Veronika Yankovskaya

Veronika Yankovskaya Elena B. Gerasimova2

Elena B. Gerasimova2 Vladimir S. Osipov

Vladimir S. Osipov Svetlana V. Lobova

Svetlana V. Lobova

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

OPINION article

Front. Environ. Sci., 11 July 2022

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.953996

This article is part of the Research TopicEvolution of Environmental Economics & Management in the Age of Artificial Intelligence for Sustainable DevelopmentView all 18 articles

Environmental corporate social responsibility (CSR) is the practice of voluntary environmental protection by business in excess of fulfilling mandatory requirements (norms, standards, environmental taxes and fees, etc.) of the state, manifested in the form of environmental initiatives (for example, the creation of an environmentally friendly urban environment), in the form of the introduction of “green” innovations (for example, waste reduction) and in the form of responsible investments (for example, co-financing of clean energy development programs) (Popkova et al., 2021; Popkova and Zavyalova, 2021; Huo et al., 2022; Lin et al., 2022; Zhang and Cheng, 2022).

In the existing literature, Madaleno et al. (2022), Schiessl et al. (2022), Yang et al. (2022), Yu et al. (2022) indicate the non-commercial nature of environmental CSR. The development of this responsibility is associated with the progress of society. The prevalence of environmental CSR practices is explained, on the one hand, by the ability of society (consumers) to assess the importance of these practices and the tendency to give preference to responsible business products and, on the other hand, by the internal motivation of business leaders to protect the environment. Since society is continuously progressing, the process of development of environmental CSR is considered linear and is described as an upward trend.

The works of Awawdeh et al. (2022), Cheng and Zhang (2022), Godefroit-Winkel et al. (2022), Sadiq et al. (2022) note the contradictory interests of business and society in the implementation of environmental CSR. Consumers expect companies to be willing to donate part of their profits to environmental CSR as a charity and therefore do not always give preference to “green” products with similar consumer properties compared with less environmentally friendly analogues. For businesses, in turn, environmental CSR is associated with additional costs, while sources of financing are often limited, and high market competition dictates the need to recover their investments. The noted conflict of interests constrains the development of environmental CSR and limits its scale.

In the works of Inshakova and Solntsev (2022), Liu and Gao (2022), Madaleno et al. (2022), breakthrough technologies are considered as a deterrent to environmental CSR. Since this responsibility increases the cost of products anyway, technological modernization further increases this cost and limits the possibility of selling products on the target market (Astafyeva et al., 2020; Osipov et al., 2022).

In this regard, the scientific and practical problem of the development of environmental CSR in the era of artificial intelligence (the AI era) comes to the fore. The combination of intensive social progress (the development of society and the knowledge economy) with technological progress can exacerbate the conflict of stakeholders’ interests, thereby increasing barriers to the development of environmental CSR. Nevertheless, environmental CSR in the AI era is poorly studied, which is as a gap in the literature. This gives rise to the following research question (RQ): What is the impact of technological capabilities of the AI era on environmental CSR?

The available individual scientific studies (Gao et al., 2021; Wang et al., 2021) demonstrate the advantages of technological progress for environmental CSR. In his work, Camilleri (2021) outlined the strategic attributes of corporate social responsibility and environmental management. Camilleri (2022) justified the significance of ISO 14001 certification for corporate social responsibility and environmental management of business. Ligozat et al. (2022) proved that artificial intelligence (AI) solutions have an impact on the environment throughout the life cycle of these solutions. Tavana Amlashi et al. (2021) demonstrated that AI allows creating environmentally friendly practical solutions for the production sector. Pagliarini and Lund (2020) developed and introduced an eco-friendly approach to artificial intelligence and robotics.

Based on this, the hypothesis is put forward that the breakthrough technologies available in the AI era do not aggravate, but enable solving the problem with the right approach to their use in the practice of environmental CSR. The purpose of the article is related to the study of the prospects for the development of environmental CSR in the AI era. To achieve this goal, further in this article, a factor analysis of environmental CSR is carried out on the example of the United States and Russia in 2019–2022. Then environmental CSR is reinterpreted from the standpoint of Stakeholder Theory and technological capabilities of the AI era.

The originality of the study consists in the fact that environmental CSR is studied from the standpoint of Stakeholder Theory and is reinterpreted taking into account the new context that has developed in the AI era. Stakeholder Theory allows us to form a systematic understanding of the existing practices of implementing environmental CSR, as well as to offer recommendations for improving environmental CSR practices based on breakthrough technologies, taking into account the current era of artificial intelligence.

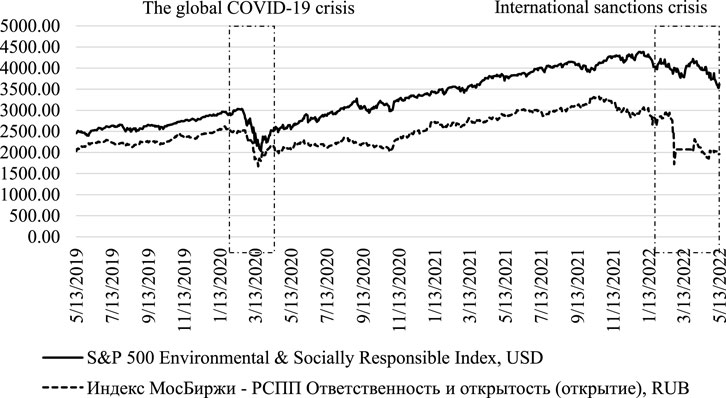

To determine the factors of environmental CSR development, we will analyze the dynamics of changes in the corresponding equity indices on the example of the United States and Russia in 2019–2022. (Figure 1).

FIGURE 1. Dynamics of equity indices of environmental CSR of Dow Jones (United States) and Moscow Exchange (Russia) in 13.05.2019–13.05.2022.

Source: built by the authors based on materials from Dow Jones (2022), Moscow Stock Exchange (2022).

The dynamics of the Dow Jones (United States) and Moscow Stock Exchange (Russia) environmental CSR equity indices in 2019–2022 and the factor analysis of environmental CSR based on it on the example of the United States and Russia in 2019–2022 showed that the development of environmental CSR is largely determined by financial and economic factors. This is evidenced by the fact that in conditions of stability (in 2019 and in 2021), due to social progress, environmental CSR indices are increasing. And in conditions of instability and crisis, in particular, the global COVID-19 crisis in 2020 and the international sanctions crisis in 2022, these indices show a sharp decline. This indicates the cyclical development of environmental CSR, which coincides with the cyclical development of the economy.

To make the obtained results of a quantitative factor analysis more specific, we shall supplement them with a qualitative factor analysis. Amid the global COVID-19 crisis, in the course of implementation of environmental CSR, environmental concern came to the fore to prevent the spread and emergence of a new viral threat. The works of many scientists, such as Gaisie et al. (2022), Hu et al. (2022) are indicative of natural causes of emergence (COVID-19 as a zoonotic disease which originated from introduction of infection from a sick animal to a human) and spread (poor level of sanitation which promotes the transmission of viruses in society, and an increase in the level of sanitation and social distancing as the measures to reduce the disease incidence) of the COVID-19 pandemic.

Amid the international sanctions crisis, environmental CSR has taken on new significance. Environmental concern has become a mechanism for linking companies to communities (Larch et al., 2022). Environmental CSR can and most likely will become a significant criterion making decisions on the inclusion of companies in newly-emerging international value chains (Le and Hoang, 2022). In the coming years, environmental ECO may transform from a voluntary environmental initiative of business to a new form of competition (environmental competition) and even a new (environmental) market barrier to international expansion (Hagen and Schneider, 2021).

Therefore, environmental CSR depends not only on financial and economic factors (stability of the market environment and favorability of the cyclical phase), which are the same for crises, but also on social factors which are specific to each crisis. Thus, amid the global COVID-19 crisis in environmental CSR, companies and local communities preferred waste minimization and circular business practices, while amid the international sanctions crisis—to “green” workplaces and the reduction of resource consumption (improved resource efficiency of business). This requires a flexible approach to environmental CSR management taking into account the financial, economic and social nature of each particular crisis.

As a result of rethinking of environmental CSR from the standpoint of Stakeholder Theory, the following prospects and advantages of using technological capabilities of the AI era have been established. Entrepreneurs with the help of artificial intelligence can rationalize their practice of environmental CSR, receiving intellectual support for the growth of its effectiveness both by saving resources (reducing costs) and by increasing the return on investment (high-precision forecasting of demand for products with improved environmental properties). Also, enterprises get the opportunity to automate the process of notifying all other stakeholders about the implemented practices of environmental CSR. This will provide more complete informational support for environmental CSR and increase its value for stakeholders (Wut and Ng, 2022).

Shareholders and investors, thanks to the high technologies of the AI era, become more fully aware of the activities of the business they finance in the field of environmental CSR. This helps to increase the transparency of environmental CSR and prevent a formal business approach to its implementation. Also, due to artificial intelligence, shareholders and investors can conduct flexible analysis of the effectiveness of environmental CSR and make more informed investment decisions (Ben Hmiden et al., 2022; Halkos et al., 2022; Islam et al., 2022).

Employees of companies can be more aware of the activities of their companies in the field of environmental CSR. This makes it possible to overcome the fragmentation of knowledge, when an employee knows only about his contribution, but is not aware of all the “green” initiatives implemented by the business. Breakthrough artificial intelligence technologies make it possible to turn environmental CSR into a powerful tool for attracting and retaining the best personnel, as well as non-financial motivation to increase productivity and innovative activity of employees with high ecological values. With the use of artificial intelligence, it is possible to form working and professional teams with similar eco-friendly motives and values, as well as to develop highly effective work incentive programs for them (Hongxin et al., 2022; Latif et al., 2022).

State regulators and non-governmental independent organizations (for example, audit companies, industry expert organizations and rating agencies) can conduct automated environmental monitoring of business, compile environmental ratings of companies. Thanks to this, state regulators are able to stimulate environmental CSR by providing tax, credit and other incentives depending on this responsibility (Karwowski and Raulinajtys-Grzybek, 2021; van Balen et al., 2021).

Consumers and the general public get the opportunity to rationalize consumer behavior in the market. High technologies of the AI era can automatically pick up a product with the best (specified) characteristics of price, quality and environmental friendliness. This allows us to support social progress, increasing environmental values with each responsible purchase and stimulating further responsible purchases. The purchase of products from environmentally responsible suppliers can become a social trend, increasing the supply and demand of these products, as well as keeping an equilibrium (fair) price for it (Ye et al., 2021; Yin et al., 2021).

The contribution of the article to the literature is related to the development of scientific provisions of the concept of environmental CSR. In contrast to Madaleno et al. (2022), Schiessl et al. (2022), Yang et al. (2022), Yu et al. (2022), it has been proved that environmental CSR has not only a non-commercial nature, but combines commercial (due to economic factors) and non-commercial (determined by social factors) nature. In this regard, the most comprehensive and clear criteria for assessing the potential for the development of environmental CSR are the market opportunities for the payback of responsible investments and the volume of effective demand for “green” products. The development of environmental CSR is not linear, but cyclical—it is superimposed on the model of the economic cycle. In the phase of economic recovery, social factors prevail and the non–commercial nature manifests itself, and in the phase of economic recession, financial and economic factors prevail and the commercial nature of environmental CSR manifests itself.

In contrast to Awawdeh et al. (2022), Cheng and Zhang (2022), Godefroit-Winkel et al. (2022), Sadiq et al. (2022), it has been proved that the interests of stakeholders (interested parties) do not contradict each other, but on the contrary are balanced with environmental CSR. That is, environmental CSR is a mechanism for establishing and maintaining the balance of industrial markets. Unlike Inshakova and Solntsev (2022), Liu and Gao (2022), Madaleno et al. (2022), it has been proved that breakthrough technologies of the AI era do not aggravate, but allow overcoming the “market failure” of environmental CSR associated with the conflict of interests of stakeholders. Thanks to the technological capabilities of the era of artificial intelligence, the potential of environmental CSR is most fully used to balance the interests of stakeholders and maintain market equilibrium. Therefore, artificial intelligence does not constrain, but stimulates the development of environmental CSR.

Thus, the article filled a gap in the literature, clarifying the essence and prospects for the development of environmental CSR in the AI era. The theoretical significance of the results obtained in the article is related to the fact that they clarified the essence of environmental CSR from the standpoint of Stakeholder Theory. This made it possible to substantiate a new (previously unknown) role of environmental CSR associated with overcoming and ensuring a balance of interests of stakeholders (interested parties).

Further theoretical significance of this paper is that it has revealed social factors of environmental CSR amid the crisis. Drawing on the example of the global COVID-19 crisis and the international sanctions crisis, it has been demonstrated that social factors determine the priorities of environmental CSR amid the crisis, and determine the economic potential of environmental CSR through the loyalty of stakeholders to companies. This has given rise to a new idea of environmental CSR, which, from mainly environmental practical experience, has got a new theoretical interpretation—as a socioeconomic and environmental practice that requires system management from the perspective of sustainable development.

The practical significance of the authors’ conclusions is that broad prospects and favorable opportunities for the development of environmental CSR in the AI era are revealed. The social significance of the research results lies in the fact that the advantages of using breakthrough technologies of the AI era for each stakeholder, justified in this article, allow us to increase the scale and effectiveness of environmental CSR through making it a widespread practice, as well as using its potential in striking a balance between branch markets.

All authors listed have made a substantial, direct, and intellectual contribution to the work and approved it for publication.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenvs.2022.953996/full#supplementary-material

Astafeva, O. V., Astafyev, E. V., Khalikova, E. A., Leybert, T. B., and Osipova, I. A. (2020). XBRL Reporting in the Conditions of Digital Business Transformation. Bus. Transformation//Lect. Notes Netw. Syst. 84, 373–381. doi:10.1007/978-3-030-27015-5_45

Awawdeh, A. E., Ananzeh, M., El-khateeb, A. I., and Aljumah, A. (2022). Role of Green Financing and Corporate Social Responsibility (CSR) in Technological Innovation and Corporate Environmental Performance: a COVID-19 Perspective. Cfri 12 (2), 297–316. doi:10.1108/CFRI-03-2021-0048

Ben Hmiden, O., Rjiba, H., and Saadi, S. (2022). Competition through Environmental CSR Engagement and Cost of Equity Capital. Finance Res. Lett. 47, 102773. doi:10.1016/j.frl.2022.102773

Camilleri, M. A. (2021). Strategic Attributions of Corporate Social Responsibility and Environmental Management: The Business Case for Doing Well by Doing Good!, 30. Sustainable Development, 409–422. doi:10.1002/sd.2256Strategic Attributions of Corporate Social Responsibility and Environmental Management: The Business Case for Doing Well by Doing Good!Sustain. Dev.

Camilleri, M. A. (2022). The Rationale for ISO 14001 Certification: A Systematic Review and a Cost-Benefit Analysis. Corp. Soc. Responsib. Env. doi:10.1002/csr.2254

Cheng, S., and Zhang, F. (2022). Regulatory Pressure and Consumer Environmental Awareness in a Green Supply Chain with Retailer Responsibility: A Dynamic Analysis. Manage Decis. Econ. 43 (4), 1133–1151. doi:10.1002/mde.3444

Gaisie, E., Oppong-Yeboah, N. Y., and Cobbinah, P. B. (2022). Geographies of Infections: Built Environment and COVID-19 Pandemic in Metropolitan Melbourne. Sustain. Cities Soc. 81, 103838. doi:10.1016/j.scs.2022.103838

Gao, F., Liu, H., Zhao, C., Li, X., and Shi, J. (2021). Research on the Impact of Green Technological Innovation and Environmental Responsibility on the Performance of Resource-Based Enterprises under the Low-Carbon Background. Conf. Proc. 9th Int. Symposium Proj. Manag. ISPM 2021, 661–667.978-192171277-7

Godefroit-Winkel, D., Schill, M., and Diop-Sall, F. (2022). Does Environmental Corporate Social Responsibility Increase Consumer Loyalty? Ijrdm 50 (4), 417–436. doi:10.1108/IJRDM-08-2020-0292

Hagen, A., and Schneider, J. (2021). Trade Sanctions and the Stability of Climate Coalitions. J. Environ. Econ. Manag. 109, 102504. doi:10.1016/j.jeem.2021.102504

Halkos, G., Nomikos, S., and Tsilika, K. (2022). Evidence for Novel Structures Relating CSR Reporting and Economic Welfare: Environmental Sustainability-A Continent-Level Analysis. Comput. Econ. 59 (2), 415–444. doi:10.1007/s10614-020-10091-5

Hongxin, W., Khan, M. A., Zhenqiang, J., Cismaș, U., and Ali, L. (2022). Unleashing the Role of CSR and Employees’ Pro-environmental Behavior for Organizational Success: The Role of Connectedness to Nature. Sustain. Switz. 14(6), 3191. doi:10.3390/su14063191

Hu, Z., Yang, L., Han, J., Zhu, L., and Hu, B. (2022). Human Viruses Lurking in the Environment Activated by Excessive Use of COVID-19 Prevention Supplies. Environ. Int. 163, 107192. doi:10.1016/j.envint.2022.107192

Huo, W., Ullah, M. R., Zulfiqar, M., Parveen, S., and Kibria, U. (2022). Financial Development, Trade Openness, and Foreign Direct Investment: A Battle between the Measures of Environmental Sustainability. Front. Environ. Sci. 10, 851290. doi:10.3389/fenvs.2022.851290

Inshakova, A. O., and Solntsev, A. M. (2022). Advances in Research on Russian Business and Management. Charlotte, NC, USA: Information Age Publishing, 267–276.Modification of International Mechanisms for Protecting Human Rights under Conditions of Anthropogenic Environmental Impact with the Intensive Development of Technology of the Sixth Technological Order

Islam, T., Ahmad, S., and Ahmed, I. (2022). Linking Environment Specific Servant Leadership with Organizational Environmental Citizenship Behavior: the Roles of CSR and Attachment Anxiety. Rev. Manag. Sci. doi:10.1007/s11846-022-00547-3

Jones, Dow (2022). S&P 500 Environmental & Socially Responsible Index. URL: https://www.spglobal.com/spdji/en/indices/esg/sp-500-environmental-socially-responsible-index/#overview (data accessed 05 14, 2022).

Karwowski, M., and Raulinajtys-Grzybek, M. (2021). The Application of Corporate Social Responsibility (CSR) Actions for Mitigation of Environmental, Social, Corporate Governance (ESG) and Reputational Risk in Integrated Reports. Corp. Soc. Responsib. Environ. Manag. 28 (4), 1270–1284. doi:10.1002/csr.2137

Larch, M., Shikher, S., Syropoulos, C., and Yotov, Y. V. (2022). Quantifying the Impact of Economic Sanctions on International Trade in the Energy and Mining Sectors. Econ. Inq. 60 (3), 1038–1063. doi:10.1111/ecin.13077

Latif, B., Ong, T. S., Meero, A., Abdul Rahman, A. A., and Ali, M. (2022). Employee-Perceived Corporate Social Responsibility (CSR) and Employee Pro-environmental Behavior (PEB): The Moderating Role of CSR Skepticism and CSR Authenticity. Sustain. Switz. 14 (3), 1380. doi:10.3390/su14031380

Le, H. T., and Hoang, D. P. (2022). Economic Sanctions and Environmental Performance: The Moderating Roles of Financial Market Development and Institutional Quality. Environ. Sci. Pollut. Res. 29 (13), 19657–19678. doi:10.1007/s11356-021-17103-3

Ligozat, A.-L., Lefevre, J., Bugeau, A., and Combaz, J. (2022). Unraveling the Hidden Environmental Impacts of AI Solutions for Environment Life Cycle Assessment of AI Solutions. Sustain. Switz. 14 (9), 5172. doi:10.3390/su14095172

Lin, R., Ma, X., Li, B., Chen, X., and Liang, S. (2022). A Study on the Participation of Peasants in Rural Environmental Improvement from the Perspective of Sustainable Development. Front. Environ. Sci. 10, 853849. doi:10.3389/fenvs.2022.853849

Liu, T., and Gao, H. (2022). Does Supply Chain Concentration Affect the Performance of Corporate Environmental Responsibility? the Moderating Effect of Technology Uncertainty. Sustain. Switz. 14 (2), 781. doi:10.3390/su14020781

Madaleno, M., Dogan, E., and Taskin, D. (2022). A Step Forward on Sustainability: The Nexus of Environmental Responsibility, Green Technology, Clean Energy and Green Finance. Energy Econ. 109, 105945. doi:10.1016/j.eneco.2022.105945

Moscow Exchange (2022). RUIE Index Sustainable Development Vector. URL: https://www.moex.com/ru/index/MRRT (data accessed 05 14, 2022).

Osipov, V. S., Vorozheykina, T. M., Bogoviz, A. V., Lobova, S. V., and Yankovskaya, V. V. (2022). Innovation in Agriculture at the Junction of Technological Waves: Moving from Digital to Smart Agriculture. Smart Innovation, Syst. Technol. 264, 21–27. doi:10.1007/978-981-16-7633-8_3

Pagliarini, L., and Lund, H. H. (2020). Approaching AI and Robotics in an Eco-Friendly Way. J. Robotics, Netw. Artif. Life 6 (4), 217–220. doi:10.2991/jrnal.k.200222.002

Popkova, E., DeLo, P., and Sergi, B. S. (2021). Corporate Social Responsibility amid Social Distancing during the COVID-19 Crisis: BRICS vs. OECD Countries. Res. Int. Bus. Finance 55, 101315. doi:10.1016/j.ribaf.2020.101315

Popkova, E. G., and Zavyalova, E. (2021). “New Institutions for Socio-Economic Development: The Change of Paradigm from Rationality and Stability to Responsibility and Dynamism. New Institutions for Socio-Economic Development,” in The Change of Paradigm from Rationality and Stability to Responsibility and Dynamism, 1–192. doi:10.1515/9783110699869

Sadiq, M., Nonthapot, S., Mohamad, S., Ehsanullah, S., and Iqbal, N. (2022). Does Green Finance Matter for Sustainable Entrepreneurship and Environmental Corporate Social Responsibility during COVID-19? China Finance Rev. Int. 12 (2), 317–333. doi:10.1108/CFRI-02-2021-0038

Schiessl, D., Korelo, J. C., and Mussi Szabo Cherobim, A. P. (2022). Corporate Social Responsibility and the Impact on Economic Value Added: the Role of Environmental Innovation. Eur. Bus. Rev. 34 (3), 396–410. doi:10.1108/EBR-03-2021-0071

Tavana Amlashi, A., Alidoust, P., Pazhouhi, M., Khabiri, S., and Ghanizadeh, A. R. (2021). AI-Based Formulation for Mechanical and Workability Properties of Eco-Friendly Concrete Made by Waste Foundry Sand. J. Mater. Civ. Eng. 33 (4), 04021038. doi:10.1061/(ASCE)MT.1943-5533.0003645

van Balen, M., Haezendonck, E., and Verbeke, A. (2021). Mitigating the Environmental and Social Footprint of Brownfields: The Case for a Peripheral CSR Approach. Eur. Manag. J. 39 (6), 710–719. doi:10.1016/j.emj.2021.04.006

Wang, Y., Yang, Y., Fu, C., Fan, Z., and Zhou, X. (2021). Environmental Regulation, Environmental Responsibility, and Green Technology Innovation: Empirical Research from China. PLoS ONE 16 (9 September), e0257670. doi:10.1371/journal.pone.0257670

Wut, T. M., and Ng, P. M.-L. (2022). Perceived CSR Motives, Perceived CSR Authenticity, and Pro-environmental Behavior Intention: an Internal Stakeholder Perspective. Soc. Responsib. J. doi:10.1108/SRJ-08-2020-0350

Yang, D., Song, D., and Li, C. (2022). Environmental Responsibility Decisions of a Supply Chain under Different Channel Leaderships. Environ. Technol. Innovation 26, 102212. doi:10.1016/j.eti.2021.102212

Ye, Q., Rafique, Z., Zhou, R., Anwar, M. A., and Siddiquei, A. N. (2021). Embedded Philanthropic CSR in Digital China: Unified View of Prosocial and Pro-environmental Practices. Front. Psychol. 12, 695468. doi:10.3389/fpsyg.2021.695468

Yin, C., Ma, H., Gong, Y., Chen, Q., and Zhang, Y. (2021). Environmental CSR and Environmental Citizenship Behavior: The Role of Employees’ Environmental Passion and Empathy. J. Clean. Prod. 320, 128751. doi:10.1016/j.jclepro.2021.128751

Yu, F., Jiang, D., and Wang, T. (2022). The Impact of Green Innovation on Manufacturing Small and Medium Enterprises Corporate Social Responsibility Fulfillment: The Moderating Role of Regional Environmental Regulation. Corp. Soc. Responsib. Environ. Manag. 29 (3), 712–727. doi:10.1002/csr.2231

Keywords: environmental CSR, stakeholder theory, “market failure”, breakthrough technologies, the era of artificial intelligence

Citation: Yankovskaya V, Gerasimova EB, Osipov VS and Lobova SV (2022) Environmental CSR From the Standpoint of Stakeholder Theory: Rethinking in the Era of Artificial Intelligence. Front. Environ. Sci. 10:953996. doi: 10.3389/fenvs.2022.953996

Received: 26 May 2022; Accepted: 21 June 2022;

Published: 11 July 2022.

Edited by:

Bruno Sergi, Harvard University, United StatesReviewed by:

Steven Kayambazinthu Msosa, Mangosuthu University of Technology, South AfricaCopyright © 2022 Yankovskaya, Gerasimova, Osipov and Lobova. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Veronika Yankovskaya, dmVyb25pa2EyOC0yQG1haWwucnU=

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.