95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 15 March 2024

Sec. Environmental Economics and Management

Volume 12 - 2024 | https://doi.org/10.3389/fenvs.2024.1362932

This article is part of the Research Topic Green Finance & Carbon Neutrality: Strategies and Policies for a Sustainable Future View all 36 articles

Wenjie Liu1

Wenjie Liu1 Peng Zhu2*

Peng Zhu2*Carbon emissions have become a global challenge that threatens human development. Governments have taken various measures to reduce carbon emissions, and green finance is an important and innovative way to realize carbon emission reductions. This paper uses data on a prefecture-level city in China to explore the impact of green finance on carbon emission intensity from both theoretical and empirical perspectives, and analyzes the mechanisms by which green finance affects carbon emission intensity. On this basis, this paper further analyzes the impact of green finance on carbon emission efficiency. In addition, this paper introduces variables related to the digital economy to perform a comprehensive examination of the moderating effect of digital economy development on the relationship between green finance and both carbon emission intensity and efficiency. The results indicate that green finance reduces carbon emission intensity and that green innovation, green total factor productivity and the transformation and upgrading of industry are important mediating mechanisms. Meanwhile, analysis shows that green finance improves carbon emission efficiency. This paper also finds that the digital economy significantly enhances the role of green finance in reducing carbon emission intensity and promoting carbon emission efficiency, and makes a positive contribution to promoting carbon emission reduction. The findings will contribute to strengthening the government’s capacity for environmental protection, developing green finance, and reducing carbon emissions.

Climate change is a major and urgent global challenge for humanity. Anthropogenic carbon emissions that seriously threaten sustainable development worldwide (Glasnovic et al., 2016; Yang et al., 2021) and are of great global concern (Rezanezhad et al., 2020; Pan et al., 2022a). Realizing carbon emission reduction cannot only rely on the regulation of the market, but also requires the government to formulate effective environmental policies for regulation. Green finance is one of the important policy tools. As a way to promote sustainable development, green finance has been developing rapidly and is attracting increasing attention globally (Bai and Lin, 2024), and is recognized as an effective tool to reduce carbon emissions.

Green finance aims to facilitate the development of green projects by providing financial services such as investment, financing, and funding (Ji and Zhang, 2019). The term “green finance” covers green credit, green bonds, green funds, green insurance, green investment, and other financial instruments with green characteristics. Green finance has the dual functions of financial resource allocation and environmental regulation (Tolliver et al., 2021), and is widely recognized as the key to combating climate change (IFC, 2016). Therefore, green finance may be an important way to reduce carbon emissions and achieve both the Paris Agreement and the United Nations Sustainable Development Goals (Umar et al., 2023). In this context, this paper attempts to explore the impact of green finance on carbon emission intensity and the intrinsic mechanism by which this influence occurs, and further to analyze the impact of green finance on carbon emission efficiency.

In addition, the rapid development of the digital economy has led scholars and policymakers to consider its role in environmental protection and sustainable development. As a new economic form, the digital economy takes data resources as the key production factor, relies on digital technology innovation as the core driving force, and continuously improves the digitization, networking, and intelligence of the society through the mode of digital industrialization and industrial digitization. This can provide technical support for green development (Balcerzak and Pietrzak, 2017; Yi, Liu, Sheng, Wen, 2022), and produce certain beneficial environmental effects while effectively promoting high-quality economic development. At the same time, the advantages of the digital economy–in terms of efficient information dissemination, data creation and sharing–can enhance the production and operation efficiency of enterprises, thus reducing energy consumption and carbon emissions (Koch and Windsperger, 2017). The digital economy also empowers the traditional financial sector to improve the efficiency with which green finance is implemented, optimize resource allocation by green finance, and strengthen the environmental regulation function of green finance. Thus, another central question of this research concerns the impact of the digital economy on the relationship between green finance and carbon emissions.

China, the world’s second largest economy, has become the world’s largest emitter of carbon dioxide (CO2), which has a significant impact on global climate change and poses a threat to China’s own sustainable development (Shao et al., 2019; Ibrahim and Ajide, 2021; Jia et al., 2022). In 2020, China accounted for 30.7% of global CO2 emissions, a greater share than that of the United States (13.8%) or Europe (11.1%) (Statistical Review of World Energy, 2021). To reduce carbon emissions, the Chinese government has set the solemn goal of achieving carbon neutrality by 2060 (Lin and Ma, 2022). Exploring feasible carbon reduction measures can not only solve the serious greenhouse effect problem and realize the above commitment, but also provide Chinese solutions for other countries to achieve carbon reduction and promote green development. Meanwhile, China’s digital economy is developing rapidly: it reached a size of 39.2 trillion yuan in 2020, accounting for 38.6% of China’s GDP (Zhang et al., 2022). These facts motivated our analysis of the core issues of this paper in the context of China.

We use prefecture-level data to comprehensively measure the degree of green finance development, carbon emission intensity and efficiency, and the digital economy index in China based on a constructed measurement system. Using the results, the impact of green finance on carbon emission intensity and efficiency is empirically examined. Meanwhile, we select three indicators, namely, green innovation, green total factor productivity and the upgrading of industrial structure, to examine the mediating mechanisms through which green finance affects carbon emission reduction. Further, we explore the moderating effect of digital economy on the relationship between green finance and carbon emission intensity and efficiency.

The contribution of this paper is threefold. First, we analyze the role green finance plays in carbon emission intensity and efficiency. The extant literature mostly examines important factors for carbon emission reduction from the perspectives of environmental regulation, green innovation, urbanization, and industrial development, but less so from the perspective of green finance. In addition, extant studies on carbon emissions focus on the intensity or total amount of carbon emissions, while ignoring the efficiency of carbon emissions. This paper not only analyzes the impact of green finance on carbon emission intensity, but also further examines the impact of green finance on carbon emission efficiency using a variety of measurement methods.

Secondly, unlike extant research which uses green credit, green investment, green funds or other single indicators to measure green finance, we utilize a variety of indicators to construct the measurement system of green finance, which can comprehensively evaluate the degree of green financial development and enhance the accuracy of the study.

Thirdly, we introduce the digital economy, a new and rapidly developing economic model, and measure the digital economy development index of prefecture-level cities on the basis of multiple indicators. We then link the digital economy, green finance, and carbon emissions to explore the moderating effect of the digital economy on the relationship between green finance and carbon emission intensity and efficiency. This broadens research on the effect of the digital economy on carbon emission reduction.

The paper is organized as follows. The second section presents our theoretical analysis and hypotheses; the third section details the empirical design employed in the study; the fourth section contains an analysis of the results; the fifth section presents further analysis; the sixth section analyzes the moderating effect of the digital economy; and the final section draws conclusions from the study.

Carbon dioxide (CO2) emissions are an important contributor to global warming and a major environmental challenge that mankind is currently facing (Koengkane et al., 2019). Many studies have examined ways to reduce the intensity of carbon emissions. Estrada and Santabarbara (2021) argued that through the imposition of carbon tax, an environmental tax reform, technological innovation and clean energy use can be promoted, thus reducing the amount of carbon emissions; Chen and Lin (2021) found that carbon emissions trading is also an important market mechanism to promote carbon emission reduction and realize low-carbon economic development. In addition, some studies have analyzed carbon emission efficiency. Lin et al. (2017) used the Shephard input distance function and the nonparametric common Frontier method to construct a carbon emission performance index to assess the carbon emission efficiency of energy-intensive industries in China.

Among the many studies on carbon emission reduction, the role played by finance has received attention from scholars. Jeucken (2001) studied the relationship between financial institutions and sustainable development, and points out that reducing carbon emissions requires attention to the key role of banks. Altaghlibi et al. (2022) argued that banks and financial regulators can promote green finance through the regulation of money, credit, and financial systems to guide the flow of capital to low-carbon sectors, thus promoting a low-carbon transition. Based on these studies, some scholars have examined the relationship between finance and the environment. Koengkan et al. (2018) examined the impact of national financial openness on environmental degradation and found that financial openness increased carbon emissions in both the short and long term; Koengkan et al. (2020) found that financial openness, economic growth, and primary energy consumption increased environmental degradation in both the short and long term after conducting a study using data from Latin American and Caribbean countries.

Some scholars further analyze the relationship between green finance and carbon emissions. Studies have used different dimensions of data to conduct empirical tests, and most of them found that a certain type of green finance can effectively reduce the intensity of carbon emissions. Wan et al. (2022) examined the relationship between green real estate financing and carbon dioxide emissions from the construction sector in 100 developed and emerging countries, and found that there is a negative correlation between the two, and that this relationship is particularly obvious in emerging countries. In addition, the carbon emission reduction effects of green bonds, green credit, and green venture capital have also been confirmed by the study. Mamun et al. (2022) found that green bonds can promote global economic decarbonization; Hu and Zheng (2022) and Wang et al. (2021b) showed that green financial instruments such as green credit and green venture capital can all reduce carbon emission intensity; Qin and Cao (2022) used the Green Credit Guidelines as a green financial policy and constructed a difference-in-differences model, and found that green finance represented by green credit can significantly reduce the carbon emissions of highly polluting enterprises.

Meanwhile, some studies construct the measurement system of green finance and use a variety of indicators to measure green finance, and then use the measurement results to analyze the impact of green finance on carbon emissions. Pretis et al. (2017) combined the time series test of different countries and found that green finance plays a positive role in carbon emission reduction; Khan et al. (2019) analyzed the data of the BRICS countries and found that the development of green finance can inhibit carbon dioxide emissions; Chen and Chen (2021) used a spatial dynamic panel model and found that green finance can promote carbon emission reduction in the region. Chen and Chen (2021) use a spatial dynamic panel model and find that green finance can promote carbon reduction and emission reduction in the region, and inhibit carbon emissions in neighboring regions; Guo et al. (2022) test the impact of green finance on agricultural carbon emissions based on the perspective of meso-industry, and the study shows that green finance can effectively reduce carbon emissions in the agricultural sector.

The concept of digital economy was first proposed by Tapscott (1994), who described digital economy as an emerging form of economy that expresses information technology and communication economy, production, and lifestyle. Existing studies have mainly used the entropy weight method, principal component analysis, and input-output method to measure the degree of development of the digital economy. Peng and Dan (2023) chose the three indicators of the Internet, mobile telephony, and digital inclusion, and used the entropy weight method to measure the digital economy. Ma et al. (2022b) constructed a digital economy measurement system using principal component analysis, and measured China’s digital economy development index by utilizing the development of telecommunication industry, Internet industry, computer service industry and software industry on China’s digital economy.

Research on the digital economy has focused on urban development (Zhu and Chen, 2022), corporate innovation (Luo et al., 2023), income distribution (Peng and Dan, 2023), fintech (Chen et al., 2022), and total factor productivity (Pan et al., 2022b). Yang et al. (2023a) found that the digital economy plays an important role in promoting industrial green transformation, and that the evolution of the digital economy is strongly correlated with industrial green transformation in space and time. 2023) found that the digital economy plays an important role in promoting the green transformation of industries, and that the evolution of the digital economy has a strong spatial and temporal correlation with the green transformation of industries. Ren et al. (2023) confirmed that the technology and efficiency revolution triggered by the digital economy will upgrade the existing production processes across the chain and accelerate the transformation. Chen et al. (2022) argued that the digital economy promotes fintech through technological advancement and credit asset quality.

Unlike the traditional economy, the digital economy, as a new key driver of the economy and society (Cong et al., 2021), has given rise to new economic forms and driven profound changes in the mode of production and governance, leading to lower resource consumption and less environmental pollution (Murthy et al., 2021). Xiao et al. (2023) empirically examined the direct, indirect, spatial spillover and non-linear effects of the digital economy on green development using data from 284 prefecture-level cities in China, and all found that the digital economy significantly promoted green development; Ma and Zhu (2022) proposed that the green financial system can accelerate the green transformation of traditional manufacturing industry, improve the technological maturity of manufacturing industry, and reduce environmental problems.

In addition, some studies have directly analyzed the relationship between digital economy and carbon emissions. Chen et al. (2023) analyzed the impact of digital economy on carbon emissions by constructing a two-way fixed-effects model using provincial panel data in China, and found that the development of digital economy significantly reduces the intensity of carbon emissions, and that government support positively moderates the relationship between digital economy and carbon emissions. Wang and Li (2023) concluded that the development of digital economy significantly reduces carbon emissions, and this effect has economic dimension heterogeneity, industrial heterogeneity, production and life heterogeneity, and urban-rural heterogeneity. Yi et al. (2022) constructed a spatial panel Durbin model and a mediation effect model to study the mechanism and impact of digital economy on carbon emission reduction. The results showed that the development of digital economy has a significant spatial spillover effect on carbon emission reduction, which means that carbon emission reduction can be indirectly affected by the digital economy through the transformation of energy structure.

Although existing studies have examined the paths affecting carbon emissions from different aspects, they have mostly analyzed them from the aspects of fiscal policy, tax policy, environmental regulation, and there are fewer studies that have constructed green finance indicators from multiple perspectives and analyzed the relationship between green finance and carbon emissions. At the same time, these studies have not reached a unified conclusion. In addition, the existing studies have only analyzed the impact of these factors on carbon emission intensity, and fewer studies have further examined the impact on carbon emission efficiency. Furthermore, the digital economy is a new type of economic development, which has an impact on the environment, society, and economy. However, existing studies have less systematically measured the degree of digital economy development, and less examined the carbon emission reduction effect of digital economy. Therefore, this paper systematically constructs the measurement system of the carbon emission intensity, carbon emission efficiency, green finance, and digital economy to measure these variables. On this basis, this paper further combines green finance, digital economy, and carbon emission intensity, and examines the impact of green finance on carbon emission reduction, and further examines the moderating effect of digital economy on the relationship between the two. This paper enriches the existing research on the realization path of carbon emission reduction, the environmental effect of green finance and the carbon emission reduction effect of digital economy, thus making up for the shortcomings of the existing research.

Due to the non-competitive and non-exclusive nature of air resources, carbon emissions have strong negative externalities, which makes it difficult to clearly define their property rights and therefore leads to market failure. At this point, it is difficult to rely solely on the market to achieve Pareto optimality of carbon emissions, as market players will not spontaneously internalize the social costs that are higher than the private costs, and market decisions in the equilibrium state will bring unnecessary losses. Therefore, as the “visible hand,” the government should intervene in the carbon emission market to realize the optimal allocation of resources. There are many government policies to intervene in the carbon market, and green finance is an important market-incentivized environmental policy tool. Green finance refers to the fact that financial institutions take into consideration the environmental behavior of market players when making decisions, and through a series of institutional arrangements, allocate more financial resources to environmentally friendly market players, industries, and products, reflecting the green preference of financial decision-making (Freebairn, 2012; Huang et al., 2022).

With the dual characteristics of environmental regulation and financial allocation (Lu et al., 2021), green finance can inhibit the access to capital of high-carbon emitting enterprises, rationally allocate financial resources to green industries and green projects, and utilize financial leverage to achieve climate goals, which is widely considered an effective policy tool to promote carbon emission reduction and green development (Freebairn, 2012; Jin et al., 2022). Specifically, green finance provides market players with differentiated and preferred financial products and services based on their environmental behavior. At the same time, it relies on the resource allocation function of the financial market to establish an incentive and constraint mechanism, which influences the production and operation activities of market players, and thus has an impact on the intensity of carbon dioxide emissions (Jalil and Feridun, 2011; Khan et al., 2018). For example, green finance sets higher lending rates and reduces the amount of credit up to for high-pollution and high-emission enterprises, which limits the financing of these enterprises and incentivizes them to shift towards low-carbon and cleaner production and operation models, thus reducing the carbon emission intensity. On the contrary, for environmentally friendly enterprises, green finance has incentivized them to operate continuously by lowering the lending rates and financing thresholds, promoting their sustainable development, and further reducing the carbon emission intensity, thus realizing a virtuous cycle of enterprise development and carbon emission reduction (Wang and Wang, 2021; Mirza et al., 2023). Therefore, Hypothesis 1 of this paper is proposed.

H1. Green finance reduces carbon emission intensity.

Green technology innovation has the disadvantages of large investment amount, long investment cycle and high investment risk, and enterprises face greater difficulties in carrying out green innovation (Hall, 2002). Therefore, it is necessary for the government to give certain incentives to promote the green innovation of enterprises. Green finance can guide the flow of financial resources to green innovation activities through resource allocation, which reduces the risk of innovation and research and development of enterprises, thus promoting green innovation (Haas and Popov, 2019; Wang and Yang, 2020). On the one hand, green finance can provide financial support for green innovation. External financing from financial institutions is an important source of funds for enterprises to carry out green innovation activities (Su et al., 2022). Green finance provides lower loan interest rates and financing thresholds for enterprises’ green innovation activities, which encourages enterprises’ green innovation and thus promotes their green technological innovation (Zhao et al., 2023). In addition, green finance can effectively solve the problems of large initial investment, long profit cycle, and unpredictable risk of green innovation funds, and alleviate the financial constraints of enterprises at the initial stage of green innovation (Du et al., 2022).

On the other hand, green finance incentivizes high-energy consumption and high-emission enterprises to reduce their reliance on high-pollution production experience patterns, prompting them to change to an environmentally friendly production mode, thereby promoting green innovation (Berrone et al., 2013). Due to industry constraints, high-polluting and high-emission firms are forced to transform their original crude production methods, which requires the support of green technological innovation. Therefore, green financial instruments can also promote heavy polluting enterprises to reduce carbon emissions through technological innovation (Bruce, 2014; Hong et al., 2021). Some studies have showed that green finance can promote green innovation. For example, Han et al. (2022) found that green finance can promote green innovation in heavy polluters. Wang et al. (2023a) employed China’s 2017 green finance reform pilot as a quasi-natural experiment, and found that the green finance pilot promotes green innovation. Based on the above analysis, Hypothesis 1a is proposed.

H1a. Green finance promotes green innovation, thereby reducing carbon emission intensity.

Total factor productivity (TFP) is the increase in output due to technological progress in addition to labor and capital inputs. Endogenous growth theory considers it to be the driving force for achieving sustainable economic growth. Unlike TFP, green total factor productivity (GTFP) is TFP under environmental constraints, which considers the negative externalities of environmental regulations (Chung et al., 1997). GTFP utilizes inputs, outputs, and undesired outputs to test economic growth (Li et al., 2022a; Liu et al., 2022). The development of green finance can reduce energy consumption on the input side and excessive environmental hazards on the output side, improve energy efficiency, and thus enhance GTFP (Li et al., 2022b). Meanwhile, green finance can improve the GTFP of enterprises, realize high-quality development of the economy, and promote green economic development. It improves environmental performance while increasing productivity, thus increasing GTFP (Xia and Xu, 2020; Yan et al., 2020). Some studies have also confirmed that green finance contributes to GTFP (Liu et al., 2021; Meo and Abd Karim, 2021). Based on this, Hypothesis 1 b is proposed.

H1b. Green finance enhances GTFP, thereby reducing carbon emission intensity.

Green finance is characterized by capital orientation and industrial integration. It guides the flow of capital from backward industries to green industries, restricts the financing of polluting industries, and encourages the upgrading of crude traditional industries, thus realizing industrial transformation (Bai and Lin, 2024). Specifically, green finance guides the transfer of financial resources from high-pollution and high-emission industries to green and low-carbon industries and environmentally friendly industries, and guides the direction of industrial development with the flow of funds, which realizes the transformation of industrial structure, optimizes the industrial structure, and then reduces the intensity of carbon emissions (Wang and Wang, 2023). At the same time, green finance guides enterprises to realize resource reconfiguration under the guidance of the green development concept and gradually forms an industrial structure with green industry as the core, promoting the adjustment of industrial structure within enterprises (Song et al., 2021; Zhang et al., 2021). Under the constraints of green financial development, high-pollution and high-emission industries face greater survival pressure, which hinders the development of these industries. To seek their own sustainable development, these enterprises will endogenously carry out industrial transformation and choose to transform into environmentally friendly tertiary industries (Wang et al., 2021a). In addition, the green finance policy, as a signal for the government to promote green development and phase out high-pollution and high-energy-consumption industries, plays a warning role for high-pollution and high-energy-consumption industries. The green finance policy guides private capital to flow spontaneously to green projects and activities (Zhang et al., 2021). These enterprises actively realize the green transformation of production and operation as well as industrial structure, eliminate backward production capacity, and build a green pro-duction system through external regulation and their own actions. Therefore, Hypothesis H1c is proposed.

H1c. Green finance promotes industrial transformation and upgrading, thereby reducing carbon emission intensity.

Carbon emission efficiency is the maximum desired output and the minimum carbon emissions that can be achieved when input factors such as capital, labor and energy are certain. Carbon emission efficiency, as a key indicator of green and low-carbon development, accurately utilizes the input-output relationship to reflect the relationship between economic growth and carbon emissions. Therefore, any behavior that can reduce carbon emissions without reducing economic output or in-crease economic output without increasing carbon emissions can improve carbon emission efficiency. The theoretical analysis in the previous section shows that green finance can reduce carbon emission intensity through the tendentious allocation of resources. Similarly, green finance can achieve carbon emission efficiency by strategically allocating financial resources and incentivizing market players to use the least amount of energy to achieve the greatest economic output (Sohail et al., 2022; Tian et al., 2022). For example, green finance can promote green innovation, which reduces the amount of energy consumption required to reduce the unit output of enterprises, improves the efficiency of energy use of enterprises, and thus reduces the carbon emissions. Some studies have also demonstrated the positive effect of technological progress on improving carbon emission efficiency (Fan et al., 2021). Green finance can also facilitate the transformation of industries and energy infrastructure, promote the op-timization of energy structure and upgrade of industrial structure, and thus improve carbon efficiency (Wang and Wang, 2021; Sun and Chen, 2022). In addition, green finance’s preference for environmentally friendly enterprises incentivizes them to take effective measures to improve carbon efficiency (Zhang et al., 2022). Based on the above analysis, Hypothesis 2 is proposed.

H2. Green finance improves carbon efficiency.

Digital economy is a new economic model that takes big data as its support, the Internet as its platform, and artificial intelligence as its main mode of operation. Its rapid development can improve the allocation efficiency of green financial resources, and better develop the role of green finance in reducing carbon emission intensity and improving carbon emission efficiency (Lange et al., 2020; Liu et al., 2021). Specifically, the digital economy plays a role in regulating the relationship between green finance and carbon emissions in three ways.

First, the digital economy applies digital technologies such as big data, cloud computing, and artificial intelligence to the production and operation of enterprises, which can not only promote the transformation and upgrading of enterprise production technology and organizational form, improve the output efficiency of enterprise production, reduce the dependence on energy in the production process, and realize the efficient use of energy and resources (Dong et al., 2022; Yi et al., 2022), but also lead to the reform of the internal management of the enterprise, reduce the cost of operation, and alleviate the financing constraints of green technology development and reduce green production costs. As a result, enterprises can reduce unnecessary carbon emissions, so that green finance can better play a positive role in reducing carbon emission intensity and enhancing carbon emission efficiency (Koch and Windsperger, 2017; Hao and Wu, 2021).

Second, the advanced digital technology and massive data elements spawned by the development of the digital economy can apply technologies such as big data, artificial intelligence and distributed management to the production and operation of market entities, which is conducive to the integration of fragmented corporate information and the promotion of low-carbon technological innovation as well as cleaner energy production (Marcel and Stefanie, 2020). At the same time, digital technology links green finance, carbon foot printing and carbon sink systems and visualization, which can provide all-round and multidimensional supervision and detection of production enterprises. This can also accurately calculate the carbon intensity and efficiency of enterprises and incentivize them to reduce carbon emissions (Ding et al., 2022), thus deepening the relationship between green finance and carbon intensity and efficiency.

Finally, the development of digital technology has enhanced the effectiveness and availability of corporate carbon information, allowing resources to be better matched through the market. The continuous integration of the digital economy and the real economy can realize the effective use of resources and better promote green and low-carbon development (Ren et al., 2021; Zhang et al., 2022). In addition, the development of digital economy accelerates the development of digital finance, which, combined with green finance, give rise to the new product of green digital finance, thus strengthening the relationship between green finance and carbon emissions. Based on the above analysis, Hypotheses 3a and 3 b of this paper are proposed.

H3a. The development of digital economy strengthens the role of green finance in reducing carbon emission intensity.

H3b. The development of digital economy strengthens the role of green finance in promoting carbon emission efficiency.

We construct the following Models (1) and (2) to identify the impact of green finance on carbon emission intensity and carbon emission efficiency respectively. Following Yang et al. (2023b) and Ran et al. (2023), we construct two-way fixed effects for empirical testing. The two-way fixed effects model can control for individual effects and time fixed effects while dealing with heteroskedasticity and autocorrelation in panel data, thus improving the accuracy of the estimation results (Guo et al., 2022).

where i and t are prefecture-level city and year, respectively;

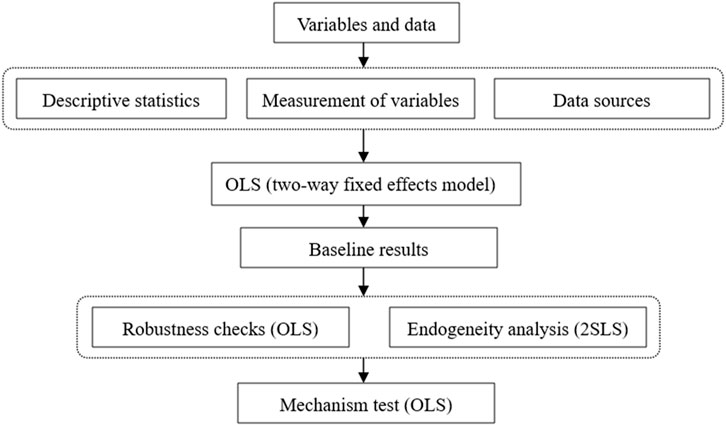

FIGURE 1. The method framework of this study.

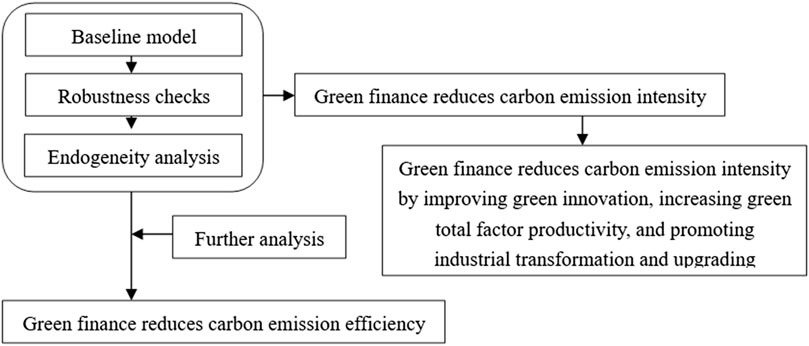

FIGURE 2. The findings of this study.

We study the impact of green finance on carbon emissions and examine the moderating role of the digital economy in it. Therefore, the dependent variable is carbon emission, the core independent variable is green finance, and the moderating variable is digital economy.

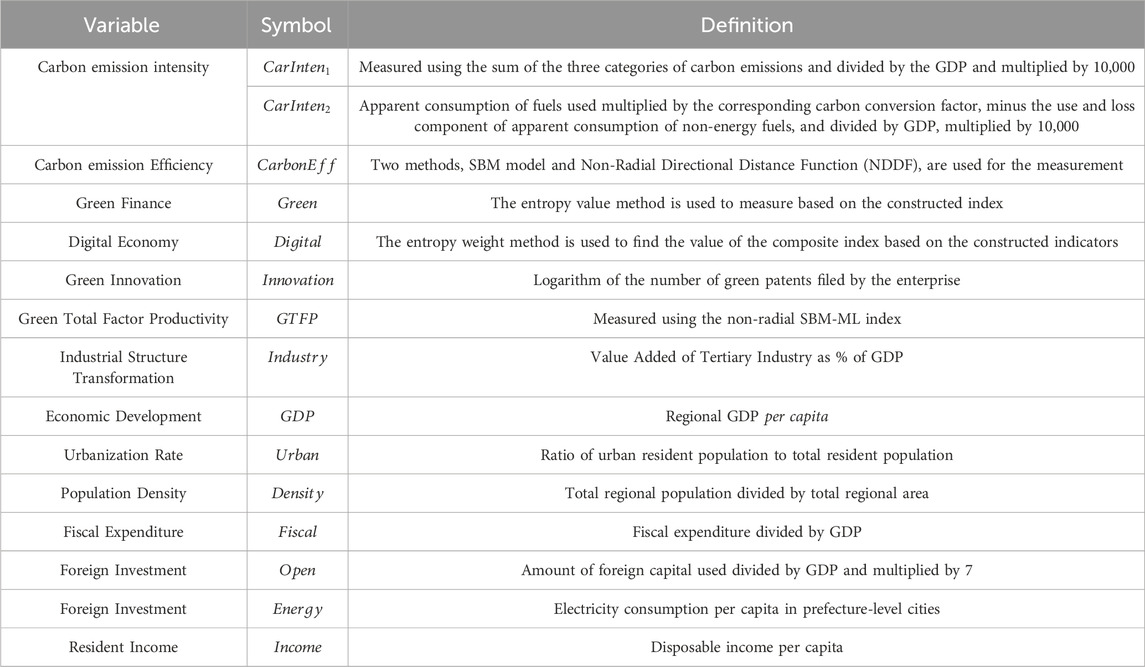

The dependent variables are carbon emission intensity (CarInten) and carbon emission efficiency (CarEff). For the carbon emission intensity variable, we use the sum of the three scopes of carbon emissions to measure the total carbon emissions at the prefecture-level city. Specifically, carbon emissions include three main aspects: first, all direct emissions within the urban jurisdiction, including those from transportation and buildings, industrial processes, agriculture, forestry and land-use change, and waste disposal activities; second, indirect energy-related emissions that occur outside the city’s jurisdiction, including emissions generated for electricity, heating and/or cooling; third, other indirect emissions caused by activities within the city that occur outside the jurisdiction but are not included in the second category, including emissions from the production, transportation, use and waste disposal of all goods purchased from outside the jurisdiction.

In terms of direct or indirect emissions, scope 1 includes all direct emissions within the city’s jurisdiction; scope 2 refers to energy-related indirect emissions that occur outside the city’s jurisdiction; and scope 3 refers to other indirect emissions caused by activities within the city that occur outside the jurisdiction but are not covered by scope 2.

In addition, we use the alternative measure of carbon emissions intensity for the robustness test. Following Shan et al. (2018), we use energy supply statistics to calculate carbon dioxide emissions from fossil fuel combustion (crude coal, crude oil, and natural gas). This is done by multiplying the apparent consumption of the fuel by the corresponding carbon conversion factor and subtracting the use and loss portion of the apparent consumption of non-energy fuels, thus yielding the total carbon emissions.

In terms of the carbon emission efficiency variable, following Tone (2011), we use both the SBM model and the Non-Radial Directional Distance Function (NDDF) to measure. Among them, the input variables include capital stock, total urban unit employees, and energy consumption; the output variables include GDP; and the non-expected outputs are carbon emissions, involving coal, coke, crude oil, gasoline, kerosene, diesel oil, fuel oil, and natural gas. The process of calculating non-expected outputs is based on the measurement methodology of the IPCC Guidelines for National Greenhouse Gas Emission Inventories, 2006 edition (IPCC, 2006).

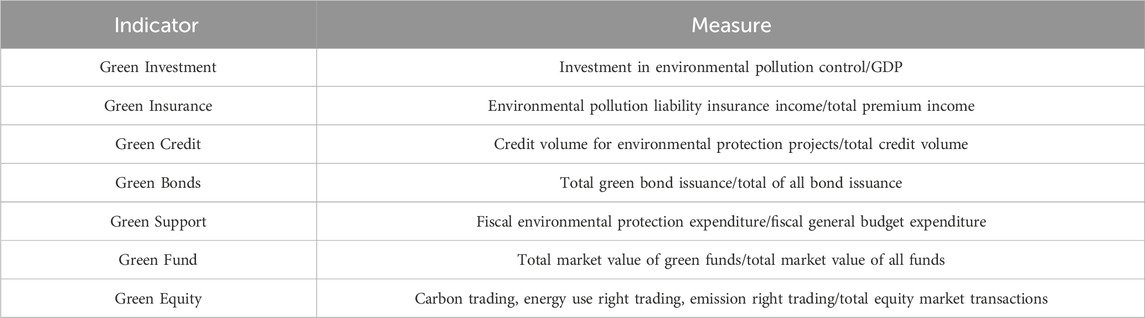

The key independent variable is green finance (Green). The green finance index data of each prefecture-level city is measured by the entropy method. Entropy method is a mathematical method used to determine the degree of dispersion of an index. The greater the degree of dispersion, the greater the influence of the index on the comprehensive evaluation. Indicators for the construction of the Green Finance Index are shown in Table 1.

TABLE 1. Indicators for the construction of the Green Finance Index.

The moderating variable is digital economy (Digital). The number of Internet broadband access users per 100 people, the proportion of employees in computer services and software industry in urban units, the total amount of telecommunication services per capita, the number of cell phone subscribers per 100 people, and the digital financial inclusion index are selected, and the entropy weighting method is used to obtain the composite index value. The entropy method is a mathematical method used to determine the degree of dispersion of an indicator. The greater the degree of dispersion, the greater the impact of the indicator on the overall evaluation. The entropy value can be used to determine the degree of dispersion of an indicator. We use the entropy weight method to measure the development of the digital economy through Stata 17.0, including six steps. Step 1: data standardization; Step 2: calculate the weight of each indicator; Step 3: calculate the entropy value; Step 4: calculate the value of the utility of information; Step 5: calculate the weight of each indicator; Step 6: calculate the samples to derive a comprehensive score. These six steps are all operated in stata17.0, involving the commands of global, qui su, gen, replace, egen, rowtotal, drop.

Mechanism variables include green innovation level (Innovation), green total factor productivity (GTFP), and industry structural transformation (Industry). First, we use the number of green patent applications to measure the level of green innovation. Second, we incorporate corporate environmental pollution into the evaluation system, and use the non-radial SBM-ML index to measure green total factor productivity. The input and output indicators of green total factor productivity include factor inputs, desired outputs, and non-desired outputs. Among them, factor inputs include labor inputs, capital inputs and energy inputs. Labor input is measured by the number of employees in the enterprise; capital input is measured by the net fixed assets of the enterprise; energy inputs are converted by the industrial electricity consumption of the city where the enterprise is located according to the proportion of the enterprise’s employees in the employment of urban personnel in the city; desired output is measured by the enterprise’s business revenue; non-desired output is converted to industrial sulfur dioxide, industrial wastewater, and industrial dust emissions by the proportion of employees in the city where the enterprise is located. Finally, we measure the degree of industrial transformation using the share of tertiary value added in GDP.

Following Koengkan et al. (2018), Qin and Cao (2022), Jin et al. (2021), Lee and Lee (2022), Wang et al. (2023b), we introduce a series of city-level control variables over time to minimize the impact of other factors on the empirical results. The control variables include the level of economic development (GDP), urbanization rate (Urban), population density (Density), fiscal expenditure (Fiscal), foreign investment (Open), energy consumption (Energy) and residential income (Income). Specifically, we use regional GDP per capita to measure the level of regional economic development, the ratio of urban population to total resident population to measure the urbanization rate, the total regional population divided by the total area of the region to measure the population density, fiscal expenditure divided by GDP to measure the level of regional fiscal expenditure, the amount of foreign investment divided by GDP to measure the level of openness degree, the per capita electricity consumption to measure the level of energy consumption, the per capita energy consumption to measure the level of energy consumption, and residential income disposable income per capita in the region the measure the residential income. The definition of the variables is shown in Table 2.

TABLE 2. Variable definitions.

Carbon emissions data. Carbon emission data include both carbon intensity and carbon efficiency data. The data sources are China’s statistical yearbooks, such as China Urban Statistical Yearbook, China Industrial Statistical Yearbook, and China Environmental Statistical Yearbook. In addition, some of the missing data were supplemented using the IPCC emission factor database. Emission factor data were obtained from the Provincial Greenhouse Gas Emission Inventory Guidelines (Trial) and the carbon emission inventory guidelines issued by the government.

Green finance data. The data required to measure the level of green finance come from the Statistical Yearbook and Environmental Status Bulletins of each region.

Digital economy data. The raw data for measuring the digital economy index comes from the China Urban Statistical Yearbook.

Prefecture-level data. A series of city-level control variables are introduced in the regression, and city-level mechanism variables are also introduced in the mechanism analysis. The above data come from China Urban Statistical Yearbook, China Environmental Statistical Yearbook, and provincial statistical yearbooks.

Enterprise-level data. In the mechanism analysis, we match the city-level data with enterprise micro data to analyze the impact of green finance on carbon emissions. The enterprise-level data comes from CSMAR database and websites of listed companies.

Based on the variables needed to measure carbon emissions, green finance, and digital economy, we select databases that can obtain data on these variables. In China, government statistics are the most authoritative, official, and complete database to obtain macro indicators, so we choose several Chinese statistical databases. In addition, the CSMAR database is mostly used for the study of Chinese micro-enterprises, which contains complete data on Chinese listed companies and can be updated to the most recent year. The use of the most authoritative official statistics in China and the most widely used microenterprise statistics enhances the credibility of the empirical results of the study. We process the samples as follows: (1) we exclude prefecture-level cities with missing samples; (2) we exclude four municipalities directly under the control of the central government, two special administrative regions, Taiwan Province, and the Tibet Autonomous Region samples; and (3) to exclude the outlier effect, we winsorized all the continuous variables at 1% and 99%. To eliminate the effect of some extreme values on the study, continuous variables are generally subjected to winsorize. Studies usually treat extreme values at the 1% and 99% quantiles. For values less than 1%, the 1% value is assigned; for numbers greater than 99%, the 99% value is assigned. We used the econometric software Stata 17.0 in our study. The Stata commands used in this study included sum, winsor2, global, reghdfe, ivreghdfe.

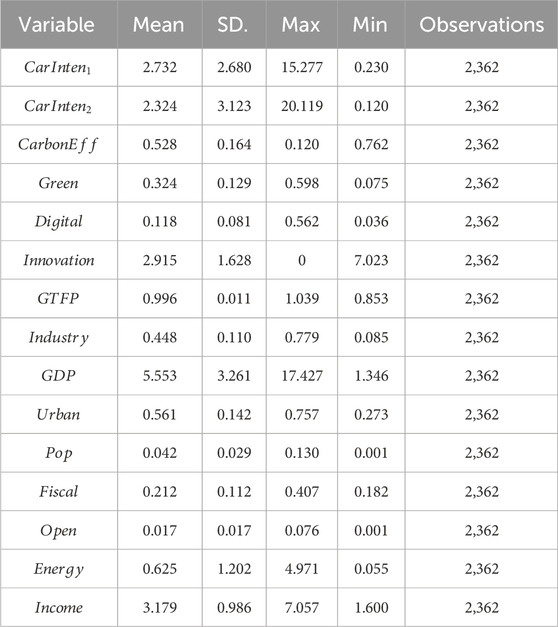

The descriptive statistics of the main variables are shown in Table 3. As can be seen from Table 3, the mean values of carbon emission intensity measured using the two methods are 2.732 and 2.324, and the standard deviations are 2.680 and 3.123, respectively, indicating that there are large differences in carbon emission intensity among Chinese prefectural-level cities. Meanwhile, the mean and standard deviation of carbon emission efficiency are 0.528 and 0.164, respectively, indicating that the carbon emission efficiency of Chinese prefectural-level cities is not high. In addition, the measured mean values of the degree of green finance development and the degree of digital economy development are 0.324 and 0.118, respectively, and the standard deviation is 0.129 economy 0.081, respectively.

TABLE 3. Descriptive statistics of variables.

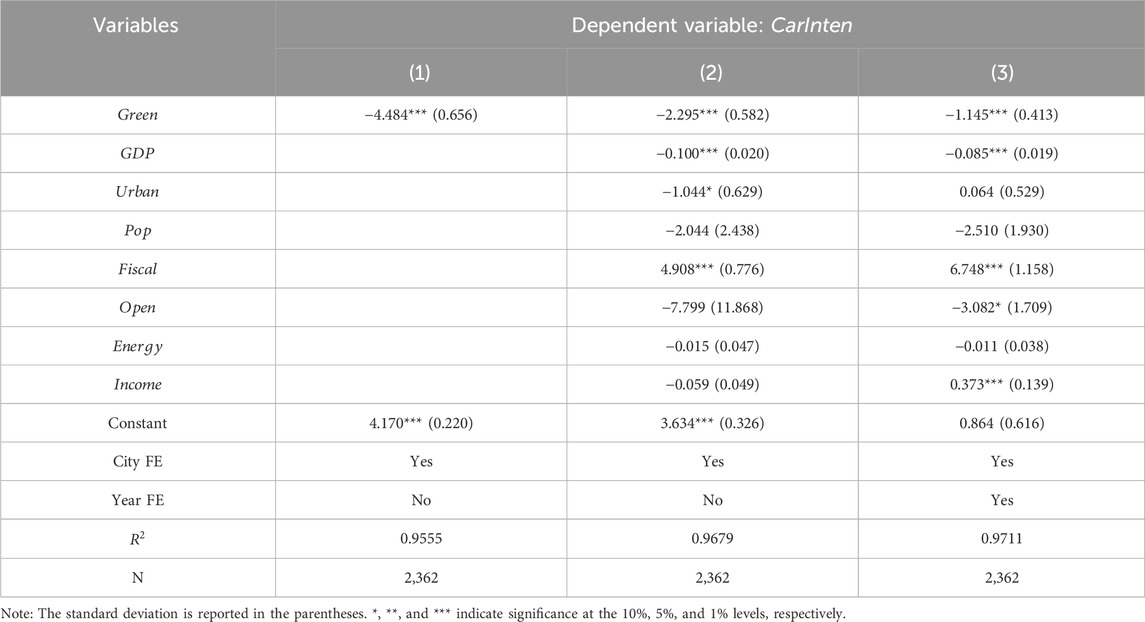

We use Model (1) for the baseline regression. Table 4 shows the regression results. In Table 4, Column (1) shows the regression results without introducing any control variables, Column (2) introduces control variables, and Column (3) further introduces fixed effects. When no control variables are added, the results in Column (1) show that the coefficient of Green is −4.484 and is significant at the 1% statistical level, indicating that green financial development can reduce carbon emission intensity, while the results in Column (2) show that the coefficient of Green is −2.295 after the introduction of the control variables and remains significant at the 1% statistical level. When all the control variables and city and year fixed effects are introduced, the absolute value of the coefficient of Green decreases to −1.145 and remains significantly positive at the 1% statistical level. Taken together, the results in Columns (1)–(3) indicate that the development of green finance significantly reduces carbon emission intensity, which verifies Hypothesis 1.

TABLE 4. Baseline results.

For the other variables, as can be seen in Column (3) of Table 4, the coefficient of GDP is −0.085 and is significant at the 1% statistical level, indicating that an increase in the level of economic development significantly reduces carbon emissions. Generally, the increase in the level of economic development may exacerbate environmental pollution. However, China has attached great importance to environmental protection and carbon emission reduction in recent years, and has proposed the goal of high-quality development to reduce environmental pollution and carbon emissions while developing the economy. Our results confirm the effectiveness of China’s high-quality development. In addition, the coefficient of Fiscal is 6.748 and is significant at the 1% statistical level, suggesting that an increase in fiscal inputs may increase carbon emission intensity. This is because the increased fiscal investment may be used in areas that can promote economic development, such as production, manufacturing, and construction. These areas can generate many carbon emissions, thus increasing carbon emission intensity. The coefficients of Open and Income are −0.382 and 0.373 and are significant at the 10% and 1% statistical levels, respectively, which implies that increased openness up can significantly reduce carbon emission intensity, but increased per capita income increases carbon emission intensity.

After the baseline regression, we conduct a series of robustness checks to examine the robustness of the baseline regression results.

In addition to the carbon emission intensity measure used in the baseline regression, we use another carbon emission intensity measure in the variable description section and conducts robustness checks based on this measure. The results of the alternative carbon emission intensity measure are shown in Column (1) of Table 5. Column (1) of Table 5 shows that the coefficient of Green is −1.920 and is significant at the 1% statistical level, which is consistent with the results in the baseline regression and proves the robustness of the baseline regression results.

TABLE 5. Robustness check results.

Green finance, as a means of government intervention in the market, may need some time to have an impact on carbon emissions. Therefore, we include green finance lagged by one period in Model (1), so as to reconstruct Model (1) as the following model and re-regress based on this model.

where,

Factors that change over time in a region, such as economic fluctuations, also have an impact on carbon emission intensity, and these factors differ among prefecture-level cities. Therefore, we additionally introduce a city-year trend term in Model (1) to explain the influence of possible time-varying factors among cities on the results. The regression results with the additional introduction of the area-time trend term are shown in column (3) of Table 5. The results show that the coefficient of Green is −1.913 and significant at the 1% statistical level, indicating that the results after the additional introduction of the city-year trend term support the baseline results, which also proves the robustness of the baseline results.

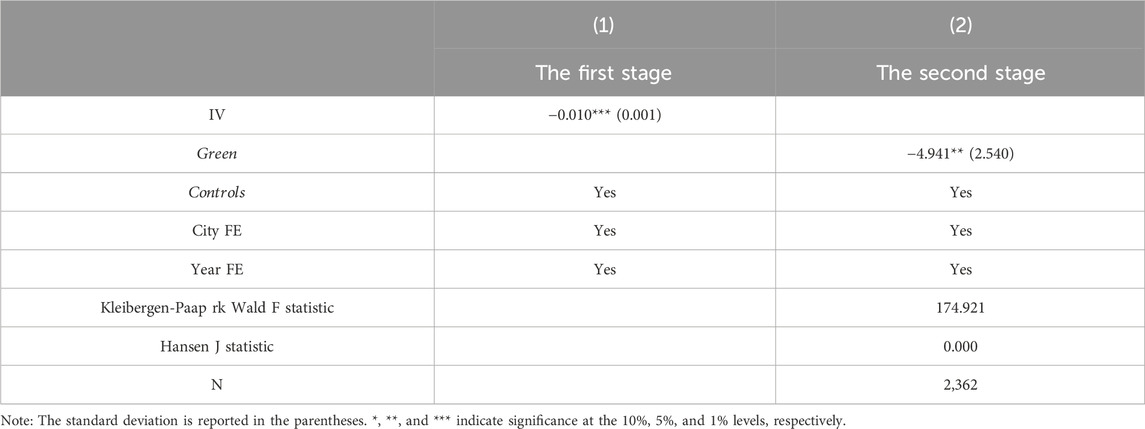

This paper explores the impact of green finance on carbon emissions. However, if a region has a lower carbon emission intensity, its own green financial system may be better, which may lead to the reverse causality problem. Meanwhile, although we introduce many other control variables that affect carbon emission intensity to alleviate the impact of the omitted variable problem on the empirical results, it is difficult to control all the factors affecting carbon emissions and there may also be a certain measurement error problem. Therefore, we construct appropriate instrumental variables and conducts endogeneity analysis based on the two-stage least squares method.

In this paper, instrumental variables are constructed using the product of the average of the lagged one-period value of the green finance index for all prefecture-level cities in a province and the spatial distance of the prefecture-level city from the prefecture-level city with the highest green finance index in the province. A suitable instrumental variable is correlated with the endogenous explanatory variables but uncorrelated with the disturbance term, i.e., it satisfies both the correlation and exogeneity assumptions.

For the relevance assumption, green finance, as an innovation in the environmental regulatory system, is characterized by policy diffusion. When a prefecture-level city introduces an innovative policy, there may be imitation behavior in other prefecture-level cities, leading to the immediate-neighborhood effect of institutional innovation. Therefore, the instrumental variable constructed in this paper is correlated with the endogenous explanatory variables, and this instrumental variable satisfies the correlation assumption. In addition, the green financial development in the lagged period does not affect the degree of previous green financial development, and the spatial distance between two prefectures is a non-time-varying variable that does not affect green financial development. Therefore, the instrumental variables constructed also satisfy the exogeneity assumption of instrumental variables.

Using the constructed instrumental variables, we analyze using two-stage least squares. The results of the two-stage least squares regression are shown in Table 6. Panel A and Panel B report the first and second stage regression results, respectively. From the regression results of Panel A, the coefficient of the instrumental variable is −0.010 and significant at the 1% statistical level, which indicates that the instrumental variable is correlated with the endogenous explanatory variables, once again proving the correlation assumption of the instrumental variable. In addition, the results of Panel B show that the coefficient of Green is −4.941 and is significantly negative at the 5% statistical level. After the analysis using two-stage least squares, the coefficient of Green becomes smaller, indicating that the results in the baseline regression underestimate the impact of green finance on carbon emission intensity. The endogeneity analysis shows that the regression results of the two-stage least squares method using instrumental variables also prove that the development of green finance can reduce the intensity of carbon emissions, which is consistent with the results of the baseline regression.

TABLE 6. Endogeneity analysis results.

We construct a mediating effect model based on model (1) to identify the mediation mechanism of green finance affecting carbon emission intensity. The models are as follows:

where

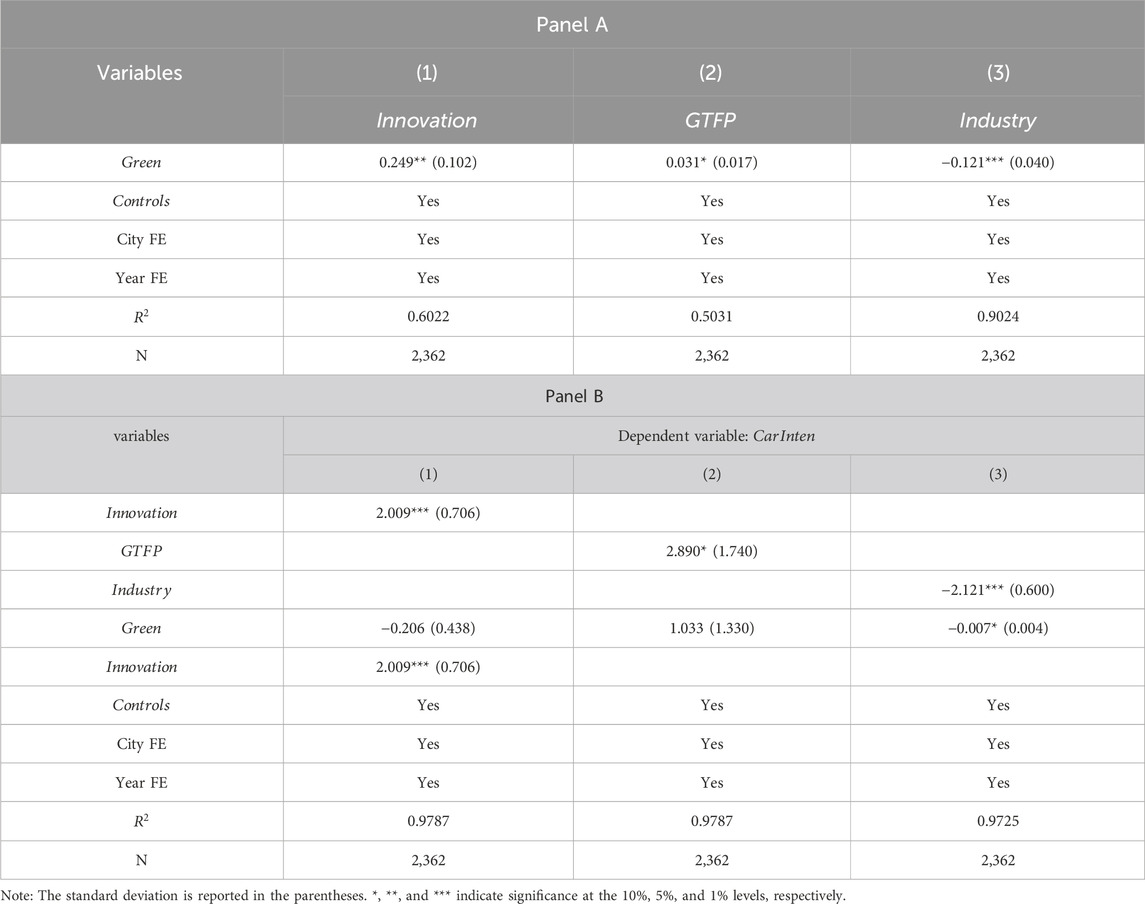

The results of the mechanism test are shown in Table 7. Panel A and Panel B are the regression results of Model (3) and Model (4), respectively. Columns (1)–(3) are the mediating effects of green innovation, green total factor productivity and industrial transformation and upgrading, respectively. The coefficients of Green in Columns (1)–(3) of Panel A are 0.249, 0.031, and −0.121, and are significant at the statistical levels of 5%, 10%, and 1%, respectively, which indicates that the development of green finance significantly improves the green innovation, increases green total factor productivity, and promotes industrial transformation and upgrading. In addition, the regression results of Panel B show that the coefficients of Innovation, GTFP and Industry in Columns (1)–(3) are 2.009, 2.890 and −2.121 respectively, and are significant at 1%, 10% and 1% statistical levels respectively. This indicates that the increase of green innovation, green total factor productivity and industrial transformation and upgrading significantly reduces carbon emission intensity, which also means that the mediating effect of green innovation, green total factor productivity and industrial transformation and upgrading is established.

TABLE 7. Mechanism analysis results.

The above results show that green finance reduces carbon emission intensity by improving green innovation, increasing green total factor productivity and promoting industrial transformation and upgrading, which verifies Hypothesis 1a, Hypothesis 1 b and Hypothesis 1c.

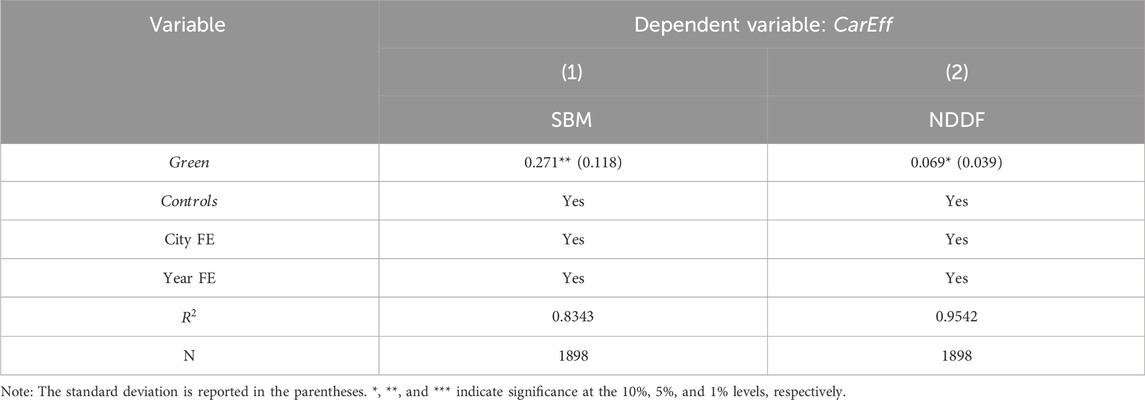

After examining the impact of green finance on carbon emission intensity, we further analyze the impact of green finance on carbon emission efficiency. Carbon emission efficiency indicates that the maximum desired output and the minimum carbon emission can be achieved when the input factors such as capital, labor, and energy are certain, and it is a key indicator for measuring green and low-carbon development. Therefore, examining the impact of green finance on carbon emission efficiency is of great significance to comprehensively test the carbon emission reduction role of green finance. In analyzing the impact of green finance on carbon emission intensity, we use data at the prefecture-level city level. However, due to data limitations, we can only obtain provincial-level data when using both SBM and NDDF methods to measure carbon emission efficiency. Therefore, we use provincial-level data to test the impact of green finance on carbon emission efficiency in China.

The results are shown in Table 8. Columns (1) and (2) of Table 8 show the regression results of green finance on carbon emission efficiency measured by SBM and NDDF methods, respectively. The results show that the coefficients of Green in Columns (1) and (2) are 0.271 and 0.069, respectively, and are significant at 5% and 10% statistical levels, respectively. This indicates that the results using the two different carbon emission efficiency measures all show that the development of green finance improves carbon emission efficiency, which verifies Hypothesis 2.

TABLE 8. The results of the impact of green finance on carbon efficiency.

The results in Table 8 also support the conclusion of the benchmark regression in Table 4. Green finance development reduces carbon emission intensity by enhancing the level of green innovation, improving green total factor productivity and promoting industrial structure transformation. In this process, carbon emission efficiency is also greatly improved, which once again verifies the positive role of green finance in realizing carbon emission reduction and environmental protection.

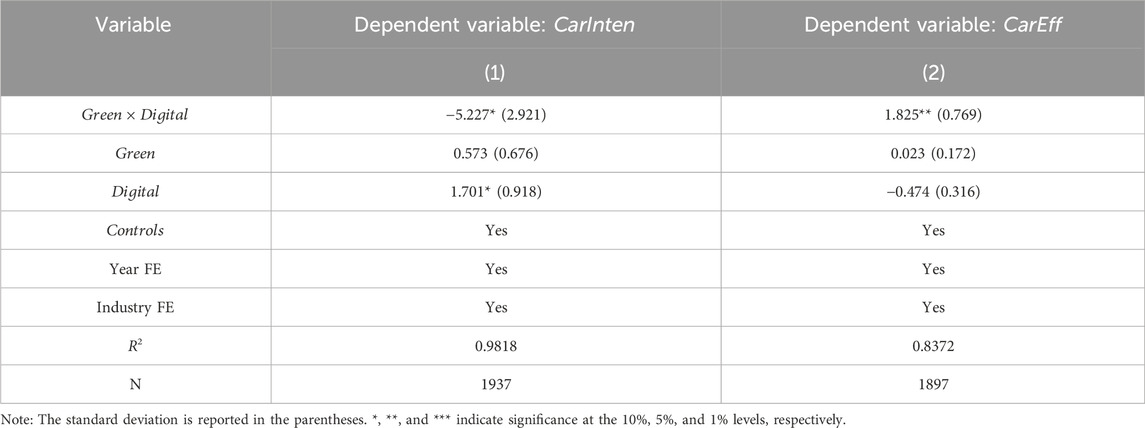

We further introduce the interaction term between green finance and digital economy based on Model (1) to investigate the moderating effect of green finance on the relationship between green finance and carbon emission intensity and efficiency, and construct the following model:

where Model (6) is used to identify the effect of digital economy on the relationship between green finance and carbon intensity; Model (7) is used to identify the effect of digital economy on the relationship between green finance and carbon efficiency;

The results of the moderating effect of digital economy are shown in Table 9. Columns (1) and (2) of Table 9 demonstrate the moderating effect of digital economy on the relationship between green finance and carbon intensity and carbon efficiency, respectively. In Column (1), the coefficient of

TABLE 9. Moderating effects analysis results.

This study discusses the relationship between green finance, the digital economy and carbon emissions in the context of China. Reducing carbon emissions is an important issue of global concern. China is the country with the largest carbon emissions in the world, and the reduction of its carbon emissions is of great significance to the realization of global carbon emission reduction. Meanwhile, green finance has been highly valued as an important way for governments to reduce carbon emissions. This study confirms the positive effect of green finance on carbon emission reduction, which provides a reference for global carbon emission reduction, especially for many developing countries facing the choice between economic development and carbon emission reduction. In addition, with the rapid development of the digital economy, its role in promoting carbon emission reduction has also been emphasized. This study also provides a reference for better utilizing the digital economy to play the role of green finance in carbon emission reduction on a global scale.

Therefore, this study is not only conducive to promoting the development of green finance and carbon emission reduction, enhancing the efficiency of carbon emission, and realizing green and sustainable development in China, but also provides references for carbon reduction in other developing countries, which are also facing the threat of carbon emission.

The feasibility of this study has several aspects: first, the Chinese government attaches great importance to the development of green finance, regards green finance as an important tool for environmental governance, and continues to innovate green financial instruments; second, the central government of China has made “carbon neutrality and carbon peaking” a national strategic goal, and is committed to realizing this goal on schedule; third, the central government requires local government officials to consider carbon emission reduction as an important task, and this task is closely linked to the officials’ future, which motivates local officials to fulfill carbon emission reduction goals. However, using green finance to reduce carbon emission needs to solve some challenges, such as insufficient financial resources for environmental protection, spillover of carbon emission reduction externalities, and conflicts between economic development and environmental protection.

Using data at the prefecture-level city level in China, this paper theoretically and empirically examines the impact of green finance on carbon emission intensity and efficiency, and further examines the moderating role of the digital economy therein. The conclusions are as follows: (1) green finance reduces carbon emission intensity; (2) green finance reduces carbon emission intensity by promoting green innovation, increasing green total factor productivity, and facilitating the transformation of industrial structure; (3) green finance improves carbon emission efficiency; (4) the development of the digital economy strengthens the reduction effect of green finance on carbon emission intensity; and (5) the development of digital finance strengthens the promotion effect of green finance on carbon emission efficiency.

Based on the above findings, we put forward the following policy recommendations to facilitate and promote the development of green finance, reduce the intensity of carbon emissions, and improve the efficiency of carbon emissions. First, regional green technology innovation should be upgraded. The government should further encourage green innovation, strengthen the development and support of green technology, and improve the quality of green innovation while improving the quantity, so as to continuously improve the innovation capacity of green technology and better utilize its role in promoting green development; second, the green total factor productivity of regions should be further enhanced. Green total factor productivity is an important intermediary linking green finance and carbon emissions. Green total factor productivity incorporates environmental factors into the input-output evaluation system and is an important indicator of production quality. The government should continuously improve the green output level of enterprises and regions, thereby promoting the improvement of green total factor productivity and better playing its role as a bridge to promote carbon emission reduction; thirdly, industrial transformation and upgrading should be promoted. The government and policymakers should continuously optimize the industrial structure, accelerate the transformation of highly polluting and energy-consuming enterprises, promote the development of the structure of polluting highly polluting and energy-consuming industries in the direction of cleanliness, advancement and greening, and guide the allocation of the factor resources of these enterprises to the tertiary industry, so as to give full play to the positive effect of upgrading the industrial structure in connecting green finance and carbon emission reduction; fourthly, the digital economy should be vigorously developed. The development of digital economy will not only apply a variety of digital technologies to the production and operation activities of enterprises, but also promote the resource allocation and efficiency of the financial industry. The government should vigorously develop the digital economy, and fully link and organically integrate it with the green financial industry. At the same time, the government should vigorously introduce the digital economy into environmental governance, carbon monitoring, carbon measurement and carbon sinks to better utilize its role in promoting carbon emission reduction.

This paper focuses on the impact of green finance on the intensity and efficiency of carbon emissions and the moderating role of the digital economy therein. However, carbon emissions in one region may have an impact on carbon emissions in another region, which requires further analysis of the spatial spillover effects of green finance on carbon emissions. In addition, since environmental pollution and carbon emissions have market failures and require government intervention to achieve optimal allocation of resources, future research can also focus on other government intervention policies, such as regional financial subsidy policies and tax incentives to analyze the impact of these policies on carbon emissions. At the same time, since green finance includes multiple dimensions, it is possible to compare the differences in the impact of different green financial instruments on carbon emissions, and then design a better combination of green financial instruments to reduce carbon emissions. In addition, future research can examine the moderating effect of other factors on the relationship between green finance and carbon emissions to better utilize the carbon emission reduction effect of green finance.

The raw data supporting the conclusion of this article will be made available by the authors, without undue reservation.

WL: Data curation, Formal Analysis, Investigation, Methodology, Software, Validation, Writing–original draft. PZ: Conceptualization, Funding acquisition, Methodology, Project administration, Supervision, Writing–review and editing.

The author(s) declare financial support was received for the research, authorship, and/or publication of this article. This research is funded by the National Natural Science Foundation of China (71971100); the Project of Department of Education of Hubei Province of Humanities and Social Sciences Research (Number: B2022456).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Altaghlibi, M., Tilburg, R. V., and Sanders, M. (2022). Quantifying the impact of green monetary and supervisory policies on the energy transition. Sustainable finance lab. Available from: https://inspiregreenfinance.org/.

Bai, R., and Lin, B. Q. (2024). Green finance and green innovation: theoretical analysis based on game theory and empirical evidence from China. Int. Rev. Econ. Finance 89, 760–774. doi:10.1016/j.iref.2023.07.046

Balcerzak, A. P., and Pietrzak, B. M. (2017). Digital economy in visegrad countries. Multiple-criteria decision analysis at regional level in the years 2012 and 2015. J. Compet. 9 (2), 5–18. doi:10.7441/joc.2017.02.01

Berrone, P., Fosfiru, A., Gelabert, L., and Gomez-Meijia, L. R. (2013). Necessity as the mother of ‘green’ inventions: institutional pressures and environmental innovations. Strat. Manag. J. 34 (8), 891–909. doi:10.1002/smj.2041

Bruce, S. (2014). The 2015 Paris Climate Agreement: design options and incentives to increase participation and ambition. Available at SSRN 2525957.

Chen, L., Lu, Y. Q., Meng, Y., and Zhao, W. Y. (2023). Research on the nexus between the digital economy and carbon emissions -Evidence at China’s province level. J. Clean. Prod. 413, 137484. doi:10.1016/j.jclepro.2023.137484

Chen, X., and Chen, Z. G. (2021). Can green finance development reduce carbon emissions? Empirical evidence from 30 Chinese provinces. Sustainability 13 (21), 12137. doi:10.3390/su132112137

Chen, X., and Lin, B. (2021). Towards carbon neutrality by implementing carbon emissions trading scheme: policy evaluation in China. Energy Pol. 157 (157), 112510. doi:10.1016/j.enpol.2021.112510

Chen, X., Yan, D., and Chen, W. (2022). Can the digital economy promote FinTech development? Growth Change 53 (1), 221–247. doi:10.1111/grow.12582

Chung, Y. H., Färe, R., and Grosskopf, S. (1997). Productivity and undesirable outputs: a directional distance function approach. J. Environ. Manag. 51, 229–240. doi:10.1006/jema.1997.0146

Cong, L. W., Xie, D., and Zhang, L. (2021). Knowledge accumulation, privacy, and growth in a data economy. Manage. Sci. 67 (10), 6480–6492. doi:10.1287/mnsc.2021.3986

Ding, C. H., Liu, C., Zheng, C. Y., and Li, F. (2022). Digital economy, technological innovation and high-quality economic development: based on spatial effect and mediation effect. Sustainability 14, 216. doi:10.3390/su14010216

Dong, F., Hu, M., Gao, Y. J., Liu, Y., Zhu, J., and Pan, Y. (2022). How does digital economy affect carbon emissions? Evidence from global 60 countries. Sci. Total Environ. 852, 158401. doi:10.1016/j.scitotenv.2022.158401

Du, M. Y., Hou, Y. F., Zhou, Q. J., and Ren, S. Y. (2022). Going green in China: how does digital finance affect environmental pollution? Mechanism discussion and empirical test. Environ. Sci. Pollut. Res. 29, 89996–90010. doi:10.1007/s11356-022-21909-0

Estrada, Á., and Santabarbara, D. (2021). “Recycling carbon tax revenues in Spain,” in Environmental and economic assessment of selected green reforms. Banco de Espana: working papers.

Fan, H., Peng, Y., Wang, H., and Xu, Z. (2021). Greening through finance? J. Dev. Econ. 152, 102683. doi:10.1016/j.jdeveco.2021.102683

Freebairn, J. (2012). Policy forum: designing a carbon Price policy: reducing greenhouse gas emissions at the lowest cost. Aust. Econ. Rev. 45 (1), 96–104. doi:10.1111/j.1467-8462.2011.00670.x

Glasnovic, Z., Margeta, K., and Premec, K. (2016). Could Key Engine, as a new open-source for RES technology development, start the third industrial revolution? Renew. Sustain. Energy Rev. 57, 1194–1209. doi:10.1016/j.rser.2015.12.152

Guo, L. L., Zhao, S., Song, Y. T., Tang, M. Q., and Li, H. J. (2022). Green finance, chemical fertilizer use and carbon emissions from agricultural production. Agriculture-Basel 12 (3), 313. doi:10.3390/agriculture12030313

Hall, B. H. (2002). The financing of research and development. Oxf. Rev. Econ. Pol. 18, 35–51. doi:10.1093/oxrep/18.1.35

Han, S., Zhang, Z., and Yang, S. (2022). Green finance and corporate green innovation: based on China’s green finance reform and innovation pilot policy. J. Environ. Public Health 2022, 1–12. doi:10.1155/2022/1833377

Hao, Y., and Wu, H. (2021). The role of internet development on energy intensity in China-Evidence from a spatial econometric analysis. Asian Econ. Lett. 1 (1), 1–6. doi:10.46557/001c.17194

Hong, M., Li, Z., and Drakeford, B. (2021). Do the green credit guidelines affect corporate green technology innovation? Empirical research from China. Int. J. Environ. Res. Public Health 18 (4), 1682. doi:10.3390/ijerph18041682

Hu, Y., and Zheng, J. Y. (2022). How does green credit affect carbon emissions in China? A theoretical analysis framework and empirical study. Environ. Sci. Pollut. Res. 29 (39), 59712–59726. doi:10.1007/s11356-022-20043-1

Huang, Y. M., Chen, C., Lei, L. J., and Zhang, Y. P. (2022). Impacts of green finance on green innovation: a spatial and nonlinear perspective. J. Clean. Prod. 365, 132548. doi:10.1016/j.jclepro.2022.132548

Ibrahim, R. L., and Ajide, K. B. (2021). The dynamic heterogeneous impacts of nonrenewable energy, trade openness, total natural resource rents, financial development and regulatory quality on environmental quality: evidence from BRICS economies. Resour. Pol. 74, 102251. doi:10.1016/j.resourpol.2021.102251

International Finance Corporation, I. F. C. (2016). Green finance: a bottom-up approach to track existing flows. Washington, D.C: IFC.

Jalil, A., and Feridun, M. (2011). The impact of growth, energy and financial development on the environment in China: a cointegration analysis. Energy Econ. 33, 284–291. doi:10.1016/j.eneco.2010.10.003

Jeucken, M. (2001). Sustainable finance and banking: the financial sector and the future of the planet. London: Routledge.

Ji, Q., and Zhang, D. (2019). How much does financial development contribute to renewable energy growth and upgrading of energy structure in China? Energy Pol. 128, 114–124. doi:10.1016/j.enpol.2018.12.047

Jia, Z., Wen, S., and Sun, Z. (2022). Current relationship between coal consumption and the economic development and China’s future carbon mitigation policies. Energy Pol. 162, 112812. doi:10.1016/j.enpol.2022.112812

Jin, H., Yu, L. H., and Xu, Y. (2022). Green finance innovation policy and enterprise productivity difference: evidence from Chinese listed companies. Econ. Rev. 5, 83–99. doi:10.19361/j.er.2022.05.06

Jin, Y., Gao, X., and Wang, M. (2021). The financing efficiency of listed energy conservation and environmental protection firms: evidence and implications for green finance in China. Energy Pol. 153, 112254. doi:10.1016/j.enpol.2021.112254

Khan, A. Q., Saleem, N., and Fatima, S. T. (2018). Financial development, income inequality, and CO2 emissions in Asian countries using STIRPAT model. Environ. Sci. Pollut. Control Ser. 25 (7), 6308–6319. doi:10.1007/s11356-017-0719-2

Khan, S., Peng, Z., and Li, Y. (2019). Energy consumption, environmental degradation, economic growth and financial development in globe: dynamic simultaneous equations pan el analysis. Energy Rep. 5 (3), 1089–1102. doi:10.1016/j.egyr.2019.08.004

Koch, T., and Windsperger, J. (2017). Seeing through the network: competitive advantage in the digital economy. J. Organ Dysfunct. 6, 6–30. doi:10.1186/s41469-017-0016-z

Koengkan, M., Fuinhas, J. A., and Marques, A. C. (2018). Does financial openness increase environmental degradation? Fresh evidence from MERCOSUR countries. Environ. Sci. Pollut. Res. 25, 30508–30516. doi:10.1007/s11356-018-3057-0

Koengkan, M., Fuinhas, J. A., and Vieira, I. (2020). Effects of financial openness on renewable energy investments expansion in Latin American countries. J. Sus. Financ. Inves 10 (1), 65–82. doi:10.1080/20430795.2019.1665379

Koengkan, M., Santiago, R., Fuinhas, J. A., and Marques, A. C. (2019). Does financial openness cause the intensification of environmental degradation? New evidence from Latin American and Caribbean countries. Environ. Econ. Policy Stud. 21, 507–532. doi:10.1007/s10018-019-00240-y

Lange, S., Pohl, J., and Santarius, S. (2020). Digitalization and energy consumption. Does ICT reduce energy demand? Ecol. Econ. 176, 106760–106773. doi:10.1016/j.ecolecon.2020.106760

Lee, C. C., and Lee, C. C. (2022). How does green finance affect green total factor productivity? Evidence from China. Energy Econ. 107, 105863. doi:10.1016/j.eneco.2022.105863

Li, W., Fan, J., and Zhao, J. (2022a). Has green finance facilitated China’s low-carbon economic transition? Environ. Sci. Pollut. Control Ser. 29 (38), 57502–57515. doi:10.1007/s11356-022-19891-8

Li, W., Lin, X., Wang, H., and Wang, S. (2022b). High-quality economic development, green credit and carbon emissions. Front. Environ. Sci. 10, 992518. doi:10.3389/fenvs.2022.992518

Lin, B. Q., and Ma, R. Y. (2022). How does digital finance influence green technology innovation in China? Evidence from the financing constraints perspective. J. Environ. Manag. 320, 115833. doi:10.1016/j.jenvman.2022.115833

Lin, J., Yu, Z., Wei, Y. D., and Wang, M. (2017). Internet access, spillover and regional development in China. Sustainability 9 (6), 946. doi:10.3390/su9060946

Liu, Y., Lei, J., and Zhang, Y. (2021). A study on the sustainable relationship among the green finance, environment regulation and green-total-factor productivity in China. Sustainability 13 (21), 11926. doi:10.3390/su132111926

Liu, Y., Yang, Y., Li, H., and Zhong, K. (2022). Digital economy development, industrial structure upgrading and green total factor productivity: empirical evidence from China’s cities. Int. J. Environ. Res. Publ. Health 19 (4), 2414. doi:10.3390/ijerph19042414

Lu, J., Yan, Y., and Wang, T. X. (2021). The microeconomic effects of green credit policy—from the perspective of technological innovation and resource reallocation. China Ind. Econ. 01, 174–192. doi:10.19581/j.cnki.ciejournal.2021.01.010

Luo, S., Yimamu, N., Li, Y., Wu, H., Irfan, M., and Hao, Y. (2023). Digitalization and sustainable development: how could digital economy development improve green innovation in China? Bus. Strategy Environ. 32 (4), 1847–1871. doi:10.1002/bse.3223

Ma, D., and Zhu, Q. (2022). Innovation in emerging economies: research on the digital economy driving high-quality green development. J. Bus. Res. 145, 801–813. doi:10.1016/j.jbusres.2022.03.041

Ma, Q., Tariq, M., Mahmood, H., and Khan, Z. (2022b). The nexus between digital economy and carbon dioxide emissions in China: the moderating role of investments in research and development. Technol. Soc. 68, 101910. doi:10.1016/j.techsoc.2022.101910

Mamun, M. A., Boubaker, S., and Nguyen, D. K. (2022). Green finance and decarbonization: evidence from around the world. Finance Res. Lett. 46 (46), 102807. doi:10.1016/j.frl.2022.102807

Marcel, M., and Stefanie, K. (2020). Structural change and digitalization in developing countries: conceptually linking the two transformations. Technol. Soc. 63, 101428. doi:10.1016/j.techsoc.2020.101428

Meo, M. S., and Abd Karim, M. Z. (2021). The role of green finance in reducing CO2 emissions: an empirical analysis. Borsa istanb. Rev. 22, 169–178. doi:10.1016/j.bir.2021.03.002

Mirza, N., Umar, M., Afzal, A., and Firdousi, S. F. (2023). The role of fintech in promoting green finance, and profitability: evidence from the banking sector in the euro zone. Econ. Anal. Policy 78, 33–40. doi:10.1016/j.eap.2023.02.001

Murthy, K. V., Kalsie, A., and Shankar, R. (2021). Digital economy in a global perspective: is there a digital divide? Transnatl. Corp. Rev. 13 (1), 1–15. doi:10.1080/19186444.2020.1871257

Pan, W., Gulzar, M. A., Wang, Z., and Guo, C. (2022a). Spatial distribution and regional difference of environmental efficiency based on carbon reduction goals: evidence from China. Front. Environ. 647, 816071. doi:10.3389/fenvs.2021.816071

Pan, W., Xie, T., Wang, Z., and Ma, L. (2022b). Digital economy: an innovation driver for total factor productivity. J. Bus. Res. 139, 303–311. doi:10.1016/j.jbusres.2021.09.061

Peng, Z., and Dan, T. (2023). Digital dividend or digital divide? Digital economy and urban-rural income inequality in China. Telecommun. Policy 47, 102616. doi:10.1016/j.telpol.2023.102616

Pretis, F., and Roser, M. (2017). Carbon dioxide emission-intensity in climate projections comparing the observational record to socio-economic scenarios. Energy 135 (10), 718–725. doi:10.1016/j.energy.2017.06.119

Qin, J., and Cao, J. (2022). Carbon emission reduction effects of green credit policies: empirical evidence from China. Front. Environ. Sci. 10 (23), 1 76–185. doi:10.3389/fenvs.2022.798072

Ran, Q., Yang, X., Yan, H., Xu, Y., and Cao, J. (2023). Natural resource consumption and industrial green transformation: does the digital economy matter? Resour. Policy 81, 103396. doi:10.1016/j.resourpol.2023.103396

Ren, S., Hao, Y., and Wu, H. (2023). Digitalization and environment governance: does internet development reduce environmental pollution? J. Environ. Plann. Manag. 66 (7), 1533–1562. doi:10.1080/09640568.2022.2033959

Ren, S., Hao, Y., Xu, L., Wu, H., and Ba, N. (2021). Digitalization and energy: how does internet development affect China's energy consumption? Energy Econ. 98, 105220. doi:10.1016/j.eneco.2021.105220