M. R. Rabbani1†

M. R. Rabbani1†- 1Department of Economics and Finance, College of Business Administration University of Bahrain, Sakhir, Bahrain

- 2Department of Accounting, College of Business, King Faisal University, Al-Ahsa, Saudi Arabia

- 3Applied Science Research Center, Applied Science Private University, Amman, Jordan

- 4Visiting Faculty Member at Department of Accountancy Superior, University of Lahore, Lahore, Pakistan

- 5Associate Professor Department of Business Management College of Business Administration, Kingdom University, Riffa, Bahrain

- 6Department of Commerce, Bahauddin Zakariya University Multan, Multan, Pakistan

This study seeks to find the moderating role of AI in the association between a bank’s innovative financial process and the bank’s market share. The data were analyzed using SPSS and SmartPLS software. The estimations were performed using structural equation modeling estimation techniques such as the measurement model, outer loading, convergent validity, discriminant validity, and SEM estimations. The initial estimations indicated factor as well as construct reliability and validity. The study concluded that an innovative financial process plays a vital role in enhancing the bank’s market share. However, artificial intelligence could not significantly moderate the relationship. The policymakers in the banking industry of Pakistan need to consider the up-gradation in the system of their financial process by innovation and artificial intelligence usage awareness in their existing staff as well their banking customers. Future research may include a similar model for Islamic as well as commercial banks in a comparative model. Additionally, future research may also include more banks as innovative financial institutions to get a greater sample size for a possible influence of artificial intelligence.

1 Introduction

The technological advancement of the banking sector in the modern era is based on the type of services provided as per the requirements and facilitation of customers backed by an innovative process of financial services along with the right use of artificial intelligence (Omoge et al., 2022). The usage of AI in the bank’s financial system has accelerated the financial data in the banking industry providing a broader customer base in the form of digital apps, digital payments, and chat-bot systems (Karim et al., 2021; Rabbani 2022). Pakistan is one of those countries where the system of AI for the banking industry is still under process as compared to developed nations (Hassan et al., 2020; Khan et al., 2021; Rabbani et al., 2022a, b). A company’s market share is indeed the percentage of total income it earns in a given industry (Hussain M. K et al., 2022). Artificial intelligence is regarded as the future of banking as it brings innovative financial solutions to prevent fraudulent financial transactions, brings efficiency, and also improves compliance (Doumpos et al., 2022). It is important to study the role of artificial intelligence in moderating the innovative financial services in the banking sector.

Market share is typically measured by dividing a firm’s revenue for a certain time by some sector’s total sales for the same time (Caminal and Vives, 1996). The market share of such a corporation is a vital indicator of its performance (Tash et al., 2014). A firm’s profitability can be improved by increasing its market share (Akhisar et al., 2015). Offering breakthrough technologies to clients, building customer loyalty, attracting brilliant workers, and gaining a competitive advantage are all ways for an organization to generate its market share (Goyal et al., 2016). Innovation is one strategy for a company to obtain market share (Musiega, 2016). When a company provides new products/services that its competitors do not currently offer, buyers who need them will buy them from another company, even if they previously dealt with a competitor (Nisar, 2017, August 28). The field of financial innovation has emerged as an important domain to consider for increasing the market share of any organization (Gruin and Knaack, 2020; Kaur, 2020). The majority of those individuals become repeat customers, boosting the corporation’s market share and simultaneously diminishing the market share of the company from which they switched (Nazaritehrani and Mashali, 2020).

Shannak (2013) discussed some benefits and drawbacks of using an internet banking facility which includes the fast service for the transfer of funds but includes the risk of sharing information on multiple devices. Today’s world is transforming toward a cashless economy through internet banking facilities as the mode of innovative financial service (Fung et al., 2015). There are many factors responsible for the variation in the market share of a bank such as internet, mobile, telephone, and ATM banking (Saravani et al., 2015). The banking sector around the globe is rapidly changing the types of services offered to its customers by introducing more convenient and cost-effective channels through innovation (Nisar, 2017, August 28). With the addition of innovative financial services, a bank can enhance its share in the market (Ahamed and Mallick, 2019). Those banks which could not compete with the modern era requirements lose their market share as compared to other banks (Nazaritehrani and Mashali, 2020). Pakistan is amongst the developing nations that are facing continuous challenges to adopt modern tools and techniques to upgrade their banking systems as per the changing needs of their customer and to compete for the global banking system around the world (SAMA, 2020, September 11). The innovative finance process not only provides the acceleration for the bank’s market share but also cost efficiency (Khalifaturofi’ah, 2021; Yang, 2021; Zouari-Hadiji, 2021).

To be competitive in the modern world, the banks need to be innovative in terms of their financial process which requires the adoption of innovative financial services with the application of artificial intelligence in the financial industry (Işık et al., 2021; Karim et al., 2021; Rabbani et al., 2022a; Rabbani et al., 2022b). The study adds to the existing strand of literature by being the first study to highlight the role of artificial intelligence in moderating the innovation process in the banking sector. The outcomes of this study are comparable within the banking sector.

The primary goal of this investigation was to determine the direct role of digital financial processes mostly on the market share of the most innovative bank in Pakistan. The secondary area of research interest is to examine the influence of artificial intelligence on Pakistan’s most innovative bank in terms of creative financial procedures for market share. The specific aims of the study are—first, examining the impact of the innovative financial process such as internet, mobile, telephone, ATMs, and POS banking on the market share of the most innovative bank in Pakistan. The second is to analyze the impact of artificial intelligence for accelerating the market share of the most innovative bank in Pakistan. The third is to explore the moderation effect of artificial intelligence concerning the innovative financial processes and the market share of the most innovative bank in Pakistan.

The primary and secondary focus of the present research study is analyzed by considering the following research questions.

RQ1. How does the usage of innovative financial processes such as the internet, mobile phones, ATMs, and POS terminals affect the market share of Pakistan’s most innovative bank?

RQ2. Does artificial intelligence affect the market share of the most innovative bank in Pakistan?

RQ3. How does artificial intelligence play its role in moderating the relationship between innovative financial processes and the market share of the most innovative bank in Pakistan?

Since this helps banks enhance their operations and cost-effectiveness by requiring fewer workers and conventional branches, innovation has been used by the commercial banks to build business intelligence as well as a strategic advantage. Customers may easily execute online transactions mostly as a result of the impact of information systems on financial products, which improves confidence in banking and enables the growth of technology that can first provide a more rapid and efficient operation.

The remaining study is organized as follows. In Section 2, we provide an extensive review of the literature along with the theoretical background. Section 3 describes the methodology used in the study. Section 4 analyzes data and provides the measurement model used in the study, and finally, in Section 5 and Section 6, we conclude and provide the further scope of the study.

2 Literature review

Financial risk is more concerning to the banking industry (Işık et al., 2020; Lutfi et al., 2022). Operational risk and liquidity risk are more concerning for the policymakers and shareholders because this may cause loss of capital (Hussain S et al., 2022). But the use of new technological innovation in the financial industry may cause a decrease in the cost of business (Xiang et al., 2022). Financial services are provided through the telephone; internet cards have impact on the financial preface of the banking industry (Isik et al., 2021). This is the era of the digital economy which affects the overall country’s growth and financial development (Işık et al., 2022). The purpose of this study was to look first at the direct impact of innovative financial processes on increasing the market share of banks in Pakistan. In addition, the study also tries to find the moderation impact of artificial intelligence adaptation for the same sector in Pakistan. For achieving these objectives, the study critically analyzes the historical findings to explore the aforementioned relationships in their default form.

2.1 Internet banking impact on market share

An electronic payment system allows the customer to perform various monetary transactions on the website of the bank (Rajasulochana and Khizerulla, 2022). Internet banking allows the customer to engage with their transaction on the website 24 h and 7 days a week (Chauhan et al., 2022). At home, customers enjoy the same facilities as those at traditional branch banking. Online banking or internet banking reduces the dependency on branch banking which ultimately cuts the cost of banking operation (Akhter et al., 2022). It is a secure, convenient, and easy approach to customer bank accounts on which payments are made through the internet (Cui and Xu, 2022). Internet banking has a positive impact on market share in emerging economy of Syariah Indonesia (Siska, 2022). Pakistan has been using internet banking for over a decade, although evidence indicates that it is increasing the bank’s market share (Raza et al., 2017). Internet banking does have a greater impact on the financial sector’s market share in Nigeria unlike manual banking (Sathiyavany and Shivany, 2018). Similarly, due to the extreme heterogeneity in internet banking with market share, the outcomes of a comprehensive investigation revealed that several variables had the anticipated negative association (Akhisar et al., 2015). Keeping in view the majority of studies indicating the positive link of online banking with the market share of banks, the present research study establishes the following hypotheses to be tested.

2.2 Telephone banking impact on market share

Telephone banking service is provided by the banks which is a financial transaction performed by its customer without visiting a bank branch and without any cash or financial instrument (Payne e al., 2021a). Telephone banking and market share have a positive relationship (Jagathi, 2021). Modern world customers want easy services and on the spot payment without delay and transportation cost (Mahardini et al, 2022). Al Shawi et al. (2022) suggested that the private banking market share is relevant to the mobile banking, telephone banking, and ATM transaction. The main reason is on the spot transaction without delay and waiting for the check clearance. The importance of telephone banking after the COVID-19 situation increased (Hussain I et al., 2022; Irwan et al., 2022). In Kenya, a comparable study discovered that new financial processes such as phone banking used to have a favorable impact on the banking industry’s share of the market (Mwangi, 2014a). Finally, consumers with smartphones can use the phone banking facility to monitor their balances, pay bills, as well as send money via texting, and this type of banking has a solid association with boosting the market share of banks (Raghavan, 2006). As no adverse relationship could be determined in the past literature for telephone banking and its market share, the following hypotheses are being established to test its application in the banking sector of Pakistan.

2.3 Mobile banking impact on market share

Mobile banking means to use any mobile device to carry on the financial transaction (Uddin, 2022). Financial institutions allow their customers to carry forward remote transactions with the help of devices such as mobiles or tablets (Isik et al., 2021; Uddin, 2022). Market share means the percentage of company sales within a given industry (Nguyen et al., 2022). Mobile banking enhances the market share due to easy transaction and on the spot sale (Ma and Zhu, 2022). Mobile banking has positive and significant impact on Islamic banks’ market share (Payne et al., 2021a). Furthermore, a vast majority of banks now provide mobile banking, which boosts bank profits, market share, as well as provide economic advantages (Mullan et al., 2017). In the same way, a study by Muthinja and Chipeta (2018) concluded that technological development in the banking sector in the form of mobile banking can strongly influence the bank’s market share. In contrast, according to Turkish study research, the banks use mobile banking mostly when overall deposits, as well as loans, improve and then their revenue, including interest revenue, and market share fall (Onay and Öztaş, 2018). As per a survey of European nations’ banking sectors, digital technologies and modern mobile banking prospects have a significant impact on the market share of banking institutions (Druhov et al., 2019a). Consequently, the decisive outcomes of an investigation revealed that financial innovations such as financial inclusion, mobile, internet, including ATM banking had a beneficial effect on commercial banking performance, hence, increasing its market share (Ahmed and Wamugo, 2019). The historical literature provides the majority of evidence in support of the optimistic behavior of mobile banking for enhancing the market share, so the present research investigation expects the positive behavior of the same for the market share of the banking sector in Pakistan in the following way.

2.4 Impact of ATM on market share

An ATM is an electronic outlet which allows the customer to perform financial transactions without going to bank branches (Oluwafemi et al., 2022). Simple ATMs are used for cash withdrawals, balance enquiry, and fund transfers, while advanced ATMs are used for cheque deposits and cheque transfers at any time without interference from bank staff (Gautam et al., 2022). The use of ATMs has an effect on market share of the banking industry (Siska, 2022). Mobile banking and ATMs enhance the market share in the Afghan banking sector (Faryal and Tikhomirov, 2022). Furthermore, according to the conclusions of the research, the use of ATMs would have a positive behavioral impact on the banking industry’s market share (Abd El Aziz et al., 2014b). Another survey found that Thailand seems to have a big potential for ATM but also mobile banking services, as well as a significant retail system, indicating the banking industry’s market share increase (Wonglimpiyarat, 2014). Similarly, a Kenyan study looked at financial intermediation as a crucial component of such a banking system and found that ATMs have a major effect on a bank’s market share (Kithinji, 2017). Similarly, the research investigated by Muthinja and Chipeta (2018) showed that ATM and bank market share had an optimistic strong link. Furthermore, a study conducted on Kenyan banks found that banks throughout the vicinity should boost their volume of ATM locations while also expanding their branch offices to significantly improve existing market share (Ahmed and Wamugo, 2019). In the same way, a research investigation by Le and Ngo (2020) discovered that when the volume of ATMs grows, the bank’s share in the market grows as well, coupled with the presence of ATMs at all hours of the day and night in any nearby area. On the contrary, a study found that ATMs are inversely associated with the market share of banks due to a lack of understanding of cashless transactions (Kamboh and Leghari, 2016). Furthermore, another study found that ATMs need not significantly increase a corporate bank’s share in the market (Victor et al., 2017). Keeping in view the direction of a large number of studies as being optimistic in relation to ATM usage and bank’s market share, the present research establishes the following hypotheses for the banking sector of Pakistan.

2.5 POS terminals’ impact on the market share

POS terminal is a device which is used to make payments in a retail environment (Shafei and Sijanivandi, 2022). A portable device is used by the local card holder for the payment of goods and services in the local retail market (Kajdi and Kiss, 2022). POS has a positive effect on market share in Kenya banking context (Mukira et al., 2022). Earlier studies have shown that point of sale is favorably related to financial industry market share as per the conclusive findings of Kamboh and Leghari (2016). Similarly, as per the research investigation of Le and Ngo (2020), growth in the volume of POS terminals boost the bank’s profit including its market share, and yet this element must be regarded vital if the bank’s share in the market in the region is to be increased. As small pieces of evidence supported the usage of POS concerning bank’s market share worldwide and indicated the optimistic relationship between both, the following hypotheses in this regard could be established to facilitate the same domain in the case of the banking sector of Pakistan.

2.6 Artificial intelligence and innovative financial services

The concept of artificial intelligence was introduced in recent years. Especially, in the case of the financial industry, its usage was confirmed in the form of chat-box and virtual assistants in social media, websites, and mobile apps of the banks as evidenced by Kruse et al. (2019). More specifically, the AI application in innovating financial processes such as mobile banking, internet banking, ATMs, and POS has accelerated the banking services with time and cost-saving and has increased the market share of banks (Ayllon, 2020). AI provides an opportunity for banking customers to naturally interact with banks in terms of gesturing, writing, and talking, especially in the case of mobile banking with the inclusion of artificial intelligence technology (Payne et al., 2021b). Similarly, another research investigation in the same domain asserted that artificial intelligence in the form of mobile and digital banking, social media interactions, messenger chat-bots, automated decision-making, and friendly customer journey can transform the traditional financial process into an innovative finance process to accelerate the banking’s market share (Ashta and Herrmann, 2021). As the limited number of studies provides the optimistic moderating relationship of AI usage for accelerating the innovative finance process for gaining the higher market share, the following hypotheses can be established in the case of the banking sector of Pakistan.

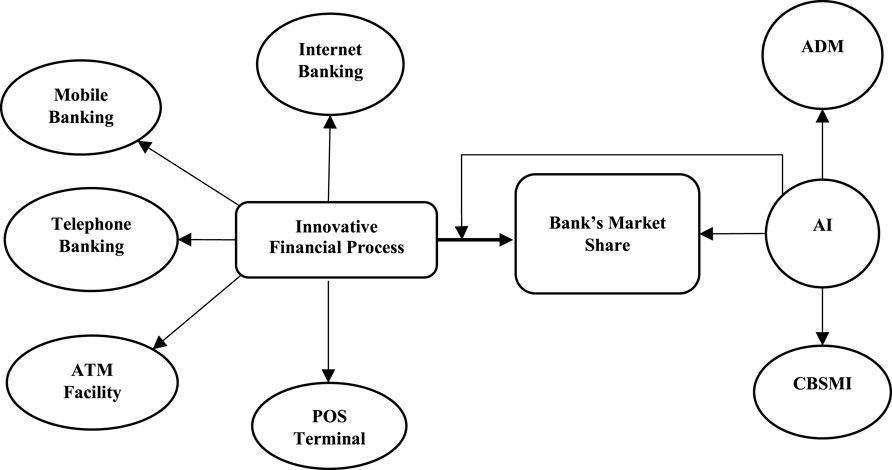

FIGURE 1. Conceptual model source: author’s own architecture.

3 Methodology

The present research study is primarily meant to explore the direct impact of the innovative finance process on the market share of the most innovative bank in Pakistan. In addition, artificial intelligence as moderation is also considered between innovative financial processes and market share of the most innovative bank in Pakistan.

3.1 Population and sampling

As per the recent report of SAMA (2020, September 11), the Silkbank was awarded as the most innovative retail bank in Pakistan. The population of the study consists of 123 branches of the Silkbank located in 39 cities in Pakistan. The unit of analysis comprises each bank branch, while the respondent includes the branch as well as the operation manager. The study uses cluster-based sampling to locate the branches on geographical grounds at first. Then, the final sample is drawn based on a cluster simple random sampling approach as per the suggestions of Acharya et al. (2013).

3.2 Data collection

To collect data, the study uses a self-administrative type of survey questionnaire. The questionnaire consisted of four sections. Section 1 consisted of socio-economic and demographic factors such as gender, age, qualification, experience, the term of employment, and average monthly salary. Section 2 consisted of question statements related to innovative financial processes such as internet banking, mobile banking, telephone banking, ATMs, and point-of-sale terminals. Section 3 consisted of question statements related to the bank’s market share. Finally, Section 4 consisted of question statements related to artificial intelligence applications in the banking sector of the Silkbank. The online questionnaire was divided into two separate booklets. Both separate booklets were targeted from the same respondents at a different point in time for avoiding the issue of common method biases (CMBs). The first booklet contained Section 1 and Section 2 of the questionnaire. The second booklet contained the question statements related to Sections 3 and Section 4. The first booklet was emailed to the targeted respondents in the Silkbank at one point in time. The respondent was allowed to provide his/her valuable responses within a week of receiving the first booklet. After collecting the booklet, the second booklet was sent to the same respondent after a gap of 3–7 days to control the common method biases. The questionnaire in the form of two separate booklets was sent to more than 200 respondents (branch managers and operation managers). Out of these 200 booklets, the researcher received 154 booklets with only 1 + 2 completed in all respects with unbiased responses.

3.3 Operationalization of variables

The present study aimed at investigating the impact of the innovative financial process on the market share of the most innovative banks in Pakistan. Additionally, artificial intelligence was used to analyze the moderation impact concerning the innovative financial processes and the bank’s market share in Pakistan. The dependent variable of the study was market share which was measured by considering 10-item statements as adopted by the study of Nazaritehrani and Mashali (2020). We used five-point type of Likert categories comprising, “1 = Strongly disagree—5 = Strongly agree.” The innovative financial process was used as the independent variable in the form of internet banking (4 items), mobile banking (4 items), telephone banking (3 items), ATM facility (4 items), and point-of-sale terminals (4items), adopted from the study of Raza et al. (2017); Nazaritehrani and Mashali (2020). It was also scaled on five-point type of Likert categories comprising, “1 = Strongly disagree—5 = Strongly agree.” Finally, artificial intelligence was used as the moderating variable with the help of two dimensions such as automated decision making (4 items) and chat-bot and social media interactions (4 items), adopted from the study of Kruse et al. (2019); Ayllon (2020). It was scaled too on five-point type of Likert categories comprising, “1 = Strongly disagree—5 = Strongly agree.”

3.4 Methods of estimation

We applied structural equation modeling techniques to analyze and interpret the primary data collected for the study. For this purpose, SPSS was used for the estimation of descriptive statistics for the socio-economic and demographic factors, while the remaining estimations were executed with the help of SmartPLS in the form of factor analysis, reliability and validity of construct estimation, structural equation modeling, and their estimations, etc.

4 Data analysis and result discussion

The examination of the present research requires investigating the effect of the innovative financial processes on the market share of the most innovative bank in Pakistan. Additionally, artificial intelligence was used to assess the moderation impact between innovative financial processes and the market share of the innovative banks in Pakistan. For achieving these aims and objectives, the study used a questionnaire based on survey research for primary data using the method adopted by Nazaritehrani and Mashali (2020) for measuring the market share of banks, similarly, an innovative financial process was adopted from the study of Raza et al. (2017; Nazaritehrani and Mashali (2020). Finally, the moderating variable; artificial intelligence was adopted from the study of Kruse et al. (2019); Ayllon (2020). All the measures were scaled at a five-point Likert type of scale measure. The data were collected using a cluster-based sampling technique due to the fact of the geographical distribution of banks in different cities. A total number of more than 200 questionnaires were shared while 154 respondents actively filled out the responses. Therefore, the response rate was 77%. For analyzing the research, structural equation modeling using SmartPLS was adopted for evaluating the hypothesis of the study. These estimations include demographic and socio-economic summary using SPSS, measurement model, outer loadings, convergent and discriminant validity as well as the SEM estimates using SmartPLS. The estimations were interpreted under their specific headings as follows.

4.1 Socio-economic and demographic summary

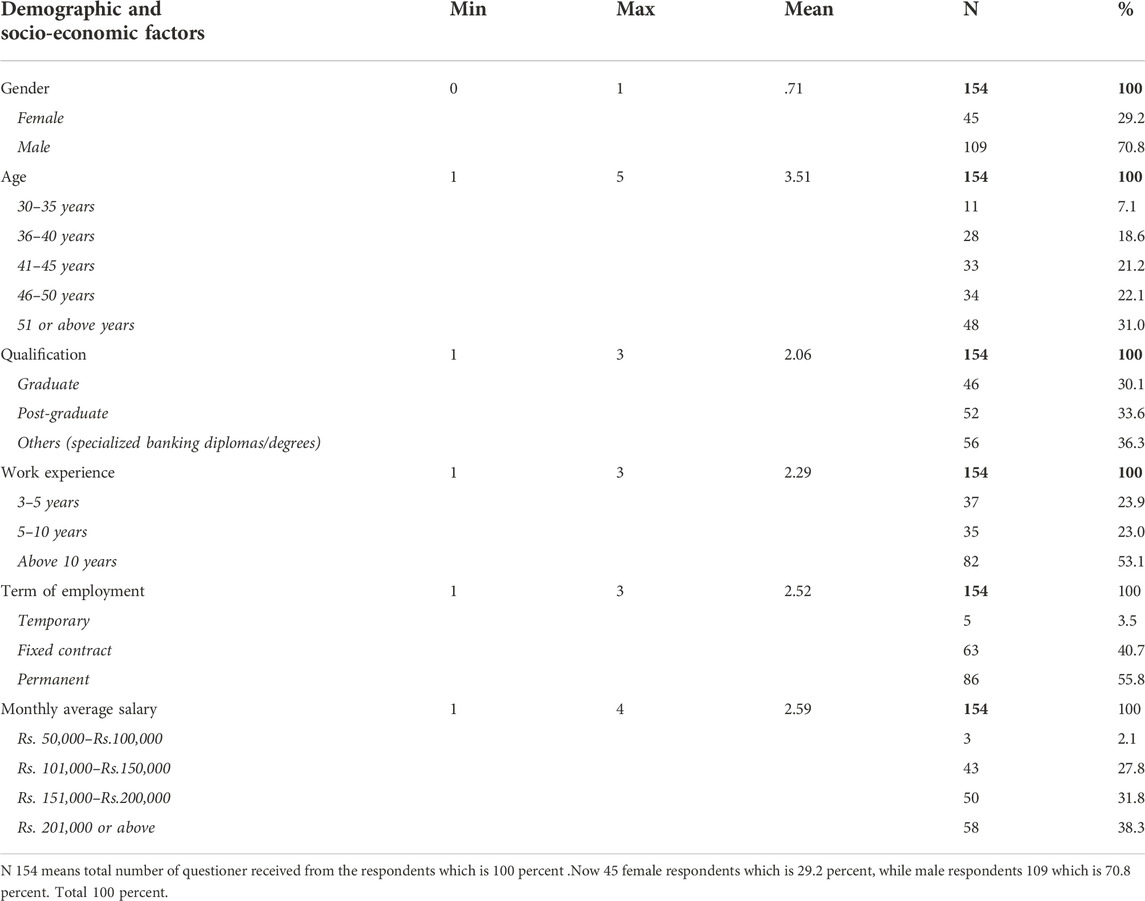

Table 1 reports the socio-economic and demographic details of the respondents in the form of gender, age, qualification, working experience, term of employment, and monthly average salary. The first demographic feature such as gender represents a total number of 154 respondents that comprised 45 females (representing 29.2%) and 109 males (representing 70.8%). As the study was targeted toward the operational and branch managers of the banking sector in Pakistan, especially in Silkbank, therefore, we conclude that this bank is male-dominated. The second demographic feature such as age represents that the majority of the respondents were from the age category of 41 or greater. As the respondent is from the operational and branch managerial levels, so most of the respondents have more experience than others. Similarly, the qualification of the respondents indicates that the majority of the respondents are post-graduate or have other specialized certifications such as IBP qualification/ACCA/CA. Additionally, the working experience of the majority of the respondents is >5 years. However, the term of employment indicates that five of the respondents are holding temporary positions, 63 for fixed contracts, and 86 are holding their position permanently in Silkbank. It infers that the majority of the senior staff is holding either fixed contract or permanent positions at operational or branch banking. Finally, the collected data indicated that the majority of the respondents are earning >151,000 PKR as the average monthly salary in the Silkbank.

TABLE 1. Socio-economic and demographic summary.

It is inferred from the previous table that the majority of the respondents from the Silkbank are male, having the age category of 41 or >, holding a qualification of post-graduate or higher, with an experience of >5 years for working in the banking sector, and they have fixed or permanent employment with a salary package of 151,000 or greater.

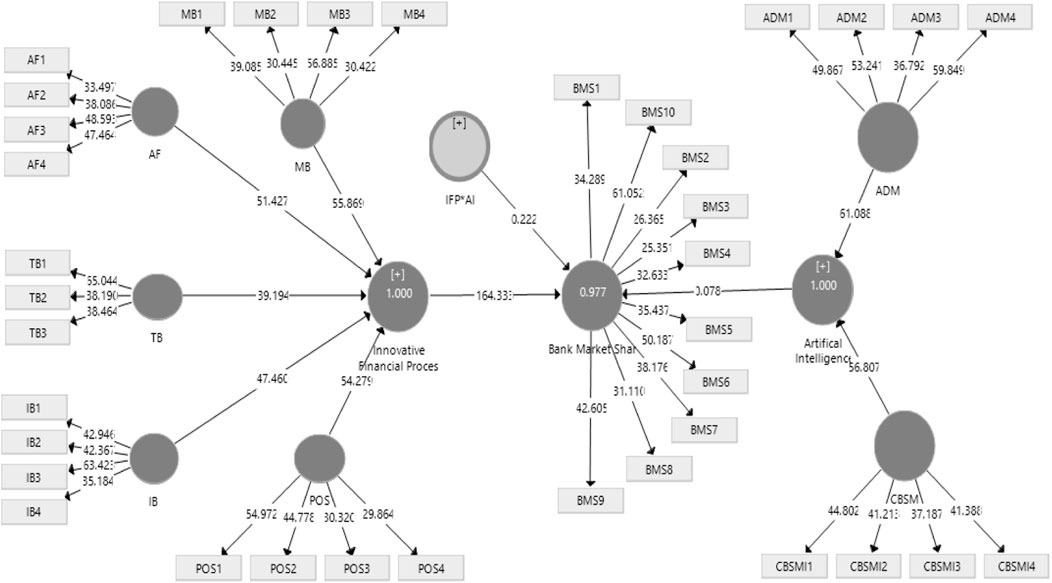

4.2 Measurement model

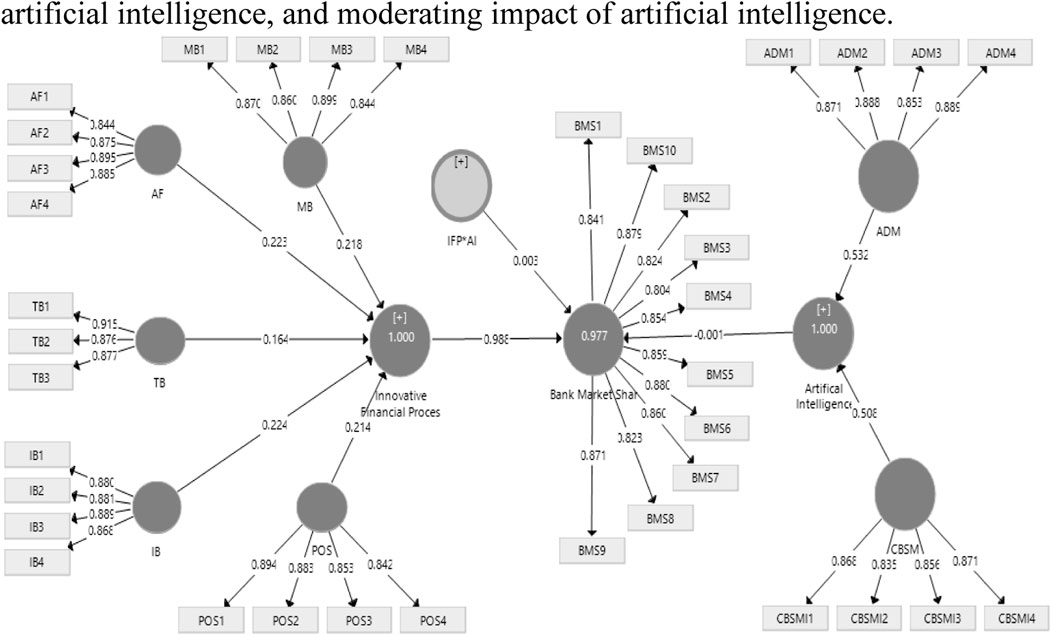

Figure 2 indicates the measurement model which consists of the indicators measuring their latent variables as well as the path coefficients between constructs along with the R-square values. According to Hair Jr, Hult, Ringle, and Sarstedt (2016), the measurement model indicates how the latent variable is measured using related indicators. As per the reliability of the measurement model is concerned, Hair, Anderson, Babin, and Black (2019) stated the rule of thumb reliability indicator in the measurement model with a loading value of 0.708 or greater. By considering this rule of thumb, it is inferred that all the latent variables of this study are valid and dependable. Additionally, Figure 2 indicates that a positive relationship is observed between innovative financial processes and a bank’s market share with a path coefficient value of 0.988. Similarly, there is a negative relationship between artificial intelligence and a bank’s market share which is indicated by a path coefficient value of −0.001. Likewise, a positive relationship was estimated between the moderating impact of artificial intelligence between innovative financial processes and the bank’s market share with a path coefficient of 0.003. Finally, the bank’s market share as the dependent variable of the study indicates an R-square of 0.977 which indicates that approximately 98% of the variance in the bank’s market share is explained by the variance in the innovative financial process, artificial intelligence, and moderating impact of artificial intelligence.

FIGURE 2. Measurement model.

4.3 Outer loadings and convergent validity

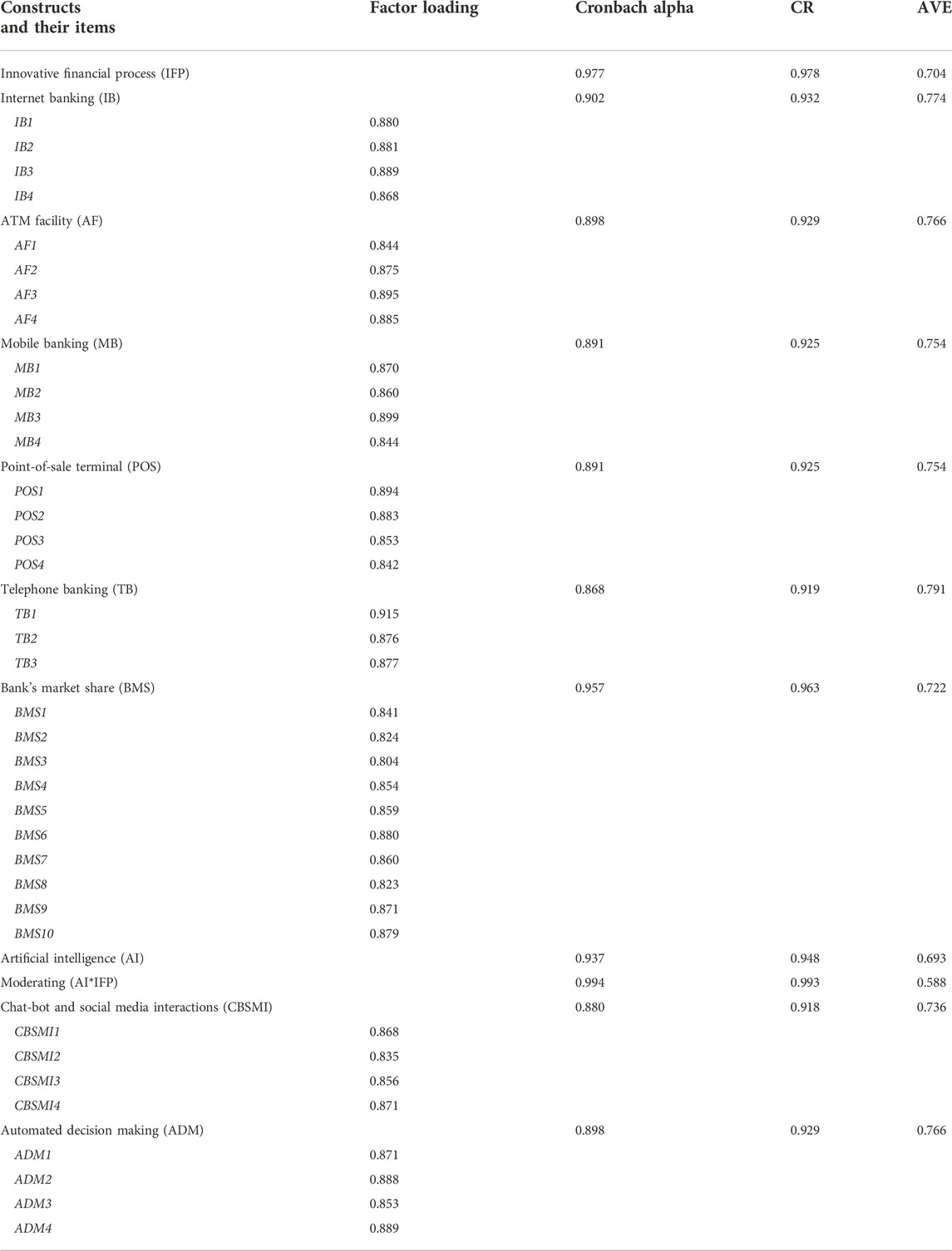

Table 2 indicates the values of the outer loading of factors used for measuring the constructs of the study. It also includes the convergent validity measures such as Cronbach alpha, composite reliability, and average variance extracted from the study. Cronbach alpha and composite reliability indicate the internal validity of the constructs while the average variance extracted indicates the external validity of constructs. As per the reliability of individual factors/indicators is concerned, Hair et al. (2019) stated the rule of thumb for indicator/factor reliability for outer loading values with a value of 0.708 or greater. It is inferred that all the factors measuring their relevant constructs are reliable and valid. Similarly, the rule of thumb for convergent reliability and validity as per the suggestions of Hair et al. (2019) is 0.708 for Cronbach alpha, 0.70 for composite reliability, and 0.50 for average variance extracted. Therefore, it is inferred that the constructs of the study are valid and reliable as per the rule of thumb established by Hair Jr et al. (2016); Hair et al. (2019).

TABLE 2. Outer loadings and convergent validity.

4.4 Discriminant validity

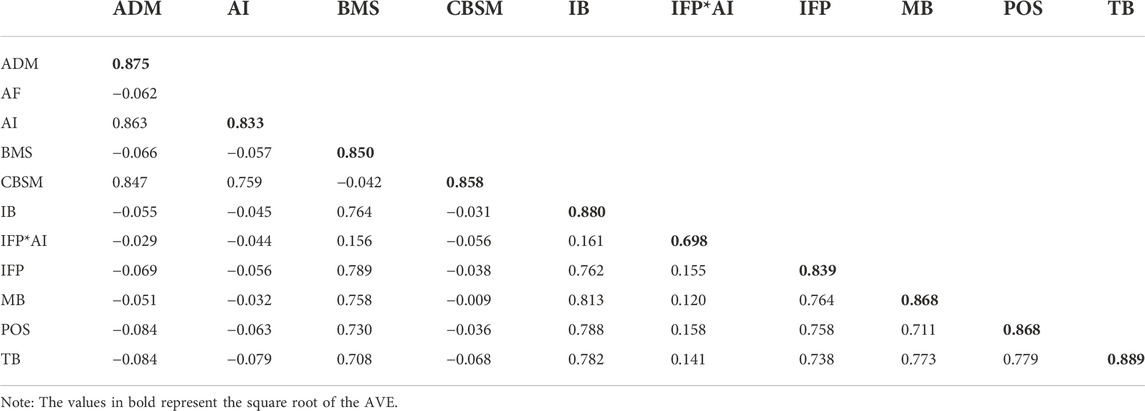

According to the arguments and suggestions of Hair Jr et al. (2016), the discriminant validity of constructs ensures the uniqueness of one construct from all other constructs. Similarly, Hair et al. (2019) stated that discriminant validity is established when the shared variance of one construct is greater than that of all other constructs. The rule of thumb for this criterion is that the square root of AVE for each construct should be > the highest correlation values of other constructs (Hair Jr et al., 2016; Hair et al., 2019). Therefore, using Table 3 values of Fornell and Larcker (1981) for each construct, the discriminant validity is established in this study.

TABLE 3. Discriminant validity of constructs (Fornell–Larcker criterion).

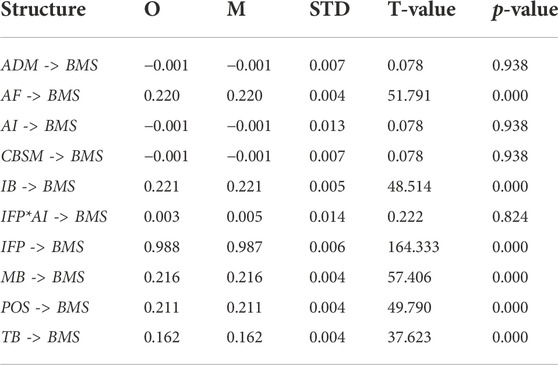

4.5 Structural model

According to Hair Jr et al. (2016), a structural model can be described as a model that indicates the relationship between constructs/latent variables of the study. The rule of thumb for the significance of these relationships is that the t-values must be 1.96 or greater (Hair et al., 2019). Figure 3 indicates that there is a statistically significant link between innovative financial processes and a bank’s market share with a t-value of 164.33 which is higher than the minimum threshold level. However, the link between artificial intelligence and bank’s market share and the link between moderating variable and bank’s market share are insignificant due to t-values of 0.078 and 0.222, respectively.

FIGURE 3. Structural model source: SmartPLS output.

4.6 Estimation of the SEM model

Table 4 indicates the structural equation modeling estimation using the robust technique used in SmartPLS in the same way as the OLS technique in regression. The objective of the study was to determine the direct impact of the innovative financial process as well as the moderation impact of artificial intelligence for the bank’s market share on the most innovative bank in Pakistan, Silkbank. The table reports that innovative financial processes have a positive as well as highly significant impact on the bank’s market share in Pakistan. The path coefficient for this structural link between IFP and BMS is 0.988 with a p-value of 0.000 (p <0.01) which confirms the positive and highly significant link between the variables. The positive and highly significant (strong) link between IFP and BMS accepted the first hypothesis (

TABLE 4. SEM model estimations.

However, the study could not find a strong link between artificial intelligence and a bank’s market share. In fact, a negative and insignificant link was estimated between the variables with the path coefficient value as −0.001 and p-value as 0.938 (p > 0.10). This finding rejects the hypothesis (

The findings of this study inferred that innovative financial processes have a strong and optimistic potential in determining the bank’s market share for innovative banks in Pakistan. However, the banking sector of Pakistan needs to upgrade its innovative banking channels such as mobile banking, telephone banking, internet banking, point-of-sale terminals, and ATMs to align with the modern technology of artificial intelligence and give awareness to their customers regarding its efficient and effective usage to further accelerate their market share.

5 Conclusion

This research study aimed to examine the role of the innovative financial process along with its dimensions; IB, MB, ATM, AF, POS, and TB in explaining the bank’s market share of the most innovative bank, Silkbank. Additionally, artificial intelligence with its dimension; ADM, chat-bot and social media interactions were used as moderating variables of the study. The present study was primarily with quantity data collection procedure using a survey questionnaire. The target population was Silkbank being nominated as the most innovative bank in Pakistan (SAMA, 2020, September 11). A total number of 200 questionnaires were shared with different branches of Silkbank across the country for which 154 respondents completely responded to the questionnaire with two booklets comprising Section 1 and Section 2 were shared at a different point in time with the gap of 3–7 days for each. The study uses cluster-based sampling due to the fact that Silkbank’s branches are located in different cities and towns across Pakistan. The research instrument used in the present study was a survey questionnaire comprising four segments; first for socio-economic and demographic features, second for statements of the innovative finance process, third for the statements related to bank’s market share, and finally, the fourth part related to the statements of artificial intelligence and its dimensions.

For analyzing the present research study, the structural equation modeling technique was used with the help of SmartPLS software due to the fact of the limited sample size of 154. The estimations include the demographic and socio-economic summary using SPSS, measurement model, convergent validity, outer loadings, discriminant validity, and structural equation modeling with the help of SmartPLS software. All the factors in the relevant table estimates indicate that the constructs of the study such as innovative financial process, bank’s market share, and artificial intelligence along with their dimensions are strongly measured by their relevant factors as indicated in Table 2; Figure 2. The threshold level of the factor to be considered for measuring a construct is 0.70, therefore, the factor less than this level is removed from the analysis procedure. Only final values indicating the factor loading for each construct were included and reported in the final estimations. It is inferred that the constructs of the study are valid and reliable as per the rule of thumb for convergent validity as 0.70 for Cronbach alpha, 0.70 for composite reliability, and 0.50 for average variance extract. Therefore, all the constructs are valid and dependable according to this criterion. The rule of thumb for this criterion is that the square root of AVE for each construct should be more than the highest correlation values of other constructs. By meeting this criterion, all the constructs are valid using the Fornell–Larker rule of thumb.

6 Recommendations

The findings of this study inferred that innovative financial processes have a strong and optimistic potential in determining the bank’s market share for innovative banks in Pakistan. However, the banking sector of Pakistan needs to upgrade its innovative banking channels such as mobile banking, telephone banking, internet banking, point-of-sale terminals, ATMs, and digital banking to align with the modern technology of artificial intelligence and give awareness to their customers regarding its efficient and effective usage to further accelerate their market share. The study concluded that an innovative financial process plays a key role in enhancing the bank’s market share. However, there is a lack of awareness regarding the usage of artificial intelligence in the banking sector of Pakistan, which needs to be efficiently upgraded in the running system of innovative financial processes to further accelerate the banking sector in Pakistan. The study implies that the policymakers and decision-makers in the banking industry should focus to consider innovative financial processing channels such as mobile banking, internet banking, point-of-sale, telephone banking, and ATMs to enhance the market share of their respective banks. Additionally, they need to enhance public awareness as well as the training of existing staff to properly utilize the benefits of artificial intelligence integration in their existing financial process. This study adds to the existing literature with the usage of artificial intelligence in the banking sectors and their process of financial transactions, especially in the banking industry of Pakistan. The present study is analyzed on the banking industry with a specific focus on the most innovative financial bank in Pakistan, Silkbank. The findings of the present research are only generalizable in the banking sector only and cannot apply to other industries due to the specific nature of their business. Future research may include the Islamic and traditional bank comparison based on this study. Additionally, more than one bank can be selected to enhance the sample size, which may change the impact of artificial intelligence in future studies.

Data availability statement

The original contributions presented in the study are included in the article/Supplementary Material; further inquiries can be directed to the corresponding author.

Ethics statement

Ethics review and approval/written informed consent were not required as per local legislation and institutional requirements.

Author contributions

Conceptualization; MA, WAW, and AL; Methodology; MA, WAW, and AL; Formal analysis; MA, WAW, and AL; Investigation; MA, WAW, and AL; Writing—original draft preparation MA, WAW, and AL; Writing—review and editing; MRR and NN; Funding; MRR and NN; Project administration; MRR and NN; All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded through the annual funding track by the Deanship of Scientific Research, vice presidency for graduate studies and scientific research, King Faisal University, Saudi Arabia [GRANT876].

Acknowledgments

Methodology: MS, ITW; formal analysis: AB; investigation AB, ITW: writing—original draft preparation: ES; and writing—review and editing: DNSW.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors, and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Abd El Aziz, R., El Badrawy, R., and Hussien, M. I. (2014a). ATM, internet banking and mobile banking services in a digital environment: The Egyptian banking industry. Int. J. Comput. Appl. 90 (8), 45–52. doi:10.5120/15598-4408

Abd El Aziz, R., El Badrawy, R., and Hussien, M. I. (2014b). ¬ ATM, internet banking and mobile banking services in a digital environment: The Egyptian banking industry. Int. J. Comput. Appl. 90 (8), 45–52. doi:10.5120/15598-4408

Acharya, A. S., Prakash, A., Saxena, P., and Nigam, A. (2013). Sampling: Why and how of it. Indian J. Med. Spec. 4 (2), 330–333. doi:10.7713/ijms.2013.0032

Ahamed, M. M., and Mallick, S. K. (2019). Is financial inclusion good for bank stability? International evidence. J. Econ. Behav. Organ. 157, 403–427. doi:10.1016/j.jebo.2017.07.027

Ahmed, O. N., and Wamugo, L. (2019). Financial innovation and the performance of commercial banks in Kenya. Int. J. Curr. Aspects Finance 4 (2), 133. Available at: https://www.ijcab.org/Journal_Articles/2018/11/IJCAF.2018.001.67.pdf.

Akhisar, I., Tunay, K. B., and Tunay, N. (2015). The effects of innovations on bank performance: The case of electronic banking services. Procedia - Soc. Behav. Sci. 195, 369–375. doi:10.1016/j.sbspro.2015.06.336

Akhter, A., Karim, M. M., Jannat, S., and Islam, K. A. (2022). Determining factors of intention to adopt internet banking services: A study on commercial bank users in Bangladesh. Banks Bank Syst. 17 (1), 125–136. doi:10.21511/bbs.17(1).2022.11

Al Shawi, J. M., Abdulrahman, H., and Gopalappa, D. (2022). Impact of technology on the financial performance of selected nationalized and private sector banks in India. Int. J. Nonlinear Analysis Appl. 13 (1), 3633. doi:10.22075/ijnaa.2022.6142

Ashta, A., and Herrmann, H. (2021). Artificial intelligence and fintech: An overview of opportunities and risks for banking, investments, and microfinance. Strateg. Change 30 (3), 211–222. doi:10.1002/jsc.2404

Ayllon, T. W. I. (2020). Digital transformation in the banking sector and its impact on financial inclusion: BIM Peru case study. Portuguesa: Universidade Católica Portuguesa. Master in Marketing).

Caminal, R., and Vives, X. (1996). Why market shares matter: An information-based theory. RAND J. Econ. 27 (2), 221–239. doi:10.2307/2555924

Chauhan, S., Akhtar, A., and Gupta, A. (2022). Customer experience in digital banking: A review and future research directions. International Journal of Quality and Service Sciences.

Cui, X., and Xu, J. (2022). Understanding the E-banking channel selection behavior of elderly customers: A small-world network perspective. J. Organ. End User Comput. (JOEUC) 34 (6), 1–21. doi:10.4018/joeuc.300765

Doumpos, M., Zopounidis, C., Gounopoulos, D., Platanakis, E., and Zhang, W. (2022). Operational research and artificial intelligence methods in banking. Eur. J. Operational Res. doi:10.1016/j.ejor.2022.04.027

Druhov, O., Druhova, V., and Pakhenko, O. (2019a). The influence of financial innovations on EU countries banking systems development. Mark. Manag. Innov. (3), 167–177. doi:10.21272/mmi.2019.313

Druhov, O., Druhova, V., and Pakhenko, O. (2019b). The influence of financial innovations on EU countries banking systems development. Mark. Manag. Innovations (3), 167–177. doi:10.21272/mmi.2019.313

Faryal, D., and Tikhomirov, A. (2022). Investigating the impact of market share on profitability of Afghan banks. Вестник Науки 1 (449), 93. Available at: file:///C:/Users/Lenovo/Downloads/investigating-the-impact-of-market-share-on-profitability-of-afghan-banks.pdf.

Fornell, C., and Larcker, D. F. (1981). Structural equation models with unobservable variables and measurement error: Algebra and statistics. J. Mark. Res. 18 (3), 382–388. doi:10.1177/002224378101800313

Fung, B., Huynh, K. P., and Stuber, G. (2015). The use of cash in Canada, 2015. Bank of Canada review, 45–56. Spring).

Gautam, R. S., Rastogi, S., Rawal, A., Bhimavarapu, V. M., Kanoujiya, J., and Rastogi, S. (2022). Financial technology and its impact on digital literacy in India: Using poverty as a moderating variable. J. Risk Financ. Manag. 15 (7), 311. doi:10.3390/jrfm15070311

Goyal, S., Chawla, D., and Bhatia, A. (2016). Innovation: Key to improve business growth of banking industry. Int. J. Adv. Eng. Technol. 9 (3), 331–346.

Gruin, J., and Knaack, P. (2020). Not just another shadow bank: Chinese authoritarian capitalism and the ‘developmental’promise of digital financial innovation. New polit. Econ. 25 (3), 370–387. doi:10.1080/13563467.2018.1562437

Hair, J. F., Anderson, R. E., Babin, B. J., and Black, W. C. (2019). Multivariate data analysis. 8th Ed. United Kingdom: Cengage Learning.

Hair, J. F., Hult, G. T. M., Ringle, C., and Sarstedt, M. (2016). A primer on partial least squares structural equation modeling (PLS-SEM). United States of America: Sage publications.

Hassan, M. K., Rabbani, M. R., and Ali, M. A. (2020). Challenges for the Islamic Finance and banking in post COVID era and the role of Fintech. J. Econ. Coop. Dev. 41 (3), 93. Available at: https://www.researchgate.net/profile/Mustafa-Rabbani/publication/349138882.

Hassan, M. K, M. K., Rabbani, M. R., Brodmann, J., Bashar, A., and Grewal, H. (2022). Bibliometric and Scientometric analysis on CSR practices in the banking sector. Rev. Financ. Econ. doi:10.1002/rfe.1171

Hussain, I, I., Rehman, A., and Işık, C. (2022). Using an asymmetrical technique to assess the impacts of CO2 emissions on agricultural fruits in Pakistan. Environ. Sci. Pollut. Res. 29 (13), 19378–19389. doi:10.1007/s11356-021-16835-6

Hussain, S, S., Hoque, M. E., Susanto, P., Watto, W. A., Haque, S., and Mishra, P. (2022). The quality of fair revaluation of fixed assets and additional calculations aimed at facilitating prospective investors’ decisions. Sustainability 14 (16), 10334. doi:10.3390/su141610334

Irwan, I. F., Reynaldi, V., Paulina, W., Wahyuni, N. S., Aghniya, S. S., and abdul Hadi, D. (2022). Credit restructuring and financial performance before and during the covid-19 pandemic. Central Asia And Cauc. 23 (1). Available at: file:///C:/Users/Lenovo/Downloads/CAC-10+(163)-ok-(1687-1696).pdf.

Işık, C., Ahmad, M., Ongan, S., Ozdemir, D., Irfan, M., and Alvarado, R. (2021). Convergence analysis of the ecological footprint: Theory and empirical evidence from the USMCA countries. Environ. Sci. Pollut. Res. 28 (25), 32648–32659. doi:10.1007/s11356-021-12993-9

Işık, C., Ongan, S., Bulut, U., Karakaya, S., Irfan, M., Alvarado, R., et al. (2022). Reinvestigating the Environmental Kuznets Curve (EKC) hypothesis by a composite model constructed on the Armey curve hypothesis with government spending for the US States. Environ. Sci. Pollut. Res. 29 (11), 16472–16483. doi:10.1007/s11356-021-16720-2

Isik, C., Ongan, S., Ozdemir, D., Ahmad, M., Irfan, M., Alvarado, R., et al. (2021). The increases and decreases of the environment Kuznets curve (EKC) for 8 OECD countries. Environ. Sci. Pollut. Res. 28 (22), 28535–28543. doi:10.1007/s11356-021-12637-y

Işık, C., Sirakaya-Turk, E., and Ongan, S. (2020). Testing the efficacy of the economic policy uncertainty index on tourism demand in USMCA: Theory and evidence. Tour. Econ. 26 (8), 1344–1357. doi:10.1177/1354816619888346

Jagathi, P. H. (2021). A study on correlation between ATMs and financial performance of select banks with reference to virtual banking. Asian J. Manag. 12 (1), 1. doi:10.5958/2321-5763.2021.00001.9

Kajdi, L., and Kiss, M. (2022). The impact of policy effects on the Hungarian payments card market. J. Bank. Regul. 23 (2), 107–119. doi:10.1057/s41261-021-00152-6

Kamboh, K. M., and Leghari, M. E. J. (2016). Impact of cashless banking on profitability: A case study of banking industry of Pakistan. Paradigms 10 (2), 82–93. doi:10.24312/paradigms100208

Karim, Sitara, Akhtar, M. U., Tashfeen, R., Raza Rabbani, M., Rahman, A. A. A., and AlAbbas, A. (2021). Sustainable banking regulations pre and during coronavirus outbreak: The moderating role of financial stability. Econ. Research-Ekonomska Istraživanja 35, 3360–3377. doi:10.1080/1331677x.2021.1993951

Karim, S., Rabbani, M. R., and Bawazir, H. (2022). Applications of blockchain technology in the finance and banking industry beyond digital currencies. Blockchain Technol. Comput. Excell. Soc., 5.0, 216. doi:10.4018/978-1-7998-8382-1.ch011

Kaur, J. (2020). Innovation in Indian banking sector. Parichay Maharaja Surajmal Inst. J. Appl. Res. 3 (2), 1–7.

Khalifaturofi'ah, S. O. (2021). Cost efficiency, innovation and financial performance of banks in Indonesia. J. Econ. Adm. Sci, 34–43. doi:10.1108/JEAS-07-2020-0124

Khandelwal, S. (2012). E banking innovations: Trends in India. Int. J. Manag. (IJM) 3 (3), 200. Available at: https://d1wqtxts1xzle7.cloudfront.net/30882133/E_BANKING_INNOVATIONS__TRENDS_IN_INDIA-with-cover-page.

Kithinji, E. (2017). Effects of digital banking strategy on financial Inclusion among commercial banks in Kenya. Kenya: Unpublished Masters Project, University of Nairobi.

Kruse, L., Wunderlich, N., and Beck, R. (2019). “Artificial intelligence for the financial services industry: What challenges organizations to succeed,” in Paper presented at the proceedings of the 52nd Hawaii international conference on system sciences (Hawaii.

Le, T. D., and Ngo, T. (2020). The determinants of Bank profitability: A cross-country analysis. Central Bank Review 20 (2), 65–73. doi:10.1016/j.cbrev.2020.04.001

Lutfi, A., Ashraf, M., Watto, W. A., and Alrawad, M. (2022). Business sustainability of small and medium enterprises during the COVID-19 pandemic: The role of AIS implementation. Sustainability 14 (19), 5362. doi:10.3390/su14095362

Ma, D., and Zhu, Q. (2022). Innovation in emerging economies: Research on the digital economy driving high-quality green development. J. Bus. Res. 145, 801–813. doi:10.1016/j.jbusres.2022.03.041

Mahardini, S., Kurnia, S., Maura, Y., Haryanto, P., and Barus, Y. P. (2022). An analysis of the effect of online banking on bank performance in Indonesia. J. Gov. Risk Manag. Compliance Sustain. 2 (1), 54. doi:10.31098/jgrcs.v2i1.904

Mukira, A. R., Kariuki, P., and Muturi, W. (2022). Financial innovation strategies and performance of commercial banks in Kenya. J. Strategic Manag. 7 (2), 36–48. doi:10.47672/jsm.1130

Mullan, J., Bradley, L., and Loane, S. (2017). Bank adoption of mobile banking: Stakeholder perspective. Int. J. Bank Mark. 35, 1154–1174. doi:10.1108/ijbm-09-2015-0145

Musiega, M. (2016). Factors influencing financial performance of E-banking of commercial banks in kakamega county, Kenya. Int. J. Manag. Res. Rev. 6 (6), 805. Available at: https://www.researchgate.net/profile/Maniagi.

Muthinja, M. M., and Chipeta, C. (2018). What drives financial innovations in Kenya’s commercial banks? An empirical study on firm and macro-level drivers of branchless banking. J. Afr. Bus. 19 (3), 385–408. doi:10.1080/15228916.2017.1405705

Mwangi, J. M. (2014a). The effect of financial innovation on financial returns of deposit taking microfinance institutions in Kenya. Master Research Project.

Mwangi, J. M. (2014b). The effect of financial innovation on financial returns of deposit taking microfinance institutions in Kenya. Nairobi: MBA University of Nairobi.

Nazaritehrani, A., and Mashali, B. (2020). Development of E-banking channels and market share in developing countries. Financ. Innov. 6 (12), 12–19. doi:10.1186/s40854-020-0171-z

Nguyen, Y. T. H., Tapanainen, T., and Nguyen, H. T. T. (2022). Reputation and its consequences in fintech services: The case of mobile banking. Int. J. Bank Mark. (ahead-of-print). doi:10.1108/ijbm-08-2021-0371

Nisar, A. (2017). Innovation and technological advancement in the top five banks of Pakistan. Pakistan & Gulf Economist. Retrieved from https://www.pakistangulfeconomist.com/2017/08/28/innovation-technological-advancement-top-five-banks-pakistan/.

Oluwafemi, O. O., Yusuf, A. A., and Shuaibu, H. (2022). Impact of internet banking on profitability of fidelity bank plc. Int. J. Manag. Soc. Sci. Peace And Confl. Stud. 5 (2).

Omoge, A. P., Gala, P., and Horky, A. (2022). Disruptive technology and AI in the banking industry of an emerging market. Int. J. Bank Mark. 40, 1217–1247. (ahead-of-print). doi:10.1108/ijbm-09-2021-0403

Onay, C., and Öztaş, Y. E. (2018). Why banks adopt mobile banking? The case of Turkey. Int. J. Electron. Finance 9 (2), 95–120. doi:10.1504/IJEF.2018.092194

Payne, E. H. M., Peltier, J., and Barger, V. A. (2021a). Enhancing the value co-creation process: Artificial intelligence and mobile banking service platforms. J. Res. Interact. Mark. 15, 68–85. doi:10.1108/jrim-10-2020-0214

Payne, E. H. M., Peltier, J., and Barger, V. A. (2021b). Enhancing the value co-creation process: Artificial intelligence and mobile banking service platforms. J. Res. Interact. Mark. 15 (1), 68–85. doi:10.1108/JRIM-10-2020-0214

Rabbani, M. R., Bashar, A., Nawaz, N., Karim, S., Ali, M. A. M., Rahiman, H. U., et al. (2021b). Exploring the role of islamic fintech in combating the aftershocks of Covid-19: The open social innovation of the islamic financial system. JOItmC. 7 (2), 136. doi:10.3390/joitmc7020136

Rabbani, M. R., Kayani, U., Bawazir, H. S., and Hawaldar, I. T. (2022b). A commentary on emerging markets banking sector spillovers: Covid-19 vs GFC pattern analysis. Heliyon 8 (3), e09074. doi:10.1016/j.heliyon.2022.e09074

Rabbani, M. R., Bashar, A., Hawaldar, I. T., Shaik, M., and Selim, M. (2022a). What do we know about crowdfunding and P2P lending research? A bibliometric review and meta analysis. J. Risk Financ. Manag. 15, 451. doi:10.3390/jrfm15100451

Rabbani, M. R., Mohammed Sarea, A., Khan, S., and Abdullah, Y. (2021a). Ethical concerns in artificial intelligence (AI) implementation: The role of RegTech and islamic finance. Int. Conf. Glob. Econ. Revolutions 238, 381. doi:10.1007/978-3-030-93464-4_38

Rabbani, M. R. (2022). Fintech innovations, scope, challenges, and implications in islamic finance: A systematic analysis. Int. J. Comput. Digital Syst. 11 (1), 1. Available at: https://www.researchgate.net/profile/Mustafa-Rabbani/publication/359040780_Fintech_innovations_scope_challenges_and_implications_in_Islamic_Finance_A_systematic_analysis/links/6223db439f7b32463412490e/Fintech-innovations-scope-challenges-and-implications-in-Islamic-Finance-A-systematic-analysis.pdf.

Rajasulochana, D., and Khizerulla, M. (2022). Service quality in SBI: An assessment of customer satisfaction on E-banking services. J. Posit. Sch. Psychol. 6 (6), 4585–4590. Available at: file:///C:/Users/AALKHA∼1/AppData/Local/Temp/MicrosoftEdgeDownloads/f5f573e1-6a91-40ca-83a2-98d5bd299153/JPSP+-+2022+-+395.pdf.

Raza, M. A., Naveed, M., and Ali, S. (2017). Determinants of internet banking adoption by banks in Pakistan. Manag. Organ. Stud. 4 (4), 12. doi:10.5430/mos.v4n4p12

Saravani, Z., Tash, M. N. S., and Mahmodpour, K. (2015). Evaluation of bank market share and its affective determinants: Sepah bank. Int. Res. J. Appl. Basic Sci. 3 (12A), 240–248. doi:10.12816/0018865

Sathiyavany, N., and Shivany, S. (2018). E-Banking service qualities, E-customer satisfaction, and e-loyalty: A conceptual model. int. jou. soc. hum. inve. 5 (6), 4808–4819. doi:10.18535/ijsshi/v5i6.08

Shafei, R., and Sijanivandi, S. (2022). The intra-sectional marketing maturity and the E-banking market share; involvement of other units in marketing activities. Mark. Sci. Technol. J. 1 (1), 13–28.

Shannak, R. O. (2013). Key issues in e-banking strengths and weaknesses: The case of two Jordanian banks. Eur. Sci. J. 9 (7), 239. Available at: 867-2663-1-PB-with-cover-page-v2.pdf (d1wqtxts1xzle7.cloudfront.net).

Siska, E. (2022). Financial technology (FinTech) and its impact on financial performance of islamic banking. arbitrase. 2 (3), 102= 108. doi:10.47065/arbitrase.v2i3.338

Siyanbola, T. T. (2013). Impact of electronic banking instruments on the intermediation efficiency of the Nigerian economy. eCanadian J. Account. Finance 1 (2), 19–27. doi:10.12816/0001140

Tash, M. N. S., Mahmodpour, K., and Saravani, Z. (2014). Evaluation of Bank market share and its affective determinants: Sepah bank. Kuwait Chapter Arabian J. Bus. Manag. Rev. 3 (12A), 240–248. doi:10.12816/0018865

Tinashe, C. D., and Kelvin, C. (2016). The impact of electronic banking on the competitiveness of commercial banks in Zimbabwe (2014-2015). Int. J. Case Stud. 5 (11), 13. Available at: https://ssrn.com/abstract=2881134.

Uddin, M. K. (2022). Assessing financial performance of mobile banking services organization in Bangladesh. Eur. J. Bus. Manag. Res. 7 (2), 240–245. doi:10.24018/ejbmr.2022.7.2.1365

Victor, O. I., Obinozie, H. E., and Echekoba, F. (2017). The effect of information communication technology and financial innovation on performance on Nigerian commercial banks (2001–2013). Int. J. Contemp. Appl. Sci. 4, 34–43. Available at: https://core.ac.uk/download/pdf/234677231.pdf.

Wonglimpiyarat, J. (2014). Competition and challenges of mobile banking: A systematic review of major bank models in the Thai banking industry. J. High Technol. Manag. Res. 25 (2), 123–131. doi:10.1016/j.hitech.2014.07.009

Xiang, H., Shaikh, E., Tunio, M. N., Watto, W. A., and Lyu, Y. (2022). Impact of corporate governance and CEO remuneration on bank capitalization strategies and payout decision in income shocks period. Front. Psychol. 13, 901868. doi:10.3389/fpsyg.2022.901868

Yang, M. (2021). Financial innovation regulations and firm performance: Evidence from Chinese listed firms. Aust. Econ. Pap. 61, 24–41. doi:10.1111/1467-8454.12231

Zouari-Hadiji, R. (2021). Financial innovation characteristics and banking performance: The mediating effect of risk management. Int. J. Fin. Econ. 7 (2), 1–14. doi:10.1002/ijfe.2471

Glossary

ACCA association of chartered certified accountants

ADM automated decision making

ATM automated teller machine

BMS bank market share

CA chartered accountant

CMB common method biases

IB internet banking

IBP integrated business planning

IFP innovative financial process

MB mobile banking

OLS ordinary least square

PR Pakistani rupees

PLS partial least squares

POS point of sale

RQ research question

SAMA Saudi Arabia monetary agency

SEM structural equation modeling

SPSS software package for social sciences

TB telephone banking

Keywords: innovative financial process, bank's market share, artificial intelligence, Silkbank, silk

Citation: Rabbani MR, Lutfi A, Ashraf MA, Nawaz N and Ahmad Watto W (2023) Role of artificial intelligence in moderating the innovative financial process of the banking sector: a research based on structural equation modeling. Front. Environ. Sci. 10:978691. doi: 10.3389/fenvs.2022.978691

Received: 26 June 2022; Accepted: 10 October 2022;

Published: 03 January 2023.

Edited by:

Cem Işık, Anadolu University, TurkeyReviewed by:

Muhammad Kamran Khan, Bahria University, PakistanMaria Khakwani, The Women University, Pakistan

Rabia Saleem, University of Derby, United Kingdom

Copyright © 2023 Rabbani, Lutfi, Ashraf, Nawaz and Ahmad Watto. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: W. Ahmad Watto, waqasbzu67@gmail.com

†ORCID: Mustafa Raza Rabbani, orcid.org/0000-0002-9263-5657