95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Sustain. , 08 May 2020

Sec. Sustainable Organizations

Volume 1 - 2020 | https://doi.org/10.3389/frsus.2020.00001

Rodrigo Lozano1*

Rodrigo Lozano1* Iciar Garcia2

Iciar Garcia2Organizations (i.e., civil society, corporations, and public sector organizations) have been instrumental in driving sustainability. In the last decade, there has been an increasing interest in organizational sustainability, and an increase of organizational change management for sustainability. Although, there have been many efforts aimed at incorporating sustainability in organizations, incorporating, integrating, and institutionalizing sustainability in organizations is still under-researched. A survey was developed for investigating the importance of how sustainability has been embedded in organizations' system elements. The survey was sent to a database of 5,299 contacts from different organizations worldwide. From the total, 281 useable responses (6.78%) for the organizational change part were obtained. The variables analyzed were mainly ordinal scales, therefore, non-parametric methods were used for the analyses, including descriptive, Friedman test for ranking, and Kruskal Wallis and Wilcoxon tests for comparisons. More than 90% of the responding organizations have been working with sustainability for more than 5 years. The main driving forces for sustainability have been motivated equally by external stimuli and internal factors. The focus on sustainability and recognition of the impacts that the organization has are fairly aligned. The findings show that the main areas, from the start and during the changes, have been on governance, management and strategy, and operations and production. The majority of the changes were effected between six and seven systems elements, which indicates a large degree of institutionalization. The comparison tests show that the nature of the organization plays a key role for where the sustainability changes start, and how the changes affect system elements. The research highlights that it inconsequential where sustainability changes start, as long as sustainability is adopted throughout all the system elements, including internal and external stakeholders. Planning sustainability changes must address its four dimensions holistically, as well as technical, managerial, and organizational issues, and the organization's stakeholders.

Organizations [i.e., civil society, corporations, and public sector organizations (PSOs)] have been instrumental in driving sustainability (Jennings and Zandbergen, 1995; Danter et al., 2000; Holliday et al., 2002; Jennings, 2002). In the last decade, there has been an increasing interest in organizational sustainability (Pfeffer, 2010; Lozano, 2018), where the importance of sustainability's dimensions depends on an organization's nature and purpose (Soyka, 2012).

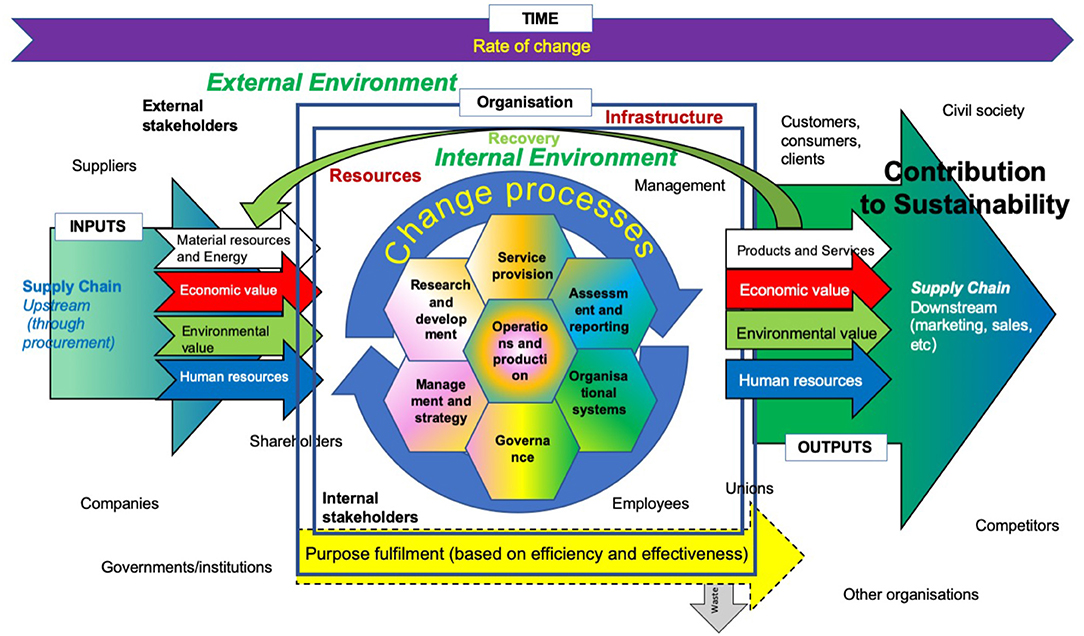

A number of definitions of organizational sustainability have appeared. Leon (2013) proposed a sustainable organization to be an economic entity that develops its plans and structures to achieve economic, environmental, social objectives and ensure its growth by allocating its resources rationally. For Rodríguez-Olalla and Avilés-Palacios (2017), organizational sustainability is a multidimensional process based on efficiency and effectiveness that focusses on results, knowledge, capacity building, networks of partners, and products and services. Although the definitions provide a base for organizational sustainability, they are limited in explaining its principles, elements, relations to stakeholders, and commonalities and specificities in the different organizations when addressing and contributing to sustainability, while Lozano (2018) proposed organizational sustainability as (see Figure 1): “The contributions of the organization to sustainability equilibria, including the economic, environmental, and social dimensions of today, as well as their inter-relations within and throughout the time dimension (i.e., the short-, long-, and longer-term). This entails the continuous incorporation and integration of sustainability issues in the organization's system elements (operations and production, strategy and management, governance, organizational systems, service provision, and assessment and reporting), as well as change processes and their rate of change. The system elements and change processes transform the inputs (in regard to material and resources that have economic, environmental, and social value) into outputs (products, services, and waste, with their economic, environmental, and social value). These fulfill the organization's goal or objective, based on resource efficiency and effectiveness. The organization is affected by the organization's non-human and human resources (i.e., individuals, groups, culture, values, attitudes, and norms), its infrastructure, its supply chain (upstream and downstream), and the interactions with its stakeholders (internal, inter-connecting, and external).” This paper is based on the last definition, since it provides a more holistic perspective.

Figure 1. Organizational sustainability framework (Lozano, 2018).

During the two last decades, there has been an increase on research of organizational change management for sustainability. Long-lasting change toward sustainability requires changes in management (Doppelt, 2003), as well as in mental models, incremental changes in the organizational structure and its operations (Diesendorf, 2000). Although, there have been many efforts aimed at incorporating sustainability in organizations, yet, incorporating, integrating, and institutionalizing sustainability in organizations is still under-researched. This paper is aimed at scrutinizing these latter aspects.

This paper is structured in the following way: section 2 reviews organizational change management for sustainability; section 3 presents the methods; section 4 provides the results; section 5 discusses the results; and section 6 provides the conclusions.

A limited number of organizations have successfully incorporated sustainability into their systems and culture (Hussey et al., 2001; Siebenhüner and Arnold, 2007; Linnenluecke and Griffiths, 2010). Many sustainability approaches have been based on techno-centric solutions and managerial ploys, which neglect culture, the supply chain, and the interactions between the system elements and the four dimensions of sustainability (Lozano, 2012b, 2015).

Organizational change management for sustainability has focussed on “soft issues” (values, visions, philosophies, policies, and employee empowerment), i.e., change management practices (Doppelt, 2003; Dunphy et al., 2003), organizational and behavioral change management practices (Lozano, 2012a); drivers for sustainability (Sayce et al., 2007; Lozano, 2015; Lozano and von Haartman, 2018); barriers to change (Lozano, 2013; Blanco-Portela et al., 2017); and the link between organizational change management and assessment and reporting, with in many cases reinforcing effects (Ceulemans et al., 2015; Lozano et al., 2016; Domingues et al., 2017). Sustainability assessment and reporting has been considered to be an important catalyst for change toward sustainability and one of its main drivers (Doppelt, 2003; Adams and McNicholas, 2007; Lozano, 2015; Lozano et al., 2016).

Organizational change management provides a dynamic perspective through addressing the time dimension of sustainability (O'Connor, 1991; Lozano, 2009). It aims to move from the current state to one that is more desirable (Ragsdell, 2000), ranging from minor to radical changes (Rogers, 1962; Dawson, 1994, 2001). Organizational changes are complex (Dawson, 1994), systemic (Ben-Eli, 2018), continuous, iterative and uncertain (Pettigrew and Whipp, 1991).

When addressing sustainability change, organizations are influenced by internal and external stakeholders (Freeman, 1984). In general, organizations have more control over internal changes than external ones (Freeman, 1984; DeSimone and Popoff, 2000). The former tends to be proactive, whilst the latter reactive (Lozano, 2012a). Internally, changes can be done through managerial measurement and control (Henriques and Richardson, 2005), or focusing on internal change and innovation (Doppelt, 2003; Henriques and Richardson, 2005). The former rely on strategic top-down changes, whilst the latter are on participative collaborative changes (Lozano, 2013). Long-lasting sustainability change requires a holistic perspective (Hjorth and Bagheri, 2006; Linnenluecke et al., 2009; Lozano and Huisingh, 2011). The organizations that have engaged in sustainability have done it mainly through upper management level initiatives (Siebenhüner and Arnold, 2007).

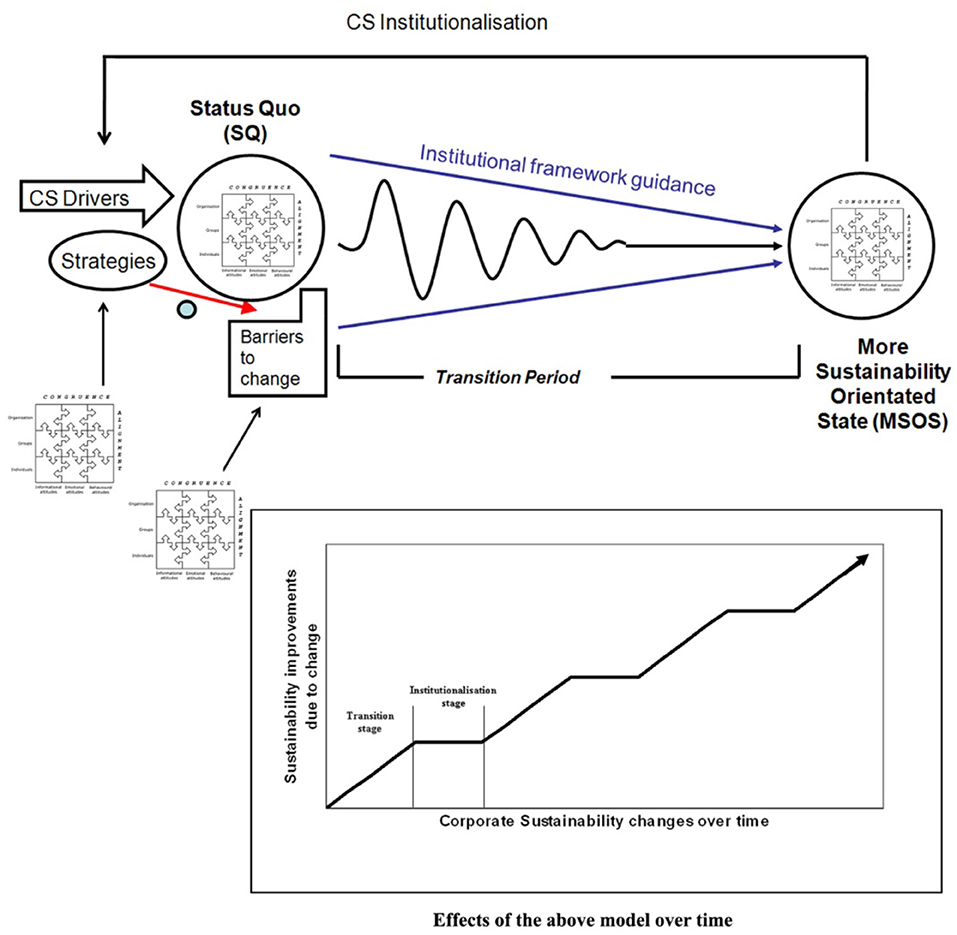

Lozano (2012a, 2013, 2015), based on the works of Lewin (1947a,b); Bennis et al. (1969); Anderson and Ackerman Anderson (2001) and Luthans (2002), proposed an “Orchestrating Change for Corporate Sustainability” model (see Figure 2) to help explain the process of organizational changes for corporate sustainability. The framework posits that “Orchestrated planned change can disrupt the status quo (SQ) and help move toward a more sustainability-orientated state (MSOS), in a continuously iterative process. The entire system and its elements, as well as their respective attitudes, need to be addressed. In this process, it is important to foster the drivers to change, and apply the appropriate strategies to overcome the barriers to change. The institutional framework can help to maintain stability during the changes, and thus facilitate sustainability institutionalization. During these changes, the system would pass through a transitional period, where the different balance of forces adjusts to each other, to reach the MSOS. Once all the forces are rebalanced, and the new structure and goals are set, the MSOS starts becoming the status quo novo (SQN). Because of the dynamism of sustainability, the process has to start again after stabilization. Planning organizational changes, whilst engaging with the different organizational levels and their attitudes, could help companies to better overcome resistance to change and integrate their efforts for sustainability more holistically, including technological and human changes, i.e., taking a more holistic perspective to contribute to sustainability.”

Figure 2. Framework for explaining the dynamics of Orchestrating Change for Corporate Sustainability. Source: Lozano (2013).

Lozano (2018) analyzed sustainability change efforts in organizations. The results highlighted that organizations agree (53% of all, 62% of civil society, 52% of companies, and 31% of PSOs) or strongly agree (34% of all, 26% of civil society, 35% of companies, and 54% of PSOs) that they are proactively engaging with sustainability. The impacts of organizations are highest on the social dimension (67%), followed by the economic one (61%), and then the environmental one (55%). Sustainability has been, in general, equally driven by external stimuli and internal factors (47% of all, 38% of civil society, 54% of companies, and 38% of PSOs), followed mainly by internal factors, but with some external stimuli (32% of all, 38% of civil society, 28% of companies, and 31% of PSOs).

There have been many efforts aimed at incorporating sustainability in organizations (e.g., Lozano, 2006; Adams and McNicholas, 2007; Verhulst and Lambrechts, 2015); however, there have been few studies (Lozano, 2006; Saviano et al., 2018) on organizational change management for sustainability particularly focussing where the change has started in the organizational system and how it has permeated throughout the organization's system elements, i.e., its institutionalization.

A survey was developed for investigating how sustainability has been incorporated and insitutionalised in organizations. The survey was carried out using the online survey tool (Qualtrics, 2018)1. The data collection took place over the period May to November 2018. The survey consisted of five sections:

1. Organization characteristics, including country of origin, size and product-service-focus.

2. Role of sustainability for the organization and role of the respondent in the company.

3. Sustainability questions, such as importance of environmental, economic, and social issues.

4. Organizational change toward sustainability, and incorporation of sustainability.

5. Stakeholders role in the organization's sustainability engagement.

6. Role of the supply chain.

The survey was sent to a database of 5,299 contacts from different organizations worldwide obtained from the Global Reporting Initiative (GRI) list, and personal contacts. In addition, 107 anonymous links were sent out. Three reminders were sent out, one in July 2018, one in September 2018 and one in October 2018. From the total list of emails, 616 emails bounced back. From the total, 325 full responses were obtained, with a response rate (after removing the ones that bounced back), but only 281 useable responses (6.78%) for the organizational change part were obtained.

The variables for section 42 (Organizational change toward sustainability, and incorporation of sustainability) were non-parametric with the following options: 5-point Likert scale for the role of sustainability (Strongly disagree, Somewhat disagree, Neither agree nor disagree, Somewhat agree, and Strongly agree); 3-point (not actively, to some extent, and to a large scale) for sustainability engagement; 5-point for the focus and impact variables (not important, slightly important, moderately important, very important, and extremely important); 6-point scale for the time working with sustainability (<1 year, between 1 and 3 years, between 3 and 5 years, between 5 and 10 years, between 10 and 15 years, and more than 15 years); 5-point for the sustainability driving forces; nine options for the start of sustainability (from the system elements); and ranking of the nine system elements in four change groups (mostly, somewhat, least, and no change).

The overall change in each system element was calculated from the ranking of the system elements in four change groups: mostly; somewhat; least; and no change. In each of these groups the respondents indicated the elements that had been affected. From the nine elements, a maximum of seven were mentioned in each of the groups. Thus, the element that was ranked first was given a seven, and the one ranked last a one, when seven were mentioned. In case three were mentioned, the first was ranked with a seven and the last one with a five. To provide a weight between the groups' importance, the ranking in the mostly group was multiplied by three, the somewhat ranking by two, and the least by one. The no change ranking was disregarded for the calculation of the institutionalization variable.

The variables analyzed were mainly to ordinal scales, therefore, non-parametric methods were used for the analyses, including descriptive, Friedman test for ranking, and Kruskal Wallis and Wilcoxon test for comparisons. These were done using SPSS Statistics 22 for Windows software (IBM, 2016).

The internal validity of this research might have been limited by the survey, which may not have offered a complete picture of sustainability changes in organizations. The number of respondents (281) may not allow a complete generalization to all types of organizations. The generalisability of results to all organizations may be limited to the application of a non-random sampling procedure and the focus on companies listed in the GRI Disclosure Database with additional input from personal contacts and “snowballing” methods. A non-response bias may be caused by companies from sectors which were contacted but refused to complete the survey. Generalisability could be improved by a study based on a randomly selected sample drawn from the total number of organizations active in sustainability. The respondents might have come from top-levels of the organizations, which may result in bias toward answers on the governance and management elements of the system.

From the respondents, 195 were from corporations (69.40%), 44 from PSOs (15.66%), and 42 from civil society (14.95%). Most of the respondents were from European countries (88.25%), with answers from Germany (12.81%), Sweden (12.81%), Spain (11.39%), Netherlands (8.19%), Belgium (4.98%), United Kingdom (4.98%), Finland (4.27%), Austria (3.91%), Italy (3.91%), and Switzerland (3.20%) covering 70% of the answers.

There were 51 respondents from organizations with 1–49 employees, 28 respondents with 50–249, 19 respondents with 250–499, 12 respondents with 500–999, 78 respondents with 1,000 to 4,999, and 93 with more than 5,000 employees.

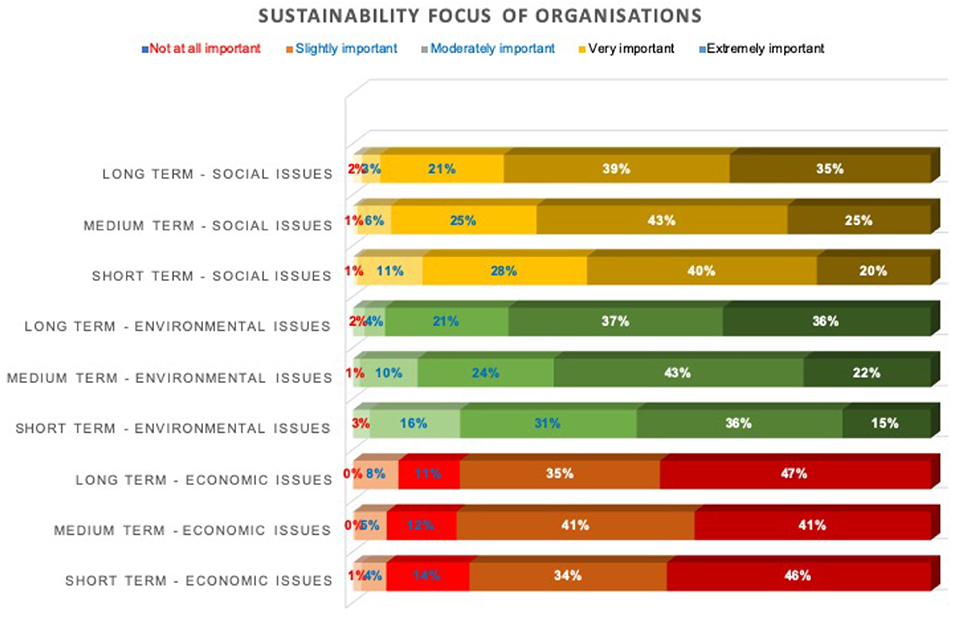

Figure 3 shows the sustainability focus of the responding organizations. As it can be seen, the economic dimension is predominant almost equally in the short-, medium-, and long-terms (80% very and extremely important in average). The focus on the environmental and social dimensions tend to be more important in the future, i.e., the long-term (circa 73%) is more important than the medium-term (around 66%), and this in turn than the short-term (51% for the environmental dimension and 59% for the social one).

Figure 3. Sustainability focus of the organizations according to the respondents.

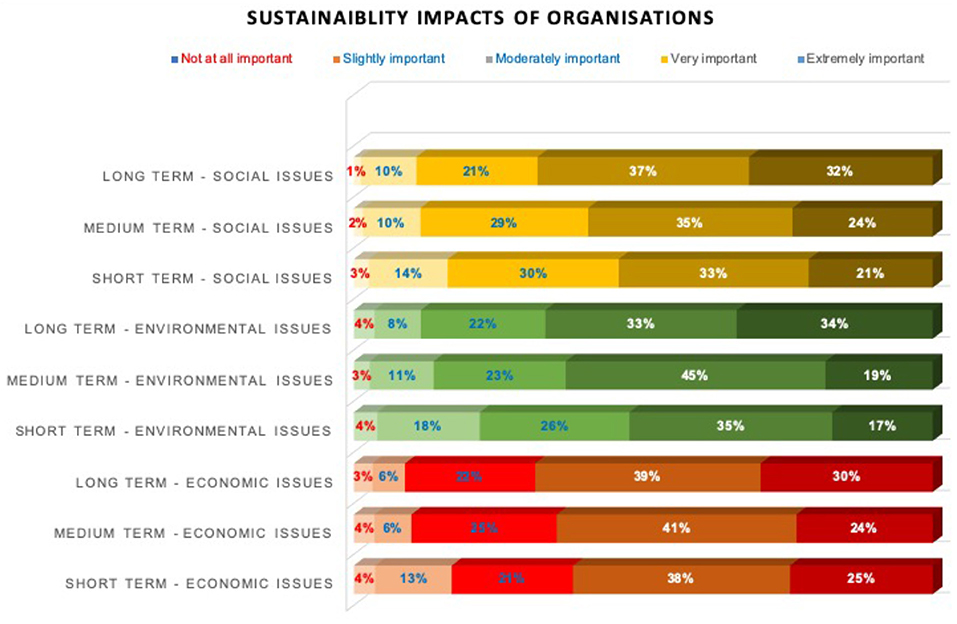

Figure 4 shows the sustainability impacts of the responding organizations. As it can be seen, the economic dimension is either very or extremely important almost equally in the medium-, and long-terms, with the short-term having slightly less importance (between 62 and 69%). The environmental and social dimensions tend to be more important in the future, i.e., the long-term (almost 70%) is more important than the medium-term (around 60%), and this in turn than the short-term (around 50%), with very similar responses for both dimensions. These responses are similar to the focus ones (see Figure 3), but the importance of impacts tends to be slightly less in the environmental and social dimensions (from 1 to 9%), whereas for the economic dimension the importance decreases more in the short- and medium-term (around 18%), than in the long-term (13%). This indicates that the focus on sustainability and recognition of the impacts are fairly aligned.

Figure 4. Sustainability impacts of the organizations according to the respondents.

Over 90% of the respondent indicated that sustainability plays an important role in their organizational activities (61.65% strongly agreed and 28.67% somewhat agreed), 5.38% neither agreed nor disagreed, 2.87% somewhat disagreed, and 1.43% strongly disagreed.

The respondents indicated that they have been proactively engaging with sustainability (52.33% to a large extent, and 46.24% to some extent). Only four organizations indicated that they have not been engaging proactively with sustainability. This coincides with previous findings (see Lozano, 2018).

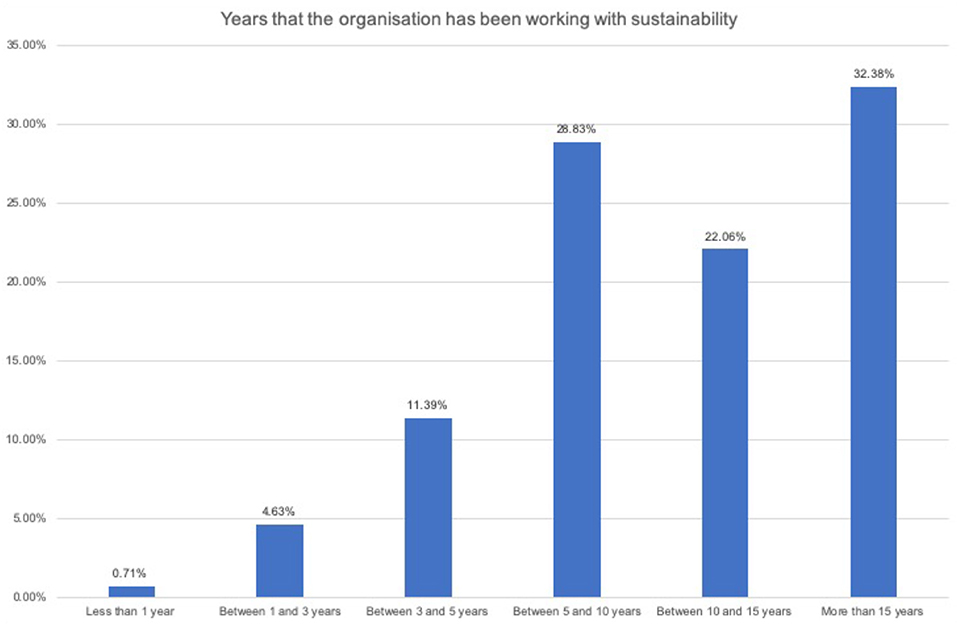

As it can be seen from Figure 5, more than 90% of the 281 responding organizations have been working with sustainability for more than 5 years (32.38% more than 15 years, 22.06% between 10 and 15 years, 28.83% between 5 and 10 years, and 11.39% between 3 and 5 years). Thirteen organizations (4.63%) have been working with sustainability between 1 and 3 years, and 2 (0.71%) less than a year. These shows that the majority of the respondents' organizations have been working with sustainability long enough to facilitate its institutionalization.

Figure 5. Years that the responding organizations have been working with sustainability.

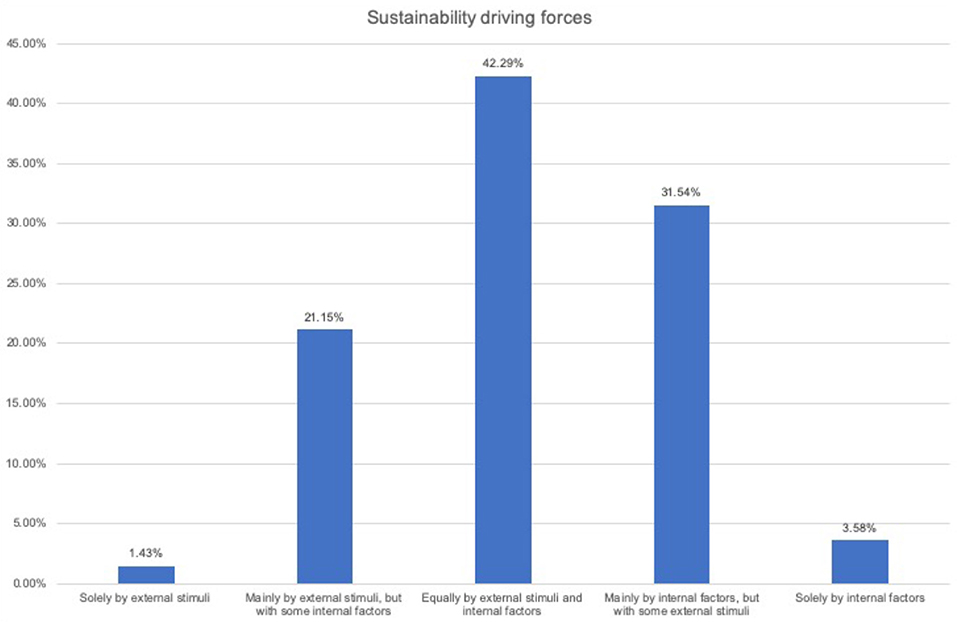

The main driving forces for sustainability have been (see Figure 6) equally due to external stimuli and internal factors (42.29%), followed by mainly by internal factors, but with some external stimuli (31.54%), mainly by external stimuli, but with some internal factors (21.15%). The extremes were low, i.e., solely by internal factor (3.58%) and solely by external stimuli (1.43%). This reaffirms the findings of Lozano (2018).

Figure 6. Sustainability driving forces.

The respondents indicated that sustainability changes have started (see Figure 7) mainly in management and strategy (26.71%) and governance (25.99%), followed by operations and production (13.00%), assessment and reporting (11.55%), organizational systems (9.03%), research and development (6.14%), service provision (4.33%), supply chains (3.25%), and collaboration with other organizations (1.08%). This indicates that organizational changes for sustainability are more prone to be top-down following managerial measures and control (concurring with Henriques and Richardson, 2005), rather than first emphasizing the importance of internal change and innovation (as proposed by Doppelt, 2003; Henriques and Richardson, 2005; Lozano, 2013). These findings disagree with the literature which indicates that sustainability assessment and reporting has been considered to be an important catalyst for change, and one of its main drivers (Doppelt, 2003; Adams and McNicholas, 2007; Lozano, 2015; Lozano et al., 2016).

Figure 7. Start of sustainability changes in the system elements.

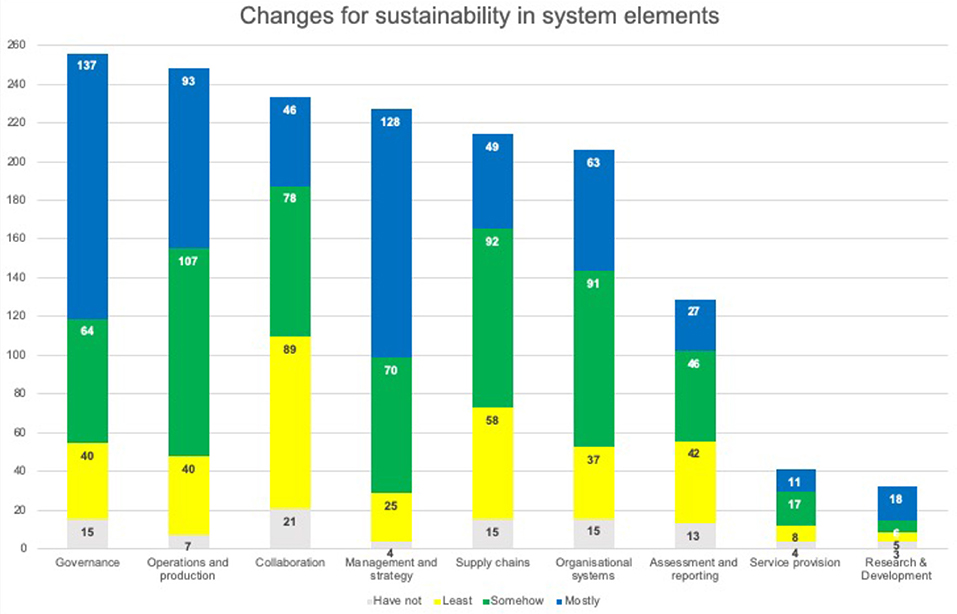

Figure 8 shows the responses on changes for sustainability in the system elements. As it can be seen the highest changes have been (total responses of each system element in brackets) on governance (256), operations and production (248), collaboration (233), management and strategy (227), supply chains (214), organizations systems (206), assessment and reporting (129), service provision (41), and research and development (32). It should be noted that collaboration is number four, but this is due to a large number of responses on “least” changes. Governance and management and strategy had the highest number of responses on “mostly,” followed by operations and production. The two system elements with the lowest responses were research and development and service provision, which may be due to such elements not being widely present in many of the respondents' organizations. When “mostly” and “somewhat” changes are considered the three highest ones were governance (201), operations and production (200), and management and strategy (198). Organizational systems (153) were higher than supply chains (141), and collaboration (124). These findings highlight that sustainability changes have taken place mainly on system elements that are internally focussed (governance, management and strategy, and operations and production), as opposed to those externally oriented (such as supply chains and collaboration), thus concurring with the view that organizations have more influence over internal changes (see Freeman, 1984; DeSimone and Popoff, 2000; Lozano, 2012a).

Figure 8. Sustainability changes affecting the system elements.

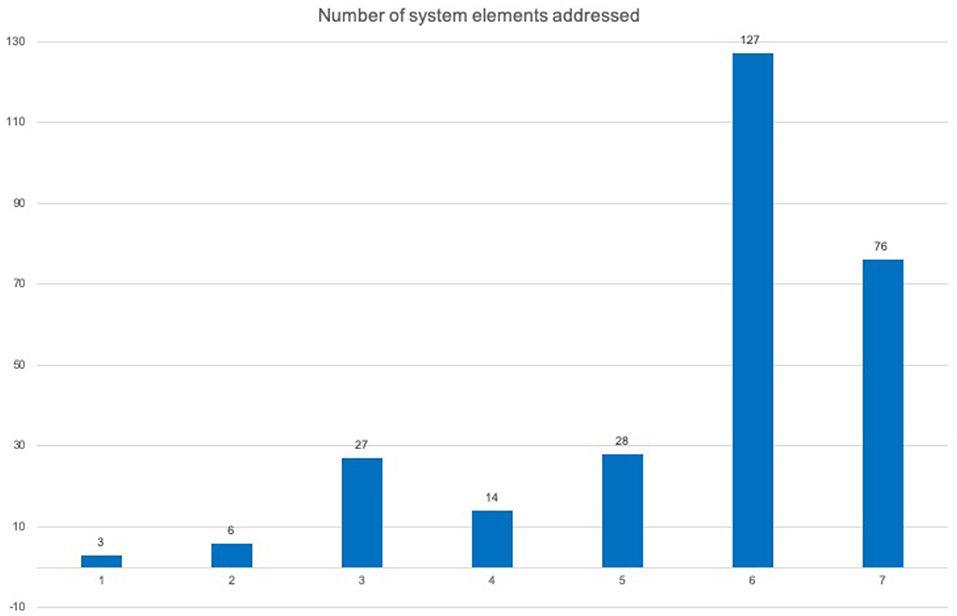

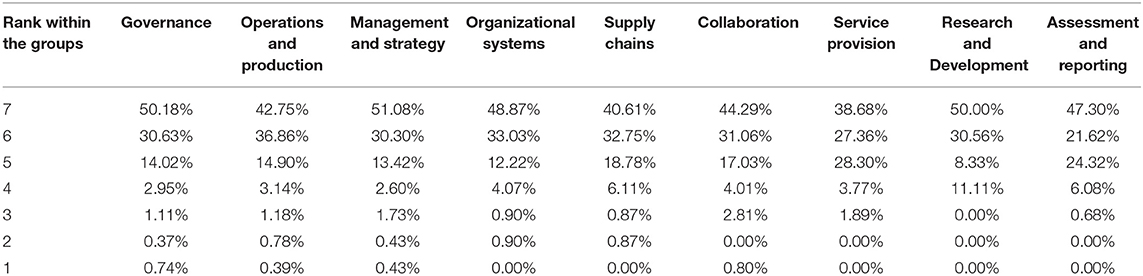

The respondents mentioned changes between one and seven system elements (see Figure 9), where the majority of the changes were in six systems elements, followed by seven, five, three, four, two, and one system elements. Table 1 shows the distribution of the ranking within the three change groups (mostly, somewhat, and least), where it can be seen that, in general, the changes took place between five and seven system elements, covering more than 90% of the distribution, with the exception of research and development, where it was close to 89%. In the case of the latter, there were the rankings were from four to seven system elements that changed. This denotes a high degree of institutionalization, where most of the system elements have been affected by sustainability changes. It should be noted that there were few responses for service provision and research and development, therefore, it could be posited that full institutionalization takes place when seven system elements are affected by the changes.

Figure 9. Number of elements that had sustainability changes.

Table 1. Ranking of the system elements according to their changes.

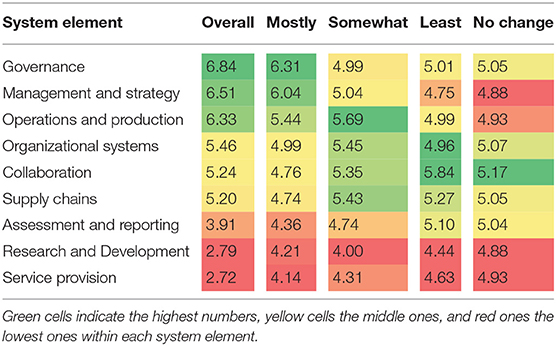

Friedman tests were carried out for the mostly, somewhat, least, no change, and overall changes (calculated as indicated in the methods section). The results are presented in Table 2, where it can be seen that: governance (1st rank), management and strategy (2nd), and operations and production (3rd) have the highest ranks in the overall and mostly changes; operations and production (1st), organizational system (2nd), supply chains (3rd), collaboration (4th) have the highest ranks in the somewhat group; collaboration (1st), supply chains (2nd) and assessment and reporting (3rd) on the least groups; and collaboration, organizational systems, supply chains, governance, and assessment and reporting in the no change group. The system elements that were consistently ranked the lowest in all groups were research and development, and service provision. It should be noted that the difference between average ranks is highest in the overall group (with a difference of 4.12 points, followed by mostly with 2.17, somewhat with 1.69, least with 1.4, and no change with 0.29. This highlights that the biggest changes were for internal system elements (governance, management and strategy, and operations and production), the middle changes were for a combination of technical (operations and production), internal change and innovation (organizational systems), and connection to external stakeholders (collaboration and supply chains). The lowest changes occurred on those connecting to external stakeholders, and the element with no change was collaboration. This reinforces the view that major changes are mainly internally focussed (see Freeman, 1984; DeSimone and Popoff, 2000; Lozano, 2012a) and top-down (concurring with Henriques and Richardson, 2005); however, there have been some changes with an external perspective and addressing internal change and innovation.

Table 2. Friedman test rank of the system elements within the overall, mostly, somewhat, least, and no change groups.

As it can be from Table 3, sustainability changes started on management and strategy, governance, and operations, which were the ones with the highest overall changes. The major changes in ranks were for collaboration (with an increase of four ranks), assessment and reporting (with a drop of three), supply chains (an increase of two), research and development and service provision (with a drop of two), and governance and organizational system (with an increase of one) and management and strategy (with a drop of one). Operations and production did not suffer any change in rank. These findings show that the key focus, in the start and during the changes, has been on governance, management and strategy, and operations and production. They also indicate that perhaps the importance of assessment and reporting may be overestimated (as proposed by Doppelt, 2003; Adams and McNicholas, 2007; Lozano, 2015; Lozano et al., 2016), whereas that of collaboration with other organizations has been undervalued.

Table 3. Rank change between where the organizational changes started and the system elements affected.

A Wilcoxon test was carried out for proactive engagement with sustainability. Kruskal Wallis tests were carried out to test for the start of changes, and changes in the system elements for the following variables; years working with sustainability; sector type; and organization size. The comparison tests were done at p < 0.05. The only variables for which there were no statistical differences were for the years working with sustainability and the start of the changes, and the years working with sustainability and changes in the system elements.

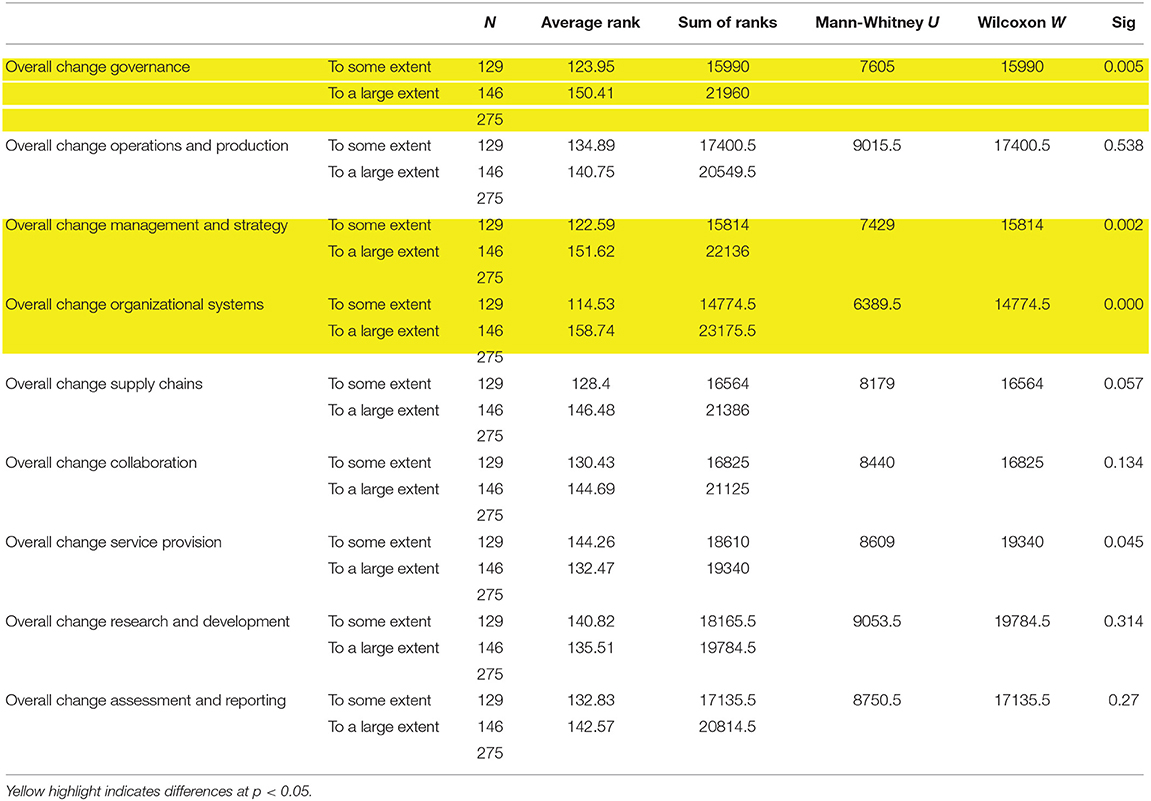

A Wilcoxon test was done to test the differences between changes “to some extent” and “to a large” extent, see Table 4. The results show that “to some extent” had a lower mean on governance, management and strategy, and organizational systems. This means that for these three element systems the proactive engagement with sustainability is quite high, whereas for the other system elements it is similar in the “to some extent” and “to a large extent.”

Table 4. Wilcoxon test to compare the “to some extent” and “to a large extent” changes of the system elements.

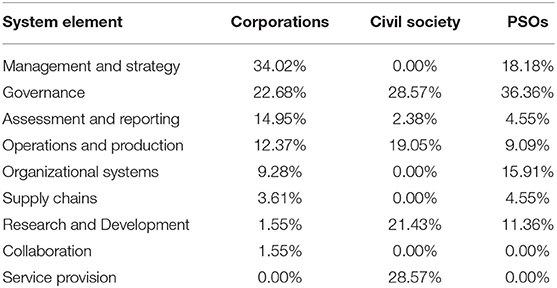

The Kruskal Wallis tests showed differences with respect to sector type for the start of sustainability changes and for organization size. Table 5 shows the start for the organization types, where it can be seen that: for corporations, it was mainly at management and strategy, governance, assessment and reporting, and operations and production; for civil society, it was on governance, service provision, research and development, and operations and production; and for PSOs, it was on governance, management and strategy, organizational systems, and research and development. This shows that the nature of the organization plays a key role for where the sustainability changes start, which strenghtens and provides more insights into Soyka's (2012) argument.

Table 5. Comparison of where sustainability change started in the different types of organizations.

The Kruskal Wallis tests on organization type showed statistical differences at p < 0.05 (see Table 6), where: civil society had a lower mean than corporations and PSOs on management and strategy, organizational systems, and supply chains; civil society had a higher mean than corporations and PSOs on service provision, and research and development; and corporations had a lower mean than civil society and PSOs on assessment and reporting. This shows that the nature of civil society organizations affects where the changes in the system elements take place, which strenghtens and provides more insights into Soyka's (2012) argument.

Table 6. Kruskal Wallis comparison test on the organization type for the system elements affected by change.

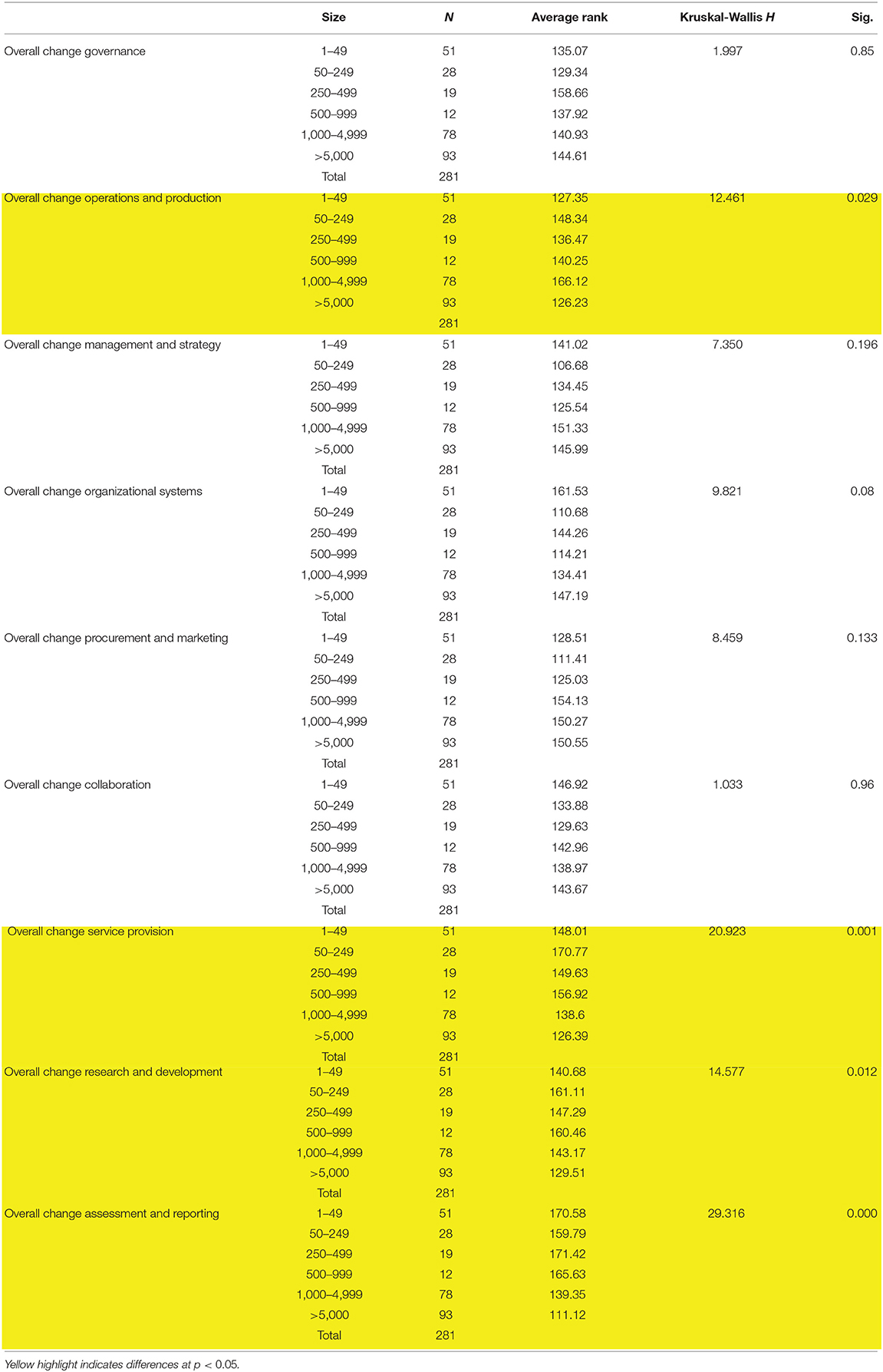

The Kruskal Wallis on organization size (see Table 7) shows statistical differences at p < 0.05 for: service provision, and assessment and reporting were the larger organizations had lower means, this indicates that smaller organizations have larger changes in these two system elements; for operations and production, where the extremes (the smallest and largest organizations) had the lowest means, and the highest mean was at 1,000–4,999 employees; for research and development, where the lowest mean was for organizations with more than 5,000 employees, and the highest mean for those with 50–249 and with 500–999 employees. These results show that for change in some system elements size is important.

Table 7. Kruskal Wallis comparison test on the organization size for the system elements affected by change.

Organizations have been instrumental in driving sustainability. During the last decade, there has been an increase on organizational change management for sustainability, where many efforts have been aimed at incorporating sustainability in organizations. However, incorporating, integrating, and institutionalizing sustainability in organizations is still under-researched. This paper has aimed to provide insights into this topic.

A survey was developed for investigating the importance of how sustainability has been embedded in organizations. The survey was sent to a database of 5,299 contacts from different organizations worldwide. From the total list of organizations, 281 useable responses for the organizational change part were obtained.

The results show that more than 90% of the responding organizations have been working with sustainability for more than 5 years. The main driving forces for sustainability have been equally by external stimuli and internal factors. The focus on sustainability and recognition of the impacts are fairly aligned. The findings show that the key focus, in the start and during the changes, has been on governance, management and strategy, and operations and production. The majority of the changes were in between six and seven systems elements. The comparison tests show that the nature of the organization plays a key role for where the sustainability changes start, and how the changes affect system elements. The results also show that for change in some system elements size is important. It should be noted that the time working with sustainability does not seem to affect where changes start, or the system elements affected.

This research scrutinizes the start of sustainability changes and the system elements affected by such changes, where it can be seen that in the majority of the cases six or seven of the elements are addressed. This indicates a large degree of institutionalization; however, there are some system elements that are more prominent as catalysts and subjected to change, such as governance, management and strategy, and operations and production.

Although sustainability changes have been mainly top-down, there are some changes in system elements that engage with external stakeholders, and internal change and innovation.

The research shows that it is inconsequential where sustainability changes start, as long as they are implemented throughout all the system elements, including internal and external stakeholders. Planning sustainability changes must address its four dimensions holistically, as well as technical, managerial, and organizational issues, and the organization's stakeholders.

Further research should be carried out, e.g., through case studies, to obtain responses from individuals occupying different roles and levels to check if there are differences of opinion about organizational changes. The causes of change in the system elements should also be explored, as well as the links between them.

The datasets for this article are not publicly available because the dataset was generated in a group and the complete dataset is to be used in separate publications. Partial access to the dataset (in particular to this research) may be provided. Requests should be made to Prof. Rodrigo Lozano (Rodrigo.lozano@hig.se).

RL prepared the introduction and literature review, and proposed the framework. IG carried out the analyses. Both authors discussed the results and co-wrote the paper.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

1. ^Qualtrics (2018). Qualtrics. Available online at: https://www.qualtrics.com/uk/customer-experience/surveys/

2. ^The other sections are analyzed in other papers published and currently under preparation.

Adams, C. A., and McNicholas, P. (2007). Making a difference. Sustainability reporting, accountability and organisational change. Account. Audit. Accountabil. J. 20, 382–402. doi: 10.1108/09513570710748553

Anderson, D., and Ackerman Anderson, L. (2001). Beyond Change Management. Jossey-Bass/Pfeiffer (Hoboken, NJ: Wiley).

Ben-Eli, M. U. (2018). Sustainability: definition and five core principles, a systems perspective. Sustain. Sci. 13, 1337–1343. doi: 10.1007/s11625-018-0564-3

Bennis, W. G., Benne, K. D., and Chin, R. (1969). The Planning of Change (Second). Holt: Rinehart and Winston, Inc.

Blanco-Portela, N., Benayas, J., Pertierra, L. R. L. R., and Lozano, R. (2017). Towards the integration of sustainability in Higher Education Institutions: a review of drivers of and barriers to organisational change and comparison against those found of companies. J. Clean. Prod. 166, 563–578. doi: 10.1016/j.jclepro.2017.07.252

Ceulemans, K., Lozano, R., Alonso-Almeida, M., and del, M. (2015). Sustainability reporting in higher education: interconnecting the reporting process and organisational change management for sustainability. Sustainability 7, 8881–8903. doi: 10.3390/su7078881

Danter, K. J., Griest, D. L., Mullins, G. W., and Norland, E. (2000). Organizational change as a component of ecosystem management. Soc. Nat. Resourc. 13, 537–547. doi: 10.1080/08941920050114592

Dawson, P. (1994). Organizational Change. A Processual Approach. London, UK: Paul Chapman Publishing Ltd.

DeSimone, L. D., and Popoff, F. (2000). Eco-Efficiency. The Business Link to Sustainable Development. Cambridge, MA: MIT Press.

Diesendorf, M. (2000). “Sustainability and sustainable development,” in Sustainability: The Corporate Challenge of the 21st Century, Vol. 2, eds D. Dunphy, J. Benveniste, A. Griffiths, and P. Sutton (Crows Nest, NSW: Allen & Unwin), pp. 19−37.

Domingues, A. R. A. R., Lozano, R., Ceulemans, K., and Ramos, T. B. T. B. T. B. (2017). Sustainability reporting in public sector organisations: exploring the relation between the reporting process and organisational change management for sustainability. J. Environ. Manage. 192, 292–301. doi: 10.1016/j.jenvman.2017.01.074

Doppelt, B. (2003). Leading Change Toward Sustainability. A Change-Management Guide for Business, Government and Civil Society. Austin, TX: Greenleaf Publishing.

Dunphy, D., Griffiths, A., and Benn, S. (2003). Organizational change for corporate sustainability. 3rd ed. London, UK: Routledge.

Henriques, A., and Richardson, J. (2005). The Triple Bottom Line. Does it All Add Up? London, UK: Earthscan.

Hjorth, P., and Bagheri, A. (2006). Navigating towards sustainable development: a system dynamics approach. Futures 38, 74–92. doi: 10.1016/j.futures.2005.04.005

Holliday, C. O. J., Schmidheiny, S., and Watts, P. (2002). Walking the Talk. The Business Case for Sustainable Development. Austin, TX: Greenleaf Publishing.

Hussey, D. M., Kirsop, P. L., and Meissen, R. E. (2001). Global reporting initiative guidelines: an evaluation of sustainable development metrics for industry. Environ. Qual. Manage. 11, 1−20.

Jennings, D. (2002). Strategic sourcing: benefits, problems and a contextual model. Manage. Decision 40, 26–34. doi: 10.1108/00251740210413334

Jennings, P. D., and Zandbergen, P. A. (1995). Ecologically sustainable organizations: an institutional approach. Acad. Manage. Rev. 20, 1015–1052. doi: 10.5465/AMR.1995.9512280034

Leon, R.-D. (2013). From the sustainable organization to sustainable knowledge-based organization. Econ. Insight. Trends Challenges 2, 63–73.

Lewin, K. (1947a). Frontiers in group dynamics. Concept, method and reality in social science; social equilibria and social change. Hum. Relat. 1, 5–41.

Lewin, K. (1947b). “Group decision and social change,” in Readings in Social Psychology, eds T. Newcomb and E. Hartley. (Holt:Reinhardt and Winstong, Inc), 197–211.

Linnenluecke, M. K., and Griffiths, A. (2010). Corporate sustainability and organizational culture. J. World Bus. 45, 357–366. doi: 10.1016/j.jwb.2009.08.006

Linnenluecke, M. K., Russell, S. V., and Griffiths, A. (2009). Subcultures and sustainability practices: the impact on understanding corporate sustainability. Bus. Strategy Environ. 18, 432–452. doi: 10.1002/bse.609

Lozano, R. (2006). Incorporation and institutionalization of SD into universities: breaking through barriers to change. J. Cleaner Prod. 14, 787–796. doi: 10.1016/j.jclepro.2005.12.010

Lozano, R. (2009). Orchestrating Organisational Change for Corporate Sustainability. Strategies to Overcome Resistance to Change and to Facilitate Institutionalization. Business School: (PhD thesis). Cardiff University.

Lozano, R. (2012a). Orchestrating organisational changes for corporate sustainability: overcoming barriers to change. Greener Manage. Int. 43–67.

Lozano, R. (2012b). Towards better embedding sustainability into companies' systems: an analysis of voluntary corporate initiatives. J. Cleaner Prod. 25, 14–26. doi: 10.1016/j.jclepro.2011.11.060

Lozano, R. (2013). Are companies planning their organisational changes for corporate sustainability? an analysis of three case studies on resistance to change and their strategies to overcome it. Corporate Soc. Responsibil. Environ. Manage. 20, 275–295. doi: 10.1002/csr.1290

Lozano, R. (2015). A holistic perspective on corporate sustainability drivers. Corporate Soc. Responsibil. Environ. Manage. 22, 32–44. doi: 10.1002/csr.1325

Lozano, R. (2018). Proposing a definition and a framework of organisational sustainability: a review of efforts and a survey of approaches to change. Sustainability 10:1157. doi: 10.3390/su10041157

Lozano, R., and Huisingh, D. (2011). Inter-linking issues and dimensions in sustainability reporting. J. Cleaner Prod. 19, 99–107. doi: 10.1016/j.jclepro.2010.01.004

Lozano, R., Nummert, B., and Ceulemans, K. (2016). Elucidating the relationship between sustainability reporting and organisational change management for sustainability. J. Cleaner Prod. 125, 168–188. doi: 10.1016/j.jclepro.2016.03.021

Lozano, R., and von Haartman, R. (2018). Reinforcing the holistic perspective of sustainability: analysis of the importance of sustainability drivers in organizations. Corporate Soc. Responsibil. Environ. Manage. 25, 508–522. doi: 10.1002/csr.1475

O'Connor, M. (1991). Entropy, structure, and organisational change. Ecol. Econ. 3, 95–122. doi: 10.1016/0921-8009(91)90012-4

Pettigrew, A., and Whipp, R. (1991). Managing Change for Competitive Success. Hoboken, NJ: Blackwell Publishers Ltd.

Pfeffer, J. (2010). Building sustainable organizations: the human factor. Acad. Manage. Perspect. 24, 34–45. doi: 10.5465/AMP.2010.50304415

Ragsdell, G. (2000). Engineering a paradigm shift? An holistic approach to organisational change management. J. Org. Change 13, 104–120. doi: 10.1108/09534810010321436

Rodríguez-Olalla, A., and Avilés-Palacios, C. (2017). Integrating sustainability in organisations: an activity-based sustainability model. Sustainability 9:1072. doi: 10.3390/su9061072

Saviano, M., Bassano, C., Piciocchi, P., Di Nauta, P., and Lettieri, M. (2018). Monitoring viability and sustainability in healthcare organizations. Sustainability 10, 1–23. doi: 10.3390/su10103548

Sayce, S., Ellison, L., and Parnell, P. (2007). Understanding investment drivers for UK sustainable property. Build. Res. Inform. 35, 629–643. doi: 10.1080/09613210701559515

Siebenhüner, B., and Arnold, M. (2007). Organizational learning to manage sustainable development. Bus. Strategy Environ. 16, 339–353. doi: 10.1002/bse.579

Keywords: organizations, sustainability, change management, institutionalization, drivers, impacts

Citation: Lozano R and Garcia I (2020) Scrutinizing Sustainability Change and Its Institutionalization in Organizations. Front. Sustain. 1:1. doi: 10.3389/frsus.2020.00001

Received: 08 February 2020; Accepted: 08 April 2020;

Published: 08 May 2020.

Edited by:

Bankole Osita Awuzie, Central University of Technology, South AfricaReviewed by:

Primiano Di Nauta, University of Foggia, ItalyCopyright © 2020 Lozano and Garcia. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Rodrigo Lozano, Um9kcmlnby5sb3phbm9AaGlnLnNl

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.