Yuan-Bo Zhang

Yuan-Bo Zhang Shi-You Qu1*

Shi-You Qu1* Hai-Bo Li

Hai-Bo Li Miao-Miao Li

Miao-Miao Li

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 12 September 2022

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.952057

This article is part of the Research TopicGreen Innovation and Industrial Ecosystem Reconstruction in Achieving Environmental SustainabilityView all 34 articles

This article investigates how talent policies affect corporate green technological innovation through executive incentive strategies based on signaling theory and principal-agent theory, by examining samples from 1,536 A-share listed companies between 2010 and 2020. The findings indicate that talent policy helps enterprises boost green technological innovation while accelerating it by improving executive compensation incentives. This effect path is more significant in high-tech enterprises and enterprises with weak solvency ratios. However, we find that the current talent policy has inhibited the green innovation of enterprises. The conclusions provide micro-evidence for the impact mechanism by which talent policy affects enterprise green technological innovation and offer scientifically based guidelines for optimizing talent policy to promote innovation-driven development strategy.

To cultivate, introduce, and maximize talent holistically while incorporating it into a vital talent center and global innovation hub, China has implemented a strategy of reinforcing the country’s talent in line with Xi Jinping’s New Era of Socialism with Chinese Characteristics (hereafter the “New Era”) (Lo and Pan, 2021; Jacob and Subba, 2022). To this end, in response to the world’s emerging technological frontiers and the country’s major needs, governments at all levels in China have gradually established a corresponding talent policy system that includes initiatives such as the Changjiang Scholars Program sponsored by the Ministry of Education, the National Million Talents Project sponsored by the State Personnel Board, the Pearl River Talents Program of Guangdong Province, the Qianjiang Scholars of Zhejiang Province, and Shandong Province’s Taishan Scholars (Shi et al., 2018; Chen et al., 2019a; Yue et al., 2020; Miao et al., 1978-2020). Talent, particularly at the highest level, is the pre-eminent resource for enterprise innovation (Rao and Drazin, 2002; Doloreux and Dionne, 2008; Hu, 2008; Lewin et al., 2009). This prompts the question of whether the government’s macro-level talent policy can provide the necessary critical support for micro-level enterprise technological innovation activities. In particular, what is the impact of the current talent policy on the green innovation of enterprises? This scientific issue has attracted significant attention in both political and academic circles in recent years.

Chinese and international scholars have conducted extensive research on the impact that talent policy has on enterprise technological innovation, but the conclusions offered to date are inconsistent (Yang et al., 2019; Zhu et al., 2021). Some studies have suggested that government talent policies positively impact corporate technological innovation, given that talent policy signals government recognition and preferential treatment of talents to the outside world and makes it convenient for enterprises to secure the various requisite resources for innovation (Feldman and Kelley, 2006; Meuleman and De Maeseneire, 2012; Wu, 2017; Wei and Zuo, 2018; Li et al., 2019). Meanwhile, other studies maintain that enterprises manipulate their talent numbers to cater to policies, resulting in a considerable waste of innovation resources (Wang et al., 2021). Moreover, a small number of studies believe that, because government investment in talent policy is significantly lower than investment in R and D subsidy policies, talent policy’s impact on enterprises’ technological innovation is limited (Yang and Pan, 2020).

Among the reasons for the divergent conclusions of existing research is that of the tendency to overlook the role of executives in corporate innovation activities (Shao et al., 2020). As the main decision-making body, who are also responsible for the execution and supervision of innovation activities, enterprise executives’ decisions and willingness with respect to innovation directly affect the allocation efficiency of innovation resources, which in turn impacts the extent to which enterprises engage in technological innovation (Hao et al., 2019; Sarfraz et al., 2020; Ersahin et al., 2021; Zhao et al., 2021; Zhou et al., 2021). Research based on principal-agent theory has demonstrated that, as a result of the high uncertainty and lengthy return cycles associated with innovation activities, executives choose less innovation investment based on self-interest, resulting in diminished resource allocation efficiency (Huang et al., 2014; Si et al., 2020; Zheng et al., 2020; Jin et al., 2022). The implementation of incentives for corporate executives can effectively reduce the agency costs that enterprises incur in the allocation of innovation resources and improve the efficiency of innovation resource allocation (Coles et al., 2006; Xu et al., 2019). Given that talent policy offers the dual incentive effects of currency and reputation, it can directly affect executives’ approach to innovation decision-making and willingness, thereby affecting the allocation efficiency of innovation resources (Shapiro et al., 2017; Ullah et al., 2022). However, few studies have explored the relationship between talent policy, executive incentives, and corporate technological innovation.

To this end, based on signaling theory and principal-agent theory, this paper is focused on the relationship between talent policy, executive incentive strategy, and corporate technological innovation based on panel data from China’s A-share listed companies for the period between 2010 and 2020. The findings indicate that talent policy can directly promote enterprises’ technological innovation while indirectly promoting investment through executive compensation incentives; this effect path varies considerably as a result of enterprises’ divergent solvency ratios and the heterogeneity of the industry.

This paper is distinguished from existing research in several respects. First, in light of the “New Era” initiative, this paper is focused on the unique tool of talent policy, revealing its impact on enterprises’ technological innovation while resolving the research dilemma caused by the generalization of non-R&D subsidy policy in the existing literature. Second, it reveals how the macro talent policy system can influence enterprises’ technological innovation through executive incentives at the micro level. Finally, it reveals that the role played by talent policy in incorporating technological innovation through executive incentives varies significantly as a result of corporate heterogeneity. The research conclusions thus provide crucial theoretical support for the formulation of more effective talent policies.

As a significant measure that allows the government to intervene in enterprises’ technological innovation, talent policy can compensate for various resources required for technological innovation via signal transmission. First, talent policy support is conducive to enterprises’ accumulation of human resources and attraction of outstanding international talent. An enterprise’s implementation of talent policy signals that it values and treats talent preferentially. A high level of human capital, the positive external effects of knowledge sharing, and the knowledge spillover formed by the accumulation of human resources are all conducive to mutual exchange and learning, and facilitate knowledge and technology accumulation for the development of enterprise innovation activities (Peter, 1999; Jiang et al., 2020; Zygmunt, 2020). Second, talent policy support allows enterprises to access policy resources. Enterprises that receive talent policy support are often more likely to gain the government’s trust, and the government, for its part, is more inclined to extend policy support to such enterprises to save on the costs associated with prior inspection, in-process supervision, and post-assessment (Kleer, 2010; Sein and Prokop, 2021). For example, the acquisition of R&D subsidies or tax incentives can reduce the innovation risk to enterprises or minimize R&D costs (Colombo et al., 2013; Jourdan and Kivleniece, 2017; Chen et al., 2019b). These policies directly or indirectly stimulate enterprises’ enthusiasm for technological innovation. Third, talent policy provides enterprises with access to financial resources, conveying the seal of government approval to the outside world and indicating that the company has strong innovation capabilities and superior innovation projects. This helps secure the favor of external investors, relieves the company’s financing constraints to a certain extent, and supplements the resources required for technological innovation. Accordingly, this paper proposes the following hypothesis:

Hypothesis 1. (H1): Talent policy can significantly improve enterprises’ technological innovation levels.

Two main types of incentives are available to corporate executives: short-term compensation incentives and long-term equity incentives. First, talent policy can significantly strengthen executives’ compensation and incentive levels. From the perspective of policy content, most talent policies emphasize cash rewards or individual tax incentives for talents, thus directly increasing executives’ salaries. For example, the Jingxian Plan sponsored by Beijing’s Shijingshan District provides appropriate individual tax incentives to corporate executives who have made outstanding contributions, and appropriate incentives for their annual individual income tax exceeding 15% of their taxable income. Second, talent policy can significantly boost executives’ equity incentive levels, with some policies providing important guarantees that allow executives to increase their shareholding ratios by establishing relevant equity incentive funds. For example, to enhance enterprises’ innovation abilities and stimulate talent vitality, Wuhan’s Optical Valley has issued Administrative Measures for Equity Incentive Special Funds to help enterprises establish and improve their long-term incentive systems. The pain point associated with equity incentives is that large amounts of capital are required to invest in shares; this special fund policy requires only the equity of senior executives as a pledge, and the loan has no interest, which allows the proportion of equity held by senior executives to be increased. Accordingly, this paper proposes the following hypothesis:

Hypothesis 2a. (H2a): Talent policies can significantly improve executive compensation incentive levels.

Hypothesis 2b. (H2b): Talent policies can significantly improve executive equity incentive levels.

As the direct object of talent policy, executives’ innovation decisions and willingness to innovate affect enterprises’ innovation output. First, talent policy has a salary compensation effect, and the misalignment of executives’ and shareholders’ goals is the chief cause of the principal-agent problem. Since the level of executive compensation is often related to the company’s performance, in consideration of short-term benefits, such as wages and bonuses, executives typically avoid the innovative activities that can bring shareholders long-term benefits (Holmstrom, 1989; Tosi et al., 2000; Wang et al., 2022). The compensatory effect of talent policy inhibits this risk aversion tendency, encouraging executives to invest in innovation based on the long-term benefits, thereby improving the enterprise’s technological innovation level (Gibbons and Murphy, 1992; Lui et al., 2016). Second, talent policy has a reputational incentive effect: executives who are supported by talent policies have greater prestige and are more likely to receive equity incentives. According to agency theory, equity incentives can bind the interests of executives and shareholders together, prompting executives to opt for innovation investments based on the company’s long-term interests while also helping to sustain the innovation process (Jensen and Meckling, 1976; Bertrand and Mullainathan, 2003; Alessandri and Pattit, 2014). This solidarity is conducive to the development of enterprises’ technological innovation activities (Lin et al., 2011). Because of the dual externalities faced by green innovation, the problem of innovation power becomes more serious. The above effect may be reversed. And, accordingly, this paper proposes the following hypothesis:

Hypothesis 3a. (H3a): Talent policy can positively impact corporate technological innovation by improving executive compensation incentive levels. The above effect may be reversed for green innovation.

Hypothesis 3b. (H3b): Talent policy can positively impact corporate technological innovation by improving executive equity incentive levels. The above effect may be reversed for green innovation.

This paper takes China’s A-share listed companies from 2010 to 2020 as the research sample using data derived from the Guotai’an China Stock Market & Accounting Research (CSMAR) database. During the research process, the initial samples were screened according to the following principles: first, eliminate samples with missing or ambiguous data on the main variables; second, eliminate financial industry and real estate enterprises in view of the particularity of their business objectives and financial structures; and third, exclude ST, *ST, PT, and other financially abnormal enterprise samples to avoid extreme value interference. Ultimately, 1,536 companies were retained, with 5,004 valid observations.

(1) Enterprise Technological Innovation: The existing literature mainly measures enterprises’ technological innovation from two aspects: innovation output and innovation input (Balkin et al., 2000; Argyres and Silverman, 2004; Lerner and Wulf, 2007; Cornaggia et al., 2015). As such, this paper mainly discusses how talent policy affects corporate technological innovation by influencing executives’ decision-making and willingness with respect to innovation, thus adopting corporate technological innovation investment to measure corporate technological innovation. At present, the enterprise’s R&D investment index is commonly applied to measure the technological innovation investment of enterprises (Flor and Oltra, 2004; Falk, 2012). Moreover, to eliminate the dimension problem, this study adopts the natural logarithm of corporate R&D investment as a measure of corporate technological innovation (lnRD). For green innovation, we use the enterprise green patent measurement and match the samples (Grepat). Because green patents belong to counting data, we use Poisson regression.

(2) Talent Policy: Referring to the measurement method devised by Chen et al. (2018) for talent policy, a keyword search was conducted on the government subsidy details in the appendix of the financial statements from the Guotai’an database, screening for the keywords “talent” (rencai), “person” (renwu), and “excellent” (yingcai). The project finally verified whether the enterprise had obtained talent policy support. If the enterprise government subsidy detail contains the above keywords, the talent policy variable (Tal) is 1; otherwise, it is 0. This paper also uses the above retrieval method to test the model’s robustness and use the corresponding subsidy amount as a surrogate variable for talent policy (Tal 1).

(3) Executive Incentive Strategies: Executive incentives mainly include compensation incentives and equity incentives. The current standard practices reported in domestic and foreign literature are adopted. Among these, the measurement of compensation incentives is expressed by the total compensation of the sample enterprises’ executives in accordance with Mehran’s (1992) methods); equity incentive is expressed by the shareholding ratio of senior executives, drawing on the practices implemented by Lin et al. (2011).

(4) Controlled Variables: To control the influence of other factors on the research results, based on the relevant literature, the controlled variables used in this paper include Enterprise Size (Size), Human Capital (HC), Separation Rate of Two Rights (SRTR), Main Business Income Growth Rate (Grow), Operating Cash Flow (CF), the Gearing Ratio (GR), Return on Total Assets (Roa), Nature of Property Rights (NPR), Board Size (Bsize), and Enterprise Age (Age). The specific variable names and their descriptions are shown in Table 1.

TABLE 1. Variable names and descriptions.

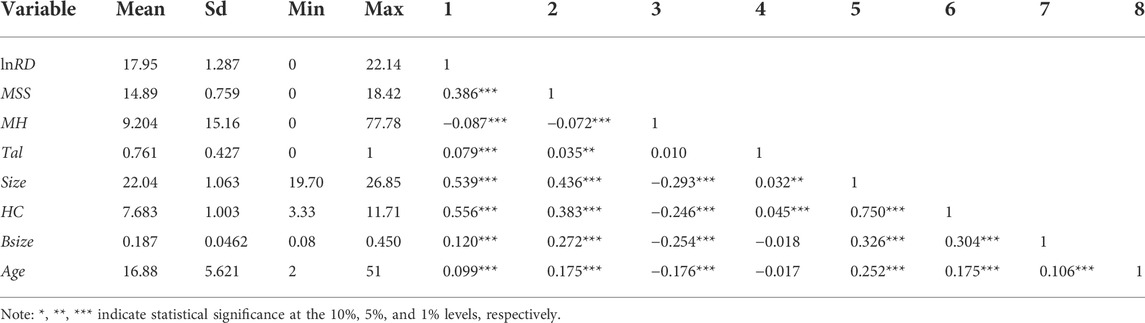

Table 2 presents the samples’ descriptive statistics and the Pearson correlation coefficient matrix. The average value of enterprise R&D investment cost is 17.95, and the standard deviation is 1.287, indicating that the observed sample enterprises’ technological innovation levels are relatively discrete. The mean and standard deviations of executive compensation incentives are 14.89 and 0.759; the mean and standard deviation of equity incentives are 9.204 and 15.16, indicating that the dispersion degree of executive equity incentives in sample companies is greater than that of salary incentives. Table 2 also shows that 76.08% of enterprises have received talent subsidies, indicating that it has become common for listed companies to obtain government talent subsidies. The average company size is 22.04, the average human capital is 7.683, the average board size is 0.187, and the average company age is 16.88. The correlation coefficient matrix demonstrates that talent policy is positively correlated with executive compensation incentives and corporate technological innovation indicators, which initially supports the positive relationship between talent policy and corporate technological innovation. Executive equity incentives and corporate technological innovation are negatively correlated, which is inconsistent with this paper’s hypothesis and warrants further testing. The variance inflation factor test was also performed on the variables, and the mean value of the variance inflation factor was 1.46, indicating no severe multicollinearity problem.

TABLE 2. Descriptive statistics and correlation coefficients of core variables.

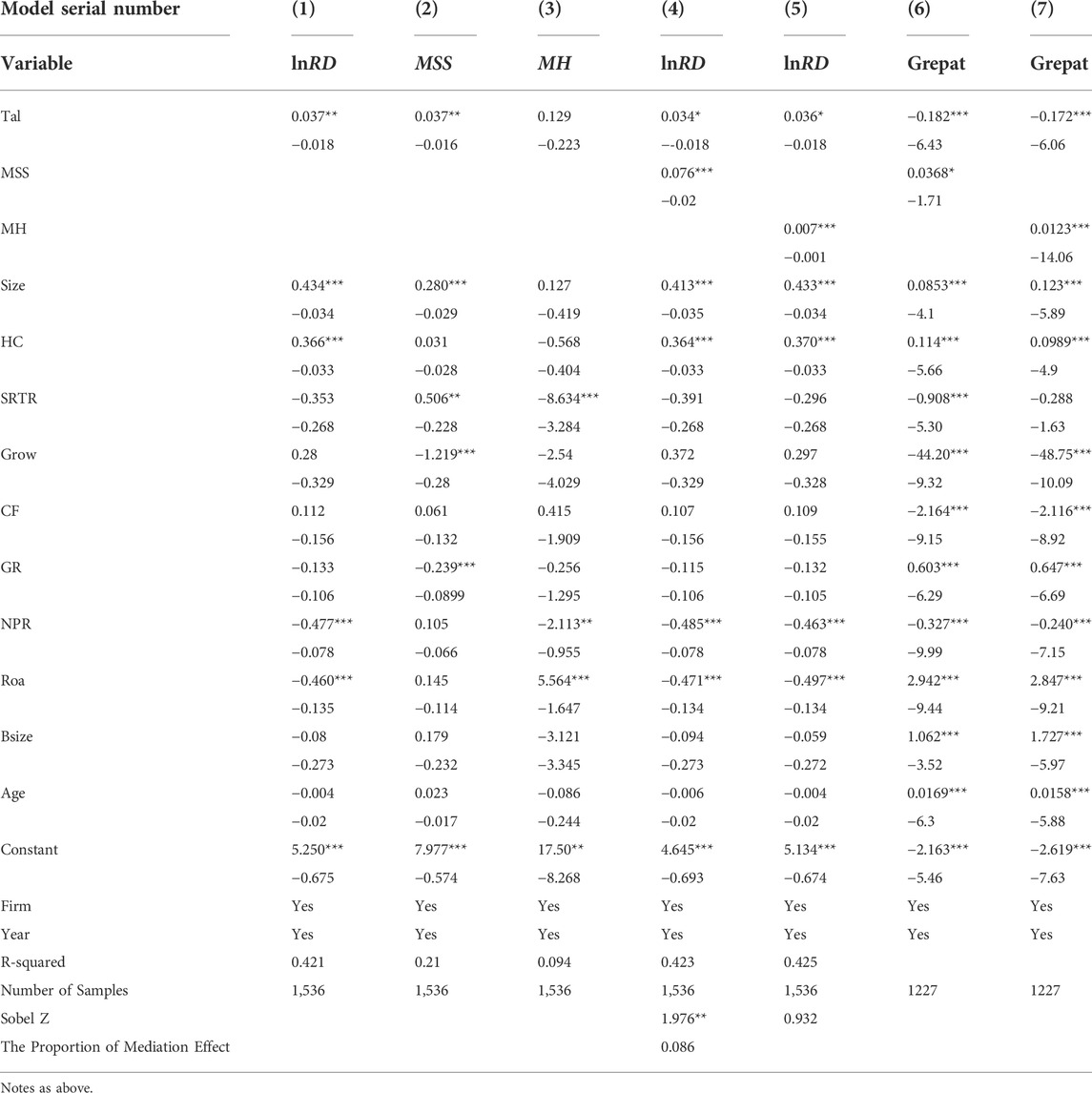

After the Hausman Test, the two-way fixed effect model was selected, and the specific analysis results are shown in Table 3.

TABLE 3. Regression analysis and sobel test.

First, Model 1) in Table 3 shows that the talent policy positively impacts enterprises’ technological innovation and is significant at the 5% level (

According to the Sobel test, the ratio of the mediation effect to the total effect of executive compensation incentives is 0.086, indicating that the executive compensation incentive level can explain 8.6% of government talent policies’ promotion of corporate technological innovation. Executive compensation incentives partially mediate the relationship between talent policy and corporate technological innovation; thus, Hypothesis 3a is verified. Finally, Model 5) in Table 3 is used to test the mediating effect of executive equity incentives—that is, to test Hypothesis 3b. Model 5) in Table 3 reveals that, after adding executive equity incentives, equity incentives have a significant positive impact on enterprises’ technological innovation (

We added green patent as a new dependent variable, and compared it with the previous analysis, and obtained more abundant research conclusions and enlightenment, which also provided better guidance and scientific basis for the specific implementation of the policy. From models 6 and 7, the talent policy significantly inhibited green innovation. We argue that on the one hand, the talent subsidy may be used for human capital accumulation, crowding out green R&D; On the other hand, technology R&D is a long-term process, especially the invention of green technology. At present, the impact of human capital investment on green technology has not been effective.

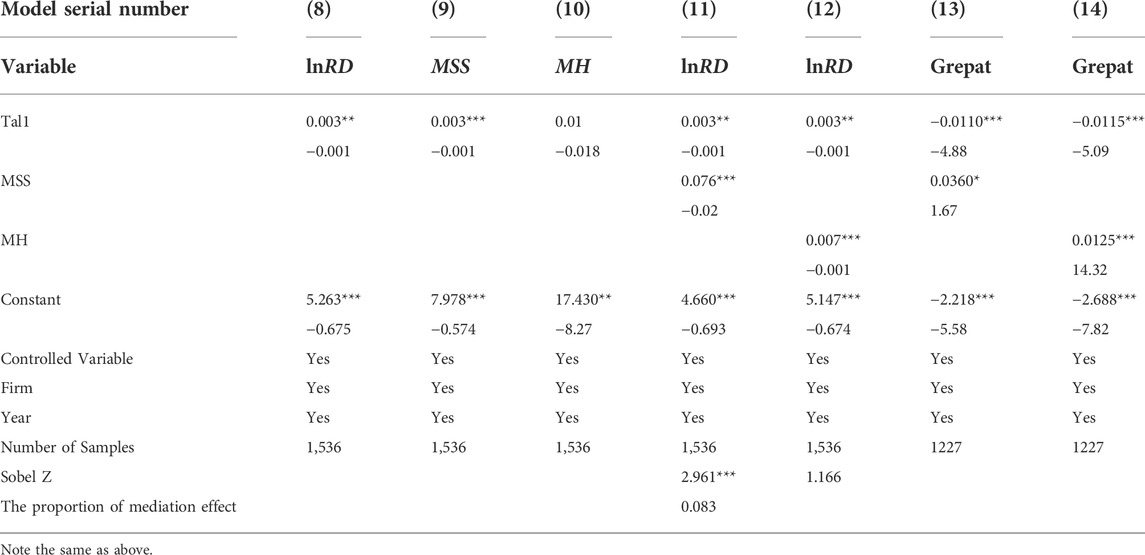

We used the cost of replacing the talent subsidy to test the reliability of the regression results’ reliability. The results of the regression analysis are shown in Table 4. The results demonstrate that the relationship between talent policy and corporate technological innovation remains significant, and the direction remains unchanged. The direction of the regression coefficients of executive equity incentives and other controlled variables is also highly consistent with the previous regression results. Therefore, the previous empirical results are robust.

TABLE 4. Robustness test.

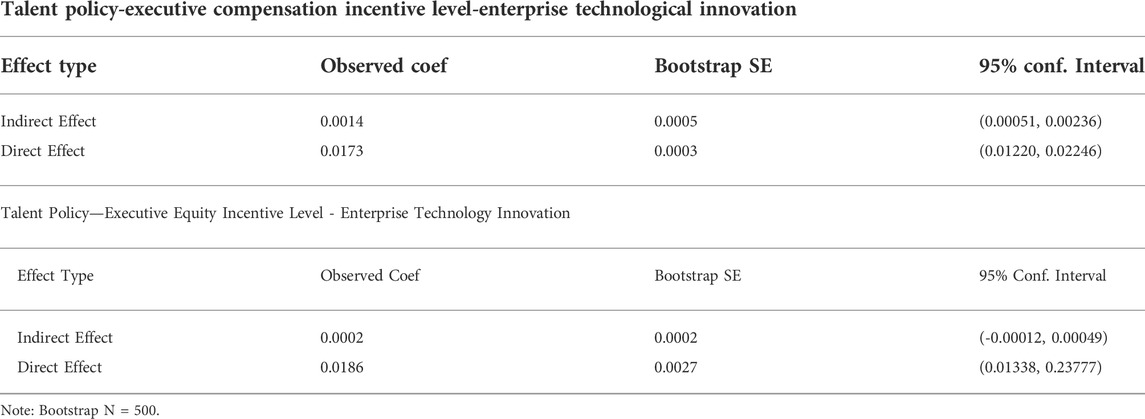

This study also used a different method to test the mediation effect. Newton and Raftery 1994) (Newton and Raftery, 1994) suggested using the bootstrap test without prior information. Compared with the stepwise regression method and the Sobel test, the confidence interval obtained by the bootstrap test is more accurate and effective. Therefore, this paper uses the bootstrap test method in the robustness test to determine whether executive incentives have a mediating effect. Table 5 presents the results. The results proved consistent with the conclusions reported in previous studies. Talent policy also significantly inhibited green innovation.

TABLE 5. Bootstrap test method.

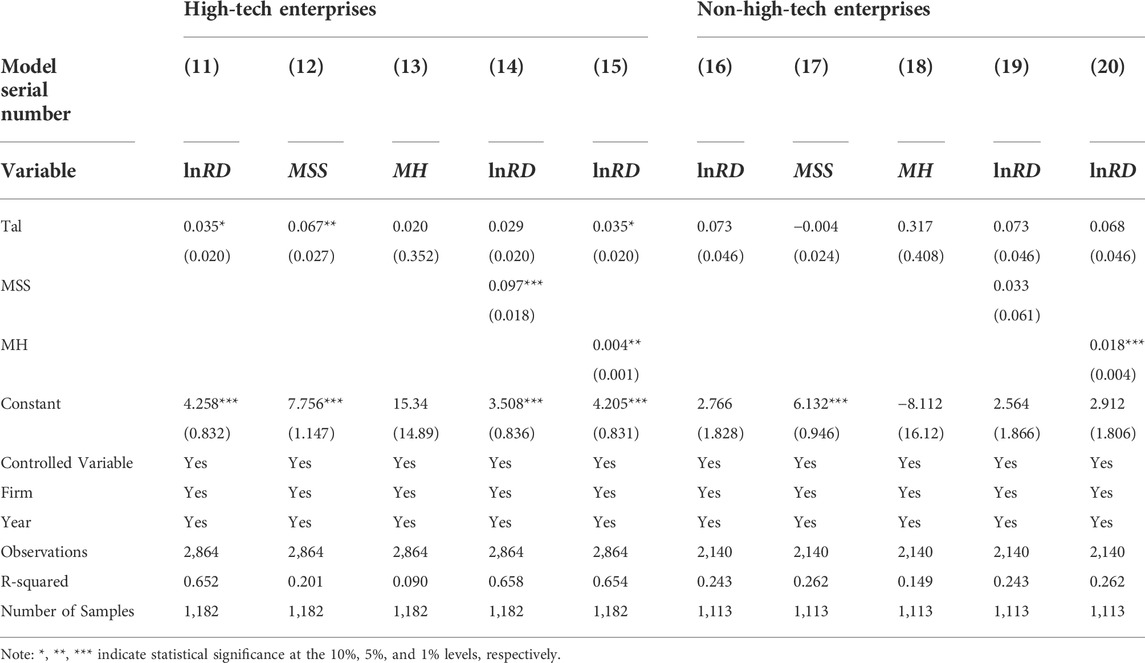

Intermediary model analysis of the total sample confirmed that talent policy can promote enterprises’ technological innovation by improving executive compensation levels. This section is focused on whether this path differs significantly as a result of the heterogeneity of the enterprises’ industry types and solvency ratios. The first difference pertains to the type of industry in which the company operates. Referring to the classification method devised by Sun et al. (2021a), if a company has obtained the national or provincial high-tech enterprise qualification certification, the enterprise is defined as a high-tech enterprise; otherwise, it is a non-high-tech enterprise. After differentiating enterprise types, Table 6 reports relationships between talent policies, executive compensation incentives, and corporate technological innovation. The results reveal that the influence coefficient of talent policy on the technological innovation of high-tech enterprises is positive and statistically significant at the 10% level. The executive incentives of technology enterprises and the technological innovation of enterprises are not significant. The main reason is that the technology of high-tech industries changes and the problem of technology spillover are faster and more severe than in non-high-tech enterprises. Therefore, the imbalance between innovation risks and benefits borne by high-tech enterprise executives and the principal-agent problem is more prominent and severe than that of non-high-tech enterprises (Aboelmaged and Hashem, 2019; Khalili et al., 2019; Sun et al., 2019; Sun et al., 2020; Sun et al., 2021b; Sun et al., 2021c; Shao and Chen, 2022). Talent policy support directly affects executives. It alleviates the principal-agent problem by improving executives’ compensation and incentive levels in high-tech enterprises, thereby improving the innovation willingness of executives, which is conducive to the development of innovation activities. The Sobel test demonstrated that, regardless of whether it is a high-tech or non-high-tech enterprise, the executive’s equity incentive does not have a significant mediating role, which further verifies that H3b does not hold.

TABLE 6. Sub-sample Regression of whether it is a high-tech enterprise.

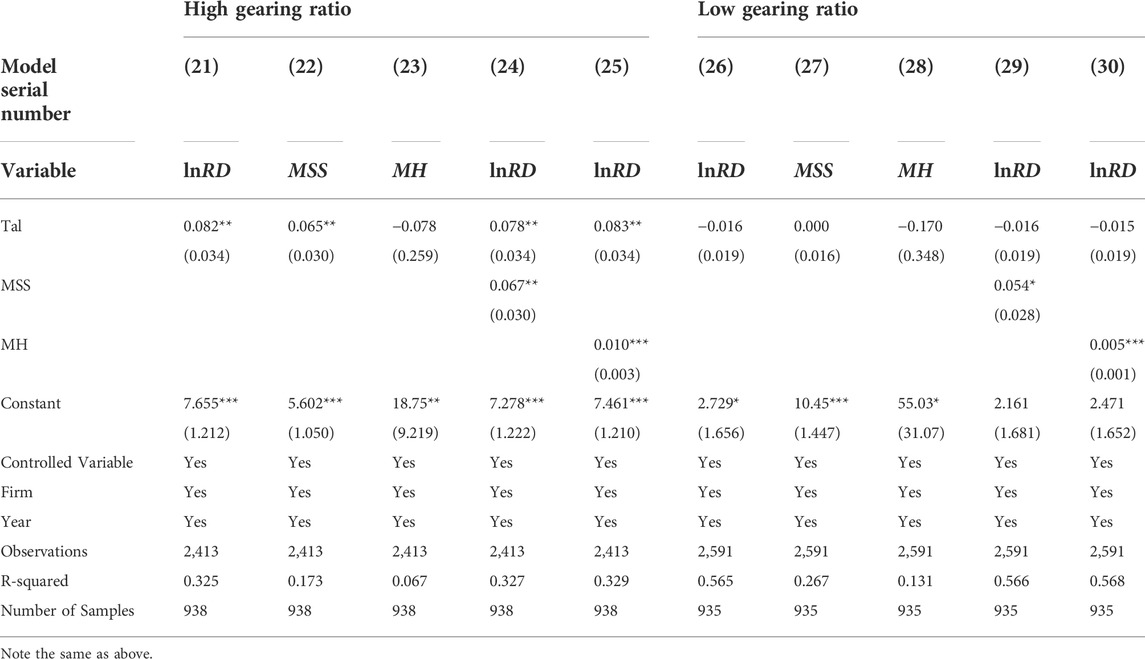

The second difference relates to the differential impact of corporate solvency. In this paper, the average value of the sample enterprises’ asset-liability ratio is used as the standard, and the enterprises are categorized based on whether they are high or low asset-liability ratio enterprises. Table 7 reports the relationship between talent policy, executive incentives, and technological innovation after distinguishing the company’s debt level. The results show that the influence coefficient of talent policy on the technological innovation of enterprises with high asset-liability ratios is 0.082, and it is significant at the level of 5%. This confirms that talent policy contributes to the technological innovation of enterprises with a high asset-liability ratio. Companies with high debt ratios are often more cautious about innovation investments, associated with higher risks and uncertain returns. The talent policy helps them obtain financial resources and government support, reducing their innovation costs and uncertainties and thus benefiting their technological innovation activities. Models (31), (32), and (34) reveal a mediating effect between executive compensation and incentive levels. The main reason for this is that when a company’s debt level is high, shareholders may reduce compensation to the company’s executives, to preserve the company’s cash flow. Talent policy indirectly helps companies with high asset-liability ratios to ease their financing constraints and enrich their cash flow. It directly increases executives’ remuneration levels through subsidies, thereby improving the efficiency of executives’ innovation resource allocation, which is conducive to technological innovation. Companies with low debt-to-equity ratios face relatively low innovation and bankruptcy risks, and so talent policies may play a minimal role. The Sobel test further revealed that, regardless of whether a company is high or low asset-liability, executive equity incentives do not play a significant mediating role, further confirming that H3b does not hold.

TABLE 7. Sub-sample regression of solvency level.

In recent years, governments at all levels—from central to local—have gradually established a relatively complete talent policy system to cultivate, attract, and capitalize on talent through talent policies and provide the necessary support for the innovation and development of local enterprises. This study took 1,536 A-share listed companies from 2010 to 2020 as samples and built a two-way fixed effect model to investigate how macro-level talent policy affects corporate technological innovation through micro-level incentives for corporate executives. The findings indicate that talent policy significantly boosts enterprises’ technological innovation levels. Talent policy can also indirectly promote technological innovation by increasing executive compensation rather than equity incentive levels. The main reason for this is that the talent policy has a salary compensation effect, protecting executives’ short-term benefits and effectively improving the imbalance between executives’ innovation risk-taking and benefits, thus supporting enterprises in performing innovation activities. Moreover, analysis of enterprises’ solvency ratios and the heterogeneity of their industries reveal that talent policy exerts a more significant effect on innovation incentives for high-tech enterprises and enterprises with weak solvency. While we find the talent policy significantly inhibited green innovation. Our results are different from those of Shao, which may be due to differences in our variable measurement methods and different perspectives of the mechanism analyzed.

Encouraging the innovation consciousness of enterprise executives will help to guide the scientific innovation of enterprise talents and put enterprises in a favorable position in the incentive competition. Modern enterprises generally adopt salary incentive to encourage technological innovation. Enterprises should be good at equity incentive and give certain equity to senior executives to ease the conflict of interests between senior executives and shareholders in the R and D process. The requirement of high-quality economic development has further increased the attention of environmental protection issues, and all stakeholders have put forward higher requirements for environmental protection. Green technology innovation is becoming an important emerging field in the new round of global industrial revolution and scientific and technological competition. To speed up the construction of a market-oriented green technology innovation system, the government needs to expand the “breadth” of the transformation of scientific and technological achievements, improve the “intensity” of gathering innovation resources, further reduce the burden of scientific and technological personnel, clear the obstacles to the flow of talents, and further improve the enthusiasm of scientific and technological personnel in developing and transforming science and technology. Universities and scientific research institutes that transform their scientific and technological achievements into positions and give individual rewards to scientific and technological talents in the form of shares or capital contribution ratio may temporarily exempt from individual income tax. At the same time, it is necessary to actively create a green scientific and technological innovation achievement transformation trading platform integrating R and D transformation, technology transfer, achievement transformation and talent training. This paper’s conclusions have the following implications for talent policy formulation.

First, the implementation modes of different talent policies should be further reinforced. This study found that talent policy can safeguard the short-term benefits that executives derive through the compensation effect, thereby improving the efficiency with which executives allocate innovation resources. Therefore, government departments should focus on direct support methods, such as monetary incentives and personal tax protection, when introducing talent policies. Meanwhile, enterprises should also incorporate innovation performance into executives’ performance appraisals to rectify further the imbalance between innovation risks and benefits and provide necessary guarantees for corporate executives to carry out innovation activities.

Second, the talent policy system should be further refined to improve the efficiency of talent policy support. Through heterogeneity analysis, this study found that talent policy has a more significant effect on high-tech enterprises’ technological innovation than other factors. Therefore, talent policy should be further refined and tailored toward high-tech enterprises as much as possible. Governments should thus formulate targeted talent policies, talent service systems, and mechanisms to effectively boost high-tech enterprises’ innovation levels and accelerate the realization of high-tech enterprises’ high-quality development.

Third, security enterprises should be further screened, and the marginal role that talent policy currently plays should be maximized. This study found that talent policy has a greater impact on the technological innovation of companies with weak solvency through executive compensation incentives. In companies with higher debt ratios, the level of executive compensation is often lower, and talent policy has a more significant marginal effect on executives’ compensation levels through cash incentives and personal tax protection. It is thus recommended that a more accurate and targeted talent policy system be formulated for highly indebted enterprises.

Fourth, the role that talent policy plays in transmitting positive signals to enterprises should be maximized. This study also found that talent policy can send positive signals, such as preferential treatment of talents and government recognition, to talents, investors, and stakeholders outside the enterprise and help enterprises obtain various innovative resources. Therefore, companies that have obtained talent policies should disclose relevant positive information to the outside world via multiple channels to reinforce further the role that talent policies play in transmitting positive signals.

Our study also has some limitations. Due to the availability of data, we only tested the sample of Listed Companies in China. Future analysis data can further expand the sample to better test the assumptions and theoretical assumptions of this study, including comparative analysis of scenarios in different regions and countries.

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding authors.

Doctoral candidate YZ wrote the draft, and Professor SQ revised the paper; Professor HL data analysis, Associate Professor ML data processing.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Aboelmaged, M., and Hashem, G. (2019). Absorptive capacity and green innovation adoption in SMEs: The mediating effects of sustainable organizational capabilities. J. Clean. Prod. 220, 853–863. doi:10.1016/j.jclepro.2019.02.150

Alessandri, T. M., and Pattit, J. M. (2014). Drivers of R&D investment: The interaction of behavioral theory and managerial incentives. J. Bus. Res. 67, 151–158. doi:10.1016/j.jbusres.2012.11.001

Argyres, N. S., and Silverman, B. S. R&D. (2004). R&D, organization structure, and the development of corporate technological knowledge. Strateg. Manag. J. 25, 929–958. doi:10.1002/smj.387

Balkin, D. B., Markman, G. D., and Gomez-Mejia, L. R. (2000). Is CEO pay in high-technology firms related to innovation? Acad. Manage. J. 43, 1118–1129. doi:10.5465/1556340

Baron, R. M., and Kenny, D. A. (1986). The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Personality Soc. Psychol. 51, 1173–1182. doi:10.1037/0022-3514.51.6.1173

Bertrand, M., and Mullainathan, S. (2003). Enjoying the quiet life? Corporate governance and managerial preferences. J. Polit. Econ. 111, 1043–1075. doi:10.1086/376950

Chen, J., Heng, C. S., Tan, B. C., and Lin, Z. (2018). The distinct signaling effects of R&D subsidy and non-R&D subsidy on IPO performance of IT entrepreneurial firms in China. Res. Policy 47, 108–120. doi:10.1016/j.respol.2017.10.004

Chen, S., Lin, Y., Zhu, X., and Akbar, A. (2019). Can international students in China affect Chinese ofdi—empirical analysis based on provincial panel data. Economies 7, 87. doi:10.3390/economies7030087

Chen, S., Huang, Z., Drakeford, B. M., and Failler, P. (2019). Lending interest rate, loaning scale, and government subsidy scale in green innovation. Energies 12, 4431. doi:10.3390/en12234431

Coles, J. L., Daniel, N. D., and Naveen, L. (2006). Managerial incentives and risk-taking. J. Financ. Econ. 79, 431–468. doi:10.1016/j.jfineco.2004.09.004

Colombo, M. G., Croce, A., and Guerini, M. (2013). The effect of public subsidies on firms’ investment–cash flow sensitivity: Transient or persistent? Res. Policy 42, 1605–1623. doi:10.1016/j.respol.2013.07.003

Cornaggia, J., Mao, Y., Tian, X., and Wolfe, B. (2015). Does banking competition affect innovation? J. Financ. Econ. 115, 189–209. doi:10.1016/j.jfineco.2014.09.001

Doloreux, D., and Dionne, S. (2008). Is regional innovation system development possible in peripheral regions? Some evidence from the case of La pocatière, Canada. Entrepreneursh. Regional Dev. 20, 259–283. doi:10.1080/08985620701795525

Ersahin, N., Irani, R. M., and Le, H. (2021). Creditor control rights and resource allocation within firms. J. Financ. Econ. 139, 186–208. doi:10.1016/j.jfineco.2020.07.006

Falk, M. (2012). Quantile estimates of the impact of R&D intensity on firm performance. Small Bus. Econ. Group 39, 19–37. doi:10.1007/s11187-010-9290-7

Feldman, M. P., and Kelley, M. R. (2006). The ex ante assessment of knowledge spillovers: Government R&D policy, economic incentives and private firm behavior. Res. Policy 35, 1509–1521. doi:10.1016/j.respol.2006.09.019

Flor, M. L., and Oltra, M. J. (2004). Identification of innovating firms through technological innovation indicators: An application to the Spanish ceramic tile industry. Res. Policy 33, 323–336. doi:10.1016/j.respol.2003.09.009

Gibbons, R., and Murphy, K. J. (1992). Optimal incentive contracts in the presence of career concerns: Theory and evidence. J. Polit. Econ. 100, 468–505. doi:10.1086/261826

Hao, Y., Fan, C., Long, Y., and Pan, J. (2019). The role of returnee executives in improving green innovation performance of Chinese manufacturing enterprises: Implications for sustainable development strategy. Bus. Strategy Environ. 28, 804–818. doi:10.1002/bse.2282

Holmstrom, B. (1989). Agency costs and innovation. J. Econ. Behav. Organ. 12, 305–327. doi:10.1016/0167-2681(89)90025-5

Hu, T. S. (2008). Interaction among high-tech talent and its impact on innovation performance: A comparison of Taiwanese science parks at different stages of development. Eur. Plan. Stud. 16, 163–187. doi:10.1080/09654310701814462

Huang, S., Ding, D., and Chen, Z. (2014). Entrepreneurial leadership and performance in Chinese new ventures: A moderated mediation model of exploratory innovation, exploitative innovation and environmental dynamism. Creativity Innovation Manag. 23, 453–471. doi:10.1111/caim.12085

Jacob, J., and Subba, B. B. (2022). Towards exceptionalism: The communist party of China and its uses of history. China Rep. 58, 7–27. doi:10.1177/00094455221074169

Jensen, M. C., and Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 3, 305–360. doi:10.1016/0304-405X(76)90026-X

Jiang, X., Fu, W., and Li, G. (2020). Can the improvement of living environment stimulate urban Innovation. J. Clean. Prod. 255, 120212. doi:10.1016/j.jclepro.2020.120212

Jin, X., Zhang, M., Sun, G., and Cui, L. (2022). The impact of COVID-19 on firm innovation: Evidence from Chinese listed companies. Financ. Res. Lett. 45, 102133. doi:10.1016/j.frl.2021.102133

Jourdan, J., and Kivleniece, I. (2017). Too much of a good thing? The dual effect of public sponsorship on organizational performance. Acad. Manage. J. 60, 55–77. doi:10.5465/amj.2014.1007

Khalili, S., Rantanen, E., Bogdanov, D., and Breyer, C. (2019). Global transportation demand development with impacts on the energy demand and greenhouse gas emissions in a climate-constrained world. Energies 12, 3870. doi:10.3390/en12203870

Kleer, R. (2010). Government R&D subsidies as a signal for private investors. Res. Policy 39, 1361–1374. doi:10.1016/j.respol.2010.08.001

Lerner, J., and Wulf, J. (2007). Innovation and incentives: Evidence from corporate R&D. Rev. Econ. Stat. 89, 634–644. doi:10.1162/rest.89.4.634

Lewin, A. Y., Massini, S., and Peeters, C. (2009). Why are companies offshoring innovation? The emerging global race for talent. J. Int. Bus. Stud. 40, 901–925. doi:10.1057/jibs.2008.92

Li, L., Chen, J., Gao, H., and Xie, L. (2019). The certification effect of government R&D subsidies on innovative entrepreneurial firms’ access to bank finance: Evidence from China. Small Bus. Econ. Group 52, 241–259. doi:10.1007/s11187-018-0024-6

Lin, C., Lin, P., Song, F. M., and Li, C. (2011). Managerial incentives, CEO characteristics and corporate innovation in China’s private sector. J. Comp. Econ. 39, 176–190. doi:10.1016/j.jce.2009.12.001

Lo, T., and Pan, S. (2021). The internationalisation of China’s higher education: Soft power with “Chinese characteristics. Comp. Educ. 57, 227–246. doi:10.1080/03050068.2020.1812235

Lui, A. K., Ngai, E. W., and Lo, C. K. (2016). Disruptive information technology innovations and the cost of equity capital: The moderating effect of CEO incentives and institutional pressures. Inf. Manag. 53, 345–354. doi:10.1016/j.im.2015.09.009

Mehran, H. (1992). Executive incentive plans, corporate control, and capital structure. J. Financial Quantitative Analysis 27, 539–560. doi:10.2307/2331139

Meuleman, M., and De Maeseneire, W. (2012). Do R&D subsidies affect SMEs’ access to external financing? Res. Policy 41, 580–591. doi:10.1016/j.respol.2012.01.001

Miao, L., Zheng, J., Jean, J. A., and Lu, Y. (1978-2020). China’s international talent policy (ITP): The changes and driving forces. J. Contemp. China 31, 1985843. doi:10.1080/10670564.2021.1985843

Newton, M. A., and Raftery, A. E. (1994). Approximate Bayesian inference with the weighted likelihood bootstrap. J. R. Stat. Soc. Ser. B 56, 3–26. doi:10.1111/j.2517-6161.1994.tb01956.x

Peter, H. (1999). Steady endogenous Growth with population and R&D inputs growing. J. Polit. Econ. 107, 715–730. doi:10.1086/250076

Rao, H., and Drazin, R. (2002). Overcoming resource constraints on product innovation by recruiting talent from rivals: A study of the mutual fund industry, 1986–1994. Acad. Manage. J. 45, 491–507. doi:10.5465/3069377

Sarfraz, M., He, B., and Shah, S. G. M. (2020). Elucidating the effectiveness of cognitive CEO on corporate environmental performance: The mediating role of corporate innovation. Environ. Sci. Pollut. Res. 27, 45938–45948. doi:10.1007/s11356-020-10496-7

Sein, Y. Y., and Prokop, V. (2021). Mediating role of firm R&D in creating product and process innovation: Empirical evidence from Norway. Economies 9, 56. doi:10.3390/economies9020056

Shao, D., Zhao, S., Wang, S., and Jiang, H. (2020). Impact of CEOs’ academic work experience on firms’ innovation output and performance: Evidence from Chinese listed companies. Sustainability 12, 7442. doi:10.3390/su12187442

Shao, Y., and Chen, Z. (2022). Can government subsidies promote the green technology innovation transformation? Evidence from Chinese listed companies. Econ. Analysis Policy 74, 716–727. doi:10.1016/j.eap.2022.03.020

Shapiro, D., Tang, Y., Wang, M., and Zhang, W. (2017). Monetary incentives and innovation in Chinese SMEs. Asian Bus. manage. 16, 130–157. doi:10.1057/s41291-017-0017-3

Shi, J., Jo, L., Hu, M., and Li, J. (2018). The dynamics and macro strategy of structural reform in higher education in China: Case study of two critical periods (1949–1960 and 1998–2009). Front. Educ. China 13, 245–266. doi:10.1007/s11516-018-0013-1

Si, K., Xu, X. L., and Chen, H. H. (2020). Examining the interactive endogeneity relationship between R&D investment and financially sustainable performance: Comparison from different types of energy enterprises. Energies 13, 2332. doi:10.3390/en13092332

Sun, H., Edziah, B. K., Sun, C., and Kporsu, A. K. (2019). Institutional quality, green innovation and energy efficiency. Energy policy 135, 111002. doi:10.1016/j.enpol.2019.111002

Sun, H., Pofoura, A. K., Mensah, I. A., Li, L., and Moshin, M. (2020). The role of environmental entrepreneurship for sustainable development: Evidence from 35 countries in sub- saharan africa. Sci. Total Environ. 741, 140132. doi:10.1016/j.scitotenv.2020.140132

Sun, Z., Wang, X., Liang, C., Cao, F., and Wang, L. (2021). The impact of heterogeneous environmental regulation on innovation of high-tech enterprises in China: Mediating and interaction effect. Environ. Sci. Pollut. Res. 28, 8323–8336. doi:10.1007/s11356-020-11225-w

Sun, H., Edziah, B. K., Sun, C., and Kporsu, A. K. (2021). Institutional quality and its spatial spillover effects on energy efficiency. Socio-Economic Plan. Sci. 83, 101023. doi:10.1016/j.seps.2021.101023

Sun, H., Edziah, B. K., Kporsu, A. K., Sarkodie, S. A., and Taghizadeh-Hesary, F. (2021). Energy efficiency: The role of technological innovation and knowledge spillover. Technol. Forecast. Soc. Change 167, 120659. doi:10.1016/j.techfore.2021.120659

Tosi, H. L., Werner, S., Katz, J. P., and Gomez-Mejia, L. R. (2000). How much does performance matter? A meta-analysis of ceo pay studies. J. Manag. 26, 301–339. doi:10.1177/014920630002600207

Ullah, S., Khan, F. U., Cismaș, L.-M., Usman, M., and Miculescu, A. (2022). Do tournament incentives matter for CEOs to Be environmentally responsible? Evidence from Chinese listed companies. Int. J. Environ. Res. Public Health 19, 470. doi:10.3390/ijerph19010470

Wang, Y., Stuart, T., and Li, J. (2021). Fraud and innovation. Adm. Sci. Q. 66, 267–297. doi:10.1177/0001839220927350

Wang, P., Bu, H., and Liu, F. (2022). Internal control and enterprise green innovation. Energies 15, 2193. doi:10.3390/en15062193

Wei, J., and Zuo, Y. (2018). The certification effect of R&D subsidies from the central and local governments: Evidence from China. R&D Manag. 48, 615–626. doi:10.1111/radm.12333

Wu, A. (2017). The signal effect of government R&D subsidies in China: Does ownership matter? Technol. Forecast. Soc. Change 117, 339–345. doi:10.1016/j.techfore.2016.08.033

Xu, X. L., Chen, H. H., Li, Y., and Chen, Q. X. (2019). The role of equity balance and executive stock ownership in the innovation efficiency of renewable energy enterprises. J. Renew. Sustain. Energy 11, 055901. doi:10.1063/1.5116849

Yang, L., Xu, C., and Wan, G. (2019). Exploring the impact of TMTs’ overseas experiences on innovation performance of Chinese enterprises: The mediating effects of R&D strategic decision-making. Chin. Manag. Stud. 13, 1044–1085. doi:10.1108/CMS-12-2018-0791

Yang, Z., and Pan, Y. (2020). Human capital, housing prices, and regional economic development: Will “vying for talent” through policy succeed? Cities 98, 102577. doi:10.1016/j.cities.2019.102577

Yue, M., Li, R., Ou, G., Wu, X., and Ma, T. (2020). An exploration on the flow of leading research talents in China: From the perspective of distinguished young scholars. Scientometrics 125, 1559–1574. doi:10.1007/s11192-020-03562-x

Zhao, S., Zhang, B., Shao, D., and Wang, S. (2021). Can top management teams’ academic experience promote green innovation output: Evidence from Chinese enterprises. Sustainability 13, 11453. doi:10.3390/su132011453

Zheng, W., Shen, R., Zhong, W., and Lu, J. (2020). CEO values, firm long-term orientation, and firm innovation: Evidence from Chinese manufacturing firms. Manag. Organ. Rev. 16, 69–106. doi:10.1017/mor.2019.43

Zhou, M., Chen, F., and Chen, Z. (2021). Can CEO education promote environmental innovation: Evidence from Chinese enterprises. J. Clean. Prod. 297, 126725. doi:10.1016/j.jclepro.2021.126725

Zhu, X., Zuo, X., and Li, H. (2021). The dual effects of heterogeneous environmental regulation on the technological innovation of Chinese steel enterprises—based on a high-dimensional fixed effects model. Ecol. Econ. 188, 107113. doi:10.1016/j.ecolecon.2021.107113

Keywords: enterprise green technological innovation, executive incentive, talent policy, China A-shares listed companies, innovation-driven development strategy

Citation: Zhang Y-B, Qu S-Y, Li H-B and Li M-M (2022) An empirical analysis of talent policy, executive incentive, and enterprise green technological innovation based on China’s A-share listed companies. Front. Environ. Sci. 10:952057. doi: 10.3389/fenvs.2022.952057

Received: 24 May 2022; Accepted: 24 August 2022;

Published: 12 September 2022.

Edited by:

Huaping Sun, Jiangsu University, ChinaReviewed by:

Fanxin Meng, Beijing Normal University, ChinaCopyright © 2022 Zhang, Qu, Li and Li. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Yuan-Bo Zhang, emh5YjMzM0AxNjMuY29t; Shi-You Qu, cXVzaGl5b3VAaGl0LmVkdS5jbg==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.