94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 28 May 2024

Sec. Environmental Economics and Management

Volume 12 - 2024 | https://doi.org/10.3389/fenvs.2024.1332748

Lili Lyu

Lili Lyu Fang Xiao*

Fang Xiao*Climate change has become a critical global issue and challenge, with significant implications for financial enterprises as an integral part of economic activities. A thorough analysis of the impact of climate change on the high-quality development of financial enterprises is of great importance for financial sustainability. This paper first conducts an in-depth mathematical analysis of the intrinsic mechanisms through which climate change affects the high-quality development of financial enterprises by establishing a game theory model. Secondly, using data from listed companies for the years 2000–2020, an econometric model is constructed to empirically examine the relationship between climate change and the high-quality development of financial enterprises. The research findings demonstrate that climate change significantly inhibits the high-quality development of financial enterprises, as evidenced by robust results obtained through various methods such as data truncation, variable substitution, and changes in sample periods. Furthermore, this study addresses the endogeneity of the regression model using propensity score matching (PSM), instrumental variable methods, and system generalized method of moments (GMM). Additionally, climate change impacts the high-quality development of financial enterprises through technological innovation. Given the backdrop of climate change, understanding the relationship and logic between climate change and the high-quality development of financial enterprises and discerning the channels and mechanisms through which climate change affects their development are crucial. This research provides a new perspective and expands the research frontier on the high-quality development of financial enterprises, enriching the theoretical foundations in this field.

In recent years, climate change has emerged as a critical global problem (Atsu and Adams, 2021), with anthropogenic greenhouse gas emissions as the foremost driving factor behind it (Pottier et al., 2021). The issues arising from climate change have significantly impacted human livelihoods and production.

Climate change affects various aspects of human life. The continuous fluctuation of temperature has adverse effects on per capita output. However, without climate mitigation policies, a yearly increase of 0.04°C in global average temperature is projected to reduce per capita GDP by over 7% by 2100 (Engelhardt et al., 2019). Furthermore, climate change is also associated with increased mortality rates (Lupi and Marsiglio, 2021). It significantly impacts agricultural production and poses significant challenges to the industrial sector, while the service sector may benefit from climate change (Olper et al., 2021; Weerasekara et al., 2021). Moreover, the impacts of climate change on agricultural production vary across countries, with developing countries experiencing more severe effects than developed countries (Newell et al., 2021).

The high-quality development of enterprises is a micro-dynamic source of high-quality economic development. Based on the state and process of enterprise development, high-quality development of enterprises can be roughly divided into two parts: state-based high-quality development and process-based high-quality development. Regarding state-based high-quality development, enterprises transform from a low-level, mediocre state to a high-level, and excellent state. In process-based high-quality development, enterprises transform from extensive development focusing on scale expansion to intensive development focusing on quality improvement (Huang et al., 2018). Similarly, the high-quality development of financial enterprises encompasses state- and process-based dimensions. Depending on the economic and social development stage, financial enterprises achieve sustainable growth in asset size and profits by innovating products and services, enhancing social responsibility awareness, simplifying internal management processes, and strengthening risk control capabilities.

Scholars mainly focus on the macro and theoretical aspects of high-quality development in the financial sector. At the macro level, to explore the status of high-quality development in China’s financial industry, some researchers have constructed an indicator system from financial input and output perspectives. They have utilized the SBM-DEA model to calculate the level of high-quality development in China’s financial industry. The results indicate that China’s financial industry is generally experiencing a positive trend in high-quality development, but there are significant regional disparities (Gao et al., 2020; Yin, 2022; Zhang and Zhang, 2022). The above research only provides a macro-level measurement of the high-quality development of China’s financial industry. It does not provide an in-depth analysis of the internal logic affecting such development or conduct empirical testing. While macro-level measurements can provide strategic guidance for governments and enterprises, conducting thorough analysis and empirical testing is still essential. The internal logic affecting the high-quality development of the financial industry is complex. It involves multiple factors, including policy environment, market mechanisms, and technological innovation, requiring comprehensive analysis and research of all factors.

Moreover, empirical testing is essential to validate the accuracy and reliability of macro-level measurements. This requires collecting and analyzing large amounts of data, as well as systematic research and evaluation. Only in this way can we better understand the internal characteristics and patterns affecting the high-quality development of the financial industry in China and provide more robust support for the long-term development of China’s financial sector. More research articles must explore the high-quality development of financial enterprises at the micro level. Financial enterprises, as crucial vehicles and actual operators in risk management, capital trading, and investment consulting, play an essential role in economic and social development. Therefore, conducting an in-depth analysis of the high-quality development of financial enterprises holds significant importance.

How will climate change affect the high-quality development of the financial industry? Climate change itself can influence financial stability (Wang and Song, 2020; Pagnottoni et al., 2022), with the core mechanism being “uncertainty-mispricing-financial instability” (Yin, 2022). Extreme climate events can exacerbate systemic risks in the financial system (Gao et al., 2022a; Curcio et al., 2023; Ma and Song, 2023; Mao et al., 2023). These risks can generally be categorized into physical, liability, and transition risks, each with different transmission mechanisms (Carney, 2015). Furthermore, news related to climate change can also impact financial markets. However, the effects vary across countries, with climate change news having a relatively minimal impact on the Chinese financial market compared to the United States. Additionally, climate policy uncertainty can lead to market volatility (Raza et al., 2024).

Climate change affects the global economy and has wide-ranging implications for the financial industry. Researching the relationship between climate change and financial enterprises can help in several ways. Firstly, it can assist financial enterprises in better identifying and managing climate change risks, providing more accurate information for investment decision-making and enabling them to respond to the challenges posed by climate change effectively. Secondly, financial enterprises can contribute to addressing climate change issues by innovating financial products and redirecting investment towards sustainable solutions. Understanding the impacts of climate change on the financial industry is crucial for developing strategies that promote high-quality development while addressing environmental concerns. By integrating climate-related considerations into financial operations, such as risk assessment, product development, and investment planning, financial enterprises can enhance their resilience and create opportunities for sustainable growth.

Additionally, by offering financial products that support climate mitigation and adaptation efforts, such as green bonds, carbon offset instruments, and renewable energy financing, financial enterprises can play a vital role in mobilizing finance towards a low-carbon and climate-resilient future. In conclusion, studying the relationship between climate change and financial enterprises facilitates the identification and management of climate risks, enables more informed investment decisions, and enhances the ability of financial institutions to contribute to climate change mitigation and adaptation efforts. This research contributes to the sustainable development of the financial industry and the global economy. An analysis of the above literature reveals several areas for improvement in existing studies on the impact of climate change on finance. Firstly, more research needs to analyze climate change’s impact on financial enterprises. Secondly, existing studies mainly rely on empirical analysis rather than mathematical modeling to assess the impact of climate change on the financial industry. Compared to the existing research, this paper makes the following marginal contributions.

(1) Against the backdrop of climate change, this paper aims to clarify the intrinsic logic of how climate change impacts the high-quality development of financial enterprises and elucidate the channels and mechanisms through which climate change affects the high-quality development of financial enterprises.

(2) Compared to the current dominance of empirical analysis in existing studies, this paper first conducts an in-depth mathematical analysis of the intrinsic logic of how climate change impacts the high-quality development of financial enterprises by establishing a game theory model. Secondly, an econometric model is constructed to empirically test the relationship between climate change and the high-quality development of financial enterprises.

The remaining structure of this paper is as follows: Part II establishes a game theory model to conduct a mathematical analysis of the intrinsic logic of how climate change impacts the high-quality development of financial enterprises, leading to the formulation of the core hypothesis of this paper. Part III establishes an econometric model to examine the relationship between climate change and the high-quality development of financial enterprises. Part IV involves mechanism analysis, where an intermediary mechanism model is constructed to test the channels through which climate change affects the high-quality development of financial enterprises. Part V concludes and discusses the findings.

An in-depth analysis of the underlying mechanisms by which climate change affects financial enterprises is beneficial for strengthening climate risk management and adjusting future investment directions. Furthermore, financial enterprises need to consider the impact of climate change on their long-term strategies to develop effective response strategies and plans for sustainable development. This study employs a game-theoretic model to provide an in-depth analysis of the underlying mechanisms through which climate change influences the development of financial enterprises. The detailed analysis is presented in the following sections.

Hypothesis 1:. Financial enterprises invest significant human, material, and financial resources to address climate change, such as developing innovative financial products and identifying climate risks. Additionally, financial enterprises can guide and support clients to invest in low-carbon economy, renewable energy, and other environmentally friendly sectors, thus fostering sustainable socio-economic development. Let

Hypothesis 2:. As the level of effort exerted by financial enterprises and the government to address climate change increases, their costs also increase. Let

Hypothesis 3:. Financial assets are essential indicators of the high-quality development of financial enterprises. The size of financial assets is related to the level of effort exerted by financial enterprises and the government. For example, financial enterprises can enhance their efficiency by diversifying their financial products and services and improving their operational management. Research has shown that improving efficiency in financial enterprises significantly increases their asset size (Li et al., 2019). In addition, financial enterprises can also improve the efficiency and effectiveness of non-performing asset disposal and mitigate the risks faced by their asset portfolios through the securitization of non-performing assets. The reduction of non-performing assets indirectly indicates an increase in the assets of financial enterprises (Dai and Guo, 2016). The government can influence the asset size of financial enterprises through monetary policy. Specifically, monetary policy impacts the prices of financial assets, especially stock prices. When investment increases and leads to a rise in commodity and labor prices, expansionary monetary policy in the long term increases both the general price level of goods and the prices of stocks (Yi and Wang, 2002). However, climate change can lead to the loss of financial assets. Let us assume that financial assets satisfy the following differential Eq. 1.

Let

Hypothesis 4:. The increase in financial assets brings significant benefits to society, which not only refers to economic gains but also includes reputation and goodwill benefits. The increase in financial assets indicates a favorable state of financial market development. A well-developed financial market not only increases employment but also raises the income of those employed (Sun and Chai, 2023; Lin et al., 2019). On the other hand, it can also indicate strengthened regulation of the financial market. Research has shown that by bringing shadow banking under regulation it not only reduces the overall volatility of macroeconomic and financial variables but also significantly enhances the welfare level of society (Ma and Lv, 2022). Let’s assume this welfare is defined as follows Eq. 2:

Hypothesis 5:. The coefficients for the allocation of social welfare by financial institutions and governments are denoted as

This paper establishes a cooperative game model based on the assumptions mentioned above, with the specific objective function given by Equation 3.

This paper, the

To solve Equation 4, it is necessary to construct a continuously bounded differentiable function

According to Equation 5, the Hessian matrix of the

Substituting the above equations for the optimal effort levels of financial institutions and governments into the

According to Equation 8, the

By substituting the above two equations into Eqs 6, 7, the optimal effort levels of financial institutions and governments can be calculated, as expressed in Eqs 11, 12 respectively.

By substituting the optimal effort levels of financial institutions and governments into the financial asset stock equation, and based on the initial condition

In Equation 13,

By substituting the optimal effort levels of financial institutions and governments into

The partial derivative of the overall optimal revenue of financial institutions and governments with respect to climate change can be obtained, i.e.,

The above conclusion is derived from the analysis based on mathematical models. The following analysis focuses on the theoretical aspects of the relationship between climate change and the high-quality development of financial enterprises. The impact of climate change on financial enterprises can be broadly classified into several categories. Firstly, climate change leads to systemic risks for financial enterprises. Scholars have utilized data from 16 listed commercial banks in China to examine the impact of climate change on systemic risk in the banking sector. The results indicate that climate change significantly increases systemic risk overflow in banks. Moreover, compared to state-owned commercial banks, climate change poses a greater systemic risk to non-state-owned commercial banks (Chabot and Bertrand, 2023; Wu et al., 2023). The systemic risks arising from climate change manifest as increased debt, liquidity, and exchange rate risks (Gao et al., 2022b).

Secondly, climate change leads to asset devaluation for financial enterprises. Due to the impact of climate change, energy-intensive industries, carbon-intensive industries, and infrastructure sectors will face low-carbon and green transformations, which will undoubtedly result in the reassessment of asset values in these sectors, thereby affecting financial stability (Ploeg and Rezai, 2020; Roncoroni et al., 2021). Furthermore, as the low-carbon and green transformations progress, bank risks increasingly depend on the new energy industry compared to traditional energy industries (Zhang et al., 2022). In addition, the risks of climate change have a significant negative impact on bank stocks (Boungou and Urom, 2023).

Thirdly, climate change affects the balance sheets of financial enterprises. Climate change impacts the value of assets for businesses and households, thereby influencing insurance companies’ balance sheets. If insurance companies underestimate the extent of physical losses caused by climate change, it can lead to insolvency (Batten, 2018). The deterioration of insurance company balance sheets can further reduce the supply of related insurance services and products. Insurers in distress may engage in large-scale asset sell-offs, causing a decline in asset prices (Von Peter et al., 2018). Whether climate change leads to systemic risks for financial enterprises, asset depreciation, or impacts on balance sheets, it indicates that climate change will, to some extent, restrain the high-quality development of financial enterprises. Based on the analysis of the mathematical model and theoretical analysis mentioned above, this article presents the core research Hypothesis 1.

Hypothesis 1:. There is a negative correlation between climate change and the high-quality development of financial enterprises.

In general, climate change has two main types of impacts on financial enterprises. The first is the physical impact of climate change on financial enterprises, which refers to the direct effects of climate change itself, such as the impact of extreme weather events, on financial enterprises. The second is the impact of climate policy uncertainty on financial enterprises. This refers to the effects of volatile climate policies on financial enterprises.

In terms of the direct impact of climate change on financial enterprises, climate change shocks reduce output, lower capital prices and capital return rates, and increase corporate leverage and credit default rates, thereby triggering credit tightening (Zhang et al., 2023). Due to the decrease in capital prices and capital return rates caused by climate change, the profitability of financial enterprises decreases, leading to a corresponding reduction in their expenditure on research and development. Moreover, financial enterprises will conduct climate risk assessments to measure how much their assets are exposed to climate-related risks and adopt corresponding asset allocation strategies to address climate change. However, research has shown that corporate financial asset allocation is mainly characterized by a “crowding-out” effect, significantly inhibiting green technological innovation. This inhibition is primarily achieved through reducing corporate performance and increasing corporate risk exposure (Chen and Yang, 2022). Due to the characteristics of financial enterprises, the proportion of financial assets is much more significant than that of physical assets. Therefore, the impact of financial asset allocation by financial enterprises on technological innovation is far more significant than that of non-financial enterprises.

Furthermore, financial enterprises respond to climate change by innovating financial products, such as using green bonds, sustainable bonds, and climate derivatives, to guide the flow of social capital towards climate change mitigation. Research has shown that financialization significantly inhibits different types of technological innovation in enterprises, with a powerful impact on breakthrough innovations (Zhao and Cao, 2021). Due to the higher level of financialization in financial enterprises compared to non-financial enterprises, the inhibiting effect of financialization on technological innovation is much more significant for financial enterprises.

Regarding the impact of uncertain climate policies on financial enterprises, Chinese provincial governments have established energy-saving and emission-reduction targets to address climate change. Research has shown that government environmental targets inhibit green technological innovation in enterprises, primarily through reduced profits and increased fixed asset investments (Liu et al., 2022). In addition, scholars have used text analysis methods to construct the Media Perception Index of Climate Policy Uncertainty in China and studied the impact of climate policy uncertainty on green innovation in enterprises. The results indicate a negative effect of climate policy uncertainty on green innovation in enterprises (Guo and Yong, 2023).

Hypothesis 2:. Climate change will inhibit the high-quality development of financial enterprises through its impact on technological innovation.

This empirical study used temperature and listed company data, with a statistical scope from 2000–2020. Temperature and precipitation data were obtained from the annual “China Climate Statistical Yearbook,” while listed company data were obtained from the China Securities Market and Accounting Research (CSMAR) database. The temperature and precipitation data contained variables such as province, year, average temperature, and average precipitation. The listed company data contained various indicator variables. In this study, only data from financial enterprises were retained, and missing data were imputed using mean imputation. Additionally, data that did not comply with accounting standards, such as samples with negative operating income, were eliminated. Finally, with province and year variables as the vital matching variables, temperature data, and listed company data were merged. 920 samples were obtained after merging (excluding Hong Kong, Macao, and Taiwan regions).

The dependent variable: The variable of primary interest in this study is the high-quality development of financial institutions. Following the approach of Huo et al. (Xiao et al., 2020; Wang and Wang, 2022; Huo et al., 2023), we adopt the total factor productivity of financial institutions as a proxy variable for high-quality development. Companies with high total factor productivity tend to have advanced technological levels and innovation capabilities, enabling them to continuously introduce and apply new technologies and methods to improve production efficiency and product quality. Companies with solid innovation capabilities have a competitive advantage, as they can produce goods or provide services at lower costs and higher efficiency.

The core explanatory variable: This study primarily explores the impact of climate change on the high-quality development of financial institutions. Drawing from the approach of Liu et al. (Hong et al., 2016; Liu et al., 2023), we select the annual average temperature in different regions as a proxy variable for climate change. However, the annual average temperature can vary with latitude, topography, and slope changes, among other indicators. To ensure horizontal comparability of annual average temperature fluctuations between regions, we conduct dimensionless quantification of the annual average temperature. Typically, climate change can lead to extreme weather events (such as floods, droughts, hurricanes, etc.), exposing financial institutions to more significant risks and losses. For example, insurance companies may need to handle more natural disaster insurance claims; banks may face increased challenges in lending risks, and physical assets in investment portfolios (such as real estate) may also face devaluation risks.

Control variables: In empirical research, this study aims to control for other factors that may influence the high-quality development of financial institutions to analyze the impact of climate change on such development more accurately. Drawing from the approach of Wang et al. (Qi et al., 2018; Li and Xiao, 2020; Wang and Xia, 2023), the following variables are selected as control variables.

Age: Calculated as the difference between the sample observation year and the firm’s establishment year, then taking the natural logarithm of this difference. Size: Represented by taking the logarithm of the firm’s total assets. Growth: Calculated as the difference between the current period’s operating income and the operating income of the previous period, divided by the operating income of the period before the previous period. Equity: Assigned a value 1 for state-owned firms and 0 for all others. Leverage: Measured by the ratio of total liabilities to total firm assets. Performance: Measured by the ratio of net profit to the firm’s total assets. Mediating Variable: Climate may affect the high-quality development of financial companies through its impact on technological innovation. This study selects the number of patent applications by financial firms as a proxy variable for technological innovation to analyze the channels and mechanisms through which climate change influences the high-quality development of financial enterprises.

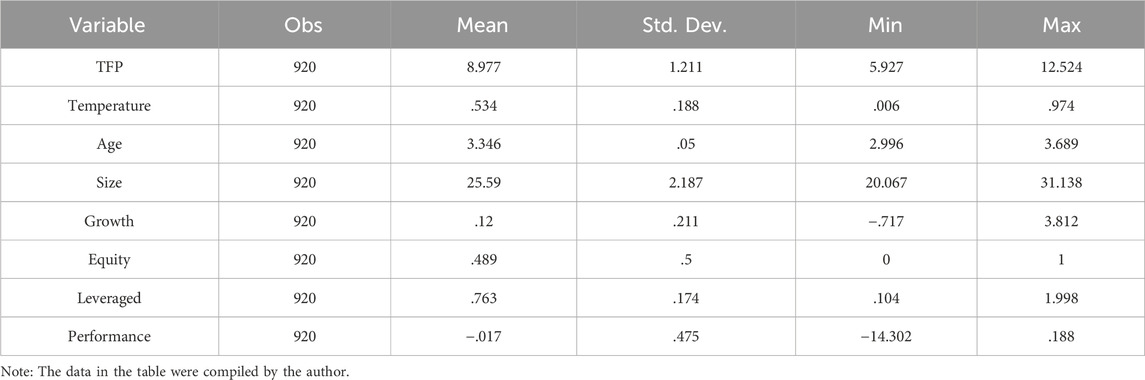

Table 1 presents the descriptive statistical analysis results of the variables above. Please refer to Table 1.

Table 1. Variable definitions.

This study employs panel data from 2000–2020, consisting of temperature data and data on listed company mergers, to test the hypotheses proposed in the theoretical analysis section empirically. In order to obtain more accurate estimates of the critical variables, this study adopts a panel data model with fixed effects in both dimensions. The specific model specification is as follows:

In Eq. 15, the subscripts

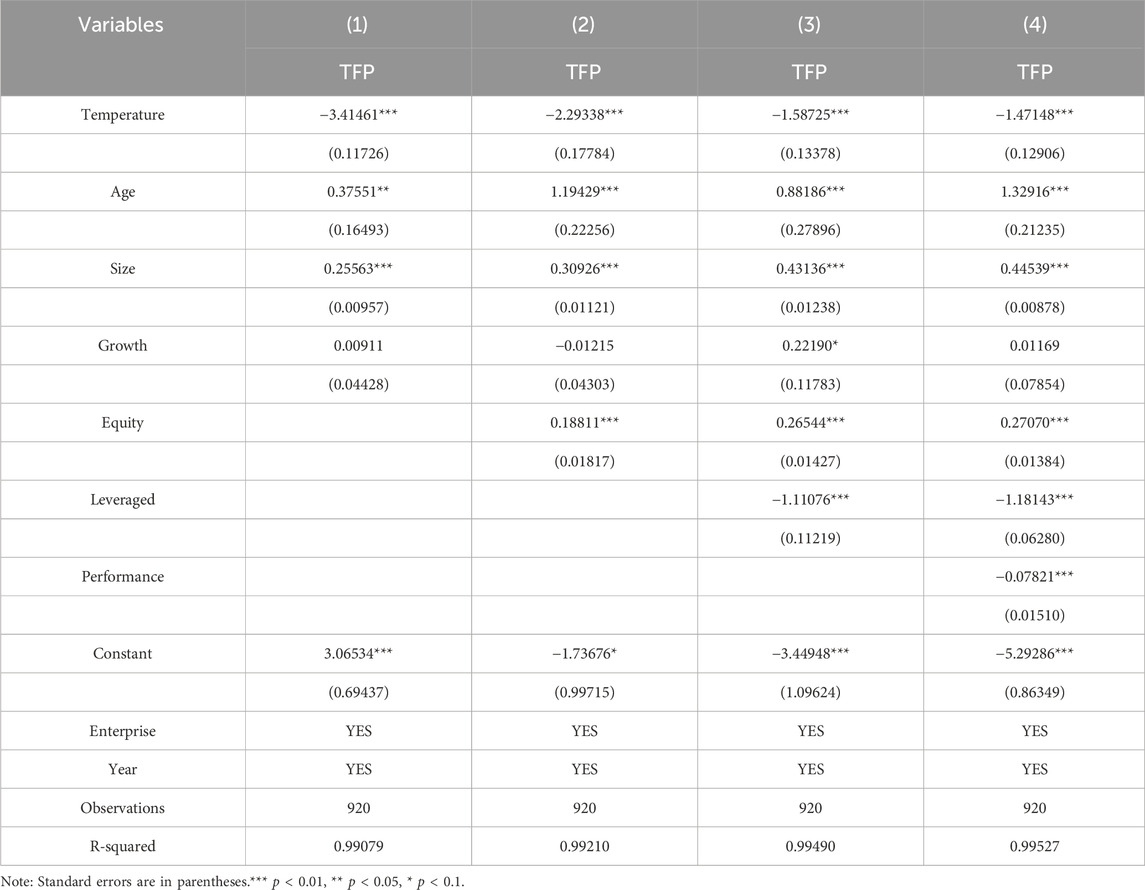

Table 2 presents the baseline regression results of climate change on the high-quality development of financial enterprises. Table 2 shows that climate change significantly inhibits the high-quality development of financial enterprises, thus providing strong support for Hypothesis 1. Columns (1) to (4) in Table 2 include control variables such as ownership nature, financial leverage, and historical performance. The regression results indicate that including control variables does not change the significance level and sign of the core explanatory variable. Climate change can significantly inhibit the high-quality development of financial enterprises, and there are several possible reasons for this. Firstly, extreme weather events and climate-related risks triggered by climate change may increase the risks faced by financial enterprises. For instance, natural disasters like floods, hurricanes, and droughts may lead to asset losses, loan default risks, and increased insurance claim risks for financial enterprises. These risks may hurt financial enterprises’ profitability and capital adequacy, thereby restraining their high-quality development. Secondly, climate change may result in asset devaluation and losses, particularly in industries and assets related to carbon emissions and fossil fuels. Tightening global regulations on carbon emissions may cause the transformation and depreciation of the energy industry, thereby influencing the credit and investment of financial enterprises in these industries. This could limit the development of financial enterprises in relevant sectors and affect their high-quality development. Thirdly, climate change may trigger capital flows and market volatility, increasing the uncertainty in financial markets. Market investors may adopt a cautious approach towards industries and companies related to climate change, leading to changes in capital allocation and fluctuations in market value. This may hurt the business and profitability of financial enterprises, thereby inhibiting their high-quality development. For detailed information, please refer to Table 2.

Table 2. Baseline regression results.

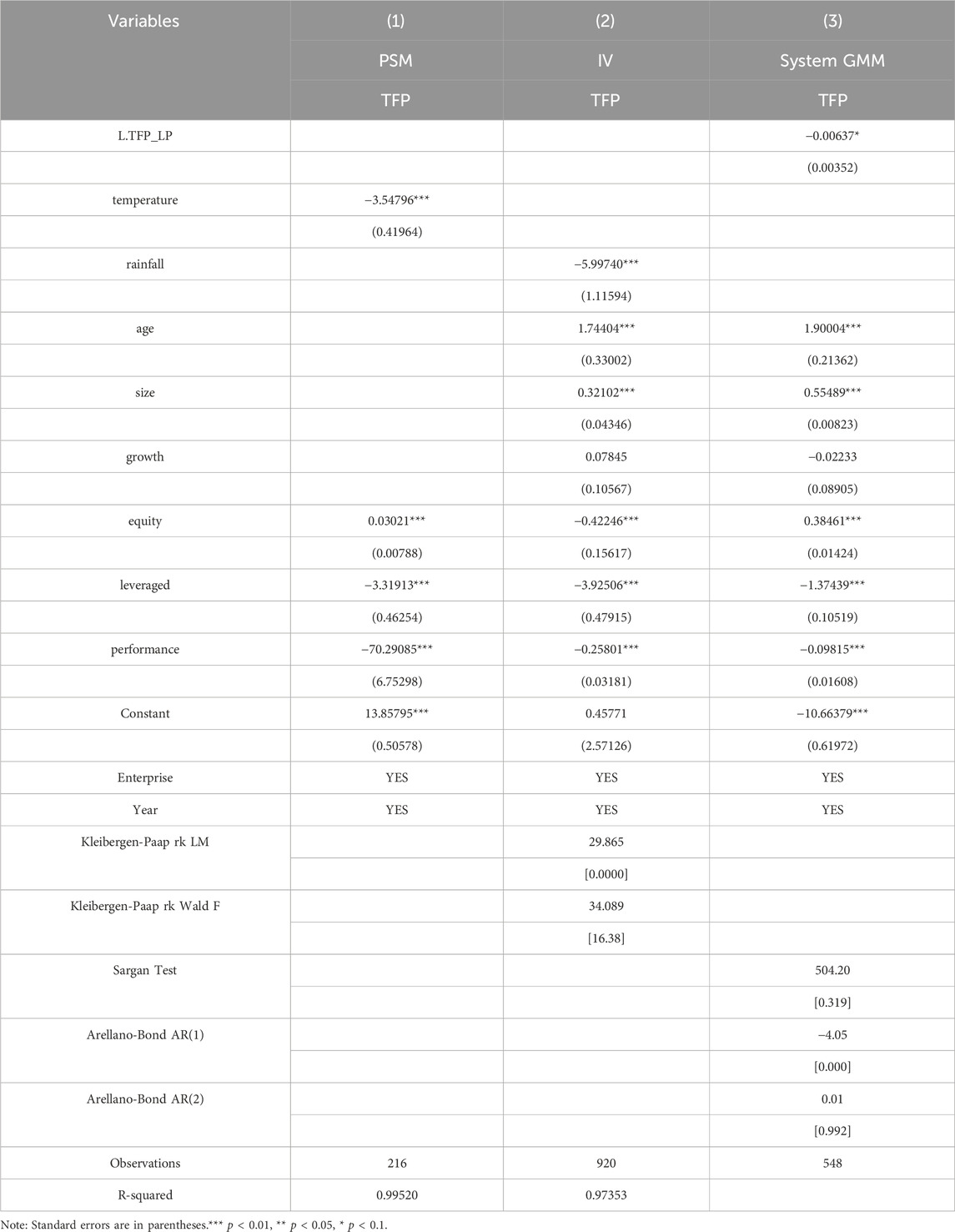

Due to measurement errors, endogeneity, omitted variables, and selection bias, the model suffers from endogeneity issues that cannot be avoided. To address this concern, this study employs three methods, namely PSM (Propensity Score Matching), instrumental variable approach, and System GMM, to handle endogeneity. The sample data is divided into two groups based on the mean value of the dependent variable. Then, variables such as firm age, firm size, and firm growth are used as matching variables, and the 1:1 nearest neighbor matching method is applied to match the samples. Finally, regression is conducted using the matched sample data and compared with the benchmark results. The regression results of the matched data are presented in column (1) of Table 3, which shows no significant difference from the benchmark regression results. In addition, the instrumental variable approach alleviates endogeneity caused by omitted variables. Specifically, the average annual rainfall is chosen as the instrumental variable. A correlation exists between average annual rainfall and average temperature, as higher-temperature regions generally tend to have more rainfall.

Table 3. Endogeneity handling.

Furthermore, average annual rainfall has no direct relationship with the high-quality development of financial enterprises. Therefore, the instrumental variable used in this study meets the criteria of relevance and exogeneity. The instrumental variable regression results are shown in column (2) of Table 3. The KP WaldF statistic is greater than 16.38, indicating the absence of weak instrumental variable problem. The results from the System GMM regression, presented in column (3) of Table 3, show no significant difference from the benchmark regression results. For detailed information, please refer to Table 3.

To ensure the robustness of the research findings, four methods were employed in this study for robustness tests. Firstly, data truncation was performed to replace values below the 1st percentile and above the 99th percentile with their respective critical values. The results of the truncated data are presented in column (1) of Table 4, which shows no significant differences from the baseline regression. Secondly, the estimation strategy was altered from using OLS to other methods. The OLS regression results are presented in column (2) of Table 4, which indicates no significant differences from the baseline regression. Thirdly, the dependent variable was changed from total factor productivity (TFP) estimated using the Levinsohn-Petrin (LP) method to TFP estimated using the Olley-Pakes (OP) method. The regression results with the OP method are presented in column (3) of Table 4, which shows no significant differences from the baseline regression. Lastly, the sample period was changed from 2000–2020 to 2010–2020. The regression results with the revised sample period are presented in column (4) of Table 4, indicating no significant differences from the baseline regression. These four methods demonstrate the robustness of the regression results in this study. For more details, please see Table 4.

Table 4. Robustness test.

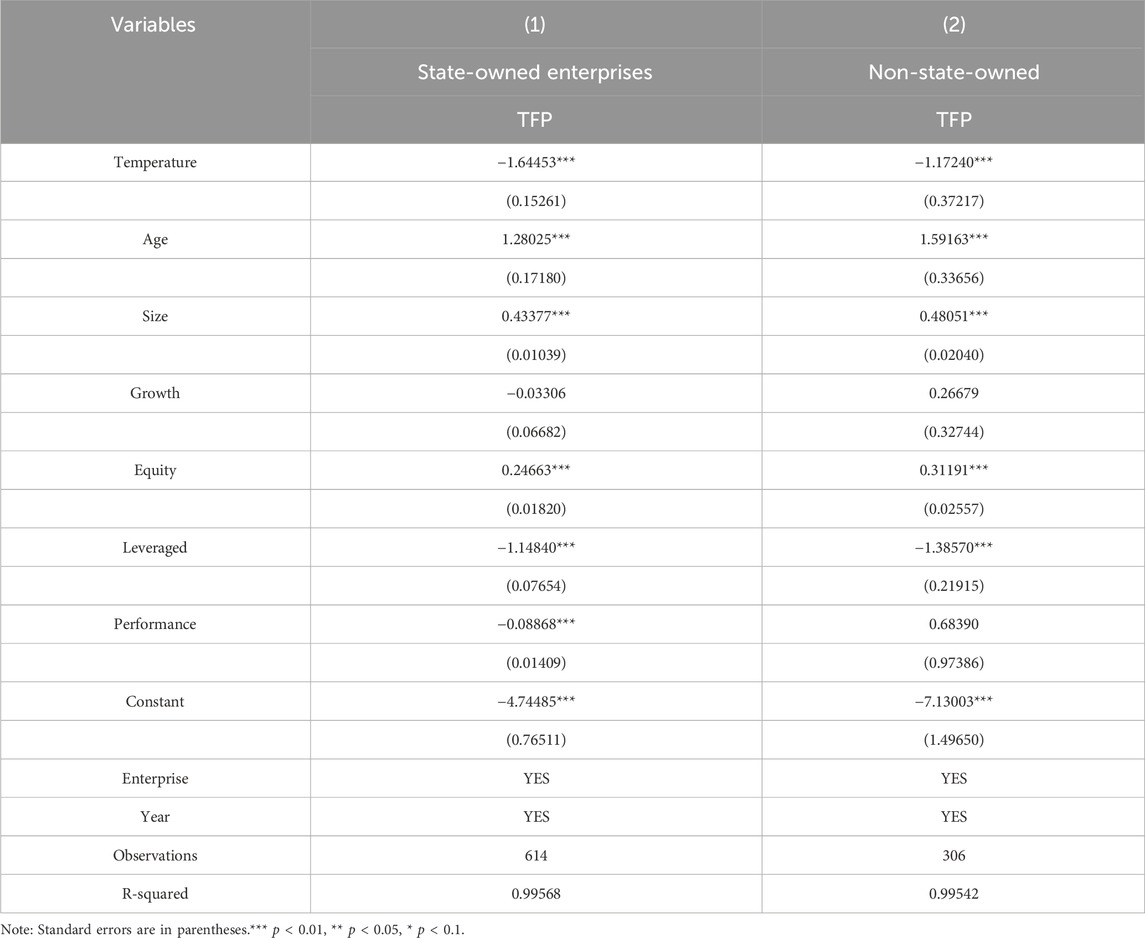

In this study, the regression analysis was conducted on the data based on corporate ownership. The regression results are presented in Table 5. The first column of Table 5 shows the impact of climate change on state-owned enterprises, while the second column shows the impact of climate change on enterprises with other types of ownership. According to the regression results of heterogeneity in corporate ownership presented in Table 5, there is no significant difference in the impact of climate change on state-owned enterprises and enterprises with other types of ownership. For more specific details, please refer to Table 5.

Table 5. Regression results of heterogeneity in corporate ownership.

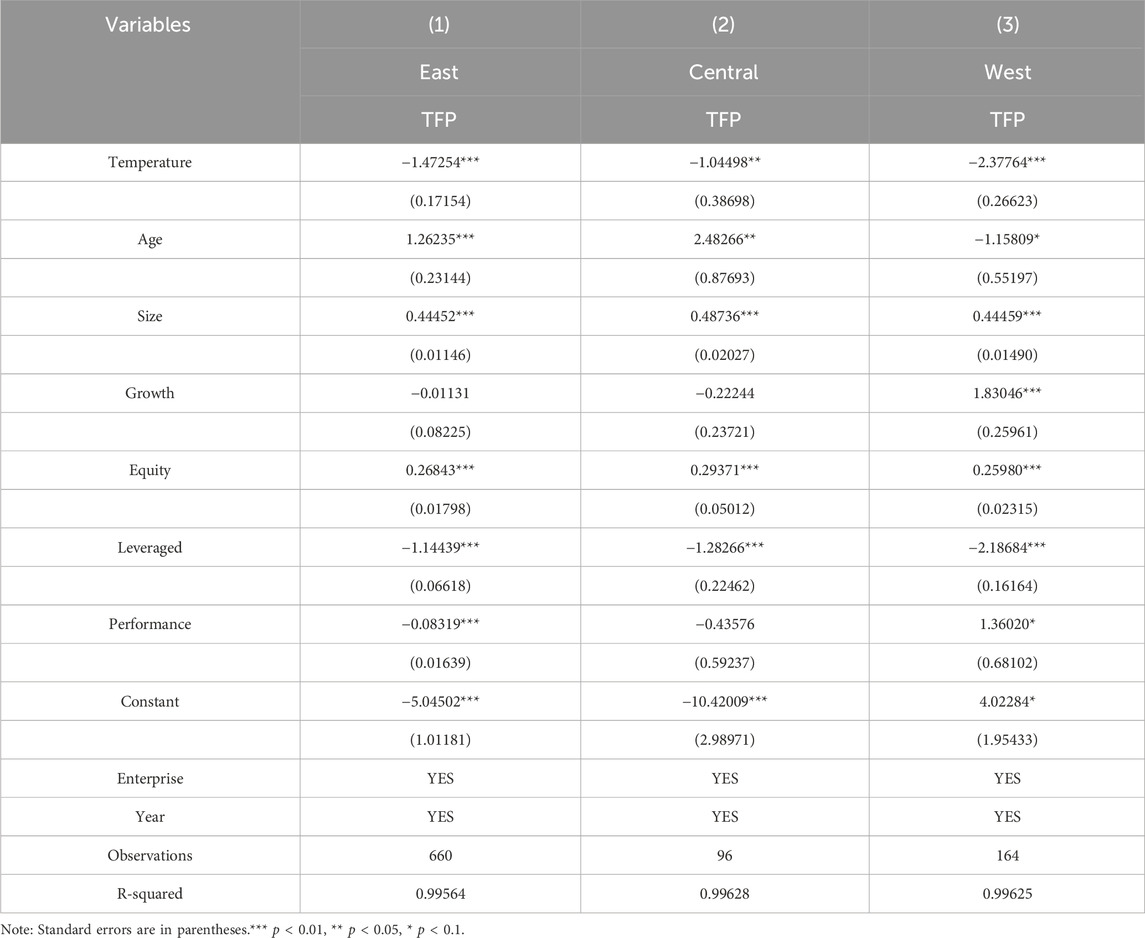

According to the National Bureau of Statistics classification criteria, the sample data in this study were divided into three regions: East, Central, and West. Regression analyses were conducted separately for each region; the results are presented in Table 6. The first column of Table 6 shows the regression results for the East region, while the second and third columns present the results for the Central and West regions, respectively. The regression results indicate that climate change has a greater impact on financial enterprises in the western region compared to the eastern and Central regions. There are several potential reasons for this finding. Firstly, financial enterprises in the West region face greater pressure regarding social responsibility and sustainable development. Due to the prominent environmental challenges in the West region, there are higher societal expectations for financial enterprises to take greater responsibility for environmental protection and climate change mitigation. Financial enterprises must actively respond to these social pressures by strengthening environmental governance and sustainable development practices to safeguard their reputation and risk management. Secondly, financial enterprises in the West region may face increased ecosystem risks. Climate change can lead to ecosystem degradation and biodiversity loss, adversely affecting financial enterprises’ investment portfolios and assets. For instance, financial enterprises investing in industries and regions highly vulnerable to climate change may face environmental risks and asset devaluation. For more specific details, please refer to Table 6.

Table 6. Regression results of regional heterogeneity.

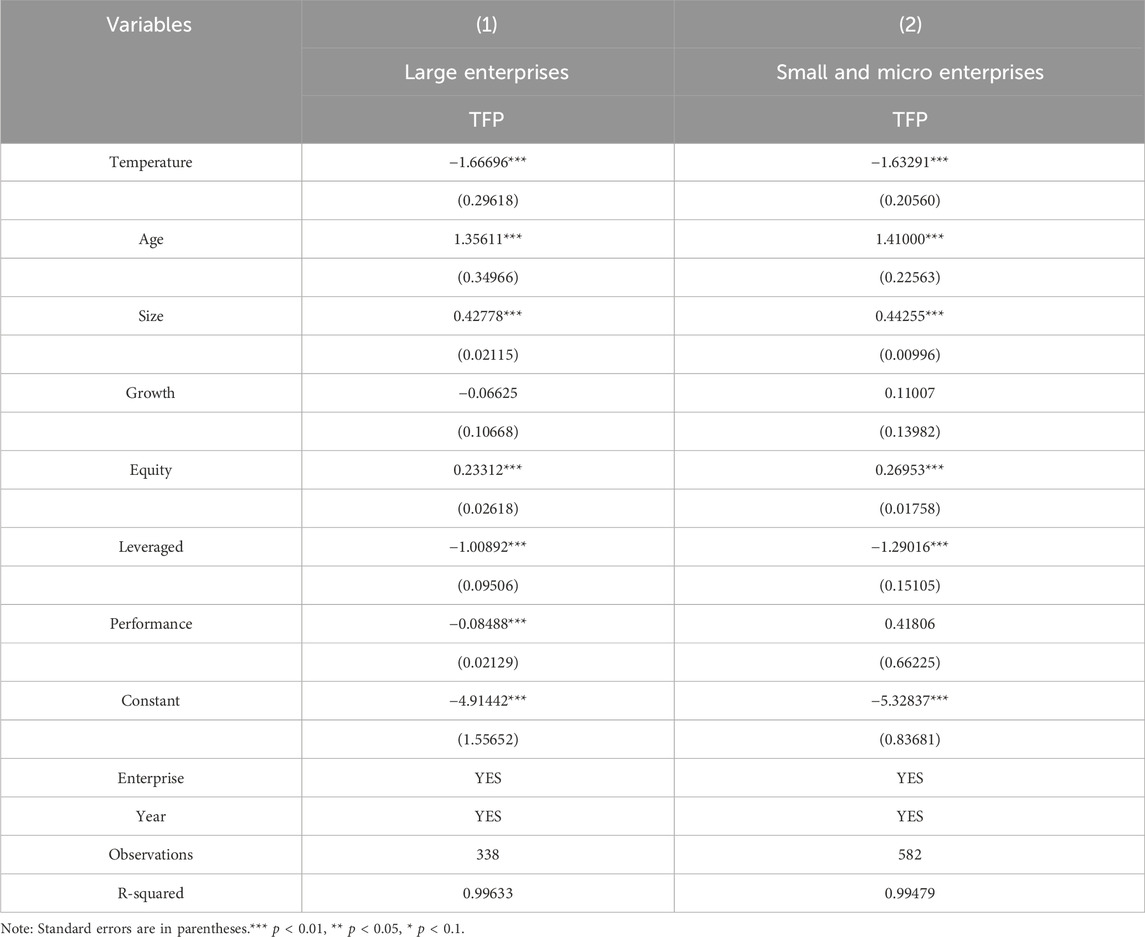

In this study, the enterprises were divided into two groups based on the average number of employees: those with more than the average were classified as large enterprises, while those with fewer employees were classified as small and micro enterprises. According to the regression results of firm size heterogeneity presented in Table 7, there is no significant difference in the impact of climate change on either large or small and micro enterprises. The specific results are shown in Table 7.

Table 7. Regression results of firm size heterogeneity.

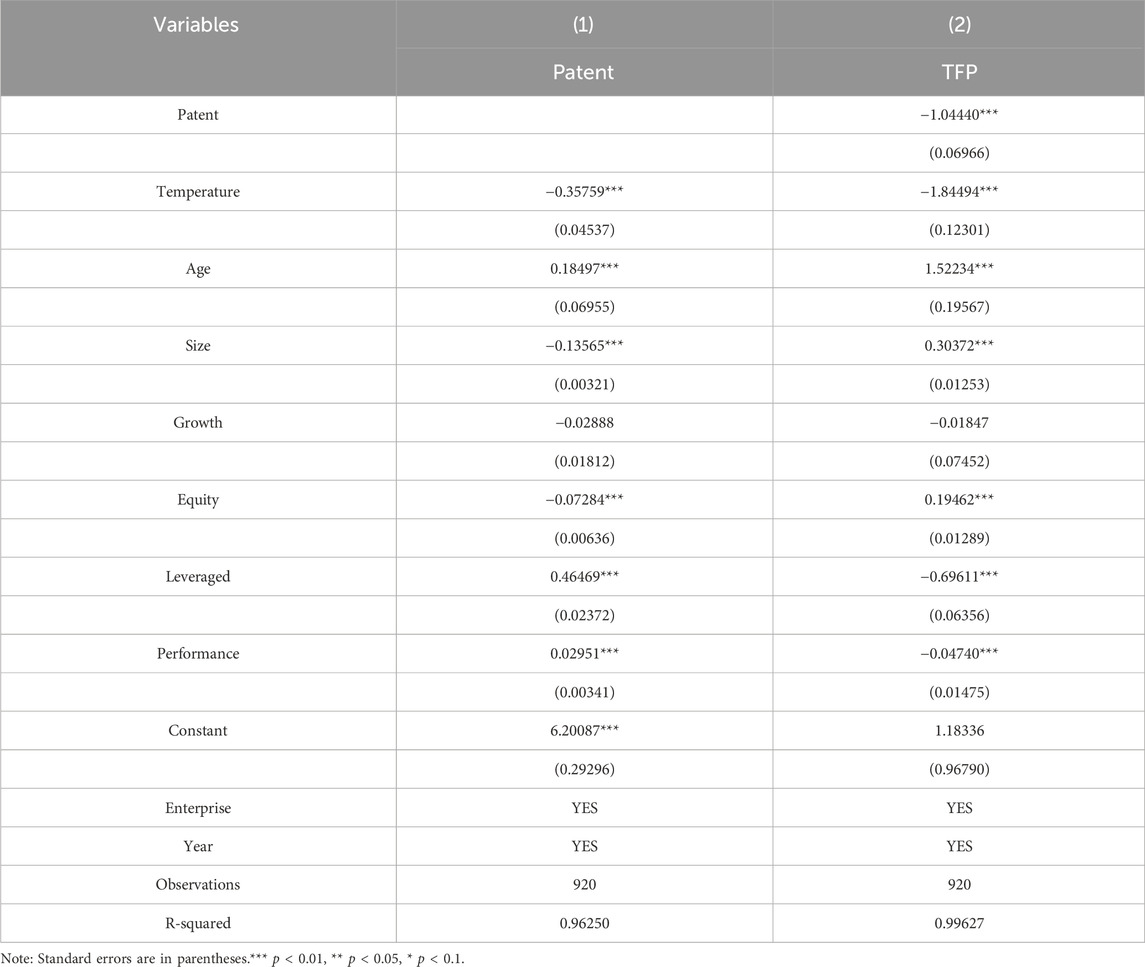

This section examines the channels and mechanisms through which climate change affects the high-quality development of financial enterprises. Theoretical analysis indicates that climate change can affect enterprise innovation and influence high-quality development. Using the number of patent applications as a proxy for technological innovation, this study constructs a mediation model to test the mechanism, as illustrated in Eqs 16, 17.

The regression results of the mechanism test are shown in Table 8. In the regression, variable

Table 8. Regression results of the mechanism.

In the context of climate change, it is crucial to study the relationship and logic between climate change and the high-quality development of financial enterprises and clarify the channels and mechanisms through which climate change affects the high-quality development of financial enterprises. This paper first establishes a game model to conduct a deep mathematical analysis of the internal mechanism of the impact of climate change on the high-quality development of financial enterprises. Secondly, based on the data of listed companies from 2000–2020, this study uses econometric models to empirically test the relationship between climate change and the high-quality development of financial enterprises. This research provides a new perspective on the high-quality development of financial enterprises. It expands the research margin of the high-quality development of financial enterprises, enriching the theory of the high-quality development of financial enterprises.

The research findings indicate that climate change significantly inhibits the high-quality development of financial enterprises. However, the impact of climate change on the high-quality development of financial enterprises does not vary with different ownership and company sizes. Considering the endogeneity issue of the model, this study addresses the endogeneity problem by applying the instrumental variable approach, propensity score matching (PSM) method, and the system GMM method. It partially overcomes the endogeneity issue. To examine the robustness of the regression results, this paper conducts robustness tests using four methods: data truncation, alternative estimation strategies, replacement of the dependent variable, and changes in the sample period. The results of the robustness tests show that regardless of which method is used, the coefficients and significance levels of the core explanatory variable remain unchanged, and the coefficients of other control variables are similar to the benchmark regression results. This indicates the robustness of the regression results in this study. This study establishes a mediation effect model to investigate the mediating effect of technological innovation. The regression results of the mediation effect model show that climate change affects the high-quality development of financial enterprises through its impact on technological innovation.

Based on the research findings, this paper puts forward the following policy recommendations: Firstly, financial enterprises should strengthen their assessment and management of climate change-related risks. This includes comprehensive identification and assessment of risks such as asset depreciation, fund flows and market fluctuations, and regulatory changes. Establishing a risk management framework and implementing relevant risk management measures, such as diversifying investment portfolios and insurance and reinsurance mechanisms, can help mitigate the impact of risks on enterprises. Secondly, financial enterprises can address the challenges of climate change by increasing investments in sustainable development and the low-carbon economy. Financial enterprises can promote sustainable development and obtain returns that align with environmental, social, and governance standards by directing funds towards projects in areas such as environmental technologies and energy, renewable energy, green buildings, and carbon emissions reduction. Thirdly, financial enterprises should enhance the disclosure and communication of climate-related information to increase transparency and trust. This includes disclosing climate-related risks and opportunities of enterprises and the measures and achievements taken.

Additionally, financial enterprises can participate in external standards and frameworks, such as the reporting requirements of TCFD (Task Force on Climate-related Financial Disclosures), to improve the industry’s overall disclosure level. Fourthly, financial enterprises can actively collaborate and advocate with multiple stakeholders to drive policy and regulatory reforms and innovations. By collaborating with other stakeholders such as governments, academia, non-governmental organizations, and social enterprises, financial enterprises can collectively promote sustainable development and actions to address climate change. Moreover, financial enterprises can advise and support policy formulation and implementation by participating in industry organizations and advocacy groups.

Although this paper conducts a thorough mathematical analysis of the internal mechanisms of climate change’s impact on the high-quality development of financial enterprises by establishing a game model and empirically tests the relationship between climate change and the high-quality development of financial enterprises through econometric models, there are still some limitations in this study. One of the limitations is that the spatial correlation of climate change needs to be taken into account. Specifically, climate change has a spatial correlation among geographically adjacent regions. Therefore, it would be valuable to incorporate the spatial correlation of climate change into the study and conduct further analysis in future research.

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding authors.

LL: Writing–original draft. FX: Writing–review and editing.

The author(s) declare financial support was received for the research, authorship, and/or publication of this article. This research was funded by open research project of CMA Key Open Laboratory of Transforming Climate Resources to Economy (No.2023013); 2022 Specialized Research Funding Projects of Institute for Development and Program Design of China Meteorological Administration (ZCYJ2022008); 2022 Soft Science Research Project of China Meteorological Administration (2022ZDIANXM23).

We extend our gratitude to Chunxiang Leng, Dan Yu, Yixi Fan, Ping Li, and Binbing Zhang from the Institute for Development and Programme Design, China Meteorological Administration, for their significant contributions and valuable feedback on earlier drafts of this paper.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Atsu, F., and Adams, S. (2021). Energy consumption, finance, and climate change: does policy uncertainty matter? Econ. Analysis Policy 70 (4), 490–501. doi:10.1016/j.eap.2021.03.013

Batten, S. (2018). Climate change and the macro-economy: a critical review. Social Science Electronic Publishing. Rochester, NY, USA.

Boungou, W., and Urom, C. (2023). Climate change-related risks and bank stock returns. Econ. Lett. 224, 111011. doi:10.2139/ssrn.4339882

Carney, M. (2015). Breaking the tragedy of the horizon - climate change and financial stability. England, UK: Bank of England.

Chabot, M., and Bertrand, J. (2023). Climate risks and financial stability: evidence from the European financial system. J. Financial Stab. 69, 101190. doi:10.1016/j.jfs.2023.101190

Chen, L., and Yang, J. (2022). Does corporate financial assets inhibit green technological innovation? J. Financial Dev. Res. (7), 15–23. doi:10.1088/0143-0807/27/4/00710.19647/j.cnki.37-1462/f.2022.07.002

Curcio, D., Gianfrancesco, I., and Vioto, D. (2023). Climate change and financial systemic risk: evidence from US banks and insurers. J. Financial Stab. 66, 101132. doi:10.1016/j.jfs.2023.101132

Dai, Y., and Guo, H. (2016). The actual demands and the constraining factors in commercial banks' non-performing asset securitization. Contemp. Econ. Manag. 38 (7), 79–83. doi:10.13253/j.cnki.ddjjgl.2016.07.013

Engelhardt, B. (2019). Long-term macroeconomic effects of climate change: a cross-country analysis. New York, NY, USA: Globalization Institute Working Papers.

Gao, R., Wang, Y., and Cao, T. (2022a). Climate change and macro-financial risk: international evidence. Nankai Econ. Stud. 3, 3–20.

Gao, R., Wang, Y., and Cao, T. (2022b). Climate change and macro-financial risk: international evidence. Nankai Econ. Stud. (3), 3–20. doi:10.14116/j.nkes.2022.03.001

Gao, Y., Xu, Y., Ji, C., and Zhong, Y. (2020). The measurement and characteristics of China's financial industry high-quality development. J. Quantitative Technol. Econ. 37 (10), 63–82. doi:10.13653/j.cnki.jqte.2020.10.004

Guo, J., and Yong, Z. (2023). Climate policy uncertainty and corporate green innovation: a measure based on the text analysis method of news Media. Finance Econ. (9), 75–86. doi:10.19622/j.cnki.cn36-1005/f.2023.09.007

Hong, H., Li, F. W., and Xu, J. (2016). Climate risks and market efficiency. Social Science Electronic Publishing. Rochester, NY, USA.

Huang, S., Xiao, H., and Wang, X. (2018). Study on high-quality development of the state-owned enterprises. China Ind. Econ. (10), 19–41. doi:10.19581/j.cnki.ciejournal.2018.10.002

Huo, C., Tian, W., and Pang, M. (2023). Anti-corruption and high-quality development of enterprises: an empirical study of A-share listed companies in Shanghai and shenzhen. J. Liaoning Univ. Soc. Sci. Ed. 51 (1), 31–45. doi:10.16197/j.cnki.lnupse.2023.01.017

Li, Q., and Xiao, Z. (2020). Heterogeneous environmental regulation tools and green innovation incentives: evidence from green patents of listed companies. Econ. Res. J. 55, 192–208.

Li, X., Tong, Y., and Zhu, Y. (2019). The effect of loan market competition on banking efficiency in the presence of risk-A study based on an unexpected-output-DEA model. East China Econ. Manag. 33 (01), 112–118. doi:10.19629/j.cnki.34-1014/f.180307009

Lin, C., Kang, K., and Sun, Y. (2019). Financial inclusion and employment increase: direct and spatial spillover effects. J. Guizhou Univ. Finance Econ. (3), 23–36.

Liu, B., Li, Y., and Jiang, Y. (2023). Climate changes and the total factor productivity of manufacturing enterprises:mechanism analysis and empirical tests. J. Hunan Univ. Sci. 37 (1), 78–87. doi:10.16339/j.cnki.hdxbskb.2023.01.011

Liu, Z., Liu, Y., and Yang, Z. (2022). Whether environmental targets of local governments affect enterprises green Technology innovation: an empirical study based on the data of listed companies in China's manufacturing industry. J. South China Normal Univ. Sci. Ed. (5), 126–138+207.

Lupi, V., and Marsiglio, S. (2021). Population growth and climate change: a dynamic integrated climate-economy-demography model. Ecol. Econ. 184 (1), 107011. doi:10.1016/j.ecolecon.2021.107011

Ma, Y., and Lv, L. (2022). Shadow banking, financial regulation and macrostability. J. Manag. Sci. China 25 (6), 1–21. doi:10.19920/j.cnki.jmsc.2022.06.001

Ma, Z., and Song, Y. (2023). The impact of climate change on financial stability: theoretical interpretation. South China Finance (3), 19–36.

Mao, X., Wei, P., and Ren, X. (2023). Climate risk and financial systems: a nonlinear network connectedness analysis. J. Environ. Manage 340, 117878. doi:10.1016/j.jenvman.2023.117878

Newell, R. G., Prest, B. C., and Sexton, S. E. (2021). The GDP-temperature relationship: implications for climate change damages. J. Environ. Econ. Manag. 108, 102445. doi:10.1016/j.jeem.2021.102445

Olper, A., Maugeri, M., Manara, V., and Raimondi, V. (2021). Weather, climate and economic outcomes: evidence from Italy. Ecol. Econ. 189, 107156. doi:10.1016/j.ecolecon.2021.107156

Pagnottoni, P., Spelta, A., Flori, A., and Pammolli, F. (2022). Climate change and financial stability: natural disaster impacts on global stock markets. Phys. A Stat. Mech. its Appl. 599, 127514. doi:10.1016/j.physa.2022.127514

Ploeg, F. V. D., and Rezai, A. (2020). Stranded assets in the transition to a carbon-free economy. Annu. Rev. Resour. Econ. 12, 281–298. doi:10.1146/annurev-resource-110519-040938(1)

Pottier, A., Fleurbaey, M., Méjean, A., and Zuber, S. (2021). Climate change and population: an assessment of mortality due to health impacts. Ecol. Econ. 183, 106967. doi:10.1016/j.ecolecon.2021.106967

Qi, S., Shen, L., and Cui, J. (2018). Do environment right trading schemes induce green innovation? Evidence from listed firms in China. Econ. Res. J. 53 (12), 129–143.

Raza, S. A., Khan, K. A., Benkraiem, R., and Guesmi, K. (2024). The importance of climate policy uncertainty in forecasting the green, clean and sustainable financial markets volatility. Int. Rev. Financial Analysis 91, 102984. doi:10.1016/j.irfa.2023.102984

Roncoroni, A., Battiston, S., Escobar-Farfán, L. O., and Martinez-Jaramillo, S. (2021). Climate risk and financial stability in the network of banks and investment funds. J. Financial Stab. 54, 100870. doi:10.1016/j.jfs.2021.100870

Sun, J., and Chai, Z. (2023). The impact of digital financial inclusion on regional employment quality. J. Macro-quality Res. 11 (4), 38–48. doi:10.13948/j.cnki.hgzlyj.2023.04.004

Von Peter, G., Von Dahlen, S., and Saxena, S. C. 2018. Unmitigated disasters? New evidence on the macroeconomic cost of natural catastrophes. Social Science Electronic Publishing, Rochester, NY, USA.

Wang, B., and Song, Y. (2020). Impact of transition risks of climate change on macroeconomic and financial stability. Econ. Perspect. 11, 84–99.

Wang, Y., and Xia, L. (2023). Promoting or inhibiting: the impact of government R&D subsidies on the green innovation performance of firms. China Ind. Econ. (2), 131–149. doi:10.19581/j.cnki.ciejournal.2023.02.008

Wang, Z., and Wang, H. (2022). Low-carbon city pilot policy and high quality development of enterprises: from the perspective of economic efficiency and social benefit. Bus. Manag. J. (6), 43–62. doi:10.19616/j.cnki.bmj.2022.06.003

Weerasekara, S., Wilson, C., Lee, B., Hoang, V. N., Managi, S., and Rajapaksa, D. (2021). The impacts of climate-induced disasters on the economy: winners and losers in Sri Lanka. Ecol. Econ. 185 (2), 107043. doi:10.1016/j.ecolecon.2021.107043

Wu, X., Bai, X., Qi, H., Lu, L., Yang, M., and Taghizadeh-Hesary, F. (2023). The impact of climate change on banking systemic risk. Econ. Analysis Policy 78, 419–437. doi:10.1016/j.eap.2023.03.012

Xiao, S., Peng, W., and Huang, X. (2020). Is the financing constraint of the current manufacturing enterprises excessive or insufficient: the review and judgment based on the requirments of high quality development. Nankai Bus. Rev. 23 (2), 85–97.

Yi, G., and Wang, Z. (2002). Monetary policy and financial assets price. Econ. Res. J. (3), 13–20+92.

Yin, Y. (2022). Measurement and spatial-temporal evolution of financial high-quality development level. Statistics Decis. 38 (17), 129–133. doi:10.13546/j.cnki.tjyjc.2022.17.025

Zhang, T., et al. (2023). Carbon cycle, climate change, and financial risks: based on the DSGE model. China Population,Resources Environ. 33 (8), 1–12.

Zhang, W., and Zhang, M. (2022). Construction and measurement of high-quality development evaluation system of financial industry. Statistics Decis. 38 (22), 35–39. doi:10.13546/j.cnki.tjyjc.2022.22.007

Zhang, X., Zhang, S., and Lu, L. (2022). The banking instability and climate change: evidence from China. Energy Econ. 106, 105787. doi:10.1016/j.eneco.2021.105787

Keywords: climate change, financial enterprises, high-quality development, mathematical analysis, PSM

Citation: Lyu L and Xiao F (2024) Has climate change promoted the high-quality development of financial enterprises? Evidence from China. Front. Environ. Sci. 12:1332748. doi: 10.3389/fenvs.2024.1332748

Received: 03 November 2023; Accepted: 09 February 2024;

Published: 28 May 2024.

Edited by:

Mobeen Ur Rehman, Shaheed Zulfikar Ali Bhutto Institute of Science and Technology (SZABIST), United Arab EmiratesReviewed by:

Xiaojing Cai, Okayama University, JapanCopyright © 2024 Lyu and Xiao. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Fang Xiao, eGlhb2ZAY21hLmdvdi5jbg==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.