Yu Chen

Yu Chen Yuantao Xie

Yuantao Xie

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 15 July 2024

Sec. Environmental Economics and Management

Volume 12 - 2024 | https://doi.org/10.3389/fenvs.2024.1363199

This paper begins by establishing a three-party game model involving three key players: the insurer, the firm, and the government. This model is used to analyze the utility of each party in various scenarios, one of which encourages green innovation within the firm. According to this model, when the insurer rejects insurance coverage and the government maintains a neutral stance on environmental liability insurance, the firm may opt to engage in green innovation. Green innovation fundamentally serves as a mechanism to mitigate environmental pollution risks stemming from the firm’s operational processes. In cases where the insurer declines underwriting, it becomes rational for the firm to enhance its risk management through green innovation, which can be viewed as a mitigating factor in the context of environmental liability insurance. To comprehensively examine the overall impact of environmental liability insurance on the green innovation endeavors of firms, we use a mediation effect model utilizing firm-level data from heavily polluting industries. This paper delves into the intricate relationship between environmental liability insurance and the capacity of heavily polluting firms to engage in green innovation, along with the mediating influence of financing constraints between these two factors. The findings of this analysis suggest that the acquisition of environmental liability insurance enhances the green innovation capabilities of firms operating in heavily polluting industries by alleviating financing constraints, serving as a mediating factor in this regard.

Environmental pollution liability insurance is a type of insurance that covers the risk of sudden environmental pollution accidents, which will induce serious damage and require a huge amount of compensation. The insurance product plays an important role in reducing the impact of environmental pollution on firms and the external environment. Green innovation refers to measures aimed at managing and controlling environmental pollution risks in advance. Purchasing environmental pollution liability insurance is a behavior with positive externality considering the nature of environmental liability insurance, which means that firms that conduct this activity have a strong awareness of environmental protection, imposing a positive effect on green innovation development. On the other hand, the ex-post moral hazard brought by environmental liability insurance may make firms care less about green innovation, which is a negative effect. In order to study the impact of environmental liability insurance on green innovation, this paper first conducts a three-party game model of environmental liability insurance with the government firm and insurer as players to analyze various behaviors and results and makes an intermediary effect analysis through firm-level data, which explores the impact of environmental liability insurance on green innovation. This study sheds light on the effects of environmental liability insurance on firm green innovation using game theory and mediation effect models, which not only show the negative effect but also the positive effect, contributing to the literature. The remainder of this study is organized as follows: Section 2 provides the relevant literature about the environmental liability insurance system, willingness to purchase insurance, and green innovation. Section 3 refers to the third-party game theory model. Section 4 represents empirical results. Finally, Section 5 gives the conclusion.

In the field of the environmental liability insurance system, Cheng Yu (2017) put forward policy suggestions to promote the clarification of legal liability rules for environmental pollution damage and the stabilization of judicial judgment rules and suggest that insurers introduce new insurance measures to improve insurers’ underwriting capabilities, which can control the adverse impact to insurers of progressive pollution risks. Yu et al. (2017) summed up the elements of domestic and foreign environmental liability insurance systems including underwriting objects, coverage, premium rate, and claim amount, contributing suggestions about the establishment of a sub-regional, sub-industry, sub-type insurance rate system, and a national environmental liability insurance database to improve China’s environmental liability insurance system based on the status quo of environmental damage assessment technology. Gu Xiangyi and Chen Shiyi (2020) suggested improving legislation to promote the development of the evaluation mechanism and compulsory system for environmental liability insurance in industries featured by a substantial risk. Zhang Ruigang and Li Xuezhen (2021) put forward feasible suggestions for strengthening the construction of the legal system and technical support system and promoting policy publicity by extracting the commonalities of the development of the environmental liability insurance system and considering differences in various regions of China. Among research on the environmental liability insurance system, literature that emphasizes the role of the government mainly includes the following: Tian Hui (2014) discussed the status quo and future development of China’s green insurance, which mainly refers to environmental liability insurance, and put a great emphasis on the government’s important role in environmental liability insurance development. Wang Xiangnan (2014) analyzed some characteristics of environmental liability insurance in the United States and suggested that China should improve relevant laws and regulations, strengthen the product design of environmental liability insurance, use a relatively long claim period, and establish the environmental relief fund and other risk diversification mechanisms. Wang Haiping and Li Xiurong (2022) proposed that the government should grasp the key points of its own responsibilities under the premise of conducting the market survey and further clarifying the nature of the environmental liability insurance system to improve it.

As for literature about purchasing environmental liability insurance, Wang Kang and Sun Jian (2016) established a binary logistic model based on the firm-level data of Hebei Province in China to study the willingness to buy environmental liability insurance, which was found to be significantly influenced by scale, income status and pollution degree of firms, reputation of insurers, propaganda of the country, and coverage on environmental liability insurance, among which coverage contributes most. Li Minxin and Wang Jianghan (2021) found that purchasing environmental liability insurance significantly improved the quality of firms’ environmental information disclosure.

Considering literature about the impact on green innovation, Reinhilde Veugelers (2012) concluded that the firm-level evidence presented in contribution to the motives of private sector firms for introducing clean innovations from the latest Flemish CIS eco-innovation survey confirms that firms are responsive to eco-policy demand interventions. Chan et al. (2017) put forward that green insurance cannot improve innovation and expect profits from firms but reduces the risk using the game theory model. Qi et al. (2018) used the triple difference method based on the green patent data of listed companies in China’s Shanghai and Shenzhen stock markets from 1990 to 2010 to study the inducing effect of environmental rights’ trading market policies on firms’ green innovation by comparing the proportion of green patent applications before and after the implementation of the pilot policy of emission trading, between pilot and non-pilot areas, and among polluting and clean industries. Hu Jun and Mu Yanru (2022) found that environmental liability insurance can help firms carry out environmental governance and green innovation and guide the high-quality development of the real economy, based on their analysis of China’s heavily polluting firms.

Considering the literature about reinsurance, a single pollution liability risk may be insured by several large international reinsurance companies, with no one company taking any more of the risk than is economically manageable through reinsurance (Robert L. Brown, 1991). Alberto Monti (2002) focused on the role of insurance and reinsurance companies in the management of environmental risks.

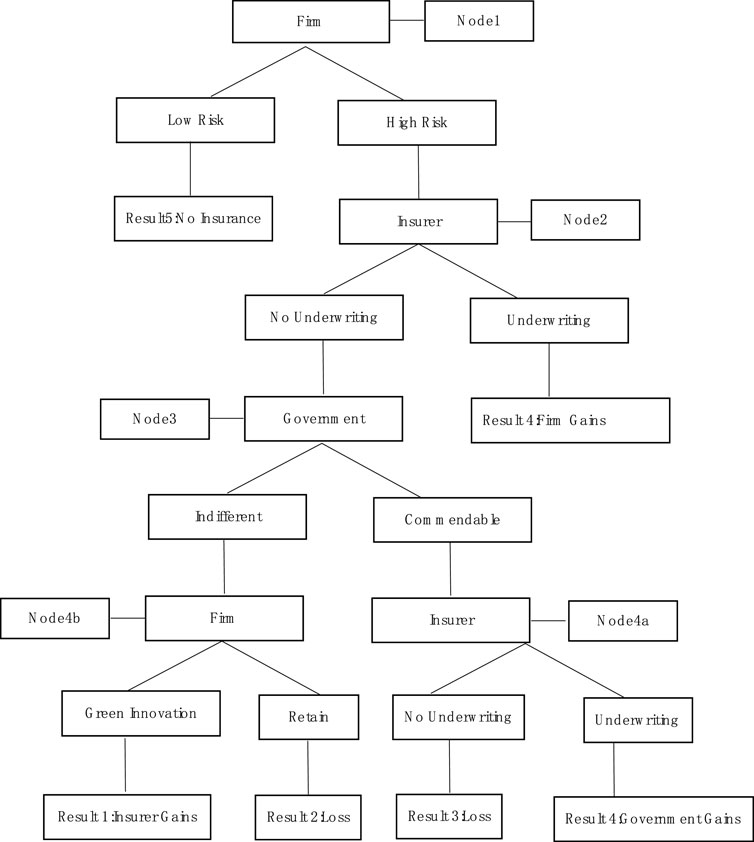

Suppose there are two types of firms: G, which means that the firm supports environmental protection, and N, which means that the firm has an indifferent attitude about it. At the same time, there are also two types of governments: G, which means that the government supports environmental protection, and N, which means that the government has an indifferent attitude about it too. Insurers are classified into two types: H type, which denotes high identification ability about risk, and L type, which denotes low identification ability about risk, according to their ability to identify firm risks. Figure 1 is the process of the game model.

Figure 1. Process of the game model.

At node 1, the probabilities of the firm with high environmental pollution risks, which is supportive or indifferent about environmental protection, are

The firm at node 4 b, which supports environmental protection, tends to achieve result 2 by treating the sudden environmental pollution risk of their own firm as a high risk and choosing the strategy of a high environmental pollution risk processing manner. The indifferent firm tends to arrive at result 1 and then ultimately chooses low environmental pollution risk strategies, which involve carrying out green innovation activities. If the firm, which is supportive or indifferent about environmental protection, obtains the utility of result 2 in order of

The insurer with a high identification ability of risk will choose result 3 at node 4a; the insurer with a low identification ability of risk is more inclined to choose result 4. If the utility of the insurers with two different identification capabilities of risk in result 3 is denoted as

When the government adopts a commendable attitude about environmental liability insurance, the insurer with a high identification ability of risk would take a no-underwriting strategy, and the insurer with a low identification ability of risk would underwrite, reaching results 3 and 4. If the government is different about insurance, the utility of the government can be expressed by

According to the formula above, when the government supports environmental protection, the commendable method is an optimal strategy, namely,

The government supports environmental protection, and it will take the following approaches: if

When the insurer is at node 2, it needs to decide whether to underwrite or not. In the first situation where the insurer adopts the underwriting strategy, the game result will be result 5; when it adopts the opposite strategy, any of the results from result 1 to result 4 may be reached. For insurers, the optimal result is result 1, which means that the firm tends to conduct green innovation activities. Results 4 and 5 are the worst results for the insurer, and its choice is determined by the level of its risk identification ability.

The utilities are, respectively,

If the insurer with a high identification ability of risk does not adopt the underwriting strategy, even with a commendable attitude toward insurance from the government, it will still keep the decision, which means that result 3 is reached, making this strategy better than the underwriting manner, namely, result 5. However, if the government chooses to take a neutral approach and not promote environmental liability insurance, results 1 and 2 are both better than result 5 for it. Therefore, if the insurer has a high identification ability of risk, it will take the non-insurance strategy at node 2, which means that

The insurer with a low identification ability of risk will underwrite or not. If the non-insurance method is adopted, when the government chooses a commendable attitude toward insurance, result 5 with underwriting is better than result 4, which means that the insurer should take the underwriting strategy at this time.

When the government chooses to be different, the result will be determined by the type of firm. Generally speaking, if the firm supports environmental protection, it will adopt the method of retaining risk and result 2 is reached; the firm tends to undertake green innovation to reduce risk exposure and reaches result 1. If there is no difference between two ways of non-coverage and coverage, then we have

If the insurer has a low identification ability of risk, the following two requirements not to underwrite for the insurer at node 2 are as follows: the government supports environmental protection and is indifferent in insurance, which means that

At node 1, when the firm adopts a processing manner with high environmental pollution risk, it will produce one of the results from result 1 to result 5; when the firm adopts a way with low environmental pollution risk, it will not purchase insurance as result 6. Results 4 and 5 are the best results; 6 is worse result; and 1 to 3 are the worst results. The firm will choose results according to its type.

If the firm supports environmental protection and there is no difference between the two strategies, then we have

Here,

If the insurer has a low identification ability of risk, it will underwrite or not. If

If

At node 1, if there is no difference between manners of high environmental pollution risk and low environmental pollution risk for the indifferent firm, then we have

Here,

If the insurer has the ability to identify high risks from the firm, it will not underwrite. If

If the insurer has a low identification ability of risk, it will underwrite or not. If

According to the relevant regulations of the “Environmental information disclosure guidance for listed companies” issued by the Ministry of Ecology and Environment of China, firms in heavy polluting industries mainly include thermal power generation, steel, cement, metallurgy, chemical industry, and petrochemical, which totals 16 types. These industries are the key customers of insurers selling environmental pollution liability insurance products and the main research object of this paper, and they are required by the environmental protection department to regularly disclose pollutant emissions and other environmental protection information. In accordance with the regulations on the classification of heavy polluting firms in the “Guidelines for the industry classification of listed companies” of the China Securities Regulatory Commission and the principle of consistency in sample selection, the petrochemical steel industry, cement metallurgy industry, thermal power generation industry, brewing and paper printing industry, mining industry, textile industry, building material industry, tanning industry, food and beverage industry, plastic industry, water, electricity, gas, and biopharmaceutical industry are the heavy polluting industries that are studied in this paper. At the same time, according to the lists of environmental liability insurance issued by the Ministry of Ecology and Environment in 2014 and 2015, there are a total of 2,985 firms. On the basis of removing sample anomalies, a total of 2,556 sample observations were screened out. The data above are all obtained from the CNRDS database. The data were winsorized at the 1% and 99% levels to exclude the influence of outliers.

The dependent variable of this paper is the firm green innovation, whose notation is ino. The measurement standard is the sum of the number of green invention patent applications and the number of green utility model patent applications.

Table 1 provides a summary of the variables used in this paper. Considering the existing research and achievements, the control variables in this paper are variables except the financing constraint (FC) and dependent variable. Among them, firm green innovation is the dependent variable, environmental liability insurance is the core explanatory variable, and financing constraints are the mediating variable of this paper.

Table 1. Variable definition.

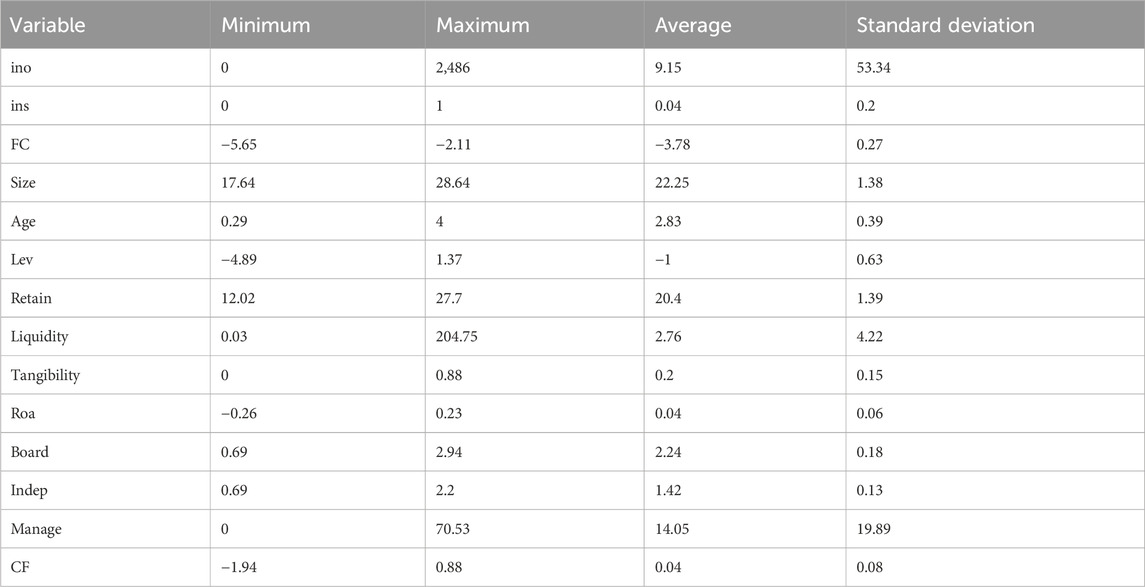

Table 2 lists the descriptive statistics for variables in the full sample. The average value of green innovation is 9.15, and the difference between the maximum and minimum values is large, indicating that there is a large difference in the level of green innovation among firms. The average value of environmental liability insurance is 0.04, which means that only 4% of firms are insured and shows that the situation of firms investing in environmental liability insurance is not optimistic.

Table 2. Descriptive statistics of the whole sample.

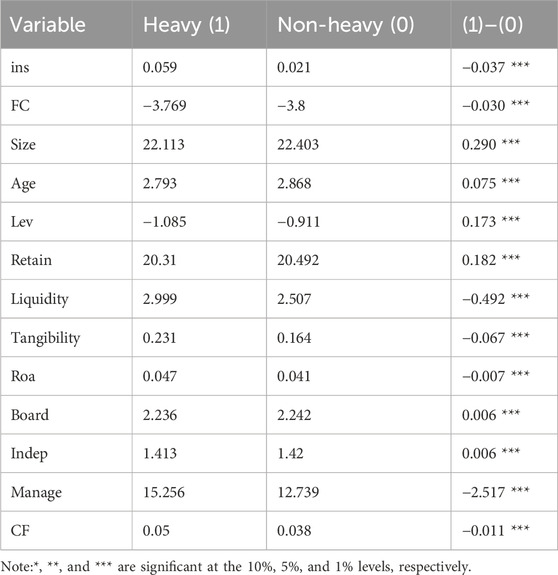

The sample comprises firm-level data selected from firms in heavy polluting industries because firms in non-heavy polluting industries have low demand for environmental liability insurance. Table 3 provides the test result of the mean difference of variables between the firms in the heavy polluting industries and non-heavy polluting industries. It shows that the average value of insurance coverage of firms in heavy polluting industries is 0.059, which is higher than the 0.021 of firms in non-heavy polluting industries at a significant level of 1%, indicating that firms in heavily polluting industries are significantly more insured than those in non-heavy polluting industries.

Table 3. Difference between mean test results.

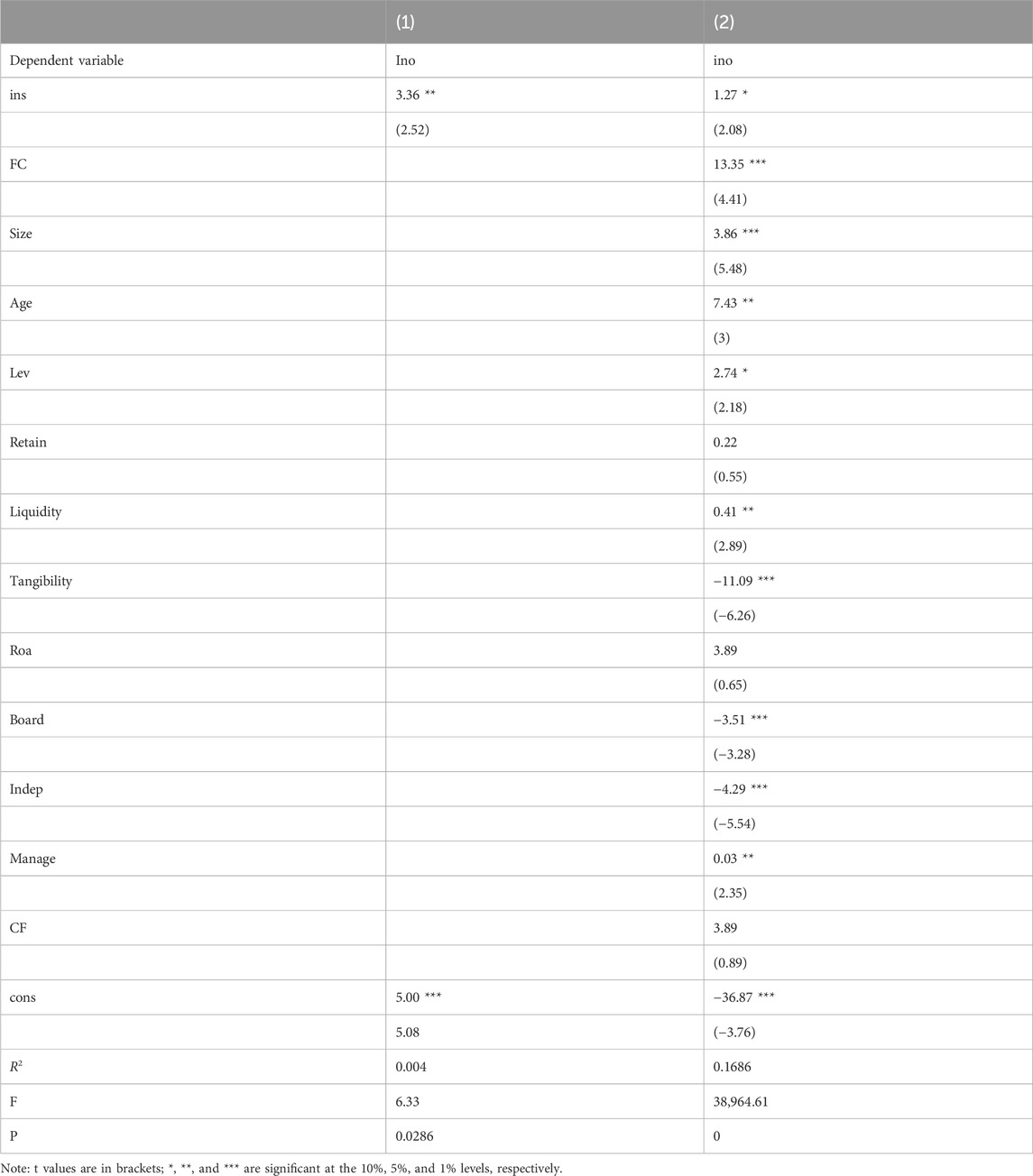

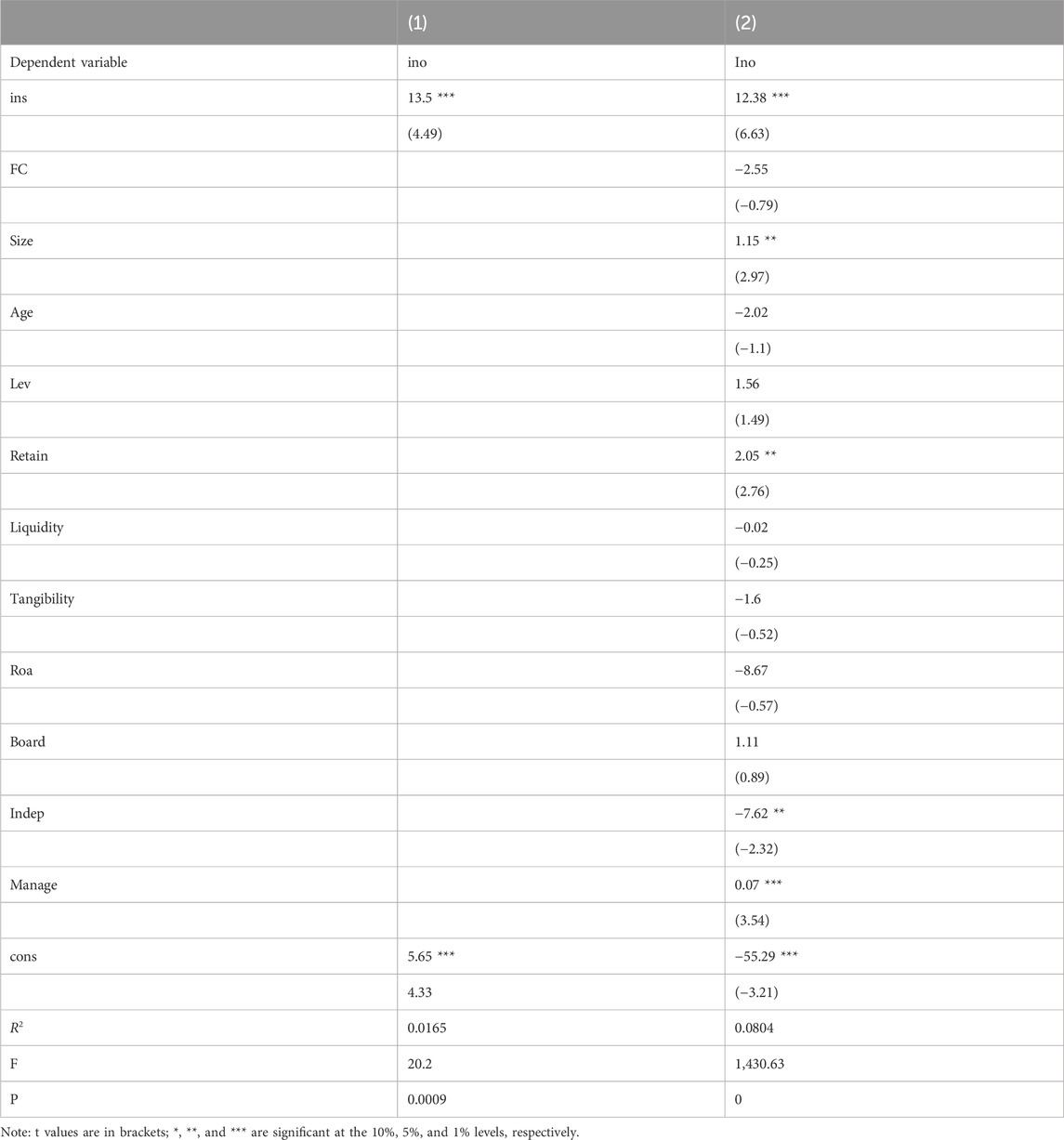

Table 4 shows the regression results of environmental liability insurance and firm green innovation. Column (1) reports the regression results of the impact of environmental liability insurance on corporate green innovation, and column (2) adds multiple control variables. The results show that the coefficients of columns (1) and (3) ins are 3.26 and 1.27, respectively. The coefficient of column (1) is significantly positive at the 5 % level, and the coefficient of column (3) is significantly positive at the 10% level, with a value of 1. It can be seen that environmental liability insurance is conducive to enhancing the green innovation capability of firms. Taking out environmental liability insurance can be regarded as a manifestation of environmental awareness, which can motivate firms to improve their green innovation capabilities. In terms of control variables, the larger the size of firms, the higher the level of green innovation, in that large firms have financial advantages, intellectual property protection capabilities, and innovation failure risk tolerance. Profitability is positively related to firm green innovation because the stronger the firm’s profitability, the more cash flow it can provide for green innovation activities, thereby promoting firm green innovation.

Table 4. Basic regression results.

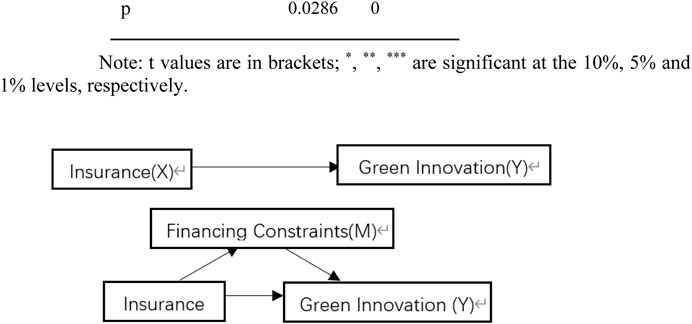

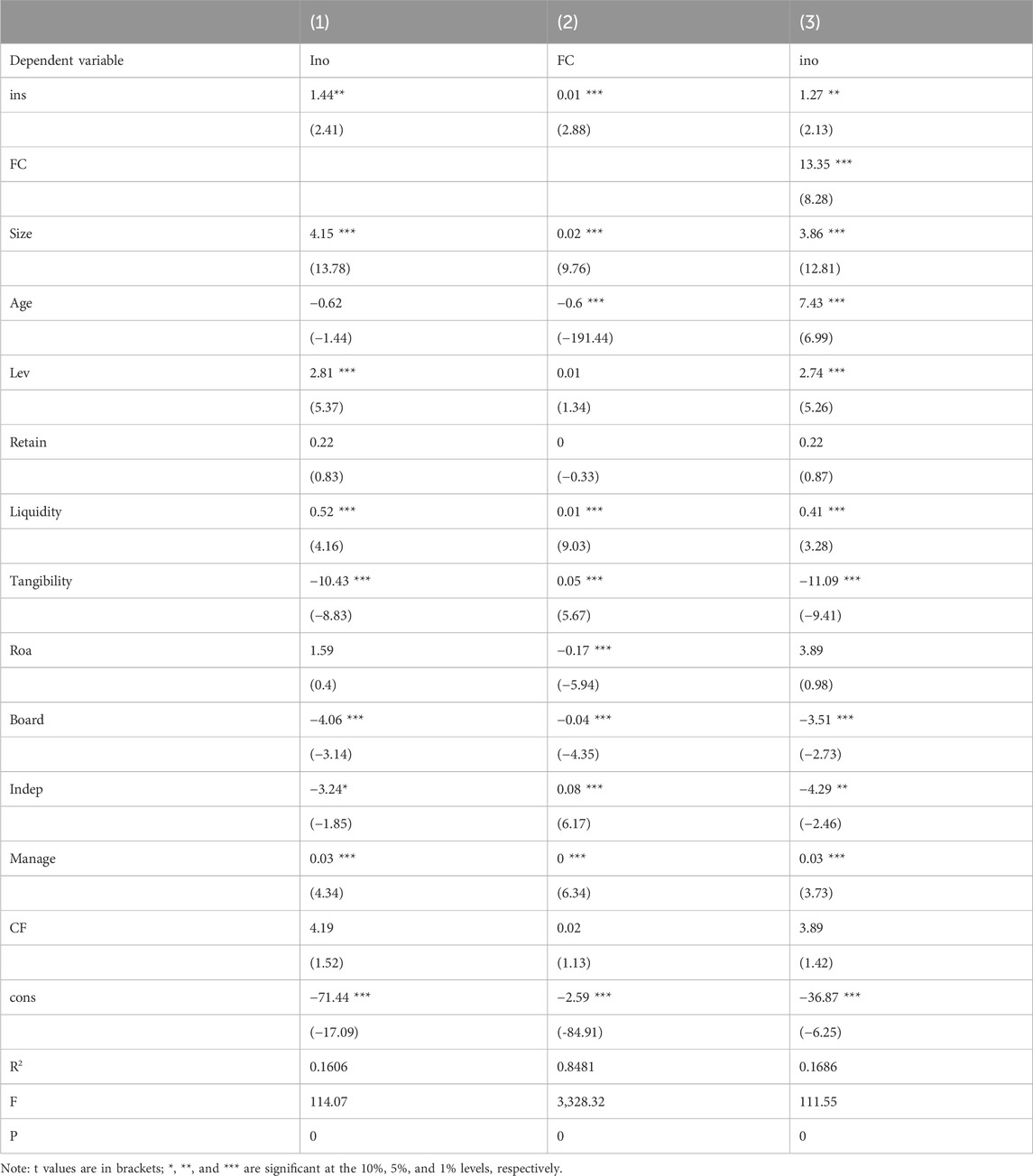

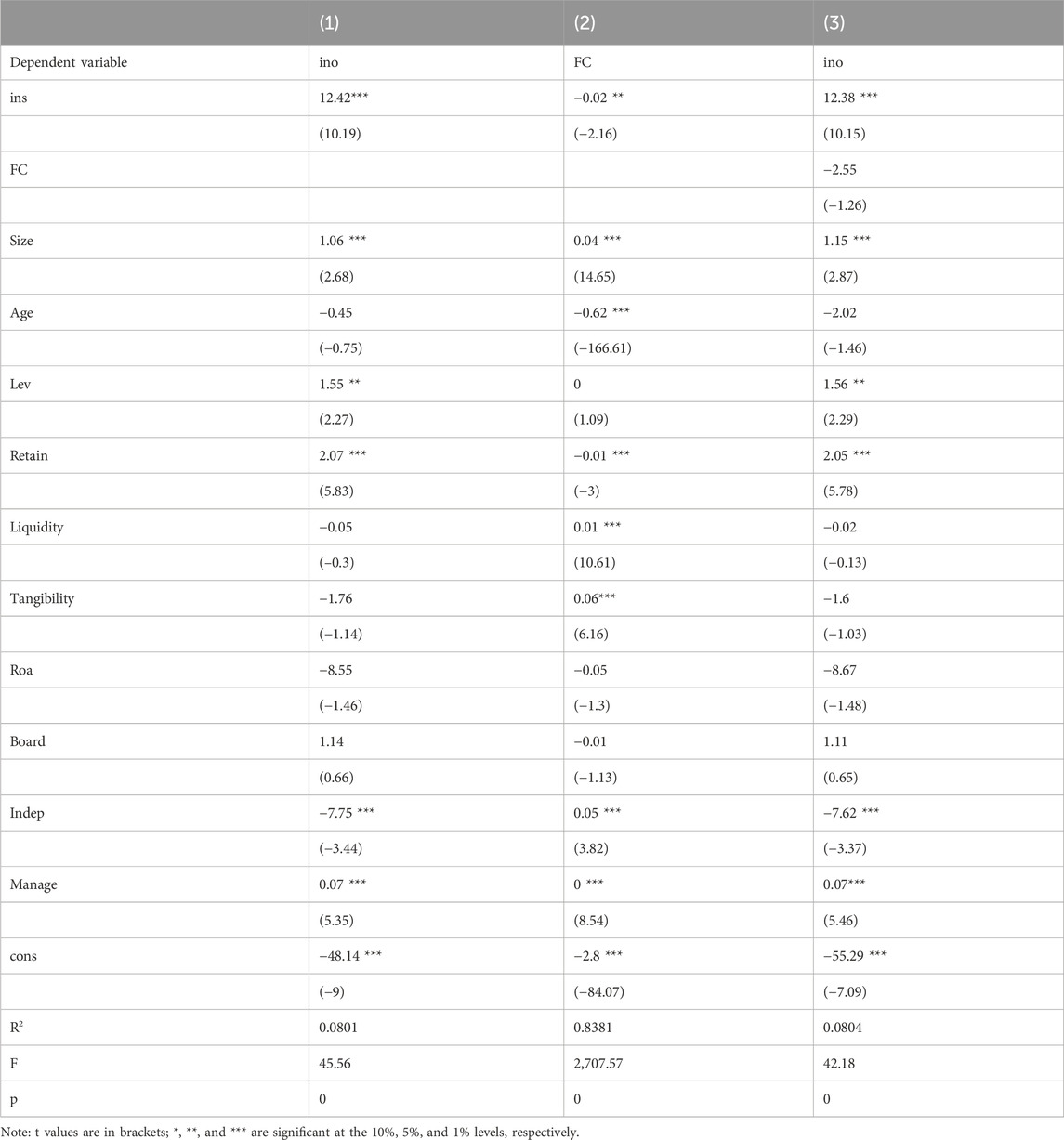

Table 5 shows the results of the mediation effect test. Column (1) is the regression result of purchasing environmental liability insurance on the green innovation of firms. The coefficient of ins is significantly positive at the level of 5%, indicating that purchasing environmental liability insurance promotes the improvement of the level of firm green innovation. Column (2) is the regression result of purchasing environmental liability insurance based on financing constraints. The coefficient of ins is significantly positive, indicating that the investment in environmental liability insurance has eased the financing constraints of firms. Column (3) is the impact of adding environmental liability insurance and financing constraints on the regression of firm green innovation; the coefficients of ins and FC are both significantly positive, indicating that reducing financing constraints is an important path for environmental liability insurance to improve the level of green innovation in firms. To sum up, it can be seen that firms’ purchasing environmental liability insurance can reduce the risk of firm operation, play a role in alleviating the financing constraints of firms, ensure the development of green innovation activities, and then improve the level of green innovation of firms. Figure 2 is the mediating effect model. Table A1 is basic results of non-heavy polluting industries. Table A2 is results of the mediation effect of non-heavy polluting industries.

Figure 2. Mediating effect model.

Table 5. Regression results of the mediation effect.

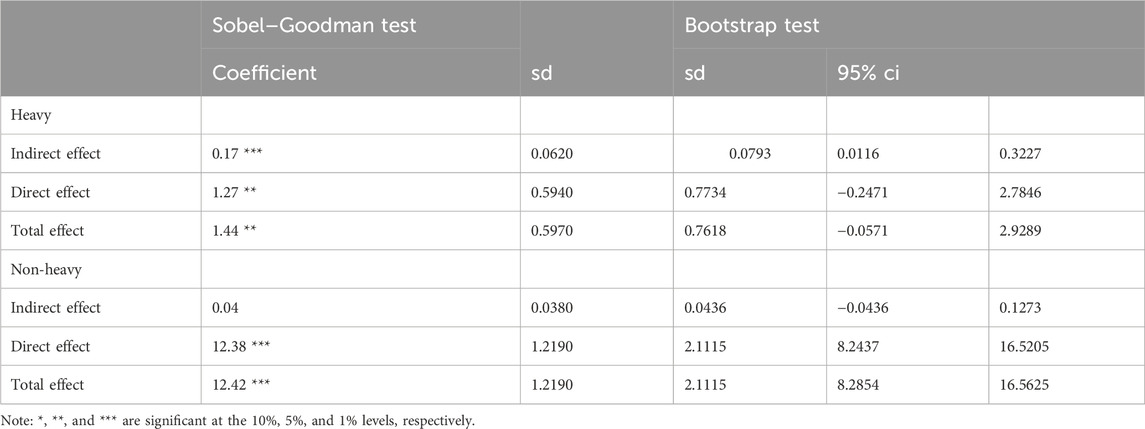

The results in Table 6 show that in the Sobel–Goodman mediation tests, the p-value of the indirect effect of non-heavy polluting firms is not so small and not significant. The Sobel test p-value of the mediating effect is also not so small, indicating that no mediating effect is established. However, the p-values of the indirect and direct effects of heavy polluting firms are very small and the Sobel test p-value of the mediating effect is less than 1%, indicating that the mediating effect is established. This supports financing constraints as an intermediary variable for the impact of environmental liability insurance on firm green innovation. In addition, after taking into account the effect of financing constraints, the proportion of the mediation effect in the total effect is 13.2%. The results in the table above show that the 95% confidence interval of the indirect effect of heavy polluting industries is [0.01, 0.32], which excludes 0 and establishes the mediating effect. The 95% confidence interval of the indirect effect of non-heavy polluting industries is [-0.04, 0.13], which includes 0 and no mediating effect is established.

Table 6. Results of the mediation effect test.

This paper first constructs a three-party game model of three players: the insurer, firm, and government, which analyzes the utility of all parties under various results, one of which promotes green innovation in the firm. According to the model, under the circumstance that insurance rejection by the insurer happens and the government is indifferent to environmental liability insurance, the firm may undertake green innovation. The behavior of purchasing environmental liability insurance can be considered to indicate that the firm has a strong awareness of environmental protection, imposing a positive effect on green innovation; however, on the other hand, the ex-post moral hazard brought by environmental liability insurance may make firms care less about green innovation, which is a negative effect. The paper tackles a relevant and understudied topic—the potential role of environmental liability insurance in driving green innovation within polluting firms. Green innovation is essentially a means of controlling environmental pollution risks from firm activities. In the case that the insurer rejects to underwrite, it is reasonable for the firm to improve risk management through green innovation, which can be considered a negative effect of environmental liability insurance. In order to explore the total effects of environmental liability insurance on the green innovation of firms, the mediation effect model is applied with firm-level data in heavily polluting industries. This paper analyzes the relationship between environmental liability insurance and the green innovation ability of heavily polluting firms and the mediating effect of financing constraints between the two, concluding that purchasing environmental liability insurance improves the green innovation ability of firms from heavily polluting industries by easing financing constraints as a mediating effect. The potential policy implications of the findings, such as designing environmental liability insurance schemes that incentivize green innovation while considering financing limitations, can be discussed later, which would strengthen the paper’s practical relevance.

The original contributions presented in the study are included in the article/Supplementary Material; further inquiries can be directed to the corresponding author.

YC: Writing–original draft. YX: Writing–review and editing.

The author(s) declare that financial support was received for the research, authorship, and/or publication of this article. This paper is funded by the “Beijing Publicity and Culture High-level Talent Training Funding Project.”

The authors thank teachers from the University of International Business and Economics for insightful comments.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors, and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Brown, R. L. (1991). Environmental liability insurance: an economic incentive for responsible corporate action. Alternatives, 18–25.

Cheng, Yu. (2017). Reflections on the coverage of environmental liability insurance in China: also on the insurability of progressive pollution. Insur. Res. (04), 102–117. doi:10.13497/j.cnki.is.2017.04.008

Fang, Yu, Niu, K., and Jia, Q. (2017). On environmental risk and environmental damage assessment in environmental liability insurance. Environ. Prot. 45 (14), 51–55. doi:10.14026/j.cnki.0253-9705.2017.14.024

Gu, X., and Chen, S. (2020). Evolution and path selection of environmental pollution liability insurance system. Fudan J. Soc. Sci. Ed. 62 (03), 151–159.

Hu, J., and Mu, Y. (2022). Environmental pollution liability insurance and corporate financialization: an analysis based on China's heavy polluting enterprises. Insur. Res. (02), 48–63. doi:10.13497/j.cnki.is.2022.02.004

Lam, H. L., Varbanov, P. S., Klemeš, J. J., and Yan, J. (2016). Green applied energy for sustainable development. Appl. Energy 161, 601–604. doi:10.1016/j.apenergy.2015.10.084

Li, M., and Wang, J. (2021). Environmental pollution liability insurance and corporate environmental information disclosure. Insur. Res. (12), 55–73. doi:10.13497/j.cnki.is.2021.12.004

Liu, Y., Zuo, J., Pan, M., Ge, Q., Chang, R., Feng, X., et al. (2022). The incentive mechanism and decision-making behavior in the green building supply market: a tripartite evolutionary game analysis. Build. Environ. 214, 108903. doi:10.1016/j.buildenv.2022.108903

Monti, A. (2002). Environmental risks and insurance. A comparative analysis of the role of insurance in the management of environment-related risks, Available at: https://www.oecd.org/finance/financial-markets/1939368.pdf.

Qi, S., Qi, L., and Cui, J. (2018). Can the environmental rights trading market induce green innovation?-evidence based on the green patent data of listed companies in China. Econ. Res. 53 (12), 129–143.

Sayadian, S., and Honarvar, M. (2021). A Stackelberg game model for insurance contracts in green supply chains with government intervention involved. Environ. Dev. Sustain. 24 (6), 7665–7697. doi:10.1007/s10668-021-01752-y

Tian, H. (2014). Current situation problems and future development of China's green insurance. Dev. Res. (05), 4–7.

Veugelers, R. (2012). Which policy instruments to induce clean innovating? Res. Policy 41 (10), 1770–1778. doi:10.1016/j.respol.2012.06.012

Wang, C., Nie, P.-y., Peng, D.-h., and Li, Z.-h. (2017). Green insurance subsidy for promoting clean production innovation. J. Clean. Prod. 148, 111–117. doi:10.1016/j.jclepro.2017.01.145

Wang, H., and Li, X. (2022). Investigation on the market environment of environmental pollution liability insurance in China: model construction and research analysis. Financial Theory Pract. (03), 97–106.

Wang, K., and Sun, J. (2016). An empirical study on the willingness to purchase environmental liability insurance. Insur. Res. (05), 71–81. doi:10.13497/j.cnki.is.2016.05.007

Wang, X. (2015). Characteristics and reference significance of environmental pollution liability insurance in the United States. Finance Econ. (09), 55–57. doi:10.19622/j.cnki.cn36-1005/f.2015.09.013

Zhang, R., and Li, X. (2021). A regional comparative study on the implementation of China's environmental liability insurance system. Financial Theory Pract. (09), 98–107.

TABLE A1. Basic results of non-heavy polluting industries.

TABLE A2. Results of the mediation effect of non-heavy polluting industries.

Keywords: game model, mediating effect model, environmental liability insurance, green innovation, pollution risk

Citation: Chen Y and Xie Y (2024) Environmental liability insurance, green innovation, and mediation effect study. Front. Environ. Sci. 12:1363199. doi: 10.3389/fenvs.2024.1363199

Received: 30 December 2023; Accepted: 07 March 2024;

Published: 15 July 2024.

Edited by:

Hanxi Wang, Harbin Normal University, ChinaReviewed by:

Ismail Suardi Wekke, Institut Agama Islam Negeri Sorong, IndonesiaCopyright © 2024 Chen and Xie. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Yuantao Xie, eGlleXVhbnRhb0B1aWJlLmVkdS5jbg==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.