94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 12 January 2023

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.993931

Zhen Deyun1,2

Zhen Deyun1,2 Pan Yiqing3*

Pan Yiqing3*As China’s economy enters a new era, fiscal pressure is growing rapidly. How will local governments select their preference of tax efforts under pressure? Are they facing or retreating? This paper selects macro data of 30 provincial administrative regions from 2000 to 2018 and uses the instrumental variable method and threshold regression model. While the paper put fiscal pressure, land-transferring fees, local government debt, and transfer payments into the same regression equation to test the causal relationship between fiscal pressure and the selection preference of tax efforts among Chinese local government. We found that local governments prefer to increase tax efforts under fiscal pressure. Moreover, the heterogeneity analyses prove that eastern local governments prefer higher tax efforts. When the tax and economic growth rates are low, local governments have less selection preference to strengthen tax efforts. Threshold regression tests show that transfer payments have a moderating effect on local tax efforts, and transfer payments have a threshold effect. When transfer payments are under the minimum threshold value or above the maximum threshold value, it may lead to the inaction of local governments, who do not try their best to raise tax efforts. These findings are valuable in policy-making for the construction of sustainable public finance.

As China’s economic development enters a new era, problems of fiscal pressure grow rapidly. In particular, the global spread of COVID-19 in 2020 has significantly impacted on both the production and consumption end of economic activities (Wang and Su, 2020; Hao et al., 2023). It also caused a red light to the local fiscal, which has put a pause button on the Chinese economy, which has just stepped on the right track. According to the data released by China Statistical Yearbook 2021, the fiscal revenue of China’s public budget in 2020 was 18,291.39 billion yuan, with a growth rate of −3.9%, which was the first negative growth of fiscal revenue since 1978. The fiscal expenditure of the public budget was 24,567.90 billion yuan, with a growth rate of 2.9%. The government deficit reached 6,276.51 billion yuan, a record high since 2004. Especially under the impact of COVID-19, the economy and society need a more extended period of recovery, and the contradiction between fiscal revenue and expenditure cannot be alleviated temporarily or even is growing. Against this background, it is considered critical to stimulate the local government with an internal impetus to ease the fiscal pressure, which prevents systematic financial risk and boosts the role of financial governance in the country. Therefore, high-quality economic and social development is within reach.

Since the Tax-Sharing Reform, taxes, land-transferring fees, local government debt, and transfer payments have become the main fiscal policy tools for local governments to raise fiscal funds and relieve fiscal pressure (Bird and Tarasov, 2004; Qun et al., 2015; Bai et al., 2019; Tang et al., 2019; Cheng H. et al., 2022). Different local governments have heterogeneous preferences in the choice of fiscal policy tools. Some local governments prefer solidifying fiscal policy tools, while others prefer discretional ones (Chen et al., 2022; Cheng Y. et al., 2022; Wu et al., 2022). However, local governments have always regarded tax as the most potential intrinsic policy tool, no matter solidified fiscal policy tool or a discretional fiscal policy tool. That can be seen from the “movement-style” investment attraction from local governments because such attraction is essentially a kind of tax competition among local governments for high-quality tax resources. Because of such fierce tax competition, local governments see changing the tax efforts as essential in tax competition. They often urge tax authorities to strengthen tax collection and administration with administrative tax tasks. However, will tax efforts be enough in the face of rising fiscal pressures? Or is fiscal pressure an intrinsic incentive mechanism for tax efforts? With regard to this, some scholars1 empirically tested the correlation between fiscal pressure and tax effort. She confirmed that fiscal pressure positively correlates with tax effort. However, in the traditional literature, there are several deficiencies in the research on the effect of fiscal pressure on tax efforts. First, these studies did not incorporate fiscal pressure, transfer payments, local debt, and land-transferring fees into a unified framework. In other words, they do not exclude the impact of other fiscal policy tools on tax efforts. Such an empirical test can hardly be called a causal test, and its empirical research conclusion is more likely to have an estimated error. An estimated error may mislead the selection preference of local governments. Second, formal studies generally start from the overall and geographical position perspective to study the impact of fiscal pressure on the selection preference of local governments’ tax efforts. They ignore that the differences in tax growth will affect the selection preferences of tax efforts among local governments under fiscal pressure. Specifically, some local governments prefer to face the pressure and increase tax efforts when fiscal pressure rises. Some local governments prefer to retreat from difficulties and adopt a negative tax collection strategy. Third, transfer payment is one of the central fiscal policy tools. However, the traditional literature has ignored the vital role of transfer payment in the process of fiscal pressure affecting the selection preferences of tax efforts among local governments.

This paper tries to make up for the above three deficiencies. The research contribution is as follows: First, from the selective perspective of research, fiscal pressure, transfer payment and tax effort are incorporated into a unified theoretical analysis framework to avoid the serious deviation of single indicator for the calculation results of tax efforts and estimated error. This paper overcomes the narrowness of previous studies which only focus on a certain influence variable. It clarifies the impact of various factors on tax efforts from a theoretical viewpoint. Second, from the perspective of heterogeneity of tax growth, this paper studies the differences in the selection preference of tax efforts among different local governments under fiscal pressure. It expands the research perspective of traditional literature. Third, the paper revealed that transfer payment has a negative moderating effect and threshold effect on the selection preference of tax efforts among local governments affected by fiscal pressure by comprehensive use of the moderating effect test and the non-linear threshold model effect test. From the perspective of practical significance, it not only deepens the interpretation of the effect of fiscal pressure on tax efforts but also provides a reference for local governments to select tax efforts in the future.

The rest of the structure of this paper is as follows: the second chapter puts forward the research hypothesis through theoretical analysis to discuss whether it is necessary to strengthen tax efforts when the fiscal pressure of local governments increases; The third and fourth chapters set up the econometric model and test the empirical results to verify the theoretical hypothesis of the second part; In the fifth chapter, the panel threshold model is used for further analysis; The sixth chapter is the conclusion and suggestions of the full text.

Since the reform of the tax-sharing system in 1994, the Chinese government has established a fiscal and taxation system framework dominated by tax sharing and supplemented by transfer payment. The year 2020 works as an example. The central government’s revenue concentration ratio is 45.25%, and the proportion of expenditure is 14.29%, while the proportion of local government fiscal is 54.75% and 85.71% respectively. The gap between revenue and expenditure is as high as 30 percent.2 This model causes inefficient use of tax money from the central government’s perspective and a deficit for local governments. It deviates significantly from the principle of matching financial authority and financial power pursued by the institutional design, and the local governments bore more responsibilities with a limited budget (Lin and Zhang, 2015). In order to make up for this deviation, and try to obtain transfer payment funds, local governments prefer to choose financial policy tools such as local government debt and land-transferring fees to obtain financial funds and resolve fiscal pressure. These financial policy tools restore the fiscal imbalance of governments to some extent, play the role of a financial equalizer, and make up the fiscal gap moderately (Han and Kung, 2015). However, the transfer payments may cause moral hazard problems such as “public pools” and “soft budget constraints,” thus distorting the behaviors of local governments (Eyraud and Lusinyan, 2013), and inducing the greater risk of fiscal pressure. Local government debt also has its drawback. First, a current debt must repay the previous debt and its interest, and the current debt will only increase future fiscal pressure. Relying on borrowing new debt to repay old debt for an extended time is like drinking poison to quench thirst (Cheng H. et al., 2022). Second, long-term high-level debt overhangs the local government may eventually hinder China’s efforts to alleviate the imbalance of economic structure (Tsui, 2011), and the effect of issuing debt to reduce fiscal stress is diminished. The land economy has been generally favored by local governments for some time and has become an essential tool to obtain development funds. However, when “houses are for living in and not for speculative investment” becomes the leading tone of the real estate industry regulation, land finance has gradually stepped down. In addition, tax competition to promote local economic growth, promotion incentives for officials, and investment impulse all have significant and steady promoting effects on the land economy (Qun et al., 2015). Fiscal pressure may not be the real motivation for the land economy. Unlike the three fiscal policy tools of transfer payment, local government debt, and land-transferring fees, tax has always been an essential part of the national economy. It plays a fundamental pillar and guarantees a role in national governance. A country’s tax revenue growth depends not only on the tax base and structure but also on the level of tax collection and administration (Mukherjee, 2017). There is a certain “tax collection and administration space” in the design of China’s tax system. Local governments can promote tax growth by strengthening tax collection and administration (Gao, 2006). Therefore, local governments prefer strengthening tax efforts to relieve financial pressure, which has been regarded as an important way to build sustainable public finance.

As an important way to build sustainable public finance, tax efforts have always been a hot topic. Scholars explore the influencing factors of tax efforts from different dimensions. First, from the perspective of tax sharing reform, study its impact on tax efforts. Huang et al. (2012) believed that optimizing fiscal decentralization improved local governments’ tax efforts. However, Bird et al. (2006) found that fiscal decentralization had no statistically significant impact on tax efforts, no matter whether they were measured by the ratio of tax revenue to GDP or the ratio of current revenue excluding grants to GDP through empirical research. Secondly, from the perspective of the impact of the transfer payment system on tax efforts, some scholars reckoned that the more transfer payments from the central government, the lower the enthusiasm of local governments in tax collection and administration (Litvack et al., 1998; Baretti et al., 2002; Panda, 2009; Mohanty et al., 2020). Some scholars oppose that when the transfer payment of the central government is reduced, local governments will increase their financial efforts to obtain more revenue to make up for the shortage caused by the transfer payment reduction. Therefore, transfer payment has a positive incentive effect (Buettner, 2006; Egger et al., 2010; Sobel and Crowley, 2014). Liu and Zhao (2011) discussed the impact of total transfer payment, equal transfer payment and, tax rebates on the tax efforts of the local government. The research results show that the first two will inhibit the tax efforts of local government, while tax rebates have a positive incentive effect on tax efforts (Liu H. et al., 2022; Xue et al., 2022). The third dimension discusses the impact of fiscal imbalance or fiscal pressure on tax efforts. The main view is that the vertical fiscal imbalance will inhibit the tax efforts of local governments (Boetti et al., 2012; Jia and Ying, 2016), and the horizontal fiscal imbalance amplifies the negative impact of the vertical fiscal imbalance on the tax efforts of local governments (Di Liddo et al., 2019). A few scholars believe that when the local fiscal pressure increases, the tax efforts of the local governments will also increase (Chen, 2017; Dang et al., 2019; Xiao and Shao, 2020). However, Ma and Li (2012) believed that local governments would not only maintain tax collection and administration under fiscal pressure but also directly transfer the pressure to enterprises.

Scholars believe that fiscal pressure has certain impacts on the tax efforts of local governments, but whether the impact effect is facing or retreating is still controversial. The possible reason is that the taxation behavior of local governments is the result of the joint action of many factors, such as fiscal pressure, fiscal policy tools, and economic development. These papers have made a univariate analysis of whether fiscal pressure inhibits or stimulates the tax efforts of local governments. In their research, some scholars have also analyzed the substitution effect of different fiscal policy tools on tax efforts. However, few scholars analyzed the impact of fiscal pressure on local government taxation from the two essential aspects of fiscal policy tools and the imbalance between revenue and expenditure. The previous research did not include fiscal pressure, transfer payment, local government debt, and land-transferring fees into a unified regression equation for analysis. They lack research on whether the substitution effect brought by other fiscal policy tools plays a regulatory role in this impact mechanism.

Tax revenue occupies the main position of fiscal revenue and plays a vital role in ensuring fiscal revenue and coping with more significant fiscal pressure. There are three main ways to increase tax revenue: first, the level of economic development, such as economic growth, industrial structure upgrade, foreign trade improvement, an increase of economic benefits of enterprises, improvement of the degree of marketization, which promotes a significant increase in the tax base, followed by a significant increase in tax revenue (Arvin et al., 2021). However, China’s economic growth is currently slowing down, and there is great pressure on the economic downturn. It is difficult to increase tax revenue by relying on economic growth in the short term. Second, tax system factors include the choice of tax types, the design of tax rates, and differences in tax structure (Lu and Guo, 2012). However, China’s tax category, rate, and scale are all decided by the central government, and local governments have no right to determine the composition and scale of their tax revenue. Third, adjust the level of tax collection and administration (Zheng et al., 2022; Zhu and Yang, 2022). China’s tax collection and administration law stipulates that local governments are responsible for leadership, implementation, coordination, and supervision of local tax collection and administration (Huang and Soyano, 2022). Affected by the particular national conditions, China’s current tax system has a “tax collection and administration space,” the difference between the actual tax burden and the legal tax burden, which provides an effective way to adjust the level of tax collection and administration (Gao, 2006). Tax authorities and their staff have certain discretion in tax collection and administration and have flexibility in tax collection and administration (Liu J. et al., 2022).

So how will local governments choose their tax collection and administration policies to deal with the increasing fiscal pressure? On the one hand, when local governments face more significant fiscal pressure, they usually require the tax department to complete higher tax tasks (Yu et al., 2018). In the face of heavy tax pressure, the tax department may strengthen the tax collection and administration, standardize the tax behavior of enterprises, strictly supervise tax evasion, improve the degree of tax efforts, and achieve “all taxes due are collected,” to complete the tax tasks assigned by the local government. On the other hand, local governments may reduce the actual tax burden of enterprises by reducing the efficiency of tax collection and administration, attracting more enterprises, and increasing the tax base (Jia and Ying, 2016). Relaxed tax collection and administration policies are conducive to attracting investment and promoting local economic development. In addition, the normalization of extra-budgetary revenue is lower than that of tax. In terms of project approval and collection standards, the extra-budgetary revenue of local governments have greater financial autonomy. From the perspective of official political competition, local governments will strive to pursue more economic resources and find ways to break budget constraints. Therefore, local governments may use extra-budgetary revenue as a substitute for tax revenue, thus reducing the enthusiasm of tax efforts. In other words, the decision maker’s choice of tax effort results from psychological comparison, and there is a selection preference. This paper puts forward the following competitive hypothesis based on the above analysis.

Hypothesis 1a Fiscal pressure may increase tax efforts.

Hypothesis 1b Fiscal pressure may inhibit tax effort.

The fiscal pressure caused by the imbalance of fiscal revenue and expenditure may promote or inhibit the tax efforts of local governments. Will the three fiscal policy tools of transfer payment, local government debt, and land-transferring fees weaken or strengthen this influence mechanism, to produce a moderating effect? Superficially, transfer payment, local government debt, and land-transferring fees are equivalent to adding additional fiscal revenue to local governments. The funds obtained from these three ways may have a substitution effect on tax efforts which could have weakened the promotion of fiscal pressure on tax efforts. However, only transfer payments may have a sustained moderating effect for the following reasons.

One is substitution cost. The transfer payment is a system in which the central government allocates part of the central fiscal revenue to local governments to compensate for the gap between local fiscal revenue and expenditure. For local governments, the transfer payment cost is almost negligible (Xie and Fan, 2015). However, local governments need to repay the interest and return the principal. The land transfer cost is the government’s compensation expenditure to compensate farmers or urban enterprises and residents due to land transfer. Based on the hypothesis of rational revenue maximization, local governments may prefer to use cost-free transfer payment instead of cost tax efforts which inflict costs (Liu and Zhao, 2011). Unless the cost of local government debt and land-transferring fees is lower than the tax cost, it may produce a substitution effect. However, the cost of the first two will also fluctuate greatly with economic fluctuations. Therefore, they are not robust even if local debt and land-transferring fees occasionally produce a moderating effect.

Second, sustainability. The central government dominates the transfer payment system to specifically deal with the imbalance of local fiscal revenue and expenditure. The central allocation policy can be directly transmitted to the local government without the interference of local administrative levels, which has long-term stability. As a natural resource, the endowment of land is limited, and the transfer of land depends on one-time financial revenue and cannot rise indefinitely. Therefore, there is an upper limit on land transfer. In addition, structural imbalance, lack of dynamic mechanisms, low-income efficiency, and unstable land financing have seriously hindered the sustainable development of land finance (Geng et al., 2018). There is also a theoretical upper limit for local government debt. A moderate level of local government debt can improve welfare and promote growth. Once the local government debt exceeds a certain level, it will produce debt risk, affect the normal financial operation, and drag down economic growth (Checherita and Rother, 2012). Although, local governments will reduce the cost of debt repayment through debt replacement which repays old debts with new debts. But with the increasing pressure of the economic downturn, the theoretical debt ceiling of local governments will be gradually reduced, which will bring about the debt sustainability problem. This paper believes that local government debt and land-transferring fees do not have a scientific, stable and, sustainable moderating effect. However, to eliminate the possible direct impact on tax efforts in individual years or provinces, local government debt and, land-transferring fees are listed as control variables in subsequent empirical research to avoid estimation errors in the research results.

As the transfer payment will change the tax revenue sharing relationship between the central and local governments, if the local governments take the transfer payment from the central government as a substitute for the tax efforts, which increases costs in a jurisdiction and reduce tax collection and administration, the transfer payment may weaken the promoting effect of fiscal pressure on the preference of tax efforts. On the one hand, due to the “sticky fly paper” effect of transfer payment, the elasticity of local government expenditure to transfer payment is much greater than its fiscal revenue. Local governments tend to use lower-cost transfer payments to replace local tax collection and administration with higher costs, thus reducing the degree of tax effort. On the other hand, there is information asymmetry between the central and local governments. Bordignon et al. (2001) believed that the competition between the central government and local government often leads to insufficient or excessive tax revenue of local government to profit from balanced schemes at the expense of other government departments. Besfamille and Sanguinetti (2004) studied the moral hazard in local tax collection and administration under the tax-sharing system. They believed that central transfer payments tended to induce local governments to reduce tax efforts. Based on the above analysis, this paper puts forward Hypothesis 2.

Hypothesis 2 Transfer payment has a stable moderating effect, and local government debt and land-transferring fees have no sustained and stable moderating effect.

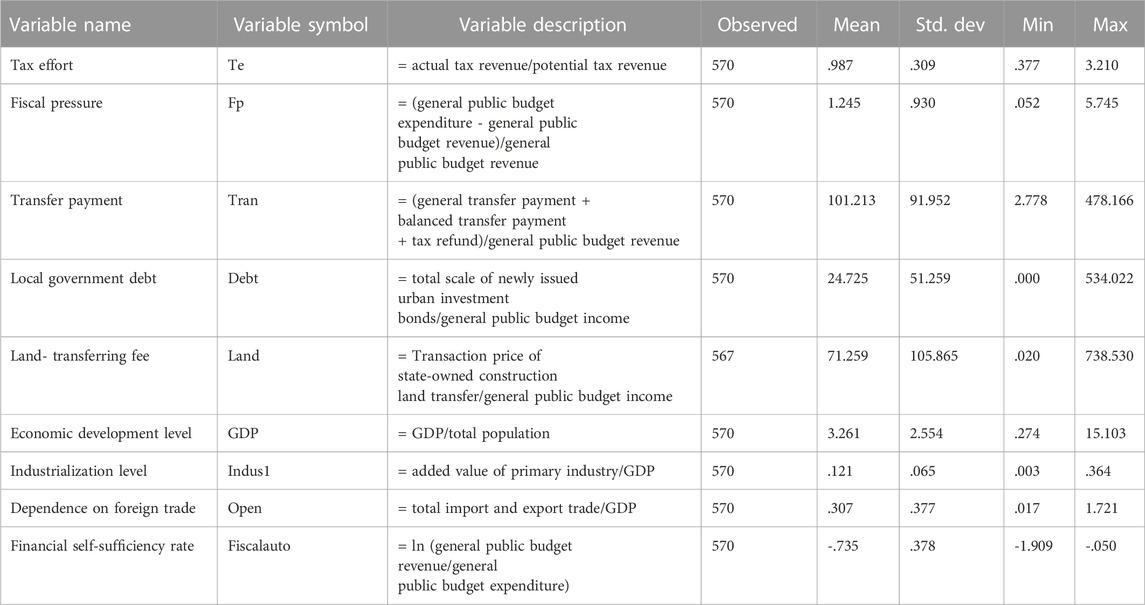

The tax effort index refers to the utilization of potential tax capacity by tax collection and management departments, which is expressed as “actual tax revenue/potential tax revenue” in terms of measurement indicators. Because the potential tax revenue cannot be observed directly, this paper uses the “Tax Handles” to calculate the potential tax revenue. “Tax handle” is the main influencing factor of potential tax revenue. Scholars generally believe that the tax revenue of a country or region mainly depends on the quantity, quality, and structure of its tax sources (Leuthold, 1991). In this paper, the gross domestic product (GDP) of each province (autonomous region and municipality directly under the central government) is used to represent the number of tax sources (Wu et al., 2021) and the degree of opening to the outside world (total import and export trade/GDP) is used to represent the quality of tax sources. However, the tax structure is affected by the industrial structure, so the proportion of primary industry in GDP is used to represent the tax structure. This paper first uses the cross-sectional data to establish the following multiple regression model, then fits the potential tax revenue of each province (autonomous region and municipality directly under the central government) according to the regression results, and finally estimates the tax effort of each region

Where, the subscript i indicates the province; the subscript t indicates the year;

Fiscal pressure is mainly manifested as the gap between fiscal revenue and expenditure formed by the imbalance between the supply of fiscal revenue and the demand of fiscal expenditure. Referring to the research of Bai et al. (2019), this paper measured regional fiscal pressure from the perspective of the fiscal revenue gap and used " (local public budget expenditure—local public budget revenue)/local public budget revenue” to measure fiscal pressure (FP).

In order to scientifically and effectively measure the impact of fiscal pressure on local governments’ tax efforts, this paper makes full use of available data and refers to previous relevant literature on factors affecting fiscal pressure and tax efforts, and finally selects the control variables that may affect the degree of tax efforts: the level of economic development (GDP) is expressed by the per capita real GDP of each province; Transfer payment (Tran) is the sum of general transfer payment, equalization transfer payment and tax refund; Local government Debt (Debt) is expressed by the total size of new urban investment bonds issued by provinces each year; Land-transferring fees (Land) is the sale price of state-owned construction Land in each province; Industrialization level (Indus1), that is, the proportion of the added value of the primary industry in GDP; Foreign trade dependence (Open), expressed as the proportion of total import and export trade in the region’s GDP; Fiscal self-sufficiency rate is expressed by the natural logarithm of the ratio of local public budget revenue to local public budget expenditure.

Considering the regional fixed effect and year fixed effect, as well as the influence of unobservable factors in control (including the periodic changes of regional economy and Policy) on the empirical results, this paper constructs a two-way fixed effect regression econometric model with regional tax effort as the explained variable and fiscal pressure as the explanatory variable. The benchmark measurement equation is as follows:

Where the subscript i represents provinces, autonomous regions, and municipalities directly under the central government; the subscript t represents the year; Te represents tax effort; Fp represents fiscal pressure; X represents other control variables affecting tax effort, including economic development level (GDP), transfer payment (Tran), local government debt (Debt), land-transferring fees (Land), industrialization level (Indus1), foreign trade dependence (Open), and fiscal self-sufficiency rate (Fiscalauto);

Due to the lack of some data in the Tibet Autonomous Region, the panel data used in this paper is from 2000 to 2018. There are 30 provinces, autonomous regions, and municipalities directly under the central government except for the Tibet Autonomous Region, and a total of 570 samples are involved in this sampling interval. The original data used in this paper are mainly from the National Statistical Yearbook, China Financial Statistical Yearbook, China land and resources Yearbook and, the wind database. The variables of some years (including land-transferring fees in 2018 and transfer payment in 2014) are from the government final accounts report and financial final accounts report published on the official website of relevant government departments. The descriptive statistical results of relevant variables are shown in Table 1.

TABLE 1. Descriptive statistics of variables.

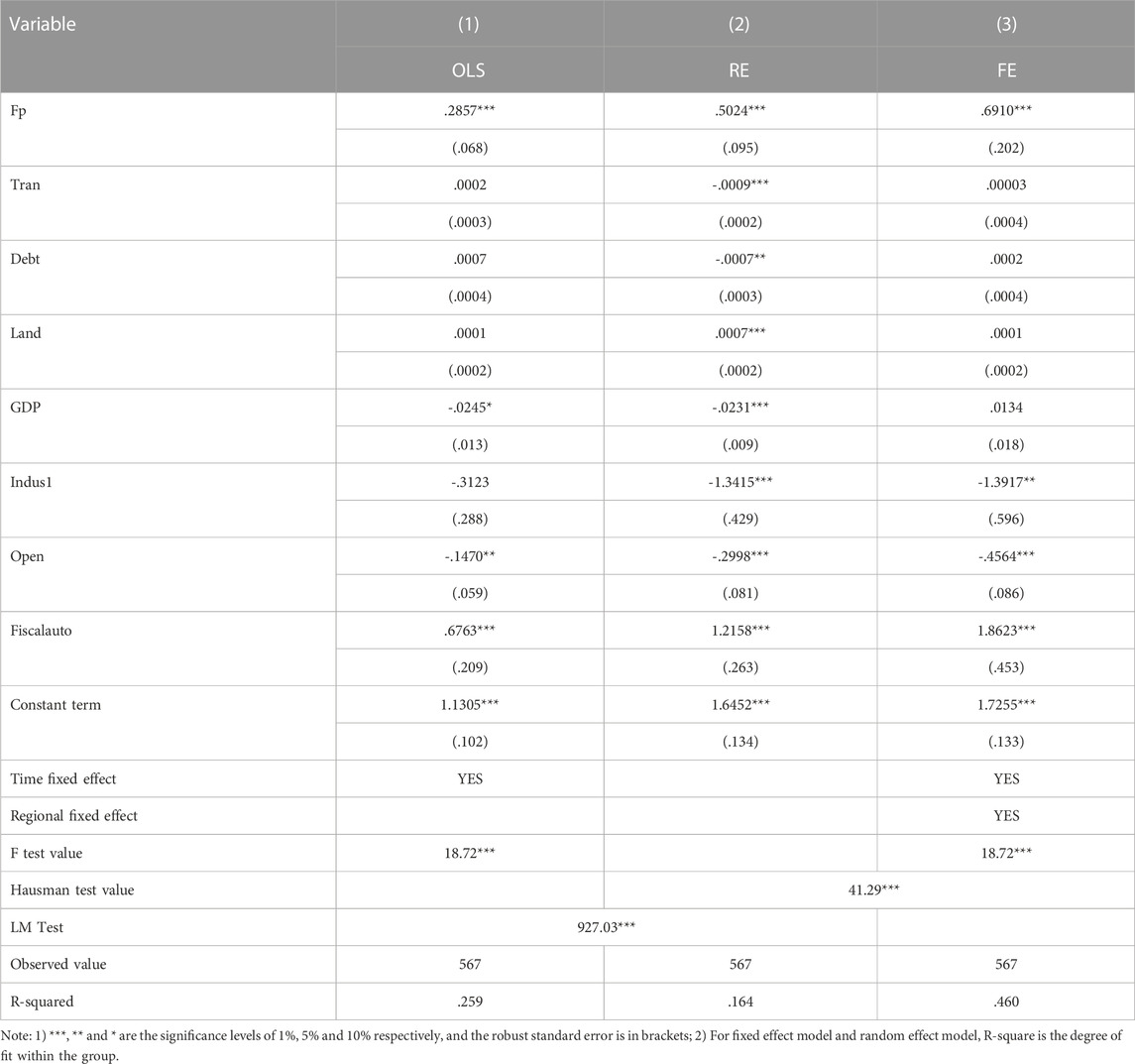

First, this paper focuses on the impact of fiscal pressure on the selection preferences of tax efforts among local governments. Table 2 shows the estimation results of the econometric model (2) using mixed OLS, random effect and fixed effect estimation methods respectively. By explained variable is the tax effort index, and the core explanatory variable is fiscal pressure, controlling transfer payment, local government debt, land-transferring fees, economic development level, industrialization level, dependence on foreign trade, financial self-sufficiency rate and other variables. According to the test results of F statistics, the estimation results of the fixed effect model should be selected instead of the mixed OLS regression model. According to the results of Hausman test, the estimation results of the fixed effect model should be selected instead of the random effect model.

TABLE 2. Test results of the impact of fiscal pressure on tax efforts.

In conclusion, the results estimated by the fixed effect model in column 3 shall prevail. We find that the regression coefficient of fiscal pressure is .6910, which is significant at the level of 1%, indicating that if the fiscal pressure increases by 1 unit, the selection preference of local governments to improve tax efforts will increase by .6910. The result shows that fiscal pressure has a significant positive effect on the selection preference of tax efforts among local governments. The greater the local fiscal pressure, the more local governments prefer to strengthen tax efforts. The result can confirm the validity of research Hypothesis 1a. The reason may be that there is a serious imbalance between the supply of regional fiscal revenue and the demand of fiscal expenditure, resulting in a large gap in fiscal revenue and expenditure. Therefore, local governments will choose to strengthen tax collection and administration to deal with greater fiscal pressure.

The regression results of other variables are as follows.

a) The estimation coefficient of industrialization level (Indus1) is significantly negative, which indicates that the increase of the proportion of the primary industry in the regional industrial structure will reduce local governments’ tax efforts. The reason may be that the lower the level of industrial structure, the lower the level of tax source structure, and the less tax revenue can be obtained, resulting in a decrease in the selection preference of tax efforts.

b) The estimated coefficient of foreign trade dependence (Open) is significantly negative, indicating that the increase in trade dependence has an inhibitory effect on the selection preference of local governments’ tax efforts. The higher the degree of economic opening to the outside world, the lower the tax effort. The reason may be that it is easier for regions with a higher degree of economic openness to the outside world to obtain tax revenue than regions with a lower degree of openness. Therefore, local governments prefer to relax the degree of tax effort, which is called the “paradox of tax effort".

c) The estimated coefficient of fiscal self-sufficiency rate (Fiscalauto)is significantly positive, indicating that fiscal self-sufficiency has a positive effect on the selection preference of tax efforts. The reason is that the high rate of fiscal self-sufficiency indicates that the region does not rely much on transfer payments, local government debts and land-transferring fees, and can better meet the needs of fiscal expenditure through its tax revenue and fiscal revenue. In this case, local governments prefer strengthening tax efforts as the main fiscal policy tool. Since the estimation results of other variables are insignificant, they will not be described here.

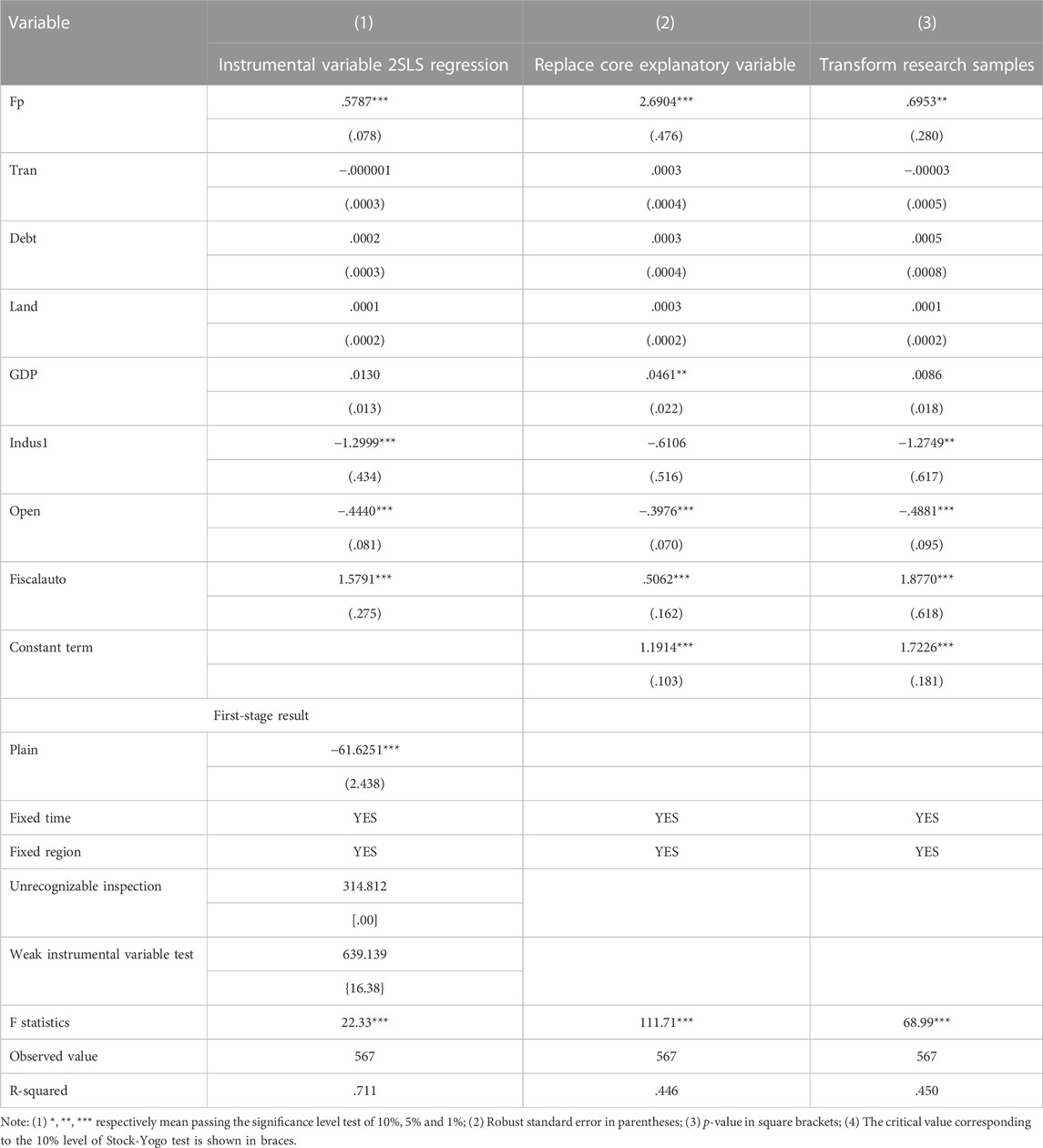

This paper tries to test the robustness of the above benchmark regression results from multiple dimensions by means of the instrumental variable method, substitution of the core explanatory variable method, and transformation of the research sample method.

Tax efforts are influenced by complex factors that cannot be controlled for all variables. In order to avoid adverse causality, omitted variables, endogeneity and other problems affecting the results as much as possible, this paper refers to the research method of Mo (2018). Based on SRTM data jointly measured by NASA and NIMA, the mean and highest elevations of each provincial administrative region were extracted and processed. We chose the plain development (Plain), which measures the number of developable land resources used as an instrumental variable of fiscal pressure, i.e., Plain development = −ln (Average

The regression results of instrumental variables show (Table 3, Column 1) that in the first-stage regression, the amount of plain development has a significant negative correlation with fiscal pressure. The result of “Underidentification test” can prove that it is identifiable to choose the variable measuring the amount of developable land resources as the instrumental variable. The “Weak identification test” results confirm that the instrumental variables selected in this paper are reasonable and effective. In the two-stage regression, the regression coefficient of fiscal pressure was .5787, which still passed the significance test of 1%. They indicate that fiscal pressure will still positively stimulate the selection preference of local tax efforts after the instrumental variable method is adopted, and the test results support the previous research Hypothesis 1a. From the test results of control variables, the regression coefficients of industrialization level (Indus1), foreign trade dependence (Open) and fiscal self-sufficiency rate (Fiscalauto) are completely consistent with the coefficient direction and significance of benchmark regression.

TABLE 3. Robustness test results.

This paper improves the measurement method of Esteve et al. (2000). It takes " (local public budget expenditure—local public budget revenue)/GDP” as the proxy variable to replace the fiscal pressure index in the benchmark regression. The results in column 2 of Table 3 show that the regression coefficient of fiscal pressure is 2.6904, which is significant at the level of 1%. The regression results of this robustness test verify the hypothesis that local governments prefer to strengthen tax efforts when local fiscal pressure is high. In addition, the regression coefficient of the level of economic development (GDP) is significantly positive, indicating that the higher the level of economic development, the higher the level of tax efforts. Existing literature on the impact of economic development level on local tax efforts is mainly divided into positive effects and negative effects. Different scholars draw different conclusions based on different models. Some scholars believe that in less developed areas, the greater the degree of tax effort is, the “tax effort paradox” exists. This paper argues that the level of economic development has a positive effect on tax efforts, but the effect is weak because the coefficient is small.

In order to prevent the research conclusions from being affected by extreme values, the sample data of the benchmark results are excluded from some extreme values (.5% above and below for each variable, 1% in total). The empirical analysis of the two-way fixed effect in column 3 of Table 2 is repeated. The regression coefficient of fiscal pressure is .6953, which is significant at the level of 5%. The regression results are shown in column 3 of Table 3, indicating that fiscal pressure has a significant positive incentive effect on the selection preference of tax efforts among local governments. After removing more extreme values from the sample data, the result of benchmark regression remains unchanged.

In conclusion, according to the robustness test results in Table 3, the regression coefficient direction and significance level of fiscal pressure are completely consistent with the research conclusions of the fourth part, indicating that the positive promotion effect of fiscal pressure on the selection preference of local government’ tax efforts is robust, and the test results support the previous research Hypothesis 1a.

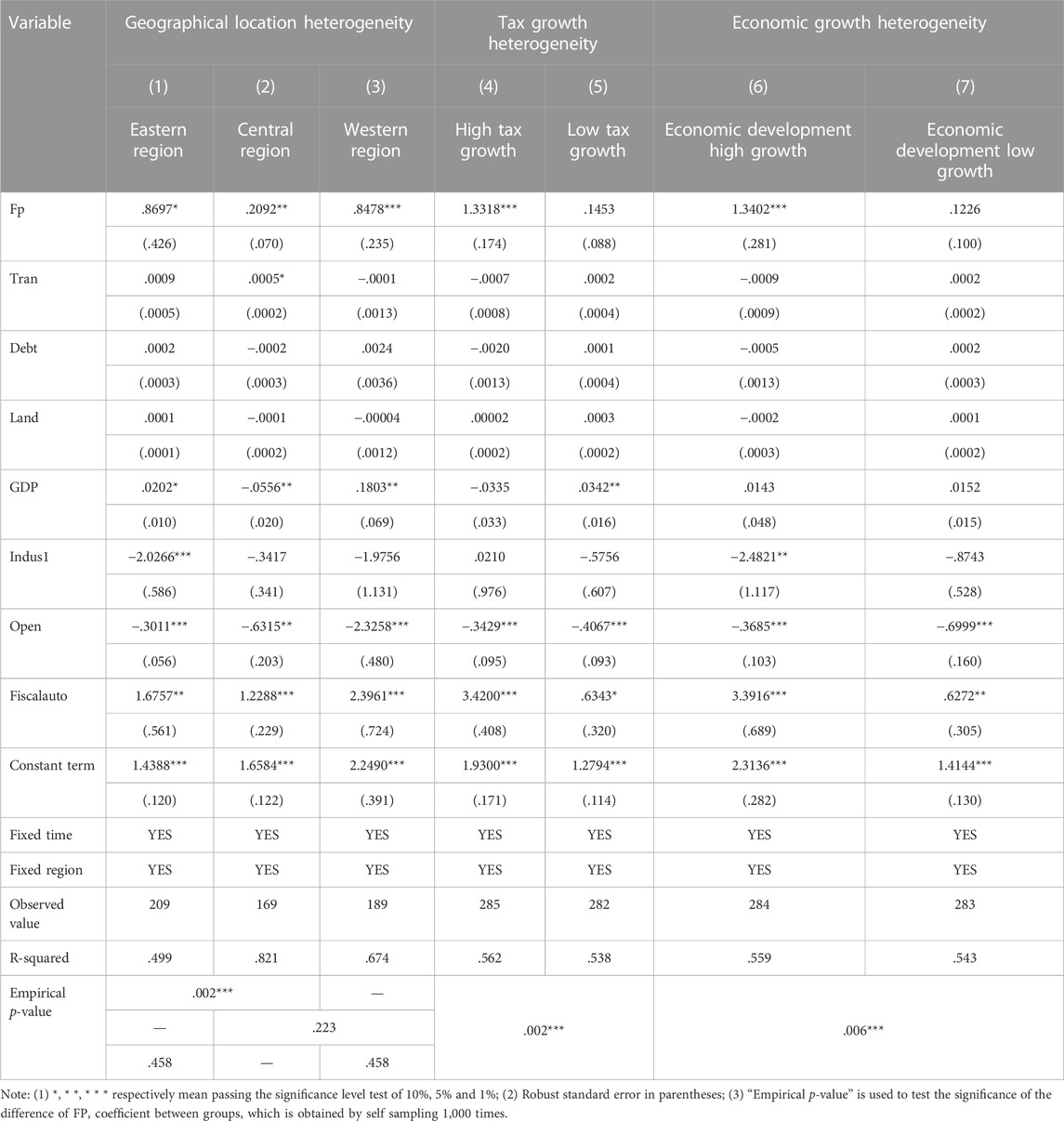

Considering the different geographical locations of each provincial administrative region may lead to differences in transfer payment, government financial self-sufficiency, and regional tax collection and management preference, which may lead to the heterogeneity of the impact of fiscal pressure on the tax efforts. In order to explore whether there is geographical heterogeneity in the impact of fiscal pressure on tax efforts. In this paper, the sample of provincial administrative regions is divided into the eastern region, central region, and western region using the division method of the National Bureau of Statistics on the three regions.3

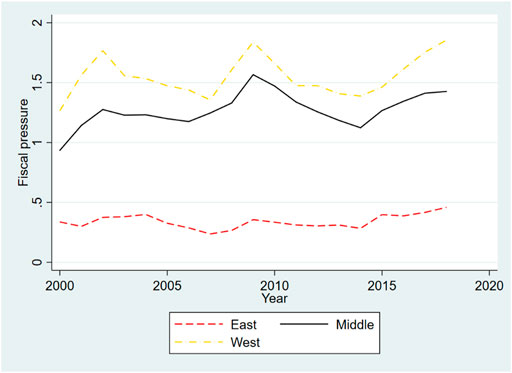

The results of heterogeneity analysis in columns (1)–(3) of Table 4 show that the fiscal pressure in China’s east, central and western regions has a significant positive effect on the selection preference of tax efforts among local government, with FP coefficients of .8697, .2092, and .8478. On the surface, the eastern regions of China have the strongest promoting effect of fiscal pressure on tax efforts, followed by the western and central regions. However, according to Fisher’s permutation test, the empirical p-value of China’s eastern and central regions is .002, which is significant at the level of 1%, indicating that the regional difference is statistically significant. However, the empirical p-value between China’s eastern and western regions did not pass the 10% significance level test, nor did the central and western regions. It indicates that the regional difference in the impact effect of fiscal pressure on the selection preference of tax efforts between the eastern and western regions and the regional difference between the central and western regions are not statistically significant. Therefore, the method of inferring only by comparing the size of intergroup coefficients is too arbitrary. The data results only show that the fiscal pressure in the eastern regions has a stronger promoting effect on the selection preference of tax efforts than that in the central regions, and eastern local governments prefer higher tax efforts than central regions and western regions. The possible reason is that the eastern regions have a more solid economic foundation, stronger sustainable development ability, less fiscal pressure (see Figure 1), and less fiscal gap to be filled. Therefore, the governments of eastern regions prefer to complete the fiscal gap by relying on their tax efforts than the central regions.

TABLE 4. Results of heterogeneity analysis of fiscal pressure on tax efforts.

FIGURE 1. Financial pressure in eastern, central and Western Regions.

Generally, when the tax growth is relatively high, the tax source base and tax potential are richer, and the government is more willing to strengthen tax collection and administration. In order to test whether there is tax growth heterogeneity in the impact of fiscal pressure on tax efforts, this paper refers to the methodology of Zheng and Lu (2021). The median tax revenue growth rate was used as the dividing standard to reclassify the research samples. Those higher than the median tax revenue growth rate were classified as high tax revenue growth rate, while those lower than the median tax revenue growth rate were classified as low tax revenue growth rate. According to the heterogeneity analysis results in columns (4)–(5) of Table 4, when the tax growth is high, fiscal pressure significantly promotes the selection preference of tax efforts. When the tax growth is low, the fiscal pressure has a weak positive impact on the selection preference of tax efforts and fails to pass the significance level test. According to Fisher’s permutation test, the empirical p-value of high tax growth and low tax growth is .002, which is significant at the 1% level. They show that only when tax growth is high, more significant fiscal pressure will stimulate local governments to choose to raise tax efforts firmly. However, when tax growth are low, the willingness of local governments to strengthen efforts is weak and wavering. The possible reason is that the tax source base and tax space of low tax growth is smaller than that of high growth, and no amount of tax efforts can make up for the large fiscal gap. Therefore, the local government has less willingness to strengthen tax collection and administration when tax growth is low.

GDP growth is an important factor affecting tax collection and administration. When the level of economic development is high, the growth is usually accompanied by the improvement of the quantity and quality of tax sources, which may lead to the improvement of the efficiency of tax collection and administration of the local government. In order to verify whether there is economic growth heterogeneity in the impact of fiscal pressure on the selection preference of tax efforts, this paper redivides the research samples based on the median GDP growth rate. Those higher than the median GDP growth rate are classified as high growth of economic development, and those lower than the median GDP growth rate are classified as low growth of economic development. According to the heterogeneity analysis results in columns (6)–(7) of Table 4, when the economic development is high, the fiscal pressure significantly increases the tax efforts. When economic development is low, fiscal pressure positively affects the selection preference of tax efforts among local governments. However, it fails to pass the significance level test. According to Fisher’s permutation test, the empirical p-value of high tax growth and low tax growth is .006, which is significant at the 1% level. They show that the impact of fiscal pressure on the selection preference of tax efforts does have heterogeneity in economic growth. When economic growth is high, local governments prefer to increase efforts, but when economic growth is low, local governments’ decision to strengthen tax efforts is not stable. The possible reason is that with the rapid development of the economy, the quantity and quality of tax sources are improved, and the concentration of tax sources is increased, which leads to the reduction of tax costs of tax authorities. In the process of transformation from tax source to tax revenue, the transformation efficiency of high economic growth is higher, so it’s the selection preference of tax effort is often higher.

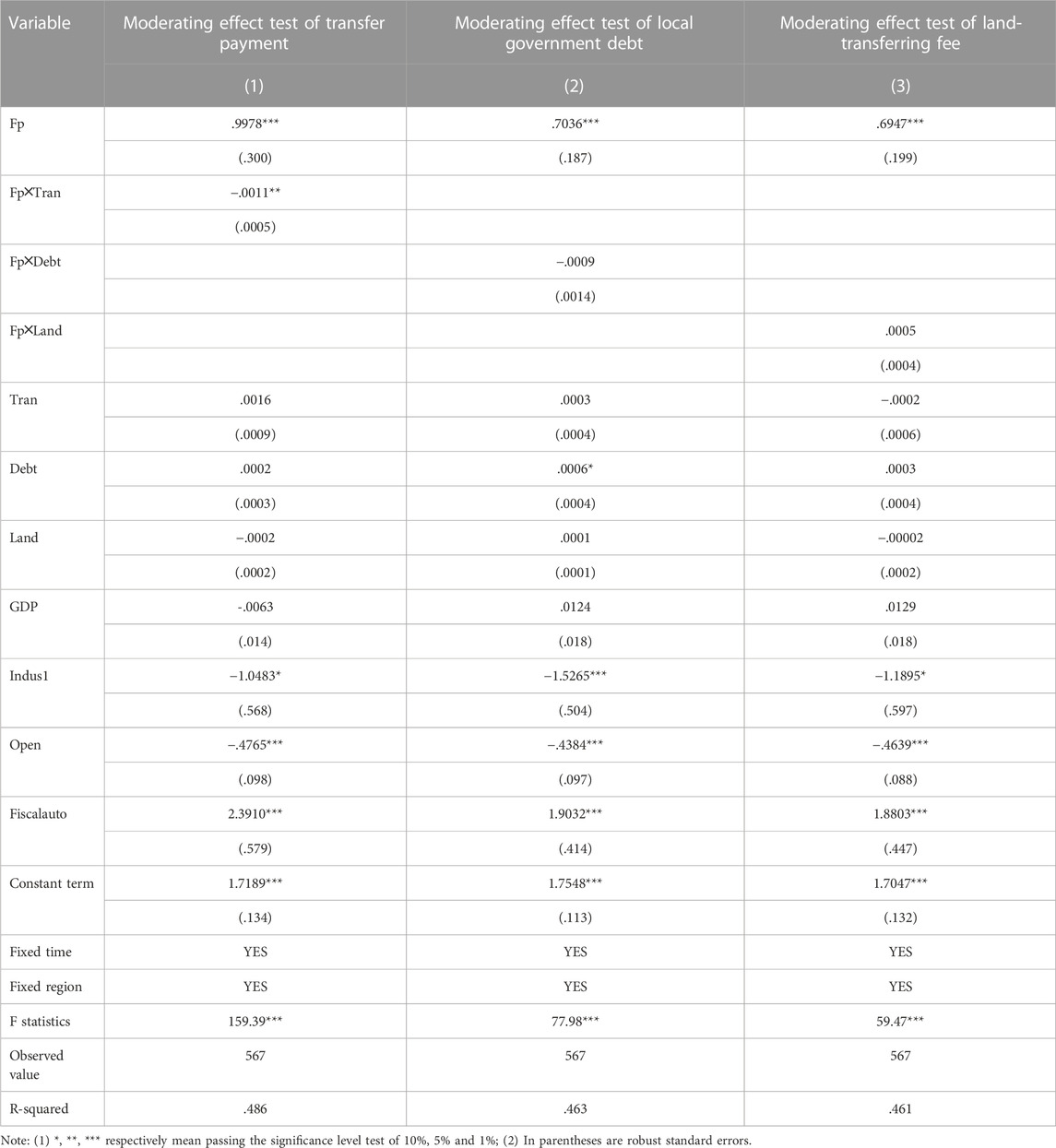

According to the previous theoretical analysis, transfer payment is the moderator of fiscal pressure affecting the selection preference of tax efforts among local governments. In contrast, local government debt and land-transferring fees do not have a steady and sustainable moderating effect. If the fiscal pressure does affect the improvement of the preference of tax efforts through the moderating effect of transfer payment, it can be inferred that when the transfer payments are high, local governments will select less preference of tax efforts under the fiscal pressure. This paper introduces the interaction term of fiscal pressure and a moderator to test the moderating mechanism of fiscal pressure affecting the selection preference of tax efforts. First, the interaction term Fp×Tran between fiscal pressure and total transfer payments is added to the benchmark regression model (2). If the regression coefficients of fiscal pressure and interaction term are significant, it shows that transfer payment has a moderating effect on the degree of fiscal pressure promoting tax efforts.

According to the test results in column (1) of Table 5, fiscal pressure still has a significant positive effect on the selection preference of tax efforts among local governments. However, the regression coefficient of the interaction term Fp×Tran is −.0001, which is significant at the level of 5%. They show that transfer payment, as a moderator of fiscal pressure, has a significant negative moderating effect. With the increase in transfer payments, local governments are less willing to strengthen tax efforts, which confirms the validity of research Hypothesis 2. The possible reason is that the higher transfer payment amount will increase local governments’ fiscal revenue, increase the marginal cost of local governments providing public services through taxation, and then reduce the level of tax efforts.

TABLE 5. Moderating effect test results of each moderator.

This paper tests the moderating mechanism of local government debt and land-transferring fees. The results in columns (2)–(3) of Table 5 show that the interaction term between local government debt, land-transferring fees and fiscal pressure is not significant, indicating that its moderating effect is not stable. It also confirms that the view that “local government debt and land-transferring fees do not have a stable and sustainable moderating effect” proposed in the theoretical hypothesis analysis is tenable.

To sum up, from the overall perspective, increased fiscal pressure will encourage local governments to prefer higher tax efforts, which is consistent with the conclusions of traditional literature. Second, from the perspective of heterogeneity, this paper creatively sets out from the perspective of economic and tax growth. The study believes that when the fiscal pressure increases, the economic and tax growth are higher than their low growth, encouraging local governments to prefer higher tax efforts. Third, from the perspective of the moderating effect test, the study believes that only transfer payment will have a robust negative moderating effect on the selection preference of tax efforts which are affected by fiscal pressure. The traditional literature believes that local government debt and land-transferring fees can also produce negative effects. The possible reason is that the traditional literature only considers a single fiscal policy tool for research and does not put the fiscal policy tools that may affect fiscal pressure and tax efforts into a unified model. This approach will lead to some deviation in the research conclusions.

The above research shows that fiscal pressure has a significant positive role in promoting the preference of local governments’ tax efforts and confirms that transfer payment is a moderator to weaken the impact of fiscal pressure on the selection preference of tax efforts. Therefore, when other conditions remain unchanged, the difference between the central and local transfer payments will lead to different degrees of impact of fiscal pressure on tax efforts, and local governments will have different selection preferences in tax collection and administration. However, from the perspective of transfer payment, when facing higher transfer payments, the local governments believe that they can make up the fiscal gap through transfer payment, which reduces tax collection and administration. Nevertheless, will lower transfer payments certainly strengthen the role of fiscal pressure in promoting tax efforts? With the reduction of transfer payment, will its moderating effect show structural changes? Is there an optimal threshold? We speculate that when the transfer payment is lower than a certain critical value, the local government will produce negative emotions due to the difficult fiscal gap, which will relatively weaken the promotion effect of fiscal pressure on the preference of tax efforts. In order to answer the above questions, this paper takes the transfer payment as the threshold variable for empirical tests according to the panel regression model.

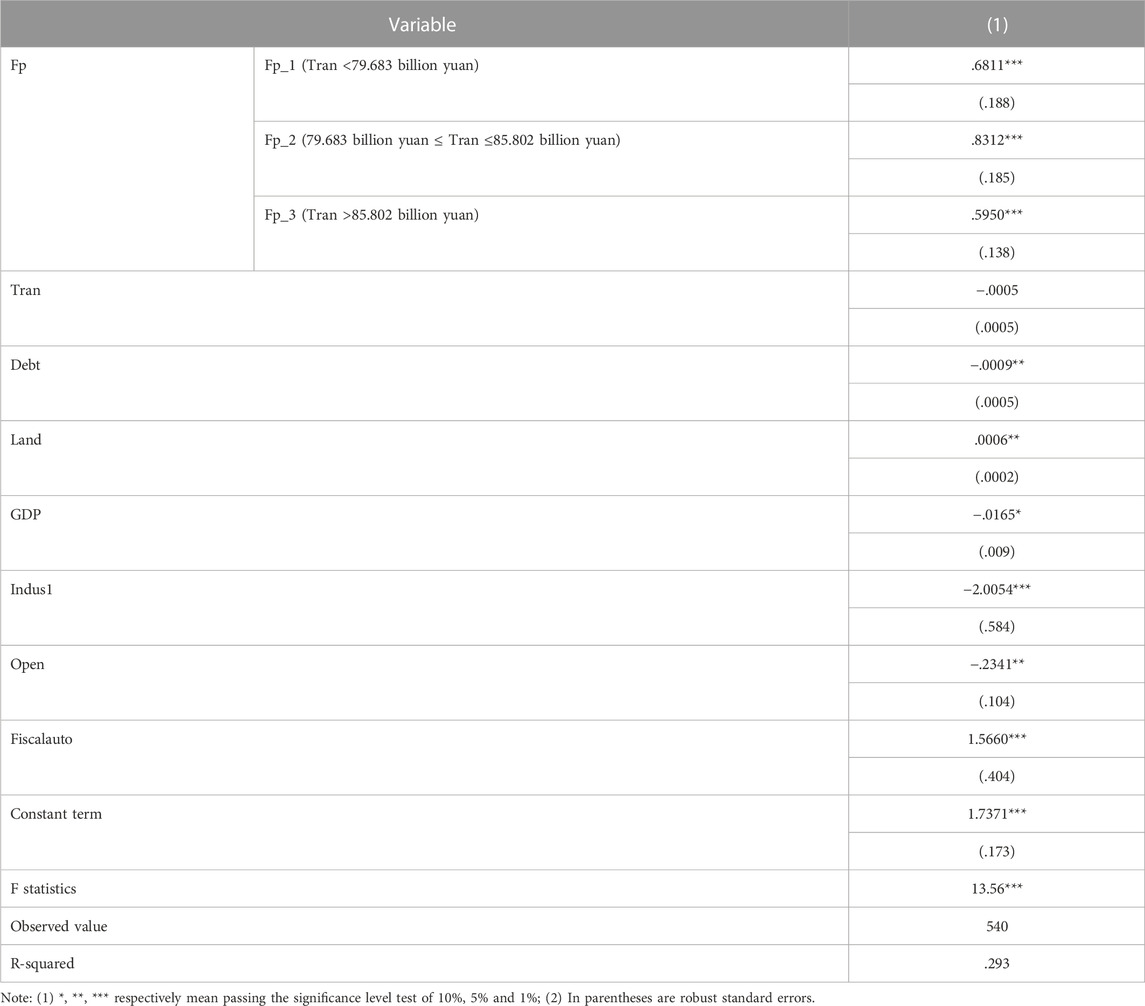

According to the regression results in Tables 6, 7, and Figure 2 when the transfer payment as the threshold variable is between 79.683 billion yuan and 85.802 billion yuan, the regression coefficient of fiscal pressure is .8312, which is significant at the level of 1%. With the increase of the transfer payment, when the transfer payment crosses the threshold value of 85.802 billion yuan, the fiscal pressure still plays a significant role in promoting the selection preference of tax efforts, but the regression coefficient decreases to .5950. When the transfer payments continued to decline, which was 79.683 billion yuan lower than the threshold value, the regression coefficient of fiscal pressure did not continue to increase due to the reduction of transfer payments but decreased to .6811 and passed the significance test of 1%. They show that too high or too low transfer payment may lead to the laziness of local governments, which do not try their best to raise tax efforts and will weaken the incentive effect of fiscal pressure on tax efforts to a certain extent. In conclusion, the impact of fiscal pressure on tax efforts has a threshold effect based on transfer payments. Controlling the central to local transfer payment within a reasonable range is more conducive to giving full play to the role of fiscal pressure in promoting the selection preference of tax efforts among local governments and improving the efficiency of tax collection and administration.

TABLE 6. Significance test and confidence interval of threshold variable transfer payment.

TABLE 7. Panel threshold regression results.

FIGURE 2. Threshold estimate and confidence interval.

This paper takes the data from 30 provinces, autonomous regions, and municipalities directly under the central government from 2000 to 2018 as the research sample. We measure each provincial administrative region’s fiscal pressure and tax efforts and empirically analyze the impact of fiscal pressure on the selection preference of tax efforts among local governments. We can draw the following research conclusions: first, in the face of substantial fiscal pressure, local governments do not retreat from difficulties. However, they choose to increase the preference for tax efforts. The conclusion is still valid after a series of robustness tests, such as the instrumental variable method, transformation of core explanatory variables, the transformation of research samples and so on. Second, the positive stimulating effect of fiscal pressure on the selection preference of tax efforts is heterogeneous. Although the fiscal pressure in the eastern, central and western regions has a significant incentive effect on the selection preference of tax efforts, eastern local governments prefer a higher preference of tax efforts. Compared with high tax growth and high economic growth, when the growth of tax and economy is low, local governments have less selection preference to strengthen tax efforts. Third, transfer payment is the moderator of fiscal pressure on the selection preference of tax efforts, which will have a significant negative moderating effect on the promoting effect of fiscal pressure on the preference of tax efforts. The impact of fiscal pressure on the selection preference of tax efforts has a threshold effect based on transfer payment. When transfer payment crosses the highest threshold or is less than the lowest threshold, it may lead to the laziness of local governments, which do not try their best to raise tax efforts. When transfer payment is between the lowest and highest threshold, local governments are most willing to strengthen tax efforts.

The policy implications of this paper are: first, there is no need for the central or federal government to intervene excessively with tax efforts of local governments. Although the increase of fiscal pressure has its drawbacks, it objectively promotes the improvement of the tax efforts of states or local governments. Local tax authorities and state governments will also take pressure as a driving force in the face of difficulties, and there will not be phenomena of negative tax collection and administration. Therefore, local or state governments’ subjective initiative should be brought into full play, relying on the positive incentive mechanism of fiscal pressure. Local or state governments can choose tax collection and administration strategies independently, which is conducive to improving the efficiency of tax collection and administration efficiency. Second, develop the real economy and steadily expand tax sources. Only when the economy grows steadily can the tax source be rich, and local or states government will have the motive and space to make efforts in tax collection and administration. The world’s nations need to rely on the complete system and autonomy of the real economy to meet the residents’ basic needs and economic development to achieve national stability and social development. Therefore, local or state governments should promote the development of the real economy as the leading tone of macro policies. The central and western regions of China and other developing countries should adjust and optimize the industrial structure and tax source structure according to their conditions, develop advantageous industries with high quality, extend the industrial chain through the development of the real economy, expand the industrial scope, enrich the tax sources, realize the sustainable growth of tax revenue, and provide growth space for tax efforts. Third, the central allocation and transfer payment should be controlled within a reasonable range. Reduce the randomness and temporary nature of transfer payments, avoid directly determining transfer payment funds by means of “bargaining” and “running for money” between local or states governments and the central or federal government, and improve the objectivity, rationality, and standard of transfer payment allocation calculation. The central government of China should control transfer payments between 79.683 billion yuan and 85.802 billion yuan to reduce the substitution effect of tax efforts caused by too high or too low transfer payments. Transfer payments or government subsidies in other countries may also have a similar threshold effect. By giving full play to the incentive effect of fiscal pressure, promote the high-quality development of the real economy, control the reasonable allocation scope of transfer payment, and jointly drive the improvement of local government tax efforts.

This paper also has shortcomings. Since the relevant data at the county and city in China have not been released to the public, this study only obtained provincial data for research. However, the sample size of provincial data is smaller than county and city data, which is vulnerable to the impact of outliers. Moreover, due to the limitation of provincial sample data, provincial transfer payment data cannot be subdivided into general transfer payment, equalization transfer payment and tax refund. The paper is also unable to empirically study the influence of three different types of transfer payments on the selection preference of tax efforts among local governments under fiscal pressure. In the future, after the release of China’s county and city data, we will continue to deeply study the selection preference of tax efforts among county and city’s governments under fiscal pressure and compare whether there are differences in the selection preference of tax efforts between grassroots governments and provincial governments.

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding author.

ZD: conceptualization. ZD: methodology. ZD and PY: data. ZD and PY: writing and original draft preparation. ZD and PY: writing, review, and editing.

This paper is funded by GuiZhou Philosophy and Social Science Program “Research on the Emergency Procurement Supply System of People’s Livelihood Security and Social Assistance in Guizhou Province: Under the Background of Significant Emergent Events (20GZQN19)”.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

1Shen, Z. (2018). Fiscal Pressure and Local Government tax efforts: an empirical study based on provincial data. Taxation Research. 10, 108-114.

2National Bureau of Statistics, China Statistical Yearbook 2021.

3Note: The eastern region includes Beijing, Tianjin, Hebei, Liaoning, Shanghai, Jiangsu, Zhejiang, Fujian, Shandong, Guangdong and Hainan, the central region includes Shanxi, Jilin, Heilongjiang, Anhui, Jiangxi, Henan, Hubei and Hunan, and the western region includes inner Mongolia, Guangxi, Chongqing, Sichuan, Guizhou, Yunnan, Shaanxi, Gansu, Qinghai, Ningxia and Xinjiang.

Arvin, M. B., Pradhan, R. P., and Nair, M. S. (2021). Are there links between institutional quality, government expenditure, tax revenue and economic growth? Evidence from low-income and lower middle-income countries. Econ. Analysis Policy 70, 468–489. doi:10.1016/j.eap.2021.03.011

Bai, J., Lu, J., and Li, S. (2019). Fiscal pressure, tax competition and environmental pollution. Environ. Resour. Econ. 73 (2), 431–447. doi:10.1007/s10640-018-0269-1

Baretti, C., Huber, B., and Lichtblau, K. (2002). A tax on tax revenue: The incentive effects of equalizing transfers: Evidence from Germany. Int. Tax Public Finance 9 (6), 631–649. doi:10.1023/A:1020925812428

Besfamille, M., and Sanguinetti, P. (2004). Exerting local tax effort or lobbying for central transfers? Econ. Soc. 2004 Lat. Am. Meet. 249, 1–18. Available at: http://repec.org/esLATM04/up.16682.1082059515.pdf.

Bird, R. M., Martinez-Vazquez, J., and Torgler, B. (2006). Societal institutions and tax effort in developing countries. challenges tax reform a Glob. Econ. 15, 283–332. doi:10.2139/ssrn.662081

Bird, R. M., and Tarasov, A. V. (2004). Closing the gap: Fiscal imbalances and intergovernmental transfers in developed federations. Environ. Plan. C Gov. Policy 22 (1), 77–102. doi:10.1068/c0328

Boetti, L., Piacenza, M., and Turati, G. (2012). Decentralization and local governments' performance: How does fiscal autonomy affect spending efficiency? FinanzArchiv/Public Finance Anal. 68, 269–302. doi:10.1628/001522112X653840

Bordignon, M., Manasse, P., and Tabellini, G. (2001). Optimal regional redistribution under asymmetric information. Am. Econ. Rev. 91 (3), 709–723. doi:10.1257/aer.91.3.709

Buettner, T. (2006). The incentive effect of fiscal equalization transfers on tax policy. J. Public Econ. 90 (3), 477–497. doi:10.1016/j.jpubeco.2005.09.004

Checherita, -W. C., and Rother, P. (2012). The impact of high government debt on economic growth and its channels: An empirical investigation for the euro area. Eur. Econ. Rev. 56 (7), 1392–1405. doi:10.1016/j.euroecorev.2012.06.007

Chen, L., Zhu, J., and Yang, C. (2022). Forecasting parameters in the SABR model. J. Econ. Analysis 1 (1), 102–117.

Chen, S. X. (2017). The effect of a fiscal squeeze on tax enforcement: Evidence from a natural experiment in China. J. Public Econ. 147, 62–76. doi:10.1016/j.jpubeco.2017.01.001

Cheng, H., Liu, X., and Xu, Z. (2022). Impact of carbon emission trading market on regional urbanization: An empirical study based on a difference-in-differences model. Econ. Anal. Lett. 1 (1), 15–21.

Cheng, Y., Jia, S., and Meng, H. (2022). Fiscal policy choices of local governments in China: Land finance or local government debt? Int. Rev. Econ. Finance 80, 294–308. doi:10.1016/j.iref.2022.02.070

Dang, D., Fang, H., and He, M. (2019). Economic policy uncertainty, tax quotas and corporate tax burden: Evidence from China. China Econ. Rev. 56, 101303. doi:10.1016/j.chieco.2019.101303

Di Liddo, G., Longobardi, E., and Porcelli, F. (2019). Fiscal imbalances and fiscal effort of local governments. BE J. Econ. Analysis Policy 19 (3), 20180315. doi:10.1515/bejeap-2018-0315

Egger, P., Koethenbuerger, M., and Smart, M. (2010). Do fiscal transfers alleviate business tax competition? Evidence from Germany. J. Public Econ. 94 (3-4), 235–246. doi:10.1016/j.jpubeco.2009.10.002

Esteve, V., Sosvilla-Rivero, S., and Tamarit, C. (2000). Convergence in fiscal pressure across EU countries. Appl. Econ. Lett. 7 (2), 117–123. doi:10.1080/135048500351942

Eyraud, L., and Lusinyan, L. (2013). Vertical fiscal imbalances and fiscal performance in advanced economies. J. Monetary Econ. 60 (5), 571–587. doi:10.1016/j.jmoneco.2013.04.012

Geng, B., Zhang, X., Liang, Y., Bao, H., and Skitmore, M. (2018). Sustainable land financing in a new urbanization context: Theoretical connotations, empirical tests and policy recommendations. Resour. Conservation Recycl. 128, 336–344. doi:10.1016/j.resconrec.2016.11.013

Han, L., and Kung, J. K. S. (2015). Fiscal incentives and policy choices of local governments: Evidence from China. J. Dev. Econ. 116, 89–104. doi:10.1016/j.jdeveco.2015.04.003

Hao, X., Li, Y., Ren, S., Wu, H., and Hao, Y. (2023). The role of digitalization on green economic growth: Does industrial structure optimization and green innovation matter? J. Environ. Manag. 325, 116504. doi:10.1016/j.jenvman.2022.116504

Huang, J. T., Lo, K. T., and She, P. W. (2012). The impact of fiscal decentralization on tax effort of China's local governments after the tax sharing system. Singap. Econ. Rev. 57 (01), 1250005. doi:10.1142/S0217590812500051

Huang, Y., and Soyano, K. (2022). Which component of deposit drives systemic risk volatility. Econ. Anal. Lett. 1 (1), 1–7.

Jia, J. X., and Ying, S. W. (2016). Fiscal decentralization and corporate tax incentives: An analysis from views of local government competition. China Ind. Econ. 10, 23–39.

Leuthold, J. H. (1991). Tax shares in developing economies a panel study. J. Dev. Econ. 35 (1), 173–185. doi:10.1016/0304-3878(91)90072-4

Lin, G. C., and Zhang, A. Y. (2015). Emerging spaces of neoliberal urbanism in China: Land commodification, municipal finance and local economic growth in prefecture-level cities. Urban Stud. 52 (15), 2774–2798. doi:10.1177/0042098014528549

Litvack, J. I., Ahmad, J., and Bird, R. M. (1998). Rethinking decentralization in developing countries. Washington, DC: World Bank Publications.

Liu, H., Lei, H., and Zhou, Y. (2022). How does green trade affect the environment? Evidence from China. J. Econ. Analysis 1 (1), 1–27.

Liu, J., Xue, Y., Mao, Z., Irfan, M., and Wu, H. (2022). How to improve total factor energy efficiency under climate change: Does export sophistication matter? Environ. Sci. Pollut. Res. 2022, 1–11. doi:10.1007/s11356-022-24175-2

Liu, Y., and Zhao, J. (2011). Intergovernmental fiscal transfers and local tax efforts: Evidence from provinces in China. J. Econ. Policy Reform 14 (4), 295–300. doi:10.1080/17487870.2011.591175

Lu, B., and Guo, Q. (2012). Why China’s tax revenue is likely to maintain its rapid growth: An explanation within the framework of tax capacity and tax effort. Soc. Sci. China 33 (1), 108–126. doi:10.1080/02529203.2012.650413

Ma, G., and Li, L. (2012). Government size, local governance and corporate tax evasion. J. World Econ. 35 (06), 93–114.

Mo, J. (2018). Land financing and economic growth: Evidence from Chinese counties. China Econ. Rev. 50, 218–239. doi:10.1016/j.chieco.2018.04.011

Mohanty, A., Sethi, D., and Mohanty, A. R. (2020). Central transfer a curse or blessing? Evidence from the relative revenue effort of Indian states. Aust. Econ. Rev. 53 (2), 214–227. doi:10.1111/1467-8462.12358

Mukherjee, S. (2017). Changing tax capacity and tax effort of Indian states in the era of high economic growth, 2001-2014. NIPFP Work. Pap. Ser. 196, 1–28. doi:10.13140/RG.2.2.16502.60484

Panda, P. K. (2009). Central fiscal transfers and states’ own-revenue efforts in India: Panel data models. Margin J. Appl. Econ. Res. 3 (3), 223–242. doi:10.1177/097380100900300302

Peiyong, G. (2006). Riddle of the sustained and rapid tax increase in China. Econ. Res. J. 12, 13–23.

Qun, W., Yongle, L., and Siqi, Y. (2015). The incentives of China’s urban land finance. Land Use Policy 42, 432–442. doi:10.1016/j.landusepol.2014.08.015

Shen, Z. (2018). Fiscal pressure and local government tax efforts: An empirical study based on provincial data. Tax. Res. 10, 108–114.

Sobel, R. S., and Crowley, G. R. (2014). Do intergovernmental grants create ratchets in state and local taxes? Public Choice 158 (1), 167–187. doi:10.1007/s11127-012-9957-5

Tang, P., Shi, X., Gao, J., Feng, S., and Qu, F. (2019). Demystifying the key for intoxicating land finance in China: An empirical study through the lens of government expenditure. Land Use Policy 85, 302–309. doi:10.1016/j.landusepol.2019.04.012

Tsui, K. Y. (2011). China's infrastructure investment boom and local debt crisis. Eurasian Geogr. Econ. 52 (5), 686–711. doi:10.2747/1539-7216.52.5.686

Wang, Q., and Su, M. (2020). A preliminary assessment of the impact of COVID-19 on environment–A case study of China. Sci. total Environ. 728, 138915. doi:10.1016/j.scitotenv.2020.138915

Wu, H., Sun, M., Zhang, W., Guo, Y., Irfan, M., Lu, M., et al. (2022). Can urbanization move ahead with energy conservation and emission reduction? New evidence from China. Energy and Environ. 2022, 0958305X221138822.

Wu, H., Xia, Y., Yang, X., Hao, Y., and Ren, S. (2021). Does environmental pollution promote China's crime rate? A new perspective through government official corruption. Struct. Change Econ. Dyn. 57, 292–307. doi:10.1016/j.strueco.2021.04.006

Xiao, C., and Shao, Y. (2020). Information system and corporate income tax enforcement: Evidence from China. J. Account. Public Policy 39 (6), 106772. doi:10.1016/j.jaccpubpol.2020.106772

Xie, Z., and Fan, Z. (2015). Chinese-style tax-sharing system, tax collection centralization and tax competition. Econ. Res. J. 4, 92–106.

Xing, W., and Zhang, Q. (2018). The effects of vertical and horizontal incentives on local tax efforts: Evidence from China. Appl. Econ. 50 (11), 1222–1237. doi:10.1080/00036846.2017.1355546

Xue, Y., Jiang, C., Guo, Y., Liu, J., Wu, H., and Hao, Y. (2022). Corporate social responsibility and high-quality development: Do green innovation, environmental investment and corporate governance matter? Emerg. Mark. Finance Trade 58, 3191–3214. doi:10.1080/1540496x.2022.2034616

Yu, W., Yin, H., and Liang, P. (2018). Fiscal decentralization and corporate tax incentives-an analysis from views of local government competition. China Ind. Econ. 01, 100–118.

Zheng, C., Deng, F., Zhuo, C., and Sun, W. (2022). Green credit policy, institution supply and enterprise green innovation. J. Econ. Analysis 1 (1), 28–51.

Zheng, W., and Lu, Y. Q. (2021). Fiscal pressure, government innovation preference and urban innovation quality. Finance Res. 08, 63–76. doi:10.19477/j.cnki.11-1077/f.2021.08.005

Keywords: fiscal pressure, local tax efforts, transfer payments, local government debt, land-transferring fees, selection

Citation: Deyun Z and Yiqing P (2023) Facing or retreating? Evaluating the impact of fiscal pressure and the selection preference of tax efforts among Chinese local government. Front. Environ. Sci. 10:993931. doi: 10.3389/fenvs.2022.993931

Received: 14 July 2022; Accepted: 28 December 2022;

Published: 12 January 2023.

Edited by:

Rongrong Li, China University of Petroleum, ChinaReviewed by:

Xiaodong Yang, Xinjiang University, ChinaCopyright © 2023 Deyun and Yiqing. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Pan Yiqing, cGFueWlxaW5nMTk5Mjc1QDE2My5jb20=

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.