Yumna Ashraf

Yumna Ashraf Fahad Ali

Fahad Ali- 1Department of Business Studies, Pakistan Institute of Development Economics (PIDE), Islamabad, Pakistan

- 2School of Finance, Zhejiang University of Finance and Economics, Hangzhou, China

Rapid globalization during the last few decades has caused many difficulties for firms to survive, sustain, and maximize shareholders’ wealth. The Enterprise Resource Planning (ERP) system provides extensive access to data and upgraded information to achieve the specified objectives. This study examines how Innovative Organizational Culture (IOC) affects firm performance in Pakistan. In doing so, this study collects a comprehensive dataset from 234 high- and medium-level managers working in different sectors across six major cities of Pakistan. We construct several hypotheses and employ Partial Least Squares Structural Equation modeling to test the selected premises. The results reveal that IOC and the benefits of ERP are positively related to firm performance, IOC is also positively associated with the implementation of ERP, and the implementation of ERP is positively related to the benefits of ERP. Regarding mediating relationship among the constructs, this study shows that the implementation of ERP mediates the relationship between IOC and the benefits of ERP and the benefits of ERP mediate the relationship between the implementation of ERP and firm performance. Given that Pakistan has been facing a chronic energy crisis for the last few decades, this study conducts a subsample analysis and divides the sample into two groups—“energy and manufacturing” and “service and non-manufacturing” sector firms. Our robustness tests reveal that the implementation of ERP is positively and significantly related to firm performance only in the subsample of service and non-manufacturing sector firms. In contrast, it is negatively and insignificantly related to firm performance in the subsample of energy and manufacturing sector firms. The findings of this study provide numerous operational insights to managers to adequately emphasize and strengthen IOC to sustain the change management system. Specifically, this study suggests that senior- and medium-level managers should continuously monitor the implementation of ERP and determinedly engage themselves in the team management and communication process to achieve higher firm performance.

1 Introduction

In recent times, the quest for better performance is progressively increasing. However, achieving higher firm performance is undoubtedly challenging for managers and leaders. Thus, the ever-changing business competition requires a firm to be nimbler and innovative to achieve a competitive edge. Likewise, vindicating and endearing stakeholders’ expectations are other important factors to consider (Gursoy and Swanger 2007).

Enterprise Resource Planning (ERP) is one of the recent tools that integrate business activities with management processes for automation (Kazemi and Sullivan 2014). Information Technology (IT) penetration enables a firm to become more digitalized and utilize more extensive datasets that may increase decision-making precision as up-to-date information facilitates firms to comprehensively interpret both micro- and macro-level factors to make efficient and effective decisions (Aydiner et al., 2019).

Innovative organizational culture signifies a working culture where creative ideas are determined, encouraged, and implemented (Uzkurt et al., 2013). The extant literature shows that IOC only not fosters innovation and encourages new ideas but also produces novel solutions (Jamrog et al., 2006; Li et al., 2018). It similarly relates to behaviors involved in adapting and implementing innovative processes. The Innovative Organizational Culture (IOC) oriented firms are supposed to be more creative, risk-taking, open to new ideas, and have an entrepreneurial mindset (Jamrog et al., 2006). Thus, it offers the basis for state-of-the-art solutions, future market trends, and improved communication through adopting and implementing new technologies (Martín-de Castro et al., 2013). The integration of business activities and change management in organizations are other factors that are positively influenced by IOC (Brettel and Cleven, 2011). The extant literature reveals that the utilization of IT and IOC are the most important drivers of higher firm performance.

As discussed above, ERP is a state-of-the-art integrative management tool that helps in identifying, capturing, and monitoring the flow of both internal and external information (Beheshti and Beheshti 2010) and micro (among the department) and macro (vendors and contractors) factors of a firm (Razaq et al., 2017). It depends on several modules and activities linked with different business functions such as accounting, supply chain management, financial management, human resource, customer relationship management, and the entire information accessible to the organization (Liang et al., 2007; Addo-Tenkorang and Helo 2011). Thus, an efficaciously implemented ERP system is expected to provide better solutions to problems, optimal use of resources, sets of reliable information, and opportunities for firm development (Ruivo et al., 2012). Likewise, it provides firms with access to client and market information that permits a firm to examine and gauge external opportunities (HassabElnaby et al., 2012). The extant literature reveals that an efficient and effective implementation of ERP also facilities intra- and inter-firm relationships to maintain customer relationships and knowledge management (Soliman and Noorliza. 2022). In sum, several benefits can be achieved by accurately implementing ERP. However, implementing ERP requires huge costs and strong commitments to bring a noteworthy change in the firm’s operations. Thus, this study is developed on the resource-based view (RBV) model that emphasizes efficient utilization of resources, implementation of innovative strategies, and reassurance of IOC.

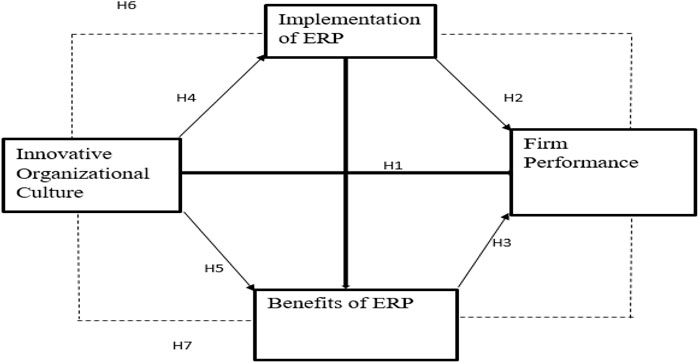

The main objective of this study is to examine the processes through which the Innovative Organizational Culture (IOC) affects firm performance (FP), illustrated in Figure 1 (constructs are defined in Table 1). Specifically, we first analyze the effect of IOC, ERP implementation, and ERP benefits on FP. Following that, we study the impact of IOC on the implementation of ERP, and the impact of ERP implementation on the benefits of ERP. Finally, this study explores the mediating role of 1) the implementation of ERP in the relationship between IOC and the benefits of ERP and 2) the benefits of ERP in the relationship between the implementation of ERP and FP. In addition, this study conducts a subsample analysis and tests the outlined objectives separately for energy- and non-energy-sector firms. The extant literature indicates that the energy sector in Pakistan is poorly administrated, underdeveloped, facing a severe financial crisis and circular debt, unable to control electrical power theft, and provides low quality of service and insufficient transmission and distribution infrastructures (Ali et al., 2017; EIA 2016). While existing studies have examined various techno-economic feasibilities (Ali et al., 2021), determinants of renewable energy adoption (Ahmar et al., 2022a), and households’ energy choices to overcome the chronic energy crisis in Pakistan (Ahmar et al., 2022b), the firm performance of energy sector firms in Pakistan is not examined in the context of IOC, implementation of ERP and benefits of ERP. Therefore, investigating the role of IOC, implementation of ERP, and ERP benefits on firm performance of energy sector firms is an interesting question that needs a comprehensive assessment. In sum, this study first conducts a market-wide analysis that includes all firms, followed by a separate examination of energy- and non-energy-sector firms for comparison purposes.

FIGURE 1. Research model.

TABLE 1. Literature defining the construction of variables/constructs.

This study contributes to the extant literature examining the process through which IOC affects FP in the presence of ERP benefits and implementation of ERP. Further, this study contributes to the literature concerning the differences between energy and non-energy sector firms, specifically, in the context of IOC, implementation of ERP, and ERP benefits as influencing factors for firm performance. Major findings of this study show that 1) IOC and benefits of ERP are positively related to firm performance, 2) IOC is positively related to implementation of ERP, 3) implementation of ERP is positively related to ERP benefits, 4) IOC and benefits of ERP are mediated by the implementation of ERP, and 5) the relationship between implementation of ERP and firm performance is mediated by the benefits of ERP. Overall, the findings of this study support our hypotheses with one exception, implementation of ERP is not related to firm performance in Pakistan. Our subsample analysis reveals that the insignificant impact of ERP implementation on FP is confined to energy and manufacturing sector firms. In contrast, the effect of ERP implementation on FP is significantly positive in the subsample of service and non-manufacturing sector firms, which require less energy (electrical power), in Pakistan.

The remainder of this study is structured as follows. Section 2 provides the theoretical background and literature review to explain the hypotheses development. Section 3 of the study describes the methodology employed in this study. Section 4 discusses the main results of the study. Finally, Section 5 provides conclusions, implications, and future extensions of the study.

2 Theoretical framework and hypotheses development

2.1 The resource-based view and innovative organizational culture

The resource-based view (RBV) states that firms utilize all their resources to foster IOC to achieve a competitive edge in the market and increase FP. IOC is an intangible asset used to respond to inventions, effectually take risks efficiently, and proficiently forecast future market trends (Brettel and Cleven. 2011). IOC enhances the power of creativity, shared responsibility, and decentralized decision-making, leading to higher employee motivation. Similarly, the implementation and execution of creative solutions are also encouraged by a resource-based view (Wamba et al., 2017; Uzkurt et al., 2013).

2.2 Implementation of enterprise resource planning

ERP is a comprehensive integrative system of planning, arrangement, and testing that improves the efficiency of an organization’s operations. It also provides real-time data, reliable information, effective channel coordination, and enhances customer service through the integration of the resources (Chofreh et al., 2018). Organizations that have efficaciously implemented the ERP system are found to provide state-of-the-art solutions to existing problems. Similarly, implementing ERP enhances employees’ ability to fulfill tasks and efficiently make optimal decisions. Other well-documented benefits include improved operational performance and replacing existing systems and processes with new advanced alternatives to improve firm performance (Awa et al., 2021).

2.3 Benefits of enterprise resource planning

The value attained as the outcome of the ERP implementation—quick generation of financial information, reduced cycle time, decreased operational cost, increased operational capacity, and rapid response to customers and suppliers—is considered a benefit of ERP. Yang and Lim (2009) state that ERP has numerous benefits, which can be categorized into five dimensions: operational, managerial, strategic, technological (IT and infrastructure), and organizational. Operational benefits are associated with automating cross-sectional processes (Yang and Lim 2009). ERP enables firms to standardize, rebuild, streamline, and automate internal tasks to improve the operations of firms. For instance, effective inventory management, cost reduction, decreased time lags, and enhanced customer services (Psarakis 2015). Managerial benefits include efficiently managing human resources, production, and inventory (Yang and Lin 2014). It is also associated with monitoring and controlling the financial outcome of firms’ activities (Yang and Lim 2009).

Strategic benefits focus on the capability of the system to support business growth. ERP implementation enables firms to reduce costs, enhance differentiation, improve innovation, have reliable information, and strengthen external linkages (Bradford and Florin 2003). The benefits of Information Technology (IT) infrastructure consist of profits arising from a cost reduction to maintain the legacy systems. ERP systems, with their integrated and standard applications, support business flexibility for future changes, abridged IT costs, and enhance the competency for quick and economical implementation of new applications (Shang and Seddon 2002). In sum, the benefits of ERP include the facilitation of business learning, empowerment of staff, higher employee morale, and job satisfaction.

2.4 Firm performance

Firm performance indicates several concepts, such as growth, profitability, productivity, efficiency, return, competitiveness, directing, evaluation, efficacy, and quality (Taouab and Issor 2019). It is a combination of two aspects, namely efficiency and effectiveness, as firms show good performance simultaneously when they are efficient and effective (Siminica et al., 2020). Therefore, firm performance is measured by its actions, efficacy, and effectiveness (Al-Matari et al., 2014). However, organizational effectiveness and firm performance are different concepts: organizational effectiveness consists of three layers, while firm performance is a subset of organizational effectiveness covering operational and financial outcomes (Selvam et al., 2016). Firm performance can also be determined by operational- and financial-performance. Operational performance includes employees’, customers’, and suppliers’ satisfaction.

As employees’ satisfaction, customers’ satisfaction, and better firm performance are highly correlated factors, the “service profit chain” is developed based on three disciplines: employee capability, customer loyalty, and financial outcome. This practice reduces the training cost of new employees and turnover rate, which collectively enhances employee satisfaction and retention (Hosseini et al., 2022). Thus, the motivated employees turn to comparatively satisfied employees. Such highly enthusiastic employees also perform their tasks actively and ensure high-quality service; as a result, such firms generate higher sales and profits (Bernhardt et al., 2000).

Customers’ satisfaction plays a decisive role in the high performance of a firm (Johnson et al., 1996): it leads to repurchase intention and customer loyalty to meet customer expectations. Since all firms emanate in the market with the same objective—to meet customers’ expectations and improve the quality of the products and services (Santos and Brito 2012)—existing and loyal customers help achieve such outcomes compared to new customers (Munthe et al., 2022).

Suppliers’ satisfaction also plays a vital role in supply chain management. For example, recently, firms have been more focused on just-in-time delivery (JIT) and eliminating unnecessary carriage activities to reduce the distributive cost, boost the collaborative environment, and improve delivery and reliability (Soliman and Noorliza 2022).

2.5 Research model and hypotheses development

This part of the study explains the research model and hypotheses.

2.5.1 Innovative organizational culture and firm performance

Valencia et al. (2015) report that IOC has a positive relationship with FP: since it promotes creativity, initiative taking, and decentralized decision-making, employee motivation to improve firm performance substantially increases. Chen et al. (2020) report that IOC has a direct and significant relationship with FP, and boosts a firm’s outcomes, including higher profitability, production, improved growth, and better competitive advantage. Soft or non-economic outcomes consist of higher customer satisfaction, reduced employee turnover, and improved stakeholder relationship, which lead to comparatively higher firm performance. Artz et al. (2010) spotlight the direct and significant link between IOC and FP: the IOC-oriented firms enjoy higher profitability, growth, and competitiveness; thus, IOC leads to increased firm performance.

Contrarily, for organizations with a collective culture, bringing innovations is problematic and negatively affects the firm performance (Wang and Zatzick 2019). Khan et al. (2018) show an insignificant effect of IOC on FP, transformational leadership, and a conducive learning role in improving a firm’s internal capabilities. It is found that these two factors empower a firm’s internal environment and foster innovations. The absence of these elements in the Chinese industry leads to the low performance of firms. A higher distinctive culture in a firm tends to weaken the practices and effectiveness of collective culture, which leads to lower efficiency of group-oriented innovative ideas in the firm. It brings an inverse impact on the FP (Steenkamp et al., 1999).

Given the above discussion, this study examines whether the following hypothesis regarding the relationship between IOC and firm performance holds in Pakistan.

H1: Innovative Organizational Culture (IOC) is positively related to FP.

2.5.2 Implementation of enterprise resource planning and firm performance

The extant literature shows that higher firm performance is attained through implementing ERP, i.e., by reducing many employees, intensifying more reliable automation processes, providing reliable information, and bolstering a firm to scrutinize its development. Thus, Hunton et al. (2002) find that implementation of ERP brings a higher return on assets (ROA), return on sales (ROS), and return on investments (ROI). In addition, increased internal and external collaborations, improved communication processes by accessing wide-ranging information, enhanced organizational efficacy and productivity, and a strong decision-making process to attain a competitive edge in the market are other benefits well-documented in the literature (Haberli et al., 2017).

Contrary to the above findings, Rajan and Baral (2015) document an insignificant association between the implementation of ERP and FP due to the absence of entrepreneurial culture. Wieder et al. (2006) similarly find that a higher level of complexity in the implementation process incurs huge pre- and post-implementation costs; therefore, firms with an extensive ERP implementation history failed to achieve overall FP. From the perspective of the learning curve, existing literature shows that extensive trainings frustrate employees, which is also an important reason for reduced firm performance (Poston and Grabski 2000; Al-Dhaafri et al., 2016). This study proposes the following hypothesis regarding the relationship between ERP implementation and firm performance:

H2: Implementation of ERP is positively related to FP.

2.5.3 Benefits of enterprise resource planning and firm performance

The extant literature shows that ERP benefits advance both horizontal integration (i.e., the components of the value chain) and vertical integration (i.e., the supporting functions). Davenport (1998), Shang and Seddon (2002), and Wieder et al. (2006) document that ERP benefits include automation of business processes and incremental operational performance of firms by improving their quantity and quality of customer service. Yang and Lim (2009) report a positive association between the operational benefits of ERP and FP. By facilitating daily operations, improving cash management, and decreasing operating costs, ERP prompts production growth, boosts customer service quality, improves the management system, reduces costs and enhances the information flow. Esteves (2009) reports that the benefits of ERP and FP are significantly linked as ERP enhances the progress in financial processes, efficiently manages a firm’s operations, cuts down the inventory and administrative costs, and improves the approachability to market demands. ERP also upgrades the inbound logistics by diminishing the cost of raw material, personnel costs in accounts payable, purchases, and inventory management. In addition, Shang and Seddon (2002) report that strategic benefits make efficient internal and external linkages.

Sari et al. (2012) also report a direct link between both constructs, as firms may enjoy both IT infrastructure and organizational benefits. These benefits include improved customer satisfaction, enhanced vendor performance, enlarged flexibility, improved business innovations and sweeping changes, efficient communication between employees and management, enhanced employee morale, reduced quality costs, improved resource utility, higher information accuracy, and decision-making capability.

However, Rouhani and Mehri (2018) show that the benefits of ERP and FP have an insignificant relationship due to the lack of learning and training sessions. In the wake of existing literature proposes the following hypothesis regarding the relationship between the benefits of ERP and firm performance:

H3: Benefits of ERP are positively related to FP.

2.5.4 Innovative organizational culture and implementation of enterprise resource planning

Several relevant studies discuss the positive association between IOC and the implementation of ERP. Firms with higher IOC are more inclined toward adaptability, implementation of innovative techniques, business integration, management principles, learning opportunities, effective training sessions, retaining the knowledge workers, and effective decision-making (Amoako-Gyampah and Salam, 2004; Yusuf et al., 2004; Hsu et al., 2008; Damanpour and Schneider, 2009; Ruivo et al., 2012; Rouyendegh et al., 2014). On the contrary, Chou et al. (2014), Gajic et al. (2014), and Khan et al. (2018) did not find such a relation between IOC and implementation of ERP as the ERP implementation in their studies did not achieve the objectives of business process control, cutting down of cost, and increase in revenue. A further investigation suggests that the failure is the main reason for the loss, improper use of the system, lack of transformational leadership, and non-availability of top management support. Based on the above discussion, this study proposes the following hypothesis regarding the relationship between IOC and the implementation of ERP:

H4: IOC is positively related to the implementation of ERP.

2.5.5 Implementation of enterprise resource planning and benefits of enterprise resource planning

It is well established that ERP improves the flow of information across departments. The integration and standardization of the business processes smooth an organization’s operations, reducing the implementation and maintenance costs. Different from the above-stated well-established empirical findings, Gajic et al. (2014) report a reciprocal relationship between the implementation of ERP and the Benefits of ERP due to inefficient use of the technology and lack of perceived ease of use. This study, therefore, proposes the following hypothesis regarding the relationship between the implementation of ERP and the benefits of ERP.

H5: Implementation of ERP is positively related to the benefits of ERP.

2.5.6 The mediating role of implementation of enterprise resource planning

Martins and Terblanche (2003) and Matolcsy et al. (2005) document that the implementation of ERP mediates IOC and the benefits of ERP. Stratman (2007) reports a similar finding: it decreases the operational uncertainty, enhances the flow of information, improves the proper accessibility of a firm’s data, and empowers operational planning and decision-making. Unlike other outlined studies, implementation of ERP is not found to mediate the relationship between IOC and the benefits of ERP (Chou et al., 2014; Gajic et al., 2014): given that the improper use of the system and extended training leads to fewer benefits of ERP. This study proposes the following hypothesis regarding the mediation of the relationship between the IOC and the benefits of ERP by the implementation of ERP.

H6: The relationship between IOC and the benefits of ERP is mediated by the implementation of ERP.

2.5.7 The mediating role of benefits of enterprise resource planning

Stratman (2007) reports that the benefits of ERP mediate the relationship between the implementation of ERP and FP. ERP allows managers to align the structure and goals of firms to get better control of expenses, expand the efficiency of the supply chain, bring value to the customer, and improve the understanding of customers’ demands. A recent study by Menon (2019) reports that the benefits of ERP mediate the relationship between the implementation of ERP and FP in Canada. ERP enables firms to achieve fast and efficient business processes and standardized reporting through higher access to data sets, which are directly linked with a higher return on assets (ROA), returns on sales (ROA), and return on investments (ROI). Beheshti and Beheshti (2010) report that the benefits of ERP mediate the relationship between the implementation of ERP and FP. Thus, ERP is found to be vigorous in improving a firm’s productivity in two ways: operational effciency and customer satisfaction (Poston and Grabski 2000; Wieder et al., 2006). Report that the benefits of ERP do not mediate the relationship between the implementation of ERP and FP because recruitment of ERP engineers and knowledge workers is a costly activity, which may decrease the FP. Given the above discussion, this study proposes the following hypothesis.

H7: The relationship between the implementation of ERP and FP is mediated by the benefits of ERP.

3 Research methodology

3.1 Survey, instrument, sample, and data collection

This study employs primary data, which is collected with the help of an online survey: the questionnaire we use is adapted from prior seminal studies. The development of the measurement items, design and structure of the questionnaire is in line with the guidelines from existing studies (Aydiner et al., 2019). The questionnaire is divided into two parts: dummy variables and constructs. Dummy variables include the nature of the firm, experience with ERP, number of employees, and designation of the respondent. All the questionnaire items of constructs are measured on the five-point Likert scale ranging from Strongly Disagree = 1 to Strongly Agree = 5, following Chang et al. (2008).

The unit of analysis of the current study is the medium to higher-level managers from 1) Energy and Manufacturing sector firms and 2) Services and other non-Manufacturing sector firms using ERP packages in their operations. Since Pakistan is an energy-deprived country (Ali et al., 2017), we divide the sample into two groups based on the type of business they are doing: 1) firms in the energy sector and those businesses that require extensive energy to produce their goods; firms in the services sector and those businesses that need comparatively little energy to produce their goods (or run their main operations). According to Abacus, the total population of firms using ERP package in their operations are six hundred (600), belonging to energy, manufacturing, services, and different other sectors in Pakistan Data was collected from 239 medium to higher-level managers using the purposive sampling technique, from six big cities of Pakistan: Karachi, Lahore, Islamabad, Peshawar, and Quetta. The target sample size was calculated using the sample size table proposed by Krejice and Morgan (1970). Respondents were personally contacted on LinkedIn. This research uses the technique of structural equation modeling (SEM) using Smart-PLS (Version 3). Hair et al. (2017) mention that this technique examines the structural relationships among the constructs. SEM technique is a combination of multiple regression and factor analysis, well-applied in relevant studies.

3.2 Response rate

A detailed bifurcation of the number of respondent services and other industries is as follows (detailed in Table 2): investment, banking and finance = 20; transportation, telecommunication and media = 10; information systems and technology = 50; real estate = 5; health and social services = 10; consulting industry = 10; marketing industry = 10; pharmaceutical industry = 9; educational industry = 2; and distribution industry = 5. Similarly, a detailed bifurcation of number of respondent energy and manufacturing industries is as follows: textile industry = 30; petroleum (energy) industry = 20; glass industry = 5; steel industry = 20; sugar industries = 5; food and beverages = 6; Automobile industry = 5; cotton industry = 10; paint industry = 5; and plastic and leather industry = 6.

TABLE 2. Characteristics of sample.

4 Results and discussion

4.1 Confirmatory factor analysis

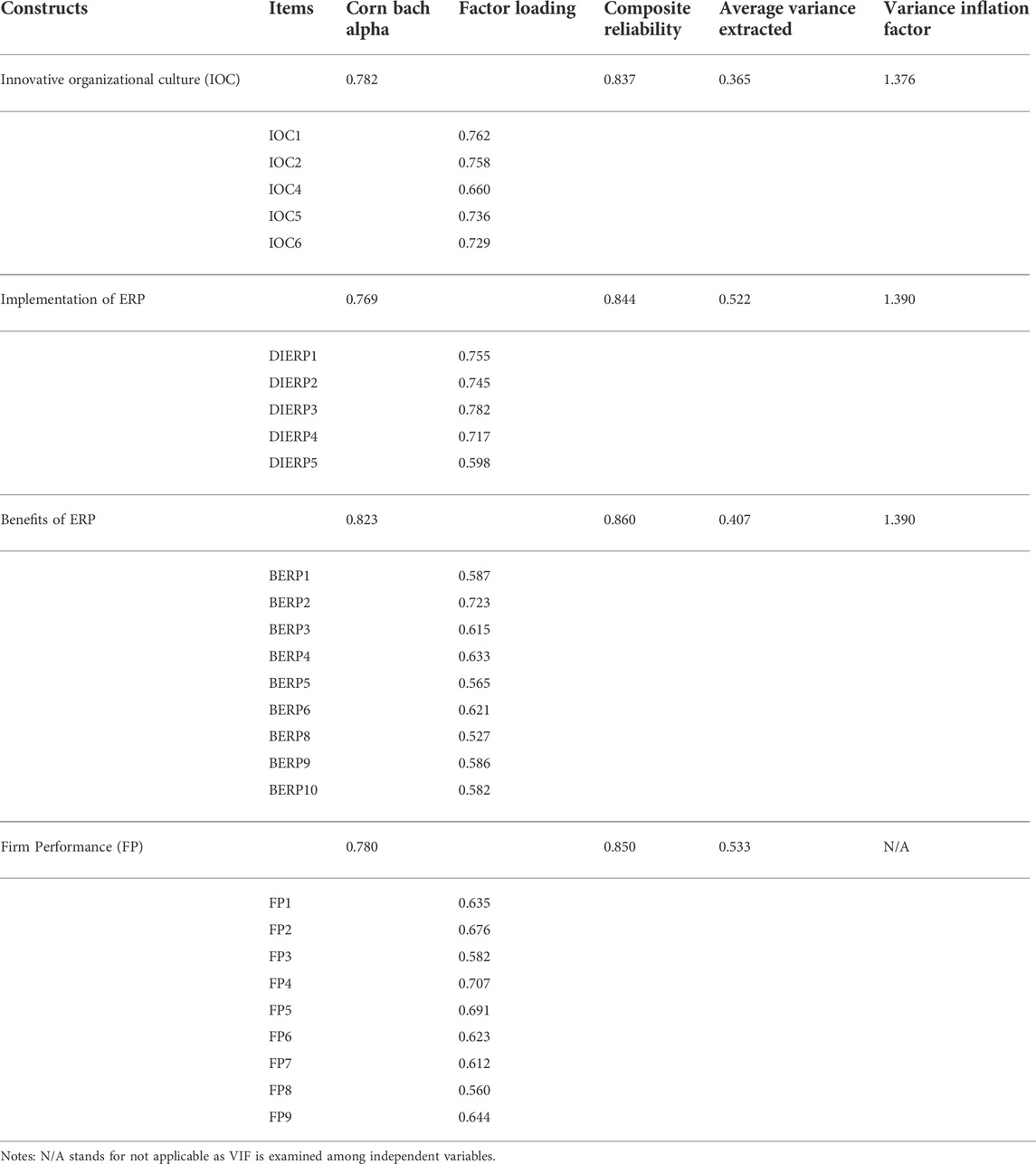

Harrington (2009) reports that Confirmatory Factor Analysis (CFA) is a type of structural equation modeling (SEM) that deals with the measurement model to test the hypothesis. It shows the relationship between the observed measures (indicators) and the latent construct of a particular research model to test the measurement model or the outer loadings. This study employs PLS-SEM to test the outlined hypotheses empirically. Bootstrapping with a subsample of 1,000 is practiced by Smart-PLS 3 to agree or reject the path coefficient. PLS algorithm does not support t-statistics, p-values, or standard error (Chin 1998). Suhr (2003) reports that CFA relies on statistical tests, namely convergent validity and discriminant validity. The concurrent validity consists of three other categories, namely factor loading (FL), composite reliability (CR), and average variance extracted (AVE), to determine the adequacy of model fitness. Table 3 shows the confirmatory factor analysis. A detailed description of each item mentioned in Table 3 is presented in the Supplementary Appendix. Note that we do not report those items that produce very small and insignificant values, for example, IOC3 and BERP7.

TABLE 3. Results of confirmatory factor analysis (CFA).

In this table, Cronbach’s alpha shows the consistency among the items of constructs. The value of Cronbach’s alpha should be greater than 0.6 (Hair et al., 2017). Average Variance Extracted is used to measure errors in data; its value should be 0.5 or above. If the value of AVE is less than 0.5 and the value of the alpha is greater than 0.6, then AVE is valid and acceptable. Since the implementation of ERP and the benefits of ERP could be highly correlated, we check multicollinearity among all the selected variables using Variance Inflation Factor (VIF) analysis. The acceptable range of VIF value is largely considered 4, whereas in some cases, 5 and 10 are also considered within the acceptable range (Ahmar et al., 2022a; 2022b). In this study, the VIF values of constructs are less than 4, indicating no multicollinearity among the constructs.

4.2 Discriminant validity

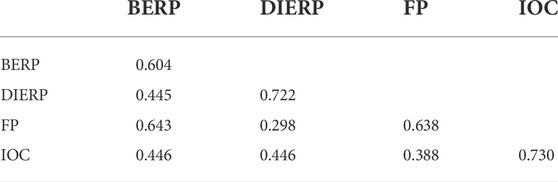

Ab Hamid et al. (2017) report that discriminant validity explains whether one construct empirically differs from the other. It also measures the degree of differences between the overlapping constructs. This study is focused on assessing discriminant validity using the Fornell-Lacker., 1996 criterion. It shows that all items belong to different constructs and are non-overlapping constructs. The square root of each construct’s AVE (diagonal) should have a greater value than all relative constructs’ correlations (off-diagonal). Table 4 reports the results of discriminant validity.

TABLE 4. Results of discriminant validity.

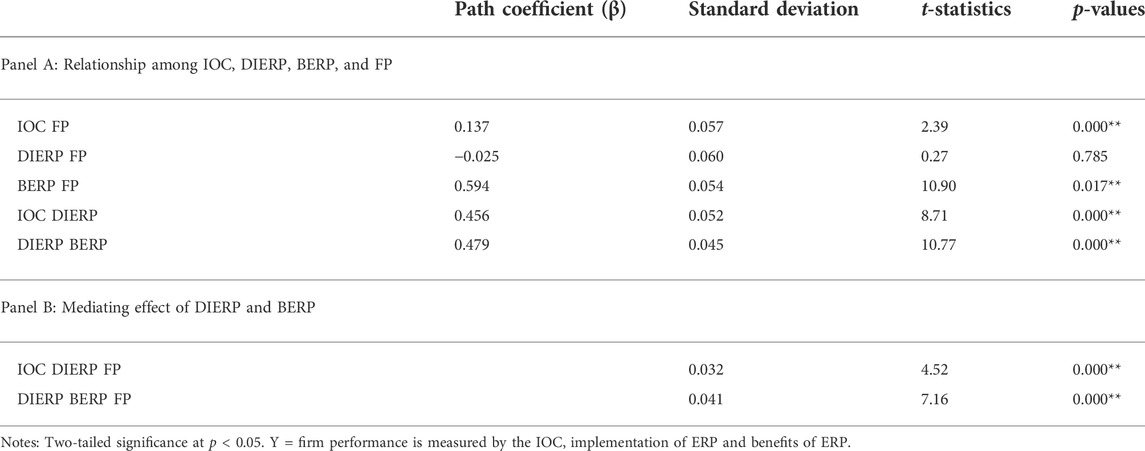

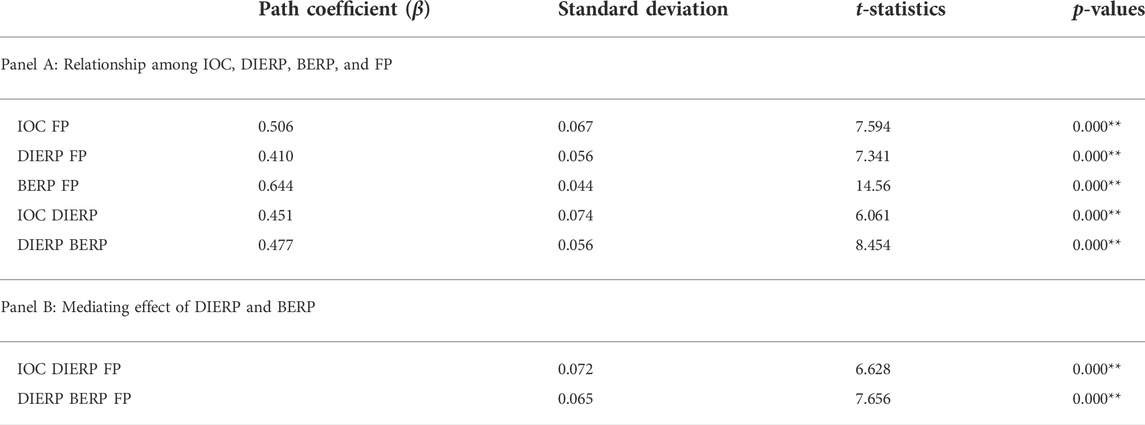

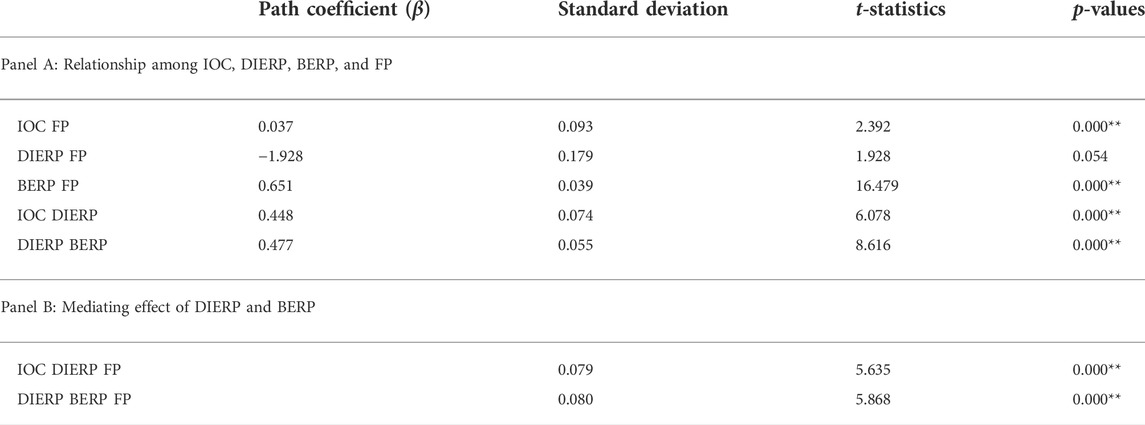

Table 5 reports the regression analysis results and shows that both IOC and the benefits of ERP (BERP) have a positive and significant relationship with FP: the path coefficients are 0.137 (p = 0.000) and 0.594 (p = 0.017), respectively. However, the relationship between the implementation of ERP (DIERP) and FP shows a negative and insignificant relationship; the value of the path coefficient is −0.025 (p = 0.785). These findings indicate that while hypotheses H1 (IOC-FP) and H3 (BERP-FP) are accepted, hypothesis H2 (DIERP-FP) must be rejected. Our further analysis shows that the relationship between IOC and DIERP and between DIERP and BERP is positive and significant, with path coefficients 0.456 (p = 0.000) and 0.479 (p = 0.000), respectively. Thus, we accept both H4 (IOC-DIERP) and H5 (DIERP-BERP) hypotheses.

TABLE 5. Relationship among IOC, DIERP, BERP and FP, and the mediating role of BERP and DIERP.

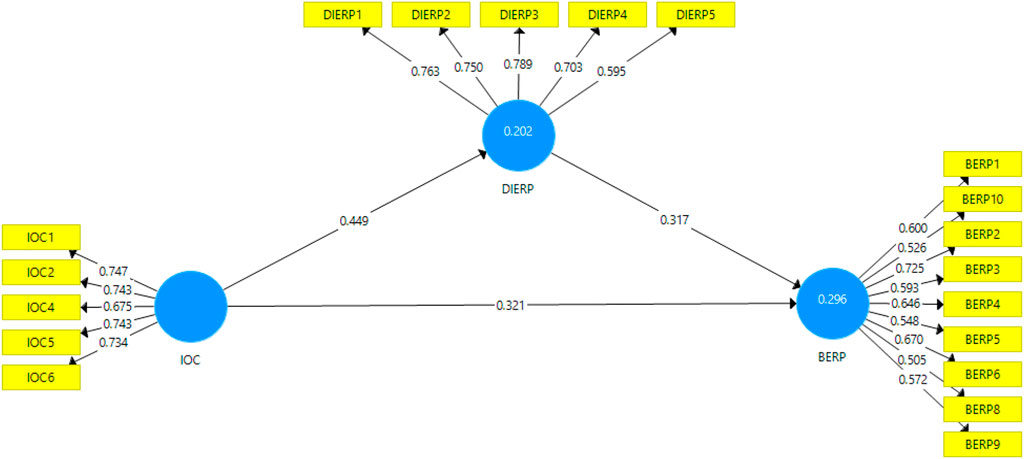

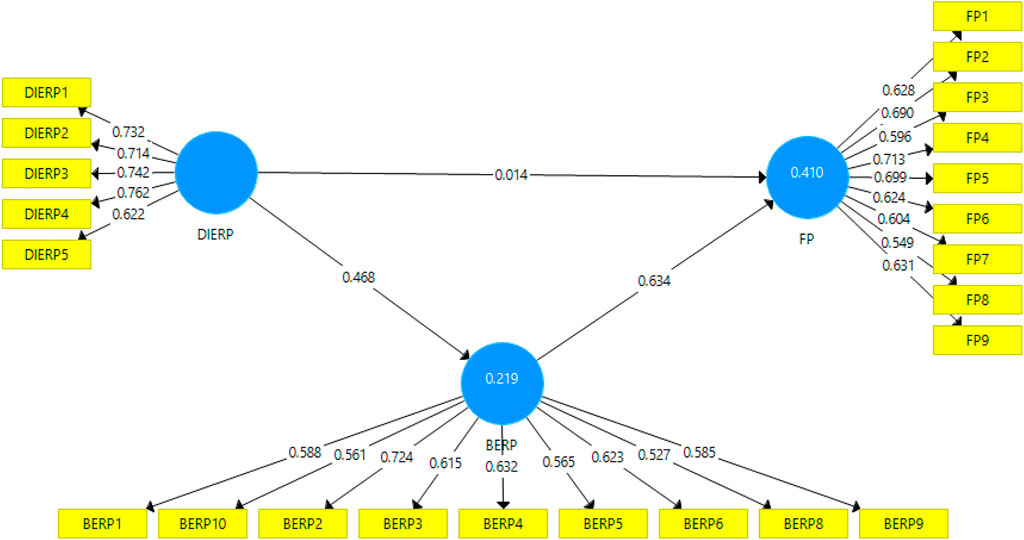

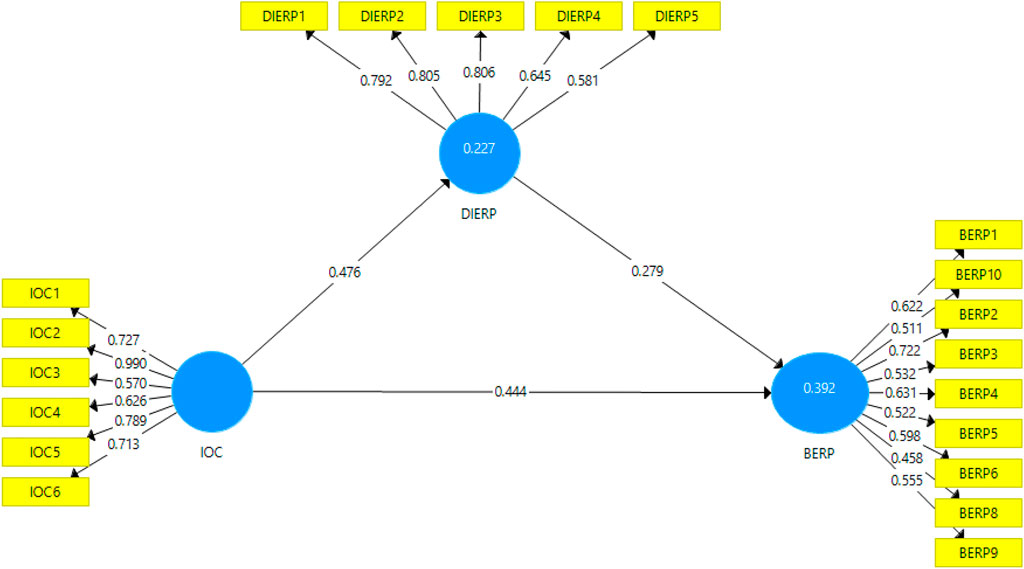

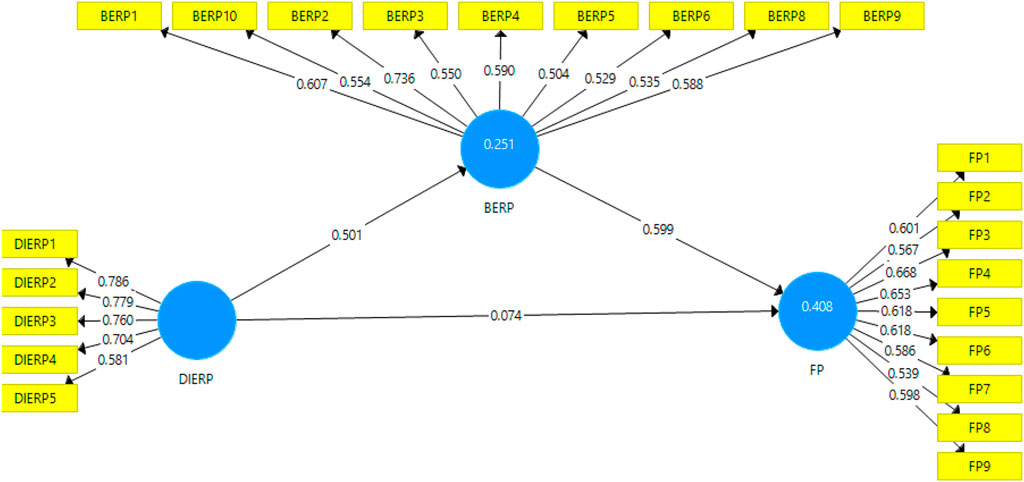

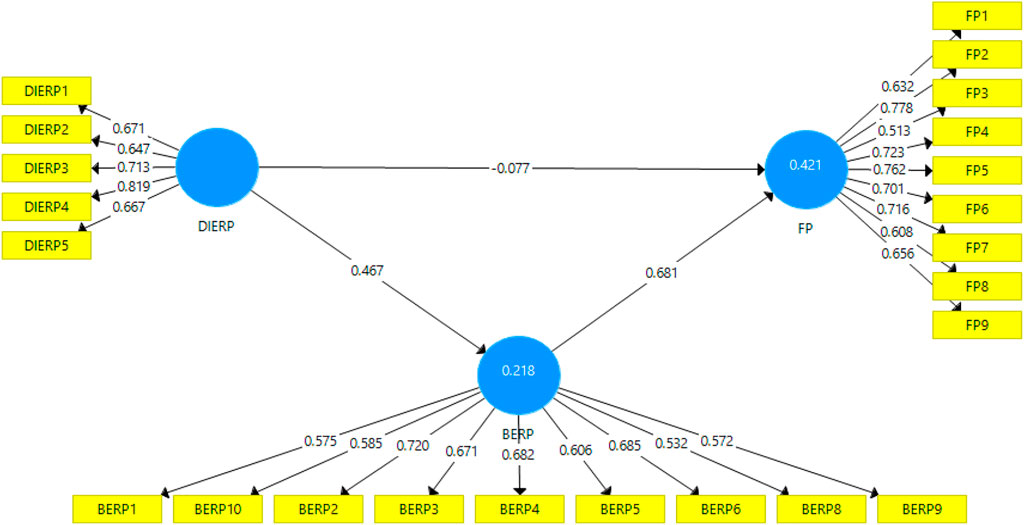

The results examining whether DIERP mediates IOC and BERP and BERP mediates DIERP and FP are presented in Panel B of Table 5. We find that the mediating relationship is significant and acceptable at a 95% confidence level for both DIERP and BERP; thus, we must accept hypotheses H6 (IOC-DIERP-FP) and H7 (DIERP-BERP-FP). The mediating role of BERP and DIERP are detailed in Figures 2, 3.

FIGURE 2. Mediating role of DIERP in the relationship between IOC and BERP.

FIGURE 3. Mediating role of BERP in the relationship between DIERP and FP.

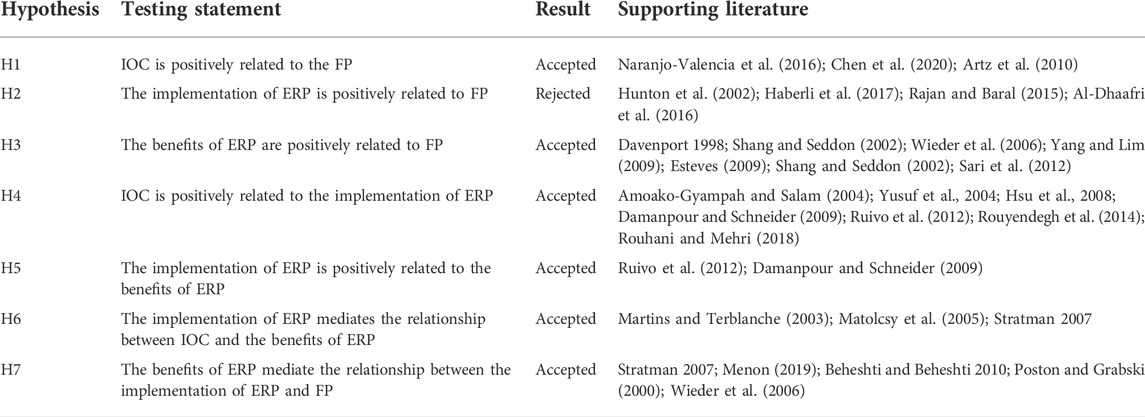

In sum, our regression analysis shows that all the outlined hypotheses are accepted except the negative and insignificant relationship between DIERP and FP, indicating that firms should emphasize the mechanism to shape, encourage and strengthen the ERP implementation to sustain the change and enhance FP accurately. It is evident that implementing ERP without IOC and a project management team creates various stressful situations for the firms. However, senior managers’ continuous monitoring of the implementation of ERP system and engagement in the overall team management and communication process could be the remedy. As a precise exposition of our major findings, the hypotheses we test and their corresponding empirical results are outlined in Table 6.

TABLE 6. Hypotheses testing and corresponding empirical results.

4.3 Robustness test

As discussed earlier, Pakistan is facing a chronic energy crisis that has severely affected the Pakistani society, economy, and business cycle variables, conceivably impacting many other factors (Ali et al., 2017, 2018). Therefore, for the robustness of our findings, we conduct a subsample analysis by dividing the sample firms into two groups: firms in the energy (petroleum) and manufacturing (energy-intensive) sectors; firms in the service and non-manufacturing (less energy-intensive) sectors. The results are presented in Table 7 (service and non-manufacturing firms) and Table 8 (energy and manufacturing firms).

TABLE 7. Relationship among IOC, DIERP, BERP, and FP, and the mediating role of BERP and DIERP: Service and non-manufacturing sector subsample.

TABLE 8. Relationship among IOC, DIERP, BERP, and FP, and the mediating role of BERP and DIERP: Energy and manufacturing sector subsample.

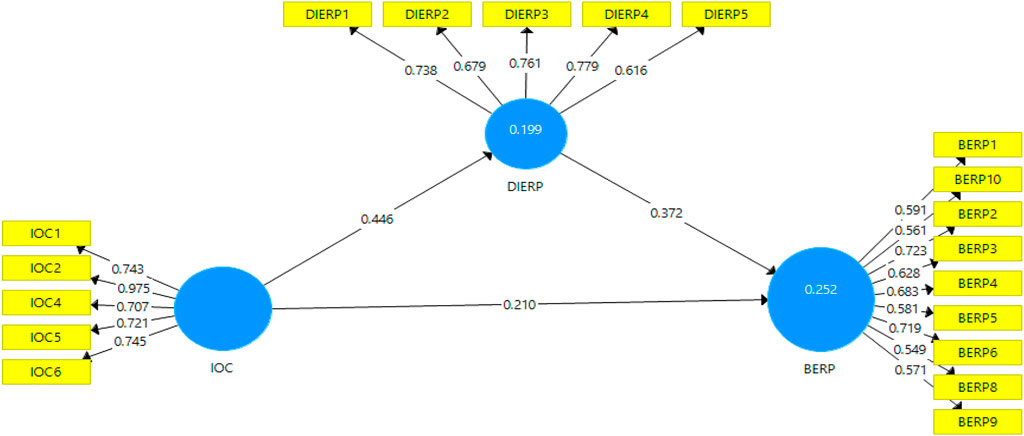

A straightforward comparison between Tables 6 and 7 demonstrates that while all the seven hypotheses (H1, H2, H3, H4, H5, H6, and H7) are accepted in the subsample of service and non-manufacturing sectors firms, six of them are accepted in the subsample of energy and manufacturing sector firms. H2 (DIERP-FP) is the only exception, which is negative and statistically insignificant at a 95% confidence interval (p = 0.054). Our results indicate that the insignificant and negative relationship between the implementation of ERP and FP in the full sample, reported in Table 4, is determined by the energy and manufacturing sector firms. Thus, once we exclude energy and manufacturing sector firms from the full sample, the negative relationship between the implementation of ERP and FP turns to positive and significant in the subsample of service and non-manufacturing sector firms. Therefore, we likewise suggest senior managers’ continuous monitoring and engagement in the overall team management and communication process while implementing the ERP system. Our further testing that examines the mediating role of DIERP and BERP in both subsamples is presented between Figures 4 and 7. Figures 4, 5, 6, 7 detail the mediating role of 1) DIERP in the relationship between IOC and BERP and 2) BERP in the relationship between DIERP and FP for the subsample of service and non-manufacturing (energy and manufacturing) sector firms, respectively.

FIGURE 4. Mediating role of DIERP in the relationship between IOC and BERP: A subsample of service and non-manufacturing sector firms.

FIGURE 5. Mediating role of BERP in the relationship between DIERP and FP: A subsample of service and non-manufacturing sector firms.

FIGURE 6. Mediating role of DIERP in the relationship between IOC and BERP: A subsample of energy and manufacturing sector firms.

FIGURE 7. Mediating role of BERP in the relationship between DIERP and FP: A subsample of energy and manufacturing sector firms.

5 Conclusions, implementations, and future recommendations

This study examines the processes through which Innovative Organizational Culture (IOC) affects firm performance (FP) in the wake of Enterprise Resource Planning (ERP) implementation and benefits. In addition, this study examines the mediating role of the implementation of ERP in the relationship between IOC and the benefits of ERP, and the benefits of ERP in the relationship between the implementation of ERP and FP. In doing so, we collect a comprehensive dataset from all major cities of Pakistan: the final sample includes 234 responses from medium-to high-level managers of firms that employ ERP systems. Given the well-documented energy crisis and circular debt of energy sector firms in Pakistan, our sample maintains a comparable number of firms between “energy and manufacturing” (112) and “service and non-manufacturing” (122) sectors.

In the light of existing literature, we test seven (7) hypotheses: 1) IOC is positively related to FP; 2) Implementation of ERP is positive related to FP; 3) Benefits of ERP are positively related to FP; 4) IOC is positively related to the implementation of ERP; 5) Implementation of ERP is positive to benefits of ERP; 6) Implementation of ERP mediates the nexus between IOC and benefits of ERP; and 7) Benefits of ERP mediates the relationship between implementation of ERP and FP. By employing Smart-PLS 3, we find that 6 out of 7 hypothesized relationships are true; thus, we accept 6 (H1 and H3–H7) hypotheses. The only exception is H2, indicating that the implementation of ERP is negatively and insignificantly related to firm performance. These findings suggest that IOC plays a crucial role in change management, which fosters innovations, encourages new ideas, and facilitates higher performance. IOC-oriented firms are likely to invest capital in technological innovations to adopt and implement advanced packages (e.g., ERP systems) in their operations to enhance FP. The negative and insignificant relationship between the implementation of ERP and FP shows that the implementation of ERP in the absence of IOC may create a stressful situation for a firm that possibly leads to decreased performance. In addition, we find that implementation of ERP mediates the relationship between IOC and benefits of ERP, and benefits of ERP mediates the relationship between implementation of ERP and FP.

Finally, we conduct a subsample analysis to understand whether the inter-relationships among IOC, the implementation of ERP, the benefits of ERP, and FP are diverse across firms in the “energy and manufacturing sector” and “service and non-manufacturing sector”. Our results show that while 6 of 7 hypotheses are true for the “energy and manufacturing” sector (similar to full sample analysis), all 7 hypotheses are accepted for the “service and non-manufacturing” sector. These findings indicate that the negative and insignificant relationship between the implementation of ERP and FP is confined to energy and manufacturing sector firms. Our empirical results and its interpretation in the light of extant literature together reveal that the implementation of ERP in the energy and manufacturing sector firms in the absence of IOC and project management experts could produce a stressful situation for a firm and its employees, which possibly are the main reasons of reduced firm performance. This study, therefore, suggests that senior- and medium-level managers should continuously monitor the implementation of ERP and determinedly engage themselves in the overall team management and communication process to achieve higher firm performance. Additional practical and managerial implications, specifically for Pakistan’s energy and manufacturing sector firms, include highlighting transformational leadership and efficient training sessions to sustain the change management system.

Further studies can take the perceived ease of the digital business ecosystem, environmental factors, and firm size, among other constructs, as exogenous variables affecting firm performance or moderators in the model. In addition, examining sector-wise sustainable business performance determinants (Hadi and Baskaran 2021), implementation of ERP in the light of industry 4.0 environment (Ferrari et al., 2021), and establishing guidelines for the implementation of sustainable ERP systems (Chofreh et al., 2020) can be interesting extensions of this study.

Data availability statement

The raw data supporting the conclusion of this article will be made available by the authors, without undue reservation.

Author contributions

YA: Conceptualization, data curation, software, formal analysis, methodology, writing—original draft; FA: Supervision, investigation, writing—review and editing.

Acknowledgments

We thank the Editor, the Associate Editor, the Subject Editor, the Special Issue Editors, and the reviewers for their rigorous review.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Supplementary material

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenvs.2022.991319/full#supplementary-material

References

Ab Hamid, M. R., Sami, W., and Sidek, M. M. (2017). Discriminant validity assessment: Use of Fornell & Larcker criterion versus HTMT criterion. J. Phys. Conf. Ser. 890, 012163. doi:10.1088/1742-6596/890/1/012163

Abdinnour-Helm, S., Lengnick-Hall, M. L., and Lengnick-Hall, C. A. (2003). Pre-implementation attitudes and organizational readiness for implementing an enterprise resource planning system. Eur. J. operational Res. 146 (2), 258–273. doi:10.1016/s0377-2217(02)00548-9

Addo-Tenkorang, R., and Helo, P. (2011). “Enterprise resource planning (ERP): A review literature report,” in Proceedings of the World Congress on Engineering and Computer Science 2 (5), 19–21.

Ahmar, M., Ali, F., Jiang, Y., Alwetaishi, M., and Ghoneim, S. S. M. (2022b). Households' energy choices in rural Pakistan. Energies 15 (9), 3149. doi:10.3390/en15093149

Ahmar, M., Ali, F., Jiang, Y., Wang, Y., and Iqbal, K. (2022a). Determinants of adoption and the type of solar PV technology adopted in rural Pakistan. Front. Environ. Sci. 10, 895622. doi:10.3389/fenvs.2022.895622

Al-Dhaafri, H. S., Al-Swidi, A. K., and Yusoff, R. Z. B. (2016). The mediating role of TQM and organizational excellence, and the moderating effect of entrepreneurial organizational culture on the relationship between ERP and organizational performance. TQM J. 28, 991–1011. doi:10.1108/tqm-04-2014-0040

Al-Matari, E. M., Al-Swidi, A. K., and Fadzil, F. H. B. (2014). The measurements of firm performance's dimensions. Asian J. Finance Account. 6 (1), 24. doi:10.5296/ajfa.v6i1.4761

Ali, F., Ahmar, M., Jiang, Y., and AlAhmad, M. (2021). A techno-economic assessment of hybrid energy systems in rural Pakistan. Energy 215, 119103. doi:10.1016/j.energy.2020.119103

Ali, F., He, R., and Jiang, Y. (2018). Size, value and business cycle variables. The three-factor model and future economic growth: Evidence from an emerging market. Economies 6 (1), 14. doi:10.3390/economies6010014

Ali, F., Jiang, Y., and Khan, K. (2017). “Feasibility analysis of renewable based hybrid energy system for the remote community in Pakistan,” in 2017 IEEE International Conference on Industrial Engineering and Engineering Management (IEEM), Singapore, 10-13 December 2017 (IEEE).

Amoako-Gyampah, K., and Salam, A. F. (2004). An extension of the technology acceptance model in an ERP implementation environment. Inf. Manag. 41 (6), 731–745. doi:10.1016/j.im.2003.08.010

Annamalai, C., and Ramayah, T. (2011). Enterprise resource planning (ERP) benefits survey of Indian manufacturing firms: An empirical analysis of SAP versus Oracle package. Bus. Process Manag. J. 17 (3), 495–509. doi:10.1108/14637151111136388

Artz, K. W., Norman, P. M., Hatfield, D. E., and Cardinal, L. B. (2010). A longitudinal study of the impact of R&D, patents, and product innovation on firm performance. J. Prod. innovation Manag. 27 (5), 725–740. doi:10.1111/j.1540-5885.2010.00747.x

Awa, H. O., Nwobu, C. A., and Igwe, S. R. (2021). Service failure handling and resilience amongst airlines in Nigeria. Cogent Bus. Manag. 8 (1), 1892924. doi:10.1080/23311975.2021.1892924

Aydiner, A. S., Tatoglu, E., Bayraktar, E., Zaim, S., and Delen, D. (2019). Business analytics and firm performance: The mediating role of business process performance. J. Bus. Res. 96, 228–237. doi:10.1016/j.jbusres.2018.11.028

Beheshti, H. M., and Beheshti, C. M. (2010). Improving productivity and firm performance with enterprise resource planningEnterprise Information Systems 4 (4), 445–472.

Bernhardt, K. L., Donthu, N., and Kennett, P. A. (2000). A longitudinal analysis of satisfaction and profitability. Journal of Business Research 47 (2), 161–171.

Bradford, M., and Florin, J. (2003). Examining the role of innovation diffusion factors on the implementation success of enterprise resource planning systems International journal of accounting information systems 4 (3), 205–225.

Brettel, M., and Cleven, N. J. (2011). Innovation culture, collaboration with external partners and NPD performance. Creativity innovation Manag. 20 (4), 253–272. doi:10.1111/j.1467-8691.2011.00617.x

Chang, M. K., Cheung, W., Cheng, C. H., and Yeung, J. H. (2008). Understanding ERP system adoption from the user's perspective. Int. J. Prod. Econ. 113 (2), 928–942. doi:10.1016/j.ijpe.2007.08.011

Chen, Y. S., Lin, S. H., Lin, C. Y., Hung, S. T., Chang, C. W., and Huang, C. W. (2020). Improving green product development performance from green vision and organizational culture perspectives. Corp. Soc. Responsib. Environ. Manag. 27 (1), 222–231. doi:10.1002/csr.1794

Chin, W. W. (1998). The partial least squares approach to structural equation modeling. Modern methods for business research, 295 (2), 295–336.

Chofreh, A. G., Goni, F. A., Klemeš, J. J., Malik, M. N., and Khan, H. H. (2020). Development of guidelines for the implementation of sustainable enterprise resource planning systems. J. Clean. Prod. 244, 118655. doi:10.1016/j.jclepro.2019.118655

Chofreh, A. G., Goni, F. A., and Klemeš, J. J. (2018). Sustainable enterprise resource planning systems implementation: A framework development. J. Clean. Prod. 198, 1345–1354. doi:10.1016/j.jclepro.2018.07.096

Chou, H. W., Lin, Y. H., Lu, H. S., Chang, H. H., and Chou, S. B. (2014). Knowledge sharing and ERP system usage in post-implementation stage. Comput. Hum. Behav. 33, 16–22. doi:10.1016/j.chb.2013.12.023

Cruz-Torres, W., Alvarez-Risco, A., and Del-Aguila-Arcentales, S. (2021). Impact of enterprise resource planning (ERP) implementation on performance of an education enterprise: A structural equation modeling (SEM). Stud. Bus. Econ. 16, 37–52. doi:10.2478/sbe-2021-0023

Damanpour, F., and Schneider, M. (2009). Characteristics of innovation and innovation adoption in public organizations: Assessing the role of managers. J. public Adm. Res. theory 19 (3), 495–522. doi:10.1093/jopart/mun021

Davenport, T. H. (1998). Putting the enterprise into the enterprise system. Harvard business review 76 (4), 121–131.

EIA (2016). US Energy Information Administration. Pakistan’s key energy statistics Analysis- Energy Sector Highlights. Available at: http://www.eia.gov/beta/international/analysis.cfm?iso=PAK

Esteves, J. (2009). A benefits realisation road‐map framework for ERP usage in small and medium‐sized enterprises. J. Enterp. Inf. Manag. 22, 25–35. doi:10.1108/17410390910922804

Ferrari, A. M., Volpi, L., Settembre-Blundo, D., and García-Muiña, F. E. (2021). Dynamic life cycle assessment (LCA) integrating life cycle inventory (LCI) and Enterprise resource planning (ERP) in an industry 4.0 environment. J. Clean. Prod. 286, 125314. doi:10.1016/j.jclepro.2020.125314

Fornell, C., Johnson, M. D., Anderson, E. W., Cha, J., and Bryant, B. E. (1996). The American customer satisfaction index: Nature, purpose, and findings. J. Mark. 60 (4), 7–18. doi:10.2307/1251898

Gajic, G., Stankovski, S., Ostojic, G., Tesic, Z., and Miladinovic, L. (2014). Method of evaluating the impact of ERP implementation critical success factors–a case study in oil and gas industries. Enterp. Inf. Syst. 8 (1), 84–106. doi:10.1080/17517575.2012.690105

Gursoy, D., and Swanger, N. (2007). Performance-enhancing internal strategic factors and competencies: Impacts on financial success. Int. J. Hosp. Manag. 26 (1), 213–227. doi:10.1016/j.ijhm.2006.01.004

Haberli, C., Oliveira, T., and Yanaze, M. (2017). Understanding the determinants of adoption of enterprise resource planning (ERP) technology within the agri-food context: The case of the midwest of Brazil. Int. Food Agribus. Manag. Rev. 20 (1030-2018-023), 729–746. doi:10.22434/ifamr2016.0093

Hadi, S., and Baskaran, S. (2021). Examining sustainable business performance determinants in Malaysia upstream petroleum industry. J. Clean. Prod. 294, 126231. doi:10.1016/j.jclepro.2021.126231

Hair, J. F., Matthews, L. M., Matthews, R. L., and Sarstedt, M. (2017). PLS-SEM or CB-SEM: Updated guidelines on which method to use. Int. J. Multivar. Data Analysis 1 (2), 107–123. doi:10.1504/ijmda.2017.10008574

HassabElnaby, H. R., Hwang, W., and Vonderembse, M. A. (2012). The impact of ERP implementation on organizational capabilities and firm performance. Benchmarking Int. J. 19, 618–633. doi:10.1108/14635771211258043

Hendricks, K. B., Singhal, V. R., and Stratman, J. K. (2007). The impact of enterprise systems on corporate performance: A study of ERP, scm, and crm system implementations. J. operations Manag. 25 (1), 65–82. doi:10.1016/j.jom.2006.02.002

Hosseini, C., Humlung, O., Fagerstrøm, A., and Haddara, M. (2022). An experimental study on the effects of gamification on task performance. Procedia Comput. Sci. 196, 999–1006. doi:10.1016/j.procs.2021.12.102

Hsu, C. L., and Lin, J. C. C. (2008). Acceptance of blog usage: The roles of technology acceptance, social influence and knowledge sharing motivation. Information and management, 45 (1), 65–74.

Hunton, J. E., McEwen, R. A., and Wier, B. (2002). The reaction of financial analysts to enterprise resource planning (ERP) implementation plans (retracted). J. Inf. Syst. 16 (1), 31–40. doi:10.2308/jis.2002.16.1.31

Johnson, M. D., Nader, G., and Fornell, C. (1996). Expectations, perceived performance, and customer satisfaction for a complex service: The case of bank loans. Journal of Economic Psychology 17 (2), 163–172. doi:10.11114/ijsss.v4i7.1662

Jamrog, J., Vickers, M., and Bear, D. (2006). Building and sustaining a culture that supports innovation. People Strategy 29 (3), 9.

Kazemi, V., and Sullivan, J. (2014). “One millisecond face alignment with an ensemble of regression trees,” in Proceedings of the IEEE conference on computer vision and pattern recognition, 1867–1874.

Khan, M. A., Akram, T., Sharif, M., Awais, M., Javed, K., Ali, H., and Saba, T. (2018). CCDF: Automatic system for segmentation and recognition of fruit crops diseases based on correlation coefficient and deep CNN features. Computers and electronics in agriculture, 155, 220–236.

Krejcie, R. V., and Morgan, D. W. (1970). Determining sample size for research activities. Educ. Psychol. Meas. 30 (3), 607–610. doi:10.1177/001316447003000308

Lee, Y. C., Lu, S. C., Hsieh, Y. F., Chien, C. H., Tsai, S. B., Dong, W., et al. (2016). An empirical research on customer satisfaction study: A consideration of different levels of performance. SpringerPlus 5 (1), 1577–1579. doi:10.1186/s40064-016-3208-z

Li, W., Deng, N., Yang, Y., and Wang, L. (2018). Process focus and accentuation at different positions in dialogues: an ERP study. Language, Cognition and Neuroscience 33 (2), 255–274.

Li, W., Du, J., Zhao, Z., and Long, J. (2018). Fusion of medical sensors using adaptive cloud model in local Laplacian pyramid domain. IEEE Trans. Biomed. Eng. 66 (4), 1172–1183. doi:10.1109/tbme.2018.2869432

Liang, H., Saraf, N., Hu, Q., and Xue, Y. (2007). Assimilation of enterprise systems: the effect of institutional pressures and the mediating role of top managementMIS quarterly), 59–87.

Lotfy, M. A., and Halawi, L. (2015). A conceptual model to measure ERP user-value. Issues Inf. Syst. 16 (3), 54.

Lutfi, A. (2021). Understanding cloud based enterprise resource planning adoption among SMEs in Jordan. J. Theor. Appl. Inf. Technol. 99, 5944–5953.

Malik, M. O., and Khan, N. (2021). Analysis of ERP implementation to develop a strategy for its success in developing countries. Prod. Plan. Control 32 (12), 1020–1035. doi:10.1080/09537287.2020.1784481

Martín-de Castro, G., Delgado-Verde, M., Navas-López, J. E., and Cruz-González, J. (2013). The moderating role of innovation culture in the relationship between knowledge assets and product innovation. Technol. Forecast. Soc. Change 80 (2), 351–363. doi:10.1016/j.techfore.2012.08.012

Martins, E. C., and Terblanche, F. (2003). Building organisational culture that stimulates creativity and innovation. Eur. J. innovation Manag. 6, 64–74. doi:10.1108/14601060310456337

Matolcsy, Z. P., Booth, P., and Wieder, B. (2005). Economic benefits of enterprise resource planning systems: Some empirical evidence. Account. Finance 45 (3), 439–456. doi:10.1111/j.1467-629x.2005.00149.x

Melin, M., Astvik, W., and Bernhard-Oettel, C. (2014). New work demands in higher education. A study of the relationship between excessive workload, coping strategies and subsequent health among academic staff. Qual. High. Educ. 20 (3), 290–308. doi:10.1080/13538322.2014.979547

Menon, S. (2019). Effective strategies to overcome challenges in ERP projects: Perspectives from a Canadian exploratory study. Int. Bus. Res. 12 (7), 12. doi:10.5539/ibr.v12n7p12

Munthe, H., Lee, C., Hong, S., and Anggelinata, F. (2022). Increasing dividend payout ratio with financial performance strategy and the role of CEO in Indonesian consumer goods company. Enrich. J. Manag. 12 (2), 2027–2037. doi:10.35335/enrichment.v12i2.516

Naranjo-Valencia, J. C., and Calderon-Hernández, G. (2018). Model of culture forinnovation. Organ. Cult. 13, 34. doi:10.5772/intechopen.81002

Naranjo-Valencia, J. C., Jiménez-Jiménez, D., and Sanz-Valle, R. (2016). Studying the links between organizational culture, innovation, and performance in Spanish companies. Revista Latinoamericana de Psicología, 48 (1), 30–41.

Poston, R., and Grabski, S. (2000). The impact of enterprise resource planning systems on firm performance. Int. J. Account. Inf. Syst. 12, 20–39. doi:10.1016/j.accinf.2010.02.001

Psarakis, S. (2015). Adaptive control charts: Recent developments and extensions. Qual. Reliab. Eng. Int. 31, 1265–1280. doi:10.1002/qre.1850

Rajan, C. A., and Baral, R. (2015). Adoption of ERP system: An empirical study of factors influencing the usage of ERP and its impact on end user. IIMB Manag. Rev. 27 (2), 77–117. doi:10.1016/j.iimb.2015.04.004

Razaq, M., Zhang, P., and Shen, H. L. (2017). Influence of nitrogen and phosphorous on the growth and root morphology of Acer monoPloS one 12 (2), e0171321

Rauter, R., Globocnik, D., Perl-Vorbach, E., and Baumgartner, R. J. (2019). Open innovation and its effects on economic and sustainability innovation performance. J. Innovation Knowl. 4 (4), 226–233. doi:10.1016/j.jik.2018.03.004

Rouhani, S., and Mehri, M. (2018). Empowering benefits of ERP systems implementation: Empirical study of industrial firms. J. Syst. Inf. Technol. 20, 54–72. doi:10.1108/jsit-05-2017-0038

Rouyendegh, B. D., Baç, U., and Erkan, T. E. (2014). Sector selection for ERP implementation to achieve most impact on supply chain performance by using AHP TOPSIS hybrid method. Teh. Vjesnik-Technical Gaz. 21 (5), 933–937.

Ruivo, P., Oliveira, T., and Neto, M. (2012). ERP use and value: Portuguese and Spanish SMEs. Industrial Manag. Data Syst. 112, 1008–1025. doi:10.1108/02635571211254998

Santos, J. B., and Brito, L. A. L. (2012). Toward a subjective measurement model for firm performance. BAR Braz. Adm. Rev. 9, 95–117. doi:10.1590/s1807-76922012000500007

Sari, N. A., Hidayanto, A. N., and Handayani, P. W. (2012). Toward catalog of enterprise resource planning (ERP) implementation benefits for measuring ERP success. J. Hum. Resour. Manag. Res. 2012, 1–16. doi:10.5171/2012.869362

Schwieger, W., Machoke, A. G., Weissenberger, T., Inayat, A., Selvam, T., Klumpp, M., et al. (2016). Hierarchy concepts: Classification and preparation strategies for zeolite containing materials with hierarchical porosity. Chem. Soc. Rev. 45 (12), 3353–3376. doi:10.1039/c5cs00599j

Selvam, M., Gayathri, J., Vasanth, V., Lingaraja, K., and Marxiaoli, S. (2016). Determinants of firm performance: A subjective model. International Journal of Social Science Studies 4 (7), 90–100. doi:10.11114/ijsss.v4i7.1662

Shang, S., and Seddon, P. B. (2002). Assessing and managing the benefits of enterprise systems: The business manager's perspective. Inf. Syst. J. 12 (4), 271–299. doi:10.1046/j.1365-2575.2002.00132.x

Shi, J., Deng, G., Ma, S., Zeng, X., Yin, X., Li, M., et al. (2018). Rapid evolution of H7N9 highly pathogenic viruses that emerged in China in 2017. Cell host microbe 24 (4), 558–568.e7. doi:10.1016/j.chom.2018.08.006

Siminică, M., Avram, M., Roxana, L. P., and Avram, L.The University of Craiova, RomGnia (2020). The adoption of national green procurement plans from the perspective of circular economy. Amfiteatru Econ. 22 (53), 15–27. doi:10.24818/ea/2020/53/15

Soliman, M., and Noorliza, K. (2022). Adopting enterprise resource planning (ERP) in higher education: A SWOT analysis. Int. J. Manag. Educ. 16 (1), 20–39. doi:10.1504/ijmie.2022.119681

Spathis, C., and Ananiadis, J. (2005). Assessing the benefits of using an enterprise system in accounting information and management. J. Enterp. Inf. Manag. 18, 195–210. doi:10.1108/17410390510579918

Stratman, J. K. (2007). Realizing benefits from enterprise resource planning: does strategic focus matter?. Production and Operations Management, 16 (2), 203–216.

Steenkamp, J. B. E., Ter Hofstede, F., and Wedel, M. (1999). A cross-national investigation into the individual and national cultural antecedents of consumer innovativeness. J. Mark. 63 (2), 55–69. doi:10.2307/1251945

Suhr, K. I., and Nielsen, P. V. (2003). Antifungal activity of essential oils evaluated by two different application techniques against rye bread spoilage fungi. Journal of Applied Microbiology, 94 (4), 665–674.

Taouab, O., and Issor, Z. (2019). Firm performance: Definition and measurement models. Eur. Sci. J. 15 (1), 93–106. doi:10.19044/esj.2019.v15n1p93

Uzkurt, C., Kumar, R., Kimzan, H. S., and Eminoğlu, G. (2013). Role of innovation in the relationship between organizational culture and firm performance: A study of the banking sector in Turkey. Eur. J. innovation Manag. 16, 92–117. doi:10.1108/14601061311292878

Valencia, A., Mugge, R., Schoormans, J., and Schifferstein, H. (2015). The design of smart product-service systems (PSSs): An exploration of design characteristics. International Journal of Design 9 (1) Available at: http://www.ijdesign.org/index.php/IJDesign/article/view/1740/677

Wamba, S. F., Gunasekaran, A., Akter, S., Ren, S. J. F., Dubey, R., and Childe, S. J. (2017). Big data analytics and firm performance: Effects of dynamic capabilities. Journal of Business Research 70, 356–365.

Wang, T., and Zatzick, C. D. (2019). Human capital acquisition and organizational innovation: A temporal perspective. Acad. Manage. J. 62 (1), 99–116. doi:10.5465/amj.2017.0114

Wieder, B., Booth, P., Matolcsy, Z. P., and Ossimitz, M. L. (2006). The impact of ERP systems on firm and business process performance. J. Enterp. Inf. Manag. 19, 13–29. doi:10.1108/17410390610636850

Williams, M. D., Dwivedi, Y. K., Lal, B., and Schwarz, A. (2009). Contemporary trends and issues in IT adoption and diffusion research. Journal of Information Technology, 24 (1), 1–10.

Yang, S.-F., and Lin, L.-Y. (2014). Monitoring and diagnosing process loss using a weighted-loss control chart. Qual. Reliab. Eng. Int. 30, 951–959. doi:10.1002/qre.1670

Yang, S. U., and Lim, J. S. (2009). The effects of blog-mediated public relations (BMPR) on relational trust. J. public Relat. Res. 21 (3), 341–359. doi:10.1080/10627260802640773

Keywords: enterprise resource planning, RBV, firm performance, innovative organizational culture, ERP, energy sector, Pakistan

Citation: Ashraf Y and Ali F (2022) How innovative organization culture affects firm performance in the wake of enterprise resource planning? evidence from energy- and non-energy-sector firms in Pakistan. Front. Environ. Sci. 10:991319. doi: 10.3389/fenvs.2022.991319

Received: 11 July 2022; Accepted: 05 September 2022;

Published: 13 October 2022.

Edited by:

Munir Ahmad, Ningbo University of Finance and Economics, ChinaCopyright © 2022 Ashraf and Ali. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Fahad Ali, ZmFoYWRhbGlAemp1LmVkdS5jbg==