Qingzhen Yao

Qingzhen Yao Liangshan Shao1,2

Liangshan Shao1,2

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 29 September 2022

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.916352

This article is part of the Research TopicCircular Economy Business Models for Sustainable ProductionView all 5 articles

Implementing low-carbon houses is inseparable from the carbon tax and subsidy policies. Appropriate carbon taxes and subsidies can help to reduce household carbon emissions. This study aims to identify a suitable carbon tax and subsidy policy and investigate how this policy will affect the adoption of low-carbon housing. We classify programs including carbon taxes and subsidies into four categories: static carbon tax static subsidy, static carbon tax dynamic subsidy, dynamic carbon tax dynamic subsidy, and dynamic carbon tax static subsidy. Additionally, under various carbon tax and subsidy systems, the evolutionary stability strategies (ESS) of real estate developers and governments will be examined using evolutionary game theory. The case simulation results show that static carbon tax and dynamic subsidies are the best strategies. Government regulation is essential for the implementation of low-carbon housing. The higher the carbon tax and the property developer’s profit, the higher the willingness of property developers to implement low-carbon houses and the higher the willingness of government regulation. Appropriate low-carbon subsidies will help property developers implement low-carbon houses. However, after reaching a certain point, low-carbon subsidies will make property developers less inclined to build low-carbon houses. The higher the cost of government regulation, the lower the probability of the low-carbon strategy of property developers, but the cost of government regulation has little impact on the government’s regulation strategy.

China’s building energy consumption is nearly 900 million tons of standard coal (China Building Energy Conservation Association, 2019a). The average annual growth rate of urban residential power consumption from 2009 to 2018 was 11.9 percent, according to the “China Statistical Yearbook” (National Bureau of Statistics of china, 2020). It nonetheless showed a pattern of rapid expansion. Therefore, there is an urgent need to use low-carbon housing to reduce carbon emissions. Low carbon housing can minimize carbon dioxide emissions in the life cycle and provide appropriate comfort for residents (Shen and Li., 2011).

However, there is a pressing need to find a solution for how to direct real estate developers to implement low-carbon houses actively. The use of carbon trading, carbon taxes, and carbon quotas to encourage businesses to make reasonable emissions reductions is widespread globally. On 16 July 2021, China officially opened its national carbon trading market. However, carbon trading can only direct businesses to decrease emissions proactively under the joint action of the competition mechanism and the market supply and demand mechanism. As a result, it can only rely on carbon pricing to cut emissions (Shen, 2021). The carbon tax is typically viewed as an effective market-based approach in the face of the climate change challenge. In the worldwide community, it has received much attention and utilization (Liu, 2022). Thirty-five nations (regions) have implemented carbon taxes, with eight local and 27 national carbon tax programs. The carbon tax is expected to cover 2.99 billion tons of carbon equivalent globally in 2021, accounting for 5.5% of greenhouse gas emissions (Lu and Bai., 2021).

The carbon tax is levied on greenhouse gas emissions such as carbon dioxide from fossil fuel consumption, and it is an effective tool to internalize pollution externalities (Wang et al., 2016). The “double dividend” of the carbon tax has become an essential theoretical basis for countries to promote environmental tax reform (Pearce., 1991). The first carbon tax dividend is an environmental dividend to raise the price of carbon-containing energy, reduce the demand for high carbon energy, improve energy efficiency, and accelerate the development and utilization of clean energy to reduce carbon dioxide emissions. The second dividend is social welfare which lowers other tax rates while imposing a carbon tax or raises transfer payments to citizens and businesses to lessen the burdensome tax burden of skewed taxes like income tax and enhance social welfare (Lu and Bai., 2021). The carbon tax will have a particular impact on China’s GDP and consumption. The level of impact on the economy varies on the carbon tax rate, but the financial harm brought on by its adoption is minor, and the benefit of reducing carbon emissions is discernible (Liu and Li., 2011; Liu and Lu., 2015; Weng et al., 2018; Lu et al., 2010; Orlov and Grethe., 2012; Chen et al., 2015; Allan et al., 2014; Wang et al., 2005). Subsidies in the context of carbon trading are conducive to helping carbon emission reduction, and appropriate high tax rates are conducive to sustainable development of the environment (Li and Yang., 2019); Implementing carbon tax policies in the area of automobile emission reduction can increase the equity of people’ income distribution while simultaneously reducing carbon emissions (Li and Wang, 2016); The government’s effective and active carbon tax policy can direct businesses and consumers to actively cut emissions in the game between the government and firms (Liu and Dong, 2022); Freire-Gonzalez and Ho. (2019) used a dynamic CGE model to simulate the environmental and economic effects of three different carbon tax price schemes in Spain, and found that controlling the carbon tax price within €10 can achieve a “double dividend” of carbon tax policy; An economic optimization model is employed in the context of Chile’s carbon tax policy to simulate the effects of various taxes on the emission of various air pollutants, and it is suggested to further broaden the carbon tax’s area of application to maximize its impact (Mardones and Cabello., 2019); Concerning Brazil’s carbon tax, compensation mechanisms are critical in the context of a complex tax system and can effectively reduce the economic burden of low-income households (Moz Christofoletti and Pereda, 2021).

Enterprise investment in low-carbon emission reduction will dampen enterprise enthusiasm for reducing carbon emissions. As a result, the government must implement various preferential policies to compensate enterprises for the costs of carbon emission reduction activities, such as tax breaks, subsidies, government priority procurement, etc. Subsidies are recognized as effective policies among them (Fogarty and Sagerer., 2016). Subsidy policies, according to the subsidy objects, can be divided into subsidies for manufacturers upstream of the supply chain and subsidies for consumers downstream of the supply chain, and these two subsidy strategies are beneficial to increasing supply chain members’ profits and the greenness of products (Wen et al., 2018). Carbon trading does not always improve manufacturer profits, and low-carbon subsidy policies can boost manufacturer profits (Cao et al., 2017). Low-carbon subsidies can effectively address the issue of insufficient funds for enterprise low-carbon technology research and development while also increasing enterprise enthusiasm for low-carbon technology innovation (Toshimitsu, 2010). Liu and Mu. (2016) investigated the impact of government low-carbon subsidies on supply chain decision-making and provided a theoretical foundation for government decision-making. Yi and Jinxi. (2018) established a Stackelberg game model to study the role of low-carbon subsidies in supply chains.

Consumers who are affected by low-carbon consumption and green technology innovation activities sometimes find it challenging to transform their low-carbon consumption willingness into practical low-carbon consumption behavior (Ma et al., 2013). Low-carbon subsidies, on the other hand, have efficient welfare protection, value compensation, and economic intervention: if firms’ low-carbon behavior provides larger environmental advantages without commensurate economic benefits, suitable financial compensations must be made (Zhu et al., 2019). From the standpoint of social behavior guidance, subsidies can direct economic entities to engage in desirable behaviors that benefit their own interests and long-term social growth (Wang et al., 2020). Many domestic and international parties have investigated carbon subsidy schemes recently, including South Korea’s green credit card system, Japan’s environmental protection point system, the Netherlands’ green point reward system, and China’s green point mechanism. According to the evidence presented above, carbon tax policies can effectively cut carbon emissions and improve social well-being.

Existing studies have examined the topic of reducing carbon emissions through carbon tax policy or subsidy policy, but what would happen if carbon tax and subsidy policy were combined? On the other hand, carbon tax measures should be handled differently in different industries. The residential building industry has significant potential for reducing carbon emissions, and carbon trading regimes can successfully support the development of low-carbon housing (Yao and Sho, 2022). However, few academics have studied carbon taxes in the residential construction business. Therefore, this paper aims to analyze the carbon tax and subsidy policy in the sector of residential development and attempt to solve the following issues:

• Among the various forms of the carbon tax and carbon emission reduction subsidies, which form can most effectively achieve carbon emission reduction.

• Does the carbon tax and subsidy policy have a positive guiding effect on implementing low-carbon housing? How should we understand this guidance mechanism?

• What are the implications of carbon tax rates, regulatory costs, and subsidies on reducing carbon emissions?

Evolutionary game theory is a popular tool for studying the interactions of multi-agent agents. By recreating the dynamic mechanism under the premise of constrained rationality, evolutionary game theory may well portray the process of each game party gradually learning and eventually attaining equilibrium (Friedman, 1998). Traditional classical game theory differs from evolutionary game theory. It blends the concepts of evolution with game theory. The concept of evolution originated in the science of biology. Darwin believed that the evolution of the biological world is a continuous process. The theory of evolutionary economics, which emerged at the end of the 20th century, attempts to transform Darwin’s biological process of “variation, selection, and inheritance” into a process of “innovation, selection, and dissemination.”

In the evolutionary game, both sides gradually explore the evolutionary stable strategy (ESS) through continual comparison, learning, and imitation, rather than the stable Nash equilibrium as the final option structure of the strategy. The key to distinguishing evolutionary game theory from conventional game theory is that it advocates that the decision-making of game participants is made under the condition of restricted rationality. It abandons the assumption that conventional game theory is entirely rational and enables researchers to use evolutionary game theory to be more scientific (Friedman, 1998). China is experimenting with a carbon price and subsidy scheme. The government and real estate developers’ understanding of carbon tax and subsidy is constantly changing, so the strategies adopted are also being adjusted dynamically. As the game’s significant actors, the government and real estate developers will choose the best approach to maximize their interests.

When a group develops tactics, most participants will select strategies that maximize their interests. Individuals will eventually pick behavioral strategies that follow the same path since they share common interests. In the case of the carbon tax and subsidy policies, some real estate developers would rather pay a carbon tax than build low-carbon housing. However, when they discovered that other real estate developers were encouraged by the government to build low-carbon housing and receive government subsidies, they decided to build low-carbon housing as well. This is a classic bounded rationality behavior, the outcome of ongoing learning and imitation of other group members.

Building energy consumption is the world’s second-largest energy consumption sector, accounting for roughly 40% of worldwide energy consumption. Residential building energy consumption accounts for three-quarters of worldwide building energy consumption, consumes 27 percent of the world’s final energy in operation, and emits 17 percent of carbon dioxide (International Energy Agency, 2008). As a result, residential buildings are a major source of carbon reduction. China’s residential construction business is growing in size. The year-on-year rise in completion area causes China’s stock of residential construction areas to outgrow. In 2015, China’s urban residential construction area was 21.9 billion square meters, while rural residential was 23.8 billion square meters (Building Energy Efficiency Research Center of Tsinghua University’s, 2017). Residential building energy usage in China accounts for 13% of total national energy consumption during the operation cycle. Carbon emissions account for 12.1 percent of national energy carbon emissions (China Building Energy Conservation Association, 2019b), including energy consumption of urban heating in northern cities (for residential buildings) and energy consumption of urban residential buildings (excluding heating in northern cities). Without adequate policy intervention, the residential building sector will likely become a bottleneck for China’s energy conservation and emission reduction, hindering the smooth realization of the nationally determined contribution emission reduction target (Building Energy Efficiency Research Center of Tsinghua University’s, 2017). There is significant space for improvement in energy efficiency on both the energy consumption and supply sides of residential buildings, and the residential building sector will continue to be an essential driving factor for energy conservation and emission reduction for a long time to come (Zhou et al., 2018; Zheng et al., 2014). Residential building carbon emissions in the operating phase account for more than 80% of total life cycle carbon emissions (Li et al., 2021). Low carbon residential buildings focus on minimizing carbon emissions during the operational phase. However, at present, Chinese property developers tend to consider the cost and profit while ignoring the low-carbon attributes of residential buildings. The government hopes that property developers can improve the low carbon content of residential buildings through innovation. Property developers and the government will adapt to each other’s strategic decisions to pursue their best interests. As a result, whether low-carbon technology are used to produce low-carbon residential buildings is a game played by the government and property developers.

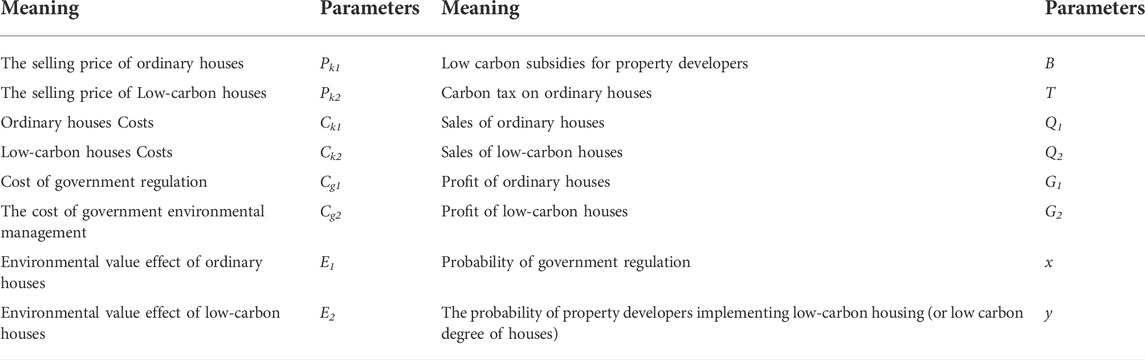

We assume that property developers and the government are both restricted economic persons. The methods of property developers and the government were not optimal at first due to insufficient information. However, through trial and error, they eventually discovered the ideal strategy. We divide residential buildings into ordinary houses and low-carbon houses. Ordinary houses are priced at Pk1, whereas low-carbon houses are priced at Pk2. The cost of ordinary houses is Ck1, and the cost of low-carbon houses is Ck2. The cost of government control is Cg1, and the remediation cost due to carbon emissions from ordinary houses is Cg2. The environmental value of ordinary houses is E1, and the environmental value effect of low-carbon houses is E2. The government’s low-carbon subsidy to property developers is B, and the carbon tax levied on ordinary houses is T. The government has the option of regulating or not regulating the behavior of property developers, and the strategic space is (regulated, not regulated). The likelihood of regulation by the construction government is x (

TABLE 1. Details of main variables.

The carbon tax and subsidy models are classified into four types based on the assumptions stated above:1 static carbon tax, static subsidies; 2 static carbon tax, dynamic subsidies; 3 dynamic carbon tax, dynamic subsidies; 3 dynamic carbon tax, static subsidies.

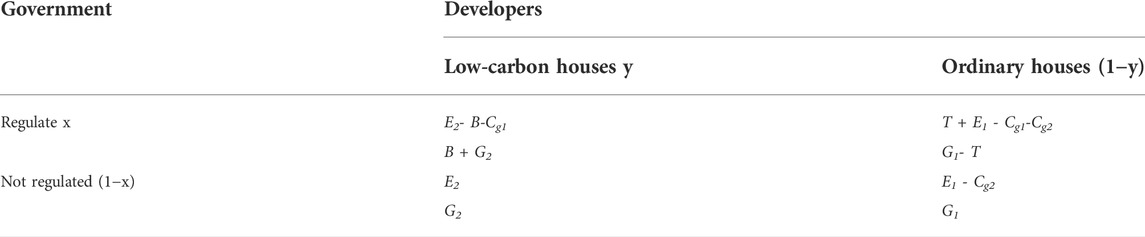

In this case, the government formulates low-carbon housing criteria, and those that do not meet the standards are considered ordinary houses. Under the premise of government supervision, low-carbon houses will be subsidized, and a carbon tax will be levied on ordinary houses. The game pay-off matrix is shown in Table 2.

TABLE 2. Game pay-off matrix.

Expected benefits of property developers not implementing low-carbon housing:

Expected benefits of property developers implementing low-carbon housing:

Average income for property developers:

Expected benefits of government regulation:

Expected benefits of government without regulation:

The average revenue for the government:

The replication dynamic equation of government regulation and property developers implementing low-carbon houses is:

Let F(x) = 0, F(y) = 0,get:

The solution of the equations is (0,0), (1,0), (1,0), (1,1),

Jacobian matrix:

When the equilibrium point satisfies

• Equilibrium (0,0)

When

The final strategic of the government and property developers is (Not regulated, Ordinary houses).

• Equilibrium (1,0)

a: When

The final strategic of the government and property developers is (Regulated, Ordinary houses).b: When

The final strategic of the government and property developers is (Regulated, Ordinary houses).

• Equilibrium (1,1)

When

The final strategic of the government and property developers is (Regulated, Low-carbon houses).

• Equilibrium (0,1)

When

The final strategic of the government and property developers is (Not Regulae, Low-carbon houses).

• Equilibrium

In this case, the government formulates low-carbon housing standards, and those that are not standards-compliant are ordinary residences. Under the supervision of the government, the government will subsidize low-carbon houses and levy a carbon tax on ordinary houses based on low-carbon degrees. Substituting T in Eqs. 5, 6 with

Let F(x)=0, F(y)=0,get:

The equilibrium points are (0,0), (1,0), (1,0), (1,1) and

• Equilibrium (0,0)

When

• Equilibrium (0,1)

When

• Equilibrium (1,1)

In this case,

• Equilibrium (1,0)

When

• Equilibrium

In this case,

In this case, the government dynamically levies carbon taxes and dynamic low-carbon subsidies according to the low-carbon level of residences. The carbon tax levied by the government is

Let

The Equilibrium points are (0,0), (1,0), (1,0), (1,1) and

• Equilibrium (0,0)

When

• Equilibrium (0,1)

When

• Equilibrium (1,1)

In this case,

• Equilibrium (1,0)

When

• Equilibrium

In this case,

In this situation, the government develops low-carbon house criteria, and those that do not meet the standards are considered ordinary houses. Subsidies will be paid based on the low-carbon degree, and a carbon tax will be levied on ordinary houses under the supervision of the government. The carbon tax levied is yB. Substituting B in Eqs. 5, 6 with yB, we get the replicator dynamic equation for the static carbon tax and dynamic subsidy case:

Let F(x)=0, F(y)=0,get:

The Equilibrium points are (0,0), (1,0), (1,0), (1,1)and .

• Equilibrium (0,0)

When

• Equilibrium (1,0)

When

• Equilibrium (0,1)

When

• Equilibrium (1,1)

In this case,

• Equilibrium

In this case,

In 2020, the average sales price of commercial houses in China was 9860 ¥/m2 (National Bureau of Statistics, 2021), and the profit of ordinary housing was 986 ¥/m2 according to a profit margin of 10%. Because of the higher cost of low-carbon buildings, the high selling price may lower profits for low-carbon houses than ordinary houses (Li and Hao., 2014). It is assumed that the profit of low-carbon houses is 5% lower than that of ordinary houses, that is, 936 ¥/m2.

Since there is no subsidy for low-carbon houses in China, the initial low-carbon subsidy is assumed to be 100 ¥/m2, and the initial value of government supervision cost (Cg1) is 10 ¥/m2.

China has not established a carbon price, although the number of countries and areas that have done so has risen to 29 (ICAP.2019). Each country has its carbon tax structure and price. European countries have high tax rates, and developing countries have low tax rates. Sweden, for example, charges 127 $/tCO2, while developing countries charge between 4 and 8 $. (Zheng, 2019). Considering that China is a developing country, the initial price of the carbon tax is 40 yuan (6.3$). The carbon emission of ordinary houses in the life cycle is about 45 Kg CO2/(m2. year) (Mao, 2018). Calculated according to the 50-year service cycle, the carbon emissions generated by the life cycle of ordinary houses are 2.25 tCO2/m2, so the initial carbon emission tax positioning is 110 ¥/m2.

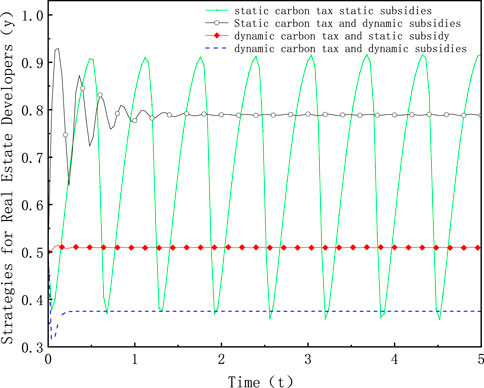

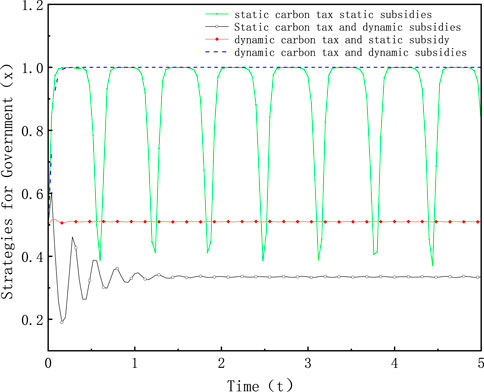

The evolution of property developers’ strategy options under four situations are depicted in Figure 1: static carbon tax and static subsidies, static carbon tax and dynamic subsidies, dynamic carbon tax and static subsidies, and dynamic carbon tax and dynamic subsidies. In the case of the static carbon tax and static subsidies, the strategy choice of property developers continues to fluctuate and is the most unstable. In the case of the dynamic carbon tax and dynamic subsidies, property developers’ low-carbon strategy value is stable at roughly 0.509. The property developer’s strategy value is consistent at roughly 0.375 in the case of the dynamic carbon tax and dynamic subsidies. The strategic value of property developers remained consistent at roughly 0.790 in the case of the static carbon tax and dynamic subsidies. As a result, the government’s strategy of adopting a static carbon tax and dynamic subsidies can more effectively support low-carbon houses development. Figure 2 depicts the government’s strategic decisions. The government’s supervision strategy is unstable in the event of the static carbon tax and static subsidies. When property developers are unwilling to implement low-carbon houses, the government’s willingness to supervise is powerful. However, when developers were eager to build low-carbon houses, the government’s willingness to regulate declined precipitously. The government’s regulatory strategy eventually converges to 1 in the case of the dynamic carbon tax and dynamic subsidies. In the case of the static carbon tax and dynamic subsidies, the government’s regulatory strategy gradually stabilized around 0.335. In the case of the dynamic carbon tax and static subsidies, the government’s regulatory strategy gradually stabilizes around 0.510. As shown in Figures 1, 2, the advantages of the static carbon tax and dynamic subsidy policy are more apparent than the other three policies.

FIGURE 1. The strategy evolution process of property developers.

FIGURE 2. The strategy evolution process of government.

The static carbon tax and dynamic subsidy are the best policies among the four, and we will use this strategy as the research object in the following study.

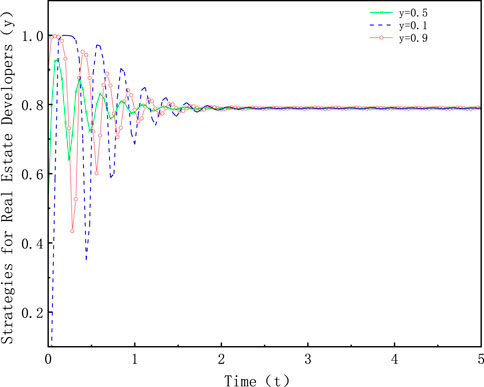

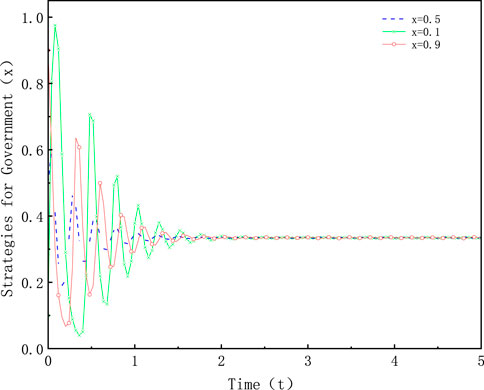

In the case of the static carbon tax and dynamic subsidies, changing the initial strategy value of government supervision of property developers (y = 0.1, y = 0.5, y = 0.9; x = 0.1, x = 0.5, x = 0.9), the evolution process of property developers and government strategies is shown in Figure 3 and Figure 4. Figures 3, 4 show that differing initial strategy settings have no effect on the end evolution results. The low-carbon strategy values of property developers are all stable at around 0.790; The government supervision strategy values are stable at around 0.375.

FIGURE 3. Strategies evolution of property developers under different initial values.

FIGURE 4. Strategies evolution of government under different initial values.

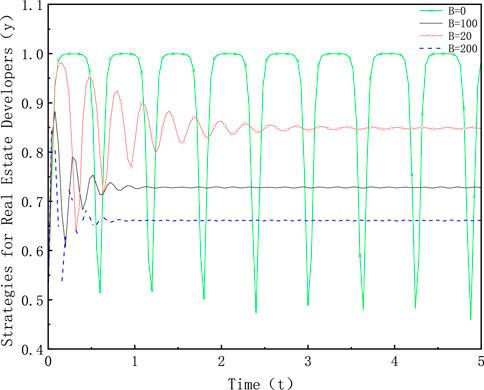

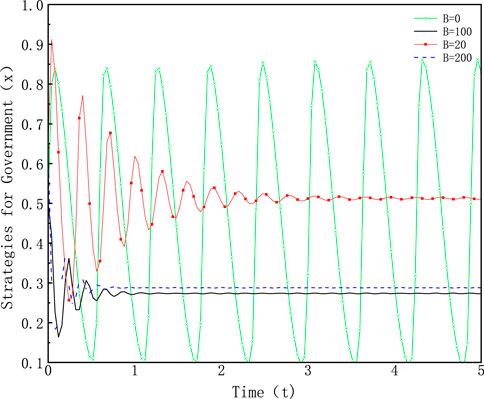

The low-carbon subsidies (B) were altered (B = 0, B = 20, B = 100, B = 200) to investigate the impact of low-carbon subsidies on the strategic choices of property developers and the government, and the strategies of property developers and the government followed the changes in B. Figures 5, 6 depict the evolution process. When the low-carbon subsidy is zero, property developers and the government’s strategies become unstable. In this case, the government’s strong supervision strategy can prompt property developers to implement low-carbon strategies. In the case of B = 20, B = 100, and B = 200, the low-carbon strategy of property developers and the government’s regulation strategy will finally stabilize. Compared with lower low-carbon subsidies, higher low-carbon subsidies can shorten the evolutionary stability; the higher the low-carbon subsidies, the higher the evolutionary stability value of property developers’ low-carbon strategies, and the lower the evolutionary stability value of government supervision strategies. The greater the government’s low-carbon subsidies, the less likely property developers will implement low-carbon houses.

FIGURE 5. Strategies evolution of property developers under different subsidies.

FIGURE 6. Strategies evolution of government under different subsidies.

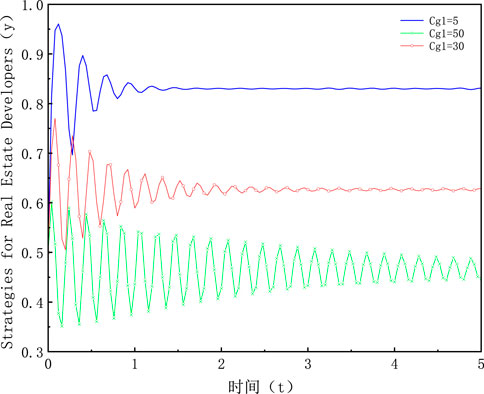

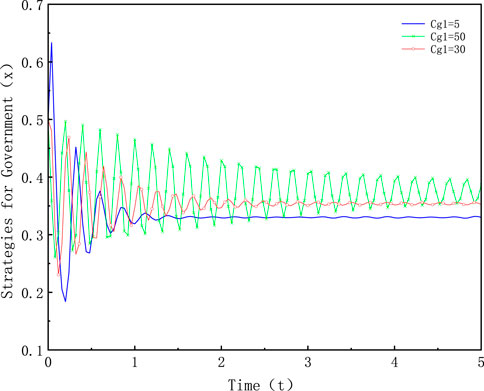

Change the government regulation cost (Cg1) (Cg1 = 5, Cg1 = 30, Cg1 = 50) to investigate the impact of government regulation cost (Cg1) on property developers and government strategies. Figures 7, 8 depict the strategy evolution process of property developers and the government. Property developers’ and the government’s strategies have become increasingly unstable as government supervision costs have risen. The higher the cost of government regulation, the lower the level of property developers’ low-carbon strategy. The cost of government supervision has little influence on the strategy chosen by the government, and the government’s supervision strategy is constant at roughly 0.35.

FIGURE 7. Strategies evolution of property developers under different Cg1.

FIGURE 8. Strategies evolution of government under different Cg1.

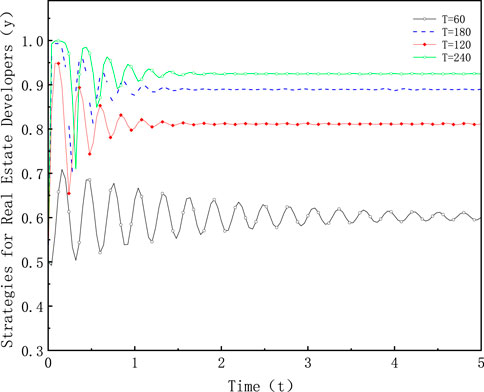

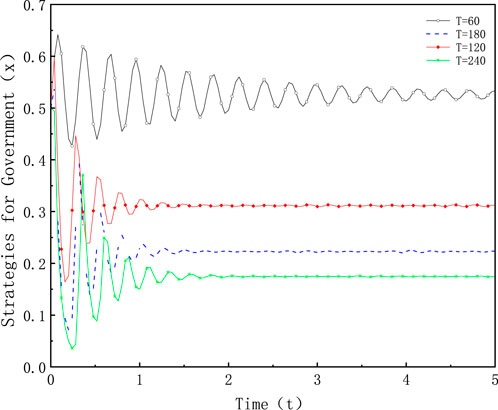

Change the carbon tax (T) to investigate the influence on the strategies of property developers and the government (T = 60, T = 120, T = 180, T = 240). Figures 9, 10 depict the strategy evolution process of property developers and the government. When the carbon tax is high, the government’s supervision strategy is low, and property developers’ implementation of low-carbon housing is high. When the carbon tax is excessively high, the government’s and property developers’ strategies change dramatically in the early stages of the evolution process, causing the property industry to suffer greatly.

FIGURE 9. Strategies evolution of property developers under different T.

FIGURE 10. Strategies evolution of government under different T.

This research uses evolutionary game theory to assess the influence of various policies on the implementation of low-carbon houses and determines the optimum approach to encourage the development of low-carbon housing. It also examines the impact of tax rates, low-carbon subsidies, and regulatory costs on the low-carbon strategies of property developers and government regulatory strategies. To take on the burden of global carbon emission reduction, China has promised to strive for a peak in carbon emissions by 2030, a reduction in carbon intensity of more than 65 percent compared to 2005, and “carbon neutrality” by 2060. Carbon taxes and subsidies have been proved to be effective policies to promote carbon emission reduction (Weng et al., 2018; Lu et al., 2010; Orlov and Grethe, 2012). Carbon taxes and subsidies are required to meet China’s carbon emission reduction goals. As a result, this study can serve as a theoretical foundation for the Chinese government to establish a low-carbon houses policy. Policy differences have varying implications on the government’s and property developers’ strategies. The ideal method would be for property developers to construct low-carbon houses without government supervision or intervention. However, under the common-sense assumption, there is no ESS in the method described above in this study. Therefore, government regulation is the norm for property developers to implement low-carbon houses. To encourage the development of low-carbon houses, the government can implement the following four policies: static carbon tax static subsidy, dynamic carbon tax dynamic subsidy, static carbon tax dynamic subsidy, and dynamic carbon tax static subsidy. Among these four measures, the dynamic subsidy of static carbon tax proved to be the most effective policy. The static subsidy of static carbon tax proved to be the most ineffective strategy.

In the case of the optimal strategy, the upper limit of the strategy of property developers to implement low-carbon houses is 0.92 and eventually stabilizes around 0.790. Static carbon tax and static subsidies will not make property developers’ strategies of government supervision tend to be stable. Therefore, dynamic carbon tax subsidies are more effective than static carbon tax subsidies. However, the study found that the higher the low-carbon subsidy, the lower the strategy of property developers to implement low-carbon houses, which seems to be contrary to common sense. This situation can be explained as follows: the bigger the low-carbon subsidy, the better the chance for property developers to obtain subsidies through “fraud.” However, the low-carbon subsidy of 0 will make the low-carbon strategy of both property developers and the government unstable.

This study, however, has several drawbacks. First, low-carbon technology is a major element limiting property developers’ deployment of low-carbon houses, not merely economics. As a result, in addition to supervising property developers, the government should actively encourage the development of low-carbon technology. Second, the carbon tax and carbon subsidy strategies may face unexpected challenges during implementation, which are beyond the scope of this analysis.

Using evolutionary game theory, the evolution law of property developers and government strategies under different carbon tax policies and regulatory policies are studied. Concluded as follow:

• When the common-sense assumption is satisfied, the point (0,1) is not the stable point of the strategic evolution of both parties. Property developers will not take the initiative to implement low-carbon houses, and government regulation is the norm for property developers to implement low-carbon houses.

• Static carbon tax and dynamic subsidies are the most effective strategies. Under this strategy, the value of the government regulation strategy is lower (x = 0.375), while the willingness of property developers to implement low-carbon houses is higher (y = 0.790).

• The greater the carbon tax rate, subsidy, and property developer’s profit, the higher the property developer’s choice of low-carbon strategy, and the lower the government’s choice of supervision strategy. Appropriate low-carbon subsidies will help property developers implement low-carbon houses. However, when a certain threshold is exceeded, low-carbon subsidies will reduce the willingness of property developers to implement low-carbon houses. The higher the cost of government regulation, the lower the low-carbon strategy value of property developers, but the cost of government regulation has little effect on the government’s choice of regulation strategy.

This study can give the government and real estate developers enough information to formulate low-carbon strategies. Consumer preference for low-carbon houses also affects the implementation of low-carbon houses. Therefore, further research can aim to answer how the consumers’ preference promotes the development of low-carbon housing.

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

QY: Conceptualization (lead); writing-original draft (lead); formal analysis (lead); writing-review and editing (equal); LS: writing-review and editing (equal); software (lead). ZY, JW, and YL: Conceptualization (supporting); review and editing (equal).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Allan, G., Lecca, P., and Mcgregor, P., (2014). The economic and environmental impact of a carbon tax for scotland: A computable general equilibrium analysis[J]. Ecol. Econ. 100, 40–50. doi:10.1016/j.ecolecon.2014.01.012

Building energy efficiency research center of Tsinghua University (2017). Annual development research report on building energy efficiency in China[M]. Beijing: China Construction Industry Press.

Cao, K., Xu, X., Wu, Q., and Zhang, Q. (2017). Optimal production and carbon emission reduction level under cap-and-trade and low carbon subsidy policies[J]. J. Clean. Prod. 167 (20), 505–513. doi:10.1016/j.jclepro.2017.07.251

Chen, W., and Hu, Z. H. (2018). Using evolutionary game theory to study governments and manufacturers’ behavioral strategies under various carbon taxes and subsidies[J]. J. Clean. Prod. 201, 123–141. doi:10.1016/j.jclepro.2018.08.007

Chen, Z. M., Liu, Y., and Qin, P., (2015). Environmental externality of coal use in China: Welfare effect and tax regulation[J]. Appl. energy 156, 16–31. doi:10.1016/j.apenergy.2015.06.066

China Building Energy Conservation Association (2019a). China building energy consumption research report [J]. Architecture (2), 26–31.

China Building Energy Conservation Association (2019b). Research Report on building energy consumption in China[R]. Shanghai.

Fogarty, J. J., and Sagerer, S. (2016). Exploration externalities and government subsidies: The return to government. Resour. Policy 47. doi:10.1016/j.resourpol.2016.01.002

Freire-González, J., and Ho, M. S. (2019). Carbon taxes and the double dividend hypothesis in a recursive-dynamic CGE model for Spain[J]. Econ. Syst. Res. 31 (2), 267–284. doi:10.1080/09535314.2019.1568969

Friedman, D. (1998). On economic applications of evolutionary game theory[J]. J. Evol. Econ. 8 (1), 15–43. doi:10.1007/s001910050054

International Energy Agency (2008). Energy efficiency requirements in building codes, energy efficiency policies for new buildings[R]. Paris: IEA.

Li, D. D., and Yang, J,Y. (2019). Research on the optimal emission reduction technology selection of enterprises based on government subsidies [J]. China Manag. Sci. 27 (7), 177–185. doi:10.16381/j.cnki.issn1003-207x.2019.07.017

Li, F., and Wang, W. J. (2016). Fairness of levying carbon tax on household consumption -- Taking Automobile carbon tax as an example [J]. Econ. Manag. Res. 37 (12), 66–72. doi:10.13502/j.cnki.issn1000-7636.2016.12.008

Li, P. S., and Hao, S. Y. (2014). Cost-benefit analysis of low-carbon residential development: Taking Tianjin "Tuanbo Lake Island" project as an example [J]. Ecol. Econ. 30 (03), 109–112. doi:10.3969/j.issn.1671-4407.2014.03.025

Li, Y. Y., Zhang, K., and Li, J. L. (2021). Comparative analysis of life cycle carbon emissions of residential buildings and carbon reduction strategies [J]. J. Xi'an Univ. Archit. Technol. Nat. Sci. Ed. 53 (05), 737–745. doi:10.15986/j.1006-7930.2021.05.017

Liu, C., and Mu, J. (2016). Low carbon supply chain coordination under the condition of random demand and government subsidie[J]. Operations Res. Manag. 25 (04), 142–149. doi:10.12005/orms.2016.0134

Liu, J., and Li, W. (2011). Demonstration of the impact of carbon tax on China's economy[J]. China Popul. Resour. Environ. 21 (9), 99–104. doi:10.3969/j.issn.1002-2104.2011.09.017

Liu, Q. (2022). Theoretical basis and system construction of carbon tax under the goal of "double carbon" [J]. J. Huazhong Univ. Sci. Technol. Soc. Sci. Ed. 36 (02), 108–116. doi:10.19648/j.cnki.jhustss1980.2022.02.11

Liu, Y., and Dong, F. (2022). What are the roles of consumers, automobile production enterprises, and the government in theprocess of banning gasoline vehicles? Evidence from a tripartite evolutionary game model[J]. Energy 238, 122004. doi:10.1016/j.energy.2021.122004

Liu, Y., and Lu, Y. Y. (2015). The economic impact of different carbon tax revenue recycling schemes in China: A model-based scenario analysis [J]. Appl. energy 141 (1), 96–105. doi:10.1016/j.apenergy.2014.12.032

Lu, C. Y., Tong, Q., and Liu, X. M. (2010). The impacts of carbon tax and complementary policies on Chinese economy [J]. Energy policy 38 (11), 7278–7285. doi:10.1016/j.enpol.2010.07.055

Lu, S. L., and Bai, Y. F. (2021). International practice of carbon tax and its Enlightenment to China's goal of "reaching the peak of carbon" by 2030 [J]. Int. Tax. (12), 21–28. doi:10.19376/j.cnki.cn10-1142/f.2021.12.004

Ma, W. M., Zhao, Z., and Ke, H. (2013). Dual-channel closed-loop supply chain with government consumption-subsidy[J]. Eur. J. Operational Res. 226 (2), 221–227. doi:10.1016/j.ejor.2012.10.033

Mao, X. K. (2018). Research on prediction model of building life cycle carbon emissions[D]. Tianjin: Tianjin University. doi:10.27356/d.cnki.gtjdu.2018.001300

Mardones, C., and Cabello, M. (2019). Effectiveness of local air pollution and GHG taxes: The case of Chilean industrialsources[J]. Energy Econ. 83, 491–500. doi:10.1016/j.eneco.2019.08.007

Moz Christofoletti, M. A., and Pereda, P. C. (2021). Winners and losers: The distributional impacts of a carbon tax in Brazil [J]. Ecol. Econ. 183, 106945. doi:10.1016/j.ecolecon.2021.106945

National Bureau of Statistics of China (2020). China statistical Yearbook [M]. Beijing: China Statistics Press.

National Bureau of Statistics of China (2021). China statistical Yearbook [M]. Beijing: China Statistics Press.

Orlov, A., and Grethe, H. (2012). Carbon taxation and market structure: A CGE analysis for Russia[J]. Energy policy 51, 696–707. doi:10.1016/j.enpol.2012.09.012

Pearce, D. (1991). The role of carbon taxes in adjusting to global warming[J]. Econ. J. 101, 938–948. doi:10.2307/2233865

Shen, L. F., and Li, Q. M. (2011). “Research on the connotation of "low carbon housing" and the path of construction and development [J]. Mod. Manag. Sci. 31–33.10.0.2011-10-010.

Shen, X. Y. (2021). Carbon tax will be levied at the right time under the "double carbon" goal [J]. Explor. contention (09), 20–22.

Toshimitsu, T. (2010). On the paradoxical case of a consumer-based environmental subsidy policy[J]. Econ. Model. 27 (1), 159–164. doi:10.1016/j.econmod.2009.08.002

Wang, C., Chen, J. N., and Zou, J. (2005). Impact of CO2 emission reduction on China's economy based on CGL model [J].. J. Tsinghua Univ. Nat. Sci. Ed. 45 (12), 1621–1624. doi:10.3321/j.issn:1000-0054.2005.12.011

Wang, Q., Hubacek, K., and Feng, K. S. (2016). Distributional effects of carbon taxation[J]. Appl. Energy 184, 1123–1131. doi:10.1016/j.apenergy.2016.06.083

Wang, Y., Fan, R., Shen, L., and Miller, W. (2020). Recycling decisions of low-carbon e-commerce closed-loop supply chain under government subsidy mechanism and altruistic preference[J]. J. Clean. Prod. 259, 120883. doi:10.1016/j.jclepro.2020.12088

Weibull (2006). Evolutionary game theory [M]. Shanghai: Shanghai People's Publishing House, 40-48–88-93.

Wen, X., Cheng, H., Cai, J., Chao, L. U., and University, W. (2018). Government subside policies and effect analysis in green supply chain[J]. Chin. J. Manag. 15 (4), 625–632. CNKI:SUN:GLXB.0.2018-04-017.

Weng, Z. X., Ma, Z. Y., and Cai, S. F. (2018). “Research on the economic and environmental impact of China's carbon tax policy -- Based on the analysis of Dynamic CGE model [J]. China price (08) 10.13.0.2018-08-004.

Yao, Q. Z., and Shao, L. S. (2022). Research on emission reduction strategies of building materials manufacturers and property developers in the context of carbon trading[J]. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.84826010.1016/j.jclepro.2020.120883

Yi, Y., and Jinxi, L. (2018). Cost-sharing contracts for energy saving and emissions reduction of a supply chain under the conditions of government subsidies and a carbon tax[J]. Sustainability 10 (3), 895. doi:10.3390/su10030895

Zheng, S. (2019). The progress of international carbon price policy and its enlightenment to my country [J]. China Energy 41 (10), 33–37. CNKI:SUN:ZGLN.0.2019-10-007.

Zheng, X., Wei, C., and Qn, P. (2014). Characteristics of residential energy consumption in China: Findings from a household survey[J]. Energy Policy 75, 126–135. doi:10.1016/j.enpol.2014.07.016

Zhou, N., Khanna, N., and Feng, W. (2018). Scenarios of energy efficiency and CO2 emissions reduction potential in the buildings sector in China to year 2050[J]. Nat. Energy 3, 978–984. doi:10.1038/s41560-018-0253-6

Keywords: low-carbon houses, carbon tax, subsidies, evolutionary game, evolutionary stability strategies

Citation: Yao Q, Shao L, Yin Z, Wang J and Lan Y (2022) Strategies of property developers and governments under carbon tax and subsidies. Front. Environ. Sci. 10:916352. doi: 10.3389/fenvs.2022.916352

Received: 09 April 2022; Accepted: 12 August 2022;

Published: 29 September 2022.

Edited by:

Mariana Petrova, St. Cyril and St. Methodius University of Veliko Tarnovo, BulgariaReviewed by:

Xinzhu Zheng, China University of Petroleum, Beijing, ChinaCopyright © 2022 Yao, Shao, Yin, Wang and Lan. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Qingzhen Yao, eWFvYW8wMjEzQDEyNi5jb20=

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.