). Sustainability reporting in higher education: interconnecting the reporting process and organisational change management for sustainability. Sustainability 7, 8881–8903. doi: 10.3390/su7078881

Ceulemans, K., Molderez, I., and Liedekerke, L. V. (2015b). Sustainability reporting in higher education: a comprehensive review of the recent literature and paths for further research. J. Clean. Prod. 106, 127–143. doi: 10.1016/j.jclepro.2014.09.052

Council of Europe. (1998). Recommendation No. R (98) 14 of the Committee of Ministers to Member States on Gender Mainstreaming. Strasbourg: Council of Europe.

Cronbach, L. J. (1951). Coefficient alpha and the internal structure of tests. Psychometrika 16, 297–334.

Daub, C. (2007). Assessing the quality of sustainability reporting: an alternative methodological approach. J. Clean. Prod. 15, 75–85. doi: 10.1016/j.jclepro.2005.08.013

Daub, C., Hasler, M., Verkuil, A. H., and Milow, U. (2020). Universities talk, students walk: promoting innovative sustainability projects. Int. J. Sustain. High. Educ. 21, 97–111. doi: 10.1108/IJSHE-04-2019-0149

Del Sordo, C., Farneti, F., Guthrie, J., Pazzi, S., and Siboni, B. (2016). Social reports in Italian universities: disclosures and preparers' perspective. Meditari Account. Res. 24, 91–110. doi: 10.1108/MEDAR-09-2014-0054

Dempsey, N., Bramley, G., Power, S., and Brown, C. (2011). The social dimension of sustainable development: defining urban social sustainability. Sustain. Dev. 19, 289–300. doi: 10.1002/sd.417

DeSimone, L. D., and Popoff, F. (2000). Eco-Efficiency. The Business Link to Sustainable Development. Cambridge, MA: MIT Press.

Disterheft, A., Ferreira da Silva Caeiro, S. S., Ramos, M. R., and de Miranda Azeiteiro, U. M. (2012). Environmental Management Systems (EMS) implementation processes and practices in European higher education institutions: top-down versus participatory approaches. J. Clean. Prod. 31, 80–90. doi: 10.1016/j.jclepro.2012.02.034

Domingues, A. R., Lozano, R., Ceulemans, K., and Ramos, T. B. (2017). Sustainability reporting in public sector organisations: exploring the relation between the reporting process and organisational change management for sustainability. J. Environ. Manage. 192, 292–301. doi: 10.1016/j.jenvman.2017.01.074

Doppelt, B. (2000). Leading Change Toward Sustainability. A Change-Management Guide for Business, Government and Civil Society. Sheffield, UK: Greenleaf Publishing.

Dunphy, D., Griffiths, A., and Benn, S. (2003). Organizational Change for Corporate Sustainability. London, UK: Routledge.

Farinha, C., Caeiro, S., and Azeiteiro, U. (2019). Sustainability strategies in Portuguese higher education institutions: commitments and practices from internal insights. Sustainability 11:3227. doi: 10.3390/su11113227

Ferrero-Ferrero, I., Fernández-Izquierdo, M. Á., Muñoz-Torres, M. J., and Bellés-Colomer, L. (2018). Stakeholder engagement in sustainability reporting in higher education: an analysis of key internal stakeholders' expectations. Int. J. Sustain. High. Educ. 19, 313–336. doi: 10.1108/IJSHE-06-2016-0116

Findler, F., Schönherr, N., Lozano, R., and Stacherl, B. (2018). Assessing the impacts of Higher Education Institutions on sustainable development-an analysis of tools and indicators. Sustainability 11:59. doi: 10.3390/su11010059

Fioravanti, C., Andreozzi, V., Borelli, S., et al. (2015). GerPA. Bilancio di Genere Nelle Pubbliche Amministrazioni. Naples: Jovene Editore.

Freeman, R. E. (1984). Strategic Management. A Stakeholder Approach. Boston, MA: Pitman Publishing Inc.

Galizzi, G. (2011). Gender auditing vs gender budgeting: il ciclo della accountability di genere. Azien. Pubbl. 4, 379–394.

Galizzi, G., and Siboni, B. (2016). Positive action plans in Italian universities: does gender really matter? Medi. Account. Res. 24, 246–268. doi: 10.1108/MEDAR-09-2015-0062

GRI. (2011). G4 Sustainability Reporting Guidelines. Globlar Reporting Initiative. Available online at: www.globalreporting.org (accessed January 20, 2021).

Halford, S. (1991). Feminist change in a patriarchal organisation: the experience of women's initiatives in local government and implications for feminist perspectives on state institutions. Sociol Rev. 39(1_Suppl), 155–185. doi: 10.1111/j.1467-954X.1991.tb03359.x

Hayter, C. S., and Cahoy, D. R. (2016). Toward a strategic view of higher education social responsibilities: a dynamic capabilities approach. Strateg. Organ. 16, 1–23. doi: 10.1177/1476127016680564

Hesselbarth, C., and Schaltegger, S. (2014). Educating change agents for sustainability – learnings from the first sustainability management master of business administration. J. Clean. Prod. 62, 24–36. doi: 10.1016/j.jclepro.2013.03.042

Hill, L. M., and Wang, D. (2018). Integrating sustainability learning outcomes into a university curriculum: a case study of institutional dynamics. Int. J. Sustain. High. Educ. 19, 699–720. doi: 10.1108/IJSHE-06-2017-0087

Hoover, E., and Harder, M. K. (2015). What lies beneath the surface? The hidden complexities of organisational change for sustainability in higher education. J. Clean. Prod. 106, 175–188. doi: 10.1016/j.jclepro.2014.01.081

Hopper, T. (2019). Stop accounting myopia: – think globally: a polemic. J. Account. Organ. Chang. 15, 87–99. doi: 10.1108/JAOC-12-2017-0115

Hopwood, B., Mellor, M., and O'Brien, G. (2005). Sustainable development: mapping different approaches. Sustain. Dev. 13, 38–52. doi: 10.1002/sd.244

Huber, S., and Bassen, A. (2018). Towards a sustainability reporting guideline in higher education. Int. J. Sustain. High. Educ. 19, 218–232. doi: 10.1108/IJSHE-06-2016-0108

Ioannides, I. (2017). EU Gender Action Plan 2016-2020 at Year One: European Implementation Assessment Study. European Parliamentary Research Service. Brussels, Belgium: European Parliament.

Italian Parliament. (2005). Legislative Decree 198/2006. Codice Delle Pari Opportunità tra Uomo e Donna, a Norma Dell'articolo 6 Della Legge 28 Novembre 2005, n. 246.

Italian Parliament. (2009). Legislative Decree 150/2009. Attuazione Della Legge 4 Marzo 2009, n. 15, in Materia di Ottimizzazione Della Produttività del Lavoro Pubblico e di Efficienza e Trasparenza Delle Pubbliche Amministrazioni.

Jongbloed, B., Enders, J., and Salerno, C. (2008). Higher education and its communities: interconnections, interdependencies and a research agenda. High. Educ. 56, 303–324. doi: 10.1007/s10734-008-9128-2

Kolk, A. (2010). Trajectories of sustainability reporting by MNCs. J. World Bus. 45, 367–374. doi: 10.1016/j.jwb.2009.08.001