Xuesong Gu

Xuesong Gu Yiling Wang

Yiling Wang

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 20 December 2023

Sec. Environmental Economics and Management

Volume 11 - 2023 | https://doi.org/10.3389/fenvs.2023.1281165

This article is part of the Research Topic Determinants of Sustainable Development from a Global Perspective View all 5 articles

Green credit is an important way to achieve global green development. Using the adoption of the Green Credit Guidance (GCG) policy implemented by the Chinese government in 2012 as a quasi-natural experiment, this article examines the impact of the GCG on the digital transformation of highly polluting firms. This research uses text analysis to assess the extent of digital transformation. The empirical findings show that the GCG has a considerable detrimental effect on the digital transformation of significantly polluting businesses. According to the underlying mechanics, the GCG prevents extremely polluting firms from digitalization by tightening financial restrictions and lowering innovation inputs. The GCG’s disincentive effect on heavy polluters is especially more pronounced in state-owned listed corporations and the Central and Western areas of China, as demonstrated by heterogeneity research. Our research offers novel ideas for creating a digital economy and promoting sustainable development in emerging developing nations like China.

Developing countries such as China, while realizing their own rapid development, will unavoidably face issues including overcapacity and inefficient resource utilization. With the worsening global warming crisis, all countries must address the issue of how to regulate carbon emissions in order to achieve global sustainable development. In the process of achieving green development goals, digital transformation will support the innovation and upgrading of heavily polluted industries and promote the development of clean energy (Chen, 2022a). According to the data disclosed in the Digital China Development Report, the size of China’s digital economy has become a major driver of China’s economic growth. Since the release of the green credit policy, the financial and talent markets have continued to be popular, and the contribution of green industries to the overall industrial structure has been increasing (Ke and Lin, 2017).

The essence of green credit policy is to guide enterprises to green development. Green credit policy incentivizes and constrains the production behavior of heavily polluting enterprises. For heavily polluting businesses, digital transformation is a key tool for achieving technological innovation, energy efficiency, and emission reduction. Utilizing the means effectively can achieve the goals required by the green credit policy (Chen, 2022b). Therefore, it is valuable to explore the impact of the Green Credit Guidance (GCG) policy on the digital transformation of heavy-polluting enterprises. Theoretically, there are two effects of green credit on the digitalization of highly polluting businesses. On the one hand, green credit increases the cost of environmental regulation for highly polluting enterprises by reallocating resources to equal or even exceed the advantages of crude expansion, improving corporate environmental performance (Chen and Hao, 2022). In addition, digital technologies such as big data reduce the cost of green manufacturing and information search for products. Together, these factors promote green technological innovation in enterprises, making digitalization an important method of reducing the adverse effects of green credit. On the other hand, the increase in borrowing costs further increases the pressure on enterprises to implement digital transformation. Heavily polluting firms that have difficulties in financing and tend to be risk-averse will not make major strategic adjustments, which will hinder their digital transformation. Moreover, the paths of clean transformation and digital transformation are incompatible (Wen et al., 2022; Zhong et al., 2022). These findings suggest that companies will not choose digital means to achieve sustainability. Whether green credit helps or hinders the digital transformation of polluters depends on how the positive and negative impacts are balanced.

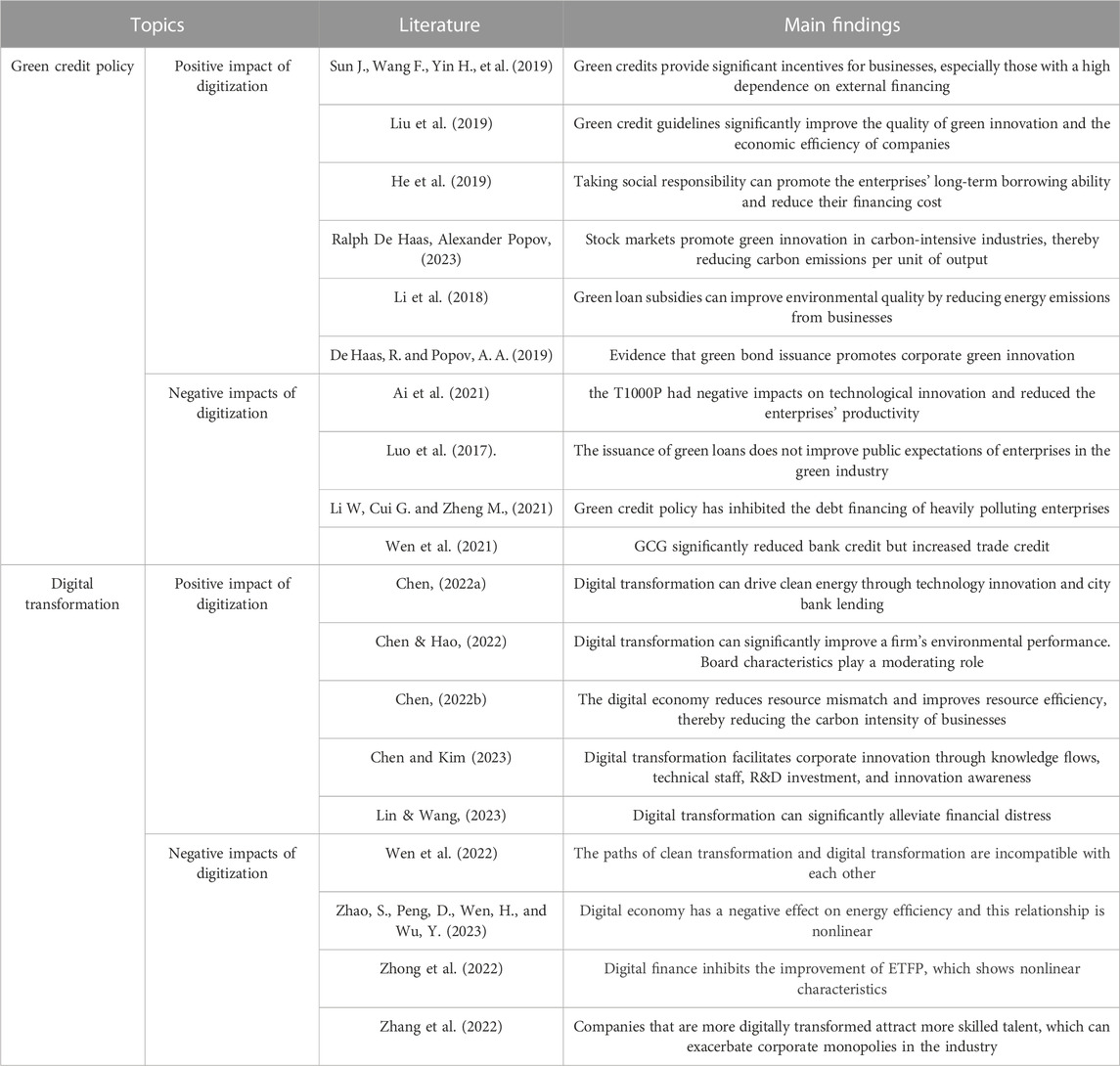

As green credit policies continue to improve, their impact has been an intense academic discussion. In terms of their positive impacts, effective environmental regulation can drive firms to innovate and improve competitiveness (Porter and Linde, 1995). Through subsequent studies, several scholars have come to similar conclusions (Hu et al., 2021; Wang et al., 2022). Theoretically, Li et al. (2018) confirmed that green credit can encourage cleaner production. In terms of negative effects, Li W. et al. (2022) and Wen et al. (2021) proved that the constraint effect generated by credit has a negative impact on the cost of credit financing, operational efficiency, and total factor productivity of enterprises. Other scholars believe that there is a certain threshold for the effect of green credit to appear (Qiu et al., 2017). Academic research on enterprise digitization mainly focuses on the impact of enterprise digital transformation (Nambisan et al., 2019; Kraus et al., 2021). In terms of favorable impacts, the integration of the digital economy with the physical economy can effectively improve the precise matching of various aspects of enterprises (Xiao, 2020), leading to a double increase in output efficiency and a reduction in energy consumption. Chen and Kim (2023) and Feng et al. (2022) argued that digital transformation can encourage innovation in enterprises by encouraging innovation in enterprises. Wen et al. (2022) found that digitalization increases the total factor productivity of manufacturing firms. In terms of negative impacts, Zhang et al. (2022) argued that firms with higher levels of digital transformation attract more skilled talent, leading to talent barriers and exacerbating firms’ industry monopoly. In addition, digital transformation increases the management costs of firms. Relevant information on some of the key literature can be found in Table 1.

TABLE 1. Summary of literature on green credit and digital transformation.

With regard to existing research, there are still some gaps. First of all, there is still a lot of debate on the effectiveness of the implementation of green credit policies. Existing studies mainly focus on aspects such as green innovation and operational efficiency to measure the effectiveness of green credit, lacking measurement of digital transformation. Second, there is little study on the factors that influence business digital transformation, instead, they mostly focus on the effects of digital transformation. Third, existing measurements on enterprise digital transformation research are mostly analyzed from a qualitative perspective, lacking empirical research based on microdata.

Therefore, this study focuses on how the GCG affects the digital transformation of listed companies in heavy-polluting industries by developing a DID model. Compared with the existing studies, the contributions of this paper are as follows. Firstly, this paper improves the empirical evidence on the impact of the GCG to test its effect on digital transformation. It takes highly polluting enterprises as the research object and evaluates the impact of policy implementation from a novel perspective of digital transformation, which offers an empirical foundation for the implementation of green credit policy in developing countries. Secondly, the article reveals the impact mechanism of green credit on digital transformation in terms of financing constraints and R&D investment, filling the research gap of the impact factors of digital transformation. Understanding these two microtransmission mechanisms provides policy support for making green credit work better for the digital transformation of heavy polluters. Thirdly, for the measurement of enterprise digital transformation, this article combines existing research and synthesizes multiple classification criteria quantitatively. It creates a more thorough frequency of digitization-related words and logarithmically processes the data to improve data accuracy and comprehensiveness.

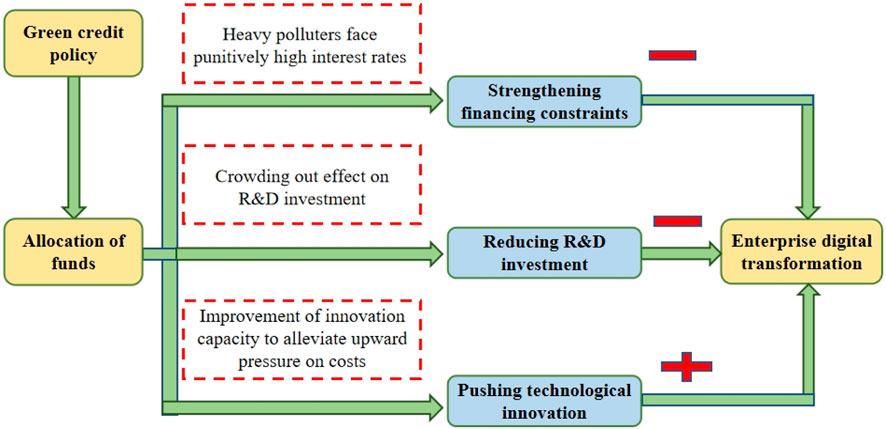

Green credit can reduce corporate pollution by setting different dynamic credit rules for different projects. According to institutional theory, government actions that grant some groups access to resources and authority also impose restrictions on the actions of other components of an economy (Jakobsen and Richard, 2014). To achieve the allocation of capital resources, financial institutions offer credit support and favorable interest rates for green firms while restricting loan amounts and charging punitively high-interest rates to large polluters (Liu et al., 2019). Heavy polluters must upgrade their industries because there is less bank financing accessible to them (Yao et al., 2021). However, both innovation and transformation increase the uncertainty of a firm’s future growth (Luo et al., 2017). The digital technologies have positive externalities. Businesses are unable to fully profit from digital technology, which causes their real degree of digital technology development to be lower than it should be. The green credit policy’s pressure to lower their financing costs further increases the loss of positive externalities and impedes the digital transformation of businesses. At the same time, the resources of an enterprise are limited. According to resource-based theory, management decisions are to determine the specific use of a firm’s resources. Constrained by environmental goals, heavy-polluting firms do not have the resources to invest in digital technology development in the short term, which inhibits the productivity-enhancing effects of digitalization (Ai et al., 2021). Heavy polluters have found it challenging to advance their digital transformation goals due to a lack of funding for the purchase, use, and maintenance of digital equipment and technology. Based on this, we agree that the good effects of green credit policy are outweighed by the negative effects on the digital transformation of large polluters, and propose the following.

Hypothesis 1:. The implementation of the GCG has a disincentive effect on the digital transformation of heavily polluting enterprises.

Heavy polluters are under pressure to undergo digital transformation due to financial restrictions. The supply side of financial institutions can influence how businesses choose to finance themselves (Faulkender and Petersen, 2005). Bank loans are the main way to finance corporate obligations in China’s banking-centered economic system (Jiang et al., 2020). If banks follow green credit and take environmental compliance as the basis for credit, it means heavy polluters face high financing costs and investment risks. Based on modern contract theory, the principal-agent costs between banks and enterprises increase with the risk of the project (Braun and Guston, 2003). Not only does it have to take responsibility for credit violations, but also faces the risk of difficulty in recovering loan funds once the heavily polluting project is punished by relevant authorities. Therefore, banks are increasingly strict in their review of project loans to reduce the losses caused by information asymmetry (Peng et al., 2022). Heavy polluters face greater public condemnation, the risk of environmental litigation, and credit ratings are affected. At this time, external creditors will be more cautious that they disinvestment their capital or refuse to roll over due to enterprise development prospects and default risks (Yao et al., 2021). Overall, coupled with the complex and changing international situation, the cash flow operation of heavily polluting enterprises is affected. Digital transformation brings about novel actors and values, replacing existing rules of the game within organizations. (Hinings et al., 2018). The digital transformation of highly polluting businesses faces obstacles due to the current financial position. The use of digital technology serves as the cornerstone of digital transformation, the development of digital infrastructure, and the creation of a team of digital experts all demand considerable financial backing. Financially constrained heavily polluting businesses might not be able to secure the expensive, protracted capital requirements needed for a digital transformation. As a result, businesses could decide to postpone digital transformation even if it would have long-term economic advantages. In light of this, the following theory is put out in this study.

Hypothesis 2:. The GCG discourages the digital transformation of heavily polluting enterprises by strengthening financing constraints.

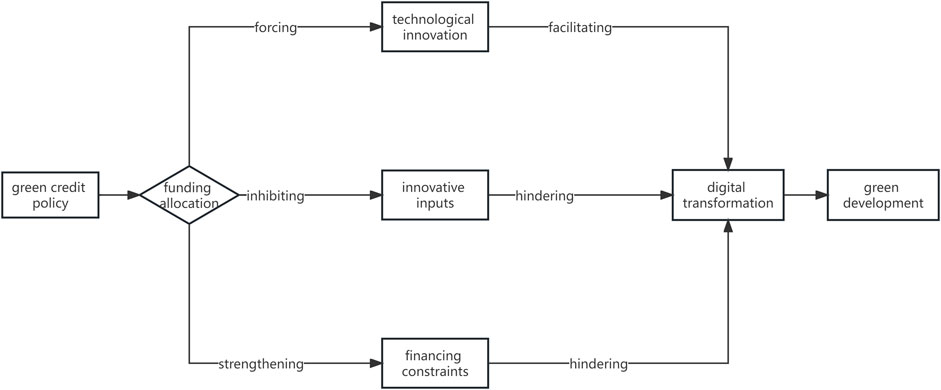

The lack of innovative investment puts another obstacle in the way of heavy polluters’ digital transformation. Green credit is a method for environmental control that transfers some of the environmental costs that were initially incurred by society to businesses (Xie et al., 2022). However, the “cost compliance effect” claims that the implementation of the green credit policy forced businesses to standardize their buildings and machinery, build pollution control infrastructure, and upgrade their technical staff in order to ensure the smooth operation of their production and operation activities. This behavior will result in a significant increase in manufacturing and pollution prevention expenses in the short future, squeezing out technological innovation efforts such as R&D spending (Wang et al., 2022). High costs and uncertainty characterize R&D investment. Given the activity’s input-output ratio, many large polluters may be unable to support such a risky investment. The core technology is the bottom and motivation to achieve digitalization, but only very few enterprises have successfully realized the transformation. It means that the core technology is concentrated in a few developed regions, and the polarization effect of key technology monopolies in advantageous industries continues to be highlighted (Xiao and X. Y., 2020). The hardware and software foundation for industrial digitization receives less investment due to this lack of innovation. The digital infrastructure and associated supporting systems are not sufficiently reliable, which limits the creative creation of industrial digitization application scenarios. The high objective difficulty of technological innovation coupled with the low subjective willingness of enterprises to innovate has led to the increasingly rocky road of digital transformation of enterprises. In this case, the following theory is advanced in this work. Figure 1.

FIGURE 1. Theoretical mechanism.

Hypothesis 3:. The GCG curtails the digital transformation of heavy polluters by reducing corporate innovation inputs.

From 2005 to 2020, the sample used in this article is data from China’s listed A-share firms in Shanghai and Shenzhen, which are obtained from the Wind Economic Database. This paper treats the data as follows in accordance with the needs of the study. We remove data from the financial industries, as well as samples of ST, *ST, and PT organizations, as well as sample companies with outliers and significant data incompleteness. All continuous variables are treated to a 1% up and down tailing technique to eliminate the negative effects of extreme values. Following the foregoing processing, the final sample contains 2,767 listed enterprises, of which 735 are in significantly polluting industries. The experimental group has 735 samples, while the rest are recorded as the control group, totaling 2030.

Enterprise digital transformation (DIGT) is the dependent variable that we use. For the measure of this variable, we use textual analysis. Data on the digital transformation of companies is available in corporate annual reports, which are obtained from the Wind Economic Database. There is currently little agreement among researchers about research methodology, and the majority of study on digital transformation focuses on qualitative analysis rather than measuring the degree of digitalization. The data in the yearly financial reports of publicly traded corporations can lay out future strategic objectives for businesses and show how those businesses are progressing. From academic and industrial domains, Lin and Wang (2023) defined the word spectrum of digital transformation characteristics. We build the index system for corporate digital transformation by matching and searching the annual report text against the word spectrum, classifying and aggregating the results to create the final word frequency. This research logarithmizes the data while taking into account their “right skewness” to create the final index of the level of digital transformation.

If a company is a heavy polluter, the imaginary variable for those companies is 1, otherwise, it is 0. The Ministry of Environmental Protection’s 2008 Notice on the Issuance of the “List of Listed Companies for Environmental Verification Industry Classification and Management” is used to identify highly polluting businesses. Heavy polluters among the 16 categories of industry include thermal power, cement, textile, tannery, and mining. Post is another dummy variable that was equal to 0 prior to the GCG’s implementation and is now equal to 1. “Green Credit Guidelines” released by the China Banking Regulatory Commission (CBRC) was enacted in 2012. Therefore, 2012 is taken as the time of occurrence of the policy. The interaction term reflects the extent to which implementation has affected the digital transformation of significantly polluting industries.

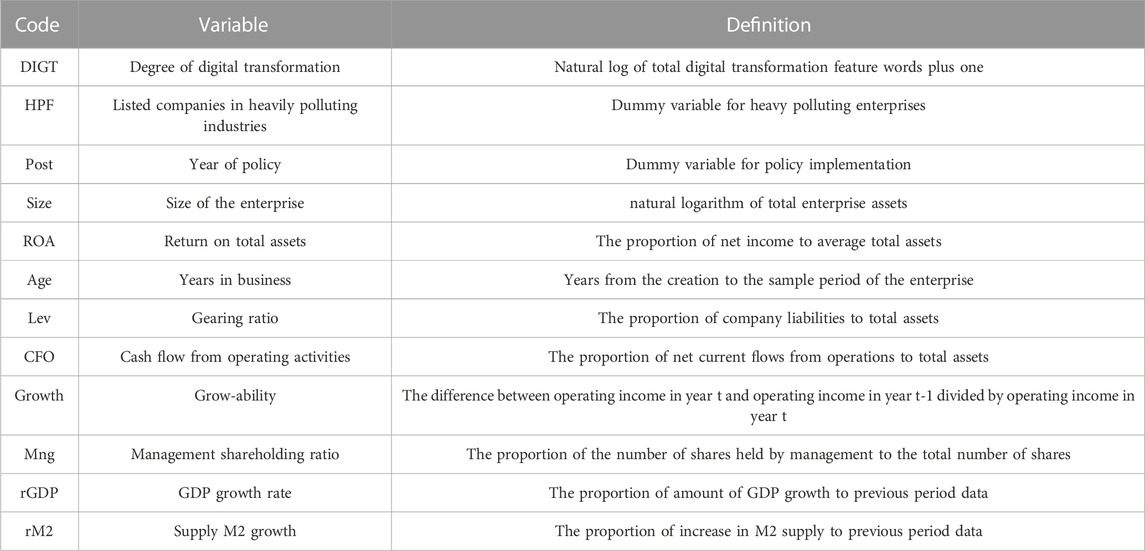

At the micro level, the structure and nature of the firm will have some impact on the results. Referring to the existing literature, the following variables are set as control variables. Specifically, firm size (Size), return on total assets (ROA), firm age (Age), gearing ratio (Lev), cash flow from operating activities (CFO), growth (Growth), and management shareholding ratio (Mng). At the macroeconomic level, the benchmark regression model’s control variables are the GDP growth rate (rGDP) and M2 growth rate (rM2). The China Stock Market & Accounting Research (CSMAR) database is the source of the above data. Table 2 shows the definition of each variable.

TABLE 2. Variable definition.

This study uses a two-way fixed effects model with listed businesses in the extremely polluting industry as the experimental group to investigate the effects of the GCG implementation on the digital transformation of heavily polluting enterprises.

Where i stands for the company and t for the year. Enterprises’ level of digital transformation is indicated by the acronym DIGTit. With a value of 1 for businesses in the badly polluting group and 0 for businesses in the control group, HPFi is a dummy variable for heavily polluting organizations. Postt is a dummy variable that takes 1 for policy implementation in 2012 and later and 0 for all previous years. The HPFi×Postt double difference variable’s coefficient assesses how enforcing a policy will affect significantly polluting businesses. A number of firm-level control variables are part of Controlit. τi represents annual fixed effects and δi represents industry-fixed effects.

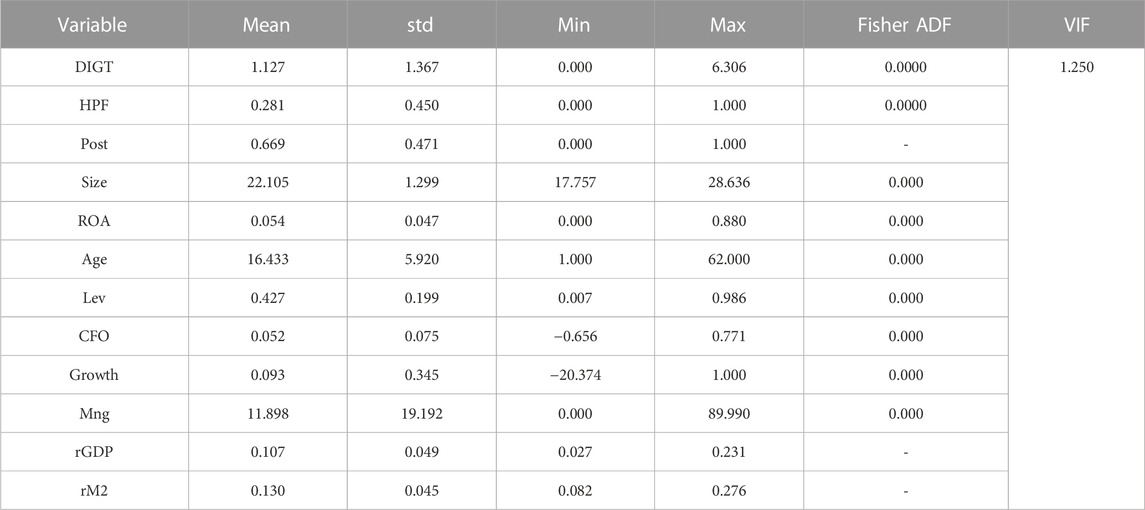

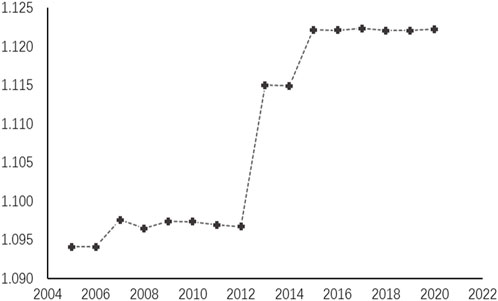

Table 3 displays the outcomes of descriptive statistics for each variable. The index of the degree of digital transformation (DIGT) ranges from 0 to 6.306 with 6.306 being the maximum number. As can be seen in Figure 2, there has been a significant increase in the overall digitization of businesses after 2012. The sample businesses’ levels of digitalization vary greatly, as seen by the standard deviation being more than 1. The observations of heavily polluting firms account for around 28% of the entire sample, according to the mean value of strongly polluting enterprises (HPF), which is 0.281. In addition, each control variable’s mean, maximum value, and deviation from the mean are all within acceptable bounds when compared to earlier research. In the meantime, the level of covariance of the variables is assessed to assure the accuracy of the results of the regression by calculating the variance inflation factor to reflect the rise in variance owing to multi-collinearity. The endogeneity test is passed since the average variance inflation factor is 1.25 and less than 10. It shows that there is not much multi-collinearity among the variables. Additionally, this study runs an ADF test on each variable before regression to see if it has a unit root in order to guarantee the smoothness of the variables. All variables reject the null hypothesis at a 99% level of significance, and all variables are smooth.

TABLE 3. Results of descriptive statistics for sample enterprises.

FIGURE 2. The trend of digital transformation.

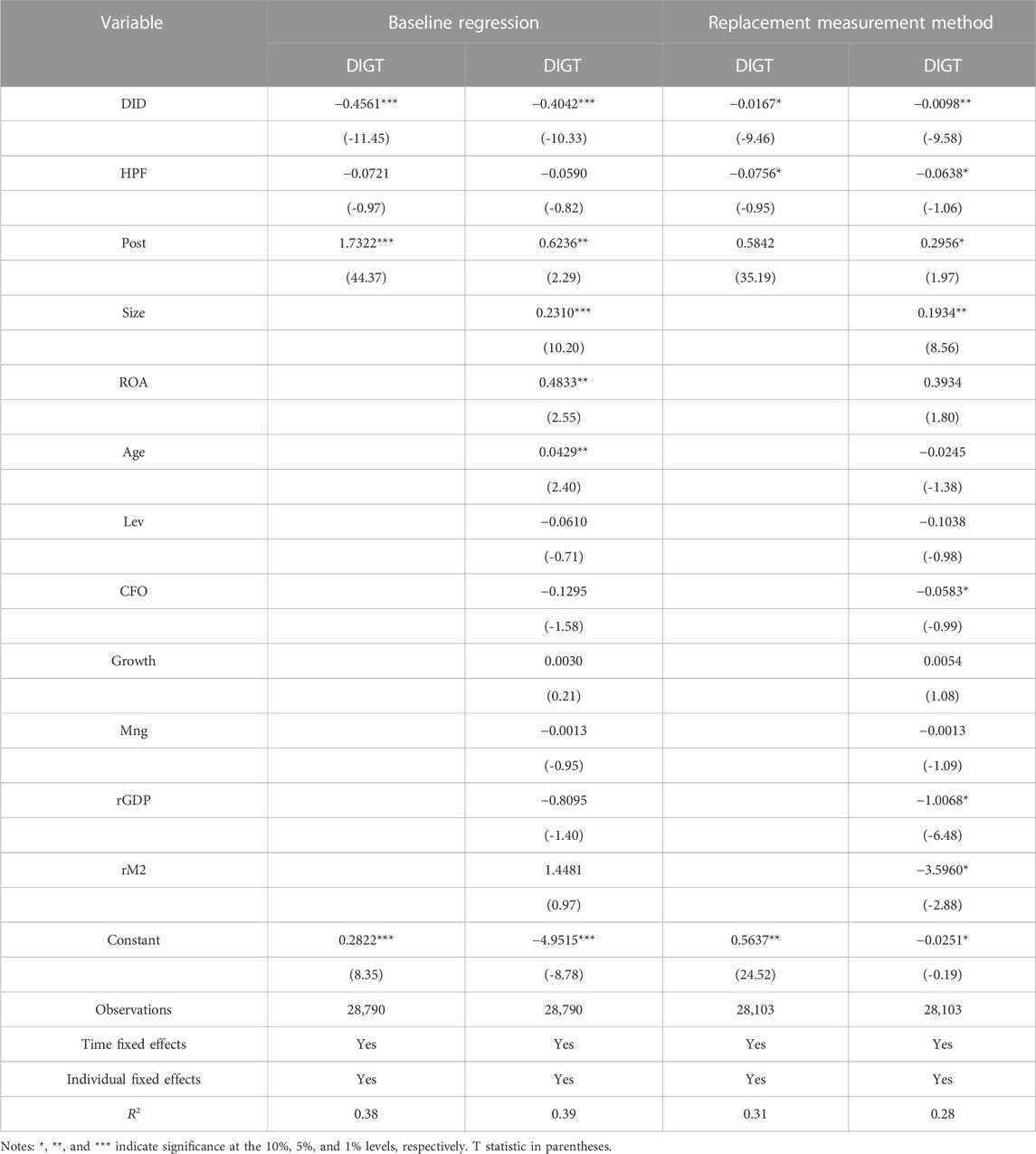

Based on the study presented above, a baseline regression of the model containing the aforementioned variables is carried out, and the outcomes are displayed in Table 4. The findings without and with the addition of control variables are displayed in the first and second columns of the table, respectively. The main emphasis is on the HPFi×Postt coefficients, and all of the DID coefficients are significant at the 1% level. It shows that after the adoption of the GCG, heavy polluters experience a materially detrimental impact on digital transformation compared to non-heavy polluters. The aforementioned findings support the aforementioned premise by demonstrating that the GCG considerably reduces the degree of digitization of highly polluting firms.

TABLE 4. Impacts of green credit on digital transformation.

The above studies suggest that green credit policies have not achieved the expected results. From existing literature, some scholars believe that green credit has a positive effect on green innovation. Wang and Wang, (2021) argued that with the strengthening of intellectual property protection, the function of green credit policy in fostering green innovation grows. However, the findings of this paper are diametrically opposed. It suggests that green credit policy has a greater inhibitory effect on technological innovation than a promotional effect under the data selected for this article. Several more researches that have already been conducted support the conclusions of this paper. According to Wang et al. (2023), green credit policies have an adverse impact on innovation in performance-deficient enterprises. Xie et al. (2022) found that green credit policy inhibits the implementation of innovation in firms from the perspective of the cost of credit financing. This paper, on the other hand, starts from enterprise digital transformation, a segment of technological innovation, and concludes that green credit has an inhibitory effect on enterprise digital transformation. In today’s world energy era, developing countries especially need to pay attention to the development of digitalization and realize green transformation in order to achieve global sustainable development. Inevitably, many problems will arise from this. The green credit policy needed to be further improved in light of the effects of existing implementation.

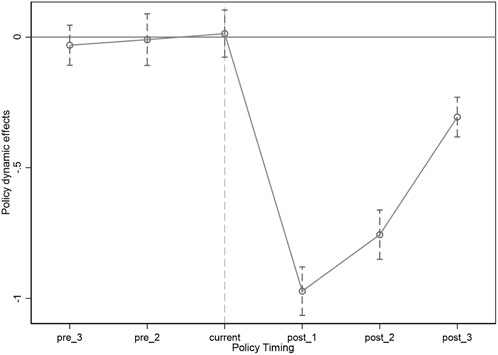

According to the aforementioned regression data, the assumption of parallelism in the control and experimental groups must be met in order to use the interaction term coefficient as a foundation for evaluation. The event analysis suggested by Jacobson (Jakobsen and Richard, 2014) is used to analyze the parallel trend between the comparison control and experimental groups in order to confirm that the degree of digitalization of enterprises in heavily polluting and non-heavily polluting enterprises prior to the implementation of the GCG is largely consistent in time trend. The 3 years prior to and following 2012 are designated in the model set as pre_3, pre_2, pre_1, post_1, post_2, and post_3. Figure 3 depicts the outcomes of the parallel trend test. The 95% confidence interval at each moment contains 0, suggesting that the period was not significant prior to the introduction of the policy. Each coefficient is significant for all years following the introduction of the policy, and the parallel trend test is successful. The curve also indicates that the implementation of the GCG has a major negative impact on the digital transformation of organizations because it exhibits an upward trend following a considerable reduction after the legislation of the GCG in 2012.

FIGURE 3. Parallel trend testing.

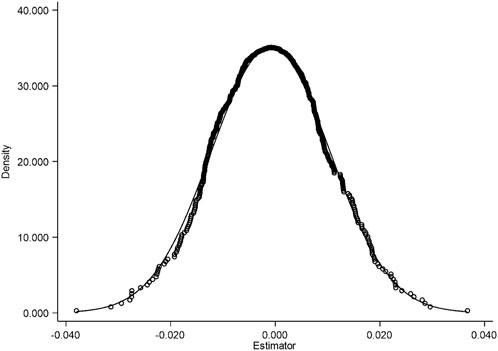

In the above model, several columns of the control variables matrix controlling for firm characteristics level are introduced in consideration of the various characteristics of various industries, and temporal effects and individual effects are also fixed. However, there are still additional unpredictable variables and random events that could affect how businesses change to be digital. Therefore, this paper randomly selects 123 samples from all samples as a pseudo-experimental group for a placebo test to determine whether the degree of digital transformation of heavy polluters is due to time variation and to rule out the impact of unobserved firm sample characteristics on the regression results. Following a 500-time run of the regression with DID as the primary explanatory variable, the predicted coefficient distribution of the coefficients is eventually plotted as follows. The estimated coefficients of DID are spread around zero under the random treatment, as shown in Figure 4. It shows that sufficiently significant factors are not left out of the model set and that the outcomes of the regression are unaffected by unobserved firm characteristics. The outcome of the policy in this research is indeed what causes the benchmark regression, demonstrating the validity of the aforementioned conclusions.

FIGURE 4. Placebo testing.

There is currently no uniform standard to assess the extent of enterprise digital transformation. The research findings from Liu et al. (2023) are used in this paper as the indicator of an enterprise’s digital transformation. He et al. (2019) measured the ratio of the digital economy-related portion of the intangible asset line items to the total intangible assets at the end of the year as disclosed in the notes to the financial reports of listed companies as an indicator of digital transformation. Specifically, when the intangible asset item contains keywords related to digital technology such as “software”, “network” and other keywords related to digital technology, the item will be labeled as “Digital Economy Technology Intangible Assets”. And then a number of digital economy technology intangible assets of the same company in the same year are summed up and calculated. The total number of digital economy technology intangible assets of the same company in the same year will be added up. The proportion of intangible assets in the current year is calculated, which is a measure of the degree of digital transformation of the enterprise. Based on robustness concerns, this paper uses the pertinent indicators put forward by He et al. (2019) to quantify digital transformation and then runs regressions to produce the results shown in Table 4 above. It demonstrates methodologies will have no impact on this paper’s estimation conclusions.

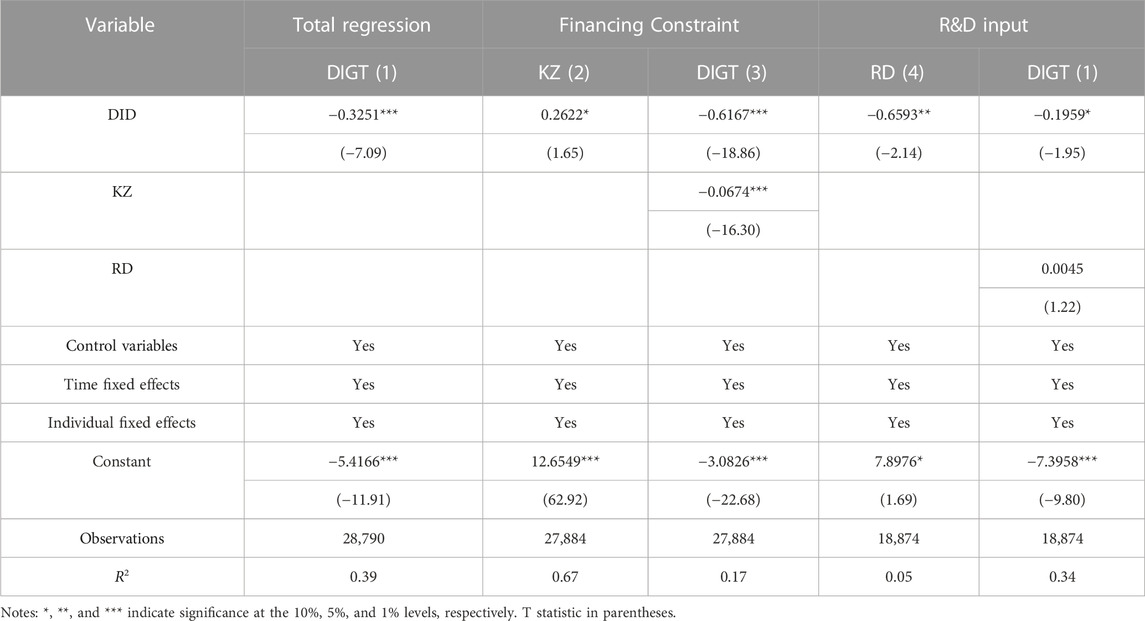

The above findings suggest that the GCG significantly reduces the digitalization of enterprises, so what mechanism does the policy work? Based on the above hypotheses, the GCG has negative effects on digital transformation by achieving financing constraints and inhibiting innovation inputs. This paper draws on the new mediating effects model proposed by Wen and Ye (2014), which improves on the traditional stepwise method, to examine whether the GCG achieves its effects on the digital transformation of listed firms in strongly polluting industries. The specific model is as follows.

The coefficient c of Eq. 2 is checked first, and if it is significant, the coefficients a and b of Eqs 3, 4 are then tested further. The indirect influence becomes significant if a and b are both significant at a level of trust of 95%. The Bootstrap approach, which has a better level of precision, is used to test it directly if more than one of them is not significant at a 95% confidence level. The following stage of analysis is carried out only if it is relevant. The coefficient c' of Eq. 4 is next examined, and its lack of significance suggests that there is just a mediating impact. It is important to further compare the signs of ab and c' to determine their significance. It falls under the partial mediating effect if the signs are the same, and the role of masking if the signs are different.

Among these, the KZ index is used to gauge the firm’s level of financing constraint, the higher the index, the greater the constraint. The ratio of R&D investment to operating revenue, abbreviated as RD and representing the two mediating factors, is used to calculate the level of innovation investment. The results of the precise estimation are shown in Table 5.

TABLE 5. Mediator effect of KZ and R&D.

The coefficient c is considerably negative for finance limitations, demonstrating that the execution of the GCG has an adverse impact on the digital transformation of highly polluting companies. The adoption of the GCG exacerbates the financing constraint of firms, according to the coefficient b, which is significant, however, it fails to meet the 95% confidence level. The coefficient a is considerably positive at a 90% confidence level. Therefore, in order to directly verify H0: ab = 0, the Bootstrap approach must be used. According to the findings, the indirect effect interval after 1,000 random samples lies between [0.002,0.01], excluding zero. The initial hypothesis is then disproved, proving that the ab and the indirect impact are both significant. The direct influence is significant because the coefficient c' is also significant. Additionally, ab and c' share the same sign, which has a partial mediating effect. This shows that financial constraints have a constraining impact on businesses’ efforts to change into digital businesses and that the GCG’s implementation increases the level of financial constraints. Green credit policies make it more difficult for businesses that produce a lot of pollution to become digital. H2 above is proven to be true.

The aforementioned regression findings show that the coefficient c counts for innovation inputs. The introduction of the GCG greatly reduces the heavy polluters’ innovation input, as seen by the significantly negative coefficient a. However, since coefficient b is not significant, we must use the Bootstrap method to determine whether or not ab is significant. Since ab’s indirect effect interval is [−0.217, −0.179], which lacks zero, ab is significant as well, and this is confirmed by the Bootstrap method. Finally, the coefficient of c' is notably negative, showing that the GCG prevents extremely polluting businesses from going digital by limiting their innovation contributions, supporting the aforementioned hypothesis H3.

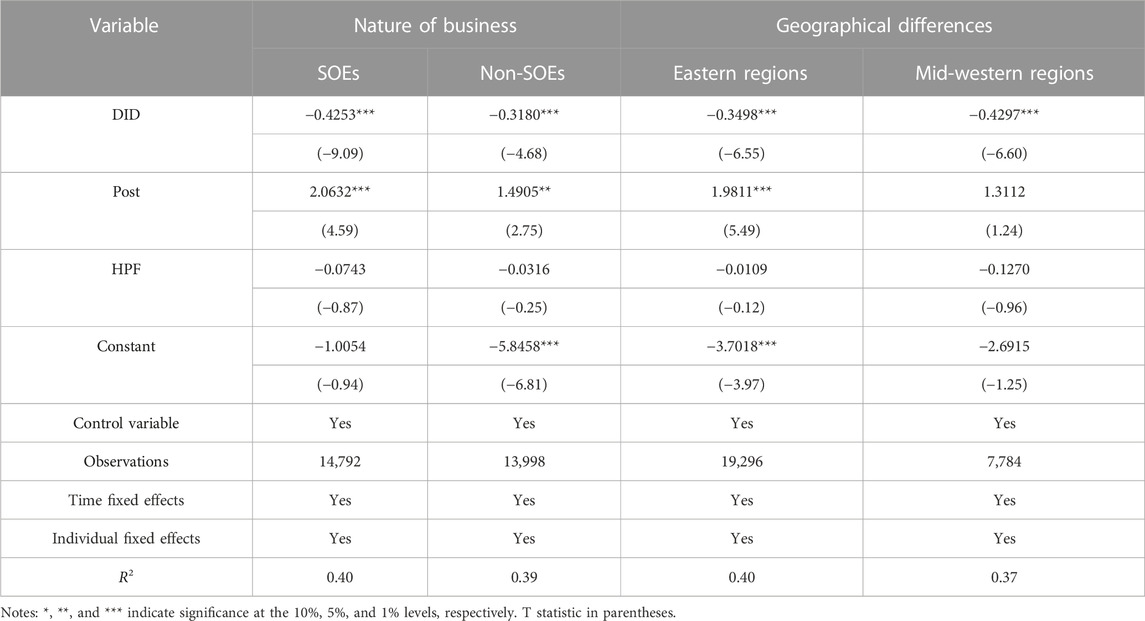

For SOEs and non-SOEs alike, China’s unique institutional structure has resulted in fierce market competitiveness and a significant level of information asymmetry. It is evident from the research above that there are significant differences between organizations in the level of digital transformation. SOEs are essential to the process of digital transformation as the main engines of China’s economic growth. While other businesses are only just beginning the process of going digital. The fact that non-SOEs are still less aware of digital transformation and less sensitive to the constraining effect of green financing is due to the significant disparity in the initial degrees of digital transformation between them. This study makes the case that the GCG considerably hinders the digital transformation of SOEs that pollute more than non-SOEs. This study uses a grouping test based on the property rights nature variable to evaluate the aforementioned hypothesis, and Table 6 presents the pertinent findings. The coefficient of DID is significant in both samples, as the table shows. With a higher absolute value of the coefficient, it is more important for SOEs, showing that the GCG greatly hinders the digital transformation of heavily polluting SOEs compared to non-SOEs.

TABLE 6. Heterogeneity analysis.

China is a huge, populous country, and the distribution of its natural resources varies widely from one region to another. Due to the specific policy assistance, the Eastern area developed far more quickly than the central and Western regions once the regional economy was implemented. Environmental issues have become a significant barrier impeding the eastern region’s prosperity as the level of finance and economic growth has increased. The level of green transformation of significantly polluting businesses is higher as a result of the increased attention given to green behavior by the government and businesses. The Eastern region also tends to have a high level of financialization, which is less constrained by green rules and has more plentiful financing sources. This article comes to the conclusion that the GCG severely inhibits the digital transformation of heavy polluters more in the Central and Western regions than in the Eastern regions. Businesses from the Central and Western regions are chosen as two samples and separate group regression analyses are carried out to evaluate the aforementioned hypothesis. Table 6’s findings indicate that both the Eastern and Midwestern areas’ DID coefficients are considerably negative, but the Central and West China area’s absolute value of the coefficients is much greater compared to that of the Eastern region. It shows that the Midwestern region’s substantially polluting businesses are more considerably negatively impacted by the GCG, proving the above theory.

Green credit is a vital financial tool for easing the environmental burden and is essential for the management of economic resources and the preservation of the natural world. This study examines whether and how China’s GCG affects the digital evolution of polluting companies. This study builds a double-difference model to examine how the GCG affects the digital transformation of businesses that produce a lot of pollution in order to test this hypothesis. Based on the “Green Credit Guidelines” released by the China Banking Regulatory Commission (CBRC) in 2012, the paper focuses on the impact of the GCG on the digital transformation of highly polluting industries. The study and analysis led to the following three conclusions. Firstly, it is discovered that the GCG’s implementation considerably impedes businesses’ efforts to go digital. Secondly, the mechanism analysis demonstrates that the GCG prevents listed companies in highly polluting industries from going digital through two mechanisms: tightening finance requirements and limiting innovative inputs. Thirdly, according to heterogeneity research, the GCG significantly hinders the digitization of SOEs and businesses in China’s central and western regions that work in extremely polluting businesses.

Green growth in other developing countries and emerging economies around the world can learn from China’s experience in transforming highly polluting enterprises. Other countries have to differentiate their policies based on unique socio-economic and policy landscapes (Ramakrishnan et al., 2016; Li X. et al., 2022; Udeagha and Muchapondwa, 2023). Based on the above conclusions and the current status of China’s green credit policy implementation, the article puts forward the following policy recommendations. First, it is necessary to improve the types of green credit products and application scenarios and expand the scope of the application of green credit policies to reduce the adverse effects of green credit on digitalization. Secondly, the research on the influence mechanism mentioned above suggests heavily polluting enterprises should seek new financial instruments to obtain sufficient financial support to avoid financing difficulties due to the punitive effect of the policy. At the government level, it is necessary to formulate incentive policies related to R&D investment and improve green credit policies, guiding businesses to the technical innovation of the digital development of the road forward. Finally, the results of the heterogeneity analysis can be optimized from banks and other financial institutions. While ensuring the control of credit thresholds, financial institutions can implement differentiated standards for green credit according to the nature of enterprise ownership and the region in which the enterprise is located. For State-owned enterprises and heavily polluting industries in the Central and Western regions of China, green credit-related restriction requirements can be deregulated. Others need to develop appropriate policies according to national circumstances.

There are still some limitations of this article that need to be noted. First, the source of data was mainly databases and annual reports of enterprises, and some companies that did not disclose data were not measured. Due to the limitations of the study data, we are unable to capture the long-term impact of green credit on digital transformation. Secondly, for the metric of enterprise digitization, the textual analysis does not fully represent that the company has achieved digital transformation. Therefore, more objective and comprehensive indicators of digital transformation need further research. Finally, for the study of the influence mechanism, the relationship between digitalization and environmental policies is intricate. For further research, we can test the impact of other environmental policies on digital transformation. At the same time, there may be potential synergies between environmental policies and digital transformation in addition to direct impacts. These are directions that could be worthwhile for future research in the article.

Publicly available datasets were analyzed in this study. This data can be found here: https://www.gtarsc.com/.

XG: Writing–review and editing, Conceptualization, Funding acquisition, Project administration. YW: Data curation, Investigation, Writing–original draft.

The author(s) declare financial support was received for the research, authorship, and/or publication of this article. We are grateful for the financial support from the Fundamental Research Funds for the Central Universities in Beijing Forestry University (2023SKQ04), the National Social Science Foundation Project of China (No. 23BJY079) and the Research Project of the Humanity and Social Science Fund of the Ministry of Education of China (No. 22YJA790015).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Ai, H., Hu, Y., and Li, K. (2021). Impacts of environmental regulation on firm productivity: evidence from China’s Top 1000 Energy-Consuming Enterprises Program. Appl. Econ. 53 (7), 830–844. doi:10.1080/00036846.2020.1815642

Braun, D., and Guston, D. H. (2003). Principal-agent theory and research policy: an introduction. Sci. Public Policy 30 (5), 302–308. doi:10.3152/147154303781780290

Chen, P. (2022a). Is the digital economy driving clean energy development?New evidence from 276 cities in China. J. Clean. Prod. 372, 133783. doi:10.1016/j.jclepro.2022.133783

Chen, P. (2022b). Relationship between the digital economy, resource allocation and corporate carbon emission intensity: new evidence from listed Chinese companies. Environ. Res. Commun. 4 (7), 075005. doi:10.1088/2515-7620/ac7ea3

Chen, P., and Hao, Y. (2022). Digital transformation and corporate environmental performance: the moderating role of board characteristics. Corp. Soc. Responsib. Environ. Manag. 29 (5), 1757–1767. doi:10.1002/csr.2324

Chen, P., and Kim, S. (2023). The impact of digital transformation on innovation performance-The mediating role of innovation factors. Heliyon 9 (3), e13916. doi:10.1016/j.heliyon.2023.e13916

Faulkender, M., and Petersen, M. A. (2005). Does the source of capital affect capital structure? Rev. Financial Stud. 19 (1), 45–79. doi:10.1093/rfs/hhj003

Feng, H., Wang, F., Song, G., and Liu, L. (2022). Digital transformation on enterprise green innovation: effect and transmission mechanism. Int. J. Environ. Res. public health 19 (17), 10614. doi:10.3390/ijerph191710614

He, L., Wu, C., Yang, X., and Liu, J. (2019). Corporate social responsibility, green credit, and corporate performance: an empirical analysis based on the mining, power, and steel industries of China. Nat. Hazards 95 (1-2), 73–89. doi:10.1007/s11069-018-3440-7

Hinings, B., Gegenhuber, T., and Greenwood, R. (2018). Digital innovation and transformation: an institutional perspective. Inf. Organ. 28 (1), 52–61. doi:10.1016/j.infoandorg.2018.02.004

Hu, G., Wang, X., and Wang, Y. (2021). Can the green credit policy stimulate green innovation in heavily polluting enterprises? Evidence from a quasi-natural experiment in China. Energy Econ. 98, 105134. doi:10.1016/J.ENECO.2021.105134

Jakobsen, M., and Richard, M. W. (2014). Institutions and organizations: ideas, interests, and identities. Cph. J. Asian Stud. 32 (2), 136–138. doi:10.22439/cjas.v32i2.4764

Jiang, F., Jiang, Z., and Kim, K. A. (2020). Capital markets, financial institutions, and corporate finance in China. J. Corp. Finance 63, 101309. doi:10.1016/j.jcorpfin.2017.12.001

Ke, L., and Lin, B. (2017). Economic growth model, structural transformation, and green productivity in China. Appl. Energy 187 (11), 489–500. doi:10.1016/j.apenergy.2016.11.075

Kraus, S., Jones, P., Kailer, N., Weinmann, A., Chaparro-Banegas, N., and Roig-Tierno, N. (2021). Digital transformation: an overview of the current state of the art of research. Sage Open 11 (3), 215824402110475. doi:10.1177/21582440211047576

Li, W., Cui, G., and Zheng, M. (2022a). Does green credit policy affect corporate debt financing? Evidence from China. Environ. Sci. Pollut. Res. 29 (4), 5162–5171. doi:10.1007/S11356-021-16051-2

Li, X., Ozturk, I., Majeed, M. T., Hafeez, M., and Ullah, S. (2022b). Considering the asymmetric effect of financial deepening on environmental quality in BRICS economies: policy options for the green economy. J. Clean. Prod. 331, 129909. doi:10.1016/j.jclepro.2021.129909

Li, Z., Liao, G., Wang, Z., and Huang, Z. (2018). Green loan and subsidy for promoting clean production innovation. J. Clean. Prod. 187, 421–431. doi:10.1016/j.jclepro.2018.03.066

Lin, C., and Wang, Y. (2023). Can corporate digital transformation alleviate financial distress? Finance Res. Lett. 55, 103983. doi:10.1016/j.frl.2023.103983

Liu, M., Wang, S., and Li, Q. (2023). Digital transformation, risk-taking, and innovation: evidence from data on listed enterprises in China. J. Innovation Knowl. 8 (1), 100332. doi:10.1016/J.JIK.2023.100332

Liu, X., Wang, E., and Cai, D. (2019). Green credit policy, property rights and debt financing: quasi-natural experimental evidence from China. Finance Res. Lett. 29 (03), 129–135. doi:10.1016/j.frl.2019.03.014

Luo, C., Fan, S., and Zhang, Q. (2017). Investigating the influence of green credit on operational efficiency and financial performance based on hybrid econometric models. Int. J. Financial Stud. 5 (4), 27. doi:10.3390/ijfs5040027

Nambisan, S., Wright, M., and Feldman, M. (2019). The digital transformation of innovation and entrepreneurship: progress, challenges and key themes. Res. policy 48 (8), 103773. doi:10.1016/j.respol.2019.03.018

Peng, B., Yan, W., Elahi, E., and Wan, A. (2022). Does the green credit policy affect the scale of corporate debt financing? Evidence from listed companies in heavy pollution industries in China. Environ. Sci. Pollut. Res. 29, 755–767. doi:10.1007/S11356-021-15587-7

Porter, M. E., and Linde, C. V. D. (1995). Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 9 (4), 97–118. doi:10.1257/jep.9.4.97

Qiu, L., Zhou, M., and Xu, W. (2017). Regulation, innovation, and firm selection: the porter hypothesis under monopolistic competition. J. Environ. Econ. Manag. 92 (11), 638–658. doi:10.1016/j.jeem.2017.08.012

Ramakrishnan, R., He, Q., and Black, A., (2016). Environmental regulations, innovation and firm performance: a revisit of the Porter hypothesis. J. Clean. Prod. 155 (2), 79–92. doi:10.1016/j.jclepro.2016.08.116

Udeagha, M. C., and Muchapondwa, E. (2023). Green finance, fintech, and environmental sustainability: fresh policy insights from the BRICS nations. Int. J. Sustain. Dev. World Ecol. 30, 633–649. doi:10.1080/13504509.2023.2183526

Wang, H., Qi, S., Zhou, C., Zhou, J., and Huang, X. (2022). Green credit policy, government behavior and green innovation quality of enterprises. J. Clean. Prod. 331, 129834. doi:10.1016/J.JCLEPRO.2021.129834

Wang, H., Wang, S., and Zheng, Y. (2023). China green credit policy and corporate green technology innovation: from the perspective of performance gap. Environ. Sci. Pollut. Res. Int. 30 (9), 24179–24191. doi:10.1007/S11356-022-23908-7

Wang, X., and Wang, Y. (2021). Research on the green innovation promoted by green credit policies (in Chinese). Manag. World 37, 173–218. doi:10.19744/j.cnki.11-1235/f.2021.0085

Wen, H., Lee, C., and Zhou, F. (2021). Green credit policy, credit allocation efficiency and upgrade of energy-intensive enterprises. Energy Econ. 94, 105099. doi:10.1016/J.ENECO.2021.105099

Wen, H., Wen, C., and Lee, C. C. (2022). Impact of digitalization and environmental regulation on total factor productivity. Inf. Econ. Policy 61, 101007. doi:10.1016/j.infoecopol.2022.101007

Wen, Z., and Ye, B. (2014). Analyses of mediating effects: the development of methods and models. Adv. Psychol. Sci. 22 (5), 731–745. doi:10.3724/sp.j.1042.2014.00731

Xiao, X. Y. (2020). “Research on the integration of digital economy and real economy to promote high-quality economic development,” in 2020 Management Science Informatization and Economic Innovation Development Conference (MSIEID), Guangzhou, China, 18-20 December 2020, 8–11. doi:10.1109/MSIEID52046.2020.00009

Xie, Q., Zhang, Y., and Chen, L. (2022). Does green credit policy promote innovation: a case of China. Manag. Decis. Econ. 43 (7), 2704–2714. doi:10.1002/MDE.3556

Yao, S., Pan, Y., Sensoy, A., Uddin, G. S., and Cheng, F. (2021). Green credit policy and firm performance: what we learn from China. Energy Econ. 101, 105415. doi:10.1016/J.ENECO.2021.105415

Zhang, C., Chen, P., and Hao, Y. (2022). The impact of digital transformation on corporate sustainability-new evidence from Chinese listed companies. Front. Environ. Sci. 10, 1047418. doi:10.3389/fenvs.2022.1047418

Keywords: green credit policy, digital transformation, heavy polluting business, differencein-differences model, green development

Citation: Gu X and Wang Y (2023) Green credit policy and digital transformation of polluting firms: a quasi-natural experiment from China. Front. Environ. Sci. 11:1281165. doi: 10.3389/fenvs.2023.1281165

Received: 22 August 2023; Accepted: 04 December 2023;

Published: 20 December 2023.

Edited by:

Marius Dan Gavriletea, Babes-Bolyai University Faculty of Business, RomaniaReviewed by:

Bin Xu, Xiamen University, ChinaCopyright © 2023 Gu and Wang. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Yiling Wang, d2FuZ3lpbGluZzIwMDJAMTYzLmNvbQ==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.