Yan Li

Yan Li Yueru Mei1,2

Yueru Mei1,2- 1School of International and Public Affairs, Shanghai Jiao Tong University, Shanghai, China

- 2School of Emergency Management, Shanghai Jiao Tong University, Shanghai, China

- 3Xinjiang Zhongtai Innovation and Technology Institute Co., Ltd., Urumqi, China

- 4China International Engineering Consulting Corporation, Beijing, China

Chemical industry is an important pillar industry of China’s economy with high energy consumption and carbon emissions. In the context of “peaking carbon emissions and carbon neutrality” target in China, it is imperative for the chemical industry to reduce carbon emissions. Based on literature on carbon emission reduction path and the analysis of the development status of chemical industry, this paper identifies the opportunities and challenges of carbon emission reduction in the chemical industry and proposes several feasible paths for China’s chemical industry to achieve carbon neutrality.

1 Introduction

The report Climate Change 2022: Impacts, Adaptation and Vulnerability released by the United Nations Intergovernmental Panel on Climate change (IPCC, 2022) in 2022 shows that climate change will have negative impacts on most species, and some of the ecological losses caused by climate change are irreversible or nearly irreversible (IPCC, 2022). As the social, economic and ecological environment problems caused by climate change have become more and more serious, the international community also pays more attention to carbon emission reduction. As a large developing country, China has also actively promoted carbon emission reduction and put forward the influential “peaking carbon emissions and carbon neutrality” target, that is, China will strive to reach the peak of carbon dioxide emissions by 2030 and achieve carbon neutrality by 2060. Since then, the Chinese government has issued a series of policy documents to guide and urge all production sectors to reduce carbon emissions. For example, the fourteenth Five-year plan for National Economic and Social Development of the People’s Republic of China and the outline of long-term goals for 2035 propose that during the “fourteenth five-year plan” period, energy consumption and carbon dioxide emissions per unit of GDP should be reduced by 13.5% and 18% respectively; The Opinions on Completely, Accurately and Comprehensively Implementing the New Development Concept and Doing a Good Job on carbon peak and carbon neutralization have systematically deployed the carbon peaking and carbon neutralization work (General Office of the Communist Party of China Central Committee, 2021); Action Plan for Carbon Dioxide Peaking Before 2030 clearly requires that the industrial structure and energy structure must be developed in a clean manner, and the energy utilization efficiency of key industries needs to be greatly improved (The State Council Of the People’s Republic of China, 2021). China’s deployment and planning of carbon emission reduction are gradually specific and in-depth.

As a pillar industry of economic development, the chemical industry is a typical industry with high energy consumption, high pollution, and high carbon emissions (Gu et al., 2013). Under the background of low-carbon economic development, the chemical industry is facing great pressure on carbon emission reduction, which also means that the chemical industry has rich potential in carbon emission reduction. The path of carbon emission reduction and achieving carbon neutrality in the chemical industry has become one of the research focuses internationally.

In this paper, Section 2 summarizes research on carbon dioxide emission reduction in chemical industry; Section 3 analyzes the current development status of chemical industry in China; Section 4 identifies major opportunities and challenges for chemical industry in China under the national carbon neutrality goal. Finally, Section 5 discusses paths and policy implications.

2 Manuscript formatting

2.1 Relevant research on carbon emission reduction paths in chemical industry

At present, many scholars have studied the carbon emission reduction measures in chemical industry. In the short term, the main measures to reduce carbon dioxide emissions from coal chemical industry are the application of advanced technology and the elimination of backward production capacity. The main measures to reduce carbon emissions in the medium and long term, however, are to promote the transformation of energy structure and to improve of energy efficiency (Huang et al., 2019). At the same time, improving the circularity of resources and promoting value chain collaboration can also reduce carbon emissions (ECF, 2014).

Some studies focus on the comparative analysis of the role of advanced technology on carbon emission reduction in chemical industry. For example, the mixed SD-LEAP model is used to compare the carbon dioxide emissions and emission reduction potential of the South Korea’s oil refining industry under different technology scenarios (Park et al., 2010). Other studies use scenario analysis to examine the impacts of technological improvement on carbon dioxide emission reduction in China’s chemical industry (Zhu et al., 2010). However, some studies have found that the reduction of carbon dioxide emissions brought by technological improvement cannot offset the increase of carbon dioxide caused by scale effect (Liang and Zhang, 2013), while optimizing the energy structure can promote carbon emission reduction (Fan et al., 2013). Carbon capture and utilization (CCU) also has the technical potential to achieve carbon neutrality in the chemical industry, but it will also lead to a massive increase of demand in greenhouse gas emits from low-carbon electricity (Kätelhön et al., 2019), and the technical cost of carbon capture and storage (CCS) is very expensive (The European Chemical Industry Council Cefic, 2013). Griffin et al. (2018) believes that promoting CCS, improving energy efficiency, the use of bioenergy and other key technologies are considered to be the keys to effectively reduce carbon emissions. Gabrielli et al. (2020) evaluated three technology paths (CCS path, CCU path and BIO path (Use of biomass for particular purposes in the production of chemicals)) which can achieve carbon neutrality in the chemical industry in a qualitative and quantitative way and analyzed the advantages and disadvantages of each technology path.

Other studies have discussed the possible ways of emission reduction in the chemical industry from a more comprehensive perspective of project technology management and information management, such as improving project standardization, strengthening the training of professional technicians, and establishing enterprise energy-saving information platform (Wang, 2008). In addition, based on the concept of circular economy, eco-industrial parks can also reduce the carbon emissions from chemical enterprises by realizing rational allocation and efficient utilization of resources (Gao et al., 2009).

2.2 Development status of chemical industry in china

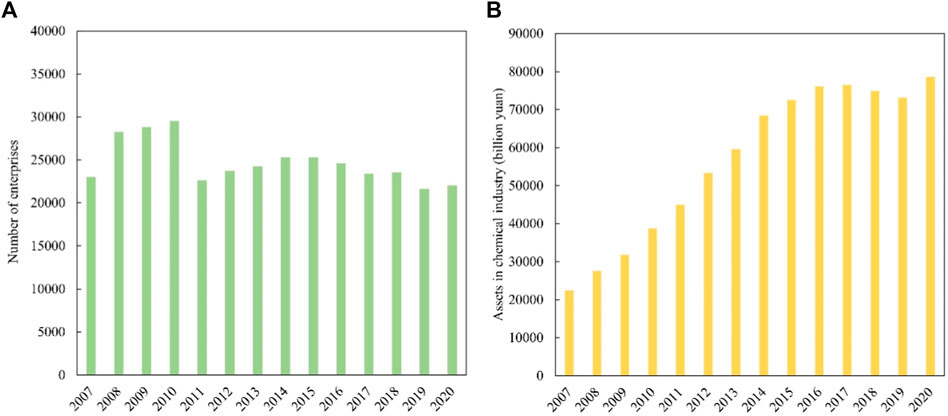

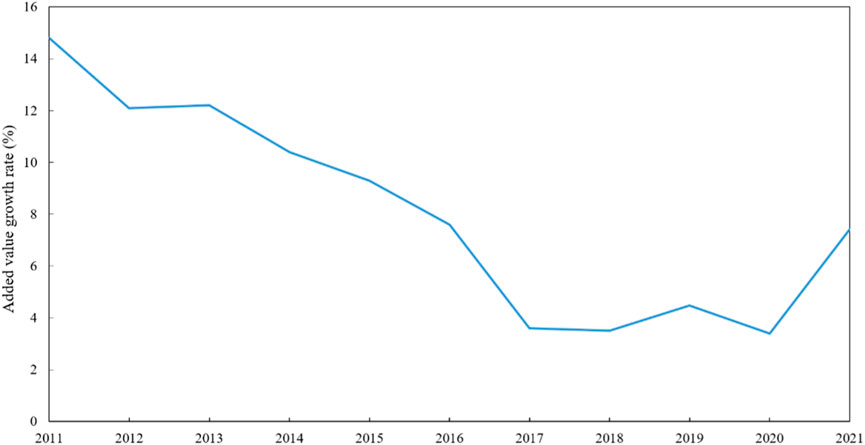

China is one of the largest producers and consumers of chemical products in the world (Lin et al., 2012). Due to the large scale of the chemical industry and a wide range of products, different studies define the scope of the chemical industry differently. Referring to the method of Wei et al (2018), the statistical caliber of the chemical industry in this paper is chemical raw materials and chemical products manufacturing (except Figure 2). Although the number of enterprises in the chemical industry has remained generally stable since 2011, the assets of the chemical industry have shown an upward trend (Figure 1). By 2020, the number of chemical industry enterprises in China has reached 22,008, with total assets of 7,865.15 billion yuan. According to Figure 2, the growth rate of the added value of China’s chemical industry has been in a downward trend since 2011, falling from 14.8% in 2011 to 3.4% in 2020. In 2021, the growth rate is estimated to be 7.4% (National Development and Reform Commission, 2021).

FIGURE 1. Number of enterprises (A) and total assets (B) in the chemical industry (Data source: China Statistical Yearbook).

FIGURE 2. Growth rate of added value of chemical industry (Data source: https://www.ndrc.gov.cn/fggz/jjyxtj/hgjjyx/?code=&state=123)

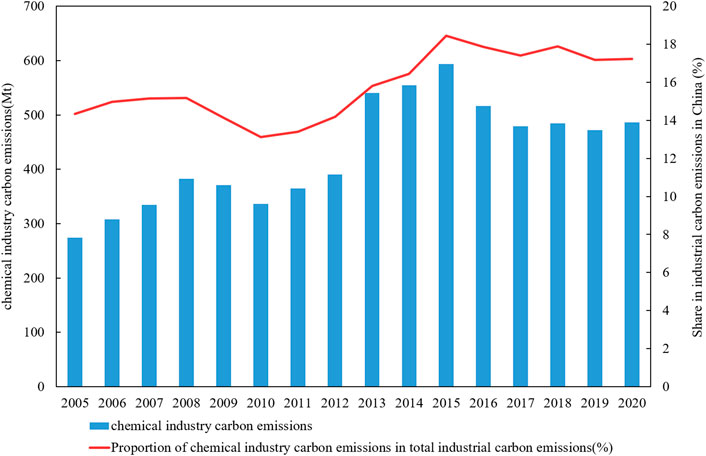

From the perspective of the product structure of the chemical industry, China has a high proportion of low value-added and rough-processed chemical products, showing the current product structure of low-end surplus and high-end shortage. On the whole, there is a gap between China and developed countries in terms of the diversity and quality of chemical products (Wang and Li, 2018). It can be found that the production process technology of China’s chemical products is still relatively backward, and the negative impacts of chemical products on the environment is significant. Methanol, synthetic ammonia, oil refining, ethylene, and modern coal chemical industry are the top five key emission sub-industries of China’s chemical industry (Wen et al., 2022). Generally speaking, since 2005, the carbon emissions of China’s chemical industry have fluctuated and increased, reaching a peak of 593.89 million tons in 2015, accounting for 18.46% of the total industrial carbon emissions. After that, with the strengthening of China’s response to global climate change, the carbon emissions of the chemical industry have steadily decreased. In 2020, the carbon emissions of the chemical industry were 486.33 million tons, a decrease of 18.11% compared with 2015, and the proportion of the chemical industry in the industrial carbon emissions decreased to 17.24% (Figure 3).

FIGURE 3. Carbon dioxide emissions of chemical industry and its proportion in total industrial carbon dioxide emissions (Data source: China Energy Statistics Yearbook, 2021).

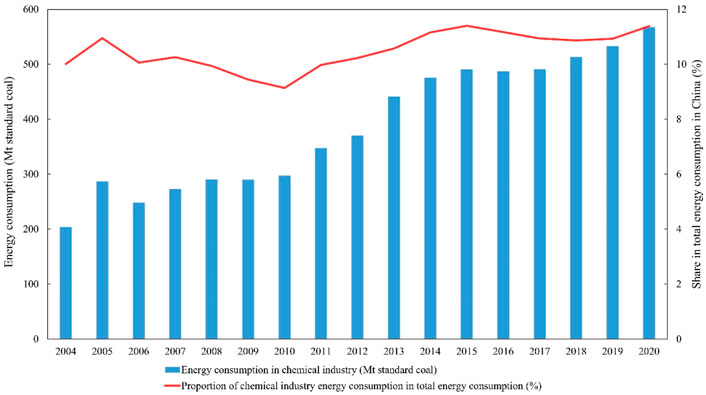

In general, the energy consumption of the chemical industry shows an upward trend (Figure 4). In 2020, China’s total energy consumption was 4,983.14 million tons of standard coal, and the chemical industry consumed 567.23 million tons of standard coal, accounting for 11.38% (China Statistical Yearbook, 2021). China is rich in coal but has oil and gas shortages; therefore, coal contributes the most to the energy consumption in the chemical industry (Lin and long, 2016). According to Figure 5, the proportion of raw coal consumption has shown a downward trend since 2015, but it is still the most important energy source, contributing to 55.92% of total energy consumption in chemical industry in 2020; The proportion of coke consumption has continued to rise since it surpassed natural gas in 2014, ranking second steadily; Natural gas consumption occupies the third place. Among the numerous chemicals in the chemical industry, the largest energy consumption is coal-based ammonia, calcium carbide, caustic soda, coal-based methanol, sodium carbonate and yellow phosphorus (Zhu et al., 2010).

FIGURE 4. Energy consumption in the chemical industry and its proportion in total energy consumption in China (Data source: China Statistical Yearbook).

FIGURE 5. Energy consumption structure of chemical industry (Data source: China Energy Statistics Yearbook).

2.3 Opportunities and challenges

2.3.1 Opportunities for chemical industry under carbon neutrality target

In long run, low-carbon development in the chemical industry is an inevitable trend. In the context of high-quality economic development, various national departments have issued a series of policies and measures to promote the high-quality development of the chemical industry. For example, The Guiding Opinions on Promoting the High-quality Development of the Petrochemical and Chemical Industry During the 14th Five-year Plan (The Central People’s Government of the People’s Republic of China, 2022) clearly proposed to speed up the transformation and upgrading of traditional industries and to improve the level of cleaner production in the chemical industry. This means that the approval of projects with high energy consumption and high emissions will be stricter, and the future development space of enterprises with poor carbon emission control ability will be compressed. In the same time, the development advantages of clean production enterprises will gradually become prominent, and the market influence of chemical enterprises with “green advantages” will increase. Furthermore, these policies and measures will improve consumers’ consumption preference and stimulate the demand for green products, thus encouraging enterprises to put more effort on research, development and demonstration (RD&D) and large-scale practice of low-carbon technologies. The two-way interaction between consumers and chemical enterprises will accelerate the diversification and low-carbon development of chemical products.

2.3.2 Challenges for chemical industries to reduce carbon emissions

On the one hand, in the terminal primary energy consumption structure of the chemical industry, coal consumption accounts for the highest proportion (Figure 5). The energy structure needs to be changed to cleaner. However, there are still some obstacles to the universal, efficient and stable application of clean energy (such as wind energy and solar energy), and it takes time for people to change their cognitive level and habits on energy consumption. Therefore, it is difficult to change the energy structure in a short time.

On the other hand, As China’s carbon emission reduction efforts continue to increase, the chemical industry and its related upstream and downstream industries are facing the demand of carbon reduction. However, at present, China’s chemical product structure shows a pattern of “low-end surplus and high-end shortage” (Ministry of industry and information technology, 2016; Wang and Li, 2018), and backward production capacity still needs to be digested and eliminated. However, many enterprises are used to the extensive development mode of emphasizing quantity over quality and have not formed sufficient attention on emission reduction. In addition, the RD&D of advanced green technologies and equipment need significant capital investments, high-end talents and other supportive conditions, which will also bring more difficulties to put advanced technologies into practice.

2.4 Feasible paths for china’s chemical industry to achieve carbon neutrality

Firstly, China needs to develop high-end and green chemical products. Outdated production capacity should be eliminated in a timely manner and replaced, transformed and upgraded. With the development of national economy and improvement in living standard, people also have a more qualitative and diversified demands for chemical products. High-end and diverse production has gradually become the new trend for the development of the chemical industry. This requires relevant enterprises to increasingly support RD&D and professional technicians, to break through the bottleneck of key technology research, and to promote the transformation of products from low value-added and extensive development mode to specialized and intensive development mode.

Secondly, promote green technology support and application in chemical industry. On the one hand, the breakthrough of renewable energy exploitation and application technology will promote the transformation of energy consumption structure in the chemical industry; On the other hand, the combination of the renewable energy sector and the chemical industry sector may be an important way to reduce carbon emissions. For example, using green hydrogen (converting renewable energy into hydrogen) instead of traditional gray hydrogen (using traditional fossil fuels to produce hydrogen) has great potential to reduce carbon emissions. Therefore, the government should focus on promoting industry-university-research cooperation, actively provide policy and funding support for green chemical enterprises at the start-up stage, and shorten the cycle of green technology from RD&D to landing and then to large-scale application.

Thirdly, large-scale green integrated chemical industrial parks should be built to save resource and costs and to reduce carbon emissions. In the process of planning and construction, industrial park needs to consider the supply of energy and materials, the layout of upstream and downstream industries, and the construction of public infrastructure, so that chemical companies can share public resources and improve the efficiency of resource and logistics utilization. In terms of operation management, it is necessary to implement unified and standardized management of project access and production process technology to control the quality of the entire life cycle of products, as well as to improve the quality of chemical products. Since the product quality of many small and medium-sized chemical enterprises varies, after these companies enter the park, the quality of their products will be improved accordingly under the unified management of the park. In addition, by building a smart production management platform, a refined management of carbon emissions in the parks can be achieved through real-time monitoring of the production carbon emissions; this can also improve the green competitiveness of the chemical products.

Fourth, the government should collaborate with industries to promote the development of CCUS. CCUS is an important technology to realize carbon neutrality, and the development of CCUS technology is increasingly valuable internationally. Currently, remarkable technical progress has been made in various steps along the production chain of CCUS in China (Cai et al., 2021). The captured high concentration carbon dioxide can be used as basic raw materials for food processing, chemical manufacturing and other industries (Gan et al., 2022). The production process of petrochemical industry will produce high concentration of carbon dioxide, and the application cost of CCUS technology is lower than that of low concentration carbon emission sources (Cai et al., 2021). Therefore, the petrochemical industry has significant advantages in reducing carbon emissions and achieving carbon neutrality by applying CCUS. In order to achieve the goal of carbon neutrality in China’s chemical industry, China still needs to speed up the research of CCUS technology, establishing an integrated cooperation framework between industry, university and research institutes to actively explore the practical path of carbon dioxide resource utilization and promote the recycling of resources.

Last but not the least, carbon dioxide emission reduction in chemical industry is an opportunity to promote cross-regional cooperation between energy supply regions and demand regions in China. Western China is rich in renewable energy, but the level of local economic development limits its capacity to consume renewable energy. The proposed “West-East Gas Transmission” project and the “West-East Power Transmission” project are of great significance to alleviate the spatial imbalance of resources, promote the transformation of energy structure, improve the quality of ecological environment, and accelerate the economic development of the Western China. For example, Xinjiang has great potential to develop wind and solar energy, while the level of economic development is relatively backward; yet Shanghai has a high level of economic development and high efficiency of resource utilization, but the local resource endowment is limited. Through the cross-regional transmission of clean energy, the exchange of advantageous resources between two regions is realized, which is conducive to clean energy transformation in Shanghai’s chemical industry, and Xinjiang’s economic development can also benefit from it. Therefore, it is necessary to further improve the inter-provincial and cross-regional transmission channels by implementing relevant policies and establishing collaboration networks among energy supply regions and demand regions.1

Author contributions

YL: Formal analysis, Writing—review and editing, Data curation, Writing—original draft. YM: Formal analysis, Writing—review and editing, Visualization. TZ: Writing—review and editing. YX: review.

Conflict of interest

TZ was employed by Xinjiang Zhongtai Innovation and Technology Institute Co., Ltd. YX was employed by China International Engineering Consulting Corporation.

The remaining authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Footnotes

1https://data.cnki.net/Yearbook/Navi?type = typeandcode = A

References

China Statistical Yearbook (2021). Available at: https://data.cnki.net/yearbook/Single/N2021110004.

General Office of the communist party of China central committee (2021). The Opinions on completely, accurately and comprehensively implementing the new development concept and doing a good job on carbon peak and carbon neutralization. Available at: http://www.gov.cn/zhengce/2021-10/24/content_5644613.htm.

The state Council of the People's republic of China (2021). Action Plan for Carbon Dioxide Peaking before 2030. Available at: http://www.gov.cn/zhengce/content/2021-10/26/content_5644984.htm.

Cai, B., Li, Q., and Zhang, X. (2021). Annual report on carbon dioxide capture, utilization and storage (CCUS) in China (2021) -- Study on the path of CCUS in China. Environmental Planning Institute of the Ministry of ecological environment, Wuhan Institute of geotechnical mechanics of Chinese Academy of Sciences. Beijing: The Administrative Center for China. (in Chinese).

European Climate Foundation [ECF] (2014). Europe’s Low-carbon Transition: Understanding the challenges and opportunities for the chemical sector. Brussels (Belgium): ECF.

Fan, T., Luo, R., Fan, Y., Zhang, L., and Chang, X. (2013). Study on the influencing factors of carbon dioxide emission in China's chemical industry. Chin. Soft Sci. (03), 166–174. doi:10.3969/j.issn.1002-9753.2013.03.017

Gabrielli, P., Gazzani, M., and Mazzotti, M. (2020). The role of carbon capture and utilization, carbon capture and storage, and biomass to enable a net-zero-CO2 emissions chemical industry. Ind. Eng. Chem. Res. 59 (15), 7033–7045. doi:10.1021/acs.iecr.9b06579

Gan, F., Jiang, X., Chang, Y., Jin, Z., Wang, H., and Shi, J. (2022). Carbon neutrality technology path exploration in petrochemical industry. Chem. Industry Eng. Prog. 41 (03), 1364.

Gao, Z., Li, W., Pan, W., and Ma, Y. (2009). Management mode of carbon emission reduction in chemical industry based on improving comprehensive benefits. Mod. Chem. Ind. 29 (02), 5–9. (in Chinese). doi:10.16606/j.cnki.issn0253-4320.2009.02.026

Griffin, P. W., Hammond, G. P., and Norman, J. B. (2018). Industrial energy use and carbon emissions reduction in the chemicals sector: A UK perspective. Appl. Energy 227, 587–602 .doi:10.1016/j.apenergy.2017.08.010

Gu, B., Tan, X., Chi, H., and Wang, Y. (2013). Analysis model and application of carbon dioxide emission reduction potential in chemical industry. Chin. J. Manag. Sci. 21 (05), 141

Huang, Y., Yi, Q., Kang, J. X., Zhang, Y. G., Li, W. Y., Feng, J., et al. (2019). Investigation and optimization analysis on deployment of China coal chemical industry under carbon emission constraints. Appl. Energy 254, 113684. doi:10.1016/j.apenergy.2019.113684

IPCC (2022). Climate change 2022: Impacts, adaptation, and vulnerability. Contribution of working Group II to the Sixth Assessment Report of the Intergovernmental Panel on climate change. Editors H.-O. Pörtner, D. C. Roberts, M. Tignor, E. S. Poloczanska, K. Mintenbeck, A. Alegría, M. Craig, S. Langsdorf, S. Löschke, V. Möller, A. Okem, and B. Rama (Cambridge: Cambridge University Press). In Press. Available at: http://www.ipcc.ch/report/sixth-assessment-report-working-group-ii/.

Kätelhön, A., Meys, R., Deutz, S., Suh, S., and Bardow, A. (2019). Climate change mitigation potential of carbon capture and utilization in the chemical industry. Proc. Natl. Acad. Sci. U. S. A. 116 (23), 11187–11194. doi:10.1073/pnas.1821029116

Liang, R., and Zhang, L. (2013). Research on decoupling and rebound effect of carbon emissions from China's chemical industry from 1990 to 2008. Resour. Sci. 35 (02), 268.

Lin, B., and Long, H. (2016). Emissions reduction in China׳ s chemical industry–Based on LMDI. Renew. Sustain. Energy Rev. 53, 1348–1355. doi:10.1016/j.rser.2015.09.045

Lin, B., Zhang, L., and Wu, Y. (2012). Evaluation of electricity saving potential in China's chemical industry based on cointegration. Energy Policy 44, 320–330. doi:10.1016/j.enpol.2012.01.059

Ministry of industry and information technology (2016). Notice of the Ministry of industry and information technology on printing and distributing the development plan of petrochemical and chemical industry. Beijing, China: Ministry of industry and information technology.

National Development and Reform Commission. (2021). Operation of chemical industry in 2021. Available at: https://www.ndrc.gov.cn/fggz/jjyxtj/hgjjyx/?code=&state=123.

Park, S., Lee, S., Jeong, S. J., Song, H. J., and Park, J. W. (2010). Assessment of CO2 emissions and its reduction potential in the Korean petroleum refining industry using energy-environment models. Energy 35 (6), 2419–2429. doi:10.1016/j.energy.2010.02.026

The Central People’s Government of the People’s Republic of China (2022). The guiding Opinions on promoting the high-quality development of the petrochemical and chemical industry during the 14th five-year plan. (in Chinese) Available at: http://www.gov.cn/zhengce/zhengceku/2022-04/08/content_5683972.htm (Accessed July 5, 2022).

The European Chemical Industry Council Cefic (2013). European chemistry for growth: Unlocking a competitive, low carbon and energy efficient future. Brussels (Belgium): Cefic.

Wang, M., and Li, F. (2018). Development status and trend of fine chemical industry. Yunnan Chem. Technol. 45 (10), 21. (in Chinese). doi:10.3969/j.issn.1004-275X.2018.10.007

Wang, W. (2008). Obstacles and countermeasures of energy-saving technology progress in chemical enterprises. Mod. Chem. Ind. 28 (01), 2–7. (in Chinese). doi:10.16606/j.cnki.issn0253-4320.2008.01.025

Wei, Y., Liao, H., Yu, B., and Tang, B. (2018). China energy report green transition in energy intensive sectors. Beijing: Science Press.

Wen, Q., Zheng, B., Wang, Y., Zhao, W., Jia, L., Wang, M., et al. (2022). Discussion on carbon peak and carbon neutrality path in petrochemical and chemical industry. Chem. Ind. 40 (01), 12–18. (in Chinese). doi:10.3969/j.issn.1673-9647.2022.01.003

Keywords: chemical industry, carbon neutrality, carbon emission reduction path, CCUS, technology

Citation: Li Y, Mei Y, Zhang T and Xie Y (2022) Paths to carbon neutrality in china’s chemical industry. Front. Environ. Sci. 10:999152. doi: 10.3389/fenvs.2022.999152

Received: 20 July 2022; Accepted: 22 August 2022;

Published: 30 September 2022.

Edited by:

Jiashuo Li, Shandong University, ChinaReviewed by:

Yadong Yu, East China University of Science and Technology, ChinaLingna Liu, China University of Geosciences, China

Copyright © 2022 Li, Mei, Zhang and Xie. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Yan Li, MTAyOTg2ODUyOEBxcS5jb20=