Jiefei Zhang

Jiefei Zhang Kexin Ge

Kexin Ge Li Wang

Li Wang

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 11 April 2025

Sec. Environmental Economics and Management

Volume 13 - 2025 | https://doi.org/10.3389/fenvs.2025.1543949

Our study moves beyond conventional constraints that primarily examine patent counts, establishing a novel conceptual framework that comprehensively synthesizes dual dimensions—both the volume and caliber of environmental innovations—in the aftermath of environmental taxation implementation. In contrast to prior scholarship, this investigation extends past the mere assessment of policy-driven innovation promotion, conducting an in-depth examination of how environmental fiscal measures reconfigure innovation architecture and elevate innovation excellence. Using a comprehensive panel dataset of Chinese A-share listed companies from 2012 to 2022, we employ a difference-in-differences methodology with multiple robustness checks to establish causal relationships. Our findings reveal three key insights: First, contrary to the Porter Hypothesis, EPT implementation shows a negative correlation with green innovation activities in pollution-intensive sectors, particularly pronounced among private enterprises, smaller firms, and highly competitive markets. Second, the tax policy demonstrates asymmetric effects across patent categories, predominantly constraining invention patents while having a lesser impact on utility models. Third, while the aggregate volume of environmental patent applications decreases, we document a significant improvement in mean innovation quality, especially in utility model patents. The quality-enhancement effect strengthens over time, even as the quantity-reducing impact gradually attenuates. Through detailed mechanism analysis, we identify corporate liquidity constraints and reduced R&D expenditure as primary channels through which EPT affects innovation outcomes. These findings contribute to the theoretical discourse on environmental regulation and corporate innovation by highlighting the quality-quantity trade-off in green innovation responses to environmental taxation. Our results provide important policy implications for optimizing environmental fiscal instruments to promote sustainable technological advancement while maintaining innovation quality.

The nexus between environmental regulation and corporate ecological innovation has emerged as a critical research domain amid intensifying global environmental challenges. Environmental taxation, as a market-based regulatory mechanism, holds particular significance in stimulating sustainable technological advancement. The theoretical foundation, rooted in endogenous growth theory, was substantively advanced by Acemoglu et al. (2016), who constructed a dual-sector framework encompassing clean and pollution-intensive technologies. Their model demonstrates how calibrated environmental levies and research incentives can reorient corporate innovation trajectories toward sustainable technologies. Empirical validation of this theoretical frame-work has emerged through various studies. Research by Calel and Dechezleprêtre (2016) documented a 10% increase in low-carbon innovation among firms regulated under the EU Emissions Trading System. Similarly, Sharif et al. (2023) confirmed the positive correlation between environmental fiscal measures and ecological technological advancement in ASEAN nations. However, contrasting perspectives exist, as evidenced by Stucki et al. (2018), whose analysis of Central European firms suggests regulatory constraints may impede eco-friendly product development.

Given China’s prominence as the world’s second-largest economic entity and principal carbon contributor, its environmental governance strategies hold considerable exemplary value for global policy discourse. The nation’s transition from pollution charges to a comprehensive environmental tax regime in 2018 constitutes an unprecedented policy experiment for examining the interplay between fiscal environmental instruments and corporate ecological innovation. Contemporary scholarship examining this policy transformation has yielded heterogeneous findings, predominantly concentrating on quantitative patent metrics. Empirical evidence from Zhao et al. (2022), derived from emission-intensive sectors within China’s A-share market, indicates that ecological taxation catalyzes innovative activities while generating positive economic externalities. This finding aligns with Deng et al. (2023), who document increased R&D allocation in response to environmental fiscal measures. Conversely, Wang S. et al. (2023) present contradictory evidence, suggesting a dampening effect on ecological innovation initiatives. A notable limitation in existing research lies in its disproportionate emphasis on patent volume metrics, overlooking qualitative dimensions. Song et al. (2020) highlight the inherent heterogeneity in patent significance, while Li and Zheng (2016) underscore the superior value generation potential of high-caliber innovations. Consequently, a holistic evaluation framework incorporating both quantitative and qualitative patent indicators becomes imperative for robust policy assessment and refinement of environmental fiscal mechanisms.

A comprehensive examination of the literature reveals five distinct dimensions relevant to this investigation. The theoretical discourse regarding environmental taxation’s influence on innovation has evolved into two contrasting schools of thought. The first theoretical framework, embodied in the seminal work of Porter and Linde (1995), introduces the concept of “innovation-induced compensation,” suggesting that strategically implemented environmental regulations can catalyze technological advancement, optimize resource efficiency, and generate benefits exceeding regulatory compliance expenditures. This conceptual foundation has undergone substantial evolution. Through general equilibrium analysis, Goulder and Schneider (1999) elucidated the mechanisms through which carbon taxation reallocates research resources toward emission-reduction technologies. Subsequently, Popp (2002) furnished empirical substantiation of the correlation between energy cost escalation and efficiency-focused patent development. Acemoglu et al. (2012) further advanced this understanding by constructing a dual-sector endogenous growth framework encompassing both environmentally benign and harmful technologies, demonstrating the synergistic potential of coordinated environmental taxation and research incentives.

The alternative perspective, grounded in neoclassical economics, emphasizes the “resource displacement hypothesis.” Palmer et al. (1995) contested the Porter framework, emphasizing the burden of regulatory compliance on corporate innovation capacity. Jaffe et al. (2005) synthesized extensive literature documenting how market imperfections may cause environmental levies to constrain rather than facilitate innovation. The research by Hall and Lerner (2010) highlighted the critical dependence of innovation funding on internal financial resources, suggesting potential innovation constraints from environmental compliance requirements. Dechezleprêtre and Sato (2017) elaborated on the immediate economic implications, particularly for resource-intensive sectors.

In reconciling these divergent perspectives, Ambec et al. (2013) identified multiple contingent factors mediating regulatory impacts on innovation, including implementation mechanisms, regulatory frameworks, organizational characteristics, and competitive dynamics. Calel and Dechezleprêtre (2016) emphasized the significance of policy architecture, market conditions, and technological evolution in determining outcomes. Popp et al. (2010) introduced the concept of “bifurcated effects,” acknowledging simultaneous stimulation and suppression across different innovation domains. This theoretical foundation illuminates the multifaceted relationship between environmental taxation and innovation outcomes.

Contemporary empirical investigations have yielded substantial insights. Analysis of the EU ETS framework has proven particularly instructive, with Calel and Dechezleprêtre (2016) documenting a substantial increase in environmental innovation among regulated entities. Martin et al. (2016) identified differential impacts across organizational scales and sectors. In the automotive sector, Aghion et al. (2016) demonstrated the relationship between fuel costs and clean technology innovation, while accounting for organizational and systemic factors. Calel (2020) identified distinct mechanisms of technology adoption and development. Recent work by Rastegar et al. (2024) documented significant increases in sustainable energy innovation across developed economies.

The qualitative dimension of innovation remains comparatively unexplored. While Squicciarini et al. (2013) established methodological frameworks for innovation quality assessment, their application to environmental policy analysis remains limited. Popp et al. (2010) suggested a predisposition toward incremental rather than transformative innovation under environmental regulation. Ley et al. (2016) established quantitative relationships between energy costs and both the volume and relative proportion of environmental innovations.

Examining the implementation of environmental protection taxation within China’s regulatory framework reveals that scholarly attention has predominantly centered on quantitative measures of eco-innovation outcomes. A substantial body of empirical evidence supports the policy’s efficacy in stimulating environmental innovation. Provincial-level analysis by Liu Q. et al. (2022) demonstrates enhanced regional eco-patent activity following tax implementation. Municipal-level investigations by Guo et al. (2022) corroborate these findings through urban innovation metrics. Sector-specific research by Huang et al. (2022) documents elevated environmental patent acquisition among high-emission enterprises, while Liu and Xiao (2022) identify increased proportional representation of environmental patents within manufacturing entities’ intellectual property portfolios. Contrasting perspectives emerge from alternative empirical investigations. Wang S. et al. (2023) document diminished environmental patent procurement among publicly traded non-financial entities, while Zhao Z. et al. (2024) identify particularly pronounced negative effects on qualitative innovation metrics within the manufacturing sector. The relationship’s complexity is further illuminated by investigations revealing non-monotonic patterns. Wei et al. (2023) identifies curvilinear dynamics in process innovation, characterized by initial stimulation followed by subsequent decline at elevated tax thresholds. Jiang et al. (2023) documents transitional innovation responses, with initial suppression yielding to enhanced activity as taxation intensifies.

Mechanistic investigations have elucidated various pathways of policy influence. Liang et al. (2023) emphasizes institutional legitimacy pressures in high-emission sectors, while Lu and Zhou (2023) delineate dual pathways of legitimacy influence. Cao et al. (2024) highlights the mediating roles of digital transformation and sustainability performance metrics.

The policy’s impact exhibits substantial heterogeneity across organizational characteristics. Li and Li (2022) document differential effects based on ownership structures and geographic locations. Deng et al. (2023) reveals varying responses across organizational life cycles and market development levels. Lu and Zhou (2023) identifies distinctive patterns related to financial constraints and regional economic conditions.

Synthetic analysis of extant literature reveals four critical knowledge gaps: (1) predominant focus on quantitative metrics at the expense of qualitative innovation assessment; (2) insufficient theoretical integration of compensatory and compliance perspectives in explaining differentiated innovation outcomes; (3) limited temporal analysis of policy effects across different time horizons; and (4) incomplete evaluation of policy outcomes within China’s specific institutional context. This investigation seeks to address these limitations through development of a comprehensive analytical framework integrating qualitative and quantitative dimensions of environmental innovation outcomes.

The scholarly significance of this investigation extends across multiple dimensions: (1) This study advances beyond conventional approaches that emphasize patent volume metrics by introducing and implementing a comprehensive analytical framework integrating both qualitative excellence and quantitative dimensions of innovation, establishing fresh methodological paradigms for environmental policy assessment; (2) The research identifies previously unrecognized policy dynamics wherein environmental protection taxation exhibits dual effects: a constraining influence on innovation frequency coupled with enhancement of innovation sophistication, illuminating nuanced policy implications that prior investigations have not addressed; (3) The investigation offers granular analysis of policy impacts across diverse innovation categories (encompassing both invention patents and utility models) while examining differential responses across varied organizational characteristics; (4) Through temporal decomposition of policy effects, this study illuminates evolutionary patterns in regulatory impact, specifically documenting the progressive intensification of quality-enhancement outcomes concurrent with diminishing quantity-suppression effects, thereby contributing novel chronological insights for policy refinement. The manuscript proceeds as follows: Section 2 establishes the theoretical foundation and hypotheses development; Section 3 outlines methodological considerations; Section 4 presents core empirical findings; Section 5 explores effect heterogeneity; Section 6 offers supplementary analyses; and Section 7 concludes with policy recommendations and future research directions.

The interplay between environmental regulatory frameworks and firm-level innovation dynamics represents a fundamental research paradigm in environmental economics. Contemporary theoretical discourse is characterized by two contrasting perspectives: the dynamic efficiency approach derived from Porter’s paradigm, and the static burden hypothesis grounded in neoclassical economic theory. The Porter framework suggests that strategically designed environmental governance mechanisms can catalyze technological advancement, enhancing operational efficiency and market competitiveness, thereby generating compensatory benefits that exceed regulatory compliance expenditures (Porter and Linde, 1995). The longitudinal implications of environmental policies manifest primarily through innovative adaptations, which function as essential catalysts for environmental performance enhancement and facilitate the ecological modernization of economic systems (Lv and Guo, 2025). The implementation of eco-innovative technologies enables organizations to achieve dual objectives: minimizing resource utilization and environmental impact while optimizing operational efficiency and output quality (Guo et al., 2025). Conversely, the neoclassical paradigm prioritizes immediate cost implications, positing that despite potential societal benefits, environmental mandates impose significant private sector burdens. This framework suggests that compliance-related resource allocation constraints may impede innovation investment through resource displacement mechanisms (Wang Y. et al., 2023).

The transition from pollution charges to environmental taxation represents a fundamental shift toward more stringent regulatory enforcement with enhanced judicial authority. This policy transformation intensifies institutional pressure on emission-intensive sectors regarding environmental compliance. The immediate economic implications include elevated tax obligations and pollution mitigation costs, potentially necessitating resource reallocation away from research initiatives to maintain financial viability. Additionally, the inherent characteristics of ecological innovation - substantial capital requirements, elevated uncertainty, and extended development horizons - present significant barriers to near-term innovative output (Gong et al., 2020). Based on these theoretical considerations, we propose.

Hypothesis 1. The implementation of environmental taxation policies exhibits a negative cor-relation with green innovation metrics in pollution-intensive enterprises.

The efficacy of environmental fiscal instruments exhibits substantial heterogeneity across organizational structures, particularly between state-controlled and private entities, due to variations in resource accessibility, strategic objectives, and institutional support. Private enterprises encounter significant barriers in accessing debt and equity financing (Lu et al., 2012; Ling et al., 2024), constraining their capacity for ecological technological advancement. These entities typically emphasize profit optimization, displaying reluctance toward discretionary environmental investments under regulatory pressure (Cai et al., 2020), particularly given the limited private returns from ecological innovation (Liu et al., 2021). Conversely, state-controlled enterprises benefit from enhanced policy alignment, preferential financing channels, and robust governmental support, while private entities adopt more conservative strategies due to resource limitations (Lin and Zhang, 2023). Consequently, the implementation of environmental taxation may disproportionately constrain innovation initiatives in private enterprises.

Organizational scale emerges as another critical determinant of innovation response to environmental fiscal measures. Large-scale enterprises possess inherent advantages in absorbing policy-induced shocks. Their robust financial capabilities and sophisticated management infrastructures facilitate substantial investment in environmental compliance and research activities (Lin and Zhang, 2023). Conversely, smaller entities face significant resource constraints in pursuing ecological innovation (Huang et al., 2022; Beck and Demirguc-Kunt, 2006). Scale economies and specialized operational structures enable large enterprises to optimize production efficiencies while maintaining continuous innovation through technological reserves (Sun and Wang, 2014; Dean et al., 1998). Smaller entities often struggle with technological limitations and information asymmetries, impeding their adaptive responses to policy shifts (Long et al., 2022). Additionally, enhanced public scrutiny and regulatory oversight motivate larger enterprises to prioritize ecological innovation, enabling them to mitigate compliance costs through technological advancement (Long et al., 2022; Huang et al., 2022), while smaller entities often bear direct compliance expenses (Cheng et al., 2022). These dynamics suggest amplified innovation constraints for smaller enterprises under environmental taxation regimes.

Market structure significantly moderates the relationship between environmental regulation and innovation outcomes. Research indicates a non-linear relationship between competitive intensity and innovation propensity, with moderate competition fostering innovation while excessive competition diminishes returns (Aghion et al., 2005). The dual externalities characteristic of ecological innovation - knowledge spillovers and environmental benefits - create appropriability challenges that affect investment incentives (Liu et al., 2021). Entities in highly competitive markets face persistent market share pressures while balancing immediate profitability against sustainability objectives (Liu et al., 2021). Conversely, enterprises in concentrated markets benefit from enhanced pricing power (Su et al., 2023), superior financing capabilities (Ping and Zhou, 2007), and comprehensive industry expertise (Blundell et al., 1999), facilitating ab-sorption of regulatory costs and sustained innovation investment. This aligns with Schumpeterian growth theory, suggesting that intense competition erodes monopolistic rents necessary for sustained R&D investment (Aghion and Howitt, 1992). Empirical evidence indicates that environmental fiscal measures have diminished impact on ecological productivity in competitive sectors relative to concentrated industries (Sun et al., 2023), with concentrated sectors demonstrating superior innovation outcomes (Liu et al., 2021). Therefore.

Hypothesis 2. The negative impact of environmental taxation on ecological innovation demon-strates greater magnitude in private enterprises, smaller entities, and highly competitive sectors, compared to their respective counterparts.

Research by Liu et al. (2021) reveals distinct risk-return profiles between invention and utility model patents in the ecological domain. While invention patents potentially generate superior returns, they entail complex validation protocols, extended examination periods, substantial initial capital requirements, and significant outcome uncertainty (Sun et al., 2022). In contrast, utility model patents offer a more expedient pathway to regulatory compliance while maintaining moderate performance benefits. This efficiency-effectiveness trade-off frequently leads firms to adopt utility model patents as a pragmatic innovation strategy. Li B. et al. (2024) document industrial entities’ systematic preference for utility models, attributed to enhanced success probability and reduced technical thresholds. Moreover, the accessibility of governmental innovation subsidies increases for lower-complexity utility model applications (Li and Zheng, 2016). Consequently, under environmental fiscal pressure, emission-intensive enterprises likely prioritize utility model patents while curtailing invention patent initiatives. This analysis leads to.

Hypothesis 3. The implementation of environmental taxation demonstrates asymmetric effects across patent categories, with more pronounced constraints on invention patents relative to utility models in emission-intensive sectors.

Environmental taxation mechanisms directly impact corporate liquidity through elevated compliance expenditures. Czarnitzki and Hottenrott (2011) emphasize the prohibitive costs of external R&D financing, highlighting firms’ reliance on internal capital allocation for research initiatives. Seminal work by Hall et al. (2016) underscores how information asymmetries and outcome uncertainties in R&D activities necessitate internal funding sources. Brown et al. (2009) document the critical dependence of research activities on internal capital flows, with R&D expenditures frequently serving as primary adjustment variables under financial constraints. Hall and Lerner (2010) provide empirical validation of this relationship, demonstrating substantial R&D investment sensitivity to cash flow fluctuations. Furthermore, environmental taxation may deteriorate investor sentiment toward emission-intensive sectors, elevating their capital acquisition costs. Jaffe et al. (2002) establish that escalating external financing expenses significantly constrain R&D investment capacity. These interconnected factors culminate in reduced research investment and diminished innovation output. Therefore.

Hypothesis 4. Environmental taxation policies constrain ecological innovation in emission-intensive enterprises through dual channels of reduced liquidity and diminished R&D investment capacity.

The synthesized theoretical architecture of this investigation is schematically represented in Figure 1.

Figure 1. Theoretical framework.

Our empirical analysis utilizes ecological patent data extracted from the WinGo Financial Text Data Platform. The classification of environmental patents follows the taxonomic framework established by the World Intellectual Property Organization’s “International Patent Green Inventory” (2010), which delineates seven distinct subcategories. These patents are subsequently differentiated into invention patents and utility models within the environmental domain. Supplementary firm-level indicators are compiled from the China Research Data Services Platform (CNRDS) and CSMAR database. The study population encompasses firms listed on both Shanghai and Shenzhen exchanges during 2012–2022. Sample refinement procedures include: (1) elimination of financial sector entities; (2) removal of companies under special treatment designations (ST, *ST, PT); and (3) mitigation of outlier effects through winsorization of continuous variables at the first and ninety-ninth percentiles.

This paper employs a difference-in-differences (DID) model to examine the impact of environmental protection tax on corporate green innovation, as specified in Equation 1:

The subscripts i and t designate the individual entity and temporal dimensions respectively. The outcome variable yi,t quantifies ecological patent quality at the firm level, while our coefficient of interest β1, associated with the interaction term Postt*Pollutedi, captures the differential impact of environmental fiscal policy implementation on innovative output. The binary indicator Postt demarcates the regulatory regime shift, complemented by Pollutedi which categorizes firms based on emission intensity. The vector Xi,t encompasses time-varying firm characteristics that influence innovation propensity. Our econometric specification incorporates both temporal (Timet) and entity-specific (Firmi) fixed effects to account for unobserved heterogeneity. Statistical inference relies on firm-clustered standard errors to address potential serial correlation, except where explicitly noted otherwise.

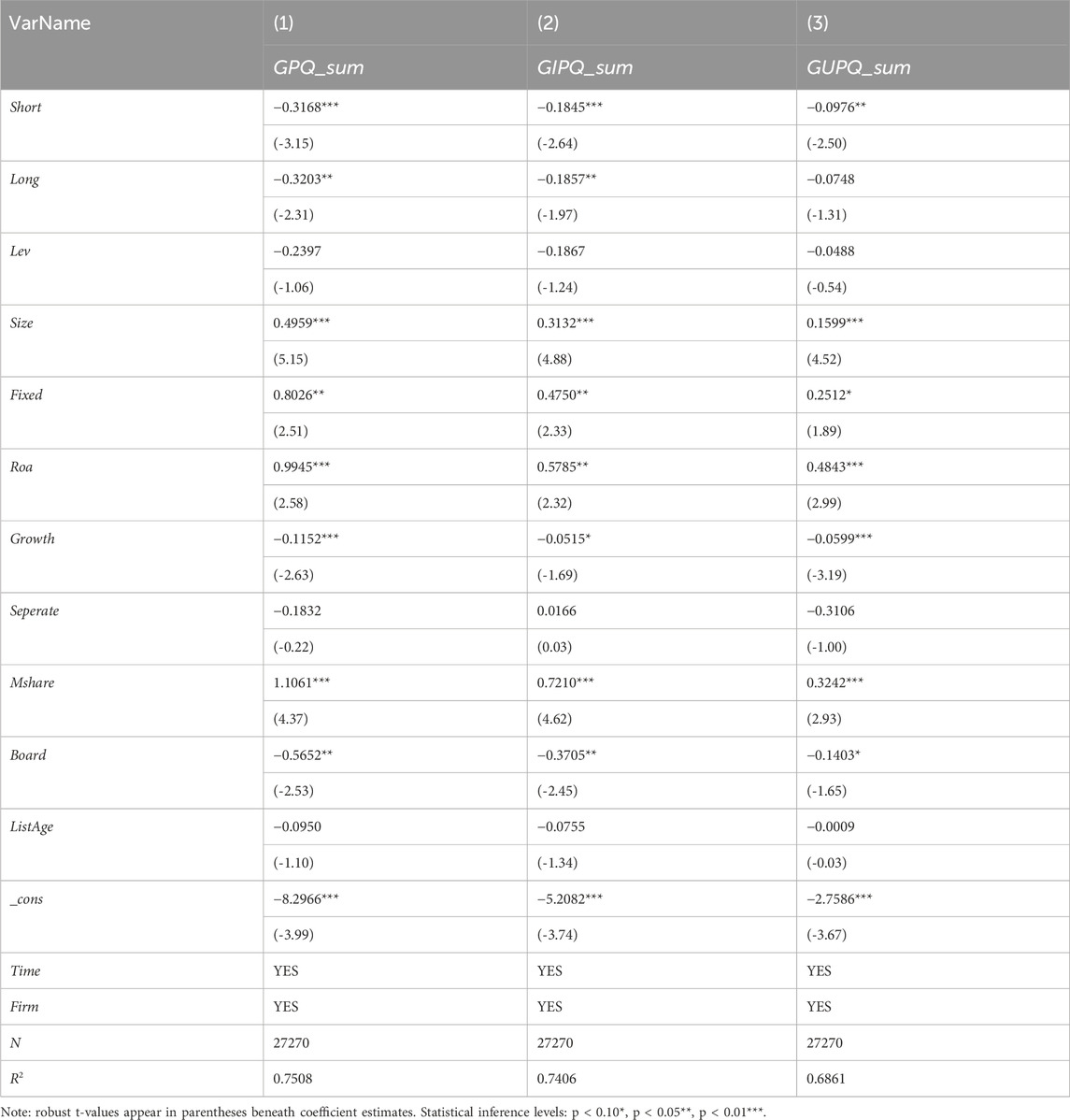

Contemporary empirical investigations have adopted divergent approaches to quantifying ecological innovation: some emphasize volumetric measures of environmental patent applications or grants (Liu and Xiao, 2022; Lin and Ma, 2022; Xue et al., 2022), while others focus exclusively on qualitative dimensions (Cao et al., 2022). Our methodological framework integrates both quantitative and qualitative aspects of innovation output. Building upon methodological foundations established by Aghion et al. (2019) and Zhang and Zheng (2018), we employ knowledge breadth methodology to assess individual patent significance. These pa-tent-level indicators are subsequently aggregated to construct firm-year observations of cumulative ecological patent quality (GPQ_sum). Complementing this approach and following Zhang et al. (2023) and Liu L. et al. (2022), we incorporate patent ap-plication frequency (GP) and derive mean quality metrics (GPQ_mean) through the ratio GPQ_sum/GP.

Recognizing the distinct characteristics of different intellectual property protection mechanisms, we further decompose our analysis between invention patents and utility models. This differentiation yields six distinct metrics: aggregated quality measures for invention patents (GIPQ_sum) and utility models (GUPQ_sum), frequency counts for each category (GIP, GUP), and corresponding mean quality indicators (GIPQ_mean, GUPQ_mean). This comprehensive measurement framework enables nuanced analysis of innovation patterns across patent types.

Our focal explanatory term comprises the interaction Postt*Pollutedi (did), capturing differential policy effects across firm categories and time periods. The temporal indicator Postt demarcates the regulatory regime transition, with pre-2018 observations coded as 0 and subsequent periods as 1. The cross-sectional classifier Pollutedi distinguishes emission-intensive sectors (1) from other industries (0), utilizing classifications established by the former Ministry of Environmental Protection’s “Listed Company Environmental Protection Inspection Industry Classification Management Directory1,” consistent with Sun et al. (2023).

Following Liu and Xiao (2022) and Lu and Zhou (2023), we incorporate several firm-specific characteristics: (1) Leverage ratio (Lev), measured as year-end total liabilities to assets ratio; (2) Enterprise scale (Size), computed as the natural logarithm of deflator-adjusted total assets; (3) Fixed asset intensity (Fixed), calculated as net fixed assets to total assets ratio; (4) Profitability (Roa), expressed as net profit to total assets ratio; (5) Revenue expansion (Growth), measured by year-over-year revenue growth; (6) Control-ownership divergence (Separate), reflecting the disparity between control rights and cash flow rights; (7) Managerial ownership (Mshare), indicating the proportion of shares held by executive officers; (8) Board composition (Board), expressed as the natural logarithm of director count; (9) Listing maturity (Listage), computed as the natural logarithm of years since initial public offering plus one. Table 1 presents descriptive statistics for these variables.

Table 1. Descriptive statistics of main indicators.

Table 1 reveals several noteworthy patterns in our sample characteristics. The aggregate ecological patent quality metric (GPQ_sum) exhibits substantial cross-sectional heterogeneity, with a mean of 1.3447 and standard deviation of 3.946. A notable qualitative differential emerges between invention patents (GIPQ_sum: 0.8158) and utility models (GUPQ_sum: 0.4943), reflecting systematic variation in innovation sophistication. The distribution of innovation activity appears highly concentrated, evidenced by the patent frequency indicator (GP) displaying a mean of 3.7712 but median of zero, suggesting ecological innovation clustering among select market participants.

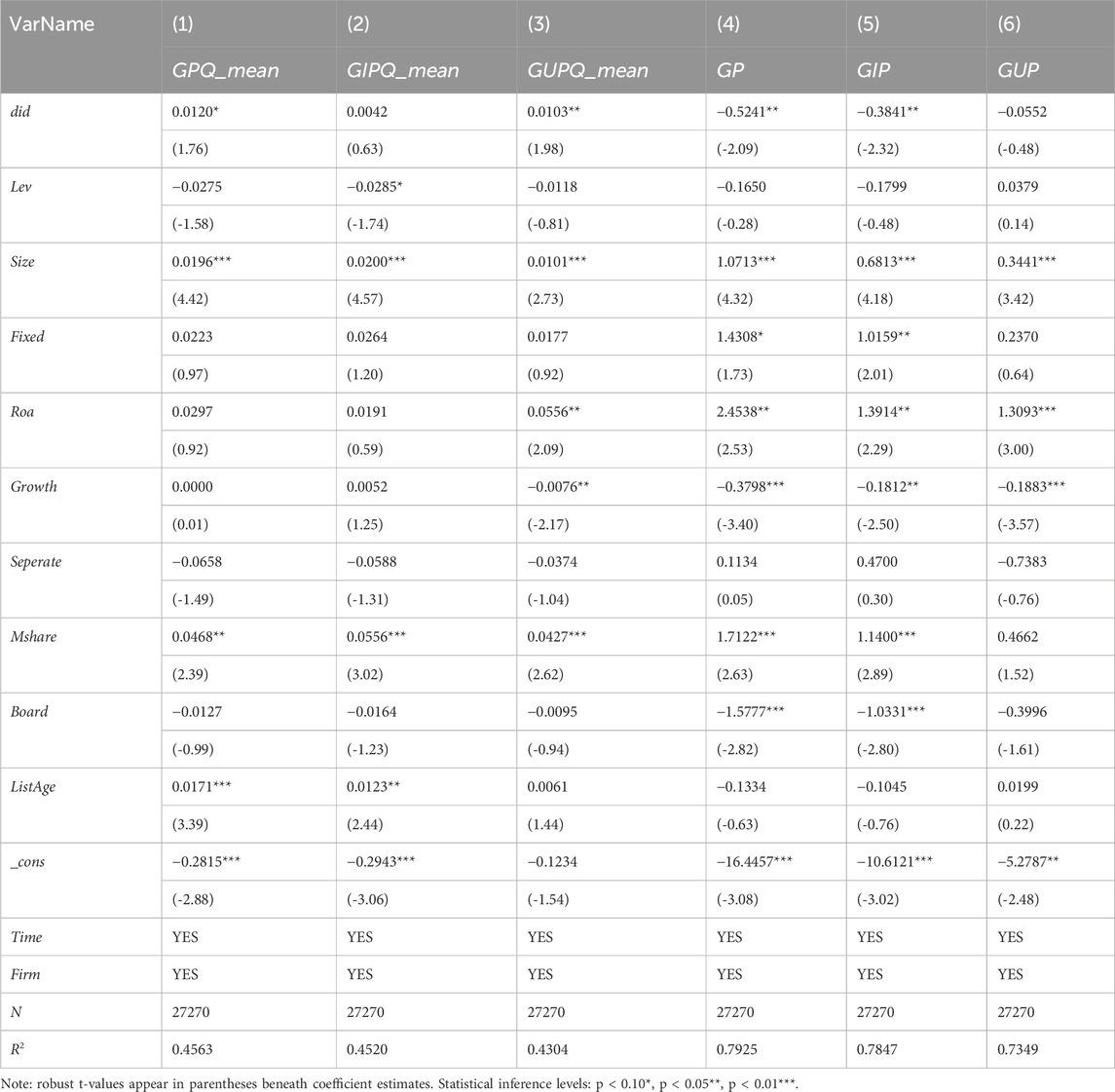

The estimation outcomes from our baseline specification (Equation 1) are presented in Table 2. We implement a sequential approach to model construction: specification (1) incorporates our focal interaction term with firm-level controls (Xi,t); specifications (2) and (3) progressively introduce temporal and entity-fixed effects. The coefficient of interest (did) maintains statistical significance and negative directionality across all specifications, providing robust empirical support for Hypothesis 1 regarding the dampening effect of environmental taxation on ecological innovation in emission-intensive sectors. This relationship potentially stems from the policy’s impact on production economics, where increased environmental compliance expenditures may divert resources from research initiatives to immediate regulatory adaptation measures. Empirical analysis from Column (3) demonstrates that the introduction of environmental taxation corresponds with a diminution in aggregate green patent quality metrics among pollution-intensive enterprises, with an observed decline of 0.3175, representing 23.61% of the baseline mean (1.3447). This magnitude suggests substantial alterations in organizational resource deployment strategies. Entities predominantly opt for tactical operational modifications (operational scaling, input substitution, or direct fiscal compliance) rather than technological advancement initiatives when confronting environmental fiscal pressures. This behavioral pattern characterizes the distinctive adaptive responses of enterprises during China’s economic transformation—where innovative capability development necessitates sustained temporal investment and cannot readily materialize as an immediate response to regulatory stimuli. Within the economic framework, the internalization mechanisms for negative externalities primarily operate through immediate price elasticity rather than innovation-driven adaptations, distinguishing these outcomes from observations in industrialized economies. This apparent innovation constraints should not be interpreted as regulatory ineffectiveness but rather illuminates the sequential adaptation methodology in Chinese enterprises—prioritizing regulatory adherence before innovation enhancement—potentially exemplifying a broader pattern among developing economies. From a transitional economics perspective, these temporary innovation constraints may represent necessary structural adjustments; as market equilibrium evolves and organizational innovation frameworks mature, sustained benefits may emerge.

Table 2. Primary econometric estimates of environmental taxation effects on ecological innovation.

This analytical outcome corresponds with Wang Y. et al. (2023) observations from Chinese capital markets, confirming innovation-constraining effects of environmental taxation. However, our findings diverge from certain contemporary investigations. Notably, Deng et al. (2023) examination of pollution-intensive sectors identified positive correlations between environmental taxation and research investment intensification.

Several methodological distinctions may explain these analytical variations: our investigation encompasses a more comprehensive enterprise sample including non-pollution-intensive sectors; our temporal framework extends through 2022, capturing extended policy implications; crucially, our methodology implements more nuanced innovation assessment metrics, integrating both quantitative and qualitative dimensions. Within theoretical frameworks, our evidence contradicts Porter and Linde’s (1995) innovation compensation paradigm, while substantiating the resource constraint hypothesis proposed by Palmer et al. (1995) and Jaffe et al. (2005), emphasizing how environmental compliance requirements constrain research and development resources. This effect manifests distinctively within China’s transitional economic context, potentially characterizing the immediate adaptive mechanisms of enterprises responding to environmental policy implementation.

The causal interpretation of difference-in-differences estimation fundamentally depends on the assumption of comparable temporal trajectories between experimental groups prior to intervention. As emphasized by Angrist and Pischke (2009), this methodological prerequisite necessitates demonstrable similarity in outcome evolution between treatment and control cohorts in the pre-policy period. To empirically evaluate this identifying assumption, we implement the dynamic effects framework developed by Jacobson et al. (1993), as specified in Equation 2:

In this specification, Yeark denotes temporal indicators, while βk captures the relative innovation divergence between emission-intensive and non-intensive sectors across the sample period. The temporal index k measures displacement from the reference period (designated as “-1”), corresponding to the year immediately preceding policy enactment. Remaining parameters maintain their definitions from the baseline specification. The critical coefficients of interest are the pre-intervention βk estimates (k < 0), whose statistical insignificance would validate the assumption of parallel pre-trends between experimental groups. The temporal evolution of point estimates and associated 90% confidence bands is visualized in Figure 2.

Figure 2. Dynamic effects analysis: Pre-treatment evolution and post-policy response.

As observed in Figure 2, before policy implementation (k < 0), the estimated βk coefficients are statistically insignificant, with confidence intervals containing zero, indicating no significant differences in green innovation trends between treatment and control groups pre-policy, thus satisfying the parallel trends assumption. This provides empirical support for our use of the DID model. Furthermore, after policy implementation (k > 0), the estimated βk coefficients become significantly negative, though their absolute values begin to decline rapidly after the fourth period. Initial findings demonstrate that while environmental taxation measures have generated sustained constraints on ecological innovation within pollution-intensive industries, the magnitude of these effects experiences significant attenuation beyond the fourth observation period, indicating progressive organizational adaptation to fiscal pressures through either cumulative technological capabilities or regulatory accommodation mechanisms.

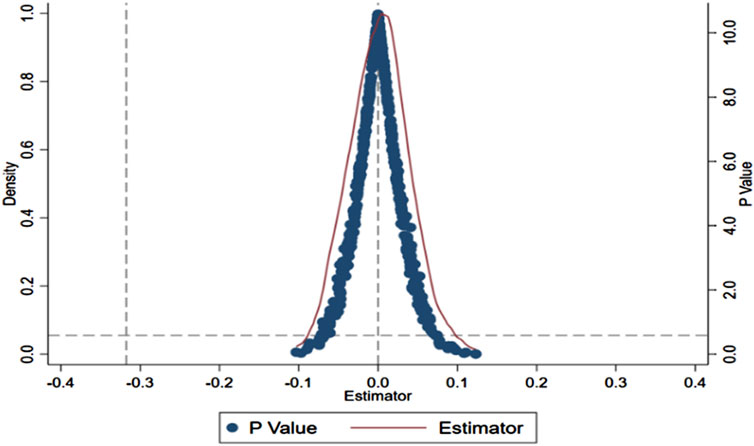

To substantiate our empirical findings and address potential confounding influences in treatment assignment, we implement a comprehensive randomization protocol. Our procedure utilizes the full sample of 27,270 firm-year observations, employing Monte Carlo techniques to generate counterfactual treatment assignments. The methodology involves stochastic allocation of treatment status, construction of synthetic policy intervention indicators, and estimation of our baseline specification using these artificially generated treatment variables. This simulation process is iterated 500 times to establish a robust null distribution. Figure 3 illustrates the kernel density estimation of simulated treatment effects and their corresponding statistical significance levels. The resulting coefficient distribution exhibits characteristics consistent with random noise: centrality around zero, approximate normality, and predominant statistical insignificance at conventional thresholds. The empirically observed treatment effect, demarcated by the vertical reference line, demonstrates substantial deviation from this null distribution. This systematic divergence between simulated and actual estimates provides compelling evidence that our documented policy effects reflect genuine regulatory impacts rather than spurious correlations or unobserved heterogeneity, thereby reinforcing the validity of our identification strategy.

Figure 3. Placebo test.

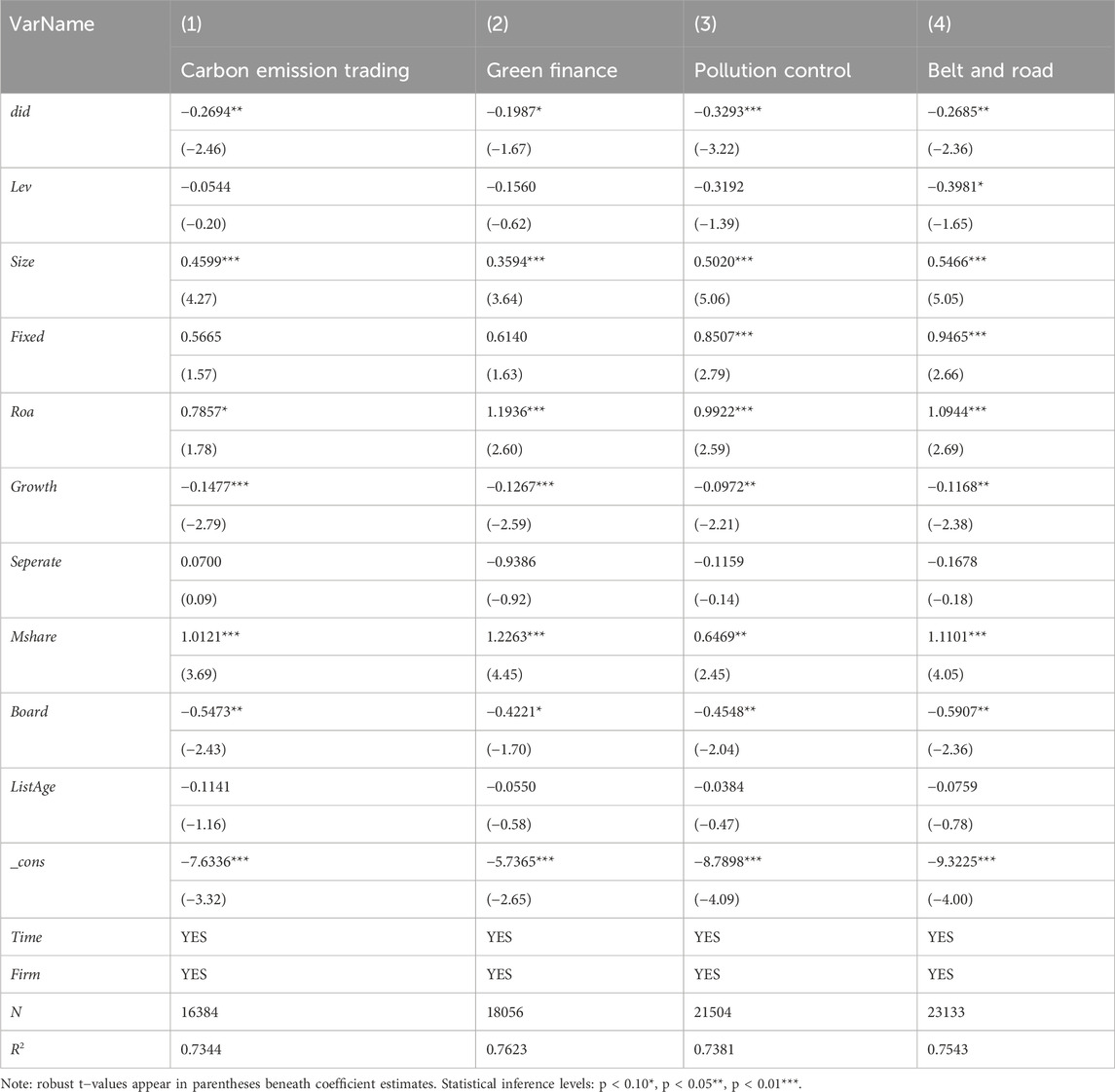

To isolate the causal effect of environmental taxation, we systematically account for concurrent regulatory initiatives that potentially influence ecological innovation. Our analysis addresses four significant policy interventions: Market-Based Environmental Mechanisms: Following the 2013 introduction of emissions trading in seven pilot jurisdictions (Beijing, Tianjin, Shanghai, Guangdong, Hubei, Chongqing, Shenzhen), we estimate our model on the subsample excluding these regions. Column (1) of Table 3 demonstrates persistence of the negative treatment effect (β = −0.2694, p < 0.05). Financial Innovation Zones: To address the 2017 establishment of ecological finance experimental regions (Zhejiang, Jiangxi, Guangdong, et al.), we conduct analysis excluding these provinces. Results presented in Column (2) maintain statistical significance (β = −0.1987, p < 0.1). Regional Environmental Oversight: Consistent with Li et al. (2023), we examine the impact of enhanced atmospheric pollution monitoring implemented in Beijing-Tianjin-Hebei and adjacent territories (April 2017). The coefficient estimate from the restricted sample remains robust (β = −0.3293, p < 0.01), as shown in Column (3). International Development Strategy: Acknowledging potential environmental compliance pressures associated with the 2014″Belt and Road” Initiative (Li B. et al., 2024), we exclude firms in participating municipalities. Column (4) demonstrates maintained significance of the treatment effect (β = −0.2685, p < 0.05). The consistency of our findings across these various policy-controlled subsamples provides strong evidence for the robustness of our primary conclusions.

Table 3. Heterogeneous policy environment analysis.

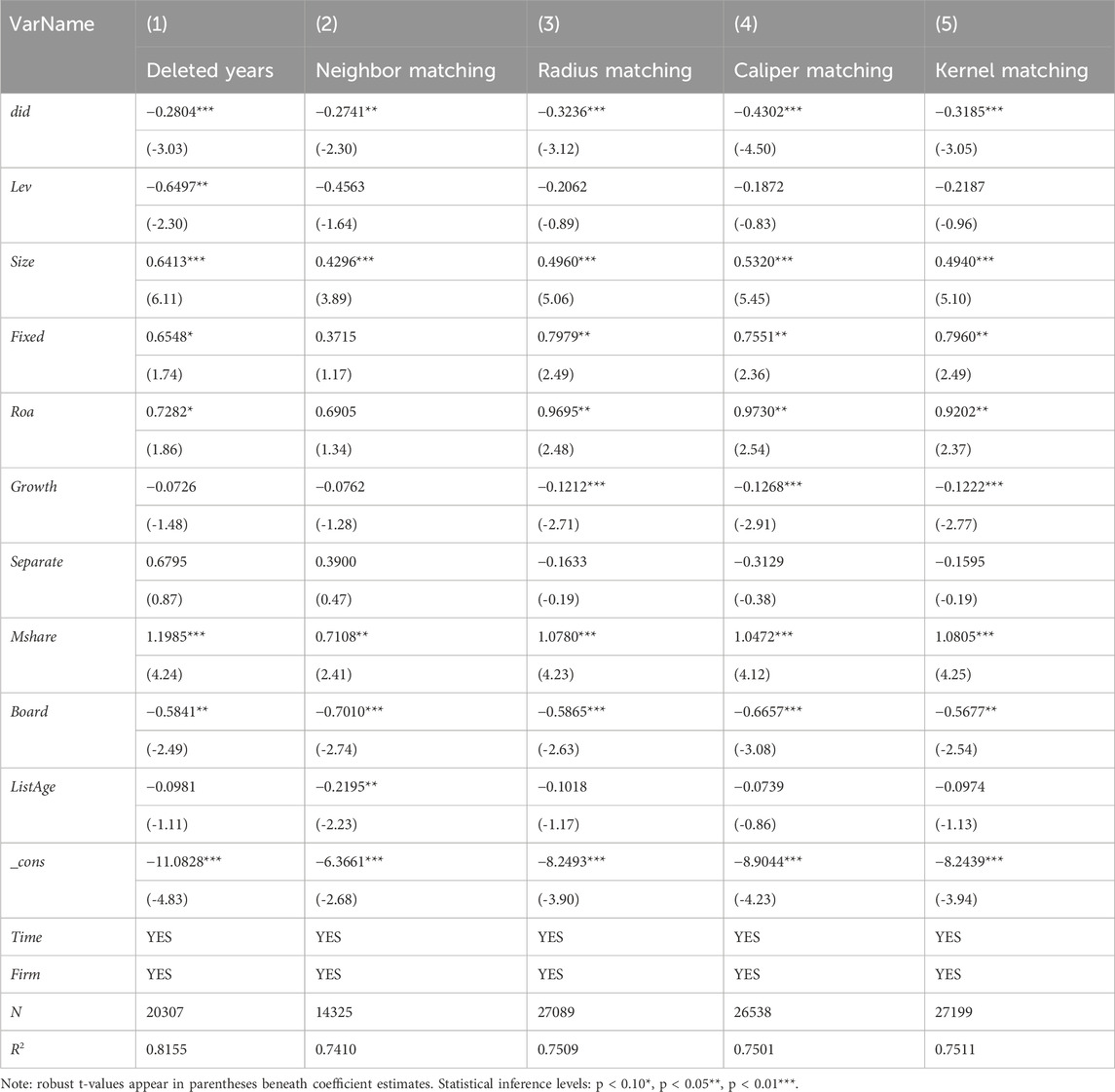

We implement two complementary methodological refinements to address anticipatory responses and potential selection concerns. First, following Li C. et al. (2024), we constrain our analysis to the 2016–2022 interval to account for behavioral adjustments potentially triggered by the 2015 legislative amendments preceding the 2018 implementation. Column (1) of Table 4 presents estimates from this temporally restricted sample, revealing persistent negative policy effects (β = −0.2804, p < 0.01) consistent with our primary specifications.

Table 4. Adjusted sample period and PSM-DID.

Adopting the methodological framework of Duan and Rahbarimanesh (2024), we employ a matched-sample approach to address potential selection concerns and enhance cross-group comparability. Propensity score estimation was conducted via Logistic regression incorporating the covariates specified in model (1). The analysis employed multiple matching algorithms - nearest-neighbor, radius-based, caliper-defined, and kernel density estimation approaches - to establish treatment-control paired samples. Subsequent difference-in-differences estimation was performed on these matched datasets, with results presented in Table 4, columns (2)–(5). The core interaction term did exhibits statistically significant negative coefficients across all matching specifications. This convergence between matched-sample estimates and baseline specifications substantively reinforces our identification strategy and strengthens the causal interpretation of our findings.

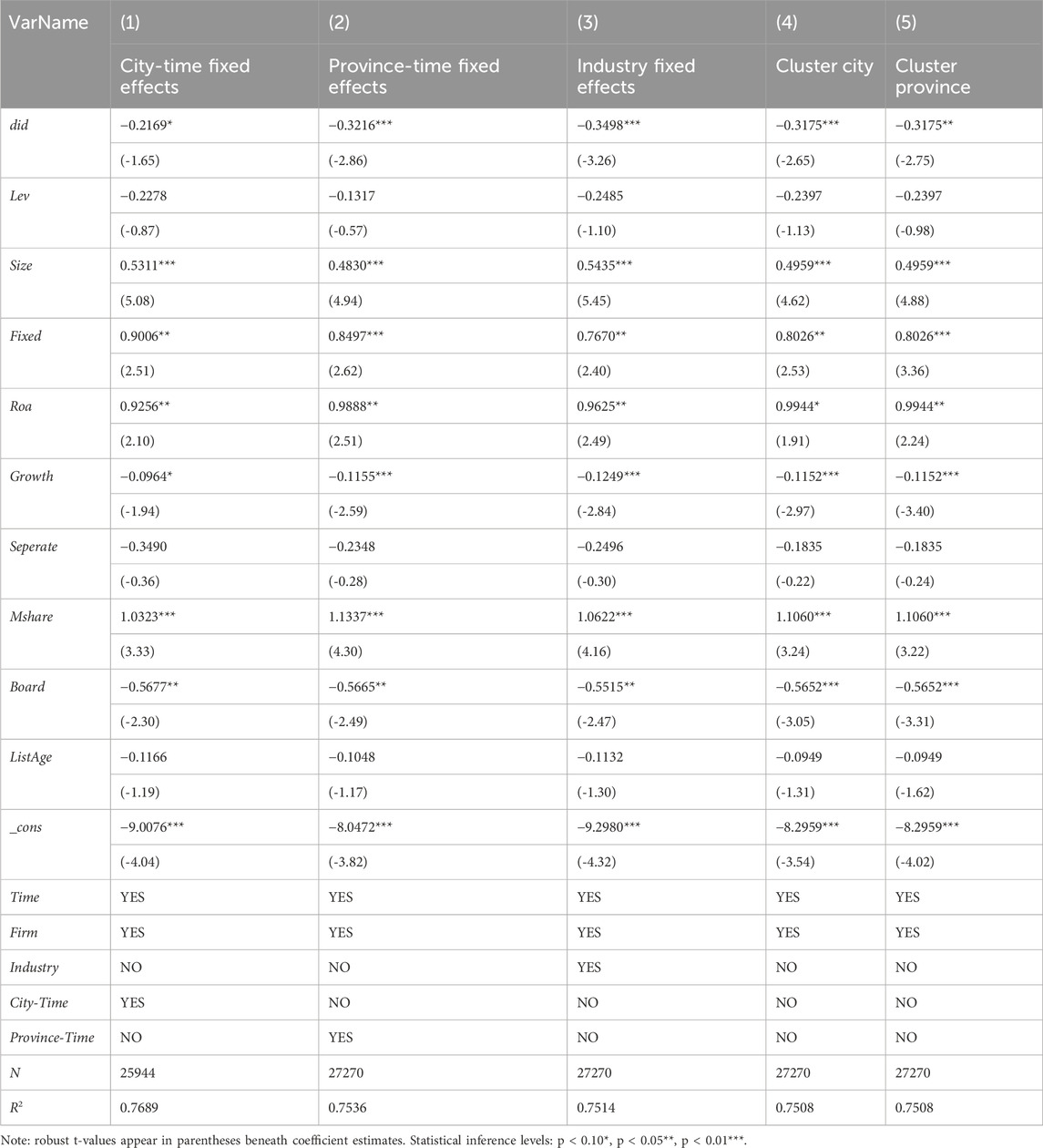

To substantiate our causal interpretation and address endogeneity concerns, we implement dual methodological refinements: augmented fixed-effects specifications and multi-level clustering protocols. The first approach systematically incorporates additional dimensional controls to account for unobserved heterogeneity in regional and sectoral dynamics. Specifically, we progressively augment our baseline specification with city-temporal interactions, province-temporal interactions, and industry-specific effects. The estimation results, documented in Columns (1)–(3) of Table 5, demonstrate persistence of the negative treatment effect across all specifications, suggesting robustness to potential omitted variable bias.

Table 5. Adding fixed effects and changing clustering levels.

Our second methodological refinement addresses spatial dependence through hierarchical standard error clustering at municipal and provincial administrative tiers. The corresponding estimates, presented in Columns (4) and (5), maintain statistical significance under both clustering protocols. This resilience to alternative variance-covariance structures provides additional validation of our statistical inference.

The convergence of evidence across these econometric specifications - spanning both enhanced fixed-effects architectures and spatial correlation controls - provides comprehensive support for our primary finding regarding the inhibitory effect of environmental taxation on ecological innovation in emission-intensive sectors. This systematic robustness to alternative model specifications substantially strengthens our causal interpretation.

Supplementing our robustness analyses, we address potential identification challenges and their implications for empirical estimation. Within our difference-in-differences analytical framework, methodological concerns arise from three primary sources: unobserved heterogeneity, non-random sampling, and bidirectional causation.

Policy outcomes may be confounded by contemporaneous regulatory initiatives and latent factors. Our methodological approach incorporates multiple dimensions of fixed effects in the baseline specification, while Table 5 augments this with municipality-temporal, provincial-temporal interaction parameters, and sectoral controls to account for spatiotemporal variation in unobservable characteristics (Chen et al., 2024). Additionally, Table 3 presents estimates excluding jurisdictions with concurrent environmental initiatives (including emissions trading mechanisms, ecological financial programs, enhanced atmospheric pollution monitoring) to isolate policy effects. The stability of core parameter estimates across these specifications suggests robust identification.

The utilization of publicly traded enterprise data introduces potential selection concerns. Our empirical strategy employs propensity score matching combined with difference-in-differences estimation to establish appropriate counterfactuals (Table 4, specifications 2–5). The consistency of negative and statistically significant coefficients across alternative matching algorithms, approximating baseline estimates, demonstrates the robustness of our findings to sample composition.

Environmental innovation intensity could potentially influence regulatory implementation. However, the centralized determination of environmental taxation policy implementation timing minimizes individual firm influence on regulatory decisions, partially mitigating endogeneity concerns. Furthermore, our mechanism analysis (Table 6) delineates specific transmission channels from environmental taxation to innovation outcomes, reinforcing the proposed causal direction.

Table 6. Channel decomposition analysis.

Our investigation acknowledges several methodological constraints despite these identification strategies: the absence of suitable instrumental variables, the challenge of establishing pure control groups under nationwide policy implementation, and data limitations regarding firm-specific tax obligations. While these constraints may influence estimation precision, they do not fundamentally alter our primary analytical conclusions.

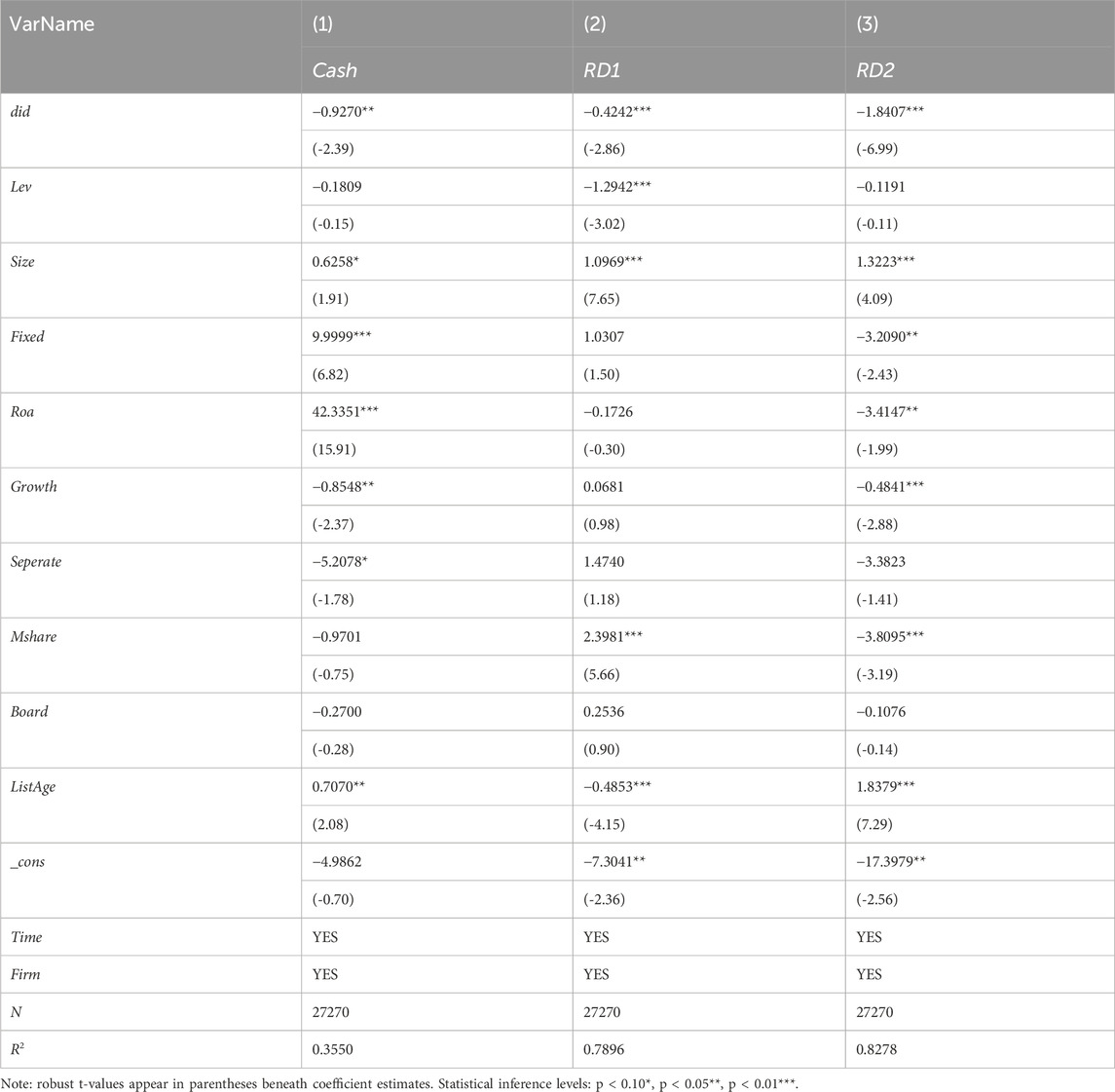

Having established the dampening effect of environmental taxation on ecological innovation, we examine potential causal mechanisms. Our theoretical framework posits that fiscal environmental interventions may constrain innovation through liquidity constraints and reduced research capacity. Given that existing literature has extensively argued that corporate cash flow, R&D funding investment, and the increase in R&D personnel can promote green innovation (Chen et al., 2021; Sánchez-Sellero and Bataineh, 2022), we focus specifically on: the impact of environmental protection tax on corporate cash flow, R&D funding investment, and R&D personnel. Following Wang S. et al. (2023), we formalize this analysis through the following Equation 3:

where Mi,t encompasses three channel variables: operational liquidity (Cash), research capital allocation (RD1), and scientific personnel intensity (RD2). Other parameters maintain their baseline definitions.

Ecological innovation demands substantial sustained investment across multiple dimensions, with extended gestation periods and delayed returns. Operating liquidity, measured by the natural logarithm of operational cash flows (Feng et al., 2023), represents a critical enabling factor. Column (1) of Table 6 documents significant negative treatment effects on corporate liquidity, suggesting environmental taxation constrains discretionary resources available for innovation activities, consistent with Wang Y. et al. (2023).

We decompose innovation inputs into capital allocation and human capital dimensions. The former is quantified through logarithmic R&D expenditure, while the latter reflects the proportion of research personnel in total employment. Columns (2) and (3) reveal significant negative treatment effects across both metrics. This pattern suggests environmental compliance expenditures may crowd out innovation investments, potentially reflecting optimal resource allocation under regulatory constraints (Liu et al., 2024).

These empirical patterns validate Hypothesis 4, demonstrating that environmental taxation influences innovation through both liquidity and investment channels.

Our identification of fiscal constraints as a transmission channel between environmental taxation and ecological innovation yields substantial insights for understanding corporate finance and innovation dynamics. The observed behavioral patterns align with internal financing theoretical predictions: organizations respond to environmental compliance costs by prioritizing liquidity preservation through reduction in long-term research investments. This empirical pattern illuminates how regulatory interventions translate into modified innovation strategies through financial pathways.

Our mechanistic analysis provides more direct empirical validation of resource constraint channels compared to alternative explanatory frameworks in contemporary literature. While Lu and Zhou (2023) emphasize institutional legitimacy considerations, and Cao et al. (2024) focus on technological transformation and sustainability metrics, Liang et al. (2023) identifies regulatory legitimacy as driving increased environmental patent applications. Our investigation reveals more fundamental financial mechanisms, complementing Wang Y. et al. (2023) observations while extending the analysis across both liquidity and research investment dimensions. This comprehensive mechanistic examination enhances our understanding of regulatory impacts on organizational innovation strategies.

Financial analysis reveals a tripartite mechanism through which environmental taxation influences innovation trajectories: immediate resource displacement effects constraining innovation funding; reputational implications elevating capital costs for emission-intensive enterprises; and strategic portfolio realignment toward environmentally oriented research initiatives. This multifaceted framework explains the observed temporal variation in policy effects, with initial constraints potentially yielding to more nuanced long-term outcomes.

The findings carry significant implications for policy coordination between environmental and financial regulatory frameworks. Complementary ecological financing initiatives, including sustainable credit facilities and environmental bonds, may mitigate innovation constraints arising from environmental taxation. This consideration becomes particularly salient for smaller and privately-held enterprises, where pre-existing financial constraints may amplify regulatory impacts, necessitating targeted support mechanisms to maintain innovation continuity.

This section examines systematic heterogeneity in policy response across organizational characteristics and institutional environments.

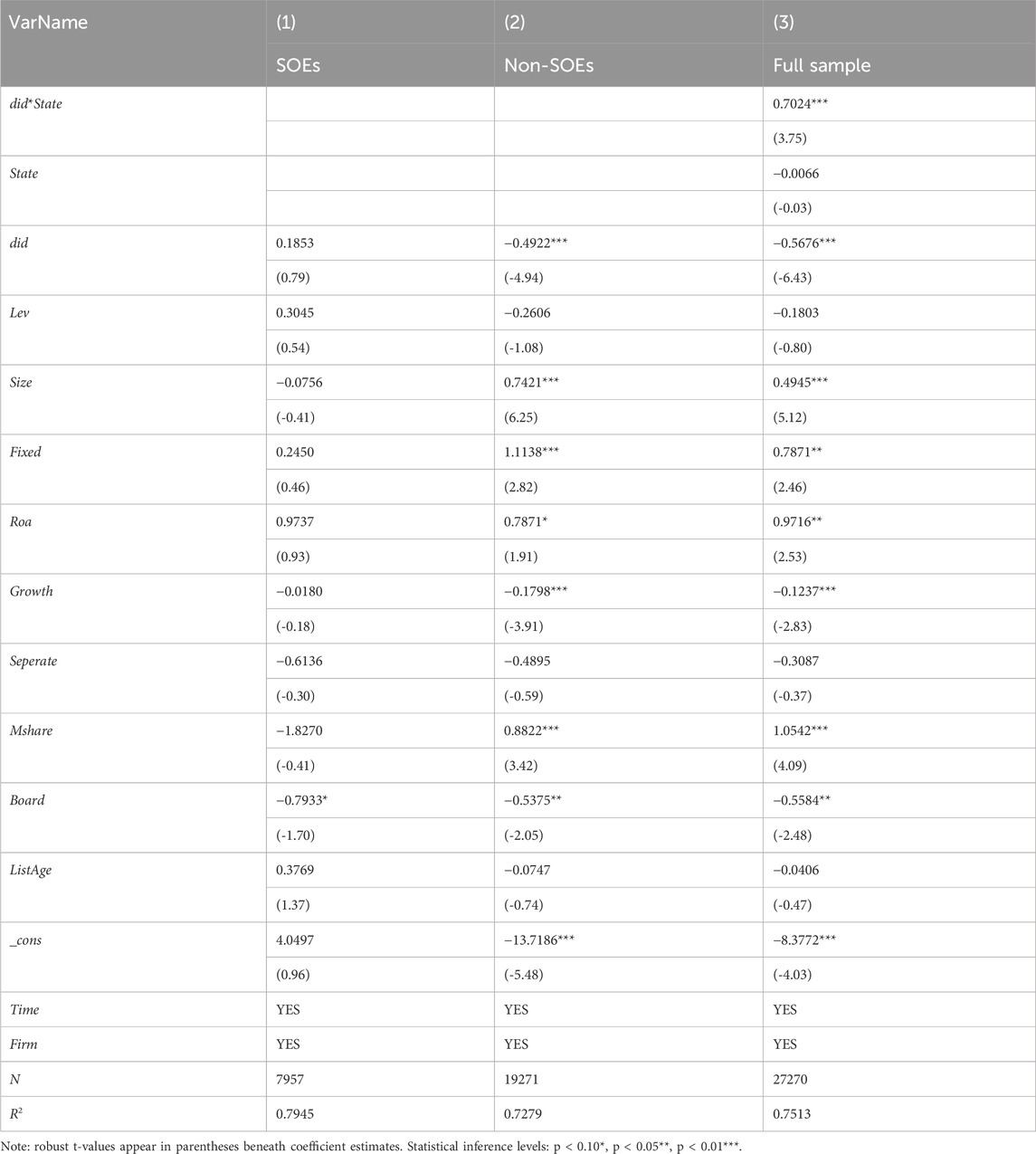

Corporate governance structures potentially moderate institutional responses to environmental fiscal policy, particularly regarding ecological innovation initiatives. To examine this heterogeneity systematically, we bifurcate our sample based on state ownership, implementing a binary indicator (State) in our baseline specification to distinguish state-controlled enterprises (coded 1) from private sector firms (coded 0). The empirical evidence, presented in Table 7, reveals asymmetric policy impacts: private enterprises exhibit significant innovation suppression effects, while state-controlled firms demonstrate resilience to policy intervention. The positive coefficient on the governance-policy interaction term (did*State) in aggregated analysis confirms the attenuating effect of state control, corroborating findings from Zhao X. et al. (2024). Multiple institutional mechanisms potentially underlie this heterogeneous response. State-controlled enterprises command superior innovation capacity and risk-bearing capabilities, facilitating regulatory adaptation, while private firms experience innovation displacement effects under binding resource constraints. Additionally, preferential access to governmental resources and policy consideration insulates state-controlled entities from adverse regulatory impacts, while broader policy mandates encourage sustained innovation. Private enterprises face heightened capital constraints and limited banking relationships, with environmental taxation potentially amplifying these frictions. Furthermore, private sector emphasis on immediate performance metrics may discourage long-horizon innovation investments under increased regulatory burden. Finally, state control potentially enhances environmental stewardship consciousness, facilitating the transformation of regulatory pressure into innovation stimulus.

Table 7. Policy response heterogeneity: Ownership structure analysis.

The observed heterogeneity in regulatory impacts corresponds with empirical evidence from Wang S. et al. (2023) and Zhao Z. et al. (2024), who document heightened innovation constraints among private sector entities under environmental regulation. These findings contrast with conclusions drawn by Li and Li (2022) and Deng et al. (2023), whose investigations indicate positive innovation effects within state-controlled enterprises while detecting no significant response among private sector firms. Such analytical divergence potentially derives from methodological variations and underscores the contextual nature of environmental policy outcomes.

The asymmetric innovation responses between state-controlled and private enterprises illuminate fundamental institutional characteristics within China’s distinctive economic framework. The divergent behavioral patterns reflect the intersection of governmental and market-based incentive structures: state-controlled entities integrate multiple policy objectives and societal obligations into their operational frameworks, extending beyond pure economic considerations to encompass political and social imperatives. Conversely, private sector organizations exhibit stronger alignment with market mechanisms and demonstrate enhanced sensitivity to economic signals. These institutional distinctions manifest in divergent innovation adaptation strategies under uniform environmental policies.

Within the broader context of China’s economic transformation, these findings yield substantial macroeconomic implications. State-controlled enterprises function as policy implementation anchors, maintaining technological advancement trajectories despite regulatory pressures. Simultaneously, the acute policy responsiveness exhibited by private enterprises reflects progressive market liberalization. This bifurcated innovation response pattern represents a distinctive feature of China’s gradual reform approach within environmental governance, balancing policy stability through state sector consistency while facilitating market-driven adaptation through private sector flexibility.

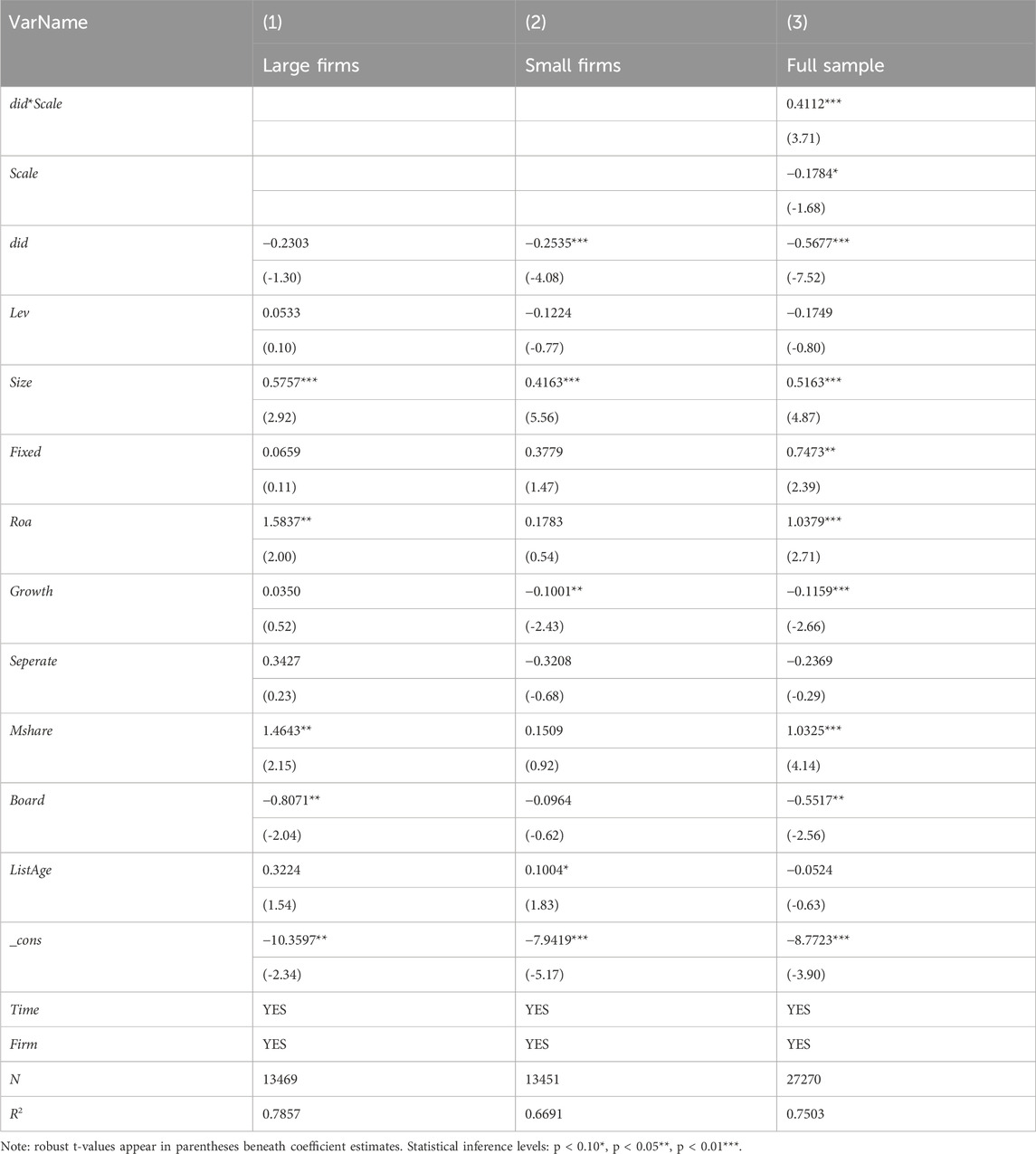

Organizational scale potentially mediates the transmission of environmental fiscal policy to innovation outcomes. Following Liu and Xiao (2022), we implement a scale-based analysis using median total assets as the bifurcation threshold, introducing a dimensional indicator (Scale) to distinguish large enterprises (coded 1) from their smaller counterparts (coded 0). Table 8 documents differential policy sensitivity: smaller entities exhibit pronounced innovation contraction, while larger institutions demonstrate impact resilience. The positive coefficient on the scale-policy interaction (did*Scale) in aggregate estimation validates the moderating influence of institutional scale. The observed pattern corresponds with empirical evidence documented by Huang et al. (2022) and Liu and Xiao (2022), demonstrating superior adaptive capacity of larger organizations to environmental regulatory changes, attributable to their enhanced resource endowments and operational scale economies.

Table 8. Innovation response heterogeneity: Dimensional analysis.

This systematic heterogeneity likely reflects multiple economic mechanisms. Larger institutions command superior resource endowments across capital, human capital, and technological dimensions, facilitating absorption of regulatory costs while maintaining innovation trajectories. Their enhanced capital market access and reduced financing frictions enable sustained research investment despite regulatory pressures. Scale economies in innovation processes generate efficiency gains unavailable to smaller entities. Market power asymmetries enable cost transmission through value chains, while smaller firms bear disproportionate regulatory burden. Strategic orientation differences emerge as larger institutions emphasize long-horizon competitive positioning through ecological innovation, contrasting with survival-focused smaller entities preferring direct compliance. Additionally, institutional capacity for environmental policy analysis and strategic adaptation varies systematically with scale.

The asymmetric responses to environmental taxation across organizational scale dimensions yield substantive economic ramifications. Microeconomic analysis reveals these disparities as manifestations of scale-dependent variations in innovative capabilities and uncertainty tolerance. Through an industrial organization lens, this heterogeneity potentially catalyzes strategic segmentation within sectors, generating bifurcated innovation hierarchies comprising dominant technological pioneers and adaptive followers. The temporal evolution of these dynamics may fundamentally alter industrial power structures and value distribution mechanisms, as larger entities leverage environmental innovation capabilities to reinforce market dominance, while smaller organizations navigate toward specialized niches within innovation networks. Within the broader economic restructuring context, this organizational realignment may enhance systemic innovation efficiency through resource optimization, though vigilance is warranted regarding potential consequences of market power consolidation and diminished innovation heterogeneity.

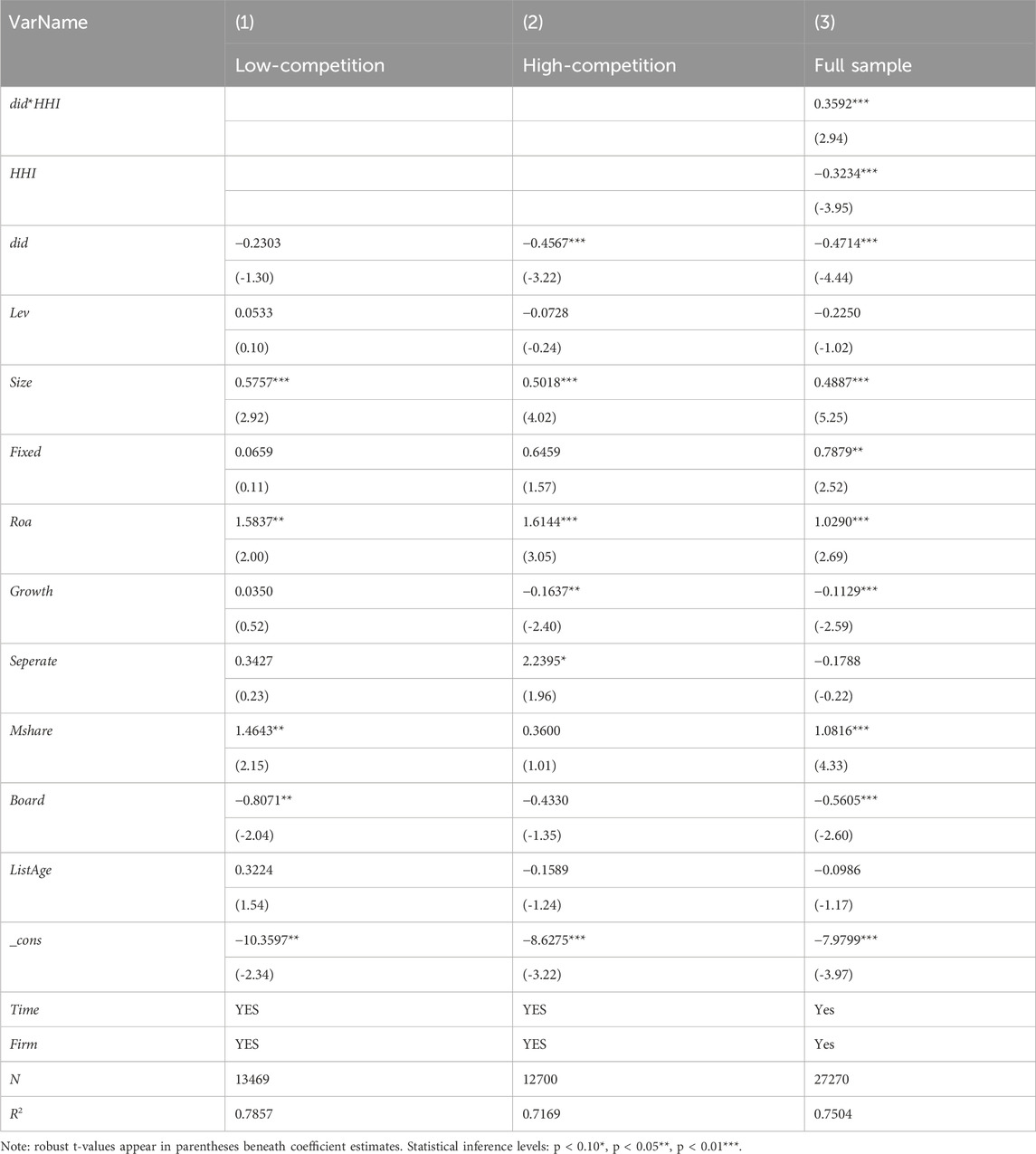

Industrial organization characteristics potentially mediate environmental policy transmission to innovation outcomes. Following Zhao X. et al. (2024), we employ the Herfindahl-Hirschman concentration metric to quantify market structure, partitioning our sample at median concentration levels. We introduce a structural indicator (HHI) distinguishing concentrated sectors (above-median HHI, coded 1) from competitive markets (coded 0). Table 9 reveals systematic variation in policy sensitivity: competitive sectors exhibit significant innovation suppression, while concentrated industries demonstrate impact resilience. The positive coefficient on the structure-policy interaction (did*HHI) in aggregate estimation validates the attenuating effect of market power. These patterns align with both the non-monotonic competition-innovation relationship postulated by Aghion et al. (2005) and Schumpeterian innovation theory (Schumpeter, 2013). Multiple economic mechanisms potentially drive this heterogeneity. Price-setting capacity in concentrated markets facilitates regulatory cost transmission, preserving innovation resources, while competitive pressure constrains such adjustment. Margin compression in competitive environments incentivizes cost-minimization strategies over uncertain innovation investments. Resource allocation dynamics under competitive pressure may prioritize immediate market share preservation over long-horizon innovation initiatives (Vives, 2008). Additionally, scale economies and excess returns in concentrated sectors enhance both internal innovation funding and external capital access. These empirical patterns provide robust support for Research Hypothesis 2.

Table 9. Innovation response heterogeneity: Market structure analysis.

The heterogeneous responses to environmental taxation across market structures yield substantial implications for industrial economic theory. The findings illuminate how regulatory interventions function as external catalysts in reconfiguring competitive dynamics and innovation incentives. Within concentrated markets characterized by limited competition, organizations leverage market power to distribute environmental compliance costs while sustaining research investments through monopolistic rents. Conversely, entities operating in highly competitive sectors face intensified pricing constraints and margin pressures, compromising their capacity for sustained innovation investment.

Through the lens of economic restructuring, these asymmetric effects potentially catalyze organizational evolution within industries. Environmental taxation functions as a market-driven selection mechanism, potentially facilitating consolidation within fragmented sectors toward more efficient operational scales and enhanced innovation capabilities. Simultaneously, within concentrated markets, the increased cost burden may counterbalance monopolistic inefficiencies, incentivizing competitive advantage through technological advancement rather than market power exploitation. This bidirectional regulatory mechanism potentially fosters optimal competitive equilibrium, balancing innovation incentives while preventing the inefficient dispersion of research resources characteristic of hypercompetitive markets.

We decompose environmental policy effects across both qualitative and quantitative innovation metrics. Table 10 documents systematic variation in policy impacts: positive coefficients for mean patent quality indicators (GPQ_mean, GUPQ_mean) contrast with insignificant effects on invention patent quality (GIPQ_mean). Simultaneously, negative treatment effects emerge for aggregate patent counts (GP) and invention patent volumes (GIP), while utility model quantities (GUP) remain unaffected. These patterns, supporting Hypothesis 3, reveal multifaceted policy transmission mechanisms. The empirical evidence suggests strategic adaptation along several dimensions. First, the policy induces a quality-quantity trade-off, enhancing average innovation value while contracting aggregate output, particularly pronounced in utility models. Second, regulatory cost pressures appear to catalyze strategic reorientation toward quality-focused innovation portfolios, concentrating resources on selective high-potential initiatives. Third, temporal optimization dynamics emerge as firms balance immediate regulatory compliance costs against extended-horizon invention patent returns, potentially favoring expedited utility model development. Fourth, the policy appears to trigger systematic innovation resource reallocation, with concentrated investment in promising projects offsetting reduced initiative breadth. Finally, heterogeneous responses across patent categories, notably pronounced in utility model quality enhancement, suggest differential innovation elasticities to regulatory intervention.

Table 10. Environmental policy impact: Qualitative and quantitative innovation metrics.

The identified inverse relationship between innovation quality and quantity represents a novel contribution to scholarly discourse. While Song et al. (2020) acknowledged patent heterogeneity, they stopped short of examining regulatory impacts on innovation excellence. Our investigation advances beyond previous frameworks, complementing Aghion et al. (2016) observations regarding policy-induced directional shifts in innovation while illuminating specific qualitative transformations. The findings substantiate Popp et al. (2010) theoretical proposition regarding bifurcated policy effects, where regulatory interventions simultaneously stimulate and constrain distinct innovation categories. This heterogeneity manifests through differential impacts across patent classifications, underscoring the multifaceted nature of environmental policy consequences on technological advancement.

The observed enhancement in innovation sophistication concurrent with quantitative decline yields substantial economic insights. The phenomenon reflects fundamental alterations in marginal innovation benefit calculations: regulatory cost pressures induce strategic portfolio optimization, prioritizing high-return innovative initiatives while discontinuing marginal projects. This reallocation mechanism potentially corrects market inefficiencies by redirecting resources toward qualitative excellence rather than numerical expansion, enhancing aggregate productivity dynamics. The surge in sophisticated environmental innovations, particularly in practical applications, aligns with China’s industrial modernization objectives.

This qualitative transformation carries profound implications for China’s economic evolution. Historical emphasis on quantitative metrics has generated substantial but often superficial innovation outputs. Environmental taxation introduces selective pressures that encourage strategic innovation portfolio management, potentially catalyzing systemic enhancement through “constructive disruption.” This structural realignment facilitates technological advancement beyond basic innovation paradigms toward higher-value creation. The documented improvement in practical innovation quality suggests emergence of an implementation-focused development trajectory, particularly suited to China’s current industrial transformation requirements. Furthermore, enhanced innovation quality potentially strengthens organizational resilience against market volatility, reducing systemic vulnerabilities and fostering sustainable economic growth amid global uncertainties.

To capture the dynamic policy transmission mechanisms, we examine differential innovation responses across temporal horizons.

Following Cao and Su (2023), we establish a dynamic effect model specified in Equation 4:

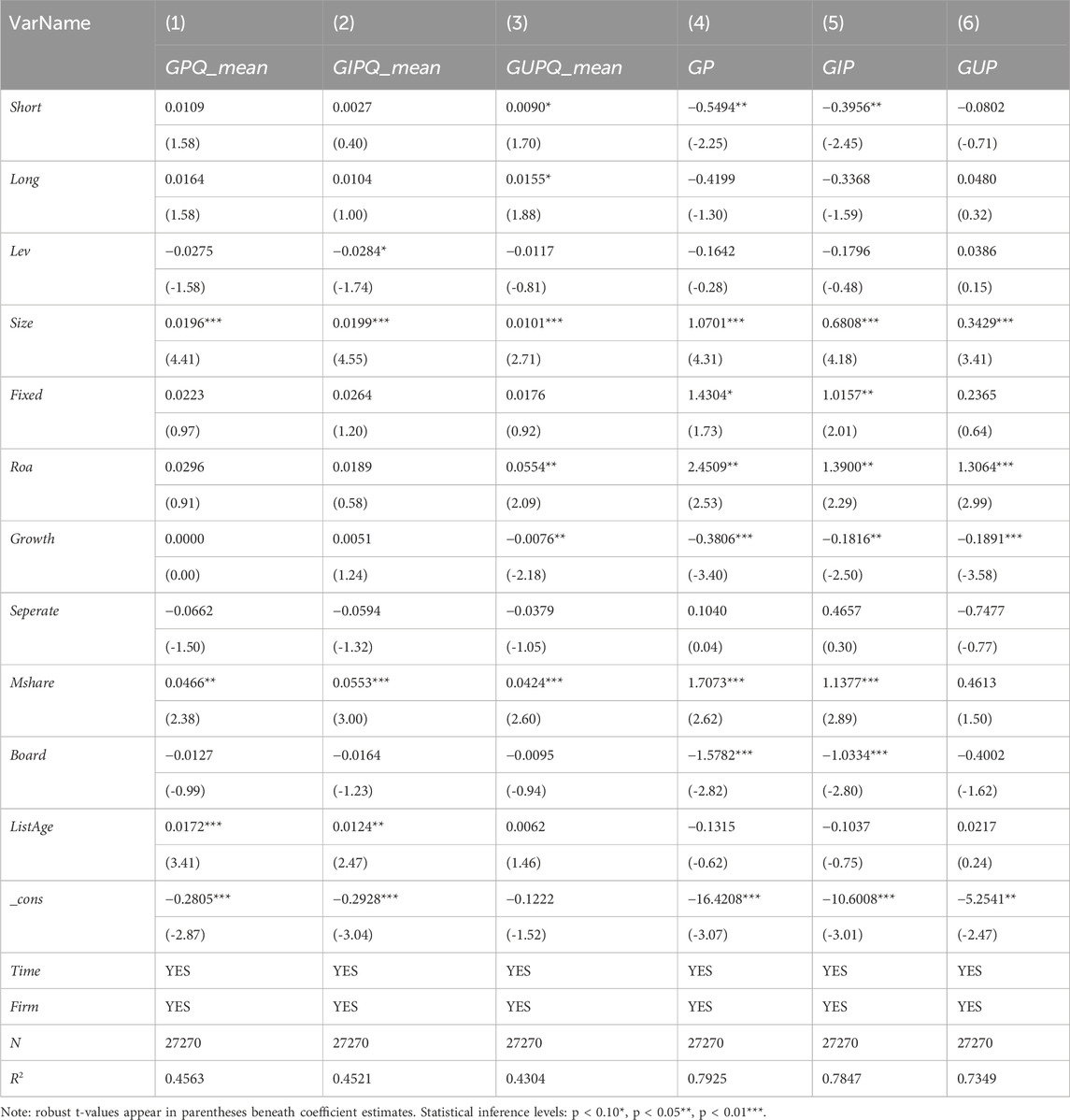

where Shorti,t indicates immediate policy exposure (years 1-4 post-implementation) for emission-intensive firms, Longi,t captures extended exposure (year 5 onwards), and remaining parameters maintain baseline specifications. Table 11 documents systematic variation in temporal response patterns. Initial policy implementation generates significant quality contractions across all innovation metrics (GPQ_sum, GIPQ_sum, GUPQ_sum). Extended exposure exhibits persistent negative effects on aggregate and invention patent quality measures, while utility model quality impacts attenuate to statistical insignificance.

Table 11. Innovation quality response: Temporal decomposition analysis.

This temporal heterogeneity suggests nuanced adaptation mechanisms. Initial regulatory shock appears to constrain high-quality innovation investment uniformly. However, extended exposure reveals differential adaptation capacity, particularly evident in utility model quality resilience, potentially reflecting strategic reorientation toward practical innovation initiatives under sustained regulatory pressure.

This investigation extends the analytical framework established by Cao and Su (2023) regarding temporal variations in carbon market policy effectiveness, by illuminating differential evolutionary patterns across distinct innovation categories. While Wei et al. (2023) and Jiang et al. (2023) identified nonlinear relationships between environmental taxation and innovative activities, our analysis specifically examines longitudinal transformation processes, contributing novel insights into policy impact trajectories. The identified temporal asymmetry in regulatory outcomes carries substantial implications for policy assessment methodologies, emphasizing the necessity of incorporating both immediate responses and sustained adaptation mechanisms in environmental policy evaluation frameworks.

Utilizing specification (4), we examine granular temporal variation in innovation metrics. Table 12 reveals systematic heterogeneity across dimensions and horizons. Initial policy exposure generates neutral effects on aggregate (GPQ_mean) and invention patent quality means (GIPQ_mean), while positively impacting utility model quality (GUPQ_mean). Extended exposure amplifies utility model quality enhancement, maintaining neutral impacts on other quality metrics. Simultaneously, immediate implementation suppresses aggregate (GP) and invention patent volumes (GIP), with attenuation to insignificance under extended exposure. Utility model quantities (GUP) demonstrate resilience across all horizons.

Table 12. Temporal-dimensional innovation response analysis.

The empirical evidence illuminates multifaceted strategic responses to environmental fiscal intervention. Initial policy exposure triggers a distinctive quality-volume trade-off: regulatory cost pressures induce investment contraction, manifesting in reduced patent volumes, while extended exposure catalyzes strategic reorientation toward qualitative enhancement, particularly pronounced in utility model innovations. Patent category analysis reveals systematic response heterogeneity: invention patents demonstrate sustained sensitivity to regulatory intervention, while utility models exhibit quality improvements, suggesting strategic migration toward efficiency-optimized innovation channels. This asymmetric response pattern indicates rational portfolio adjustment under resource constraints. Temporal decomposition reveals progressive organizational adaptation to the regulatory framework. The evolution of long-horizon effects indicates strategic rebalancing across innovation dimensions, providing crucial insights into policy effectiveness trajectories. Additionally, the amplified positive responses in specific metrics (notably GUPQ_mean) under extended exposure highlight implementation latency, emphasizing the necessity of extended evaluation horizons for comprehensive impact assessment.

The observed temporal asymmetry in environmental taxation’s impact on ecological innovation illuminates organizational strategic evolution and systemic adaptation processes. Initial regulatory effects manifest primarily through immediate cost transmission mechanisms, inducing contractionary resource reallocation within innovation portfolios. Subsequently, organizations progressively accommodate regulatory parameters, implementing strategic realignments with emphasis on qualitative enhancements. This evolutionary sequence of adaptive responses characterizes the nonlinear dynamics of economic systems under policy stimuli.

Within macroeconomic cyclical frameworks, these temporal variations yield substantial implications. Initial regulatory implementation may exacerbate recessionary pressures, particularly through innovation constraints that potentially decelerate technological advancement and productivity growth. However, extended temporal horizons reveal potential benefits through quality-enhanced innovation and structural modernization, potentially catalyzing renewed economic momentum. This pattern necessitates strategic policy patience, acknowledging temporary adjustment costs while awaiting sustained benefits. Transitional challenges might be mitigated through complementary policy instruments, including temporary innovation incentives and financial support mechanisms.

Examining resource allocation dynamics, the temporal divergence in policy effects demonstrates inherent market equilibration processes. Initial market responses exhibit potential oversensitivity to regulatory signals, manifesting in innovation activity contraction. Progressive market adjustment reveals new equilibrium states, transforming organizational approaches from reactive to proactive innovation strategies, enhancing allocative efficiency. The sustained enhancement in practical environmental innovation quality suggests organizational discovery of strategically aligned ecological innovation pathways. This endogenous adaptation process potentially yields more sustainable innovation paradigms compared to direct regulatory intervention.

Our longitudinal analytical framework advances beyond the static methodologies employed by Liu et al. (2021), enabling enhanced identification of organizational innovation strategy evolution. While their research documented diminishing regulatory impacts on environmental patent applications, our investigation illuminates concurrent qualitative enhancements alongside quantitative adjustments. The temporal patterns we identify correspond with Jiang et al. (2023) documented U-shaped relationship between environmental taxation and innovation outcomes, while extending the analysis to demonstrate differential trajectories across qualitative and quantitative dimensions. These insights contribute to both theoretical frameworks for regulatory assessment and empirical understanding of ecological innovation dynamics within Chinese enterprises.

The temporal decomposition of environmental taxation’s innovation effects reveals pronounced chronological heterogeneity in policy outcomes. Initial regulatory implementation generates substantial constraints on patent generation; however, extended observation reveals progressive strategic adaptation, characterized by sustained improvement in practical innovation quality concurrent with diminishing quantitative constraints. This evolutionary pattern demonstrates organizational progression from reactive to proactive strategic orientation, illuminating complex regulatory transmission mechanisms. These findings carry substantial implications for policy architecture and evaluation methodologies, emphasizing the necessity of longitudinal assessment frameworks incorporating multiple innovation metrics.

Empirical analysis of Chinese A-share listed firms (2012–2022) utilizing difference-in-differences methodology reveals systematic patterns in environmental fiscal policy transmission to innovation outcomes. (1) Environmental taxation generates significant innovation contraction in emission-intensive sectors, robust to specification variations and falsification tests, suggesting regulatory cost displacement of research investment. (2) Response heterogeneity emerges across institutional characteristics: heightened sensitivity among private enterprises, smaller institutions, and competitive sectors reflects differential adaptation capacity. (3) Categorical decomposition indicates asymmetric impacts: invention patent suppression contrasts with utility model resilience, highlighting strategic portfolio adjustment. (4) The mechanistic investigation reveals that environmental taxation constrains ecological innovation initiatives through multiple channels: elevated regulatory compliance expenditures, diminished operational liquidity, and reduced research expenditure. (5) Quality-quantity trade-offs emerge: volume contraction accompanies average quality enhancement, particularly pronounced in utility models, with temporal evolution toward quality dominance.

These findings motivate several policy refinements.

(1) Implementation strategies accommodating organizational diversity. Private sector entities warrant graduated taxation frameworks incorporating progressive rate structures; complemented by targeted ecological innovation financing mechanisms addressing capital constraints. Small and medium enterprises require stratified fiscal obligations supplemented by dedicated innovation funding; establish collaborative frameworks incentivizing larger organizations to facilitate technological advancement among smaller entities. Competitive sectors necessitate adaptive environmental levies promoting cooperative innovation initiatives; less competitive industries benefit from reinvestment incentives directing surplus capital toward environmental technology development.

(2) Integrated policy architecture reconciling immediate constraints with sustained development objectives. Institute environmental investment credit systems enabling certified research expenditure offsets against environmental obligations; allocate taxation proceeds toward ecological innovation initiatives. Implement quality-centric evaluation frameworks incentivizing excellence over quantity; establish technological development guidelines providing strategic direction. Acknowledging implementation lags, adopt graduated enforcement intensification; maintain systematic assessment procedures enabling dynamic policy calibration.

(3) Tailored support mechanisms reflecting innovation diversity. Invention patents warrant sustained research support incorporating extended funding horizons and risk distribution mechanisms; enhance quality incentives for utility innovations while facilitating technological sophistication; develop progressive support frameworks enabling technological advancement trajectories. Modernize assessment methodologies emphasizing qualitative metrics; implement sector-specific quality evaluation frameworks.

(4) Cultivate integrated innovation frameworks. Harmonize regional environmental policies preventing regulatory arbitrage; develop territorial innovation consortiums optimizing resource utilization; facilitate institutional collaboration integrating industrial, academic, and research capabilities; enhance technological commercialization mechanisms.

Despite certain findings, this study has several limitations. First, data availability constraints limiting sample data to 2022 may affect long-term policy effect assessment. Second, missing environmental protection subsidy and related environmental data may lead to potential endogeneity issues. Additionally, analysis based solely on Chinese A-share listed company data may involve sample selection bias. Future research could attempt to expand sample scope, include non-listed enterprises and longer time series, further exploring interaction mechanisms between environmental protection tax and enterprise innovation, providing more comprehensive empirical evidence for environmental policy optimization.

Publicly available datasets were analyzed in this study. This data can be found here: All the data used in this paper are openly available from Chinese Research Data Services Platform (CNRDS), China Stock Market and the Accounting Research (CSMAR) database and WinGo Financial Text Data Platform and for more details on the website: https://www.cnrds.com/Home/Index#/, https://data.csmar.com//, http://www.wingodata.cn/#/dash/index.

JZ: Writing–original draft, Writing–review and editing. KG: Writing–original draft, Writing–review and editing. LW: Writing–review and editing.

The author(s) declare that financial support was received for the research and/or publication of this article. This research is supported by the National Social Science Fund of China (Grant No. 24CJY077), Special Project for Science and Technology Strategy Research of Shanxi Province (Grant No. 202404030401127), the Start-up Fund for Scientific Research at Taiyuan University of Science and Technology (Grant No. W20242009).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

The author(s) declare that no Generative AI was used in the creation of this manuscript.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

1Pollution-intensive sectors are identified through matching the Directory’s classifications with the 2012 CSRC industry codes: B06, B07, B08, B09, B10, C15, C17, C18, C19, C22, C25, C26, C27, C28, C29, C30, C31, C32, C33, and D44.

Acemoglu, D., Aghion, P., Bursztyn, L., and Hemous, D. (2012). The environment and directed technical change. Am. Econ. Rev. 102 (1), 131–166. doi:10.1257/aer.102.1.131

Acemoglu, D., Akcigit, U., Hanley, D., and Kerr, W. (2016). Transition to clean technology. J. Polit. Econ. 124 (1), 52–104. doi:10.2139/ssrn.2534407