Manru Peng1,2

Manru Peng1,2 Shichun Peng

Shichun Peng

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 10 November 2023

Sec. Environmental Economics and Management

Volume 11 - 2023 | https://doi.org/10.3389/fenvs.2023.1204970

Environmental problem is the key to the healthy development of China’s eco-economy, and the environmental responsibility of micro-enterprises under the vision of “Dual Carbon” has attracted more attention. Under the effect of formal environmental regulation, firms will improve their environmental performance by improving technology and resource utilization. As an informal environmental system, can government environmental information disclosure (GEID) guide firms to actively carry out green innovation, ultimately improve the carbon emission problem of firms, have a positive impact on the carbon performance of enterprises, and provide strong support to protect ecological environment? To address this question, this study used the Pollution Information Transparency Index (PITI) to measure GEID, and empirically tested the impact of GEID on corporate carbon performance using a sample of listed companies involved in China’s mining and manufacturing industries from 2013 to 2018. The study found that the higher the degree of GEID, the better was the corporate carbon performance. However, the improved public participation weakened the effect of GEID on corporate carbon performance. GEID reduced the carbon emission intensity of firms and improved their carbon performance via green innovation. Further research indicated that the enhanced GEID in state-owned enterprises significantly improved carbon performance of firms. This study provides empirical evidence for GEID to improve corporate carbon performance, and also proposes a policy strategy for the government to guide firms to undertake green innovation and promote firms to improve efficient carbon use.

Climate change is a serious challenge facing the whole world. All countries have taken positive actions to achieve the temperature control goal in the Paris Agreement. According to the BP World Energy Statistical Yearbook of 2022, China’s total primary energy consumption increased from 16.65 EJ to 157.65 EJ, representing an increase from 6.11% to 26.5% of the world’s total primary energy consumption between 1978 and 2021. Meanwhile, Energy carbon emissions of China increased from 1.419 billion tons to 10.523 billion tons, and the share of global carbon emissions increased from less than one-tenth to nearly one-third. As a major energy consumer and carbon emitter, China has set the goal of achieving the emission peak by 2030 and carbon neutrality by 2060. In order to achieve the dual carbon target, the Chinese State Council issued the Comprehensive Work Plan for Energy Conservation and Emission Reduction for “14th Five Year Plan” in January 2022. The Plan emphasized improvement in policy mechanism for energy conservation and emission reduction, and promotion of green transformation of economic and social development. Further, China clearly formulated and revised the emission standards of air pollutants for key industries.

Over the years, under the economic model of government-led and vigorous development of heavy industry in China, enterprises have achieved rapid development, but at the same time, they have brought serious ecological and environmental problems (Yang et al., 2023). In 1973, China implemented the earliest environmental regulation: the “three simultaneities” system, but practice proved that it lacked sufficient resources to implement effective supervision and severe punishment mechanism (Fang and Guo, 2018). In 1982, China promulgated the Interim Measures for the Collection of Sewage Charges, which made an important contribution to energy conservation and emission reduction. However, due to its lack of compulsion, execution and supervision, there were some problems in its implementation, such as underreporting and incomplete government collection (Maung et al., 2016). The implementation of China’s environmental policies is constrained by “active government, passive firms and inactive public” (Tu and Shen, 2015) due to the high cost and low efficiency of implementation of formal environmental regulations, and the rent-seeking behavior leading to “regulation capturing.” In addition, factors such as the scale economy led to some firms paying pollution taxes or trade permits to pollute rather than change the production patterns of high pollution (Chen and Zhen, 2022).

The government and firms can only attach importance to environmental governance via “bottom-up” informal environmental regulations when the effects of “top-down” formal environmental regulations have no obvious effects. With the enhancement of public awareness to environmental protection, informal environmental regulation with the public as the main body has gradually developed and grow (Liu et al., 2021). Environmental problems are closely related to residents’ daily lives. With the popularization of environmental protection concepts and the wide application of the Internet, increasing micro-subjects join the ranks of ecological protection (Michael et al., 2023). This kind of environmental regulation force with the public as the main body is called informal environmental regulation. Different from government regulation, this kind of public-led, relatively informal regulation often has no policy effect, and its mode of action is more random and flexible (Shen et al., 2023), mainly by guiding public opinion to form a soft constraint on enterprises and guiding enterprises to consciously move towards the road of green environmental protection.

Evidence suggests that informal environmental regulation is conducive to reducing the level of environmental pollution (Li, 2018). However, in academic circles, no consensus has been reached on the impact of informal environmental regulations on corporate carbon emissions (Cole et al., 2005; Kathuria, 2007; Lu, 2021). As one of the informal environmental regulations, government environmental information disclosure (GEID) may play an important role in guiding firms to improve pollution discharge and carbon performance.

In the existing literature, studies investigating the factors affecting carbon emissions mainly focus on the national and provincial levels. At the national level, the influencing factors mainly include the actual urbanization rate, per capita GDP, the proportion of tertiary and secondary industries, fixed asset investment, and the proportion of renewable energy (Shuai et al., 2018; Chen and Zhen, 2022). The influencing factors at the provincial level involve economic activities, energy structure, energy-saving technology and energy-use efficiency (Liu and Xu, 2023). Firms at the micro level, as a major participant in China’s carbon emission reduction, have an important effect on the development of China’s eco-friendly economy.

Hence, this study used the Pollution Information Transparency Index (PITI) to measure GEID, and evaluated the impact of GEID on corporate carbon performance and its mechanism based on a sample of China’s A-share manufacturing and mining listed companies from 2013 to 2018. The results showed that GEID significantly improved corporate carbon performance, and green innovation was the primary mechanism of GEID affecting corporate carbon performance. Further, public participation could substitute GEID, which inhibited the positive impact between GEID and corporate carbon performance. The analysis of heterogeneity revealed that the impact of GEID on corporate carbon performance occurred mainly in state-owned enterprises with a close relationship with the government.

Compared with the existing studies, the marginal contribution of the study is as follows. First, this study enriches the research on factors influencing carbon emission reduction by firms at the micro level from the perspective of informal environmental regulation. Most of the existing studies focus on the impact of formal environmental regulation on environmental performance, and there are few studies on the role of environmental regulation and micro-enterprises. This study focuses on the influence of GEID, an informal environmental regulation, on corporate carbon performance, which supplements the perspective of existing literature.

Second, the research effectively tests the mechanism of GEID promoting corporate carbon performance, and provides a path for the government to guide firms to strengthen green innovation. Based on Porter’s theory, this study demonstrates that GEID drives green innovation by firms, guides firms to improve environmental governance and thus improves corporate carbon performance.

Third, the study effectively reveals the factors influencing corporate carbon performance based on the degree of environmental information disclosure, which provides decision-making basis for the government to improve the “bottom-up” environmental governance system. The higher the level of GEID, the better the carbon performance of firms. However, currently, the Pollution Information Transparency Index (PITI) only measures and scores 120 cities in China. Therefore, it is necessary for the government to improve the degree of environmental information disclosure, increase the number of cities participating in PITI, and improve the degree of public participation in environmental governance.

The second part of this article is a literature review and hypothesis development. The third segment presents the research design. The fourth section provides empirical results. The fifth section discusses analysis of mechanism. The sixth section provides further analysis; The seventh section deals with study conclusion and discussion.

Compared with developed countries and other developing countries, China’s effort on environmental information disclosure is relatively late. The Environmental Protection Law of the People’s Republic of China promulgated in 1989 formally established the environmental information disclosure system, requiring the central and provincial environmental protection departments to regularly issue environmental status bulletins.

For a long time, there has been a heavy ecological cost behind China’s rapid economic growth. Frequent environmental pollution incidents not only damaged people’s health, but also ran counter to the trend of the “double carbon.” In order to promote energy conservation and emission reduction of enterprises, China has successively launched command based and market incentive based environmental regulation policies, but local governments often refuse to disclose environmental information for various reasons, resulting in that whether the environmental regulation system only involving the government and enterprises can promote sustainable economic development is still questionable (Tu and Shen, 2015).

In order to build an environmental governance system with multiple participation of the government, firms and the public, the former National Environmental Protection Administration issued the Environmental Information Disclosure Measures (for Trial Implementation) in 2007, requiring local governments to disclose environmental information such as enterprises with excessive emissions and the objects of pollution charges in a timely manner, opening the first year of environmental information disclosure. After the implementation of the Environmental Information Disclosure Measures (for Trial Implementation), the Institute of Public and Environmental Affairs (IPE) and the Natural Resources Defense Council (NRDC) jointly developed the Pollution Information Transparency Index (PITI), which has been evaluating the GEID of Chinese cities year by year since 2008.

Environmental regulation can be divided into three types: 1) mandated regulation led by government, 2) formal regulation based on market incentives, and 3) informal regulation led by non-governmental organization (Ren et al., 2018). The mandated environmental regulation led by government, under the principle of unified planning, monitoring and supervision, can lead to enhanced cooperation and coordination among regions to effectively ameliorate environmental pollution (Yu and Yin, 2022). However, collaborative governance is a challenge, and there may be rent-seeking or other inefficiencies during the implementation (He and Wang, 2016). Studies show that the effect of compound emission reduction via mandated regulation and market-incentive regulation is often better than that of the single policy. Market-incentive environmental regulations, such as carbon emission trading policy (Dong and Wang, 2021; Tang and Xu, 2023) and ecological transfer payment policy (Pan, 2021), can effectively improve the progress of green technology, reduce carbon dioxide emissions, and better protect the ecological environment. Informal environmental regulation, however, often exerts a binding force on irregular behaviors outside the scope of formal environmental regulation via public criticism, resistance to polluting firms’ products and pressure exerted by media and environmental non-governmental organizations in the face of weak or absent formal environmental regulation (S. Pargal and D. Wheeler, 1996). Informal environmental regulations combined with laws and formal regulations, such as environmental taxes and emission trading permits, can prevent local firms from committing environmental violations (Han et al., 2016) and drive the government and firms to implement eco-friendly decisions to solve environmental challenges (M. Brigglio, 2017).

The academic community has yet to reach an agreement on whether GEID, one of the informal environmental regulations, is effective in improving corporate environmental performance. Many scholars believe that environmental information disclosure can contribute to the routine supervision of the entire society, resulting in environmental supervision with the participation of the government, firms, social organizations and the public (Du, 2022). It can guide strongly polluting firms to improve their environmental performance by increasing R&D investment, green innovation and other activities (Feng and He, 2020; Zhang and Feng, 2020; Wang et al., 2023). Other experts believe that due to the lack of public accountability and the characteristics of long cycle and large demand for funds to improve environmental performance, firms are likely to pursue short-term interests without focusing on environmental issues, suggesting that environmental information disclosure is not effective in improving environmental performance (Tu et al., 2019). The different perspectives of the existing studies question whether the GEID can be an effective tool in promoting environmental governance.

Obviously, the aforementioned research findings provide a solid theoretical basis for this study. However, the existing literature mainly considers environmental information disclosure as a quasi-natural experiment to test the impact of informal environmental regulation. The mechanism of the impact is not clear. It is also not clear whether the impact of PITI on corporate carbon performance is sustainable after 14 years of environmental information disclosure. Therefore, we conducted a supplementary study to analyze the impact mechanism of GEID indicators on corporate carbon performance.

In the context of market-oriented economy, the Chinese government not only intervenes in economic and social activities through laws and taxes, but also regulates corporate environmental behavior via licensing, environmental information disclosure and other channels (Shen and Jin, 2018). No government rules and regulations are available to mitigate the intensity of corporate carbon emissions despite the assessment of regional carbon emissions as one of the indicators of performance evaluation of local officials. Therefore, local governments restrict corporate carbon emissions from the purview of informal environmental regulations.

GEID belongs to the category of informal environmental regulation. It is a specific form of public participation in environmental governance (Zhang et al., 2021) and plays an important role in environmental governance of green development. First, GEID has increased public access to adverse information such as environmental laws and regulations, penalties and environmental litigation and alleviated the asymmetric environmental information between firms and external stakeholders. Second, GEID facilitated public participation in the supervision of corporate environmental issues substantially. Firms focus increasingly on environmental issues based on external pressure. Therefore, GEID can improve the efficiency of environmental supervision of firms.

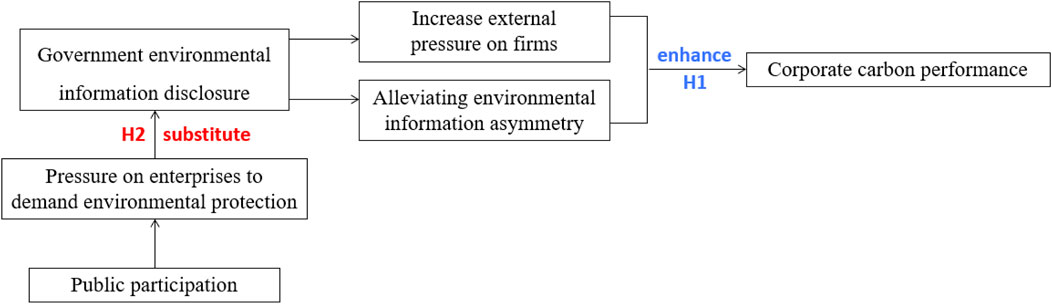

GEID plays an important role in carbon emission reduction of local firms, when carbon emission reduction is supported by the central government. Therefore, as an informal environmental regulation policy, GEID affects the carbon emission performance of firms. This study proposes the following hypothesis:

Hypothesis 1(H1). GEID can reduce the carbon emission intensity of firms and improves their carbon performance.

The public can participate in the supervision system via GEID, thus alleviating the problem of information asymmetry. The disclosure of environmental information has increased the exposure rate of illegal activities by firms. Equipped with information regarding firms’ environmental violations, the public can influence corporate decisions through complaints, protests, and refusal to purchase products or services (Lu, 2021). To prevent loss of reputation, image and other factors, and to avoid the risk of environmental violations disclosure, firms will choose to reduce emissions during the production process (Zhao and Zhang, 2020). Therefore, when the public has access to corporate environmental information, firms will improve environmental performance to address the environmental needs of the public (Yan et al., 2023).

Under a high degree of public participation regionally, the monitoring of environmental information of firms and government not only involves active disclosure of environmental information by the government, but also act under the pressure to address the need for public environmental protection. Firms will improve their carbon performance to meet public needs (Yang et al., 2020). Therefore, public participation may substitute the role of GEID. This study proposes the following hypothesis:

Hypothesis 2(H2). Public participation has a moderating effect on GEID to promote corporate carbon performance.

Figure 1 illustrates the research hypotheses of this study.

FIGURE 1. Research hypothesis.

The carbon performance measured in this study is a manual collection of data from China Energy Statistical Yearbook and China Industrial Economic Statistical Yearbook. This data only contains detailed data of secondary classification of mining and manufacturing firms. In addition, the number of cities measured by the PITI index has increased year by year since its launch, and has stabilized at 120 since 2013. Therefore, considering the accuracy of data processing, this paper selected the listing of China’s A-share mining and manufacturing industries from 2013 to 2018 as samples, and processed the data as follows: 1) exclusion of samples with abnormal trading status (ST, * ST) during the observation period; 2) elimination of samples with missing financial data; 3) removal of the samples not belonging to cities with open environmental information; 4) shrinking the main continuous variables by 1% in order to avoid the impact of extreme values. Finally, 7,705 observations of 1,576 listed companies were obtained. The financial data of this study were derived from the China Stock Market and Accounting Research Database (CSMAR), and the carbon emission intensity data were obtained from the China Energy Statistical Yearbook and the China Industrial Economic Statistical Yearbook.

Corporate carbon performance (CEPI) was used as the dependent variable in this study. Considering the availability of micro-level data, this study selected enterprise carbon emission intensity (CEP) to measure carbon performance, that is, carbon emissions per unit income (Clarkson et al., 2011). The greater the CEP, the lower the CEPI. According to (Yan et al., 2019), the carbon emissions of firms were estimated based on industrial carbon emissions, which were calculated by referring to the industrial energy consumption published in the China Energy Statistical Yearbook and the reference coefficient of energy carbon emissions listed in the carbon emissions trading network (Table 1); Industry operating costs are collected from China Industrial Economic Statistical Yearbook. According to the industry operating cost indicators in the statistics of main economic indicators of industrial enterprises above designated size, the legal entities above designated size with annual main business income of 20 million yuan or more are included in the industry. The CEP of firms and industry carbon emissions were calculated using the following formula:

TABLE 1. Energy standard coal conversion coefficient and carbon emission coefficient.

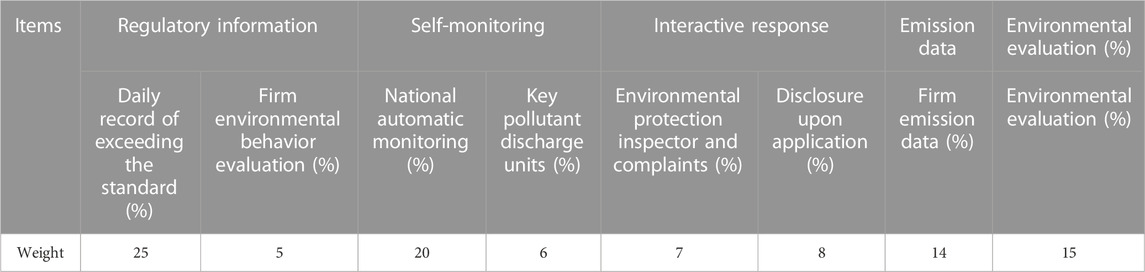

The core explanatory variable in this study was GEID. The Measures for the Disclosure of Environmental Information (for Trial Implementation) came into effect in 2008, and the Institute of Public and Environmental Affairs (IPE) and the Natural Resources Defense Council (NRDC) jointly released the pollution source regulatory information disclosure index (PITI). The PITI index scores the open index of government environmental pollution supervision in 113 cities in China, and the number of evaluated cities has increased to 120 by 2013. The index includes eight secondary evaluation items, and the weight of each item is shown in Table 2.

TABLE 2. Evaluation index of PITI.

PITI index is a systematic evaluation of local government’s environmental information disclosure level by third-party non-government organizations, which can objectively and fairly reflect the implementation of relevant laws and regulations on environmental information disclosure by local government departments (Guo et al., 2014). Therefore, this study measures GEID with PITI index. The higher the PITI score, the higher the degree of GEID of the local government (Feng et al., 2021).

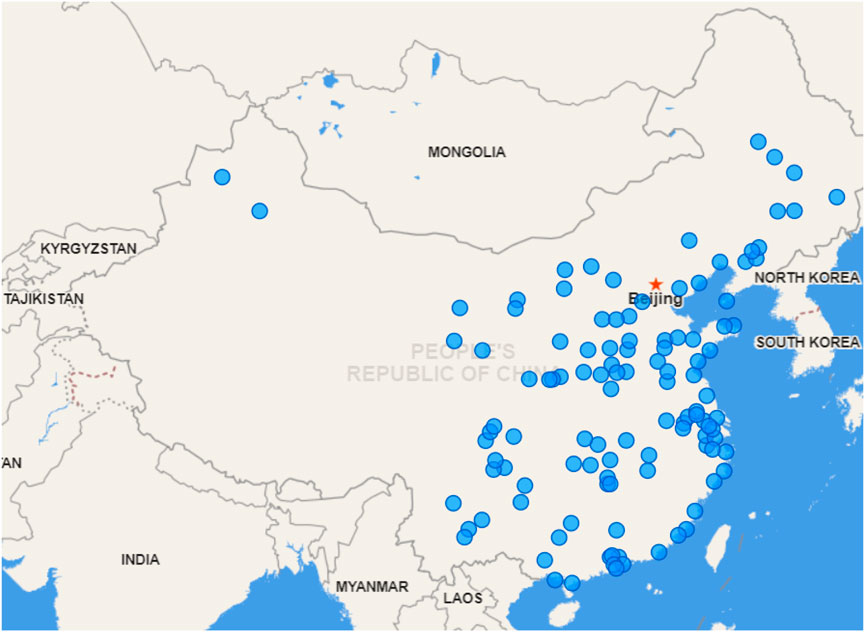

The geographical distribution of 120 cities scored by PITI of China is mainly concentrated in the eastern coastal areas and around the capital Beijing as shown in Figure 2.

FIGURE 2. Geographical distribution of PITI cities of China.

The moderating variable in this study was the degree of public participation (PUB). Based on the practice of Yan et al. (2022), and according to the Statistical Yearbook of Chinese Cities, the public participation in the city is measured as 100 times the ratio of the number of Internet connections in the city to the permanent population of the city (i.e., the number of Internet connections per 100 people). Generally speaking, the higher the proportion of urban residents accessing the Internet, the higher the Internet penetration rate. Government information is mainly spread through the Internet medium. This study selected the Internet penetration rate to measure the degree of public participation in the city.

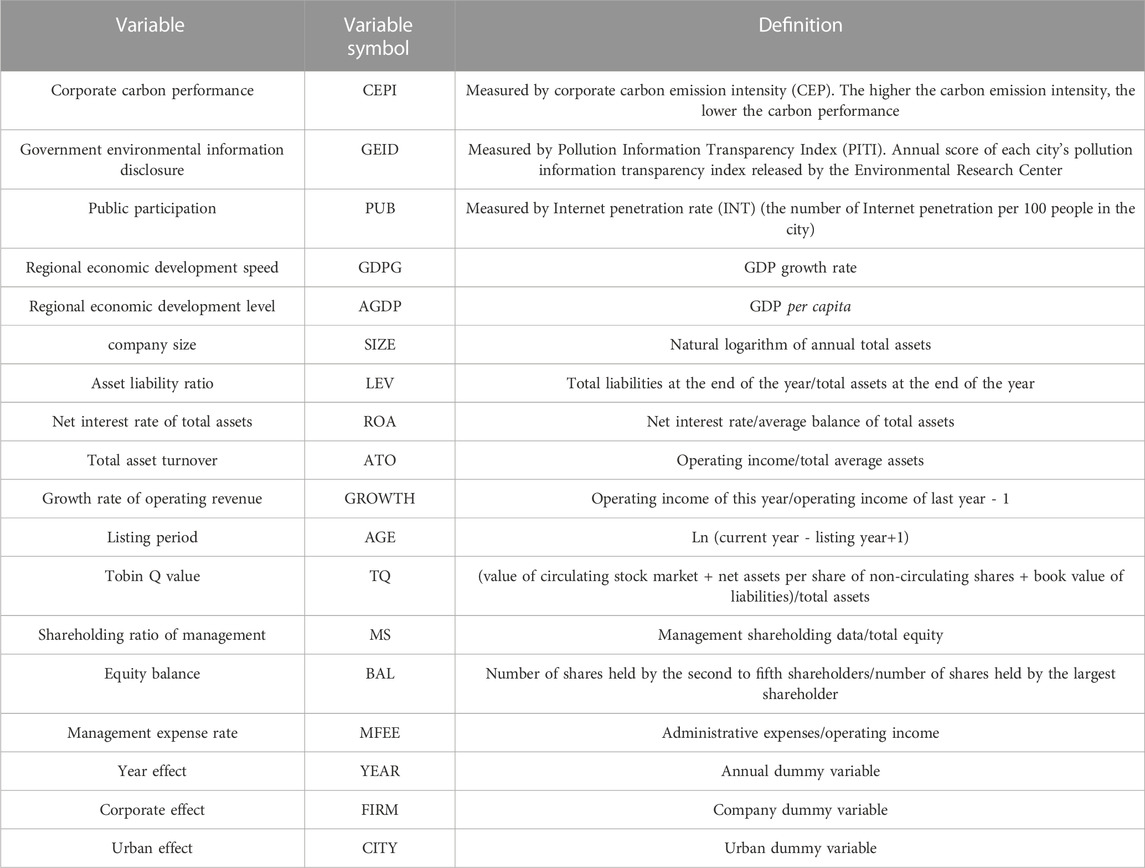

To control any factors that may explain the change in carbon emission performance, this study selected the following intermediary variables that may affect the carbon performance of firms, including regional level and enterprise level (Meng et al., 2022; Yu et al., 2022). They include GDP growth rate (GDPG) and per capita GDP (AGDP) were selected at the regional level. Company size (SIZE), asset liability ratio (LEV), total asset net interest rate (ROA), total asset turnover (ATO), operating income growth rate (GROWTH), age of listing (AGE), Tobin Q value (TQ), management shareholding ratio (MS), equity balance (BAL), and management fee rate (MFEE) at the firm level. In addition, this study also controlled the annual dummy variable (YEAR), the company dummy variable (FIRM), and the city dummy variable (CITY). The specific definitions are presented in Table 3.

TABLE 3. Variable definition.

To test the relationship between GEID and corporate carbon performance, this study constructed the following multiple regression model (Sun and Wei, 2022):

To verify the moderating effect of public participation on the relationship between GEID and corporate carbon performance, the following model was set (Tian and Zhang, 2020; Zheng et al., 2021), in which the explanatory variable is the cross term of the degree of GEID and public participation:

The

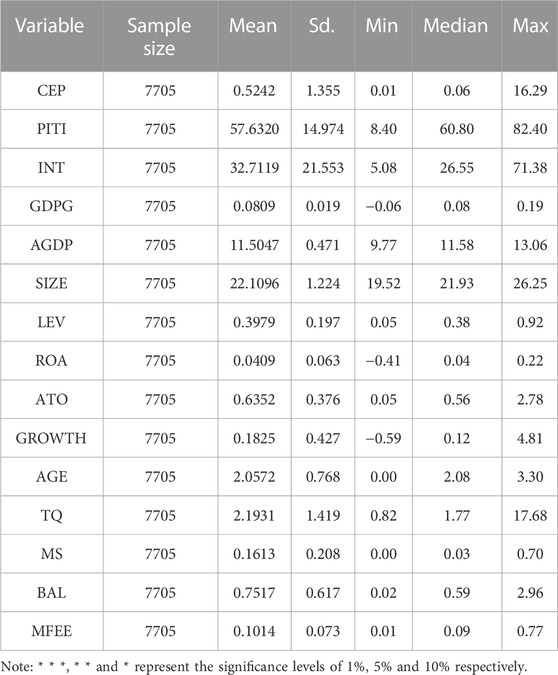

Table 4 presents the descriptive statistics of the main variables. As shown in Table 4, the minimum and maximum carbon emission intensities of firms were 0.01 and 16.29, respectively, with a large difference in CEP among listed companies. Under the same operating revenue, the carbon emissions of some firms differ thousand-fold, which may be because the firms with high carbon emissions are mainly involved in oil processing, coking and nuclear fuel processing industries, and power and heat production and supply industries. Their operating costs mainly focus on coal, coke, oil and other energy sources, so their carbon emissions intensity is high. The standard deviation of PITI is 14.974, which indicates a large difference in the degree of environmental information disclosure among cities, with an average of 57.6242. Thus, the overall level of environmental information disclosure in China is not high.

TABLE 4. Full sample descriptive statistics.

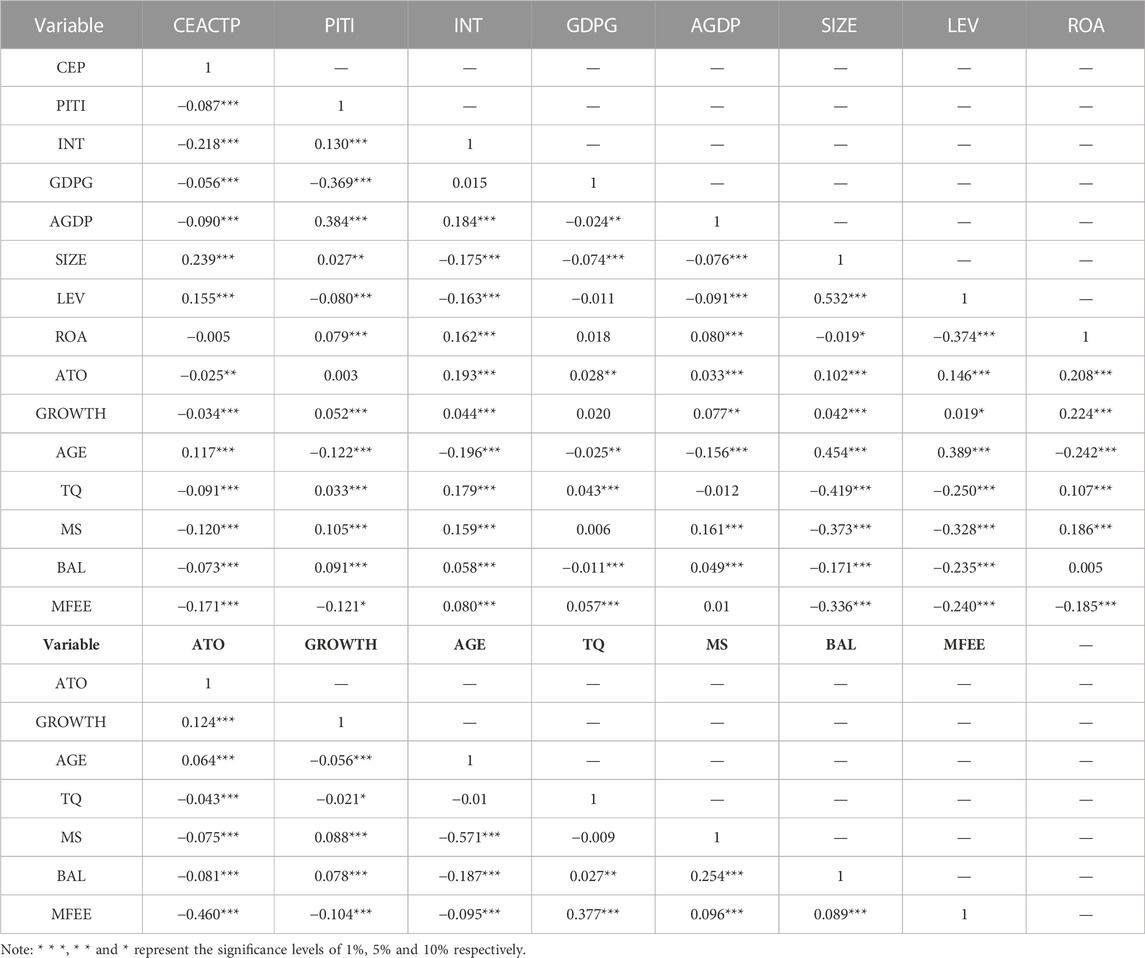

Table 5 presents the correlation coefficient matrix of each variable. The explanatory variables CEP and PITI show a significant negative correlation at the level of 1%, indicating that the GEID is negatively related with the CEP of firms, which preliminarily verifies the Hypothesis H1. The correlation coefficient between other variables does not exceed 0.5, indicating that the introduction of the above variables into the model does not lead to serious multicollinearity problems.

TABLE 5. Pearson correlation coefficient test.

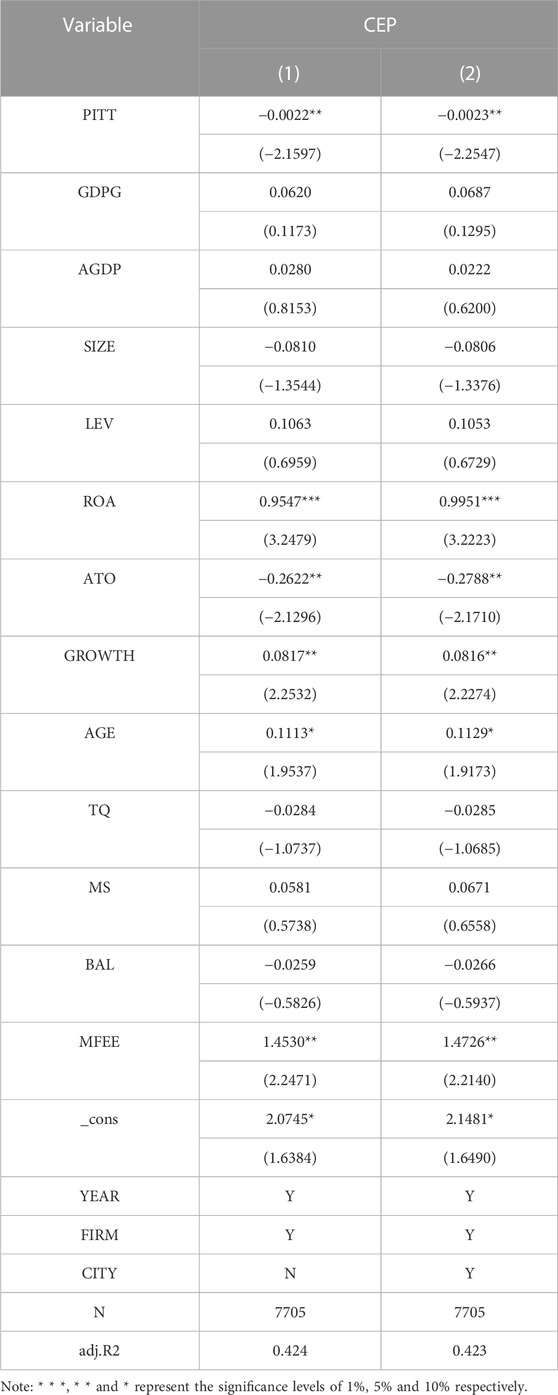

In order to further verify Hypothesis H1, this study conducted multiple linear regression analysis (2). Table 6 shows the results of inspection. Column (1) provides the results of regression of the fixed effect of the year and company under control, and column (2) indicates the results of regression analysis of the fixed effects of the city. The results show that the coefficient of PITI is negative and significant at the level of 5% with CEP, indicating that the higher the degree of GEID, the lower the

TABLE 6. Main effect regression test results.

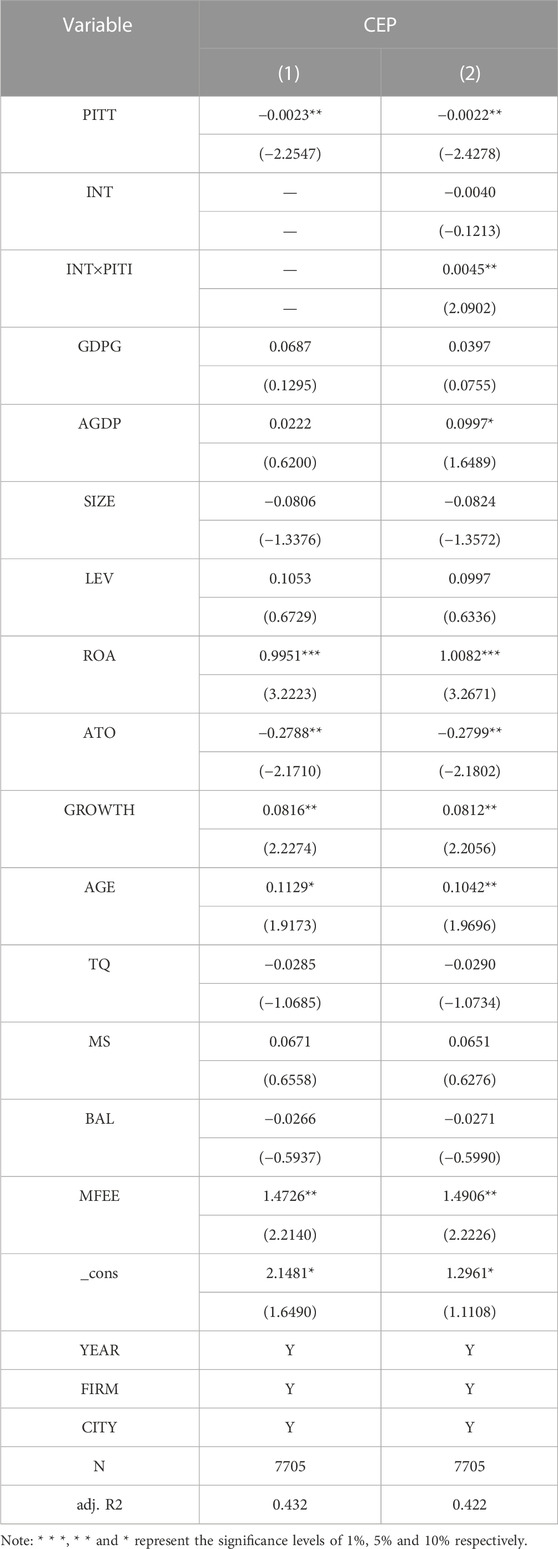

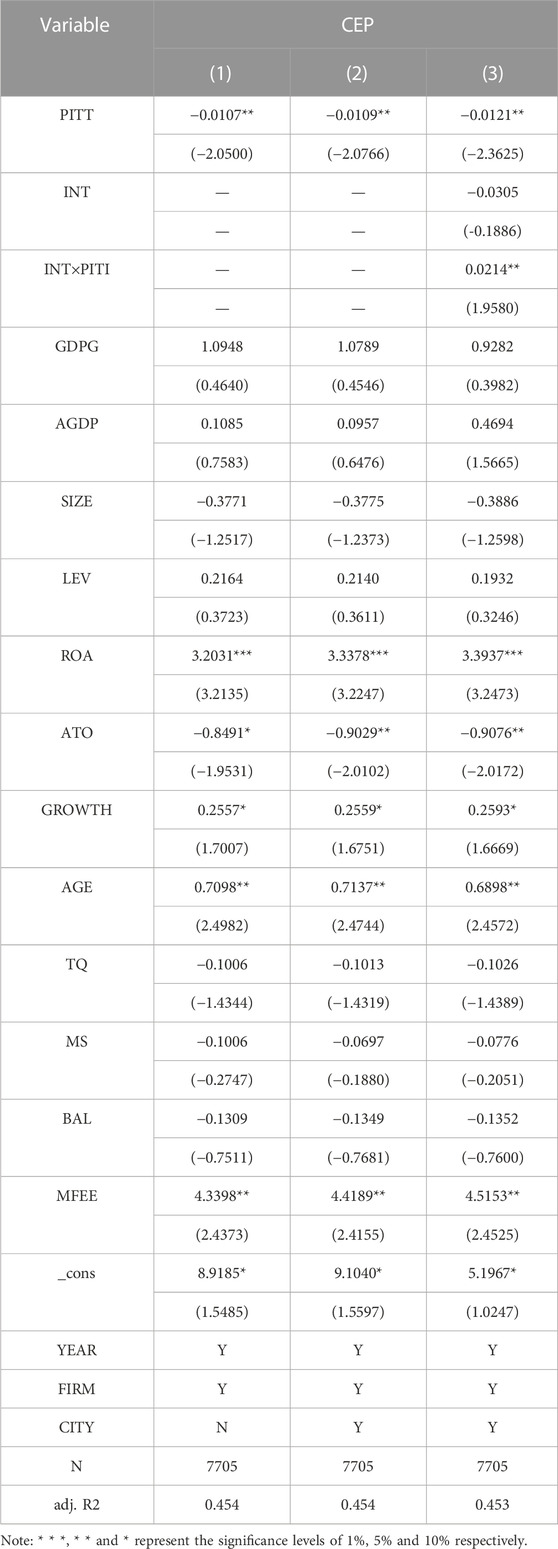

In order to verify the moderating effect of public participation on the relationship between GEID and CEPI, this study conducted a multiple linear regression analysis of model (4). Table 7 presents the results of regression. Column (1) is the main effect of regression analysis. Item (2) is listed as Internet penetration rate and PITI transportation item (INT×PITI). The results of column (2) show that the coefficient of the cross-multiplication term is significantly positive at the level of 5%, while the coefficient of the explanatory variable PITI in the main regression is negative, which means that public participation has an attenuating effect on the main effect. Thus, the degree of public participation has a substitution effect on GEID, thereby H2 is verified.

TABLE 7. Adjustment of Internet penetration.

According to the coefficient of PITI listed in column (1) and (2), public participation did not play a positive role in promoting the effect of GEID on carbon emission intensity. Previous studies have shown that Internet penetration can affect the direction of China’s regulation on enterprise pollution emissions to a certain extent, and when the Internet penetration rate is lower than a certain extent, regulation will aggravate the pollution emission intensity of enterprises (Zhang and Kou, 2018). However, China’s Internet penetration rate has already crossed the threshold. China’s Internet advantages have not been effectively utilized (Tao et al., 2023), resulting in public participation not enhancing the effect of GEID on carbon emission intensity.

1) Replacement of the interpreted variable

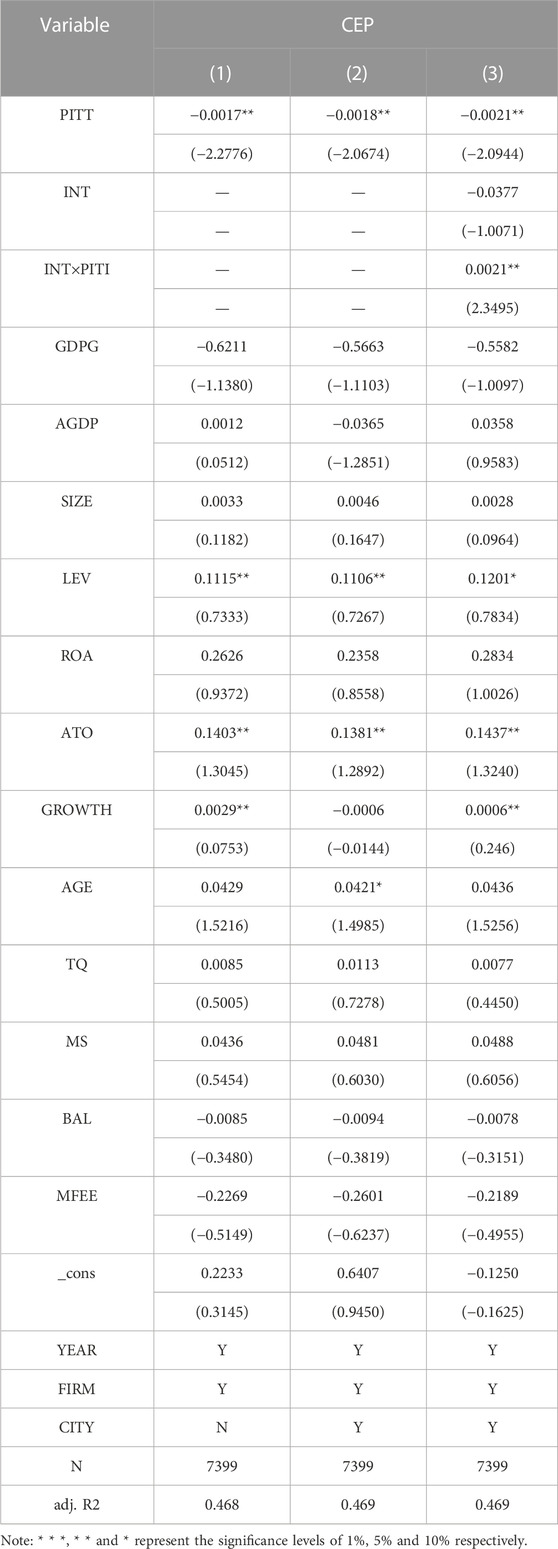

In order to avoid errors in the results of single carbon emission calculation and measurement method, this study obtained industry carbon emission data calculated by a third-party authority based on “carbon neutrality” database of CSMAR, and then re-estimated corporate carbon emissions based on the proportion of operating costs in the operating costs of the industry. The corporate carbon emission intensity CEP2 was calculated based on the ratio of corporate carbon emission data and operating income. The higher the corporate carbon emission intensity, the lower the CEPI.

The empirical results are shown in Table 8. Columns (1) to (2) present the regression results of control year, firm and control year, firm and city, respectively, and the results are basically consistent with the main test above. The adjustment effect test of adding INT×PITI cross item was listed in column (3), which obtained the same result as the previous test. Therefore, the measurement of CEPI in this study is robust, and the replacement of industry carbon emission data did not affect the results of the test hypothesis. Thus, the results again suggest that GEID improves CEPI and public participation has a substitution effect on GEID.

2) Subsample test

TABLE 8. Regression results of alternative carbon performance indicators.

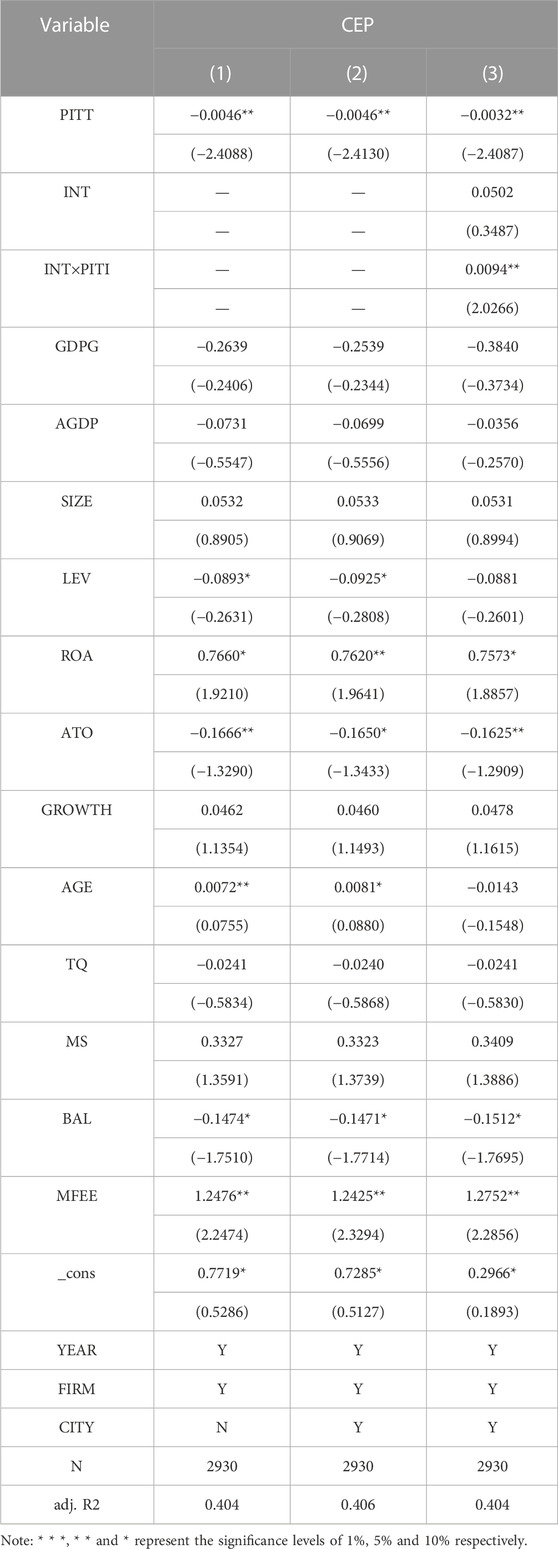

According to the industry classification standards mentioned in the Guidelines for Industrial Classification of Listed Companies issued by the CSRC in 2012, nearly 90% of the sample firms in this study represent manufacturing industry. Most of the energy consumption and carbon emissions of listed manufacturing companies directly affect the production process, so the carbon emission intensity of manufacturing firms more directly reflect the relationship between input and output to a certain extent.

Table 9 shows the results of robustness test involving manufacturing companies in the whole sample. The columns (1) and (2) represent the results of regression of the manufacturing subsamples of control year, firm and control year, firm and city, respectively. Column (3) represents the adjustment effect of adding INT×PITI cross item, which confirms the robustness of the regression analysis.

3) Eliminate other policy shocks

TABLE 9. Regression results of subsamples.

The National Development and Reform Commission issued the Notice on Pilot Work of Low Carbon Provinces and Cities on 19 July 2010, which identified the first batch of low carbon cities as Guangdong, Liaoning, Hubei, Shaanxi, and Yunnan provinces, and eight cities as Tianjin, Chongqing, Shenzhen, Xiamen, Hangzhou, Nanchang, Guiyang, and Baoding. The second batch of pilot cities was organized in April 2012. Currently, there are 42 low-carbon pilot provinces and cities in China. China requires pilot areas to set carbon dioxide emission targets, establish carbon emission trading systems, and perform efficiently to develop leading low-carbon cities. The timing of low-carbon city pilot policy coincides with the time of sample selection in this study, and the existing literature shows that the low-carbon environment pilot policy reduces the carbon emissions of firms. In order to ensure the robustness of the study conclusions reported here, we excluded firms in the low-carbon city pilot policy, and only ensured GEID for the remaining 57 cities, but not in the low-carbon city pilot policy. Regression analysis of samples was conducted again.

The results of regression analysis are shown in Table 10. The columns (1)–(2) represent the results of regression analysis involving the sample firms whose control year, firm and control year, firm and city were not in the low-carbon city pilot policy, respectively. The column (3) represents the adjustment effect due to the addition of the INT×PITI cross-item. It shows that excluding firms in low-carbon pilot cities, the negative impact of GEID on CEP was strengthened, which proves the robustness of the conclusions.

TABLE 10. Excluding other policy shocks.

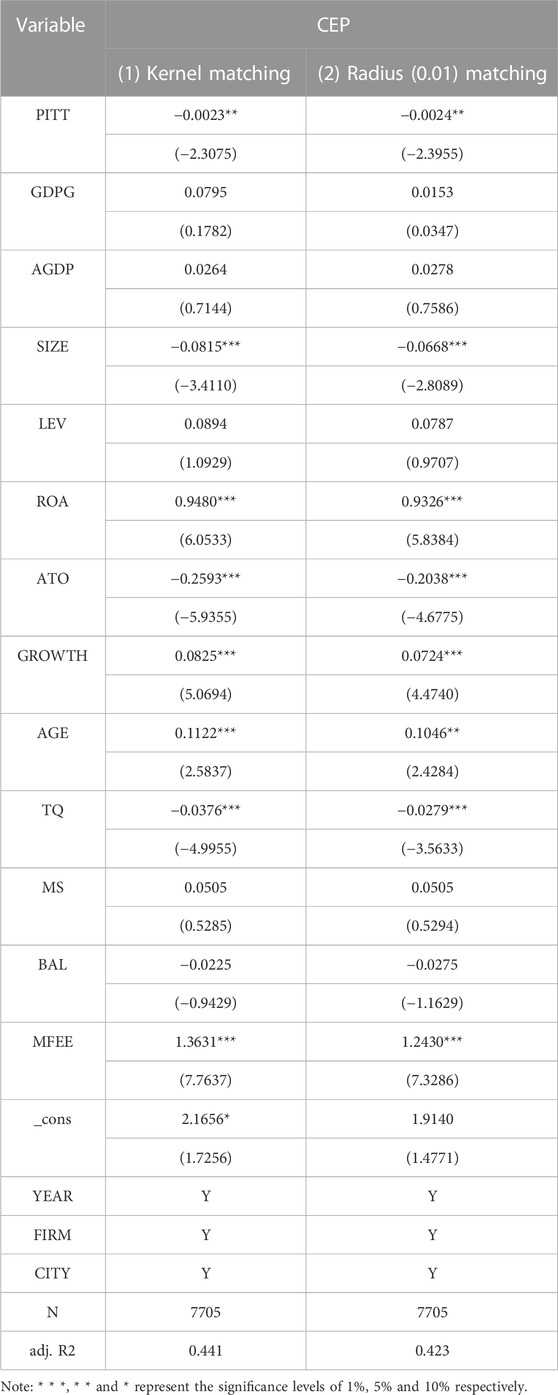

In the PITI sample of explanatory variables analyzed in this study, only cities participating in environmental information disclosure scoring were included. Other cities may not participate in environmental information disclosure scoring due to the high carbon emission intensity level of local firms. Therefore, the conclusions of this study may be affected by sample selection errors. In order to eliminate such issues, this study matched the PSM propensity scores of firms belonging to cities with GEID with those of firms not belonging to cities with GEID. The results are shown in Table 11. Column (1) in the table represents the kernel matching result, and column (2) is the radius (0.01) matching regression. After controlling for sample self-selection error, the coefficient of PITI was still significantly negative, which was consistent with the results of main regression analysis.

TABLE 11. PSM propensity score matching.

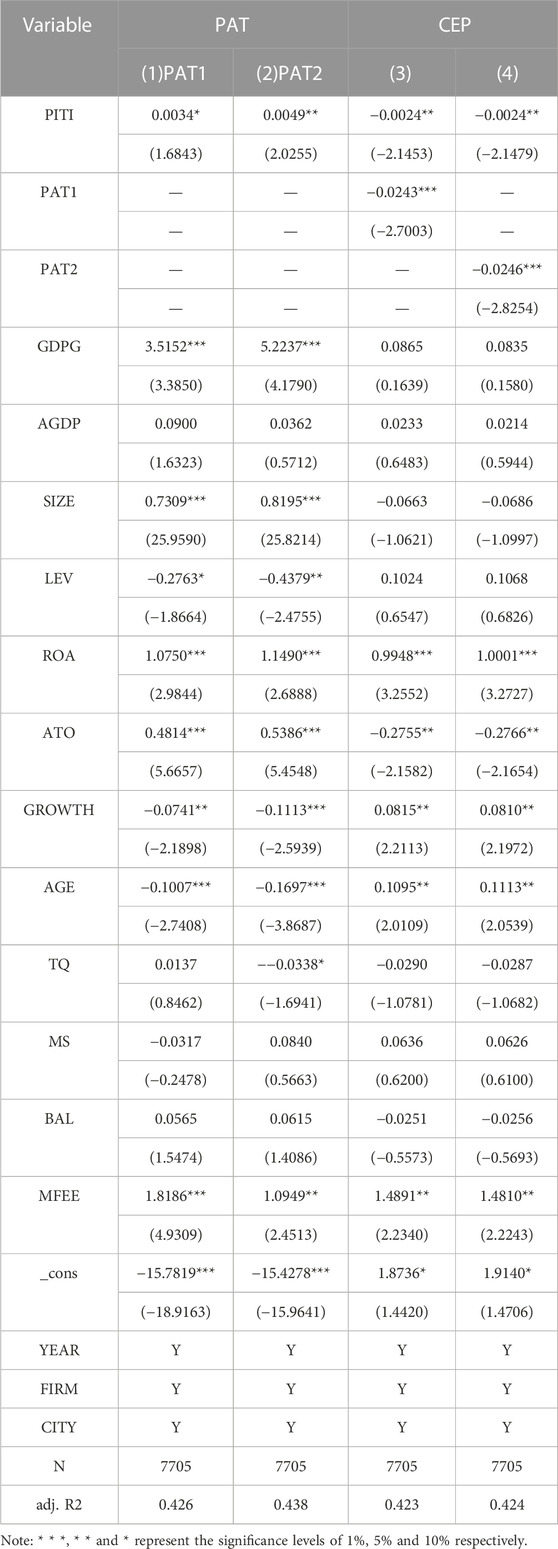

With the strengthening of environmental protection education in recent years, the public attention on environmental protection issues has increased. With the emergence of informal environmental systems (such as GEID), the public can monitor the performance of environmental protection obligations of firms in several ways. The firm and its stakeholders interact and benefit each other. Firms are subject to dual supervision of the government and the public under GEID. The strengthening of the environmental protection concept of stakeholders has increased the corporate cost of environmental default (Ren et al., 2023). Therefore, considering their own reputation and image, firms tend to increase R&D investment in green product innovation (Zeng et al., 2022) and promote the transformation of green technology innovation from “end management” to “source management” (Li et al., 2022).

In order to further investigate whether the internal green innovation of firms is an important strategy for GEID to improve CEPI, based on the practices of (Dong and Wang, 2019; Xu and Cui, 2020), the number of green patent applications in Chinese Research Data Services (CNRDS) was used as an indicator to measure green innovation. The number of green patent applications of firms was divided into two categories: the number of green inventions and the number of green practical inventions. In order to eliminate the right-biased distribution of green patent application data, based on the study of (Wang and Wang, 2021), the number of green inventions and the number of green practical inventions were treated logarithmically, represented by PAT1 and PAT2, respectively, to determine whether GEID affects corporate green innovation. The higher the green patent applications of the firm in the current year, the stronger the green innovation of the firm. The intermediary effect model constructed was as follows:

In the model, PAT refers to the number of green patent applications of the company in the current year, and is represented by PAT1 and PAT2. Other variables are defined as above.

Table 12 shows the intermediary effect of green innovation of firms tested by model (5) and model (6). Columns (1) and (2) represent the results of model (5), which shows that the higher the GEID, the stronger the green innovation of local firms. Columns (3) and (4) list the results of model (6) and verify the previous conclusion, suggesting that GEID can reduce the intensity of corporate carbon emissions and improve CEPI by improving corporate green innovation.

TABLE 12. Mediation effect test.

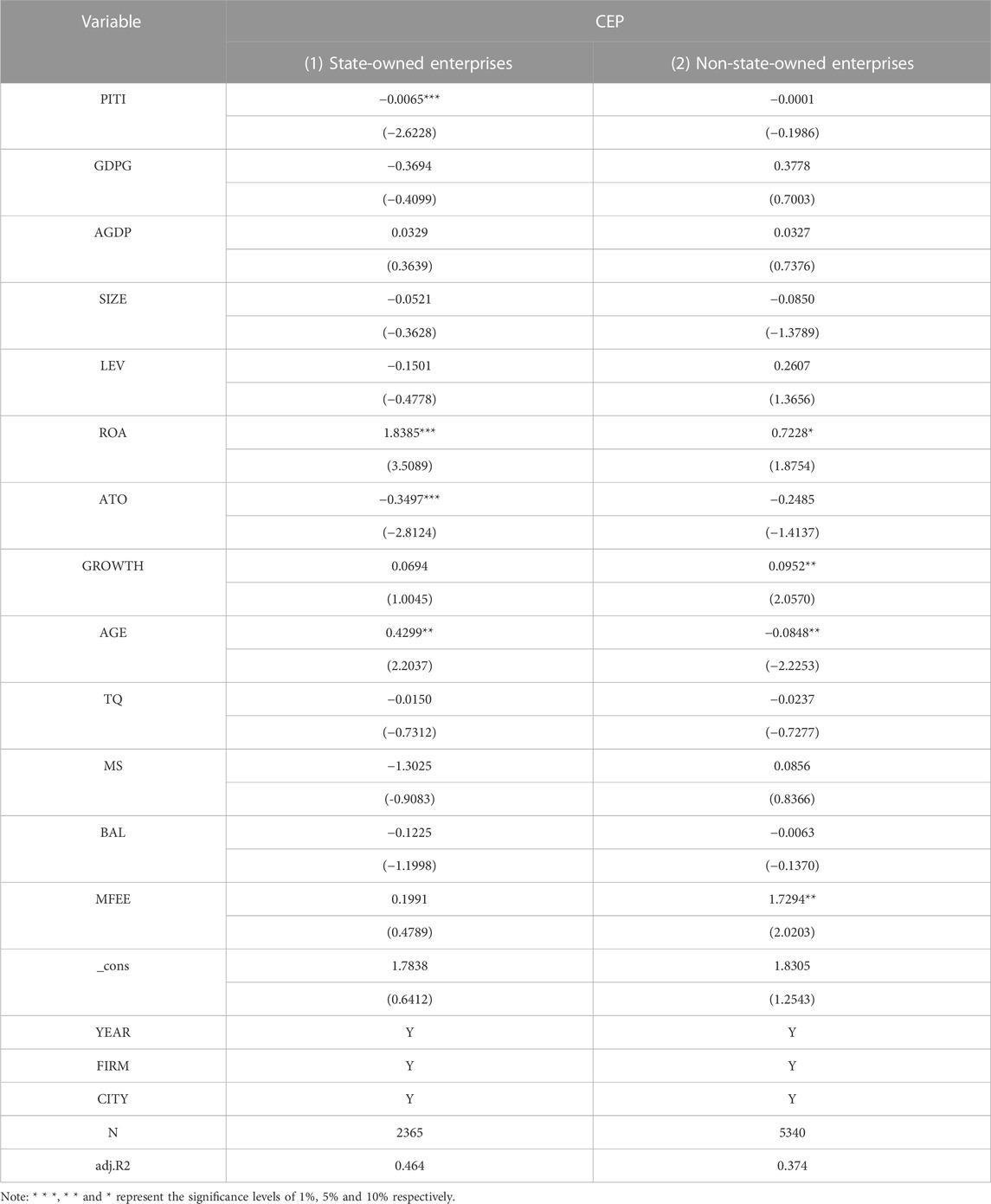

Firms with different property rights exhibit different responses to policies. First, as a subsidiary of the government, state-owned enterprises need to take more responsibility for carbon emission reduction (Li et al., 2019). The leaders of state-owned enterprises are appointed and evaluated by their subordinate government agencies, and their management is composed of government officials. Their performance is mainly evaluated by government officials, who may not focus on profitability, but on the implementation of government policy authorization (Zhuang et al., 2022). State-owned enterprises are largely influenced by national policies and assist the government in achieving its broader political and social goals. However, state-owned enterprises not only bear the economic responsibility of increasing GDP and fiscal revenue, but also bear specific social and environmental responsibilities. Therefore, state-owned enterprises are more likely to reduce carbon emissions under the impact of greater responsibilities and obligations.

Second, compared with other firms, state-owned enterprises have a natural “blood relationship” with the government, and have several resource advantages in carbon emission reduction (Shi, 2022). Compared with non-state-owned enterprises, state-owned enterprises have closer political relations with the government and are more likely to obtain government resources (Liu and Hu, 2020), such as short-term bank loans, lower price equity than the stock market, government firm assistance and financial subsidies, tax incentives and other policies, which facilitate environmental protection activities by firms. Therefore, state-owned enterprises can obtain additional resource subsidies related to carbon emission reduction and respond more positively to government policies.

To test the effect of ownership type on the relationship between GEID and CEPI, this study conducted multiple linear regression analysis of state-owned and non-state-owned enterprises. Table 13 presents the results of regression analysis of property heterogeneity test.

TABLE 13. Property right heterogeneity test.

Column (1) represents the results of regression of state-owned enterprises. The coefficient of PITI is negative and significant at the level of 1%. Column (2) lists the results of regression of non-state-owned enterprises. The coefficient of PITI is negative and the result is not significant. The controlling shareholders of state-owned listed companies are directly or indirectly governments. It indicates that the higher the degree of GEID, the greater the environmental supervision that state-owned enterprises may be subjected to. Compared with non-state-owned enterprises, state-owned enterprises have more obligations to reduce their CEP and improve their carbon performance in order to improve their regional environmentally-friendly image.

As China pays more and more attention to environmental issues, how to guide firms to save energy and reduce carbon dioxide emissions has become a key issue to explore. As an informal environmental regulation system, GEID combines the participation of the public, the government and enterprises, which can not only enable the public to monitor enterprise emission information, but also urge the government to participate in enterprise environmental protection and emission reduction through the government information disclosure platform. In this context, literature research shows that local government carbon emissions indicators, promotion of government officials and the promulgation of local environmental laws and regulations are directly related to local carbon performance. When the degree of government environmental information disclosure is higher, the government mainly exposes the excessive emission behavior of enterprises through public supervision. Good government information disclosure can improve the carbon performance level of enterprises.

This study analyzed a sample of China’s A-share listed companies in manufacturing and mining industries from 2013 to 2018, and empirically tested whether GEID affected CEPI. The results show that the higher the degree of GEID where the firm is registered, the greater the attention on its carbon-use efficiency, and the better its carbon performance. In addition, the higher the degree of local public participation, the greater the public supervision of firms and governments. Public participation weakens the positive impact of GEID on CEPI, and acts as a substitute for GEID. In terms of mechanism, GEID improves carbon performance by promoting green innovation of firms. Further analysis shows that compared with non-state-owned enterprises, state-owned enterprises are more closely connected with the government, and experience greater pressure to reduce carbon emissions and improve carbon performance independently. The policy implications of this study include:

1) Continuous improvement of the environmental regulation system is needed and the combination of informal and formal environmental system should be promoted. GEID can effectively improve the carbon performance of firms, and promote and encourage firms to improve carbon-use efficiency via technological innovation and other ways. Therefore, it is necessary to further expand the scope of cities participating in PITI scoring and improve the quality and frequency of GEID. It is necessary to establish a diversified environmental governance system involving local governments, firms, non-governmental environmental organizations and the public, ensure the sustainability of PITI in promoting environmental efficiency, and develop a coordinated and complementary environmental community. It is necessary to enhance the advantages of formal environmental systems (such as mandatory environmental information disclosure), clearly regulate relevant environmental standards, and urge firms to independently improve carbon utilization efficiency and fulfill environmental protection obligations.

2) The government should play the role of guide and supervisor to promote energy conservation and emission reduction by firms. Governments at all levels should provide subsidies for green innovation to firms and encourage corporate investment. At the same time, through the Internet and other channels, the corporate performance and environmental responsibility should be evaluated in a timely manner to ensure the public’s right to information. Firms that discharge emissions in violation of regulations should be reported promptly to urge them to comply with environmental protection agreements.

3) Firms should increase investment in green innovation and improve carbon-use efficiency. GEID can improve CEPI via corporate green innovation. Firms should improve their environmental awareness and carry out green innovation independently, so as to ease the pressure of GEID on corporate carbon emissions, improve their competitiveness while improving carbon performance, and promote sustainable development.

The study limitations may be addressed in the future. First, this study estimates corporate carbon emissions based on industry carbon emissions. Although this method of calculation is similar at the firm level, different firms were not analyzed. Thus, the data may be biased. In the future, if corporate carbon emissions are included in the mandatory disclosure project, further accurate data can be collected for additional research. Second, the study data only include the main board listed companies, so whether the relationship between regional environmental information disclosure and CEPI in non-listed companies is similar to that of listed companies is unknown. In the future, data of non-listed companies that independently disclose carbon emission data should be collected to further validate the results.

Publicly available datasets were analyzed in this study. This data can be found here: The datasets for this study can be found in the China Stock Market and Accounting Research Database (https://www.gtarsc.com) and National Bureau of Statistics of China (www.stats.gov.cn).

MP, SP, YJ, and SW contributed to conceptualization, formal investigation, analysis, methodology, and writing and editing of the original draft. All authors contributed to the article and approved the submitted version.

This research was supported by National Social Science Foundation of China (No. 21BGL180) and Education Accounting Society of China (No. JYKJ 2021-009ZD).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Chen, H., and Zhen, J. (2022). The impact of technical progress and industrial structure adjustment on China's carbon emission intensity. J. Commer. Res. 6, 1–12. doi:10.13902/j.cnki.syyj.2022.06.007

Clarkson, P. M., Li, Y., Richardson, G. D., and Vasvari, F. P. (2011). Does it really pay to be green? Determinants and consequences of proactive environmental strategies. J. J. Account. Public Policy 30, 122–144. doi:10.1016/j.jaccpubpol.2010.09.013

Cole, M. A., Elliott, R. J. R., and Shimamoto, K. (2005). Industrial characteristics, environmental regulations and air pollution: an analysis of the UK manufacturing sector. J. J. Environ. Econ. Manag. 50, 121–143. doi:10.1016/j.jeem.2004.08.001

Dong, Z. Q., and Wang, H. (2019). Local-neighborhood effect of green technology of environmental regulation. J. China Ind. Econ. 1, 100–118. doi:10.19581/j.cnki.ciejournal.2019.01.006

Dong, Z. Q., and Wang, H. (2021). Validation of market-based environmental policies: empirical evidence from the perspective of carbon emission trading policies. J. Stat. Res. 38, 48–61. doi:10.19343/j.cnki.11-1302/c.2021.10.005

Du, Y. F. (2022). Environmental information disclosure, pollutant emission and ecological civilization construction. J. Statistics Decis. 38, 184–188. doi:10.13546/j.cnki.tjyjc.2022.21.036

Fang, Y., and Guo, J. (2018). Is the environmental violation disclosure policy effective in China? —evidence from capital market reactions. J. Econ. reserch J. 53, 158–174.

Feng, Y. C., and He, F. (2020). The effect of environmental information disclosure on environmental quality: evidence from Chinese cities. J. J. Clean. Prod. 276, 124027. doi:10.1016/j.jclepro.2020.124027

Feng, Y. C., Wang, X. H., and Liang, Z. (2021). How does environmental information disclosure affect economic development and haze pollution in Chinese cities? The mediating role of green technology innovation. J. Sci. Total Environ. 775, 145811. doi:10.1016/j.scitotenv.2021.145811

Kathuria, V. (2007). Informal regulation of pollution in a developing country: evidence from India. J. Ecol. Econ. 63, 403–417. doi:10.1016/j.ecolecon.2006.11.013

Li, G. R., Wen, S. H., and Wang, L. N. (2019). The influence of corporate environmental responsibility on enterprise value under different property rights. J. J. Hebei Univ. Econ. Bus. 40, 92–100. doi:10.14178/j.cnki.issn1007-2101.2019.05.012

Li, Z. H., Shen, T., Yin, Y. F., and Chen, H. H. (2022). Innovation input, climate change, and energy-environment-growth nexus: evidence from OECD and non-OECD countries. J. Energies. 15, 8927. doi:10.3390/en15238927

Li, Q. (2018). A research on emission reduction effects on formal and informal environmental regulation: taking the Yangtze River Economic Belt as an example. J. Mod. Econ. Res. 5, 92–99. doi:10.13891/j.cnki.mer.2018.05.013

Liu, F. R., and Hu, L. J. (2020). The influence of rent-seeking competition on enterprise performence: the prisoner's dilemma of enterprise rent-seeking. J. Econ. Surv. 37, 125–133. doi:10.15931/j.cnki.1006-1096.2020.02.016

Liu, Z. H., and Xu, J. W. (2023). Equity and influence factors of China's provincial carbon emissions under the "Dual Carbon" goal. J. Sci. Geogr. Sin. 43, 92–100. doi:10.13249/j.cnki.sgs.2023.01.010

Liu, L., Jiayu, J., Jiacong, B., Yazhou, L., Guanghua, L., and Yingkai, Y. (2021). Are environmental regulations holding back industrial growth? Evidence from China. J. J. Clean. Prod. 306, 127007. doi:10.1016/j.jclepro.2021.127007

Lu, M. (2021). The impact of formal and informal environmental regulations on environmental performance and economic performance of manufacturing industry in China. J. Statistics Manag. 36, 10–17. doi:10.16722/j.issn.1674-537x.2021.09.004

Maung, M., Wilson, C., and Xiaobo, T. (2016). Political connections and industrial pollution: evidence based on state ownership and environmental levies in China. J. J. Bus. Ethics 138, 649–659. doi:10.1007/s10551-015-2771-5

Meng, X., Gou, D., and Chen, L. (2022). The relationship between carbon performance and financial performance: evidence from China. J. Environ. Sci. Pollut. Res. 30, 38269–38281. doi:10.1007/s11356-022-24974-7

Michael, A., Mingxing, L., Abubakr, N. M., and Sitara, K. (2023). Greening the globe: uncovering the impact of environmental policy, renewable energy, and innovation on ecological footprint. J. Technol. Forecast. Soc. Change 192, 122561. doi:10.1016/j.techfore.2023.122561

Pan, D. (2021). The impact of command-and-control and market-based environmental regulations on afforestation area: quasi-natural experimental evidence from county data in China. J. Resour. Sci. 43, 2026–2041. doi:10.18402/resci.2021.10.08

Ren, C. T., Wang, T., Wang, Y., Zhang, Y. Z., and Wang, L. W. (2023). The heterogeneous effects of formal and informal environmental regulation on green technology innovation-an empirical study of 284 cities in China. J. Int. J. Environ. Res. Public Health 20, 1621. doi:10.3390/ijerph20021621

Ren, S. G., Li, X. L., Yuan, B. L., Li, D. Y., and Chen, X. H. (2018). The effects of three types of environmental regulation on eco-efficiency: a cross-region analysis in China. J. J. Clean. Prod. 173, 245–255. doi:10.1016/j.jclepro.2016.08.113

Shen, K. R., and Jin, G. (2018). The policy effect of the environmental governance of Chinese local government: a study based on the progress of the River Chief System. J. Soc. Sci. China 5, 92–115+206.

Shen, Q., Yuxi, P., and Yanchao, F. (2023). Identifying and assessing the multiple effects of informal environmental regulation on carbon emissions in China. J. Environ. Res. 237, 116931. doi:10.1016/j.envres.2023.116931

Shuai, C. Y., Chen, X., Wu, Y., Tan, Y. T., Zhang, Y., and Shen, L. Y. (2018). Identifying the key impact factors of carbon emission in China: results from a largely expanded pool of potential impact factors. J. J. Clean. Prod. 175, 612–623. doi:10.1016/j.jclepro.2017.12.097

Sun, C., and Wei, X. (2022). Market-incentive environmental Regulations,Government Subsidies,and firm performance. J. Public Finance Res. 97–112. doi:10.19477/j.cnki.11-1077/f.2022.07.008

Tang, A. B., and Xu, N. (2023). The impact of environmental regulation on urban green efficiency-evidence from carbon pilot. J. Sustain. 15, 1136. doi:10.3390/su15021136

Tao, Y., Hou, W., Liu, Z., and Yang, Z. (2023). How can public environmental concerns enhance corporate ESG performance? Based on a dua perspective of external pressure and internal concerns. J. Sci. Sci. Manag. S.and Trans., 1–28.

Tian, X., and Zhang, G. (2020). Environmental information disclosure, environmental regulation and business performance. J. Friends Account., 43–49. doi:10.3969/j.issn.1004-5937.2020.06.008

Tu, Z. G., Hu, T. Y., and Shen, R. J. (2019). Evaluating public participation impact on environmental protection and ecological efficiency in China: evidence from PITI disclosure. J. China Econ. Rev. 55, 111–123. doi:10.1016/j.chieco.2019.03.010

Tu, Z., and Shen, R. (2015). Can the emissions trading scheme achieve porter effect in China? J. Econ. Res. J. 50, 160–173.

Wang, X. Y., Chai, Y. Z., Wu, W. S., and Khurshid, A. (2023). The empirical analysis of environmental regulation's spatial spillover effects on green technology innovation in China. J. Int. J. Environ. Res. Public Health 20, 1069. doi:10.3390/ijerph20021069

Wang, X., and Wang, Y. (2021). Research on the green innovation promoted by green credit policies. J. J. Manag. World. 37, 173–188+11. doi:10.19744/j.cnki.11-1235/f.2021.0085

Xu, J., and Cui, J. B. (2020). Low-carbon cities and firms' green technological innovation. J. China Ind. Econ. 12, 178–196. doi:10.19581/j.cnki.ciejournal.2020.12.008

Yan, H. H., Jiang, J., and Wu, Q. F. (2019). The effects of carbon performance on financial performance which is based on the perspective of ownership type. J. J. Appl. Statistics Manag. 38, 94–104. doi:10.13860/j.cnki.sltj.20180817-003

Yan, Y. Z., Cheng, Q. W., Huang, M. L., Lin, Q. H., and Lin, W. H. (2023). Government environmental regulation and corporate ESG performance: evidence from natural resource accountability audits in China. J. Int. J. Environ. Res. Public Health 20, 447. doi:10.3390/ijerph20010447

Yang, S., Atif, J., and Razib, H. M. (2023). Does China's low-carbon city pilot intervention limit electricity consumption? An analysis of industrial energy efficiency using time-varying DID model. J. Energy Econ. 121, 106636. doi:10.1016/j.eneco.2023.106636

Yang, Y., Lu, A. J., and Zhang, Z. Q. (2020). Dose government environmental information transparency promote environmental governance?An empirical study on 120 cities, China. J. J. Beijing Inst. Technol. Sci. Ed. 22, 41–48. doi:10.15918/j.jbitss1009-3370.2019.7721

Yu, Y. Z., and Yin, L. P. (2022). The evolution of Chinese environmental regulation policy and its economic effects: a summary and prospect. J. Reform. 3, 114–130.

Yu, X., Shi, J., Wan, K., and Chang, T. (2022). Carbon trading market policies and corporate environmental performance in China. J. J. Clean. Prod. 371, 133683. doi:10.1016/j.jclepro.2022.133683

Zeng, X. W., Jin, M., and Pan, S. (2022). Do environmental regulations promote or inhibit cities' innovation capacity? Evidence from China. J. Int. J. Environ. Res. Public Health 19, 16993. doi:10.3390/ijerph192416993

Zhang, H., and Feng, F. (2020). Does informal environmental regulation reduce carbon emissions? evidence from a Quasi-natural experiment of environmental information disclosure. J. Res. Econ. Manag. 41, 62–80. doi:10.13502/j.cnki.issn1000-7636.2020.08.005

Zhang, Q., Chen, W. Y., and Feng, Y. C. (2021). The effectiveness of China's environmental information disclosure at the corporate level: empirical evidence from a quasi-natural experiment. J. Resour. Conservation Recycl. 164, 105158. doi:10.1016/j.resconrec.2020.105158

Zhang, Y., and Kou, P. (2018). Environmental regulation, Internet penetration rate and enterprise pollution emission. J. Ind. Econ. Rev. 9, 128–139. doi:10.14007/j.cnki.cjpl.2018.06.010

Zhao, L., and Zhang, L. (2020). The impact of media attention on enterprise green technology innovation: the moderating effect of marketization level. J. Manag. Rev. 32, 132–141. doi:10.14120/j.cnki.cn11-5057/f.2020.09.011

Zheng, Y., Sun, X., Zhang, C., Wang, D., and Mao, J. (2021). Can emission trading scheme improve carbon emission performance? Evidence from China. J. Front. Energy Res. 9. doi:10.3389/fenrg.2021.759572

Keywords: environmental information disclosure, carbon performance, green innovation, informal environmental regulation, public participation

Citation: Peng M, Peng S, Jin Y and Wang S (2023) Government environmental information disclosure and corporate carbon performance. Front. Environ. Sci. 11:1204970. doi: 10.3389/fenvs.2023.1204970

Received: 13 April 2023; Accepted: 30 October 2023;

Published: 10 November 2023.

Edited by:

Chuanwang Sun, School of Economics, Xiamen University, ChinaReviewed by:

Jiachao Peng, Wuhan Institute of Technology, ChinaCopyright © 2023 Peng, Peng, Jin and Wang. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Youliang Jin, amlueW91bGlhbmcyNkBjc3UuZWR1LmNu

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.