95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 18 October 2022

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.982160

This article is part of the Research TopicESG Investment and Its Societal ImpactsView all 28 articles

Xueping Wang

Xueping Wang Shichao Hu*

Shichao Hu*Finance is a pillar industry of national governance. It also provides a solid guarantee for achieving the official Double Carbon target. The question of how to forefront the role of environmental governance in the reform of fiscal and taxation systems, whilst also motivating enterprises to enhance Environment in Environmental, Social, and Governance (EESG) considerations is worth investigating in depth. This study takes A-share listed companies in China from 2001 to 2020 as examples. The effect of Performance-Based Budgeting (PBB) reform on the EESG of these enterprises is empirically examined through quasi-natural experiments using a multi-time difference-in-difference model. We find that PBB significantly optimizes the EESG of the enterprises. The placebo test, the difference-in-difference method, and a series of other robustness tests all support this conclusion. Furthermore, it is suggested that the environmental governance effect of PBB is more significant in areas with heavy financial pressure and stronger government audit. The environmental governance effect of the PBB reform is significant for enterprises with government contracts, strong green innovation capabilities, or high financing constraints. The mechanism test is performed, and the results suggest that the influence mechanism of this environmental governance role lies in the fact that PBB has improved environmental protection subsidies and enhanced fiscal transparency. Through the economic consequences test, we find that enterprise EESG can bring economic benefits to enterprises, which is reflected in the improvement of enterprise return on total assets, price-to-book ratio, and total patent authorization. This study enriches literature on the economic consequences of PBB, and has significance in deepening current fiscal and tax system reform, vigorously optimizing the major strategy of carbon peak and carbon neutrality.

Beyond meeting their financial objectives, many firms have striven to integrate a wide variety of Environmental, Social, and Governance (ESG) goals into their business models over the past few years (Gillan et al., 2021). ESG is an acronym that dates back to 2004 when a report commissioned by the UN called for “better inclusion of environmental, social and corporate governance (ESG) factors in investment decisions.”1 Analysis by asset manager Pimco suggests that from May 2005 to May 2018 ESG was mentioned in fewer than 1% of earnings calls, while by 2021 it was mentioned in almost a fifth of earnings calls.2 According to Bloomberg, global ESG assets are expected to exceed $53 trillion by 2025, this accounts for approximately over a third of the $140.5 trillion in projected total assets under management.3

With the rising use of ESG, corporate ESG has become an increasingly important topic that has received considerable attention and research effort from academic researchers in a wide variety of disciplines (e.g., finance, economics, accounting, and management). The question of how to motivate and improve corporate ESG performance is a key subject of these studies. Academic researchers have started to explore a wide spectrum of management characteristics-, firm-, market-, as well as country-level determinants of corporate ESG over the past few decades. The first refers to the level of management characteristics, including female directors (Dyck et al., 2022), young CEOs (Borghesi et al., 2014), and overconfident CEOs (McCarthy, Oliver and Song, 2017). The second refers to the firm level, including institutional Investors (Dyck et al., 2019), family businesses (Abeysekera and Fernando, 2020), and state-owned enterprises (Hsu, Liang, and Matos, 2021). The third refers to the market level, including import competition (Xu and Wu, 2021), cross-listing (Boubakri et al., 2016), and banks (Houston and Shan, 2022). The fourth refers to the country level, including economic development (Cai, Pan, and Statman, 2016) and the legal system (Liang and Renneboog, 2017). However, empirical inquiries have received limited attention from the position of government policy.

The fiscal policy implemented by the government is a vital tool for intervening and stimulating the behavior of micro-enterprises. It is also the foundation and an important pillar of national governance. National governance capacity largely originates from budgetary capacity (Allen, 1990). An essential cornerstone of building a modern budget system is to implement performance-based budgeting (PBB), which refers to “the systematic use of performance information to inform budget decisions, either as a direct input to budget allocation decisions or as contextual information to inform budget planning, and to instill greater transparency and accountability throughout the budget process by providing information to legislators and the public on the purposes of spending as well as the results achieved.” 4PBB refers to an elastic concept, including program evaluation, spending reviews, and performance management. It links resources to results through injections of information on performance into the stream of budget work. It also becomes part of a process that facilitates monitoring of social trends and progress, while improving managerial accountability and citizen participation in budget decisions (Schick, 2014).

In the spirit of New Public Management, PBB has attracted the interest of academics and practitioners (Mauro, Cinquini and Grossi, 2017). There is a rich body of academic research on PBB, focusing on the connotation, realization path, factors, and incentive and restraint mechanisms of PBB (Hou et al., 2011; Schick, 2014; Park, 2019; Sung and Sungkyu, 2021). However, scholars have rarely paid attention to the economic consequences of PBB. For instance, countries with a higher share of ministries using performance targets in budget negotiation tend to have lower government debt and higher GDP growth rates (Kwon, 2018). In addition, PBB affects the managerial performance of government officials (Yuhertiana and Fatun, 2020). Budgeting use based on performance in improving the quality of financial reporting of organizations in the Iranian Province of Ardabil takes on a positive and meaningful significance (Shahvalizadeh and Fouman Ajirlou, 2020). However, most of the existing research on the economic consequences of PBB has focused on the government level and few studies have examined it at the micro-enterprise level. Environmental responsibility accounts for a vital part of corporate ESG. In this setting, the question of how PBB shapes enterprise environment in Environmental, Social and Governance (EESG) behavior is further explored in this paper.

China is the research context for this study, first, because it has an ambitious goal to achieve peak carbon by 2030 and carbon neutrality by 2060. Efforts are being made to achieve green government procurement, fiscal policy support, tax incentives for carbon emission reduction, building a carbon emission trading market, and promoting the upgrading of industrial structure to ensure carbon peak and carbon neutrality as scheduled. Second, as the largest developing country, China is still in a stage of economic transformation. Compared with other developed countries, the management behaviors of Chinese companies are more easily affected by government policies. Third, China is currently carrying out a comprehensive reform of budget performance management. In 2003, the Third Plenary Session of the 16th Central Committee of the Communist Party of China proposed the establishment of a budget performance evaluation system, thus starting the pace of China’s budget performance reform. These factors mean that China is an interesting research context for exploring the impact of PBB reform on corporate EESG.

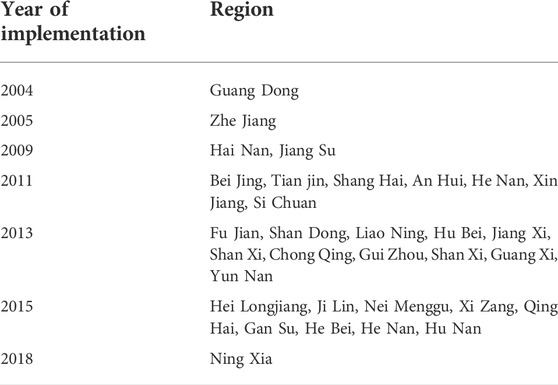

China’s PBB reform can be divided into two stages. The first was the project-based budget performance management stage between 2003 and 2017. The main feature of this stage was that the scope of performance management was limited to general public budgets. The main content of the project, performance evaluation results, and budget arrangements are not organically combined. The second was the comprehensive performance-based budgeting management stage, from 2018 to the present. The main feature of this stage is that the scope of performance management has been expanded to government fund budgets, state-owned capital operating budgets, and social insurance fund budgets; departmental and unit budgets are the main content of performance evaluation, and performance evaluation results are linked to budget arrangement mechanisms. From the perspective of local governments, in 2004 the Guangdong Provincial Government of China implemented the PBB reform, the first example of it being piloted by local government in China. In 2009, the Jiangsu Provincial Department of Finance conducted a performance evaluation of 22 projects at the provincial level with an investment of 14.5 billion yuan. Local governments have successively issued relevant documents for the implementation of PBB in light of the actual conditions of their regions, gradually expanding from the provincial government level to the city and county government level, and from focusing on project expenditure to gradually transitioning to the budget performance of units and departments. Thus, the progress of reforms by China’s local governments in batches and years has provided a good quasi-natural experiment scenario for us to study the economic consequences of PBB.

This study takes China’s A-share listed companies from 2001 to 2020 as a sample and uses a difference-in-difference (DID) identification strategy to analyze the effect of the PBB reform on the enterprise EESG. It found that the PBB reform has significantly improved enterprise EESG. Placebo tests, difference-in-difference-in difference, and a range of other robustness tests were undertaken and support these conclusions. Furthermore, the effect of the PBB reform on the enterprise EESG is more obvious it is found that in areas with high financial pressure and strong government auditing. The environmental governance effect of the PBB reform is more significant for enterprises that have government contracts, have strong green innovation capabilities, and have high financing constraints. The result of the mechanism test reveals the influence mechanism of this environmental governance role (i.e., PBB reform has increased environmental protection subsidies and fiscal transparency). The result of the economic consequences test indicates that the enterprise EESG can bring economic benefits to the company, which is reflected in the improvement of the company’s return on assets, price-to-book ratio, as well as total patent authorization.

Compared with previous studies, the marginal contribution of this study is mainly reflected in the following three aspects. First, in terms of research perspectives, prior literature is more focused on the effect of the PBB reform on economic development, government behavior, and other macro-level factors. In contrast, this study discusses the environmental governance effect of the PBB reform from a micro-perspective, which is helpful for understanding the effect of fiscal and tax system reform on micro-market entities and its mechanism and enriches research on macroeconomic policy and micro-enterprise behavior. Second, at the level of empirical identification, compared with existing research, the PBB reform is adopted as a quasi-natural experiment for empirical tests. There are fewer impurities in the research scenarios, and concerns about endogeneity are reduced to a greater extent, meaning the empirical test evidence is more convincing. Third, at the level of policy enlightenment, this study provides new evidence to evaluate the effect of PBB policy. The findings of this study can provide insights into the policy effects of the PBB reform while providing an important reference for China to deepen fiscal and tax system reform.

The rest of the paper is organized as follows. In Section 2, our hypotheses are developed. In Section 3, the data and sample construction processes are outlined. In Section 4, the relationships between PBB and the enterprise EESG, robustness analyses, heterogeneity test, mechanisms test, and the real consequences of enterprise EESG are examined. In Section 5, we draw our conclusions.

PBB is expected to produce and use performance information to guide the budgeting process and affect the allocation of resources, directly or indirectly, to manage the efficiency and effectiveness of governments and their agencies, facilitate budgetary decision-making and allocation of resources, achieve cost savings, and enhance transparency and accountability (Curristine, 2005). ESG stresses that companies will integrate a wide variety of ESG goals into their business models (Gillan et al., 2021). Building on budget-maximization and principal-agent theory, we analyze the impact and internal mechanism of PBB on the enterprise EESG.

The first impact is that the compensation effect–PBB implemented by the government reduces the information asymmetry between taxpayers and the government, the financial department, and the budget department. PBB widens the spatial of government environmental subsidies and boosts the efficiency and effectiveness of the subsidy program, which ultimately promotes enterprise EESG.

Management needs to balance the cost and income when making an ESG investment (CAI et al., 2016). When ESG outcomes can be perfectly measured, directly subsidizing the ESG outcome is more effective to improve enterprise ESG; and when ESG cannot be reliably measured, regulators can indirectly improve ESG outcomes by subsidizing the financial performance of firms with socially desirable technologies (Bonham and Riggs, 2022). PBB can reduce the information asymmetry between taxpayers and the government, financial departments, and budget departments, effectively reduce agency conflict, and broaden the space for government environmental subsidies.

Relying on principal-agent theory, there are two main types of principal-agent relationships in the field of government budgets. First, taxpayers entrust the government to provide public services by providing tax revenue. Budget-maximization theory argues that bureaucrats do indeed seek to maximize their budgets because increased budgets gave bureaucrats greater access to salary, people, and power (Niskanen, 1971; Niskanen, 1975). In contrast, it is difficult for taxpayers to supervise the use and efficiency of government budgetary money, and there is a severe principal-agent problem between taxpayers and governments. Second, there is a principal-agent relationship between the financial department and the budget department. The finance department is responsible for the disposition and management of budget funds, and the budget department accounts for the use of budget funds to provide public services. Compared with the financial department, the budget department is more aware of the authenticity, effectiveness, and efficiency of the use of its budget funds. Therefore, the budget department has an incentive to pursue the maximization of the department budget with its information superiority.

On the one hand, PBB directly reduces information asymmetries between the tax payer and the government. PBB establishes an information transparency mechanism by publicly disclosing information, such as budget implementation and performance evaluation. The more information the budget discloses, the less the politicians can use fiscal deficits to achieve opportunistic goals (Benito and Bastida, 2009). By easing the information asymmetry, principals will detect malfeasance or failure to deliver public services on the part of agents and will enact punishment, thus deterring the abuse of public power and helping to channel government resources in a fair and efficient manner (Besley, 2006). PBB provides output and outcome data that can be linked with input data in a way that provides transparency as to the efficiency and effectiveness of spending, so that budget officials and parliament can monitor and steer the limited budgetary resources to where they matter most in a given political context (Shaw, 2016), which provides a restrictive tool to contain the maximization of a government’s budget. Thus, PBB can reduce the waste of budget resources, improve the use efficiency of government budget funds, increase the government’s support for the sustainable development of enterprises, and increase environmental subsidies for enterprises, thus stimulating the EESG of enterprises.

On the other hand, PBB directly reduces information asymmetries between the financial department and the budget department and enables inefficient or even invalid use of budget resources to be addressed in good time. Because the budget targets approved for the current year are larger than the actual budget resources needed by the department, at the end of the budget year, to use budget resources in a timely way without reducing the budget targets for the next year, many organizations whose budgets are due at the end of the fiscal year may face an incentive to rush to spend resources on low-quality projects at the end of the year (Liebman and Mahoney, 2017). By providing more information about the production costs of public services to the legislature as budget sponsors, the legislative adoption of PBB can mitigate the information asymmetry between bureaucrats and the legislature, which leads to more effective control of budgetary slack by budget sponsors (Sung and Sungkyu, 2021). After PBB is implemented, the financial department can monitor the budget implementation of a department in actual time and promptly judge the use of funds. In the process of budgetary execution, if a the efficiency of budget item use is relatively low and it is difficult to meet the budget plan goal, then the financial department can reduce or withdraw invalid investments in good time, enabling them to instead allocate precious budget resources to more efficient areas.

After the completion of budget implementation, the financial department must evaluate the performance of funds used by the budget department (e.g., funds relevance, effectiveness, efficiency, and economy). Ex-post evaluations of budget items are conducted on a rolling basis, and performance information is systematically fed back into next year’s budget preparation. The inefficient and ineffective budget items are reduced, efficient and effective budget expenditure items are simultaneously increased, and budget funds can be redirected to support priority goals. PBB is capable of reducing the waste of budget resources, increasing the efficiency of budget fund allocation, and finally expanding the financial space for the government to stimulate the EESG of enterprises.

PBB reform is capable of deepening the connection between the implementation effect of budget projects and the allocation of budget funds, thus increasing the use efficiency of government subsidy projects, achieving a more accurate and scientific compensation effect, and enhancing the EESG performance of enterprises. For parliaments, performance budgeting more clearly expounds on the purposes of spending, and what goods and services will be delivered in exchange for the resources that they have voted on, as well as a means of holding officials to account for the achievement of results. For finance ministries, performance budgeting provides novel types of information that help them make resource allocation decisions based on evidence of what works, plus tools to make line ministries more accountable for the effectiveness and efficiency of spending (Blazely, 2018). China has issued numerous documents and policies over the past few years to enhance accountability for PBB. For instance, in 2018, the Ministry of Finance issued a policy on implementing the opinions of the CPC Central Committee and the State Council on the comprehensive implementation of PBB, which emphasizes that: “In accordance with the principle of rewarding the good and punishing the bad, the government should give priority to stabilizing projects with high performance, and all inefficient and ineffective funds should be reduced or canceled, and funds transferred to vital areas of public financial expenditure for support. Accountability should be held for departments and their responsible persons whose budget execution deviates significantly from performance objectives.” Accordingly, PBB will increase the efficiency and effectiveness of environmental subsidy projects and can give more support to enterprises to invest in ESG, thus improving the EESG performance of enterprises. Meanwhile, the guiding effect of PBB has improved financial transparency, reduced regional corruption, improved the business environment, and reduced the institutional transaction costs of enterprises, thus saving funds for enterprises and enabling them to implement investment in EESG.

Opinions on the comprehensive implementation of PBB issued by the CPC Central Committee and the State Council in September 2018 indicate that it is necessary to vigorously improve the openness and transparency of performance information, take the initiative to report to the People’s Congress at the same level and disclosing these results publicly, meaning they consciously accept the supervision of the People’s Congress and wider society.

PBB is capable of improving the quality of financial reporting of the public sector in terms of comparability, timeliness, and understandability (Shahvalizadeh and Fouman, 2020), increasing fiscal transparency in the government, raising the function of the public sector, fostering greater accountability, and fighting against the corruption (Cai et al., 2016). The higher the levels of regional corruption, the greater the obstacles to enterprise in terms of financing channels, procedures, processes, and others, and the larger the financing cost. Moreover, the rent-seeking behavior of officials brings more rent-seeking costs to enterprises, thus encroaching on the original investment resources in the EESG of enterprises. The improvement of government transparency can optimize the business environment, helping to form a novel “qin qing” government business relationship, meaning enterprises have more energy and resources to engage in production and operation activities. Decker (2020) has suggested that the Army’s PBB programs are beneficial to enhancing quality performance. Facilities participating in PBB programs enhance performance after program implementation, relative to comparison facilities.

PBB is capable of improving the quality of public services, enabling enterprises to enjoy more convenient, fast, and high-quality services, meaning they can respond more directly to market demand, and reduce institutional transaction costs. Thus, PBB saves funds for enterprises, meaning they can carry out ESG activities, as it lowers the cost involved in implementing EESG. Formally, our first hypothesis is presented as follows.

Hypothesis 1:. PBB motivates enterprise EESG.Since it undertook tax reform, China’s central and local governments have seen a rise in wealth and a decline in power. With the gradual implementation of fiscal and tax system reforms (e.g., the reform of the income tax sharing system, the abolition of agricultural tax, and the replacement of business tax with value-added tax), the original financial resources of local governments continue to be squeezed and rigid expenditure (e.g., infrastructure, people’s livelihood security, and education) continue to increase. The recent COVID-19 pandemic has involved repeatedly waves, and the policy of reducing taxes and fees has been vigorously implemented. Under this superposition effect, the local government’s financial pressure is highlighted. With increasing financial pressure, local governments need to consider how to make good use of existing budget resources and increase the efficiency of fiscal expenditure to solve the contradiction between revenue and expenditure. Increasing the efficiency of fiscal expenditure can effectively avoid the distortion of resource allocation by the government’s “grabbing hand.” Higher expenditure efficiency usually causes lower corruption and abuse of funds (Xu et al., 2020). Compared with local governments that face low levels of fiscal austerity, government officials facing a high level of fiscal austerity use more budget performance information (Bjørnholt et al., 2016). Under larger financial pressure, the budget resources become relatively scarce. To ensure public services are at an acceptable level, local governments should tap into potential through budget performance management, thus reducing the unnecessary waste of resources, promoting PBB, and the corresponding reform may more significantly affect the enterprise EESG.As the “immune system” of the national governance system, government audit is an important tool for local governments to improve the efficiency of fiscal expenditure (Xu et al., 2020). China’s Budget Law emphasizes that audit departments of governments at and above the county level should supervise budget implementation and final accounts in accordance with the law. Specifically, an audit can play a greater supervisory role in budget implementation, results application, and other links. On the one hand, in the process of budget implementation, the audit department can check the budget implementation status of the budget department or the project at any time, and verify the matching degree with the performance objectives. For budget units and projects with poor performance, a timely request from the financial department to cut or terminate the use of funds to reduce the loss and waste of funds, and play a supervisory role. On the other hand, after the budget, the audit department can reevaluate the budget department or projects; review the authenticity, reliability, and rationality; and audit whether or not assessment indicators are unscientifically set, or if there is poor operability and other problems. At the same time, the audit department can also check whether the budget department prepares the budget for the next year based on the performance evaluation results of the previous year, and whether the results of the budget performance evaluation have been fully utilized. When the audit department is conducting an economic responsibility audit on the head of the budget department, it can reevaluate the performance of the relevant responsible persons; find out their waste of budget funds, fraud, and inadequate performance of budget performance work; and timely hold them accountable. In addition, the audit can also further improve the quality of financial reporting in the public sector, enhance the transparency of the public sector, alleviate the information asymmetry between taxpayers and the government, and improve the public’s trust in the government. In other words, in the areas with a stronger government audit, PBB plays a more significant role in environmental governance. Accordingly, this study proposes the second hypothesis:

Hypothesis 2:. The incentive effect of PBB on the enterprise EESG is more significant in areas with greater financial pressure and stronger government audit.Companies with government contracts are affected by PBBs. On the one hand, government customers can play a supervisory effect to support the development of enterprises and enhance the resources and motivation of enterprises to implement EESG. Compared with ordinary corporate customers, creditors use fewer contracts and performance pricing terms (Cohen et al., 2022). When loans to corporate suppliers with key government customers, because signing with key government customers face low demand uncertainty, which enables companies to generate more revenue from the investments of specific customers, profit margins increase with government customer concentration (Cohen and Li, 2020). Compared with similar enterprises, companies with large government customers have higher capital capitalization, capital spending, and higher bank credit (Goldman, 2020). On the other hand, China’s Government Procurement Law stipulates that government procurement refers to the behavior of state organs at all levels using financial funds to purchase goods, projects, and services. China’s Budget Law stipulates that all government revenue and expenditure should be included in the budget. The government procurement funds belong to the budget expenditure, and the signing, implementation, and settlement of the government contracts will be affected by PBB. Thus, this study concludes that for enterprises with government contracts, PBB will have a greater incentive effect on their EESG.Green innovation of enterprises can reduce environmental pollution and save energy, while achieving environmental and social benefits, and improving the core competitiveness of enterprises (Li and Xiao, 2020). Green innovation can improve the existing production process or develop a new process to reduce harmful substances and the emission of pollutants, and increase the efficiency of energy. Moreover, green innovation emphasizes the integration of environmental protection concepts into the product of raw material selection, design, production, packaging, after-sales service, and other links to improve the performance of environmental and social responsibility (Xie and Zhu, 2021). The level of green innovation represents the environmental governance ability of the enterprises. Accordingly, this study concludes that enterprises with strong green innovation ability pay more attention to environmental protection, and PBB has a greater incentive effect on their EESG.The resource-based view considers that the heterogeneity of resources and capabilities can explain the performance differences between enterprises. In particular, those valuable, rare, and high-cost resources of imitation have the greatest potential to create economic rent, and the resources owned by enterprises are the important factors in their decision-making. Enterprise initiative to implement EESG investment is affected by the enterprise’s inherent resources. In particular, enterprises with a weak resource base have a low willingness to carry out EESG investments. Moreover, the income brought by the enterprise environment in ESG investment has positive externalities, and enterprises cannot enjoy all of the income of their investment. The management will conduct a cost-income analysis of ESG investment (Cai et al., 2016), such that government intervention should stimulate companies to invest in EESG. As a policy tool, PBB increases the efficiency of fiscal expenditure and expands the space for government subsidies and tax incentives. For enterprises with high financing constraints, their internal resources are insufficient to support enterprises to carry out large-scale EESG investments, and they are more dependent on government support. Thus, PBB for enterprises with higher financing constraints has a greater incentive effect on EESG. In brief, our third hypothesis states that:

Hypothesis 3:. For enterprises with strong government contracts, strong green innovation ability, or high financing constraints, the environmental governance effect of PBB is more significant.

In this study, listed non-financial companies in China from 2001 to 2020 were selected as the research samples. The provincial-level data, financial data, and data of the environment in ESG originated from the China Research Data Service platform (CNRDS). In addition, we deleted samples with negative values of assets, cash, MB, and so on, and all continuous variables were winsorized at 1% to reduce the effect of variable outliers in the sample. Accordingly, this study ended up with 40,959 annual company samples.

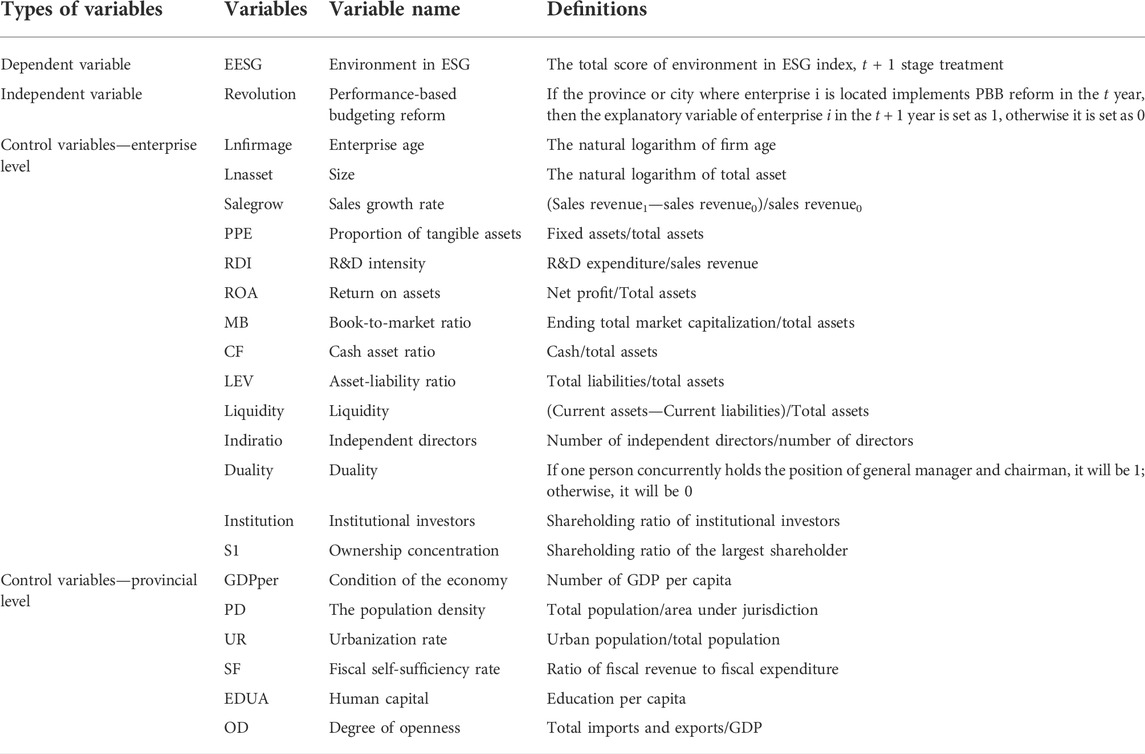

The dependent variable is “Enterprise Environment in ESG,” which is denoted as EESG. This study uses the CNRDS database to get the total score of the EESG index, in which the highest score is 8 and the lowest score is 0. The specific sub-indicators are as follows. First, if the company has developed or applied innovative products, equipment, or technology that are beneficial to the environment, then the value will be 1; otherwise, the value will be 0. Second, if the company has adopted policies, measures, or technologies to reduce emissions of waste gas, waste water, waste residue, and greenhouse gases, then the value will be 1; otherwise, the value will be 0. Third, if the company has used policies and measures of renewable energy or circular economy, then the value will be 1; otherwise, the value will be 0. Fourth, if the company has policies, measures, or technologies to save energy, then the value will be 1; otherwise, the value will be 0. Fifth, if the company has green office policies or measures, then the value will be 1; otherwise, the value will be 0. Sixth, if the company’s environmental management system has passed ISO 14001 certification, then the value will be 1; otherwise, the value will be 0. Seventh, if the company has received environmental recognition or other positive evaluation, then the value will be 1; otherwise, the value will be 0. Finally, if other enterprise environmental advantages are not covered in these indicators, then the value will be 1; otherwise, the value will be 0. Because there is a time lag for enterprises affected by policies, t + 1 stage treatment will be applied to EESG index numbers.

Unlike existing research, this study suggests that the year when the respective region implemented PBB reform is neither the year when each region issued the PBB document nor the pilot year but should be the year of large-scale promotion and implementation, such that the implementation of the reform can have a significant impact on the local government.

This study obtains the actual implementation year through field research, interviews with government officials, and consulting the websites of the Ministry of Finance and the financial departments of local governments. For instance, Beijing issued the Interim Measures for the Management of Performance Evaluation of Budget Expenditure of Municipal Departments of Beijing in 2006. The reform of the government performance budget was piloted in 2002, but it covered the whole process from 2011. Thus, this study takes 2011 as the year for the implementation of the PBB reform in Beijing.

There is a lag in the implementation of the PBB reform. This means that the PBB reform is implemented in the current year, which will have a substantial impact on the enterprise EESG in the next year. For instance, If the province or city where enterprise i is located implements PBB in the t year, then the explanatory variable of enterprise i in the t + 1 year is set to 1, otherwise it is set to 0. The specific implementation year of the respective region is shown in Table 1.

TABLE 1. Year of implementation of PBB reform by region.

Control variables are assigned to enterprise and provincial levels in accordance with existing literature on enterprise ESG. Enterprise-level variables involve enterprise age, size, sales growth rate, the proportion of tangible assets, R&D intensity, return on assets, book-to-market ratio, cash asset ratio, asset-liability ratio, liquidity, independent directors, duality, institutional investors, and ownership concentration. Enterprise Age measures an enterprise’s experience in implementing EESG. According to the theory of enterprise life cycle, enterprise development is similar to the growth curve in biology, which goes through a process from prosperity to decline. In different stages, the economic, market, and technological environment faced by enterprises and the strategies adopted are different to some extent. Size measures the size of an enterprise. Large enterprises have stronger R&D capability, risk resistance ability, and financing ability, which is more conducive to the implementation of EESG. However, a scale that is too large can easily cause bureaucracy and more rigid management, while small enterprises are more flexible. Sales growth rate, return on assets, R&D intensity, and book-to-market ratio reflect the enterprise’s future growth opportunities. Enterprises with more future growth opportunities will have more optimistic development prospects and more opportunities for R&D investment. Investors and creditors may be more optimistic about the company’s expectations, which increases the company’s financing ability. Therefore, the future growth opportunities of enterprises are also an important factor influencing the implementation of EESG. The proportion of tangible assets measures a firm’s borrowing capacity. Compared with intangible capital, physical capital is more often used as collateral for debt financing because the market for physical capital is more transparent and its value can be easily assessed from a creditor’s point of view. Therefore, the proportion of tangible assets can measure the borrowing ability of enterprises, and the financing ability of enterprises is related to the fund source of EESG investment and affects the EESG output of enterprises. The cash asset ratio reflects the impact of cash holdings on EESG. The implementation of EESG investment requires a large amount of capital to promote, and the sustainability of EESG activities depends on the cash flow status of enterprises. The asset-liability ratio reflects the level of debt that a company has taken on and the possibility of further borrowing. When issuing loans, banks need to examine the debt-to-asset ratio of borrowers to assess the future solvency and current loan scale of enterprises. Liquidity also reflects the current solvency of the company. Corporate financing capacity is closely related to EESG. Provincial-level variables, including economic status, population density, urbanization rate, financial self-sufficiency rate, human capital, and degree of opening to the outside world, are selected. The specific meanings are listed in Table 2.

TABLE 2. The definitions of the main variables.

Government PBB reform is gradually implemented in different provinces and cities by year, which is a quasi-natural experiment with multiple shocks. To accurately measure the effect of government PBB reform on the enterprise EESG, this study builds a multi-time difference-in-difference (DID) model (Bertrand and Mullainathan, 2003). The basic model is as follows:

where EESGi,t represents enterprise environment in ESG, and Revolutioni,t represents government performance-based budgeting reform, which is a dummy variable. If the province or city where enterprise i is located implements the government PBB reform in the t year, then the value of enterprise i in the t + 1 year will be 1; otherwise, it will 0. Controli,t represents control variables affecting enterprise EESG; χi, δt, and εi,t represent industry fixed effect, year fixed effect, and random disturbance term, respectively. β is the effect of PBB reform on enterprise EESG. When β is positive, PBB reform improves enterprise EESG.

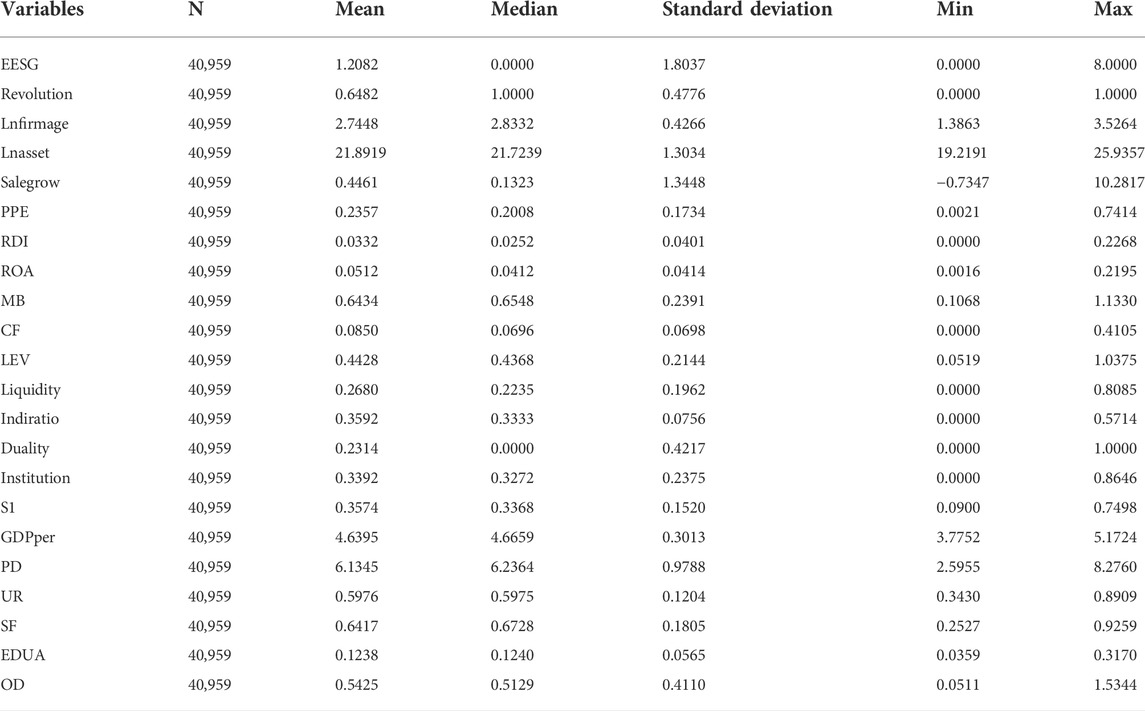

The descriptive statistics are listed in Table 3. The highest EESG score is 8, while the lowest is 0, and the average value is 1.2082. This suggests that the EESG score of the sample enterprises is not high, and there is still considerable room for improvement. Meanwhile, 64.82% of the samples were affected by PBB reform during the sample period. The descriptive statistics of other variables are listed in Table 3.

TABLE 3. Descriptive statistics.

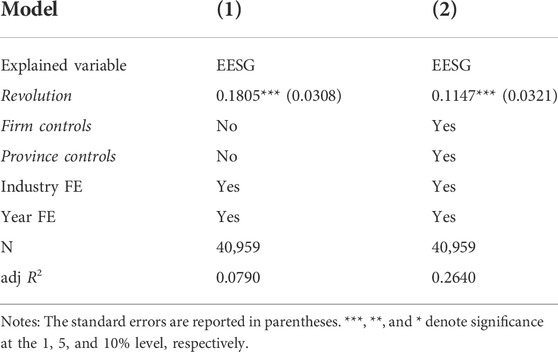

Table 4 provides the baseline results from estimating model (1) with different model specifications. In column 1, we include industry fixed effects and year fixed effects to control for the industry-varying and time-varying characteristics of firms. In column 2, we add both control variables and fixed effects to estimate the effect of PBB reform on the enterprise EESG. In all columns, the coefficient estimates on enterprise EESG are positive and significant at the 1% level. Specifically, the results suggest that the PBB reform significantly improves the enterprise environment in ESG and verifies research Hypothesis 1. We label the more comprehensive specification in column 2 as our baseline model. Our findings support the positive incentive effect of PBB reform, the effect is also consistent with evidence found in prior research on the promotional effect of PBB (Kwon, 2018; Decker, 2020). The possible explanation for this is that PBB widens the spatial of government environmental subsidies, and boosts the efficiency and effectiveness of the subsidy program. Meanwhile, PBB improves financial transparency and reduces the institutional transaction costs of enterprises, ultimately promoting enterprise EESG.

TABLE 4. PBB reform and enterprise EESG.

From a theoretical perspective, the PBB reform is taken as a pure exogenous shock. This study adopts the double difference method to test the effect of the PBB reform on the enterprise EESG, which can avoid endogeneity problems to a large extent. However, to guarantee the robustness of empirical results, we adopt the following endogenous inspection: Dynamic Effect Test and Entropy Balancing Matching + Dual Difference Method Test.

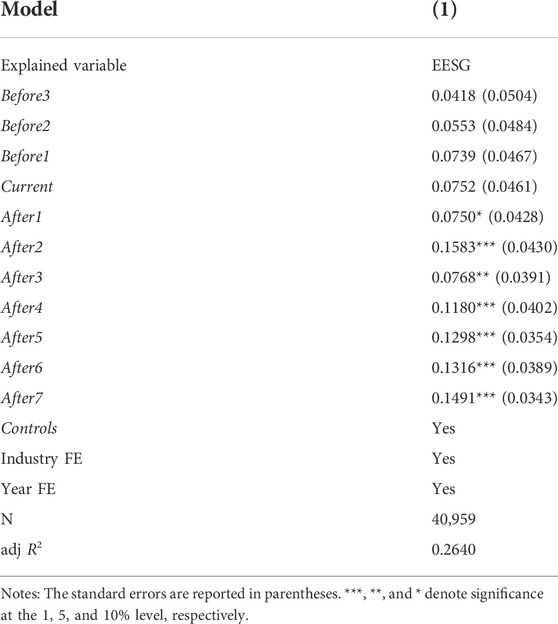

We follow Beck et al. (2010) and examine the dynamics of the relation between PBB reform and enterprise EESG. We do this by including a series of dummy variables in the standard regression to trace out the year-by-year effects.

We consider an 11-year window, spanning from 3 years before PBB reform until 7 years after PBB reform. We include year dummy variables for the 3 years before the reform, the current year, and the 7 years after the reform. Dummy variables are constructed as follows: when the sample time is 3 years before the exogenous shock, we built the Before3 variable with a value of 1 and 0 in other cases; when the sample time is 2 years before the exogenous shock, we built a Before2 variable and assigned 1. The others were treated similarly.

Table 5 reports the estimation results. As depicted in Table 5, the regression coefficients before the reform and the current reform year are not significant. The regression coefficient is significantly positive in the years after the reform, which suggests that the PBB reform can significantly optimize the enterprise EESG.

TABLE 5. Dynamic effect.

Selection bias may exist in the DID method, meaning that there is no guarantee that the experimental group and control group will have the same individual characteristics before the policy implementation and there are large individual differences in samples of this article. Therefore, we further use the entropy balancing matching method to match the enterprise of the experimental and control groups, and use the difference-in-difference method to regression the matched samples. Compared with the PSM matching method that is commonly used in previous literature, the Entropy Balance Matching method shows the following advantages. First, a high degree of covariable balance can be achieved by setting moment conditions (i.e., the treatment group and the control group balance on sample features). Second, valuable information is retained in the pre-processed data. In PSM matching, unmatched samples are deleted, thus causing large information loss. Third, the matching method exhibits a strong versatility. In the absence of pre-processing, researchers can apply any other standard statistical model, thus suggesting a low model dependence. Fourth, it has strong computing performance and fast computing speed (Hainmueller, 2012). Based on these advantages, entropy balance matching is adopted to solve the possible selection bias of samples, and PSM matching is applied to the comparison in the robustness test.

The basic steps of entropy balance matching are presented as follows. First, the moment conditions are set for the feature variables that may be biased, such that the samples of the treatment group and the control group are balanced, and the weight of each sample is obtained. Second, the weight is used for regression analysis. In this study, all of the enterprise-level control variables are selected as characteristic variables for processing. The matching results suggest that the mean, variance, and skewness of the characteristic variables of the enterprises in the treatment group and the control group are significantly similar after the entropy balance matching method is used, and the enterprises in the treatment group and the control group become balance5.

Based on the samples matched by entropy balance, the difference-in-difference method is adopted to empirically test the relationship between the PBB reform and the enterprise EESG. After differences in characteristic variables are excluded, the PBB reform can still promote enterprise EESG, and endogenous problems can be significantly reduced. This suggests that the conclusions of this study are reliable (the empirical test results are presented in the Supplementary Appendix).

To check the robustness of our baseline model, we provide a set of additional analyses using different subsamples, methods, models, and different measures of variables.

The difference-in-difference-in-difference model is employed for empirical estimation to reduce the estimation bias caused by other factors for the grouping of the treatment group and the control group. Enterprises EESG may differ between the two groups because highly polluting enterprises are more likely to attract the attention of government environmental regulation. The difference-in-difference-in-difference method is adopted to test the robustness of the main regression relationship. To be specific, the group for enterprises in high-pollution industries is set to 1; otherwise, it is 0, and the Revolution_Group variable is set. Under the setting of the triple difference in the difference model, the PBB reform will more significantly increase the EESG of high-pollution enterprises, which is consistent with the benchmark regression result and verifies the robustness of the conclusion6.

A placebo test is performed to exclude the possible effect of unobservable factors on the regression results of this study. If the main regression result is caused by unobservable factors, then the regression result will not change after the sample mismatch.

To be specific, this study randomly selects a group of sample enterprises from the sample pool (the number of samples is consistent with the number of sample enterprises affected by PBB reform) as the pseudo-treatment group and the remaining samples as the pseudo-control group.

Model (1) is employed for pseudo-treatment group and pseudo-control group samples and repeated regression 1,000 times. The distribution of estimated coefficients fluctuates significantly around 0. The proportion of significantly positive and significantly negative estimated coefficients is significantly low, and there is no virtual processing effect. As revealed by the results, the research conclusion of this study is still valid after excluding the effect of unobserved factors7.

The following series of robustness tests are performed in this study. First, the EESG metrics we used in the baseline regression may not accurately measure a firm’s EESG. Other ESG Indicators are adopted in the robustness test. At present, Hua Zheng ESG Rating Data is widely used in China’s listed companies. In this evaluation system, a three-level indicator system is built in accordance with the core connotation and development experience of ESG. To be specific, this system comprises three first-level indicators, 14 second-level indicators, 26 third-level indicators, and over 130 underlying data indicators. All Chinese A-share listed companies are assigned a nine-level ESG rating of “AAA-C.” Therefore, the ESG data of Hua Zheng will be used to replace the EESG index in the benchmark regression. The test results show that our research conclusions are not affected by the measures of replacing the explanatory variables.

Second, we use firm fixed effects to control for firm characteristics that do not change over time. Simultaneously, we conduct a test by further including province–year fixed effects to control for any potential province varying shocks. In addition, we change robustness to clustering of industry and year, which would solve the possible bias of standard errors in OLS estimation and reflect the real variability of the estimated coefficients. The test results show that our conclusion still exists.

Third, this study will eliminate interference from concurrent policies. The PBB reform and other fiscal and taxation reforms (e.g., reform to replace business tax with value-added tax) will eliminate double taxation and reduce the corporate tax burden, thus motivating enterprises to perform the environment in ESG. There may be a time overlap between the two policies, such that this study only retains samples of manufacturing enterprises to make an empirical test, to eliminate the possibility of such interference. Furthermore, China revised the Environmental Protection Law in 2014, and the new Environmental Protection Law came into effect in 2015. Therefore, to exclude the interference of environmental protection laws, we exclude the data from 2015 to 2020. It is tested that the conclusion of this paper is still robust after excluding the interference of other policies.

Finally, we change the matching method, and we use the traditional PSM Matched samples to eliminate individual differences in the samples. The test results show that the research conclusions of this paper still exist after changing the matching method.

In conclusion, the robustness test results all support the conclusion that the PBB reform significantly improves the enterprise EESG. This suggests that the conclusion of this study is relatively reliable and the effect of the external environment will not lead to significant changes in the conclusion of this study8.

To further understand the specific effects of the PBB reform, this study analyzes the effect of heterogeneity from the government level and enterprise level.

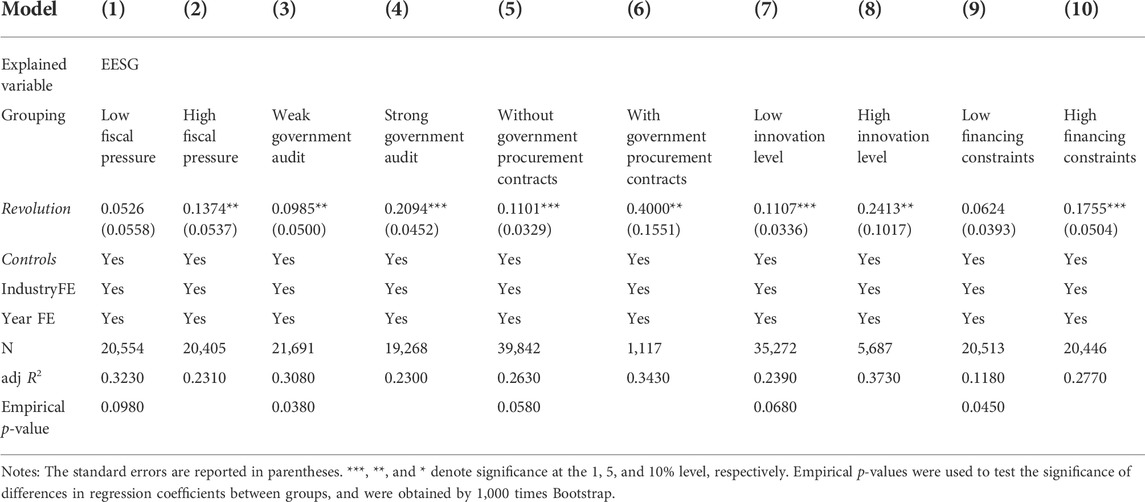

At present, the tide of anti-globalization and the COVID-19 pandemic are overlapping with each other, and geopolitical risks such as the conflict between Russia and Ukraine have slowed the global economic recovery. With the domestic economy trending downward and the implementation of tax and fee reduction policies, the financial pressure on local governments in China has increased sharply. PBB reduces the government expenditure growth rate and financial deficit level (Lee and Wang, 2009). Therefore, we investigate the effect of the PBB reform on the enterprise EESG from the perspective of financial pressure, where fiscal pressure is equal to the difference between local fiscal expenditure minus local fiscal revenue divided by local fiscal revenue. Groups are divided by median into high and low financial stress. The regression results in Table 6 suggest that the regression coefficient of column (1) is not significant, while the regression coefficient of column (2) is significantly positive at the 5% level. The coefficient equality test reveals that the difference achieves statistical significance, with an empirical p-value of 0.098. The regression results show that in the region with great financial pressure, the PBB reform can more significantly motivate the enterprise EESG. This verifies Hypothesis 2. The possible reason for this is that government revenue is limited in financially stressed areas so that the government will more actively promote the reform of PBB, increase the efficiency of fiscal capital stock of spending, and allocate limited resources to areas more conducive to high-quality economic development, thus stimulating the enterprise EESG.

TABLE 6. PBB and enterprise environment in ESG (Heterogeneity Analysis).

As the “immune system” of the national governance system, a government audit is an important tool for local governments to improve the efficiency of fiscal expenditure (Xu et al., 2020). Therefore, we investigate the impact of PBB reform on enterprise EESG from the perspective of a government audit and use the proportion of the fiscal expenditure that should be turned over to the current fiscal expenditure in the audit to indicate the local government audit. According to the median, two groups of high and low audit intensity are divided. The regression results in Table 6 suggest that the regression coefficient of column (3) is 0.0985, which is significant at 5%; and the regression coefficient of column (4) is 0.2094, which is positive at the significance level of 1%. The coefficient equality test reveals that the difference achieves statistical significance, with an empirical p-value of 0.038. The regression results show that in areas with high government audit intensity, PBB reform is more effective in promoting enterprise EESG. This verifies Hypothesis 2. The possible explanation is that the audit can play a more important role in governance in stronger strength of the government audit, and can more effectively supervise the use of unreal and non-compliant financial funds by the government. In addition, the audit can put forward the corresponding budget preparation, implementation, and other links of risk control suggestions. The quality of financial reports of the public sector can be improved, and the information asymmetry between taxpayers and the government can be reduced. Therefore, a government audit can strengthen the environmental governance effect of PBB reform and has a greater incentive effect on enterprise EESG.

Dhaliwal et al. (2016) show that the concentration of corporate customers is positively associated with the cost of equity, while the concentration of government customers is negatively associated. Cohen and Li (2020) document that demand uncertainty decreases with the concentration of government customers but increases with the concentration of corporate customers. Cohen et al. (2022) find that government strictly monitors its corporate suppliers, and it can be a better monitor than a major corporate customer. Meanwhile, government procurement expenditure is an important part of budget expenditure. Therefore, we investigate the impact of PBB reform on enterprise EESG from the perspective of government procurement, and we group enterprises according to whether or not they have government procurement contracts. As can be seen from the regression results in Table 6, the regression coefficient of column (5) is 0.1101, positive and significant at 1%; the regression coefficient of column (6) is 0.4, positive and significant at 5%. The coefficient equality test reveals that the difference achieves statistical significance, with an empirical p-value of 0.058. The regression results show that for enterprises with government procurement contracts, the environmental governance effect of the PBB reform is stronger. Therefore, the empirical test results verify Hypothesis 3. The possible reasons for this are as follows: on the one hand, government customers can exert supervision effect and enhance the resources and motivation of enterprises to implement EESG, while on the other hand, government procurement funds are budgetary expenditures (i.e., the signing, execution, and settlement of government contracts will be directly affected by the PBB reform).

The level of green innovation represents the environmental governance ability of enterprises. We anticipate that the enterprises with strong green innovation ability pay more attention to environmental protection, and PBB has a greater incentive effect on their EESG. Therefore, we investigate the effect of the PBB reform on the enterprise EESG from the perspective of an enterprise’s green innovation level. In accordance with the median, enterprises are divided into two groups of high and low green innovation, and green innovation is measured by green invention patent authorization. The regression results in Table 6 suggest that the regression coefficient of column (7) is 0.1107, which is significant at 1%; and the regression coefficient of column (8) is 0.2413, which is positive at the significance level of 5%. The coefficient equality test reveals that the difference achieves statistical significance, with an empirical p-value of 0.068. The regression results show that for enterprises with higher green innovation levels, the environmental governance effect of budget performance management reform is stronger. This confirms Hypothesis 3. The possible explanation for this is that enterprises with a high level of green innovation have higher investment intention for EESG and a stronger ability to achieve enterprise EESG, and the PBB reform has a more obvious incentive effect on enterprise EESG.

The resource-based view believes that the heterogeneity of resources and capabilities can explain the performance differences between enterprises. The management will conduct a cost-income analysis of ESG investment (Cai et al., 2016). Enterprises implementing EESG investment will be restricted by financing constraints, and we expect that enterprises with lower financing constraints will have better EESG performance. Therefore, we further investigate the effect of the PBB reform on the enterprise EESG from the perspective of enterprise financing constraints. Based on Hadlock and Pierce (2010), the SA index is used to measure financing constraints. SA = 0.043*Size2 − 0.040*Firmage − 0.737*Size, where Size is the enterprise size, measured by the logarithm of the total assets. Firmage indicates when the organization was established, indicating the time it has been operating. Enterprises are divided into two groups with high and low financing constraints in accordance with the median. As can be seen from the regression results in Table 6, the regression coefficient of column (9) is not significant, while the regression coefficient of column (10) is significantly positive at 1%. The coefficient equality test reveals that the difference achieves statistical significance, with an empirical p-value of 0.045. Regression results show that for enterprises with high financing constraints, the environmental governance effect of the PBB reform is stronger. This verifies Hypothesis 3. The possible reason for this is that PBB reform can reduce the local government’s financial pressure; make more room for government subsidies, and tax and fee cuts; and reduce the financing constraints of the enterprise. For enterprises with more limited financial resources, government subsidies and tax and fee cuts will have a greater impact, and therefore these enterprises are more vulnerable to the effect of the PBB reform.

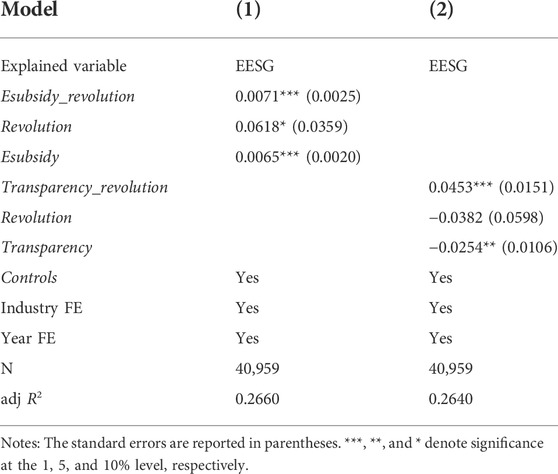

Through this empirical test of the relationship between the PBB reform and the enterprise EESG, we find that the PBB reform can significantly optimize the enterprise EESG. However, the following question is raised: What is the mechanism of the PBB reform affecting enterprise EESG? We will conduct two tests to shed light on which underlying theoretical mechanism best explains our findings. The first is the compensation effect. The PBB reform reduces the information asymmetry between the taxpayer and the government, and between the financial department and the budget department. The allocation of budget resources is more efficient. The government is capable of implementing more environmental subsidies, reducing the cost of EESG implementation, and enhancing the performance of enterprise EESG. The second is the guiding effect. The performance-based budget management reform has increased regional financial transparency, reduced the regional corruption, optimized the business environment, reduced institutional transaction costs for enterprises, and saved funds for the enterprise EESG activities. The moderating effect model is built to accurately measure the mechanism, which is presented as follows:

where Moderatori,t represents moderating factor and Moderator_Revolutioni,t represents interaction item between government PBB reform and moderating factor. When β3 is positive, the positive effect of the PBB reform on the enterprise EESG increases with the increase of the moderator.

Our proposed mechanism assumes that the environmental protection subsidy implemented by local governments provides resources for enterprises to invest in environmental protection and compensates their environmental protection costs. The data of environmental protection subsidy originate from the government subsidy data, which is manually sorted and obtained by the author. The results in Table 7 indicate that the regression coefficient of the interaction item is significant at 1%, which suggests that the positive effect of the PBB reform on the enterprise EESG increases with the increase of environmental subsidies. The empirical results suggest that environmental subsidy is the internal mechanism of budget performance reform to optimize the enterprise EESG.

TABLE 7. Mechanism analysis.

Our proposed mechanism assumes that the PBB reform has increased fiscal transparency, reduced regional corruption, optimized the business environment, and reduced institutional transaction costs for enterprises, thus guiding enterprises to implement more EESG. The data on financial transparency originate from the China Financial Transparency Report released by the Shanghai University of Finance and Economics, in which the weights of the respective item are presented as follows. The weight of the general public budget is 25%; government-managed funds account for 8% of the budget; state capital operations account for 2% of the budget; social security funds account for 19% of the budget; 4% of the budget for special accounts; the weight of assets and liabilities of government departments accounts for 9%; the weight of the department’s budget is 15%; state-owned enterprises account for 15%; and the weight of the respondents’ attitude is 3%. The results in Table 7 indicate that the regression coefficient of the interaction item is significant at 1%, which suggests that the positive effect of the PBB reform on the enterprise EESG increases with the increase in fiscal transparency. The empirical results reveal that fiscal transparency is the internal mechanism of the PBB reform to promote enterprise EESG.

In summary, through the compensation effect, the increase in environmental subsidies caused by PBB reform would alleviate financing constraints faced by enterprises implementing EESG investment. Through the guide effect, PBB reform will promote transparency of local government, and will bring about a series of improvements in the business environment and the quality of public services, thereby reducing the institutional transaction costs of enterprises and guiding enterprises to increase EESG investment.

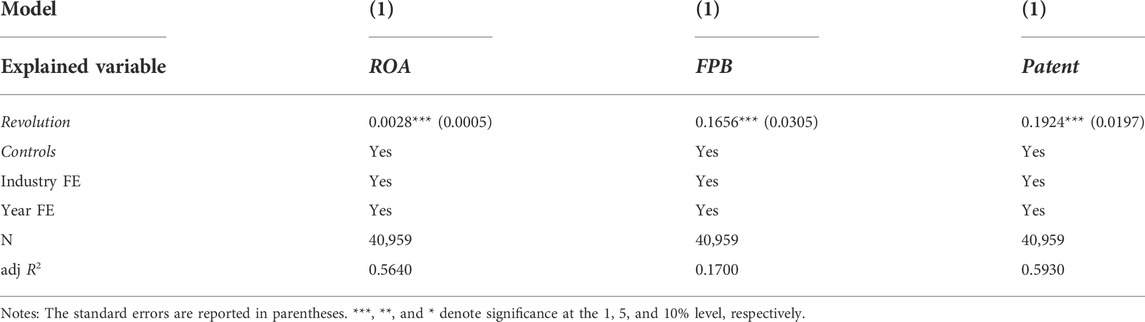

In the preceding sections, this paper has shown that PBB has a positive impact on enterprise EESG. However, a question remains about whether there is an economic benefit arising from PBB pushing enterprises for greater EESG. In this section, we examine what economic consequences PBB brings to an enterprise. We postulate that an enterprise’s improved EESG will enhance their brand and reputation effect, improve the consumer’s satisfaction with their product quality and safety, increase the supplier’s willingness to cooperate with them in the long term, and improve the investor’s and creditor’s confidence in their future performance. We learn from Dai et al. (2021), and we use the return on assets, price-to-book ratio, and the average value of total patent authorization of an enterprise in the next 3 years as indicators to measure the enterprise performance. Compared with the benchmark regression, the control variables of the economic consequences test deleted the control variables at the provincial level and kept the control variables at the enterprise level. As shown in Table 8, the regression results show that the regression coefficients are positive at the significant 1% level. Our findings demonstrate that PBB can further boost the future firm performance after improving firm EESG, which also implies that the implementation of ESG investment can improve firm performance. This is consistent with evidence found in prior research by Zhang and Lucey (2022), who found that ESG performance improves firm performance by alleviating financial constraints.

TABLE 8. Economic consequence test.

The global economy is currently reviving but still faces many uncertain factors as the pandemic persists and geopolitical risks increase. The question of how to shape the behavior of local governments, stimulate the enterprise EESG, and promote high-quality economic development through the reform of the fiscal and taxation system is a topic worth in-depth discussion. Taking China’s A-share listed companies from 2001 to 2020 as a sample, and based on quasi-natural experiments and using a multi-time difference in the difference model, this study empirically examines the effect of performance-based budgeting reform on the enterprise EESG, thus enriching the literature on the effect of macroeconomic policies on the behavior of micro-enterprises, and providing micro-evidence for the evaluation of the effectiveness under the performance-based budgeting management policy in the reform of China’s fiscal and taxation system.

The main conclusions of this study are as follows. First, the performance-based budgeting management reform has significantly optimized the enterprise EESG. This conclusion is still true after using the following endogenous and robustness tests: the dynamic effect test, entropy matching method, difference-in-difference-in-difference method, placebo test, adjustment of measurement indicators, and so on. Second, the effect of the PBB reform on the enterprise EESG is more obvious in places with heavy financial pressure or strong government auditing. For enterprises with government contracts, strong green innovation capabilities, or high financing constraints, the environmental governance effect of the PBB reform is more obvious. Third, the result of the mechanism inspection indicates that the influence mechanism of this environmental governance role is that the PBB reform has improved environmental protection subsidies and improved financial transparency. Finally, through the economic consequences test, we find that the enterprise EESG can bring economic benefits to the enterprise, which is reflected in the improvement of the enterprise’s return on assets, market net market rate, as well as total patent authorization.

The research conclusion of this study reveals that the reform of PBB can affect the government’s behavior and economic development at the macro-level while penetrating the behavior of microeconomic subjects and stimulating the enterprise EESG. The suggestions are presented as follows. First, local governments at all levels should further improve performance-based budgeting management, enhance the transparency of budget performance information, optimize the linkage mechanism between budget performance evaluation results and budget arrangements, increase the efficiency of the utilization of budget funds, and channel resources to support the green and sustainable development of enterprises. Second, enterprises should bear environmental and social responsibility autonomously; integrate the concept of environmental protection from the selection, design, processing, packaging, after-sales service, and other links of products; and increase the green content of products to serve the green development strategy, thus contributing to the realization of the dual carbon goal for China.

We expand the factors at the government level for the research on corporate ESG. In future research, an in-depth study can be conducted at the government level, especially in countries or regions with economies in transition as the research background. In such countries or regions, the level of government intervention in the economy is higher. At the government level, we can attempt to explore the effect of government factors on corporate ESG in terms of industrial policy, fiscal policy, monetary policy, as well as tax policy.

The original contributions presented in the study are included in the article/Supplementary Material. Further inquiries can be directed to the corresponding author.

Conceptualization, SH; investigation, XW; visualization, SH; writing—original draft preparation, SH and XW; project administration, SH and XW; funding acquisition, SH and XW.

This study was supported by the Humanity and Social Science Research Program at Universities in Jiangxi Province of China during 2020 (GL20235).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors, and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenvs.2022.982160/full#supplementary-material

1“Who Cares Wins” https://www.ifc.org.

2https://www.ft.com/content/5ec1dfcf-eea3-42af-aea2-19d739ef8a55

3https://www.gobyinc.com/2022-another-historic-year-for-esg/

4Blazely A. OECD Best Practices for Performance Budgeting [J]. Organisation for Economic Co-operation and Development–2018. https://one.oecd.org/document/GOV/PGC/SBO, 2018, 7.

5The matching results are shown in Supplementary Tables A1, A2 in the Supplementary Appendix.

6The empirical test results are shown in Supplementary Table A3 in the Supplementary Appendix.

7Distribution of estimated coefficients and statistical analysis of regression results are shown in Supplementary Figure A1 and Supplementary Table A4 in the Supplementary Appendix.

8The empirical test results are shown in Supplementary Table A5 in the Supplementary Appendix.

Abeysekera, A. P., and Fernando, C. S. (2020). Corporate social responsibility versus corporate shareholder responsibility: A family firm perspective. J. Corp. Finance 61, 101370. doi:10.1016/j.jcorpfin.2018.05.003

Beck, T., Levine, R., and Levkov, A. (2010). Big bad banks? The winners and losers from bank deregulation in the United States. J. Finance 65 (5), 1637–1667. doi:10.1111/j.1540-6261.2010.01589.x

Benito, B., and Bastida, F. (2009). Budget transparency, fiscal performance, and political turnout: An international approach. Public Adm. Rev. 69 (3), 403–417. doi:10.1111/j.1540-6210.2009.01988.x

Bertrand, M., and Mullainathan, S. (2003). Enjoying the quiet life? Corporate governance and managerial preferences. J. political Econ. 111 (5), 1043–1075. doi:10.1086/376950

Besley, T. (2006). Principled agents?:The political economy of good government. London: Oxford University Press on Demand.

Bjørnholt, B., Bækgaard, M., and Houlberg, K. (2016). Does fiscal austerity affect political decision-makers’ use and perception of performance information? Public Perform. Manag. Rev. 39 (3), 560–580. doi:10.1080/15309576.2015.1137766

Blazely, A. (2018). OECD best Practices for performance budgeting. Paris, France: Working Party of Senior Government Officials, Organisation for Economic Co-operation and Development. Working paper GOV/PGC/SBO (2018) 7 Available at: https://one. oecd. org/document/GOV/PGC/SBO (2018) 7/en/pdf.

Bonham, J., and Riggs-Cragun, A. (2022). An accounting framework for ESG reporting. SSRN. doi:10.2139/ssrn.4016659

Borghesi, R., Houston, J. F., and Naranjo, A. (2014). Corporate socially responsible investments: CEO altruism, reputation, and shareholder interests. J. Corp. Finance 26, 164–181. doi:10.1016/j.jcorpfin.2014.03.008

Boubakri, N., El Ghoul, S., Wang, H., Guedhami, O., and Kwok, C. C. (2016). Cross-listing and corporate social responsibility. J. Corp. Finance 41, 123–138. doi:10.1016/j.jcorpfin.2016.08.008

Cai, Y., Pan, C. H., and Statman, M. (2016). Why do countries matter so much in corporate social performance? J. Corp. Finance 41, 591–609. doi:10.1016/j.jcorpfin.2016.09.004

Chen, C., and Neshkova, M. I. (2020). The effect of fiscal transparency on corruption: A panel cross‐country analysis. Public Adm. 98 (1), 226–243. doi:10.1111/padm.12620

Cohen, D. A., and Li, B. (2020). Customer-base concentration, investment, and profitability: The US government as a major customer. Account. Rev. 95 (1), 101–131. doi:10.2308/accr-52490

Cohen, D., Li, B., Li, N., and Lou, Y. (2022). Major government customers and loan contract terms. Rev. Acc. Stud. 27 (1), 275–312. doi:10.1007/s11142-021-09588-7

Curristine, T. (2005). Government performance: Lessons and challenges. OECD J. Budg. 5 (1), 127–151. doi:10.1787/budget-v5-art6-en

Dai, R., Liang, H., and Ng, L. (2021). Socially responsible corporate customers. J. Financial Econ. 142 (2), 598–626. doi:10.1016/j.jfineco.2020.01.003

Decker, K. L. (2020). Impact of performance-based budgeting on quality outcomes in US military healthcare facilities. Virginia: Virginia Common wealth University. doi:10.25772/YWP2-7Q91

Dhaliwal, D., Judd, J. S., Serfling, M., and Shaikh, S. (2016). Customer concentration risk and the cost of equity capital. J. Account. Econ. 61 (1), 23–48. doi:10.1016/j.jacceco.2015.03.005

Dyck, A., Lins, K. V., Roth, L., and Wagner, H. F. (2019). Do institutional investors drive corporate social responsibility? International evidence. J. financial Econ. 131 (3), 693–714. doi:10.1016/j.jfineco.2018.08.013

Dyck, I. J., Lins, K. V., Roth, L., Towner, M., Wagner, H. F., Karl, V., et al. (2022). Renewable governance: Good for the environment? Renewable Governance: Good for the Environment SSRN. doi:10.2139/ssrn.3224680

Gillan, S. L., Koch, A., and Starks, L. T. (2021). Firms and social responsibility: A review of ESG and csr research in corporate finance. J. Corp. Finance 66, 101889. doi:10.1016/j.jcorpfin.2021.101889

Goldman, J. (2020). Government as customer of last resort: The stabilizing effects of government purchases on firms. Rev. Financ. Stud. 33 (2), 610–643. doi:10.1093/rfs/hhz059

Hadlock, C. J., and Pierce, J. R. (2010). New evidence on measuring financial constraints: Moving beyond the KZ index. Rev. Financ. Stud. 23 (5), 1909–1940. doi:10.1093/rfs/hhq009

Hainmueller, J. (2012). Entropy balancing for causal effects: A multivariate reweighting method to produce balanced samples in observational studies. Polit. Anal. 20 (1), 25–46. doi:10.1093/pan/mpr025

Ho, K. C., Yang, L., and Luo, S. (2022). Information disclosure ratings and continuing overreaction: Evidence from the Chinese capital market. J. Bus. Res. 140, 638–656. doi:10.1016/j.jbusres.2021.11.030

Hou, Y., Lunsford, R. S., Sides, K. C., and Jones, K. A. (2011). State performance‐based budgeting in boom and bust years: An analytical framework and survey of the states. Public Adm. Rev. 71 (3), 370–388. doi:10.1111/j.1540-6210.2011.02357.x

Houston, J. F., and Shan, H. (2022). Corporate ESG profiles and banking relationships. Rev. Financ. Stud. 35 (7), 3373–3417. doi:10.1093/rfs/hhab125

Hsu, P. H., Liang, H., and Matos, P. (2021). Leviathan Inc. and corporate environmental engagement. Manag. Sci. doi:10.1287/mnsc.2021.4064

Kwon, I. (2018). Performance budgeting: Effects on government debt and economic growth. Appl. Econ. Lett. 25 (6), 388–392. doi:10.1080/13504851.2017.1324607

Lee, J. Y. J., and Wang, X. (2009). Assessing the impact of performance‐based budgeting: A comparative analysis across the United States, taiwan, and China. Public Adm. Rev. 69, S60–S66. doi:10.1111/j.1540-6210.2009.02090.x

Li, Q. Y., and Xiao, Z. H. (2020). Heterogeneous environmental regulatory tools and corporate green innovation incentives: Evidence from green patents of listed companies [J]. Econ. Res. (9), 192–208.

Liang, H., and Renneboog, L. (2017). On the foundations of corporate social responsibility. J. Finance 72 (2), 853–910. doi:10.1111/jofi.12487

Liebman, J. B., and Mahoney, N. (2017). Do expiring budgets lead to wasteful year-end spending? Evidence from federal procurement. Am. Econ. Rev. 107 (11), 3510–3549. doi:10.1257/aer.20131296

Mauro, S. G., Cinquini, L., and Grossi, G. (2017). Insights into performance-based budgeting in the public sector: A literature review and a research agenda. Public Manag. Rev. 19 (7), 911–931. doi:10.1080/14719037.2016.1243810

McCarthy, S., Oliver, B., and Song, S. (2017). Corporate social responsibility and CEO confidence. J. Bank. Finance 75, 280–291. doi:10.1016/j.jbankfin.2016.11.024

Niskanen, W. A. (1975). Bureaucrats and politicians. J. law Econ. 18 (3), 617–643. doi:10.1086/466829

Park, J. H. (2019). Does citizen participation matter to performance-based budgeting? Public Perform. Manag. Rev. 42 (2), 280–304. doi:10.1080/15309576.2018.1437050

Park, S. J., and Jang, S. (2021). Asymmetric information and excess budget: The influence of performance-based budgeting on budgetary slack in US states. Int. Rev. Public Adm. 26 (4), 353–372. doi:10.1080/12294659.2022.2027599

Pollitt, C. (2013). The logics of performance management. Evaluation 19 (4), 346–363. doi:10.1177/1356389013505040

Schick, A. (2014). The metamorphoses of performance budgeting. OECD J. Budg. 13 (2), 49–79. doi:10.1787/budget-13-5jz2jw9szgs8

Shahvalizadeh, A., and Fouman Ajirlou, N. (2020). The impact of performance based budgeting on improving the quality of financial reporting (case study: Ardabil province social security). J. Account. Manag. Vis. 3 (31), 137–154.

Shaw, T. (2016). Performance budgeting practices and procedures. OECD J. Budg. 15 (3), 65–136. doi:10.1787/budget-15-5jlz6rhqdvhh

Xie, X. M., and Zhu, Q. W. (2021). How to solve the problem of "harmonious symbiosis" in the practice of enterprise green innovation? J. Manag. World (1), 128–149+9. doi:10.19744/j.cnki.11-1235/f.2021.0009

Xu, C., Pang, Y. M., and Liu, D. (2020). Local fiscal pressure and government expenditure efficiency: A quasi-natural experiment analysis based on income tax sharing reform [J]. Econ. Res. (6), 138–154.

Xu, H., and Wu, Y. (2021). The China trade shock and the ESG performances of US firms. Available at SSRN. doi:10.2139/ssrn.4018683