Zhiqiang Liang

Zhiqiang Liang Yao Shen

Yao Shen Kunyu Yang

Kunyu Yang Jinsong Kuang

Jinsong Kuang

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 10 March 2025

Sec. Environmental Economics and Management

Volume 13 - 2025 | https://doi.org/10.3389/fenvs.2025.1539990

This article is part of the Research TopicA Strategic Nexus for Enhancing System Resilience: Advancing Energy Efficiency, Reducing Carbon Emissions, Managing Water Resources, and Controlling Air Pollution in the Industrial SectorView all 4 articles

Sustainable development comes from a balance between economic growth and environmental protection, with due consideration of long-term impacts on environment. Leveraging policy tools to promote green innovation is a critical strategy for achieving this objective. This paper examines the impact of high-tech certification on corporate green innovation, distinguishing between substantive and strategic green innovation. It develops a theoretical framework to analyze how high-tech certification influences enterprise green innovation through mechanisms such as tax preferences, government subsidies, financing constraints, and leveraging capital market attention. The study employs a zero-inflated negative binomial regression model and utilizes data of A-share listed companies from 2006 to 2023 to systematically assess the impact of high-tech certification on enterprise green innovation strategies, underlying mechanisms, and their heterogeneity. The research discovers that in general, high-tech certification significantly promotes enterprise green innovation, having a more prominent facilitating effect on strategic green innovation, resulting in a certain degree of green patent false prosperity. From the perspective of underlying mechanisms, high-tech certification increases the resources actually obtained by enterprises through tax preferences and government subsidies and alleviates financing constraints, thereby guiding enterprises to undertake more substantive green innovation; while enhancing capital market attention increases the expected resources obtained by enterprises, prompting enterprises to be more inclined towards strategic green innovation. Further analysis reveals that the impact of high-tech certification on corporate green innovation varies significantly across different ownership structures, industries, and regions. Specifically, in state-owned enterprises, technology-intensive sectors, and enterprises located in the central regions, the positive effect on substantive green innovation is particularly pronounced. This study contributes to the literature on policy tools and corporate green innovation strategies by offering robust empirical evidence to optimizing policy design, mitigating policy arbitrage, and preventing patent bubbles.

Extensive economy inflicts severe damage upon natural environment and we are seeing more proofs of an increasingly over-stressed ecological system. Henceforth, environmental protection has emerged as the focus of current global public governance. Based on the experience of Western and European economies and the practice of the East Asian economic miracles, technological factors have played a core role in both economic growth and environmental protection (Tomizawa et al., 2020). In the context of escalating resource and environmental pressures, reducing energy consumption, mitigating environmental pollution, and achieving sustainable development have become central themes in national policies (Kou et al., 2024). With enterprises serving as both the primary source of pollution and the key driver of technological research and development, fostering green innovation within enterprises is essential for promoting economic transformation and addressing resource and environmental challenges (Cao and Yu, 2024). Specifically, from the perspective of development models, green technological innovation enables high-quality economic growth within environmental constraints. From an industrial development standpoint, such innovations leads the way for future industry development to drive industrial upgrading and transformation. From the perspective of individual enterprise, it helps enhance the international competitiveness of their products (Du et al., 2019). Therefore, advancements in green technologies is essential for achieving sustainable development and facilitating green transformation of economies (Wan et al., 2022). As the largest developing country in the world, China has promised to fulfill its international obligation for environmental protection and has committed to achieving carbon peaking and carbon neutrality targets. Consequently, stimulating green innovation among domestic enterprises and promoting green economic transformation have emerged as critical research priorities (Xu et al., 2023).

Enterprise innovation can be categorized into two types: substantive innovation, which involves development of new products or processes that significantly alter market dynamics; and strategic innovation, which focuses on redefining business models and competitive strategies to achieve a sustainable competitive advantage. Generally, R&D costs and risks of substantive innovation are far higher than those of strategic innovation. Substantive innovation is disruptive and can fundamentally transform production processes, technological flows, and product performances. By contrast, strategic innovation mainly concentrates on improvements in aspects such as appearance design and trademarks (Li et al., 2023). Hence, it can be reasonably deduced that there exist remarkable differences in nature between substantive green innovation and strategic green innovation for enterprises. Regarding factors impacting enterprise green innovation, scholars have carried out extensive discussions from multiple levels. External factors mainly comprise government policies (Xu et al., 2024), carbon trading systems (Xi and Jia, 2025), environmental legislation (Ma and Li, 2025), financial markets (Fang et al., 2024), international trade (Liu et al., 2024), green propensity of financial system (Wang et al., 2022), and public opinion supervision from stakeholders (Song et al., 2024). Internal factors include leadership inclination (Hu and Shi, 2025), ESG responsibility (Liu et al., 2024), and corporate governance (Amore and Bennedsen, 2016). In reality, promoting enterprise green innovation requires analysis from a more macroscopic perspective. Enterprise green innovation is the outcome of dynamic interactions between the government, enterprises, and stakeholders (Dore, 1988).

However, enterprises possess more patent information than government staff, thus having the motivation to exploit this information advantage to obtain policy dividends, which might result in the generation of a green patent bubble (Xie and Wang, 2024). Hu et al. (2023), using the “Green Credit Guidelines” issued by the Chinese government as the research focus, found that enterprises tend to increase the quantity of low-quality green innovations to meet basic requirements for accessing green finance and securing green financing support (Hu et al., 2023). Zhao et al. (2024), focusing on the government’s special subsidies for R&D projects, found that government subsidies have a promoting effect on strategic green innovation. However, their impact on substantive green innovation exhibits a threshold effect. When subsidies are below the threshold, they can alleviate cash flow constraints in enterprise R&D and enhance substantive green innovation capabilities. Conversely, when subsidies exceed the threshold, enterprises may engage in policy arbitrage by exploiting information asymmetry, leading to a decline in their enthusiasm for substantive green innovation (Zhao et al., 2024). Chen and Kim (2024), through an analysis of carbon emissions trading, found that carbon trading has a direct impact on enterprise profits. Consequently, when carbon prices increase, enterprises are more likely to pursue substantive green innovation (Chen et al., 2024). These findings indicate that enterprise green innovation strategies result from rational evaluations of external regulations and internal cost-benefit analyses. Based on these assessments, enterprises will choose between substantive and strategic green innovations. Therefore, the government should tailor policy tools according to enterprises’ green innovation performance to promote greater engagement in substantive green innovation.

This paper examines the impact of high-tech certification on enterprise substantive and strategic green innovation. High-tech certification influences green innovation through multiple channels. Firstly, from a resource-based perspective, it not only reduces tax rate for certified enterprises but also enhances government subsidies (Liu et al., 2020; Li et al., 2019; She et al., 2022). These financial benefits provide enterprises with additional resources to invest in green technologies and practices, thereby promoting both substantive and strategic green innovations. Secondly, due to government’s emphasis on environmental protection, environmental protection guiding policies have been introduced for high-tech enterprises, promoting their green technological innovation. High-tech Certification enhances technological advancement of enterprises, promoting their investment in and output from green innovation (Chen et al., 2023; Liu et al., 2020). These studies have analyzed mechanisms such as tax incentives, government subsidies, and financing constraints but have not thoroughly examined the impact of high-tech certification on substantive and strategic green innovations. Consequently, further research is critically needed to address this gap and provide a comprehensive understanding of how high-tech certification influences green innovation strategies.

To summarize, this paper focuses on analyzing the influence of high-tech certification on enterprises’ substantive and strategic green innovations. By utilizing data from Chinese listed companies between 2006 and 2023, and accounting for the characteristics of the dependent variables, this study employs a zero-inflated negative binomial regression model to investigate the impact of high-tech certification on green innovation strategies, as well as its underlying mechanisms and heterogeneous effects.

The marginal contributions of this paper are primarily reflected in the following aspects. (1) From a research perspective, existing literature primarily focuses on the impact of high-tech enterprise qualification on traditional growth attributes such as total factor productivity (Pang et al., 2024) and export product quality (Chen and Chen, 2022). Although a limited number of studies have explored the effect of high-tech enterprise qualification on technological innovation and green innovation (Tang et al., 2023; Liang et al., 2025), these studies tend to be overly general and often fail to thoroughly examine the effectiveness and multidimensional nature of innovation. Specifically, corporate innovation behavior encompasses both substantive technological breakthroughs and more superficial innovations driven by strategic adjustments, such as optimizing operations or entering new markets. By distinguishing between substantive and strategic innovation, this paper systematically analyzes the driving effect of high-tech enterprise qualification on corporate green innovation. This approach not only enriches the existing literature on technological innovation and growth effects but also provides a novel theoretical perspective on green innovation. Furthermore, it contributes to a deeper understanding of the complexity inherent in green innovation. (2) In terms of research methodology, this paper employs the negative binomial regression model to empirically examine the driving effect of high-tech enterprise qualification on corporate green innovation. Although the difference-in-differences (DID) method is frequently utilized in the existing literature to assess the impact of high-tech enterprise qualification on firms (Chen and Kim, 2024; Dai and Wang, 2019), it is important to note that corporate green innovation is a count variable whose data do not meet the normal distribution assumption required by the OLS regression model (Schober and Vetter, 2021). Additionally, due to significant variations in the emphasis placed on green innovation across different firms, the data exhibit substantial overdispersion. In this context, the OLS regression model faces inherent limitations in applicability. Conversely, the negative binomial regression model is better suited to address these issues, as it introduces an additional dispersion parameter that effectively models the variance in the data, accommodating situations where the mean and variance are unequal. Consequently, the negative binomial regression model provides a more accurate fit for count data with high variance, thereby improving the model’s reliability and robustness. Particularly when green innovation is measured using the number of green patent applications, the negative binomial regression method outperforms the traditional DID approach, as it more precisely captures the influence of high-tech enterprise qualification on green innovation. Therefore, the methodological approach adopted in this paper offers a more appropriate empirical analysis framework, allowing for a more accurate measurement of the role of high-tech enterprise qualification in fostering both strategic and substantive green innovation. (3) From the perspective of an internal and external multi-factor system, this paper systematically analyzes the transmission pathways through which high-tech enterprise qualification influences corporate green innovation. Existing studies typically examine the impact of high-tech enterprise qualification on corporate behavior by focusing on a single external factor, such as government policies or the macroeconomic environment (Shan et al., 2018; Gregoire and Shepherd, 2012). In contrast, this paper not only highlights the role of external factors, such as government interventions, but also incorporates the influence of relevant stakeholders, including financial institutions and capital markets. It develops a comprehensive analytical framework that encompasses four channels: tax incentives, government subsidies, alleviation of financing constraints, and increased attention from capital markets. By integrating external policy incentives with the internal innovation motivations of enterprises, this paper deepens the understanding of the effects of high-tech enterprise qualification and uncovers its complex impact on green innovation through multiple pathways. This perspective not only expands the research scope of the existing literature but also provides a more nuanced theoretical foundation and practical guidance for policymakers and business managers.

The structure of this paper is organized as follows: chapter 2 presents the policy background and theoretical framework; chapter 3 outlines the research design; chapter 4 conducts an empirical analysis; and chapter 5 summarizes the findings, aside from providing policy recommendations and outlining future research directions.

The Chinese government has placed significant emphasis on the support of high-tech enterprises and has promulgated a series of policies, among which the core document is the “Administrative Measures for the Recognition of High-tech Enterprises.” This policy document has undergone five major development phases.

(1) During the Early Period of Reform and Opening Up (1978–1988): In 1978, China initiated extensive engagements with developed countries. Government leadership gradually recognized and reached consensus on the significant technological gap between China’s high-tech industry and that of advanced foreign nations. Therefore, corresponding policy support needed to be in place for high-tech enterprises. For this purpose, the State Council released the “Outline of the National Science and Technology Development Plan from 1978 to 1985,” proposing to attract foreign capital and to encourage domestic enterprises to transform in order to cultivate high-tech enterprises (Poo and Wang, 2015).

(2) Establishment of Zhongguancun High-tech Industrial Park (1988): Through the economic development from 1978 to 1988, a batch of high-tech enterprises with development potential had been cultivated in Beijing. To offer these enterprises special policy support, in 1988 the Beijing Municipal Government, upon the approval of the State Council, established the Zhongguancun High-tech Industrial Park. To attract high-tech enterprises to settle down in the park, the Beijing Municipal Government promulgated specialized documents, providing supportive policies including talent residency, bank loans, government subsidies, tax exemptions and preferential land supply. As a national-level high-tech development zone, Zhongguancun incubated a large number of high-quality enterprises within a short time span. After its example, other local governments followed suit in quick succession. Various types of high-tech parks were subsequently established nationwide, and local governments introduced region-specific preferential policies (Zhu and Tann, 2005).

(3) The Formation of the Policy System (1991): In 1991, the central government concluded the initiatives by summarizing the experience and lessons learnt from establishing the various high-tech parks, and in an effort to direct future industrial development, promulgated the “Conditions and Measures for the Recognition of High-tech Enterprises in National High-tech Industrial Development Zones.” This document focused on enterprises within national-level high-tech parks, selected eight industries including information technology and new energy, and awarded high-tech enterprise certification to those enterprises that met the standards based on sales revenue and research and development expenses. This policy document signified that high-tech enterprise certification received governmental endorsement nationwide, significantly helping enhance the credibility of enterprises (Yan et al., 2024).

(4) Policy popularization (2008): Between 1991 and 2008, domestic high-tech enterprises experienced significant growth, with a substantial number of promising enterprises emerging outside the parks. In response to the global financial crisis, traditional industries faced significant export challenges, which highlighted the urgent need to prioritize the development of high-tech industries within the country. In 2008, the Ministry of Science and Technology, in collaboration with the Ministry of Finance and the State Taxation Administration, jointly issued the “Administrative Measures for the Recognition of High-tech Enterprises.” Key features of these measures are: Recognizing enterprises outside national high-tech development zones for the first time, and encouraging local governments to formulate corresponding supportive policies; Easing application standards and industry restrictions for enterprises; Clarifying preferential tax policies, setting income tax rate for qualified enterprises at 15%, in contrast with 25% for general enterprises. This measure significantly relieved cash flow pressure on enterprises (Liu et al., 2020).

(5) Introduction of Special Support Policies (2016): In 2016, the Ministry of Science and Technology, in collaboration with other relevant departments, revised the “Administrative Measures for the Recognition of High-tech Enterprises” once again. The revision further relaxed standards for the recognition of high-tech enterprise certification, specifically by introducing special support policies for small and medium-sized enterprises (SMEs). This adjustment aimed to lower entry threshold for SMEs, encourages greater participation in high-tech innovation, thereby facilitating industrial upgrading and economic transformation nationwide.

To sum up, the optimization and refinement of high-tech enterprise certification policy not only facilitate technological innovation of enterprises at the policy level but also offer the academic community abundant research domains and theoretical development opportunities.

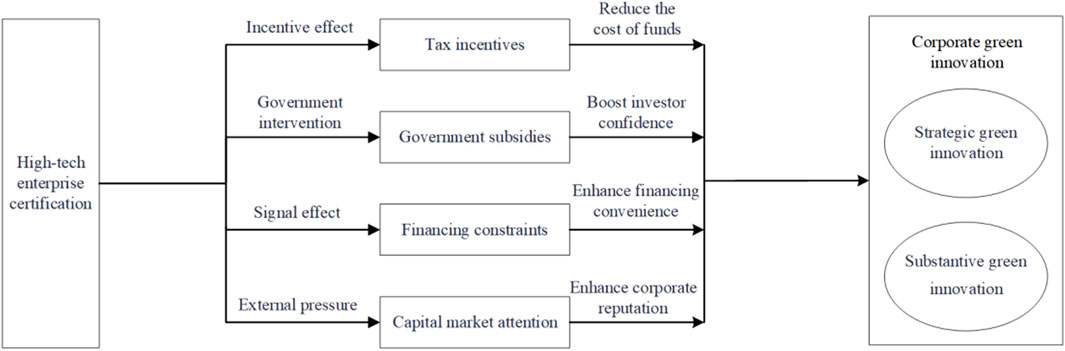

Under the current policy environment, the government has introduced a series of supportive policies for enterprises that have obtained high-tech certification. Concurrently, the state places significant emphasis on green transformation of the economy and has established corresponding social responsibility requirements for high-tech enterprises, highlighting their critical role in actively contributing to the country’s green transformation (Liu et al., 2020). As a result, high-tech certification not only influences enterprise R&D investment but also facilitates green technological innovation (Chen et al., 2023). This paper provides a comprehensive analysis of the impact of high-tech certification on substantive and strategic green innovations from two perspectives: direct effects and action mechanisms. Specifically, these action channels include tax preferences, government subsidies, financing constraints, and capital market attention. The research framework is illustrated in Figure 1.

Figure 1. Theoretical analysis framework.

According to the Resource-Based View (RBV) theory, the capabilities of an enterprise originate from its accessible resources. Hence, the green innovation capabilities of an enterprise are closely associated with its resource foundation (Barney, 1991). High-tech certification, as a strategic resource for enterprises, is both authoritative and scarce. Enterprises have to meet rigorous standards to acquire them. This certification not only represents government endorsement (Bitektine, 2011) but also conveys positive signals to the external environment, assisting enterprises in obtaining external support such as banks and venture capital investment, thereby facilitating R&D activities and promoting greener innovations (Dai and Wang, 2019).

However, an issue of information asymmetry exists between the government and enterprises (Millar et al., 2012). On one hand, when allocating resources to enterprises, the government sets fundamental requirements for their green innovation performance. On the other hand, enterprises face significant challenges in green innovation: substantive green innovation, as opposed to strategic green innovation, demands more resources and a longer R&D cycle, and entails a higher risk of failure (Bi et al., 2024). Hence, under the constraints of internal resources and the asymmetry of external information from the government’s side, enterprises have more incentive to engage in policy arbitrage. Furthermore, there is internal agency risk within companies to consider. In pursuit of performance the management tends to prioritize the quantity of innovation at the expense of its quality exploiting investors’ lack of information (Jia et al., 2019), thereby giving rise to the emergence of a green patent bubble.

Based on the above, we put forward the following hypothesis:

Hypothesis 1. High-tech certification is capable of promoting enterprises’ green innovation, and the promoting effect on strategic green innovation is greater than that on substantive green innovation.

Based on Chinese legal provisions, enterprises can enjoy preferential tax rates upon obtaining high-tech certification, thereby alleviating their tax burden. Saved funds can be redirected toward green innovation initiatives (Wang H. et al., 2024). Jia and Ma (2017) analysed data from Chinese listed companies between 2007 and 2013, demonstrating that tax preferences can effectively encourage corporate R&D expenditure. Since tax preference to high-tech enterprises is a right explicitly stipulated by national law, enterprises have no motivation for policy arbitrage. In addition, in accordance with the current tax law, R&D expenses of enterprises can be deducted from taxable income. The greater the R&D expenses are, the larger the amount of tax that can be deducted. By definition, substantial green innovation demands a longer R&D cycle and higher investment. Institutional rationalization of corresponding R&D expenses effectively incentivizes enterprises to undertake significant green innovation initiatives.

Based on the above, we put forward the following hypothesis:

Hypothesis 2. High-tech certification enhances green innovation capacity of enterprises by reducing their tax burden, and the promoting effect of tax preferences on substantive green innovation is greater than that on strategic green innovation.

High-tech certification enhances the competitive advantage of enterprises, thereby facilitating them to obtain more government subsidies. These subsidies can effectively alleviate the issue of financial shortage for enterprises in green innovation (Shao and Chen, 2022). Generally, the stronger the fiscal autonomy of local governments is, the greater the amount of subsidies granted to enterprises will be. Hence, government subsidies are to some extent an unstable source of income for enterprises. Nevertheless, substantive green innovation demands a considerable amount of resources and long-term stable investment. Therefore, only when government subsidies reach a certain scale and last for a duration of time can they significantly help enhance innovation efficiency of enterprises (Wu et al., 2024). Ying et al. (2023) examined the impact of government R&D subsidies on Chinese new energy listed companies and found that enterprises often exploit loopholes in the subsidy system and the inadequate review capabilities of officials, thereby prioritizing strategic green innovation.

Based on the above, we put forth the following hypothesis:

Hypothesis 3. High-tech certification facilitates enterprise green innovation by augmenting government subsidies, and the facilitating effect of government subsidies on strategic green innovation is greater than that on substantive green innovation.

High-tech certification of enterprises effectively boosts their political connectivity, reduces tax burdens and augments government subsidies (Cheng et al., 2019). Government subsidies not only enhance the creditworthiness of enterprises (Meuleman and Maeseneire, 2012), but also convey positive signals to venture capitalists, thereby escalating financing opportunities for enterprises (Wu, 2017). In regions where the credit system is defective, governmental certification and endorsement significantly heighten the likelihood of enterprises obtaining bank loans (Li et al., 2019). Consequently, high-tech certification contributes to alleviating financing constraints on enterprises.

From the perspective of financial institutions such as banks, which operate in a more market-oriented mode, banks have a more pronounced motivation than the government to evaluate the green innovation strategies of enterprises and determine whether to provide financing. Therefore, although substantive green innovation requires a longer R&D cycle, it can assist enterprises in gaining a competitive edge over their counterparts (Jiang and Bai, 2022). Consequently, as the financing constraints on enterprises are alleviated, they are more likely to opt for substantive green innovation to secure long-term financing advantages.

Based on the above, we put forth the following hypothesis:

Hypothesis 4. High-tech certification facilitates enterprise green innovation by alleviating financing constraints, and the facilitating effect on substantive green innovation is greater than that on strategic green innovation.

The attainment of high-tech certification demands that enterprises fulfil certain requirments. Hence, obtaining such certification can enhance an enterprise’s visibility in the capital market (Min et al., 2022). The influence of the capital market on an enterprise’s green innovation presents a complex pattern. On one hand, at present, corporate social responsibility and ESG performance are the focus of attention in the capital market. Negative information can directly impact an enterprise’s reputation and stock price. Thus, the attention from the capital market can exert external pressure to push enterprises to undertake green innovation (Spyros, 2022; Nguyen et al., 2023). On the other hand, the current Chinese capital market is relatively deficient in long-term investors and is inundated with short-term investors who require enterprises to continuously provide stock price promoting news. When comparing substantive green innovation and strategic green innovation, enterprises tend to select strategic green patents that have lower costs and are equally capable of signifying to the capital market within a short period (Ji et al., 2021). Short-term arbitrageurs in the capital market often utilize such information for securities speculation and short-term arbitrage. In contrast, substantive green innovation requires a longer period to release information to the capital market and has a higher risk of R&D failure (Ning, 2018). Therefore, though pressure from the capital market can promote enterprise green innovation, the scarcity of long-term value investors in the market may contribute to the formation of a green patent bubble.

Based on the above, this study puts forward the following hypothesis:

Hypothesis 5. High-tech certification facilitates enterprise green innovation by heightening attention from the capital market, and the facilitating effect on strategic green innovation is greater than that on substantive green innovation.

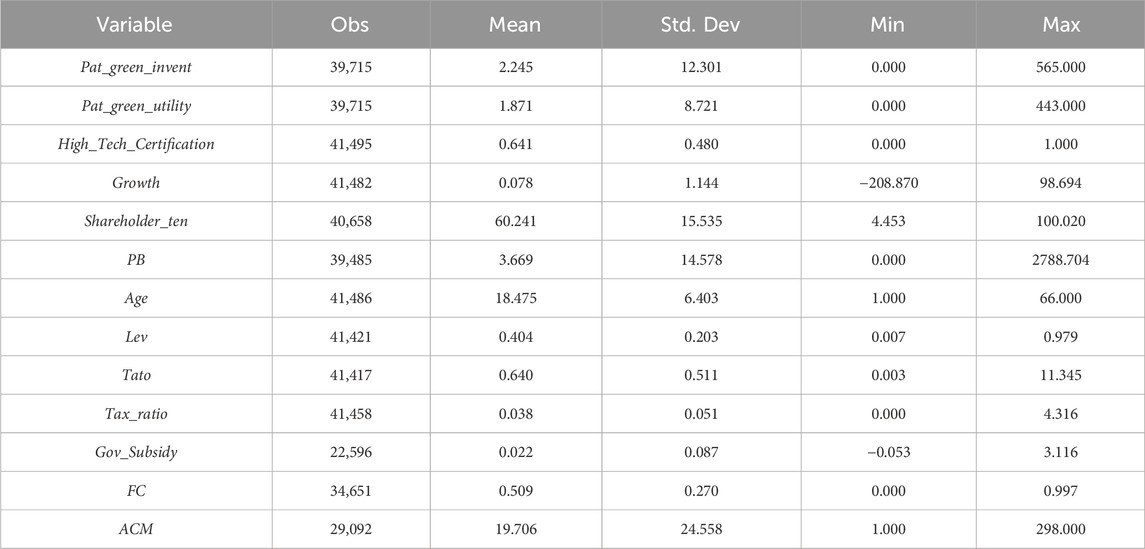

We examine the impact of high-tech enterprise certification on both substantive and strategic green innovation through an empirical analysis of data from Chinese A-share listed companies spanning 2006 to 2023. Green innovation data are sourced from the CNRDS database, whereas data on high-tech enterprise certification, control variables, and mediating variables are obtained from the CSMAR database. To guarantee the accuracy of the research findings, the data underwent rigorous screening and cleaning: Firstly, company samples that have been marked as ST, *ST, or PT in the securities market were eliminated. Secondly, companies at the brink of financial warning, namely those with liabilities exceeding assets, negative operating profits or net profits, and those relying on government tax rebates for operation (indicated by negative taxes), were excluded. Finally, the impact of financial factors was mitigated by removing the samples of companies listed on both A and B shares. Furthermore, the control variables and mediating variables were subjected to winsorization to mitigate the potential impact of extreme values on the analysis results. We use the number of green patent applications filed by listed companies as an indicator to measure corporate green innovation.

The dependent variable in this study is enterprise green innovation. Following the research of Zhao and Sun (2025) and Zhang et al. (2024), we use the number of green invention patent applications to measure substantive green innovation and the number of green utility model patent applications to measure strategic green innovation (Zhao and Sun, 2025; Zhang et al., 2024). In subsequent robustness tests, we employ the number of granted patents for analysis.

In this study, the independent variable is whether an enterprise acquires high-tech enterprise certification. Drawing on She et al. (2022), based on data from the CSMAR database, if a listed company is approved by the National High-tech Enterprise Certification Group, this variable is set to 1 in the year of approval and subsequent years. Otherwise, it is set to 0. With reference to the research of Liu et al. (2020) and Chen et al. (2023), we employ the following indicators to measure the distinct features of enterprises: the sustainable growth rate (Growth), which is utilized to evaluate the development potential of enterprises; the shareholding ratio of the top ten shareholders (Shareholder_ten), which is employed to measure the equity concentration of enterprises; the price-to-book ratio (PB), which is used to reflect the valuation expectations of the capital market for listed companies; the enterprise age (Age), which is adopted to measure the operating years of enterprises; the debt-to-asset ratio (Lev), which is utilized to measure the financial leverage level of enterprises; the total asset turnover (Tato), which is employed to measure the operating efficiency of enterprises. Referring to existing studies (Lu and Cheng, 2024; Li et al., 2023; Abbas et al., 2023; Wang et al., 2024b), we investigate its mechanism of action from the following four aspects. (1)Tax Incentives: tax reduction policies enjoyed by enterprises are measured by tax rate (Lu and Cheng, 2024); (2)Subsidy: it refers to direct financial support that enterprises obtain from the government, represented by the total amount of government subsidies specified in financial statements of the current year (Li et al., 2020); (3) Financing constraints: it reflects the degree of difficulty for enterprises to obtain financial support from financial institutions (such as banks), and is characterized by the cash flow ratio (Abbas et al., 2023); (4) Attention in capital markets (ACM): the popularity of enterprises in the capital market is measured by the frequency of analysis of enterprises in research reports of financial institutions (Wang et al., 2024a).

The data of the mediating variables are derived from the CSMAR database, and the descriptive statistics of the main variables are presented in Table 1.

Table 1. Descriptive statistics of the main variables.

The dependent variables in this paper are substantive green innovation and strategic green innovation of enterprises, measured by the number of green invention patent applications and the number of green utility patent applications, respectively. Given that these dependent variables are typical count data, count models are preferred for analysis. Common count models include Poisson regression model and negative binomial regression model. The dependent variables in this study exhibit two key characteristics: First, the variance of the dependent variables significantly exceeds the mean, indicating an over-dispersed distribution; second, there is a substantial number of zero values in the dependent variables (Endawkie et al., 2024; Zhou et al., 2024; Zhang et al., 2024). Based on these characteristics, we prioritize the zero-inflated negative binomial regression model. The specific settings are as follows:

In Equations 1, 2, The subscript i represents the code of the listed company in the A-share market, and the subscript t represents the corresponding year of the listed company. Pat_green_invent denotes substantive green innovation, measured by the number of applications for green invention patents; Pat_green_utility indicates strategic green innovation, measured by the number of applications for green utility patents. The variable is employed to measure whether the enterprise has obtained certification of a high-tech enterprise. If it has, it is set to 1; otherwise, it is set to 0. In the model,

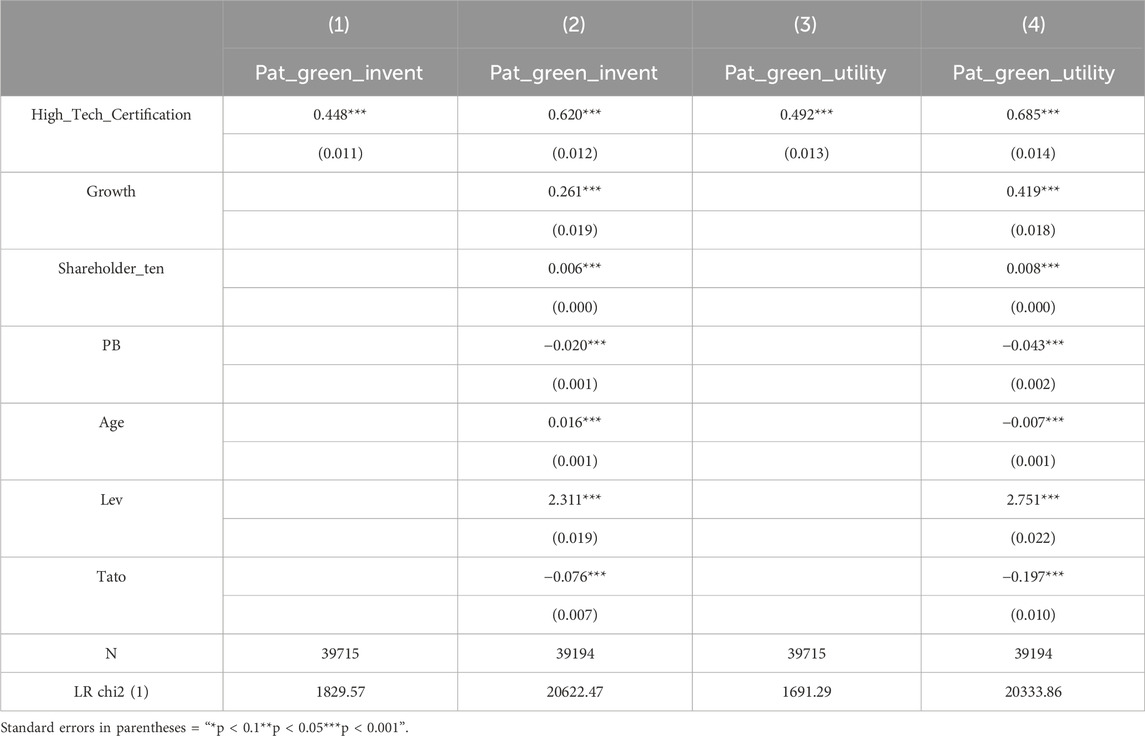

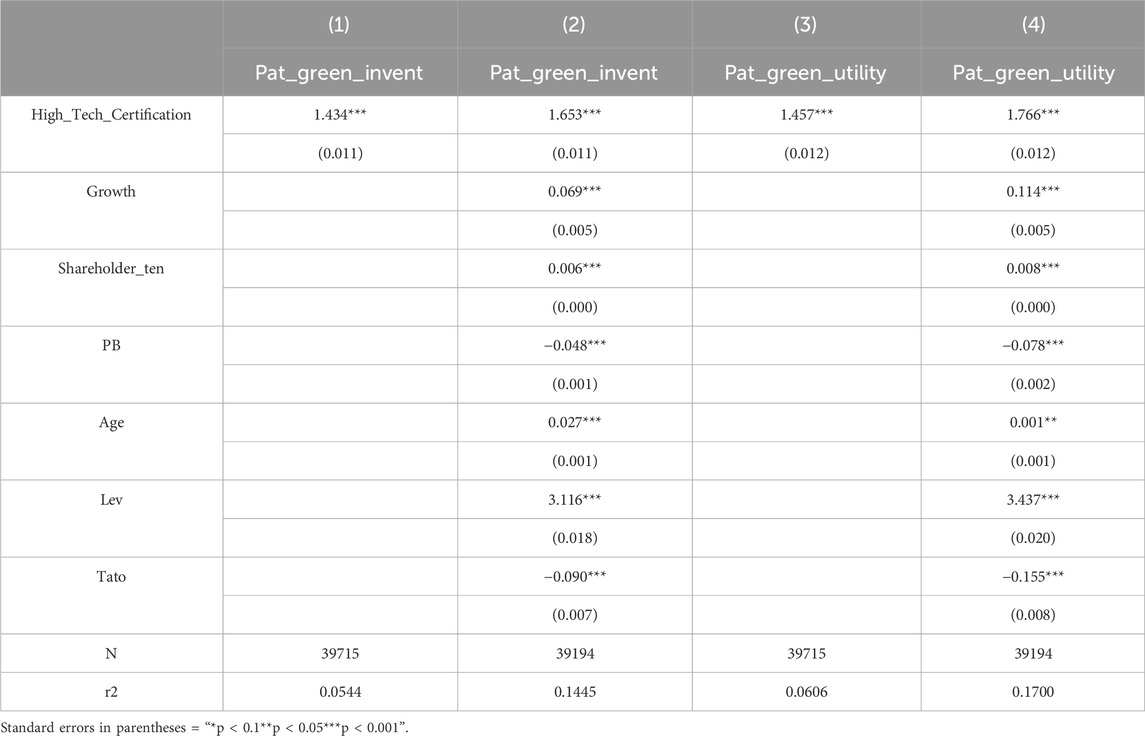

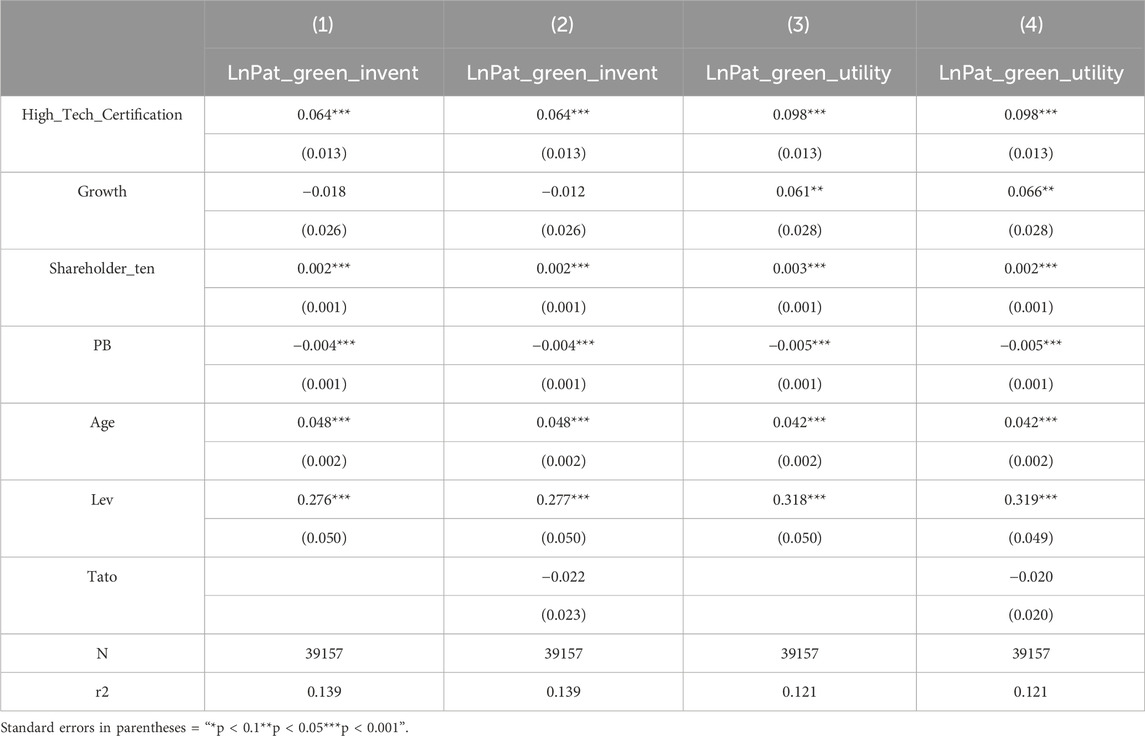

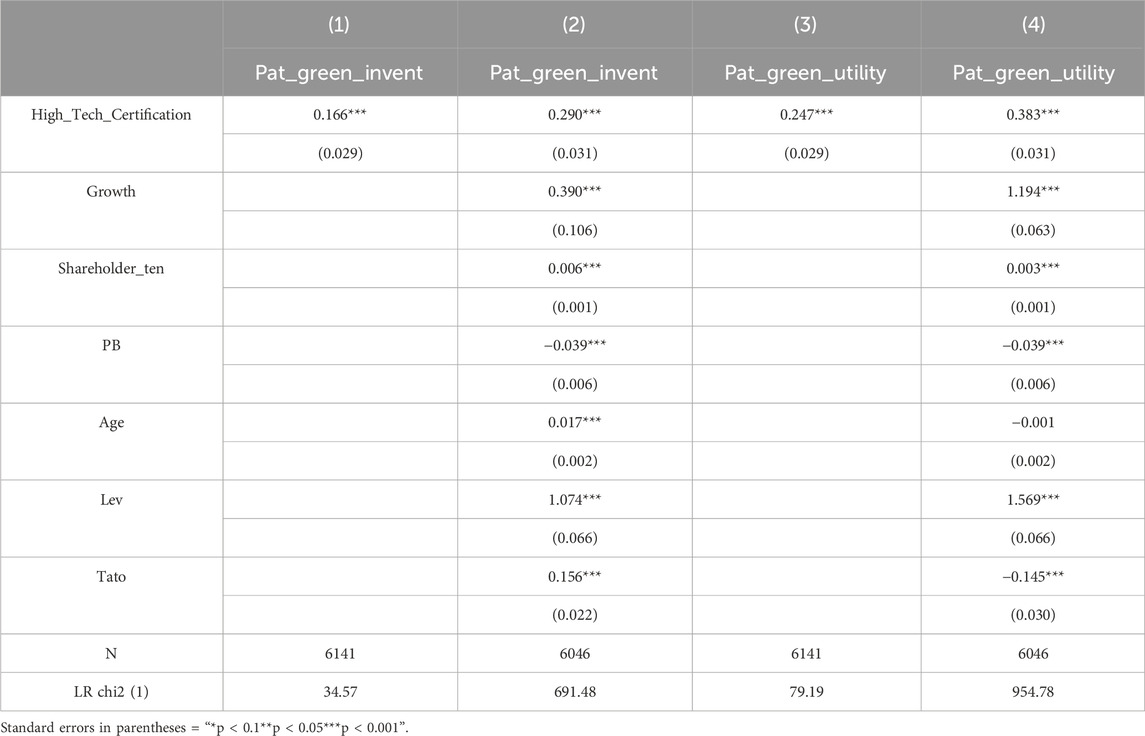

The benchmark testing outcomes of this study are summarized in Table 2. Columns 1 and 2 report the regression results for Equation 1, showing the effect of high-tech certification on substantive green innovation. Columns 3 and 4 report the regression results for Equation 2, showing the effect of high-tech certification on strategic green innovation. Regression results indicate that the coefficient of High_Tech_Certification is positive and significant at the 1% level, suggesting a substantial promoting effect of high-tech certification on enterprises’ green innovation. Further comparison of the coefficients reveals that the promoting effect on strategic green innovation is notably greater than that on substantive green innovation. This finding suggests the potential presence of green patent bubbles within enterprises. Specifically, high-tech certification can offer enterprises tax preferences, government subsidies, and can help alleviate their financing constraints and enhance their visibility in the capital market. These policy benefits will stimulate green innovation competition among enterprises, thereby augmenting the quantity of green patents held by enterprises. From individual enterprise’s perspective, on the one hand, they will try to balance the costs and benefits of green innovation: substantive green innovation involves higher R&D costs, longer durations, and greater risks, while strategic green innovation has lower R&D costs, shorter periods, and smaller risks; on the other hand, enterprises will exploit their information advantage over the government and give priority to the development of strategic green innovation to obtain more policy support. Hence, although high-tech certification facilitates green innovation, they may also trigger a green patent bubble (Xue et al., 2024). Therefore, Hypothesis 1 is verified.

Table 2. Baseline regression result.

From the aspect of control variables, the coefficient of the enterprise’s sustainable growth rate (Growth) is significantly positive and highly significant at the 1% level. This suggests that the higher the growth rate of an enterprise is, the more optimistic the external expectations for its future, thereby enhancing the enterprise’s financing capacity and enabling it to acquire more resources for research and development (He, 2021). On the other hand, enterprises will plan green innovation based on future development trends. The more optimistic future development prospects are, the greater the emphasis enterprises will place on green innovation. To maintain external information transparency and market image, enterprises will give priority to the development of strategic green patents. The coefficient of enterprise equity concentration (Shareholder_ten) is also significantly positive and highly significant at the 1% level. Given the high-risk nature of green innovation investment, internal consensus is essential. Higher equity concentration enhances the supervisory role of major shareholders over management, thereby reducing agency costs and facilitating internal consensus within individual enterprise (Zhang and Zhang, 2022). Under the current guidance of green policies, this consensus is more likely to align with policy objectives and promote green innovation. Moreover, in the face of limited resources, enterprises prioritize strategic green innovation to promptly respond to policy demands. The coefficient of the enterprise’s age (Age) is also significantly positive and highly significant at the 1% level. This indicates that the longer the operating years of a company are, the more experience it accumulates in research and development and the stronger its financing ability (Yang et al., 2023). Against this backdrop, enterprises will pay greater attention to future development and tend to focus on substantive green innovation, while relatively reducing investment on strategic green innovation.

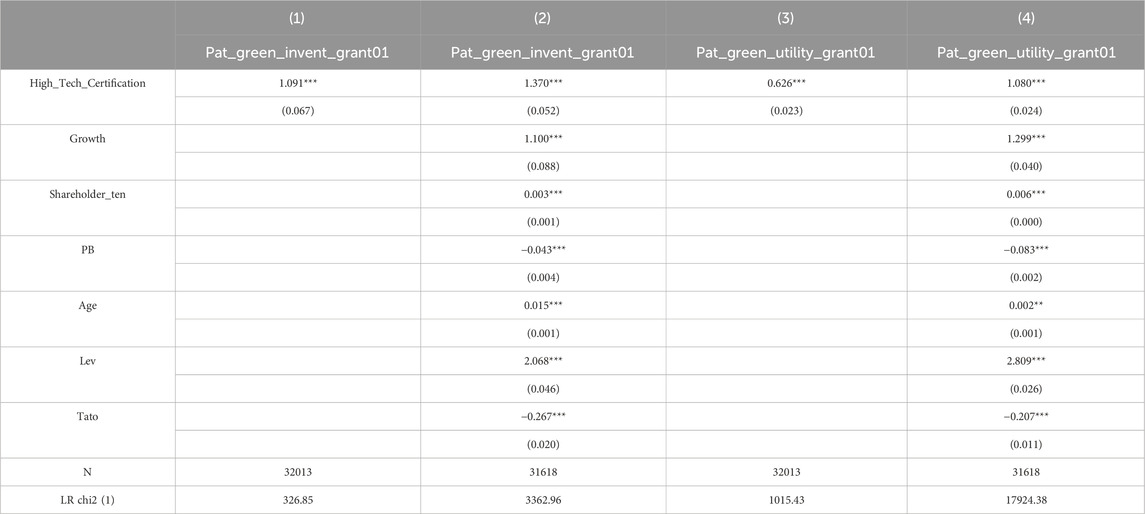

To ensure the robustness of the research findings, firstly, considering that the explained variable is the number of applications for green patents, in this paper the explained variable is replaced and the number of granted green patents is used for analysis. From patent application to authorization, it needs to undergo the review of relevant government departments, and this process encounters two major issues: one is that the review period is relatively long, especially for patent applications of complex technologies; the other is that not all patent applications can be granted. Therefore, in this paper, the number of granted patents lagged by 1 year is employed as the outcome variable for regression analysis. In conjunction with the data analysis in Table 3, it can be observed that among the strategic green patent applications submitted by enterprises, a considerable proportion ultimately failed to obtain patent authorization. This suggests that enterprises may be inclined to leverage the policy advantages brought by the certification of high-tech enterprises, resulting in the occurrence of the green patent bubble phenomenon.

Table 3. Replace the explained variable.

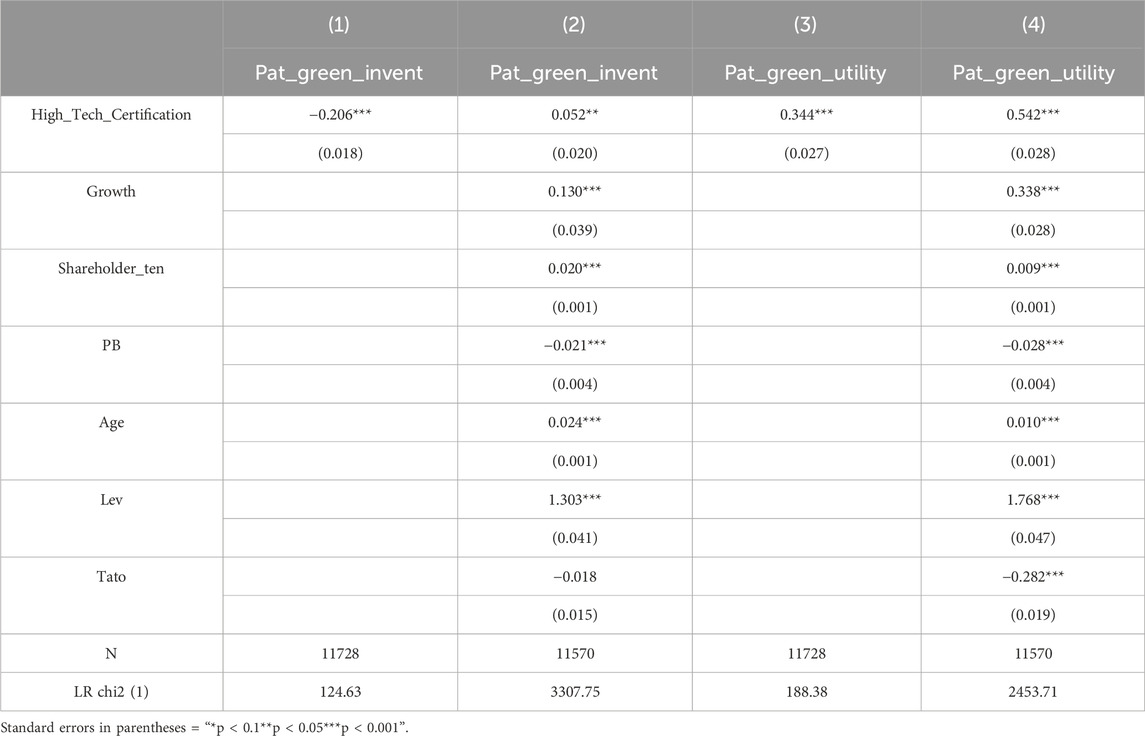

From the perspective of the dependent variable, the number of green patent applications is a typical count data. Therefore, in the robustness analysis, we substituted the original zero-inflated negative binomial regression model with a Poisson regression model for examination (Gu et al., 2025). Results are presented in Table 4. The results indicate that coefficient of the core explanatory variable High_Tech_Certification is positive and significant at the 1% level, suggesting that high-tech certification has a significant promoting effect on enterprises’ green innovation. By comparing columns 1 and 3 with columns 2 and 4, we find that the impact of high-tech certification on strategic green innovation is greater than that on substantive green innovation, and this conclusion is confirmed in the robustness test.

Table 4. Poisson method.

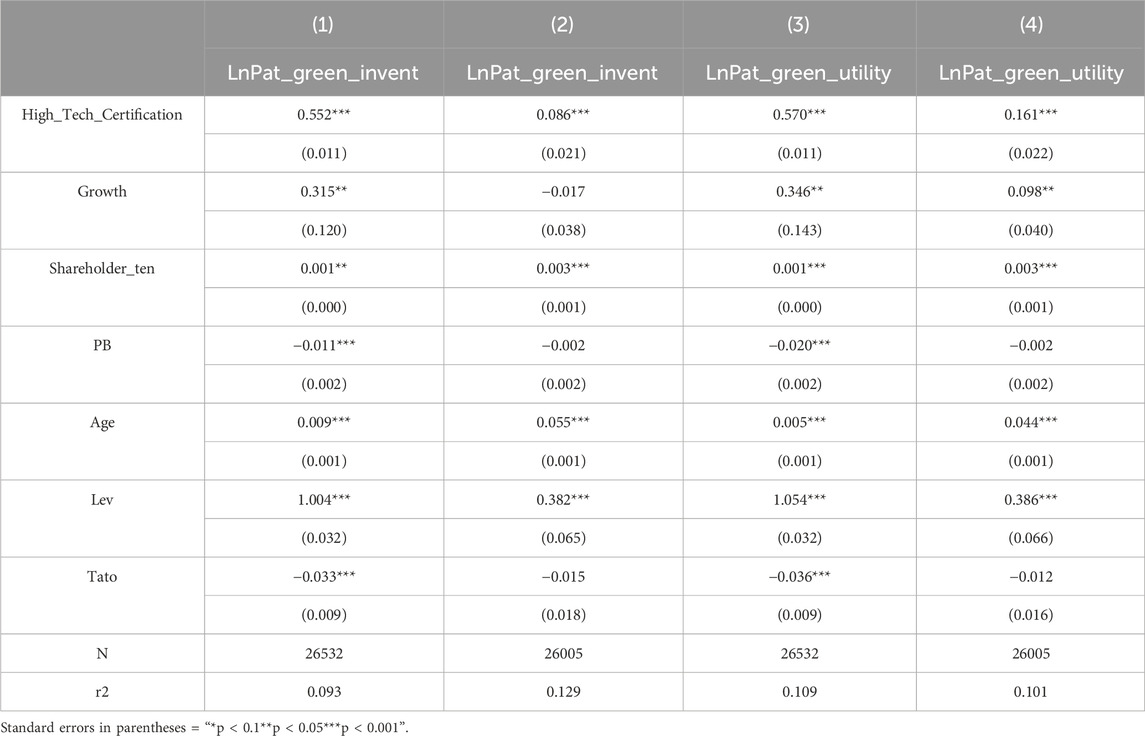

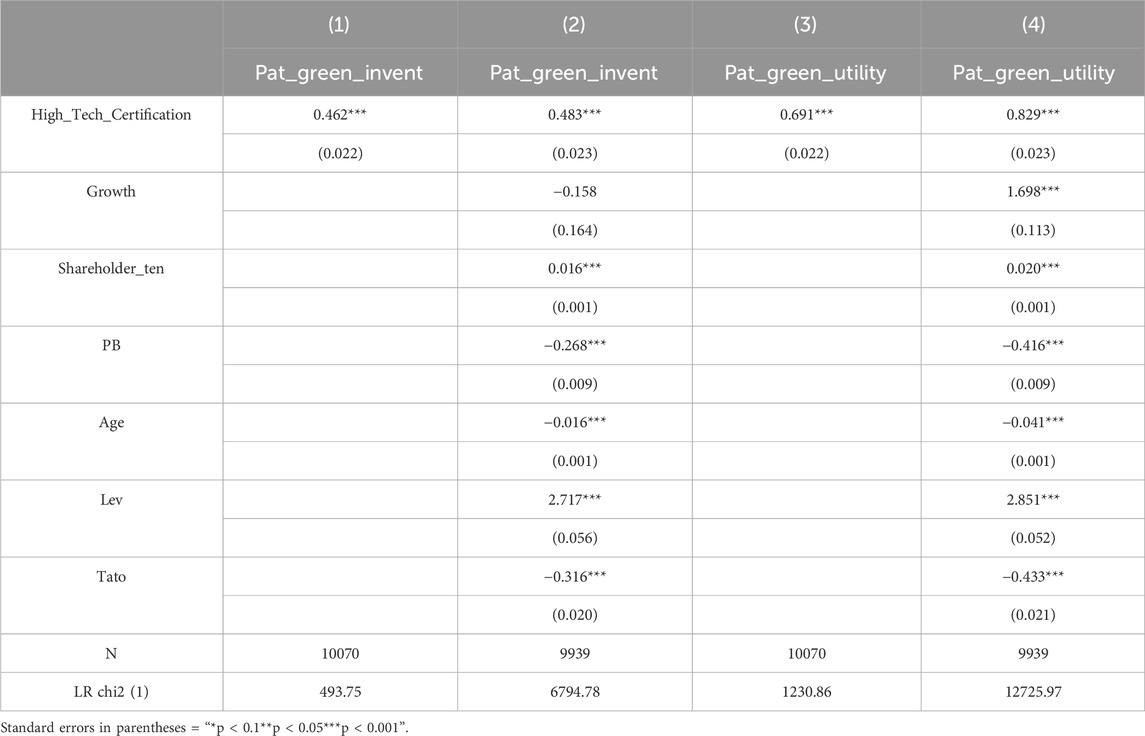

Drawing on Wang et al. (2022b), this study conducts a robustness test by altering the dependent variable. Specifically, the natural logarithm of the number of patent applications plus one is used to measure green innovation. The instrumental variable approach requires selecting appropriate instrumental variables from the control variables. From an enterprise perspective, the asset-liability ratio reflects financial leverage and risk, thereby influencing growth rate, price-to-book ratio, and total asset turnover. Therefore, the lagged one-period and two-period asset-liability ratios are utilized as instrumental variables in this study. Results are presented in Table 5, where Columns 1 and 3 use the system GMM regression method, and Columns 2 and 4 employ the panel instrumental variable method. The results indicate that coefficient of the core explanatory variable High_Tech_Certification is positive and significant at the 1% level. Moreover, the promoting effect of high-tech certification on strategic green innovation is stronger than that on substantive green innovation, confirming this conclusion in the robustness test.

Table 5. Instrumental variable method.

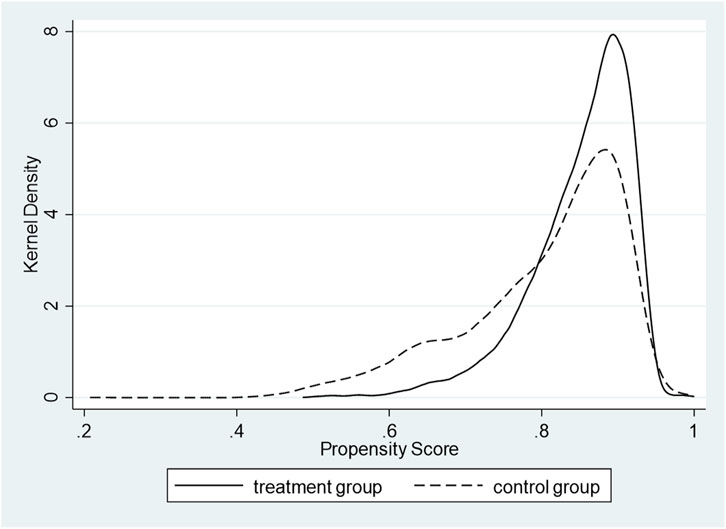

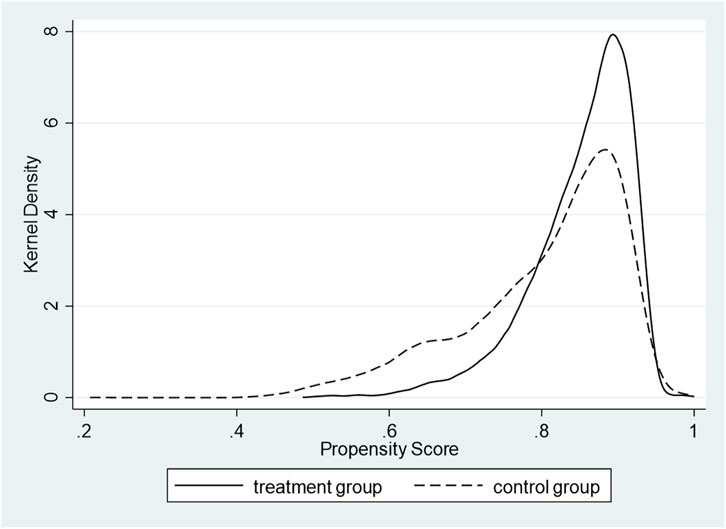

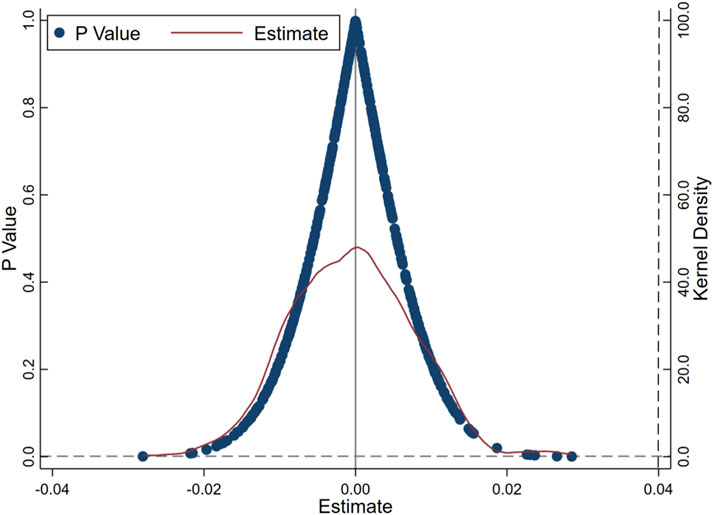

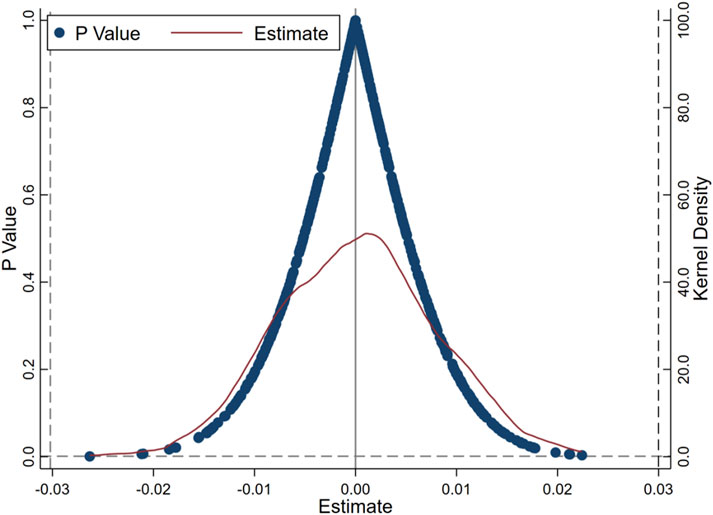

Referring to the study of Ye et al. (2024), we adopt the PSM-DID approach for robustness analysis. Results after data matching are depicted in Figures 2, 3. Outcomes of the PSM-DID approach are presented in Table 6. The results reveal that coefficient of the core explanatory variable, High_Tech_Certification, is positive and significant at the 1% level. Furthermore, the promoting effect of high-tech Certification on strategic green innovation is stronger than that on substantive green innovation, suggesting that the benchmark regression results exhibit considerable robustness.

Figure 2. PSM-DID (lnPat_green_invent).

Figure 3. PSM-DID (lnPat_green_utility).

Table 6. PSM-DID method.

In this paper, a placebo test is carried out by establishing virtual policies. Specifically, samples are randomly selected from the data to generate virtual policies, and this process is repeated 500 times to obtain corresponding policy coefficients (Xiao et al., 2023; Duan et al., 2023). Figure 4 displays the placebo test results for substantive green innovation, while Figure 5 presents those for strategic green innovation. The outcomes reveal that coefficients of the virtual policies show a normal distribution and significantly differ from the actual policy coefficients, further verifying the validity of the placebo test.

Figure 4. Placebo test (lnPat_green_invent).

Figure 5. Placebo test (lnPat_green_utility).

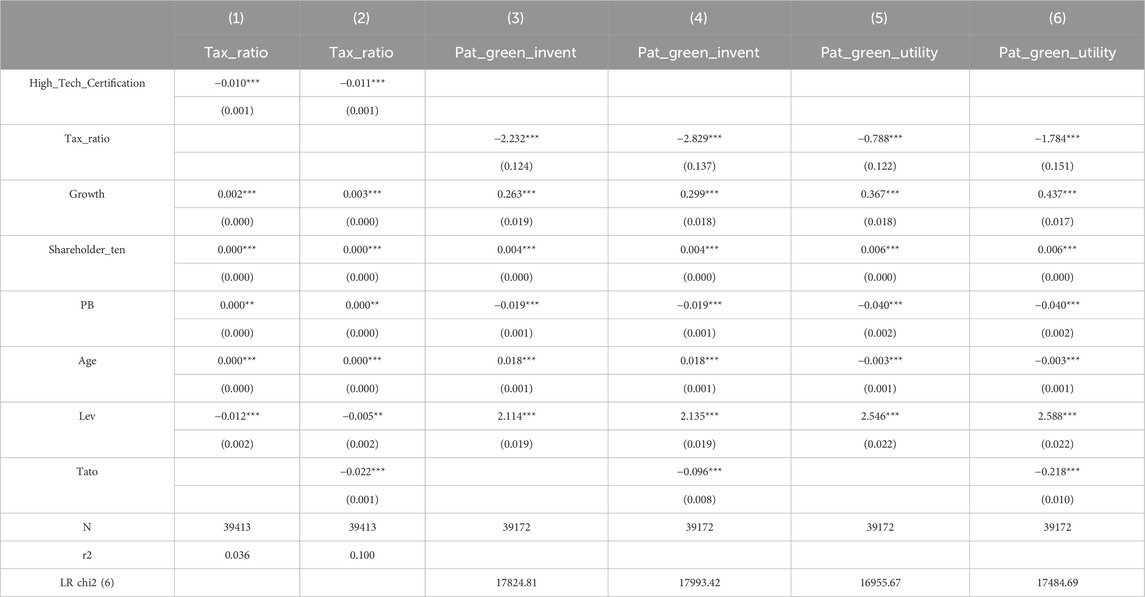

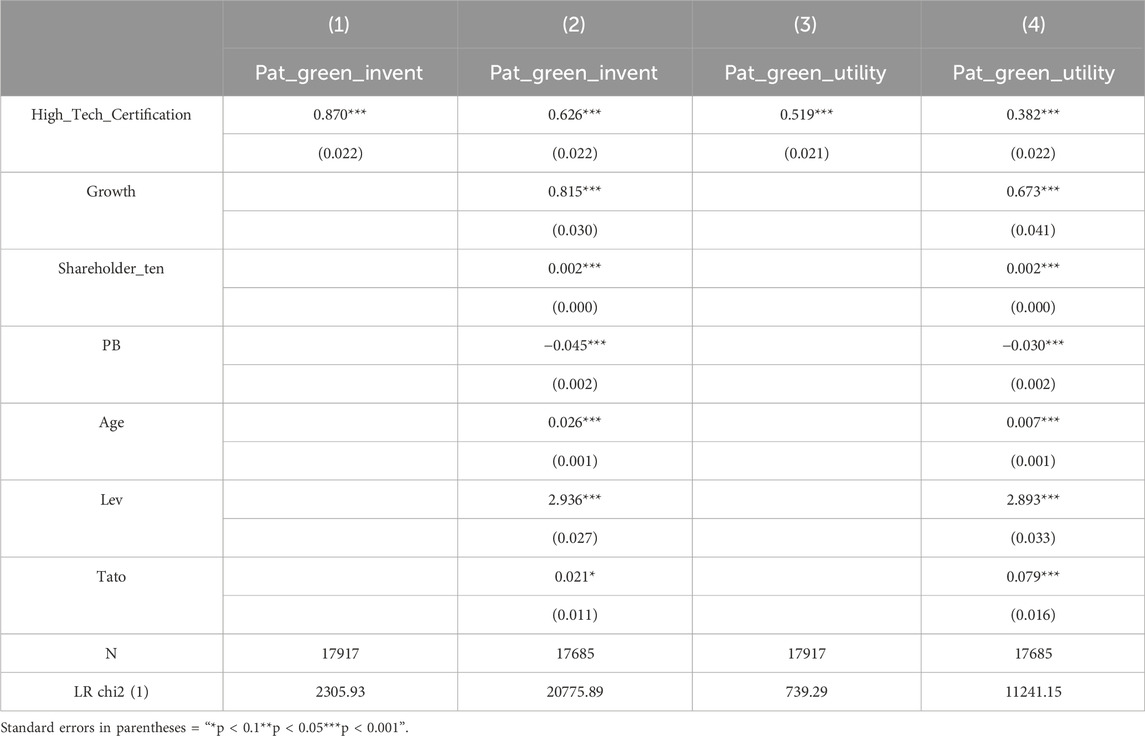

The impact mechanism of tax rates is summarized in Table 7. In accordance with national laws and regulations, enterprises obtaining high-tech certification are eligible for preferential tax policies. Columns 1 and 2 of Table 7 reveal that high-tech certification significantly lowers the tax rate of enterprises. Columns 3 and 4 present the influence of tax rates on substantive green innovation, while columns 5 and 6 show the impact of tax rates on strategic green innovation. The results demonstrate that reduced tax rate can effectively promote green innovation. By comparing the various coefficients, it is observed that the promoting effect of reduced tax rate on substantive green innovation is stronger than that on strategic green innovation. This finding suggests that the guiding role of tax rates on green innovation has a favorable impact on enterprises, indicating that the government should further optimize green tax policy to stimulate technological innovation. Therefore, Hypothesis 2 is verified.

Table 7. Mechanism test (Tax_ratio).

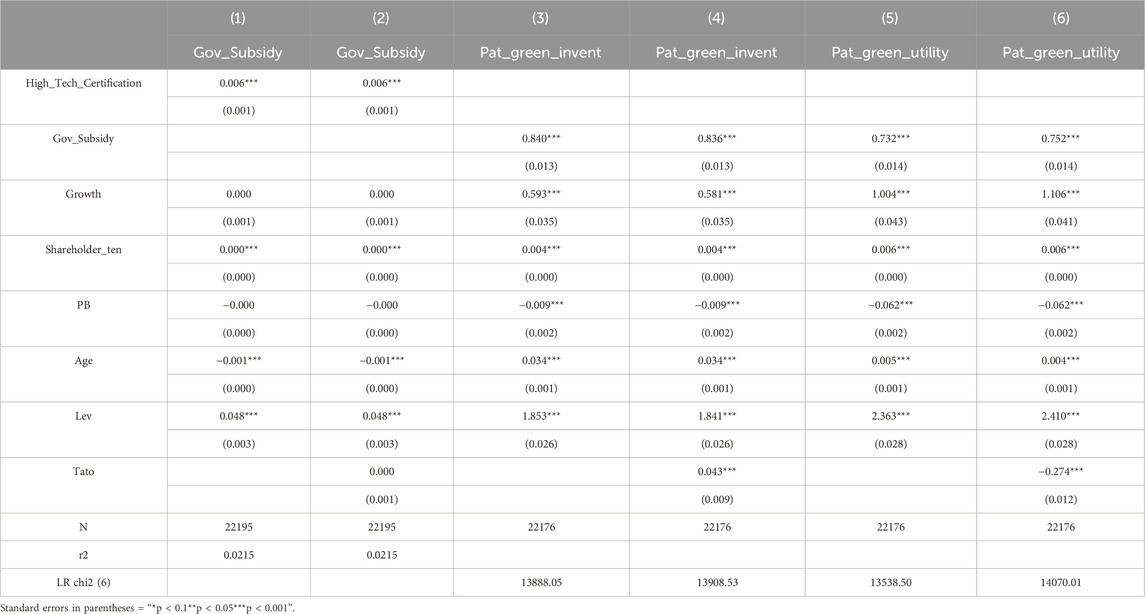

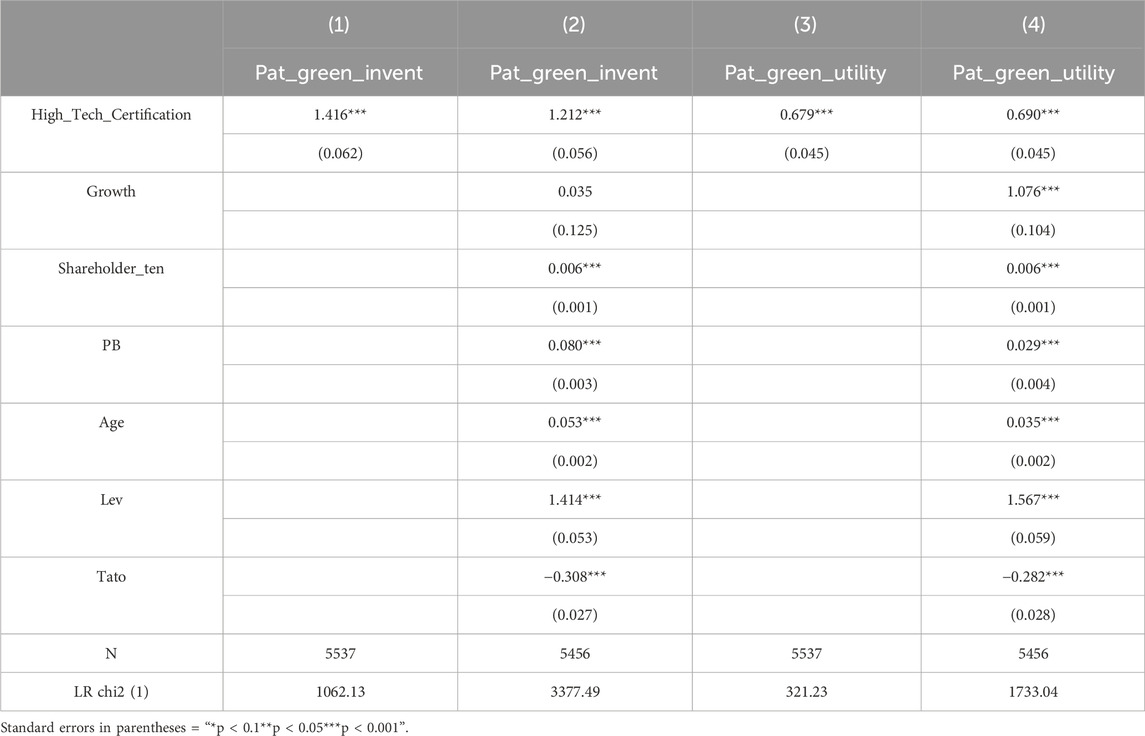

The influence mechanism of government subsidies is summarized in Table 8. Columns 1 and 2 indicate that enterprises can acquire more government subsidies after obtaining high-tech certification. Columns 3 and 4 present the effect of government subsidies on substantive green innovation, while columns 5 and 6 show their impact on strategic green innovation. The results reveal that government subsidies significantly boost enterprises’ green innovation, with a stronger promoting effect on substantive green innovation compared to strategic green innovation. This outcome is closely linked to the current management policies for government subsidies: within the existing policy framework, there is a repeated game relationship between the government and enterprises, where the government allocates subsidies for the next development stage based on enterprises’ green innovation performance. In this mechanism, enterprises tend to utilize these subsidies for substantive green innovation to secure additional government support. Therefore, Hypothesis 3 is verified.

Table 8. Mechanism test (Gov_Subsidy).

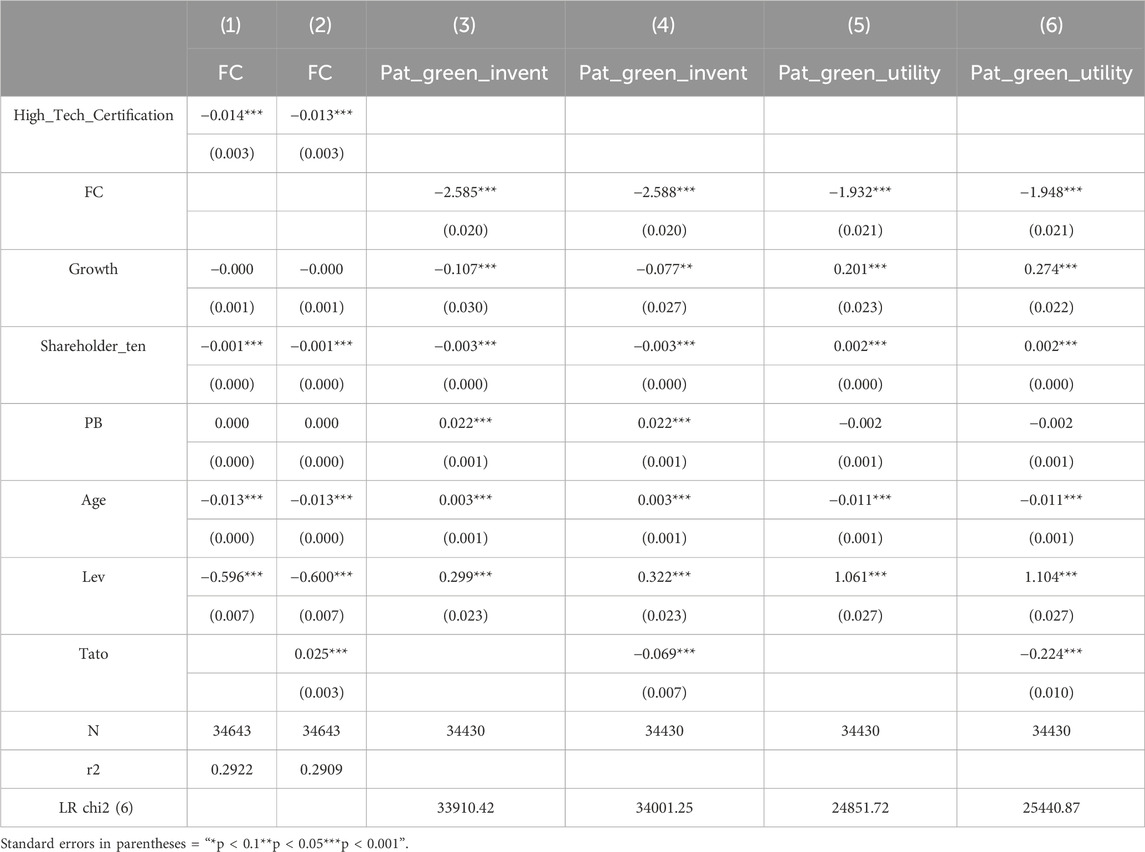

The influence mechanism of financing constraints is recapitulated in Table 9. Columns 1 and 2 indicate that enterprises markedly alleviate financing constraints subsequent to obtaining high-tech certification. Columns 3 and 4 illustrate the effect of high-tech certification on substantive green innovation, while Columns 5 and 6 delineate their influence on strategic green innovation. From the viewpoint of financial institutions, they are mandated to enforce green credit policies by the government. Consequently, financial institutions represented by banks are more predisposed to supporting enterprises with commendable green innovation performance. Under such a policy milieu, high-tech certification efficaciously mitigates the financing constraints of enterprises. Once enterprises receive support from banks and other financial institutions, they are obliged to fulfill policy requisites of these institutions, thereby more prone to undertaking substantive green innovation rather than strategic green innovation. Therefore, Hypothesis 4 is verified.

Table 9. Mechanism test (FC).

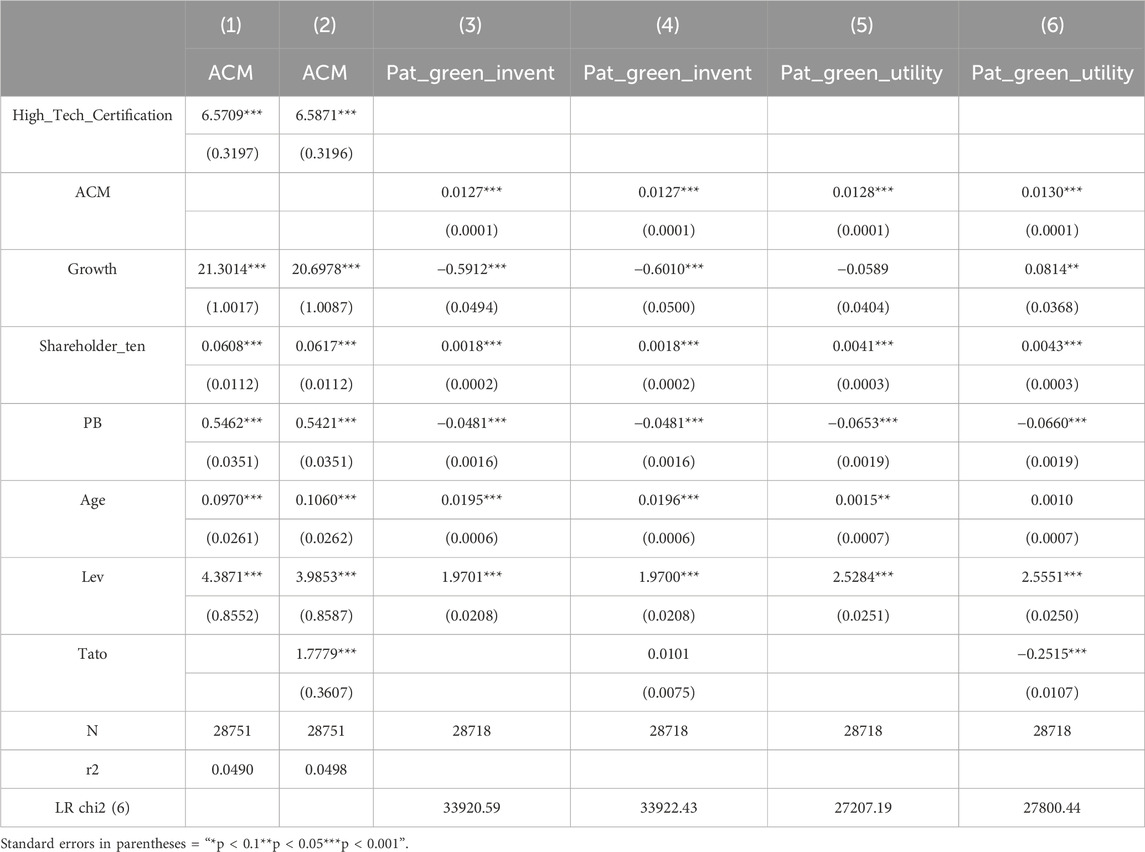

The influence mechanism of capital market attention is recapitulated in Table 10. Columns 1 and 2 evince that enterprises conspicuously augment capital market attention on them subsequent to obtaining high-tech certification, which reflects sensitivity of the capital market to enterprise value. Specifically, enterprises receiving high-tech certification can procure more government resources and policy dividends, thereby increasing their investment value and augmenting capital market attention to them. Columns 3 and 4 delineate the effect of capital market attention on substantive green innovation, while columns 5 and 6 portray its impact on strategic green innovation. The outcomes reveal that in current capital market milieu, enterprises adopt flexible research and development strategies. Owing to the capital market’s relatively greater emphasis on positive information, strategic innovation boasts a shorter research and development cycle and prompts efficacy, thus being capable of emitting positive signals in a short term. Hence, driven by this mechanism, the influence of capital market attention on strategic green innovation preponderates over that on substantive green innovation. Therefore, Hypothesis 5 is verified.

Table 10. Mechanism test (ACM).

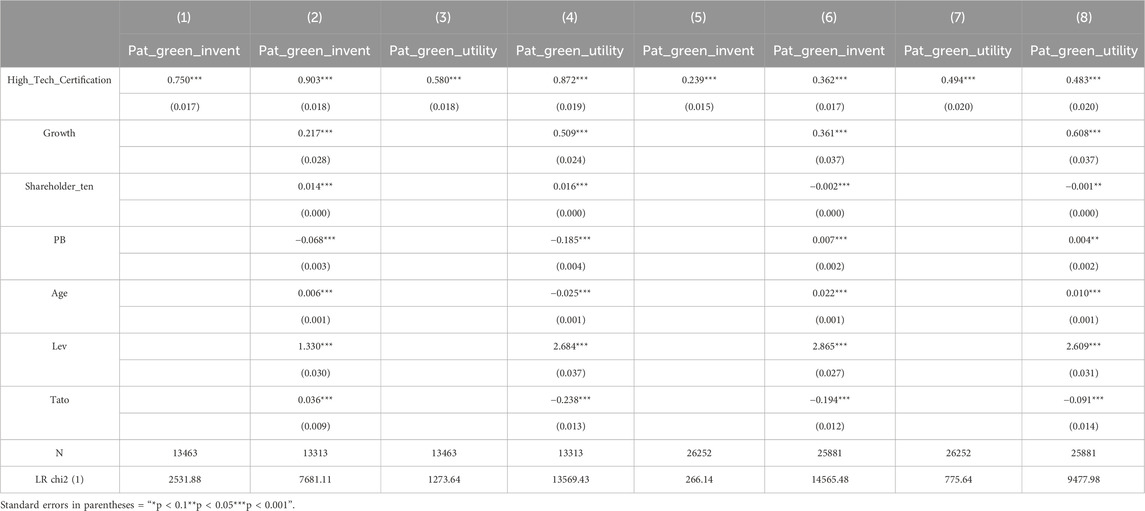

From the perspective of property rights heterogeneity, the impact of high-tech certification on state-owned enterprises (SOEs) are summarized in columns (1) to (4) of Table 11. The results indicate that for SOEs, the stimulative effect of high-tech certification on substantive green innovation is significantly stronger than that on strategic green innovation. This suggests that SOEs have a robust response and execution efficacy in implementing government policies. The impact of high-tech certification on non-state-owned enterprises (NSOEs) is presented in columns (5) to (8). The findings reveal that after obtaining certification, NSOEs tend to prioritize the advancement of strategic green innovation. This implies that green innovation decisions of NSOEs are predominantly driven by their own interests. Therefore, the government is advised to intensify its guidance for NSOEs and to encourage them to place greater emphasis on substantive green innovation.

Table 11. Property rights heterogeneity.

The influence of high-tech certification on labor-intensive industries is summed up in Table 12. The findings reveal that the promoting effect of high-tech certification on strategic green innovation is significantly stronger than that on labor-intensive green innovation. This suggests that current labor-intensive industries in China might be gradually losing their international competitiveness. In this context, labor-intensive enterprises are more prone to giving priority to the development of strategic green innovation in anticipation of obtaining more government support.

Table 12. Industry heterogeneity (labour-intensive).

The influence of high-tech certification on capital-intensive enterprises is summed up in Table 13. Outcomes indicate that the promoting effect of high-tech certification on strategic green innovation is significantly higher than that on substantive green innovation. This might be attributed to the fact that based on China’s industrial classification, there are a considerable number of heavily polluting enterprises in capital-intensive industries. Hence these enterprises, owing to the pollution they have caused, need to uphold their corporate image through more strategic green innovations.

Table 13. Industry heterogeneity (capital-intensive).

The influence of high-tech certification on technology-intensive enterprises is summed up in Table 14. Findings demonstrate that the promoting effect of high-tech certification on substantive green innovation is significantly greater than that on strategic green innovation. This suggests that the supportive policies and guiding measures associated with high-tech certification have exerted a positive influence on the technology-intensive sector.

Table 14. Industry heterogeneity (technology-intensive).

The influence of high-tech certification on enterprises in the eastern region is manifested in Table 15. Findings reveal that for enterprises in the eastern region, the facilitating effect of high-tech certification on strategic green innovation is conspicuously greater than that on substantive green innovation. Possible causes encompass: Firstly, there are more non-state-owned enterprises in the eastern region, and these enterprises take actions mostly taking into account their own interests. Secondly, the eastern region is rich in government resources, giving enterprises incentives to go for policy arbitrage. Finally, a considerable number of venture capital institutions are concentrated in the eastern region, and enterprises need to release positive signals to them. The combined action of these factors makes enterprises in the eastern region more prone to opting for strategic green innovation.

Table 15. Regional heterogeneity (eastern region).

The influence of high-tech certification on enterprises in the central region is summarized in Table 16. Results indicate that the facilitating effect of high-tech certification on substantive green innovation is significantly greater than that on strategic green innovation. This might be attributed to the relatively lower degree of marketization in the central region, where enterprises rely more on policy supports such as government subsidies and tax preferences. Under the existing policy guidance, enterprises are more prone to choosing substantive green innovation.

Table 16. Regional heterogeneity (central region).

The influence of high-tech certification on enterprises in the western region is recapitulated in Table 17. Outcomes demonstrate that the facilitating impact of high-tech certification on strategic green innovation is significantly greater than that on substantive green innovation. This could be ascribed to the fact that the main industries in the western region encompass capital-intensive industries such as mining and labor-intensive industries like textiles. The features of these industries render enterprises more prone to undertaking strategic green innovation.

Table 17. Regional heterogeneity (western region).

For developing nations, the traditional development model of “pollution first and then treatment” is unsustainable. Therefore, it is crucial for the government to utilize policy tools to steer enterprises toward substantive green innovation. We systematically evaluate the high-tech enterprise certification policy, a key policy tool driving enterprise innovation, using data from Chinese A-share listed companies from 2006 to 2023. We employ the zero-inflated negative binomial model, Poisson model, instrumental variable approach, and PSM-DID method to assess the impact of high-tech enterprise certification on both substantive and strategic green innovation. The mechanisms of actions are examined from four perspectives: tax incentives, government subsidies, financing constraints, and capital market attention. Considering the characteristics of the China market, heterogeneity analyses are conducted across three dimensions: property rights, industry, and region. The research reveals that, overall, there is significant policy arbitrage in the green innovation behaviors of enterprises, leading to a notable issue of green patent bubbles. Specifically, the promotional effect of high-tech enterprise certification on strategic green innovation is significantly stronger than that on substantive green innovation. This suggests that the government should place greater emphasis on the implementation of policies, and rationally allocate policy dividends based on enterprises’ green innovation performance, adjusting evaluation criteria for enterprise green innovation performance promptly.

From the perspective of the functioning mechanism, high-tech enterprise certification can directly enhance cash flow by reducing corporate tax rates, increasing government subsidies, and alleviating financing constraints. Adequate cash flow support leads enterprises to prefer substantive green innovation over strategic green innovation. This reflects two key aspects:

Firstly, in the long term, substantive green innovation significantly enhances the competitiveness and development potential of enterprises. Therefore, after easing cash flow pressure, enterprises are more inclined to investing in substantive green innovation.

Secondly, the repeated games between the government and enterprises, as well as between banks and other financial institutions and enterprises, have formed an effective supervision mechanism, encouraging enterprises to prioritize substantive green innovation.

However, from the perspective of capital market attention, this study finds that high-tech enterprise certification has increased the attention enterprises receive from the capital market. Due to the lack of a long-term investment mindset among Chinese investors, under the pressure of capital market, enterprises tend to favor strategic green innovation. From the perspective of property rights differences, state-owned enterprises actively respond to the policy call for green development. Stimulated by the policy dividends brought by high-tech enterprise certification, performance of substantive green innovation by state-owned enterprises surpasses that of strategic green innovation. From the perspective of industry differences, technology-intensive enterprises, after obtaining high-tech enterprise certification, can significantly alleviate cash flow pressure in R&D activities and thus are more inclined toward substantive green innovation. From the perspective of regional differences, enterprises in the central region exhibit a significantly stronger preference for substantive green innovation over strategic green innovation under the influence of high-tech enterprise certification.

The conclusion of this paper enriches and extends the research on the influence of high-tech certification and the theory of green innovation. The following policy recommendations are put forth: Firstly, intensify governmental guidance on green innovation and refine management and assessment mechanism for high-tech enterprises. In light of the distinct requirements of substantive green innovation and strategic green innovation of enterprises, the government ought to incorporate specific considerations for green technological innovation during the certification process, encouraging enterprises to undertake substantive innovations that are both technologically ground-breaking and market-oriented. For this purpose, the government should establish a more elaborate assessment system, differentiating between enterprises that rely on certification to drive strategic innovation and those that are genuinely dedicated to green technology research and development, ensuring precise allocation of green innovation resources. Simultaneously, differentiated incentive measures should be implemented, providing more ample policy support to enterprises with technological innovation at their core operation and avoiding excessive appropriation of policy resources for strategic innovation.

Secondly, optimize allocation of resources to alleviate pressures of enterprise financing and resource shortages. Particularly in terms of the influence of high-tech certification on financing and resource allocation, the government could offer corresponding support for enterprises of different innovation types through differentiated financial support policies. For enterprises possessing substantive green innovation potential, higher amounts of green credit and tax preferences should be provided to expedite their technological innovation processes, whereas for enterprises mainly dependent on strategic green innovation, a phased support approach should be adopted to guarantee efficient utilization of resources and sustainability of green innovation.

Thirdly, Strengthen the leading role of state-owned enterprises to promote balanced regional development. State-owned enterprises exert a considerable exemplary effect in the research and development as well as market application of green technologies. Hence, the government ought to support their in-depth collaboration with non-state-owned enterprises in domains such as green technology standards and environmental protection technologies. Through technology sharing and experience inheritance, assist the latter in breaking through technical bottlenecks of green innovation and in accelerating the transformation of innovation outcomes. Additionally, the government should be attentive to regional disparities and implement differentiated policy support in response to the green innovation demands of enterprises in diverse regions. Particularly in the central and western regions where technology relatively lags behind, provide them with more policy and resource support to facilitate balanced development of green innovation across regions.

Fourthly, enhance capital market regulation and external supervision to promote transparency in green innovation. To facilitate long-term development of enterprises’ green innovation, the government is required to further refine the capital market regulatory framework, enhance transparency of green innovation projects, and upgrade the evaluation criteria for investors. The influence of high-tech certification on the capital market must not be overlooked, particularly in the capital operation of green innovation projects. The government should intensify the standardization of enterprises’ green innovation information disclosure to ensure accurate assessment of enterprises’ long-term technological innovation capabilities by the capital market. By augmenting information transparency in the capital market and averting investment behaviors that lean towards short-term profits, the government can steer investors to pay greater attention to enterprises’ technological accumulation and long-term value in green innovation, thereby propelling enterprises towards substantive innovation.

Fifthly, formulate differentiated high-tech certification standards and incentive measures to promote coordinated development of regional green innovation. Given the distinct characteristics of strategic green innovation and substantive green innovation, the government can provide necessary support to enterprises engaging in strategic green innovation via certification, but should place greater emphasis on promoting enterprises with innovation potentials to achieve substantive breakthroughs in green technologies. Additionally, in supporting green innovation in both central and western regions and non-state-owned enterprises, the government should enhance the green technological innovation capabilities of these regions and enterprises by strengthening technical guidance and resource support, thereby promoting balanced green innovation development across the regions.

In subsequent studies, In subsequent studies, refinement can be carried out from the following two aspects:

1) This study primarily examines the influence of high-tech certification on enterprises from a literature review perspective. Future research could introduce mathematical models to comprehensively consider multiple factors affecting green innovation in enterprises and construct a tripartite game model involving the government, enterprises, and the public. This would provide robust theoretical support for the government to formulate more detailed green innovation policies.

2) This study conducts an empirical analysis using green patent application data. Future research can undertake comparative studies from the perspective of patent authorization to offer the government a more comprehensive reference for optimizing the management of high-tech certification.

The datasets presented in this study can be found in online repositories. The names of the repository/repositories and accession number(s) can be found below: https://data.csmar.com.

ZL: Funding acquisition, Investigation, Visualization, Writing–original draft, Writing–review and editing. YS: Funding acquisition, Supervision, Writing–review and editing. KY: Data curation, Writing–original draft, Writing–review and editing. JK: Funding acquisition, Project administration, Supervision, Writing–review and editing.

The author(s) declare that financial support was received for the research, authorship, and/or publication of this article. The National Natural Science Foundation Project of China “The Coordination Mechanism of Trade Policy and industry policy from the Perspective of Industrial Dynamic Development” (71573171); The Major Project of Philosophy and Social Sciences Research of the Ministry of Education “Research on the Influences and Responses of the “Dual Construction” of Global Value Chain and International Trade Policy System” (22JZD041). The Key Scientific Research Project of Hunan Provincial Education Department “Research on Theory and Policy of New Quality Productivity Promoting Common Prosperity in Hunan” (24A0445).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

The author(s) declare that no Generative AI was used in the creation of this manuscript.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Abbas, S. F., Tariq, I., and Waseem, F. (2023). Linking green innovation, corporate environmental performance with financing constraints: a sustainable transition towards environmental protection. Bus. Rev. 18 (2), 20–31. doi:10.54784/1990-6587.1543

Amore, M. D., and Bennedsen, M. (2016). Corporate governance and green innovation. J. Environ. Econ. Manag. 75, 54–72. doi:10.1016/j.jeem.2015.11.003

Barney, J. (1991). Firm resources and sustained competitive advantage. J. Manag. 17, 99–120. doi:10.1177/014920639101700108

Bi, Q., Feng, S., Qu, T., Ye, P., and Liu, Z. (2024). Is the green innovation under the pressure of new environmental protection law of PRC substantive green innovation. Energy Policy 192, 114227. doi:10.1016/j.enpol.2024.114227

Bitektine, A. (2011). Toward a theory of social judgments of organizations: the case of legitimacy, reputation, and status. Acad. Manag. Rev. 36 (1), 151–179. doi:10.5465/amr.2009.0382

Cao, W., and Yu, J. (2024). Evolutionary game analysis of factors influencing green innovation in Enterprises under environmental governance constraints. Environ. Res. 248, 118095. doi:10.1016/j.envres.2023.118095

Chen, M., Li, Z., and Liu, Z. (2024). Substantive response or strategic response? The induced green innovation effects of carbon prices. Int. Rev. Financial Analysis 93, 103139. doi:10.1016/j.irfa.2024.103139

Chen, P., and Kim, S. (2024). The relationship between industrial policy and exploratory innovation–evidence from high-tech enterprise identification policy in China. Kybernetes 53 (5), 1636–1652. doi:10.1108/K-12-2022-1699

Chen, Y., and Chen, G. (2022). Effectiveness of industrial policy in supporting innovation: the role of internal and external corporate governance mechanism. Appl. Econ. 54 (19), 2181–2193. doi:10.1080/00036846.2021.1985074

Chen, Z., He, Y., and Kwan, Y. (2023). The high-tech enterprise certification policy and innovation: quantity or quality? J. Knowl. Econ. 15, 14135–14171. doi:10.1007/s13132-023-01610-4

Cheng, L., Cheng, H., and Zhuang, Z. (2019). Political connections, corporate innovation and entrepreneurship: evidence from the China Employer-Employee Survey (CEES). China Econ. Rev. 54, 286–305. doi:10.1016/j.chieco.2018.12.002

Dai, X., and Wang, F. (2019). Does the high- and new-technology enterprise program promote innovative performance? Evidence from Chinese firms. China Econ. Rev. 57, 101330. doi:10.1016/j.chieco.2019.101330

Dore, R. (1988). Technology policy and economic performance; lessons from Japan: christopher freeman. (London, New York, 1987: Frances Printer Publishers), 155. [UK pound] 20.00. Research Policy, 17(5), 309-310. doi:10.1016/0048-7333(88)90011-X

Du, J. L., Liu, Y., and Diao, W. X. (2019). Assessing regional differences in green innovation efficiency of industrial enterprises in China. Int. J. Environ. Res. Public Health 16 (6), 940. doi:10.3390/ijerph16060940

Duan, Z., Lee, S., and Lee, G. (2023). Evaluation of the effect of a low-carbon green city policy on carbon abatement in South Korea: a city-level analysis based on PSM-DID and LSA models. Ecol. Indic. 158, 111369. doi:10.1016/j.ecolind.2023.111369

Endawkie, A., Kebede, N., Asmamaw, D. B., and Tsega, Y. (2024). Predictors and number of antenatal care visits among reproductive age women in Sub-Saharan Africa further analysis of recent demographic and health survey from 2017-2023: zero-inflated negative binomial regression. PLOS ONE 19, e0302297. doi:10.1371/journal.pone.0302297

Fang, X., Liu, M., and Li, G. (2024). Can the green credit policy promote green innovation in enterprises? Empirical evidence from China. Technol. Econ. Dev. Econ. 30 (4), 899–932. doi:10.3846/tede.2024.20497

Grégoire, D. A., and Shepherd, D. A. (2012). Technology-market combinations and the identification of entrepreneurial opportunities: an investigation of the opportunity-individual nexus. Acad. Manag. J. 55 (4), 753–785. doi:10.5465/amj.2011.0126

Gu, J., Chen, M., Yuan, Y., Guo, X., Zhou, T. Y., and Fu, Q. (2025). Drink like a man? Modified Poisson analysis of adolescent binge drinking in the US, 1976–2022. Soc. Sci. and Med. 364, 117553. doi:10.1016/j.socscimed.2024.117553

He, S. (2021). Growth, innovation, credit constraints, and stock price bubbles. J. Econ. 133 (3), 239–269. doi:10.1007/s00712-021-00734-y

Hu, W., and Shi, S. (2025). CEO green background and enterprise green innovation. Int. Rev. Econ. and Finance 97, 103765. doi:10.1016/j.iref.2024.103765

Hu, Y., Jin, S., Ni, J., Peng, K., and Zhang, L. (2023). Strategic or substantive green innovation: how do non-green firms respond to green credit policy? Econ. Model. 126, 106451. doi:10.1016/j.econmod.2023.106451

Ji, Q., Quan, X., Yin, H., and Yuan, Q. (2021). Gambling preferences and stock price crash risk: evidence from China. J. Bank. and Finance 128, 106158. doi:10.1016/j.jbankfin.2021.106158

Jia, J., and Ma, G. (2017). Do R&D tax incentives work? Firm-level evidence from China. China Econ. Rev. 46, 50–66. doi:10.1016/j.chieco.2017.08.012

Jia, N., Huang, K. G., and Man Zhang, C. (2019). Public governance, corporate governance, and firm innovation: an examination of state-owned enterprises. Acad. Manag. J. 62 (1), 220–247. doi:10.5465/amj.2016.0543

Jiang, L., and Bai, Y. (2022). Strategic or substantive innovation? The impact of institutional investors' site visits on green innovation evidence from China. Technol. Soc. 68, 101904. doi:10.1016/j.techsoc.2022.101904

Kou, G., Yüksel, S., Dinçer, H. A., and Hefni, M. (2024). Integrated approach for sustainable development and investment goals: analyzing environmental issues in European economies. Ann. Operations Res. 342, 429–475. doi:10.1007/s10479-023-05679-7

Li, L., Chen, J., Gao, H., and Xie, L. (2019). The certification effect of government R&D subsidies on innovative entrepreneurial firms'access to bank finance: evidence from China. Small Bus. Econ. 52, 241–259. doi:10.1007/s11187-018-0024-6

Li, X., Guo, F., Xu, Q., Wang, S., and Huang, H. (2023). Strategic or substantive innovation? The effect of government environmental punishment on enterprise green technology innovation. Sustain. Dev. 31, 3365–3386. doi:10.1002/sd.2590

Li, Y., Tong, Y., Ye, F., and Song, J. (2020). The choice of the government green subsidy scheme: innovation subsidy vs. product subsidy. Int. J. Prod. Res. 58, 4932–4946. doi:10.1080/00207543.2020.1730466

Liang, Z., Shen, Y., Yang, K., and Kuang, J. (2025). The impact of high-tech enterprise certification on green innovation: evidence from listed companies in China. Sustainability 17 (1), 147. doi:10.3390/su17010147

Liu, H., Xing, F., Li, B., and Yakshtas, K. (2020). Does the high-tech enterprise certification policy promote innovation in China? Sci. Public Policy 47 (5), 678–688. doi:10.1093/scipol/scaa050

Liu, X., Huang, N., Su, W., and Zhou, H. (2024). Green innovation and corporate ESG performance: evidence from Chinese listed companies. Int. Rev. Econ. and Finance 95, 103461. doi:10.1016/j.iref.2024.103461

Lu, S., and Cheng, B. (2024). Does the value-added tax reduction policy promote a firm's green innovation? Evidence from China. Appl. Econ. 56, 5302–5317. doi:10.1080/00036846.2023.2244253

Ma, B., and Li, H. (2025). Antitrust laws, market competition and corporate green innovation. Int. Rev. Econ. and Finance 97, 103768. doi:10.1016/j.iref.2024.103768

Meuleman, M., and Maeseneire, W.De (2012). Do R&D subsidies affect SMEs'access to external financing? Res. Policy 41, 580–591. doi:10.1016/j.respol.2012.01.001

Millar, C., Udalov, Y., and Millar, H. (2012). The ethical dilemma of information asymmetry in innovation: reputation, investors and noise in the innovation channel. Creativity and Innovation Manag. 21, 224–237. doi:10.1111/j.1467-8691.2012.00642.x

Min, B., Shihe, Li., Donald, L., and Chia-Feng, Yu (2022). The winner’s curse in high-tech enterprise certification: evidence from stock price crash risk. Int. Rev. Financial Analysis 82, 102175. doi:10.1016/j.irfa.2022.102175

Nguyen, D. T., Tran, V. T., Dinh, H., and Bach, P. (2023). Does green activity impact stock price crash risk? The role of climate risk. Finance Res. Lett. 55, 103879. doi:10.1016/j.frl.2023.103879

Ning, J. (2018). Corporate innovation strategy and stock price crash risk. J. Corp. Finance 53, 155–173. doi:10.1016/j.jcorpfin.2018.10.006

Pang, Y., Zhang, F., Wang, Q., Wang, L., and Wang, C. (2024). High-and new-technology enterprise certification, enterprise innovation ability and export product quality. Technol. Analysis and Strategic Manag. 36 (2), 349–364. doi:10.1080/09537325.2022.2033719

Poo, M. M., and Wang, L. (2015). Guan-hua Xu: China's move toward being a country of innovation. Natl. Sci. Rev. 2 (2), 237–240. doi:10.1093/nsr/nwv032

Schober, P., and Vetter, T. R. (2021). Count data in medical research: Poisson regression and negative binomial regression. Anesth. and Analgesia 132 (5), 1378–1379. doi:10.1213/ANE.0000000000004511

Shan, S., Jia, Y., Zheng, X., and Xu, X. (2018). Assessing relationship and contribution of China's technological entrepreneurship to socio-economic development. Technol. Forecast. Soc. Change 135, 83–90. doi:10.1016/j.techfore.2017.12.022

Shao, Y., and Chen, Z. (2022). Can government subsidies promote the green technology innovation transformation? Evidence from Chinese listed companies. Econ. Analysis Policy 74, 716–727. doi:10.1016/j.eap.2022.03.020

She, M., Wang, Y., and Hu, D. (2022). Effect of HTE certification on external resource acquisition and firm performance: evidence from China. Technol. Analysis and Strategic Manag. 34, 609–624. doi:10.1080/09537325.2021.1915475

Song, G., Wang, F., and Feng, D. (2024). Can digital economy foster synergistic increases in green innovation and corporate value? Evidence from China. PLoS ONE 19, 1–29. doi:10.1371/journal.pone.0304625

Spyros, T. (2022). Information disclosure and the feedback effect in capital markets. J. Financial Intermediation 49, 100897. doi:10.1016/j.jfi.2020.100897

Tang, M., Liu, Y., Hu, F., and Wu, B. (2023). Effect of digital transformation on enterprises' green innovation: empirical evidence from listed companies in China. Energy Econ. 128, 107135. doi:10.1016/j.eneco.2023.107135

Tomizawa, A., Zhao, L., Bassellier, G., and Ahlstrom, D. (2020). Economic growth, innovation, institutions, and the Great Enrichment. Asia Pac. J. Manag. 37, 7–31. doi:10.1007/s10490-019-09648-2

Wan, X., Wang, Y., Qiu, L., Zhang, K., and Zuo, J. (2022). Executive green investment vision, stakeholders’ green innovation concerns and enterprise green innovation performance. Front. Environ. Sci. 10, 997865. doi:10.3389/fenvs.2022.997865

Wang, H., Yang, J., and Zhu, N. (2024a). Does tax incentives matter to enterprises' green technology innovation? The mediating role on R&D investment. Sustainability 16 (14), 5902. doi:10.3390/su16145902

Wang, Q., Chen, M., and Liu, T. (2024b). Research on green innovation spillover effects of peers issuing green bonds: evidence from China's green bond market. SAGE Open 14, 1–14. doi:10.1177/21582440241289210

Wang, T., Liu, X., and Wang, H. (2022). Green bonds, financing constraints, and green innovation. J. Clean. Prod. 381, 135134. doi:10.1016/j.jclepro.2022.135134

Wu, A. (2017). The signal effect of Government R&D Subsidies in China: does ownership matter? Technol. Forecast. Soc. Change 117, 339–345. doi:10.1016/j.techfore.2016.08.033

Wu, Y., Li, X., Zhang, Ce., and Wang, S. (2024). The impact of government subsidies on technological innovation of new energy vehicle enterprises: from the perspective of industry chain. Environ. Dev. and Sustain. 26, 25589–25607. doi:10.1007/s10668-023-03697-w

Xi, B., and Jia, W. (2025). Research on the impact of carbon trading on enterprises' green technology innovation. Energy Policy 197, 114436. doi:10.1016/j.enpol.2024.114436

Xiao, D., Yu, F., and Guo, C. (2023). The impact of China's pilot carbon ETS on the labor income share: based on an empirical method of combining PSM with staggered DID. Energy Econ. 124, 106770. doi:10.1016/j.eneco.2023.106770

Xie, X., and Wang, M. (2024). “Can green subsidies really promote firms’ and peers’ substantive green innovation?”. in Proceedings, academy of management proceedings 2024 1, 20065. Valhalla, NY 10595: Academy of Management. doi:10.5465/AMPROC.2024.20065abstract

Xu, J., Ye, F., and Li, X. (2024). Carbon intensity constraint policy and firm green innovation in China: a quasi-DID analysis. Sustain. Account. Manag. Policy J. 15 (3), 704–730. doi:10.1108/SAMPJ-08-2023-0572

Xu, L., Zhang, R., Liu, M., Han, C., Liu, H., Hou, G., et al. (2023). Promoting low-carbon behaviors through increased media exposure of carbon peak and carbon neutrality: low-carbon awareness as a mediator. Soc. Behav. Personality Int. J. 51 (7), 1–11. doi:10.2224/sbp.12467

Xue, X., Liang, P., Xue, F., Hu, N., and Liu, L. (2024). Trade policy uncertainty and the patent bubble in China: evidence from machine learning Asia-Pacific. J. Account. Econ., 1–22. doi:10.1080/16081625.2023.2298934

Yan, S., Zou, L., Growe, A., and Wang, Q. (2024). Propositions for place-based policies in making regional innovation systems. Evidence from six high-tech industrial development zones in China. Cities 154, 105322. doi:10.1016/j.cities.2024.105322

Yang, X., Gu, X., and Yang, X. (2023). Firm age and loan financing with patents as collateral of Chinese startups: the roles of innovations and experience. Econ. Innovation New Technol. 32 (3), 343–369. doi:10.1080/10438599.2021.1916486

Ye, Y., Li, C., Li, X., Tao, Y., and Wu, H. (2024). The role of tax enforcement on green innovation: evidence from the consolidation of state and local tax bureau (CSLTB). Struct. Change Econ. Dyn. 70, 221–232. doi:10.1016/j.strueco.2024.02.004

Ying, Q., Yang, S., and He, S. (2023). Government R&D subsidies and the manipulative innovation strategy of Chinese renewable energy firms. Econ. research-Ekonomska istraživanja 36 (2). doi:10.1080/1331677x.2022.2142823