Zehua Tian

Zehua Tian Wusong Yang2

Wusong Yang2

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 10 April 2025

Sec. Environmental Policy and Governance

Volume 13 - 2025 | https://doi.org/10.3389/fenvs.2025.1528831

Corporate environmental governance has emerged as a critical global priority amid escalating environmental challenges. In recent years, many countries have implemented laws such as “Supply Chain Laws” and “Corporate Due Diligence Laws” to strengthen corporate environmental accountability. In China, the introduction of the Administrative Measures for the Legal Disclosure of Corporate Environmental Information in 2021 marked a significant shift toward mandatory corporate environmental governance. This study traces the evolution of China’s corporate environmental governance policies through a policy text analysis of 140 documents issued by the central government between 1982 and 2023. The analysis identifies three distinct developmental stages: (1) the pollution control phase (1982–2006), characterized by command-and-control measures; (2) the social responsibility advocacy phase (2007–2020), emphasizing voluntary and market-based mechanisms; and (3) the mandatory environmental obligations phase (2021–present), introducing stricter regulatory requirements. While the current framework reflects principles of collaborative governance, significant challenges remain, including weak communication channels, free-rider problems, and limited extraterritorial application of environmental policies. This study provides a comprehensive analysis of China’s corporate environmental governance policies, offering insights and actionable recommendations to enhance their effectiveness and contribute to global discussions on sustainable corporate governance.

Corporate environmental governance has garnered increasing attention from governments worldwide as a critical pathway for addressing environmental crises, such as widespread environmental degradation and the intensification of extreme weather events. Corporations are key agents of economic development and significantly influence environmental protection regulations under government oversight. Strengthening corporate environmental governance not only curbs pollution, but also promotes cleaner production processes, and raises public awareness about environmental responsibility. Over the past 3 decades, governmental bodies and societal actors have progressively recognized the significance of corporate environmental governance, guiding corporate actions through policy formulation and enforcement mechanisms.

The concept of corporate environmental governance can be traced back to the 1930s, when Corporate Social Responsibility (CSR) was first introduced (Agudelo et al., 2019). Over time, CSR expanded to encompass a broad spectrum of concerns, including labor rights, social welfare, and environmental protection. CSR gained international recognition in 2011 with the adoption of the United Nations Guiding Principles on Business and Human Rights (United Nations Human Rights Council, 2011). In recent years, the focus of national legislation has shifted towards strengthening corporate due diligence obligations, with many countries enacting laws under names such as “Corporate Code of Conduct,” “Due Diligence Law,” and “Supply Chain Law,” thus ushering corporate environmental governance into a new phase. China, as one of the largest countries in the world, hosts numerous corporations of varying scales. Analyzing its corporate environmental governance policies and exploring future development trends is therefore crucial.

Policies serve as crucial guidelines for corporate behavior, and the text of these policies forms the backbone of their content (Zhang and Ma, 2017). Since the enactment of the Environmental Protection Law in 1979, China’s CSR governance policies have evolved significantly. Between 1979 and 2023, China issued over 100 policies related to CSR governance, including corporate environmental standards, social responsibility guidelines, and enforcement notices. These policies have been instrumental in shaping China’s legal framework for corporate environmental governance, reflecting national goals and conditions. In this context, key questions of this research arise regarding how corporate environmental governance policies are defined, how they have evolved over time, and what issues persist between policy enactment and implementation.

From a policy tool perspective, this study systematically analyzes relevant policies through textual analysis, identifying key phases in the evolution of corporate environmental governance in China. Additionally, the study explores the challenges of policy implementation and offers potential avenues for improvement. By doing so, it aims to support the future development of corporate environmental governance policies tailored to China’s specific circumstances. The findings are expected to provide both theoretical insights and practical recommendations for policymakers in China and other countries.

This paper is organized into seven chapters. The introduction (Chapter 1) and literature review (Chapter 2) provide an overview of the development of corporate environmental governance policies and current research status. Chapter 3 outlines the theoretical foundation, research framework, and methodology. Chapter 4 presents a quantitative analysis of corporate environmental governance policies, classifying them and exploring various dimensions of environmental policy texts. Chapter 5 details the evolution of China’s corporate environmental governance policies, identifying key characteristics and stages of development. Chapter 6 examines the transition process across different phases, the compliance and effectiveness of the relevant policies, and identifies the key challenges within China’s current policy framework. It also presents policy recommendations to address these issues. The final chapter (Chapter 7) offers a concluding summary of the findings.

National policy serves as a crucial mechanism for guiding the development of enterprises, particularly in the context of environmental governance. Environmental policy, in particular, plays an essential role in managing pollution and mitigating environmental degradation (Wei and Hu, 2021). With the evolution of environmental policy and the growing public awareness of corporate environmental responsibility, both international and Chinese scholars have increasingly turned their attention to the interaction between environmental policy and corporate development. This growing body of research seeks to understand how national policies influence corporate environmental governance and how enterprises adapt their strategies in response to regulatory changes.

International research on environmental policy and corporate development can broadly be divided into two main categories. The first category focuses on the mechanisms through which national policies influence corporate environmental governance (Glicksman and Markell, 2018; Liu, 2021; OECD, 2007; Wang et al., 2021). This body of work often integrates both qualitative and quantitative methods to analyze the dynamic relationship between national policies and specific areas of corporate development. For example, research has shown that market-based environmental policies—those that leverage market mechanisms—tend to have a significant impact on corporate environmental innovation, whereas policies that fail to incentivize research and development may limit the scope of corporate innovation (Liao, 2018). Tilt’s analysis of Australia’s environmental policies highlights that while corporate environmental disclosure levels have improved under regulatory influence, the content and quality of disclosures still lag behind other countries. This gap is often attributed to corporate resistance, which can be mitigated through enhanced public participation (Tilt, 2001). Additionally, Dechezlepretre and Sato’s research on the impact of national environmental policies on corporate competitiveness provides a valuable reference for both policymakers and business stakeholders (Dechezlepretre and Sato, 2017).

Another category focuses on specific environmental policies. For instance, empirical studies on environmental policies, such as those examining the role of environmental taxes, suggest that while such policies can reduce pollutant emissions, their overall impact is limited (Chen et al., 2022). Some literature also delves into how companies develop and implement their own environmental policies (Jose and Lee, 2007). For instance, Jose and Lee conducted a textual analysis of environmental disclosure documents from the world’s 200 largest companies, offering key recommendations for future policy development. Similarly, Alnajjar’s analysis of CSR disclosure documents from the top 500 U.S. companies revealed a significant correlation between CSR disclosure effectiveness and corporate profitability, as well as between company size and the nature of the disclosures (Alnajjar, 2000).

In China, research on environmental policy and corporate development has largely focused on the impact of corporate environmental policies on overall environmental performance, as well as the pathways through which these policies influence corporate outcomes in different sectors. In recent years, there has been growing interest in examining how environmental policies affect the development of green technologies and the green transformation of enterprises. A review of the relevant literature in China reveals that current research primarily centers on three key areas: the impact of environmental policies on environmental quality, the relationship between environmental policies and corporate performance, and the role of environmental policies in promoting green innovation and transformation.

First, the effects of environmental policies on environmental quality are explored. Scholars have employed econometric analyses to assess the effects of various environmental policy instruments on China’s carbon productivity (Fan and Zhang, 2023). Other studies applied differential game theory to determine the optimal policies for controlling corporate pollution (Liu et al., 2021; Zeng et al., 2016; Zheng, 2019; Xu and Tan, 2023). Some studies also investigate the impact of different environmental policies on corporate governance (Hu et al., 2017; Jin, 2017; Lin et al., 2015; Liu, 2015; Zhang, 2016). For example, certain studies have explored how environmental policies can best allocate resources. These analyses propose strategies to enhance China’s comprehensive system of environmental policy instruments, while also considering corporate perspectives (Lu and Yan, 2022; Wang et al., 2016).

Second, research on the relationship between environmental policies and firm performance predominantly focuses on the dual impact of such policies on corporate environmental performance and economic performance. In terms of environmental performance, scholars have employed micro-empirical methods to analyze the correlation between local government environmental policy innovations and corporate environmental performance. Some studies have also examined the impact of environmental enforcement mechanisms, such as the “river chief system,” on corporate performance (Li et al., 2023). Other analyses explore the relationship between environmental law enforcement, corporate supervision, and pollution reduction (Shen and Zhou, 2017). For small and medium-sized enterprises (SMEs), studies have shown that administrative environmental policies tend to have a greater impact on environmental performance than economic policies (Long et al., 2018). Regarding economic performance, research has focused on topics such as corporate social responsibility, the impact of corporate collusion on economic performance, the role of government subsidies in promoting environmental investment, and the relationship between environmental information disclosure and the cost of equity financing (Deng et al., 2022; Ye et al., 2015; Wang et al., 2021).

Finally, research on the role of environmental policies in driving green innovation and corporate transformation has garnered increasing attention. Studies have found that China’s current carbon tax levels promote investment in environmental R&D and innovation (Hong et al., 2022). Moreover, the relationship between incentive-based environmental policies and green technological innovation tends to follow an inverted U-shaped curve, whereas punitive environmental policies exhibit a positive U-shaped relationship with green innovation (Wang et al., 2022). However, stringent environmental policies may inhibit pollution-intensive enterprises from investing in technological innovation (Tian and Han, 2021). The regional impact of environmental policies on innovation also varies, with differences observed between China’s eastern, central, and western regions (Zhang et al., 2021). Both domestic and international environmental policies have been shown to positively impact renewable energy technology innovation in China, although there is often a time lag in realizing these effects (Li et al., 2021). Additionally, corporate environmental responsibility has been found to mediate the relationship between media attention and green innovation, highlighting the role of external scrutiny in driving corporate environmental efforts (Li et al., 2022; Yang et al., 2023). Other scholars have examined how China’s green credit policy (Si and Cao, 2022; Wang and Wang, 2021) and green tax system (Wang et al., 2022) influence corporate environmental performance, noting that environmental policies facilitate the green transformation of enterprises by altering the cost-benefit analysis of green initiatives (Wang et al., 2022; Ye and Wu, 2023; Haken, 1984; Hu, 2016).

In summary, a review of both Chinese and international literature reveals several key insights. First, while research on corporate environmental governance in China has largely focused on specific areas—such as the impact of environmental policies on corporate green innovation, corporate performance, and environmental quality—there is a notable lack of comprehensive, historical analysis of China’s corporate environmental governance policies. Second, although the methodologies employed in existing studies incorporate both qualitative and quantitative analyses, Chinese research has generally underutilized textual analysis methods when compared to international studies. As a result, there is still considerable room for expanding the scope of research in this area.

In response to these gaps, this study adopts a policy tool perspective, conducting a textual analysis of China’s corporate environmental governance policies from 1982 to 2023. By examining the evolutionary characteristics of these policies, the study identifies key features and developmental stages, analyzes internal and external factors that constrain improvements in corporate environmental governance, and provides policy recommendations for optimizing China’s governance framework. This approach offers a new perspective for the study of corporate environmental governance policies, contributing both to theoretical understanding and practical policymaking.

What constitutes an effective corporate environmental governance policy? Academic discussions on this topic have primarily revolved around fostering responsible corporate behavior, enhancing public participation, and optimizing government legislative strategies. Collaborative governance theory offers valuable insights in this context.

The concept of collaborative governance, or synergistic governance, originates from the field of synergetic, which was pioneered by German physicist Hermann Haken in 1974. Initially developed to study the self-organization of non-equilibrium systems (Haken, 1984), synergetic has since evolved into a multidisciplinary framework, incorporating elements of governance theory from the social sciences. At its core, collaborative governance theory seeks to transcend the limitations of governance led solely by the government, market, or society. Instead, it emphasizes the need for structural coupling and resource sharing among these key actors to maximize the effectiveness of governance, particularly in addressing complex social issues (Hu, 2016). In China, the theory has been applied primarily in areas such as emergency management, network regulation, and governmental oversight (Gao and Zhang, 2021; Gui and Pan, 2022; Li, 2012; Liu, 2018; Shen and Chen, 2017; Wu, 2015; Xu and Huang, 2020; Zhang et al., 2022). Within environmental governance, collaborative governance theory has proven useful in examining approaches to pollution control and related governance methods (Wei and Zhao, 2016).

This theory operates on the premise that social systems are inherently complex and multifaceted, characterized by both competitive and cooperative dynamics. The nature of these dynamics may shift based on the stage of development. For governance to be effective, policy formulation must account for the contributions of all stakeholders involved, fostering cooperation between them to optimize overall outcomes. In modern society, as various social subsystems become increasingly specialized and diverse, achieving synergy between these subsystems presents a greater challenge. Therefore, policymakers must carefully design policies that maximize the synergistic effects of these specialized subsystems, while respecting their unique development trajectories. Collaborative governance theory thus provides a strong theoretical foundation for improving China’s corporate environmental governance policies, helping to achieve more holistic and effective governance outcomes.

In line with the principles of collaborative governance, an effective corporate environmental governance policy should encourage collaboration among key stakeholders—government, social forces, and enterprises. Such policies should adhere to the following principles and requirements to fully harness the potential of synergistic governance:

First, it is essential to guide all stakeholders toward establishing unified governance objectives. Collaborative governance theory asserts that a successful corporate environmental governance policy must foster alignment among stakeholders by promoting common environmental goals. Goal setting is the foundation upon which governance mechanisms operate and provides direction for stakeholders to take concrete actions. However, in practice, complex public affairs often involve conflicting interests among stakeholders, leading to goal misalignment or deviation. Therefore, an effective policy should employ incentives and other mechanisms to align the interests of the government, society, and enterprises, ensuring that individual and public interests are compatible and reinforcing each other.

Second, the establishment of robust information communication channels is crucial. Information asymmetry poses a significant barrier to social governance, leading not only to market failures (Li and Li, 2021) but also hindering collaboration among governance actors, thus reducing the effectiveness of governance. If participants in the governance process operate under disparate communication systems or exacerbate information asymmetry, the potential for collaborative governance is greatly diminished. Accordingly, collaborative governance theory advocates for policies that promote open information channels, dismantle communication barriers, and reduce transaction costs among stakeholders. Effective information exchange between governments, enterprises, the public, and social organizations is key to enhancing coordination and preventing resource waste (Gao and Zhang, 2021).

Third, the issue of “free-riding” must be effectively addressed. In the context of collaborative governance, various stakeholders must work together to maximize the benefits of governance. However, due to the diversity of interests among actors, free-riding—the avoidance of responsibilities while still benefiting from the collective effort—is a common issue (Mankiw and Taylor, 2020). Collaborative governance theory therefore stresses the need for government intervention to ensure that all stakeholders contribute decently. In the context of corporate environmental governance, policies should be designed to allocate responsibilities fairly, using a combination of positive incentives and punitive measures to balance power and responsibility. This approach ensures that each governance actor fully contributes to the overall effort, maximizing the effectiveness of corporate environmental governance.

In the subsequent sections, this paper will analyze the evolution of corporate environmental governance policies in China, drawing on the principles of collaborative governance theory. Additionally, it will propose recommendations for improving future policies to enhance the effectiveness and sustainability of corporate environmental governance.

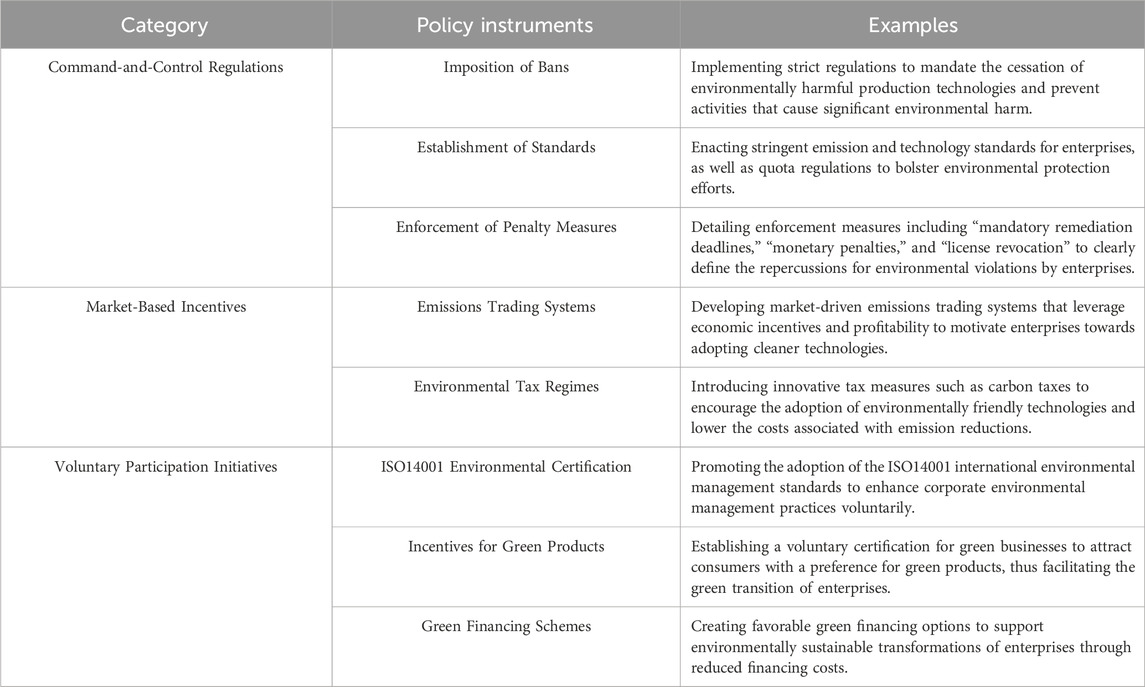

Building on existing literature, this paper categorizes corporate environmental governance policies enacted by the Chinese government into three major types (see Table 1): command-and-control regulations, market-based incentives, and voluntary participation initiatives (Li and Li, 2021).

Table 1. Categories of relevant policy instruments.

Command-and-control regulations are characterized by mandatory government-imposed requirements, which rely on administrative directives to manage corporate environmental practices. Examples include the “Three Simultaneous Requirements” system, which mandates that environmental protection facilities be designed, constructed, and operated alongside the main project, and the “Compliance Deadline Policy,” which sets fixed deadlines for corporate compliance. This category also includes punitive measures, such as mandatory pollution fines (Wang et al., 2022). In contrast, market-based incentive policies, which began to emerge in China during the 1990s, utilize economic mechanisms that operate based on cost-benefit principles. These policies aim to internalize environmental costs for corporations, encouraging them to adopt sustainable practices. Notable examples include the “Sewage Fee,” Environmental Impact Assessments (EIA), and the “Corporate Environmental Target Responsibility System.” By providing financial incentives, these policies motivate companies to implement lower-emission practices and uphold higher environmental standards. Voluntary participation initiatives, typically guided by the government or industry associations, encourage companies to adopt environmentally friendly practices at their discretion. The key distinction between market-based incentives and voluntary initiatives lies in the element of choice, as voluntary mechanisms allow companies the autonomy to opt-in, whereas market-based policies still impose economic consequences.

In China, these three categories of environmental policy tools—command-and-control, market-based, and voluntary—are widely employed to regulate corporate pollution and enhance environmental governance. By integrating these tools, the government creates a comprehensive framework for promoting sustainable business practices.

The three types of corporate environmental governance policies—command-and-control, market-based incentives, and voluntary participation initiatives—employ distinct mechanisms to achieve environmental goals.

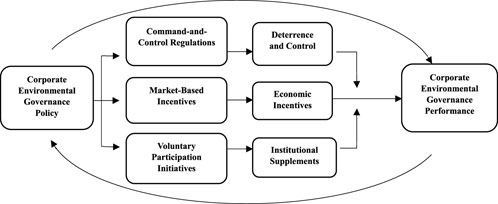

As shown in Figure 1, Command-and-control policies function by setting clear, legally enforceable standards that define optimal environmental practices. These regulations prescribe specific production methods and outline the legal penalties for non-compliance (Ambec and Barla, 2002; Greaker, 2006; Mohr, 2002). Through direct regulatory oversight, they ensure adherence to environmental standards, often by imposing fines or other sanctions on violators. Market-based incentives, in contrast, influence corporate behavior by leveraging economic factors. These policies create a system of rewards and penalties, giving environmentally responsible companies a competitive advantage (Acemoglu et al., 2012; Hart, 2004). For instance, carbon tax policies encourage businesses to adopt clean technologies, as doing so reduces their tax burden and improves their market position. Voluntary environmental policies, on the other hand, rely on indirect incentives to stimulate corporate participation. Companies may benefit from enhanced consumer preference for eco-friendly products, improved reputations, increased employee engagement, and lower financing costs by demonstrating environmental responsibility (Baron, 2007; Brekke and Nyborg, 2008; Kotchen, 2006; Lyon and Maxwell, 2003). Unlike market-based incentives, which still involve a degree of compulsion, voluntary policies offer companies greater flexibility, as participation is not mandated by law.

Figure 1. Mechanisms of corporate environmental governance policies.

These three categories of policies work in concert to foster improved corporate environmental governance in China. As corporate governance practices improve, they, in turn, provide positive feedback to policymakers, helping to refine and enhance the effectiveness of environmental governance policies.

This study relies on data collected from the “Peking University Law Database (PKU Law Database)”, using the keywords “enterprise,” “social responsibility,” “environmental protection,” and “green” to identify relevant policy texts. A total of 416 policy documents on corporate environmental governance, issued by the central government of China between 1982 and 2023, were initially downloaded. These documents underwent preliminary screening and data processing.

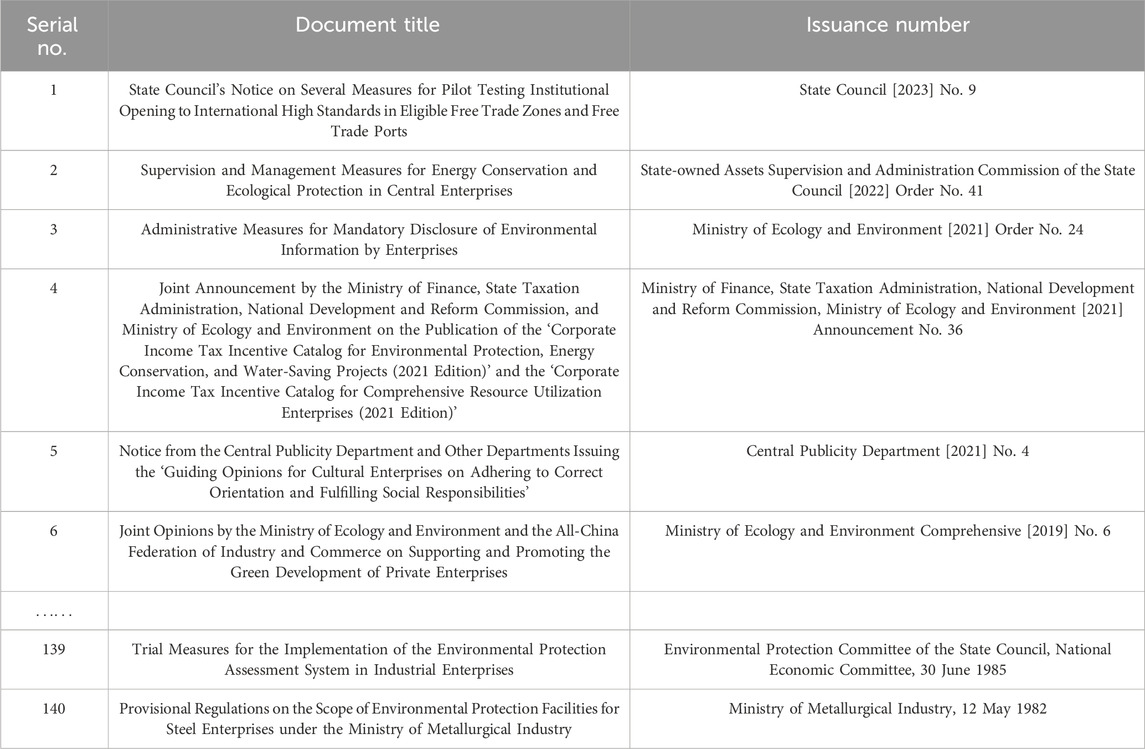

To ensure the relevance and authority of the selected documents, the study focuses exclusively on national-level corporate environmental governance policies issued by authoritative bodies, such as the National People’s Congress and its Standing Committee, the State Council, and ministries and commissions under the State Council. This selection includes laws, central regulations, and departmental regulatory documents. Working documents with lower legal validity were excluded, as they do not represent formal national policy. By limiting the scope of the analysis to these authoritative sources, the study ensures both the reliability and the universality of its findings. After this process, a total of 140 national corporate environmental governance policy texts were selected for analysis, as shown in (Table 2).

Table 2. Selected list of national-level corporate environmental governance policy documents included in the study.

This study uses textual analysis to examine 140 selected corporate environmental governance policies. The analysis begins by applying NVivo14, a qualitative data analysis software, to code the policy texts, converting qualitative language into quantifiable data for objective analysis. This approach allows for a systematic and quantitative evaluation of the policy documents. Following this digital analysis, the study integrates qualitative research methods to investigate key issues such as the evolution of corporate environmental governance policies, emerging trends, and the alignment of these policies with collaborative governance theory. Based on these insights, the study offers recommendations for enhancing China’s corporate environmental governance policy framework, with implications that are also valuable on a global scale.

China’s legal system has a rich historical tradition with unique characteristics. The recent 2023 amendment to the Legislation Law of the People’s Republic of China clarifies the authority of legislative and governmental bodies to issue various legal instruments, including laws, administrative regulations, local regulations, and rules. At the top of this hierarchy, the National People’s Congress and its Standing Committee have the exclusive right to create and amend laws, granting them the highest legal authority. Meanwhile, the State Council has the power to draft administrative regulations for issues requiring detailed interpretation in conjunction with existing laws or matters that fall within its public administration responsibilities. These administrative regulations obtain their validity from the broader legal framework.

In the meanwhile, ministries and commissions under the State Council can establish rules within their specialized areas, referred to as departmental rules. Importantly, despite the variations in names and jurisdictional scope, all laws, administrative regulations, and rules are legally binding and enforceable in judicial processes, underscoring the robustness of China’s legal framework. Furthermore, ministries and commissions under the State Council have the authority to issue regulatory documents, classified as “soft laws.” Unlike legally binding laws, soft laws, such as regulatory documents, are voluntary and nonbinding in court. Although they lack enforceability, these documents serve as guidance tools and reflect potential legislative trends, carrying less weight than laws enacted by the National People’s Congress, administrative regulations from the State Council, or departmental rules by State Council institutions.

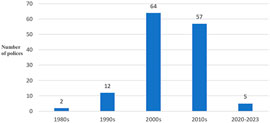

From 1982 to 2023, the distribution of corporate environmental governance policy documents issued by the central government reveals distinct periods of heightened activity. As shown in Figure 2, the majority of policy documents were issued during the periods from 2000 to 2009 (64 documents) and from 2010 to 2019 (57 documents). This surge in policy issuance correlates with the increased emphasis on environmental protection and corporate governance during China’s Tenth through Thirteenth Five-Year Plans. The importance of corporate environmental governance during these periods reflects the government’s growing focus on sustainable development. It is worth noting, however, that the data for policies issued after 2020 remains incomplete as this study extends only until 2023.

Figure 2. Number of corporate environmental governance policies issued in various periods.

Regarding the issuing bodies, 20 of the corporate environmental governance policy documents were jointly formulated by multiple agencies, including the Ministry of Ecology and Environment, the Ministry of Finance, the State Administration of Taxation, and the National Development and Reform Commission. These joint issuances account for 14.29% of the total. In contrast, single-department issuances make up the remaining 85.71%, with the Ministry of Ecology and Environment being the leading issuer, responsible for 108 documents (77.14%). This dominance highlights the central role of the Ministry of Ecology and Environment in shaping China’s corporate environmental governance policies. However, the involvement of other agencies, such as the Ministry of Finance and the State Administration of Taxation, underscores the necessity of multi-agency collaboration in addressing the complex challenges of environmental governance. This aligns with the principles of collaborative governance, where multifaceted cooperation is essential for effective policy implementation.

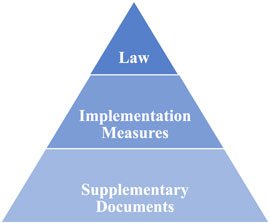

From the perspective of document classification, corporate environmental governance policies in China primarily consist of laws, opinions, notices, announcements, and replies. Laws, exemplified by the “Environmental Impact Assessment Law of the People’s Republic of China” (2018), hold the highest legal authority but constitute the smallest portion, accounting for only 0.71%. Next are implementation measures related to corporate environmental governance, categorized as departmental and military regulations. These carry slightly lower legal authority and represent a moderate proportion, accounting for 3.57%. Furthermore, there is a significant volume of supplementary documents, such as notices on tax incentives for environmentally friendly enterprises, replies regarding the implementation of specific environmental policies, guiding opinions aimed at enhancing corporate environmental governance, and announcements on compliant enterprises and relevant matters, comprising 95.71% of the total. As illustrated in Figure 3, the structure of corporate environmental governance policies in China is primarily composed of laws, implementation measures (departmental regulations), and supplementary provisions (normative documents), reflecting a pyramid-like distribution in terms of authority and quantity, consistent with typical patterns. However, the relatively limited number of binding and authoritative legal documents suggests that China’s corporate environmental governance policies are still in the process of development, indicating that timely legislative advancements should be pursued in the future.

Figure 3. Types and proportions of corporate environmental governance policies.

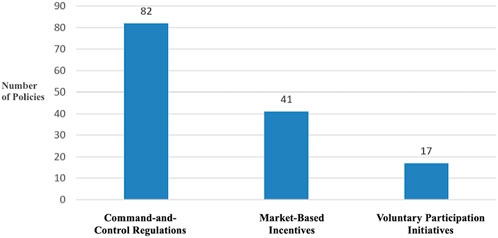

As mentioned above, an analysis of the dimensions of China’s corporate environmental governance policy texts from 1982 to 2023 reveals three main categories: command-and-control policies, market-based incentives, and voluntary participation policies. As shown in Figure 4, command-and-control policies dominate, accounting for 58.57% (82 documents) of total documents. Market-based incentive policies account for 29.29% (41 documents). And voluntary participation policies, which account for 12.14% (17 documents).

Figure 4. Number of corporate environmental governance policies by type.

The predominance of command-and-control policies reflects China’s reliance on regulatory measures to govern corporate environmental behavior, while market-based incentives and voluntary participation serve as supplementary tools. Together, these three types of policies complement one another, addressing different aspects of corporate environmental governance while working in tandem to achieve broader environmental goals.

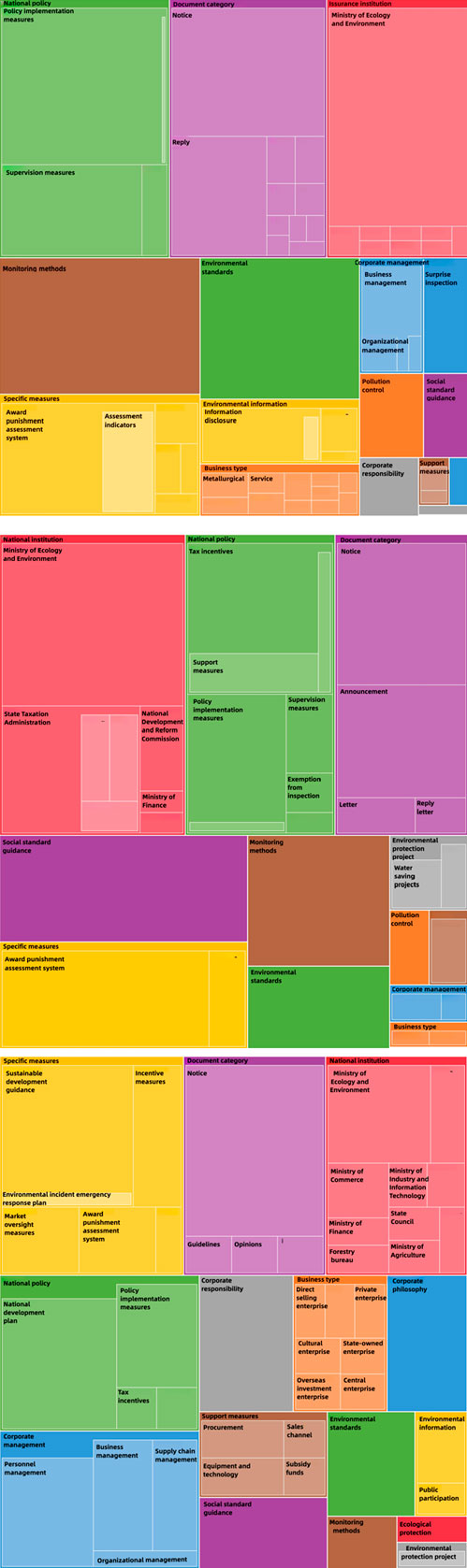

Additionally, as shown in Figure 5, by coding and analyzing the three types of policy texts, the differences between them become more apparent. Command-and-control policy texts primarily focus on the implementation and supervision of national policies, reward and penalty assessment systems, the establishment of environmental standards. The top three most frequent terms in this category are “pollutants,” “pollution sources,” and “person in charge.” Market-based incentive policy texts mainly revolve around national tax incentive policies, the guidance and promotion of social norms, reward and penalty mechanisms with a benefit-driven approach, and specific environmental protection projects. The top three most frequent terms in this category are “limited company,” “pollutants,” and “income tax.” Voluntary participation policy texts mainly focus on sustainable development guidelines, national development plans, corporate management, and supporting measures. The top three most frequent terms in this category are “consumers,” “suppliers,” and “host country.”

Figure 5. Comparison of coding types and quantities for different corporate environmental governance policies (The arrangement from top to bottom corresponds to command-and-control policy, market-based incentive policy, and voluntary participation policy, respectively).

Overall, the classification and dimensional analysis of China’s corporate environmental governance policies indicate alignment with the principles of collaborative governance. These policies encompass a wide range of stakeholders, including government entities, enterprises, and market actors, and are designed to encourage collaboration in improving environmental governance. The policies excel in setting consistent governance goals across stakeholders, using both negative incentives (such as penalties) and positive incentives (such as market-based rewards) to guide participants toward higher standards of environmental governance.

By examining the development of China’s corporate environmental governance policies from 1982 to 2023, it is possible to identify distinct evolutionary stages and regulatory models. Understanding these stages is crucial for predicting future trends and improving policy frameworks. Through a comprehensive quantitative and qualitative analysis, it becomes evident that China’s corporate environmental governance has undergone three distinct phases from 1982 to 2023.

As shown in Table 3, across these three stages, the regulatory model of corporate environmental governance has evolved. Initially dominated by command-and-control approaches, the governance model has gradually incorporated market incentives and voluntary participation, reflecting a more synergistic relationship between different policy instruments. As market-based and voluntary mechanisms have increased in prominence, the overall reliance on administrative orders has diminished, creating a more balanced and integrated framework for corporate environmental governance.

Table 3. Analysis of developmental phases of corporate environmental governance policies.

Using NVivo software to conduct text analysis and comparative research on 140 corporate environmental governance policy documents, we can identify the key regulatory themes within each evolutionary stage. In the centralized pollution control phase (1982–2006), policy texts predominantly focused on the supervision and monitoring of environmental protection facilities, the establishment and enforcement of environmental standards, and the development of reward and punishment systems for enterprises. The policies of this period were primarily geared toward ensuring compliance with national regulations, with an emphasis on controlling heavily polluting industries.

In the social responsibility advocacy phase (2007–2020), while maintaining regulatory oversight of corporate compliance with national environmental policies, the policy texts expanded to include guidelines on CSR, sustainable development, and alignment with national development plans. The state placed increasing importance on guiding enterprises to adopt CSR philosophies, with policies emphasizing the creation of benefit-oriented mechanisms and the establishment of a sustainability-oriented corporate ethos. Although the regulations during this phase were still largely non-binding, the shift in focus toward integrating CSR into corporate practices represented a significant evolution in China’s environmental governance framework.

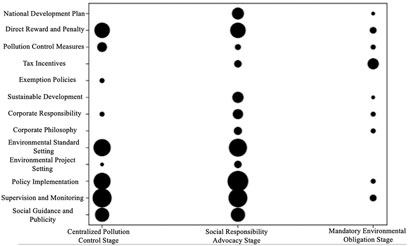

Since 2021, the mandatory environmental obligations phase has introduced policies with a much sharper focus on enforcing defined environmental obligations for enterprises. Although only a few years have passed since the onset of this phase, early policy texts already reflect a clear shift toward enforcing mandatory environmental information disclosure, as well as addressing issues like supply chain accountability and compliance with national development plans. As shown in Figure 6, the analysis of policy documents during this phase reveals an increasing emphasis on corporate responsibility for environmental reporting and transparency, marking a significant departure from the previous emphasis on voluntary participation and soft law measures.

Figure 6. Comparison of regulatory focus at different evolutionary stages of corporate environmental governance policies.

The textual analysis of policy documents highlights the progression of China’s approach to corporate environmental governance, evolving from the pollution control phase (1982–2006) to the mandatory environmental obligation phase (2021–present). This transformation has been profoundly shaped by the dynamics of China’s economic and social development.

First, economic factors have played an important role in this transformation. The relationship between economic growth and environmental change has been widely explored (Bhattarai, 2000; Anderson and Leal, 2001; Lahey and Doelle, 2012; Jaeger et al., 2023), with the Environmental Kuznets Curve serving as a key example. This curve suggests that environmental degradation initially increases with economic development but eventually decreases as countries reach higher levels of income. In China’s case, rapid economic growth, particularly in technology sectors such as the expansion of electric vehicle markets, has driven a corresponding shift in environmental policies, transitioning from pollution control to incentive-based and voluntary approaches.

In parallel, social development has been another significant driver of policy change. During the pollution control phase (1982–2006), China’s environmental policies were shaped by the country’s economic reform and opening up, which led to industrial expansion and, consequently, rising pollution levels. The policies of this phase predominantly focused on command-and-control measures to curb environmental damage. With the social responsibility advocacy phase (2007–2020), the focus expanded to include not only pollution control but also the promotion of CSR. Influenced by international CSR frameworks, China’s environmental policies broadened from focusing solely on pollution control to incorporating broader social issues such as labor protection and community welfare. The shift to the mandatory environmental obligations phase (2021–present) aligns with international trends in corporate due diligence laws, and reflects China’s efforts to demonstrate its growing global responsibility as a major player in environmental governance.

The compliance and effectiveness of these policies are critical concerns in assessing their true impact.

While the issuance of environmental policies has undoubtedly played a role in improving environmental protection in China, particularly with the introduction of implementation measures that are both specific and comprehensive, there have been challenges in achieving full compliance. The pollution control policies, in particular, were not fully enforced by relevant companies for a prolonged period. One reason for this non-compliance was that the penalties for violating environmental regulations were not sufficiently stringent to deter companies from engaging in polluting activities. Additionally, local government agencies, in some instances, allowed such non-compliance to continue, prioritizing economic growth over environmental protection. However, despite these challenges, the introduction of over a hundred relevant policies has contributed to shaping corporate environmental behavior, even if the full impact is not yet realized.

Moreover, the effectiveness of these policies has been influenced by the legislative tools employed. For example, the information disclosure law, which mandates companies to publicly disclose their environmental protection measures, has been an effective driver in encouraging corporate transparency and improving environmental performance. Additionally, many policies have shifted from relying solely on punitive measures to incorporating more motivational approaches. Tools such as green loans, incentives for companies to adopt environmentally friendly practices, and initiatives aimed at increasing public awareness about the benefits of choosing eco-friendly products have all proven to be valuable strategies for encouraging better environmental practices.

These methods have collectively enhanced environmental protection in China. Nonetheless, there remains room for improvement, particularly in the consistency and enforcement of regulations, to ensure that environmental policies lead to sustained and meaningful changes in corporate behavior.

Despite advancements in China’s environmental governance, several challenges persist, particularly regarding the authority of policies, non-conformity with collaborative governance theory, and the inadequacy of supply chain regulations.

One key issue facing China’s corporate environmental governance is that many relevant documents are issued as notifications, which carry relatively low legal authority. This often limits the enforceability of these policies, reducing their potential to drive significant changes in corporate behavior. Although recent policies in the mandatory environmental obligations phase have highlighted corporate environmental information disclosure, there is still no comprehensive framework mandating disclosure across all corporations. This gap undermines transparency and accountability.

To address this issue, it is crucial to issue more legally authoritative documents that regulate corporate environmental governance. Specifically, the National People’s Congress should enact more relevant laws, and the State Council should issue additional administrative regulations. One such example is the Administrative Measures for the Legal Disclosure of Corporate Environmental Information (2021), which represents a positive step toward addressing these issues. However, there remains a need for further regulations of this nature to strengthen the legal framework.

Collaborative governance theory emphasizes the need for cooperation among government, enterprises, communities, and other stakeholders to achieve effective governance. While China’s policies have made progress in aligning these actors toward common governance objectives, there are two critical areas where improvement is needed: the establishment of efficient communication channels and the mitigation of free-riding behavior.

First, efficient communication mechanisms must be implemented to address information asymmetry. While China’s Administrative Measures for the Legal Disclosure of Corporate Environmental Information (2021) mandates the centralized disclosure of environmental information, enforcement remains inconsistent across regions, particularly in smaller cities. Even in areas with more robust systems, the disclosed information often lacks depth and is limited to basic compliance statements rather than meaningful data (Guangzhou Municipal Bureau of Ecology and Environment). This deficiency impedes transparency and undermines efforts to assess corporate environmental practices effectively. Future policies should focus on enhancing the design and functionality of disclosure platforms, establishing clearer standards for disclosure content, and implementing more rigorous review processes. These efforts, aligned with collaborative governance theory, will help dismantle communication barriers, reduce inefficiencies, and foster stronger collaboration between government, enterprises, and the public.

Second, free-riding remains a significant obstacle in the implementation of collaborative governance. Some companies take a “wait-and-see” approach, relying on others to lead the way in enhancing industry environmental standards. Similarly, some consumers hesitate to support eco-friendly products, assuming that others will shoulder the cost burden. To combat this, future policies should integrate stricter enforcement mechanisms, such as tiered penalties for violators, and expand subsidies for the adoption of green technologies. Governments should also consider strengthening monitoring and evaluation systems to ensure ongoing oversight of corporate behavior and to ensure that corporate environmental commitments are met. Differentiated incentives, such as tax breaks or subsidies for companies that comply with environmental standards, and penalties for non-compliance, will encourage proactive engagement. Furthermore, promoting green finance could alleviate the financial burden on companies investing in environmental protection, while public education campaigns could increase consumer demand for sustainable products. Expanding the mandatory environmental information disclosure system will also foster greater transparency, enabling enhanced social oversight.

As corporate environmental governance becomes increasingly globalized, it is essential for countries to develop policies with extraterritorial effects. Several nations, including those in the European Union and North America, have introduced measures such as supply chain laws and carbon border adjustments to hold companies accountable for their environmental impacts beyond their borders. In comparison, China’s current supply chain regulations are still insufficient. While China has made strides by implementing information disclosure requirements for domestic firms and encouraging higher environmental standards for Chinese multinational corporations, there is a need for a more comprehensive and operational framework for extraterritorial governance (Tian, 2024; Tian et al., 2023).

Therefore, China should closely examine international models, such as the EU’s Supply Chain Act, and adapt them to its national context. A systematic framework for extraterritorial corporate environmental governance could include strengthening mandatory information disclosure requirements for both domestic companies and their foreign subsidiaries. Furthermore, the government should encourage academic and industry research to better understand the unique characteristics of corporate environmental governance, ensuring that policies remain innovative, practical, and aligned with global environmental trends. This approach will help enhance the competitiveness of Chinese enterprises in the international market and ensure China’s compliance with global environmental standards.

In conclusion, this study provides a comprehensive analysis of the evolution of China’s corporate environmental governance policies, identifying three distinct stages from 1982 to 2023: pollution control, social responsibility advocacy, and mandatory environmental obligations. While significant progress has been made in aligning these policies with collaborative governance theory, challenges persist, including weak enforcement authority, insufficient information disclosure mechanisms, free-rider problems, and limited extraterritorial application of regulations. Addressing these gaps through enhanced communication channels, stronger incentives, and globally aligned governance frameworks is essential to improving policy effectiveness. The findings and recommendations presented in this study not only contribute to refining China’s policy framework but also offer valuable insights for the global discourse on corporate environmental governance.

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

ZT: Conceptualization, Investigation, Methodology, Software, Validation, Visualization, Writing – original draft, Writing – review and editing. WY: Data curation, Resources, Supervision, Formal Analysis, Writing – review and editing. XT: Writing – review and editing, Conceptualization, Formal Analysis, Resources.

The author(s) declare that financial support was received for the research and/or publication of this article. This research was funded by the National Social Science Council of the Republic of China, grant number West Project-22XKS016, and the Ministry of Education Humanities and Social Sciences Research Planning Fund Project-22YJA820020.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

The author(s) declare that Generative AI was used in the creation of this manuscript. Language refinement.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Policy files and information are available upon request to the corresponding author.

Acemoglu, D., Aghion, P., Bursztyn, L., and Hemous, D. (2012). The environment and directed technical change. Am. Econ. Rev. 102 (1), 131–166. doi:10.1257/aer.102.1.131

Agudelo, L., Johannsdottir, B., and Davidsdottir, A. (2019). A literature review of the history and evolution of corporate social responsibility. Int. J. Corp. Soc. Responsib. 4 (1), 1–17. doi:10.1186/s40991-018-0039-y

Alnajjar, F. K. (2000). Determinants of social responsibility disclosures of U.S. Fortune 500 firms: an application of content analysis. Adv. Environ. Acc. Manag. 1, 163–200. doi:10.1016/s1479-3598(00)01010-4

Ambec, S., and Barla, P. (2002). A theoretical foundation of the Porter hypothesis. Econ. Lett. 75 (3), 355–360. doi:10.1016/s0165-1765(02)00005-8

Baron, D. P. (2007). Corporate social responsibility and social entrepreneurship. J. Econ. Manag. Strategy 16 (3), 683–717. doi:10.1111/j.1530-9134.2007.00154.x

Bhattarai, M. (2000). The environmental kuznets curve for deforestation in Latin America, Africa, and Asia: macroeconomic and institutional perspectives. Ph.D. Thesis. Clemson, SC: Clemson University.

Brekke, K. A., and Nyborg, K. (2008). Attracting responsible employees: green production as labor market screening. Res. Energy Econ. 30 (4), 509–526. doi:10.1016/j.reseneeco.2008.05.001

Chen, M., Sohail, S., and Majeed, M. T. (2022). Revealing the effectiveness of environmental policy stringency and environmental law on environmental performance: does asymmetry matter? Environ. Sci. Pollut. Res. 29 (60), 91190–91200. doi:10.1007/s11356-022-21992-3

Dechezlepretre, A., and Sato, M. (2017). The impacts of environmental regulations on competitiveness. Rev. Environ. Econ. Policy 11 (2), 183–206. doi:10.1093/reep/rex013

Deng, Z., Gao, T., Pang, R., and Yang, C. (2022). Research on the phenomenon of “passive collusion' of enterprises: analysis of the welfare effects of environmental regulation under the 'dual-carbon” goal. China Ind. Econ. 2022 (7), 122–140. doi:10.19581/j.cnki.ciejournal.2022.07.006

Fan, Q., and Zhang, Y. (2023). The impact of different environmental policy instruments on carbon productivity in China. Stat. Decis. 39 (16), 59–63. doi:10.13546/j.cnki.tjyjc.2023.16.011

Gao, H., and Zhang, J. (2021). Pluralistic synergy and cross-domain co-operation: a paradigm change is urgently needed in the governance of online cultural communities. Acad. Forum 45 (05), 115–124.doi:10.16524/j.45-1002.2021.05.006

Glicksman, R. L., and Markell, D. L. (2018). Unravelling the administrative state: mechanism choice, key actors, and regulatory tools. Environ. Law J. 36, 318–385.doi:10.2139/ssrn.3125675

Greaker, M. (2006). Spillovers in the development of new pollution abatement technology: a new look at the Porter hypothesis. J. Environ. Econ. Manag. 52 (1), 411–420. doi:10.1016/j.jeem.2006.01.001

Guangzhou Municipal Bureau of Ecology and Environment Enterprise environmental information by law and green system. Available online at: http://sthjj.gz.gov.cn/zwgk/qyqyhjxxyfpl/ (Accessed October 12, 2024).

Gui, J., and Pan, Y. (2022). Mechanisms for developing archival resources with local characteristics: an analytical framework for collaborative governance. Arch. Manag. 2022 (03), 29–33.doi:10.15950/j.cnki.1005-9458.2022.03.025

Hart, R. (2004). Growth, environment and innovation - a model with production vintages and environmentally oriented research. Environ. Econ. Manag. 48 (3), 1078–1098. doi:10.1016/j.jeem.2004.02.001

Hong, L., Peng, S., and Chen, H. (2022). Can strategic environment and trade policies promote environmental R&D innovation in exporting firms? A theoretical and China-based empirical study. Int. Trade Issues 2022 (08), 85–102. doi:10.13510/j.cnki.jit.2022.08.002

Hu, J., Song, X., and Wang, H. (2017). Informal system, hometown identity and corporate environmental governance. Manag. World 2017 (3), 76-94+187–188. doi:10.19744/j.cnki.11-1235/f.2017.03.006

Hu, Y. L. (2016). Challenges of advancing collaborative governance. CPC News. Available online at: http://theory.people.com.cn/n1/2016/0125/c49150-28081271.html(Accessed October 4, 2024).

Jaeger, W. K., Kolpin, V., and Siegel, R. (2023). The environmental kuznets curve reconsidered. Energy Econ. 120, 106561. doi:10.1016/j.eneco.2023.106561

Jin, J. (2017). National environmental governance and environmental policy audit: role mechanism, realistic dilemma and development path. China Adm. 2017 (5), 20–24.

Jose, A., and Lee, S. (2007). Environmental reporting of global corporations: a content analysis based on website disclosures. J. Bus. Ethics. 72 (4), 307–321.

Kotchen, M. J. (2006). Green markets and private provision of public goods. J. Polit. Econ. 114 (4), 816–834. doi:10.1086/506337

Lahey, W., and Doelle, M. (2012). Negotiating the interface of environmental and economic governance: Nova Scotia's environmental goals and sustainable prosperity act. Dalhous. Law J. 35 (1).

Li, D. (2012). Research on government investment project audit mode based on collaborative governance theory. Acc. Res. 2012 (9), 89–95+97.

Li, F., Zhu, B., and Sun, Y. (2021). Environmental policy, institutional quality and renewable energy technology innovation: an empirical analysis of 32 countries. Res. Sci. 43 (12), 2514–2525. doi:10.18402/resci.2021.12.13

Li, H., Liu, Q., Li, S., and Fu, S. (2022). Environmental, social and governance disclosure and corporate green innovation performance. Stat. Res. 39 (12), 38–54. doi:10.19343/j.cnki.11-1302/c.2022.12.003

Li, S. L., and Li, T. Y. (2021). Improvement and reform direction of complex environmental policy instrument system: a theoretical analysis framework. J. Sun Yat-sen Univ. (Soc. Sci. Ed.) 61 (2), 155–165. doi:10.13471/j.cnki.jsysusse.2021.02.017

Li, X., Zhou, M., and Wang, C. (2023). Local government environmental policy innovation and corporate environmental performance: micro empirical evidence based on the Yangtze River Delta region’s river-long system policy. China Popul. Resour.-Environ. 33 (3), 77–90.

Liao, Z. (2018). Content analysis of China’s environmental policy instruments on promoting firms’ environmental innovation. Environ. Sci. Policy 88, 46–51. doi:10.1016/j.envsci.2018.06.013

Lin, R., Xie, Z., Li, Y., and Wang, C. (2015). Political affiliation, government subsidies and environmental disclosure: a resource dependence theory perspective. J. Public Adm. 12 (2), 30-41+154–155. doi:10.16149/j.cnki.23-1523.2015.02.004

Liu, B. (2021). China’s state-centric approach to corporate social responsibility overseas: a case study in Africa. Transnat. Environ. Law 10 (1), 57–84. doi:10.1017/s2047102520000229

Liu, C. (2015). Regulation, interaction and third-party governance of environmental pollution. China Popul. -Resour.-Environ. 25 (2), 96–104.

Liu, J. (2018). Research on the innovation of government online public opinion governance mode in the new media era. Intell. Sci. 36 (12), 66–70+89.doi:10.13833/j.issn.1007-7634.2018.12.013

Liu, Y., Huang, Z., and Liu, X. (2021). Environmental regulation, executive compensation incentives, and corporate environmental investments: evidence from the implementation of the 2015 Environmental Protection Law. Account. Res. 2021 (5), 175–192.

Long, W., Li, S., and Ding, Z. (2018). Environmental policy and environmental performance of small and medium-sized enterprises: administrative coercion or economic incentives? Nankai Econ. Res. 2018 (3), 20–39. doi:10.14116/j.nkes.2018.03.002

Lu, J., and Yan, Y. (2022). Environmental policy and resource allocation: a literature review and future prospects China Popul. Resour. Environ. 32 (12), 127–137.

Lyon, T. P., and Maxwell, J. W. (2003). Self-regulation, taxation and public voluntary environmental agreements. J. Pub. Econ. 87 (7), 1453–1486. doi:10.1016/s0047-2727(01)00221-3

Mohr, R. D. (2002). Technical change, external economies and the Porter hypothesis. J. Environ. Econ. Manag. 43 (1), 158–168. doi:10.1006/jeem.2000.1166

OECD (2007). Environmental policy and corporate Behaviour. Paris: OECD Publishing. doi:10.1787/9789264175075-en

Shen, H., and Zhou, Y. (2017). Environmental enforcement supervision and corporate environmental performance: quasi-natural experimental evidence from environmental protection interviews. Nankai Manag. Rev. 20 (6), 73–82.

Shen, Z. Y., and Chen, J. A. (2017). Research on the collaborative governance of migrant workers’ professionalisation under the new economic normal. Rural. Econ. 2017 (6), 125–128.

Si, L. J., and Cao, H. Y. (2022). Can green credit policy improve corporate environmental social responsibility – based on the perspectives of external constraints and internal concerns. China Ind. Econ. 2022 (4), 137–155. doi:10.19581/j.cnki.ciejournal.2022.04.009

Tian, C., and Han, Z. (2021). Do harsh environmental policies encourage technological innovation? Res. Manag. 42 (10), 166–173. doi:10.19571/j.cnki.1000-2995.2021.10.019

Tian, Z. H. (2024). China's due diligence legislation for environmental governance on Transnational corporations: history and future. ENVIRONMENT 66 (3), 7–25. doi:10.1080/00139157.2024.2319570

Tian, Z. H., Yang, W. S., and Tan, C. X. (2023). A Statistical Examination of the Link between environmental performance and legal practices: an evaluation of China's strategies for Residual legislative power allocation. Front. Environ. Sci. 11. doi:10.3389/fenvs.2023.1293595

Tilt, C. A. (2001). The content and disclosure of Australian corporate environmental policies. Acc. Aud. Acc. J. 14 (2), 190–212. doi:10.1108/09513570110389314

United Nations Human Rights Council. (2011). United nations guiding principles on business and human rights.

Wang, F., Zhao, Y., and Xia, J. (2022). Heterogeneous environmental policies, executive risk preferences and green technology innovation - an empirical study based on heavily polluted listed companies in China. Res. Manag. 43 (11), 143–153. doi:10.19571/j.cnki.1000-2995.2022.11.015

Wang, H., Khan, M. A. S., Anwar, F., Shahzad, F., Adu, D., and Murad, M. (2021). Green innovation practices and its impacts on environmental and organizational performance. Front. Psychol. 11, 553625. doi:10.3389/fpsyg.2020.553625

Wang, N., Qi, Y., and Dong, H. (2016). A study on the selection of environmental policy tools based on corporate attitudes. Sci. Technol. Manag. Res. 36 (16), 236–242.

Wang, X., and Wang, Y. (2021). Green credit policy for green innovation. Manag. World 37 (6), 173–188+11. doi:10.19744/j.cnki.11-1235/f.2021.0085

Wang, Y., Wang, H. Y., and Xue, S. (2022). Greening the tax system and corporate ESG performance – a quasi-natural experiment based on the Environmental Protection Tax Law. Fin. Res. 48 (9), 47–62. doi:10.16538/j.cnki.jfe.20220621.101

Wei, N., and Zhao, C. G. (2016). Research on cross-regional air pollution synergistic management – Taking Beijing-Tianjin-Hebei area as an example. Hebei J. 36 (1), 144–149.

Wei, Y., and Hu, C. (2021). A study on the relationship between environmental policy, corporate social responsibility, and corporate performance: an empirical analysis based on environmentally non-compliant enterprises in heavy pollution industries. J. East China Univ. Sci. Technol. (Soc. Sci. Ed.) 36 (3), 125–133.

Wu, F. (2015). Research on China-ASEAN cross-border regional co-operation under the perspective of collaborative governance. Soc. Sci. 2015 (7), 45–48.

Xu, C. Q., and Huang, Y. M. (2020). Collaborative governance: the role of universities in the construction of Guangdong-Hong Kong-Macao Greater Bay Area and its realisation path. Pub. Adm. Rev. 13 (2), 109–124+197.

Xu, H., and Tan, D. (2023). Analysis of pollution control and optimal environmental policy of government enterprises based on differential games. Oper. Res. Manag. 32 (7), 107–112.

Yang, Z., Chen, J., and Ling, H. C. (2023). Media attention, environmental policy uncertainty and corporate green technology innovation - empirical evidence from Chinese A-share listed companies. J. Manag. Eng. 37 (04), 1–15. doi:10.13587/j.cnki.jieem.2023.04.001

Ye, C., Wang, Z., Wu, J., and Li, H. (2015). External governance, environmental information disclosure and the cost of equity financing. Nankai Manag. Rev. 18 (05), 85–96.

Ye, C. M., and Wu, L. H. (2023). Environmental policy, dynamic capability, and corporate green transformation – a longitudinal case study of Guangxi Liuzhou Iron and Steel Group. Sci. Technol. Prog. Countermeas. 40 (10), 1–12.

Zeng, B., Zheng, J., and Qiu, Z. (2016). A study on the role of environmental policy instruments in improving environmental quality: an analysis based on inter-provincial panel data in China from 2001 to 2012. Shanghai Econ. Res. 2016 (5), 39–46. doi:10.19626/j.cnki.cn31-1163/f.2016.05.005

Zhang, D., Yang, J., and Liu, Z. (2021). Empirical analysis of the impact of heterogeneous environmental policies on firms' technological innovation capability - based on two-way fixed effects model. Bus. Res. 2021 (04), 68–74. doi:10.13902/j.cnki.syyj.2021.04.009

Zhang, H. (2016). A study of strategic interactions of interregional environmental regulation: an explanation for the prevalence of incomplete enforcement of environmental regulation. China Ind. Econ. 2016 (7), 74–90. doi:10.19581/j.cnki.ciejournal.2016.07.006

Zhang, X. R., Zhang, H. T., Li, Y. L., and Zhang, L. F. (2022). A study on the identification of key elements of information synergy in public health emergencies. Intell. Theory Pract. 45 (3), 141–148.doi:10.16353/j.cnki.1000-7490.2022.03.020

Zhang, Y. A., and Ma, Y. (2017). Quantitative analysis of regional technological innovation policy based on R language. J. Intell. 36 (3), 113–118.

Keywords: corporate environmental governance, policy instruments, policy text analysis, corporate due diligence, collaborative governance theory

Citation: Tian Z, Yang W and Tang X (2025) Evolutionary characteristics of corporate environmental governance policies in China: a policy instrument analysis (1982–2023). Front. Environ. Sci. 13:1528831. doi: 10.3389/fenvs.2025.1528831

Received: 15 November 2024; Accepted: 25 March 2025;

Published: 10 April 2025.

Edited by:

Carmine Massarelli, National Research Council of Italy - Construction Technologies Institute, ItalyReviewed by:

Oran Young, University of California, Santa Barbara, United StatesCopyright © 2025 Tian, Yang and Tang. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Zehua Tian, em9yYV90aWFuemhAZ2NjLmVkdS5jbg==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.