Florian Zenglein

Florian Zenglein- Institute for Political Science, Department of International Relations, Technical University of Darmstadt, Darmstadt, Germany

This article asks how politicization changes the standardization of biodiversity in the realm of corporate sustainable reporting (CSR) frameworks. The study encompasses three areas: First, the participatory processes in standardization; second, the substantive prioritization of conservation considerations over economic aspects within standards; and third, the interplay between private and public standard-setting bodies. It argues that the European Union (EU) is taking on a more assertive role, shaping corporate reporting practices and the standards established by private organizations. Additionally, the standard-setting process is evolving from a technical exercise to a more politicized undertaking. The introduction of the EU Green Deal (EUG) brought in new biodiversity regulations, CSR frameworks, and standards, resulting in a new dynamic in politicizing biodiversity standardization. As a result, the number of actors with opposing interests is increasing, thereby intensifying the contestation of the standardization of biodiversity. Therefore, political rather than technical considerations increasingly drive biodiversity standardization processes in the EU. The EU is progressively expanding its role in two distinct yet complementary ways. Firstly, it is implementing political objectives through targeted reporting. Secondly, it provides an arena in which various actors are included. To elaborate on this argument, a qualitative analysis in the European context is conducted, highlighting the dynamics in the development of standards in CSR frameworks. Accordingly, the analysis encompasses standards and frameworks proposed by the EU, as well as by private standard-setting bodies GRI, ISO, ISBB, and CDP.

1 Introduction

The rapid global loss of biodiversity, unprecedented in human history, has prompted increasing regulatory focus on economic activities as a primary driver of this decline (IPBES, 2019). Despite the growing recognition of the impacts and dependencies of economic sectors on biodiversity, recent analyses indicate that large multinational corporations and financial institutions have been slow to implement comprehensive measures and objectives for the management of their impacts and dependencies on biodiversity (Ascui and Cojoianu, 2019; ECB, 2022; OECD, 2023). As a result, there have been significant challenges in mainstreaming biodiversity measures into sectoral policies, particularly in terms of operationalization and institutional innovation (Persson and Runhaar, 2018; Pröbstl et al., 2023; Runhaar et al., 2024). One of the causes cited for this is the absence of coordinated action, adequate data, and standardized metrics for operationalizing biodiversity impacts and dependencies (McKinsey, 2022; PwC and WWF, 2022).

The mainstreaming of biodiversity into economic sectors is a central approach to strengthening biodiversity conservation in this area, by reducing policy incoherence and raising awareness among economic actors of their dependencies and impacts on biodiversity (Huntley, 2014; Whitehorn et al., 2019; Visseren-Hamakers and Kok, 2022). A key element of mainstreaming is corporate sustainability reporting (CSR), through which standards are established, that furnish a resilient and comparable framework for biodiversity-related data measurement and comparability (Whitehorn et al., 2019; World Economic Forum, 2020). However, recent analysis surrounding the extinction accounting literature has highlighted the shortcomings of many current CSR frameworks and standards (Maroun and Atkins, 2018; Hassan et al., 2022; Kopnina et al., 2024).

It is evident from these studies that the design of CSR frameworks and standards should incorporate comprehensive disclosure requirements to facilitate a transformation process within organizations (Adler et al., 2018; Boiral et al., 2018). To achieve this, biodiversity conservation must be accorded a higher level of priority within the context of emerging CSR frameworks and standards (Zolyomi et al., 2023). Moreover, CSR frameworks should be designed to include both negative and positive information based on uniform indicators, taking into account both financial and deep ecological factors (Atkins and Maroun, 2018; Hassan et al., 2022; Kopnina et al., 2024). In doing so, operationalizable standards can enable companies and other relevant stakeholders to more effectively manage their impacts on biodiversity in practice and motivate them to preserve biodiversity (Maroun and Atkins, 2018).

Since the introduction of the European Green Deal (EUG) in 2019, a new dynamic has emerged in the EU, in which the political landscape surrounding standardization for CSR frameworks seems to be evolving. The EUG has led to the creation of several new frameworks for reporting and accounting for greenhouse gas emissions (GHG emissions), as well as the introduction of mandatory guidelines for biodiversity (European Commission, 2023e; Baehr et al., 2024). Thus, a trend toward the politicization of biodiversity standardization can be observed, which is leading to new participatory processes and changing contents of CSR frameworks and standards. This politicization process has the potential to address the criticism of standardization that has been highlighted in the literature. Furthermore, it could help bridge the implementation gap for biodiversity measures in the business sector.

In line with these current debates and novel policy dynamics, the following research question is posed: How does politicization change the standardization of biodiversity? The analysis is structured around three areas: First, the participatory processes of actor inclusion in standardization; second, the prioritization of conservation considerations over economic aspects within standards; and third, the interplay between private and public standard-setting bodies. The European Union (EU) was chosen as the case study for this analysis because it has become a global frontrunner in the establishment of new CSR frameworks and standards since the launch of the EUG. With the strong promotion of new and influential CSR frameworks and the creation of comprehensive policy regulations, new dynamics of the politicization of biodiversity standardization are most likely to be observed. To comprehensively capture these effects, the EU Taxonomy, the Corporate Sustainability Reporting Directive (CSRD), the European Sustainability Reporting Standards (ESRS), as well as the private standard-setting bodies, the Global Reporting Initiative (GRI), the International Organization for Standardization (ISO), the International Sustainability Standards Board (ISSB), and CDP (formerly Carbon Disclosure Project), are included in this research.

This study explores how the increasing politicization of CSR frameworks in the EU is shaping new biodiversity standardization, with particular attention to participatory processes, conservation prioritization, and the public-private interplay in standard-setting. The analysis of these dynamics is essential to capture the diverse political requirements, that guide the subsequent development of accounting and reporting frameworks and data applications. This addresses a research gap caused by the predominant focus on technical aspects of standardization and by the political novelty of the issue.

The article is organized as follows: first, the theoretical and methodological framework, focusing on politicization and standardization concepts. Next, the study reviews biodiversity standardization challenges, followed by a qualitative analysis of politicization in three areas: participatory dynamics, conservation prioritization; and private and public standard-setting. Finally, policy implications for CSR and biodiversity conservation are discussed, and directions for future research are outlined.

2 Theoretical and methodological framework

2.1 Methodology

The approach of this research followed a systematic analytical procedure. It is guided by a definition of terms and an outline of the theoretical framework. This is the basis for the characterization of the politicization of standardization in current CSR frameworks, their interpretation, and the discussion of the role of various stakeholders in politicizing standardization processes and the prioritization of conservation in standards. The theoretical framework and the definition of terms are presented in section 2.2. The qualitative analysis addresses issues of participation in standardization processes, the substantive prioritization of conservation considerations over economic aspects within standards, and the alignment of private standard-setting bodies with public CSR frameworks and policy objectives. Methodologically, this analysis follows a three-step procedure: First, a review of current literature and relevant documents, second the identification of current policy dynamics and trends, and third the summarization and derivation of implications for future developments. The analysis is based on a qualitative evaluation of official legal documents, implementing regulations, delegated acts of the EU, and private standard-setting bodies since the introduction of the EUG in 2019. In the case of the EU, the delegated acts and regulations, annexes, and documents of public communication such as websites or press releases regarding the EU Taxonomy, CSRD, and ESRS were analyzed. The selection of private standard-setting bodies is limited to a selection of globally recognized organizations, namely GRI, ISO, ISSB, and CDP, and their latest standards. The analysis covers these biodiversity-related assessment and disclosure frameworks and standards, as they are widely applied and established new or revised during the period under review.

2.2 The politicization of standardization

The methodological approach is guided by the definition and theoretical framework of politicization and standardization, which are outlined as follows. The defining characteristics of politicization are the increased salience and contestation of an issue, the expansion of the number of actors with conflicting positions, and the emergence of political conflicts around that issue (Hutter and Grande, 2014; Brokema, 2016; Roland and Römgens, 2022). Consequently, previously non-political matters are introduced into the political domain by incorporating them into broader political discourses. This, in turn, results in heightened visibility, communication, and contestation of these matters in the public sphere (De Wilde, 2011; Ecker-Ehrhardt and Zürn, 2013; Botchwey and Cunningham, 2021). The range of issues that can become politicized is extensive and includes abstract political issues such as environmental protection or specific instruments such as CSR standards (Botchwey and Cunningham, 2021). The increase in the number of actors espousing conflicting positions is exemplified within the EU by shifting dynamics between EU-level institutions and non-governmental and EU actors (Schmidt, 2019; Roland and Römgens, 2022).

The contestation of specific issues and the expansion of actors exert a significant influence on the process of standardization. ISO/IEC (2004, p. 4) defines standardization as ‘an activity of establishing, concerning actual or potential problems, provisions for common and repeated use, aimed at achieving the optimum degree of order in a given context.’ As part of the wider political landscape, standards, in general, have long been incorporated into policy, beginning with directives for industry and extending to contemporary requirements for good governance (Timmermans and Epstein, 2010; Steffek and Wegmann, 2021). Following this, standards can be classified into two principal categories: technology- or product-based standards, and performance- or process-based standards (Stavins, 2003; Steffek and Wegmann, 2021). In this regard, they serve a variety of functions. This entails the generation of comparable and transparent data that inform the formulation of policies and the management of businesses by furnishing pertinent information (Runhaar et al., 2024). In the realm of the financial market, they define best-practice rules for companies, state regulators, and investors (Krewer, 2005). In doing so, standards play a central role in the construction of global economic spaces (Larner and Le Heron, 2004). In summary, standardization can be regarded as a practice that establishes uniformities by abstractly representing complexities through comparable indicators, rendering issues operationalizable and thus governable (Fransen and Bulkeley, 2024).

Standard-setting bodies can be divided into two categories: public bodies, such as the EU, which can develop mandatory standards; and private bodies, which typically establish voluntary standards, including certification schemes and eco-labels (Marx et al., 2024). Within these standard-setting bodies, standardization usually involves specific stakeholders, such as industry insiders, scientists, or government representatives, who are considered to have a high level of expertise in the field (Timmermans and Epstein, 2010). Despite the technocratic character and apparent neutrality of standardization, it is by no means objective but is shaped by the interests and values of the actors involved (Brunsson et al., 2012; Broome and Quirk, 2015; Steffek and Wegmann, 2021). This entails the possibility that the participating actors will be able to assert their specific values and interests and thus shape the idea of sustainability incorporated into CSR standards (Elgert, 2010; Sullivan, 2018). As a result, increasing politicization can change the composition of the actors involved in standardization and thus also of the values and interests embodied in standards. Furthermore, standards determined by experts are subjected to public debate and their content becomes contested.

This is particularly pertinent in the field of biodiversity policy, given that conservation practice is, in itself, a normative process, that entails determining where and how certain elements should be protected or restored (Boiral and Heras-Saizarbitoria, 2017; Fransen and Bulkeley, 2024). The analysis of politicization in this area raises the question of how the content of standards and the participatory processes in standardization are changing. For example, there is a potential for a disproportionate influence of economic interests on the standardization process due to an over-representation of economic actors. This could ultimately result in environmental problems being inadequately addressed, thereby facilitating greenwashing (Elgert, 2010; Elliot et al., 2024).

3 Challenges and requirements of biodiversity standardization

Politicization leads to new dynamics in the design of biodiversity CSR frameworks and standards. These dynamics are leading to a change in standardization processes, which are constrained by the inherent complexity of biodiversity and the diversity of economic interests involved. The resulting negotiation between economic operationalization and conservation considerations is a key challenge for standardization. Before examining new dynamics in standardization, however, it is necessary to provide a more detailed account of the distinctive characteristics of the subject of this standardization: biodiversity. To this end, the concept of biodiversity and its inherent complexities are first delineated. Second, the specifics of biodiversity standards and the challenges and expectations associated with their standardization process are described. Third, current standardization approaches and their limitations are presented. These three sections set the stage for the subsequent description of the new dynamics triggered by the politicization processes of standardization within the EU.

3.1 The multifaceted complexity of biodiversity

The narrower definition of biodiversity encompasses three dimensions: genetic, species, and ecosystem diversity. All three describe a wide range of aspects, such as the approximately 1.75 million known species and an estimated 13 million unknown species, the diversity of chromosomes, genes, and DNA within species, and the wide range of ecosystems, such as deserts, forests, wetlands, rivers, etc. (CBD, 2023). However, biodiversity is characterized as a complex system, encompassing not only variation in genetic, species, and ecosystem diversity, but also a variety of factors, including the ‘diversity of structures, forms, colors, of physiology and interactions of organisms, and also the landscape level’ (Haber, 2008, p. 92). A broader definition of biodiversity is proposed by IPBES (2024) which defines it as the ‘variability among living organisms from all sources including terrestrial, marine and other aquatic ecosystems and the ecological complexes of which they are a part. This includes variation in genetic, phenotypic, phylogenetic, and functional attributes, as well as changes in abundance and distribution over time and space within and among species, biological communities and ecosystems.’ This definition is consistent with the understanding of biodiversity underlying this study, as it encompasses its complexity and the interconnectedness of its parts, which has strong economic implications. For example, the genetic diversity of ecosystems is an important factor in their resilience, which in turn is critical to the benefits that economic actors derive from them (Pörtner et al., 2021). These economic benefits are illustrated, for example, by the $44 trillion of economic value creation that is moderately or highly dependent on nature and its services (World Economic Forum, 2020). As a result, it is these complexities that CSR frameworks seek to reflect. However, the complexity, interconnectedness, and contextuality of biodiversity lead not only to the risks and benefits of biodiversity dependencies for economic actors but also to the barriers to the standardization of biodiversity by including all facets of biodiversity in standardization. The challenge for standardization lies in the need for comparable and therefore operational standards for use by different stakeholders while preserving the fundamental interconnectedness and contextual dependencies of biodiversity.

3.2 Standards are a measure to operationalize conservation goals

Environmental management and biodiversity conservation face the challenge that actors from non-environmental sectors are often unclear about their operational meaning (Runhaar et al., 2020). Standardization attempts to bridge this ambiguity by translating complex guidelines into a technical language (Broome and Quirk, 2015; Steffek and Wegmann, 2021). In the realm of biodiversity, conservation is promoted and inconsistencies in implementation are reduced through clear guidelines. For doing so, standards cover aspects such as management of protected areas, sustainable investment of funds, assessment of the condition of protected areas, development of adaptive management approaches, or alignment of practices with CSR frameworks (Dudley et al., 2004). Standards for CSR frameworks provide clear criteria for companies to disclose information to stakeholders, investors, or government regulators through a classification of company performance or value (Broome and Quirk, 2015). Such standards also have an impact within companies by providing a means of understanding environmental dependencies and impacts. In doing so, they incorporate practices and values into new economic spheres and guide companies’ environmental, social, and governance (ESG) activities (Larner, 2004; Friske et al., 2024). Consequently, as a measure of biodiversity policy, standards serve to make the highly complex field of biodiversity policy and conservation operational, thereby creating the necessary conditions for mainstreaming biodiversity into economic processes and enabling the further integration and development of biodiversity policies. To this end, standardization functions as a government technology, that translates complex ecological conditions and conservation goals into uniform criteria (Higgins and Hallström, 2007).

However, in doing so, ‘biodiversity is broken down into abstract and standardized units to make biodiversity legible, commensurable and exchangeable, and hence governable’ (Fransen and Bulkeley, 2024, p. 81). In this process, contexts that do not fit into standards are removed to create comparable indicators. The aim is to create a form of ‘constructed objectivity’ (Broome and Quirk, 2015, p. 821). However, the complexity and context dependency of biodiversity represent a significant challenge for standardization processes and the implementation of mitigation strategies to address biodiversity loss (Smith et al., 2020). For example, the impact of land-use practices on biodiversity varies considerably depending on factors such as the existing flora and fauna in the area, the type of intervention, climatic conditions, soil characteristics, and so forth. The complexity is further enhanced by the multiple interests and values associated with biodiversity. The concept of biodiversity has a high normative content that goes beyond ecological aspects to include values and moral considerations that encompass not only ecological but also social or economic aspects (Toepfer, 2011; Beierkuhnlein, 2012).

3.3 Existing standardization approaches and emerging EU dynamics

Despite these difficulties, concepts have been developed that attempt to quantify and operationalize biodiversity appropriately. Examples of these concepts include ecosystem services and natural capital. Natural capital can be defined ‘as the world’s stocks of natural assets which include geology, soil, air, water and all living things’, that provide a wide range of ecosystem services (Dasgupta, 2021, p. 36; World Forum on Natural Capital, 2024). Biodiversity is the integral biotic part of natural capital, which is inextricably linked to the quality, quantity, and reliability of ecosystem services (Houdet et al., 2020; Cordella et al., 2022). Ecosystem services describe the ‘benefits people obtain from ecosystems.’ (Millennium Ecosystem Assessment Board, 2005, p. 5). These include services such as the provision of resources, pollination through insects, air filtration through trees or even cultural and spiritual aspects (IPBES, 2016). Here, a distinction is made between the stock of ecosystems, which includes ecosystem processes that ensure the health and functionality of ecosystems, and ecosystem services, which represent the actual benefits derived from these ecosystems (Dominati et al., 2010). The concept of ecosystem services seeks to align environmental aspects with financial and economic modes of reasoning, predominantly through monetary valuation (Stevenson et al., 2021).

Despite their highly anthropogenic perspective, it is essential to include established concepts like natural capital in CSR frameworks (Maroun and Atkins, 2018). As companies and investors can only consider the environment from a financial perspective, natural capital is a practical way to simultaneously consider the impact of biodiversity on companies and the impact of companies on biodiversity (Adler et al., 2018; Atkins and Maroun, 2018; Hassan et al., 2022). This dependency of businesses on biodiversity leads to risks such as production disruptions, loss of customers or market share, legal claims, and regulatory changes (World Economic Forum, 2020; Kedward et al., 2021, 2023). Sectors that are particularly dependent on biodiversity include agriculture, aquaculture, fisheries, and forestry (Cardona Santos et al., 2023). The disruptive effects of biodiversity loss on these sectors are reflected in the annual global decline of 2.5% of insect biomass, resulting in an estimated global loss of 4.7% of total fruit production due to insufficient pollination (Sánchez-Bayo and Wyckhuys, 2019; Smith et al., 2022). The total economic damage from biodiversity loss caused by global land use alone between 1997 and 2011 was estimated to be between $4.3 and $20.2 trillion per year (Costanza et al., 2014). Consequently, companies have a strong interest in standardizing biodiversity to effectively assess the associated impacts on business practices (Nedopil, 2023).

However, recent research suggests that large multinational corporations and finance institutions have been slow in implementing comprehensive biodiversity management policies and targets (Ascui and Cojoianu, 2019; ECB, 2022; OECD, 2023). This is the result of the absence of adequate data and standardized metrics for quantifying objectives cumulates with the lack of coordinated action for regulatory requirements for the financial-economic sector, and the requisite knowledge and expertise (McKinsey, 2022; PwC and WWF, 2022). The inadequacy of current conceptual frameworks is evident in the context of ecosystem services. Due to challenges in quantification arising from a lack of knowledge and data foundation, the concept has proven inadequate for both practical applicability for economic and civil society actors and the effective conservation of biodiversity (Stevenson et al., 2021; Allan et al., 2022). Consequently, the concept has only been partially integrated into policies and practices (Zolyomi et al., 2023).

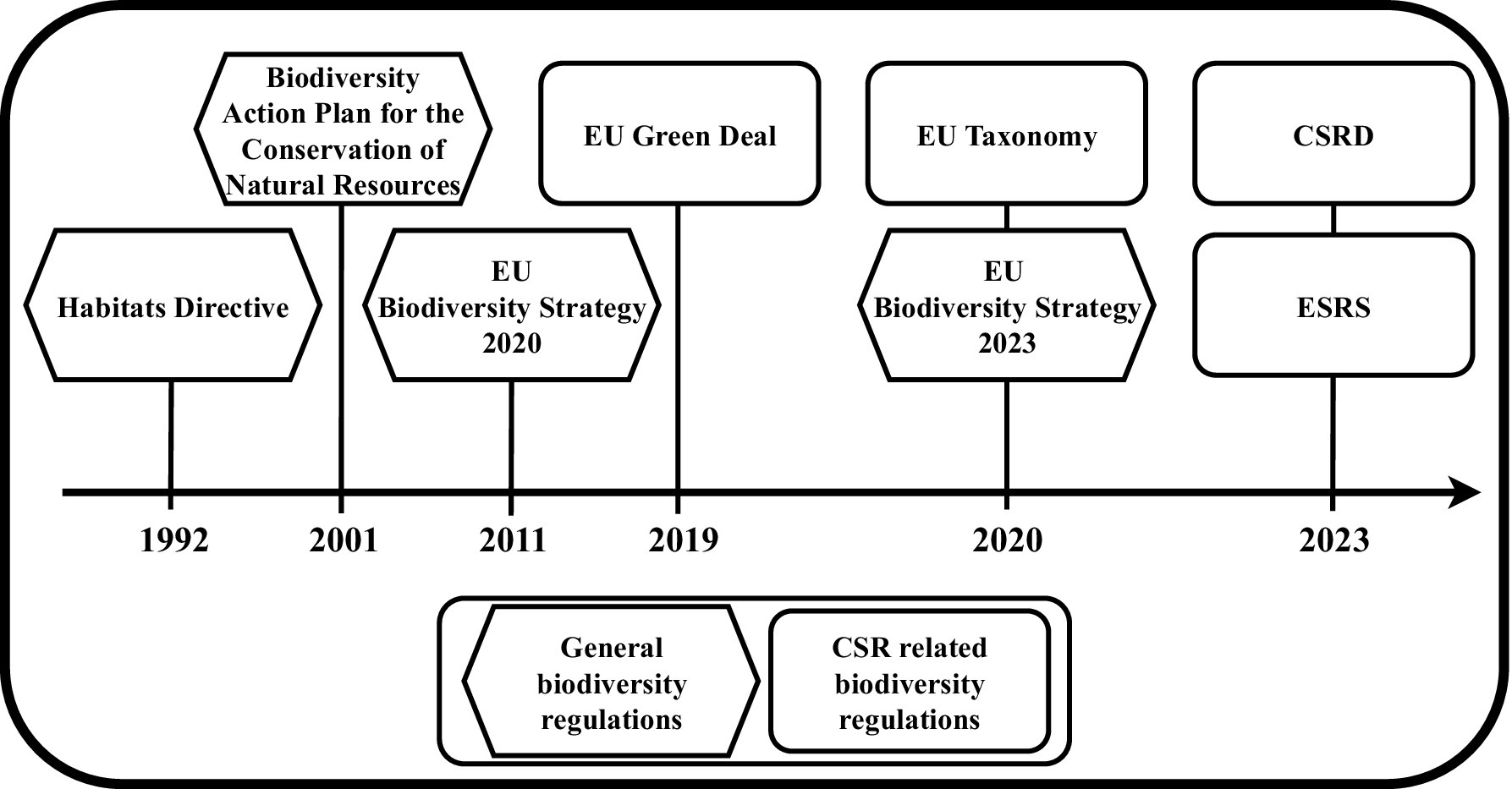

However, since the enactment of the EUG, the EU has adopted new regulations and CSR frameworks that address these gaps and requirements. These new frameworks align with the broader global and EU-wide development in corporate sustainability reporting on GHG emissions since the 1990s (Baehr et al., 2024). In the context of the EU, this trend is characterized by an increase in the mandatory reporting of emissions and the emergence of new regulatory initiatives to achieve climate neutrality by 2050. In contrast, the situation concerning biodiversity reporting and accounting is distinct. The EU’s approach to biodiversity regulation dates back to the 1992 Habitats Directive and the Natura 2000 initiative (European Commission, 2024d). Subsequently, the EU adopted three biodiversity strategies for the next decade in 2001, 2011, and 2020 (European Union, 2006, 2015; European Commission, 2020a). However, the issue of sustainable corporate reporting on impacts and dependencies on biodiversity was only addressed by the EUG, which came into force in 2019, and the most recent EU Biodiversity Strategy 2030 (European Commission, 2020a, 2024a). As a result, mandatory reporting requirements have been defined in the EU Taxonomy (2020) and the CSRD (2023) (European Parliament, 2022; European Commission, 2023c). The EU Taxonomy establishes a common classification system for sustainable economic activities to inform investors and guide financial flows. It includes the ‘conservation, including restoration, of habitats, ecosystems and species’ (European Commission, 2023a, p. 2). Thereby, the EU Taxonomy addresses the criticism that previous standards and corporate practices lacked a unified definition of sustainability (Milne et al., 2009; Maroun and Atkins, 2018). The CSRD, on the other hand, is based on the ESRS standards adopted in 2023, which specify the information that companies must disclose on biodiversity and ecosystems (European Parliament, 2022; European Commission, 2023b). ESRS includes cross-cutting standards that ‘apply to all undertakings regardless of which sector or sectors the undertaking operates in’ (European Commission, 2023b, p. 5). Since 2024, the CSRD has applied to large EU companies with over 500 employees (European Commission, 2024b) (Figure 1).

4 Politicization creates new dynamics in biodiversity standardization

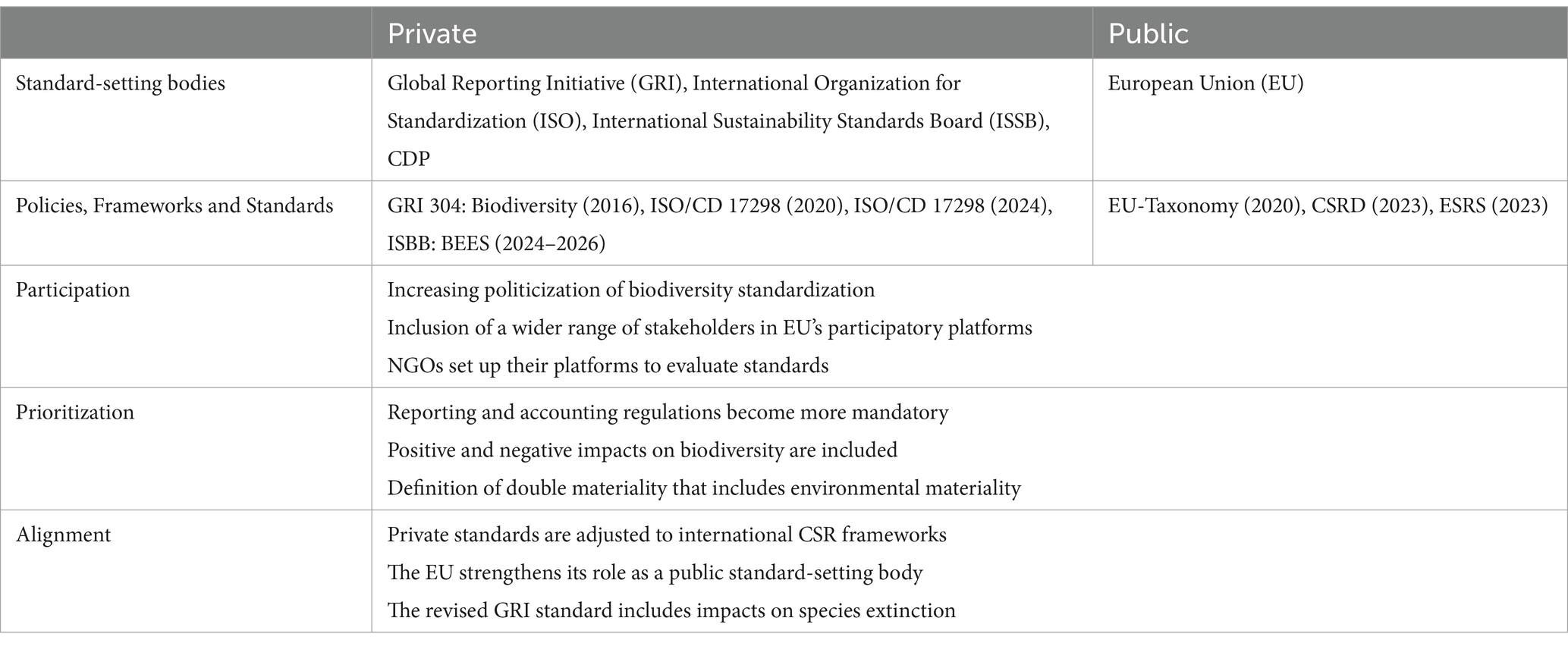

As a consequence of the new dynamics prompted by the enactment of the EGD, the political landscape surrounding CSR frameworks and standards is transforming. It is therefore worthwhile to conduct a more detailed examination of the standardization of biodiversity in the EU. The following section addresses the question of how politicization changes the standardization of biodiversity. This is done under consideration of previously discussed assumptions and challenges. It is argued that in all three areas, the EU is playing an increasingly important role, influencing both corporate reporting practices and standards set by private entities. This, in turn, is the result of the standard-setting process moving from a purely technical exercise to a more politicized endeavor. The subsequent sections are structured around three areas: First, new participatory processes and actor inclusion in standardization, second the shift in the priority given to conservation considerations in standards; and third, the changing interplay between private and public standard-setting bodies. The elements included in this approach and the results derived are presented in Table 1.

Table 1. Findings of current political dynamics and processes in the selected standards and standard-setting bodies.

4.1 A widening range of stakeholder inclusion

Standardization is increasingly integrated into broader policy frameworks and the range of actors and biodiversity aspects covered by standardization is expanding. The EU is actively promoting the involvement of a diverse range of actors in the development and evaluation of standards and indicators set out in the EU Taxonomy and the CSRD.

The broadening spectrum of actors included in standard creation is evident in the ‘Technical Expert Group on Sustainable Finance’ (TEG), whose expertise plays a pivotal role in the standardization processes of the EU (Technical Expert Group on Sustainable Finance, 2020, 36). The TEG comprises 35 members from civil society, academia, business, the financial sector, and other members and observers from EU and international public institutions (European Commission, 2020b). This includes NGOs such as the World Wide Fund (WWF), Finance Watch, and the CDP (European Commission, 2021). Another example is the Platform on Sustainable Finance, which aims to bring together expertise from the corporate and public sectors, industry, academia, civil society, and the financial industry to ‘advise the European Commission on the implementation and usability of the EU Taxonomy and the sustainable finance framework more broadly’ (European Commission, 2024c). Current members include organizations like the Climate Bonds Initiative and the International Sustainable Finance Centre (ISFC) (European Commission, 2023d).

However, environmental organizations, including WWF, left the Platform on Sustainable Finance, criticizing the political decisions that led to the criteria of the EU Taxonomy being too vague (WWF, 2022). The contested nature of the taxonomy is evidenced by the declaration published the following year by 45 NGOs, including the WWF, which called for the ‘extension of the environmental taxonomy to more categories’ and the adoption of ‘criteria for new activities’ (WWF, 2023). In 2024, NGOs and environmental organizations launched the Independent Science Based Taxonomy (ISBT) platform. It aims to independently evaluate the categories of the EU Taxonomy (ISBT, 2024; WWF, 2024). It can be observed that, although the participation process was initiated top-down by the EU, with the introduction of new formalized formats, it was also followed by the emergence of independent formats initiated by NGOs. As a result, there appears to be a growing trend toward greater politicization, resulting in the expansion of the number of actors with conflicting positions and an increasing prominence of biodiversity standardization. This aligns with other studies that demonstrate that the process of biodiversity standardization is being influenced by an increasingly diverse range of stakeholders, including those from civil society, industry, academia, and government (Visseren-Hamakers et al., 2011; Boiral and Heras-Saizarbitoria, 2017).

The broader engagement of diverse actors provides the opportunity for more cooperation, for example between civil society and economic actors. This offers the possibility of establishing new networks, enhancing transparency, anchoring the issue more firmly, and improving oversight by NGOs and state actors (Karlsson-Vinkhuyzen et al., 2017). It is therefore not only environmental organizations that require greater inclusion; there is also unused potential in engaging stakeholders of the financial sector and businesses (Cardona Santos et al., 2023). The broader inclusion of these stakeholders can lead to initiatives that aid in clarifying business expectations and supporting global objectives for improved biodiversity protection (Smith et al., 2020). To have an impact on biodiversity conservation, CSR frameworks, and standards must engage these business stakeholders and capture their attention (Atkins and Maroun, 2018).

In conclusion, the debate of participatory platforms and the contents of regulatory frameworks illustrate the growing politicization of biodiversity standardization. As a result, there is a noticeable trend in the inclusion of a wider range of stakeholders, either through the EU’s participatory platforms or NGOs’ platforms. However, the circle of actors included is still limited to specific experts from international organizations. A broad inclusion of the local level or even a democratization of the process is not to be observed. Given the significant barriers to quantifying and standardizing biodiversity with its economic and social implications, this still represents an opportunity to engage a wider range of values and interests. It also remains to be seen which actors will become the driving force behind standardization and which will ultimately be able to assert their interests (Figure 1).

Figure 1. Timeline of EU biodiversity regulations.

4.2 Prioritization between ecological and economic considerations is shifting

Due to the increase of regulations within the EU and the enhancement of international targets in the Convention on Biodiversity (CBD), CSR frameworks and standards are changing. Especially the Global Biodiversity Framework (GBF), calls to ‘encourage and enable business, and in particular to ensure that large and transnational companies and financial institutions: (a) Regularly monitor, assess, and transparently disclose their risks, dependencies and impacts on biodiversity’ (CBD, 2022). This political encouragement affects private standard-setting bodies, including organizations like GRI, ISO, ISSB, CDP, and public ones like the EU (CDP, 2021; IFRS, 2023; ISO, 2023; European Commission, 2024a; GRI, 2024).

As part of the EGD, the EU Taxonomy and the CSRD play a crucial role in providing guidance for investors and directing investments toward sustainable activities (Afolabi et al., 2022; European Commission, 2023c). Both CSR frameworks are mandatory and apply to companies with more than 500 employees. They set different cross-cutting standards that require companies to disclose their impacts and dependencies on biodiversity. The CSRD covers environmental, social and financial materiality, and includes both business dependencies and impacts on nature (European Commission, 2023b; Tin et al., 2024). Within the framework of the EU Taxonomy, companies are required to specify the condition of habitats influenced by their activities and how they affect these ecosystems or species populations, both negatively and positively (European Commission, 2023a). The regulations necessitate that companies determine the net impact of their biodiversity performance at specific sites and whether their mitigation activities outweigh the negative effects on biodiversity (Smith et al., 2019). In consequence, the CSRD has adopted a definition of double materiality that considers impacts in both positive and negative environmental impacts, thereby enhancing transparency (Hassan et al., 2022; Tin et al., 2024).

Within the EU Taxonomy, the principle of ‘doing no significant harm’ (DNSH) involves a more holistic consideration of sustainability criteria, shifting from focusing only on production to the entire lifecycle along the taxonomy criteria (Dusík and Bond, 2022). The principle states, that ‘an economic activity may not qualify as environmentally sustainable where it significantly harms at least one of the six environmental objectives’ (EPRS, 2022, p. 2). In addition, the EU Taxonomy describes ‘enabling activities’, that have, directly or indirectly, ‘a substantial positive environmental impact based on life-cycle considerations’ (EPRS, 2022, p. 3). This encompasses not only negative impacts on biodiversity due to economic activities but also positive environmental impacts. Therefore, companies are now not only obligated to describe their dependencies on nature’s services but also to report that they are not harming biodiversity (Dusík and Bond, 2022).

This shift underscores the importance of verifiable positive impacts on biodiversity by companies. To make a substantial contribution to the EU Taxonomy’s objective of ‘protection and restoration of biodiversity and ecosystems,’ companies, must demonstrate that their practices either maintain or improve the condition of ecosystems and habitats. This includes the ‘mapping of the current habitats and their condition’ and ‘characterization of the situation of the main species in terms of conservation relevance present in the area’ (European Commission, 2023a). This shows that the EU Taxonomy addresses specific environmental and conservation measures that companies must adhere to. Through such specific guidelines and objectives, best practices and values can be integrated into economic domains (Larner and Le Heron, 2004). In this way, companies are encouraged to improve the integration of these measures into planning and decision-making processes, leading to performance improvements (Adams and McNicholas, 2007; Brunsson et al., 2012). In this case, standards hold the potential to instill specific strategic goals for biodiversity protection within companies (Brunsson et al., 2012; Smith et al., 2020).

In summary, biodiversity standardization in the context of CSR in the EU is gaining political traction. There is evidence that policy objectives are increasingly giving greater weight to environmental sustainability and biodiversity within CSR frameworks and standards. In particular, the DNSH principle and the enabling activities of the EU Taxonomy require that not only negative but also positive impacts on biodiversity are covered. The EU Taxonomy also considers the inclusion of both direct and indirect impacts of activities throughout their lifecycle. In addition, the CSRD includes a definition of materiality, that includes financial, environmental, and social considerations. This demonstrates, that biodiversity considerations are becoming more and more comprehensively covered by these regulations.

4.3 Private standard-setting bodies align with policy objectives and EU CSR frameworks

Private standard-setting bodies are also responding to the increasing political pressure for greater biodiversity conservation by reevaluating their biodiversity standards. For example, the ISSB is currently developing and revising biodiversity, ecosystems, and ecosystem services (BEES) standards in a 2024–2026 work plan (IFRS, 2024). ISSB standards are applied globally in various jurisdictions, such as Australia, Brazil, Canada, and Mexico (Tin et al., 2024). The organization aims to address a fragmented landscape by developing standards for a global baseline of sustainability disclosures (ISSB, 2024). Another globally recognized standard-setting body is ISO, which has developed a large portfolio of standards since 1949 (Brunsson et al., 2012; ISO, 2024). In the realm of biodiversity policy, the ISO Technical Committee ISO/TC 331 is developing standards to enable companies and financial institutions to integrate biodiversity into their strategies. This includes the development of guidelines on specific biodiversity issues such as ecological engineering, nature-based solutions, and relevant technologies (ISO, 2020). For instance, the ISO/CD 17298 standard is designed to assist companies in the thoughtful consideration of specific measures for biodiversity conservation and the sustainable utilization of its components (ISO, 2023). GRI has also joined this process by developing or revising standards that guide companies to disclose their most significant impacts on biodiversity and, in turn, enhance their accountability (GRI, 2024). This includes the GRI 304 standard for ‘best practice on biodiversity management to support companies in addressing their impacts’ (GRI, 2024). GRI standards are widely adopted and are among the most widely used (Boiral and Heras-Saizarbitoria, 2017; Hassan et al., 2022). GRI’s 2023 report found that its standards were referenced in 512 policies in 92 countries (Chalmers et al., 2023; Tin et al., 2024).

The newly developed or revised standards are aligned with international and transnational frameworks, as is the case with ISO/CD 17298. This defines guidelines for ‘mainstreaming biodiversity’s protection, conservation, the sustainable use of its components and the fair and equitable sharing of the benefits arising out of the utilization of genetic resources, within their activities’ (ISO, 2023; GRI, 2024). The wording is identical to that of the Nagoya Convention, which aims at the ‘fair and equitable sharing of the benefits arising from the utilization of genetic resources’ (CBD, 2011, p. 4). Furthermore, the alignment of public and private standards is being actively promoted by both sides. The aim is to fill data gaps and create a uniform framework, for example, done by the CDP with the standards of ISSB, GRI, and ESRS (CDP, 2024). Also, the EU is actively exchanging information with private organizations such as the ISSB and the GRI (European Commission, 2023e).

In consequence, mandatory CSR frameworks, political objectives, and the promoted alignment of private and public standards increase the pressure on the technical exercise of standardization to align with the ideals of sustainable economies and biodiversity conservation. For instance, in the GBF, there is a requirement that reporting for ‘large as well as transnational companies and financial institutions’ must be designed to ‘progressively reduce negative impacts on biodiversity, increase positive impacts, reduce biodiversity-related risks to business and financial institutions, and promote actions to ensure sustainable patterns of production’ (CBD, 2022). Many private standard setters, such as GRI, refer to the GBF as they revise their own frameworks and standards for biodiversity to ensure their alignment with international objectives (GRI, 2024). As a result, GRI also includes standards on the type and quantity of wild species used and their risk of extinction at sites (Tin et al., 2024).

In summary, standards can serve as a valuable policy measure to support the operationalization and implementation of biodiversity policy objectives in economic sectors. This is evidenced by the significant revision of existing and development of new private standards to meet international policy objectives. The revised GRI framework, in particular, includes biodiversity mainstreaming objectives and standards that now also cover aspects of species extinction. The dynamic is also reflected in the increasing focus of private standard-setting bodies on mandatory CSR frameworks by the EU, which is establishing itself as a standard-setter and expanding its role in this area. Consequently, the EU and GBF are becoming important reference points for CSR and standard setting. However, challenges remain in implementing these CSR frameworks and standards, as they often require companies to substantially review and restructure internal and supply chain processes. But therein lies also the transformative potential of these standards.

5 Conclusion

Mandatory and voluntary biodiversity standards for CSR frameworks are gaining political traction in the EU. Since the introduction of the EUG, several new biodiversity regulations and CSR frameworks have been established. This triggered new processes for stakeholder engagement in standardization, prioritization of conservation in new and revised standards, and the alignment of voluntary standards with mandatory EU frameworks. This is the result of the politicization of standardization, as evidenced on the one hand by broader participation formats and on the other hand by the increasing prioritization of biodiversity aspects within standards. As a consequence, standardization processes are becoming increasingly shaped by political considerations rather than technical ones. Due to the increased visibility and number of stakeholders, the formulation of standards, as evidenced by the participatory processes of the EU taxonomy, is becoming more contested. Hereby, the EU is progressively expanding its role in two distinct yet complementary ways. Firstly, it is implementing political objectives through mandatory CSR frameworks. Secondly, it provides an arena in which various stakeholders are included.

One recommendation for biodiversity policy is to utilize this politicization and increase focus on broader stakeholder inclusion. For example, the local level must be actively engaged in discussions, development, and implementation, taking into consideration local knowledge. This inclusion ensures that instruments and standards can be tailored to practices in specific locations, thus aligning policy with the realities of the local context. The initial positive indications can be observed in the broader inclusion of stakeholders, particularly environmental organizations.

A second policy implication arises from the trend toward more comprehensive and detailed reporting requirements and the alignment of private standard-setters. Although there is a shift toward a greater focus on conservation considerations in standardization, there is still a need for further mandatory inclusion of positive aspects and open disclosure of impacts at the local level. While there is a tendency for more and more impacts and dependencies to be included, there is still no evidence of a sustained trend toward a more ecocentric perspective that considers the intrinsic value of nature. Such a perspective would incorporate all aspects of biodiversity, not just those that benefit humans. A changed focus on biodiversity could serve as a counterbalance to the financial considerations that typically prevail in standardization processes within this field.

The establishment of more robust CSR frameworks and standards offers a pathway for more firmly anchoring biodiversity within the economic sector, thereby addressing the existing implementation gaps based on a lack of quantifiability and information. However, financial considerations continue to exert a dominant influence, because the primary objective of companies is still to maximize shareholder value. Consequently, the subject of biodiversity will be viewed primarily through an economic lens, with reporting being regarded as a mere boundary condition or even a nuisance. In addition, there is a risk that the sharp increase in mandatory disclosure of GHG emissions, together with the now increasing requirements for biodiversity accounting and reporting, will lead to a possible overburdening of companies. As a result, there is a risk of a trend toward process standards that lead to more reporting and documentation, but with potentially less and less substance.

Consequently, it is yet to be determined whether the politicization process will ultimately result in sufficient protection of biodiversity within the context of CSR frameworks and standards. Nevertheless, the politicization of this issue may offer a potential pathway to greater prioritization of biodiversity, particularly through the involvement of environmental NGOs. This may serve as a counterweight to the economization of biodiversity, which is a result of the disproportionate influence of economic actors and interests in the standardization of biodiversity. The politicization provides an opportunity to create a countertrend to greenwashing by CSR, as it brings biodiversity standardization into the public sphere.

However, the study also has some limitations, which provide opportunities for future research. Although the study includes international aspects, it is primarily focused on the European context. Even if the EU is a frontrunner and a politically and economically significant area, it remains open whether similar trends can be observed in other areas. Furthermore, while this article has provided an overview of the macro-level dynamics, there is scope for further research into the micro-level aspects of mainstreaming. This includes, for example, how standardization can stimulate organizational and institutional change within firms. This requires an examination of the internal dynamics of firms and financial institutions to determine their alignment with policy objectives and regulations, and how these are translated into the firm context. One of the most critical issues to be addressed is how to reconcile the goal of halting biodiversity loss with existing business models, with a particular focus on conservation.

Data availability statement

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

Author contributions

FZ: Writing – original draft, Writing – review & editing.

Funding

The author(s) declare financial support was received for the research, authorship, and/or publication of this article. This work was supported by the BMBF-Research Initiative for the Conservation of Biodiversity (FEdA) under Grant number 16LW0074K.

Acknowledgments

The project on which this publication is based was funded by the German Federal Ministry of Education and Research (BMBF) within the Research Initiative for the Conservation of Biodiversity (FEdA) under the funding code 16LW0074K. The responsibility for the content of this publication lies with the authors.

Conflict of interest

The author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Adams, C. A., and McNicholas, P. (2007). Making a difference: sustainability reporting, accountability and organisational change. Acc. Auditing Acc. J. 20, 382–402. doi: 10.1108/09513570710748553

Adler, R., Mansi, M., and Pandey, R. (2018). Biodiversity and threatened species reporting by the top fortune global companies. Acc. Auditing Acc J. 31, 787–825. doi: 10.1108/AAAJ-03-2016-2490

Afolabi, H., Ram, R., and Rimmel, G. (2022). Harmonization of sustainability reporting regulation: analysis of a contested arena. Sustain. For. 14:5517. doi: 10.3390/su14095517

Allan, J. I., Auld, G., Cadman, T., and Stevenson, H. (2022). Comparative fortunes of ecosystem services as an international governance concept. Global Pol. 13, 62–75. doi: 10.1111/1758-5899.13036

Ascui, F., and Cojoianu, T. F. (2019). Implementing natural capital credit risk assessment in agricultural lending. Bus. Strateg. Environ. 28, 1234–1249. doi: 10.1002/bse.2313

Atkins, J., and Maroun, W. (2018). Integrated extinction accounting and accountability: building an ark. Acc. Auditing Acc J. 31, 750–786. doi: 10.1108/AAAJ-06-2017-2957

Baehr, J., Zenglein, F., Sonnemann, G., Lederer, M., and Schebek, L. (2024). Back in the driver’s seat: how new EU greenhouse-gas reporting schemes challenge corporate accounting. Sustain. For. 16:3693. doi: 10.3390/su16093693

Beierkuhnlein, C. (2012). “Verständnis und Politisierung des Konzeptes der Biodiversität” in Wege zu einem ziel- und bedarfsorientierten Monitoring der Biologischen Vielfalt im Agrar- und Forstbereich. ed. J. Dauber (Braunschweig: Johann Heinrich von Thünen-Institut), 41–48.

Boiral, O., and Heras-Saizarbitoria, I. (2017). Best practices for corporate commitment to biodiversity: an organizing framework from GRI reports. Environ Sci Policy 77, 77–85. doi: 10.1016/j.envsci.2017.07.012

Boiral, O., Heras-Saizarbitoria, I., and Brotherton, M.-C. (2018). Corporate biodiversity management through certifiable standards. Bus. Strateg. Environ. 27, 389–402. doi: 10.1002/bse.2005

Botchwey, B. S., and Cunningham, C. (2021). The politicization of protected areas establishment in Canada. FACETS 6, 1146–1167. doi: 10.1139/facets-2020-0069

Brokema, W. (2016). Crisis-induced learning and issue politicization in the EU: the Braer, sea empress, Erika, and prestige oil spill disasters. Public Adm. 94, 381–398. doi: 10.1111/padm.12170

Broome, A., and Quirk, J. (2015). Governing the world at a distance: the practice of global benchmarking. Rev. Int. Stud. 41, 819–841. doi: 10.1017/S0260210515000340

Brunsson, N., Rasche, A., and Seidl, D. (2012). The dynamics of standardization: three perspectives on standards in organization studies. Organ. Stud. 33, 613–632. doi: 10.1177/0170840612450120

Cardona Santos, E. M., Kinniburgh, F., Schmid, S., Büttner, N., Pröbstl, F., Liswanti, N., et al. (2023). Mainstreaming revisited: experiences from eight countries on the role of National Biodiversity Strategies in practice. Earth Syst. Governance 16:100177. doi: 10.1016/j.esg.2023.100177

CBD. (2011). Nagoya Protocol on Access to Genetic Resources and the Fair and Equitable Sharing of Benefits Arising from their Utilization to The Convention on Biological Diversity. Secretariat of the Convention on Biological Diversity: Montreal.

CBD (2022). COP15: final text of the Kunming-Montreal global biodiversity framework. Available at: https://www.cbd.int/article/cop15-final-text-kunming-montreal-gbf-221222 (Accessed October 22, 2024).

CBD (2023). Biodiversity. Available at: https://www.cbd.int/youth/biodiversity (Accessed October 22, 2024).

CDP (2021). Disclosing nature’s potential: corporate responses and the need for greater ambition. London: UK and IUCN, Gland, Switzerland.

CDP (2024). CDP's alignment with disclosure frameworks and standards. Available at: https://www.cdp.net/en/2024-disclosure/disclosure-frameworks-and-standards (Accessed October 22, 2024).

Chalmers, A., Klingler-Vidra, R., van der Lugt, C., van de Wijs, P.P., and Bailey, T. (2023). Carrots and sticks: beyond disclosure in ESG and sustainability policy: annual report September 2023. Available at: https://www.carrotsandsticks.net/ (Accessed October 22, 2024).

Cordella, M., Gonzalez-Redin, J., Lodeiro, R. U., and Garcia, D. A. (2022). Assessing impacts to biodiversity and ecosystems: understanding and exploiting synergies between life cycle assessment and natural capital accounting. Procedia CIRP 105, 134–139. doi: 10.1016/j.procir.2022.02.023

Costanza, R., Groot, R.De, Sutton, P., van der Ploeg, S., Anderson, S.J., Kubiszewski, I., et al. (2014). Changes in the global value of ecosystem services. Glob. Environ. Chang. 26, 152–158. doi: 10.1016/j.gloenvcha.2014.04.002

Dasgupta, P. (2021). The economics of biodiversity: the Dasgupta review: abridged version. 2nd Edn. HM Treasury: London.

De Wilde, P. (2011). No polity for old politics? A framework for analysing the politicization of European integration. J. Eur. Integr. 33, 559–575. doi: 10.1080/07036337.2010.546849

Dominati, E., Patterson, M., and Mackay, A. (2010). A framework for classifying and quantifying the natural capital and ecosystem services of soils. Ecol. Econ. 69, 1858–1868. doi: 10.1016/j.ecolecon.2010.05.002

Dudley, N., Hockings, M., and Stolton, S. U. (2004). Options for guaranteeing the effective Management of the World’s protected areas. J. Environ. Policy Plan. 6, 131–142. doi: 10.1080/1523908042000320713

Dusík, J., and Bond, A. (2022). Environmental assessments and sustainable finance frameworks: will the EU taxonomy change the mindset over the contribution of EIA to sustainable development? Impact Assess. Proj. Apprais. 40, 90–98. doi: 10.1080/14615517.2022.2027609

ECB (2022). Pressemitteilung: EZB setzt Fristen für Banken zum Umgang mit Klimarisiken. Available at: https://www.bundesbank.de/resource/blob/899924/e05406dca679701a9ca1a9088ccb8926/mL/2022-11-02-fristen-banken-klimarisiken-download.pdf (Accessed October 22, 2024).

Ecker-Ehrhardt, M., and Zürn, M. (2013). “Die Politisierung der Weltpolitik” in Die Politisierung der Weltpolitik- Umkämpfte Internationale Institutionen. eds. M. Zürn and M. Ecker-Ehrhardt (Berlin: Suhrkamp), 335–367.

Elgert, L. (2010). Politicizing sustainable development: the co-production of globalized evidence-based policy. Criti Policy Stud. 3, 375–390. doi: 10.1080/19460171003619782

Elliot, V., Jonäll, K., Paananen, M., Bebbington, J., and Michelon, G. (2024). Biodiversity reporting: standardization, materiality, and assurance. Curr. Opin. Environ. Sustain. 68:101435. doi: 10.1016/j.cosust.2024.101435

EPRS (2022). EU taxonomy: delegated acts on climate, and nuclear and gas. Available at: https://www.europarl.europa.eu/RegData/etudes/BRIE/2022/698935/EPRS_BRI(2022)698935_EN.pdf (Accessed October 22, 2024).

European Commission (2020a). Questions and answers: EU biodiversity strategy for 2030 – bringing nature back into our lives. Available at: https://ec.europa.eu/commission/presscorner/detail/en/qanda_20_886 (Accessed October 22, 2024).

European Commission (2020b). Technical expert group on sustainable finance (TEG). Available at: https://ec.europa.eu/info/publications/sustainable-finance-technical-expert-group_en (Accessed October 22, 2024).

European Commission (2021). Members of the commission technical expert group on sustainable finance. Available at: https://finance.ec.europa.eu/system/files/2021-05/sustainable-finance-teg-members_en.pdf (Accessed October 22, 2024).

European Commission (2023a). Annex 4: Annex to the commission delegated Regulation supplementing Regulation (EU) 2020/852. Available at: https://finance.ec.europa.eu/system/files/2023-06/taxonomy-regulation-delegated-act-2022-environmental-annex-4_en_0.pdf (Accessed October 22, 2024).

European Commission (2023b). COMMISSION DELEGATED REGULATION (EU) 2023/2772: supplementing Directive 2013/34/EU of the European Parliament and of the Council as regards sustainability reporting standard, Brussels. Available at: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=OJ:L_202302772 (Accessed October 22, 2024).

European Commission (2023c). EU taxonomy for sustainable activities: what the EU is doing to create an EU-wide classification system for sustainable activities. Available at: https://finance.ec.europa.eu/sustainable-finance/tools-and-standards/eu-taxonomy-sustainable-activities_en (Accessed October 22, 2024).

European Commission (2023d). Members and Observers of the Platform on Sustainable Finance: Overview of plenary and subgroups. Available at: https://finance.ec.europa.eu/system/files/2023-09/eu-platform-on-sustainable-finance-members_en.pdf (Accessed October 22, 2024).

European Commission (2023e). The commission adopts the european sustainability reporting standards. Available at: https://finance.ec.europa.eu/news/commission-adopts-european-sustainability-reporting-standards-2023-07-31_en (Accessed October 22, 2024).

European Commission (2024a). A European green deal: striving to be the first climate-neutral continent. Available at: https://commission.europa.eu/strategy-and-policy/priorities-2019-2024/european-green-deal_en (Accessed October 22, 2024).

European Commission (2024b). Corporate sustainability reporting. Available at: https://finance.ec.europa.eu/capital-markets-union-and-financial-markets/company-reporting-and-auditing/company-reporting/corporate-sustainability-reporting_en (Accessed October 22, 2024).

European Commission (2024c). Platform on sustainable Finance: the platform is an advisory body subject to the Commission’s horizontal rules for expert groups. Available at: https://finance.ec.europa.eu/sustainable-finance/overview-sustainable-finance/platform-sustainable-finance_en (Accessed October 22, 2024).

European Commission (2024d). The Habitats directive: EU measures to conserve Europe’s wild flora and fauna. Available at: https://environment.ec.europa.eu/topics/nature-and-biodiversity/habitats-directive_en (Accessed October 22, 2024).

European Parliament (2022). DIRECTIVE (EU) 2022/2464 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL: Amending Regulation (EU) No 537/2014, Directive 2004/109/EC, Directive 2006/43/EC and Directive 2013/34/EU, as regards corporate sustainability reporting, Brussels. Available at: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32022L2464 (Accessed October 22, 2024).

European Union (2006). Biodiversity action plan for the conservation of natural resources. Available at: https://eur-lex.europa.eu/EN/legal-content/summary/biodiversity-action-plan-for-the-conservation-of-natural-resources.html (Accessed October 22, 2024).

European Union (2015). Biodiversity strategy for 2020. Available at: https://eur-lex.europa.eu/EN/legal-content/summary/biodiversity-strategy-for-2020.html (Accessed October 22, 2024).

Fransen, A., and Bulkeley, H. (2024). Transnational governing at the climate–biodiversity frontier: employing a governmentality perspective. Glob. Environ. Polit. 24, 76–99. doi: 10.1162/glep_a_00726

Friske, W., Nikolov, A. N., and Morgan, T. (2024). Making the grade: an analysis of sustainability reporting standards and global reporting initiative adherence ratings. Corp. Soc. Responsib. Environ. Manag. 31, 2098–2108. doi: 10.1002/csr.2686

GRI (2024). Topic standard project for biodiversity. Available at: https://www.globalreporting.org/standards/standards-development/topic-standard-project-for-biodiversity/ (Accessed 22 October 2024).

Haber, W. (2008). Biological diversity – a concept going astray? GAIA Ecol. Perspect. Sci. Soc. 17, 91–96. doi: 10.14512/gaia.17.S1.4

Hassan, A., Roberts, L., and Rodger, K. (2022). Corporate accountability for biodiversity and species extinction: evidence from organisations reporting on their impacts on nature. Bus. Strateg. Environ. 31, 326–352. doi: 10.1002/bse.2890

Higgins, W., and Hallström, K. T. (2007). Standardization, globalization and rationalities of government. Organization 14, 685–704. doi: 10.1177/1350508407080309

Houdet, J., Ding, H., Quétier, F., Addison, P., and Deshmukh, P. (2020). Adapting double-entry bookkeeping to renewable natural capital: an application to corporate net biodiversity impact accounting and disclosure. Ecosyst. Serv. 45:101104. doi: 10.1016/j.ecoser.2020.101104

Huntley, B. J. (2014). Good news from the south: biodiversity mainstreaming – a paradigm shift in conservation? S. Afr. J. Sci. 110:4. doi: 10.1590/sajs.2014/a0080

Hutter, S., and Grande, E. (2014). Politicizing Europe in the National Electoral Arena: a comparative analysis of five west European countries, 1970–2010. J. Common Mark. Stud. 52, 1002–1018. doi: 10.1111/jcms.12133

IFRS (2023). Consultation now open: the ISSB seeks feedback on its priorities for the next two years. Available at: https://www.ifrs.org/news-and-events/news/2023/05/issb-seeks-feedback-on-its-priorities-for-the-next-two-years/ (Accessed October 22, 2024).

IFRS (2024). Biodiversity, ecosystems and ecosystem services. Available at: https://www.ifrs.org/projects/work-plan/biodiversity-ecosystems-and-ecosystem-services/ (Accessed October 22, 2024).

IPBES (2016). The assessment report of the intergovernmental science-policy platform on biodiversity and ecosystem services on pollinators, pollination and food production. IPBES Secretariat: Bonn.

IPBES (2019). Summary for policymakers of the global assessment report on biodiversity and ecosystem services of the Intergovernmental Science-Policy Platform on Biodiversity and ecosystem services. IPBES Secretariat: Bonn.

IPBES (2024). Glossary: biodiversity. Available at: https://www.ipbes.net/glossary/biodiversity (Accessed October 22, 2024).

ISBT (2024). ISBT: an international team of taxonomy experts. Available at: https://science-based-taxo.org/about-us/ (Accessed October 22, 2024).

ISO (2020). Biodiversity high on standards agenda: a new expert committee on biodiversity just formed. Available at: https://www.iso.org/news/ref2539.html (Accessed October 22, 2024).

ISO (2023). ISO/CD 17298: biodiversity — strategic and operational approach for organizations- requirements and guidelines. Available at: https://www.iso.org/standard/84899.html?browse=tc (Accessed October 22, 2024).

ISO (2024). About ISO. Available at: https://www.iso.org/about (Accessed October 22, 2024).

ISO/IEC (2004). Standardization and related activities—General vocabulary. ISO/IEC guide. 8th Edn. Geneva: ISO/IEC.

ISSB (2024). About the International Sustainability Standards Board. Available at: https://www.ifrs.org/groups/international-sustainability-standards-board/ (Accessed October 22, 2024).

Karlsson-Vinkhuyzen, S., Kok, M. T., Visseren-Hamakers, I. J., and Termeer, C. J. (2017). Mainstreaming biodiversity in economic sectors: an analytical framework. Biol. Conserv. 210, 145–156. doi: 10.1016/j.biocon.2017.03.029

Kedward, K., Ryan-Collins, J., and Chenet, H. (2021). Understanding the financial risks of nature loss: exploring policy options for financial authorities, Vienna, SUERF. Policy Brief 115, 1–8. doi: 10.13140/RG.2.2.16609.22884

Kedward, K., Ryan-Collins, J., and Chenet, H. (2023). Biodiversity loss and climate change interactions: financial stability implications for central banks and financial supervisors. Clim. Pol. 23, 763–781. doi: 10.1080/14693062.2022.2107475

Kopnina, H., Zhang, S. R., Anthony, S., Hassan, A., and Maroun, W. (2024). The inclusion of biodiversity into environmental, social, and governance (ESG) framework: a strategic integration of ecocentric extinction accounting. J. Environ. Manag. 351:119808. doi: 10.1016/j.jenvman.2023.119808

Krewer, D. (2005). Rules that many use: standards and global regulation. Governance 18, 611–632. doi: 10.1111/j.1468-0491.2005.00294.x

Larner, W., and Le Heron, R. (2004). “Global benchmarking participating ‘at a distance’ in the globalizing economy” in Global governmentality: Governing international spaces. ed. W. Larner (London: Routledge), 212–232.

Maroun, W., and Atkins, J. (2018). The emancipatory potential of extinction accounting: exploring current practice in integrated reports. Account. Forum 42, 102–118. doi: 10.1016/j.accfor.2017.12.001

Marx, A., Depoorter, C., Fernandez de Cordoba, S., Verma, R., Araoz, M., Auld, G., et al. (2024). Global governance through voluntary sustainability standards: developments, trends and challenges. Global Pol. 15, 708–728. doi: 10.1111/1758-5899.13401

McKinsey (2022). Where the world’s largest companies stand on nature. Available at: https://www.mckinsey.com/capabilities/sustainability/our-insights/where-the-worlds-largest-companies-stand-on-naturelargest-companies-stand-on-nature (Accessed October 22, 2024).

Millennium Ecosystem Assessment Board (2005). Ecosystems and human well-being: synthesis. Washington, DC: Island Press.

Milne, M. J., Tregidga, H., and Walton, S. (2009). Words not actions! The ideological role of sustainable development reporting. Acc. Auditing Acc. J. 22, 1211–1257. doi: 10.1108/09513570910999292

Nedopil, C. (2023). Integrating biodiversity into financial decision-making: challenges and four principles. Bus. Strateg. Environ. 32, 1619–1633. doi: 10.1002/bse.3208

OECD (2023). Assessing biodiversity-related financial risks: navigating the landscape of existing approaches. Paris: OECD.

Persson, Å., and Runhaar, H. (2018). Conclusion: drawing lessons for environmental policy integration and prospects for future research. Environ Sci Policy 85, 141–145. doi: 10.1016/j.envsci.2018.04.008

Pörtner, H.-O., Scholes, R.J., Agard, J., Archer, E., Arneth, A., Bai, X., et al. (2021). Scientific outcome of the IPBES-IPCC co-sponsored workshop on biodiversity and climate change. ES-IPCC co-sponsored workshop on.

Pröbstl, F., Paulsch, A., Zedda, L., Nöske, N., Cardona Santos, E. M., and Zinngrebe, Y. (2023). Biodiversity policy integration in five policy sectors in Germany: how can we transform governance to make implementation work? Earth Syst. Governance 16:100175. doi: 10.1016/j.esg.2023.100175

PwC and WWF (2022). Biodiversität bislang kaum auf der Agenda des deutschen Finanzsektors. Available at: https://www.pwc.de/de/pressemitteilungen/2022/biodiversitaet-rueckt-auf-die-agenda-des-finanzsektors.html (Accessed October 22, 2024).

Roland, A., and Römgens, I. (2022). Policy change in times of politicization: the case of corporate taxation in the European Union*. J. Common Mark. Stud. 60, 355–373. doi: 10.1111/jcms.13229

Runhaar, H., Pröbstl, F., Heim, F., Cardona Santos, E., Claudet, J., Dik, L., et al. (2024). Mainstreaming biodiversity targets into sectoral policies and plans: a review from a biodiversity policy integration perspective. Earth Syst. Governance 20:100209. doi: 10.1016/j.esg.2024.100209

Runhaar, H., Wilk, B., Driessen, P., Dunphy, N., Persson, Å., Meadowcroft, J., et al. (2020). “Policy integration” in Architectures of earth system governance. eds. F. Biermann and R. E. Kim (Cambridge: Cambridge University Press), 183–206.

Sánchez-Bayo, F., and Wyckhuys, K. A. (2019). Worldwide decline of the entomofauna: a review of its drivers. Biol. Conserv. 232, 8–27. doi: 10.1016/j.biocon.2019.01.020

Schmidt, V. A. (2019). Politicization in the EU: between national politics and EU political dynamics. J. Eur. Publ. Policy 26, 1018–1036. doi: 10.1080/13501763.2019.1619189

Smith, T., Beagley, L., Bull, J., Milner-Gulland, E. J., Smith, M., Vorhies, F., et al. (2020). Biodiversity means business: reframing global biodiversity goals for the private sector. Conserv. Lett. 13:e12690. doi: 10.1111/conl.12690

Smith, M. R., Mueller, N. D., Springmann, M., Sulser, T. B., Garibaldi, L. A., Gerber, J., et al. (2022). Pollinator deficits, food consumption, and consequences for human health: a modelling study. Environ. Health Perspect. 130:127003. doi: 10.1289/EHP10947

Smith, T., Paavola, J., and Holmes, G. (2019). Corporate reporting and conservation realities: understanding differences in what businesses say and do regarding biodiversity. Environ. Policy Gov. 29, 3–13. doi: 10.1002/eet.1839

Stavins, R. N. (2003). “Experience with market-based environmental policy instruments” in Handbook of environmental economics. eds. K.-G. Mäler and J. Vincent (Amsterdam, Netherlands: Elsevier Science), 355–435.

Steffek, J., and Wegmann, P. (2021). The standardization of ‘Good Governance’ in the age of reflexive modernity. Glob. Ecol. Biogeogr. 1, 1–10. doi: 10.1093/isagsq/ksab029

Stevenson, H., Auld, G., Allan, J. I., Elliott, L., and Meadowcroft, J. (2021). The practical fit of concepts: ecosystem services and the value of nature. Global Environ. Polit. 21, 3–22. doi: 10.1162/glep_a_00587

Sullivan, S. (2018). Making nature investable. Sci. Technol. Stud. 31, 47–76. doi: 10.23987/sts.58040

Technical Expert Group on Sustainable Finance (Ed.). (2020). Taxonomy Report: Technical Annex. Available at: https://finance.ec.europa.eu/system/files/2020-03/200309-sustainable-finance-teg-final-report-taxonomy-annexes_en.pdf (Accessed October 22, 2024).

Timmermans, S., and Epstein, S. (2010). A world of standards but not a standard world: toward a sociology of standards and standardization. Annu. Rev. Sociol. 36, 69–89. doi: 10.1146/annurev.soc.012809.102629

Tin, Y.K.F., Butt, H., and Calhoun, E. (2024). Accountability for Nature: Comparison of Nature-Related Assessment and Disclosure Frameworks and standards. UNEP Finance Initiative: Geneva.

Toepfer, G. (Ed.) (2011). “Historisches Wörterbuch der Biologie: Geschichte und Theorie der biologischen Grundbegriffe” in. ed. J. B. Metzler. 308th ed (Stuttgart, Weimar).

Visseren-Hamakers, I. J., Arts, B., and Glasbergen, P. (2011). Interaction management by partnerships: the case of biodiversity and climate change. Glob. Environ. Polit. 11, 89–107. doi: 10.1162/GLEP_a_00085

Visseren-Hamakers, I. J., and Kok, M. T. J. (2022). Transforming biodiversity governance. Cambridge: Cambridge University Press.

Whitehorn, P. R., Navarro, L. M., Schröter, M., Fernandez, M., Rotllan-Puig, X., and Marques, A. (2019). Mainstreaming biodiversity: a review of national strategies. Biol. Conserv. 235, 157–163. doi: 10.1016/j.biocon.2019.04.016

World Economic Forum (2020). Nature risk rising: why the crisis engulfing nature matters for business and the economy. Available at: https://www3.weforum.org/docs/WEF_New_Nature_Economy_Report_2020.pdf (Accessed October 22, 2024).

World Forum on Natural Capital (2024). What is natural capital? Available at: https://naturalcapitalforum.com/about/ (Accessed October 22, 2024).

WWF (2022). NGOs walk out of expert Taxonomy group over lack of independence. Available at: https://www.wwf.eu/?7544416/NGOs-walk-out-of-expert-Taxonomy-group-over-lack-of-independence (Accessed October 22, 2024).

WWF (2023). Joint letter: setting next steps to develop the EU taxonomy. Available at: https://www.wwf.eu/?12636891/Joint-letter-Setting-next-steps-to-develop-the-EU-taxonomy (Accessed October 22, 2024).

WWF (2024). Independent science based taxonomy: a new tool for sustainable finance. Available at: https://www.wwf.eu/?14317916/Independent-Science-Based-Taxonomy-A-New-Tool-for-Sustainable-Finance (Accessed October 22, 2024).

Keywords: biodiversity, standardization, politicization, biodiversity policy, European Green Deal, corporate reporting

Citation: Zenglein F (2025) The standardization of biodiversity: how politicization changes standardization for corporate sustainability reporting. Front. Sustain. 5:1433799. doi: 10.3389/frsus.2024.1433799

Edited by:

Omaima Hassan, Robert Gordon University, United KingdomReviewed by:

Jan-Alexander Posth, Zurich University of Applied Sciences, SwitzerlandEve Bohnett, University of Florida, United States

Copyright © 2025 Zenglein. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Florian Zenglein, emVuZ2xlaW5AcGcudHUtZGFybXN0YWR0LmRl