Kuang-Cheng Chai

Kuang-Cheng Chai Jiawei Zhu

Jiawei Zhu Hao-Ran Lan

Hao-Ran Lan Yujiao Lu

Yujiao Lu Rui-Yang Liu

Rui-Yang Liu Pingshan Liu*

Pingshan Liu*- Business School, Guilin University of Electronic Technology, Guilin, China

This paper is based on “Opinion of the Audit-Commission on Strengthening Resource and Environmental Auditing” issued by the Audit Commission in 2009. The commission suggested studies on the impact of industrial structure upgradation in the manufacturing enterprises in China, based on 2006 to 2008 stocks of the listed companies in Shanghai and Shenzhen. Propensity Score Matching (PSM) and Differences-in-Differences (DID) were used to test the induced effect of the policy on industrial structure upgradation by comparing the experimental and control groups before and after policy implementation. The study found that government environmental auditing (GEA) upgrades the structure of the manufacturing industry. The data also reveals that the positive impact of GEA on the upgradation of industrial structure was significantly manifested in state-owned enterprises (SOEs). The findings validate the governance effect of GEA, expand the perspective of industrial structure upgradation in manufacturing enterprises, and provide suggestions on the regulatory effect in the industrial transformation of enterprises.

1 Introduction

In the 1970s, environmental auditing was first introduced in Western countries, providing a model for governments to implement environmental measures. INTOSAI established the Committee on Environmental Auditing (WGEA) in the 1990s and in 2001 published “Guidance for Conducting Audits from an Environmental Perspective”, this document was used as a basis for countries around the world to gradually establish their own GEA systems. The current environmental context in China is based on the fact that natural resources per capita are far below the international average, making it necessary to implement GEA. In recent years, China’s environmental pollution has become increasingly prominent and the state of the ecological environment is worrying. For a long time, China has been under increasing pressure to protect its ecology, deteriorating resources and environmental conditions, with restrictions being placed on the sustainable development of China’s economy and society. As a result, environmental auditing began to be developed by the Chinese government, and in September 2009, the Audit Commission published “Opinion of the Audit-Commission on Strengthening Resource and Environmental Auditing” (hereinafter referred to as the Opinion). The GEA refers to the supervision, evaluation, and identification of environmental problems and responsibilities arising from the environmental management and economic activities of the government, enterprises, and institutions by the national audit institutions. As an important environmental monitoring tool, GEA has a high level of authority to act as an environmental management tool, unlike other monitoring bodies. GEA is entrusted in an indirect manner to oversee exercise of environmental stewardship, with fiduciary responsibility as the main component. This is constitutionally mandated, and its level of supervision is at the highest level. Second, the GEA is more independent and explicitly requires inspection bodies at all levels to carry out their audit responsibilities. It is not enough if mere supervision of inspection associations or local governments is made since the local governments may collude with statistical departments and others to falsify data in carrying out their energy saving and emission reduction. Therefore, the GEA will effectively break this impasse and with its independence, can perform better supervisory function. In addition, GEA with its transcendent independence and strong economic oversight can act as a command-based environmental regulation tool, if implemented in the context of the macroscopic view, where the consequences of global warming have been highlighted by the destruction of the earth’s natural environment caused by humans in recent years. At the micro level, China’s environmental policy has long been dominated by command-and-control administrative measures, and the fact that China is in the middle of its industrialization process has left much room for economic transformation, making it possible to combine command-based environmental regulation instruments with the potential for economic transformation to adjust the status quo of an extensive economy.

With the development of the economy, the problem of resource scarcity and environmental pollution is gradually expanding, and as the industrialization era ends, the production method that relies on the consumption of resources, does not meet the market trends. According to the theory of public fiduciary responsibility, the authority given to government departments and institutions by the public is the basis for their role in maintaining social order and safeguarding the interest of society. The government introduced environmental regulation to give people a good and harmonious ecological environment. According to the theory of sustainable development, the quality of economic growth is emphasized along with development of enterprises, as the core of the country’s economic development, after manufacturing enterprises followed a traditional crude production method during the industrialization period. This production relied on a large amount of resource consumption, against the concept of harmony between human beings and nature and sustainable economic development. Therefore, similar to the GEA, the introduction of environmental regulation is essential. Previous studies on the effectiveness of implementing environmental regulation have given a wealth of experience on the feasibility of government policies. For example, in an earlier study, Porter and Vander (1995), argued through theoretical analysis and case studies, that environmental regulation not only improves environmental performance but also offsets additional regulatory costs. Ambec (2013) has also found that performance- or market-based environmental regulation was consistent with the growth of innovation. Due to differences in the domestic and international environments, domestic scholars have conducted research on environmental regulation policies; for example, Han Jing (2013) used panel regressions and causal identification to confirm that environmental regulation has an enabling effect on industrial structure upgradation. Wang Jingjing (2022) observed that environmental regulation has a positive effect on industrial structure advancement. The research results at home and abroad provide rich theoretical and practical support for this study. However, there is still a gap in research that combines environmental audit policy with industrial structure upgradation and there is also no research that accurately identifies the effectiveness of government environmental audits for manufacturing firms being the source of China’s environmental pollution. This study fills up these two gaps and adopts differences in differences (DID) to identify the impact of government environmental audit policies on the industrial structure upgradation based on the following considerations: 1. DID to a great extent avoids endogeneity, as policies are made by the state and are exogenous to microeconomic agents, and thus, do not suffer from reverse causality. 2. The traditional approach to policy evaluation is done through a dummy variable for the policy existence, but the DID approach combines the existence of a policy with the point of occurrence, and is more rigorous, scientific, and effective in assessing the effect. The implications of this study may include exploratory construction of a theoretical analysis framework consisting of theoretical and practical grounds, deepening the understanding of the mechanism of government audits in promoting industrial structure upgrading, and providing a solid theoretical foundation for government audits to promote national environmental governance and green development. It enriches research in the field of government environmental audit implementation. To this end, this study provides strong empirical evidence to support the environmental governance effects of government audits in the framework of the national system and from the mandatory policy implementation. The empirical results on government environmental audits and manufacturing sectors/enterprises show that government environmental audits significantly contribute to upgradation, and micro environmental governance effects. The data also show that the structural upgrading is more significant in state-owned enterprises, helping the government to consider its effectiveness in subsequent policy formulation implementing flexible environmental regulation, and helping to precisely identify the proprietary nature of enterprises.

The innovations of this study are: 1. Existing research on GEA focuses on both theoretical construction and practical operation, and lacks micro-empirical observation. In addition, it is necessary to consider whether the cost of upgrading the industrial structure can be lower than the fines paid for failing to meet environmental obligations and whether the benefits of upgrading the industrial structure are greater than that of the original production methods. This study combines national macro policies and micro enterprise data to examine the role of environmental audits in the industrial upgradation of manufacturing enterprises, combining Chinese institutional characteristics and market environment. The findings of this study are more reliable and scientific and provide input for the implementation of subsequent environmental regulations, such as the GEA, 2. The existing literature pays insufficient attention to GEA, due to the institutional characteristics and Chinese GEA policy for national environmental regulation. GEA has transcendent independence and a strong economic supervisory role, and their environmental governance is irreplaceable. This study treats GEA as an exogenous event, and as a quasi-natural-experiment, combined with the PSM-DID model analyzing the impact of policy on the industrial upgradation to mitigate endogenous problems, providing empirical evidence to reveal GEA effects. 3. Previous studies focus on manufacturing enterprises, which can accurately identify the effects of environmental regulation policies, and also explore the heterogeneity of proprietary rights to demonstrate the diversity of GEA impact, 4. China’s environmental pollution problem is increasingly becoming serious and relying on the industrial economic model has to shift to a high-tech economic model considering the environment and market. Industrial transformation and upgradation is the premise to realize the sustainable development of any enterprise. This study also investigates industrial structure upgrade to provide an empirical perspective to alleviate environmental pollution and acts as a driving force for the transformation and upgradation of manufacturing enterprises.

2 Literature review

2.1 Government environmental auditing

Compliance is a dynamic constraint in organizational behavior that changes as the organization adapts to changing societal values and norms. When an organization faces a compliance crisis, managers can align their business and objectives with socially accepted standards of compliance (Dowling, 1975). Buckley (1991) stated that GEA refers to the inspection, assessment, testing, or verification of the environmental management of an audited entity. Maltby (1995) pointed out that an environmental audit refers to assessing whether the environmental management of the audited unit complies with the relevant environmental laws and regulations and suggests improvements. Later on, some researchers believed that environmental auditing referred to the supervision and evaluation of the environmental management system of the government, enterprises, and institutions, as well as the environmental impact of economic activities by auditing institutions, internal audit bodies, and certified public accountants. Richard (1977), argues that environmental centralization is more conducive to avoiding incomplete enforcement by the local government governance and supervision. GEA is more independent (Mimeche, 2010) unlike other regulatory policies, governance and regulatory mechanism, and can break nexus between local governments and environmental protection departments. Besides, GEA can effectively monitor and play a stronger economic overseeing role (Rika, 2009), compared to that of traditional regulation which focusses on ex-ante assessment and emission monitoring. However, the reasonableness of the investment in environmental protection equipment and the operation and maintenance costs are not fully reviewed and assessed, whereas GEA using funds to audit procedures and methods in environmental protection can effectively compensate the shortcomings of other regulatory measures. Environmental auditing refers to the supervisory activity of auditing organizations and reviews their authenticity, legality, and effectiveness and implementation of policies. There are two types of environmental audits: mandatory and voluntary, which are based on different standard documents having different objectives but relying heavily on environmental auditors (Ruban, 2018). The GEA is based on environmental auditing with the addition of government restrictions, and has a certain degree of effectiveness since the Chinese federal government is the main body of the public economy. Its decision on the environment has a certain degree of compulsion. The audit policies introduced by the state not only play a role in environmental governance but also in combating corruption, promoting integrity, and enhancing government efficiency (Ferraz, 2011; Avis and Ferraz, 2018). As an external supervision mechanism, GEA plays a role in environmental regulation and has a significant impact on the construction of an ecological civilization (Jiang and Tan, 2020).

2.2 Government environmental auditing and industrial structure upgrading of manufacturing enterprises

Environmental regulations increase the cost of production in resource-intensive industries (Gary and Shadbegian, 2003) and they would change their production methods in the long run. In practice, the level of production technology is not static, but should be viewed from a dynamic perspective, and policy makers can effectively stimulate technological innovation by imposing reasonable environmental regulations, and compensate for the additional costs in the early years through the ‘innovation compensation’ effect (Porter, 1995). From the perspective of the innovation compensation and Porter’s hypothesis, environmental regulations can increase firms’ operating costs, reduce their R&D investment and competitiveness, and discourage industrial upgradation in the short run (Xin and Bowen, 2016). However, Porter 1995) argues that appropriate environmental regulations can stimulate firms to innovate and can make enterprises invest more in R&D to reduce operating costs, and this “push-back mechanism” can promote industrial upgradation by improving enterprises’ technological innovation. As environmental issues become more prominent, national policies on environmental constraints for enterprises are emerging, and strategic drivers based on green and low-carbon technologies play a key role in the innovation of technological capabilities of enterprises and contribute to the upgrading of industrial structures (Kivimaa and Kern, 2016). The audits improve environmental problems by correcting the deviation in local government environmental regulation (Xu et al., 2022). In terms of the external environment, flexible and differentiated environmental regulation policies can directly provide goals and directions for innovation and opportunities for innovation by tech firms (Joern, 2013) and moderate environmental regulation can stimulate firms’ innovation compensation effects (Doma-zlicky and Weber, 2004). Some scholars reported that the impact of environmental regulation on enterprise innovation is not a single linear relationship, but have a non-linear relationship, showing that regulation to a certain extent can contribute to better innovation (Ma and Li, 2021). The GEA, as an important national environmental governance and regulatory body, is believed to promote upgradation of industrial structure by forcing firms to engage in technological innovation and levying heavy penalties for non-compliance.

2.3 Summary of literature

First, GEA emerged earlier in Western countries, and the development of the theory and practice is mature, and audit techniques and methods have been applied to guide practical work, while China’s GEA policy started late and is still at the stage of exploration and development. Because of institutional differences, research on the effectiveness of environmental auditing implementation abroad cannot be applied to research on domestic auditing. That coupled with the fact that most of the previous domestic research has been theoretical investigation of the concept and significance of GEA lacking empirical evidence on environmental audits. Second, because of the lack of a precise definition of the nature, objectives, content, and methods of GEA, coupled with the difficulty in integrating disciplines and the fact that it involves many disciplines such as environmental management, environmental economics, and statistics, the previous research is still vague. Third, most of the earlier empirical studies on environmental regulation have been conducted on industry-wide samples, and the starting point of implementation is to restrict the highly polluting and high-emission enterprises through policy instruments. The inclusion of other non-polluting sectors is likely to bias the findings.

3 Theoretical analysis and hypothesis

3.1 Theoretical analysis of government environmental auditing

A part of the GEA theory explains the reasons, conditions, and influencing factors for the emergence and development of GEA. Public accountability arose from the development of the principal-agent theory. Since the 1960s and the 1970s, western scholars have proposed the concept of public fiduciary responsibility, pointing out that it refers to the economic responsibility of government departments and agencies entrusted by the public using resources to engage in the management of various social and public affairs. The purpose of the GEA is to promote the improvement of the government’s public fiduciary relationship and ensure effective implementation. Among other things, the full realization of the GEA function effectively improves the production structure of enterprises and ensures effective performance of the government’s public fiduciary responsibility with regard to environmental protection and management. The theory of sustainable development was put forward by The United Nations World Commission on Environment and Development (WECD) in 1987 emphasizing that the protection of natural resources and the environment should go hand in hand with economic development, in order to achieve sustainable development, promote economic and social development and improve the ecological environment as starting points. Environmental auditing determines the direct and ultimate purpose of GEA, which is important to achieve sustainable development as a model of economic growth. Therefore, based on the theory of public accountability and sustainable development, GEA is not only a channel to connect the government and the public but also an indispensable tool for economic development with respect to the environment.

3.2 Theoretical analysis of industrial structure upgradation of manufacturing enterprises

Existing research on the factors influencing the upgradation of the manufacturing enterprises involves the government’s environmental supervision policies, subsidies, environmental protection industrial policies, taxation, and internal governance of enterprises. The government’s supervision system has effectively promoted manufacturing enterprises to upgrade their industrial structure. Moreover, legitimacy theory states that the production and operation of enterprises should be carried out recognizing social values, first, by internal recognition, and second, by the trust from external stakeholders, so as to guarantee necessary resources for the development of an enterprise. The purpose of the business is to maximize the interests of the enterprise. Because of ecological problems, if manufacturing enterprises adopt the original production methods, then production cost will increase with a consequent reduction in efficiency, which is an unfavorable signal for both the internal operation and the external stakeholders. Thus, changing the production methods and upgrading the industrial structure is the most appropriate path in line with the direction of environmental and social development trends. When the state introduces GEA policies, it will inevitably impose constraints on the production processes and outcomes in the face of mandatory laws and regulations, resulting in two alternatives to choose from: either upgrading the industrial structure to improve production process, or reducing pollution emissions. Choosing the old production processes will result in paying large amounts for emission fees and enterprises not being able to bear the increased cost become insolvent and close. If an enterprise wants to continue its business, the most suitable way is to upgrade its industrial structure by improving their production processes. This requires significant capital investment, and the cash flow may not be sufficient to pay for R&D. If the government gives a certain amount of R&D subsidies, then, the resultant new technology and new resource pooling will be conducive to improve efficiency. This will also enhance enterprise productivity, efficiency of R&D, innovation, change the supply structure in a timely manner, respond quickly to market demand, and reshape the industrial structure to drive transformation in industry upgradation. Therefore, when enterprises face this crisis, the managers within the enterprises must take certain measures to manage legality, to ensure they follow environmental regulations in order to promote industrial upgradation. Based on the comprehensive analysis as stated above, this study proposes the following hypothesis:

GEA has a positive impact on upgrading the industrial structures of manufacturing companies.

4 Model data sources, variable selection and treatment

4.1 Data sources

This work focused on the study of industrial structure upgradation of manufacturing enterprises, and based on available data, the research samples of ST and *ST situations are excluded. Because of the small unbalanced sample size from manufacturing enterprises for empirical research, this study selected similar sample sizes from non-manufacturing industries (in the context of the financial crisis in 2008, many enterprises went bankrupt and collapsed, and in 2015, the introduction of structural supply reform and the re-introduction of General Secretary Xi Jinping’s policy of “Lucid waters and lush mountains are invaluable assets” resulted in a decline in the profits and the large scale shut down of major industries, such as steel, coal, and cement. Considering the adverse impact of unbalanced samples for study, this attempts to balance the selection of samples from manufacturing and non-manufacturing enterprises to ensure scientifically sound and authentic results are obtained). The samples from the manufacturing enterprises selected was larger than that of non-manufacturing enterprises because the focus of this study was on manufacturing due to the specificity of the policy. Data from 300 enterprises with 3,900 samples for the period 2006–2018 were finally screened. The data were from the corresponding economic data of listed companies in China’s Shanghai and Shenzhen stock markets, and the economic characteristics of listed companies from the China Stock Market and Accounting Research Database Center (CSMAR). Table 1 presents the variables.

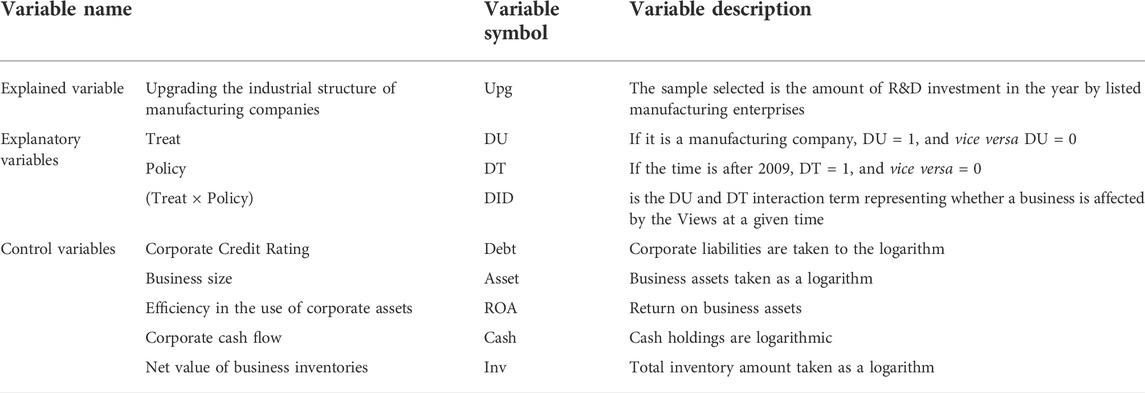

TABLE 1. Table of variable definitions.

4.2 Variable definitions

4.2.1 Explained variable

Measuring transformation and upgrading of the manufacturing industry is a difficult issue. Technological innovation is a manifestation of an enterprise’s upgradation of quality, including changes in products and processes, increasing investment in research and development, elevating industry from the middle and low to the high end of the value chain of the labor system through technological changes, promoting brands of high-quality products, improving the technological content of products and its function, and realizing upgradation. To address these issues, the extent of technological innovation in terms of innovation investment, using the total amount of dedicated R&D of listed companies was measured for technology innovation in the current year.

4.2.2 Explanatory variable

GEA refers to the supervision, evaluation, and authentication of environmental issues and liabilities arising from the environmental management systems and economic activities of governments, enterprises, and institutions by national auditing authorities in accordance with the law. To measure the role of GEA in the industrial structure upgradation of manufacturing enterprises, this study considered the Opinion expressed in 2009 as a quasi-natural experiment to investigate whether this has a promoting effect on the industrial structure upgradation, if the sampled year is after 2009 it is Treat = 1, and vice versa = 0.

4.2.3 Control variables

In this study, firm-level economic characteristics are chosen as control variables for the model. Debt, a logarithmic measure of firm liabilities, is used to measure a firm’s creditworthiness as is done for bank loans (Colombo et al., 2013). The larger the size of the enterprise, the more the amount spent on R&D investment, and the greater the effectiveness of upgrading the industrial structure. The utilization efficiency of the enterprise’s assets (ROA) as a control variable can reveal the degree of utilization. Hence, the ROA samples of heavily polluting listed companies are chosen as the control variable to measure the efficiency of the enterprise’s assets. The greater the cash flow of the enterprise (Cash), the quicker is the capital applied to the innovation. Therefore, the cash holding is selected as a control variable to measure and measure total corporate cash by taking the logarithm, represented by Cash. The net inventory value of the enterprise (Inv), assumes greater value with increasing inventory. An enterprise with more inventory is less likely to be sustainable and is expressed in logarithmic terms as Inv.

4.3 Model construction

In the 1980s, DID method was developed in foreign economics, based on effectiveness in the natural sciences (Ashenfelter, 1978, 1985) to evaluate the effects of policies and are widely cited. In an earlier study, Card and Krueger, (1994) used the DID method to calculate the effect of a minimum wage increase in New Jersey. Later, this method was widely used in policy research. From an econometric view point, the DID is a comparatively static method of regression using individual data, which avoids the endogeneity problems associated with the traditional method of treating policy as an “independent variable.” This study empirically tests mechanisms and transmission channels through which GEA affects the upgradation of industrial structure of manufacturing enterprises by constructing the econometric model shown in Eq. 1 stated below. The DID model used is as follows:

where Upgit denotes the indicator of industrial structure upgradation of manufacturing enterprises, DT is a time dummy variable; if the sample year is after 2009, DT = 1 and vice versa = 0; DU is a dummy variable that distinguishes the experimental group from the control group; if it is a manufacturing enterprise, DU = 1 and vice versa = 0; controlit is a control variable; and fe denotes a fixed effect.

5 Empirical analysis

5.1 Descriptive analysis

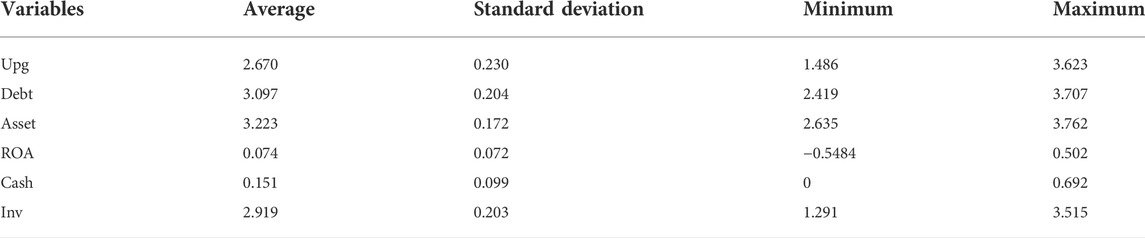

The descriptive statistics of the selected variables are shown in Table 2. The mean value of the ratio of the number of industrial upgrades is 18.469, which indicates that the Chinese manufacturing industry has been upgraded to a certain extent during the period from 2006 to 2018. The maximum value of an enterprise’s return on assets was 0.503 and the minimum value was –0.645, indicating a large variation and a negative return on assets, indicating that the assets invested were not well paid for. The minimum value of the logarithm of cash taken by enterprises is 0, which means that some enterprises do not have good capital flow efficiency, and there is a certain difference between the maximum and minimum values of the logarithm of enterprises’ cash, indicating large difference in the capital flow efficiency of these enterprises.

TABLE 2. Descriptive analysis.

5.2 Baseline regression results

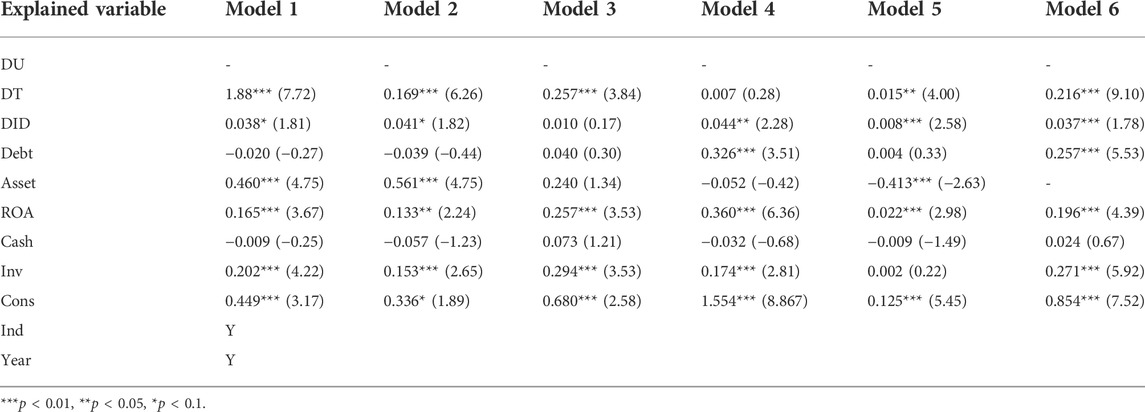

This study first conducted a benchmark regression on the impact of GEA policies on the industrial structure upgradation using the DID model (as shown in Table 3). Model 1 shows the regression results of the fixed-effects model controlling time and industry. The results reveal that the coefficient of the impact of the GEA policy on industrial structure is significantly positive at the 10% level and this opinion indicate the promotion of industrial upgradation to a certain extent.

TABLE 3. Benchmark regression results.

5.3 Heterogeneity analysis

The varied nature of shareholding implies different positioning of enterprises. Owing to the special ownership relationship of SOEs, they produce and operate in response to the state’s call, and the requirements of state policies are more prudent and stricter for SOEs. In terms of implementation, if the expected results of the policy are not achieved, then the public officials in SOEs become accountable and they take certain environmental management measures to meet the standards. Table 3 reports the results of the heterogeneity regressions for the nature of enterprises by dividing the national sample into SOEs and non-state-owned enterprises (NSOEs). As shown in Table 3, the impact coefficient of GEA is significantly positive for both SOEs (Model 2) and NSOEs (Model 3), indicating that opinion plays differently in enterprises with different equity due to the fact that SOEs have a strong political affiliation and are subject to better control by the local government, and they will ensure SOEs achieve their social responsibility. Therefore, compared with that of NSOEs, SOEs will invest more in R&D and effectively upgrade their industrial structure.

5.4 Robustness test

5.4.1 Substitution of variable

A stability test was carried out twice by replacing the variables to test the reliability of this study. The first test replaced the dependent variable with labor productivity, which not only reflects the productivity of a company but also its employee structure, resource allocation efficiency, and operational capacity measured by output per capita (business revenue/number of employees in employment). The second test replaced the dependent variable with a relative indicator of R&D investment/assets and the regression results (Model 4 and Model 5), remained similar and consistent with that of previous reports.

5.4.2 Propensity score matching

To reduce bias in sample selection, an endogeneity test was performed using PSM-DID. The control variables selected are corporate credit rating (Debt), corporate asset utilization efficiency (ROA), corporate cash flow (Cash), and corporate net inventory value (Inv) as PSM matching covariates to avoid bias, control of individual and annual fixed effects to obtain the propensity score predicted by the model, and conducting a 1:1 best-neighborly match for listed companies in the manufacturing and non-manufacturing industries. Based on these, the matched samples are used for regression analysis. The regression results are shown in Model 6, where the impact of GEA policies on manufacturing firms’ industrial structure upgradation remained consistent with the main test.

6 Conclusions, discussion and suggestions

Conclusions: The Chinese economy has made remarkable progress after reforms and is opening up. With rapid economic development, pollutant emissions in China have become serious. Therefore, this study explored the impact of GEA on upgrading the industrial structure of manufacturing enterprises. After a series of analyses, it was found that manufacturing enterprises have significantly upgraded under this policy implementation. The difference compared to other studies is that the sampling in this study combines the nature of the policy with a high degree of precision in implementation, giving a more accurate picture. Further research found that the impact of policy environmental audits on the upgradation of the industrial structure of manufacturing enterprises is more significant in SOEs, which is explained by the fact that the implementation of national policy is more stringent and effective for SOEs than that for NSOEs. The NSOEs may require additional R&D investment to achieve the expected results. This study also integrates Chinese institutional characteristics considering the diversity of the implementation effects on GEA environmental regulations in different national environments, and bridges the gap in the lack of integration of institutional characteristics such as theoretical and practical significance as per earlier reports.

Discussion: The role of GEA in promoting the structure upgradation of the manufacturing industry can be analyzed in two ways: 1. As an environmental regulatory policy introduced by the state, the GEA is mandatory for enterprises to fulfil their environmental responsibilities. As a socialist country, China’s government policies are mandatory and the intensity of GEA, penalties, and judicial force make enterprises active in fulfilling their environmental responsibilities. These also make them to invest more funds in environmental protection for building future projects and promoting industrial transformation. 2. The need for enterprises to continue their business development. As industrialization is coming to an end, resource-consuming enterprises go against environmentally sustainable development on the one hand, and on the other, GEA increases the environmental costs. Relying on information technology can enable enterprises to reduce their environmental costs by changing their production mode and adopt new structures.

The findings of this study have implications at both the macro and micro levels of management: 1. At the macro level, China is a socialist, publicly owned state, and the government is the organ that expresses its will, issues orders, and conducts affairs. The policies implemented by the Chinese government are mandatory and independent. Owing to its inviolable nature, the government should fully consider the applicability of its policies when formulating them. It should fully understand the market situation in formulating policies and implement a diversified environmental audit, considering their previous experiences on regulation. During implementation it should keep in mind that the environmental costs will be high due to excessive enforcement that may impede upgradation. To overcome these, subsidies should be given to push structural upgradation. After the implementation, the government should take the opportunity to introduce GEA and corresponding operational guidelines to promote its rapid development. 2. As a socialist public sector country, China has a policy-oriented environmental regulation that can impose greater constraints on the environmental awareness of enterprises through strong government enforcement. In such an institutional environment and business, the Chinese federal government should fully understand national policy information and market dynamics, with a high degree of political sensitivity. Considering an enterprise’s own constraints, the managers should understand the life cycle of the enterprise in order to decide the cost of implementation whether weak or strong, based on available funds. When faced with national environmental regulation, they can follow the policy concept and actively upgrade their industrial structure. However, if the life cycle of an enterprise is nearing maturity, decline, or decay, it faces greater risks in the process of upgrading and transforming its industrial structure, and therefore should take a conservative approach in implementing national environmental regulation.

The findings of this study have social implications: as the country develops and the era of industrialization coming to an end with resources in short supply, industrial upgrading is imperative. However, the business objective is to maximize profits and it is difficult to accomplish industrial upgrading solely on the basis of the degree of corporate consciousness, and hence the introduction of government environmental policy is essential. The results show that GEA has a positive impact on upgrading the industrial structure of manufacturing enterprises. There are differences between GEA and other environmental regulation policies, which helps to identify whether there is a need for diverse environmental regulation to alleviate environmental pollution and reduce resource deficiencies. These would help the government to observe social dynamics during policy implementation; understand the impact and effectiveness on enterprises, and help the government to provide subsidies in the future.

Suggestions: Based on the above findings, this study proposes the following. First, to promote the upgradation of industrial structure through precise environmental regulations. On the one hand, a moderate and reasonable environmental regulation policy can promote upgradation of the industrial structure and eliminate outdated production capacity. On the other hand, giving full consideration to the heterogeneity of proprietary rights, such as command-and-control type of environmental regulation policy to the manufacturing industries and SOEs, and considering difference between the result and policy goals, the government should be flexible when formulating environmental policy, improve environmental protection, implement different environmental regulations, especially for the manufacturing industry and SOEs, further expanding the scope of regulation to improve efficiency. This will also result in possible reductions in the scale of economic development. Second, diversification policies are combined to reshape the industrial structure. Effective environmental policies are highly unified between restrictions and incentives. While implementing strict environmental restrictions, an environmental policy should be established with regulations as the mainstay and government subsidies as supplements. Strict GEA restricts enterprises’ pollutant discharge behavior, and reasonable government subsidies encourage enterprises to increase their investment in industrial research and development. For technology-intensive industries, because of their high-tech content and low pollution emission, the elasticity coefficient of subsidies is low and hence moderate and stable R&D subsidies should be maintained. For resource-consuming labor-intensive, and pollution-intensive manufacturing industries, owing to their low technology and high emissions, further increase in subsidies will help enterprises actively reduce pollutant emissions and improve their independent green research and development capabilities. In addition, the combination of diversified policies reflects the coordination and supplementation of different types of environmental regulations. Only the reasonable composition of “mandatory” and “incentive” regulations can effectively promote the transformation of China’s economy to high quality. Third, implementing environmental regulation, in order to get positive feedback is a long-term process. To achieve this, the government can strengthen publicity, industry transformation, and continue to guide enterprises to form a new mode of industrial development and transformation, and stimulate enterprises to protect the endogenous environment, improve the enthusiasm of increasing enterprises’ environmental costs to realize positive cycle. The government has formulated policies for personnel training and introduction in order to expand their knowledge, talent and technology to strengthen their core competitiveness and promote technological innovation. In the era of the green economy, it is important to know how to push forward green innovation as a development goal. Long-term development will ensue only by adhering to the concept of innovative development and actively implementing industrial transformation.

Limitations: This study has certain limitations. First, because the policy is old and the rapid changes in the country in recent years, the study of the relationship between the Opinion and industrial upgrading has less significance for the subsequent introduction of relevant regulation policies; second, the absence of some samples and reduction in sample size is because the information disclosed on structural upgrading of few manufacturing enterprises is not comprehensive.

Future research: Environmental problems go hand-in-hand with economic development, and relying on environmental regulation to alleviate environmental pressure is in line with China’s socialist national policies. Based on the results obtained, the following research directions can be outlined. First, to integrate and categorize the channels through which policy affects industrial structure. Second, many different channels through which policy affects industrial structure. And a single window for one or several channels cannot determine policy effects. In future, the channels influencing policy can be integrated and categorized, with each category consisting of systematic and complete secondary indicators, which will improve the accuracy of policy and innovation. Industrial structure upgradation is a broad concept, and refers to the upgradation of enterprises through technology, management, enterprise structure change, product quality, production efficiency, and industrial chain. It also refers to the technology for industrial chain positioning, value added products of major enterprises thus enabling the rise to a new level. The diversity of policy without a clear definition makes the upgrading of industrial structure difficult since it relies only on indicators to measure. Future research can clarify the concept of industrial structure upgrading and establish a unified framework for the integration of the transformation process hierarchy, which can greatly reduce the degree of bias in green innovation-related research. Third, it is important to distinguish the differences in GEA policies. In the context of China’s current political system and ecological environment, the government is constantly introducing environmental regulations with the goal to alleviate environmental pressures and innovate production methods; however, the boundaries between the different environmental policies are blurred, and subsequent environmental regulation policies will follow. Therefore, it is important to clarify the specific content of these policies and to distinguish between GEA policies and other environmental regulations to avoid getting inaccurate research results.

Data availability statement

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding author.

Author contributions

K-CC and PL are responsible for article writing coordination, JZ is responsible for overall article writing, and others are responsible for data collection.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Supplementary material

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenvs.2022.995310/full#supplementary-material

References

Ashenfelter, O. C., and Card, D. (1985). Using the longitudinal structure of earnings to estimate the effect of training programs. Rev. Econ. Stat. 67 (4), 648. doi:10.2307/1924810

Ashenfelter, O. C. (1978). Estimating the effect of training programs on earnings. Rev. Econ. Stat. 60 (1), 47. doi:10.2307/1924332

Avis, E. C., Ferraz, F., and Finan, F. (2018). Do government audits reduce corruption? Estimating the impacts of exposing corrupt politicians[J]. J. Political Econ. 126 (5), 1912–1964. doi:10.1086/699209

Card, D., and Krueger, A. B. (1994). Minimum wages and employment: A case study of the fast-food industry in New Jersey and Pennsylvania[J]. Am. Econ. Rev. 84 (4), 772–793.

Colombo, M., Groce, C., and Guerini, M. (2013). The effect of public subsidies on firms' investment-cash flow sensitivity: Transient or persistent[J]. Res. Policy 42, 1605–1623. doi:10.1016/j.respol.2013.07.003

Doma-zlicky, B. R., and Weber, W. L. (2004). Does environmental protection lead to slower productivity growth in the chemical industry[J]. Environ. Resour. Econ. 28 (3), 301–324. doi:10.1023/b:eare.0000031056.93333.3a

Dowling, J. (1975). Organizational legitimacy: Social values and organizational behavior. Pac. Sociol. Rev. 18 (1), 122–136. doi:10.2307/1388226

Ferraz, C., and Finan, F. (2009). Electoral account ability and corruption: Evidence from the audits of local governments[J]. Natl. Bureau Econ. Res. 101 (4), 1274–1311. doi:10.1257/aer.101.4.1274

Gary, W. B., and Shadbegian, R. J. (2003). Plant vintage, technology and environmental regulation[J]. J. Environ. Econ. Manag. 46 (3), 384–402. doi:10.1016/S0095-0696(03)00031-7

Jiang, Q., and Tan, Q. (2020). Can GEA improve static and dynamic ecological efficiency in China? Environ. Sci. Pollut. Res. 27, 21733–21746. doi:10.1007/s11356-020-08578-7

Jiang, Q., and Tan, Q. (2021). National environmental audit and improvement of regional energy efficiency from the perspective of institution and development differences. Energy 217, 119337. doi:10.1016/j.energy.2020.119337

Kivimaa, P., and Kern, F. (2016). Creative destruction or mere niche creation? Innovation policy mixes for sustainability transitions[J]. Res. policy (45), 205–217. doi:10.1016/j.respol.2015.09.008

Ma, H. D., and Li, L. X. (2021). Could environmental regulation promote the technological innovation of China’s emerging marine enterprises? Based on the moderating effect of government grants[J]. America: Environmental Research, 202.

Maltby, J. (1995). Environmental audit: Theory and practices. Manag. Auditing J. 10 (8), 15–26. doi:10.1108/02686909510147372

Mimeche, J. D. (2010). Environmental auditing practice[J]. Water & Environ. J. 7 (1), 32–36. doi:10.1108/02686909510147372

Porter, E., and Vander, L. C. (1995). Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 9 (4), 97–118. doi:10.1257/jep.9.4.97

Richard, B. (1977). Stewart. Pyramids of sacrifice? Problems of federalism in mandating state implementation of national environmental policy[J]. Yale Law J. 86 (6), 1196–1272. doi:10.2307/795705

Rika, N. (2009). What motivates environmental auditing? Pac. Account. Rev. 21 (3), 304–318. doi:10.1108/01140580911012520

Ruban, A., and Ryden, L. (2019). Introducing environmental auditing as a tool of environmental governance in Ukraine. J. Clean. Prod. 212, 505–514. doi:10.1016/j.jclepro.2018.11.059

Xin, Z., and Bowen, S. (2016). The influence of Chinese environmental regulation on corporation innovation and competitiveness[J]. J. Clean. Prod. 112, 1528–1536. doi:10.1016/j.jclepro.2015.05.029

Keywords: goverment, PSM-DID, environmental auditing, manufacturing enterprises, industrial structure upgrading

Citation: Chai K-C, Zhu J, Lan H-R, Lu Y, Liu R-Y and Liu P (2022) Effectiveness of government environmental auditing in the industrial manufacturing structure upgradation. Front. Environ. Sci. 10:995310. doi: 10.3389/fenvs.2022.995310

Received: 15 July 2022; Accepted: 29 September 2022;

Published: 11 October 2022.

Edited by:

Tieyu Wang, Shantou University, ChinaReviewed by:

Mário Nuno Mata, Instituto Politécnico de Lisboa, PortugalBilal, Hubei University Of Economics, China

Copyright © 2022 Chai, Zhu, Lan, Lu, Liu and Liu. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Pingshan Liu, cHMubGl1QGZveG1haWwuY29t