95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 10 August 2023

Sec. Environmental Economics and Management

Volume 11 - 2023 | https://doi.org/10.3389/fenvs.2023.1256052

This article is part of the Research Topic Sustainability of Digital Transformation for the Environment View all 16 articles

Tao Fu*

Tao Fu* Jiangjun Li

Jiangjun LiIntroduction: Environmental, social, and governance (ESG) considerations have become increasingly important in the financial market and serve as concrete manifestations of sustainable development within a sector. Most corporate leaders have adopted ESG concerns as an important strategy to enhance their financial performance. Therefore, this study investigated whether ESG affects corporate financial performance, and if this relationship is moderated by digital transformation.

Method: We used A-share listed companies in China from 2015 to 2021 as samples to test this mechanism.

Results: Regression analysis showed that ESG positively and significantly affects corporate financial performance, and digital transformation drives this promoting effect. Furthermore, we found that the positive effect of current ESG on financial performance in the lag period will gradually weaken. Specifically, the heterogeneity test results show that the enhancement effect of ESG on financial performance is significant for non-state-owned companies but insignificant for state-owned companies; the same is true for companies located in the eastern region compared with those in the midwestern region. Finally, the enhancement effect of ESG on the financial performance of polluting firms is stronger than that on non-polluting firms.

Conclusion: These findings will be useful for firms and government departments in formulating relevant policies.

The concept of environmental, social, and governance (ESG) originated from responsible and ethical investment (Wang and Sarkis, 2017). Similar to social responsibility and ethics, ESG serves as a guide for corporate risk management and operations. Owing to its comprehensive effects in alignment with the current international focus on green, low-carbon, and sustainable development, ESG has become a research hotspot in the global economy and management field (Paradis and Schiehll, 2021; Finger and Rosenboim, 2022).

According to the Global Sustainable Investment Alliance (GSIA) report, global ESG assets under management reached $28.6 trillion in 2017, accounting for 30% of the total worldwide. On 15 June 2018, the China Securities Regulatory Commission (CSRC) issued a revised version of the Code of Corporate Governance for Listed Companies in China, explicitly requiring listed companies to disclose ESG information. For investors, ESG criteria have become a collection of principles that they can use to evaluate potential investments based on a company’s operational activities. For enterprises, assuming responsibility for ESG issues has become a potential driving force for economic benefits. Although investing in ESG initiatives such as purchasing environmentally friendly equipment, protecting workers’ rights, and practicing community responsibility, may significantly increase short-term costs, businesses can reap benefits over time from these sustainable investments and potentially successfully promote their products and enhance their reputations. Therefore, in this study, we aim to investigate how does ESG affects corporate financial performance.

As the ESG framework has become embedded into corporate development strategies and operational management processes, the relationship between ESG and financial performance has been extensively discussed in academic literature (Tarmuji et al., 2016; Minutolo et al., 2019). Enterprise ESG information disclosure can effectively alleviate information asymmetry and agency problems, thereby enhancing enterprises’ information transparency and reducing financing costs (Fatemi et al., 2015). It can also establish a good corporate social responsibility image, strengthen a company’s relationships with stakeholders, and enhance its reputation (Lian et al., 2023). However, the ESG concept in China remains in its early stages (Wang et al., 2023). In 2021, approximately 26% of Chinese listed companies independently published ESG reports. Although the disclosure rate of indicators in various dimensions have improved, problems with unbalanced and inadequate disclosures remain (Yang et al., 2023). Most companies currently face issues such as inadequate capabilities and high costs in ESG practices, which greatly reduce their intrinsic motivation to fulfill ESG obligations (Cong et al., 2023). Regulators and investors still encounter many difficulties in obtaining ESG data to use as a basis for decision-making (Zhang and Liu, 2022). Thus, in China, it is essential to promote ESG development, enhance the ability of companies to engage in ESG practices, and stimulate companies’ intrinsic motivation.

The innovative development and application of digital information technologies, represented by artificial intelligence (AI), blockchain technology, cloud computing, and Big Data, provide effective technical means to enhance companies’ ESG capabilities (Chen et al., 2022). First, digital technology integration with the real economy can reduce costs and improve efficiency in areas such as information collection, decision support, and operational management, while meeting companies’ ESG information disclosure and market supervision needs (Sedunov, 2017; Lv and Xiong, 2022). Second, the efficiency and convenience of digital information technology are driving many companies to shift from traditional production models to digital intelligence development. Digital transformation reduces the costs of fulfilling social responsibility obligations and improves accountability efficiency, thereby providing a foundation for improving ESG performance (Bhandari et al., 2022). Therefore, we argue that digital transformation is an important factor requiring further consideration in the context of its role in the relationship between ESG and financial performance.

The contributions of our study are as follows. Firstly, previous research on the relationship between ESG and financial performance has mainly focused on developed counties, with less attention paid to developing countries. We used Chinese listed companies as research samples to verify this relationship, thus expanding the existing literature. Second, our study is among the first to use digital transformation as a moderating variable to investigate the relationship between ESG and financial performance. Furthermore, owing to variations in property rights, regional environments, and potential for environmental pollution, businesses are subject to different policy constraints. Thus, we classified firms into various groups based on their property rights, regions, and pollution levels, and analyzed how ESG practices affect their financial performance in different contexts. This study provides guidance for policymakers and companies to develop effective policies for green sustainable development to promote economic recovery in the post-pandemic era.

The remainder of this paper is organized as follows: Section 2 presents a literature review concerning ESG and financial performance, and then proposes the hypotheses. Section 3 includes the data, variables, and research model. The empirical analysis is presented in Section 4. Section 5 reports the results of the grouped regression, and Section 6, 7 present the discussion and conclusions, respectively.

The concept of ESG was first proposed in a report published by the United Nations Principles for Responsible Investment (UNPRI) in 2006 (Hoepner et al., 2021). The UNPRI argues that responsible investors should thoroughly consider the impact of ESG factors on investment value, view that has gained increasing prominence in investment choices worldwide.

Under the backdrop of the “dual carbon” goal, interest in the connection between corporate ESG and financial performance has been increasing among academics, practitioners, and international standard-setters (Abdi et al., 2022; Wang et al., 2022). Although consensus has been reached in the literature regarding the relationship between ESG and corporate performance, at present, the academic community generally holds the view that negative ESG events harm corporate performance (Krüger, 2015). From a sustainable development perspective, enterprises should concentrate on environmental protection and rational resource utilization to provides an excellent long-term development environment for promoting sustainable business development (Jeffrey et al., 2019). By creating a green, environmentally friendly corporate image through taking a long-term view of corporate development and not pursuing short-term benefits for immediate profit, companies may obtain long-term returns (Gao and Han, 2020). According to stakeholder theory, companies that can effectively manage their relationships with all stakeholders tend to achieve success, because this theory suggests that companies should not only be accountable to shareholders but also to creditors, employees, suppliers and customers, the government, the community, and the environment (Freeman, 1984). Stakeholder theory emphasizes the external corporate governance to maximize stakeholders’ overall interests of, which, in turn, will lead to higher growth and benefits companies (Teplova et al., 2022). For example, satisfied employees are more motivated in their work and satisfied suppliers provide higher-quality raw materials. This allows a company to build a good reputation, thereby promoting performance improvement. Lev et al. (2010) noted that in consumer-sensitive industries, corporate charitable donations contribute to companies’ future income. Carnini et al. (2022) found that timely disclosure of information through announcements is crucial for companies to achieve short-term success. Through ESG disclosure, companies can effectively enhance transparency and reduce information asymmetry, thereby enhancing investor confidence in their long-term investments in the company (Cui et al., 2018). Friede et al. (2015) summarized and analyzed over 2000 ESG-related studies and found that approximately 90% indicated a positive relationship between ESG and financial performance. Therefore, we proposed the following hypothesis:

H1. When a company performs well in terms of ESG, ESG can contribute to positive financial performance.

Several studies have revealed that the application of digital technology significantly promotes economic development (Wong et al., 2021), boosts manufacturing upgrades, optimizes employment structures, enhances quality improvement, and fosters entrepreneurial activity (Papagiannidis et al., 2020). The value of digital transformation for enterprises reflects innovations and breakthroughs in not only production technology but also various aspects such as those concerning the environment, society, and corporate governance (Shimizu, 2020).

ESG practices have specific externalities that lead to insufficient investment. Company investment in environmental and social responsibility can consume corporate resources, resulting in financial expenses that damage shareholders’ rights and interests, thereby weakening a firm’s competitiveness (Friedman, 2007; Garcia and Orsato, 2020). However, resource constraints, outdated technology, and information asymmetry among stakeholders have limited the ability of many firms to enhance their ESG performance. Consequently, these firms face high costs when implementing ESG practices, and cannot be encouraged to improve them by insufficient incentives (Zhong et al., 2023). Digital transformation provides a viable solution to this problem (ElMassah and Mohieldin, 2020). First, digital transformation can promote enterprise technological innovation, particularly the innovation and application of green technology, thereby promoting companies’ sustainable development. Second, by minimizing information asymmetry, digitalization can enhance enterprise information transparency and reduce transaction costs (Gouvea et al., 2022). This enables companies to improve their governance levels and fulfill their social responsibilities effectively. Finally, digital technology enhances resource allocation and utilization efficiency, thereby improving companies’ decision-making and operational efficiency. Therefore, we propose the following hypothesis:

H2. Embracing digital transformation can help companies improve their ESG.

In the post-pandemic era, enhancing management capabilities and improving the quality of business operations have become important aspects of exploring economic development in complex environments. As the public has gained awareness of Chat AI technology, many firms have invested in the digital transformation process (Ionascu et al., 2022). First, through digital technology, companies can collect, analyze, and monitor environmental data to better identify and address environmental risks, improve energy efficiency, and reduce emissions and waste. Second, based on stakeholder value reciprocity (Freeman, 1984) and the insurance mechanism of corporate social responsibility (Godfrey, 2005), business operators often strive for minimal costs yielding maximum returns. For example, some companies intentionally reduce the quality of their information disclosure (Luo et al., 2017) and selectively manipulate the disclosure language using pseudo-corporate social responsibility to push for stakeholder support if they have limited cognitive abilities. However, the characteristics of Big Data and blockchain technology, such as recordability and traceability, effectively address this issue with information asymmetry (Nambisan et al., 2019) and increase public supervision of corporations. Digital technologies and automated processes can also reduce human resources, change how production factors are combined, and improve supply chain relationships, customer relationship management, and marketing effectiveness. These factors can reduce operational costs and increase profit margins and returns on investment for businesses. Therefore, we propose the following hypothesis.

H3. The effect of ESG on financial performance is more prominent when the degree of digital transformation is high.

Based on data availability, we selected Chinese A-share listed companies from 2015 to 2021 as our samples. We screened and processed the samples based on the following exclusion criteria: 1) listed financial companies, 2) ST and *ST companies, 3) companies with a debt-to-asset ratio greater than 1, and 4) samples with missing data. To avoid interference from outliers in the results of the empirical analysis, all continuous variables were winsorized at the 1% and 99% quantiles. Finally, we obtained a total of 15,710 unbalanced panel datapoints from 2,256 listed companies. The ESG data were collected using the Huazheng ESG rating system sourced from the Wind Information Financial Terminal Database. All other financial data were obtained from the China Stock Market and Accounting Research (CSMAR) database and National Bureau of Statistics. We used Excel and Stata15 for data processing and model estimation.

As a representative accounting-based performance measure, return on assets (ROA) reflects resource allocation effciency more accurately than other accounting information (Zabri et al., 2016). Therefore, consistent with Kim and Lee (Kim and Lee, 2020), we selected ROA as the dependent variable. The mutually influential relationship between ESG and financial performance has been widely debated; therefore we analyzed financial data for t, t+1, and t+2 years to investigate this lagging effect.

To measure ESG performance, we adopted the ESG rating system developed by Huazheng, consistent with Xie and Lu, (2022), which provides quarterly ESG ratings categorized into nine grades, As follows from high to low: AAA, AA, A, BBB, BB, B, CCC, CC, and C. We assigned ESG grades ranging from 1-9 based on these ratings; for example, ESG = 1 when the ESG rating is C, ESG = 2 when the rating is CC, ESG = 3 when the rating is CCC, and ESG = 4 when the rating is B. Higher scores represent higher ESG performance, whereas lower scores represent lower ESG performance. We used annual average ESG scores as a measure of a firm’s ESG performance. In an additional analysis, we selected the Wind ESG_1 rating as an alternative explanatory variable to ensure the robustness of our findings.

Listed companies’ annual reports provide their annual summary review and future outlook; therefore, text analysis and word frequency statistics of these reports are meaningful and feasible measures of corporate digital transformation. Thus, referring to Wu et al. (2021), we used text analysis and word frequency statistics to measure corporate digital transformation, utilizing Python to deeply mine the “digitalization” content in listed companies; annual reports and construct a digital list including five dimensions: including “AI technology,” “Big Data technology,” “cloud computing technology,” “blockchain technology,” and “digital technology application.” Then, based on the digital list, we used the “jieba” word segmentation tool in Python for text analysis and word frequency statistics. Finally, we logarithmically measured each company’s degree of digital transformation.

To control for other factors that could affect the empirical findings, we selected eight indicators identified from previous research as control variables: firm size (size), debt level (debt), operating leverage (lev), firm age (age), cash holding level (cash), equity restriction ratio (balance), executive compensation (wage), and regional development level (GDP). In addition, we included year and industry-fixed effects in the model. Table 1 presents definitions and descriptions of these variables.

TABLE 1. Description of variables.

To examine the effects of ESG levels on firms’ financial performance, Eq. 1 is established to test H1:

where ROA is the financial performance of the dependent variable, ESG is the company’s ESG performance of the independent variable, and Controls represents each control variable.

To test the moderating effect of ESG on financial performance, Eqs 2, 3 are established based on Eq. 1:

In these equations, DTB represents the digital transformation of the moderating variable. Eq. 2 focuses on checking whether digital transformation has an impact on ESG performance, and Eq. 3 analyzes whether digital transformation plays a moderating role.

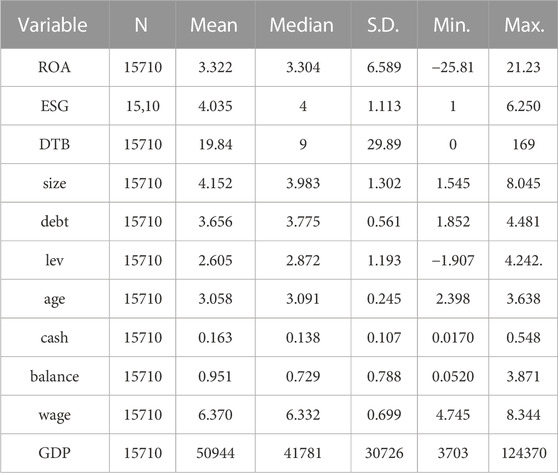

Table 2 displays descriptive statistics for the variables of interest, including ESG, financial performance (measured by ROA), and digital transformation. The mean ROA is 3.322, with a standard deviation of 6.589 and a range from −25.81 to 21.23, demonstrating significant variability across companies. The mean and median of ESG are 4.035 and 4, respectively, with a minimum value of 1 and a maximum of 6.250, signifying wide variation in ESG performance across listed companies. Digital transformation ranges from 0 to 169, indicating that some companies have not yet implemented the process. We assessed the variance inflation factor to check for multicollinearity and found an average of 1.12 (ranging from 1.01 to 1.14), which suggests that multicollinearity is unlikely to significantly impact our results.

TABLE 2. Description statistics.

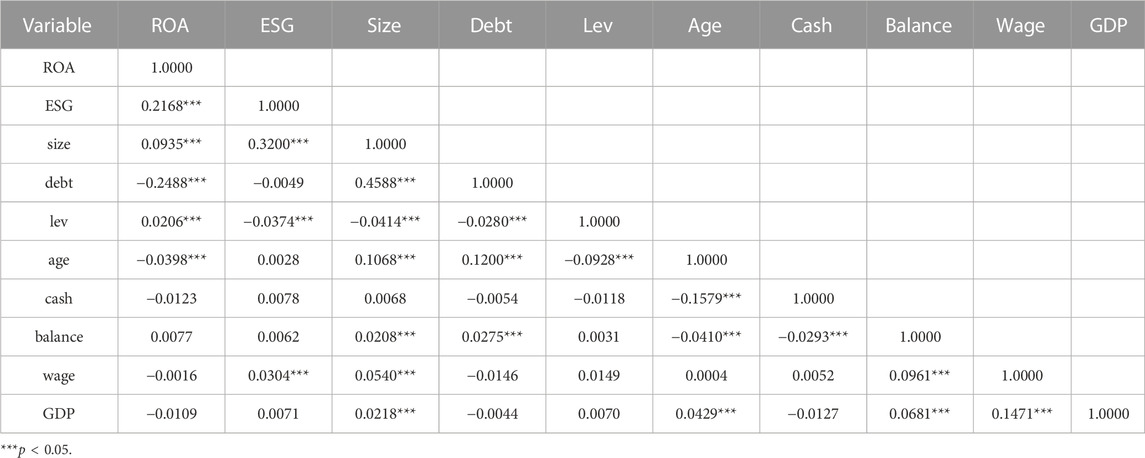

Table 3 presents the results of the correlation analysis of all variables in this study. The correlation coefficients are below 0.6 for all variables, indicating distinct differentiation among them (Zheng et al., 2022). Notably, a significantly positive correlation coefficient is observed between the dependent variable ROA and independent variable ESG (β = 0.2168, p < 0.01), suggesting a positive association between ESG performance and corporate financial performance.

TABLE 3. Correlation matrix.

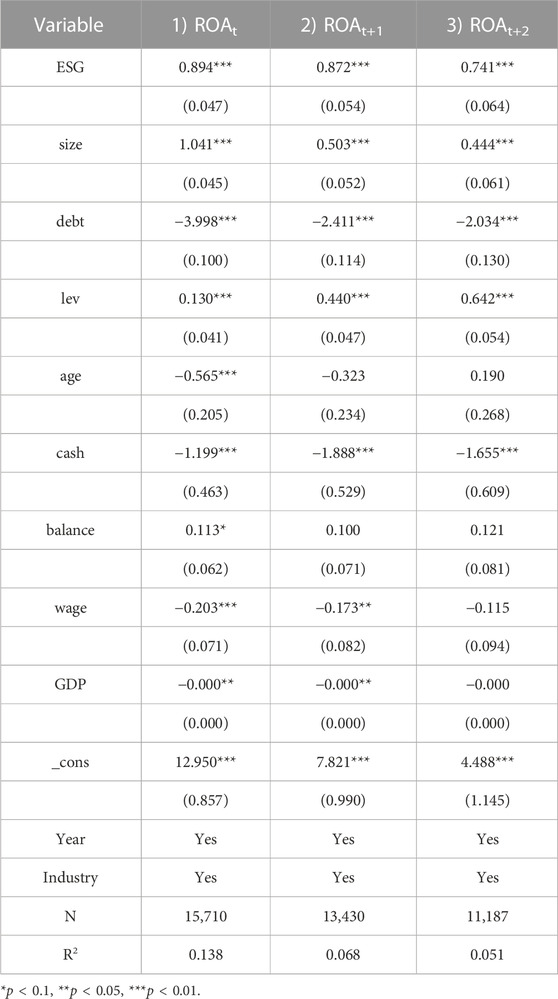

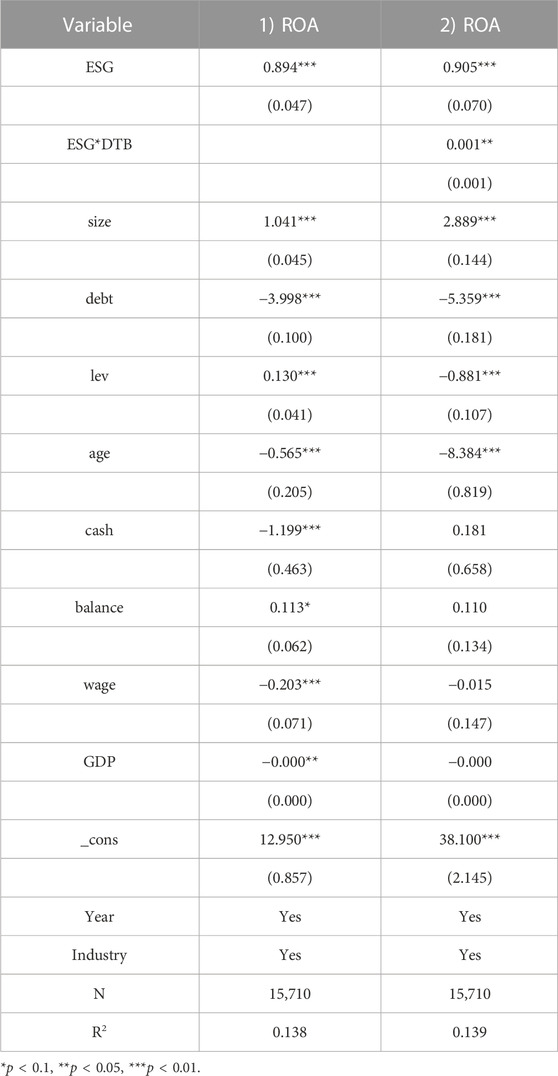

Table 4 displays the regression results for all study variables. H1 posits that an increase in ESG performance leads to improved corporate financial performance. The results support this hypothesis, in that ESG performance has a significant and positive effect on ROA (α = 0.894, p < 0.01), indicating that high ESG performance leads to better financial performance. To ensure the credibility of our study, we tested the robustness of our findings by implementing lags of one and two periods for our explained variable (ROA) in Model (1). The results show that the positive regression coefficients of ESG performance remain significant even with the lag treatment. This indicates that ESG performance has a consistent positive effect on financial improvement. Furthermore, by applying the lag method, we investigated the relationship between the two, which helps account for potential endogeneity issues. This approach indicates that our findings are unlikely to be significantly affected by endogeneity.

TABLE 4. Regression results for the impact of ESG on financial performance.

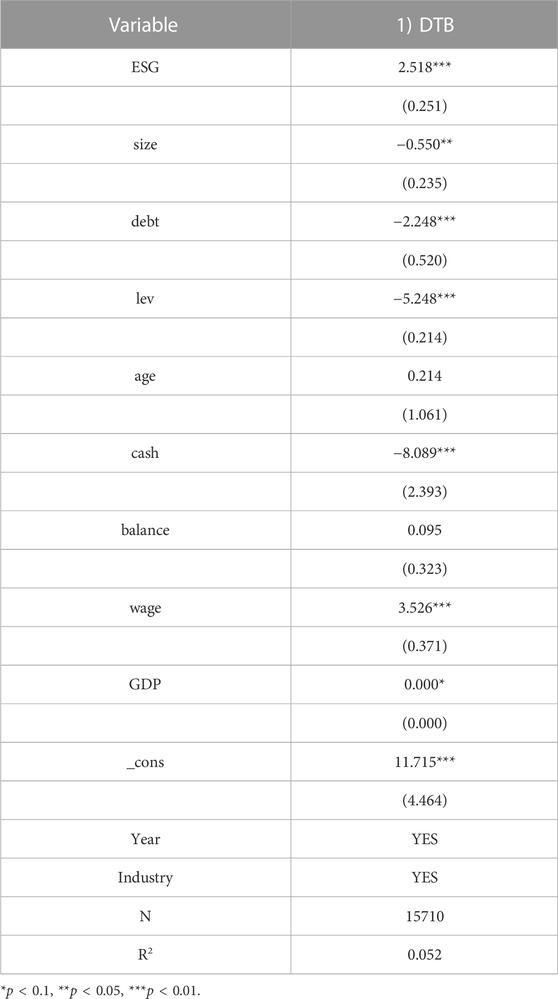

Table 5 reports the regression results of the impact of digital transformation on ESG performance as captured by Eq. 2. The coefficient of ESG is positive and significant at the 1% level (β = 2.518, p < 0.01), supporting H2. This indicates that digital transformation significantly enhances corporate ESG performance. Furthermore, the regression analysis for control variables also aligns with our expectations. Size, debt, level, cash, wage, and GDP all show a strong correlation with digital transformation.

TABLE 5. Regression results for the impact of digital transformation on ESG.

Table 6 presents the results of the test of the moderating effect of digital transformation (DTB) on the relationship between ESG and financial performance. The coefficient of ESG*DTB is the focus of this study. The regression results in column (2) show that the coefficient of the interaction term (ESG*DTB) is significantly positive (β = 0.001, p < 0.05), suggesting that digital transformation has a significant positive moderating effect between ESG and financial performance, supporting H3.

TABLE 6. Moderating effect.

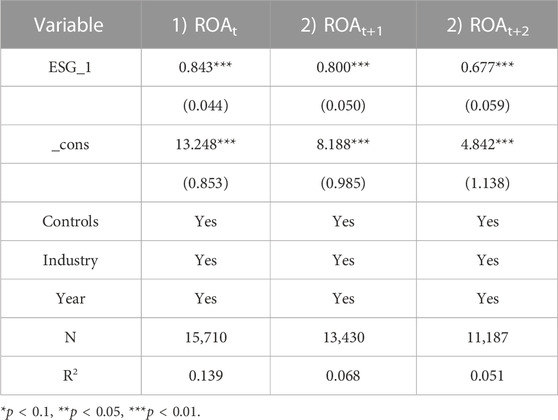

To further validate the reliability of the research results and examine the stability of the model, we conducted a robustness check by replacing Huazheng’s ESG ratings with ESG_1 scores from Wind (MSCI). Wind’s ESG_1 scores are widely used in investment portfolios and decisions. The score ranges from 0 to 10, indicating a company’s ESG performance, with 10 indicating the highest ESG performance and 0 indicating the lowest. The rating criteria include risk management, anti-corruption measures, labor standards, and community relations. Table 7 shows the regression results of ESG_1 on financial performance, including the current period and one and two lagging periods. As the table shows, the estimated coefficient of ESG_1 is 0.843, which is significant at the 1% level. When ROA lags by one or two periods, the estimation coefficient of ESG_1 remains significant at the 1% level (β1 = 0.800,p < 0.01; β2 = 0.677, p < 0.01). This is consistent with the main regression results; thus, the results are robust.

TABLE 7. Replacement of independent variable.

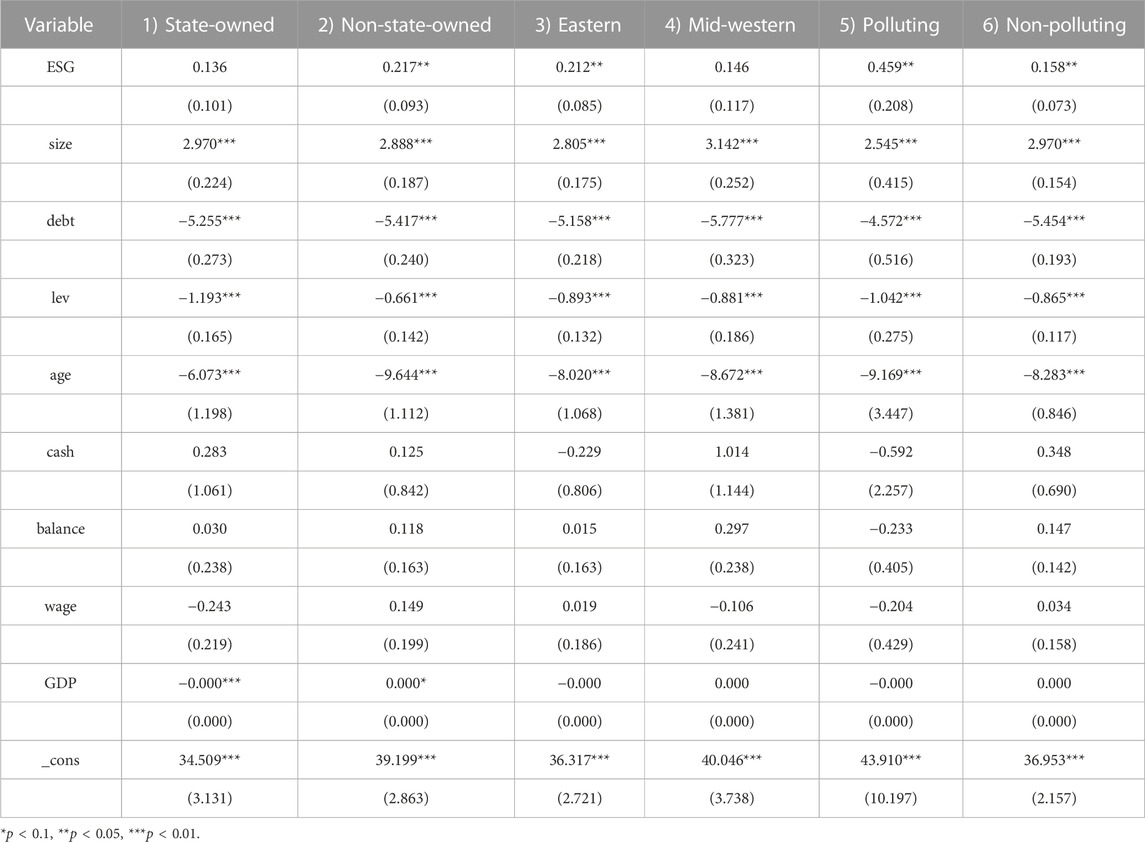

A company’s property rights directly affects its business decisions and risk controls. Different property rights may lead to significant differences in the degree of emphasis on and management of ESG, which in turn affect financial performance. Additionally, given China’s vast territory, there are significant variations in policy environments and sociocultural backgrounds across regions, affecting companies’ ESG investment and management practices. Furthermore, environmental pollution has become a global concern and grouping companies based on pollution levels can help explore the impact of environmental protection on ESG. Therefore, we conducted group testing on the samples according to property rights, regions, and whether they cause environmental pollution.

Company ownership is a significant factor affecting ESG performance, resource allocation, and decision-making (Singh and Chen, 2018). Companies with different property rights experience different effects on fulfilling their social responsibilities. Therefore, we divided the sample into state-owned and non-state-owned companies, to examine how different types of companies’ ESG performance affects their financial performance. As shown in columns (1) and (2) of Table 8, the ESG coefficient of state-owned companies is not significant, whereas that of non-state-owned companies is 0.217 and significant at the 5% level. Since state-owned companies are often subject to government administrative intervention and bear multiple responsibilities, such as economic development and employment, they often have a good reputation in terms of social image (Li and Li, 2022). However, the multiple responsibilities of state-owned companies make their operations and decision-making process relatively complex. Simultaneously, the policy environment and market competition often make it difficult for state-owned companies to compare themselves with non-state-owned companies in terms of profits and performance (Li and Xia, 2018). Therefore, good ESG performance hardly brings more economic benefits to state-owned companies. In contrast, non-state-owned companies have traditionally been more profit-oriented and often regard social responsibility and environmental protection as secondary factors. However, this situation is changing, and an increasing number of non-state-owned companies are beginning to pay attention to ESG performance, making it easier for them to enhance their corporate reputation, attract outstanding talent, and achieve better performance.

TABLE 8. Regression results in different groups.

China has regional disparities in economic development levels and institutional environments. The eastern region boasts higher economic development levels, a better institutional environment, and stricter government regulations, leading eastern enterprises to place greater emphasis on ESG performance to reduce supervision and public pressures (Cong et al., 2023). Moreover, the region’s economic prosperity, coupled with government access to abundant financial resources, allows for policy support such as funding and tax breaks for socially responsible companies, further incentivizing companies to improve their ESG performance. However, in the midwestern regions, the government attaches much more importance to economic benefits than to ESG. The lack of financial resources also increases the cost to enterprises for improving ESG performance, resulting in a low level of enterprise ESG investment (Yan et al., 2023). Therefore, we divided the full sample into two sub-samples according to regions, including the eastern and midwestern regions. Beijing, Hebei, Liaoning, Tianjin, Shandong, Shanghai, Jiangsu, Zhejiang, Fujian, Guangdong, and Hainan are located in the eastern region, whereas the remaining areas are considered to be in the midwestern region. As shown in columns (3) and (4) of Table 8, the regression coefficient of companies in midwestern region is not significant, whereas that in the eastern region is significant at the 5% level.

According to Hamori et al. (2022), environmental governance is the most important ESG component. Protecting the environment is not only a moral responsibility but also plays a crucial role in the long-term sustainable development of corporations and maintaining a stable socio-economic environment. Corporations in different industries have different attitudes toward environmental governance. Considering the differences within industries, we categorized corporations into two types based on the relevant regulations of the environmental information disclosure guidance for listed companies. We defined enterprises engaged in power generation, steel, cement, electrolytic aluminum, coal, metallurgy, chemical engineering, petrochemicals, building materials, paper-making, brewing, pharmaceuticals, fermentation, textiles, tanning, and mining as polluting enterprises, whereas the remainder are non-polluting enterprises. Columns (5) and (6) of Table 8 show that the regression coefficients of polluting and non-polluting enterprises are 0.459 and 0.158, respectively, and both are significant at the 5% level. This implies that the relationship between ESG and financial performance is stronger for polluting enterprises than for non-polluting enterprises. As polluting enterprises face greater public pressure in terms of their production and operations, they must demonstrate superior ESG performance to cope with external criticism, which brings more opportunities and challenges to their operations (Yu and Xiao 2022). Furthermore, in the context of increasingly stringent environmental requirements, polluting enterprises must take more environmental measures to avoid possible fines, making them more focused on ESG performance. In contrast, the industry characteristics and business models of non-polluting companies are less related to environmental issues; therefore, the improvement of their ESG has a relatively small promoting effect on their financial performance. Meanwhile, with the support of the “greenwashing strategy,” non-polluting companies may only need to conduct superficial green marketing without taking action, which may weaken this promoting effect.

The COVID-19 pandemic has caused significant disruptions to the global economy and accelerated the digitalization trend, resulting in risks and challenges for many businesses. Consequently, ESG considerations have become critical factors in enterprises’ long-term development.

Our study generated several interesting findings. The results shown in Tables 3, 4 indicate that a company’s ESG performance can act as a catalyst to improve its overall performance, thereby supporting H1. One noteworthy finding was the positive impact of ESG on corporate performance, which extended from the current year to the second and third years and demonstrated a lasting effect. For example, companies that integrate ESG principles into their strategies tend to attract a wider range of investors who prioritize sustainability and social responsibility. This can lead to increased capital flow and enhanced financial performance. Furthermore, ESG practices can help companies manage more effectively and efficiently environmental and social risks, potentially mitigating legal, regulatory, and reputational costs that could adversely impact financial performance. ESG practices can also contribute to better cost management, employee retention, and innovation, leading to more sustainable long-term growth prospects. These results are consistent with those of previous studies. Chang and Lee (2022) found that performance will improve when organizations increase their investment in sustainable development. Using data on Bangladesh’s manufacturing industry, Zhou et al. (2023) found that companies with better ESG performance tend to have more sustainable and innovative performance. However, most enterprises face difficulties in implementing ESG. For example, to report on ESG issues, companies may need to collect and analyze vast amounts of data. This can be time consuming and expensive, especially for companies that lack the necessary resources or expertise.

We further identified a positive relationship between ESG and digital transformation (H2), which is in line with the findings of prior studies by Zhong et al. (2023) and others. As Table 6 shows, digital transformation moderates the relationship between ESG and financial performance (H3). Zhong noted out that digitalization by enterprises creates value beyond economic impact, also encompassing social and environmental benefits. Lu et al. (2022) concluded that ESG disclosure is crucial for companies’ decision-making. Digital financial inclusion also plays a crucial role in motivating companies to disclose their ESG performance. Belousova et al. (2022) found that minimizing the negative environmental impact of digital business services companies can deliver greater positive value to client performance. Unfortunately, however, the impact of ESG factors on financial performance may vary depending on sector, market, and institutional constrains.

Thus, the samples were divided into different groups. As shown in Table 8, the positive effect of the ESG level on financial performance varies by company ownership type, region, and degree of pollution. These findings imply that non-state-owned companies may have greater incentives to improve their ESG practices and transparency because of heightened competition and scrutiny from investors and stakeholders. Compared with those in the midwestern region, companies in the eastern region may be more committed to ESG practices to meet global standards and stakeholder expectations given the presence of large international corporations and industry leaders in the region. Finally, companies with high pollution levels face greater scrutiny and public pressure to enhance their ESG practices due to the negative impact of their operations on the environment and society. These results could help companies and the government formulate more effective ESG strategies to improve finance performance, and provide investors and stakeholders with a better understanding of the potential benefits of investing in companies with strong ESG practices.

ESG is a critical factor in sustainable corporate development and is an important indicator of corporate social responsibility. We utilized unbalanced panel data of 2256 Chinese-listed companies from 2015 to 2021 to analyze the effects of ESG on corporate financial performance. Specifically, our findings demonstrate that the level of ESG performance, as tested by Huazheng, positively influences corporate performance. Moreover, our research found that digital transformation can regulate and moderate the relationship between ESG and financial performance to ensure sustainable growth for companies. Deeper research showed that the positive impact of ESG varies depending on ownership type, region, and degree of pollution.

Our study makes theoretical contributions by extending the existing literature on the relationship between ESG and financial performance, with China as the research object. China, the largest developing country, has gradually included finance and ESG in its national policies and issued a series of policies and standards. Therefore, this study has a guiding significance for ESG development and research in developing countries. For example, although sustainable development is a broad focus in Vietnam (Luu, 2019), most Vietnamese companies are still profit-oriented and lack regulatory and technical support for ESG practices and performance. The Indonesian government encourages companies to focus on ESG issues (Huang et al., 2022); however, the country lacks supervision and implementation norms, resulting in significant gaps in its ESG practices. Although the Pakistani government has formulated ESG strategies and policies, the country’s long-term economic development and investment have tended to focus on traditional industries (Shahzad et al., 2020); therefore, ESG is relatively underdevelopment in Pakistan. Furthermore, this study explored the relationship between ESG and financial performance and fills gaps in the literature by using digital transformation as a moderating variable for the first time, given the leapfrog improvement in productivity promoted by digital technology.

This study has several practical implications for firms and government. First, to promote sustainable economic development, regulatory authorities should strengthen the guidance and supervision of ESG practices and information disclosure. Our study shows that ESG implementation can improve corporate performance. Therefore, enterprises should actively participate in ESG practices. Second, the application of digital technology has brought significant changes to industrial development. Companies should use digitalization as a tool to address the risks and challenges of the information age. Digital transformation can not only improve enterprises’ resource utilization efficiency but also reduce their environmental and social impact, thereby enhancing their ability for sustainable development.

Our study has some limitations that require future research. First, our research did not focus on specific industries, although various industries are affected by distinct factors, such as policy environments, market sizes, and user behaviors. Therefore, we will focus on specific industries for an in-depth analysis, such as exploring the concrete mechanisms of the impact of ESG practices on financial performance in the energy industry. Second, considering difficulties in data collection, we only focused on listed companies that have disclosed ESG information. Non-listed and small and medium-sized enterprises play a significant role in Chinese economic development, serving as major sources of employment and providing consumers with valuable and innovative goods and services. Future studies should consider small and medium-sized enterprises and explore which of the three components of ESG has the greatest impact on their financial performance.

The raw data supporting the conclusion of this article will be made available by the authors, without undue reservation.

TF: Data curation, Formal Analysis, Investigation, Methodology, Project administration, Resources, Software, Visualization, Writing–original draft. JL: Conceptualization, Funding acquisition, Supervision, Writing–review and editing.

This work was supported by CITIC Reform and Development Research Foundation (H21319), the General Projects of Science and Technology Plan of Beijing Municipal Commission of Education (KM202110016006), and Beijing Advanced Innovation Center for Future Urban Design, Beijing University of Civil Engineering and Architecture (UDC2019021424).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Abdi, Y., Li, X., and Càmara-Turull, X. (2022). Exploring the impact of sustainability (ESG) disclosure on firm value and financial performance (FP) in airline industry: The moderating role of size and age. Environ. Dev. Sustain. 24 (4), 5052–5079. doi:10.1007/s10668-021-01649-w

Belousova, V., Bondarenko, O., Chichkanov, N., Lebedev, D., and Miles, I. (2022). Coping with greenhouse gas emissions: Insights from digital business services. Energies 15 (8), 2745. doi:10.3390/en15082745

Bhandari, K. R., Ranta, M., and Salo, J. (2022). The resource-based view, stakeholder capitalism, ESG, and sustainable competitive advantage: The firm’s embeddedness into ecology, society, and governance. Bus. Strategy Environ. 31 (4), 1525–1537. doi:10.1002/bse.2967

Carnini, P. S., Ciaburri, M., Magnanelli, B. S., and Nasta, L. (2022). Does ESG disclosure influence firm performance? Sustainability 14 (13), 7595. doi:10.3390/su14137595

Chang, Y. J., and Lee, B. H. (2022). The impact of ESG activities on firm value: Multi-level analysis of industrial characteristics. Sustainability 14 (21), 14444. doi:10.3390/su142114444

Chen, G., Han, J., and Yuan, H. (2022). Urban digital economy development, enterprise innovation, and ESG performance in China. Front. Environ. Sci. 10, 955055. doi:10.3389/fenvs.2022.955055

Cong, Y., Zhu, C., Hou, Y., Tian, S., and Cai, X. (2023). Does ESG investment reduce carbon emissions in China? Front. Environ. Sci. 10, 977049. doi:10.3389/fenvs.2022.977049

Cui, J., Jo, H., and Na, H. (2018). Does corporate social responsibility affect information asymmetry? J. Bus. Ethics. 148 (3), 549–572. doi:10.1007/s10551-015-3003-8

ElMassah, S., and Mohieldin, M. (2020). Digital transformation and localizing the sustainable development goals (SDGs). Ecol. Econ. 169, 106490. doi:10.1016/j.ecolecon.2019.106490

Fatemi, A., Fooladi, I., and Tehranian, H. (2015). Valuation effects of corporate social responsibility. J. Bank. Financ. 59, 182–192. doi:10.1016/j.jbankfin.2015.04.028

Finger, M., and Rosenboim, M. (2022). Going ESG: The economic value of adopting an ESG policy. Sustainability 14 (21), 13917. doi:10.3390/su142113917

Friede, G., Busch, T., and Bassen, A. (2015). ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J. Sustain. Finance Invest 5 (4), 210–233. doi:10.1080/20430795.2015.1118917

Friedman, (2007). The social responsibility of business is to increase its profits. Corp. Ethics Corp. Gov., 173–178. doi:10.1007/978-3-540-70818-6_14

Gao, Y., and Han, K. S. (2020). Managerial overconfidence, CSR and firm value. Asia Pac. J. Acc. Econ. 29, 1600–1618. doi:10.1080/16081625.2020.1830558

Garcia, A. S., and Orsato, R. J. (2020). Testing the institutional difference hypothesis: A study about environmental, social, governance, and financial performance. Bus. Strateg. Environ. 29 (8), 3261–3272. doi:10.1002/bse.2570

Godfrey, P. C. (2005). The relationship between corporate philanthropy and shareholder wealth: A risk management perspective. Acad. Manage. Rev. 30 (4), 777–798. doi:10.5465/amr.2005.18378878

Gouvea, R., Li, S., and Montoya, M. (2022). Does transitioning to a digital economy imply lower levels of corruption? Thunderbird Int. Bus. Rev. 64 (3), 221–233. doi:10.1002/tie.22265

Hamori, S., - Yue, X. G., Yang, L., and Crabbe, M. J. (2022). Editorial: ESG investment and its societal impacts. Front. Environ. Sci. 10, 1088821. doi:10.3389/fenvs.2022.1088821

Hoepner, A. G., Majoch, A. A., and Zhou, X. Y. (2021). Does an asset owner’s institutional setting influence its decision to sign the principles for responsible investment? J. Bus. Ethics. 168 (2), 389–414. doi:10.1007/s10551-019-04191-y

Huang, P. T. B., Yang, C. C., Inderawati, M. M. W., and Sukwadi, R. (2022). Using modified delphi study to develop instrument for ESG implementation: A case study at an Indonesian higher education institution. Sustainability 14 (19), 12623. doi:10.3390/su141912623

Ionascu, I., Ionascu, M., Nechita, E., Săcărin, M., and Minu, M. (2022). Digital transformation, financial performance and sustainability: Evidence for European union listed companies. Amfiteatru Econ. 24 (59), 94–109. doi:10.24818/EA/2022/59/94

Jeffrey, S., Rosenberg, S., and McCabe, B. (2019). Corporate social responsibility behaviors and corporate reputation. Soc. Responsib. J. 15 (3), 395–408. doi:10.1108/SRJ-11-2017-0255

Kim, B., and Lee, S. (2020). The impact of material and immaterial sustainability on firm performance: The moderating role of franchising strategy. Tour. Manage 77, 103999. doi:10.1016/j.tourman.2019.103999

Krüger, F. (2015). Corporate storytelling: Theorie und empirie narrativer public relations in der unternehmenskommunikation. Berlin, Germany: Springer-Verlag, 107.

Lev, B., Petrovits, C., and Radhakrishnan, S. (2010). Is doing good good for you? How corporate charitable contributions enhance revenue growth. Strategy Manag. J. 31 (2), 182–200. doi:10.1002/smj.810

Li, A., and Xia, X. (2018). Are controlling shareholders influencing the relationship between CSR and earnings quality? Evidence from Chinese listed companies. Emerg. Mark. Financ. Tr. 54 (5), 1047–1062. doi:10.1080/1540496X.2018.1434070

Li, J., and Li, S. (2022). Environmental protection tax, corporate ESG performance, and green technological innovation. Front. Environ. Sci. 10, 982132. doi:10.3389/fenvs.2022.982132

Lian, Y., Li, Y., and Cao, H. (2023). How does corporate ESG performance affect sustainable development: A green innovation perspective. Front. Environ. Sci. 11, 430. doi:10.3389/fenvs.2023.1170582

Lu, Y., Wang, L., and Zhang, Y. (2022). Does digital financial inclusion matter for firms’ ESG disclosure? Evidence from China. Front. Environ. Sci. 10, 1029975. doi:10.3389/fenvs.2022.1029975

Luo, X. R., Wang, D., and Zhang, J. (2017). Whose call to answer: Institutional complexity and firms’ CSR reporting. Acad. Manage. J. 60 (1), 321–344. doi:10.5465/amj.2014.0847

Luu, T. T. (2019). CSR and customer value co-creation behavior: The moderation mechanisms of servant leadership and relationship marketing orientation. J. Bus. Ethics. 155, 379–398. doi:10.1007/s10551-017-3493-7

Lv, P., and Xiong, H. (2022). Can FinTech improve corporate investment efficiency? Evidence from China. Res. Int. Bus. Finance. 60, 101571. doi:10.1016/j.ribaf.2021.101571

Minutolo, M. C., Kristjanpoller, W. D., and Stakeley, J. (2019). Exploring environmental, social, and governance disclosure effects on the S&P 500 financial performance. Bus. Strategy Environ. 28 (6), 1083–1095. doi:10.1002/bse.2303

Nambisan, S., Wright, M., and Feldman, M. (2019). The digital transformation of innovation and entrepreneurship: Progress, challenges and key themes. Res. Policy. 48 (8), 103773. doi:10.1016/j.respol.2019.03.018

Papagiannidis, S., Harris, J., and Morton, D. (2020). WHO led the digital transformation of your company? A reflection of it related challenges during the pandemic. Int. J. Inf. Manage. 55, 102166. doi:10.1016/j.ijinfomgt.2020.102166

Paradis, G., and Schiehll, E. (2021). ESG outcasts: Study of the ESG performance of sin stocks. Sustainability 13 (17), 9556. doi:10.3390/su13179556

Sedunov, J. (2017). Does bank technology affect small business lending decisions? J. Financ. Res. 40 (1), 5–32. doi:10.1111/jfir.12116

Shahzad, M., Qu, Y., Javed, S. A., Zafar, A. U., and Rehman, S. U. (2020). Relation of environment sustainability to csr and green innovation: A case of Pakistani manufacturing industry. J. Clean. Prod. 253, 119938. doi:10.1016/j.jclepro.2019.119938

Shimizu, K. (2020). Digital transformation of work and ESG: Perspectives on monopoly and fair trade. Risk Gov. Control Financial Mark. Institutions 10 (3), 75–82. doi:10.22495/rgcv10i3p6

Singh, j. n., and Chen, G. C. (2018). State-owned enterprises and the political economy of state-state relations in the developing world. Third World Q. 39 (6), 1077–1097. doi:10.1080/01436597.2017.1333888

Tarmuji, I., Maelah, R., and Tarmuji, N. H. (2016). The impact of environmental, social and governance practices (ESG) on economic performance: Evidence from ESG score. Int. J. Financ. Econ. 7 (3), 67–74. doi:10.18178/ijtef.2016.7.3.501

Teplova, T., Sokolova, T., Gubareva, M., and Sukhikh, V. (2022). The multifaceted sustainable development and export intensity of emerging market firms under financial constraints: The role of ESG and innovative activity. Complexity 2022, 1–20. doi:10.1155/2022/3295364

Wang, L., Fan, X., Zhuang, H., Liu, A., Wu, Z., Wang, Q., et al. (2023). ESG disclosure facilitator: How do the multiple large shareholders affect firms’ ESG disclosure? Evidence from China. Front. Environ. Sci. 11, 83–100. doi:10.1089/3dp.2021.0055

Wang, Y., Wang, H. Y., Xue, S., Li, F., and He, Y. (2022). Greening of tax system and corporate ESG performance: A quasi-natural experiment based on the environmental protection tax law. J. Financ. Econ. 48 (09), 47–62. doi:10.3390/mi14010047

Wang, Z., and Sarkis, J. (2017). Corporate social responsibility governance, outcomes, and financial performance. J. Clean. Prod. 162, 1607–1616. doi:10.1016/j.jclepro.2017.06.142

Wong, W. C., Batten, J. A., Ahmad, A. H., Mohamed-Arshad, S. B., Nordin, S., and Adzis, A. A. (2021). Does ESG certification add firm value? Financ. Res. Lett. 39, 101593. doi:10.1016/j.frl.2020.101593

Wu, F., Hu, H. Z., Lin, H. Y., and Ren, X. Y. (2021). Digital transformation of enterprises and capital market performance: Empirical evidence from Stock liquidity. J. Manag. World 37 (07), 130–144+10. doi:10.19744/j.cnki.11-1235/f.2021.0097

Xie, H. J., and Lu, X. (2022). Responsible multinational investment: ESG and Chinese OFDI. Econ. Res. J. 57 (03), 83–99.

Yang, Y., Xu, G., and Li, R. (2023). Official turnover and corporate ESG practices: Evidence from China. Environ. Sci. Pollut. R. 30 (18), 51422–51439. doi:10.1007/s11356-023-25828-6

Yan, Y. Z., Cheng, Q. W., Huang, M. L., Lin, Q. H., and Lin, W. H. (2023). Government environmental regulation and corporate ESG performance: Evidence from natural resource accountability audits in China. Int. J. Env. Pub. He. 20 (1), 447. doi:10.3390/ijerph20010447

Yu, X. L., and Xiao, K. T. (2022). Does ESG performance affect firm value? Evidence from a new ESG-scoring approach for Chinese enterprises. Sustainability 14 (24), 16940. doi:10.3390/su142416940

Zabri, S. M., Ahmad, K., and Wah, K. K. (2016). Corporate governance practices and firm performance: Evidence from top 100 public listed companies in Malaysia. Procedia Econ. Financ. 35, 287–296. doi:10.1016/S2212-5671(16)00036-8

Zhang, D., and Liu, L. (2022). Does ESG performance enhance financial flexibility? Evidence from China. Sustainability 14 (8), 11324. doi:10.3390/su141811324

Zheng, J., Khurram, M. U., and Chen, L. (2022). Can green innovation affect ESG ratings and financial performance? Evidence from Chinese GEM listed companies. Sustainability 14 (14), 8677. doi:10.3390/su14148677

Zhong, Y., Zhao, H., and Yin, T. (2023). Resource bundling: How does enterprise digital transformation affect enterprise ESG development? Sustainability 15 (2), 1319. doi:10.3390/su15021319

Keywords: ESG, firm performance, digital transformation, moderating effect, sustainable development

Citation: Fu T and Li J (2023) An empirical analysis of the impact of ESG on financial performance: the moderating role of digital transformation. Front. Environ. Sci. 11:1256052. doi: 10.3389/fenvs.2023.1256052

Received: 10 July 2023; Accepted: 02 August 2023;

Published: 10 August 2023.

Edited by:

Evgeny Kuzmin, Ural Branch of the Russian Academy of Sciences, RussiaReviewed by:

Maria Urbaniec, Kraków University of Economics, PolandCopyright © 2023 Fu and Li. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Tao Fu, ZnV0YW93c3N5QDE2My5jb20=

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.