Haijun Zhang

Haijun Zhang Jintao Wang2

Jintao Wang2

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 19 January 2023

Sec. Land Use Dynamics

Volume 11 - 2023 | https://doi.org/10.3389/fenvs.2023.1107489

This article is part of the Research Topic Land Use Management and Carbon Abatement in a Sustainable Development Perspective View all 12 articles

The level of green financial infrastructure is measured using a symbiometric model with the Chinese provincial panel data from 2008 to 2020, and also the carbon emission efficiency is measured using the super-efficient SBM-DEA model with the carbon emission data at the provincial level. This paper tests the carbon emission efficiency improvement and convergence effects of green financial infrastructure using fixed-effects models, non-dynamic panel threshold models and spatial econometric models, while considering the role of environmental regulation in the process. It is found that green financial infrastructure significantly contributes to the improvement of carbon emission efficiency and accelerates the convergence rate of carbon emission efficiency between regions; the carbon emission efficiency improvement and convergence effects of green financial infrastructure are influenced by the intensity of environmental regulation, and we point out that either too strong or too weak environmental regulation will weaken the effectiveness of green financial infrastructure, which means there is a significant threshold effect; the spatial durbin model shows that the effect of green financial infrastructure on carbon emission efficiency has a spatial spillover effect of “neighbors as partners”, that is, while green financial infrastructure promotes the improvement of carbon emission efficiency in the region, it also helps to promote the improvement of carbon emission efficiency in the neighboring regions. Therefore, China should accelerate the improvement of the green financial infrastructure system, improve the carbon emission rights market trading system, enhance the effectiveness of environmental regulation, and strengthen regional economic cooperation, so as to empower the development of low-carbon and green economic transformation.

As one of the world’s largest developing countries, China’s economy has made remarkable achievements since the reform and opening up, and its economic strength has been significantly improved, but some development problems have arisen in this process, among which energy consumption and environmental pollution are of great concern. The contradiction between the rough economic development mode and the resources and environment has become more and more prominent, leading to a year-on-year increase in energy consumption and high carbon emissions. Against this backdrop, the pressure on domestic resources and the ecological environment are worsening, thus severely limiting the sustainable development of the economy. In order to effectively mitigate the “dilemma” between economic development and ecological protection, the Chinese government has proposed the goals of “carbon peaking” and “carbon neutrality” in the top-level design. In addition, the Central Economic Work Conference and the 14th Five-Year Plan have formulated initiatives related to low-carbon economy to promote low-carbon emission reduction and synergy, and to push the economy forward. At this stage, due to the complexity of the causes of carbon emissions, it is questionable whether the concept of green development can be effectively transformed into policy dividends to promote environmental polluters to take a low-carbon development path. In view of this, focusing on the causes of carbon emissions and exploring the realization path of carbon emission reduction is of great theoretical value and practical significance to promote the decoupling of economic growth from carbon emissions and thus achieve high-quality economic development.

Green finance, such as green credit, green bonds and green insurance, may be able to provide new ideas to solve the carbon emission problem (Falcone and Sica, 2019; Liu et al., 2022), but the role of green finance in reducing pollution and carbon emission must be supported by a well-developed financial infrastructure system, so it is a practical necessity to innovate green financial infrastructure. Similar to the meaning of financial infrastructure, green financial infrastructure mainly refers to the infrastructure that guarantees the smooth implementation of carbon finance, including carbon emission right trading market, carbon emission right trading entities, financial products with carbon as the underlying, carbon emission trading market system and legal policies, and accounting standards for carbon financial activities (Zheng and Shi, 2017; Chen et al., 2021; Singhania and Saini, 2021). The importance of green financial infrastructure lies in the fact that it bridges the gap between the various players in the green financial system and plays an important role not only in resource allocation, but also, more importantly, has policy-oriented properties that help ensure the realization of government policy intentions (Liu et al., 2017; Liu et al., 2019). Specifically, green financial infrastructure can direct the flow of financial resources to low-carbon industries and green technology enterprises, in line with the concept of sustainable development. At the same time, a well-developed green financial infrastructure system can also force polluting enterprises to eliminate backward production capacity, realize process restructuring and value-added creation, and help them transform into low-carbon enterprises, thus improving carbon emission efficiency (Ang, 2008; Niu et al., 2020). The level of green financial infrastructure and its effect on reducing pollution and carbon emissions, however, are inevitably related to environmental regulations, and both financial market players and environmental polluters will change their strategies to cope with different environmental regulations, so the marginal benefits of constructing green financial infrastructure will vary (Dong and Wang, 2021; Wang and Huang, 2022). In other words, the impact of green financial infrastructure on carbon emission efficiency may change with the intensity of environmental regulation. It is worth further exploring whether strengthening green financial infrastructure can play a role in improving the efficiency of carbon emission when environmental regulations are at different levels. In addition, as inter-regional economic ties become closer, the allocation of green financial infrastructure gradually breaks through the constraints of spatial geography, and with the integration of ecological civilization construction into performance assessment in China at this stage, there is an obvious tendency for local governments to “protect the championship”, which implies that there may be a “local-neighborhood” effect of green financial infrastructure construction on carbon emission efficiency. The above analysis shows that improving the level of green financial infrastructure not only helps to promote regional carbon emission efficiency, but also helps to promote the convergence of regional carbon emission efficiency.

In view of this, based on Chinese provincial panel data, this paper systematically examines the impact of green financial infrastructure on carbon emission efficiency. First, the interaction mechanism between carbon emissions, green financial infrastructure and environmental regulation is analyzed and the research hypothesis is proposed; second, the indicators of carbon emission efficiency, green financial infrastructure and environmental regulation intensity are measured, and a benchmark regression model is used to analyze whether green financial infrastructure can promote the improvement and convergence of carbon emission efficiency, while the impact of environmental regulation intensity is considered; third, a non-dynamic panel threshold model is used to analyze the effects of different levels of green financial infrastructure and different environmental regulation intensity on carbon emission efficiency, and a spatial econometric model is used to analyze the spatial spillover effects of green financial infrastructure.

The marginal contribution of this paper is mainly reflected in two aspects: firstly, it is reflected in the measurement of green financial infrastructure, which is both an innovation based on the perspective of green finance and solves the problem of insufficient explanatory power of a single indicator; secondly, it is reflected in the inclusion of convergence effect analysis, which is significantly different from the existing literature, and focuses on the carbon reduction effect of green financial infrastructure while paying more attention to its impact on achieving the convergence of regional carbon emission efficiency.

This paper progresses as follows: Section 2 introduces the interaction mechanism among green financial infrastructure, environmental regulation and carbon emission efficiency; Section 3 presents the variables and econometric models; Section 4 reports the improvement effect and convergence efficiency of green financial infrastructure development on carbon emission efficiency; Section 5 concludes the whole paper and makes policy recommendations.

Integrating green financial infrastructure, carbon emission efficiency and environmental regulation into the same analytical framework requires a case-by-case analysis of the relationship between the two. In fact, green credit, green bonds and ESG funds are all important forms of green financial infrastructure, among which green credit has received much attention, so here is an insight into the impact of green financial infrastructure on carbon emission efficiency from the perspective of existing studies on green credit and carbon emission efficiency (Hossain, 2018; Gilchrist et al., 2021; Wang and Huang, 2022).

This paper argues that strengthening the construction of green financial infrastructure can help strengthen the resource optimization effect, signaling effect and social supervision effect of the financial system, and promote the transformation of the economy to green and low-carbon. From the perspective of resource optimization effect, the construction of green financial infrastructure is inevitably accompanied by the continuous improvement of financial institutions, financial systems and professional talents, especially under the guidance of green financial policies, green financial institutions provide financing facilities and preferential interest rates for low-carbon industries and green sectors, which is conducive to alleviating the financing constraints of enterprises, promoting their R&D of green technologies and improving carbon emission efficiency (Wang and Wang, 2021). At the same time, the continuous improvement of green financial infrastructure will further create financing constraints for environmental polluters and inhibit their production behavior, forcing them to make low-carbon transformation, thus helping to improve the status quo of “high consumption and high emissions” (Amore and Bennedsen, 2016; Niu et al., 2020). From the perspective of signaling effect, the construction and improvement of green financial infrastructure fits perfectly with the top-level design of the central government in energy conservation and carbon reduction. The construction of software such as carbon emission system, environmental monitoring system and carbon emission right trading market system will stimulate and guide social capital to flow to green industries and promote the overall industrial structure to leap towards low-carbon, eco-friendly and advanced direction. At the same time, the construction and improvement of green financial infrastructure at the hardware level, such as green financial institutions, carbon emission right trading institutions and carbon emission financing credit agencies, provides the possibility for the government to carry out pilot carbon right emission trading pilot projects, implement carbon emission supervision and take punitive measures. In other words, the construction of green financial infrastructure will serve as a warning to polluting enterprises, prompting relevant industries to adjust their development plans and seek green development layout. From the perspective of social supervision effect, green financial infrastructure not only helps green financial institutions to realize real-time supervision of carbon emissions, but also forces relevant enterprises to improve the disclosure of carbon emissions, thus shaping a good social image and enhancing the self-discipline of enterprises. In addition, a well-developed green financial infrastructure will also encourage the public and industry associations to participate in the supervision of enterprises’ carbon emission behaviors, forming an external monitoring mechanism. Moreover, green financial infrastructure further deepens the linkage between different regional carbon financial markets, which in turn contributes to the convergence of regional carbon emission efficiency. In summary, the following hypothesis is proposed.

Hypothesis 1:. Green financial infrastructure helps to promote the improvement and convergence of carbon emission efficiency.

The impact of green financial infrastructure on carbon emission efficiency may be closely related to environmental regulations. The reason is that while environmental regulations promote energy saving and low-carbon development of microeconomic agents, they also increase the cost of institutional compliance and pollution management (Shao et al., 2016; He et al., 2020). Therefore, as an external constraint, environmental regulations can change the costs and benefits of economic activities, thus influencing microeconomic agents’ green development transition decisions. Furthermore, as the intensity of environmental regulation varies, the costs and benefits of economic activities may be asymmetric, which can dynamically affect the carbon reduction effectiveness of green financial infrastructure.

Specifically, when the level of environmental regulation is low, microeconomic agents only need to pay a low cost to meet the requirements of environmental regulation. In contrast, if microeconomic agents make a low-carbon transition, they need to face high investment, long-cycle and risky projects. Under such circumstances, microeconomic agents, as profit-seekers, are more inclined to maintain the “inertia of change” and maintain the status quo in order to maximize their profits. What’s more, when the degree of environmental regulation is low, due to the influence of information asymmetry and other factors, strengthening the construction of green financial infrastructure may induce opportunistic behavior. In this case, microeconomic agents may distort the use of green finance (e.g., green credit) and use it for scale expansion instead of low-carbon transformation, which increases carbon emissions. When the degree of environmental regulation is high, microeconomic agents will increase the demand for green finance and pursue low-carbon development under the combined effect of internal incentives and external pressure, which is conducive to reducing carbon emissions (Yu et al., 2020). In terms of internal incentives, when the degree of environmental regulation is high, low-carbon development strategies can create “compensatory benefits” that exceed the costs of environmental regulation. The reason is that microeconomic agents can gain a first-mover advantage, occupy market share, and obtain product premiums by producing differentiated green products. In terms of external pressure, when the intensity of environmental regulation is high, polluting enterprises face more serious regulatory costs and financing constraints, and investors will also give lower market valuation to polluting enterprises, which will force microeconomic agents to carry out green innovation and product upgrading to meet stakeholders’ demands for green development (Liu et al., 2017; Zhao et al., 2022). In summary, when the degree of environmental regulation intensity is low, strengthening green financial infrastructure may increase carbon emissions, while when the level of environmental regulation intensity is high, strengthening green financial infrastructure will significantly reduce carbon emissions. This implies that the carbon reduction effect of environmental regulation on green financial infrastructure may be two-sided, and whether it can play the role of “low-carbon transition” or “pollution expansion” needs to be further verified. Based on this, this paper proposes the following hypothesis.

Hypothesis 2:. There is a threshold effect of environmental regulation on the impact of green financial infrastructure on carbon emission efficiency.

The “center-periphery” model of new economic geography suggests that the cross-regional mobility of production factors triggers spatial agglomeration or diffusion effects (Zhang and Yue, 2019; Wang and Huang, 2022). At the present stage, as factors of production such as human capital, financial resources, and technological endowments move more frequently between regions in China, the spatial correlation of economic activities rises, and it is therefore necessary to explore the spatial spillover effects of green financial infrastructure on carbon emission efficiency. In this paper, we analyze the spatial spillover effect of financial infrastructure on carbon emission efficiency from two aspects: innovation spillover and industrial agglomeration.

Specifically, in terms of innovation spillover, with the increasing spatial interaction of economic development, the level of regional innovation not only directly affects the efficiency of factor allocation in the region, but also creates an innovation spillover effect through the dynamic flow and transformation of innovation resource potential difference between regions (Guo et al., 2022). The development of green finance can help green technology innovation and form a “technology dividend”, which can improve the carbon emission performance of local and neighboring regions and promote the increase of total factor carbon productivity (Shao et al., 2022), that is, due to the existence of innovation spillover effect, the green innovation efficiency between regions will show a gradual decrease, which is conducive to the reduction of carbon emissions in the neighboring regions. In terms of industrial agglomeration, there is usually an industrial agglomeration between regions due to the division of labor in technology development, production and application (Verhoef and Nijkamp, 2002). When green financial infrastructure generates a low-carbon economy, industrial spatial agglomeration can provide favorable conditions for the vertical spillover of low-carbon technologies, thus promoting the low-carbon transformation and intrinsic value enhancement of the industrial chain. Additionally, as industries complete their green value chain restructuring, there may be a “market crowding effect” in industrial agglomerations (Andersson and Lööf, 2011). At this point, driven by competitive advantages and excessive profits, industries with low-carbon technologies will expand their markets to neighboring regions, thus leading to horizontal spillover of low-carbon industries, reducing carbon emissions in neighboring regions and promoting the convergence of carbon emission efficiency in different regions (Dong and Wang, 2021; Hao et al., 2021). Based on the above analysis, this paper suggests that green financial infrastructure can improve the carbon emission efficiency in the region and also help to improve the carbon emission efficiency in the neighboring regions and achieve the convergence of the neighboring regions, that is to say, it has the characteristic of “neighbor as partner”. Therefore, we propose the following hypothesis.

Hypothesis 3:. There is a significant spatial spillover effect on the impact of strengthening green financial infrastructure on carbon emission efficiency.

The improvement effect of green financial infrastructure on carbon emission efficiency (Hypothesis 1) is examined based on the following econometric model.

where

To analyze the impact of green financial infrastructure on the convergence of regional carbon emission efficiency (Hypothesis 1), this paper draws on the researches of Zhang and Yue (2019) to construct econometric models without (model 2) and with (model 3) spatial interaction effects, respectively, for analysis.

where 1)

To verify whether the green financial infrastructure for carbon emission efficiency improvement effect and convergence effect are related to the intensity of local environmental regulations (Hypothesis 2), this paper analyzes by constructing non-dynamic panel threshold models (Hansen, 1999; Khan and Su, 2021; Wang et al., 2021).

where γ is the threshold value to be estimated, and there may actually be a single threshold or multiple thresholds, and the model is generally corrected according to the results of the threshold search.

The main methods for measuring carbon emission efficiency mainly include Data Envelopment Analysis (DEA) model, Stochastic Epidemic Model, Technique for Order Preference by Similarity to Ideal Solution (TOPSIS), Computable General Equilibrium (CGE) model, etc. There is a large gap in the efficiency measurement results of these methods, but studies have shown that the Data Envelopment Approach method (DEA) is a more suitable method for assessing efficiency (Chen and Jia, 2017; Mardani et al., 2018). Meanwhile, in this paper, considering that carbon emissions is a non-expected output variable, so this paper draws on the research of Tone (2001) and Yang et al. (2022a) to choose the super-efficient SBM-DEA model, which based on slack variables and considering non-expected outputs, to measure the regional carbon emission efficiency. The model is as follows:

The constraints are:

where CE_EFF is a non-radial and non-oriented efficiency difference indicator considering the carbon emission efficiency of non-desired outputs, m is the total number of input indicators, x is the number of input variables, yg and yb denote desired output terms and non-desired output terms; s1 and s2 are the number of desired output and non-desired output terms, and λ is the weight vector.

The physical capital stock (K), human capital stock (H) and energy input (N) are selected as input indicators, and the output level (Y) and carbon emissions (CE) are selected as desired and undesired output indicators, respectively. The physical capital stock (K) is estimated by the perpetual inventory method based on Soni et al. (2019); the human capital stock (H) is expressed as the product of the number of employees in society and the average years of education (Zhang and Yue, 2019); the energy input (N) is the total regional energy consumption (House et al., 2009; Al-mulali and Sab, 2013; Akalpler and Hove, 2019), in million tonnes of standard coal; the output level is taken as a proxy for the regional real GDP per capita, taking into account the regional development differences; the carbon emission per capita is used as a proxy for CO2 emissions in this paper, which is obtained by dividing each province’s CO2 emissions divided by the province’s total population (Sarkodie and Strezov, 2019; Yang et al., 2022b; Wang and Huang, 2022). In particular, it should be noted that carbon emissions at the provincial level are usually difficult to account for, so there is no uniform measurement method. Therefore, this paper calculates the annual carbon dioxide emissions of each province based on the carbon dioxide emission factors of eight types of fossil fuels provided by the 2006 IPCC Guidelines for National Greenhouse Gas Inventories and the China Energy Statistical Yearbook, respectively, and the energy fossil fuel consumption of each province, calculated as follows.

where C is carbon dioxide emissions; k is the ratio of carbon dioxide to carbon molecules by weight, that is, k = 44/12; Ei is the consumption of fossil fuel type i; and δi is the emission factor of fossil fuels in category i. I denotes the eight energy sources selected for this paper, which are coal, coke, crude oil, gasoline, paraffin, diesel, fuel oil and natural gas. From this, the carbon emissions at the provincial level are obtained according to the formula CE = C/POP, where POP is the number of resident population in the region at the end of the year.

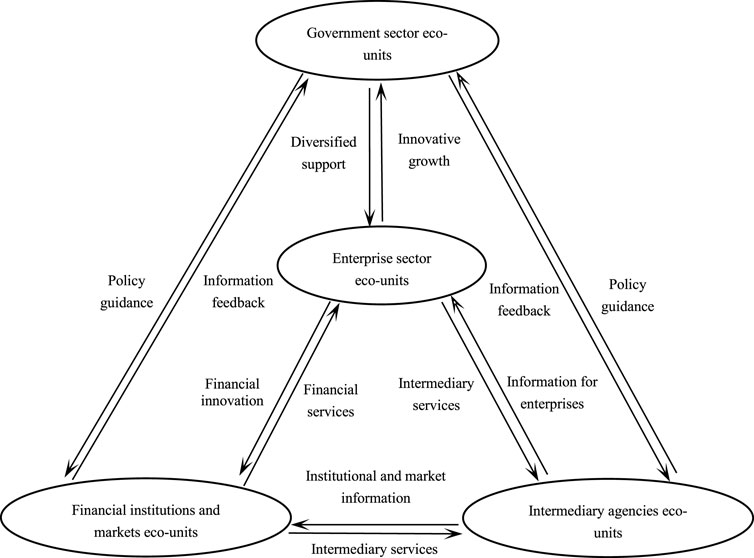

How to measure the level of regional green financial infrastructure is usually difficult because green financial infrastructure is different from green finance in that it covers not only the content of green finance (such as green credit, green bonds and green industry investment), but also the policy documents, legal foundation and financial platforms that guarantee the functioning of green finance. Especially in the context of the rapid development of financial technology, green finance for carbon emission efficiency cannot be separated from the support of digital financial networks, and these new technologies have a significant role in promoting information sharing, enhancing the efficiency of financial resource allocation, maintaining the stability of the financial system, promoting economic growth and improving the construction of green financial infrastructure (Lawless et al., 2015). Then how to incorporate numerous factors into the same framework to comprehensively and accurately evaluate the green financial infrastructure is an important part of this paper, and also the difficulty part of this paper. We argue that the symbiosis theory proposed by the biologist Anton in 1897 provides the theoretical basis for this paper, and this theory is widely used in the field of sociological research (Martin and Schwab, 2013). Based on these research results, this paper also constructs the green financial infrastructure ecosystem evaluation index system method to measure the level of green financial infrastructure in each province (region and city) with the help of ecological symbiosis idea. In a general sense, a symbiotic system is an ecosystem (e.g., an industrial ecosystem) formed by symbiotic units in a certain symbiotic environment according to a symbiotic pattern, or it can be said that a symbiotic system is an equilibrium in which different species form collaborative relationships and maintain self-fulfillment based on stakeholder relatedness (Lu et al., 2022). Based on the above literature, which shows that a complete ecosystem consists of three elements: ecological units (eco-units), symbiotic model and symbiotic environment, this paper identifies four eco-units, namely, financial institutions and markets, intermediary Agency, government sector and enterprise sector, from the perspectives of hardware facilities, software constraints and role mechanisms of green financial infrastructure. The symbiotic relationship among them is shown in Figure 1.

FIGURE 1. A green financial infrastructure ecosystem based on symbiotic theory.

Figure 1 presents the symbiotic relationship between different eco-units. It can be seen that the mutual cooperation, coordination, co-growth and harmonious coexistence of eco-units stimulate the symbiotic effect of the green financial infrastructure ecosystem, but the play of the symbiotic effect depends not only on the mutual cooperation between two eco-units, but also on the overall function brought by the comprehensive interaction of eco-units. At the same time, we can also see that the ultimate purpose of the green financial infrastructure ecosystem is to promote the green development of the enterprise eco-unit, which is mainly reflected in the improvement of the green production efficiency of the enterprise, that is, the improvement of the carbon emission efficiency in the production process.

Here it is necessary to make a brief elaboration on the symbiotic relationship between them: 1) The symbiotic relationship between the enterprise sector eco-units and the financial institutions and market eco-units is reflected in the fact that financial institutions and markets provide green credit support and green investment and financing channels for enterprises (Ren et al., 2022a); the green low-carbon transformation process of enterprises will increase the demand for specific financial services from financial institutions, thus promoting financial institutions and financial markets to strengthen green financial products and services innovation (Amore and Bennedsen, 2016; Cao et al., 2022); 2) The symbiotic relationship between of enterprise sector eco-units and intermediary agencies eco-units is reflected in the alleviation of the information asymmetry between banks and enterprises and the financial exclusion of formal financial institutions, thereby improving the accessibility of green financial services to enterprises; at the same time, intermediaries will collate and record the relevant information before and after financing obtained by enterprises in order to provide reference for decision-making in subsequent operations, thereby improving the quality and professionalism of intermediary services, and this will enhance the quality and professionalism of intermediary services (Levchenko and Ostapenko, 2016; Park and Kim, 2020); 3) The symbiotic relationship between enterprise sector eco-units and government sector eco-units is manifested by the government providing financial subsidies and taxation facilities for the green and low-carbon transformation of enterprises to stimulate their clean technology innovation; the activities of enterprises promote the growth of knowledge economy to increase the total economic volume and fiscal revenue, so that the fiscal expenditure can be returned in the form of taxation, thus ensuring the recyclability of the fiscal funds of government sector (Green and Murinde, 2021; Peng et al., 2021; Yu et al., 2021); 4) The symbiotic relationship between financial institutions and market eco-units and intermediary agency eco-units can be described as intermediary agencies alleviate the information asymmetry between banks and enterprises by transmitting enterprise related information to financial institutions and financial markets, thus enhancing the efficiency of financial services; at the same time, the interaction between financial institutions and intermediaries helps intermediaries realize the precipitation and accumulation of data and form an information warehouse, which in turn helps improve specialized business capabilities (Purves et al., 2015); 5) The symbiotic relationship between financial institutions and market eco-units and government sector eco-units can be described as follows: governmental sector can disperse and resolve the investment risks of financial institutions and financial markets and guide the development of green credit business by improving green finance-related laws and regulations, providing policy loans, establishing green development guidance funds and subsidizing green transition insurance premiums; financial institutions and financial markets can form comprehensive supervision and management of enterprises’ governance structures, management systems and credit levels, thus safeguarding the effectiveness of governmental sector’s financial funds and improving the allocation efficiency of public resources (Hossain, 2018; Falcone and Sica, 2019); 6) The symbiotic relationship between intermediary agencies eco-units and government sector eco-units is manifested in the establishment of policy guarantee institutions by government sectors and moderate equity participation in intermediaries, thus reducing the risks and costs of intermediaries’ operation and promoting the development of intermediary service institutions; at the same time, intermediaries can transmit the demands of enterprises, financial institutions and markets to government departments, thus helping them to formulate precise and effective Green financial support policies (Pan and Zhang, 2018; Liu and Zhang, 2021).

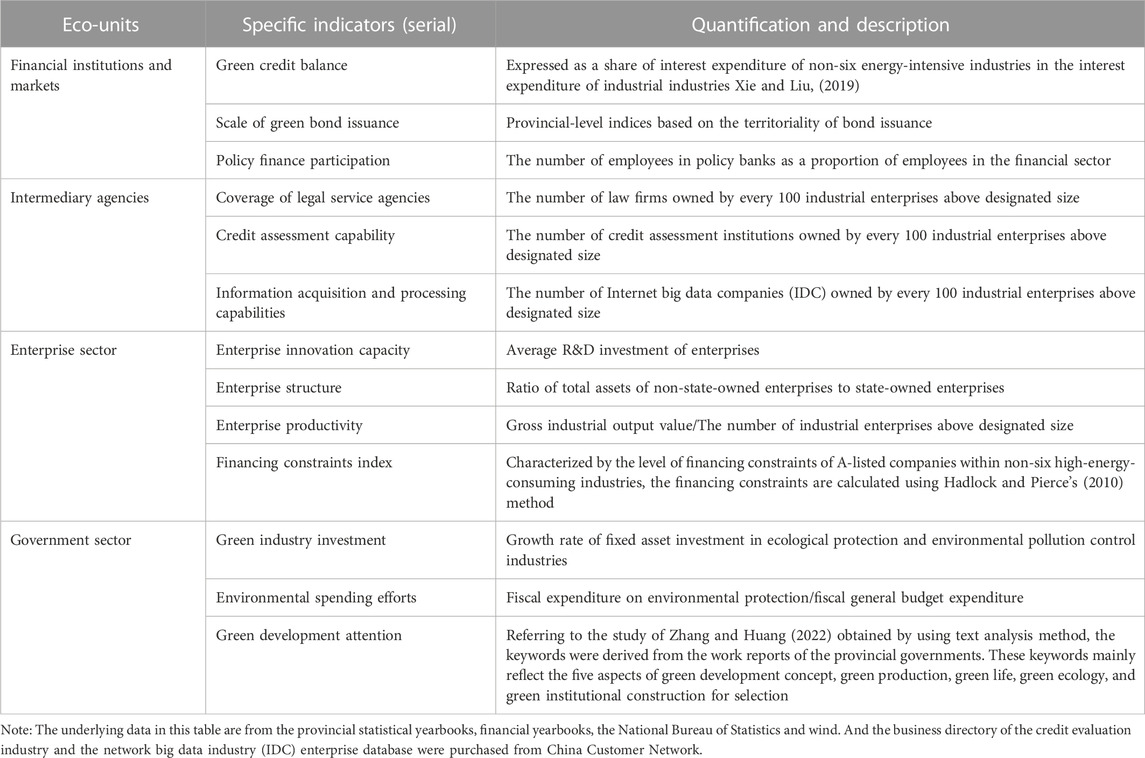

Based on the above description of the connotation, functions and components of green financial infrastructure, an evaluation indicator system is constructed here from the perspective of the four ecological units as shown in Table 1.

TABLE 1. Evaluation index system of the construction level of green financial infrastructure.

The specific measures of the level of green financial infrastructure in a region are as follows.

In the first step, the n sequences of the ith ecological unit are arranged in the order from smallest to largest and normalized as shown in Eq. 10.

where

In the second step, the orderedness (di) of the ith eco-unit is calculated and the formula is as follows.

where

Firstly, assuming that the number of sub-items of each sequence of the ith eco-unit (Bi) is n, the correlation coefficient matrix of each sequence sub-item of this eco-unit is as follows:

Secondly, the total influence degree (Ci) of the ith sequence sub-indicator on other sequence sub-indicators in this eco-unit is calculated, and the larger the value indicates the more important the sequence sub-indicator is in this eco-unit, and the calculation formula is as follows.

Finally, Ci is normalized to obtain the weights of each series sub-indicator, and the formula is calculated as follows.

In the third step, the green financial infrastructure ecosystem symbiosis (GFI) is calculated with the following equations.

where

Environmental regulation (ER) is a threshold variable. In this paper, the comprehensive index of environmental regulation intensity is calculated through three indicators: industrial wastewater emissions per unit of output value, industrial sulphur dioxide emissions per unit of output value and industrial soot emissions per unit of output value. The larger the index is, the more pollution is emitted and the weaker the intensity of environmental regulation (Dong and Wang, 2021; Wang and Huang, 2022). The specific measurement method of environmental regulation is as follows.

Firstly, industrial wastewater emissions per unit of output value, industrial sulfur dioxide emissions per unit of output value and industrial soot emissions per unit of output value are standardized in each province, as shown in Eq. 17.

Where

Where

In this paper, we consider other factors that affect the efficiency of regional carbon emissions and sets the following control variables. 1) Economic development level (EDL), measured as the logarithm of real GDP, which affects energy consumption and carbon intensity as resources are allocated on a larger scale with economic development (Ang, 2008). It should be noted that the real GDP adopts the real GDP (2008–2019) of Chen et al. (2022) based on the calibrated night light data, and uses the trend analysis method to calculate the data in 2020; 2) Population size (POP), which is represented by the logarithm of the resident population at the end of the year, generally, the expansion of the population size will increase the demand for energy consumption, thereby affecting the carbon emission intensity and efficiency (Sefeedpari et al., 2013); 3) The level of economic openness (OPEN), measured as the ratio of foreign direct investment to GDP, the Pollution Haven Hypothesis suggests that pollution-intensive industries tend to move to countries or regions with lower environmental standards, thus making the host country a pollution haven (Singhania and Saini, 2021; Ren et al., 2022b; Wang and Huang, 2022); 4) Industrial structure (INDS), measured by the ratio of secondary sector output to GDP, the secondary industry is the main source of carbon emissions in China (Li et al., 2017; Ma et al., 2020), and industrial restructuring can reflect the trend of energy intensity change (Wu et al., 2005; Xie and Liu, 2019); 5) Fiscal decentralization (FISD), measured as the ratio of fiscal expenditures to fiscal revenues, which facilitates local governments to take measures to improve the efficiency of carbon emissions according to their financial situation (Tufail et al., 2021); 6) Marketization level (MKTL), measured by the overall marketization index, affects the efficiency of resource allocation. And as marketization increases, the market share of resource-intensive industries and low value-added industries decreases, thus reducing carbon emissions (Wang and Huang, 2022).

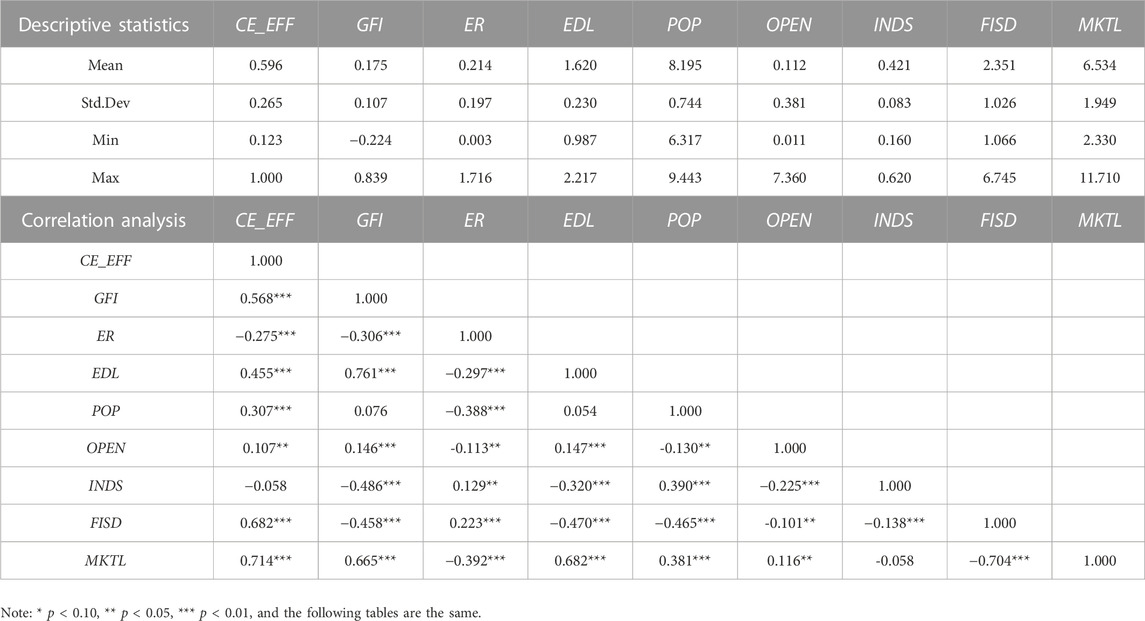

This article uses the panel data of 30 provinces in China (excluding Tibet, Hong Kong, Macau and Taiwan) from 2008 to 2020 as a sample. The data comes from the 2006 IPCC Guidelines for National Greenhouse Gas Inventories, China Energy Statistical Yearbook, Almanac of China’s Finance and Banking, China Statistical Yearbook, Marketization Index of China’s Provinces and The Statistical Yearbook of each province. In addition, the green credit data and the basic data for calculating the financing constraint index of enterprises are obtained from the Almanac of China’s Finance and Banking and also from Wind. Table 2 shows the results of descriptive statistics and correlation analysis of the variables.

TABLE 2. Descriptive statistics and correlation analysis of variables.

Focusing on the correlation test results shown in Table 2, the results show that the coefficient between the level of green financial infrastructure (GFI) and carbon emission efficiency (CE_EFF) is 0.568 and passes the 1% significance test, which means that there is a positive correlation between the two. The correlation coefficient between the threshold variable environmental regulation (ER) and carbon emission efficiency (CE_EFF) is significantly negative, indicating that the stronger the environmental regulation, the higher the carbon emission efficiency of the region. The correlation coefficients between the control variables and carbon emission efficiency were positive and passed the 1% or 5% significance level test, except for the correlation coefficient of industrial structure (INDS), which was not significant. Of course, this is only a preliminary interpretation, but it is necessary, and subsequently we will carve out the influence relationship between the variables through a rigorous econometric test. In addition, the results of the evaluation of the level of green financial infrastructure development show that only a very small number of regions show attenuation (just only 11 negative numbers in the results), so in order to present the empirical results in more detail, the negative indicators are replaced here with the positive value of the minimum value of the year in which the negative indicator is located, although the expressive statistics in Table 2 still report the original measured data.

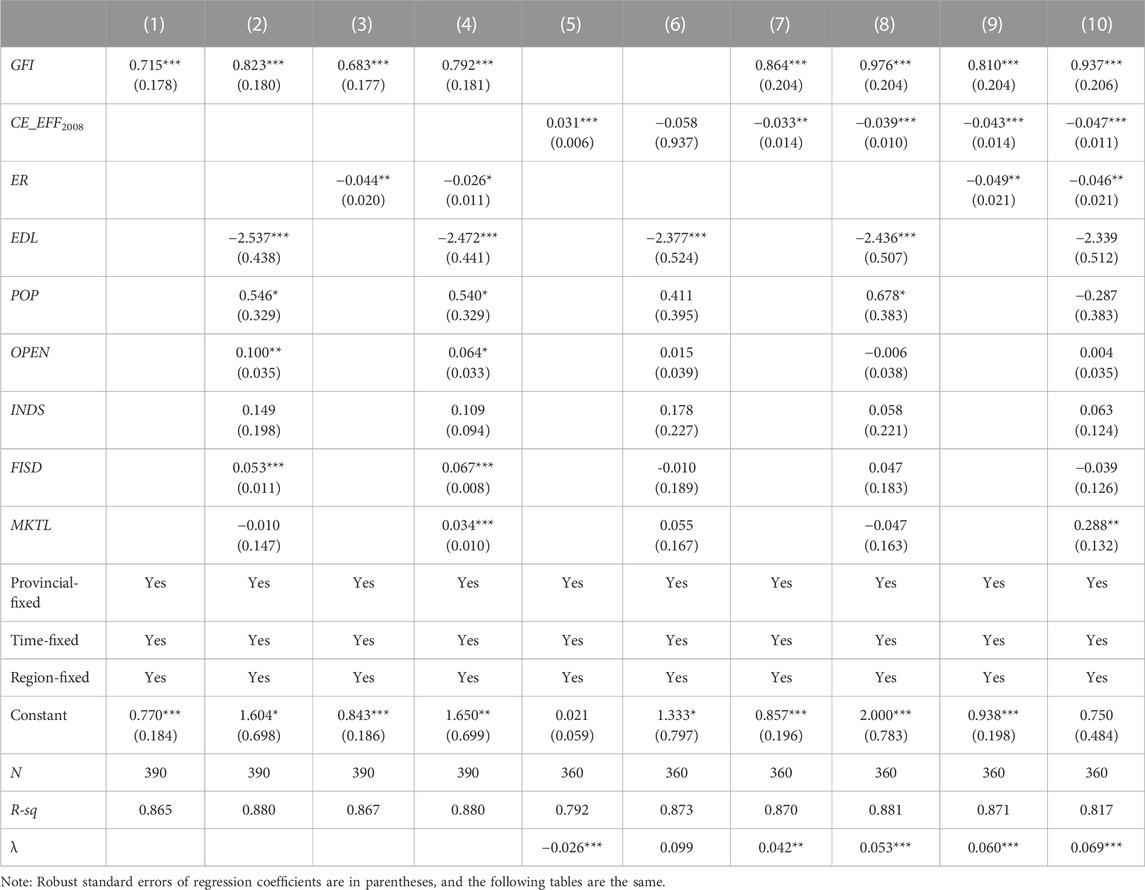

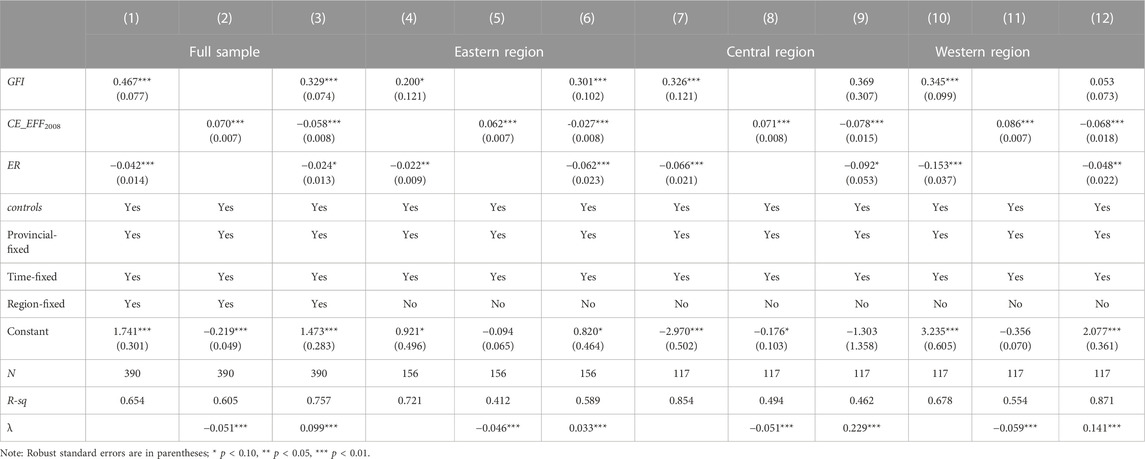

Columns (1)–(4) of Table 3 report the results of the baseline regression, with the econometric model shown in Eq. 1. Columns (1) and (2) examine the relationship between green financial infrastructure (GFI) and carbon emission efficiency (CE_EFF), where column (1) shows the measurement results without considering the control variables, and the coefficient of GFI is 0.715, which passes the 1% significance test; column (2) shows the measurement results after adding the control variables, and the coefficient of GFI is 0.823, which also passes the 1% significance test, and both results indicate that the improvement of the construction level of GFI can promote the improvement of CE_EFF. Columns (3)–(4) consider the effect of environmental regulation (ER) on the findings, and the results show that the relationship between GFI and CE_EFF remains unchanged with or without considering the effect of control variables, and all of them are significant positive promotion effects; meanwhile, the coefficient of ER is negative and passes the significance tests of 5% or 10%, respectively, indicating that the stronger the environmental regulation, the higher the efficiency of carbon emissions (note:environmental regulation is the inverse indicator).

TABLE 3. Results of baseline regression and convergence analysis.

Columns (5)–(10) of Table 3 focus on the effect of green financial infrastructure (GFI) to promote the convergence of carbon emission efficiency (CE_EFF), and the econometric model is shown in Eq. 2, and the coefficient of carbon emission efficiency in 2008 (CE_EFF 2008) is used to calculate the rate of convergence. First, columns (5) and (6) test the absolute convergence effect of carbon emission efficiency, where column (5) is the measurement result without considering the control variables, and the coefficient of CE_EFF2008 is 0.031, which passes the 1% significance test, according to which the absolute rate of convergence (λ) is calculated to be −0.026. This result indicates that it is difficult to promote the convergence development of carbon emission efficiency between different regions only by relying on the revised development of carbon emission efficiency in different regions; Column (6) considers the effect of control variables, and the coefficient of CE_EFF2008 is negative, but it does not pass the significance test, according to which the calculated convergence rate is 0.099, which still indicates that relying on the correction of carbon emission efficiency itself can hardly be to achieve the convergence development of regional carbon emission efficiency. Secondly, considering the relationship between GFI and CE_EFF in columns (9) and (10), the coefficients of GFI are 0.810 and 0.937 respectively, which both pass the 1% significance test and are consistent with the results of the above analysis, that is, the improvement of the level of green financial infrastructure helps to improve the carbon emission efficiency; meanwhile, the coefficients of CE_EFF2008 are also both significantly negative and the convergence rates (λ) obtained on this basis are 0.042 and 0.053, respectively, indicating that green financial infrastructure can significantly contribute to the convergence of carbon emission efficiency. Finally, considering the effect of ER on the convergence effect of CE_EFF, the results are presented in columns (9) and (10), with significantly negative coefficients for ER, significantly positive coefficients for GFI, and significantly negative coefficients for CE_EFF 2008, according to which the calculated convergence rate (λ) of CE_EFF are 0.060 and 0.069, which are slightly higher than the convergence speed considering only GFI, indicating that effective environmental regulation policies can curb the emission of pollutants, thereby improving carbon emission efficiency (the coefficient of GFI here is slightly higher than the coefficients in columns (7) and (8), and promote the convergence of regional carbon emissions efficiency.

The measurement results of other control variables are generally consistent with the descriptions in the variable selection section and will not be repeated here. In conclusion, the measurement results indicate that strengthening the construction of green financial infrastructure and increasing the intensity of environmental regulations can help promote the improvement and convergence of carbon emission efficiency.

In this paper, two methods are used to test the robustness of the baseline results and the convergence analysis findings. One is to replace the measures of the explanatory variables. Here, the non-radial directional distance function (NDDF) approach in the DEA framework is used to measure regional carbon emission efficiency, in line with Cheng et al. (2018); Meng and Zhang (2020), with the physical capital stock (K), the human capital stock (H) and the energy input (N) as input variables, and the output level (Y) and the carbon emissions (CE) are selected as desired and undesired output indicators. The second is to perform group regression from the three major regions in China to exclude the influence of regional heterogeneity on the robustness of the conclusions. The division of the three major regions here refers to the National Bureau of Statistics of the People’s Republic of China. And Table 4 presents the robustness test results.

TABLE 4. Results of the robustness test.

In Table 4, three sets of regression analyses are performed sequentially for both the full sample and the sub-regional sample. The first was to analyse the effect of GFI on CE_EFF, and the second was to analyse the absolute and relative effect of GFI on promoting the convergence of CE_EFF. For example, columns (1)–(3) present the results of robustness tests based on the full sample data, where column (1) describes the effect of GFI on CE_EFF, column (2) describes the absolute convergence effect of GFI contributing to CE_EFF, and column (3) describes the relative convergence effect of the GFI to promote CE_EFF, the measurement results are generally consistent with Table 3, that is, there is no absolute convergence in carbon emission efficiency. In generally, the results show that strengthen the construction of green financial infrastructure can promote the improvement and convergence of carbon emission efficiency. In addition, the results also show that the stronger the environmental regulation, the higher the carbon emission efficiency.

From the perspective of the measurement results of the three major regions, the GFI promotion effect on CE_EFF shows that the western region (0.345) > the central region (0.326) > the eastern region (0.200). However, from the perspective of the rate of GFI promotion of CE_EFF convergence (λ), the central region (0.229) > western region (0.141) > eastern region (0.033). The results of these two effects show that strengthening green financial infrastructure is more conducive to the greening transformation of the economy in the central and western regions. In this regard, we believe that the reason for the weak effect in the eastern region is mainly due to the relatively reasonable industrial structure, which is mainly dominated by light industry, manufacturing and services; while the central and western regions are relatively better endowed with resources and have more developed heavy industry and energy industries, so the effect of strengthening the construction of green financial infrastructure in the central and western regions is stronger in promoting the improvement of regional carbon emission efficiency.

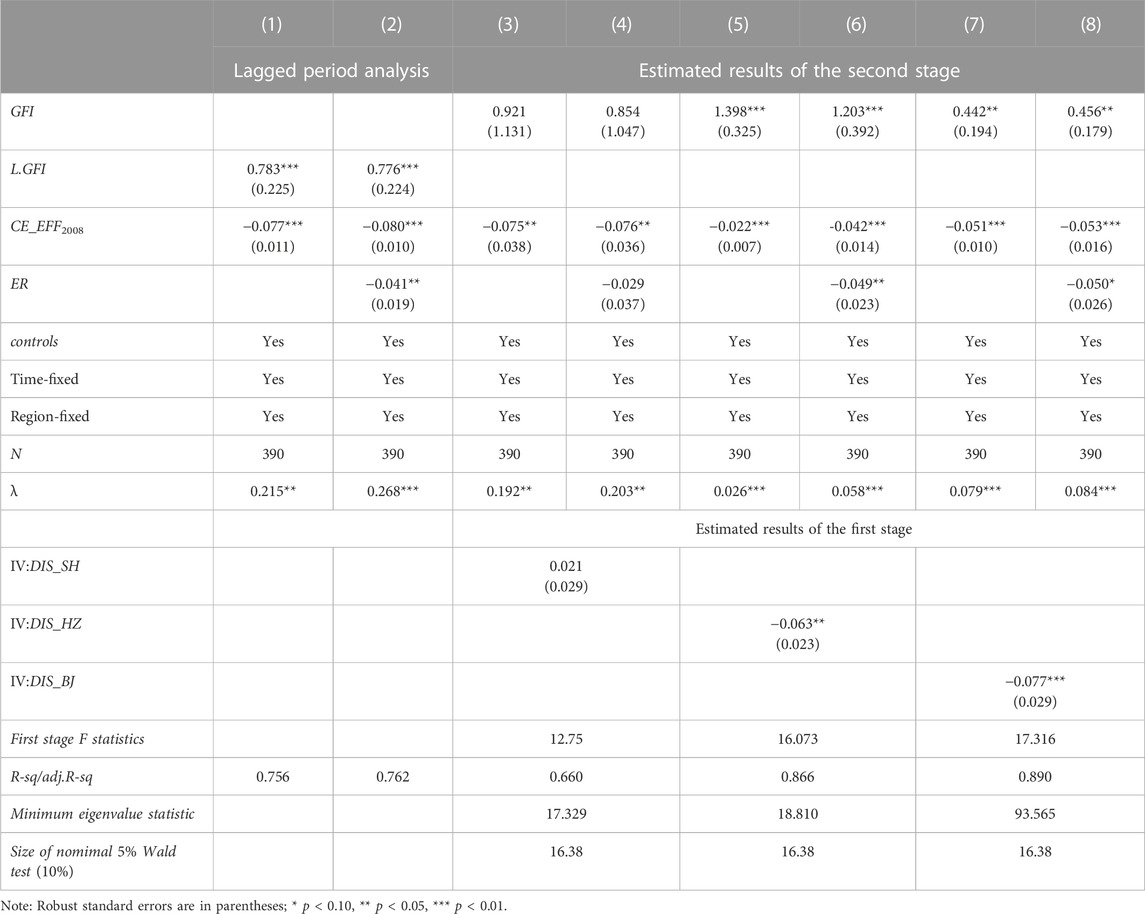

The above analysis shows that strengthen the construction of green financial infrastructure can promote the improvement and convergence of regional carbon emission efficiency, however, when the regional carbon emission efficiency is improved, correspondingly there will be a greater demand for green financial products, such as green credit and green investment, etc. Meanwhile, enterprises will also carry out green transformation by issuing green corporate bonds and other means of financing, thus forcing financial institutions to innovate green financial products and green financial service mode, thereby promoting the improvement of green financial infrastructure. In other words, there may be a reverse causal relationship between GFI and CE_EFF, thus creating an endogeneity problem. To this end, this paper adopts two approaches to alleviate the endogeneity problem: firstly, the GFI with a one-period lag (L.GFI) is used as a new explanatory variable for regression analysis; secondly, the IV-2sls was used, with the logarithm value of the road distance from provincial capitals to Shanghai (DIS_SH), Beijing (DIS_BJ) and to Hangzhou (DIS_HZ) being used as instrumental variables for the analysis. It should be noted that the selection of these three indicators as instrumental variables is mainly based on the results of the GFI measurement and the reality of China’s economic and financial development. Shanghai, as China’s financial centre, has a relatively high level of financial development; Hangzhou, as China’s financial technology centre, has an unparalleled advantage in terms of new technology application and diffusion; while Beijing, as China’s capital, has advantages in policy implementation and response. At the same time, the calculation results also show that Beijing, Shanghai and Zhejiang have higher levels of green finance development than other provinces. Of course, using regional distance as an instrumental variable not only satisfies the basic assumption of strict exogeneity, but also avoids the over-identification problem associated with too many instrumental variables. The empirical results are presented in Table 5.

TABLE 5. Empirical results of endogenous problem solving.

In Table 5, columns (1) and (2) report the results of the one-period lagged analysis of the explanatory variables, and the results show that the coefficients of L. GFI are positive and pass the significance test, regardless of whether the effect of environmental regulation is considered, indicating that strengthening green financial infrastructure can promote the improvement of regional carbon emission efficiency; the coefficient of ER in column (2) is -0.041 and passes the 5% significance test, indicating that strengthening environmental regulation and its binding force is conducive to the improvement of carbon emission efficiency; in addition, the coefficients of CE_EFF2008 are all negative and all pass the significance test, indicating that strengthening the construction of green financial infrastructure and environmental regulation can promote the convergence of regional carbon emission efficiency, and combining the coefficients of ER and L. GFI, it can be found that carbon emission efficiency has a convergence trend of positive improvement. Columns (3)–(8) show the measurement results of IV-2SLS, where columns (3) and (4) show the measurement results with the road distance from the provincial capital city to Shanghai (DIS_SH) as the instrumental variable, unfortunately, the measurement results do not support the above conclusion; columns 5) and 6), 7) and 8) report the measurement results with the distance from the provincial capital city to Hangzhou (DIS _HZ) and to Beijing (DIS_BJ) as instrumental variables, respectively, and the results well support the basic conclusions of the paper. Specifically, in the first stage of the test, the coefficients of DIS_HZ and DIS_BJ are −0.063 and −0.077, and they pass the 5% and 1% significance tests, respectively, indicating that the farther the provincial capital cities are from Hangzhou and Beijing, the lower the level of green financial infrastructure construction, which is in line with the reality of economic development; in the second stage of the test, regardless of whether the effect of environmental regulation is considered or not, the coefficients of GFI are positive, the coefficients of CE_EFF2008 and ER are negative, indicating that the better the green financial infrastructure and the higher the intensity of environmental regulation, the stronger the effect of promoting the improvement and convergence of carbon emission efficiency. A slight explanation of one phenomenon is needed here, that is, why the results with DIS_SH as the instrumental variable are insignificant, while the measured results with DIS_HZ as the instrumental variable are significant (the distance from Hangzhou to Shanghai is only 177 km)? We believe that the current green financial infrastructure is more reflected in the construction of technical level, and Hangzhou, as the financial technology center in China, has a pivotal position in the construction of technology-based green financial infrastructure, so it is more or less affected by the spillover effect of Hangzhou’s technology-based financial infrastructure construction in the improvement of green financial infrastructure in various regions.

In terms of the validity of the instrumental variables, the R2 in columns (5)–(8) are all greater than 0.6, indicating that the instrumental variables DIS_HZ and DIS_BJ both have strong explanatory strength for GFI; the F-statistic is also much greater than 10, while the value of the minimum characteristic statistic is also greater than the critical value corresponding to 10% in the Wald test (16.38), indicating that DIS_HZ and DIS_ BJ are not weak instrumental variables. In conclusion, the econometric results shown in Table 5 indicate that the benchmark findings remain robust after addressing the endogeneity issue.

In fact, carbon emission intensity and carbon emission efficiency are closely related to the intensity and effectiveness of environmental regulations, and also affects the effectiveness of green financial infrastructure to promote carbon emission efficiency. While environmental regulations promote energy conservation and low-carbon development of microeconomic agents, they also increase the costs of institutional compliance and pollution control, and as an external constraint, environmental regulations also affect the innovation of green financial products and instruments by financial institutions (Wang and Huang, 2022), so moderate environmental policy interventions are necessary and realistic. Then whether there is a reasonable interval for the intensity of environmental regulation and whether strengthening green financial infrastructure within this intensity interval can contribute to the improvement and convergence of carbon emission efficiency are analysed in this paper by means of a non-dynamic panel threshold model, and the econometric model is shown in Eq. 4. The empirical results are presented in Table 6.

TABLE 6. Empirical results of the threshold effect of environmental regulation.

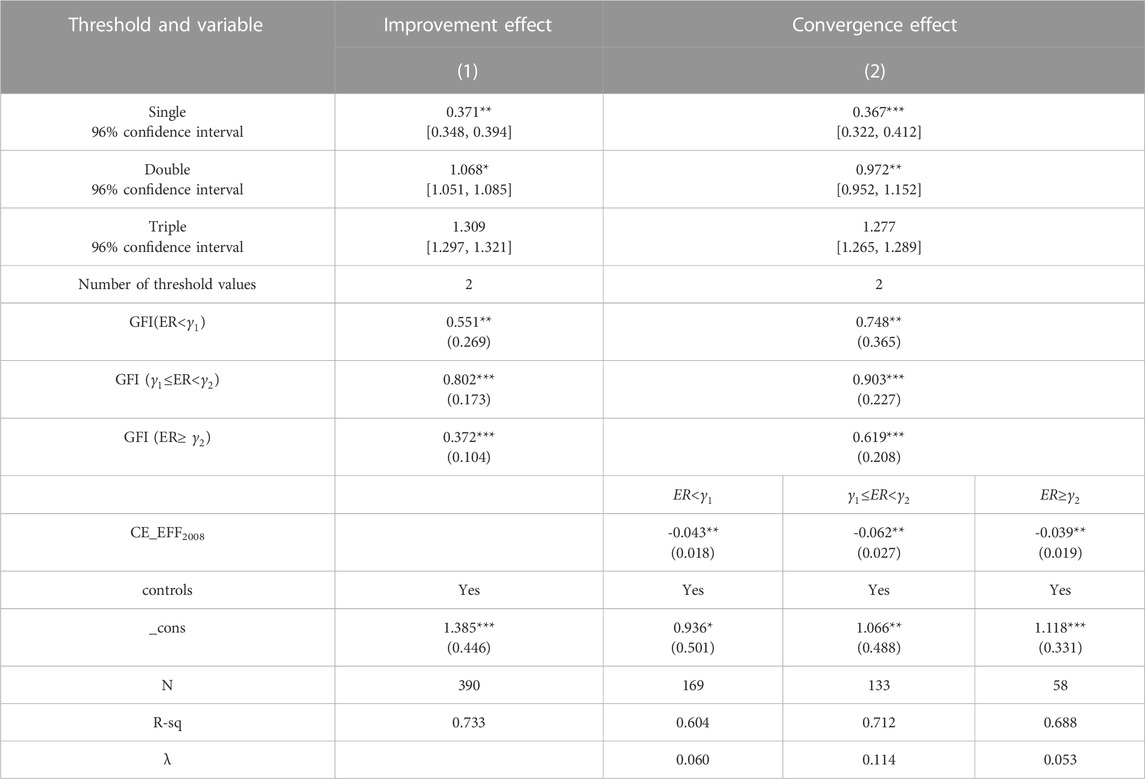

Column (1) of Table 6 reports the threshold effect of green financial infrastructure for carbon emission efficiency improvement influenced by environmental regulation. From the perspective of the threshold existence test results, environmental regulation (ER) has a double threshold with the threshold values of 0.371 and 1.068, which pass the significance tests of 5% and 10%, respectively, indicating that there is a threshold effect of environmental regulation on the impact of green financial infrastructure on carbon emission efficiency. Combined with the results of the threshold regression, it can be found that: when the intensity of environmental regulation is strong (ER < 0.371), the coefficient of GFI is 0.551, which passes the 5% significance level test; when the intensity of environmental regulation is moderate (0.371≦ER < 1.068), the coefficient of GFI is 0.802, which passes the 1% significance level test; when the intensity of environmental regulation is weak (ER≧1.068), the coefficient of GFI is 0.372, and it passes the 1% significance level test. The above results suggest that moderate environmental regulation is conducive to the role of green financial infrastructure in promoting carbon emission efficiency, that is, it is advisable to have too strong or too weak environmental regulation. The possible explanations for this are that when environmental regulations are too weak, environmental polluting firms do not care about the government’s punitive measures for polluting behaviors, so they will not take the initiative to choose more costly measures such as innovating production technology and improving clean production capacity, and therefore the carbon emission efficiency cannot be effectively improved; when environmental regulations are too strong, environmental polluting enterprises may have no incentive to produce, because the output of production may not be able to compensate for the environmental pollution penalty, thus causing the decrease of production efficiency, and of course the carbon emission efficiency can not be improved.

Column (2) of Table 6 reports the threshold effect of the green financial infrastructure for carbon efficiency convergence affected by environmental regulation, and the results again show that environmental regulation (ER) has a double threshold, with thresholds of 0.367 and 0.972, respectively. The focus here is on the coefficient of CE_EFF2008 and its corresponding rate of convergence: when environmental regulation is strong (ER < 0.367), moderate (0.367≦ER < 0.972) and weaker (ER≧0.972), the coefficients of the initial value of carbon emission efficiency (CE_EFF 2008) are -0.043, -0.062 and -0.039 respectively, and they all pass the 5% significance level test, from which the corresponding convergence rates are calculated to be 0.060, 0.114, and 0.053 respectively, this finding indicates that the effectiveness of green financial infrastructure in promoting convergence of carbon emission efficiency is affected by the strength of environmental regulation, and that either too strong or too weak environmental regulation is not conducive to the convergence of carbon emission efficiency.

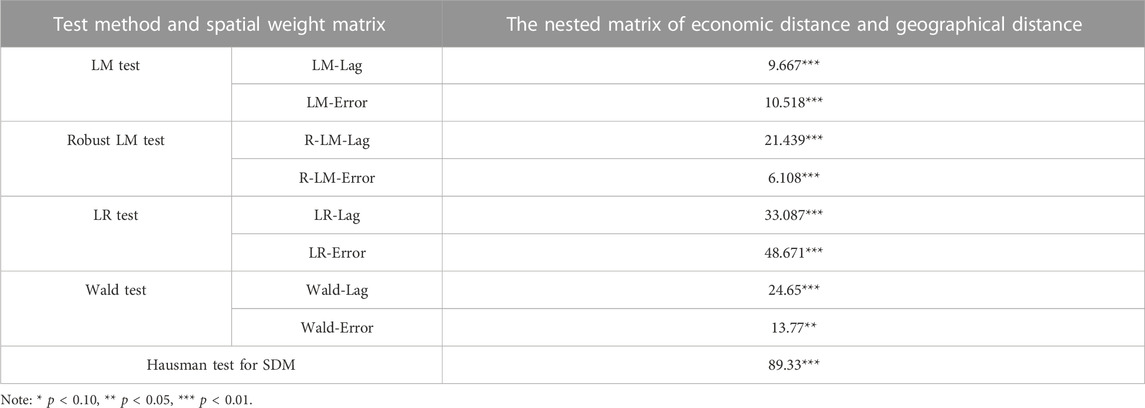

In order to more accurately analyze the effect of green financial infrastructure to promote carbon emission efficiency improvement and convergence, here we draw on the research idea of Zhang and Yue (2019) and follow the order of OLS-SEM (SLM)-SAR-SAC-SDM to select the optimal spatial econometric model. Here, two Lagrangian multipliers, LM-Error and LM-Lag, and their robust Lagrangian multipliers, R-LM-Lag and R-LM-Error, are used to test the four main spatial models, SEM, SAR, SAC and SDM, and the test results are presented in Table 7. The results show that the test values for LM-Error and LM-Lag both pass the significance test regardless of the spatial weight matrix, while R-LM-Error and R-LM-Lag also pass the significance test as well, indicating that there is not only a spatial lag effect for each variable, but also a spatial correlation for the error terms, tentatively indicating that the spatial Durbin model (SDM) should be used. The Wald spatial error test indicated that the choice of the SDM model was more reasonable compared with the SEM and SAR models. Aad the LR spatial error test values also all reject the original hypothesis that the spatial Durbin model should degenerate into a spatial lag model or a spatial error model at the 1% or 5% significance level, indicating that the SDM model has the best fitting effect. Finally, Hausman tests was conducted on the basis of the SDM model measurement, and the results all passed the significance test at the 1% level, indicating that there is significant heterogeneity among different regions, so the SDM model under fixed effects was chosen for estimation. The results of the spatial econometric analysis are presented in Table 8.

TABLE 7. Results of spatial regression optimal econometric model selection.

TABLE 8. Estimation results of the SDM model.

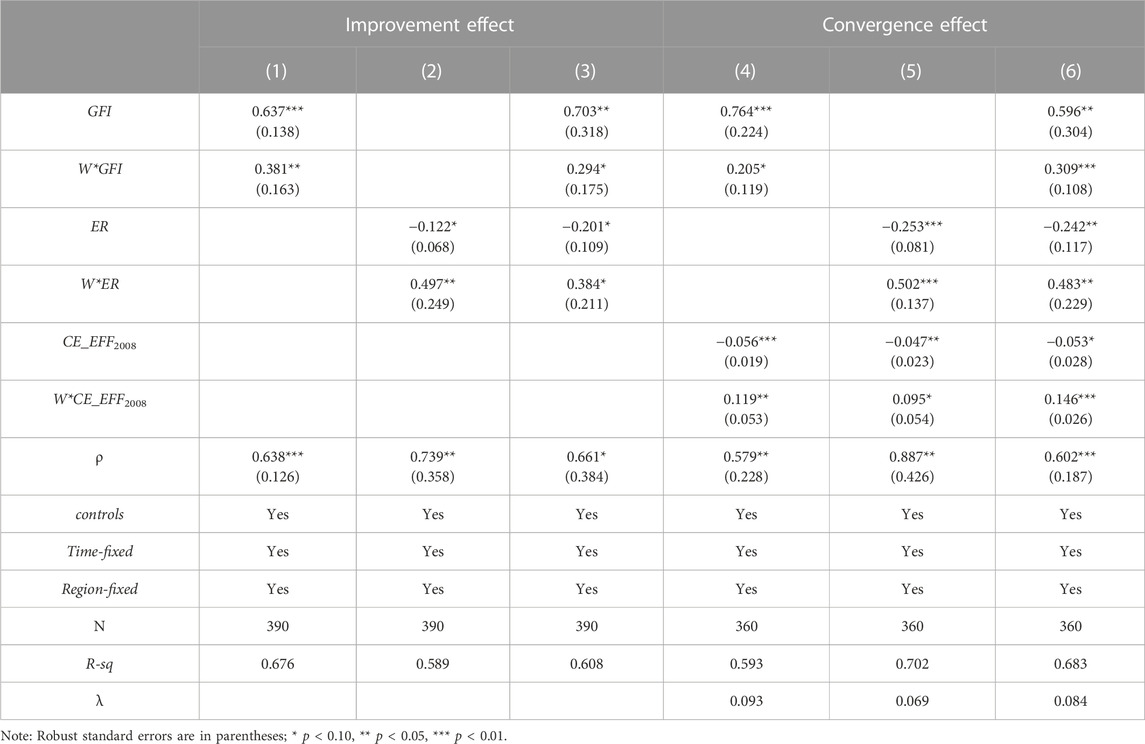

In Table 8, columns (1)–(3) analyse the spatial spillover effects of GFI for CE_EFF. The sign of the spatial autoregressive coefficient ρ is positive in all three regressions and passes the significance test, indicating that the improvement of carbon emission efficiency has a positive spatial spillover effect. The carbon emission efficiency of the local region further transmits or iterates to the carbon emission efficiency of the neighboring regions through the transmission mechanism, and it can also be said that the improvement of carbon emission efficiency of the neighboring regions can promote the improvement of carbon emission efficiency of the local region. The general regression coefficients and spatial regression coefficients of green financial infrastructure (GFI) are positive and both pass the significance test, indicating that strengthening the construction of green financial infrastructure can significantly contribute to the improvement of carbon emission efficiency, and also indicating that the carbon emission efficiency of the local region will be influenced by the level of green financial infrastructure construction in the neighboring regions. The general and spatial regression coefficients of ER in columns (2) and (3) are negative and both pass the 10% significance level test, indicating that improving the effectiveness of environmental regulations can promote the improvement of regional carbon efficiency, while the spatial regression coefficient of ER (which is significantly positive) indicates that there is a positive cross-fertilization effect of environmental regulations in the form of “neighbors as partners”. Columns (4)–(6) analyze the spatial spillover effects of green financial infrastructure (GFI) to promote the convergence of carbon emission efficiency. The coefficients of GFI and ER are basically the same as those in columns (1)–(3), that is, there is a spatial spillover effect of “neighbors as partners”. The coefficients of the initial values of carbon emission efficiency (CE_EFF 2008) are positive and all pass the significance test, and the corresponding convergence rates (λ) are positive, indicating that strengthening the construction of green financial infrastructure helps promote the convergence of carbon emission efficiency.

Based on the panel data of 30 provinces in China, this paper systematically measures the level of green financial infrastructure and carbon emission efficiency in each province, and on this basis, the impact of green financial infrastructure on carbon emission efficiency is investigated. Based on the benchmark regression model, this paper explores the non-linear influence relationship of green financial infrastructure on carbon emission efficiency using a non-dynamic panel threshold model, while focusing on the role of environmental regulation, and further analyzes the spatial spillover effects of strengthening the construction of green financial infrastructure in conjunction with the spatial Durbin model (SDM). The main conclusions are as follows: Firstly, green financial infrastructure can significantly improve carbon emission efficiency and promote the convergence of carbon emission efficiency, and the conclusion still holds after solving the endogenous problem and conducting a series of robustness tests. Secondly, the impact of green financial infrastructure on carbon emission efficiency is constrained by environmental regulation, and the effect of green financial infrastructure in promoting carbon emission efficiency improvement and convergence will be weakened when the intensity of environmental regulation is too large or too small, that is, only when the intensity of environmental regulation is in a moderate interval, can strengthening the construction of green financial infrastructure significantly promote carbon emission efficiency improvement and convergence. Finally, strengthening the construction of green financial infrastructure not only effectively promotes the improvement and convergence of carbon emission efficiency in the region but also in the surrounding areas, in other words, there is a spatial spillover effect of “neighbors as partners” on the impact of green financial infrastructure on carbon emission efficiency.

In summary, although green financial infrastructure can effectively promote the improvement and convergence of carbon emission efficiency, but the real implementation requires the joint promotion of the real economy sector, financial institutions and government policies. In view of this, this paper proposes the following recommendations: First, financial institutions should be fully encouraged to carry out green financial business, innovate green financial products, and participate in the construction and improvement of green financial system. There is no doubt that financial institutions occupy a dominant position in the green financial infrastructure: on the one hand, a sound green financial infrastructure can help the smooth development of green investment and financing projects, and strengthen the dynamic supervision mechanism afterwards; on the other hand, the government can enhance the participation enthusiasm of financial institutions by establishing risk guarantees and innovation incentives to help the low-carbon transformation of the real economy sector. Second, strengthen regional economic cooperation and give full play to the spatial spillover effect of green financial infrastructure. As mentioned in the empirical results, green financial infrastructure has the spatial spillover effect of “neighbors as partners”, so in view of this, through constructing green industry chains and green industry agglomerations to ensure the cross-regional flow of production factors such as human capital, financial resources and technological endowments, so as to promote inter-regional interconnection and complementary advantages, and realize the spatial spillover of green financial infrastructure’s carbon reduction effectiveness. Third, the government should implement environmental regulation policies according to local conditions. For example, to improve the collection, integration and disclosure of environmental protection data of the real economy by regulatory authorities, so as to provide a basis for the formulation of effective environmental regulation policies and green financial policies; and to establish an information sharing and communication mechanism between regulators and financial institutions, so as to better play the role of a bridge and supervisor of green financial infrastructure, thus promoting the exit and transformation of high-energy-consuming and high-polluting industries in an orderly manner and promoting low-carbon economic development.

The original contributions presented in the study are included in the article/Supplementary Materials, further inquiries can be directed to the corresponding author.

HZ: Software, writing, data curation, formal analysis, original draft preparation; JW: Variable design, theory and research hypothesis formulation, policy implications; ZX: Research guidance, framework design. All authors have read and agreed to the published version of the manuscript.

This work was supported in part by the Key Project of Philosophy and Social Science Research in Colleges and Universities in Anhui Province (Grant No. 2022AH051692), the Chaohu University High-level Talent Research Start-up Fund Project (Grant No. KYQD-202209).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Akalpler, E., and Hove, S. (2019). Carbon emissions, energy use, real GDP per capita and trade matrix in the Indian economy-an ARDL approach. Energy 168, 1081–1093. doi:10.1016/j.energy.2018.12.012

Al-mulali, U., and Sab, C. N. C. (2013). Energy consumption, pollution and economic development in 16 emerging countries. J. Econ. Stud. 40 (5), 686–698. doi:10.1108/JES-05-2012-0055

Amore, M. D., and Bennedsen, M. (2016). Corporate governance and green innovation. J. Environ. Econ. Manag. 75, 54–72. doi:10.1016/j.jeem.2015.11.003

Andersson, M., and Lööf, H. (2011). Agglomeration and productivity: Evidence from firm-level data. Ann. Reg. Sci. 46 (3), 601–620. doi:10.1007/s00168-009-0352-1

Ang, J. B. (2008). Economic development, pollutant emissions and energy consumption in Malaysia. J. Policy Model. 30 (2), 271–278. doi:10.1016/j.jpolmod.2007.04.010

Cao, J., Law, S. H., Samad, A. R. B. A., Mohamad, W. N. B. W., Wang, J., and Yang, X. (2022). Effect of financial development and technological innovation on green growth—analysis based on spatial Durbin model. J. Clean. Prod. 365, 132865. doi:10.1016/j.jclepro.2022.132865

Chen, J., Gao, M., Cheng, S., Hou, W., Song, M., Liu, X., et al. (2022). Global 1 km× 1 km gridded revised real gross domestic product and electricity consumption during 1992–2019 based on calibrated nighttime light data. Sci. Data. 9 (1), 202–214. doi:10.1038/s41597-022-01322-5

Chen, L., and Jia, G. (2017). Environmental efficiency analysis of China's regional industry: A data envelopment analysis (DEA) based approach. J. Clean. Prod. 142, 846–853. doi:10.1016/j.jclepro.2016.01.045

Chen, Z., Song, P., and Wang, B. (2021). Carbon emissions trading scheme, energy efficiency and rebound effect—evidence from China's provincial data. Energy Policy 157, 112507. doi:10.1016/j.enpol.2021.112507

Cheng, Z., Li, L., Liu, J., and Zhang, H. (2018). Total-factor carbon emission efficiency of China's provincial industrial sector and its dynamic evolution. Renew. Sust. Energy Rev. 94, 330–339. doi:10.1016/j.rser.2018.06.015

Dong, Z. Q., and Wang, H. (2021). Validation of market-based environmental policies: Empirical evidence from the perspective of carbon emission trading policies. Stat. Sci. 38 (10), 48–61. doi:10.19343/j.cnki.11-1302/c.2021.10.005

Falcone, P. M., and Sica, E. (2019). Assessing the opportunities and challenges of green finance in Italy: An analysis of the biomass production sector. Sustainability 11 (2), 517. doi:10.3390/su11020517

Gilchrist, D., Yu, J., and Zhong, R. (2021). The limits of green finance: A survey of literature in the context of green bonds and green loans. Sustainability 13 (2), 478. doi:10.3390/su13020478

Green, C. J., and Murinde, V. (2008). The impact of tax policy on corporate debt in a developing economy: A study of unquoted Indian companies. Eur. J. Financ. 14 (7), 583–607. doi:10.1080/13518470701705702

Guo, P., Hu, X., Zhao, S., and Li, M. (2022). The growth impact of infrastructure capital investment: The role of regional innovation capacity—evidence from China. Econ. Res.-Ekon. Istraz. 2022, 1–21. doi:10.1080/1331677X.2022.2142632

Hadlock, C. J., and Pierce, J. R. (2010). New evidence on measuring financial constraints: Moving beyond the KZ index. Rev. Financ. Stud. 23 (5), 1909–1940. doi:10.1093/rfs/hhq009

Hansen, B. E. (1999). Threshold effects in non-dynamic panels: Estimation, testing, and inference. J. Econ. 93 (2), 345–368. doi:10.1016/S0304-4076(99)00025-1

Hao, Y., Ba, N., Ren, S., and Wu, H. (2021). How does international technology spillover affect China's carbon emissions? A new perspective through intellectual property protection. Sustain. Prod. Consum. 25, 577–590. doi:10.1016/j.spc.2020.12.008

He, G., Wang, S., and Zhang, B. (2020). Watering down environmental regulation in China. Q. J. Econ. 135 (4), 2135–2185. doi:10.1093/qje/qjaa024

Hossain, M. (2018). “Green finance in Bangladesh: Policies, institutions, and challenges (No. 892),”. ADBI Working Paper (Tokyo: Asian Development Bank Institute -ADBI).

House, K. Z., Harvey, C. F., Aziz, M. J., and Schrag, D. P. (2009). The energy penalty of post-combustion CO2 capture & storage and its implications for retrofitting the US installed base. Energy Environ. Sci. 2 (2), 193–205. doi:10.1039/B811608C

Khan, K., and Su, C. W. (2021). Urbanization and carbon emissions: A panel threshold analysis. Environ. Sci. Pollut. Res. 28 (20), 26073–26081. doi:10.1007/s11356-021-12443-6

Lawless, M., O’Connell, B., and O’Toole, C. (2015). Financial structure and diversification of European firms. Appl. Econ. 47 (23), 2379–2398. doi:10.1080/00036846.2015.1005829

Levchenko, V., and Ostapenko, M. (2016). Information asymmetry on the market of non-banking financial services in Ukraine: Causes, consequences, methods of control. Public Munic. Finance 5 (1), 29–37. doi:10.21511/pmf.05(1).2016.04

Li, X., Cui, X., and Wang, M. (2017). Analysis of China’s carbon emissions base on carbon flow in four main sectors: 2000–2013. Sustainability 9 (4), 634. doi:10.3390/su9040634

Liu, L. Y. Q., and Zhang, Y. X. (2021). Research on regional sci-tech finance ecosystem symbiosis and its evolution. Sci. Technol. Prog. Policy. 38 (5), 48–58. doi:10.6049/kjjbydc.2020080136

Liu, J. Y., Xia, Y., Fan, Y., Lin, S. M., and Wu, J. (2017). Assessment of a green credit policy aimed at energy-intensive industries in China based on a financial CGE model. J. Clean. Prod. 163, 293–302. doi:10.1016/j.jclepro.2015.10.111

Liu, X., Wang, E., and Cai, D. (2019). Green credit policy, property rights and debt financing: Quasi-natural experimental evidence from China. Financ. Res. Lett. 29, 129–135. doi:10.1016/j.frl.2019.03.014

Liu, X., Zhang, W., Zhao, S., and Zhang, X. (2022). Green credit, environmentally induced R&D and low carbon transition: Evidence from China. Environ. Sci. Pollut. Res. 29 (59), 89132–89155. doi:10.1007/s11356-022-21941-0

Lu, Y., Zheng, H., Chand, S., Xia, W., Liu, Z., Xu, X., et al. (2022). Outlook on human-centric manufacturing towards Industry 5.0. J. Manuf. Syst. 62, 612–627. doi:10.1016/j.jmsy.2022.02.001

Ma, Y., Song, Z., Li, S., and Jiang, T. (2020). Dynamic evolution analysis of the factors driving the growth of energy-related CO2 emissions in China: An input-output analysis. Plos one 15 (12), e0243557. doi:10.1371/journal.pone.0243557

Mardani, A., Streimikiene, D., Balezentis, T., Saman, M. Z. M., Nor, K. M., and Khoshnava, S. M. (2018). Data envelopment analysis in energy and environmental economics: An overview of the state-of-the-art and recent development trends. Energies 11 (8), 2002. doi:10.3390/en11082002

Martin, B. D., and Schwab, E. (2013). Current usage of symbiosis and associated terminology. Int. J. Biol. 5 (1), 32. doi:10.5539/ijb.v5n1p32

Meng, W. S., and Zhang, Y. (2020). Natural resource endowment, path selection of technological progress, and green economic growth: An empirical research based on China’s provincial panel data. Resour. Sci. 42 (12), 2314–2327. doi:10.18402/resci.2020.12.05

Niu, H. P., Zhang, X. Y., and Zhang, P. D. (2020). Institutional change and effect evaluation of green finance policy in China: Evidence from green credit policy. Manag. Rev. 32 (8), 3–12. doi:10.14120/j.cnki.cn11-5057/f.2020.08.001

Pan, J., and Zhang, Y. X. (2018). The regional S&T innovation performance of government, enterprises and financial institutions of S&T investment. Stud. Sci. Sci. 36 (5), 831–838+846. doi:10.16192/j.cnki.1003-2053.2018.05.008

Park, H., and Kim, J. D. (2020). Transition towards green banking: Role of financial regulators and financial institutions. Asian J. sustain. Soc. Responsib. 5 (1), 5–25. doi:10.1186/s41180-020-00034-3

Peng, J., Song, Y., Tu, G., and Liu, Y. (2021). A study of the dual-target corporate environmental behavior (DTCEB) of heavily polluting enterprises under different environment regulations: Green innovation vs. pollutant emissions. J. Clean. Prod. 297, 126602. doi:10.1016/j.jclepro.2021.126602

Purves, N., Niblock, S. J., and Sloan, K. (2015). On the relationship between financial and non-financial factors: A case study analysis of financial failure predictors of agribusiness firms in Australia. Agr. Financ. Rev. 75 (2), 282–300. doi:10.1108/AFR-04-2014-0007

Ren, S., Hao, Y., and Wu, H. (2022a). How does green investment affect environmental pollution? Evidence from China. Environ. Resour. Econ. 81 (1), 25–51. doi:10.1007/s10640-021-00615-4

Ren, S., Hao, Y., and Wu, H. (2022b). The role of outward foreign direct investment (OFDI) on green total factor energy efficiency: Does institutional quality matters? Evidence from China. Resour. Policy. 76, 102587. doi:10.1016/j.resourpol.2022.102587

Sarkodie, S. A., and Strezov, V. (2019). Effect of foreign direct investments, economic development and energy consumption on greenhouse gas emissions in developing countries. Sci. Total Environ. 646, 862–871. doi:10.1016/j.scitotenv.2018.07.365

Sefeedpari, P., Ghahderijani, M., and Pishgar-Komleh, S. H. (2013). Assessment the effect of wheat farm sizes on energy consumption and CO2 emission. J. Renew. Sustain. Ener. 5 (2), 023131. doi:10.1063/1.4800207

Shao, S., Fan, M. T., and Yang, L. L. (2022). Economic restructuring, green technical progress, and low-carbon transition development in China: An empirical investigation based on the overall technology frontier and spatial spillover effect. Manag. World 38, 46–69. doi:10.19744/j.cnki.11-1235/f.2022.0031

Singhania, M., and Saini, N. (2021). Demystifying pollution haven hypothesis: Role of FDI. J. Bus. Res. 123, 516–528. doi:10.1016/j.jbusres.2020.10.007

Soni, S., Subrahmanya, M. B., and Bhattacharya, P. (2019). Real capital stock estimation for industries using perpetual inventory method: A methodological exploration. Indian Econ. J. 67 (1-2), 82–98. doi:10.1177/0019466220938009

Tone, K. (2001). A slacks-based measure of efficiency in data envelopment analysis. Eur. J. Oper. Res. 130 (3), 498–509. doi:10.1016/S0377-2217(99)00407-5

Tufail, M., Song, L., Adebayo, T. S., Kirikkaleli, D., and Khan, S. (2021). Do fiscal decentralization and natural resources rent curb carbon emissions? Evidence from developed countries. Environ. Sci. Pollut. Res. 28 (35), 49179–49190. doi:10.1007/s11356-021-13865-y

Verhoef, E. T., and Nijkamp, P. (2002). Externalities in urban sustainability: Environmental versus localization-type agglomeration externalities in a general spatial equilibrium model of a single-sector monocentric industrial city. Ecol. Econ. 40 (2), 157–179. doi:10.1016/S0921-8009(01)00253-1

Wang, J. T., and Huang, H. (2022). Research on the impact of green credit on carbon emissions: Empirical analysis based on PSTR model and SDM model. Contemp. Econ. Manag. 44 (9), 80–90. doi:10.13253/j.cnki.ddjjgl.2022.09.011

Wang, M., Li, Y., and Liao, G. (2021). Research on the impact of green technology innovation on energy total factor productivity, based on provincial data of China. Front. Environ. Sci. 9, 710931. doi:10.3389/fenvs.2021.710931

Wang, X., and Wang, Y. (2021). Research on the green innovation promoted by green credit policies. Manag. World. 37 (6), 173–188. doi:10.19744/j.cnki.11-1235/f.2021.0085

Wu, L., Kaneko, S., and Matsuoka, S. (2005). Driving forces behind the stagnancy of China’s energy-related CO2 emissions from 1996 to 1999: The relative importance of structural change, intensity change and scale change. Energy policy 33 (3), 319–335. doi:10.1016/j.enpol.2003.08.003

Xie, T., and Liu, J. (2019). How does green credit affect China’s green economy growth. Chin. J. Popul. Resour. Environ. 29 (9), 83–90. doi:10.12062/cpre.20190501

Yang, X., Su, X., Ran, Q., Ren, S., Chen, B., Wang, W., et al. (2022b). Assessing the impact of energy internet and energy misallocation on carbon emissions: New insights from China. Environ. Sci. Pollut. Res. 29 (16), 23436–23460. doi:10.1007/s11356-021-17217-8

Yang, X., Wang, W., Wu, H., Wang, J., Ran, Q., and Ren, S. (2022a). The impact of the new energy demonstration city policy on the green total factor productivity of resource-based cities: Empirical evidence from a quasi-natural experiment in China. J. Environ. Plan. Manag. 66 (2), 293–326. doi:10.1080/09640568.2021.1988529