95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 11 January 2024

Sec. Environmental Economics and Management

Volume 11 - 2023 | https://doi.org/10.3389/fenvs.2023.1273278

This article is part of the Research Topic Collaborative economy CE5P (Planet, People, Partnership, Prosperity, Peace) View all 6 articles

Ke Yuan1

Ke Yuan1 Bangzheng Wu2*

Bangzheng Wu2*The analysis of the impact of China’s Environmental Protection Tax (EPT) Law on company environmental, social, and corporate governance (ESG) performance is crucial for a more comprehensive understanding of the EPT Law and to improve corporate practices. Using a difference-in-differences (DID) model with a research sample of 7,055 listed firms in China from 2012 to 2020, we found that the EPT Law significantly improved firms’ overall ESG performance. However, this improvement was mainly driven by significant increases in the environmental (E) score. In contrast, the social (S) score declined significantly after the implementation of the EPT Law, indicating a trade-off between environmental regulation and social responsibility. Further analysis also reveals that the increase in production costs, which led to a decrease in employment and wages, is responsible for the crowding-out of social responsibility. This study not only enhances our understanding of the impacts of environmental regulations on companies but also offers guidelines for policymakers to consider the negative externality of policies, which could serve as a “double-edged sword.”

The disclosure and reporting of environmental, social, and corporate governance (ESG) information have been steadily increasing worldwide. These serve as pivotal indicators for measuring sustainable development within enterprises. The incentivizing role of ESG for companies involves incorporating non-financial indicators into corporate performance. This, in turn, serves as a consideration factor in investment decision-making to mitigate investment risks. Current study provides evidence that the disclosure of corporate social responsibility can promote enterprises’ R&D investment (Li et al., 2023a). However, due to the indirect and long-term nature of attracting investments through ESG and the pressure of market volatility, managerial myopia can also impede companies’ ESG performance (Hou and Wei, 2023). On the other hand, certain mandatory regulations, such as environmental tax laws, usually increase saliency in specific aspects of ESG performance. However, there is no single regulation that takes into account all aspects of ESG. Therefore, whether and how the implementation of such regulations will affect various dimensions of ESG performance is an important issue that needs further investigation, especially for achieving the sustainable development goals of society.

As global attention on environmental issues continues to rise, many countries and regions worldwide have started to regulate firms’ greenhouse gas emissions, water usage, electricity consumption, and waste management (Pranugrahaning et al., 2021). China, due to its economic development, is among the countries grappling with significant environmental challenges. Since initiating market-oriented economic reforms in the 1970s, China has achieved remarkable economic growth (Fan et al., 2011). However, this success has come at the cost of significant emissions of the “three wastes”, including water, gas, and municipal solid waste (Zhu et al., 2019). Therefore, it has become imperative for the Chinese government to implement environmental laws and policies. However, despite the government’s policy to levy fees for pollutant discharges nationwide, research has revealed that inadequate law enforcement and an ill-structured fee schedule (including a low payment threshold) have hindered the effectiveness of China’s fee system in reducing pollution significantly (Peng, 2013; Zhu and Lu, 2017; Wu et al., 2019; Yu et al., 2022). Consequently, China has initiated a “fee-to-tax” reform to address unresolved environmental issues. The Environmental Protection Tax Law of the People’s Republic of China (the EPT Law) was enacted on 25 December 2016, and implemented in January 2018. This law mandates that corporations, institutions, and other types of businesses pay environmental taxes based on their pollutant discharge volumes, thereby increasing the cost of pollution compared to the discharge fee system. Under this law, pollutants are taxed based on their type and volume, with higher taxes imposed on firms for higher emissions of the same type of pollutant (Liu et al., 2022). The implementation of environmental regulation has notably heightened corporate environmental responsibility in a short period and encouraged enterprises to innovate in green technologies (Zhang et al., 2022; Li et al., 2023b). However, the impact and mechanism of the EPT Law on companies’ overall sustainable development warrant further examination. While some studies have provided evidence of the influence of mandatory environmental policies on corporate ESG performance, it is essential to note that ESG is a multifaceted concept encompassing three distinct dimensions: environmental, social, and corporate governance. Whether the positive effect of environmental regulation on corporate ESG performance is solely channeled through the direct pathway of the environmental (E) dimension remains an area requiring further exploration.

This research delves into the impact of the EPT Law on both the overall ESG performance of corporations and the individual components of ESG, aiming to address the gap in understanding the crowding-out effect of mandatory environmental regulations on corporate sustainability. In this study, we employed a DiD (Difference-in-Differences) model to assess the influence of the EPT Law’s enactment on corporate ESG performance. Initially, we explored how the EPT Law affects the ESG performance of enterprises overall. According to neo-institutional theory, corporations not only vie for resources but also actively strive to establish legitimacy and gain social acceptance (Miller, 2006). In pursuit of compliance and development, enterprises tend to enhance their environmental measures. Furthermore, the introduction of the law coincides with increasing societal attention to environmental issues, providing companies with an additional incentive to rapidly reduce pollution emissions. Secondly, we have identified that companies have reallocated resources among various ESG dimensions, shifting resources from the social (S) dimension to the more heavily regulated environmental (E) dimension. By closely examining key indicators within the social dimension, particularly labor market factors, we have further substantiated the existence of a “crowding-out effect” of corporate environmental protection on employment and wages. We also have discovered that environmental regulations can lead to increased production costs, which can serve as the mechanism of declined employment and wages (Yip, 2018; Lu and Zhu, 2021; Qin et al., 2021; Zheng et al., 2022). As employment and wage concerns are significant aspects of a firm’s social responsibility (the “S” in ESG), we have observed that the impact of environmental taxes on their ESG performance can be a double-edged sword, with both positive and negative consequences.

Our study makes significant contributions to the existing literature in three key aspects. Firstly, our findings shed light on the impact of the EPT Law on corporate ESG performance and elucidate the primary mechanisms through which this influence operates. In earlier research, the impact of environmental policies on ESG performance was often attributed to a straightforward promoting effect without a deep exploration of the underlying mechanisms and pathways (Lu and Cheng, 2023; Zhang et al., 2023). Our study bridges this gap by revealing that the tax-induced promotion effect on ESG is predominantly driven by the legal impact on the environmental (E) dimension. Notably, once we control for the influence of the E score, the other two aspects (S and G) do not exhibit a significant increase following the implementation of the EPT Law. This outcome not only raises questions but also supplements about the “double dividend” effect resulting from environmental regulations. However, this effect can be explained by neo-institutional theory, which underscores the significance of legitimacy and social acceptance in a company’s development.

Secondly, our study highlights that environmental taxes have a notable crowding-out effect on the social (S) dimension of ESG. Following the enactment of the EPT Law, companies underwent a resource reallocation within the ESG framework, resulting in reduced allocations to the social (S) dimension. This observation signifies a negative legal externality. We deepen our understanding of the crowding-out effect by specifically examining key aspects of the social (S) dimension, including employment and wages within companies. Prior research has explored the impact of environmental regulations on the labor market, revealing negative effects on corporate labor demand and wages due to the scale effect associated with increased production costs (Wang et al., 2020; Xiao et al., 2022; Zheng et al., 2022). Our study focuses on the trade-offs within a company’s ESG system brought about by regulatory enforcement. This issue holds significant implications for safeguarding workers’ rights and genuinely implementing sustainable development strategies.

Lastly, our research findings do not align with the “double dividend” effect, which may be attributable to the conditionality of achieving this effect. Our study’s conclusion suggests that in complex organizational constraints and an unstable market environment, environmental regulations can have a negative impact on employment. Existing research indicates that the impact of environmental regulations on employment exhibits a threshold effect, with significantly positive effects observed when the regulatory requirements are below a certain threshold (Yan et al., 2012). Therefore, further investigations are warranted to comprehend the specific mechanisms and assumptions behind our study’s conclusions. Nonetheless, our findings align with the skepticism expressed in existing literature regarding the ‘double dividend’ effect (Boyd and Ibarrarán, 2002). Importantly, our conclusions find support in neo-institutional theory, offering valuable insights for policymakers across various contexts.

Neo-institutional theory posits that organizational behavior is influenced not solely by efficiency but also by the presence of institutional factors. These institutional factors, and the pressures they exert, are categorized into three distinct types by neo-institutional theory: regulative, normative, and cognitive institutional pressures (Scott, 2008). Each of these types exerts varying impacts on how organizations behave. In the context of the EPT Law, a mandatory external regulation, it primarily enhances the effectiveness of corporate environmental protection in two main aspects: First, the environmental regulation creates direct regulative pressure by partially internalizing external environmental costs for companies (Jia and Chen, 2019). Second, after the implementation of the EPT Law, normative pressures from consumers and investors also enforce companies’ environmental investment. This is because business activities need to align with societal values and norms (Suchman, 1995). Firms adopt behaviors that demonstrate a level of social consciousness that is acceptable to stakeholders (Palazzo and Scherer, 2006), thereby reinforcing their connections with them. In these respects, firms allocate internal resources to improve their external environmental behaviors to meet the demands of various stakeholders, which strengthens their overall environmental protection efforts (Wang et al., 2022). Therefore, it is reasonable to speculate that the EPT Law directly enhances companies’ environmental protection (E) levels. Moreover, given the context of relatively stable corporate investment strategies in the short term, the EPT Law compels companies to increase their expenditures on environmental aspects, which consequently elevates their overall ESG performance.

Existing research suggests that stringent government regulations can heighten companies’ awareness of their environmental responsibilities (Delmas and Toffel, 2008) and their willingness to meet their ESG requirements (Darrell and Schwartz, 1997) by internalizing environmental costs (Ji and Su, 2016). While some studies have explored the role of various central government administrative approaches, including environmental courts, green finance policies, environmental protection inspections, and environmental protection taxes (Wang et al., 2022; Li J. and Li S., 2022; Lu and Cheng, 2023), limited research has investigated the impact and mechanisms of the EPT Law on corporate ESG. The EPT Law represents a relatively mature pollution levy system in China, contributing to the strengthening of the environmental legal framework. However, some studies argue that due to factors such as a narrow tax base, low tax burden, and small-scale operations, environmental taxes have evolved into a purely fiscal revenue-raising tool and a form of “extra payment” or “government price” for polluting companies to purchase pollution rights (Mao and Zhou, 2021). Their effectiveness in emission reduction, pollution control, and technological innovation is considered inadequate. Therefore, examining the potential impact of this law on corporate ESG performance is particularly crucial for a more comprehensive policy assessment.

Accordingly, we propose the following hypothesis:

H1:. The environmental protection tax law can improve firms’ ESG performance.

H2:. The environmental protection tax law can improve firms’ environmental (E) performance.

While the impact of the EPT Law on corporate environmental protection is clear, ongoing debate surrounds its influence on the social (S) and corporate governance dimensions. The social indicators include labor practices, human rights, and contributions to customers and the supply chain (Pranugrahaning, 2021). According to stakeholder theory, some studies suggest that environmental regulations can enhance corporate ESG performance by fostering effective communication and positive stakeholder interactions. This, in turn, can lead to long-term cooperative relationships and improved corporate social (S) performance (Wang et al., 2022). Moreover, safeguarding labor standards is a crucial part of maintaining social standards (Waas, 2021). Social sustainability, as defined by the United Nations, revolves around how companies impact employees and workers throughout their value chain1. Hence, the labor force plays a pivotal role in the social component of ESG performance. Some argue for the “double dividend” effect, positing that environmental taxes can stimulate labor demand by enhancing production efficiency.

Conversely, certain researchers have noted tension between the environmental and social components of ESG. They argue that implementing environmental policy without addressing its social implications can result in an imbalanced equation of costs and benefits concerning environmental performance, potentially harming the social fabric (Gözlügöl, 2022). Further, Lu and Zhu (2021) found that tax expenses could have a crowding-out effect on corporate social responsibility. This effect can be explained through financial constraint theory and risk management theory. According to the former, tax expenses may restrict a firm’s ability to invest in social responsibility. Risk management theory suggests that corporate social responsibility might serve as compensation for inadequate tax payments and associated legitimacy risks (Pratiwi and Djakman, 2017), which also predicts a negative relationship between corporate social responsibility and tax expenses. Specifically, China’s EPT Law could influence the labor market by reducing employment and wage expenses.

Existing research has provided partial confirmation of the adverse effects of environmental taxes on the labor market. For instance, one study has attributed the crowding-out effect on employment to reduced profits and the resultant upward pressure on unemployment rates (Yip, 2018). When confronted with the constraints imposed by environmental protection taxes, companies tend to increase spending on pollution control, leading to higher production costs and subsequently elevated product prices. These higher prices, in turn, reduce consumer demand and prompt companies to scale back production, resulting in a decreased need for factors of production, including the labor force (Greenstone, 2002; Walker, 2011; Curtis, 2018), ultimately leading to job losses. Additionally, corporate expenditures on employee wages are closely intertwined with the issue of income distribution equity, which forms another crucial aspect of the social (S) component within ESG performance. Several studies have demonstrated the negative impact of environmental regulations on employees’ wage levels (Qin et al., 2021), particularly among ordinary employees rather than managers (Xiao et al., 2022). However, further investigation is warranted to comprehensively understand the effects of environmental taxes on the social (S) performance of companies.

Accordingly, we propose the following hypothesis:

H3:. The environmental protection tax law can decrease firms’ social (S) performance.

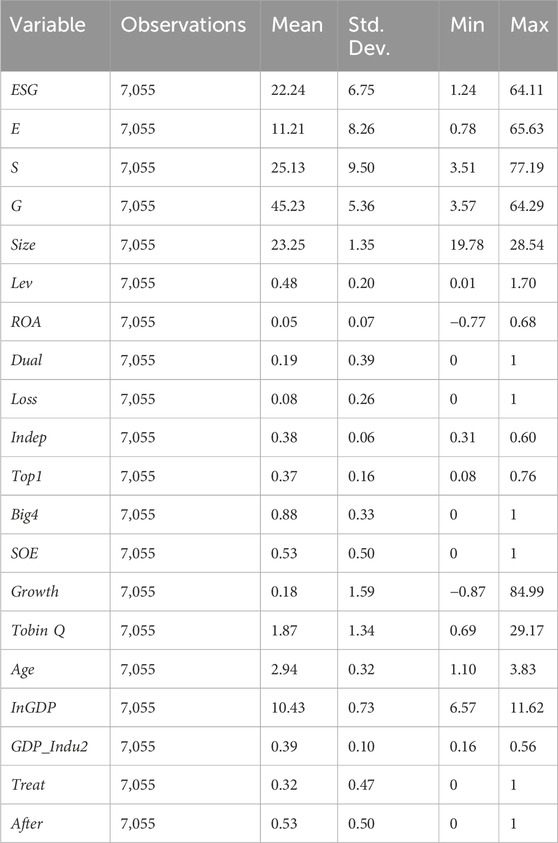

Our sample dataset was constructed from China’s A-share listed companies, utilizing ESG scores sourced from the Bloomberg database as a collective measure of corporate ESG performance, encompassing its (E), (S), and (G) components individually. To maintain a balanced sample size both before and after the enactment of the EPT Law, we utilized scores spanning the years 2012–2020. Several exclusion criteria were applied: 1) firms facing financial difficulties or undergoing listing suspension, identified as “ST” or “PT” firms, 2) firms for which ESG scores in the Bloomberg dataset were incomplete, and 3) firms with incomplete or missing data for the variables used in the baseline analysis. Following these criteria, our final dataset comprised 7,055 samples from 1,014 distinct firms. Financial and corporate governance data were sourced from the China Stock Market and Accounting Research (CSMAR) and WIND databases, while regional-level economic indicators were obtained from the China City Statistical Yearbook. This rigorous dataset selection and compilation process ensured the quality and reliability of our analysis.

In our evaluation of corporate ESG performance, we utilized the Bloomberg dataset of ESG scores, which includes three separate scores for environmental (E), social (S), and corporate governance (G) as dependent variables. This dataset has been a popular choice in many prior studies investigating Chinese corporate ESG issues due to its comprehensive coverage of Chinese companies and access to detailed second-level indicators encompassing environment, society, and corporate governance (Luo and Wu, 2022). Bloomberg, being an internet-based repository, provides access to real-time and historical financial data, business news updates, descriptive company information, research reports, and statistical data for over 52,000 firms globally (Alazzani et al., 2021). The ESG scores are derived from the assessment of 21 indicators and 122 sub-indicators, categorized into three dimensions (Luo and Wu, 2022).

The Environmental Protection Tax (EPT) Law was officially enacted on 25 December 2016, and became effective on 1 January 2018. To construct the Post variable, we used data from 2017 onwards. This choice is based on the recognition that the formal announcement of the law would likely have had a precursor impact on companies’ ESG performance and their interactions with stakeholders even before its official implementation (Tu et al., 2020). Therefore, we assigned a value of 1 to Post for samples from 2017 or later and 0 otherwise, indicating the policy’s influence.

To identify the groups affected by the EPT Law, we followed the approach outlined by Liu et al. (2022). We designated firms in heavy polluting industries as the experimental group and firms in other industries as the control group. Heavy polluting industries are naturally considered the primary sources of environmental pollution and are thus particularly susceptible to the impact of environmental regulations. Consequently, any variations in the ESG performance of heavy polluting firms can serve as a reliable gauge of the EPT Law’s impact. We established the classification criteria for heavy polluting industries by combining the 16 industries listed in the “Guidelines for Environmental Information Disclosure of Listed Companies” issued by the Ministry of Environmental Protection in 2010 with the classification standards for Chinese national economic industries specified in the National Standards of the People’s Republic of China. This resulted in the identification of 19 industries as heavy polluting, and we assigned a value of 1 to Treat when the sample included a heavily polluting company and 0 otherwise. It is important to note that due to the absence of a one-to-one correspondence between the regulatory categories for heavy polluting industries and enterprise industries in current Chinese standards, there is no uniform criterion for determining whether a firm falls under the heavy polluting industry classification. To account for this, we applied an alternative criterion to test for robustness in our study.

We incorporated several control variables into our analysis, following the methodology employed in previous research on the effects of environmental regulations (Wang et al., 2022; Wang et al., 2022; Lu and Cheng, 2023). These control variables encompass both firm-level characteristics and regional indicators. At the firm level, we considered fundamental characteristics such as firm size (Size), debt-to-asset ratio (Lev), return on total assets (ROA), CEO duality (Dual), profit or loss (Loss), the proportion of independent directors (Indep), the ownership concentration represented by the largest shareholder (Top1), the presence of Big-four accounting firms (Big4), the nature of property rights (SOE), growth in business revenue (Growth), investment opportunities (Tobin Q), and company age (Age). Additionally, we accounted for regional characteristics by incorporating economic scale and industrial structure indicators. These regional metrics were represented by regional Gross Domestic Product (InGDP) and the share of Gross Domestic Product attributed to the secondary industry sector (GDP_Indu2), respectively, as documented in previous studies (Wang et al., 2022). For your reference, Table 1 provides comprehensive definitions and descriptions of these variables.

TABLE 1. Definitions of the variables.

To examine the impact of the EPT Law on ESG performance, we employed a difference-in-difference (DiD) framework. The baseline regression model, outlined below, employs the notation i to denote the firm and t to signify the year.

In this study, the dependent variables (DV) include the total ESG score and its subcomponents, namely, the environmental (E), social responsibility (S), and corporate governance (G) indicators, represented as

The error term is denoted as

Table 2 presents the descriptive statistics for the variables. The ESG scores ranged from 1.24 to 64.11, with a mean score of 22.24 and a standard deviation of 6.75. This ESG score aligns with the findings of Luo and Wu (2022), who reported a mean value of 21.3 and a standard deviation of 7.0 for Bloomberg ESG scores from 2011 to 2020, measured as a ratio (ESG divided by 100). Our treatment company (Treat) makes up 32% of the total sample, in line with the results of Li and Li (2022). The post-event firms (After) constitute approximately 53% of the total sample, indicating a well-balanced ratio. The standard deviations of the control variables’ descriptive statistics are largely consistent with those observed in previous studies (Wang et al., 2022; Lu and Cheng, 2023).

TABLE 2. Descriptive statistics for the main variables.

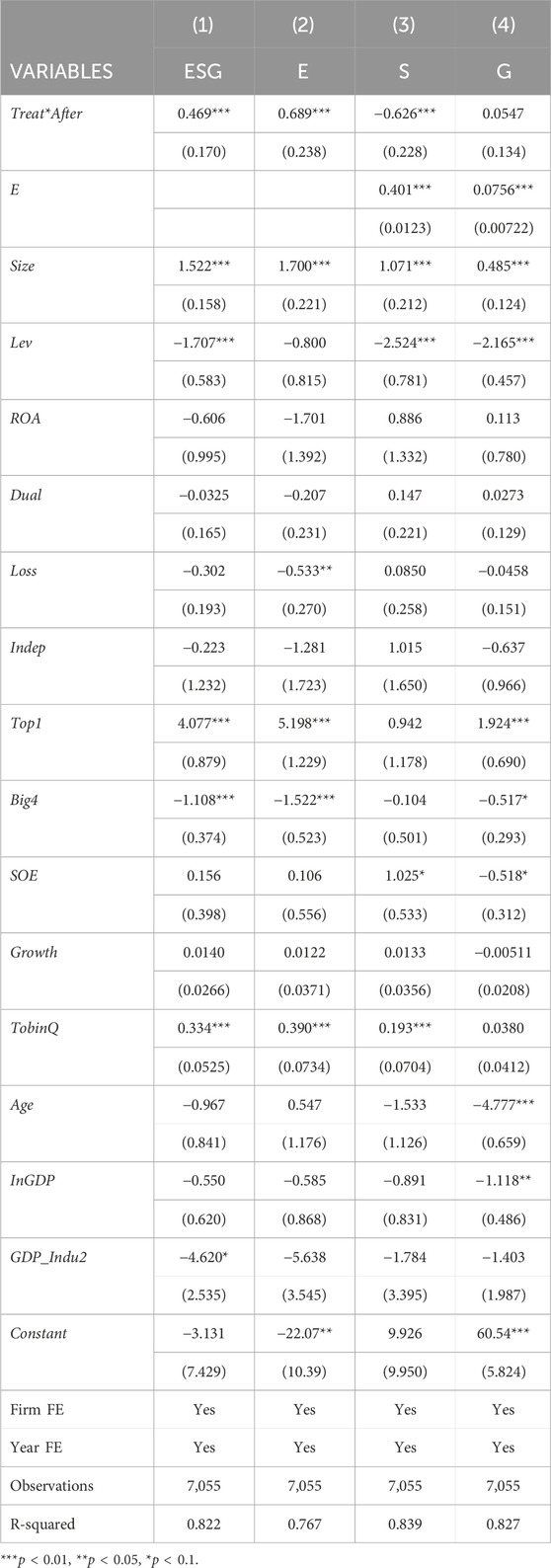

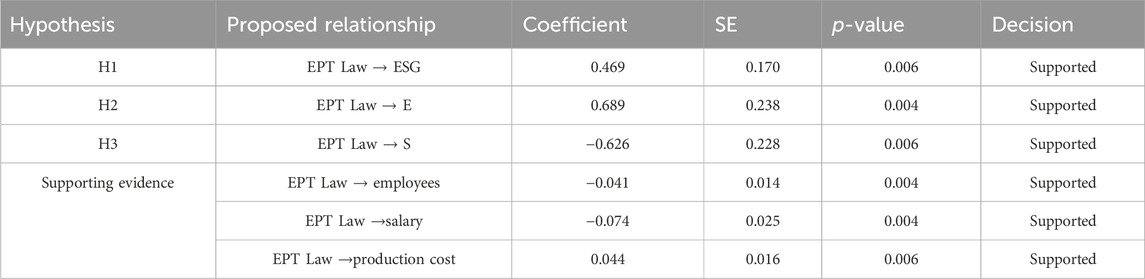

Table 3 displays the primary findings regarding firms’ ESG performance following the implementation of the EPT Law. The coefficients of ESG (0.469) and environmental (E) scores (0.689) are significantly positive at the 1% level. In terms of economic significance, heavy polluting industry firms experienced an average increase of 0.36% in their ESG scores and a 1.46% increase in their environmental (E) scores relative to the mean values. These results confirm H1 and H2, indicating that firms in heavy polluting industries improved their environmental performance and overall ESG scores in response to the EPT Law.

TABLE 3. Impact of the EPT Law on ESG performance.

However, the coefficient of the social (S) score (−0.626) is significantly negative at the 1% level. This suggests that the social (S) score decreased by 0.57% relative to the mean score for firms in heavy polluting industries after the enactment of the EPT Law, confirming H2. Interestingly, the corporate governance (G) scores did not exhibit significant changes following the law’s implementation. This implies that the increase in firms’ ESG scores after the law was enacted was primarily driven by improvements in their environmental (E) scores.

In summary, firms directly responded to the EPT Law by enhancing their environmental performance, leading to increased ESG scores. However, this improvement in environmental performance had a crowding-out effect on their social responsibility performance, as indicated by the significant decrease in social (S) scores. Corporate governance (G) scores remained relatively unaffected by the law’s implementation.

The DiD analysis relies on the crucial assumption of parallel trends, which assumes that the untreated units (control group) can serve as a suitable counterfactual for what the treated units (treatment group) would have experienced had they not received the treatment. In simpler terms, this assumption suggests that, in the absence of the treatment, the differences in outcomes between the treatment and control groups remain relatively constant over time.

To test this assumption, we applied a dynamic effect model

where

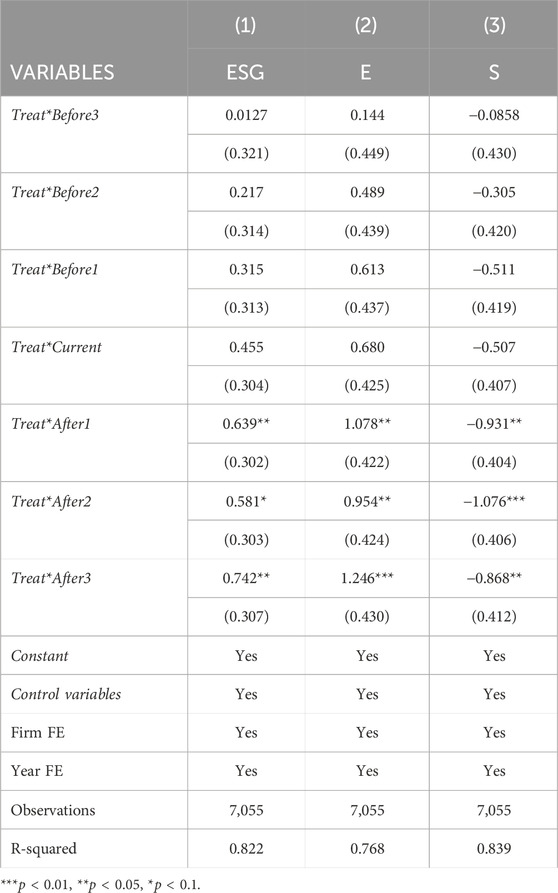

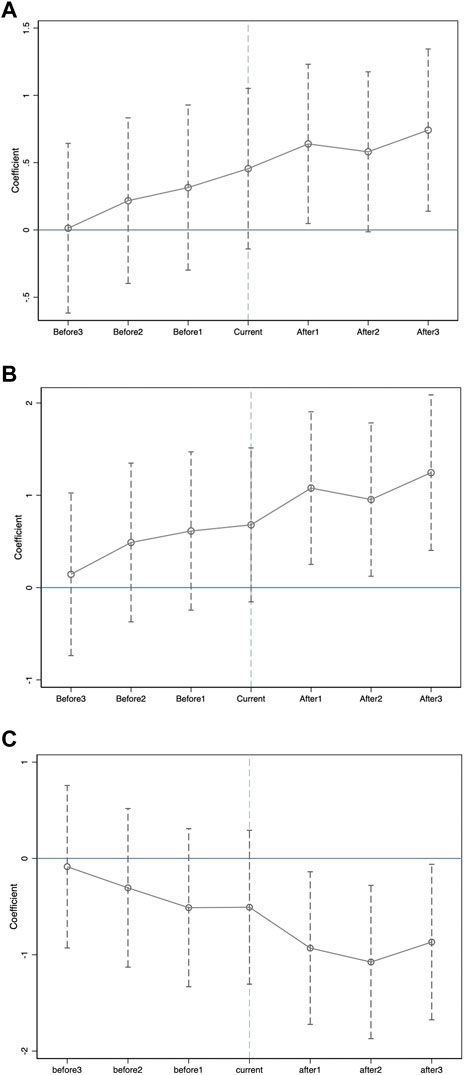

Table 4 and Figure 1 illustrates the results of the parallel trend test conducted 3 years before the enactment of the environmental tax law. The 95% confidence interval contained values around zero in all tests for the three dependent variables (ESG, E, S), and after the enactment year, there were no values around zero. This outcome confirms that the parallel trend assumption was satisfied, indicating that the treated and control groups had similar trends before the implementation of the EPT Law.

TABLE 4. Parallel trend of the EPT Law on ESG performance.

FIGURE 1. Dynamic effects of the EPT Law on ESG performance.

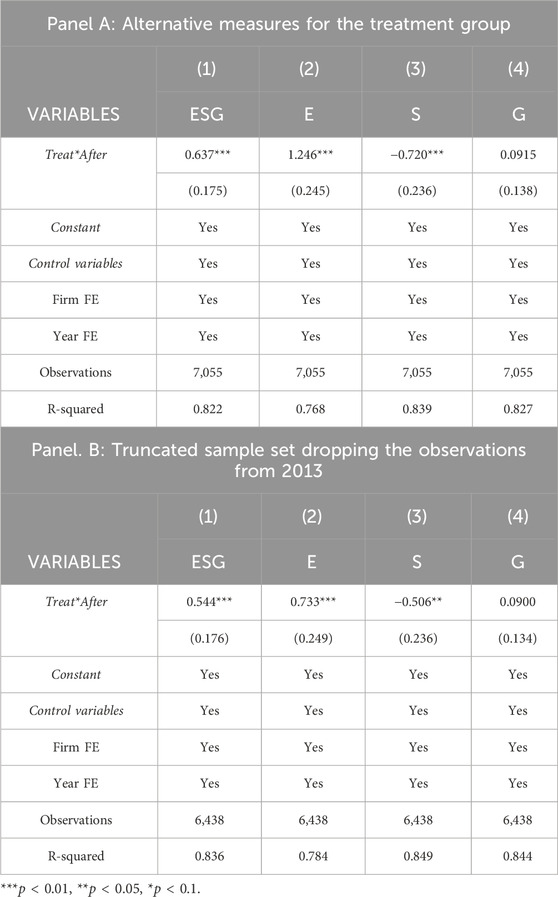

In our baseline model, we initially utilized the Guidelines for Environmental Information Disclosure of Listed Companies to identify the heavy polluting industries. However, it is worth noting that various researchers have employed different methods to classify China’s polluting industries, which could lead to variations in the outcomes of experimental groups.

To ensure the robustness and generalizability of our findings, we adopted an alternative classification standard based on the criteria provided by He et al. (2020). This classification was derived from the Announcement on the implementation of Special Emission Limits for Air Pollution issued by the Ministry of Ecology and Environment of the People’s Republic of China. We applied this new classification to the same model used in the baseline analysis.

The results of this alternative classification, presented in Panel A of Table 4, demonstrated the same level of significance (p < 0.01) and exhibited coefficients that were similar to those observed in the baseline model. These findings suggest that our original model’s results are robust and applicable across different treatment groupings.

During the period from 2012 to 2020, several other policies besides the Environmental Protection Tax (EPT) Law may have influenced firms’ ESG performance, potentially introducing bias into our baseline estimation results. One notable policy is the revised version of the China Labor Contract Law, which imposed stringent restrictions on labor dispatch. This revision was promulgated on 28 December 2012. Labor dispatch is a significant method that companies use to reduce labor costs. The restrictions imposed by this policy may have compelled companies to alter their employment strategies, leading to increased hiring costs and potential reductions in employee headcount or wages, which could have a detrimental effect on their social performance.

To mitigate the impact of this labor-related policy on our analysis, we conducted a Difference-in-Difference (DiD) analysis using a truncated dataset that excluded observations from the year 2013. The results of this analysis, presented in Panel B of Table 5, align with our baseline findings.

TABLE 5. Robustness checks.

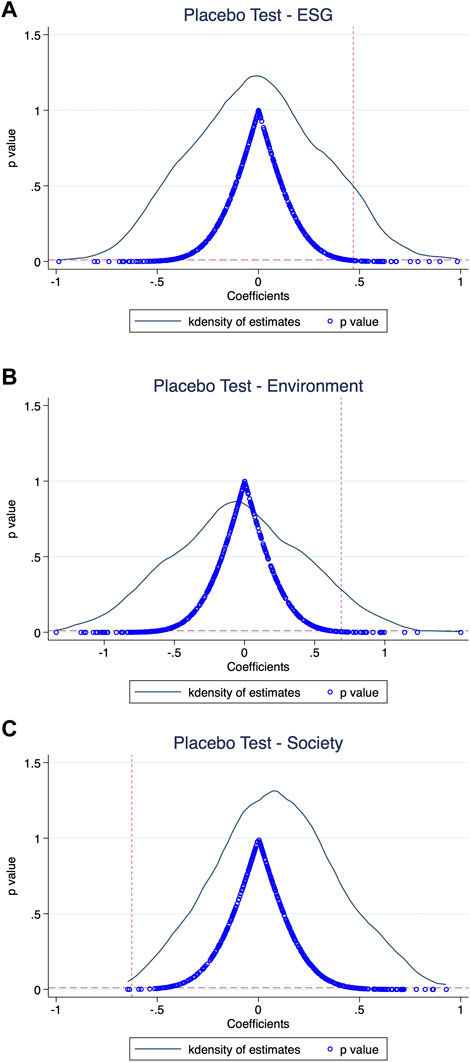

To assess the robustness of our findings and ensure that our results were not unduly influenced by random chance or omitted variables, we conducted a placebo test. In this test, we randomly selected 284 firms to serve as fictitious treatment groups from the total pool of 1,014 firms. We assumed that these randomly selected firms belonged to heavy polluting industries, with the remaining firms constituting the control group. To mitigate the potential impact of random, low-probability events on the test, we repeated this random sampling process 500 times.

For each of these 500 fictitious treatment groups, we conducted a regression analysis using the same baseline model as in our primary analysis. This resulted in 500 sets of regression coefficients for the core explanatory variables. Figure 2 displays the distribution of kernel density estimates for these coefficients along with their respective p-values.

FIGURE 2. Placebo tests for randomly assigned treatment groups.

The majority of estimated coefficients clustered around 0, and their associated p-values exceeded 0.01, indicating that these coefficients were not statistically significant. However, the estimated coefficient reported in our primary analysis stood out as a clear outlier in the figure. This suggests that our primary analysis yielded a statistically significant result that was unlikely to have been influenced by random chance factors or omitted variables.

Based on the results of this placebo test, it is unlikely that the estimators used in this study were affected by chance factors or omitted variables.

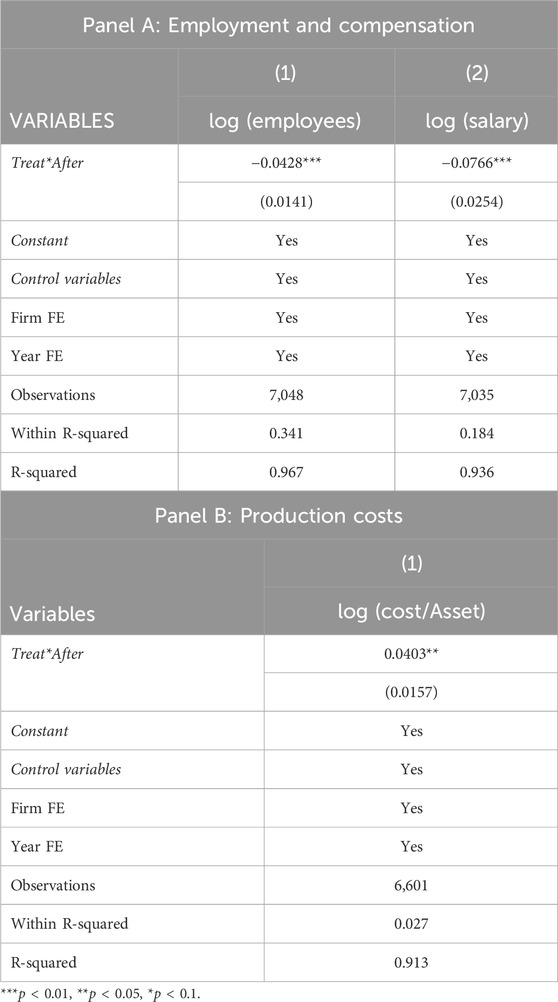

Employment and employees’ wages are critical components of a company’s social performance. The implementation of an environmental tax can have several interconnected effects, including an increase in product prices, a decrease in production scale, and subsequently, a reduced demand for production factors, including labor (Cao et al., 2017; Dechezleprêtre and Sato, 2017). The impact of environmental tax laws on wages is multifaceted and depends on various factors.

In line with the findings of Xiao et al. (2022), who observed that environmental regulations led to a significant reduction in average employee wages due to decreased firm profitability, we conducted a Difference-in-Difference (DiD) analysis. In this analysis, we used the total number of employees log(employees) and total salary expenses log(salary) as dependent variables. We held all other control variables constant, consistent with the baseline regression for the social (S) score, which already controlled for the environmental (E) score.

The results, as presented in Panel A of Table 6, indicate a statistically significant negative impact on both the number of employees and salary expenditures. Specifically, there was an average decrease of 4.28% in the number of employees and a decrease of 7.66% in salary expenses for companies operating in heavy polluting industries following the enactment of the EPT Law, in comparison to other companies.

TABLE 6. Supporting evidence.

One of the primary reasons behind the adverse impact of environmental regulations on firms’ social responsibility performance is the increase in production costs incurred due to efforts to reduce pollution. When production technology and resource limitations remain unchanged, various production factors serve as constraints on production (Li et al., 2019). Moreover, the impact of environmental regulation on enterprise production costs through two aspects: the innovation effect and cost effect. On the one hand, environmental regulations can stimulate innovation within enterprises, thereby reducing compliance costs and enhancing competitiveness. On the other hand, the cost theory suggests that stringent environmental regulations compel firms to invest significantly in compliance. When high-intensity environmental regulations reduce the overall level of enterprise R&D costs, the innovation effect cannot fully compensate for the cost effect, resulting in an increase in overall production costs (Kneller and Manderson, 2012).

The compliance cost theory posits that stringent environmental regulations compel firms to invest significantly in compliance. When production technology and resource limitations remain unchanged, various production factors serve as constraints on production (Li et al., 2019).

To estimate production costs, we used the ratio of operating costs to total assets, where a higher ratio signifies that a larger proportion of a company’s assets is allocated to cover operating expenses, resulting in decreased efficiency. In a similar manner to our previous DiD analyses, we conducted an analysis while excluding the environmental (E) score and Size, which were controlled for in the baseline model. The exclusion of the environmental (E) score was due to our focus on investigating the potential mechanism of the crowding-out effect, and Size was omitted as it is a component of the dependent variable.

The results, as presented in Panel B of Table 6, confirm that the enactment of the EPT Law had a significant negative impact on production costs, which could be the main reason for the firms’ inferior social (S) performance.

Additionally, we present results excluding fixed effects in Supplementary Appendix A, which provide more reference for meaningful R-square. Also, robustness test attached in Supplementary Appendix B.

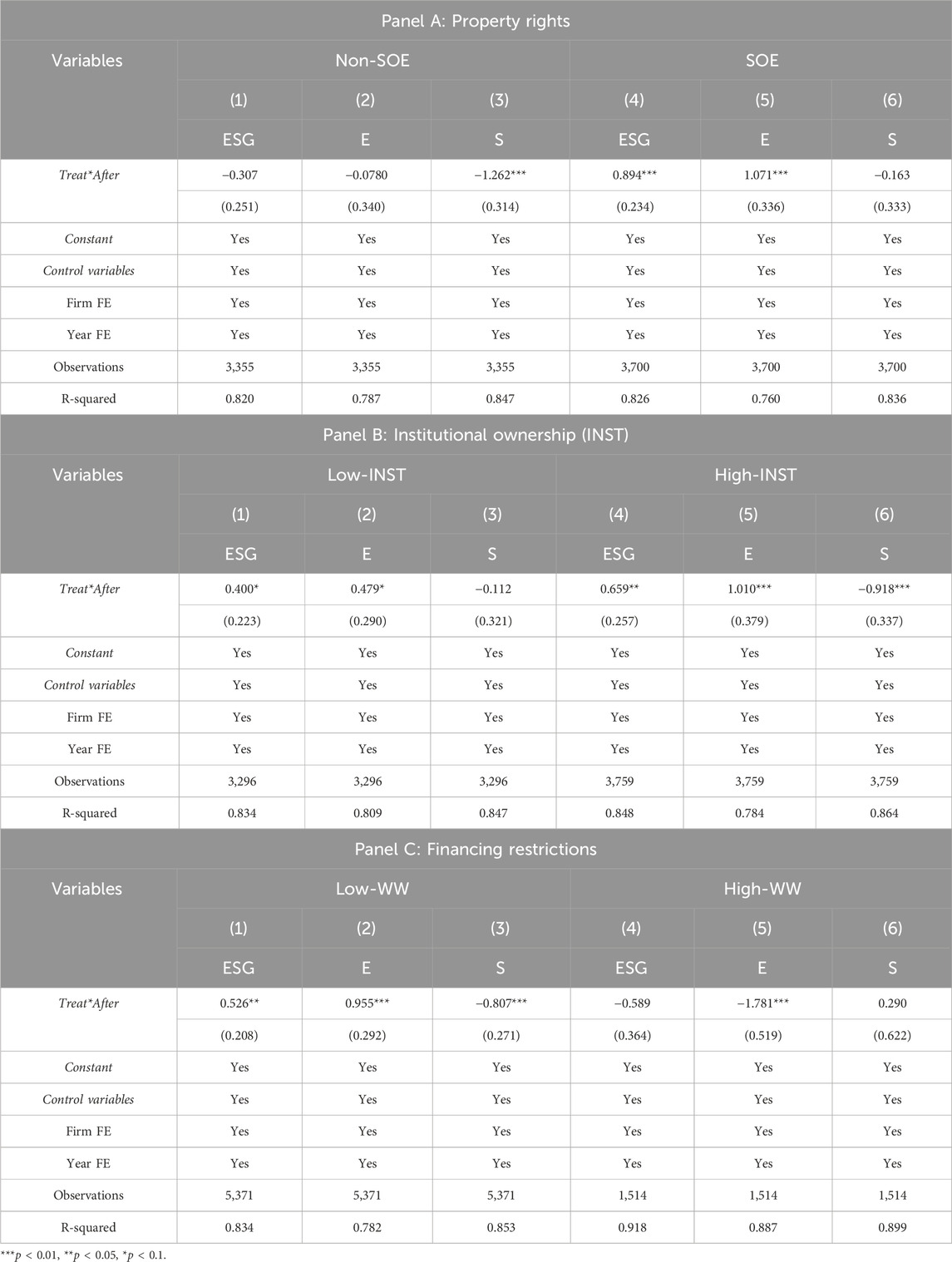

In China, state-owned enterprises (SOEs) are subject to government oversight and management, which allows for the strict and thorough implementation of national strategies, including environmental regulations, without significant hindrance from market conditions or corporate managers (Huang, 2018). Consequently, SOEs are inclined to enforce the EPT Law rigorously to reduce environmental pollution. Unlike non-SOEs, SOEs do not prioritize profit maximization as their primary objective. They often bear various social responsibilities that are unaffected by budget constraints, as they play roles in supporting social functions (Kuo et al., 2012). Existing studies have also confirmed inferior ESG performance in non-SOEs compared to SOEs (Ruan and Liu, 2021; Lu and Cheng, 2023).

Given these factors, we assumed that SOEs would exhibit better ESG performance and experience minimal crowding-out effects compared to non-SOEs. This assumption stemmed from the idea that SOEs are more willing to invest in environmental improvement without reducing their commitments to social responsibility. The results presented in Panel 1 of Table 7 support our assumption. Specifically, we observed the crowding-out effect on social responsibility solely in non-SOEs, while the environmental (E) score and overall ESG score exhibited significant improvements only in SOEs. These findings suggest that the regulatory impact of the EPT Law on emissions from heavy-polluting enterprises primarily affected SOEs, with no significant crowding-out effect on their social responsibility initiatives.

TABLE 7. Heterogeneity analyses.

In previous studies, institutional ownership (INST) has often been associated with a positive impact on a company’s ESG performance. For instance, research by Dyck et al. (2019) indicated that institutional ownership can enhance the environmental and social performance of firms due to the potential for financial and social returns (Dyck et al., 2019).

To investigate this further, we conducted a test by categorizing our samples into “low-INST” and “high-INST” groups based on whether a company’s INST was below or above the mean value of the entire sample set. The results, as presented in Panel B of Table 7, confirm a positive influence of the EPT law on ESG and environmental (E) scores in companies with high INST. However, this effect was much weaker in low-INST companies in terms of both significance level and magnitude.

It is worth noting that, in contrast to findings from Dyck et al. (2019), our results show a negative impact of the EPT law on the social (S) scores of high-INST firms. However, this discrepancy potentially reflect a “myopic” management approach in high-INST companies (Li et al., 2022; Peng, 2022). Also, our results accord with the current research that INST is positively related to corporate ESG performance (Wang et al., 2023).

The ESG performance of firms can vary based on their financing constraints (Wu et al., 2022). Firms with tight financing constraints may face limitations on their ability to invest in environmental initiatives due to uncertainties surrounding returns and sunk investment costs (Ferrando et al., 2017).

To measure the financing constraints of companies, we employed the WW score developed by Whited and Wu (2006). We then divided our sample into “low-WW” and “high-WW” subsamples using the mean WW score of the entire sample as the cutoff. The results, presented in Panel C of Table 7, are significant and align with the baseline findings for companies with relatively low financing constraints. These firms, which have more resources available, are better equipped to invest in environmental protection.

Conversely, companies with high financing constraints exhibited a different trend: a negative impact on their ESG and environmental (E) scores after the enactment of the EPT Law. Research from Shu and Tan (2023) shows that environmental policy has increased firms’ compliance costs, heightened the uncertainty of paying debts on time, and increased the difficulty of financing for these firms. As a result, firms are unable to secure sufficient funds to support ESG activities, leading to a negative impact on ESG performance (Shu and Tan, 2023). Our study supports this conclusion.

In this study, we conducted an analysis of the impact of China’s Environmental Protection Tax Law on the ESG performance of Chinese publicly listed firms. As shown in Table 8, we utilized a DID (difference-in-difference) model along with firm-level data to draw several key conclusions:

TABLE 8. Test results.

First, the law had a significant positive effect on the overall ESG performance of the analyzed firms, particularly in terms of their environmental (E) scores. Second, however, the law also had a significant negative impact on the social responsibility (S) performance of these firms, indicating the presence of a crowding-out effect. Third, we identified that the mechanism driving this crowding-out effect was the increase in production costs caused by the environmental tax. This led to a reduction in labor demand and a decrease in wage expenditures.

Furthermore, our analyses of heterogeneity revealed that state-owned enterprises (SOEs) did not experience the crowding-out effect on social responsibility when they improved their environmental and overall ESG performance. Lastly, companies with high levels of institutional shareholding and those with low financing constraints showed significant improvements in their ESG and environmental performance following the enactment of the law.

Our study has shed light on the impact of the EPT Law on corporate ESG (Environmental, Social, and Governance) performance, addressing our first and second hypotheses (H1 and H2). We found compelling evidence to support these hypotheses, aligning with previous research that has consistently shown the positive influence of environmental regulations on corporate ESG performance (Aluchna et al., 2022; Wang L. et al., 2022; Li J. and Li S., 2022). It is crucial to note that ESG performance comprises three key dimensions: environmental (E), social (S), and corporate governance (G). In our analysis, we observed a notably positive impact of the EPT Law on the environmental (E) score. However, upon adjusting for the E score, we identified a significant negative effect on the social (S) score, while no discernible impact was observed on the corporate governance (G) score. These findings collectively suggest that the enhancement of corporate ESG performance, driven by the EPT Law, primarily stems from substantial improvements in environmental (E) performance. This result underscores the response of companies to the imperative of regulatory compliance, as they allocate resources directly towards environmental protection. This allocation is fueled by the dual pressures of regulatory and normative factors according to neo-institutional theory. As a consequence, we witness an enhancement in the environmental (E) score, which subsequently bolsters the overall ESG performance of corporations.

Regarding the third hypothesis, our study found a significant negative influence of the EPT Law on corporates’ social (S) performance, which supported H3. Interestingly, our findings diverged from some prior research (Wang L. et al., 2022; Li J. and Li S., 2022) but resonated with well-established literature on the regulatory crowding-out effect, as corroborated by earlier studies (Lu and Zhu, 2021; Naatu et al., 2022). The intricacies of this phenomenon are multifaceted. On one hand, firms, grappling with financing constraints, tend to reallocate resources previously earmarked for enhancing social responsibility towards environmental protection. This shift in resource allocation is often driven by the imperative to meet rigorous regulatory mandates. On the other hand, the implementation of environmental regulations carries certain externalities. Given the inherent association between intensified environmental protection and government-enforced environmental regulation, there is a propensity for it to crowd out firms’ voluntary endeavors towards environmental responsibility (Naatu et al., 2022). This, in turn, results in diminished stakeholder interest in the firm’s commitment to environmental protection. In such a dynamic, the EPT Law can indeed lead to a decrease in corporate social (S) scores.

Additionally, our further analysis highlights a significant negative influence of the EPT Law on employment and employee salaries. These labor market dynamics, integral to the social (S) dimension within the ESG framework, warrant closer examination of the regulatory crowding-out effect. Our investigation reveals a noteworthy decrease in both the number of employees and total wage expenditures within firms following the implementation of the EPT Law, providing further support for H3. To delve into the underlying mechanisms at play, we conducted an additional inquiry into the impact of the EPT Law on production costs. The findings unveil a substantial positive effect of the regulation on production costs. Our results elucidate that as firms ramp up investments in environmental protection, production costs rise. This, in turn, often leads to price increases and reduced demand, subsequently dampening the demand for labor within firms. This phenomenon manifests as workforce reductions or salary cuts (Curtis, 2018). These outcomes challenge the existing research that supports the “double dividend” hypothesis, which posits that improving production efficiency through environmental regulations can enhance employment (Glomm et al., 2008). Instead, our findings align with research that raises concerns about the potential threat of environmental regulations to employment (Morgenstern et al., 2002; Dechezleprêtre and Sato, 2017; Yip, 2018).

At last, we explore the heterogeneity of our hypotheses across various company characteristics, including property rights, institutional ownership, and financing constraints. Firstly, after the implementation of the EPT Law, state-owned enterprises (SOEs) demonstrate significant enhancements in their ESG performance and environmental (E) scores. Importantly, this improvement does not lead to a crowding-out effect on their social (S) scores. This outcome can be attributed to the multifaceted administrative and societal functions often shouldered by Chinese SOEs, functions that are typically unaffected by budget constraints. In contrast, non-SOEs experience a noticeable decline in their social (S) scores without a corresponding increase in environmental (E) scores. It is worth noting that in ESG evaluations, a significant aspect of environmental performance for businesses revolves around pollution emissions. In this context, if non-SOEs opt to solely pay environmental taxes without actively taking measures to reduce pollution, it may also result in social (S) dimension pressures. Secondly, companies with high institutional ownership provide significant support for our research hypotheses and exhibit greater sensitivity to environmental taxes. This observation can be explained by cost-benefit theory, as institutional investors are often regarded as “sophisticated investors” who place a strong emphasis on a company’s long-term value derived from its sustainability capabilities. They are also more responsive to regulations and societal demands (Jo and Harjoto, 2012). Lastly, companies with low financing constraints align more closely with the assumptions presented in this paper, promptly reducing pollution emissions following the implementation of the EPT Law. Conversely, companies with high financing constraints exhibit a notable decrease in environmental (E) scores. This phenomenon may be attributed to companies attempting to evade regulation by no longer disclosing certain pollution indicators after the law’s enactment. In conclusion, it is evident that the impact of the EPT Law on corporate ESG performance and its various dimensions varies among different enterprises. Further exploration and analysis are needen to fully understand the nuances of these effects.

This study provides valuable insights into the impact of environmental tax laws on corporate ESG (Environmental, Social, and Governance) performance through the lens of neo-institutional theory. This perspective is crucial for enhancing the overall governance system within the government. Furthermore, it enriches the theoretical analysis of the Environmental Protection Tax (EPT) Law, going beyond the conventional confirmation of environmental regulations promoting corporate social responsibility and ESG performance, to delve into the underlying mechanisms and theoretical foundations (Wang L. et al., 2022; Wang X. et al., 2022; Lu and Cheng, 2023). The study results indicate that the EPT Law exerts pressure on companies through regulative pressure and normative pressure, compelling them to improve their environmental performance. This insight prompts policymakers to gain a deeper understanding of the drivers behind corporate compliance and the varying degrees of compliance among different types of companies. Consequently, this study contributes to unraveling the pathways and potential mechanisms through which environmental policies positively influence corporate ESG performance, thus broadening the application scope of neo-institutional theory.

Additionally, this paper explores the potential negative externalities of the EPT Law by examining crowding-out effects, dissecting the trade-offs within the corporate ESG framework and expanding the research horizon of corporate ESG. Existing studies have primarily concentrated on the policy’s impact on different dimensions of ESG, consistently yielding positive conclusions (Wang L. et al., 2022; Li J. and Li S., 2022). In contrast, this research places a stronger emphasis on resource reallocation within the ESG system. It suggests that when confronted with environmental policy pressures, firms may divert investments initially designated for the social (S) dimension towards environmental protection, resulting in a crowding-out effect on social factors. The institutional crowding-out effect pertains to the displacement of intrinsic motivations by external incentives, and environmental protection regulations may disrupt self-motivation, leading to a “price regulation” failure (Fehr and Gächter, 2001). While some studies have explored the crowding-out effects of China’s environmental tax on other forms of technological innovation (Liu and Xiao, 2022), this paper extends the analysis within the ESG framework, introducing a fresh dimension to the study of environmental policy.

Lastly, this paper challenges the notion of the “double dividend effect” by examining the influence of the EPT Law on the labor market. It demonstrates that, at least in the case of this specific law, companies cannot achieve increased employment or enhanced production efficiency. The “double dividend effect” theory posits that environmental policies, by curbing pollution emissions and enhancing resource allocation efficiency of companies, can deliver both improved environmental quality and more job opportunities (Carraro et al., 1996). However, empirical studies have increasingly cast doubt on this theory, suggesting that environmental protection regulations can, in fact, lead to a reduction in employment levels. This paper contributes further evidence to support this skepticism. Consequently, in the process of formulating environmental policies, governments should be cognizant of the potential adverse impacts of such policies. While enforcing mandatory measures within the regulatory framework, they should also incorporate incentives and guidance into environmental governance systems, encouraging businesses to partake in green innovation and improve production technologies. In doing so, they can genuinely realize the elusive “double dividend”—a harmonious balance between environmental and economic benefits.

Our study analyzed and tested the mechanism through which the EPT Law influences the ESG performance of listed firms. However, there are several limitations that warrant further investigation in future research. Firstly, this paper only examines data from the 4 years following the implementation of the EPT Law, which represents a relatively short time frame. Policy implementation typically exhibits a lag period, and thus, future research should consider employing a more extended time horizon to explore the long-term effects of policy implementation comprehensively. Secondly, while this study provides supplementary evidence regarding the impact of the EPT Law on the labor market to demonstrate the crowding-out effect of corporate social responsibility, this demonstration is not exhaustive. Future research should conduct a more comprehensive analysis encompassing all factors within the ESG framework that related to the social (S) dimension and provide a more nuanced examination. Lastly, this research has examined the heterogeneity in policy effects across different types of enterprises and speculated on potential mechanisms. Future research could delve into a more detailed investigation and validation of these mechanisms, providing a deeper understanding of the complex interactions between environmental policies and corporate types.

Publicly available datasets were analyzed in this study. This data can be found here: https://www.bloomberg.com/professional/datasets/.

KY: Conceptualization, Data curation, Funding acquisition, Methodology, Writing–original draft. BW: Conceptualization, Formal Analysis, Funding acquisition, Resources, Supervision, Writing–review and editing.

The author(s) declare financial support was received for the research, authorship, and/or publication of this article. This research is supported by the Fundamental Research Funds for the Central Universities, and the Research Funds of Renmin University of China (22XNH090).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenvs.2023.1273278/full#supplementary-material

1https://www.unglobalcompact.org/what-is-gc/our-work/social

2Results without fixed effect show in Supplementary Appendix A.

Alazzani, A., Wan-Hussin, W. N., Jones, M., and Al-Hadi, A. (2021). ESG reporting and analysts’ recommendations in GCC: the Moderation role of royal family directors. J. Risk Financial Manag. 14 (2), 72. doi:10.3390/jrfm14020072

Aluchna, M., Roszkowska-Menkes, M., and Kamiński, B. (2022). From talk to action: the effects of the non-financial reporting directive on ESG performance. Meditari Account. Res. 31 (7), 1–25. doi:10.1108/MEDAR-12-2021-1530

Boyd, R., and Ibarrarán, M. a. E. (2002). Costs of compliance with the Kyoto Protocol: a developing country perspective. Energy Econ. 24 (1), 21–39. doi:10.1016/s0140-9883(01)00080-9

Cao, W., Wang, H., and Ying, H. (2017). The effect of environmental regulation on employment in resource-based areas of China—an empirical research based on the mediating effect model. Int. J. Environ. Res. public health 14 (12), 1598. doi:10.3390/ijerph14121598

Carraro, C., Galeotti, M., and Gallo, M. (1996). Environmental taxation and unemployment: some evidence on the ‘double dividend hypothesis’ in Europe. J. Public Econ. 62 (1-2), 141–181. doi:10.1016/0047-2727(96)01577-0

Curtis, E. M. (2018). Who loses under cap-and-trade programs? the labor market effects of the nox budget trading program. Rev. Econ. Statistics 100 (1), 151–166. doi:10.1162/rest_a_00680

Darrell, W., and Schwartz, B. N. (1997). Environmental disclosures and public policy pressure. J. Account. Public Policy 16 (2), 125–154. doi:10.1016/s0278-4254(96)00015-4

Dechezleprêtre, A., and Sato, M. (2017). The impacts of environmental regulations on competitiveness. Review of environmental economics and policy.

Delmas, M. A., and Toffel, M. W. (2008). Organizational responses to environmental demands: opening the black box. Strategic Manag. J. 29 (10), 1027–1055. doi:10.1002/smj.701

Dyck, A., Lins, K. V., Roth, L., and Wagner, H. F. (2019). Do institutional investors drive corporate social responsibility? International evidence. J. financial Econ. 131 (3), 693–714. doi:10.1016/j.jfineco.2018.08.013

Fan, G., Wang, X., and Ma, G. (2011). Contribution of marketization to China’s economic growth. Econ. Res. J. 9 (283), 1997–2011. Retrieved from http://www.chinaeconomist.com/index.php/2016/07/21/the-contribution-of-marketization-to-chinas-economic-growth/.

Fehr, E., and Gächter, S. (2001). Do incentive contracts crowd out voluntary cooperation? Available at SSRN 289680.

Ferrando, A., Marchica, M. T., and Mura, R. (2017). Financial flexibility and investment ability across the Euro area and the UK. Eur. Financ. Manag. 23 (1), 87–126. doi:10.1111/eufm.12091

Glomm, G., Kawaguchi, D., and Sepulveda, F. (2008). Green taxes and double dividends in a dynamic economy. J. policy Model. 30 (1), 19–32. doi:10.1016/j.jpolmod.2007.09.001

Gözlügöl, A. A. (2022). The clash of ‘E’and ‘S’of ESG: just transition on the path to net zero and the implications for sustainable corporate governance and finance. J. World Energy Law Bus. 15 (1), 1–21. doi:10.1093/jwelb/jwab039

Greenstone, M. (2002). The impacts of environmental regulations on industrial activity: evidence from the 1970 and 1977 clean air act amendments and the census of manufactures. J. political Econ. 110 (6), 1175–1219. doi:10.1086/342808

He, G., Wang, S., and Zhang, B. (2020). Watering down environmental regulation in China. Q. J. Econ. 135 (4), 2135–2185. doi:10.1093/qje/qjaa024

Hou, D., and Wei, Y. (2023). Construction of ESG information disclosure framework for listed companies: based on the perspective of new development concept. Law Econ. (05), 3–17. (Chinese Version). doi:10.16823/j.cnki.10-1281/d.2023.05.002

Huang, D. (2018). Top-level design and fragmented decision-making: a case study of an SOE merger in China’s high-speed rail industry. J. Contemp. China 27 (109), 151–164. doi:10.1080/10670564.2017.1363027

Ji, S., and Su, M. (2016). The motivation of the environmental costs internalization: is it for policy compliance or for profits? empirical evidence from Chinese listed companies in heavy polluting industrie. Acc. Res. 11, 69–75. doi:10.4236/me.2020.111005

Jia, K., and Chen, S. (2019). Could campaign-style enforcement improve environmental performance? Evidence from China’s central environmental protection inspection. J. Environ. Manag. 245, 282–290. doi:10.1016/j.jenvman.2019.05.114

Jo, H., and Harjoto, M. A. (2012). The causal effect of corporate governance on corporate social responsibility. J. Bus. ethics 106, 53–72. doi:10.1007/s10551-011-1052-1

Kneller, R., and Manderson, E. (2012). Environmental regulations and innovation activity in UK manufacturing industries. Resour. Energy Econ. 34 (2), 211–235. doi:10.1016/j.reseneeco.2011.12.001

Kuo, L., Yeh, C. C., and Yu, H. C. (2012). Disclosure of corporate social responsibility and environmental management: evidence from China. Corp. Soc. Responsib. Environ. Manag. 19 (5), 273–287. doi:10.1002/csr.274

Li, B., Li, L., and Pi, T. (2022). Is the R&D expenditure of listed companies green? Evidence from China’s A-share market. Int. J. Environ. Res. Public Health 19 (19), 11969. doi:10.3390/ijerph191911969

Li, J., Ji, J., and Zhang, Y. (2019). Non-linear effects of environmental regulations on economic outcomes. Manag. Environ. Qual. Int. J. 30 (2), 368–382. doi:10.1108/meq-06-2018-0104

Li, J., and Li, S. (2022). Environmental protection tax, corporate ESG performance, and green technological innovation. Front. Environ. Sci. 1512. doi:10.3389/fenvs.2022.982132

Li, L., Wang, Y., Sun, H., Shen, H., and Lin, Y. (2023a). Corporate social responsibility information disclosure and financial performance: is green technology innovation a missing link? Sustainability 15 (15), 11926. doi:10.3390/su151511926

Li, L., Wang, Y., Tan, M., Sun, H., and Zhu, B. (2023b). Effect of environmental regulation on energy-intensive enterprises’ green innovation performance. Sustainability 15 (13), 10108. doi:10.3390/su151310108

Liu, G., Yang, Z., Zhang, F., and Zhang, N. (2022). Environmental tax reform and environmental investment: a quasi-natural experiment based on China’s Environmental Protection Tax Law. Energy Econ. 109, 106000. doi:10.1016/j.eneco.2022.106000

Liu, J., and Xiao, Y. (2022). China's environmental protection tax and green innovation: incentive effect or crowding-out effect? Econ. Res. J. (01), 72–88. (Chinese Version).

Lu, C., and Zhu, K. (2021). Do tax expenses crowd in or crowd out corporate social responsibility performance? Evidence from Chinese listed firms. J. Clean. Prod. 327, 129433. doi:10.1016/j.jclepro.2021.129433

Lu, S., and Cheng, B. (2023). Does environmental regulation affect firms' ESG performance? Evidence from China [Article]. Manag. Decis. Econ. 44 (4), 2004–2009. doi:10.1002/mde.3796

Luo, K., and Wu, S. (2022). Corporate sustainability and analysts’ earnings forecast accuracy: evidence from environmental, social and governance ratings. Corp. Soc. Responsib. Environ. Manag. 29 (5), 1465–1481. doi:10.1002/csr.2284

Mao, E., and Zhou, Z. (2021). Environmental tax reform and double dividend hypothesis: a theoretical review. China Popul. Resour. Environ. 12 (31), 128–139. (Chinese Version).

Miller, G. S. (2006). The press as a watchdog for accounting fraud. J. Account. Res. 44 (5), 1001–1033. doi:10.1111/j.1475-679x.2006.00224.x

Morgenstern, R. D., Pizer, W. A., and Shih, J.-S. (2002). Jobs versus the environment: an industry-level perspective. J. Environ. Econ. Manag. 43 (3), 412–436. doi:10.1006/jeem.2001.1191

Naatu, F., Nyarko, S. A., Munim, Z. H., and Alon, I. (2022). Crowd-out effect on consumers attitude towards corporate social responsibility communication. Technol. Forecast. Soc. Change 177, 121544. doi:10.1016/j.techfore.2022.121544

Palazzo, G., and Scherer, A. G. (2006). Corporate legitimacy as deliberation: a communicative framework. J. Bus. ethics 66 (1), 71–88. doi:10.1007/s10551-006-9044-2

Peng, W. (2022). Managerial myopia and corporate social responsibility activities. Front. Bus. Econ. Manag. 5 (3), 276–280. doi:10.54097/fbem.v5i3.2035

Peng, Y. (2013). Research in efficiency of environment policy in the context of economic growth——based on empirical analysis of province Panel data. Finance Trade Econ. (4), 16–23. (Chinese version).

Pratiwi, I. S., and Djakman, C. D. (2017). The role of corporate political connections in the relation of CSR and tax avoidance: evidence from Indonesia. Rev. Integr. Bus. Econ. Res. 6, 345. Retrieved from https://sibresearch.org/uploads/3/4/0/9/34097180/riber_6-s1_sp_s17-120_345-358.pdf.

Qin, M., Fan, L. F., Li, J., and Li, Y. F. (2021). The income distribution effects of environmental regulation in China: the case of binding SO2 reduction targets. J. Asian Econ. 73, 101272. doi:10.1016/j.asieco.2021.101272

Ruan, L., and Liu, H. (2021). Environmental, social, governance activities and firm performance: evidence from China. Sustainability 13 (2), 767. doi:10.3390/su13020767

Scott, W. R. (2008). Approaching adulthood: the maturing of institutional theory. Theory Soc. 37, 427–442. doi:10.1007/s11186-008-9067-z

Shu, H., and Tan, W. (2023). Does carbon control policy risk affect corporate ESG performance? Econ. Model. 120, 106148. doi:10.1016/j.econmod.2022.106148

Suchman, M. C. (1995). Managing legitimacy: strategic and institutional approaches. Acad. Manag. Rev. 20 (3), 571–610. doi:10.5465/amr.1995.9508080331

Tu, W. J., Yue, X. G., Liu, W., and Crabbe, M. J. C. (2020). Valuation impacts of environmental protection taxes and regulatory costs in heavy-polluting industries. Int. J. Environ. Res. Public Health 17 (6), 2070. doi:10.3390/ijerph17062070

Waas, B. (2021). The “S” in ESG and international labour standards. Int. J. Discl. Gov. 18 (4), 403–410. doi:10.1057/s41310-021-00121-5

Walker, W. R. (2011). Environmental regulation and labor reallocation: evidence from the clean air act. Am. Econ. Rev. 101 (3), 442–447. doi:10.1257/aer.101.3.442

Wang, L., Le, Q., Peng, M., Zeng, H., and Kong, L. (2022a). Does central environmental protection inspection improve corporate environmental, social, and governance performance? Evidence from China. Bus. Strategy Environ. 32 (6), 2962–2984. doi:10.1002/bse.3280

Wang, X., Elahi, E., and Khalid, Z. (2022b). Do green finance policies foster environmental, social, and governance performance of corporate? Int. J. Environ. Res. Public Health 19 (22), 14920. doi:10.3390/ijerph192214920

Wang, X., Yang, Q., and He, N. (2020). Research on the influence of environmental regulation on social employment—an empirical analysis based on the STR model. Int. J. Environ. Res. Public Health 17 (2), 622. doi:10.3390/ijerph17020622

Wang, Y., Lin, Y., Fu, X., and Chen, S. (2023). Institutional ownership heterogeneity and ESG performance: evidence from China. Finance Res. Lett. 51, 103448. doi:10.1016/j.frl.2022.103448

Whited, T. M., and Wu, G. (2006). Financial constraints risk. Rev. financial Stud. 19 (2), 531–559. doi:10.1093/rfs/hhj012

Wu, Q., Chen, G., Han, J., and Wu, L. (2022). Does corporate ESG performance improve export intensity? Evidence from Chinese listed firms. Sustainability 14 (20), 12981. doi:10.3390/su142012981

Wu, Y., Xu, C., and Chen, J. (2019). Study on the impact of differentiated environmental protection taxes in the imperfect competitive market. China Ind. Econ. 5 (4). (Chinese Version). doi:10.19581/j.cnki.ciejournal.2019.05.003

Xiao, R., Tan, G., Huang, B., and Luo, Y. (2022). The costs of “blue sky”: environmental regulation and employee income in China. Environ. Sci. Pollut. Res. 29 (36), 54865–54881. doi:10.1007/s11356-022-19723-9

Yan, W., Guo, S., and Shi, Y. (2012). Environmental regulation, industrial structure upgrading and employment effect: linear or nonlinear? Econ. Sci. (06), 23–32. (Chinese Version). doi:10.19523/j.jjkx.2012.06.003

Yip, C. M. (2018). On the labor market consequences of environmental taxes. J. Environ. Econ. Manag. 89, 136–152. doi:10.1016/j.jeem.2018.03.004

Yu, L., Xie, P., Liu, Q., and Bi, X. (2022). Artificial intelligence decision-making transparency and employees' trust: the parallel multiple mediating effect of effectiveness and discomfort. Contemp. Finance Econ. 12 (02), 127–137. doi:10.3390/bs12050127

Zhang, T., Zho, J.-y., Hussain, R. Y., Wang, M., and Ren, K. (2022). Research on the cultivation of green competitiveness among Chinese heavily polluting enterprises under country/district environmental regulations. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.955744

Zhang, Y., Zhang, Y., and Sun, Z. (2023). The impact of carbon emission trading policy on enterprise ESG performance: evidence from China. Sustainability 15 (10), 8279. doi:10.3390/su15108279

Zheng, J., He, J., Shao, X., and Liu, W. (2022). The employment effects of environmental regulation: evidence from eleventh five-year plan in China. J. Environ. Manag. 316, 115197. doi:10.1016/j.jenvman.2022.115197

Zhu, L., Hao, Y., Lu, Z. N., Wu, H., and Ran, Q. (2019). Do economic activities cause air pollution? Evidence from China’s major cities. Sustain. Cities Soc. 49, 101593. (Chinese Version). doi:10.1016/j.scs.2019.101593

Keywords: ESG, environmental protection tax, environmental performance, social performance, crowding-out effect, employment

Citation: Yuan K and Wu B (2024) The crowding-out effect of the environmental regulation on corporate sustainability. Front. Environ. Sci. 11:1273278. doi: 10.3389/fenvs.2023.1273278

Received: 07 August 2023; Accepted: 21 December 2023;

Published: 11 January 2024.

Edited by:

Otilia Manta, Romanian Academy, RomaniaReviewed by:

Liang Li, Nanjing University of Information Science and Technology, ChinaCopyright © 2024 Yuan and Wu. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Bangzheng Wu, d3ViYW5nemhlbmdAMTI2LmNvbQ==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.