Quan’An Fu

Quan’An Fu

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 22 July 2024

Sec. Environmental Economics and Management

Volume 12 - 2024 | https://doi.org/10.3389/fenvs.2024.1426837

To address the pressing challenges posed by environmental issues, numerous countries have been actively exploring green finance practices. Using a sample of listed companies in China from 2008 to 2020, this study aims to enrich the understanding of the economic consequences of green finance. Specifically, it is the first to investigate the causal relationship between green finance and corporate debt financing levels. Our findings reveal that green finance effectively mitigates corporate debt financing levels, and this conclusion remains robust after undergoing a series of rigorous tests. Further analysis reveals that green finance achieves this by alleviating financing constraints and enhancing executive compensation. Heterogeneity analysis demonstrates that the impact of green finance is particularly pronounced in state-owned enterprises, regions with lower marketization levels, superior industrial structures, and lower carbon emissions. Additionally, our research shows that with the strengthening of external environmental regulations, green finance significantly promotes the reduction of long-term debt financing levels but has no significant impact on short-term debt financing levels. The conclusions of this study provide valuable insights for policymakers and enterprises seeking to reduce corporate debt financing levels. Moreover, it offers a new perspective on the economic consequences of green finance, particularly in the context of debt financing.

Amidst the pressing global concerns regarding climate change and environmental degradation, the need for environmental protection and sustainable development has gained prominence. Green finance, an innovative financial paradigm, has emerged as a key instrument to facilitate environmental protection, address climate change, and propel economic sustainability. China, as the world’s largest developing nation, presents a unique and intricate context for the development of green finance.

Firstly, China faces significant environmental challenges. Years of heavy industrialization have led to severe environmental pollution and ecological damage. This has prompted the Chinese government to recognize the imperative of transforming its economic model towards a greener path. Green finance is expected to play a pivotal role in this transition by channeling capital towards environmentally friendly industries and projects. Secondly, the Chinese government has accorded high priority and policy support to green finance. This is evident from the enactment of several policy documents, such as the “Guiding Opinions on Establishing a Green Finance System.” Additionally, the government has promoted green financial products like green bonds and green credits, encouraging financial institutions to engage in green finance activities and steering social capital towards green sectors. Moreover, the development of green finance in China has garnered widespread international attention and cooperation. The escalating global demand for green finance has spurred China to actively participate in international green finance collaborations, sharing its developmental experiences and contributing to the global green finance agenda. This provides China with a broadened international perspective and collaborative opportunities for its green finance initiatives. In summary, the backdrop of China’s green finance development is complex yet promising, driven by environmental challenges, government policies, and international collaborations. The aim is to harness the power of finance to foster environmental protection and sustainable economic growth.

With the continuous evolution of traditional financial instruments, they have provided crucial assistance in addressing various corporate financial difficulties, injecting momentum into sustainable business growth. As a result, enterprises have flourished, yet their rampant development has also led to an increase in energy consumption and pollution emissions, making environmental issues particularly salient in today’s context (Shen et al., 2024). Against this backdrop, green finance, as a powerful tool to mitigate environmental pollution, has garnered extensive and profound discussions. Essentially, green finance represents a more efficient allocation of financial resources, guiding commercial banks to reduce lending to polluting enterprises, thereby decreasing their total factor productivity (Feng and Liang, 2022). This, in turn, encourages these enterprises to actively pursue green transformation, significantly enhancing their economic and environmental performance (Zhang et al., 2024). Furthermore, commercial banks play a pivotal role in promoting the development of green finance. Traditional financial tools often encounter mismatches between specific funds and projects, leading to higher risk exposure for commercial banks. However, green finance can effectively identify potential risks in the green financing process, ultimately reducing the risk exposure of these banks (Feng et al., 2024). Concurrently, green finance is increasingly becoming a pivotal force in tackling global environmental challenges and advancing sustainable development. Firstly, it strengthens the peer effect of ESG information disclosure, making environmental, social, and governance data from the same industry and similar enterprises more comparable (Liang and Yang, 2024). This not only enhances information transparency but also facilitates investors’ accurate assessment of corporate performance. Secondly, in the face of the potential impact of climate policy uncertainty on corporate investment efficiency, green finance directs capital flows towards environmentally friendly projects and prompts enterprises to enhance their total factor productivity, thereby effectively elevating investment efficiency and achieving a win-win scenario for both businesses and investors (Zhang et al., 2023). Finally, green finance fosters the development of green productivity in enterprises by supporting green technologies and innovations, and leverages the spatial spillover effect of environmental regulations to promote green productivity in neighboring regions (Feng et al., 2021). In summary, green finance plays a pivotal role in driving sustainable development and promoting environmental and social win-win outcomes.

For both businesses and households, financial literacy and green finance policies play a crucial role in alleviating financing constraints. At the household economic level, it has been proven that good financial literacy can effectively mitigate household income constraints and help families manage their financial resources better (Ling et al., 2023). On the business front, green finance policies are particularly significant for enterprises in resource-depleted cities and those committed to green innovation and renewable energy (Chen et al., 2024). Green finance not only significantly alleviates the financing constraints faced by these enterprises, thereby promoting their operations and development, especially investments in green innovation (Yu et al., 2021). Moreover, research has shown that financing constraints often limit the investment efficiency of renewable energy companies, and the development of green finance can effectively mitigate such constraints, enabling these companies to achieve higher investment efficiency (Wang and Fan, 2023). Therefore, green finance demonstrates significant effectiveness in alleviating financing constraints for enterprises. The integration of ESG factors into financial decision-making can lead to a more favorable perception among investors, who are increasingly prioritizing sustainability in their investment portfolios. This positive perception can translate into lower costs of capital for companies, as investors are willing to offer more competitive financing terms to those that demonstrate a commitment to sustainable practices. By mitigating financing constraints, green finance enables companies to access the debt markets more easily, thus supporting their overall financial stability and growth prospects. Moreover, green finance can enhance executive compensation. As companies embrace sustainable practices, executives who demonstrate leadership in this area are often recognized and rewarded with higher compensation packages. This incentive aligns executives’ interests with the long-term sustainability of the company, encouraging them to make more responsible decisions that align with the company’s strategic objectives. By rewarding sustainable performance, green finance creates a virtuous cycle where executives are motivated to further integrate ESG considerations into their financial decision-making, leading to a more sustainable and profitable operation.

The mediation of these two mechanisms—alleviated financing constraints and enhanced executive compensation—is crucial in understanding the impact of green finance on corporate debt cost. On one hand, by mitigating financing constraints, green finance enables companies to access the debt markets more efficiently, thus reducing their cost of capital and enhancing their financial flexibility. On the other hand, by enhancing executive compensation, green finance incentivizes executives to prioritize sustainable practices, which can lead to more responsible financial decision-making and strategic investments. These two mechanisms work in tandem, reinforcing the positive impact of green finance on corporate debt financing.

In addition, it is important to note that the influence of green finance extends beyond the financial realm, encompassing both strategic and operational aspects of a company. By embedding sustainability into their financial decision-making, companies can unlock new opportunities for growth and innovation, while also mitigating risks associated with environmental and social challenges. This comprehensive approach to sustainability can lead to a more resilient and sustainable business model, positioning companies to thrive in a rapidly changing global economy.

As countries across the globe aim to transition towards more sustainable development models, understanding the role of green finance in driving green economic growth and enhancing resource efficiency becomes increasingly crucial. For developing countries, this issue holds particular importance. These nations often face financial constraints in implementing green projects that can promote sustainability and address environmental issues. However, by harnessing the power of green finance, these countries can access the necessary financial resources to develop and execute projects that not only enhance their economies but also protect their natural resources. Moreover, developing countries have historically suffered from resource inefficiency due to mismanagement and lack of proper policies. Studying the links between green finance, green economic growth, and resource efficiency can help these nations identify and address the root causes of inefficiency, leading to improved utilization of their resources and enhanced economic performance. The findings of such studies can have far-reaching implications for global sustainability efforts. By promoting green finance and green economic growth, countries can contribute to mitigating climate change, preserving natural resources, and creating a more environmentally sustainable world. Therefore, studying the interconnections between these areas is not only beneficial for individual nations but also holds immense global significance.

The present study offers several incremental contributions to the existing research on the effects of green financial policies on enterprise debt financing levels. First, it addresses the limitations of He and Liu (2023) by providing a more comprehensive analysis that encompasses all enterprises, rather than focusing solely on green and highly polluting enterprises. While He and Liu relied on the classification from the Wind database, the current study adopts a more authoritative approach, utilizing national policy documents as the criterion for distinguishing high-carbon enterprises. This approach ensures a more accurate representation of enterprises’ carbon intensities. Second, this study supplements the work of Guo and Fang (2024) by incorporating green fiscal policies into the measurement of green finance indices. In the Chinese context, where the government plays a pivotal role in economic activities, green fiscal policies serve as critical guiding mechanisms. By including green fiscal policies, the current study offers a more holistic understanding of the green financial system and its influence on enterprise debt financing. Moreover, the current study improves upon the methodology employed by Guo and Fang (2024). Specifically, while they utilized the Difference-in-Differences (DID) approach to examine the impact of green credit on enterprise debt financing, their treatment and control group classification based on industry categories was suboptimal. The implementation of green credit policies in 2007 was universal, encompassing all enterprises, not just those in “two high” industries. In summary, by incorporating green fiscal policies and utilizing a more authoritative enterprise classification, this study offers a more nuanced and comprehensive understanding of the effects of green financial policies on enterprise debt financing levels. This approach not only addresses the limitations of previous research but also provides valuable insights for policymakers and stakeholders seeking to promote sustainable financing practices.

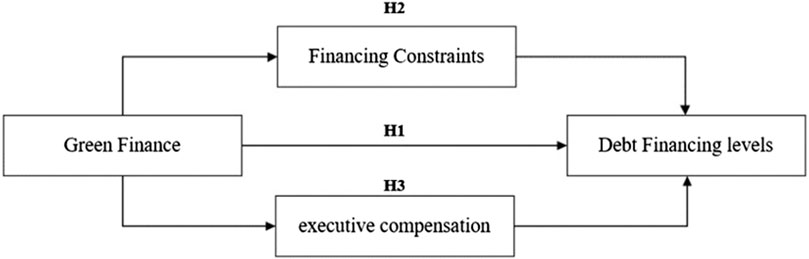

In summary, this paper aims to comprehensively explore the impact of green finance on corporate debt financing, focusing on the mediating role of alleviated financing constraints and enhanced executive compensation. By examining these relationships, we aim to contribute to the existing literature on green finance and corporate finance, providing valuable insights for companies, investors, and policymakers alike. Through a deeper understanding of the mechanisms underlying the green finance-debt financing nexus, we hope to facilitate more informed and sustainable financial decision-making that benefits both companies and society at large. The specific structure of the research design is depicted in Figure 1.

Figure 1. Research framework.

In recognition of the urgency to tackle climate change and its widespread global impacts, it is evident that carbon emissions, stemming from the non-competitive and non-excludable nature of air resources, carry significant negative externalities. This intricacy hinders the clear establishment of property rights, potentially leading to market failures. Given this context, relying solely on market forces to attain Pareto efficiency in reducing carbon emissions presents considerable challenges. Market participants are unlikely to spontaneously internalize social costs that exceed their private costs, often resulting in avoidable equilibrium losses (Liu and Zhu, 2024). Therefore, the government’s intervention, serving as the guiding force in the carbon emissions market, becomes crucial for facilitating optimal resource allocation. Among the various policy tools available, green finance stands out as a pivotal market-oriented environmental approach. Green finance provides a mechanism for channeling funds towards sustainable projects and investments, such as the development of environmentally sustainable infrastructure, clean technologies, and renewable energy sources. The Paris Agreement and other global initiatives have further emphasized the need for alignment between financial strategies and climate goals, sparking a heightened interest in researching green finance practices and regulations. Concurrently, investors and consumers are becoming increasingly aware of the environmental ramifications of their financial decisions, driving a surge in demand for environmentally responsible investing products and services. In response to these evolving trends, researchers and academics have been actively engaged in exploring green finance, thereby enriching the academic literature in this domain.

A growing body of literature has delved into the intricate relationship between green finance, energy efficiency, and carbon emissions, primarily focusing on macroeconomic and microeconomic perspectives. Macroeconomic studies often explore the impact of green finance on national or regional levels, analyzing its ability to enhance energy efficiency, mitigate carbon emissions, and foster sustainable development. On the other hand, microeconomic studies zoom in on the specific impact of green finance on individual firms or industries, examining its role in promoting green technologies, enhancing corporate sustainability practices, and driving innovative solutions. At the macroeconomic level, the establishment and growth of green finance mechanisms have been shown to effectively mitigate urban haze pollution (Zeng et al., 2022), enhance green productivity (Xu and Xu, 2022), and reduce energy intensity across both local and neighboring regions (An et al., 2023). These cumulative effects contribute significantly to the reduction of carbon dioxide and greenhouse gas emissions (Zhan et al., 2022), thereby supporting global efforts towards environmental sustainability. Furthermore, green finance has demonstrated a substantial stimulatory effect on renewable energy investments, fostering a shift towards cleaner and more sustainable energy sources (Li et al., 2022). As green finance continues to expand, it not only elevates the economic value of regions but also contributes to global value growth (Li et al., 2023). However, it is important to recognize that the impact of green finance may vary across regions and countries. While studies in East Asia have demonstrated a significant reduction in carbon dioxide emissions attributed to green finance, findings from Central and South Asia indicate that green finance has had limited effects on carbon dioxide reduction (Sun, 2023). This heterogeneity underscores the need for tailored policies and strategies that consider the unique contextual factors of different regions. At the micro level, the Green Finance Reform and Innovation Pilot Zones implemented in China in 2017 provide an excellent setting to study the economic consequences of green finance. Research conducted within these zones has revealed that green finance significantly suppresses corporate carbon emissions (Zhou and Qi, 2023), enhances corporate social responsibility (Yu et al., 2023), and stimulates green innovation among enterprises (Han et al., 2022; Li et al., 2023). Notably, the impact of green finance on corporate innovation is most pronounced in middle-to high-income regions (Wang et al., 2022), suggesting that the effectiveness of green finance may be contingent on the economic development of the region. Moreover, given the unique challenges posed by high-polluting enterprises, research has found that China’s Green Finance Reform and Innovation Pilot Zones exert a significant inhibitory effect on green innovation among these enterprises (Ren et al., 2020). This finding underscores the need for targeted policies that address the specific challenges and opportunities presented by high-polluting sectors.

A significant body of literature has explored the relationship between green finance and economic development. Du et al. (2019) and Shan et al. (2021) found that green investments and green credit facilities can facilitate the growth of a green economy. Specifically, Bai et al. (2022) demonstrated that following the COVID-19 pandemic, the increasing demand and cost of energy globally have highlighted the urgent need for green finance to mitigate potential crises. The implementation of green finance policies has notably reduced industrial gas emissions (Muganyi et al., 2021), improved environmental pollution (Dong et al., 2023), and enhanced overall energy efficiency (Zhou et al., 2022). The driving effect of green financing is particularly prominent among high-polluting industries. Due to their inherent financing constraints, the existence of green finance incentives these companies to proactively fulfill their social responsibilities (Li et al., 2023), reduce pollution and energy consumption (Qin and Cao, 2022), thereby contributing to the reduction of carbon intensity (Ren and Zhang, 2023) and ultimately enhancing ESG performance (Zhang, 2023). In the specific context of China, the steady growth of green finance in recent years (Lv et al., 2021) has optimized resource allocation, further propelling economic quality development (Li et al., 2022). However, this development is uneven, with more rapid progress in the eastern coastal regions, exhibiting distinct regional characteristics (He and Yan, 2020; Ma et al., 2023). Zhao and Qi. (2023) further reveal that green finance’s carbon emission reduction effects are limited to the central and eastern regions. Additionally, green finance policies have effectively facilitated the emergence of China’s manufacturing value chain (Lin et al., 2023), simultaneously optimizing the overall industrial structure (Hu et al., 2023). This structural upgrading, in turn, promotes the further development of green finance (Lan et al., 2023).

The determination of corporate debt financing levels is a complex process influenced by a myriad of factors. First and foremost, the external environment and policy events have been identified as crucial determinants of debt financing levels. Liu (2023) and Yu et al. (2021) emphasized the dynamic nature of the external environment, arguing that economic shifts, market fluctuations, and policy changes can significantly impact a company’s debt financing decisions. For instance, favorable economic conditions might encourage companies to increase their debt levels to fund expansion, while adverse economic events might prompt them to reduce debt to mitigate risk. Moreover, Meng and Yin. (2019) brought to light the significance of the national governance environment in shaping corporate debt financing costs. They argued that countries with stronger institutional frameworks and higher governance standards often enjoy lower debt financing costs due to increased trust and confidence among creditors. This trust is founded on the belief that well-governed countries are more likely to uphold contract enforcement, property rights, and legal systems that protect creditor interests. Furthermore, the role of investor protection mechanisms in debt financing has garnered significant attention. Scholars such as La Porta et al. (2002), López Iturriaga (2005), Qian et al. (2007), and Lin et al. (2011) have demonstrated that higher levels of investor legal protection, enforcement quality, and regional marketization can effectively mitigate moral hazard and adverse selection issues. These mechanisms, by reducing the risk of internal shareholders or managers infringing on creditor interests, encourage creditors to offer loans at lower interest rates. This, in turn, benefits both the creditor and the corporate borrower, fostering a more efficient and transparent debt financing market.

The existing literature has provided a comprehensive exploration of various topics, offering valuable theoretical insights into the subject matter at hand. However, a gap remains in the discussion of the impact of green finance on corporate debt levels. This research aims to bridge that gap, offering a novel perspective that contributes to the existing knowledge base. Previous research has delved into a wide range of factors that influence corporate debt levels, including external environmental factors, policy events, and governance structures. However, the specific implications of green finance on this aspect of corporate finance have received limited attention. Green finance, which encompasses sustainable financing practices and environmental considerations in financial decision-making, is expected to have a significant impact on corporate debt levels. This impact could manifest in terms of altered debt issuance strategies, cost of debt, or even the overall financial risk profile of a company. By exploring the nexus between green finance and corporate debt levels, this study aims to contribute to the existing theoretical framework by providing empirical evidence on the potential benefits and challenges of green financing practices. The expected findings could inform financial decision-making, corporate strategy, and policy recommendations aimed at promoting sustainable finance and environmental stewardship.

This paper argues that the regional development of green finance will lead to a reduction in the cost of corporate debt financing. A range of reasons and empirical evidence support this inference.

Firstly, the growth of green finance at the regional level typically results in the availability of specialized green financial products and services. These include green bonds, green loans, and green investment funds that are designed to finance environmentally sustainable projects. As these products become more prevalent, they provide enterprises with additional financing options that are often cheaper and more flexible than traditional debt financing. Secondly, the promotion of green finance by regional governments and financial institutions can lead to improved environmental risk management practices among enterprises. Enterprises that integrate sustainable practices into their operations are perceived as having lower environmental risks and hence are more attractive to investors. This reduces the cost of debt financing as investors are willing to offer lower interest rates to mitigate the perceived risks. Thirdly, green finance’s evolution and prominence have been instrumental in promoting transparency and disclosure among enterprises, laying the foundation for them to adopt more sustainable and environmentally responsible business practices. Before the introduction of specific green financial policies, enterprises often operated with limited visibility regarding their environmental impacts, making it difficult for investors and stakeholders to accurately assess their green credentials. However, as green finance gains traction, enterprises are increasingly compelled to disclose their environmental performance, including greenhouse gas emissions, resource utilization, and waste management practices. This transparency not only enables investors to make informed decisions about green investments but also puts pressure on enterprises to improve their environmental practices. As a result, green finance not only fosters financial innovation but also acts as a catalyst for environmental stewardship, driving enterprises towards more sustainable and responsible business models. Enterprises that are committed to green finance are more likely to provide detailed information about their environmental performance, sustainability goals, and the use of green finance. This transparency improves the trust between enterprises and investors, leading to more efficient capital allocation and lower financing costs. Moreover, the integration of green finance into regional financial systems can enhance the overall stability and resilience of financial markets. By promoting sustainable investing and managing environmental risks, green finance can mitigate the financial risks associated with climate change and other environmental challenges. This stability can translate into lower financing costs for enterprises as investors are more confident in investing in regions with well-developed green finance infrastructure.

The main hypothesis in this study is as follows:

Hypothesis 1:. Regional Development of Green Finance Reduces the Cost of Debt Financing for Enterprises.

This study hypothesizes that the regional development of green finance can effectively lower the cost of debt financing for enterprises by mitigating financing constraints. This assertion is grounded in several theoretical and empirical rationales that are central to corporate finance and sustainable development.

Firstly, green finance aims to mobilize capital towards environmentally sustainable projects and enterprises. By doing so, it creates a financing environment where enterprises with green projects or sustainable business models can access funds more easily. This reduces financing constraints, as these enterprises are no longer limited by traditional financing barriers that might exclude them due to environmental risks or non-compliance with sustainability standards. Secondly, the growth of green finance typically involves the development of specialized green financial instruments and policies. These instruments, such as green bonds and green loans, are tailored to meet the financing needs of sustainable projects and enterprises. By providing alternative financing channels, these green financial products can alleviate financing constraints by broadening the range of financing options available to enterprises. Thirdly, the integration of green finance into regional financial systems often leads to improved information disclosure and transparency among enterprises. This transparency is crucial for investors, as it allows them to better assess the environmental and financial risks associated with potential investments. By providing investors with reliable information about the environmental performance of enterprises, green finance can help mitigate information asymmetry and reduce the perception of risk, thereby lowering financing costs. Fourthly, the promotion of green finance by governments and financial institutions can foster a more favorable regulatory environment for sustainable finance. This can include tax incentives, subsidies, and other policy measures that encourage enterprises to adopt green practices and invest in sustainable projects. By reducing the financial burden and regulatory hurdles faced by sustainable enterprises, these policies can help alleviate financing constraints and lower debt financing costs.

Therefore, the second hypothesis is proposed as follows:

Hypothesis 2:. The Development of Green Finance in Various Regions Reduces Corporate Debt Financing Costs by Mitigating Financing Constraints.

This study proposes a hypothesis that the development of green finance in different regions can enhance executive compensation, which in turn, may lower the cost of debt financing for enterprises. This assertion is grounded in several theoretical frameworks and empirical evidences from the fields of corporate finance, sustainability, and executive compensation.

Firstly, the growth of green finance typically leads to an increase in investment opportunities for enterprises engaged in environmentally sustainable activities. As these enterprises become more attractive to investors seeking to align their capital with sustainable projects, they are likely to experience improved financial performance. Improved financial performance often translates into higher profits, which in turn can justify higher executive compensation packages. Secondly, executive compensation is often tied to the financial performance of the enterprise. By promoting sustainable business models and green practices, enterprises may enjoy a competitive edge in the market, leading to improved financial outcomes. These positive financial results can then be reflected in executive compensation, as a reward for their stewardship in steering the enterprise towards sustainability. Thirdly, green finance may influence executive compensation through changes in the governance structures and incentive mechanisms of enterprises. As green finance becomes more prevalent, enterprises may adopt governance practices that prioritize sustainability and environmental performance. These practices may include the integration of sustainability targets into executive compensation plans, incentivizing executives to pursue green strategies that lower the enterprise’s debt financing costs. Lastly, Higher executive compensation may enhance the enterprise’s ability to attract and retain talented executives, who are crucial in managing financial risks and optimizing debt structures. Additionally, a stronger financial position enabled by green finance can improve the enterprise’s creditworthiness, leading to more favorable lending terms and lower financing costs.

Based on the above analysis, the third hypothesis is proposed:

Hypothesis 3:. The Development of Green Finance in Various Regions Enhances Executive Compensation and Subsequently Reduces Corporate Debt Financing Costs.

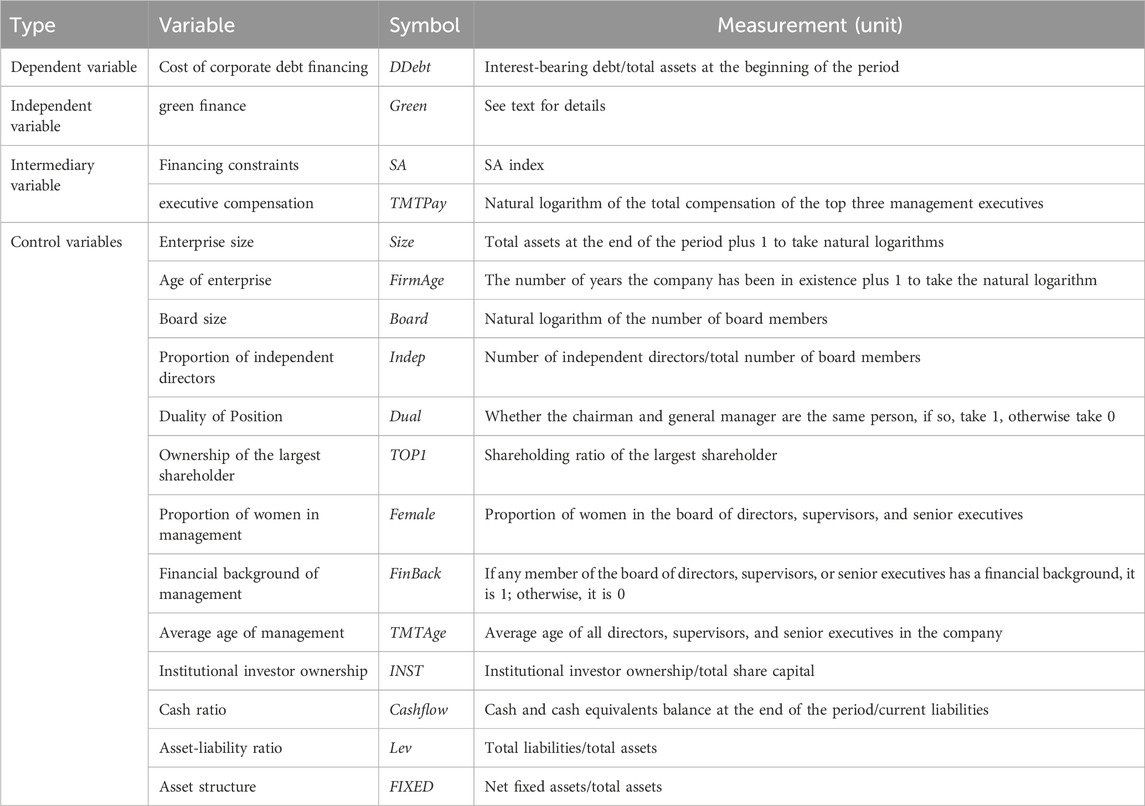

Interest-bearing debt financing, which consists of the ratio of interest-bearing debt to total assets at the beginning of the period.

This article defines green finance from two perspectives: micro and macro. Micro perspective mainly focuses on constructing an indicator evaluation system around the green proportion of financial assets, while macro perspective mainly analyzes from the perspective of innovative financial instrument selection. Therefore, the idea of constructing the relevant indicator system is to select and calculate the ratio of some representative innovative green financial instruments (green credit, green investment, green insurance, green fiscal) to the relevant overall economic data. Using entropy method as the indicator weighting method (Ran et al., 2023), this article constructs the green finance evaluation indicator system, as shown in Table 1.

Table 1. The measure of green finance.

To investigate the influence of green finance levels on the cost of corporate debt financing, this paper establishes a benchmark model denoted as Eq. 1:

Where i represents the enterprise, t represents the year. To ensure that the regression results are robust and reliable, this paper controls for industry fixed effects (

Table 2. Definitions of variables.

To delve into the possible mechanisms, this article draws inspiration from the mediation effect testing approaches employed by Shen et al. (2024), Feng et al. (2023), Hao et al. (2023), and Gao et al. (2023) and constructs the following mediation effect testing model.

where intermediary variables

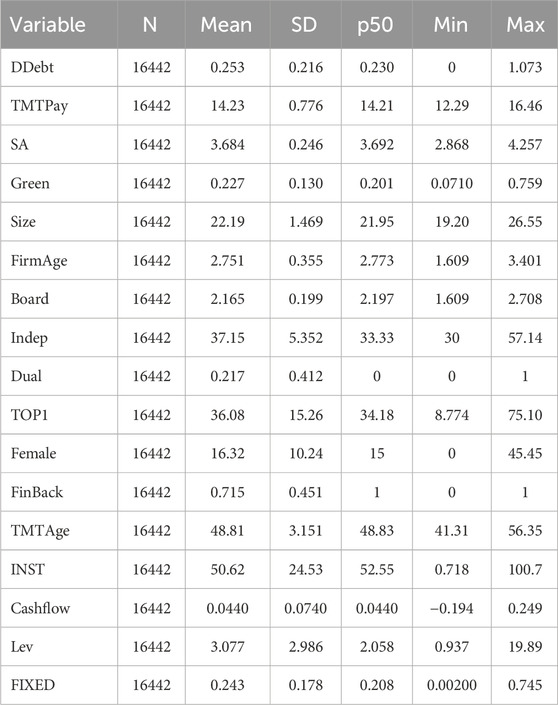

In this study, Considering that China’s introduction of new corporate accounting standards in 2008 and the occurrence of major public health and safety events after 2020 have an impact on corporate financial information, hence, we have selected Chinese A-share listed companies from 2008 to 2020 as our initial sample. Drawing from existing literature, we have excluded samples belonging to the financial, ST, and missing data categories. Additionally, all continuous variables have been truncated at the 1% level to mitigate the impact of extreme values on our research findings. This study performs clustering at the individual company level. To gather relevant data, we have utilized the CSMAR and CNRDS databases for enterprise-related information. For provincial-level data, we have referred to various provincial Statistical Yearbooks, the China Statistical Yearbook, and the China Insurance Yearbook.

For data completeness, median interpolation was taken to fill in the missing data and also removed samples with severe missing variable values. The results of descriptive statistics of the data are as Table 3. The sample consisted of a total of 16442.

Table 3. Descriptive statistics.

This section reports the primary empirical findings of the study. Firstly, we delve into the baseline regression results, offering insights into the initial findings of our analysis. Secondly, we proceed to examine the mechanistic effects of financing constraints and executive compensation, assessing their individual and combined impacts on the overall results. Subsequently, we employ a range of tests to ensure the robustness of our findings. These tests help to validate the consistency and reliability of our results, accounting for various potential confounders and alternative explanations. Lastly, we delve into the heterogeneity of the green finance’s impact on reducing financing costs. To accomplish this, we categorize our analysis based on firm ownership, regional marketization levels, industrial structure variations, economic development statuses, and carbon emission intensities.

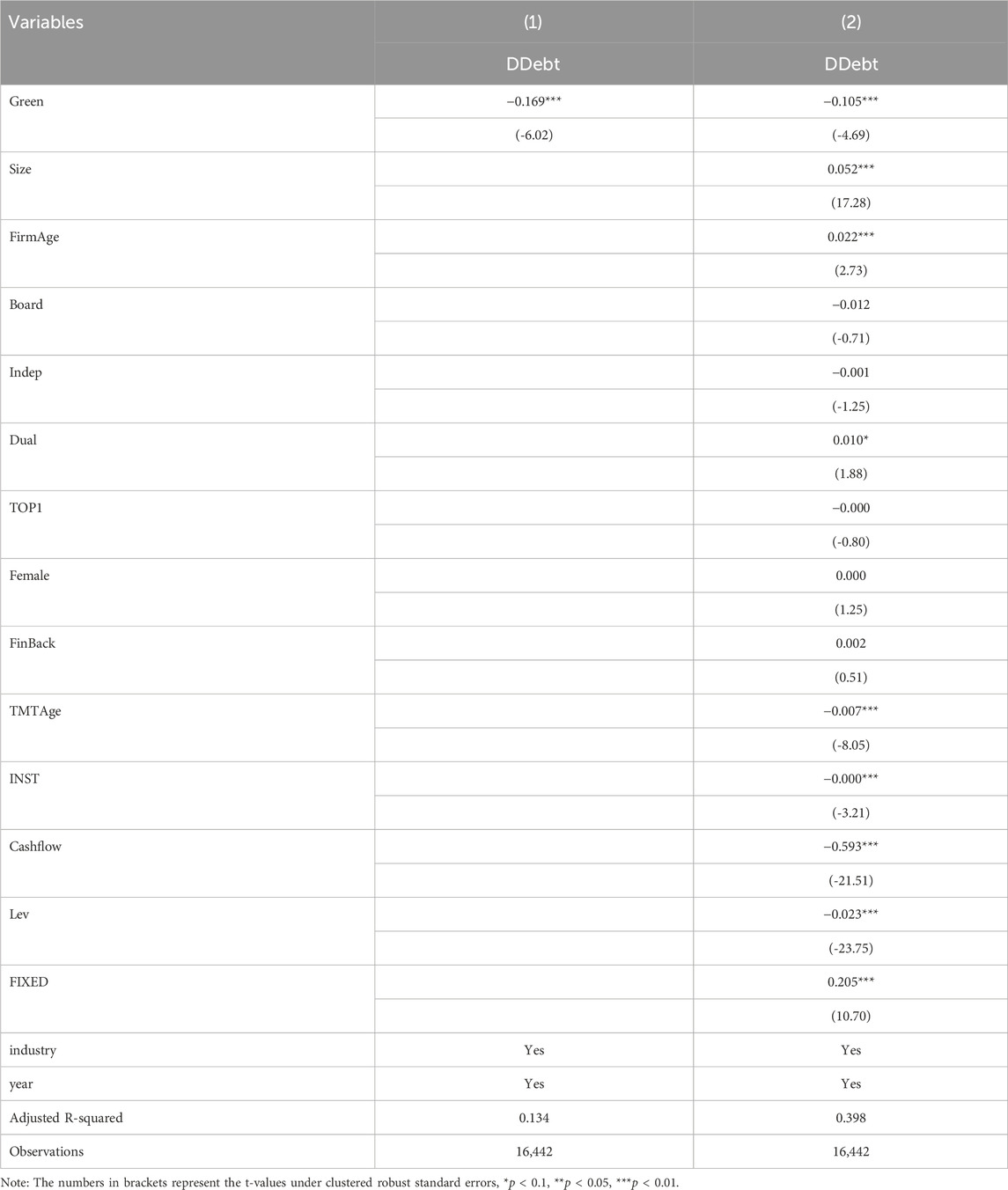

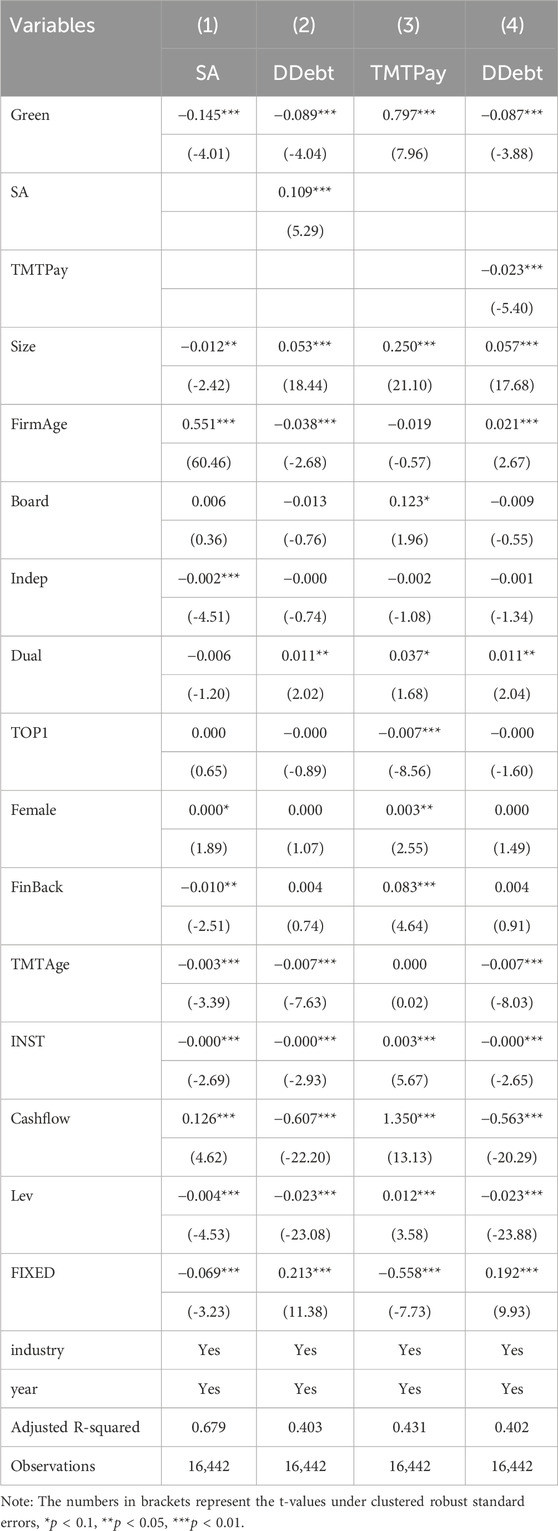

Table 4 presents the empirical results examining the impact of green finance on reducing the cost of corporate debt financing. The coefficient associated with green finance exhibits statistical significance at the 1% level, indicating that green finance is effective in mitigating the cost of corporate debt financing. This finding validates Hypothesis 1.

Table 4. Benchmark regression results.

The table below presents the baseline regression results of the model, controlling for both industry and year fixed effects across both columns. Column (1) displays coefficients that are negative at the 1% significance level, excluding the inclusion of control variables. Subsequently, the regression incorporates control variables, and the results are presented in Column (2), which align with the previous findings. The results indicate that the core independent variable remains significantly negative at the 1% level. Notably, the adjusted fit improves significantly when incorporating control variables compared to the model without control variables. This underscores the importance of considering the influencing factors represented by these variables as they impact the dynamics of corporate financing costs.

Overall, the baseline regression results provide initial evidence for the effectiveness of green finance in mitigating the cost of corporate debt financing. Building upon these findings, we argue that the implementation of green finance-related measures has facilitated progress towards reducing the cost of corporate debt financing. Consequently, financial institutions and governments should fully consider the financial implications of green finance and continue to develop and enhance the green finance system.

The results of the mediation effect test for financing constraints are presented in columns (1) and (2) of Table 5. Specifically, when controlling for various variables, green finance has a significantly negative impact on corporate financing constraints, indicating that an increase in the level of green finance can effectively alleviate financing constraints for enterprises. Green finance mitigates corporate financing constraints by channeling capital towards environmentally sustainable projects, which reduces risk and attracts investors seeking long-term returns. When the variable for corporate financing constraints is included in the regression analysis, the coefficient for green finance remains significantly negative, consistent with the baseline regression findings. Additionally, the coefficient for financing constraints is significantly positive, suggesting that the alleviation of financing constraints effectively reduces the cost of debt financing for businesses. When financing constraints are relaxed, enterprises have greater access to capital, enabling them to negotiate more favorable terms with lenders. This leads to a decrease in interest rates and easier credit access, ultimately reducing the overall cost of debt financing. This finding validates Hypothesis 2.

Table 5. Intermediary mechanism test results.

The results of the mediation effect test for executive compensation are presented in columns (3) and (4) of Table 5. Specifically, when controlling for various variables, green finance has a significantly positive impact on executive compensation in corporate settings. This indicates that an increase in the level of green finance can effectively enhance executive compensation. Investors reward companies that adopt green strategies with higher valuations, translating into increased shareholder wealth and subsequently, higher executive compensation. Green finance also attracts capital from investors seeking environmentally responsible investments, which can enhance a company’s financial standing and profitability, further justifying higher executive remuneration. When the variable for executive compensation is included in the regression analysis, the coefficient for green finance remains significantly negative, consistent with the baseline regression findings. Additionally, the coefficient for executive compensation is significantly negative, suggesting that an increase in executive compensation effectively reduces the cost of debt financing for businesses. Increased executive compensation can lower the cost of corporate debt financing by aligning executives’ incentives with the long-term financial interests of the company. By providing executives with incentives to prioritize cost-effective debt financing strategies, their compensation serves as a mechanism to align their decision-making with the financial objectives of the firm, ultimately leading to lower debt financing costs. Higher executive compensation may incentivize executives to pursue strategies that minimize debt risk and maximize shareholder value, further contributing to lower debt financing costs. This finding validates Hypothesis 3.

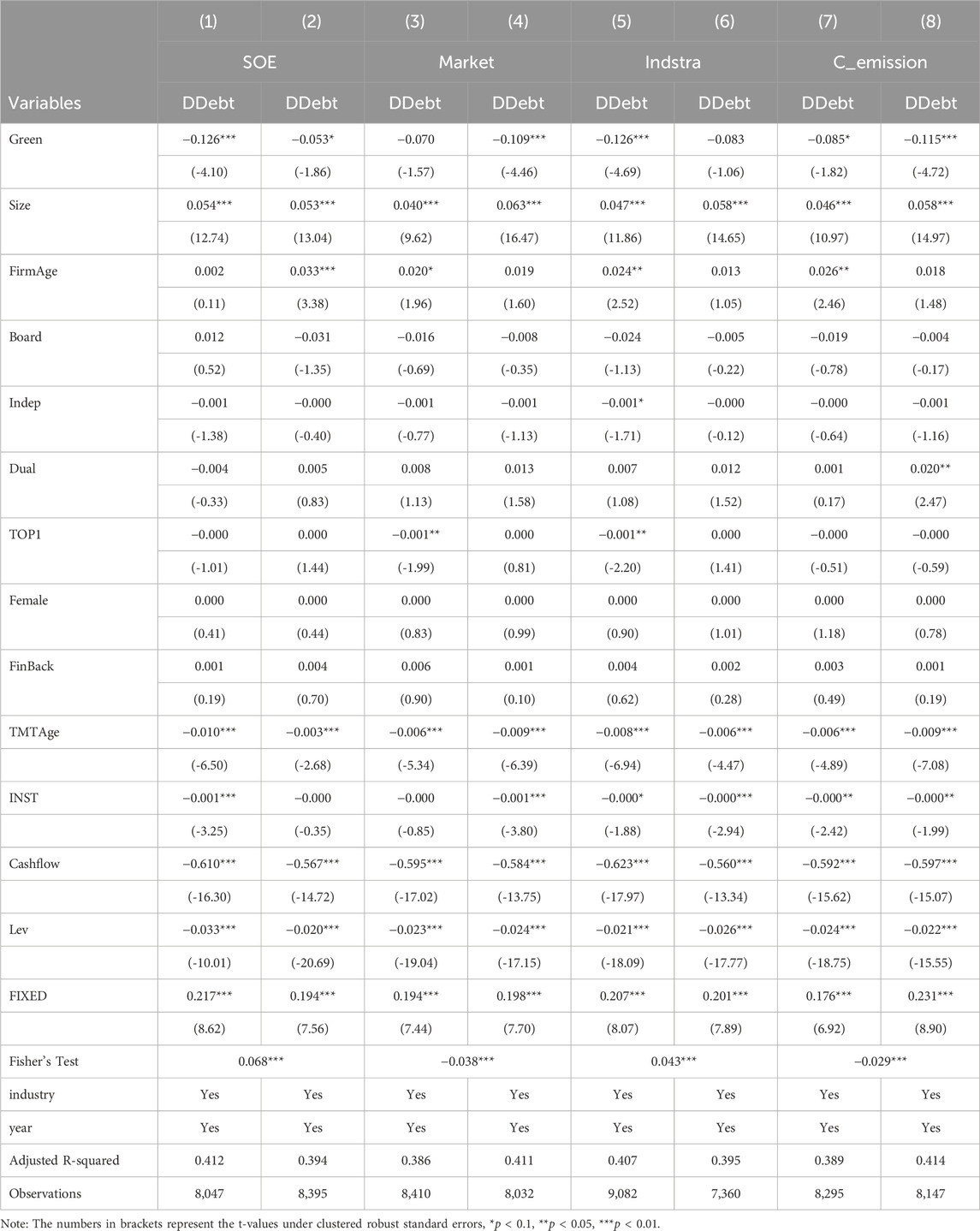

To further validate Hypothesis 1 and explore whether the impact of green finance on reducing the level of corporate debt financing is influenced by factors such as the nature of corporate ownership, the degree of regional marketization, regional industrial structure, and regional carbon emissions, we conducted a heterogeneity analysis. The estimation results are presented in Table 6.

Table 6. Heterogeneity test results.

Given that private enterprises and state-owned enterprises (SOEs) operate under distinct mandates and objectives, it is essential to unpack how these ownership dynamics impact their utilization of green finance options and subsequent debt financing levels. This exploration holds particular relevance for green finance initiatives, as it highlights the need for tailored strategies that account for the unique challenges and opportunities posed by different ownership structures. In the forthcoming analysis, we aim to provide a nuanced understanding of how the ownership nature of a company interacts with green finance opportunities, ultimately shaping its debt financing position. By doing so, we seek to contribute to the evolving discourse on green finance and its role in sustainable corporate finance practices.

As shown in Columns (1) and (2) of Table 6, the results indicate that green finance has a significant impact on reducing the level of corporate debt financing, regardless of whether the company is state-owned or private. Through the Fisher’s test, it can be observed that the effect of green finance on reducing the debt financing costs of state-owned enterprises is more pronounced. The effectiveness of green finance in reducing debt financing costs is more pronounced for state-owned enterprises (SOEs) compared to private enterprises due to several key factors. Firstly, SOEs are typically larger and have a stronger financial position, which enables them to leverage green finance initiatives more effectively. This is because SOEs have access to larger capital pools and can thus invest more in green projects, leading to cost savings and environmental benefits. Secondly, SOEs often face tighter regulatory scrutiny and social expectations, which motivate them to prioritize environmentally sustainable practices. This includes seeking financing through green finance channels, which can provide lower-cost capital due to the lower risk associated with sustainable projects. Moreover, the government often provides support and incentives for green initiatives in SOEs, such as preferential loan rates or tax breaks. These measures further enhance the cost-effectiveness of green finance for SOEs, making it a more attractive option compared to traditional financing methods.

As the present study aims to delve into the intricate relationship between green finance and corporate debt financing, it is imperative to consider the varying degrees of marketization as a critical factor that may introduce heterogeneity in the observed patterns. Marketization, referring to the varying degrees of financial market development and competitiveness across regions or economies, can significantly influence the implementation and effectiveness of green finance strategies. By examining the influence of marketization level, this study aims to provide a nuanced understanding of the contextual factors that may shape the relationship between green finance and corporate debt financing.

As shown in columns (3) and (4) of Table 6, the results indicate that the primary impact of green finance in reducing the level of corporate debt financing is observed in markets with lower degrees of marketization. In regions with lower levels of marketization, the impact of green finance in mitigating corporate debt financing is more significant compared to regions with higher levels of marketization. This is because markets with lower marketization typically exhibit a greater need for external financing, making them more reliant on alternative financing mechanisms such as green finance. In regions with high marketization, financial markets are typically more developed and efficient, providing firms with a wide range of financing options. In such markets, the role of green finance may be less prominent as firms can access capital through traditional channels. However, in regions with lower marketization, where financial markets may be less developed or efficient, green finance can play a more crucial role in bridging the financing gap for firms. Moreover, in regions with lower marketization, there is often a greater need for policy intervention and support to promote sustainable economic development. Green finance can serve as a key instrument in these regions, providing capital for green projects and sustainable businesses. By doing so, green finance can help to reduce the debt financing needs of firms, particularly those engaged in environmentally friendly activities. In summary, our argument is that the primary benefits of green finance in reducing corporate debt financing are more pronounced in markets with lower levels of marketization. This is due to the greater need for external financing, less developed financial markets, and the important role of policy intervention in promoting sustainable development in these regions.

As the present study delves into the intricate relationship between green finance and corporate debt financing, it is imperative to consider the varying levels of industrial structure as a potential moderator of this relationship. The complexity and diversity of industrial landscapes across regions can introduce heterogeneity in the observed patterns and effects. By examining the influence of industrial structure, this study aims to provide a nuanced understanding of how different industrial configurations shape the impact of green finance on corporate debt financing.

As demonstrated in columns (5) and (6) of Table 6, the findings indicate that the effectiveness of green finance in mitigating the level of corporate debt financing is primarily observed in markets with superior industrial structures. In regions with superior industrial structures, the conditions are more conducive to the effective implementation of green finance strategies, thereby enabling a more significant reduction in corporate debt financing levels. This is because regions with stronger industrial landscapes typically exhibit a higher concentration of innovative and sustainable businesses, which align with the objectives of green finance. These businesses are more likely to attract green investors and enjoy lower financing costs due to their alignment with environmentally friendly practices. Contrastingly, regions with weaker industrial structures often lack the necessary resources, technological capabilities, and institutional frameworks to support green finance initiatives. This may limit the effectiveness of green finance in these areas, as businesses may face greater challenges in accessing green financing and achieving sustainable operations. Therefore, the impact of green finance on reducing corporate debt financing may be less significant in these regions. Moreover, superior industrial structures often foster stronger collaboration and coordination among businesses, governments, and financial institutions. This collaboration can lead to the development of more comprehensive and tailored green finance solutions that are better suited to the local context. In turn, this can enhance the impact of green finance in reducing corporate debt financing levels. In summary, our argument is that the primary benefits of green finance in reducing corporate debt financing are more pronounced in markets with superior industrial structures, where the conditions are more conducive to the successful implementation of green strategies. This is due to the presence of a more conducive business environment, stronger institutional frameworks, and better alignment with sustainable practices.

Regions with high carbon emissions are expected to benefit more from green finance strategies, as they face greater pressure to transition to more sustainable economic models. Conversely, regions with low carbon emissions may already have a more favorable environmental profile, but green finance can still play a role in supporting their transition to a net-zero emissions future. By analyzing data from regions with different carbon emission levels, we aim to reveal patterns and trends that underscore the importance of considering regional carbon emissions when assessing the role of green finance in corporate finance decisions. The results of this analysis will contribute to the existing knowledge on green finance and sustainability, providing valuable insights for policymakers, financial institutions, and corporate decision-makers seeking to align their strategies with environmental objectives.

As shown in columns (7) and (8) of Table 6, the results indicate that green finance has significantly reduced the level of corporate debt financing, regardless of whether the region has a high or low carbon emission level. Specifically, in regions with lower carbon emissions, green finance has had a more pronounced positive effect on reducing the level of corporate debt financing. This study finds that green finance has played a significant role in reducing the level of corporate debt financing, regardless of the region’s carbon emission level. This conclusion is supported by the empirical evidence presented in Table 6, which demonstrates a consistent and significant relationship between green finance and debt financing across both high and low carbon-emitting regions. Specifically, in regions with lower carbon emissions, the positive impact of green finance on reducing debt financing is even more pronounced. This suggests that in areas where environmental sustainability is already a priority, green finance strategies can be more effective in supporting corporate finance decisions that align with environmental objectives. The argument is strengthened by the observation that green finance not only mitigates financing constraints but also serves as a catalyst for sustainable economic growth. By redirecting capital towards environmentally friendly projects and activities, green finance helps to create a virtuous cycle where economic growth and environmental protection go hand in hand.

In conclusion, the findings of this study underscore the importance of green finance in promoting sustainable corporate finance practices across all regions, regardless of their carbon emission levels. The positive impact is particularly strong in regions where environmental sustainability is a priority, highlighting the need for a more widespread adoption of green finance strategies in corporate decision-making.

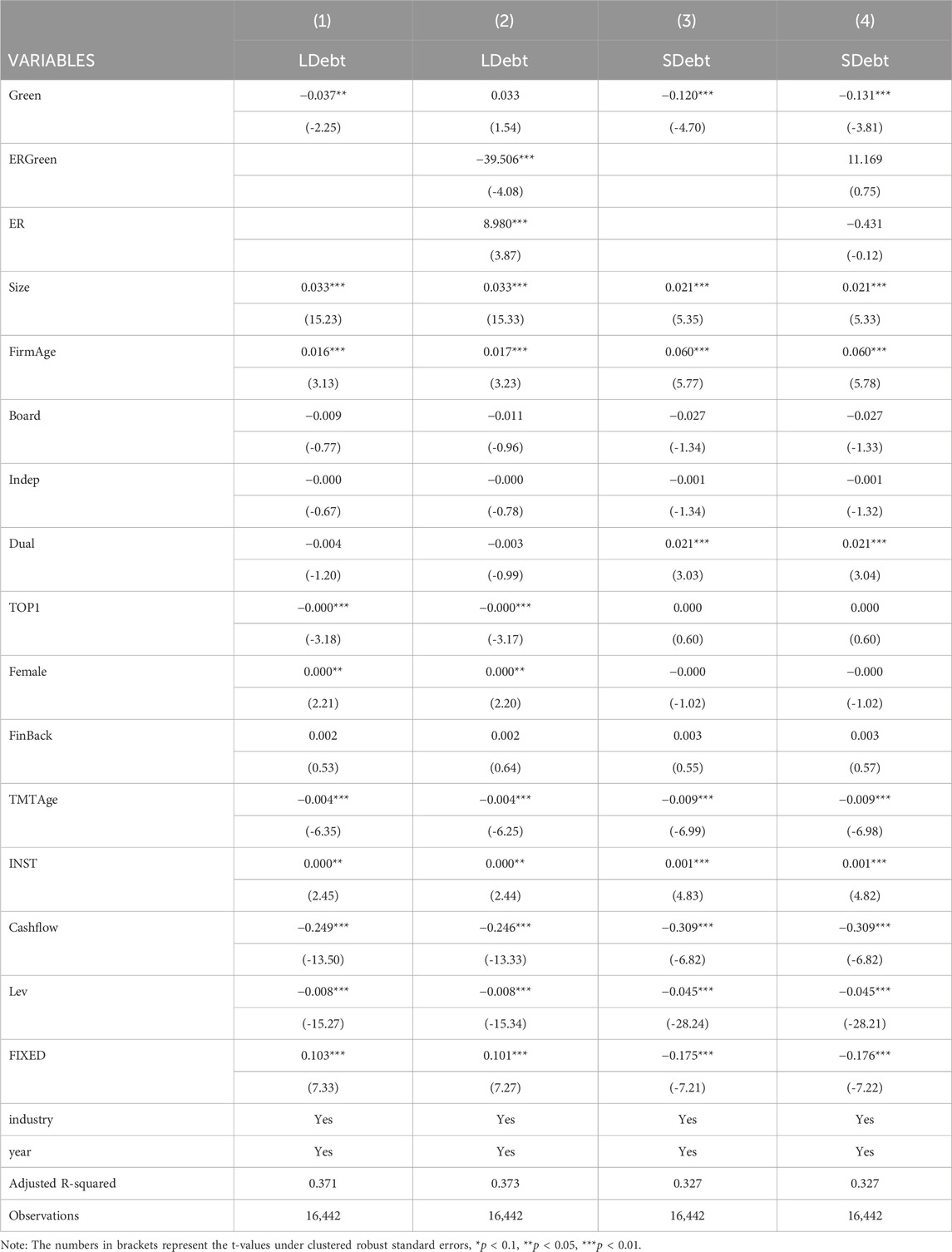

Building upon the preceding analysis of heterogeneities in the impact of green finance on corporate debt financing levels, we delve deeper into understanding the specific effects of green finance on both long-term and short-term debt financing. This examination is further nuanced by considering the crucial role of environmental regulations in shaping these relationships. By exploring the mechanisms through which environmental regulations promote green financing practices and their subsequent influence on debt financing costs and levels, we aim to provide a comprehensive understanding of the intertwined relationships between green finance, environmental policies, and corporate debt financing strategies. In doing so, we contribute to the evolving discourse on sustainable finance, highlighting the significance of environmental regulations in greening the financial system and promoting sustainable corporate financing practices.

Drawing from previous research, this study employs the ratio of short-term liabilities to total assets at the beginning of the period to measure the level of short-term debt financing (SDebt) and the ratio of long-term liabilities to total assets at the beginning of the period to measure the level of long-term debt financing (LDebt). To measure environmental regulation (ER), the ratio of investment completed for industrial pollution control to the added value of the secondary industry is employed.

As shown in columns (1) and (3) of Table 7, the results indicate that green finance has a significant impact on reducing both the level of long-term debt financing and the level of short-term debt financing for firms. Firstly, the impact of green finance on long-term debt financing is noteworthy. Green finance initiatives encourage sustainable investment practices that align with environmental objectives. This alignment reduces the risk profile of long-term debt financing, as investors become more confident in the financial viability and environmental sustainability of the projects financed. Consequently, companies are able to access cheaper and more sustainable long-term debt, thereby reducing their overall debt financing levels. Moreover, the influence of green finance on short-term debt financing cannot be overlooked. Short-term debt, though typically less sensitive to sustainability factors, still benefits from green finance initiatives. This is because green finance not only focuses on environmental sustainability but also enhances financial efficiency and risk management. By integrating green finance practices, companies can improve their liquidity management and risk mitigation strategies, which in turn leads to more favorable short-term debt financing options. As evident from columns (1) and (2) of Table 7, the strengthening of environmental regulations significantly promotes the role of green finance in reducing the level of long-term debt financing for corporate entities. Enhanced environmental regulations force companies to prioritize sustainable practices and align their financial strategies with environmental objectives. Green finance, which promotes investments in environmentally friendly projects, becomes a key enabler in this transition. By financing projects that align with environmental goals, green finance reduces the risk profile of long-term debt financing, attracting investors who are increasingly interested in sustainable investment opportunities. Moreover, as environmental regulations become more stringent, companies are incentivized to integrate green finance practices into their capital allocation decisions. This integration not only supports environmental sustainability but also enhances financial performance. By allocating capital towards environmentally friendly projects, companies can improve their financial efficiency and reduce the cost of capital, ultimately leading to a lower level of long-term debt financing.

Table 7. Results of further analysis.

As environmental regulations become more stringent, the expectation is that green finance would play a pivotal role in shaping corporate financing decisions, particularly in terms of debt financing. However, as evident from columns (3) and (4) of Table 7, the enforcement of environmental regulations does not significantly impact the role of green finance in reducing the level of short-term debt financing for corporate entities. This observation calls for a deeper understanding of the intricacies involved in the relationship between environmental regulations, green finance, and short-term debt financing. The rationale behind this finding lies in the distinct characteristics and determinants of short-term debt financing. Short-term debt is primarily utilized to finance day-to-day operational expenses and liquidity requirements, which are typically more responsive to market dynamics and macroeconomic factors. Green finance, on the other hand, is tailored towards longer-term sustainable investments, often with a focus on capital-intensive projects. This inherent mismatch in time horizons undermines the direct linkage between green finance and short-term debt financing. Moreover, the influence of environmental regulations on corporate financing decisions is complex and context-specific. While regulations may encourage firms to incorporate green practices, their translation into financing decisions is not automatic. Short-term debt decisions are influenced by a range of factors, including credit ratings, market sentiment, and access to capital. Environmental regulations, while relevant, often play a supporting role rather than being the sole determinant. Additionally, the heterogeneity of corporate responses to environmental regulations adds further complexity. Firms across different industries and with varying levels of environmental exposure may respond differently to green finance options. This heterogeneity can lead to variable impacts on short-term debt financing, often resulting in limited or no significant influence in certain cases. Finally, the limited availability and sophistication of green finance instruments also constrain their impact on short-term debt financing. Although the market for green finance is expanding, it remains fragmented and underdeveloped compared to traditional financing channels. This limits the extent to which green finance can influence short-term debt financing decisions.

In conclusion, our rigorous empirical analysis reveals a limited impact of green finance on short-term debt financing despite the enhancement of environmental regulations. This finding underscores the need for a nuanced understanding of the financing decisions of corporations, considering the multi-faceted nature of financial decision-making and the evolving regulatory landscape. Future research should delve deeper into the mechanisms that underlie the relationship between green finance and corporate financing decisions, accounting for various contextual factors and corporate-level heterogeneities.

Based on the results of the benchmark regression model, it is concluded that green finance effectively reduces the level of corporate debt financing. Subsequently, the robustness of these findings needs to be verified through various methods, including Propensity Score Matching (PSM), instrumental variable approach, Heckman two-stage selection model, controlling for the impact of industry policies, re-sampling test by adjusting the sample period, exclusion tests for municipalities directly under the central government, and variable substitution tests.

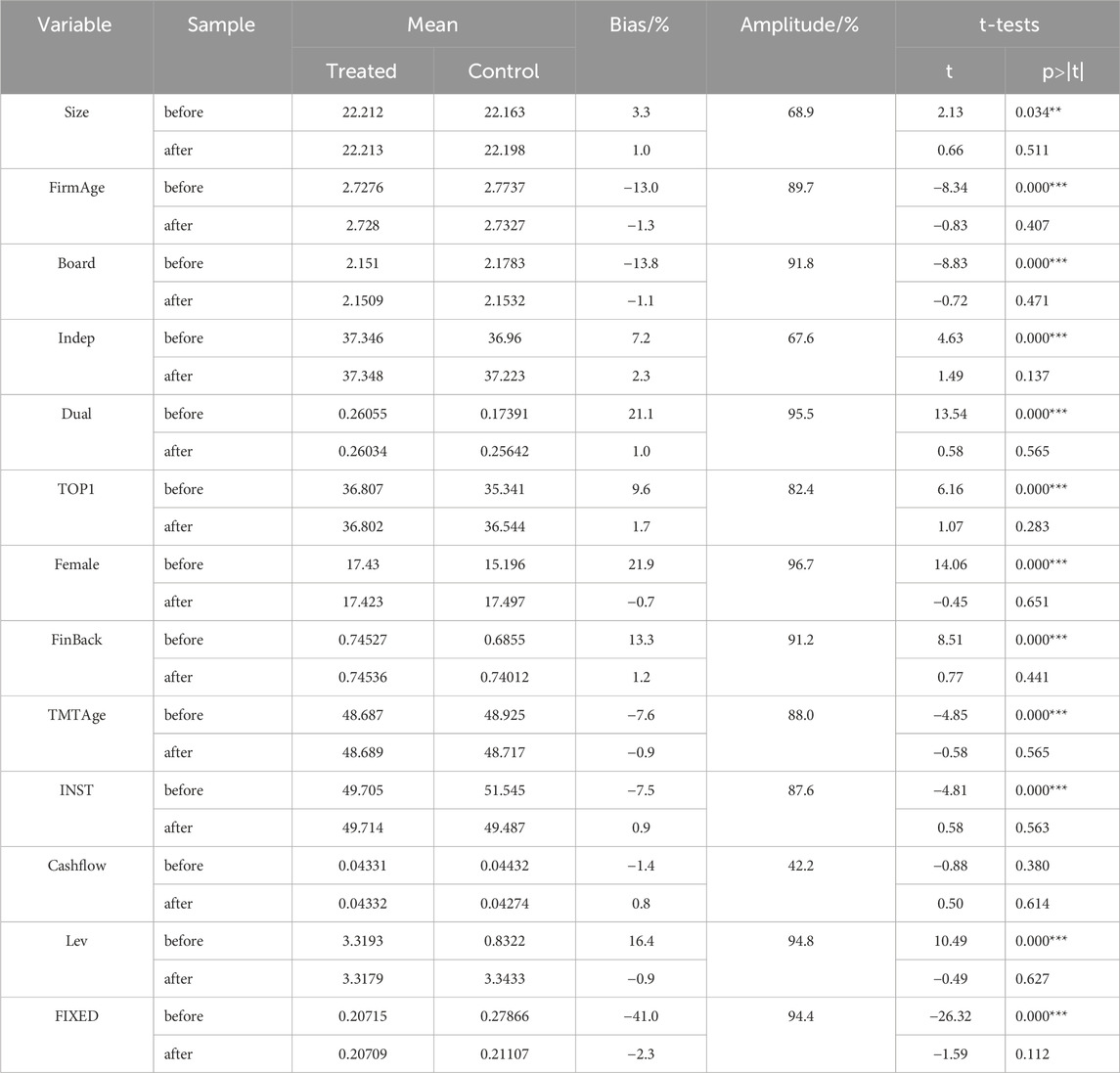

In this study, the Propensity Score Matching (PSM) methodology is employed to alleviate endogenous concerns resulting from sample selection bias and confounding offsets. Specifically, a dummy variable labeled “finance” is introduced as the grouping variable. When the green finance index exceeds its median value within its annual grouping, “finance” is assigned a value of 1; otherwise, it is assigned a value of 0. All control variables are selected as covariates, and the 1:1 nearest neighbor matching technique, as proposed by Abadie et al. (2004), is applied. The matching results are presented in Table 8. Before matching, the two sample groups exhibited significant differences across all indicators except for cash ratio. However, after matching, no significant differences were observed in any indicators between the two groups. These matching outcomes indicate an improvement in the similarity of sample characteristics, thereby mitigating the impact of selective bias on the sample.

Table 8. PSM matching results.

Using the matched samples, the PSM estimation results are presented in column (1) of Table 9. The regression outcomes align with the main regression findings, indicating a consistent and robust effect of green finance on reducing corporate debt financing levels. Specifically, the estimated coefficients are negative and statistically significant, further confirming the stability of the relationship between green finance and corporate debt financing.

Table 9. The regression results of robustness tests.

There may exist an endogenous relationship between green finance policies or practices and the level of corporate debt financing. Specifically, firms with lower debt financing levels may be more inclined to adopt green finance measures due to their financial constraints, while green finance policies might preferentially target those companies with inherently lower debt levels. In such a context, the direct utilization of green finance as an explanatory variable in empirical models may lead to estimation biases.

To address these endogeneity concerns, this study employs the lagged green finance level (i.e., green finance level from the previous period) as an instrumental variable. The regression results, presented in columns (2) and (3) of Table 9, reveal a positive correlation between the lagged green finance development level and the contemporaneous green finance development level. This positive association passes the significance test at the 1% level, indicating a strong statistical relationship. Moreover, after incorporating the instrumental variable into the regression analysis, the results suggest that green finance continues to exert a positive influence on reducing corporate debt levels. This finding further validates the robustness of the main regression results.

To mitigate the endogeneity issues arising from sample selection bias, we employ Heckman’s two-stage approach for re-examination. Drawing from existing research practices, we select the lagged green finance index as an instrumental variable. Furthermore, we construct the inverse Mills’ ratio (IMR) and incorporate it as a control variable in the previous regression model to mitigate the impact of sample selection bias.

The results presented in column (4) of Table 9 indicate that the inverse Mills’ ratio (IMR) is significant, and the regression outcomes remain largely consistent with our previous findings. This suggests the existence of sample selection bias, but it does not undermine the conclusions drawn in this study. By accounting for this bias, we ensure that our results are more robust and reliable.

Recognizing the potential influence of industry-specific macro policies on corporate green finance, this study introduces an interaction term between industry dummy variables and year dummy variables in the empirical model. Column (5) of Table 9 presents the results after controlling for the “industry × year” interaction, effectively adjusting for industry-specific policies. Despite these controls, the regression coefficients remain significantly negatively correlated at the 1% statistical level. This finding confirms that, even after accounting for industry policy factors, the development of green finance continues to lower corporate debt levels. This result aligns with our baseline regression analysis, providing further evidence of the robustness of our findings.

To ensure the robustness of our conclusions, we exclude observations from 2008 to 2015, given the potential impact of the financial crisis in 2008 and the stock market crisis in 2015 on capital markets. Regression results, presented in column (6) of Table 9, remain significantly negative and align with the baseline regression, indicating the stability and reliability of our findings. This exercise further confirms the robustness of our baseline regression results.

To ensure the accuracy of the empirical findings, this study opts to exclude the four direct-administered municipalities from further analysis. This exclusion is motivated by the unique characteristics of these municipalities, which possess a higher political status, smaller administrative areas, and diverse financing channels and methods. Additionally, their advanced application and widespread adoption of green finance, along with the flexibility of their financial policies, render them more prone to achieving reduced debt levels. Therefore, excluding these municipalities is deemed necessary. Upon re-estimating the regression model with the exclusion of the four direct-administered municipalities, the results, presented in column (7) of Table 9, indicate that the regression coefficient for green finance remains significant. This finding confirms the robustness of the regression analysis, suggesting that the observed association between green finance and debt levels is not solely driven by the exclusion of these municipalities. By accounting for potential outliers and biases introduced by the four direct-administered municipalities, this study ensures that the empirical findings are more reliable and generalize better to a broader context. The exclusion of these municipalities, therefore, serves as an important robustness check, strengthening the validity and credibility of the study’s conclusions.

To alleviate potential estimation biases arising from measurement errors, this study replaces the measurement methods for both explanatory and explained variables, drawing from existing research. Specifically, the explanatory variable is replaced with Green_two, which incorporates green funds and green equity into the original Green construction, thus broadening the scope of the green finance index. This measure is further standardized to ensure consistency. The regression results, presented in column (8) of Table 9, remain significantly negative, consistent with the baseline regression.

For the explained variable, this study adopts the method proposed by Blanchard (2019) to construct DDebt_two, which measures corporate debt levels using the ratio of interest-bearing debt to GDP. This approach provides a more comprehensive assessment of debt burden. The regression results, as shown in column (9) of Table 9, also remain significantly negative, aligning with the baseline findings.

Utilizing a comprehensive dataset of listed companies in China from 2008 to 2020, this study offers a nuanced understanding of the economic consequences of green finance, particularly its relationship with corporate debt financing levels. Our findings reveal that green finance effectively mitigates the debt financing burden of enterprises, a conclusion that remains robust across various robustness checks. This mitigation is achieved through two primary mechanisms: the alleviation of financing constraints and the enhancement of executive compensation.

Our analysis further highlights the heterogeneous impact of green finance. Notably, it has a significant influence on debt financing levels in state-owned enterprises, regions with lower levels of marketization, superior industrial structures, and lower carbon emissions. Additionally, we observe that the strengthening of external environmental regulations enhances the effectiveness of green finance in mitigating long-term debt financing levels, with no significant impact on short-term debt financing.

Based on these findings, we offer the following targeted policy recommendations: (1) Promoting Green Finance Initiatives: Governments and financial institutions should actively promote green finance practices to encourage enterprises to integrate environmental considerations into their financing decisions. This can be achieved through the development of green bond markets, green credit policies, and other incentive mechanisms. (2) Enhancing Policy Targeting: Policies should be targeted to specific groups that benefit most from green finance, such as state-owned enterprises, regions with lower marketization levels, and industries with superior environmental performance. This ensures that the limited resources are allocated efficiently to achieve maximum impact. (3) Strengthening External Environmental Regulations: Governments should strengthen environmental regulations to encourage enterprises to adopt greener production methods and reduce carbon emissions. This not only benefits the environment but also helps enterprises reduce debt financing costs through green finance mechanisms. (4) Improving Financing Constraints: Policies should aim to alleviate financing constraints faced by enterprises, especially those in the private sector and regions with lower marketization levels. This can be achieved by improving the efficiency of the financial system, enhancing transparency, and strengthening the role of financial intermediaries. (5) Incentivizing Executive Compensation Tied to Green Performance: Enterprises should consider tying executive compensation to green performance indicators, such as carbon emissions reduction and environmental compliance. This will incentivize executives to prioritize green finance practices and contribute to sustainable development. By implementing these targeted policies, governments and financial institutions can effectively promote green finance, reduce corporate debt financing levels, and foster sustainable economic growth.

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

QF: Conceptualization, Data curation, Formal Analysis, Funding acquisition, Investigation, Methodology, Project administration, Resources, Software, Supervision, Validation, Visualization, Writing–original draft, Writing–review and editing.

The author(s) declare that financial support was received for the research, authorship, and/or publication of this article. This research was funded by the Doctoral Scientific Research Project of the School of Accounting, Dongbei University of Finance and Economics, with grant number DUFEBY20240603, and the Graduate Research and Innovation Special Project of the Liaoning Provincial Department of Education.

The author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Abadie, A., Drukker, D., Herr, J. L., and Imbens, G. W. (2004). Implementing matching estimators for average treatment effects in Stata. stata J. 4, 290–311. doi:10.1177/1536867x0400400307

An, Q., Lin, C., Li, Q., and Zheng, L. (2023). Research on the impact of green finance development on energy intensity in China. Front. Earth Sci. 11, 1118939. doi:10.3389/feart.2023.1118939

Bai, X., Wang, K.-T., Tran, T. K., Sadiq, M., Trung, L. M., and Khudoykulov, K. (2022). Measuring China's green economic recovery and energy environment sustainability: econometric analysis of sustainable development goals. Econ. Analysis Policy 75, 768–779. doi:10.1016/j.eap.2022.07.005

Blanchard, O. (2019). Public debt and low interest rates. Am. Econ. Rev. 109, 1197–1229. doi:10.1257/aer.109.4.1197

Chen, H., Wu, H., Zhang, L., Tang, Y., and Lu, S. (2024). Does green financial policy promote the transformation of resource-exhausted cities? Evidence from the micro level. Resour. Policy 88, 104500. doi:10.1016/j.resourpol.2023.104500

Dong, C., Wu, H., Zhou, J., Lin, H., and Chang, L. (2023). Role of renewable energy investment and geopolitical risk in green finance development: empirical evidence from BRICS countries. Renew. Energy 207, 234–241. doi:10.1016/j.renene.2023.02.115

Du, K., Li, P., and Yan, Z. (2019). Do green technology innovations contribute to carbon dioxide emission reduction? Empirical evidence from patent data. Technol. Forecast. Soc. Change 146, 297–303. doi:10.1016/j.techfore.2019.06.010

Feng, Y., Gao, Y., Meng, X., Shi, J., Shi, K., Hu, S., et al. (2023). The impacts of casual environmental regulation on carbon intensity in China: dual mediating pathways of energy low-carbon reconstitution and industrial structure upgrading. Environ. Res. 238, 117289. doi:10.1016/j.envres.2023.117289

Feng, Y., Geng, Y., Liang, Z., Shen, Q., and Xia, X. (2021). Research on the impacts of heterogeneous environmental regulations on green productivity in China: the moderating roles of technical change and efficiency change. Int. J. Environ. Res. Public Health 18, 11449. doi:10.3390/ijerph182111449

Feng, Y., and Liang, Z. (2022). How does green credit policy affect total factor productivity of the manufacturing firms in China? The mediating role of debt financing and the moderating role of environmental regulation. Environ. Sci. Pollut. Res. 29, 31235–31251. doi:10.1007/s11356-021-17984-4

Feng, Y., Pan, Y., Sun, C., and Niu, J. (2024). Assessing the effect of green credit on risk-taking of commercial banks in China: further analysis on the two-way Granger causality. J. Clean. Prod. 437, 140698. doi:10.1016/j.jclepro.2024.140698

Gao, J., Wu, D., Xiao, Q., Randhawa, A., Liu, Q., and Zhang, T. (2023). Green finance, environmental pollution and high-quality economic development—a study based on China’s provincial panel data. Environ. Sci. Pollut. Res. 30, 31954–31976. doi:10.1007/s11356-022-24428-0

Guo, J., and Fang, Y. (2024). Green credit policy, credit discrimination and corporate debt financing. China Econ. Q. Int. 4, 42–54. doi:10.1016/j.ceqi.2024.03.004

Han, S., Zhang, Z., and Yang, S. (2022). Green finance and corporate green innovation: based on China's green finance Reform and innovation pilot policy. J. Environ. Public Health 2022, 1–12. doi:10.1155/2022/1833377

Hao, X., Wen, S., Xue, Y., Wu, H., and Hao, Y. (2023). How to improve environment, resources and economic efficiency in the digital era? Resour. Policy 80, 103198. doi:10.1016/j.resourpol.2022.103198

He, C., and Yan, G. (2020). Path selections for sustainable development of green finance in developed coastal areas of China. J. Coast. Res. 104, 77–81. doi:10.2112/jcr-si104-014.1

He, Y., and Liu, R. (2023). The impact of the level of green finance development on corporate debt financing capacity. Finance Res. Lett. 52, 103552. doi:10.1016/j.frl.2022.103552

Hu, J., Wu, Y., Irfan, M., and Hu, M. (2023). Has the ecological civilization pilot promoted the transformation of industrial structure in China? Ecolog. Indica. 155, 111053. doi:10.1016/j.ecolind.2023.111053

Lan, J., Wei, Y., Guo, J., Li, Q., and Liu, Z. (2023). The effect of green finance on industrial pollution emissions: evidence from China. Resour. Policy 80, 103156. doi:10.1016/j.resourpol.2022.103156

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., and Vishny, R. (2002). Investor protection and corporate valuation. J. finance 57, 1147–1170. doi:10.3386/w7403

Li, C., Chen, z., Wu, Y., Zuo, X., Jin, H., and Xu, Y. (2022). Impact of green finance on China’s high-quality economic development, environmental pollution, and energy consumption. Front.Environ. Sci. 10, 1032586. doi:10.3389/fenvs.2022.1032586

Li, C., Feng, X., Li, X., and Zhou, Y. (2023a). Effect of green credit policy on energy firms’ growth: evidence from China. Econ. research-Ekonomska istraživanja 36. doi:10.1080/1331677x.2023.2177701

Li, X., Wang, Z., Yu, Y., and Chen, Y. (2023b). Does green finance promote the social responsibility fulfilment of highly polluting enterprises? Empirical evidence from China. Econ. research-Ekonomska istraživanja 36. doi:10.1080/1331677x.2022.2153719

Li, Z., Kuo, T.-H., Wei, S.-Y., and Luu The, V. (2022). Role of green finance, volatility and risk in promoting the investments in Renewable Energy Resources in the post-covid-19. Resour. Policy 76, 102563. doi:10.1016/j.resourpol.2022.102563

Liang, Z., and Yang, X. (2024). The impact of green finance on the peer effect of corporate ESG information disclosure. Finance Res. Lett. 62, 105080. doi:10.1016/j.frl.2024.105080

Lin, C., Ma, Y., Malatesta, P., and Xuan, Y. (2011). Ownership structure and the cost of corporate borrowing Jour. finan. Econo. 100 (1), 1–23. doi:10.1016/j.jfineco.2010.10.012

Lin, C., Zhang, X., Gao, Z., and Sun, Y. (2023). The development of green finance and the rising status of China's manufacturing value chain. Sustainability 15. doi:10.3390/su15086395

Ling, X., Wang, L., Pan, Y., and Feng, Y. (2023). The impact of financial literacy on household health investment: empirical evidence from China. Int. J. Environ. Res. Public Health 20, 2229. doi:10.3390/ijerph20032229

Liu, J., Shi, W., Zeng, C., and Zhang, G. (2023). Does public firms’ mandatory Ifrs reporting crowd out private firms’ capital investment?. J. Account. Res. 61 (4), 1263–1312. doi:10.1111/1475-679x.12494

Liu, W., and Zhu, P. (2024). The impact of green finance on the intensity and efficiency of carbon emissions: the moderating effect of the digital economy. Front. Environ. Sci. 12. doi:10.3389/fenvs.2024.1362932

Lv, C., Bian, B., Lee, C.-C., and He, Z. (2021). Regional gap and the trend of green finance development in China. Energy Econ. 102, 105476. doi:10.1016/j.eneco.2021.105476

López Iturriaga, F. J. (2005). Debt ownership structure and legal system: an international analysis Appli. Economic. 37 (3), 355–365. doi:10.1080/0003684042000295269

Ma, H., Miao, X., Wang, Z., and Wang, X. (2023). How does green finance affect the sustainable development of the regional economy? Evidence from China. Sustainability 15, 3776. doi:10.3390/su15043776

Meng, Y., and Yin, C. (2019). Trust and the cost of debt financing. J. Int. Financial Mark. Institutions Money 59, 58–73. doi:10.1016/j.intfin.2018.11.009

Muganyi, T., Yan, L., and Sun, H. P. (2021). Green finance, fintech and environmental protection: Evidence from China Environ. Sci. Ecotech. 7, 100107. doi:10.1016/j.ese.2021.100107

Qian, J., and Strahan, P. E. (2007). How laws and institutions shape financial contracts: The case of bank loans The Jour. Fin.62 (6), 2803–2834. doi:10.1111/j.1540-6261.2007.01293.x