Petar Stankov

Petar Stankov

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Polit. Sci., 17 April 2025

Sec. Elections and Representation

Volume 7 - 2025 | https://doi.org/10.3389/fpos.2025.1565020

This article is part of the Research TopicWhat's Going On? European Electoral Change in Historical ContextView all articles

Populists weaponize economic hardships and identity conflicts for political gain. This strategy has propelled many of them to the political mainstream across Europe, the Americas, and elsewhere. However, does their toxic rhetoric necessarily map into poor management of government finances? This paper investigates one aspect of their governance—its correlation with government debt spanning the period between 1950 and 2022 in Europe and the OECD countries. Although previous evidence suggests that populist governance spells a rise in indebtedness, new evidence in this paper mitigates this conclusion. The results in this work do not provide sufficient evidence of an increase in debt specifically linked to populist governance. Three mechanisms may be at play. First, fiscal rules and checks and balances embedded in the democratic process in those countries make bad governance punishable in the following elections. Second, most populists in Europe and the OECD have so far been allocated junior coalition roles, limiting their potential damage on policy design and implementation. Third, the parliamentary democracies studied in this work may operate differently from the presidential regimes that have, until recently, dominated empirical evidence. As a result, most of the evidence in this work points to a relatively small, if at all significant, effect of populist governance on public debt. Nuances do emerge along the political spectrum, but they are evident after the Global Financial Crisis of 2008–2009.

Populism has many definitions and several credible origins (Rovira Kaltwasser et al., 2017). Its dominant definition separates society into two antagonistic camps, each one of them adopting radically different identities—“the pure people” and “the corrupt elite” (Mudde, 2004). A common denominator among the many existing approaches to defining populism is that populists weaponize economic hardships and identity conflicts for political gain (Stankov, 2020), which effectively sums up the two widely accepted explanations for the rise of populism: economic insecurity and cultural backlash (Gandesha, 2018). When used as a political strategy which is often the case (Weyland, 2017), populism has propelled many candidates to the political mainstream across Europe, the Americas, and elsewhere. But what do they do with their newly acquired powers? Do their post-election policies mimic those of the traditional elites they replace or, instead, they depart from the mainstream and map their divisive pre-election rhetoric into economic mismanagement and political carnage? To oversimplify: Are populists bad governors? The answer has been debated in both political science and economics literature over the last few decades, with the debate affecting areas of the rule of law, the justice system, specific policies on education and health, and other fundamental aspects of governance, such as free and fair elections, acceptance of electoral results, democratic erosion and the state of the media environment (Norris and Inglehart, 2019; Przeworski, 2019).

The debate on the economic and political impact of incumbent populism has acquired renewed urgency since the European far-right parties were promoted to main opposition parties and Donald Trump was reelected in 2024. Within the economics discipline, the debate started more than 35 years ago, when Sachs (1989) and Dornbusch and Edwards (1990) pioneered the economic theory of populism and witnessed it grow into a populist paradigm. To them, the answer was clear: A populist governance is bad news for the economy as it normally ignores hard budget constraints and market incentives. A brief lift-off of the economy driven by a savior government and a charismatic leader at its helm is sufficient to temporarily lift voter spirit and welfare. However, the same populist government makes the same voters permanently worse-off in the long run. It does so by spending more than it can afford to, subjugating the central bank, inflating prices, sparking exchange rate and fiscal crises, and blaming everyone else for it.

In political science, the debate created multiple focal points around the impact of populist governance on the effectiveness of rival opposition parties (Brewer-Carías, 2010), independent judiciary (Colburn, 2011; de la Torre and Lemos, 2016), as well as civil society and independent organizations (Denisova, 2017). Kendall-Taylor et al. (2019, p. 3) summarize the political impact of populist governance as a strategy using “societal dissatisfaction to gradually undercut institutional constraints on their own rule, sideline opponents, and weaken civil society.” This strategy for eroding democracy is similar in both historical and modern episodes of populist rule. As the state of democracy affects long-term growth (Acemoglu et al., 2019), populist governance may then indirectly deter economic prosperity.

For decades, case studies have broadly confirmed the detrimental impact of populist rule on both the economy and the state of democracy. The initial evidence was developed on case studies from Latin America and later extended back and forward in time to capture long-term waves of populism and authoritarianism since the start of the 20th century in a variety of electoral settings (Dalio et al., 2017; Edwards, 2019; Stankov, 2020; Funke et al., 2023).

Today, voters in most democracies accept that populists may enter parliament, or become part of the ruling coalition, or even nominate prime ministers and presidents. The promotion of populist governance from a set of isolated episodes to a global trend taking a page from authoritarian governance has created a variety of incumbent populists. It is this variety, as well as the seemingly relentless rise of its electoral appeal, that has reignited the debate on the economic effects of populist rule. Without downplaying their potentially damaging role for democracy and civil society, this paper studies their impact on an element of populist economic governance: their impact on government debt, which has become the focus of this work.

This impact will depend on the executive constraints populists face after elections. In the spirit of Taggart and Rovira Kaltwasser (2016), there are two types of constrained populists: (i) junior coalition partners and (ii) populists with a ruling majority. It is those with a ruling majority that are typically more consequential and, therefore, become the main unit of observation here. There is a third type of a populist in power as well: one for whom executive constraints are non-binding, such as the internationally and domestically hostile authoritarian regimes created by the ultra-nationalist populists like Mussolini, Hitler, Stalin and Putin. The ruin they bring to the rest of the world with little regard for the self-harm to their own societies makes everyone worse off and is a separate talking point. The constrained populists are a more domesticated bunch. The alleged harm they bring is also primarily domestic.

Like any other government, a populist one affects two broad elements of domestic life: the state of democracy and civil society, and the state of the economy. To measure the effects, widely accepted dynamic measures of democracy such as the ones produced by Freedom House (2018) and Marshall et al. (2019) can be linked to data on electoral outcomes. By combining those data sets, empirical political analysis can distill the political effects of populist rule. This combination of data sets, however, can do more than that.

The data on electoral outcomes produced by Döring and Manow (2024) can pinpoint the time populists migrate from the political fringe to the mainstream (and back) in 37 parliamentary democracies. Most of them are current or past members of either the European Union or the OECD. Studies covering both Europe and Latin America exist (Rode and Revuelta, 2015; Stankov, 2017; Stankov, 2018), but Döring and Manow (2024) deliver a preferable time coverage enabling us to track the electoral evolution of populist parties over much longer periods of time. Profound transformations of the local political landscape can then be linked to the subsequent changes in the lives and livelihoods of millions. This is what makes these political transformations interesting.

Using a version of the Döring and Manow (2024) data from 2019, Stankov (2020) links populist governance episodes to an array of fiscal, monetary, and real macroeconomic indicators. The indicators have been published by Jordà et al. (2017) and represent the longest publicly available series of macro-financial data for most of the European and OECD economies. Mapping this data to the political landscape enables Stankov (2020) to claim that economic populism does not extend to Europe and the OECD, although this still does not prevent their detrimental impact on rule of law and civil society.

This may be because most populists in Europe and the OECD have, at least until recently, settled for a somewhat irrelevant role of junior coalition partners. As such, they could only have a marginal say in the design and roll-out of core macroeconomic policies. This is valid for both far-left and far-right populists in their junior coalition roles, and for virtually all real indicators that Stankov (2020) looks at: GDP per capita, consumption, investment, and trade.

However, when a consolidated democracy elects a far-left or far-right prime minister, the game changes. As prime ministers are typically agenda-setters, their impact on policies is potentially far-reaching. By extension, their policies carry more potent economic ammunition, producing insights about how far-left and far-right populists govern. Far-left and far-right prime ministers differ in their short-run impact on the real macro economy, while governance by extreme politicians worsens the real economy in the long-run.

In contrast with experiences elsewhere, populist governance in Europe and the OECD does not have a pro-inflationary effect. We can see that for most of the monetary indicators studied: Narrow money, broad money, short-term interest rates, as well as long-term interest rates (Stankov, 2020). As before, there appears to be a distinction between cabinets formed with the help of populist parties and cabinets governed by a populist leader. Most fringe populists seem unable to leverage their political clout for monetary expansion, even though they have become part of the ruling coalition.

Therefore, when it comes to monetary policy, populists in Europe and the OECD seem closer to the political mainstream than those elsewhere. This is partly because of fortunate timing in Europe and the OECD: While populists elsewhere have had the chance to change the rules governing central banks to soften fiscal and monetary constraints, ruling populists in Europe have largely inherited those rules in an environment of strong checks and balances and strong central bank independence (Gavin and Manger, 2023; Masciandaro and Passarelli, 2020; Meyer, 2024). This heritage may have suppressed nascent political agendas to undermine central bank independence in Europe and the OECD.

Stankov (2020) offers similar conclusions on fiscal policies by linking the Jordà et al. (2017) macro-financial and Döring and Manow (2024) electoral outcomes data sets. The fiscal component of the macro-financial data tracks public debt to GDP, government revenues and expenditures, local currency exchange rate with the USD and indicates if the country has experienced a systemic financial crisis. There is weak evidence that cabinets formed with far-left parties are more prone to fiscal expansion, while cabinets formed with far-right parties limit government deficits. Some evidence emerges about the fiscal impact of far-left prime ministers. The evidence, however, is still inconclusive: The estimates alternate signs over time, suggesting a possible misspecification of the underlying econometric model.

Using instrumental variables, the evidence on the fiscal impact of far-left populists was recently extended, but it still found no conclusive evidence of fiscal expansions initiated by either far-left or far-right prime ministers in Europe and the OECD. Meanwhile, work on populist governance elsewhere has concluded that populist governance could knock off living standards and growth in the absence of strong checks and balances (Absher et al., 2020; Ball et al., 2019; Cachanosky and Padilla, 2020; Funke et al., 2023).

However, not all populists are equally perilous as their governance shows significant differences (Campos and Casas, 2021). Financial markets seem to know that. Fresh evidence from financial market performance under populist rule points to significant differences in how markets react when a populist wins an election (Hartwell, 2022). While markets in Latin America are volatile for days, those in Europe and the United States barely budge on the news that their governments will be run by populists.

A rich set of modeling choices has informed the above conclusions: Narratives have dominated the study of populist governance in the Arab World (Hinnebusch, 2020); fixed effects and Arellano-Bond dynamic panel data methods have served well in European context (Cachanosky and Padilla, 2020; Rodríguez-Pose and Dijkstra, 2021; Stankov, 2018, 2020); instrumental-variable methods have served well the study of government services (Blakeslee, 2018) and structural VAR modeling has taught us the evolution of wages under populism (Campos and Casas, 2021). The latest and perhaps the most promising direction in modeling populist governance outcomes is the synthetic control approach, represented by Absher et al. (2020), Grier and Maynard (2016) and, more recently, by Funke et al. (2023). This paper extends the above conclusions using fixed-effects methods, which are detailed below.

This work extends the above evidence with the following fixed effect panel OLS approach:

where is a policy outcome of interest , i.e., government debt levels in country in period ; indicates if the prime-minister shares far-left or far-right ideology; captures an interaction between the indicator and the share of seats in parliament for the ruling coalition, and are unobserved country- and time-specific effects, respectively, is a dummy variable capturing the specific electoral cycle of country ; is the number of years in office of the incumbent government to capture if generally do policies differently at different stages of their tenure in office, while the interaction between the dummy and captures any difference between the way extreme and the rest do policies along their tenure, and is an error term. Period may reflect either election timing or the time when the new government steps into power. To better reflect the actual policy of the incumbent populist governments, has been chosen as the start year of the government, not the year when the majority backing the government was elected. In many cases the 2 years would be identical, but we still need a criterion to resolve any ambiguity.

Note that the ideological position of the populist party and their leaders in the above model is reflective of their underlying ideology, which is assumed to be either far-left or far-right. Somewhat simplistically, this effectively assumes that populist parties and their leaders share extreme ideologies and that the inverse statement is also true—i.e., extreme politicians are, by definition, populist. Naturally, examples to the contrary exist. Mexico’s former president, López Obrador, is often described as populist but does not fit into the category of an extreme politician (Dussauge-Laguna, 2022). Similarly, Brazil’s former president Bolsonaro is invariably described as far-right (Guimarães and Dutra De Oliveira E Silva, 2021) but fitting him into the definition of a populist would perhaps be overly simplistic (Hunter and Power, 2019).

This simplifying assumption, however, is not entirely unjustified for Europe and the OECD. First, it builds on the understanding that European populist leaders, as well as the parties they represent, express views and draft manifestos which are typically close to the ideological extreme (Caiani and Della Porta, 2011; Mudde, 2007; Rooduijn and Akkerman, 2015). This is particularly notable for the phase of their political evolution spent in opposition (Mudde, 2016), which seems to be their natural state in Europe in the OECD since the 1950s. Second, from an empirical standpoint, distinguishing between extreme politicians and parties who are populist from those that are not is hard, particularly in European contexts. This is because most data sets covering Europe do not make this distinction. This may be because of an omission in the literature, which might be worth remedying, or because populism is a “thin” ideology (Bonikowski et al., 2019) which makes the distinction hard in some contexts. Drawing on earlier work by Stanley (2008), Mudde and Rovira Kaltwasser (2017) define this ‘thinness’ as an ability to borrow features of classic ideologies to appease the people and denounce the elite. It is this versatility of populism and its diverse facets that makes its disentangling from extreme ideologies difficult from an empirical standpoint in Europe. Third, such separation may not even be necessary for the sample of countries discussed in this work as for them populism has been associated with the ideological extremes for some time now (De Vries and Edwards, 2009). Therefore, the simplifying assumption is indeed restrictive, but it may be justified for the sample of countries studied in the above model.

Two sources of data are merged to allow estimation of model (1). First, the variables in the right-hand side of the model are taken from the Cabinet sheet in the Döring and Manow (2024) Parliaments and Goverments data. The data features parliamentary representative far-left and far-right parties in 37 parliamentary democracies since 1903, including all of today’s European Union, as well as those OECD countries which are not presidential systems. A full list appears in Table 1. Döring and Manow (2024) include national lower house chamber elections since 1900 and European Parliamentary (EP) elections since 1979. As the EP elections have different stakes than the local parliamentary ones, electoral outcomes on EP elections have been omitted to allow comparability across countries.

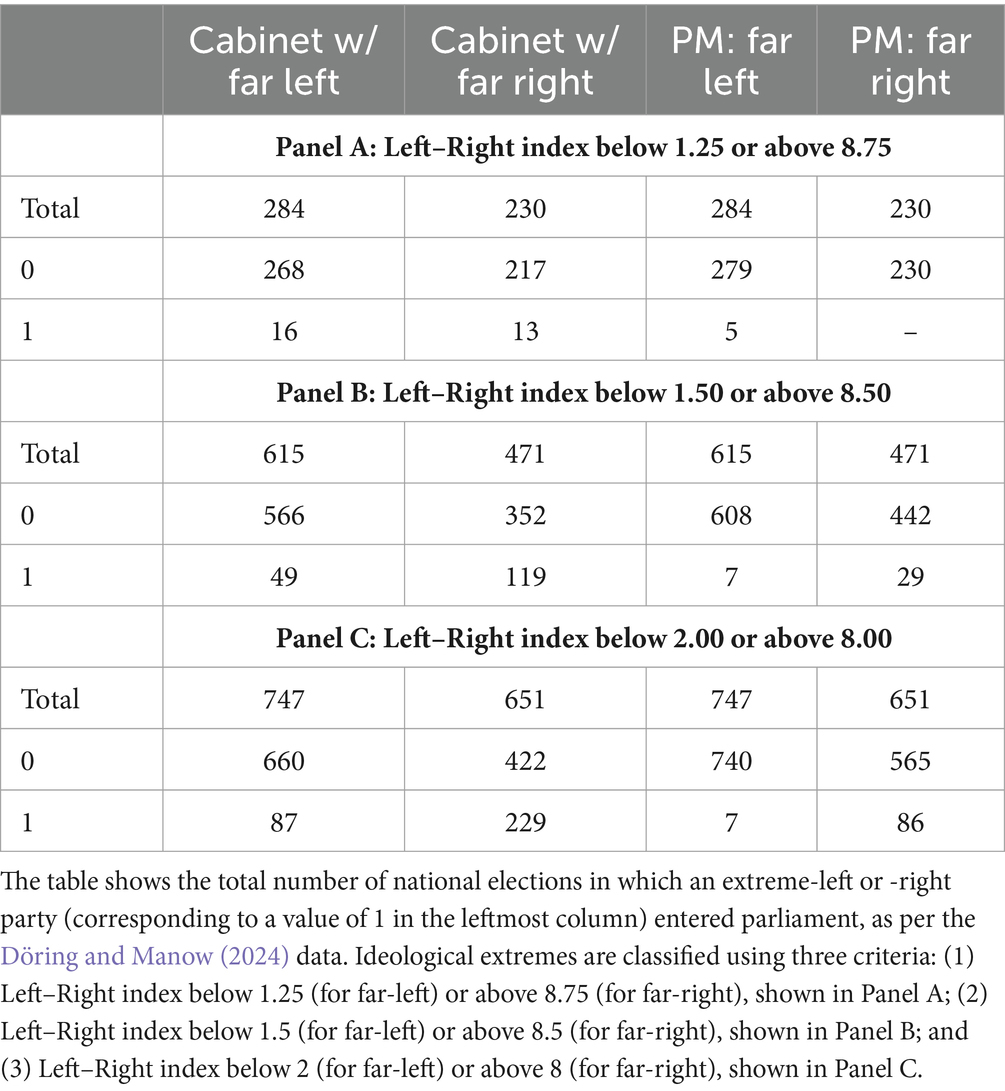

Table 1. Country and year of national parliamentary elections coverage in Döring and Manow (2024).

The data set contains 12,659 election outcomes for any party elected at national parliamentary elections. For 11,294 of them, the data set maps the elected party to its ideological affiliation using a 10-point left–right scale, where 0 is the far-left, and 10 is the far-right. The ideological position of each party, which extends to its leader as well, is calculated as the simple average of scores assigned to those in four earlier studies of party positions and spaces: Castles and Mair (1984), Huber and Inglehart (1995), Benoit and Laver (2006), and Bakker et al. (2015). Then, episodes of fer-left and far-right parties who ended up in government or produced a prime minister are listed in Table 2.

Table 2. Parliamentary representation and cabinets with extreme parties.

To measure if a party or, by extension, its PM shares an extreme ideology, we place it on an ideological scale ranging from 0 to 10, and separate it from the centrist parties. The separation thresholds in the original Castles and Mair (1984, p. 87) definition are such that a party would be classified as far-left if its ideological position is scored up to 1.25, and as far-right if its score is at least 8.75. The original scores are used in Panel A to create the initial distribution of populist and non-populist episodes in the sample.

The original definition, however, is somewhat restrictive and does not allow estimation of the above model as we do not see many extreme politicians in government belonging to those parties. For example, Germany’s AfD is positioned at 8.7, which is just short of a far-right party. Few would dispute that it is indeed a far-right party. Similarly, the Communist Party of Greece has an index of 1.253, just short of entering the far-left spectrum. The restrictiveness of this classic definition is seen in Panel A, which does not feature any far-right prime-ministers. Therefore, to allow estimation, we relax the original definition by as little as 0.25 index points on each extreme end to include parties on the very fringe of the classic extreme, which would tip parties like AfD into the extreme spectrum.

As seen in Panel B, this raises the number of episodes of populist governance, but not significantly. This is particularly valid when it comes to extreme left PMs. Using this slight modification of the original definition, we still operate with as few as 7 instances of far-left PMs and 29 instances of far-right PMs even before we merge the data with any observations of government debt. In turn, any estimates would heavily depend on particular episodes of elected populists, which may not generalize well beyond the specific episode.

To address this, we ultimately run the model using the data in Panel C, where far-left parties are positioned below 2 on the Left–Right scale, and Far-Right parties are positioned above 8. Note that even this definition may not be inclusive enough. For example, Hungary’s Fidesz party—the party Victor Orbán presides over—is positioned at 6.54, which is comfortably within the center-right spectrum; Italy’s Northern League, with its 7.80 score, is short of being classified as far-right; and UK’s Independence Party led by Nigel Farage sits at 7.84, some distance from where it realistically belongs.

Relaxing the definition of what an extreme party is still allows for observing just 7 Far-left PMs, but the number of Far-right PMs has increased significantly. So did the number of cabinets formed with the help of extreme parties, as seen in Panel C of Table 2. This limits the dependence of estimation results on any single observation and is therefore the classification we use for the benchmark estimations of the potential impact of extreme governance on fiscal outcomes.

The data on fiscal outcomes from the Global Debt Database is the second element we need to estimate Equation 1. The original methodology to collect this data has been published in Mbaye et al. (2018). The updated version of the data is available as IMF (2024), which is the version used here.1

The data set covers a variety of public and private debt indicators spanning the period between 1950 and 2022 for most economies EU and OECD economies observed in the Döring and Manow (2024) data. Two main outcome variables are used in the estimation: (i) The level of central government (CG) debt, which measures the total stock of debt liabilities issued by the central government, expressed as a share of GDP, and (ii) The general government (GG) debt, which is the total stock of debt liabilities issued by the general government, including the central government, public companies as well as private debt guaranteed by the central government, expressed as a share of GDP.

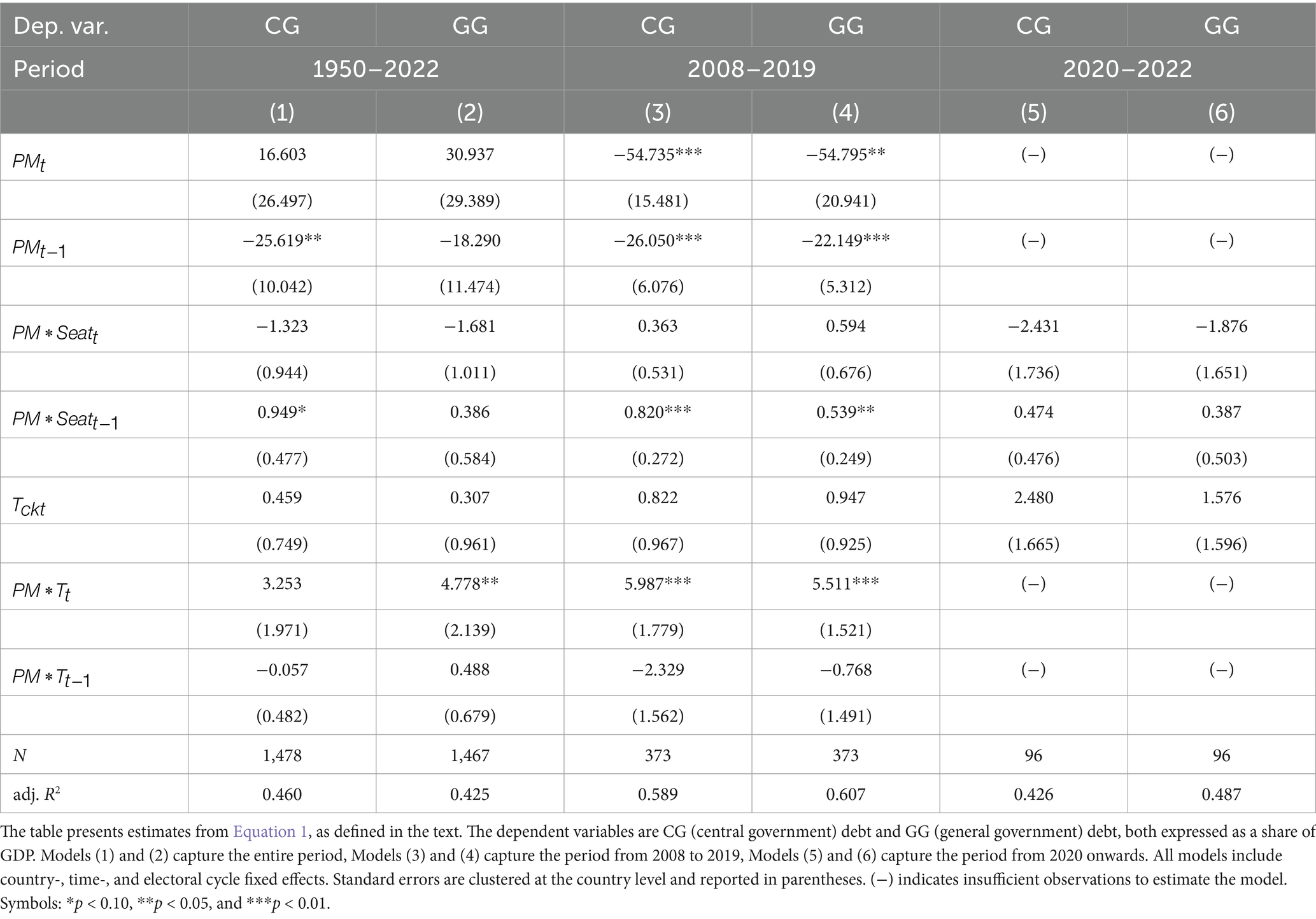

Table 3 presents estimates of Equation 1 for extreme left government in three periods: (1) 1950–2022, which spans the entire sample period; (2) 2008–2019, which spans the period from the start of the global financial crisis (GFC) to the last year before the COVID-19 pandemic; (3) 2020–2022, which should, in theory gives us an idea if COVID-19 has changed the way far-left governments approach government spending during and after the pandemic.

Table 3. Government debt with far-left prime ministers.

The key parameter of interest here is the one estimating the correlation between a far-left PM and government debt. Columns (1) and (2) provide evidence that far-left PMs in Europe and the OECD do not govern in a way that significantly raises government debt. Although positive, the estimates are insignificant. This may be because in a longer-term populist cycle, an economy optimally fluctuates between an over-spending and austerity cycles (Dovis et al., 2016), which are mutually exclusive in the longer-term. It could also be because there is no underlying causal relationship between far-left governance and government debt in the long run in the sample.

It could be possible to identify a relationship in a shorter time frame. We see this in the following 4 columns. The table provides some tentative notion that the GFC—but not COVID-19—changed the way far-left politicians in Europe and the OECD approach government spending. This is seen from columns (3) and (4). With large and statistically significant coefficients, it would be tempting to interpret these estimates as a sign that far-left PMs subscribe to the austerity principles so dominant in the aftermath of the GFC. However, let us bear in mind that with 7 far-left PMs, it is easy to have this correlation over-estimated as any single episode has an outsized impact on the overall correlation coefficient. Note that an estimation of the effect for the period during and after COVID-19 is almost entirely impossible with the current data, as there are not enough observations to perform the estimation in the first place.

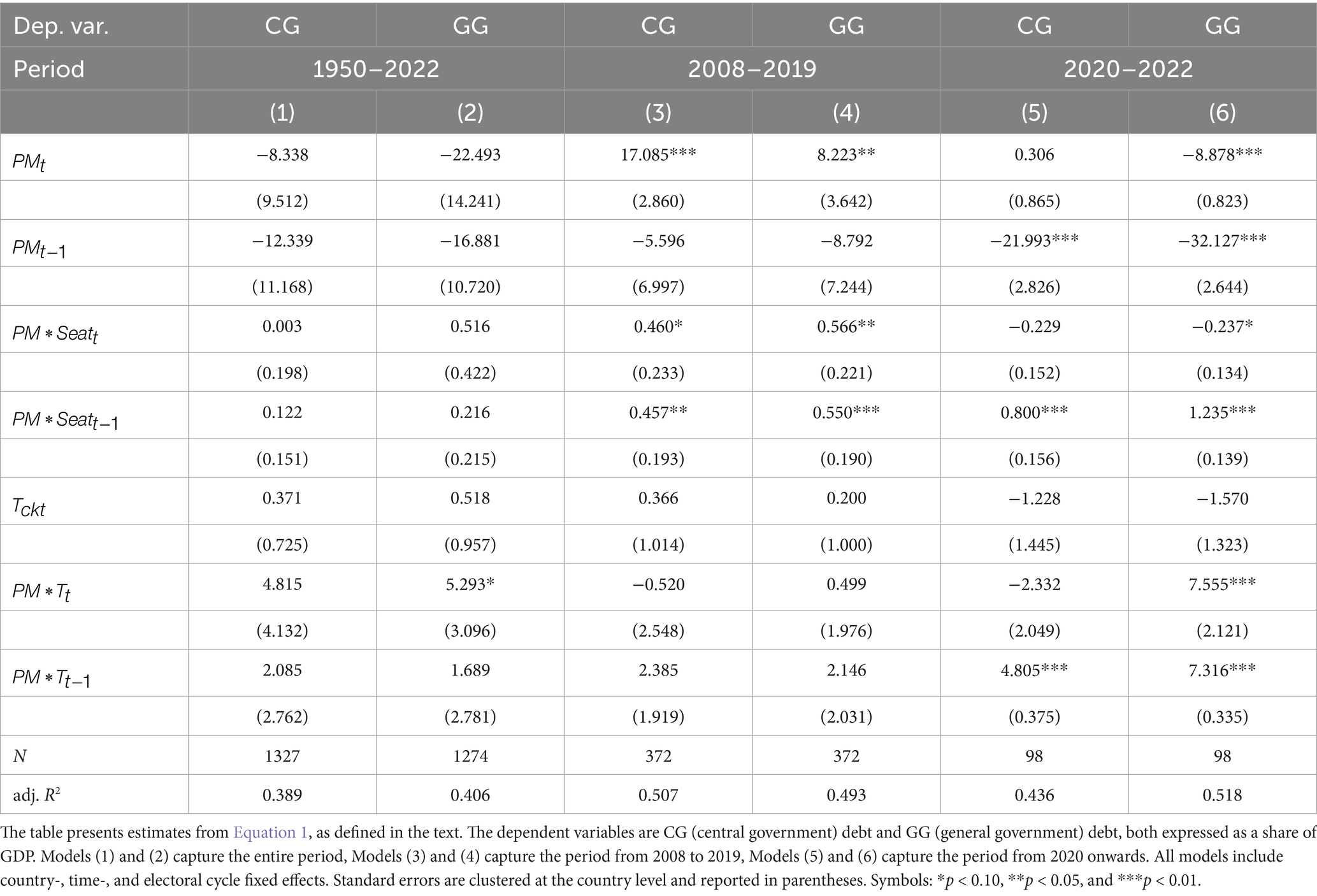

This is not the case with far-right governments, where we do have enough observations to perform estimations for all three periods. The estimates are seen in Table 4. Just like far-left governments, far-right governments do not normally have an impact on government debt that is too different from mainstream governments. This is seen in Columns (1) and (2), which present estimates for the entire period under consideration.

Table 4. Government debt with far-right prime ministers.

Unlike far-left governments, however, far-right ones have increased government debt in the aftermath of GFC. This would be counter-intuitive in the context of a Dornbusch and Edwards (1990) populist paradigm where far-left governments normally raise debt levels. To explain the contradiction, we may consider the wider populist governance framework (or “populist playbook”) offered by Dalio et al. (2017). Consistent with it, we now observe tightening links between political extremism and business interests to the right of the political spectrum in 21st century not only in the United States (Skocpol and Hertel-Fernandez, 2016), but also elsewhere (Benczes and Orzechowska-Wacławska, 2024; Elsässer and Röth, 2024; Sebők and Simons, 2022). The rising political power of large businesses in the aftermath of GFC, combined with a rising number of extreme right politicians in power, may have triggered siphoning of government support to the large corporate private sector. During the COVID-19 pandemic, however, it was mostly households and smaller firms who bore the burden of the crisis. If so, this would explain why the estimates in Columns (3) and (4) are positive and significant, while those in Columns (5) and (6) are negative or insignificant.

Two similarities emerge from Tables 3, 4 on how extreme governments manage debt. First, the duration of their tenure matters: The further they are into their tenure in government, the less careful they are with government spending. This result is seen from the positive and significant estimates for in both tables and is consistent with the political business cycle theory (Brender and Drazen, 2005; Drazen, 2000; Nordhaus, 1975). Second, the size of the parliamentary majority an extreme government operates with matters as well: A larger parliamentary majority typically means that extreme governments are less careful with borrowing. This is indicated by the positive and significant interaction terms for . This could be because they have a larger number of constituencies to cater to, or because they enjoy fewer political constraints, both in line with political economy of fiscal policy (Meltzer and Richard, 1981; Persson and Tabellini, 1999; Scartascini and Crain, 2021, among others). Either way, this implies that extreme governments in Europe and the OECD may be more mainstream than we think, at least in the way they manage government debt.

Two sensitivity checks were conducted to ensure the results do not critically depend on either the definition of extreme ideologies and its measurement, or specific episodes of populist governance. In the first one, the more restrictive definition of populist governance was used, where far-left ideology corresponded to a Left–Right index not greater than 1.5, while the far-right ideology corresponded to a Left–Right index of at least 8.5. The results for the duration of tenure in office came out slightly stronger for both the far-left and far-right PMs, as well as the results for the post-COVID reduction in debt for far-right PMs. The results remained broadly unchanged otherwise.

In the second robustness check, Japan was dropped from the sample as it has been almost continuously ruled by the Liberal Democratic Party (LDP) since 1955. The LDP has an ideological score of 8.02, which places it within the far-right spectrum according to the baseline definition, and within the center-right spectrum, according to the more restrictive definition of extremes. The fact that it has ruled for the vast majority of Japanese post-war history and that it is on the edge of the far-right spectrum warranted a check whether including it had an outsized impact on the baseline results. To perform the sensitivity check, the original definition of extreme ideology was used, but Japan was excluded from the sample. Without Japan, the main message changed little for far-right populist governance: Debt increased with the size of the majority and the duration of tenure, as expected, as it was not very different from how centrist politicians typically manage government debt.

Three mechanisms may explain this seemingly surprising result. First, fiscal rules and checks and balances embedded in the democratic process in Europe and the OECD countries make bad governance punishable in the following elections. This may drive irrational spending sub-optimal in the eyes of core constituencies, placing a break on debt expansion. Second, most populists in Europe and the OECD have so far been allocated junior coalition roles, limiting their potential damage on policy design and implementation. If this changes, we may still witness their detrimental effect on government finance over prolonged periods beyond the decade following the GFC, similar to their well-established damaging and lasting impact on the rule of law and civic society. Third, the parliamentary democracies studied in this work may operate differently from the presidential regimes that have dominated existing evidence. This could be one of the reasons for the known differences between the European populists and those elsewhere (Mudde and Rovira Kaltwasser, 2013). This difference in their modus operandi may have created a bias in the existing evidence on populist governance toward over-representation of presidential systems. As presidential regimes often face weaker executive constraints to the ones governments operate with in parliamentary democracies (Carey, 2005; Cheibub and Limongi, 2002; Moe and Caldwell, 1994; North and Weingast, 1989), over-representing them in previous research may have over-estimated the impact of populist governance on government debt. Including parliamentary democracies in this evidence may mitigate this result. The rest of the conclusions are presented below.

Populists openly dislike the rules of the game and undermine them using toxic rhetoric, at least until they come to power. However, reality does not always match their toxic rhetoric, at least in Europe and the OECD. Indeed, Trump has engaged in a trade war with major trading partners, biased the US Supreme Court for decades to come, supported autocrats in their barbaric territorial expansions, taking quite some shine off the City on the Hill; Farage has finally compelled the UK out of the EU and has emerged from the British political fringe to enter national parliament, in his 8th attempt; Le Pen may still one day wake up as a French president; and Orbán et al. will keep undermining the values of liberal democracy and plant discord among European nations for some time to come. All this will undoubtedly deliver quality entertainment to their comrades in the Kremlin, with whom they seem to enjoy ‘a very special relationship’, successfully upending the decades-old post-war order. Therefore, few will dispute that populist governance in Europe and the OECD undermines the state of liberal democracy, rule of law and civil society in the 21st century just as much as it did in the 20th century.

However, when it comes to managing government finances, European populists seem to have done their homework and appear less damaging. This is because we cannot see the expected long-term rise in government debt concurrent with populist governance in Europe and the OECD, in line with the economic populism elsewhere. Three mechanisms may contribute to this effect. First, fiscal rules and checks and balances embedded in the democratic process in those countries make bad governance punishable in the following elections. Second, most populists in Europe and the OECD have so far been allocated junior coalition roles, limiting their potential damage on policy design and implementation. Observing more cases of extreme politicians in power may still change this result. Third, the parliamentary democracies studied in this work may operate differently from the presidential regimes that have dominated previous empirical evidence. In short, most of the evidence in this work points to a relatively small long-term effect of populist governance on public debt in Europe and the OECD.

It appears that populists in Europe and the OECD exert an outsized political impact without leaving a lasting damage to the economy. Their political impact, however, may be about to wane as well. Broadly speaking, Europe is gradually slipping through the Kremlin’s oily fingers. If and when it finally decouples from its perilous dependence on Russia’s snake oil, the path to restoring political stability and mainstream politics in Europe and the OECD will be open. In anticipation of this moment, the time is now to define new mainstream policies. A new social consensus fitting the realities of the 21st century needs to be at the heart of this new definition of mainstream, so that our divided world makes its distant ends meet somewhere in the elusive middle. The last time this was done in Western Europe was in the wake of WWII and it led to more than half a century of peace and prosperity on the continent for the people, by the people. The same prosperity inspired the rest of the world to follow into the footsteps of liberal democracy and sound economics, at least until China and Russia, not without the recent boost in confidence from Washington, decided it was time to redraft the post-war order.

Perhaps this time around, and hopefully without a new global conflict, mainstream policies have a chance to evolve into something a bit more benignly populist just like they did in the wake of WWII. This can hopefully happen before the extreme rhetoric—and worse, the reality that chases it—normalizes and morphs into a new mainstream populism. You may call it democracy’s survival instinct or its embedded self-correction mechanism. Either way, it may well be the last chance to redefine classic mainstream policies to save ourselves from the perils of 20th century populism and authoritarianism. This paper has shown that extreme politicians may be learning how to do some sound policies right, particularly when it comes to managing government finances. For their own political longevity and the survival of liberal democracy as we know it, it may be time for mainstream politicians to take a page from the populist playbook as well.

The original contributions presented in the study are included in the article/supplementary material. Replication guidance is available at https://doi.org/10.17632/ff6tbnjm9x.1.

PS: Conceptualization, Data curation, Formal analysis, Investigation, Methodology, Validation, Visualization, Writing – original draft, Writing – review & editing.

The author declares that no financial support was received for the research and/or publication of this article.

I thank the Special Issue editor and the three reviewers for helpful comments and suggestions.

The author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

The author declares that no Gen AI was used in the creation of this manuscript.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

1. ^The data used in the estimation has been downloaded on 18/10/2024. Any updates to the data since the original download may affect the estimation results in subsequent replication. To replicate the baseline results here, please see the code and guidance to downloading the data here: http://doi.org/10.17632/ff6tbnjm9x.1

Absher, S., Grier, K., and Grier, R. (2020). The economic consequences of durable left-populist regimes in Latin America. J. Econ. Behav. Organ. 177, 787–817. doi: 10.1016/j.jebo.2020.07.001

Acemoglu, D., Naidu, S., Restrepo, P., and Robinson, J. A. (2019). Democracy does cause growth. J. Polit. Econ. 127, 47–100. doi: 10.1086/700936

Bakker, R., de Vries, C., Edwards, E., Hooghe, L., Jolly, S., Marks, G., et al. (2015). Measuring party positions in Europe: the Chapel Hill expert survey trend file, 1999–2010. Party Polit. 21, 143–152. doi: 10.1177/1354068812462931

Ball, C., Freytag, A., and Kautz, M. (2019). “Populism-what next? A first look at populist walking-stick economies” in CESifo Working Paper Series 7914 (CESifo Group: Munich).

Benczes, I., and Orzechowska-Wacławska, J. (2024). Governing the economy under populist rule: the cases of Hungary and Poland. Prob. Post-Commun. 71, 341–355. doi: 10.1080/10758216.2023.2301085

Benoit, K., and Laver, M. (2006). “Party policy in modern democracies” in Routledge research in comparative politics (New York, NY: Routledge).

Blakeslee, D. S. (2018). Politics and public goods in developing countries: evidence from the assassination of Rajiv Gandhi. J. Public Econ. 163, 1–19. doi: 10.1016/j.jpubeco.2017.12.011

Bonikowski, B., Halikiopoulou, D., Kaufmann, E., and Rooduijn, M. (2019). Populism and nationalism in a comparative perspective: a scholarly exchange. Nations Nationalism 25, 58–81. doi: 10.1111/nana.12480

Brender, A., and Drazen, A. (2005). Political budget cycles in new versus established democracies. J. Monet. Econ. 52, 1271–1295. doi: 10.1016/j.jmoneco.2005.04.004

Brewer-Carías, A. (2010). Dismantling democracy in Venezuela: The Chávez authoritarian experiment. Cambridge, UK: Cambridge University Press.

Cachanosky, N., and Padilla, A. (2020). A panel data analysis of Latin American populism. Constit. Polit. Econ. 31, 329–343. doi: 10.1007/s10602-020-09302-w

Caiani, M., and Della Porta, D. (2011). The elitist populism of the extreme right: a frame analysis of extreme right-wing discourses in Italy and Germany. Acta Polit. 46, 180–202. doi: 10.1057/ap.2010.28

Campos, L., and Casas, A. (2021). Rara Avis: Latin American populism in the 21st century. Eur. J. Polit. Econ. 70:102042. doi: 10.1016/j.ejpoleco.2021.102042

Carey, J. M. (2005). “Presidential versus parliamentary government” in Handbook of new institutional economics. eds. C. Ménard and M. M. Shirley (Berlin, Heidelberg: Springer), 91–122.

Castles, F. G., and Mair, P. (1984). Left-right political scales: some 'expert' judgments. Eur J Polit Res 12, 73–88. doi: 10.1111/j.1475-6765.1984.tb00080.x

Cheibub, J. A., and Limongi, F. (2002). Democratic institutions and regime survival: parliamentary and presidential democracies reconsidered. Annu. Rev. Polit. Sci. 5, 151–179. doi: 10.1146/annurev.polisci.5.102301.084508

Colburn, F. D. (2011). Dismantling democracy in Venezuela: the Chávez authoritarian experiment. Perspect. Polit. 9, 733–734. doi: 10.1017/S1537592711002295

Dalio, R., Kryger, S., Rogers, J., and Davis, G. (2017). Populism: The phenomenon. Technical Report 3/22/2017: Bridgewater Associates, LP.

De la Torre, C., and Lemos, A. O. (2016). Populist polarization and the slow death of democracy in Ecuador. Democratization 23, 221–241. doi: 10.1080/13510347.2015.1058784

De Vries, C. E., and Edwards, E. E. (2009). Taking Europe to its extremes: extremist parties and public Euroscepticism. Party Polit. 15, 5–28. doi: 10.1177/1354068808097889

Denisova, A. (2017). Democracy, protest and public sphere in Russia after the 2011–2012 anti-government protests: digital media at stake. Media Cult. Soc. 39, 976–994. doi: 10.1177/0163443716682075

Döring, H., and Manow, P. (2024). ParlGov 2024 release (version 1) [data set]. Harvard Dataverse. doi: 10.7910/DVN/2VZ5ZC

Dornbusch, R., and Edwards, S. (1990). Macroeconomic populism. J. Dev. Econ. 32, 247–277. doi: 10.1016/0304-3878(90)90038-D

Dovis, A., Golosov, M., and Shourideh, A. (2016). Political economy of sovereign debt: a theory of cycles of populism and austerity. Working Paper No. 21948. National Bureau of Economic Research.

Drazen, A. (2000). The political business cycle after 25 years. NBER Macroecon. Annu. 15, 75–117. doi: 10.1086/654407

Dussauge-Laguna, M. I. (2022). The promises and perils of populism for democratic policymaking: the case of Mexico. Policy. Sci. 55, 777–803. doi: 10.1007/s11077-022-09469-z

Edwards, S. (2019). On Latin American populism, and its echoes around the world. J. Econ. Perspect. 33, 76–99. doi: 10.1257/jep.33.4.76

Elsässer, L., and Röth, L. (2024). Fiscal implications of the populist radical right in power. J. Eur. Publ. Policy 32, 697–726. doi: 10.1080/13501763.2024.2314248

Freedom House (2018). Freedom in the world, 1973–2018. Available online at: https://freedomhouse.org/report/freedom-world.

Funke, M., Schularick, M., and Trebesch, C. (2023). Populist leaders and the economy. Am. Econ. Rev. 113, 3249–3288. doi: 10.1257/aer.20202045

Gandesha, S. (2018). “Understanding right and left populism” in Critical theory and authoritarian populism. ed. J. Morelock (London: University of Westminster Press), 49–70.

Gavin, M., and Manger, M. (2023). Populism and De facto central Bank Independence. Comp. Pol. Stud. 56, 1189–1223. doi: 10.1177/00104140221139513

Grier, K., and Maynard, N. (2016). The economic consequences of Hugo Chavez: a synthetic control analysis. J. Econ. Behav. Organ. 125, 1–21. doi: 10.1016/j.jebo.2015.12.011

Guimarães, F. D. S., and Dutra De Oliveira E Silva, I. (2021). Far-right populism and foreign policy identity: Jair Bolsonaro's ultra-conservatism and the new politics of alignment. Int. Aff. 97, 345–363. doi: 10.1093/ia/iiaa220

Hartwell, C. (2022). Populism and financial markets. Financ. Res. Lett. 46:102479. doi: 10.1016/j.frl.2021.102479

Hinnebusch, R. (2020). The rise and decline of the populist social contract in the Arab world. World Dev. 129:104661. doi: 10.1016/j.worlddev.2019.104661

Huber, J., and Inglehart, R. (1995). Expert interpretations of party space and party locations in 42 societies. Party Polit. 1, 73–111.

Hunter, W., and Power, T. J. (2019). Bolsonaro and Brazil's illiberal backlash. J. Democr. 30, 68–82. doi: 10.1353/jod.2019.0005

IMF. (2024). Global debt database (2024 release). International Monetary Fund. Available online at: https://www.imf.org/external/datamapper/datasets/GDD.

Jordà, O., Schularick, M., and Taylor, A. M. (2017). “Macrofinancial history and the new business cycle facts” in NBER macroeconomics annual. eds. M. Eichenbaum and J. A. Parker, vol. 31 (Chicago, IL: University of Chicago Press), 213–263.

Kendall-Taylor, A., Lindstaedt, N., and Frantz, E. (2019). Democracies and authoritarian regimes. Oxford, UK: Oxford University Press.

Marshall, M. G., Gurr, T. R., and Jaggers, K. (2019). Polity IV project. Political regime characteristics and transitions, 1800–2018. Available online at: http://www.systemicpeace.org/inscrdata.html.

Masciandaro, D., and Passarelli, F. (2020). Populism, political pressure and central bank (in)dependence. Open Econ. Rev. 31, 691–705. doi: 10.1007/s11079-019-09550-w

Mbaye, S., Moreno-Badia, M., and Chae, K. (2018). Global debt database: Methodology and sources (IMF working paper no. 2018/111). International Monetary Fund. Available online at: https://www.imf.org/en/Publications/WP/Issues/2018/05/14/Global-Debt-Database-Methodology-and-Sources-45838.

Meltzer, A. H., and Richard, S. F. (1981). A rational theory of the size of government. J. Polit. Econ. 89, 914–927. doi: 10.1086/261013

Meyer, B. (2024, 2024). “Populist rhetoric and central Bank Independence, Chapter 3” in The ideational approach to populism, volume: Consequences and mitigation. eds. A. Chryssogelos, E. T. Hawkins, K. A. Hawkins, L. Littvay, and N. Wiesehomeier. 1st ed (London, UK: Routledge).

Moe, T. M., and Caldwell, M. (1994). The institutional foundations of democratic government: a comparison of presidential and parliamentary systems. J. Inst. Theor. Econ. 150, 171–195. http://www.jstor.org/stable/40753031

Mudde, C. (2004). The populist zeitgeist. Gov. Oppos. 39, 541–563. doi: 10.1111/j.1477-7053.2004.00135.x

Mudde, C. (2016). Europe’s populist surge: a long time in the making. Foreign Aff. 95, 25–30. Available at: https://www.jstor.org/stable/43948378

Mudde, C., and Rovira Kaltwasser, C. (2013). Exclusionary vs. inclusionary populism: comparing contemporary Europe and Latin America. Gov. Oppos. 48, 147–174. doi: 10.1017/gov.2012.11

Mudde, C., and Rovira Kaltwasser, C. (2017). Populism: A very short introduction. Oxford, UK: Oxford University Press.

Nordhaus, W. D. (1975). The political business cycle. Rev. Econ. Stud. 42, 169–190. doi: 10.2307/2296528

Norris, P., and Inglehart, R. (2019). Cultural backlash: Trump, Brexit, and authoritarian populism. Cambridge: Cambridge University Press.

North, D. C., and Weingast, B. R. (1989). Constitutions and commitment: the evolution of institutions governing public choice in seventeenth-century England. J. Econ. Hist. 49, 803–832. doi: 10.1017/S0022050700009451

Persson, T., and Tabellini, G. (1999). The size and scope of government: comparative politics with rational politicians. Eur. Econ. Rev. 43, 699–735. doi: 10.1016/S0014-2921(98)00131-7

Rode, M., and Revuelta, J. (2015). The wild bunch! An empirical note on populism and economic institutions. Econ. Gov. 16, 73–96. doi: 10.1007/s10101-014-0154-5

Rodríguez-Pose, A., and Dijkstra, L. (2021). Does cohesion policy reduce EU discontent and euroscepticism? Reg. Stud. 55, 354–369. doi: 10.1080/00343404.2020.1826040

Rooduijn, M., and Akkerman, T. (2015). Flank attacks: populism and left-right radicalism in Western Europe. Party Polit. 23, 193–204. doi: 10.1177/1354068815596514

Rovira Kaltwasser, C., Taggart, P., Ochoa Espejo, P., and Ostiguy, P. (2017). “Populism: an overview of the concept and the state of the art” in The Oxford handbook of populism, Chapter 1. eds. P. O. Espejo, P. A. Taggart, C. R. Kaltwasser, and P. Ostiguy (Oxford, UK: Oxford University Press).

Sachs, J. (1989). Social conflict and populist policies in Latin America. NBER Working Paper 2897. Available online at: https://www.nber.org/papers/w2897.

Scartascini, C. G., and Crain, W. M. (2021). “The size and composition of government spending in multi-party systems” in Essays on government growth. eds. J. Hall and B. Khoo, Studies in public choice, vol. 40 (Cham, Switzerland: Springer), 127–147.

Sebők, M., and Simons, J. (2022). How Orbán won? Neoliberal disenchantment and the grand strategy of financial nationalism to reconstruct capitalism and regain autonomy. Soc. Econ. Rev. 20, 1625–1651. doi: 10.1093/ser/mwab052

Skocpol, T., and Hertel-Fernandez, A. (2016). The Koch network and republican party extremism. Perspect. Polit. 14, 681–699. doi: 10.1017/S1537592716001122

Stankov, P. (2017). “Crises, welfare, and populism” in Economic freedom and welfare before and after the crisis (Cham: Springer International Publishing), 135–164.

Stankov, P. (2018). The political economy of populism: an empirical investigation. Comp. Econ. Stud. 60, 230–253. doi: 10.1057/s41294-018-0059-3

Stanley, B. (2008). The thin ideology of populism. J. Polit. Ideol. 13, 95–110. doi: 10.1080/13569310701822289

Taggart, P., and Rovira Kaltwasser, C. (2016). Dealing with populists in government: some comparative conclusions. Democratization 23, 345–365. doi: 10.1080/13510347.2015.1076230

Keywords: fiscal policy, populism, populist governance, far-left, far-right, government debt

Citation: Stankov P (2025) Frugal populists: fiscal management under populist rule in Europe and the OECD. Front. Polit. Sci. 7:1565020. doi: 10.3389/fpos.2025.1565020

Edited by:

John Eaton, Florida Gateway College, United StatesReviewed by:

Pedro Mundim, Universidade Federal de Goiás, BrazilCopyright © 2025 Stankov. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Petar Stankov, cGV0YXIuc3RhbmtvdkByaHVsLmFjLnVr

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.