Huaiming Wang1†

Huaiming Wang1† Xiaojian Tang

Xiaojian Tang

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 30 October 2023

Sec. Environmental Economics and Management

Volume 11 - 2023 | https://doi.org/10.3389/fenvs.2023.1273564

This study investigates the impact of the green finance pilot reform on corporate green innovation using the formation of the China Green Finance Pilot Reform in 2017 as a quasi-natural experiment. It shows that the green finance pilot reform increases corporate green innovation. Furthermore, by highlighting the differences between green enterprises and heavily polluting enterprises, it also shows that the positive relationship between the green finance pilot reform and corporate green innovation is more pronounced in green enterprises than in heavily polluting enterprises. The mechanism analysis shows that the green finance pilot reform mainly affects corporate green innovation by easing financing constraints and reducing financing costs. The heterogeneity analysis indicates that the positive relationship between the green finance pilot reform and corporate green innovation is more pronounced in non-state-owned enterprises and large-scale enterprises. As a result, the effect of the green finance pilot reform on corporate green innovation gives rise to certain green innovation incentives. It is thus necessary to optimise the external corporate governance environment by promoting the green finance pilot reform and further offers practical implications for corporate green innovation decision-making.

This study examines the relationship between green finance pilot reform on corporate green innovation. It is particularly relevant in China, where green finance pilot reform has been implemented because of serious environmental protection problems (Cheng et al., 2022). For instance, in order to maintain its rapid economic growth, China, the world’s second-largest economy, needs to tackle numerous major environmental protection issues, such as carbon emissions (Tolliver et al., 2021; Xu et al., 2023). By creating green finances, the Chinese government has fortunately made some strides in environmental governance (Han et al., 2022). That is, the Chinese government has employed green financing to encourage businesses to increase green innovation and further safeguard the environment while also reducing carbon emissions. Furthermore, China’s experience with green finance may have some ramifications for other countries, particularly for developing countries that struggle with challenging environmental protection issues as their economies develop.

According to theory, sustainable development is the ultimate goal of green finance, which also incorporates the idea of environmental protection. Prior studies show that green finance can guide financial system funding to flow from polluting fields to green fields and attract a large amount of social funding to green fields (Zhou et al., 2020; Chen et al., 2021). Additionally, green finance can also help promote green development and achieve high-quality economic development (Lee and Lee, 2022). However, fewer studies focus on the effect of green finance on corporate green innovation based on a quasi-natural experiment from Green Finance Pilot Reform in order to overcome the endogeneity effect, especially by differentiating green enterprises and polluting enterprises. In fact, as one of the main bodies of the micro-economy, enterprises not only play a vital role in high-quality economic development but also have a great impact on the ecological environment. Innovation is the primary driving force. It is necessary to continuously improve corporate independent technological innovation capabilities and gradually cultivate their competitiveness with technological innovation as the core (Du et al., 2022).

In view of the current lack of green innovation in corporate development, which leads to low-quality corporate development, green financial policy can force enterprises to adopt environmental protection technology and engage in environmental management innovation activities by restricting the flow of funds to enterprises. In addition, innovation activities have a value-added effect, and technological innovation leads to the emergence of new production processes and production tools. Among them, green innovation can help accelerate energy conservation and emissions reduction, promote green transformation, and become an important driving force for enterprises to improve their own competitive advantages. At the same time, the literature has shown that corporate green innovation can promote high-quality economic development by reducing environmental pollution (Lee and Lee, 2022).

Moreover, although some prior studies has explored the relationship between the green finance and corporate green innovation, there are still some drawbacks as follows. Firstly, some prior studies mainly focus on the different effect of green finance on green innovation from the notion that whether the firms are heavily polluting enterprises or not (e.g., Han et al., 2022; Dong et al., 2022; Yan et al., 2022; Zhao et al., 2022; Zhang and Li, 2022; Liu and Wang, 2023; Xu et al., 2023). For example, Han et al. (2022) show that green finance can positively increase green innovation in heavily polluting enterprises. Furthermore, other prior studies simply consider the overall effect of green finance on green innovation in all enterprises (Dai et al., 2022; Yu et al., 2021; Huang et al., 2022a; Zhang et al., 2023; Gao et al., 2023; Xu, 2023) and neglect that green finance may be suitable for specific enterprises so that the research results may be biased. As a result, fewer studies focus on the effect of green finance on green innovation from green enterprises. In fact, green finance policy strictly recognize that whether the firms are green enterprises1 or not and further are more beneficial to green enterprises’ financing and high-quality development while heavily polluting enterprises may not meet the requirements of green finance policy because of their heavily polluting nature. And it is also necessary to clarify the different effect of green finance on green innovation between green enterprises and heavily polluting enterprises.

Secondly, other prior studies mainly show that green finance can impact green innovation. (e.g., Wang, 2022; Dai et al., 2022; Yu et al., 2021; Huang et al., 2022a; Wang K. H. et al., 2022; Huang et al., 2022a; Irfan et al., 2022; Wang et al., 2022b; Yang et al., 2022; Huang et al., 2022b; Zhang et al., 2023; Gao et al., 2023; Xu, 2023; Tian et al., 2023). For example, Yang et al. (2022) show that external environmental regulation can impact the relationship between green finance and green innovation. Irfan et al. (2022) find that external regional policy intervention can moderate the effect of green finance on green innovation. Tian et al. (2023) show that fintech can strengthen the relationship between green finance and green innovation. In total, these studies fail to show that how green finance impact green innovation based on corporate governance mechanisms. In fact, green finance may also impact green innovation through internal corporate governance mechanisms.

Therefore, this study examines the effect of green finance pilot reform on corporate green innovation in China. Especially, this study clarify the different effect of green finance on green innovation between green enterprises and heavily polluting enterprises. Specifically, to promote the development of green finance, the Chinese government has introduced a series of policies and measures. Among them, in August 2016, seven ministries and commissions, including the People’s Bank of China and the Ministry of Finance, issued the ‘Guiding Opinions on Building a Green Financial System’, which is a programmatic document for the development of green finance in China. In addition, at the executive meeting of the State Council in June 2017, certain areas of Guangzhou, Zhejiang, Jiangxi, Xinjiang, and Guizhou were selected as green financial reform and innovation pilot areas with their own characteristics and emphases. This is known as the Green Finance Reform and Innovation Pilot Zone programme. In these areas, innovative models and mechanisms of green finance are explored to promote the development of green innovation. In 2019, Gansu was approved to join the second batch of green finance pilot reforms, and in August 2022, the Chongqing Green Finance Pilot Reform was officially launched.

As a result, this study takes the establishment of China Green Finance Pilot Reform in 2017 as a quasi-natural experiment to empirically test whether the reform significantly affects the green innovation of enterprises. It finds that the green finance pilot reform significantly promotes the green innovation of enterprises in the pilot area, and it identifies an industry differentiation effect. In total, it shows that the positive relationship between the green finance pilot reform and corporate green innovation is more pronounced in green enterprises than in polluting enterprises. A mechanism analysis shows that the green finance pilot reform mainly affects the green innovation of enterprises by alleviating financing constraints and reducing financing costs. In addition, the positive impact of the green finance pilot reform on corporate green innovation is greatest for non-state-owned and large-scale enterprises. This shows that there is an innovation incentive effect on the impact of the green finance pilot reform on the green innovation of enterprises.

This paper makes the following contributions. Firstly, although some prior studies has explored the relationship between the green finance and corporate green innovation (e.g., Han et al., 2022; Dong et al., 2022; Yan et al., 2022), fewer studies focus on the effect of green finance on green innovation from green enterprises. Moreover, these studies fail to show that how green finance impact green innovation based on corporate governance mechanisms. Therefore, this study further examines the different effect of green finance pilot policies on corporate green innovation between green enterprises and heavily polluting enterprises. In total, it supplements and improves the literature on the resource reallocation effects of green finance pilot reform policies and further provides recommendations for green finance policy evaluation and improvement.

Secondly, prior studies mainly focus on the effect of corporate governance on green innovation (e.g., Amore and Bennedsen, 2016; Asni and Agustia, 2022; Yu et al., 2022). However, fewer studies consider the effect of external green finance pilot policies on green innovation. Therefore, this study explores the effect of external green finance pilot policies on green innovation and further examines the different effect between green enterprises and heavily polluting enterprises. In total, this study expands the research perspective of corporate green innovation and enriches the literature on corporate green innovation.

Third, the findings offer meaningful and valuable implications about the effect of green finance on green innovation around the world, especially for emerging markets. Specifically, this study shows that green finance pilot reform can increase green innovation and further finds that the positive relationship between the green finance pilot reform and corporate green innovation is more pronounced in green enterprises than in polluting enterprises. As a result, it is necessary to optimise the external governance environment of enterprises and promote the green innovation decisions of enterprises by deepening the green finance pilot reform. Specifically, this study reveals that the effect of the green finance pilot reform on corporate green innovation gives rise to certain innovation incentives when we encounter troublesome environmental protection problems in the economic development especially for emerging markets.

The national Green Finance Pilot Reform programme is an important measure that organically combines the ‘top-down’ policy promotion of China’s green financial reform with ‘bottom-up’ reform and innovation. In August 2016, seven ministries and commissions, including the People’s Bank of China, issued the ‘Guiding Opinions on Building a Green Financial System’, establishing an overall strategic framework for the development of green finance. Based on this, considering the stage of economic development, the characteristics of the spatial layout, and previous green financial practices, in June 2017, the State Council approved the first batch of green financial reform and innovation pilot zones in eight locations across five provinces, namely, Huzhou City and Quzhou City in Zhejiang Province; Guangzhou City in Guangdong Province; Ganjiang New District in Jiangxi Province; Gui’an New District in Guizhou Province; and Karamay City, Hami City, and Changji Prefecture in Xinjiang. In December 2019, the Green Finance Reform and Innovation Pilot Zone initiative was expanded for the first time, to Lanzhou New District in Gansu Province. In August 2022, the Chongqing Green Finance Reform and Innovation Pilot Zone was officially launched. Green finance reform and innovation test zones have been approved, and the systems implemented in each test zone have been targeted based on commonalities and are closely integrated with local development conditions.

The reform and innovation provided by the green finance pilot programme have led to remarkable results. As of September 2022, 231 green specialised institutions had been established in the green finance pilot reform zones, and intermediary services have been gradually improved. From a practical point of view, it is manifested in the following aspects. The first is the development of green financial instruments in a diversified direction. In the pilot zones, a green product system with green credit and bonds as the mainstay and diversified development of other green financial instruments will be gradually established. As of the end of 2021, the green loan balance of the province (region) in which a pilot zone is located was 4.7 trillion yuan, accounting for 29% of the national green loan balance, and the number of green bonds issued was 1,134, accounting for 26% of the national green bond issuance. The second is the innovation of the loan issuance model and the promotion of the green transformation of enterprises. For example, in Huzhou, a ‘Continued Loan Link’ system and a loan interest discount mechanism have been established to reduce corporate financing costs and financial pressure. Since its launch in May 2018, the ‘Green Loan Link’ has helped 30,400 companies obtain bank credit of over 300 billion yuan. As of April 2020, the Huzhou branch has newly approved 5.647 billion yuan of credit through the ‘Green Enterprise Loan’ product, reducing interest expenses by more than 20 million yuan for more than 250 enterprises. The third is the improvement of fiscal and taxation incentive policies and supervision mechanisms. The proportion of special guidance documents, such as green financial risk guarantee and compensation mechanisms, is 40 percentage points higher in test areas than in non-test areas.

The compensation and incentive measures implemented in the two reform zone cities in Zhejiang are the most comprehensive and detailed; other provinces are gradually introducing incentive policies that can quantify the performance of enterprises. For example, Zhejiang divide green enterprises into ‘dark green’, ‘medium green’, and ‘light green’ grades. Huzhou provides loan discounts at 12%, 9%, and 6% of the benchmark interest rate, while Quzhou provides 15% and 6% of the LPR at the end of the previous year loan discount. In general, the promulgation and implementation of these green finance systems provide a more realistic research scenario for exploring the impact of green finance on the financial behaviour of micro-enterprises.

Green finance has the dual characteristics of financial resource allocation and environmental regulation (Tolliver et al., 2021). Many studies have discussed the environmental governance function and effect of green finance (e.g., Dai et al., 2022; Umar and Safi, 2023; Gao et al., 2023; Tian et al., 2023). Among them, the economic effects of green financial policies related to this paper on the micro-enterprise level have mostly been reflected in research on green credit policies. Some scholars have taken environmental protection enterprises as research objects and have found that the development of environmental protection industries cannot be separated from the support of green finance (Cui and Huang, 2018; Huang, 2022), with such support mainly involving long-term capital investment. Green credit policy improves the financing convenience of green enterprises and the market-oriented credit interest rate and its fluctuations can enhance green enterprise financing (Jin et al., 2021). Furthermore, green enterprises bear lower debt financing costs (Li et al., 2022; Shi et al., 2022). Other scholars, taking the perspective of polluting enterprises, have found that the interest-bearing debt financing and long-term liabilities of heavily polluting enterprises decrease significantly after green credit policy implementation, and the increase in debt financing costs lead to a decline in their operating performance (Wang et al., 2022a). That is, polluting enterprises have financing penalty effects and investment inhibition effects. However, some scholars have found that green credit policy can reduce agency costs and improve investment efficiency (He et al., 2019).

The above literature indicates that green finance pilot reform policy plays a positive role in improving corporate governance, influencing corporate financing behaviour, enhancing the green carbon reduction mission of enterprises and their regions, and protecting the environment. Research on green finance must pay more attention to how to effectively guide the flow of funds to resource saving and ecological and environmental protection to further accelerate the transformation of economic development and better promote the construction of ecological civilization.

Furthermore, green innovation is an important way for enterprises to reduce pollution and achieve high-quality development. Many studies have analysed the influencing factors of corporate green innovation. At the level of internal enterprise characteristics, enterprises with rich green innovation experience, green dynamic capabilities, and strong green transformation leadership can significantly improve their green creativity and green product development performance (Chen and Chang, 2013; Amore and Bennedsen, 2016). In addition, executive characteristics, firm size, profitability, and R&D investment all have an impact on corporate innovation (Claessens and Yurtoglu, 2013; Fang et al., 2021).

In terms of the external environment of enterprises, reasonable environmental regulations can stimulate enterprise innovation and improve the market competitiveness of enterprises. Environmental regulations such as low-carbon pilot city policies and pilot emissions trading policies can significantly improve the green innovation of heavily polluting enterprises, thus verifying the Porter hypothesis (Porter and Linde, 1995). However, some scholars have reached the opposite conclusion, specifically that environmental regulatory tools such as green finance significantly inhibit the green innovation of heavily polluting enterprises (Ramanathan et al., 2010). According to such scholars, the additional costs paid by such enterprises under the pressure of environmental regulations put pressure on their production and operations, thereby weakening their market competitiveness and inhibiting their R&D (Levinson and Taylor, 2008; Van Leeuwen and Mohnen, 2017).

Moreover, some prior studies focus on the effect of green finance on green innovation in heavily polluting enterprises (e.g., Han et al., 2022; Dong et al., 2022; Yan et al., 2022; Zhao et al., 2022; Zhang and Li, 2022; Liu and Wang, 2023; Xu et al., 2023). And other prior studies simply consider the overall effect of green finance on green innovation in all enterprises (Dai et al., 2022; Yu et al., 2021; Huang et al., 2022a; Yang et al., 2022; Irfan et al., 2022; Tian et al., 2023; Zhang et al., 2023; Gao et al., 2023; Xu, 2023). For example, Yang et al. (2022) show that external environmental regulation can impact the relationship between green finance and green innovation. Irfan et al. (2022) find that external regional policy intervention can moderate the effect of green finance on green innovation. Tian et al. (2023) show that fintech can strengthen the relationship between green finance and green innovation. However, the above studies neglect that green finance may be suitable for specific enterprises so that the research results may be biased. That is, fewer studies focus on the effect of green finance on green innovation from green enterprises. In fact, green finance policy strictly recognize that whether the firms are green enterprises or not and further are more beneficial to green enterprises’ financing and high-quality development while heavily polluting enterprises may not meet the requirements of green finance policy because of their heavily polluting nature. And it is necessary to clarify the different effect of green finance on green innovation between green enterprises and heavily polluting enterprises.

In summary, based on this review of the two streams of research on the micro-effects of green finance and the influencing factors of corporate green innovation, previous studies have paid relatively little attention to the impact of green finance on corporate green innovation especially from green enterprises. Few studies have separated enterprises of different types (i.e., green enterprises vs. heavily polluting enterprises) to observe the differential impact of green finance on their respective green innovation. Therefore, based on the green finance pilot reform implemented by the State Council in 2017, this study explores the different impact of green finance on corporate green innovation between green enterprises and heavily polluting enterprises, seeking to determine how to optimise enterprises’ external governance environment by extending the green finance pilot reform and ultimately promoting enterprises’ green innovation decision-making.

In practice, green finance optimises the allocation of financial resources under the sustainable development goals by reducing the adverse impact on ecological environment pollution (Zhou et al., 2020). For example, green finance can resolve the problems of financing constraints for green enterprises (Yu et al., 2021) and further offer more free cash flow for corporate innovation (Umar and Safi, 2023), which is beneficial for ecological environment protection. Therefore, in view of prior literature review, China’s Green Finance Reform and Innovation Pilot Zone policy is an important way to promote green financial reform. The pilot area initiative focuses on innovation and development in the following three directions. The first direction is building a green product system with diversified development and broadening the financing channels and scale of green development among enterprises. This can be done by developing innovative loan issuance models, issuing green bonds, and securitising assets to solve corporate financing difficulties and promote enterprises’ green transformation. The second direction is providing services for the green transformation of enterprises by accelerating the gathering of specialised green finance institutions and building a comprehensive green finance service platform. The establishment of the service platform not only alleviates the problem of green financial information asymmetry but also improves the efficiency of multi-party cooperation between the government, enterprises, and banks and promotes the operation of green investment and financing. The third direction is improving fiscal and taxation incentive policies and supervision mechanisms. The establishment of each pilot zone has reduced the burden on market players, such as through interest discounts, incentives and subsidies, landing subsidies, and preferential tax policies for enterprises. In summary, the establishment of the pilot zones has had a positive resource reallocation effect and promoted the innovation and development of enterprises through the debt financing mechanism. The pilot zone initiative provides convenient financing channels for the green development of enterprises, increases the scale of financing, and promotes the provision of green services by financial institutions to enterprises. It has also strengthened the government’s fiscal and taxation incentive policies and supervision mechanisms, increased the cost of corporate pollution emissions, and prevented green financial risks.

Theoretically, by guiding the allocation of financial resources, green finance allows funds within the financial system to flow from polluting areas to green areas, producing a positive market selection effect and a significant market share reconfiguration effect (Lee et al., 2023), fundamentally eliminating environmental pollution and achieving the goal of ecological environment governance (Lee and Lee, 2022). The green finance pilot policy emphasises interest discounts on loans to green enterprises, improving the availability of financing for green enterprises to better expand production scale and improve the level of green innovation, while increasing financing costs and credit constraints on heavily polluting enterprises to force their green transition (Li et al., 2022; Shi et al., 2022). Studies have shown that the environmental regulation provided by green finance also has ‘innovation compensation effects’ on enterprises (Porter and Linde, 1995). That is, when the innovation compensation effect produced by the environmental regulation of green finance is greater than the cost effect of institutional constraints, the environmental regulation of green finance will generate excess returns for enterprises (Alpay et al., 2002). Therefore, the green finance pilot reform is likely to guide the flow of financial resources to enterprises with green technology transformation through the ‘capital allocation mechanism’, thereby generating innovation incentives for the green technology transformation of enterprises.

Overall, green finance pilot reform areas have not only formed a policy system with full coverage but also implemented special policy incentives. The implementation of these policies compensates for the shortcomings of large initial investments in green innovation funds, long profit cycles, and unpredictable risks, and provides financial support for the development of enterprises’ green innovation (Du et al., 2022). At the same time, the green innovation of enterprises can improve local environmental and social performance as well as enterprises’ own financial performance (Lee and Lee, 2022). While fulfilling their social responsibilities, enterprises can gain a ‘reputation effect’ and simultaneously enhance their own market competitiveness, which is beneficial for their sustainable development. Based on the debt financing mechanism and capital allocation mechanism perspectives, the green finance pilot reform can be expected to promote enterprises’ green innovation and development. Therefore, the following hypothesis is proposed:

H1:. The green finance pilot reform significantly promotes enterprises’ green innovation.

This paper takes A-share listed companies from 2013 to 2019 as the research object. With reference to previous literature, observations are removed from the overall sample if they pertain to 1) listed companies in the financial and insurance industries, as their report structure differs from those of other industries; 2) the observed value of a company’s IPO in the year and companies listed in 2017 and later; 3) listed companies with asset-liability ratios less than 0 and greater than 1; and 4) ST and *ST listed companies with abnormal transactions and listed companies missing relevant data.

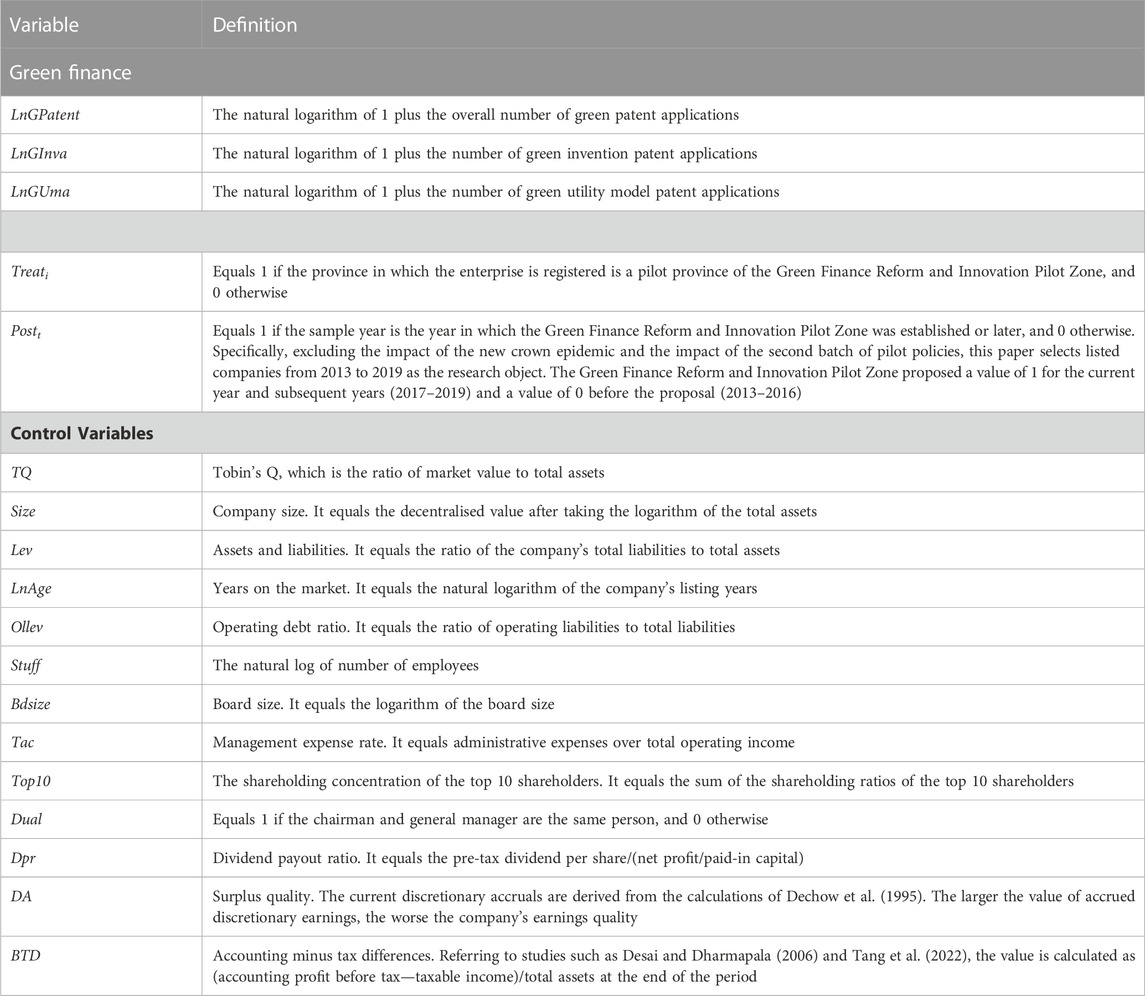

This study includes two main types of data: enterprise innovation data and green patent data. The green patent data come from the Chinese Research Data Services database (CNRDS). The paper further distinguishes between green invention patents and green utility model patents, as they differ in innovation and application value. It is generally believed that green invention patents have higher innovation value than green utility model patents; that is, a company with more invention patents is believed to have higher innovation quality. The paper also includes data on the characteristics of other companies. The main financial data come from the China Stock Market & Accounting Research database. The main continuous variables are processed at the 1% and 99% quantile levels.

This paper examines the impact of green finance pilot reform on corporate green innovation under different industry characteristics. To reduce the interference of different factors, such as enterprise characteristics, industry characteristics, and the economic environment, on the analysis results, double difference and triple difference models are used in the analysis. The following double difference model is constructed to test the impact of the green financial reform and innovation pilot areas on green innovation:

where the dependent variable LnGpatentit measures the green innovation of enterprise i in year t. Green patents can directly reflect the output of enterprises’ green innovation activities. The patent index construction method uses the number of green patent applications of listed companies to measure innovation output. To avoid the influence of zero values and the right-skewed distribution of green patent application data, the number of green patents applied by listed companies in year t + 1 is used for logarithmic processing. The indicators of the number of green patent applications include green patents as a whole (LnGPatent), green invention patents (LnGInva), and green utility model patents (LnGUma). Xit denotes a series of enterprise-level control variables, defined in detail in Table 1 μi is the individual fixed effect, νt is the time fixed effect, and ξit is the random disturbance term. This paper focuses on the coefficient β1 of the interaction term between Treati and Postt, which measures the net impact of pilot policies on corporate green innovation.

TABLE 1. Variables.

In the presence of heterogeneous treatment effects, triple differences are more informative than double differences and may produce more convincing results than traditional DID analysis (Gruber, 1994; Angrist and Pischke, 2008; Frolich and Sperlich, 2019; Olden and Møen, 2022). The green finance pilot policy may pay more attention to green enterprises and heavily polluting enterprises during the implementation process, and it has different impacts on green enterprises and heavily polluting enterprises. Thus, on the basis of using the double difference model to measure the impact of external shocks on the green innovation of enterprises, this paper constructs a triple difference model to test whether the green innovation of enterprises in different industries in the pilot provinces differs after the implementation of the policy. Furthermore, this study explores the green innovation development effect of green enterprises by taking environmental protection concept stocks as samples. According to the conceptual classification of Chinese listed companies in the Wind database, companies in 35 conceptual sectors, such as energy conservation and environmental protection, photovoltaics, beautiful China, wind power generation, nuclear energy nuclear power, green energy-saving lighting, and building energy conservation, are defined as green enterprises (Gcj = 1). This paper takes whether an enterprise belongs to this type of industry as the third difference to construct the triple difference item Treati×Postt×Gcj to test the impact of green finance policy on green energy in the pilot areas. The estimation equation for the promotion effect of the green innovation of enterprises is set as follows:

Moreover, it is mainly based on the ‘Guidelines for the Industry Classification of Listed Companies’, revised by the China Securities Regulatory Commission in 2012, the ‘List of Listed Companies’ Environmental Protection Verification Industry Classification Management List’, formulated by the Ministry of Environmental Protection in 2008 (Environmental Protection Office Letter [2008] No.373), and the ‘Guidelines for Environmental Information Disclosure of Listed Companies’ (Environmental Information Disclosure [2010] No. 78), mainly including thermal power, steel, cement, electrolytic aluminium, coal, metallurgy, chemical industry, petrochemicals, building materials, papermaking, brewing, pharmaceuticals, and fermentation. Sixteen types of industries, such as textiles, leather, and mining, are identified as having heavily polluting enterprises (Hcj = 1). Therefore, this paper takes whether an enterprise belongs to this type of industry enterprise as the third difference and examines the promotion of green innovation of heavily polluting enterprises in the pilot areas after the implementation of the green financial policy. The estimation equation is set as follows:

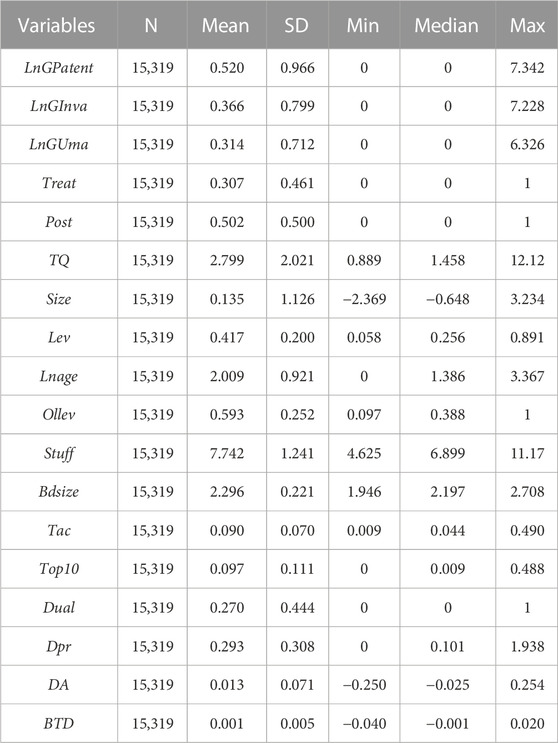

Table 2 shows the descriptive statistics of the main study variables. The average value of LnGPatent is 0.520, the maximum value is 7.342, the minimum value is 0, and the standard deviation is 0.966, indicating large differences in the level of green innovation among different enterprises. The mean value of Post is 0.5205, indicating that the sample size before and after the pilot is relatively balanced. The mean value of Treat is 0.307, indicating that the proportion of samples in the pilot areas is 30.7%.

TABLE 2. Descriptive statistics.

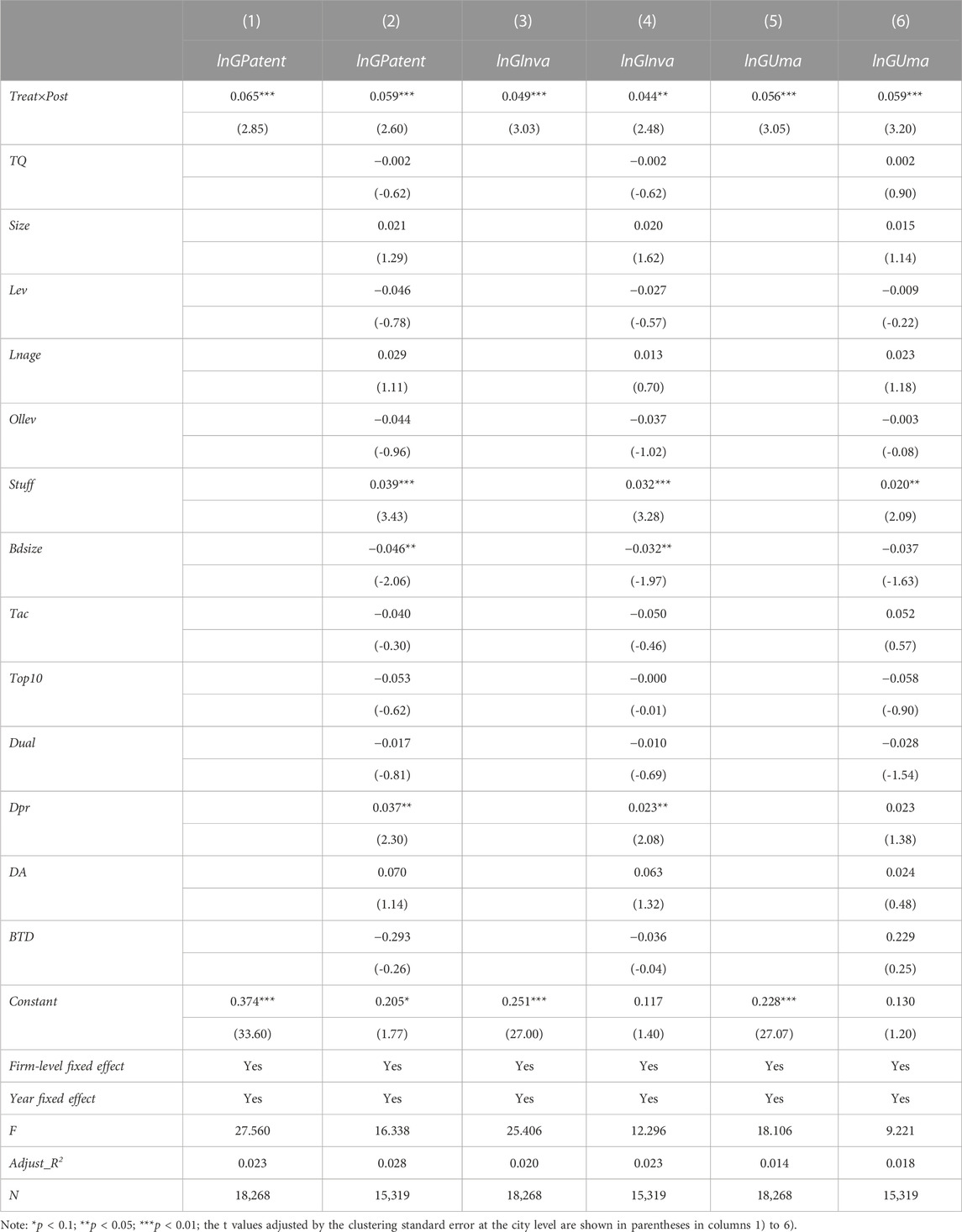

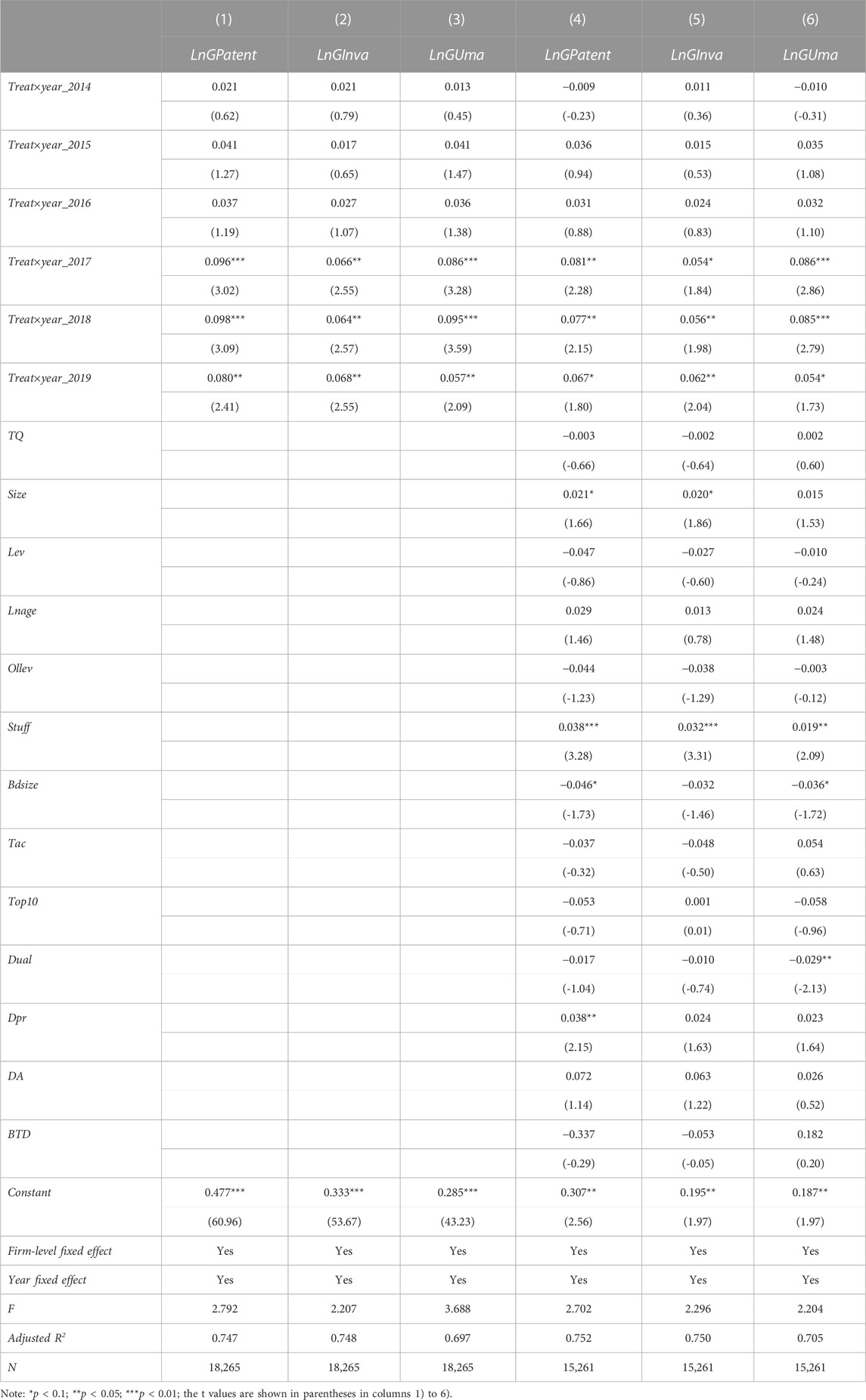

In this section, the double difference method is used to evaluate the impact of the green finance pilot reform on the green innovation of the full sample of enterprises. Table 3 presents the estimated results. Columns 1) and 2) report the regression results for total green innovation, columns 3) and 4) report the regression results for green invention patents, and columns 5) and 6) report the regression results for the green utility model patents. Among them, models 2), 4), and 6) include control variables on the basis of models 1), 3), and 5), respectively. The results show that regardless of whether the control variables are included, the implementation of the green finance pilot reform can promote green innovation in regional enterprises. In columns 1) and 2), the coefficients of the interaction item Treat×Post are both positive and significant at the 1% level, indicating that the green finance pilot reform has significantly increased the green innovation output of enterprises in the pilot areas. In columns 3) and 4), the coefficients of the cross-product item Treat×Post are both positive and significant at the 1% level, indicating that the green finance pilot reform has significantly improved the green innovation quality of enterprises in the pilot areas. In columns 5) and 6), the coefficients of the cross-product item Treat×Post are both positive and significant at the 1% level, indicating that the green finance pilot reform has significantly increased the green innovation output of enterprises in the pilot areas. In summary, H1 is supported. The empirical results show that the green finance pilot reform has significantly promoted the green innovation of enterprises in the green finance pilot provinces.

TABLE 3. Green finance pilot policy and green innovation at the overall enterprise level.

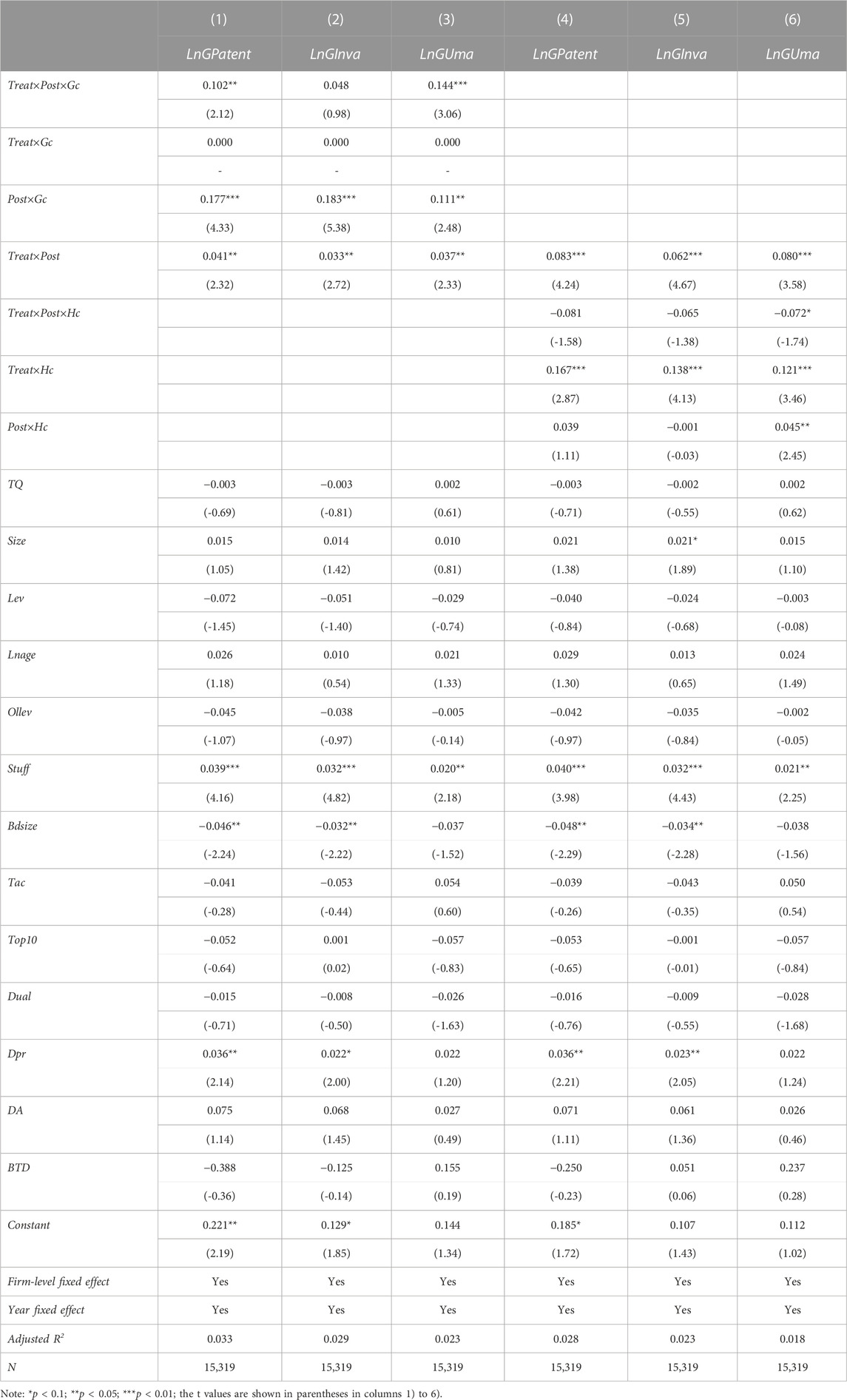

In this section, the triple difference method is used to evaluate the impact of the green finance pilot reform on the green innovation between green enterprises and heavily polluting enterprises. Table 4 presents the estimated results in green enterprises. Column 1) shows the results of the regression of the green finance pilot reform on the total number of green patent applications and indicates that the green finance pilot reform can significantly positively increase the total number of green patent applications in green enterprises. Column 3) shows the results of the regression of the green finance pilot reform on the total number of green utility model patents and indicates that the green finance pilot reform can significantly positively increase the total number of green utility model patents in green enterprises. Furthermore, although Column 2) shows the insignificantly positive results of the regression of the green finance pilot reform on the total number of green invention patents in green enterprises, the above results indicates the green finance pilot reform can increase corporate green innovation in green enterprises.

TABLE 4. Impact of green innovation on enterprises in different industries.

In addition, columns 4) to 6) show the results of regressing the green finance pilot reform on the total number of green patent applications, green invention patents, and green utility model patents in heavily polluting enterprises. Column 4) shows the results of the regression of the green finance pilot reform on the total number of green patent applications and indicates that the green finance pilot reform insignificantly negatively decrease the total number of green patent applications in heavily polluting enterprises. Column 5) shows the results of the regression of the green finance pilot reform on the total number of green invention patents and indicates that the green finance pilot reform insignificantly negatively decrease the total number of green invention patents in heavily polluting enterprises. Furthermore, Column 6) shows the significantly negative results of the regression of the green finance pilot reform on the total number of green utility model patents. In total, the above results indicates the green finance pilot reform may decrease corporate green innovation in heavily polluting enterprises. As a result, the positive relationship between the green finance pilot reform and corporate green innovation is more pronounced in green enterprises than in heavily polluting enterprises.

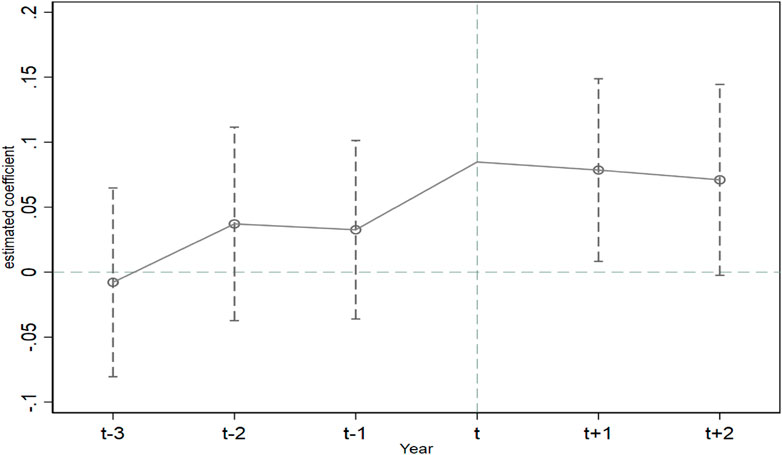

The implication of the parallel trend assumption is that before the implementation of the green finance pilot policy, the time trends of green patent applications in green finance pilot cities and non-green finance pilot cities are as consistent as possible. In Figure 1, the horizontal axis represents time and the vertical axis represents the number of green patent applications. Taking 2017 as the dividing line, before the green financial policy pilot, the green patent application curves of the experimental group and the control group are basically parallel. This shows that the change trend of green application patents is the same for the two groups of enterprises. After 2017, the number of green patent applications of enterprises in the experimental group increases significantly.

FIGURE 1. Parallel trend analysis.

The following model is used for parallel trend testing:

The method used by Beck et al. (2010) is adopted to decompose the dynamic trend of the overall impact of green finance pilot reforms on corporate green patent applications and the impact on green invention patents and green utility model patents between years through graphical methods. Specifically, this paper sets the year dummy variables year_2014, year_2015, year_2016, year_2017, year_2018, and year_2019, which equal 1 in 2014, 2015, 2016, 2017, 2018, and 2019, respectively, and 0 otherwise. Each dummy variable is then interacted with the grouping variable Treat. According to the results in Table 5, before the green finance pilot reform, the interaction coefficient between the experimental group and the control group is not significant, regardless of whether control variables are considered. However, after the green finance pilot reform, the coefficients of the interaction terms are all positive and significant. This indicates that the green finance pilot reform has significantly promoted green innovation. The empirical research in this paper supports the assumption of the difference model for parallel trends.

TABLE 5. Parallel trend and dynamic effect tests.

Each province and city independently apply for selection as green finance pilot reform test areas, and they are then considered by the National Development and Reform Commission. The initial conditions of pilot cities and non-pilot cities may differ. In addition, the treatment and control groups studied in this paper come from enterprises in different industries, and thus their individual characteristics may differ. To avoid selection bias when using the DID method, DID based on propensity score matching (PSM), or PSM-DID, is used for further testing. Specifically, a logit model is used to estimate the propensity score, taking the control variables, such as the size of the enterprise (Size), profitability (Tobin’s Q), the asset-liability ratio (Lev), and listing age (Lnage), as characteristic variables. In addition, the nearest neighbour one-to-one matching method is used to determine the weights to match the samples of the treatment and control groups. At the same time, the condition of ‘common support’ is imposed to regress model 1). As shown in column 1) of Table 6, the regression coefficient of the cross-product item Treat×Post is positive and significant at the 10% level. Thus, the green finance pilot has improved the green innovation of enterprises as a whole. However, the results in columns 2) and 3) of Table 6 show that this improvement is mainly reflected in the improvement of green invention patents, indicating that green financial policies can indeed improve the quality of enterprises’ green innovation. The baseline conclusion holds after excluding the differences in enterprise characteristics between the treatment and control groups and the differences in the pilot provinces, consistent with the results reported in Table 3.

TABLE 6. PSM-DID regression.

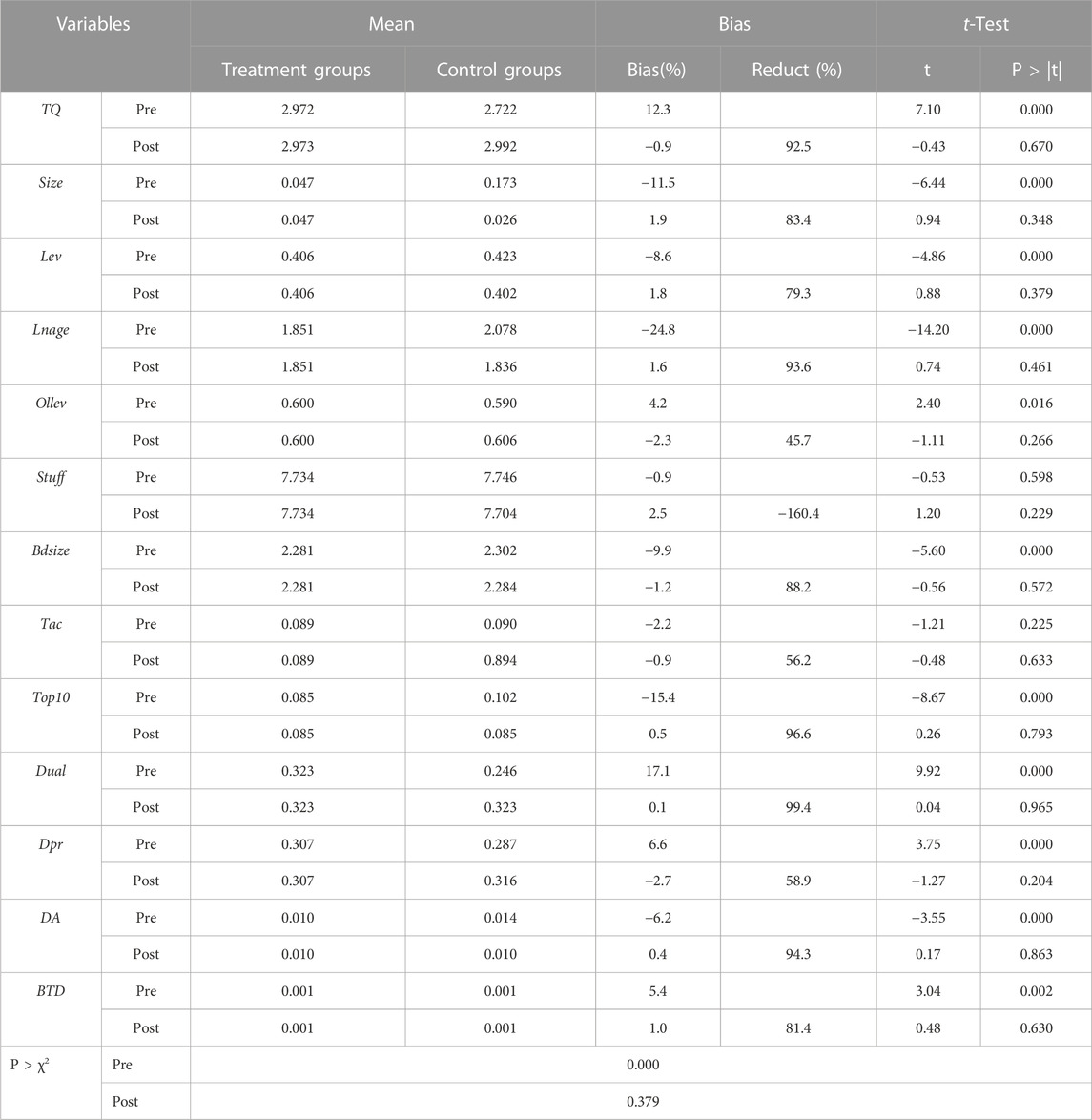

As PSM makes the characteristics of individuals in the treatment and control groups as similar as possible, the selection bias of the experimental effect is well resolved. Table 7 shows the results of the PSM balance test. After processing, the absolute value of the standard deviations of variables such as company size (Size), profitability (Tobin’s Q), listing age (Lnage), top 10 shareholders’ ownership concentration (Top10), and job duality (Dual) demonstrates a large decrease. This indicates that after PSM, there is no significant difference between the variables in the treatment and control groups. In addition, the difference in the mean values of the characteristic variables between the treatment and control group samples after matching become nonsignificant, with P > χ2 changing from 0.000 to 0.974. This confirms the appropriateness of the selected matching variables and matching methods.

TABLE 7. PSM-balance test.

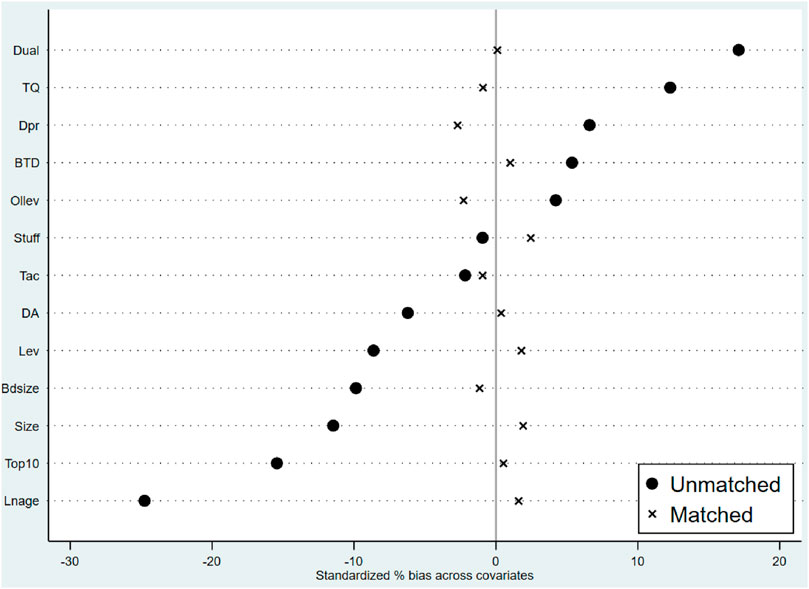

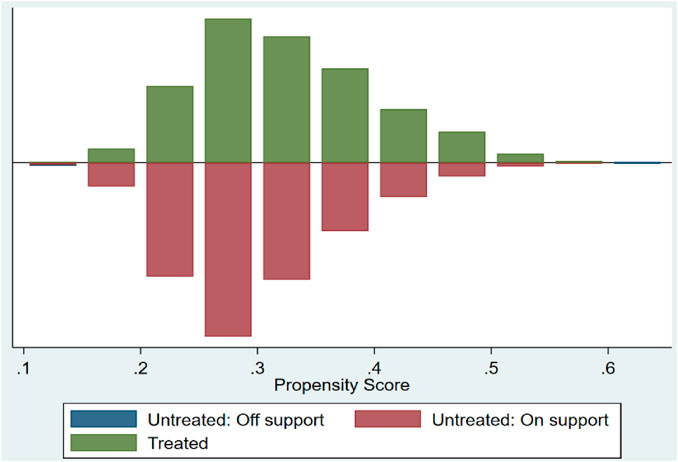

Figure 2 shows that the bias of all of the covariates is less than 10% before and after matching and is significantly smaller than their %bias before matching. The absolute value of %bias decreases by 45.7%–99.4% compared with before matching. The null hypothesis (i.e., that there is no systematic deviation in the values of covariates between the two groups) is not rejected, indicating that the PSM results well balance the data. The bar graph in Figure 3 shows that all the treatment group samples are within the common value range, and most of the samples in the treatment and control groups (support) are within the common value range.

FIGURE 2. Test of covariate balance for standardized deviation measurement.

FIGURE 3. Propensity scores match the common value range.

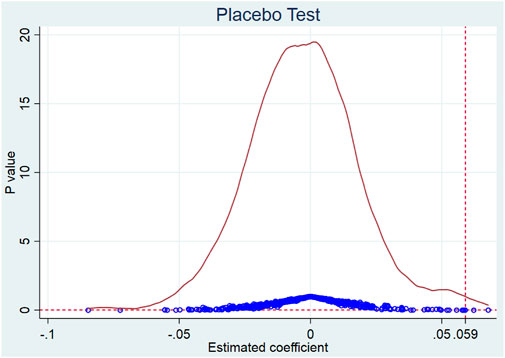

To further reduce the influence of other factors on the empirical results, the research methods of Chetty et al. (2009) are adopted, and the results are revalidated by randomly generating a placebo method of reformed individuals. Specifically, the sampling number is 1,027; that is, 1,027 of the listed companies (from the five sampled provinces) selected in the main regression are used as the virtual treatment group; in each round, 1,027 listed companies are randomly selected from the full sample as the virtual treatment group and the remainder are the control group. Regression is performed according to model 1). To further randomise the grouping, the above steps are repeated 500 times. Figure 4 shows the distribution of the estimated value of the DID coefficient of the double-difference cross-product item in 500 estimates, where the vertical line represents the regression results corresponding to column 2) of Table 3. The probability that the absolute value of the estimated value of the coefficient obtained by virtual grouping is greater than the regression result of real grouping is very low, showing a normal distribution with 0 as the mean and thus further proving the robustness of the baseline conclusion.

FIGURE 4. Coefficient distribution plot of DID in random grouping.

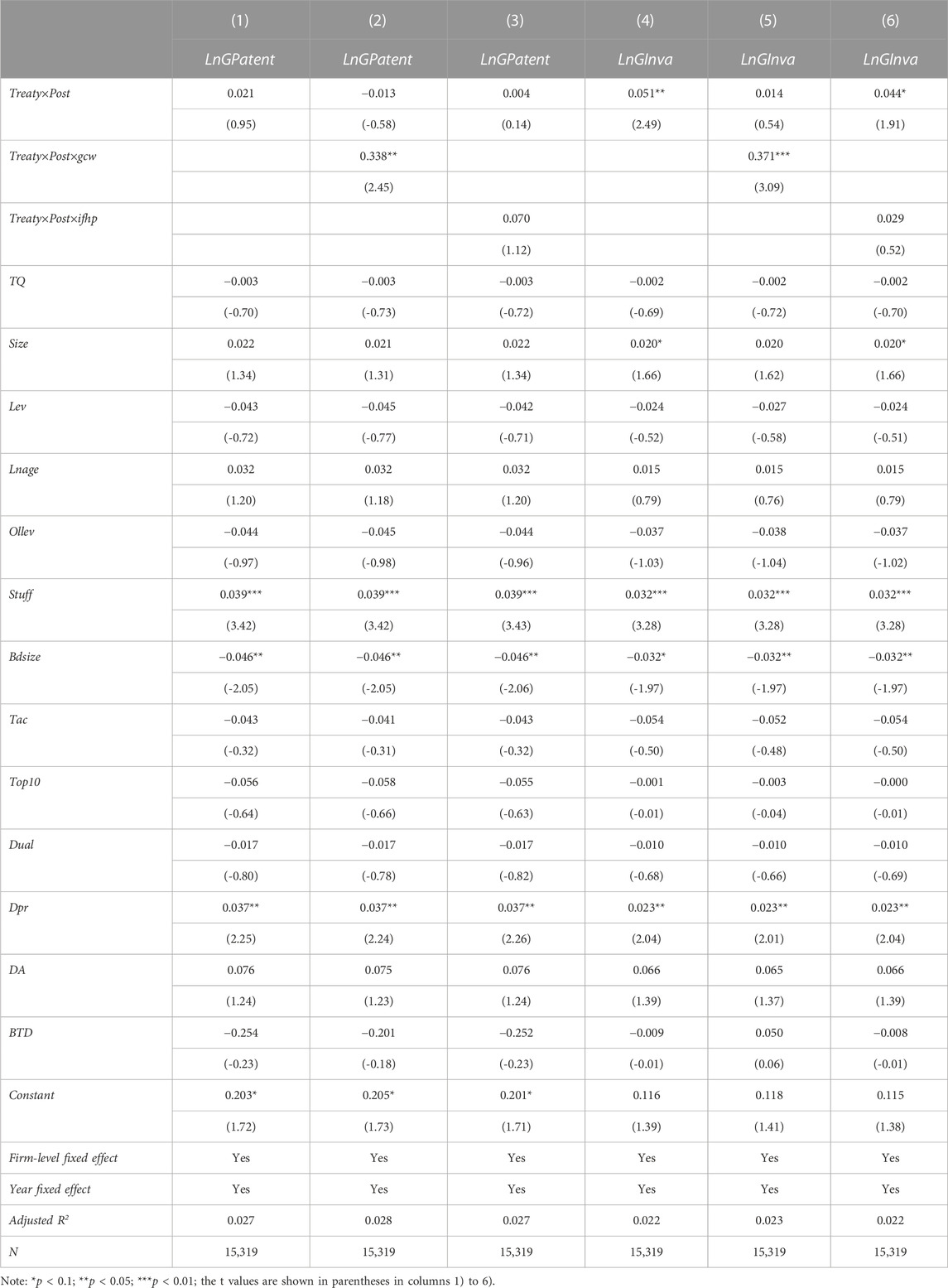

Due to a major lack of data from Changji Prefecture and Hami City in Xinjiang Uygur Autonomous Region and Jiujiang City in Jiangxi Province, only the cities of Quzhou, Huzhou, and Guangzhou are ultimately included in the treatment group. Seven cities, including Guiyang, Anshun, Nanchang, and Karamay, are selected as the treatment group, and the remaining 272 prefecture-level and above cities are used as the control group. In this paper, the interaction term between the city-level dummy variable and the time dummy variable between groups is used as the policy variable of the green finance pilot, a new core explanatory variable Treaty×Post is constructed, and the triple interaction of the enterprise nature Treaty×Post×gcw and Treaty×Post×ifhp is introduced, generating DID heterogeneity. As shown by the regression results in Table 8, the green finance pilot has significantly improved the green innovation of enterprises in the pilot regions, especially the green innovation of green enterprises, mainly reflected in the improvement of innovation quality. Thus, the baseline conclusion remains stable.

TABLE 8. Robustness checks at the city level.

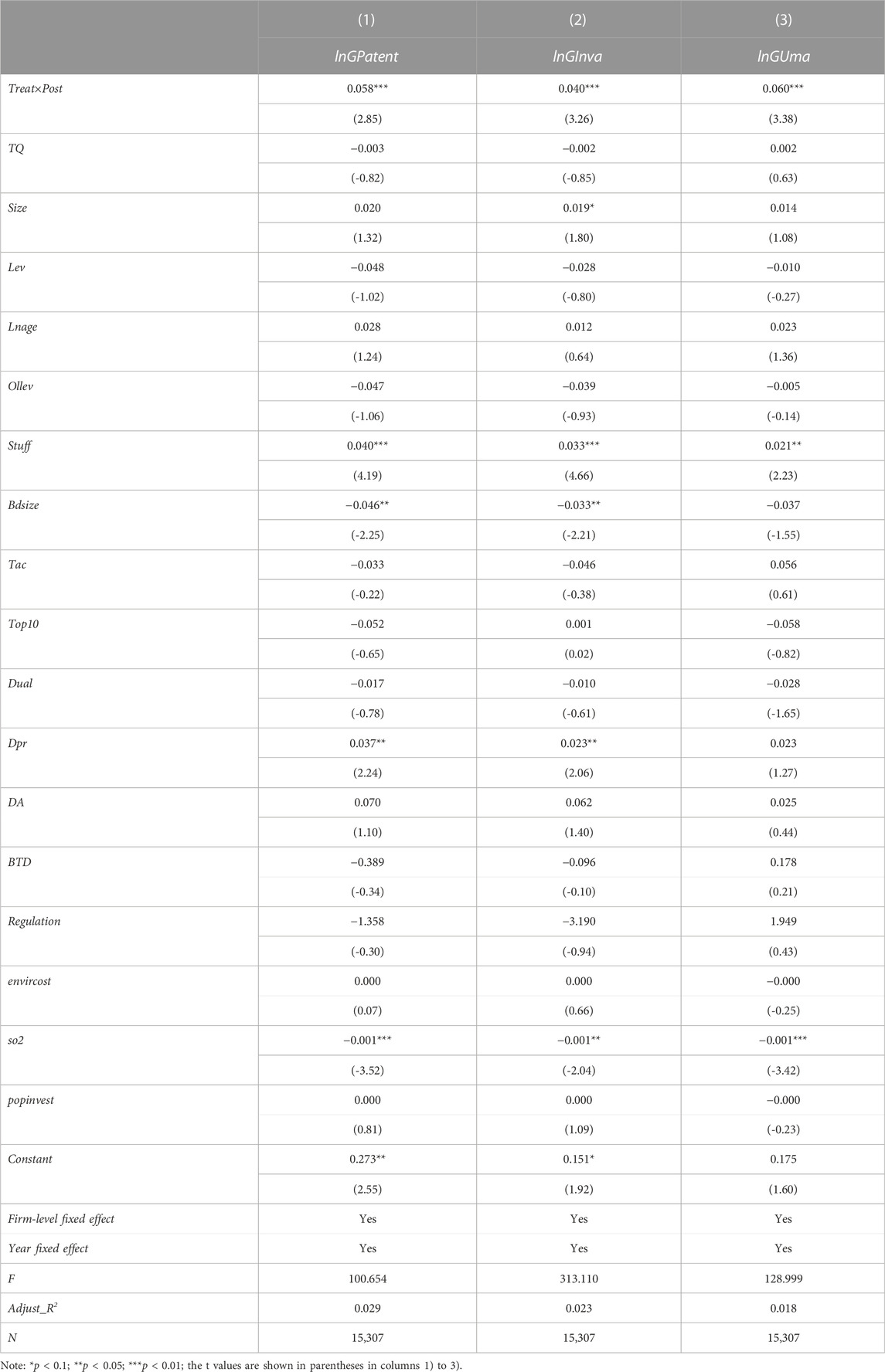

Prior studies show that the regional sustainable development strategy is an important factor in corporate green innovation (Irfan et al., 2022; Wen et al., 2022; Li and Wen, 2023). Therefore, the regional sustainable development strategy may disturb the above findings. So, we further examines the effect of green finance pilot reform on corporate green innovation. Specifically, we control the following variables of the regional sustainable development strategy: the regional environmental regulation intensity (Regulation), regional fiscal expenditure for environmental protection (envircost), regional SO2 emissions (so2) and regional investment in industrial pollution control (popinvest), which are from China national bureau of statistics website2. Table 9 presents the estimated results after controlling the effect of the regional sustainable development strategy. And the coefficients of Treat×Post in Colum 1) to 3) are both positive and significant at the 1% level, indicating that the green finance pilot reform has significantly increased corporate green innovation. That is, the findings are still supported after controlling the effect of the regional sustainable development strategy.

TABLE 9. The results after controlling the effect of regional sustainable development strategy.

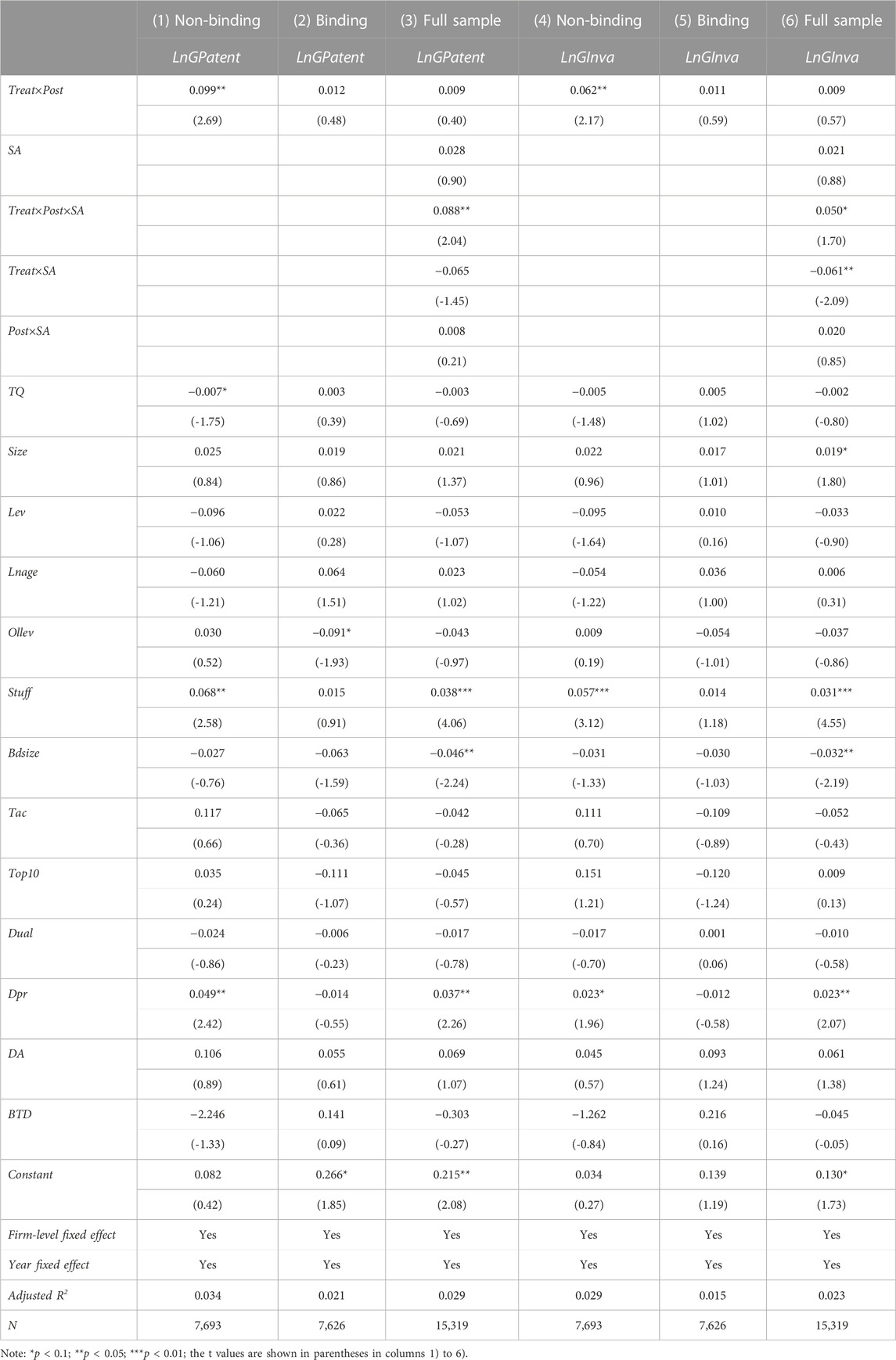

Following the theoretical analysis, this paper further empirically tests the impact of differences in corporate financing constraints on the relationship between green finance pilot reform and corporate green innovation. Drawing on studies, such as those by Hadlock and Pierce (2010), an SA index without endogenous financing constraint variables is selected to measure financing constraints. The SA index of an enterprise in an observed year is calculated as follows: SA = −0.737×Size+0.043×Size2 -0.04×Age. The index is negative, and the larger the value, the lower the degree of financing constraints. First, the sample enterprises are divided into high and low groups according to their level of financing constraint and the dummy variable SA is established. When an enterprise belongs to the high (low) financing constraint group, SA equals 0 1). The regression results in Table 10 show that the impact of the green finance pilot reform on enterprises’ total number of green innovation and green invention patents is more significant in the group without financing constraints. In addition, an interaction item test of DID×SA is used to measure the degree of financing constraint. The regression coefficient is positive and significant, which also shows that in enterprises without financing constraints, the green finance pilot reform effect is more pronounced. The promotional effect of reform on enterprises’ green innovation is more obvious. This also proves that enterprises need a certain amount of financial support to carry out green innovation activities.

TABLE 10. The results of financing constraint mechanism.

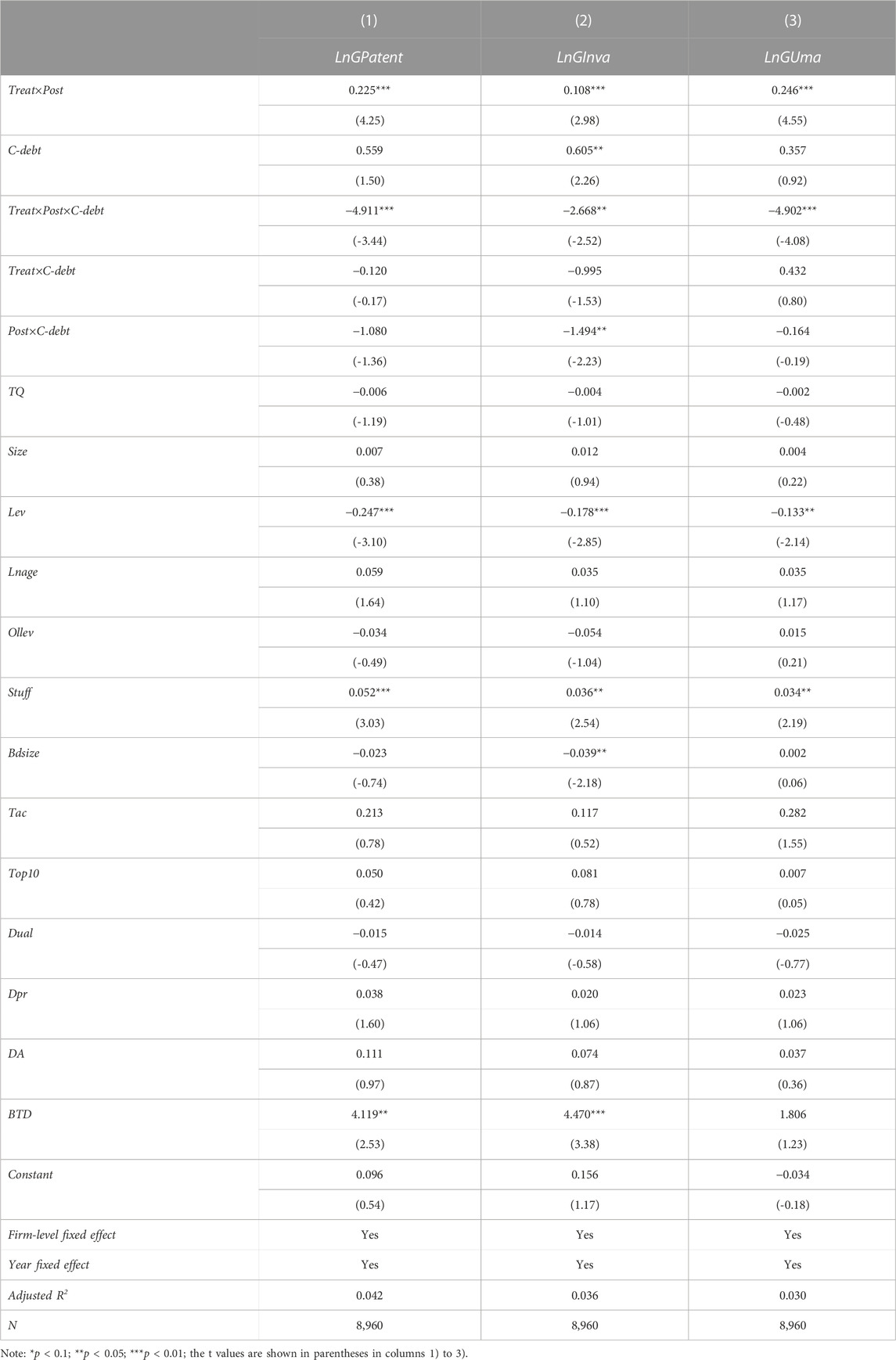

The cycle of innovation activities is long and difficult, and it is difficult for enterprises to stably support innovation activities when relying on internal financing alone. In addition, due to information asymmetry and a lack of high-quality collateral, innovative enterprises face certain discrimination when obtaining loans. To solve these problems, the document of supporting the issuance of green Debt financing instruments in the Green Finance Pilot Reform proposes policies by the People’s Bank of China to encourage and support enterprises in the pilot zone to register and issue green debt financing instruments. Generally, green debt financing instruments can broaden financing channels, reduce financing costs, and raise a large amount of funding for green innovation (Lee & Lee, 2022). Therefore, the ratio of the C-debt of financial expenses to interest-bearing liabilities is used as a proxy variable for financing costs to verify. As shown by the regression results in Table 11, the coefficient of the cross-product item Treat×Post×C-debt is significant at least at the 1% level, indicating that the green finance reform and innovation pilot zone policy indeed supports the development and growth of enterprises undertaking green projects through preferential policies that reduce debt financing costs. In summary, the green finance pilot promotes the green innovation of enterprises by increasing financing scale and reducing financing costs.

TABLE 11. The results of financing cost mechanism.

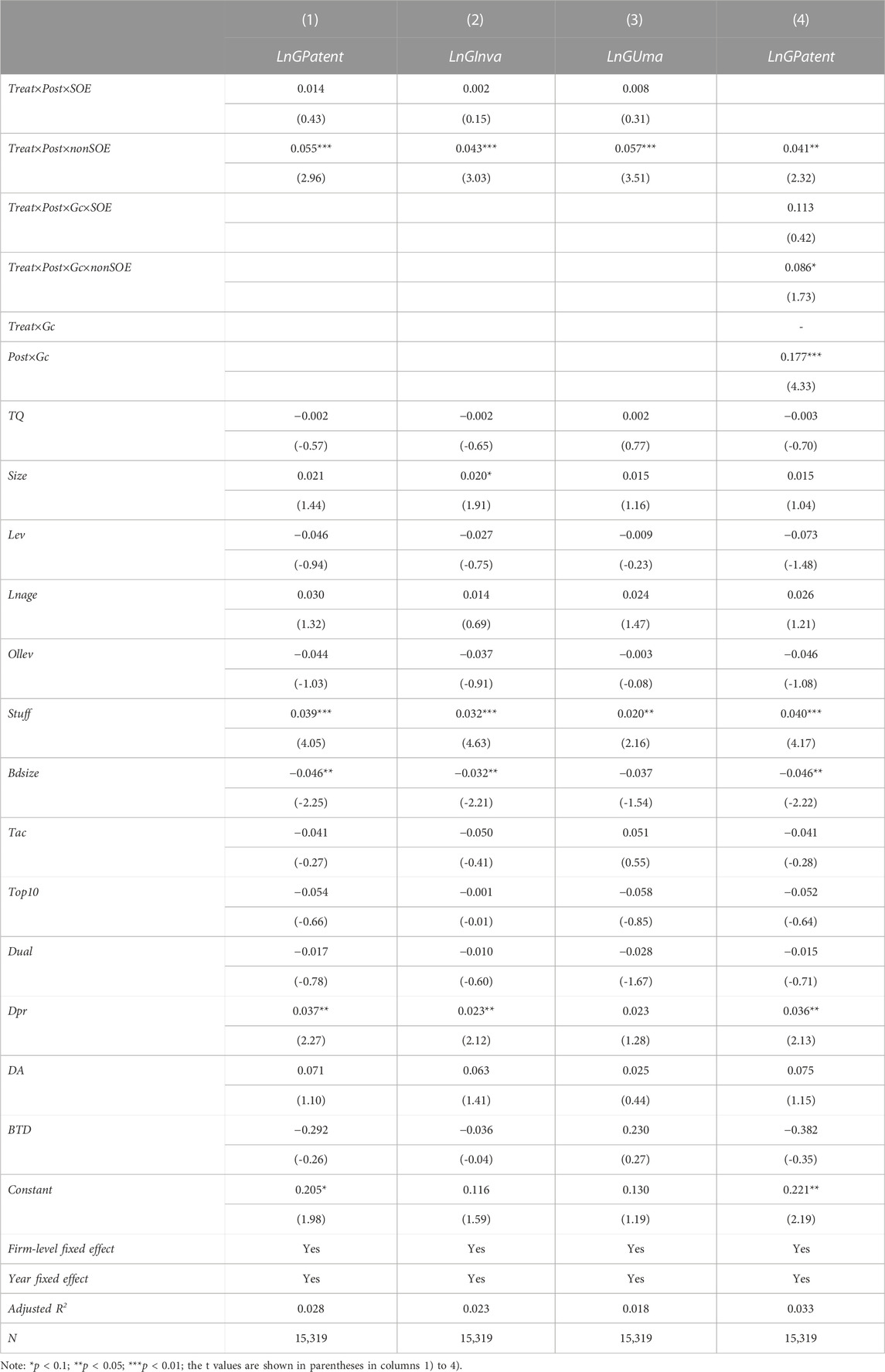

As shown by the regression results in Table 12, further examining the heterogeneity of enterprise ownership, whether for the full sample of enterprises or green enterprises, the green finance pilot reform has significantly promoted the green innovation of non-state-owned green enterprises in the pilot provinces and has had no significant impact on state-owned enterprises. This may be due to the agency problem in state-owned enterprises, such that enterprise managers lack incentives to invest in innovative projects. In addition, the green finance pilot reform has simultaneously promoted the invention patents and utility model patents of non-state-owned enterprises, whereas the policy has had no significant impact on the invention patents and utility model patents of state-owned enterprises.

TABLE 12. The effect of property rights.

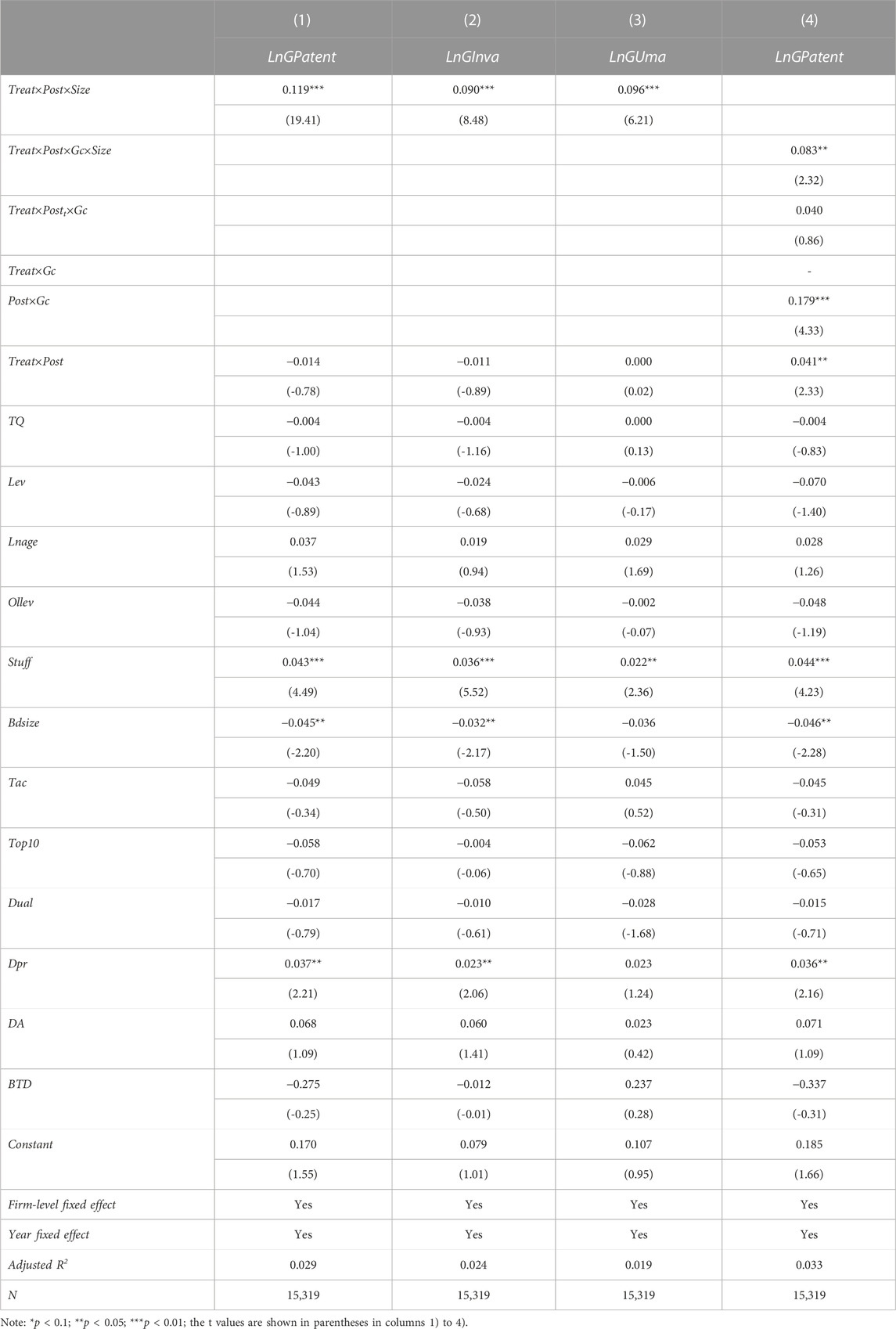

Green innovation requires sufficient financial, human, material, technical, and other resource support, and technological innovation activities are usually related to the scale of enterprises. There are certain differences in the availability and sensitivity of financial resources between enterprises of different sizes. According to the Schumpeter hypothesis, larger companies often have obvious advantages over smaller companies in terms of capital, platforms, and talent. This paper further investigates whether the promotion effect of the green finance pilot reform on the green innovation of enterprises is affected by enterprise size. The Size dummy variable is thus set. The interaction term of Size tests the heterogeneity of firm size.

Table 13 presents the regression results. As shown in columns 1) to 4), for the total number of green patents or green invention patents and green utility model patents, the coefficient of the interaction term is positive and significant. This indicates that compared with small-scale enterprises, large-scale enterprises have more obvious green innovation responses to policies, especially among green enterprises. Therefore, large-scale green enterprises are associated with a greater output of total innovation patents. In addition to having stronger demands for sustainable development, green transformation, and corporate social responsibility, large-scale enterprises are also significantly better than small-scale enterprises in terms of credit qualification and collateral. Therefore, green finance is more effective for large-scale enterprises in terms of resource support and R&D investment incentives.

TABLE 13. The effect of size.

This study takes China’s Green Finance Reform and Innovation Pilot Zone policy as a quasi-natural experiment. It uses sample data on A-share listed companies in Shanghai and Shenzhen from 2013 to 2019 and the number of green patents applied by listed companies as a measurement standard to investigate whether green finance pilot reform can promote the green innovation of enterprises. The research results based on the total number of green patents, green inventions, and green utility model patent indicators show that the green finance pilot reform can stimulate enterprises’ overall green innovation activities. At the same time, the promotion effect on green utility model patents is slightly greater than that on green patents. This conclusion holds true after conducting robustness tests, such as parallel trend assumption and stabiliser tests.

As the green finance pilot reform may focus on green enterprises and heavily polluting enterprises during the implementation process, a triple difference model is further constructed to test whether the green innovation of enterprises in different industries in pilot provinces differs after the implementation of the policy. The green finance pilot reform is found to play a greater role in promoting green innovation among green enterprises than among heavily polluting enterprises. Further testing includes the analysis of the intermediary mechanism represented by financing constraints and financing costs, and the analysis and testing of the heterogeneity of enterprise characteristics, such as enterprise size and ownership attributes. The green finance pilot reform mainly affects the green innovation of enterprises by alleviating financing constraints and reducing financing costs. The positive impact of the green finance pilot reform on corporate green innovation is greatest for non-state-owned and large-scale enterprises. Overall, this paper reveals that there is an innovation incentive effect on the impact of the green finance pilot reform on corporate green innovation. This shows that optimising enterprises’ external governance environment by extending the green finance pilot reform can promote their green innovation decision-making.

The findings of this paper have the following policy implications especially for emerging markets. First, the government should continue to enhance the scope of green financial pilot reforms to further stimulate green innovation in enterprises. Furthermore, the government may set a series of beneficial green finance standards for enterprises. Especially, financial support for green innovation in green finance should also be increased for green enterprises. For example, the financing channels for green enterprises can be broadened and the convenience of financing for green enterprises can be enhanced, so that more funds in green enterprises can be allocated to green innovation investment.

Second, the implementation of green financial policies should be tailored according to enterprise type. The impact of green finance pilot reform on the green innovation of enterprises is limited to certain enterprises, especially in green enterprises. For example, such a reform has more significant impact on the green innovation of green enterprises. Therefore, the government and financial institutions should consider more beneficial financial support for green enterprises’ green innovation and high-quality development. Furthermore, the government and financial institutions should also consider the heterogeneity of regulated enterprises when formulating green financial policies. For example, it is necessary to guide financial institutions to increase green financial support for small-scale green enterprises and transition enterprises.

Finally, especially for green enterprises, more attention should be paid to the innovation incentive effect of green finance on enterprises’ green innovation. Specifically, enterprises should pay attention to the optimisation effect of green finance pilot reform on their external governance environment, focus more on their output of green invention patents and actively shift from high to low carbonisation. Certainly, there may be some limitations in view of our research is conducted in China’s institutional setting. For example, not all countries can conduct green finance plot reform to promote green innovation. However, we admit that this research is interesting and important and further encourages us to focus in environmental protection problems from green finance.

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding author.

HW: Supervision, Writing–review and editing. DD: Data curation, Formal Analysis, Investigation, Methodology, Writing–original draft. XT: Formal Analysis, Funding acquisition, Project administration, Supervision, Writing–review and editing. ST: Conceptualization, Formal Analysis, Writing–review and editing.

The author(s) declare financial support was received for the research, authorship, and/or publication of this article. The authors gratefully appreciate the financial support of the Humanities and Social Sciences Fund of the Ministry of Education of China (Grant No. 23YJA630093), the Humanities and Social Sciences Special Fund of Fundamental Research for the Central Universities (Grant No. KYQN2023011), the National Natural Science Foundation of China (Grant No. 72202099), and China Postdoctoral Science Foundation (2021M700022).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

1The enterprises concerning energy conservation and environmental protection, photovoltaics, power generation, nuclear energy nuclear power, green energy-saving lighting, and building energy conservation industry are defined as green enterprises.

2http://www.stats.gov.cn/sj/ndsj/

Alpay, E., Kerkvliet, J., and Buccola, S. (2002). Productivity growth and environmental regulation in Mexican and US food manufacturing. Am. J. Agric. Econ. 84 (4), 887–901. doi:10.1111/1467-8276.00041

Amore, M. D., and Bennedsen, M. (2016). Corporate governance and green innovation. J. Environ. Econ. Manag. 75, 54–72. doi:10.1016/j.jeem.2015.11.003

Angrist, J. D., and Pischke, J. S. (2008). “Parallel worlds: fixed effects, differences-in-differences, and panel data,” in Mostly harmless econometrics (Princeton University Press), 221–248.

Asni, N., and Agustia, D. (2022). Does corporate governance induce green innovation? An emerging market evidence. Corp. Gov. Int. J. Bus. Soc. 22 (7), 1375–1389. doi:10.1108/cg-10-2021-0389

Beck, T., Levine, R., and Levkov, A. (2010). Big bad banks? The winners and losers from bank deregulation in the United States. J. Finance 65 (5), 1637–1667. doi:10.1111/j.1540-6261.2010.01589.x

Chen, Q., Ning, B., Pan, Y., and Xiao, J. (2021). Green finance and outward foreign direct investment: evidence from a quasi-natural experiment of green insurance in China. Asia Pac. J. Manag. 39, 899–924. doi:10.1007/s10490-020-09750-w

Chen, Y. S., and Chang, C. H. (2013). The determinants of green product development performance: green dynamic capabilities, green transformational leadership, and green creativity. J. Bus. ethics 116, 107–119. doi:10.1007/s10551-012-1452-x

Cheng, Q., Hail, L., and Yu, G. (2022). The past, present, and future of China-related accounting research. J. Account. Econ. 74 (2-3), 101544. doi:10.1016/j.jacceco.2022.101544

Chetty, R., Looney, A., and Kroft, K. (2009). Salience and taxation: theory and evidence. Am. Econ. Rev. 99 (4), 1–46. doi:10.17016/feds.2009.11

Claessens, S., and Yurtoglu, B. B. (2013). Corporate governance in emerging markets: a survey. Emerg. Mark. Rev. 15, 1–33. doi:10.1016/j.ememar.2012.03.002

Cui, L., and Huang, Y. (2018). Exploring the schemes for green climate fund financing: international lessons. World Dev. 101, 173–187. doi:10.1016/j.worlddev.2017.08.009

Dai, X., Siddik, A. B., and Tian, H. (2022). Corporate social responsibility, green finance and environmental performance: does green innovation matter? Sustainability 14 (20), 13607. doi:10.3390/su142013607

Dechow, P. M., Sloan, R. G., and Sweeney, A. P. (1995). Detecting earnings management Account. Rev. 70 (2), 193–225.

Desai, M. A., and Dharmapala, D. (2006). Corporate tax avoidance and high-powered incentives J. financ. econ. 79 (1), 145–179. doi:10.1016/j.jfineco.2005.02.002

Dong, Z., Xu, H., Zhang, Z., Lyu, Y., Lu, Y., and Duan, H. (2022). Whether green finance improves green innovation of listed companies—evidence from China. Int. J. Environ. Res. Public Health 19 (17), 10882. doi:10.3390/ijerph191710882

Du, D., Tang, X., Wang, H., Zhang, J. H., Tsui, S., and Lin, D. (2022). CEO organizational identification and corporate innovation investment. Account. Finance 62 (3), 4185–4217. doi:10.1111/acfi.12920

Fang, Z., Kong, X., Sensoy, A., Cui, X., and Cheng, F. (2021). Government’s awareness of environmental protection and corporate green innovation: a natural experiment from the new environmental protection law in China. Econ. Analysis Policy 70, 294–312. doi:10.1016/j.eap.2021.03.003

Gao, J., Murshed, M., Ghardallou, W., Siddik, A. B., Ali, H., and Khudoykulov, K. (2023). Juxtaposing the environmental consequences of different environment-related technological innovations: the significance of establishing good democratic governance. Gondwana Res. 121, 486–498. doi:10.1016/j.gr.2023.05.017

Gruber, J. (1994). The incidence of mandated maternity benefits. The American economic review, 622–641.

Hadlock, C. J., and Pierce, J. R. (2010). New evidence on measuring financial constraints: moving beyond the KZ index. Rev. financial Stud. 23 (5), 1909–1940. doi:10.1093/rfs/hhq009

Han, S., Zhang, Z., and Yang, S. (2022). Green finance and corporate green innovation: based on China’s green finance reform and innovation pilot policy. J. Environ. Public Health 2022, 1–12. doi:10.1155/2022/1833377

He, L., Liu, R., Zhong, Z., Wang, D., and Xia, Y. (2019). Can green financial development promote renewable energy investment efficiency? A consideration of bank credit. Renew. Energy 143, 974–984. doi:10.1016/j.renene.2019.05.059

Huang, D. (2022). Green finance, environmental regulation, and regional economic growth: from the perspective of low-carbon technological progress. Environ. Sci. Pollut. Res. 29 (22), 33698–33712. doi:10.1007/s11356-022-18582-8

Huang, H., Mbanyele, W., Wang, F., Song, M., and Wang, Y. (2022a). Climbing the quality ladder of green innovation: does green finance matter? Technol. Forecast. Soc. Change 184, 122007. doi:10.1016/j.techfore.2022.122007

Huang, Y., Chen, C., Lei, L., and Zhang, Y. (2022b). Impacts of green finance on green innovation: a spatial and nonlinear perspective. J. Clean. Prod. 365, 132548. doi:10.1016/j.jclepro.2022.132548

Irfan, M., Razzaq, A., Sharif, A., and Yang, X. (2022). Influence mechanism between green finance and green innovation: exploring regional policy intervention effects in China. Technol. Forecast. Soc. Change 182, 121882. doi:10.1016/j.techfore.2022.121882

Jin, Y., Gao, X., and Wang, M. (2021). The financing efficiency of listed energy conservation and environmental protection firms: evidence and implications for green finance in China. Energy Policy 153, 112254. doi:10.1016/j.enpol.2021.112254

Lee, C. C., and Lee, C. C. (2022). How does green finance affect green total factor productivity? Evidence from China. Energy Econ. 107, 105863. doi:10.1016/j.eneco.2022.105863

Lee, C. C., Wang, F., and Chang, Y. F. (2023). Does green finance promote renewable energy? Evidence from China. Resour. Policy 82, 103439. doi:10.1016/j.resourpol.2023.103439

Levinson, A., and Taylor, M. S. (2008). Unmasking the pollution haven effect. Int. Econ. Rev. 49 (1), 223–254. doi:10.1111/j.1468-2354.2008.00478.x

Li, G., and Wen, H. (2023). The low-carbon effect of pursuing the honor of civilization? A quasi-experiment in Chinese cities. Econ. Analysis Policy 78, 343–357. doi:10.1016/j.eap.2023.03.014

Li, Y., Chen, R., and Xiang, E. (2022). Corporate social responsibility, green financial system guidelines, and cost of debt financing: evidence from pollution-intensive industries in China. Corp. Soc. Responsib. Environ. Manag. 29 (3), 593–608. doi:10.1002/csr.2222

Liu, S., and Wang, Y. (2023). Green innovation effect of pilot zones for green finance reform: evidence of quasi natural experiment. Technol. Forecast. Soc. Change 186, 122079. doi:10.1016/j.techfore.2022.122079

Olden, A., and Møen, J. (2022). The triple difference estimator. Econ. J. 25 (3), 531–553. doi:10.1093/ectj/utac010

Porter, M. E., and Linde, C. V. D. (1995). Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 9 (4), 97–118. doi:10.1257/jep.9.4.97

Ramanathan, R., Black, A., Nath, P., and Muyldermans, L. (2010). Impact of environmental regulations on innovation and performance in the UK industrial sector. Manag. Decis. 48 (10), 1493–1513. doi:10.1108/00251741011090298

Shi, J., Yu, C., Li, Y., and Wang, T. (2022). Does green financial policy affect debt-financing cost of heavy-polluting enterprises? An empirical evidence based on Chinese pilot zones for green finance reform and innovations. Technol. Forecast. Soc. Change 179, 121678. doi:10.1016/j.techfore.2022.121678

Tang, X., Du, D., Xie, L., and Lin, B. (2022). Does the standardisation of tax enforcement improve corporate financial reporting quality?. China J. Account. Stud. 10 (4), 481–502.

Tian, H., Siddik, A. B., Pertheban, T. R., and Rahman, M. N. (2023). Does fintech innovation and green transformational leadership improve green innovation and corporate environmental performance? A hybrid SEM–ANN approach. J. Innovation Knowl. 8 (3), 100396. doi:10.1016/j.jik.2023.100396

Tolliver, C., Fujii, H., Keeley, A. R., and Managi, S. (2021). Green innovation and finance in Asia. Asian Econ. Policy Rev. 16 (1), 67–87. doi:10.1111/aepr.12320

Umar, M., and Safi, A. (2023). Do green finance and innovation matter for environmental protection? A case of OECD economies. Energy Econ. 119, 106560. doi:10.1016/j.eneco.2023.106560

Van Leeuwen, G., and Mohnen, P. (2017). Revisiting the Porter hypothesis: an empirical analysis of green innovation for The Netherlands. Econ. Innovation New Technol. 26 (1-2), 63–77. doi:10.1080/10438599.2016.1202521

Wang, K. H., Zhao, Y. X., Jiang, C. F., and Li, Z. Z. (2022a). Does green finance inspire sustainable development? Evidence from a global perspective. Econ. Analysis Policy 75, 412–426. doi:10.1016/j.eap.2022.06.002

Wang, Q. J., Wang, H. J., and Chang, C. P. (2022b). Environmental performance, green finance and green innovation: what's the long-run relationships among variables? Energy Econ. 110, 106004. doi:10.1016/j.eneco.2022.106004

Wang, X. (2022). Research on the impact mechanism of green finance on the green innovation performance of China's manufacturing industry. Manag. Decis. Econ. 43 (7), 2678–2703. doi:10.1002/mde.3554

Wen, H., Wen, C., and Lee, C. C. (2022). Impact of digitalization and environmental regulation on total factor productivity. Inf. Econ. Policy 61, 101007. doi:10.1016/j.infoecopol.2022.101007

Xu, A., Zhu, Y., and Wang, W. (2023). Micro green technology innovation effects of green finance pilot policy—from the perspectives of action points and green value. J. Bus. Res. 159, 113724. doi:10.1016/j.jbusres.2023.113724

Xu, X. (2023). Does green finance promote green innovation? Evidence from China. Environ. Sci. Pollut. Res. 30 (10), 27948–27964. doi:10.1007/s11356-022-24106-1

Yan, C., Mao, Z., and Ho, K. C. (2022). Effect of green financial reform and innovation pilot zones on corporate investment efficiency. Energy Econ. 113, 106185. doi:10.1016/j.eneco.2022.106185

Yang, Y., Su, X., and Yao, S. (2022). Can green finance promote green innovation? The moderating effect of environmental regulation. Environ. Sci. Pollut. Res. 29 (49), 74540–74553. doi:10.1007/s11356-022-21118-9

Yu, C. H., Wu, X., Zhang, D., Chen, S., and Zhao, J. (2021). Demand for green finance: resolving financing constraints on green innovation in China. Energy Policy 153, 112255. doi:10.1016/j.enpol.2021.112255

Yu, Z., Shen, Y., and Jiang, S. (2022). The effects of corporate governance uncertainty on state-owned enterprises' green innovation in China: perspective from the participation of non-state-owned shareholders. Energy Econ. 115, 106402. doi:10.1016/j.eneco.2022.106402

Zhang, H., Wang, Y., Li, R., Si, H., and Liu, W. (2023). Can green finance promote urban green development? Evidence from green finance reform and innovation pilot zone in China. Environ. Sci. Pollut. Res. 30 (5), 12041–12058. doi:10.1007/s11356-022-22886-0

Zhang, Y., and Li, X. (2022). The impact of the green finance reform and innovation pilot zone on the green innovation—evidence from China. Int. J. Environ. Res. Public Health 19 (12), 7330. doi:10.3390/ijerph19127330

Zhao, T., Zhou, H., Jiang, J., and Yan, W. (2022). Impact of green finance and environmental regulations on the green innovation efficiency in China. Sustainability 14 (6), 3206. doi:10.3390/su14063206

Keywords: green finance pilot reform, corporate green innovation, innovation incentive, corporate governance, quasi-natural experiment

Citation: Wang H, Du D, Tang X and Tsui S (2023) Green finance pilot reform and corporate green innovation. Front. Environ. Sci. 11:1273564. doi: 10.3389/fenvs.2023.1273564

Received: 06 August 2023; Accepted: 16 October 2023;

Published: 30 October 2023.

Edited by:

Diana Mihaela Tirca, Constantin Brâncusi University, RomaniaReviewed by:

Abu Bakkar Siddik, University of Science and Technology of China, ChinaCopyright © 2023 Wang, Du, Tang and Tsui. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Xiaojian Tang, dGFuZ3hqOEBuamF1LmVkdS5jbg==,

†These authors share first authorship

‡ORCID: Xiaojian Tang, https://orcid.org/0000-0002-0831-5440

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.