94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

PERSPECTIVE article

Front. Public Health , 16 April 2020

Sec. Public Health Policy

Volume 8 - 2020 | https://doi.org/10.3389/fpubh.2020.00110

Francisco Goiana-da-Silva1,2*†

Francisco Goiana-da-Silva1,2*† David Cruz-e-Silva3

David Cruz-e-Silva3 Oliver Bartlett4

Oliver Bartlett4 Joana Vasconcelos5

Joana Vasconcelos5 Alexandre Morais Nunes6

Alexandre Morais Nunes6 Hutan Ashrafian1Marisa Miraldo7Maria do Céu Machado8Fernando Araújo9

Hutan Ashrafian1Marisa Miraldo7Maria do Céu Machado8Fernando Araújo9 Ara Darzi10

Ara Darzi10The World Health Organization highlights fiscal policies as priority interventions for the promotion of healthy eating in its Action Plan for the Prevention and Control of Non-communicable Diseases. The taxation of sugar sweetened beverages (SSBs) in particular is noted to be an effective measure, and SSBs taxes have already been implemented in several countries worldwide. However, although the evidence base suggests that this will be effective in helping to combat rising obesity rates, opponents of SSBs taxation argue that it is illiberal and paternalistic, and therefore should be avoided. Bioethical analysis may play an essential role in clarifying whether policymakers should adopt SSBs taxes as part of wider obesity strategy. In this article we argue that no single ethical theory can account for the complexities inherent in obesity prevention strategy, especially the liberal theories relied upon by opponents of SSBs taxation. We contend that a pluralist approach to the ethics of SSBs taxation must be adopted as the only suitable way of accounting for the multiple overlapping, and sometimes, conflicting factors that are relevant to determining the moral acceptability of such an intervention.

- Evidence shows that appropriately designed fiscal policies have the potential to impact diets and must be implemented through a concerted approach with other policy actions.

- The WHO identifies levying taxes on sugar-sweetened beverages as an effective measure to tackle NCDs.

- Bioethics may play an essential role in clarifying the acceptability of levying taxes on sugar-sweetened beverages.

- Arguments on the ethicality of levying taxes on sugar-sweetened beverages that are based solely on one ethical theory should be rejected.

- Use of a pluralist, principled account of public health ethics would better reflect the complexity of the policy decision at stake, and would produce more helpful conclusions on whether these novel public health interventions are ethical.

Bioethics is a multifaceted field of study. Even though it has evolved over recent decades, it is often mistaken as only representing medical ethics (1). Bioethics is not solely concerned with genetics, euthanasia and doctor-patient relationship, and must be transversal to all daily health related operations and sectors. Bioethics therefore has a role to play in the design and implementation of public health interventions to address key societal issues. One such issue is the design of interventions to prevent non-communicable diseases (NCDs), in particular fiscal policies (2).

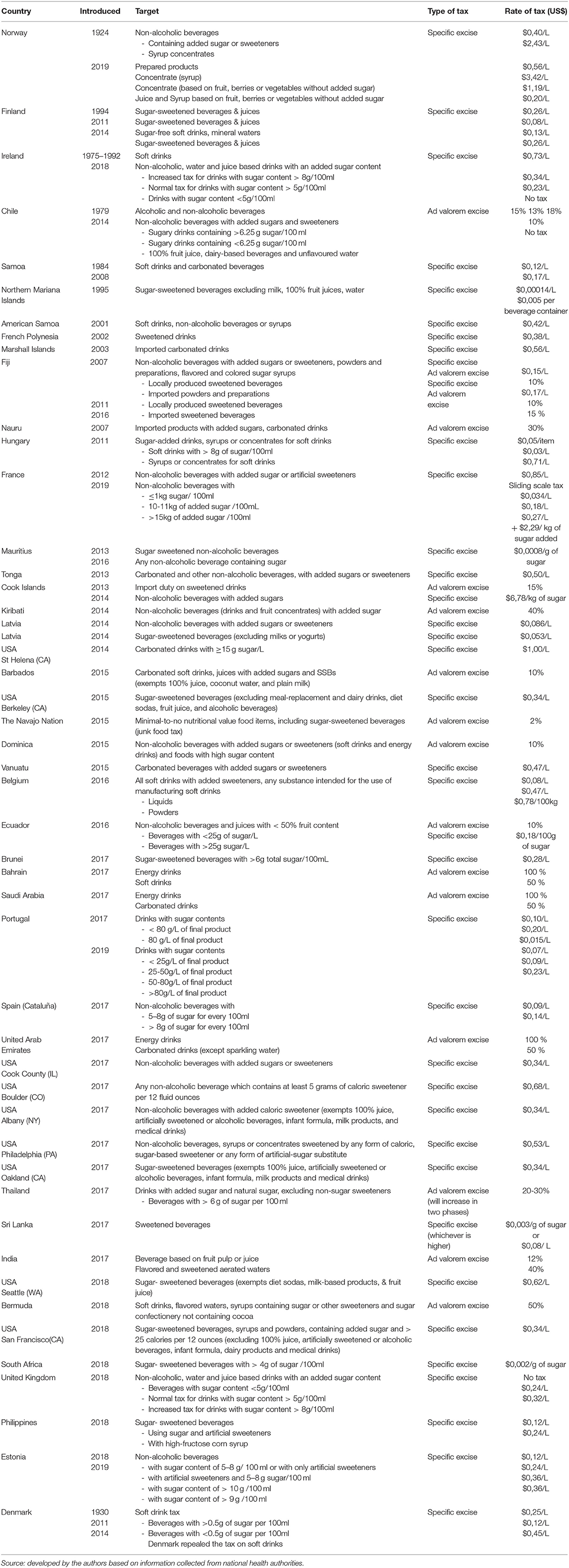

Fiscal policies are outlined as a priority intervention in the promotion of healthy eating on the Action Plan for the Prevention and Control of NCDs in the WHO European Region 2016–2025, with taxes on sweetened beverages highlighted as an effective measure (3). Both taxes and subsidies are proven to influence purchasing behaviors, particularly in relation to sweetened beverages (4). Currently, taxation policies targeting the consumption of sugar-sweetened beverages (SSBs) are already implemented in several countries worldwide (Table 1).

Table 1. List of countries where taxation policies targeting the consumption of sweetened beverages have been implemented.

Bioethical analysis can make an important contribution to the public health policymaking process by establishing a coherent moral framework for why governments should or should not intervene in public health in certain ways. This perspective article seeks to demonstrate how we can ensure that the ethical analysis we perform is as sound as possible.

Prior to analyzing the ethicality of particular public health interventions, analysts must establish why a particular health issue should be a matter of public concern and require government intervention. Several approaches to address this query are possible—some have answered it using social contract theory (5), some with political science (6). Ruger has developed a particularly powerful argument for government intervention in health that combines virtue ethics and capability theory (7). Whichever approach is taken, high prevalence of obesity in a population is generally accepted as an issue that governments should take responsibility for addressing.

In such context, analysts must evaluate whether a particular form of government intervention should be used to address a public health issue. In this paper we focus on the question of whether taxes on SSBs should be used to contribute to obesity prevention policy. The analysis we employ is doctrinal in nature. This involves looking at ethical arguments as syllogisms—a type of reasoning in which conclusions are drawn from premises—and testing whether the conclusions drawn in these arguments are logically sound. Premises are usually statements drawn from ethical doctrine—for example, interfering with autonomy is always wrong (first premise), and sugar taxes interfere with consumer autonomy (second premise). A conclusion must be based on factually accurate premises to be considered valid. The factual accuracy of premises will be assessed by examining whether they are supported by epidemiological evidence.

We first focus on the common claims that SSBs taxation is wrong because drinking SSBs does not harm others, and because taxation restricts consumer choice, which are grounded in deontological ethical theory (under which ethicality is judged according to rules or duties relating to the nature of actions). By applying the findings of behavioral science to the generalized premises on which this reasoning is based, we will show that they cannot be considered factually accurate, and therefore valid ethical conclusions cannot be drawn from them. However, we also find that changing the ethical theory does not change this outcome—claims grounded solely in other ethical theories, for example constructivism (under which ethicality is judged not according to the nature of actions but according to their outcomes), are equally unable to reflect the complexity of the evidence base surrounding SSBs consumption, and are therefore equally likely to produce unsound ethical conclusions.

We will use this brief analysis to then argue that the only way to arrive at valid conclusions on the ethicality of SSBs taxation is to ground the premises of arguments in a plurality of ethical theories. The policy decision to tax SSBs is based upon a complex evidence base, and an assessment of the ethicality of this decision must take account of this evidence base. Since basing an ethical argument on only one ethical theory tends to mean it is based on factually inaccurate premises, we argue that grounding ethical analysis in several ethical theories will result in the premises of that analysis better reflecting the complexity of the evidence base surrounding SSBs taxation (and obesity prevention generally), thus leading to sounder ethical conclusions.

To locate the information needed to conduct the above analysis, we primarily used Google Scholar keyword searches (e.g., “ethics” + “theories” + “liberalism” + “autonomy” + “sugar sweetened beverages” + “taxation”) to identify academic papers related to the ethics of SSBs taxation, the ethics of public health taxes, and the ethics of public health generally. We also used Google Scholar keyword searches (e.g., “sugar sweetened beverages” + “taxation” + “policy” + “evidence” + “impact” + “health”) to identify epidemiological literature on the population health impact of SSBs taxation and health inequality tends related to SSBs consumption, as well as behavioral science studies relating to consumer behavior (e.g., “consumer” + “behavior” + “evidence” + “soda”). We also relied specifically on similar keyword searches of leading public health ethics journals such as: Public Health Ethics; Ethics, Medicine and Public Health; and The Journal of Law, Medicine and Ethics. To ensure that our information remained current, we limited our searches to academic and policy sources dating from 2000 to the present (excepting sources that spoke to historical trends or viewpoints).

Opponents of SSBs taxes make the general argument that they are illiberal and paternalistic, and thus wrong (8). Libertarians, in the context of public health, believe that government intervention can only be ethical when it enables individual freedom and sustains the conditions for autonomous agency, (9) and this generally means limiting government intervention to non-coercive measures, or at least those coercive measures that are absolutely necessary to prevent an individual being harmed by another. This view is a form of deontological ethical theory, which broadly holds that actions should be judged by whether the nature of the action itself can be considered morally worthy. Individuals establish the rules governing whether an action is morally worthy though critical and rational self-reflection. Thus, the autonomy of human thought, and the freedom to reason critically are essential to moral conduct—anything that limits this autonomy and freedom should itself be considered unethical.

Evidently, fostering every individual's agency to make healthy decisions is important to population sustainability, however as is clear from the seminal work by Geoffrey Rose (10) and continued by others (11), promoting good health within a society requires greater attention to be devoted to how factors affecting health impact upon groups of individuals, rather than individuals in isolation. Public health interventions must therefore be designed primarily with the collective as the beneficiary of the intervention, not the individual. This means that judging the ethicality of a public health intervention, such as a tax on SSBs consumption, purely on the basis of the extent to which it interferes with individual autonomy and freedom means that we are only judging part of the motivation to adopt that intervention, and even then not the most important motivation (12). In the paragraphs below, we show how this impacts the validity of the ethical conclusions drawn from arguments based on autonomy.

Opponents of SSBs taxation usually deploy JS Mills' harm principle, stating that public health interventions should only be made to prevent harm to others, and since SSBs consumption only directly harms the individual, taxing SSBs is unethical. However, the evidence base demonstrates that population SSBs consumption clearly does have negative effects on others—higher rates of population SSBs consumption are linked to higher rates of obesity which place greater pressure on health care resources (13). This affects resource allocation decisions, which necessarily have negative implications for some areas of health and social care and impact the experiences of other individuals. Moreover, the harm principle as originally articulated by Mill does not insist that externalities must be proximate to individuals to any specific degree—in fact Mill himself insisted that government intervention in certain areas, such as consumer product regulation, should not be governed by his ideas on liberty at all, but by his doctrine on free trade in which he sets out how governments should balance economic efficiency with public welfare protection (14).

Thus, both premises in the libertarian argument are factually inaccurate—liberal ethical doctrine does not insist that public health interventions can only prevent direct harm to others, and SSBs consumption does generate significant social burdens in addition to the harms suffered by individual consumers. The reasoning of this argument does not sufficiently account for the complex relationship between high population levels of SSBs consumption, rates of obesity, and healthcare resource allocation, and government responsibility for social protection. Thus, evaluated on the strength of its reasoning, the libertarian argument that SSBs taxation is unethical should be seen as unsound.

Opponents also usually deploy ideas of autonomy and free choice, arguing that consumer autonomy holds a privileged status in moral considerations, and should be given the highest priority in the formation of public health interventions. Since taxing SSBs substantially interferes with consumers' abilities to make autonomous and free choices, taxing SSBs is unethical. However, the evidence base tells us that factors such as the availability of healthy compared to unhealthy foods and beverages (15) and pricing strategies for SSBs (16) heavily shape the choices available to individuals before they even arrive in a consumption choice situation. It is clear that when an individual makes a consumption choice, that choice is not a pure translation of individual preferences, but the outcome of a complex mix of individual preferences, marketing messages, environmental conditions and psychological pressures. Some of these influences on consumers' choices occur simply because the consumer is a certain gender, or because they were born in a particular neighborhood, meaning that different consumers will make choices about consuming healthy or unhealthy products from vastly different starting points. This is unfair, and according to the weight of evidence on the effect that health inequalities have on burdens of disease (17), combatting health inequality should be an important consideration for governments when choosing public health interventions—perhaps more important even than protecting consumer autonomy in every situation.

Moreover, this argument presumes that making SSBs more expensive will have an impact upon consumer autonomy. As recent analysis on the issue points out, autonomy and freedom should be distinguished, and reducing an individual's freedom to buy SSBs at low prices does not necessary reduce their ability to make autonomous decisions on whether to buy SSBs at higher prices (18). Furthermore, it is not clear from the epidemiological evidence that consumers' autonomy is affected by SSBs taxes. Evidence from the UK suggests that there is actually strong support for SSBs taxation, which would unlikely be the case if consumers felt that their ability to make health decisions for themselves was being compromised. Perhaps one could argue that consumers' autonomy could be compromised without them realizing, but then this would seem to support the argument for SSBs taxation—if the way in which an individual thinks about their food decisions can be easily manipulated by subtle changes to the decision-making context without the individual ever realizing this, as behavioral and marketing evidence shows that it can (19), this would support affording the protection of autonomy a less privileged position in public health decision making, and instead privileging how policies can prevent consumer decisions from being manipulated.

Thus, both premises in the deontological argument based on autonomy are factually inaccurate—governments have more (and arguably more important) duties than simply to protect consumer autonomy, and SSBs taxation probably does not appear to influence consumer autonomy to a very large extent (and testing this more forensically would constitute an acknowledgment that consumer autonomy is a frail concept). The reasoning of this argument does not sufficiently account for the complex influences that environmental conditions and social inequalities have on SSBs consumption, nor for the fact that an autonomous consumer may actually welcome public health interventions. Thus, evaluated on the strength of its reasoning, the argument from autonomy that SSBs taxation is unethical should also be seen as unsound.

The analysis above demonstrates that basing arguments on the ethics of public health practice on one ethical theory leads to unsound conclusions. This outcome is the same no matter what ethical theory is used in place of deontology, even if it seems more suited to guiding community-oriented action. For example, utilitarianism, the leading variant of constructivism, holds that an action is ethical if the consequences maximize utility (often understood as the greatest happiness experienced by the greatest number of people). These idea influences the development of obesity policy at the highest levels in the form of cost-benefit analysis of interventions (20). However, reliance on utilitarian analysis alone also cannot produce logically sound ethical conclusions where SSBs taxation is concerned, because the premises of most utilitarian argument do not account well for complexity either, and therefore are factually inaccurate. In particular, utilitarian analysis does not account well for hidden discrimination and inequality (21), which confounds utilitarian calculations of happiness.

For example, a utilitarian argument might be that the happiness produced by the health consequences of increasing SSBs prices (decreased population consumption of SSBs, contributing to reduced rates of population obesity, particularly childhood obesity) would be greater than the unhappiness produced by the economic consequences of increasing SSBs prices (somewhat lower profits for the industry on SSBs, and the inconvenience of having to pay slightly more for SSBs). However, this does not account for the fact that lower socioeconomic groups consume proportionately more SSBs, spend a greater proportion of their income on them, and suffer greater rates of obesity (22). In such circumstances, it becomes very difficult to accurately calculate the happiness gained or lost by this population, not to mention the relative weight that should be attributed to this against the gains or losses of higher socioeconomic groups. Given that the regressive nature of SSBs taxation is another common objection raised by the industry, it is particularly important that ethical analysis be capable of properly accounting for the relationship between inequality, health and fiscal policy. Utilitarian constructivist arguments are therefore, like deontological arguments, unable on their own to produce sound ethical conclusions on SSBs taxation, since they also tend to be founded on factually inaccurate premises.

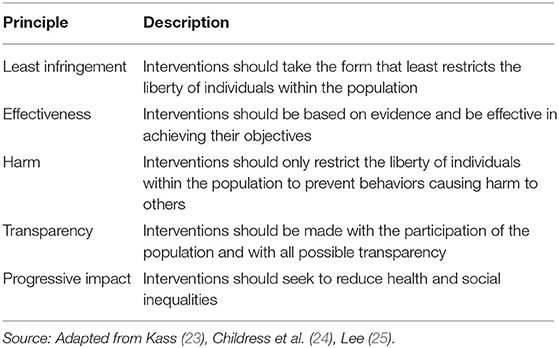

The ethical analysis of SSBs taxation therefore must be pluralist. Most new ethical theories tailored to a public health context adopt such a pluralist (or principled) approach, meaning that they identify a discrete set of different principles or values that are deemed important for ethical public health policy, and judge a public health intervention according to all of these principles simultaneously. Table 2 lists five of the most common principles found in new accounts of public health ethics, which combine a number of the traditional ethical ideas surveyed above.

Table 2. Public health ethics principles.

The potential flaws of principled ethical theories must also be recognized—the most important is the potential lack of clarity in how principles should be prioritized if they conflict, and how strong an obligation they should impose (26). In the authors' opinion, fulfilling one principle does not necessarily exclude the fulfillment of another. In the case of rights-based ethical accounts, the enjoyment of one right can exclude the enjoyment of another, and competing rights must be balanced using additional principles such as proportionality. However, fulfilling a principle does not necessarily mean that other principles cannot be simultaneously fulfilled. As long as principles are selected to be coherent with each other, a process to balance principles is not a necessity. As long as all principles carry equal weight, the only necessity is a criterion to decide how many principles an intervention must fulfill to be ethically acceptable.

Extensive evidence shows that implementing taxes on the consumption of SSBs generates significant health gains and has a positive impact on the reduction of premature mortality. The WHO has now produced detailed guidance on how to design fiscal policies relating to diet, responding to the manifest interest of many countries for more detailed advice on how to implement their international commitments to adopt effective measures to reduce premature mortality attributable to obesity (27). However, despite several countries having implemented such taxes, other countries continue to resist doing so (28). The rationale for this resistance is primarily economic in nature, however sometimes the issue of the perceived legitimacy of the measure is also raised.

Further bioethical debate in obesity policy is essential to ensure that policymakers are equipped with not just sound epidemiological evidence, but sound moral evidence on which they can base the implementation of polices that will shape healthier food environments. In this paper we sought to demonstrate that looking at the ethical legitimacy of interventions such as SSBs taxation through only one ethical lens is only likely to produce invalid ethical conclusions, since the premises on which many single-theory ethical arguments are based are ill-equipped to properly reflect the complexity of factors that must be considered in policy decisions implement SSBs taxes. A pluralist approach to the ethics of fiscal policies such as levying taxes on SSBs is therefore essential to produce a sound explanation of whether they are morally acceptable in a democratic society. Even though there are also certain issues inherent to pluralist ethical accounts of public health practice, their use is more likely to enable progress in ethical debates in the field of non-communicable disease prevention.

FG: Paper concept, design, drafting, critical analysis, and final approval. DC: Acquisition of data, Paper drafting, critical analysis, and final approval. OB: Paper concept, design, drafting, critical analysis and final approval. JV: Acquisition of data, Data analysis and final approval. AM: Acquisition of data, data analysis and final approval. HA: Paper concept, critical analysis and final approval. MM: Paper concept, critical analysis and final approval. MCM: Paper concept, critical analysis and final approval. FA: Paper concept, critical analysis and final approval. AD: Paper concept, critical analysis and final approval.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

FG holds an Imperial College London scholarship. After submission, Imperial College London kindly agreed to fund the open access fees for this paper. We thank to Imperial College London for funding the open access fees. Infrastructure support for this research was provided by the NIHR Imperial Biomedical Research Centre (BRC).

1. Galston AW, Shurr EG. New Dimensions in Bioethics. Boston, MA: Kluwer Academic Publishers (1997).

2. Murray CJ, Barber RM, Foreman KJ, Ozgoren AA, Abd-Allah F, Abera SF, et al. Global, regional, and national disability-adjusted life years (DALYs) for 306 diseases and injuries and healthy life expectancy (HALE) for 188 countries, 1990–2013: quantifying the epidemiological transition. Lancet. (2015) 28:2145–91. doi: 10.1016/s0140-6736(15)61340-x

3. World Health Organization (WHO). Action Plan for the Prevention and Control of Noncommunicable Diseases in the WHO European Region. Geneva:WHO (2016).

4. Andreyeva T, Long MW, Brownell KD. The impact of food prices on consumption: a systematic review of research on the price elasticity of demand for food. Am J Public Health. (2010) 100:216–22. doi: 10.2105/AJPH.2008.151415

5. Rothstein M. Rethinking the meaning of public health. J Law Med Ethics. (2002). 30:144–9. doi: 10.1111/j.1748-720x.2002.tb00381.x

6. Coggon J. What Makes Health Public?: A Critical Evaluation of Moral, Legal, and Political Claims in Public Health. Cambridge: Cambridge University Press (2012).

8. Pratt K. A constructive critique of public health arguments for antiobesity soda taxes and food taxes. Tulane Law Rev. (2012) 87:73–140. doi: 10.1016/j.orcp.2012.08.067

9. Radoilska L. Public health ethics and liberalism. Public Health Ethics. (2009) 2:135–45. doi: 10.1093/phe/php010

11. Beaglehole R, Bonita R, Horton R, Adams O, Mckee M. Public health in the new era: improving health through collective action. Lancet. (2004) 19:2084–6. doi: 10.1016/s0140-6736(04)16461-1

12. Dawson A. Snakes and ladders: state intervention and the place of liberty in public health. J Med Ethics. (2016) 42:510–3. doi: 10.1136/medethics-2016-103502

13. Tremmel M, Gerdtham UG, Nilsson PM, Saha S. Economic burden of obesity: a systematic literature review. Int J Environ Res Public Health. (2017) 14:435–53. doi: 10.3390/ijerph14040435

14. Powers M, Faden R, Saghai Y. Libery, mill and the framework of public health ethics. Public Health Ethics. (2012) 5:6–15. doi: 10.1093/phe/phs002

15. Duran AC, Luna de Almeida S, do Rosario DO, Latorre M, Constante Jaime P. The role of the local retail food environment in fruit, vegetable and sugar-sweetened beverage consumption in Brazil. Public Health Nutrition. (2016) 19:1093–102. doi: 10.1017/s1368980015001524

16. Mamiya H, Moodie EEM, Ma Y, Buckeridge DL. Susceptibility to price discounting of soda by neighbourhood educational status: an ecological analysis of disparities in soda consumption using point-of-purchase transaction data in Montreal, Canada. Int J Epidemiol. (2018) 47:1877–86. doi: 10.1093/ije/dyy108

17. Marmot M, Bell R. Fair society, healthy lives. Public Health. (2012) 126(Suppl. 1):S4–S10. doi: 10.1016/j.puhe.2012.05.014

18. Véliz C, Maslen H, Essman M, Smith Taillie L, Savulescu J. Sugar, Taxes, & Choice. Hastings Cent Rep. (2019) 49:22–31. doi: 10.1002/hast.1067

19. Cohen DA, Babey SH. Contextual influences on eating behaviours: heuristic processing and dietary choices. Obes Rev. (2012) 13:766–79. doi: 10.1111/j.1467-789X.2012.01001.x

20. World Health Organization (WHO). Global Strategy on Diet, Physical Activity and Health. Geneva: WHO (2016).

21. Rogers WA. Feminism and public health ethics. Journal of Medical Ethics (2006) 32:351–4. doi: 10.1136/jme.2005.013466

22. Backholer K, Sarink D, Beauchamp A, Keating C, Loh V, Ball K, et al. The impact of a tax on sugar-sweetened beverages according to socio-economic position: a systematic review of the evidence. Public Health Nutr. (2016) 19:3070–84. doi: 10.1017/s136898001600104x

23. Kass NE. An ethics framework for public health. Am J Public Health. (2001) 91:1776–82. doi: 10.2105/ajph.91.11.1776

24. Childress JF, Faden RR, Gaare RD, Gostin LO, Kahn J, Bonnie RJ, et al. Public health ethics: mapping the terrain. J Law Med Ethics. (2002) 30:170–8. doi: 10.1111/j.1748-720x.2002.tb00384.x

25. Lee LM. Public health ethics theory: review and path to convergence. J Law Med Ethics. (2012) 40:85–98. doi: 10.1111/j.1748-720x.2012.00648.x

26. Dawson A. Resetting the parameters: public health as the foundation for public health ethics. In Dawson A (ed). Public Health Ethics: Key Concepts and Issues in Policy and Practice. Cambridge: Cambridge University Press (2011).

Keywords: sweetened beverages, taxation, pricing policies, bioethics, health policy

Citation: Goiana-da-Silva F, Cruz-e-Silva D, Bartlett O, Vasconcelos J, Morais Nunes A, Ashrafian H, Miraldo M, Machado MC, Araújo F and Darzi A (2020) The Ethics of Taxing Sugar-Sweetened Beverages to Improve Public Health. Front. Public Health 8:110. doi: 10.3389/fpubh.2020.00110

Received: 08 August 2019; Accepted: 18 March 2020;

Published: 16 April 2020.

Edited by:

Paul Russell Ward, Flinders University, AustraliaCopyright © 2020 Goiana-da-Silva, Cruz-e-Silva, Bartlett, Vasconcelos, Morais Nunes, Ashrafian, Miraldo, Machado, Araújo and Darzi. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Francisco Goiana-da-Silva, ZnJhbmNpc2NvZ29pYW5hc2lsdmFAZ21haWwuY29t

†ORCID: Francisco Goiana-da-Silva Orcid.org/0000-0003-2055-6906

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.