Lin Xiao1*

Lin Xiao1* Muneeb Ahmad

Muneeb Ahmad

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 03 November 2022

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.984346

This article is part of the Research Topic Accentuating the Effects of Digital Circular Economy Transformations on Environmental Sustainability View all 25 articles

The research examined the influence of the fundamental exchange rate misalignment and Least Developed Countries (LDCs) in Asia and Africa’s financial development on CO2 emissions in Asian countries using panel data from 1970 to 2021. The methodology consists of ARDL bound testing and PMG/ARDL estimators with dynamic OLS estimators. The results reveal that the long-run real exchange rates for least developed countries (LDCs) are expected to rise in CO2 emissions in Asian and African countries with improved trade and net foreign asset positions. The relative productivity and trade openness also increase the exchange rate, which also plays a vital role in the growth of CO2 emissions. Except for Egypt, all least developed countries (LDCs) currencies are overpriced throughout the research period at the same time; it would be harmed by increased openness, foreign direct investment inflows, and currency misalignment. Overvaluation harms Bahrain’s economic growth. In comparison, undervaluation helps Egypt that currency misalignment does not affect financial growth in any LDCs over the long run. In the short-run, more real investment, net foreign assets, and official assistance inflows would enhance financial growth in Qatar, Bahrain, Singapore, and South Korea. In contrast, trade openness would slow it down in Egypt and Kuwait. The study suggested that the poor economic performance is due to RER misalignment, which occurs when exchange rate policies are improper and causes a rise in CO2 emissions in many developing countries.

The real exchange rate is considered one of the most significant relative prices in an economy and one of the key factors influencing economic growth. Therefore, maintaining a suitably valued currency is necessary for raising economic performance in emerging countries. The research investigates the impacts of RER misalignment, trade openness, technology innovation, energy consumption, and economic growth on CO2 emissions in LDCs of Asia and Africa. The study has focused on finding the answers to the questions: what is the estimation of equilibrium RER? What are the relationships between trade openness, technology innovation and CO2 emissions? One of the main obstacles to economic growth in LDCs is faulty exchange rate policy. The most significant pathways via which globalization and technological innovation are spread are the realignment of RER and trade openness. Energy use, GDP growth, and CO2 emissions are all intricately connected. According to the literature on environmental economics, it is still debatable whether or not increased trade openness may significantly contribute to CO2 emissions (Dou et al., 2021). REER has a dramatic effect on developing countries ability to CO2 emissions. However, in both the short and long run, the actual exchange rate reflected the impact of changes in trade openness. claims that the spectacular East Asian growth is due to superior accumulation of physical and net foreign assets, but also prudent government intervention in allocating those resources to highly productive investment. Most of the investigations, both on developed and developing economies, showed the constructive outcome of foreign investment towards economic growth, which is subject to some variables, for example, net foreign assets, foundation, innovation, environmental issues, and exchange transparency. The Asian countries region remains the most vulnerable in the world, with high inflation pressure, a weak external position, chronic foreign currency shortages, rising external debt, incessant public deficits, and a high saving gap despite notable financial performance in some countries over the past decade (AfDB, 2020). Thanks to the currency’s depreciation, increased economic development comes at the expense of increased energy consumption and carbon dioxide emissions (Shah et al., 2022). When it comes to international trade, foreign direct investment (FDI) flow has taken precedence over international trade in recent years (Chen and Moore, 2010). Strict enforcement of environmental rules, industry-specific policies, and promotion of renewable energy resources are just some of the immediate measures that should implement to prevent environmental pollution (Shahid et al., 2022). For industrialized countries, FDI has a greater impact on lowering emissions than developing countries (Demena and Afesorgbor, 2020). Regarding foreign direct investment (FDI), China is experiencing a boom, but it is also a major polluter and has the dirtiest cities in the world (Cole et al., 2011). In addition to a positive and statistically significant connection between population and life expectancy in the short run, the population does not affect life expectancy in the long run, provided environmental quality and spending on the environment are high (Shah et al., 2021). In contrast, foreign direct investment (FDI) and the use of renewable energy improve the environmental quality of East Asian economies (Khan et al., 2022). Understanding these factors’ role in derunining a sector’s total factor productivity (TFP) can aid in searching for novel strategies to increase TFP in these industries (Jafri et al., 2018). It raises the price of imported goods and discourages domestic and international investment because devaluation distorts pricing signals. Therefore, implementing a pro-growth RER strategy is difficult (Aguirre and Calderon, 2006). A country’s exports considerably decrease these greenhouse gas emissions, and the agreement can counteract the relationship by decreasing the promotion impact of trade openness on CO2 emissions. Although remittances and energy consumption both raise CO2 emissions, the system GMM predicts that globalization will eventually decrease these emissions (Yang et al., 2020). Asian countries have adopted fixed exchange rate regimes as part of their anti-inflation measures, which are more susceptible to overvaluation than flexible rates (IMF, 2021). According to Hao et al. (2020), FDI can reduce CO2 emissions using province-level panel data. Environment deterioration is aided greatly by authoritarianism, globalization of politics, growth of the economy, improvement in the financial sector, increased use of energy, and growth of gross fixed capital creation (Jahanger et al., 2021). Because it minimizes pollution, free trade positively affects the environment (Erdogan, 2014). Globalization, financial growth, and energy use considerably worsen the GCC countries’ environmental quality (Yang et al., 2021). There was a unidirectional causal relationship between the real exchange rate, the balance of trade, and GDP, and between the balance of trade, the real exchange rate, and CO2 emissions (Ahmad et al., 2022). According to Le et al. (2016), high-income countries are less polluted than medium- and low-income countries. It may sum up the impact of RER misalignment on growth in two ways. According to Coudert and Couharde (2008), RER misalignment is a macro-financial disequilibrium primarily in relative pricing that stifles financial growth and erodes the efficiency of resources. Reduced economic growth, exports, and export diversification, as well as an increased risk of currency crises and political instability, are all possible outcomes of an RER misalignment (Ambaw et al., 2022).With an increase in carbon productivity and a shift toward a low-carbon emission, sustainable economic growth pattern, China is well on its way to achieving its goal of sustainability (Jahangir et al., 2022a). Financial growth and RER misalignment may have a linear or nonlinear connection (Rapetti et al., 2012). The findings indicate that the RER misalignment for Asian and African countries has been criticized for overvaluing the currencies of those regions. As a result, the RER misalignment might have serious negative consequences on economic growth in the LDCs of Asia and Africa in both the short and long run. Often, LDC currencies need to create a good exchange rate regime consistent with macroeconomic policy to resolve the persistent misalignment and reduce its harmful impact on economic growth. The paper also includes preliminary estimates of the RER misalignment for previously criticized Asian countries. Since sample countries have seen a devaluation of over 50% on average over the past decade, the RER disparity may present policy challenges.

The remainder of the article is set out as follows: The literature review is discussed in Section 2, and the research framework, data analysis procedure and research methods are presented in Section 3. The results and discussion are presented in Section 4, and finally, the conclusions with future suggestions are shown in Section 5.

In countries with high levels of corruption, trade openness raises carbon emissions; in those with low levels of corruption, it lowers them, says Chang (2015). There was no substantial influence on carbon emissions in high-income and upper-middle-income countries due to trade openness, and even worse, trade openness increased carbon emissions in low-income countries (Wang and Zhang, 2021). Globalization, economic growth, and non-renewable energy contribute to rising environmental degradation, financial development and renewable energy usage significantly compress the deterioration (Usman et al., 2022a). For many economies, RER misalignment and its influence on financial development have been extensively studied using various metrics of misalignment and growth models in the extant empirical literature. According to Rodrik (2008), financial growth is negatively impacted by RER misalignment, notably overvaluation. Agricultural growth in Africa is slowed by currency misalignments that persist for an extended period (Cottani et al., 1990). Globalization and renewable energy help countries lower their ecological footprint, whereas financial development, natural resources, and non-renewable energy all have beneficial effects on the footprint (Usman et al., 2022b). Trade openness has a favorable long-run impact on emissions of CO2 in Pakistan (Nasir and Ur Rehman, 2011). Although globalization has been linked to increased pollution levels, environmental benefits have resulted from increased trade, urbanization, and workforce (Kamal et al., 2021). A country’s openness to trade positively influences financial growth (Ulaşan, 2015). There is a positive correlation between financial growth and factors such as foreign direct investment (FDI), capital creation, money supply, and openness to trade. Still, inflation negatively correlates (Yang and Shafiq, 2020). It reduced the ecological footprints due to financial growth; this was especially true for Asian countries but not those in Africa, Latin America, and the Caribbean (Jahanger et al., 2022b). The rise in CO2 emissions and financial development has harmed the environment even more (Ayeche et al., 2016). In China’s power and heating industry, the influence of energy intensity, input, and energy composition plays a crucial role in reducing CO2e. This emission reduction effect is a rising trend (Jiang et al., 2022). An inverse relationship between carbon emissions and financial development is supported by evidence of financial development’s beneficial impact on CO2 emissions (Shahbaz et al., 2013). Financial growth and development are bad for the environment, while transportation infrastructure and foreign investment are good (Nguyen et al., 2021). There’s an enduring link between CO2 emissions, financial progress, financial growth, and energy consumption, as shown by the ARDL-bound test results (Mardani et al., 2019). Long-run environmental quality is severely harmed by economic growth, high energy use, and wide-open trade (Usman and Jahanger, 2021). Increased CO2 emissions result from the interplay between ICTs (information and communication technologies) and economic growth, with the moderating influence and international trade playing a similar role (Ke et al., 2022). There are four key sources of carbon dioxide emissions in growing economies: transportation, food security, industry, and finance (Heidari et al., 2019). Environmental levies in China have significantly benefited the economic performance and technical innovation input of substantially polluting businesses (Wang Z. et al., 2022). Although the central financial districts of each province tend to remain relatively unchanged, the southeast coastline area’s rate of green technology innovation is notably higher than that of the interior region (Han et al., 2022). Short-run increases in carbon dioxide emissions will result from a rise in GDP per capita during the current (Yuan and Huang, 2022). Per capita income, foreign direct investment, and oil prices have long-run impacts on Pakistan’s carbon emissions (Malik et al., 2020). Globalization and green investment greatly mitigate long-term environmental damage (Li et al., 2022). CO2 emissions from SSA countries are positively impacted by energy usage. Industrialization, urbanization, and fossil fuel use, although only somewhat over the long run (Appiah et al., 2021). The financial growth and foreign investment have boosted carbon emissions over time, and per capita, CO2 emissions rise in China as the country becomes more open to trade (Ajaz et al., 2020). Corruption control and regulatory quality reduce environmental efficiency, whereas government effectiveness rises, even after allowing for industrialization, energy use, and population (Bahizire et al., 2022). Liu et al. (2021) used the advanced panel approach based on slope uniformity and the cross-section correlation test to investigate the long-run impact of FDI on China’s environment. GDP and FDI influence carbon emissions positively, but international trade appears to have the opposite impact (Alshubiri and Elheddad, 2019). Growth in the economy and the financial sector both boost industrial production, with the former playing a vital role. At the same time, the latter is seen negatively due to the impact of foreign direct investment (Appiah et al., 2022a). Reports indicate a favorable effect of the renewable energy-growth nexus on institutional membership and a negative moderating effect on the general population (Appiah et al., 2022b). Salahuddin et al. (2018) showed no statistical association between financial development and clean energy usage, as investments are not clean and technology is not applied in applications with advantages for cutting prices. The shift from agricultural to industrial economies in the SSA coincides with infrastructural development (Appiah et al., 2022c). To maximize the impact of RER policies, traditional industrial strategies that raise the responsiveness of the aggregate supply to the RER are necessary. To ensure a stable and competitive RER, foreign currency market intervention and capital flow restriction are among the necessary tools (Guzman et al., 2018). Carbon and energy efficiency are becoming the most important variables in GHG emissions in economies such as the BRICS (Fabbri and Ninni 2014). The middle-income countries positively correlate openness to trade and carbon emissions (Shahbaz et al., 2017). Individual variability may be accommodated by the panel DOLS since it considers varied short-run dynamics, as well as individual-specific temporal trends and fixed effects. Rapid low-carbon technology transfer from high-income to low-income countries is only conceivable because trade is global (Ahmed et al., 2015). If the CO2 emissions and actual trade prices are incorrect, the TFP productivity assessment in China’s thermal power industry may be substantially affected (Chen and Jin, 2020). Zhang et al. (2011) investigated at the provincial level shows that the increase of green TFP is reduced when pollutants are included as unwanted outcomes. According to this theory, changing exchange rate definitions and time horizons can lead to varied exchange rate behaviors, with several short, medium, and long-run horizons possible (Driver and Westaway, 2003). The long-run RER and short-run RER error correction estimates generate equilibrium RER and RER misalignment indexes for the countries he picked (Elbadawi and Soto, 1997). For the United States dollar, the Japanese yen, and the German mark, evaluated the sensitivity of FEER estimates for each of these currencies to various formulations and hypotheses. Calculations based on the FEER model are fraught with error because of these two primary influences. Monitoring real exchange rate equilibrium and misalignment is an important tool for governments/central banks to guarantee that the economy remains stable (Baffes et al., 1999). Balance in the FEER method of analyzing current exchange rates is described as macro-financial balance, and the BEER approach identifies the RER misalignment in three stages (Clark and MacDonald, 1998). There appears to be a correlation between economic expansion, elevated energy consumption, and CO2 emissions (Karim et al., 2022). When endogeneity, serial correlation, and non-stationarity are detected, the group mean DOLS based on the between-dimension provides efficient and consistent long-run. The ECOWAS region’s economic growth is not significantly aided by financial development (Appiah et al., 2020). They can improve the long-run model’s accuracy by using the ARDL method. Carbon emission in Nigeria may largely be attributed to economic growth, financial development, and stock market performance, as shown by the ARDL long-run findings (Yu et al., 2022). According to Behera and Dash (2017), who used the FMOLS and DOLS estimators, there is a positive correlation between FDI and CO2 emissions.

The study uses data from six Asian and African countries (Qatar, Bahrain, Singapore, South Korea, Egypt, and Kuwait) to assess the influence of RER misalignment on financial growth from 1970 to 2021. An average of actual bilateral exchange rates against each trading partner is used to calculate the CPI-based REER data, which is acquired from Bruegel databases (https://www.bruegel.org.com). Lane and Milesi-(2021) Ferretti’s database (https://www.ferrettigroup.com) provides the net foreign asset position statistics. The PCTOT (product runs of trade) and WEO (world economic outlook) databases of the IMF (https://www.imf.org.com) are used to collect the data on the runs of trade and gross capital creation. World bank database (https://data.worldbank.org) is used to get information on a country’s trade openness, productivity gap, official development aid, GDP real and GDP real per person, total population, and extensive currency. The data relating to CO2 emissions (metric tons per capita) has been collected from the World Bank database (https://data.worldbank.org).

A problem in international macroeconomics remains the assessment of RER misalignment because of the ambiguity in the run “RER."The purchasing power parity (PPP) model and model-based methodologies are commonly used to measure RER misalignment. Model-based techniques include the Fundamental Equilibrium Exchange Rate (FEER), the Desired Equilibrium Exchange Rate (DEER), the Behavioral Equilibrium Exchange Rate (BEER), the Permanent Equilibrium Exchange Rate (PEER), and the Natural Real Exchange Rate (NREER). The FEER is the equilibrium RER that maintains internal and external balance (Williamson, 1994). RER equilibrium, sustainability of the basics, and a clear definition of the model and methods involved. The research indicated that actual exchange rates for tradable and non-tradable currencies are closely linked. Financial factors are the basis for the BEER model, which aims to explain the exchange rate’s real behavior. If driving fundamentals have major transitory parts, Clark and MacDonald (2000) recommend augmenting the BEER method with a PEER decomposition. Both Williamson’s (1994) Fundamental Equilibrium Exchange Rate (FEER) idea and Desired Equilibrium Exchange Rate (DEER) concept are included in the first group. Real exchange rates consistent with macro-financial goals are called DEERs (Bayoumi et al., 1994).

Methodologically, DEER’s computation is a compact version of the FEER, requiring the solution of three estimations of current account elasticities (Siregar, 2011). Reducing-form Eq. 1 below estimates the long-run REER-financial variables connection, which includes both fundamental and short-run factors.

However, there may be differences in the short-run coefficients and error variances between groups, as the pooled mean group (PMG) estimator shows in this article. Still, the long-run coefficients must be comparable (Pesaran et al., 1999). While allowing for some variation in intercepts and error variance, the PMG method confines the long-run coefficients to be the same across cross-sectional samples. The cointegration form modifies the ARDL model for panel data analysis. Given Y = [lnTOT, NFA, lnPD, lnOP, lnBM], the equilibrium RER is estimated using the PMG/ARDL model from Eq. 1, which states as:

Where Δ is the first difference of variables,

Where, Y = [lnTOT, NFA, lnPD, lnOP, lnBM]; q = 1, …., k, and p = 0,1, … … K lags;

Where, μi is unrestricted intercept,

Y

A real equilibrium return for nation ‘i’ at a time ‘t’ is denoted by the run “ERER.” Eq. 5 shows that the run of trade, relative productivity differences (RPDs), investment openness (TOE), and net foreign assets (NA) influence Turkey’s equilibrium REER and that currency misalignment is at a significant level once RER misalignment is assessed.

Y is real GDP per capita, INV is a genuine investment, HC is net foreign assets, OP is openness to trade, ODA is official development aid, MIS is misaligned, and τ is erroneous. Because comprehensive data is not available for the sample LDCs in the study. The dependent variable may be calculated using the 2015 United States dollar value of real GDP per capita. The Washington Consensus predicts that the misalignment coefficient will be negative and the undervaluation coefficient will be positive.

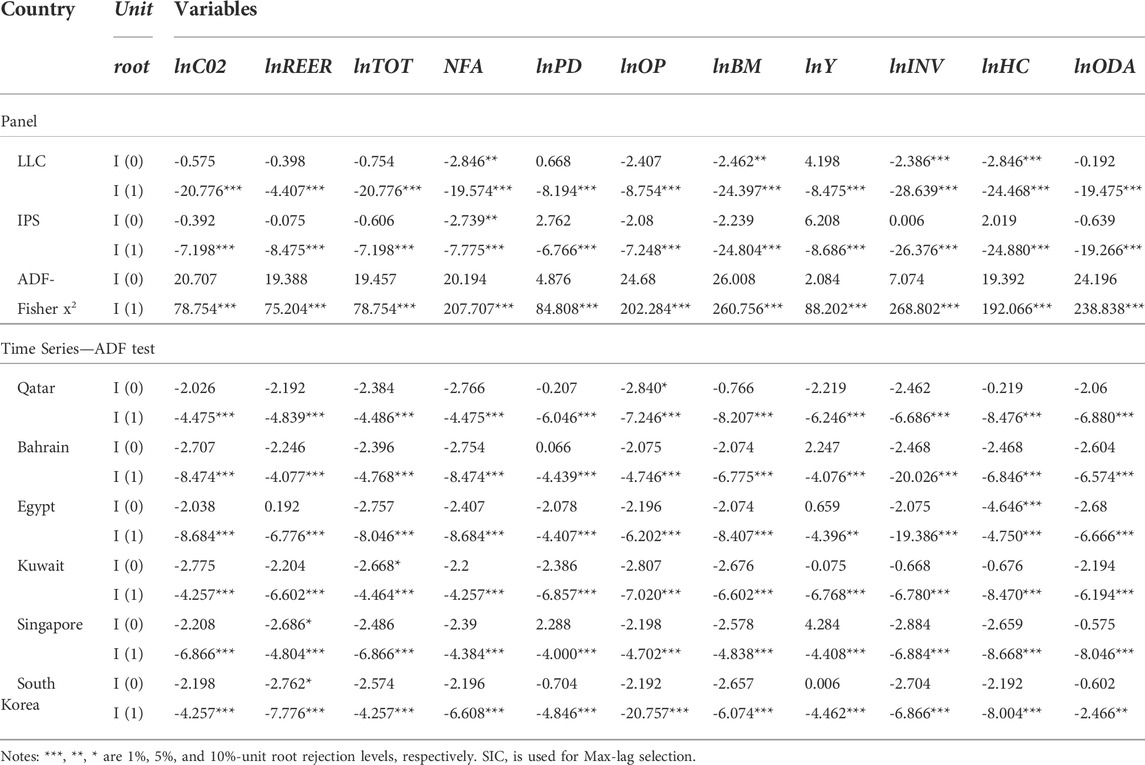

The unit root tests are carried out using the Levin-Lin-Chu (LLC), Im, Pesaran and Shin (IPS), and ADF-Fisher Chi-square tests for panel data, and Augmented Dickey-Fuller (ADF) with intercept for time series data in the Table 1 below. Even while the net foreign asset position appears stable at a certain level for the panel, unit root results demonstrated that all data series are integrated order one I (1) and may run an integration test.

TABLE 1. Shows the results of Unit Root Tests with Levin, ADF and IPS.

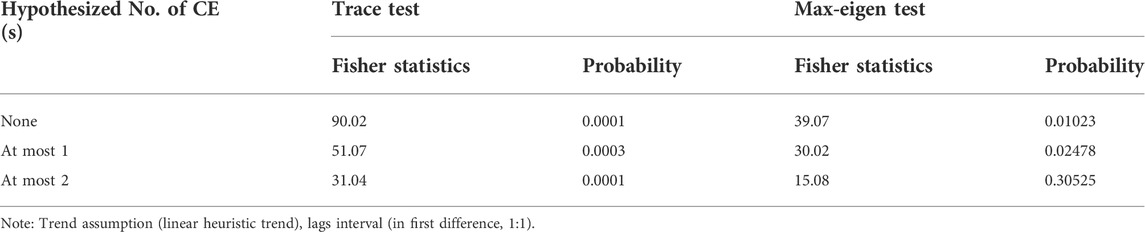

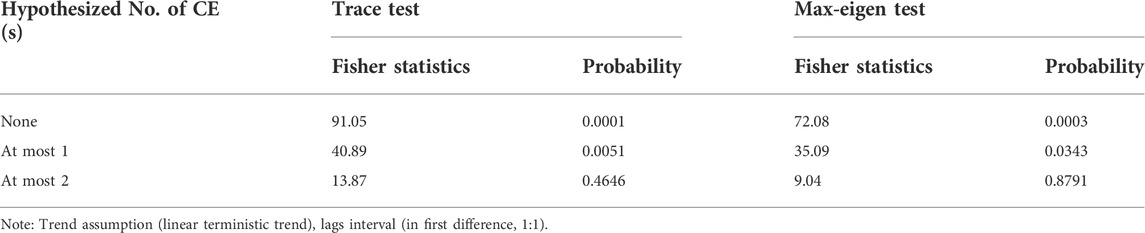

The REER and its fundamentals, such as runs of trade, net foreign asset, productivity difference, trade openness, and broad money, should be checked for cointegration to investigate the long- and short-run ruminants of REER. Table 2 shows the results of the Johansen cointegration tests, which reveal that the real exchange rate equation variables have a long-run connection with CO2 emissions. The long-run estimations are therefore possible by using an appropriate panel estimate technique.

TABLE 2. RER Model Cointegration test results from the Johansen Fisher panel.

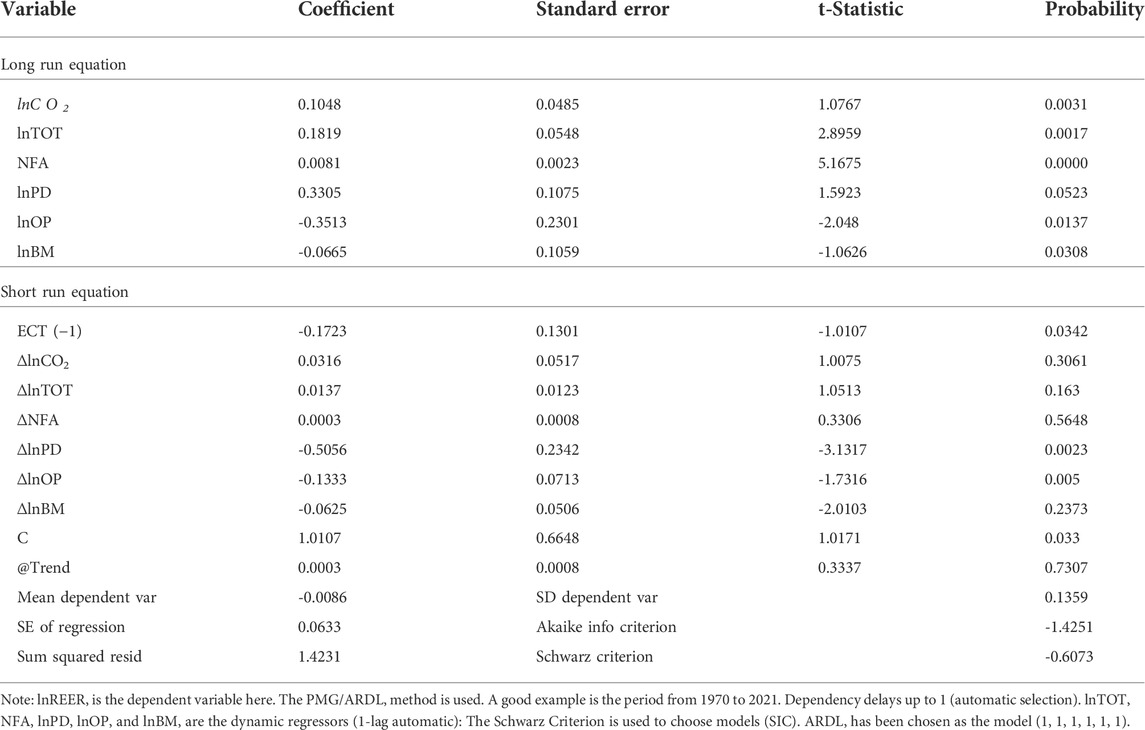

The REER panel’s long-run and dynamic short-run impacts on the REER are evaluated using the PMG technique (Pesaran et al., 1999). Table 3 shows the PMG and ARDL estimate findings. The adjustment coefficient is negative and statistically significant, indicating that REER and its fundamentals have a long-run cointegrating relationship. According to PMG data, overall fundamentals and short-run variables with their projected long-run signals drive REER. The REER is shown to appreciate in runs of trade and net foreign asset position; Although statistically significant, the net foreign asset position coefficient is negligible. The trade liberalization in LDCs may lower the price of non-tradable items relative to tradable commodities, as confirmed by the negative effect of trade openness and a strong effect to increase CO2 emissions. Sample LDCs’ currencies decline in the short run if their relative productivity and trade openness increases the CO2 emissions in Asian countries.

TABLE 3. The PMG/ARDL estimation results for real exchange rate model.

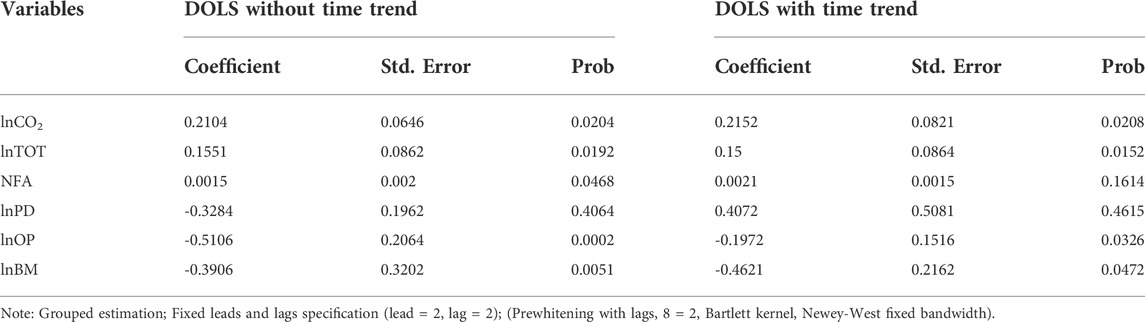

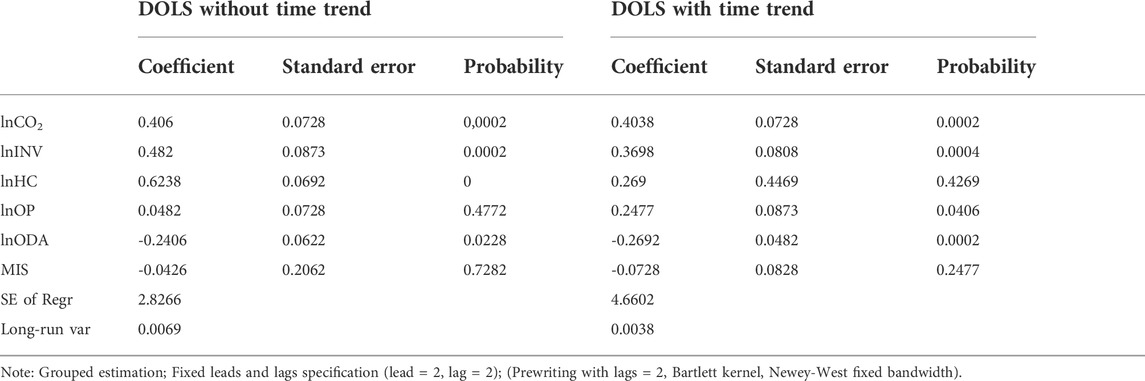

Panel DOLS with and without temporal trends are used to estimate the RER model to verify the robustness of the PMG results. According to Table 4, the DOLS results show similar conclusions to the PMG estimate and the group-mean panel DOLS estimation results for the RER model. The need for foreign currency increases as LDCs purchases more raw materials and capital goods for infrastructure development and increases CO2 emissions.

TABLE 4. Group-mean panel DOLS estimation results for the RER model.

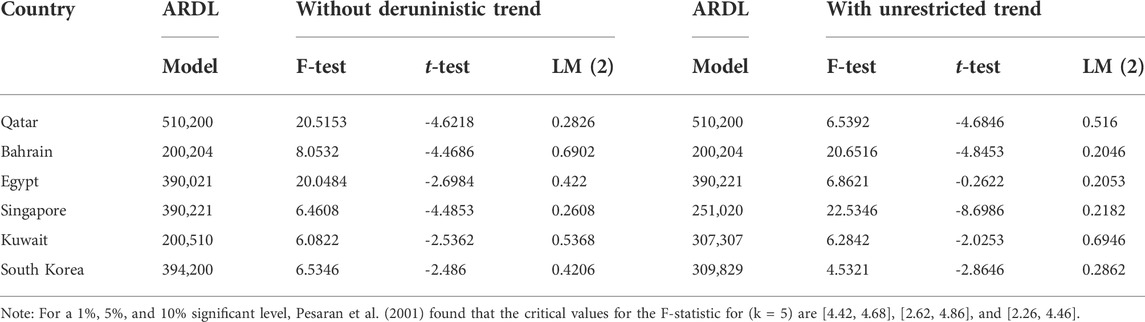

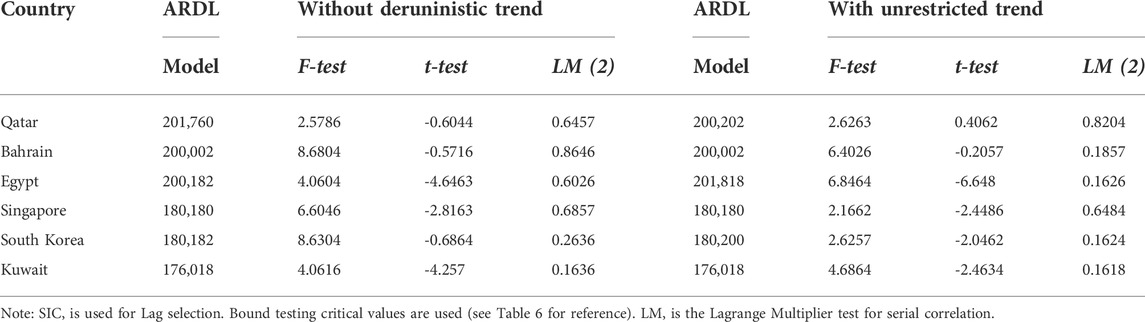

The effect of relative productivity discrepancy is statistically negligible under the DOLS estimate, which is defined to be negative. All the other variables obtained the anticipated indications and are defined to be statistically significant in LDCs to calculate the REER. Table 5 below shows the results of the bound testing based on the solid F-statistic values provided by (Pesaran et al., 2001). For all of the LDC samples, the REER’s long-run link with its fundamentals is confirmed by the F-test results. For Egypt and Kuwait, the t-statistic results of the bound testing are negligible.

TABLE 5. Bound F-test results for Real Exchange Rate Model.

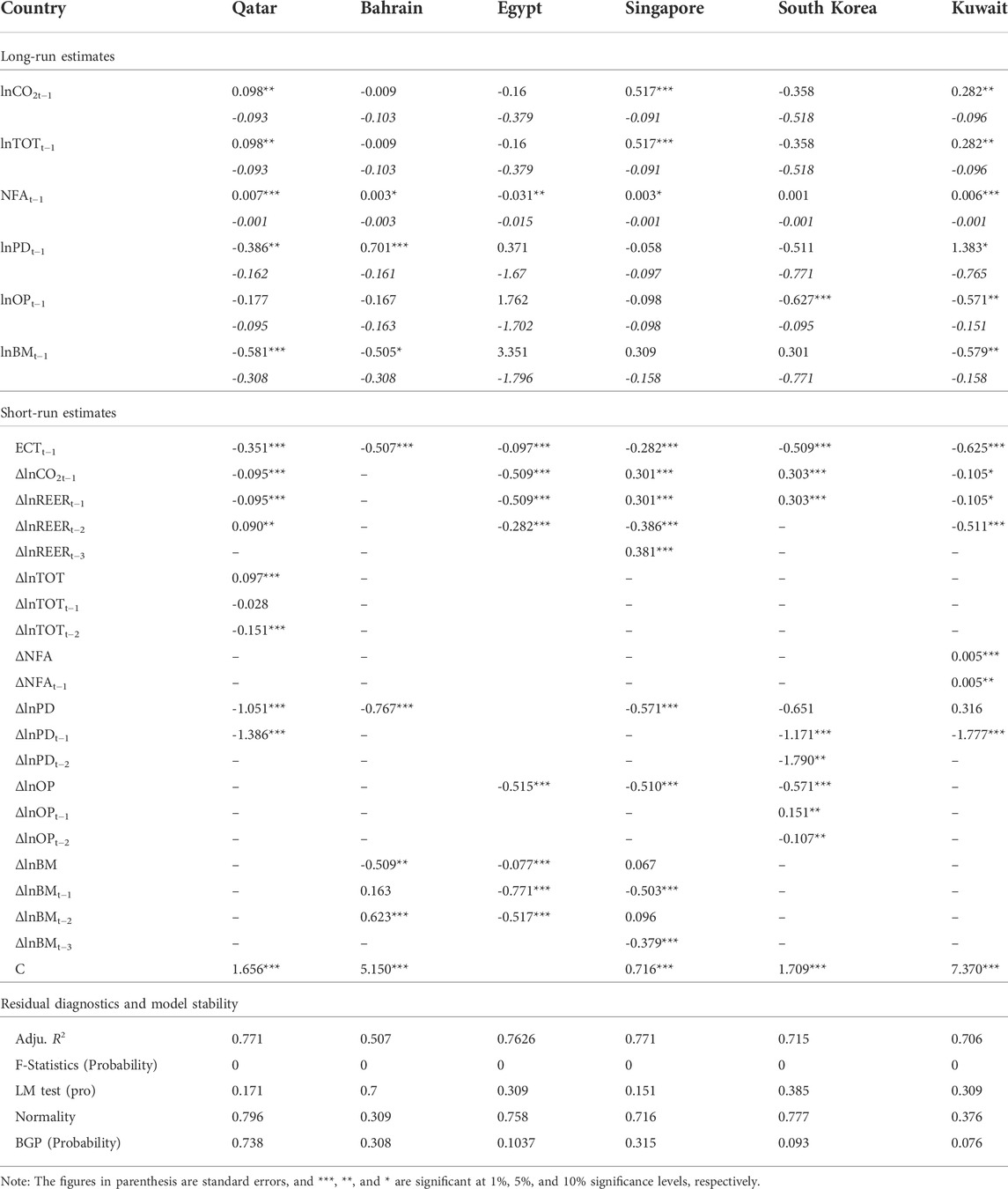

According to the ECT (1) run, the rate at which the REER returns to its equilibrium value is particularly slow in Egypt, South Korea, and Qatar. The Bound testing approach provides virtually identical outcomes when performed with or without a trend. ARDL estimates are therefore performed without considering a terministic trend since the trend is considered minor. Because of the cointegration, the ARDL technique may estimate the long-run and short-run coefficients for the REER ruminants. Table 6 shows the results of the unconstrained ARDL estimate, which are comparable to PMG findings. For Qatar and Egypt, the REER depreciates due to an improvement in relative productivity and an increase in a net foreign asset position. In the long run, the REER is appreciated in runs of trade and net foreign assets while depreciating in trade openness and comprehensive money supply for Qatar and Kuwait.

TABLE 6. Coefficients of ARDL estimation for the RER model.

Additionally, the REER appreciates in Bahrain while depreciating in the long run because of improved output. With an increasing money supply in the near run, the real exchange rate of South Korea, Egypt, and Bahrain currencies depreciates. Qatar and Kuwait’s currencies will rise in value if their trade and foreign asset improve. Due to greater trade openness, Egypt, Singapore, and South Korea REER depreciate. Popular belief one of the sample LDCs, an increase in the relative productivity gap leads to a decrease in the REER. Empirical data show a strong correlation between Asian countries’ CO2 emissions, LDCs’ real exchange rates, their runs of trade, net foreign assets, productivity, openness to trade, broad money supply, and trade openness across time.

The Johansen panel cointegration test is done again for the financial growth model. The results in Table 7 demonstrate a long-run link between the real GDP per capita and its regressors. Thus, the panel PMG/ARDL and DOLS models are estimated again to assess the influence of RER misalignment on the growth of LDCs. Indeed, the error correction run under the PMG estimation is negative and statistically significant, showing a long-run link among variables under the growth model.

TABLE 7. |Johansen fisher panel cointegration test results for growth model.

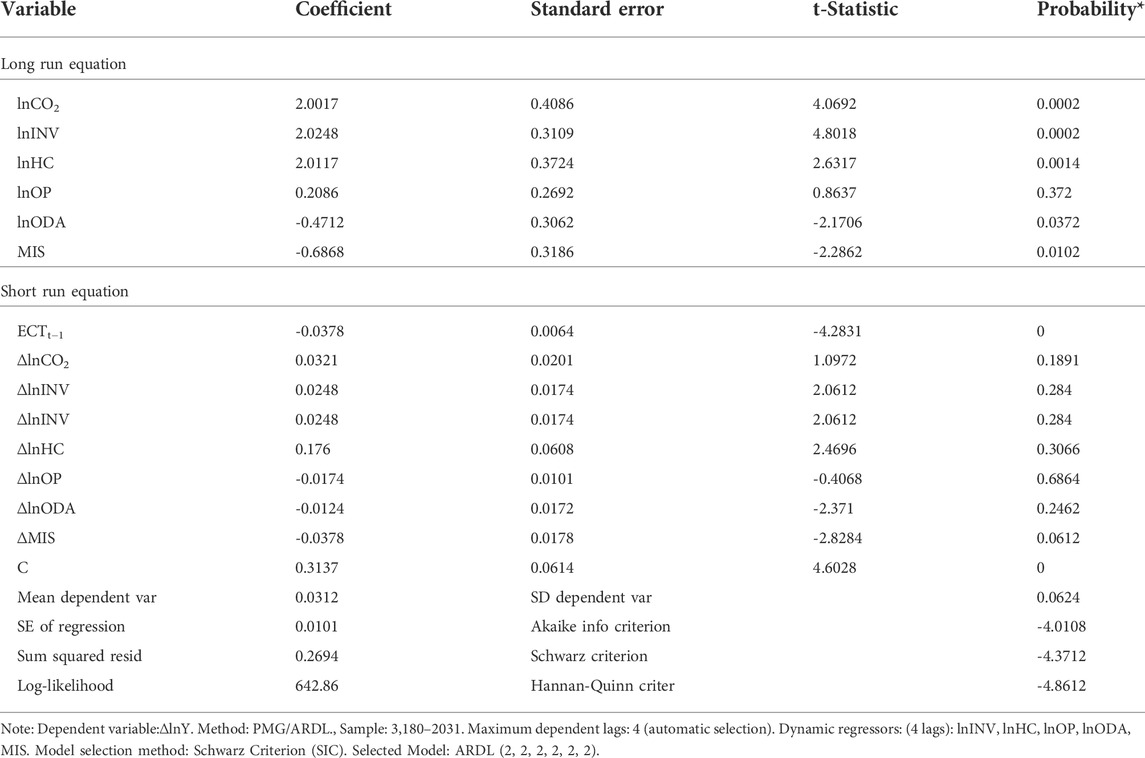

PMG and panel DOLS estimation results are shown in Tables 8, 9, and both estimations provided equivalent results. Findings reveal that financial growth in LDCs improves when real investment (gross fixed capital creation) increases and net foreign assets development increases. However, growth declines when ODA and RER misalignment increases CO2 emissions.

TABLE 8. The PMG/ARDL estimation results for the growth model.

TABLE 9. Group-mean panel DOLS estimation results for the growth model.

RER misalignment, which is fundamentally overvaluation, has both long-run (5%) and short-run (10%) negative financial consequences, similar to Rodrik (2008). RER misalignment is a severe problem for Asian countries’ LDCs’ financial progress. Because of uncertain macroeconomic policies and inadequate institutional structures and legal frameworks in LDCs, official development assistance may have a detrimental impact.

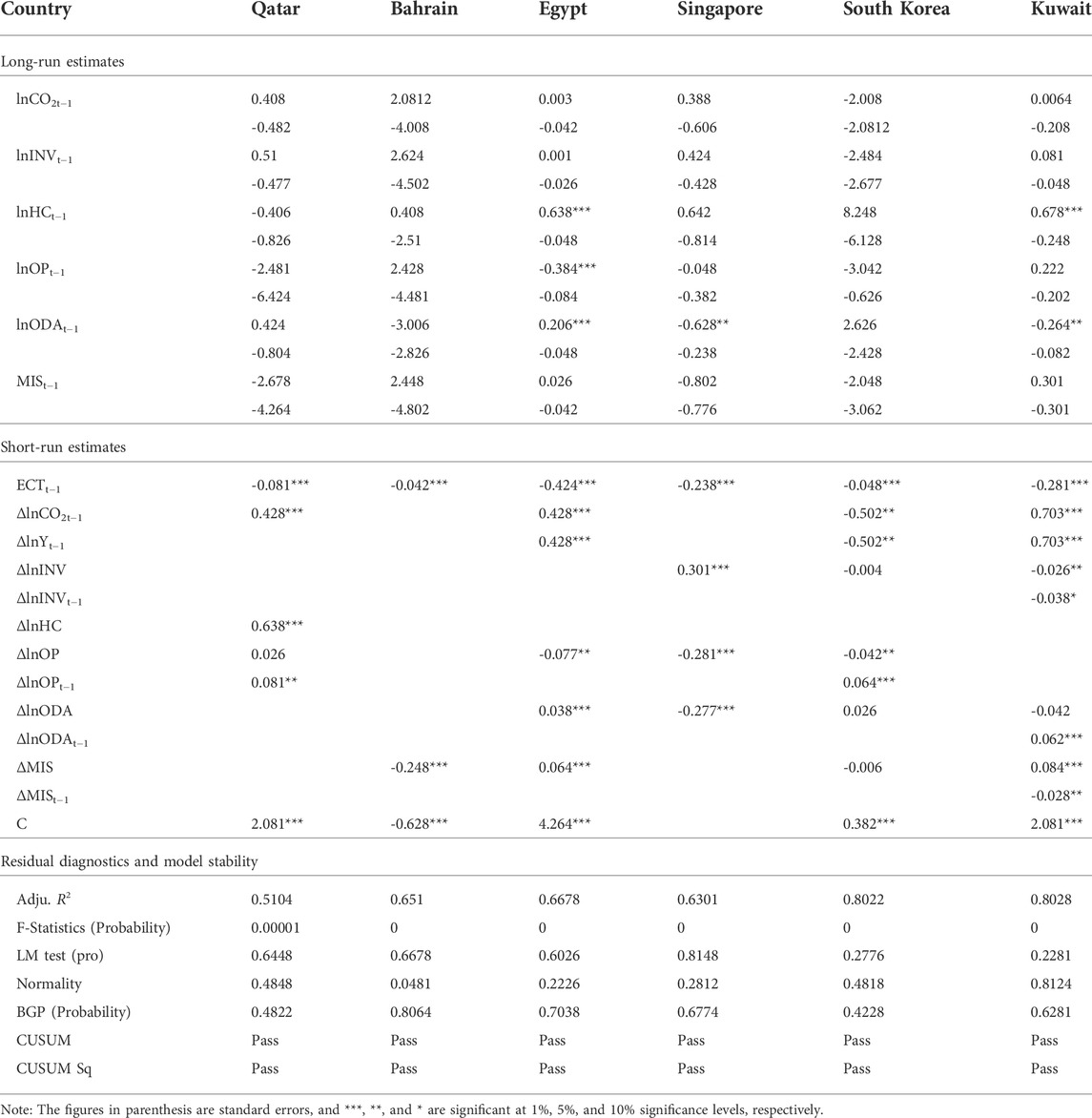

Table 10 displays the results of the Bound tests conducted on each of the sample LDCs. Except for Burundi, all countries’ real GDP per capita and regressors show a long-run correlation based on the critical values of Pesaran et al. (2001) F-test statistic. Using the constrained ARDL model, the Bound test findings are confirmed by negative and statistically significant error correction coefficients for all countries, including Qatar, presented in Table 11. Therefore, a general estimation of the ARDL model is possible for all sample LDCs to assess the long and short-run consequences of RER misalignment on financial growth.

TABLE 10. Bound testing results for the growth model.

TABLE 11. Coefficients of ARDL estimation for the growth model.

The ARDL-bounds testing results often support the PMG results. Table 11 shows the outcomes of the estimations that the long-run growth of Egypt and Kuwait is positively impacted by net foreign assets development and CO2 emissions. Egypt’s comparatively stable internal macroeconomic state may be the reason for its good impact on the growth of South Korea and Kuwait, despite the negative and significant impact of government development aid on CO2 emissions control. While trade openness hurts Egypt’s economy, the effect is negligible compared to other countries and affects CO2 emissions. Overall, the impact of misalignment is statistically negligible on CO2 emissions. LDCs’ repeated devaluations in response to their inflationary economies may blame them for their unstable exchange rate policies and CO2 emissions.

To put it another way, the undervaluation of the RER benefits Egypt’s economy in the near run. At the same time, overvaluation harms the economies of Bahrain and Kuwait and impacts the CO2 emissions, and at the very least, this lends credence to Rodrik’s (2008) argument. Investing in real estate and developing net foreign assets favor and significantly impact CO2 emissions in Singapore and Qatar, respectively. Official aid has a significant and positive impact on CO2 emissions in Egypt and Kuwait growth, but a significant and negative impact on CO2 emissions in Singapore growth. Egypt and Kuwait’s growth has been negatively impacted by opening their economies to international trade and increased CO2 emissions.

LDC economies might benefit from increased real investment and net foreign assets development, but this could be offset by a drop-in growth if RER misalignment, trade liberalization, and government development aid increase CO2 emissions. Currency misalignment has been shown to hurt financial growth through the ARDL technique (Mamun et al., 2020). With an overvalued RER, LDCs’ external competitiveness and financial performance might be improved by effective exchange rate management and consistent macroeconomic policy implementation that impact CO2 emissions. Equilibrium Real Exchange Rate (ERER), which was initially proposed, uses a “model-based approach” (Elbadawi, 1994). LDCs, on the other hand, remained the primary recipients of official development aid, increasing the CO2 emissions in developed countries, which necessitates a stable macroeconomic policy environment and robust legal frameworks in the receiving states. Aid’s influence on growth would be diminished in countries with overvalued or uncompetitive currencies, and trade openness would lead to an increase in imports while export responses in CO2 emissions would be lower, resulting in a balance of payments challenges. FDI, capital inputs, products, and services move to host countries or areas due to international trade openness, increasing CO2 emissions. Academics and scholars have debated and verified the link between trade opening and financial development (Pigka-Balanika, 2013). According to Chen and Gupta (2006), international trade leads to knowledge spillovers, higher productivity, and better net foreign assets impact on CO2 emissions because of the notion that economies may develop indefinitely due to increasing returns to scale. Asian countries’ LDCs may be negatively impacted by this shift, as they rely heavily on exports of essential agricultural commodities and behind-the-border impediments such as poor trade logistics performance and weak customs administration. If a country’s external industry is well-diversified and exports more high-value-added items, trade liberalization might favor CO2 emissions in countries.

The research looked at the influence of the real exchange rate misalignment on Asian countries’ LDCs’ financial development. The ARDL bounds testing results often support the panel estimate results. Asian LDCs’ continuing foreign currency shortages, persistent current account and fiscal deficits, growing external debt payment load, excessive inflation, and expanding saving gap, remained significant policy issues of CO2 emissions growth. If the relative productivity and trade openness grow, it also increases the exchange rate; except for Egypt, all LDCs currencies are overpriced throughout the research period. According to the panel’s estimates, the long-run financial growth of LDCs would be enhanced by a rise in real investment and net foreign assets. At the same time, it would be harmed by increased openness, net foreign assistance inflows, and currency misalignment. The RER is expected to rise if the country’s trade and net foreign asset positions improve, while it is expected to fall if the country’s trade openness and money supply increase. Overvaluation harms Bahrain’s financial growth. While undervaluation helps Egypt, currency misalignment does not affect financial growth in any LDCs over the long run. As a result of the RER misalignment, the financial growth of LDCs might be negatively impacted by CO2 emissions growth both in the short and long run. These evaluations show that if fixed capital creation and human development are increased, but trade openness and official assistance inflows are increased to a greater extent, financial growth may improve but may drop, which can help CO2 emissions growth. The exchange rate policy’s long-run viability rests on its capacity to respond to financial shocks promptly and on its ability to maintain a stable financial and political system that helps to reduce CO2 emissions in the future. In the medium run, CO2 emissions growth due to more real investment, net foreign assets, and official assistance inflows would enhance financial growth in Qatar, Bahrain, Singapore, and South Korea. In contrast, trade openness would slow it down in Egypt and Kuwait. As a result, to fix the ongoing misalignment and reduce its negative impact on financial growth, the currencies of LDCs often require the implementation of an appropriate exchange rate regime commensurate with macroeconomic policy.

The exchange rate is still a vital policy instrument for open economies because of the high financial cost and significant welfare losses from improper management raise CO2 emissions. Increasing the cost of importing raw materials and capital goods for developing businesses and infrastructure projects generates CO2 emissions in Asian countries. So, it is vital to limit imports because it would place a tremendous load on the local economy. As a result, to address the chronic overvaluation of the currency and the associated macroeconomic instability, additional policies and regulatory frameworks are necessary.

The original contributions presented in the study are included in the article/supplementary Materials, further inquiries can be directed to the corresponding author.

LX and MA directed the project. LW, MMA, LX and MA perfomed the experiments. MA and MMA analyzed the spectra and made the simulations; AK developed the theoretical framework. AK, LX and MA wrote the article. MA, LW and MMA performed the measurements. AK and MMA were involved in planning and supervised the work. LX and MA processed the experimental data, performed the analysis, drafted the manuscript, and designed the figures. MA performed the table 5 calculations. AK manufactured the samples and characterized them with environmental data analysis. AK also performed the environmental data characterization. MMA aided in interpreting the results and worked on the manuscript. All authors discussed the results and commented on the manuscript.

The author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

PMG, Pooled Mean Group; LDCs, Least Developed Countries; FEER, Fundamental Equilibrium Exchange Rate; DEER, Desired Equilibrium Exchange Rate; BEER, Behavioral Equilibrium Exchange Rate; PEER, Permanent Equilibrium Exchange Rate; MATRIX, Natural Real Exchange Rate; ARDL, Autoregressive Distributed Lag; RER, Respiratory Exchange Ratio; MIS, Misalignment; DOLS, Dynamic ordinary least square model; NFA, Net Foreign Asset; PD, Productivity difference; OP, Trade openness; BM, Broad money supply; TOT, Total Cost of Ownership; NPV, Present Net Value.

AfDB (2020). “Developing Africa's workforce in the future,” in Asian financial outlook 2020. Asian Development Bank.

Aguirre, Á., and Calderon, C. (2006). Accurate exchange rate misalignments and financial performance, 315. Working Paper of the Central Bank of Chile.

Ahmad, M., Jabeen, G., Shah, S. A. A., Rehman, A., Ahmad, F., and Işik, C. (2022). Assessing long-and short-run dynamic interplay among balance of trade, aggregate economic output, real exchange rate, and CO2 emissions in Pakistan. Environ. Dev. Sustain. 24 (5), 7283–7323. doi:10.1007/s10668-021-01747-9

Ahmed, K., Shahbaz, M., Qasim, A., and Long, W. (2015). The linkages between deforestation, energy and growth for environmental degradation in Pakistan. Ecol. Indic. 49, 95–103. doi:10.1016/j.ecolind.2014.09.040

Ajaz, A., Shenbei, Z., and Sarfraz, M. (2020). Delineating the influence of boardroom gender diversity on corporate social responsibility, financial performance, and reputation. Log. forum 16 (1), 61–74. doi:10.17270/J.LOG.2019.376

Alshubiri, F., and Elheddad, M. (2019). Foreign finance, economic growth and CO2 emissions Nexus in OECD countries. Int. J. Clim. Chang. Strateg. Manag. 12 (2), 161–181. doi:10.1108/ijccsm-12-2018-0082

Ambaw, D., Pundit, M., Ramayandi, A., and Sim, N. (2022). Real exchange rate misalignment and business cycle fluctuations in Asia and the Pacific, 651. Asian Development Bank Economics Working Paper Series.

Appiah, M., Gyamfi, B. A., Adebayo, T. S., and Bekun, F. V. (2022a). Do financial development, foreign direct investment, and economic growth enhance industrial development? Fresh evidence from sub-sahara african countries. Port. Econ. J., 1–25. doi:10.1007/s10258-022-00207-0

Appiah, M., Karim, S., Naeem, M. A., and Lucey, B. M. (2022b). Do institutional affiliation affect the renewable energy-growth nexus in the Sub-Saharan Africa: Evidence from a multi-quantitative approach. Renew. Energy 191, 785–795. doi:10.1016/j.renene.2022.04.045

Appiah, M., Li, F., and Frowne, D. I. (2020). Financial development, institutional quality and economic growth: Evidence from ECOWAS countries. Organ. Mark. Emerg. Econ. 11 (1), 6–17. doi:10.15388/omee.2020.11.20

Appiah, M., Li, F., and Korankye, B. (2021). Modeling the linkages among CO2 emission, energy consumption, and industrialization in sub-Saharan African (SSA) countries. Environ. Sci. Pollut. Res. 28 (29), 38506–38521. doi:10.1007/s11356-021-12412-z

Appiah, M., Onifade, S. T., and Gyamfi, B. A. (2022c). Building critical infrastructures: Evaluating the roles of governance and institutions in infrastructural developments in sub-sahara african countries. Eval. Rev. 46, 391–415. doi:10.1177/0193841x221100370

Ayeche, M. B., Barhoumi, M., and Hammas, M. A. (2016). Causal linkage between financial growth, financial development, trade openness and CO2 emissions in European Countries. Am. J. Environ. Eng. 6 (4), 110–122.

Baffes, J., O'Connell, S. A., and Elbadawi, I. (1999). Single-equation estimation of the equilibrium real exchange rate.

Bahizire, G. M., Fanglin, L., Appiah, M., and Xicang, Z. (2022). Research on the advance role of institutional quality on achieving environmental efficiency in Sub Sahara Africa. Front. Environ. Sci. 10:1-11. doi:10.3389/fenvs.2022.845433

Bayoumi, T., Clark, P., Symansky, S., and Taylor, M. (1994). “The robustness of equilibrium exchange rate calculations to alternative assumptions and methodologies,” in Estimating equilibrium exchange rates. Editor J. Williamson (Institute for International Financials).

Behera, S. R., and Dash, D. P. (2017). The effect of urbanization, energy consumption, and foreign direct investment on the carbon dioxide emission in the SSEA (South and southeast Asian) region. Renew. Sustain. Energy Rev. 70, 96–106. doi:10.1016/j.rser.2016.11.201

Chang, S.-C. (2015). The effects of trade liberalization on environmental degradation. Qual. Quant. 49 (1), 235–253. doi:10.1007/s11135-013-9984-4

Chen, B., and Jin, Y. (2020). Adjusting productivity measures for CO2 emissions control: Evidence from the provincial thermal power sector in China. Energy Econ. 87, 104707. doi:10.1016/j.eneco.2020.104707

Chen, M. X., and Moore, M. O. (2010). Location decision of heterogeneous multinational firms. J. Int. Econ. 80 (2), 188–199. doi:10.1016/j.jinteco.2009.08.007

Chen, P., and Gupta, R. (2006). An investigation of openness and financial growth using panel estimation”. University of Pretoria. Working Paper No. 2006-22.

Clark, M. P. B., and MacDonald, M. R. (1998). Exchange rates and financial fundamentals: A methodological comparison of BEERs and FEERs. International Monetary Fund.

Clark, P. B., and MacDonald, R. (2000). Filtering the BEER: A permanent and transitory decomposition. IMF Working Paper.

Cole, M. A., Elliott, R. J., and Zhang, J. (2011). Growth, foreign direct investment, and the environment: Evidence from Chinese cities. J. Reg. Sci. 51 (1), 121–138. doi:10.1111/j.1467-9787.2010.00674.x

Cottani, J. A., Cavallo, D. F., and Khan, M. S. (1990). Real exchange rate behavior and economic performance in LDCs. Econ. Dev. Cult. Change 39 (1), 61–76. doi:10.1086/451853

Coudert, V., and Couharde, C. (2008). Currency misalignments and exchange rate regimes in emerging and developing countries. CEPII Working Paper (07).

Demena, B. A., and Afesorgbor, S. K. (2020). The effect of FDI on environmental emissions: Evidence from a meta-analysis. Energy Policy 138, 111192. doi:10.1016/j.enpol.2019.111192

Dou, Y., Zhao, J., Malik, M. N., and Dong, K. (2021). Assessing the impact of trade openness on CO2 emissions: Evidence from China-Japan-rok FTA countries. J. Environ. Manag. 296, 113241. doi:10.1016/j.jenvman.2021.113241

Driver, R. L., and Westaway, P. F. (2003). “Concepts of equilibrium exchange rates,” in Exchange rates, capital flows and policy, 98–124.

Elbadawi, I. A. (1994). “Estimating long-run equilibrium real exchange rates,” in Estimating equilibrium exchange rates. Editor J. Williamson (Institute for International Financials).

Elbadawi, I. A., and Soto, R. (1997). Real exchange rates and macroeconomic adjustments in sub-Saharan Africa and other developing countries. J. Asian Econ. 6, 74–120.

Erdogan, A. M. (2014). Bilateral trade and the environment: A general equilibrium model based on new trade theory. Int. Rev. Econ. Finance 34, 52–71. doi:10.1016/j.iref.2014.07.003

Fabbri, P., and Ninni, A. (2014). Environmental problems and development policies for renewable energy in BRIC countries, Federalism.it, rivista di Diritto pubblico italiano, comparato, europeo.

Guzman, M., Ocampo, J. A., and Stiglitz, J. E. (2018). Real exchange rate policies for economic development. World Dev. 110, 51–62. doi:10.1016/j.worlddev.2018.05.017

Han, Z., Li, X., Yan, Z., and Zhong, K. (2022). Interaction and spatial effects of green technology innovation and financial agglomeration: Empirical evidence from China under the goal of" double carbon. Front. Environ. Sci. 10, 1376. doi:10.3389/fenvs.2022.984815

Hao, Y., Wu, Y., Wu, H., and Ren, S. (2020). How do FDI and technical innovation affect environmental quality? Evidence from China. Environ. Sci. Pollut. Res. 27 (8), 7835–7850. doi:10.1007/s11356-019-07411-0

Heidari, A. A., Mirjalili, S., Faris, H., Aljarah, I., Mafarja, M., and Chen, H. (2019). Harris hawks optimization: Algorithm and applications. Future Gener. Comput. Syst. 97, 849–872. doi:10.1016/j.future.2019.02.028

IMF (2021). Annual report on exchange arrangements and exchange restrictions 2020. Washington, DC: International Monetary Fund.

Jafri, R. A., Khan, S., Shah, M. H., and Baig, N. (2018). Total factor of productivity and its components: Evidence from cement-and energy sectors of Pakistan. J. Innovation Sustain. RISUS 9 (1), 55–73. doi:10.24212/2179-3565.2018v9i1p55-73

Jahanger, A., Usman, M., and Ahmad, P. (2022b). A step towards sustainable path: The effect of globalization on China’s carbon productivity from panel threshold approach. Environ. Sci. Pollut. Res. 29 (6), 8353–8368. doi:10.1007/s11356-021-16317-9

Jahanger, A., Usman, M., and Balsalobre-Lorente, D. (2021). “Autocracy, democracy, globalization, and environmental pollution in developing world: Fresh evidence from STIRPAT model,” in J. Public aff., e2753. doi:10.1002/pa.2753

Jahangir, A., Usman, M., Murshed, M., Mahmood, H., and Balsalobre-Lorente, D. (2022a). The linkages between natural resources, net foreign assets, globalization, economic growth, financial development, and ecological footprint: The moderating role of technological innovations. Resour. Policy 76, 102569.

Jiang, T., Yu, Y., Jahanger, A., and Balsalobre-Lorente, D. (2022). Structural emissions reduction of China's power and heating industry under the goal of" double carbon": A perspective from input-output analysis. Sustain. Prod. Consum. 31, 346–356. doi:10.1016/j.spc.2022.03.003

Kamal, M., Usman, M., Jahanger, A., and Balsalobre-Lorente, D. (2021). Revisiting the role of fiscal policy, financial development, and foreign direct investment in reducing environmental pollution during globalization mode: Evidence from linear and nonlinear panel data approaches. Energies 14 (21), 6968. doi:10.3390/en14216968

Karim, S., Appiah, M., Naeem, M. A., Lucey, B. M., and Li, M. (2022). Modelling the role of institutional quality on carbon emissions in Sub-Saharan African countries. Renew. Energy 198, 213–221. doi:10.1016/j.renene.2022.08.074

Ke, J., Jahanger, A., Yang, B., Usman, M., and Ren, F. (2022). Digitalization, financial development, trade, and carbon emissions; implication of pollution haven hypothesis during globalization mode. Front. Environ. Sci. 211. doi:10.3389/fenvs.2022.873880

Keho, Y. (2017). The impact of trade openness on economic growth: The case of Cote d’Ivoire. Cogent Econ. Finance 5 (1), 1332820. doi:10.1080/23322039.2017.1332820

Khan, Y., Hassan, T., Kirikkaleli, D., Xiuqin, Z., and Shukai, C. (2022). The impact of economic policy uncertainty on carbon emissions: Evaluating the role of foreign capital investment and renewable energy in East Asian economies. Environ. Sci. Pollut. Res. 29 (13), 18527–18545. doi:10.1007/s11356-021-17000-9

Le, T. H., Chang, Y., and Park, D. (2016). Trade openness and environmental quality: International evidence. Energy Policy 92, 45–55. doi:10.1016/j.enpol.2016.01.030

Li, S., Yu, Y., Jahanger, A., Usman, M., and Ning, Y. (2022). The impact of green investment, technological innovation, and globalization on CO2 emissions: Evidence from MINT countries. Front. Environ. Sci. 10, 868704. doi:10.3389/fenvs.2022.868704

Liu, X., Wahab, S., Hussain, M., Sun, Y., and Kirikkaleli, D. (2021). China carbon neutrality target: Revisiting FDI-trade-innovation nexus with carbon emissions. J. Environ. Manage. 294, 113043. doi:10.1016/j.jenvman.2021.113043

Malik, M. Y., Latif, K., Khan, Z., Butt, H. D., Hussain, M., and Nadeem, M. A. (2020). Symmetric and asymmetric impact of oil price, FDI and economic growth on carbon emission in Pakistan: Evidence from ARDL and non-linear ARDL approach. Sci. Total Environ. 726, 138421. doi:10.1016/j.scitotenv.2020.138421

Mamun, A. H., Bal, H., and Basher, S. (2020). Does currency misalignment matter for financial growth? Evidence from Turkey. EuroMed J. Bus. 16, 471–486. doi:10.1108/EMJB-08-2019-0101

Mardani, A., Streimikiene, D., Cavallaro, F., Loganathan, N., and Khoshnoudi, M. (2019). Carbon dioxide (CO2) emissions and economic growth: A systematic review of two decades of research from 1995 to 2017. Sci. Total Environ. 649 (1), 31–49. doi:10.1016/j.scitotenv.2018.08.229

Nasir, M., and Ur Rehman, F. (2011). Environmental kuznets curve for carbon emissions in Pakistan: An empirical investigation. Energy Policy 39 (3), 1857–1864. doi:10.1016/j.enpol.2011.01.025

Nguyen, V. C., Vu, D. B., Nguyen, T. H. Y., Pham, C. D., and Huynh, T. N. (2021). Financial growth, financial development, transportation capacity, and environmental degradation: Empirical evidence from vietnam. J. Asian Finance, Financials Bus. 8 (4), 93–104.

Pesaran, M. H., Shin, Y., and Smith, R. P. (1999). Pooled mean group estimation of dynamic heterogeneous panels. J. Am. Stat. Assoc. 94 (446), 621–634. doi:10.1080/01621459.1999.10474156

Pigka-Balanika, V. (2013). The impact of trade openness on financial growth. Evid. Dev. Ctries. Erasmus Sch. Financials 2 (3), 1–32.

Rapetti, M., Skott, P., and Razmi, A. (2012). The real exchange rate and financial growth: Are developing countries different? Int. Rev. Appl. Econ. 26 (6), 735–753. doi:10.1080/02692171.2012.686483

Rodrik, D. (2008). “The real exchange rate and financial growth,” in Brookings papers on financial activity, 2, 365–412.

Salahuddin, M., Alam, K., Ozturk, I., and Sohag, K. (2018). The effects of electricity consumption, economic growth, financial development and foreign direct investment on CO2 emissions in Kuwait. Renew. Sustain. Energy Rev. 81, 2002–2010. doi:10.1016/j.rser.2017.06.009

Shah, M. H., Ullah, I., Salem, S., Ashfaq, S., Rehman, A., Zeeshan, M., et al. (2022). Exchange rate dynamics, energy consumption, and sustainable environment in Pakistan: New evidence from nonlinear ARDL cointegration. Front. Environ. Sci. 9, 814666. doi:10.3389/fenvs.2021.814666

Shah, M. H., Wang, N., Ullah, I., Akbar, A., Khan, K., and Bah, K. (2021). Does environment quality and public spending on the environment promote life expectancy in China? Evidence from a nonlinear autoregressive distributed lag approach. Int. J. Health Plann. Manage. 36 (2), 545–560. doi:10.1002/hpm.3100

Shahbaz, M., Nasreen, S., Ahmed, K., and Hammoudeh, S. (2017). Trade openness–carbon emissions nexus: The importance of turning points of trade openness for country panels. Energy Econ. 61, 221–232. doi:10.1016/j.eneco.2016.11.008

Shahbaz, M., Solarin, S. A., Mahmood, H., and Arouri, M. (2013). Does financial development reduce CO2 emissions in the Malaysian economy? A time-series analysis. Econ. Model. 35, 145–152. doi:10.1016/j.econmod.2013.06.037

Shahid, R., Li, S. J., Yifan, N., and Jian, G. (2022). Pathway to green growth: A panel-ARDL model of environmental upgrading, environmental regulations, and GVC participation for Chinese manufacturing industry. Front. Environ. Sci., 1206. doi:10.3389/fenvs.2022.972412

Ulaşan, B. (2015). Trade openness and economic growth: Panel evidence. Appl. Econ. Lett. 22 (2), 163–167. doi:10.1080/13504851.2014.931914

Usman, M., Balsalobre-Lorente, D., Jahangir, A., and Ahmad, P. (2022b). Pollution concern during globalization mode in financially resource-rich countries: Do financial development, natural resources, and renewable energy consumption matter? Renew. Energy 183, 90–102. doi:10.1016/j.renene.2021.10.067

Usman, M., and Jahanger, A. (2021). Heterogeneous effects of remittances and institutional quality in reducing environmental deficit in the presence of EKC hypothesis: A global study with the application of panel quantile regression. Environ. Sci. Pollut. Res. 28 (28), 37292–37310. doi:10.1007/s11356-021-13216-x

Usman, M., Jahangir, A., Makhdum, M. S. A., Balsalobre-Lorente, D., and Bashir, A. (2022a). How do financial development, energy consumption, natural resources, and globalization affect arctic countries' economic growth and environmental quality? An advanced panel data simulation. Energy 241, 122515. doi:10.1016/j.energy.2021.122515

Wang, B., Dong, X., Qu, Y., Li, Y., Zheng, Y., Xu, Z., et al. (2022). New form of economic development in highly urbanized area and its effect on green development. Front. Environ. Sci. 10, 935496. doi:10.3389/fenvs.2022.935496

Wang, Q., and Zhang, F. (2021). The effects of trade openness on decoupling carbon emissions from economic growth – evidence from 182 countries. J. Clean. Prod. 279, 123838. doi:10.1016/j.jclepro.2020.123838

Wang, Z., Zhu, N., Wang, J., Hu, Y., and Nkana, M. (2022). The impact of environmental taxes on economic benefits and technology innovation input of heavily polluting industries in China. Front. Environ. Sci. 10, 959939. doi:10.3389/fenvs.2022.959939

Williamson, J. (1994). Estimating equilibrium exchange rates. Institute for International Financials.

Yang, B., Jahanger, A., and Khan, M. A. (2020). Does the inflow of remittances and energy consumption increase CO2 emissions in the era of globalization? A global perspective. Air Qual. Atmos. Health 13 (11), 1313–1328. doi:10.1007/s11869-020-00885-9

Yang, B., Jahanger, A., Usman, M., and Khan, M. A. (2021). The dynamic linkage between globalization, financial development, energy utilization, and environmental sustainability in GCC countries. Environ. Sci. Pollut. Res. 28 (13), 16568–16588. doi:10.1007/s11356-020-11576-4

Yang, X., and Shafiq, M. N. (2020). The impact of foreign direct investment, capital formation, inflation, money supply and trade openness on economic growth of asian countries. iRASD J. Eco. 2 (1), 25–34. doi:10.52131/joe.2020.0101.0013

Yu, Y., Onwe, J., Jahanger, A., Adebayo, T. S., Hossain, M. E., and Ali, D. (2022). Linking shadow economy and CO2 emissions in Nigeria: Exploring the role of financial development and stock market performance. Fresh insight from the novel dynamic ARDL simulation and spectral causality approach. Front. Environ. Sci. 10, 983729. doi:10.3389/fenvs.2022.983729

Yuan, W., and Huang, Y. (2022). Impact of foreign direct investment on the carbon dioxide emissions of East asian countries based on a panel ARDL method. Front. Environ. Sci. 10, 937837. doi:10.3389/fenvs.2022.937837

Zhang, C., Liu, H., Bressers, H. T. A., and Buchanan, K. S. (2011). Productivity growth and environmental regulations-accounting for undesirable outputs: Analysis of China’s thirty provincial regions using the malmquist–luenberger index. Ecol. Econ. 70 (12), 2369–2379. doi:10.1016/j.ecolecon.2011.07.019

Keywords: real exchange rate, economic misalignment, financial growth, LDCs technique, asian countries

Citation: Xiao L, Ahmad M, Waseem LA, Ahmad MM and Khan AA (2022) Financial development and real exchange rate misalignments effects on environmental pollution. Front. Environ. Sci. 10:984346. doi: 10.3389/fenvs.2022.984346

Received: 01 July 2022; Accepted: 12 September 2022;

Published: 03 November 2022.

Edited by:

Larisa Ivascu, Politehnica University of Timișoara, RomaniaReviewed by:

Muhammad Haroon Shah, Wuxi University, ChinaCopyright © 2022 Xiao, Ahmad, Waseem, Ahmad and Khan. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Muneeb Ahmad, bXVuZWViMTEyQGdtYWlsLmNvbQ==; Lin Xiao, amVzc2ljYXhsQDEyNi5jb20=

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.