Yiming Kuang1

Yiming Kuang1 Min Fan

Min Fan Yaojun Fan

Yaojun Fan

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 20 March 2023

Sec. Environmental Economics and Management

Volume 11 - 2023 | https://doi.org/10.3389/fenvs.2023.1090537

This article is part of the Research TopicSustainable Economic Growth, Green Deal and Macroeconomic Recovery – Most Suitable Pathways to Recovering From the Actual Evolutionary HiatusView all 14 articles

The development of low-level digital technology and communication technology such as “huge wisdom moving cloud” has driven the rise of digital economy, and various fields of social economy have gradually realized deep integration with digital technology. From the micro level of enterprises, digitalization transforms business activities such as research and development, production, supply chain and sales, and forms new data resources to help enterprises achieve lean management through data integration and analysis. To investigate whether digitalization ultimately affects firm performance, this study conducted theoretical discussions, selected Chinese listed companies to study, and empirically tested the relationship. Research has found that digitisation does boost corporate performance. After the robustness test, the conclusion remains the same. To deepen the understanding of the impact of digitalization on corporate performance, a mechanism analysis is also performed in this study. We found that digitization improves corporate performance by improving corporate innovation. In addition, we carried out an applicability analysis. We find that digitalization has a greater impact on firm performance in non-state-owned enterprises and those whose executives have an information technology background. Finally, by means of the economic consequences test, we find that the improvement in corporate performance caused by the growth of the digital hierarchy improves the corporate debt structure in the future. The findings of this study enrich theories related to digitalization and improve empirical evidence for the positive externalities of digitalization.

Since the 1990s, the rapid development of the Internet and other digital technologies has brought fresh opportunities for businesses. As micro subjects of economic development, digital transformation of enterprises is the basis for sustainable development of the digital economy (Zhong Yuehua et al., 2022). Enterprises need to actively or passively take full advantage of the opportunities brought by digital technologies to realize business processes (LI et al., 2018), business models (MUBARAK et al., 2020), overseas investment (Hu Yang et al., 2022; Huang and Huang, 2018), financial performance (He Fan, Liu Hongxia, 2019), culture and customer experience (GUENZI et al., 2020) and other aspects of value creation (Wang Haihua et al., 2022). According to the White Paper on Global Digital Economy -- A New Dawn of Recovery under the Impact of COVID-19, released by the China Academy of Information and Communications Technology at the 2021 Global Digital Economy Conference, the scale of China’s digital economy is about 5.4 trillion United States dollars, ranking the second in the world in terms of total volume and the first in terms of year-on-year growth. The digital economy has become a new driving force for China’s economic growth.

Digital technology has considerably changed the ecological environment for the survival and development of enterprises, reshaped their business models, and exerted a profound impact on various fields of enterprise operation and management (Li Lei et al., 2022). Through the introduction of digital technology, enterprises have realized the digitalization of production, management and sales at various levels, enhanced their competitiveness, and realized the strategic behavior of short-term and long-term profit increment (Vial, 2019; Verhoef et al., 2021; Hu et al, 2022). The existing literature shows that the impact of digitalization on enterprises is comprehensive and fundamental, and enterprise digitalization is not a choice of whether they are willing or not, but a mandatory task that must be completed (Lu and Lu, 2022). On the one hand, thanks to cloud computing and related auxiliary digital technologies, enterprises can rapidly gather enormous user data at low cost and in multiple dimensions, which improves the immediate response of organizations to market demands (Liu Zheng et al., 2020). On the other hand, digital technology is also a means of organization and management (Goldfarb and Tucker, 2019), which can help enterprises enhance coordination ability and improve supervision efficiency (Brynjolfsson and Mc Elheran, 2016). Digital technology is also a means of organization and management (Goldfarb and Tucker, 2019), which can help enterprises improve coordination ability and supervision efficiency (Brynjolfsson and Mc Elheran, 2016). In recent years, some literature has begun to recognize that corporate digital transformation is not only an application of digital technologies, but also a process of organizational change. That is, the process in which enterprises apply digital technologies such as the Internet of Things, big data and artificial intelligence to process, product and service innovation and promote the restructuring and transformation of enterprise production mode (Lee et al., 2015). Gregory et al. (2019) believe that in this process, enterprises alter the path of value creation through the application of digital technology, so as to improve their internal operating efficiency and organizational performance.

Enterprise performance is an essential indicator to reflect the operating conditions of enterprises in a certain period, and occupies an influential position in the evaluation of enterprise performance (Wang Wenhua et al., 2022). The pursuit of superior performance is a corporate goal. Therefore, it is of practical interest to study the impact of digitalization on corporate performance. The existing literature has made some useful explorations on the relationship between digitization and firm performance. According to some academics, digitalization has done little to improve corporate performance. They believe that when large data is not compatible with the key structure of an organization, digital technology is difficult to create value (Forman and Mc Elheran, 2019), and even causes the “IT efficiency paradox”. Another part of scholars believe that IT technology can improve enterprise performance by helping enterprises rationally plan production, quickly respond to consumer demands, and increase organizational flexibility and agility (Mikalefe et al., 2017; Qi Yudong et al., 2020). In addition, digitization can optimize internal and external communication and indirectly improve corporate performance (Alberto et al., 2013). Ferreira et al. (2019), using data from a telephone survey of 938 Portuguese companies, empirically found that the adoption of digital production processes was conducive to the introduction of different products (services). Loebbecke et al. (2015) found that the application of digital technology can influence enterprises to realize innovation transformation behavior under the original R&D innovation, generally improve operational efficiency, reduce operating costs and enhance customer experience, so as to obtain more output performance.

Although several existing studies have explored the relationship between digitization and firm performance, no consensus has been reached. In order to explore the critical factors that drive business performance improvement and provide some insights into the promotion of business digitalization, this study conducted theoretical analysis and empirical tests on the impact of digitalization on business performance. In contrast to existing studies, this study incorporates financing constraints into the research system and analyzes the moderating role of financing constraints in the digital impact on corporate performance. Moreover, based on the existing literature, we also extend the analysis of the specific mechanisms of digitalization affecting the performance of enterprises. Another contribution of this study is an empirical analysis of the economic consequences of digitalization on firm performance.

Digitization refers to the process of applying information technology to enterprise production. Digitization can use the current generation of information technology to promote industrial reform, improve the operation efficiency of the industry and build a different economic system (Li Jinyue et al., 2022). With the increasing pressure of resources and environment, the rise of labor costs and the intensification of industry competition, only by further accelerating the construction of digital infrastructure and increasing investment in digital technology can traditional enterprises gain the upper hand in the swift-moving digital trend (Liu Donghui et al., 2022). According to the resource arrangement theory, in the process of digital transformation, enterprises can optimize the allocation of internal resources, improve the productivity of enterprises and improve the performance of enterprises by relying on their own innovation and information acquisition advantages and coordinating various resources (Li Tang et al., 2020). With the development of digitalization, digital transformation has been gradually internalized and integrated into the whole process of daily operation and decision-making of enterprises (GOLDFARB ET AL., 2019). From the perspective of an enterprise, it is clear that the initiatives, capabilities and outcomes of a company’s digital transformation will also influence the degree of digitalization of an enterprise and its subsequent performance. Enterprises tend to start from the inside in digital transformation, aiming to improve their efficiency from the inside first (Chi Maomao et al., 2022), which is bound to be closely related to the promotion of enterprise innovation.

In conclusion, we propose research hypothesis H1:

Hypothesis 1: Digitization helps improve enterprise performance.

Digital transformation integrates scattered information and resources of enterprises, optimizes the connection between supply and demand (LIU et al., 2011), and enables enterprises to achieve higher marginal innovation output (Pan and Gao, 2022). Digital technology of information collection, analysis, processing and feedback is quick, comprehensive, thorough and credible, overflow and low cost, etc., characteristics, guide the enterprises around the key production elements configuration data resources, help to improve enterprise innovation ability, absorption capacity and the ability to adapt, to form a new innovation model (WenHu Hui and sheng-yun wang, 2021) and promoting breakthrough innovation (Jichang Zhang and Jing Long, 2021). Digitalization has changed the traditional pattern of technological innovation in enterprises, bringing convenience advantages to enterprises in information and communication, and enhanced connectivity between enterprises and government departments, scientific research institutions, enterprises in various industries and users. Through this connection, enterprises can pool knowledge from different fields and explore the potential of cross-border innovation (Bai Fuping et al., 2022). The integration of digital technology and production and manufacturing links promotes the formation of an efficient community of people, machines and products in the production process, improves the precision of production process and reduces the difficulty of enterprise process innovation, thus affecting the innovation willingness of enterprises (Zhang Longpeng et al., 2016). When the level of innovation in a business continues to improve, the performance of the business also improves. Technological innovation of enterprises can regularly bring iteration of production process and update of production technology, thus reducing production costs and improving profits of enterprises (Yao Juan et al., 2022). Technological innovation can also help enterprises obtain key resources from social forces for subsequent transformation of technological innovation achievements (Cheng Hong et al., 2016), thus creating competitive advantages for enterprises and improving corporate performance. In addition, large-scale production brought by enterprise innovation enables enterprises to obtain scale effect, which further enables enterprises to obtain certain monopoly profits or excess profits (Duan Haiyan and Tian Yaxing, 2021). As a result, corporate innovation drives corporate performance improvement.

In summary, we believe that enterprise innovation is the intermediary variable of digitalization affecting enterprise performance, so we propose the research hypothesis H2:

Hypothesis 2: Digitization can improve corporate performance by influencing corporate innovation.

Financing constraints are a worldwide problem affecting all aspects of business development. Therefore, it is necessary to incorporate financing constraints into the research regime on the impact of digitalization on corporate performance. The existing literature provides an in-depth analysis of the causes and effects of corporate financing constraints. The financing channels for enterprises mainly include internal financing and external financing. Internal financing is mainly based on an enterprise’s own internal surplus, while external financing mainly raises funds from financial institutions, individuals or institutional investors (Du Qianqian and Li Qiqi, 2022). Financing constraints are mainly influenced by factors such as scale and age, political association of enterprises, financial ecological environment, financial development level, relationship between government and market, etc., (Gu Leilei et al., 2018). When times are good, it will be easier for companies to get funding. When enterprises are faced with large financing constraints, they are commonly unable to timely and effectively raise funds for their potential investment projects, so they have to give up some excellent investment opportunities, including mergers and acquisitions (Pan Hongbo et al., 2022; lingling Zhai and Yuhui Wu, 2021; Blouin et al., 2021). Some scholars believe that financing constraints restrict the growth of enterprises, increase the probability of bankruptcy due to the rupture of capital (Musso et al., 2008), and reduce corporate performance and total factor productivity (Hu Xiaoping, 2021; Hua Junguo et al., 2022).

Financing constraints affect not only corporate performance but also corporate innovation. When financing constraints exist, enterprises will reduce the investment of R&D funds, thus inhibiting the improvement of innovation performance (Chen Jingpu and Hu Bo, 2020). Enterprises with severe financing constraints may have R&D projects with broad development prospects, but because of the risk and information asymmetry, the R&D activities of enterprises are stagnant, and the innovation and R&D of enterprises cannot be carried out (Ren Yuxin et al., 2022). As a result, financing constraints, as well as the pressure on the financing environment faced by enterprises, have weakened the boost to business performance from digitalization.

In summary, we believe that financing constraints can play a moderating role in the process of digital impact on enterprise performance, so the research hypothesis H3 is proposed:

Hypothesis 3: When financing constraints are more serious, digitalization plays a smaller role in improving corporate performance.

To test the theoretical hypothesis, we use data from 2011 to 2019 for A-share listed companies in mainland China to validate the relationship between digitalization and corporate performance. Given the difficulty of obtaining complete data for non-listed companies, and the advantages of public companies in terms of digitalization and service, as well as transparent data information, public companies were chosen for this study. In addition, given the particularity of financial companies, we also excluded listed companies in the financial sector. According to the following conditions: 1) Remove the samples of ST, *ST and PT; 2) Remove financial and insurance samples; 3) Eliminate the missing observed values of main research variables; 4) Shrinktail treatment for continuous variables. We end up with 19,021 sample observations. All data was collected from the CSMRA and CNRDS databases and processed using STATA 17.0.

Drawing on previous studies and considering the possible influence of company and year factors on regression results, we construct the following model (1) to test the relationship between digitalization and enterprise performance.

In Formula 1, subscript i is the enterprise and t is the year. The explained variable roa is enterprise performance, the core explanatory variable dig is digitization, and X is control variable. Φ is firm fixed effect, ω is time fixed effect.

In order to test the moderating effect of financing constraints on digitization and firm performance, the cross between dig and SA index (dig*SA) was added on the basis of model (1). The explained variables and control variables were the same as above. The specific model is as follows:

Referring to the research of Wang Wenhua et al. (2022), we use return on total assets (roa) as a measurement index of corporate performance. Because the return on assets can be a comprehensive measure of the enterprise’s asset turnover, sales profit rate and equity multiplier. The higher the return on assets, the higher the corporate performance. In addition, earnings per share (pro) is also used for stability test.

The importance an enterprise attaches to a particular strategic orientation can frequently be reflected by the frequency of keywords involved in the strategy appearing in the annual report (Wang Hongming et al., 2022). Referring to the existing research, we use Python to crawl and collate the annual reports of Shanghai and Shenzhen A-share listed companies, and extract the keywords of digitization (dig) by Jieba function. On this basis, the 30 words before and after the corresponding keywords are further extracted, and the negative expressions of “no”, “no” and additional words before the keywords are eliminated. Finally, the two kinds of word frequency are added together to get the total word frequency (Wu Fei et al., 2021). According to Wang Hongming et al. (2022), considering the obvious right-bias characteristics of such data, this study processed them logarithmically.

Following the theoretical analysis, we choose the financing constraint as the regulatory variable. Referring to the research of Ju Xiaosheng et al. (2013), we adopted the SA index as the measurement index of financing constraint (SA). Where, SA = −0.737 × SI + 0.043 × SI2-0.040 × A, SI is the natural logarithm of the total assets of the enterprise, A is the years of listing of the enterprise, SA is negative. Take the absolute value of SA. If the absolute value is larger, the financing constraint is larger.

According to the theoretical analysis, we choose enterprise innovation as the intermediary variable. For the measurement of enterprise innovation, we choose the logarithm of total patent application plus 1 to measure enterprise innovation (rd).

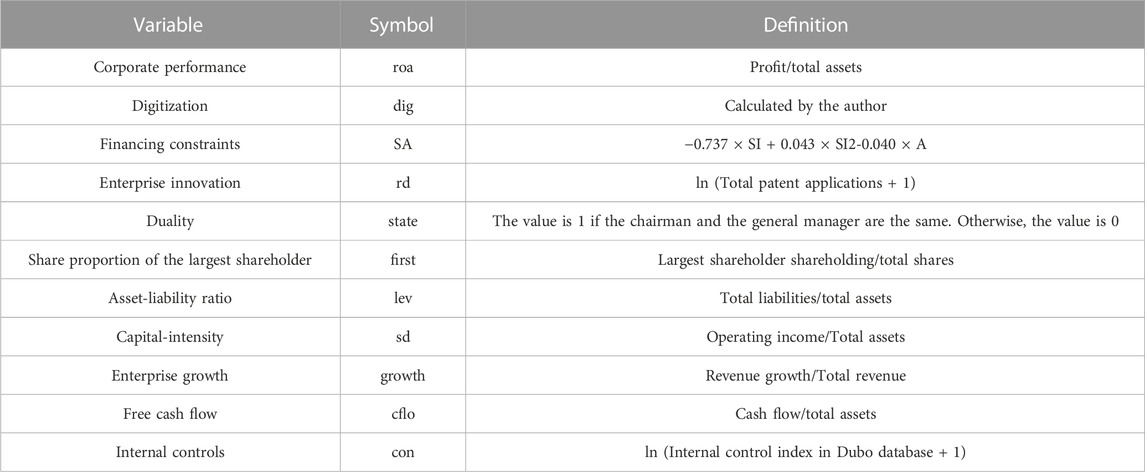

Drawing on existing literature (Pan Rongrong et al., 2022; Wang Wenhua et al., 2022), To eliminate the influence of heterogeneous factors on enterprise performance, we chose company-level factors such as state, shareholding ratio of the largest shareholder (first), asset-liability ratio (lev), capital intensity (sd), corporate growth, free cash flow (cflo), internal control (con) as the control variables of the model. See Table 1 for a table of variable definitions.

TABLE 1. Variable definition table.

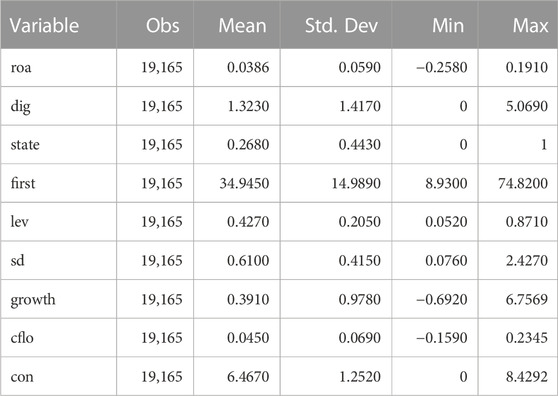

Table 2 lists the descriptive statistical results for the main variables. The mean value and standard deviation of business performance (roa) are 0.0386 and 0.0590. The mean value of digitization (dig) is 1.3230, the maximum value is 5.0690, and the minimum value is 0, indicating that there are great differences in digitization level among Chinese enterprises.

TABLE 2. Descriptive statistics.

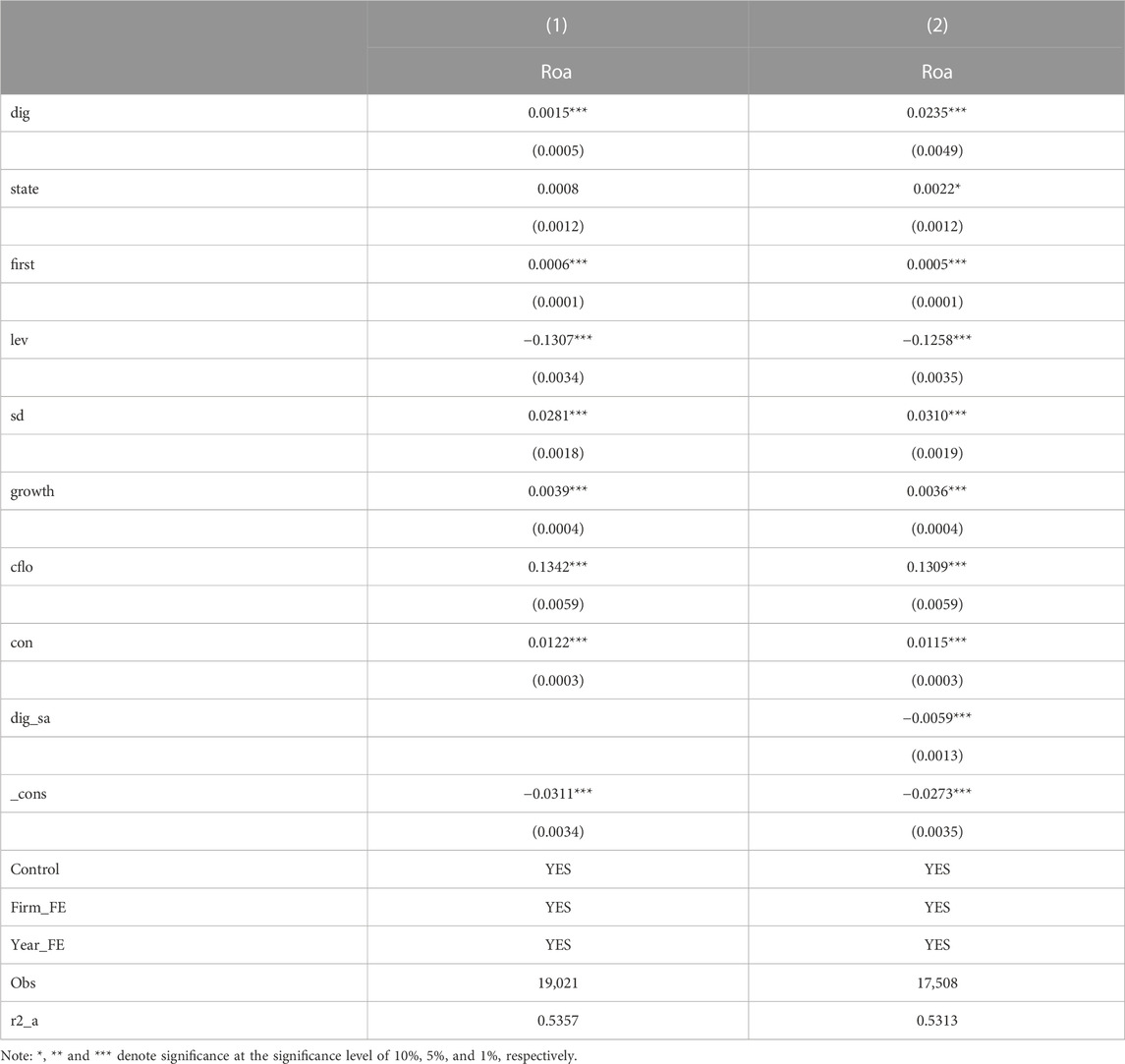

Column 1) in Table 3 shows the regression results of digitalization on enterprise performance. It can be seen that the regression coefficient of digitization (dig) is 0.0015, which is significantly positive at the 1% level. This indicates that digitalization has a positive boost on corporate performance, validating Hypothesis 1. It indicates that in the economic sense, given other variables, the enterprise performance will be 1.0015 times of the original one standard deviation increase in digitization (e^0.0015 = 1.0015). The conclusions of this study are consistent with those of previous studies (Li Yanlong et al., 2022; Wang Wenhua et al., 2022).

TABLE 3. Results of baseline regression.

Table 3 2) lists the impact of digitalization level on corporate performance after considering financing constraints as a moderating variable. The results show that the coefficient of digitization and financing constraint interaction (dig_sa) is −0.0059, which is significant at the 1% level. This suggests that more severe financing constraints will weaken the boosting effect of digitalization on corporate performance, that is, financing constraints have a negative inhibiting effect on the impact of digitalization on corporate performance, and the research Hypothesis 3 has been validated.

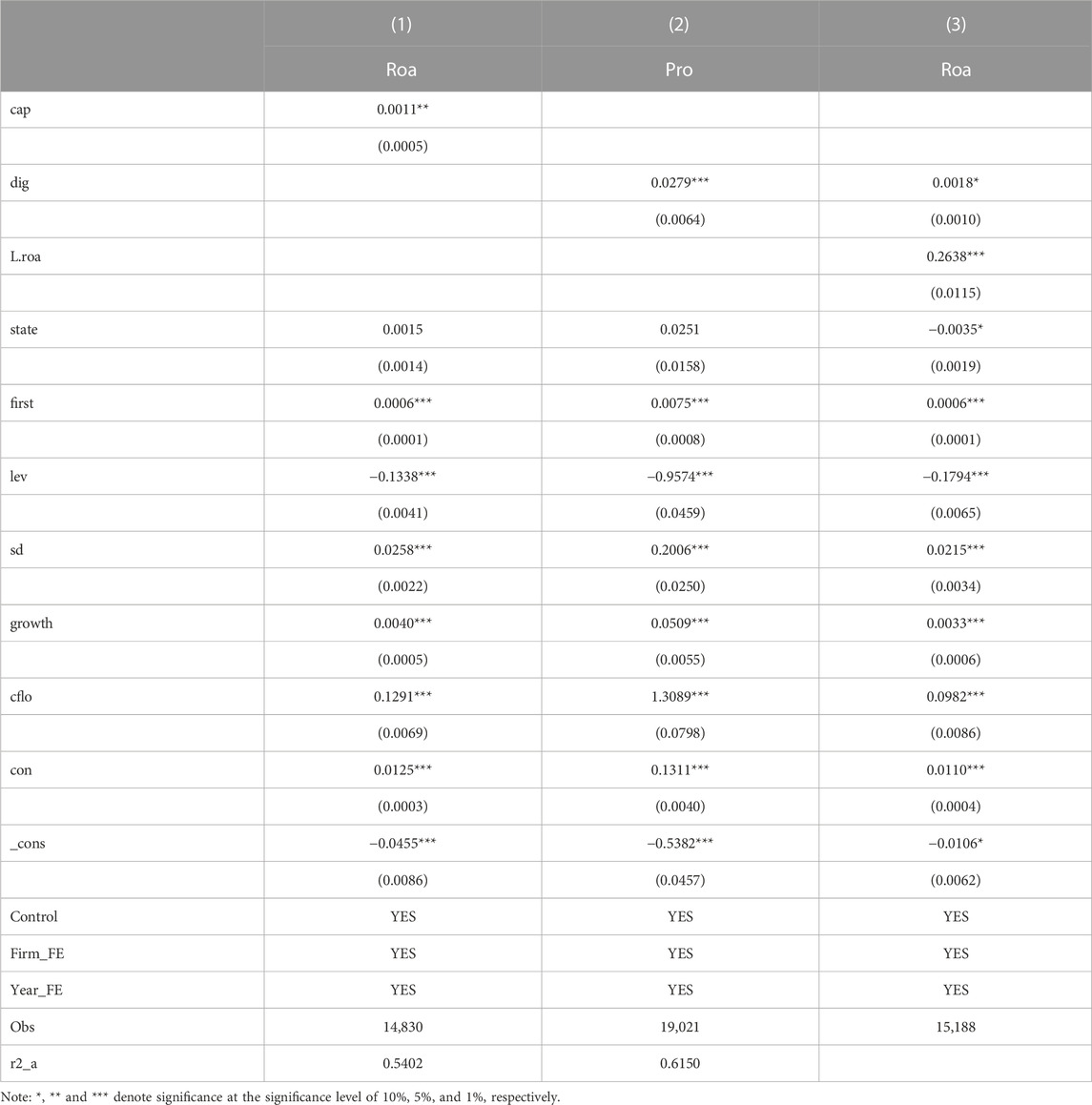

To avoid the instability of the results caused by the digitization level measured by the above method. Referring to the study of Qi Huaijin et al. (2020), we use the natural pair value (cap) of intangible assets at the end of the year to measure the digitalization level of enterprises. The regression results are shown in column (1) of Table 4. The coefficient of cap is 0.0011, which is significantly positive at the 5% level. This still suggests that digitalization can drive improvement in enterprise performance, which is similar to the results of benchmark regression.

TABLE 4. Robustness test.

Based on the study of Wang Wenhua et al. (2022), we choose earnings per share (pro) as an indicator to measure corporate performance to further test robustness. The regression results are shown in column (2) of Table 4. The coefficient of dig is 0.0279, which is significantly positive at the 1% level. It also shows that digitalization drives improved corporate performance. The conclusions of this study remain valid.

According to the studies of Roodman (2009), Li et al. (2021), Bai and Liu (2018), GMM method can effectively solve the endogeneity problem by constructing equations containing parameters based on moment conditions without assuming the distribution of variables or knowing the distribution information of random disturbance terms. In order to consider the robustness of the results and alleviate the endogenous problems of digitalization, we adopted the system GMM method with higher estimation efficiency for reference to the research of Rao Ping et al. (2022), and took the first-order lag term of digitalization as the instrumental variable of digitalization to conduct the regression again. The regression results are shown in column (3) of Table 4. The coefficient of dig is 0.0018, which is significantly positive at the 10% level. This result is consistent with the research conclusion of Li Yanlong et al. (2022), which also indicates that digitalization promotes the improvement of enterprise performance. The conclusion of this study remain valid.

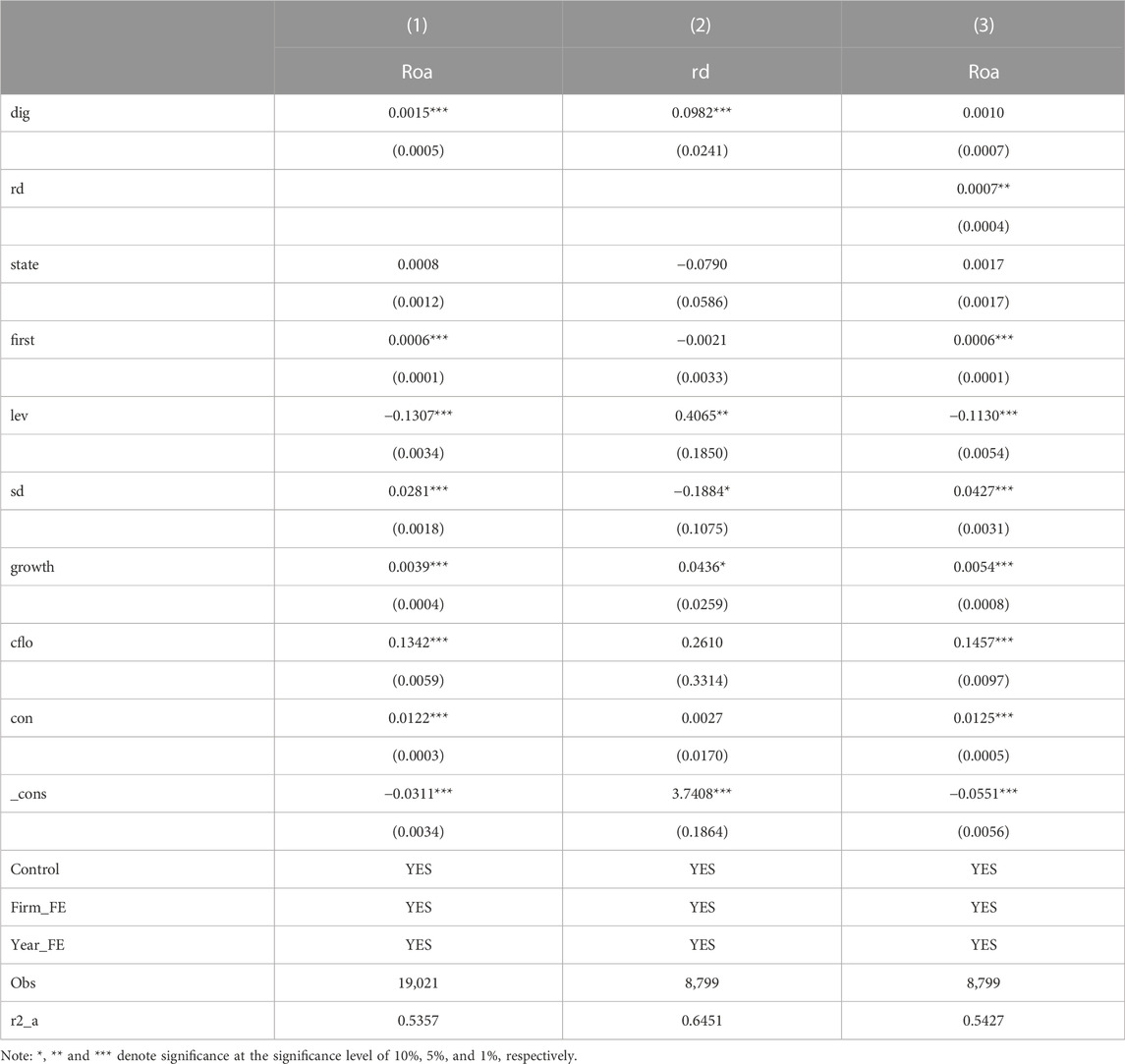

Theoretical analysis has shown that increasing the level of digitalization in a business can promote the improvement of its performance. In addition, digitization can improve corporate performance by driving corporate innovation. In the following, we perform an analysis of the mediation effect on this. Digitization plays an vital role in the promotion of enterprise innovation (rd), and can help promote the improvement of enterprise performance. Based on the three-step mediation effect model method of Wen Zhonglin and Ye Baojuan (2014), we established the following model:

Model (3) is the same as model (1).

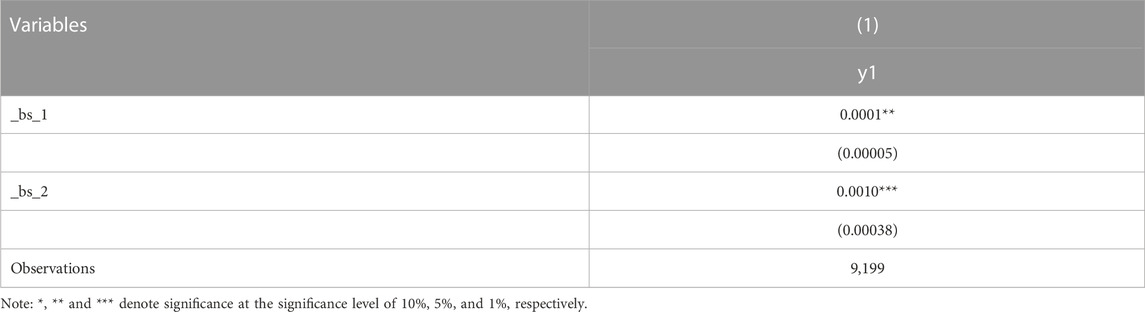

The above model is regressed and the results are shown in Table 5. In column (2), the coefficient of dig is 0.0982, which is significantly positive at the 1% level. This shows that digitization does drive innovation in businesses. In column (3), the coefficient of dig is 0.0010, but not significant, and the coefficient of rd is 0.0007, which is significantly positive at the 5% level. Since the dig coefficient was not significant, according to the study of Wen Zhonglin and Ye Baojuan (2014), we should conduct additional Bootstrap test at this time to further confirm the establishment of this mediation effect. The test results for Bootstrap are shown in Table 6. We can find that the model passes the Bootstrap test and the mediation effect is significantly established. This suggests that digitization can undoubtedly improve business performance by driving business innovation, and that the research Hypothesis 2 holds.

TABLE 5. Analysis of mediating effect.

TABLE 6. Bootstrap test.

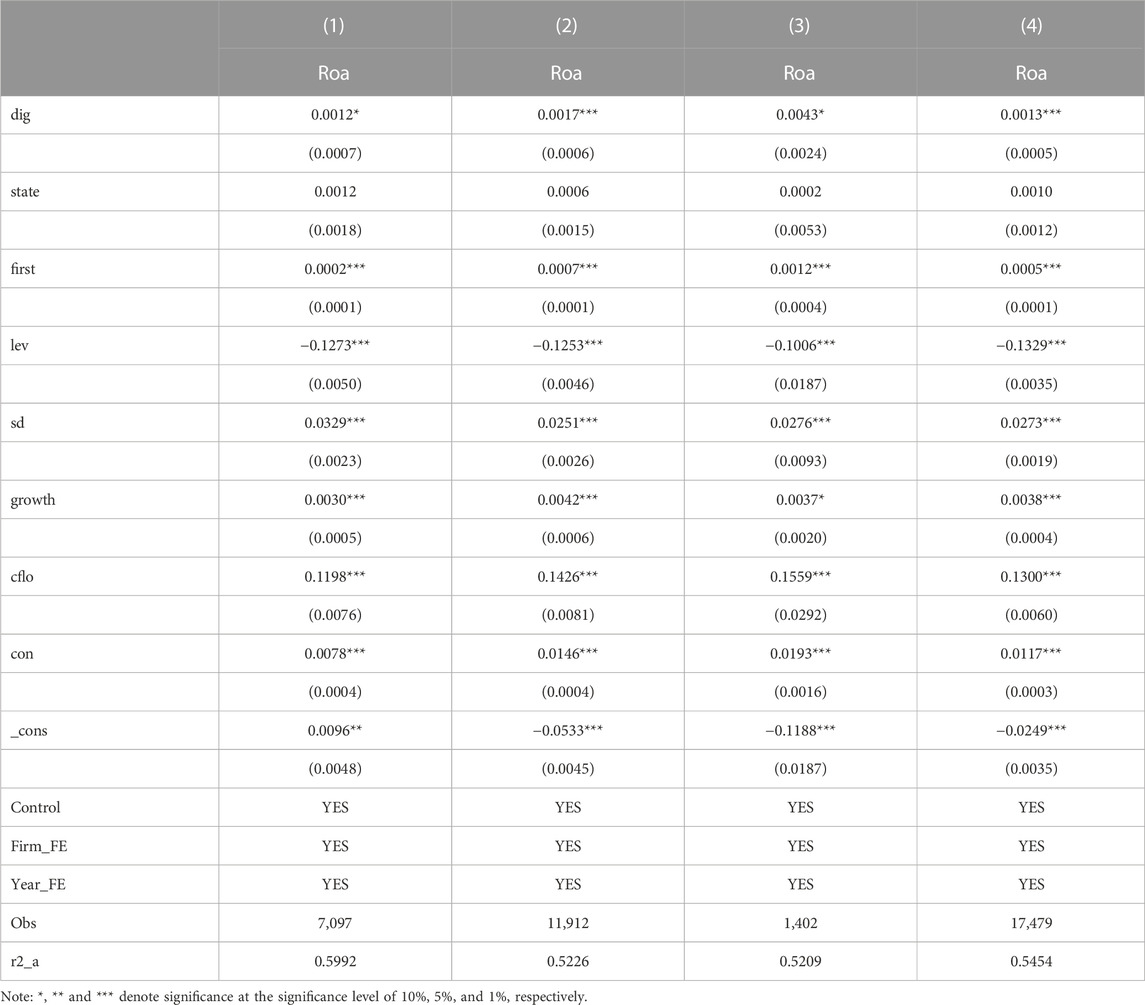

Differences in business objectives and risk control between SOEs and non-SOEs will have an impact on corporate activities, which in turn will have an impact on corporate performance. Like most scholars, this study also analyzes the effect of differences in the nature of the firms on the conclusions reached. We conducted regression for samples of state-owned enterprises and samples of non-state-owned enterprises respectively, and the regression results are shown in columns (1) and (2) of Table 7. It can be seen that digitalization has an impact coefficient of 0.0012 on corporate performance in SOEs, which is significantly positive at the level of 10 percent. The coefficient of influence of digitalization on business performance is 0.0017 for non-state-owned enterprises, which is significantly positive at the 1 percent level. This shows that improving the level of digitalization in non-state-owned enterprises can effectively improve the performance of enterprises. Compared with non-state-owned enterprises, state-owned enterprises operate with the goal of promoting the maximization of social and national interests rather than merely their own profits. As a result, SOEs have not taken all of the positive externalities of digitization into their own hands.

TABLE 7. Applicability analysis.

As the core elements of enterprise operation, senior management is an influential executor who plays the leadership function and achieves the objectives of the board of directors of the enterprise (Hua Weiqing et al., 2015). The heterogeneity of information technology backgrounds of senior executives means that they differ in the basis of their digitalisation perceptions and their ability to identify opportunities for digitalisation, resulting in differences in the impact on corporate performance. For reference to the research of Li Ruijing et al. (2022), we establish the dummy variable of senior executives’ information technology background (Dceo). Dceo has a value of 1 if the executive has an IT background; Otherwise, it is 0. Moreover, we conducted grouping regression according to the information technology background of senior executives, and the regression results are shown in columns (3) and (4) of Table 7. In column (3), the coefficient of dig is 0.0043, which is significantly positive at the 10% level. In column (4), the coefficient of dig is 0.0013, which is significantly positive at the 1% level. This suggests that the digitalization of enterprises with information technology background executives can drive the improvement of corporate performance better than that of enterprises without IT background. The information technology background of senior executives can improve the possibility of enterprises applying information technology in operation and management, and improve the application quality of information technology, so as to ensure the better implementation of various control activities and improve the efficiency of internal information communication of enterprises (Li Ruijing et al., 2022), so as to improve corporate performance.

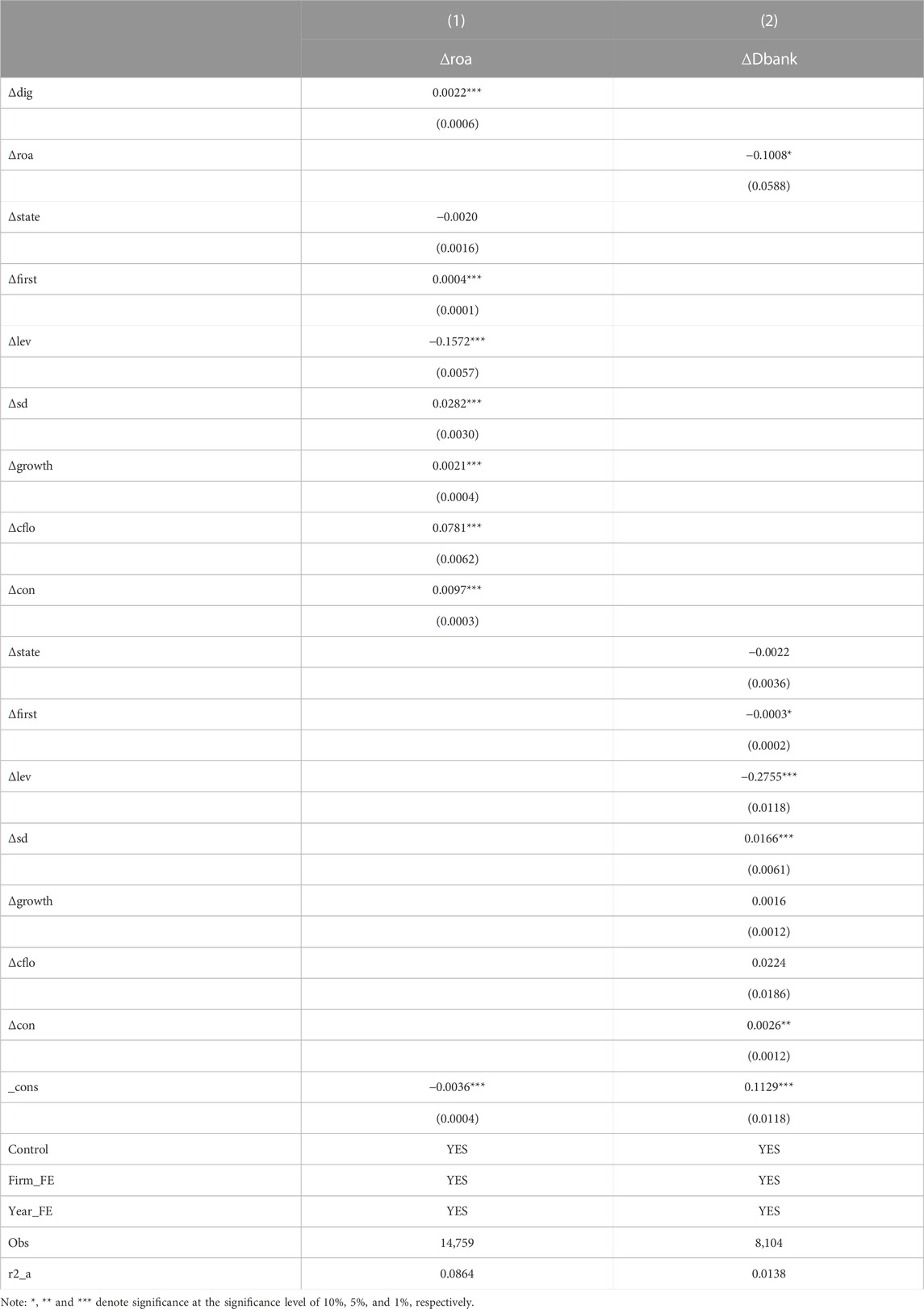

With the continuous improvement of enterprises’ digitalization level, the cooperation space of enterprises has been expanded, which makes it easy for enterprises to adopt modern technologies, different business forms and different operation modes, and realize value reconstruction through optimization measures such as penetration, integration and linkage, so as to reduce the financial pressure of enterprises and achieve high-quality development (Zhao Yan, 2022). The high-quality development of enterprises has allowed them to gradually wean themselves off bank loans and gradually improve their debt structures. To test whether the improvement in firm performance due to digitalization improves firms’ dependence on bank loans, this study conducted an economic consequence test. We use the ratio of short-term and long-term borrowings to total liabilities (Dbank) to measure the dependence of enterprises on bank loans. Referring to Kim et al. (2021), this economic consequence is identified by estimating the following two-stage model.

Among them,

TABLE 8. Analysis of economic consequences.

In the context of the rapid development of the digital economy, the development of enterprises is bound to be affected by digitalization. In this context, this study provides an in-depth analysis of the relationship between digitalization and corporate performance. Building on existing research, we incorporate financing constraints into this research regime and extend the analysis of specific mechanisms of digitalization affecting firm performance. In addition to this, we performed an economic consequences analysis. Research has found that digitization can genuinely improve corporate performance. After the robustness test, the conclusion remains valid. In the subsequent analysis of the mediation effect, we demonstrate the validity of the mediation mechanism in a theoretical analysis. We found that digitization can positively improve corporate performance by driving corporate innovation. In the applicability analysis, we find that the impact of digitalization on firm performance is more pronounced in non-state-owned enterprises and those whose executives have information technology backgrounds. Finally, in the test of economic consequences, we find that improved corporate performance due to higher levels of digitalization improves the corporate debt structure in the future.

Still, the research is not without its limitations. This article only focuses on the situation in China and lacks empirical analysis of other countries. The specific impact of digitalization on corporate performance calculated in this paper is 0.0015. However, China has a large number of listed companies and the situation of each company is different, so it is difficult for companies to make specific R&D investment plans based on this number. The study lacks additional concrete theoretical justification. In addition, this study does not further explore more mediation mechanisms and heterogeneity in the impact of digitalization on firm performance. If more empirical experience could be provided on the impact of R&D investment on firm performance, it would provide more support for the development of digitalization theory and enable a greater understanding of the positive externalities of digitalization.

In the future, researchers should consider more countries and construct different metrics to measure the level of digitalization of SMES and other hard-to-get data that should be available. Researchers should build a more in-depth theoretical model to demonstrate the impact of digitalization on corporate performance and thus accurately measure the specific magnitude of the impact of digitalization on corporate performance. In the future, researchers should also consider the long-term effects of digitization on firm performance (hu et al., 2022b; Huang and huang, 2018; Lu and Lu, 2022; pan and gao, 2022).

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding authors.

YK: Software, writing—original draft, validation, investigation, data curation, manuscript revision, financial support MF: Methodology, writing—original draft, resources, finalize, supervision, software, manuscript revision YF: Conceptualization, writing—original draft, supervision, finalize, financial support and manuscript revision YJ: Conceptualization, methodology, supervision, financial support and manuscript revision JB: Conceptualization, supervision, software, financial support and manuscript revision.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Bai, F., Dong-Hui, L., and Dong, K. Y. (2022). How Digital Transformation affects corporate Financial performance: An analysis of multiple mediating Effects based on Structural Equation. East China Econ. Manag. 36 (9), 75–87. doi:10.19629/j.cnki.34-1014/f.220224020

Bai, J., and Liu, Y. (2018). Can foreign direct investment improve China's resource mismatch? China's industrial economy. Int. J. Environ. Res. Public Health 18 (1), 60–78. doi:10.3390/ijerph18062839

Bayo-Moriones, A., Billon, M., and Lera-Lopez, F. (2013). Perceived performance effects of ICT in manufacturing SMEs. Industrial Manag. Data Syst. 113 (1), 117–135. doi:10.1108/02635571311289700

Blouin, J. L., Fich, E. M., Rice, E. M., and Tran, A. L. (2020). Corporate tax cuts, merger activity, and shareholder wealth. J. Account. Econ. 71, 101315. doi:10.1016/j.jacceco.2020.101315

Brynjolfsson, E., and Mc Elheran, K. (2016). Digitization and innovation:the rapid adoption of data-driven decision-making. Am. Econ. Rev. Pap. Proc. 106 (5), 133–139. doi:10.1257/aer.p20161016

Chen, J., and Hu, B. (2020). Financing constraints, heterogeneous R&D investment and firm performance. Commun. Finance Account. (14), 69–72+87. doi:10.16144/j.cnki.issn1002-8072.2020.14.013

Cheng, H., Hu, D., and Luo, L. (2016). The impact of technological innovation input on product quality. J. South China Agric. Univ. Soc. Sci. Ed. 15 (3).

Du, Q. Q., and Li, Q. Q. (2022). Research and Development expense deduction, financing constraints and total factor productivity of enterprises. J. Financial Theory Pract. (8), 81–91.

Duan, H., and Tian, Y. (2021). An empirical analysis of the impact of R&D investment on the future profitability of enterprises. Finance Account. Mon. (6). doi:10.19641/j.cnki.42-1290/f.2021.12.004

Ferreira, J. J. M., Fernandes, C. I., and Ferreira, F. A. (2019). To be or not to be digital, that is the question: Firm innovation and performance. J. Bus. Res. 101, 583–590. doi:10.1016/j.jbusres.2018.11.013

Forman, C., and Mc Elheran, K. (2019). Firm organization in the digital age:IT use and vertical transactions in U.S. Manufacturing. SSRN Work. Pap. Ser. doi:10.2139/ssrn.3396116

Goldfarb, A., and Tucker, C. (2019). Digital economics. J. Econ. Literature 57 (1), 3–43. doi:10.1257/jel.20171452

Gregory, V. (2019). Understanding digital transformation: A review and a research agenda. J. Strategic Inf. Syst. 28 (2), 118–144. doi:10.1016/j.jsis.2019.01.003

Gu, L., Li, J., and Peng, Y. (2018). Internal and External financing conditions, financing constraints and firm performance: New evidence from a survey of firms in the Beijing-Tianjin-Hebei region. Econ. Theory Econ. Manag. (7), 88–99.

Guenzi, P., and Habel, J. (2020). Mastering the digital transformation of sales. Calif. Manag. Rev. 62 (4), 57–85. doi:10.1177/0008125620931857

Hu, H., Song, X., and Dou, B. (2022a). The value of digitalization during the Crisis: Evidence from Corporate resilience. Finance Trade Econ. (7), 134–148. doi:10.19795/j.cnki.cn11-1166/f.20220706.008

Hu, X. (2021). An empirical study on financing constraints and firm performance. J. Heihe Univ. 12 (10), 56–60.

Hu, Y., Wang, K., and Fan, H. (2022b). Digital transformation and enterprise overseas investment: Fact investigation and mechanism analysis. Financ. Rev. 1–14. doi:10.13762/j.carolcarrollnkiCJLC.20221019.001

Hua, W., and Luo, Y. (2015). An Empirical Study on the Educational background and corporate Performance of senior executives in innovation-oriented enterprises. J. Jiangxi Normal Univ. (Philosophy Soc. Sci. Ed. (3), 120–124.

Huang, Y., and Huang, Z. (2018). The development of digital finance in China: Present and future. Econ. Q. (4), 1489–1502. doi:10.13821./.j.carol.carroll.nki.ceq.2018.03.09

Junguo, H., Chang, L., and Zhu, D. (2022). Digital transformation, financing constraints and total factor productivity. South. Finance 7, 54–65.

Lee., J., Bagheri., B., and Kao, H. A. (2015). A cyber-physical systems architecture for industry 4.0-based manufacturing systems. Manuf. Lett. 3, 18–23. doi:10.1016/j.mfglet.2014.12.001

Lei, L., Yang, S., and Chen, N. (2022). The impact of digital transformation on enterprise investment efficiency. Soft Sci (11), 23–29. doi:10.13956/j.ss.1001-8409.2022.11.04

Li, J., Ding, H., Hu, Y., and Wan, G. (2021). Dealing with dynamic endogeneity in international business research. J. Int. Bus. Stud. 52 (3), 339–362. doi:10.1057/s41267-020-00398-8

Li, J., Hu, S., Qi, X., Zhou, T., and Lu, Z. (2022c). Analysis on the impact of enterprise digital transformation on performance. Invest. Entrepreneursh. (13), 48–52.

Li, L., Su, F., Zhang, W., and Mao, J. Y. (2018). Digital transformation by SME entrepreneurs:A capability perspective. Inf. Syst. J. 28 (6), 1129–1157. doi:10.1111/isj.12153

Li, R., Dang, S., Li, B., and Yuan, R. (2022a). The Information technology Background of ceos and the quality of Internal control in Enterprises. Audit Res. (1), 118–128.

Li, Y., Jin, P., and Luo, T. (2022b). Digitalization, spillover effect and firm performance. Industrial Technol. Econ. (3), 25–33.

Liu, D. Y., Chen, S. W., and Chou, T. C. (2011). Resource fit in digital transformation: Lessons learned from the CBC Bank global e-banking project. Manag. Decis. 49 (10), 1728–1742. doi:10.1108/00251741111183852

Liu, D., Bai, F., and Dong, K. (2022). Research on the influence mechanism of digital transformation on enterprise performance. Account. Commun. (16), 120–124. doi:10.16144./.j.carol.carroll.nki.issn1002-8072.2022.16.010

Loebbecke, C., and Arnold, P. (2015). Reflections on societal and business model transformation arising from digitization and big data analytics: A research agenda. J. Strategic Inf. Syst. 24 (3), 149–157. doi:10.1016/j.jsis.2015.08.002

Lu, S., and Lu, M. (2022). Digital finance and low-carbon finance: Research on the ignition point of mutual integration, co-promotion system and symbiotic mechanism -- A case study of commercial banks. Daqing normal Univ. J. (1), 24–30. doi:10.13356./.j.carol.carroll.nki.jdnu.2095-0063.2022.01.004

Maomao, C., Wang, J., and Wang, W. (2022). Research on the influence mechanism of enterprise innovation performance under the background of digital transformation: A hybrid method based on NCA and SEM. Res. Sci. Sci. (2), 319–331. doi:10.16192/j.cnki.1003-2053.20210719.001

Mikalef, P., and Pateli, A. (2017). Information technology-enabled dynamic capabilities and their indirect effect on competitive performance:findings from PLS-SEM and fsQCA. J. Bus. Res. 70, 1–16. doi:10.1016/j.jbusres.2016.09.004

Mubarak, M. F., and Petraite, M. (2020). Industry 4.0 technologies,digital trust and technological orientation:What matters in open innovation? Technol. Forecast. Soc. Change 161, 120332. doi:10.1016/j.techfore.2020.120332

Musso, P., and Schiavo, S. (2008). The impact of financial constraints on firm survival and growth. J. Evol. Econ. 18 (2), 135–149. doi:10.1007/s00191-007-0087-z

Pan, H., and Gao, J. (2022). Digital transformation and enterprise innovation: Empirical evidence based on annual reports of Chinese listed companies. J. Central South Univ. Soc. Sci. Ed. (5), 107–121.

Pan, H., and Yang, H. (2022). Competitors financing constraints on corporate mergers and acquisitions behavior is studied. Influ. of" China's industrial Econ. 7, 159–177. doi:10.19581/j.cnki.ciejournal.2022.07.015

Pan, R., Luo, J., and Yang, Z. (2022). Servetization of manufacturing enterprises, Digitalization of Front and back office and Enterprise performance. J. Syst. Manag. (5), 988–999.

Qi, H., Cao, X., and Liu, Y. (2020). The impact of digital economy on corporate governance: From the perspective of information asymmetry and managers' irrational behavior. Reform 4, 50–64.

Qi, Y. D., and Cai, C. W. (2020). Research on the multiple impacts of digitalization on manufacturing enterprise performance and its mechanism. Learn. Explor. (7), 108–119.

Rao, P., and Wu, Q. (2022). The impact of Digital financial inclusion on Total factor productivity of enterprises. Statistics Decis. (16), 142–146. doi:10.13546/j.carol.carroll.nki.tjyjc.2022.16.028

Ren, Y., Zhang, X., Wu, J., and He, Z. (2022). Government subsidies, R&D investment and Total factor productivity: An empirical study of Chinese manufacturing enterprises. Sci. Decis. Mak. (7), 44–62.

Roodman, D. (2009). How to do Xtabond2: An introduction to difference and system GMM in stata. Stata J. 9 (1), 86–136. doi:10.1177/1536867x0900900106

Tang, L., Li, Q., and Chen, C. (2020). The effect of data management ability on firm productivity: New findings from the Enterprise-labor Matching Survey in China. China's Ind. Econ. (6), 174–192. doi:10.19581/j.carol.carroll.nki.ciejournal.2020.06.010

Verhoef, P. C., Broekhuizen, T., Bart, Y., Bhattacharya, A., Qi Dong, J., Fabian, N., et al. (2019). Digital transformation: A multidisciplinary reflection and research agenda. J. Bus. Res. 122 (1), 889–901. doi:10.1016/j.jbusres.2019.09.022

Wang, H., Ye, L., and Tan, Q. (2022b). The impact of digital transformation on enterprise performance based on Meta-analysis. J. Syst. Manag. (1), 112–123.

Wang, H., Sun, P., and Guo, H. (2022a). How can digital finance enable enterprises' digital transformation? -- empirical evidence from Chinese listed companies. Financ. Rev. (10), 3–13. doi:10.13762/j.carol.carroll.nki.CJLC.2022.0311.001

Wang, W., and Zhou, L. (2022). How can digital transformation of logistics industry improve financial performance? -- the dual path based on financing cost and management efficiency. Account. Commun. (20), 44–48. doi:10.16144/j.carol.carroll.nki.issn1002-8072.2022.20.031

Wen, H., and Wang, S. (2022). The impact of digital technology application on enterprise innovation. Sci. Res. Manag. (4), 66–74. doi:10.19571/j.cnki.1000-2995.2022.04.008

Wen, Z., and Ye, B. (2014). Analyses of mediating effects: The development of methods and models. Adv. Psychol. Sci. 22 (05), 731–745. doi:10.3724/sp.j.1042.2014.00731

Wu, F., Hu, H., Lin, H., and Ren, X. (2021). Corporate digital transformation and capital market performance: Empirical evidence from stock liquidity. Manag. World (7), 130–144+10. doi:10.19744/j.cnki.11-1235/f.2021.0097

Yao, J. (2022). Research on the impact of corporate innovation on corporate performance. Bus. Account. Account. (2), 99–102.

Zhai, L., and Wu, Y. (2021). The financing and supervision effects of credit rating: Evidence from corporate mergers and Acquisitions. Nankai Manag. Rev. (1), 27–47.

Zhang, J., and Jing, L. (2022). How digital technology application drives enterprise breakthrough innovation. J. Shanxi Univ. Finance Econ. (1), 69–83. doi:10.13781/j.cnki.1007-9556.2022.01.006

Zhang, L., and Zhou, L. (2016). Research on the influence of "Integration of the Two Aspects" on enterprise innovation -- from the perspective of enterprise value chain. J. Finance Econ. 42 (7), 99–110. doi:10.16538/j.cnki.jfe.2016.07.009

Zhao, Y. (2022). Digital transformation, strategic resource matching and high-quality enterprise development. Finance Account. Mon. 20, 62–69. doi:10.19641/j.cnki.42-1290/f.2022.20.008

Zheng, L., Yao, Y., Zhang, G., and Kuang, H. (2020). Enterprise digitalization, Specialized knowledge and organizational empowerment. China's Ind. Econ. (9), 156–174. doi:10.19581/j.carol.carroll.nki.ciejournal.2020.09.008

Keywords: digitalization, financing constraints, enterprise performance, enterprise innovation, economic consequences

Citation: Kuang Y, Fan M, Fan Y, Jiang Y and Bin J (2023) Digitalization, financing constraints and firm performance. Front. Environ. Sci. 11:1090537. doi: 10.3389/fenvs.2023.1090537

Received: 05 November 2022; Accepted: 27 February 2023;

Published: 20 March 2023.

Edited by:

Carmen Valentina Radulescu, Bucharest Academy of Economic Studies, RomaniaReviewed by:

Otilia Manta, Romanian Academy, RomaniaCopyright © 2023 Kuang, Fan, Fan, Jiang and Bin. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Yan Jiang, WGlqaWFuZ3lhbkBobnVpdC5lZHUuY24=; Min Fan, MTE2MDUyOTg4MUBxcS5jb20=; Yaojun Fan, eWFvanVuZmFuOTk2QGdtYWlsLmNvbQ==; Jie Bin, YmluamllMjAyMjA4QDE2My5jb20=

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.