Yan Zhang1,2

Yan Zhang1,2 Chengfeng Zhuo

Chengfeng Zhuo- 1School of Economics and Management, Xinjiang University, Xinjiang, China

- 2School of Economics and Management, Shihezi University, Shihezi, China

- 3Institute of Guangdong, Hong Kong and Macao Development Studies, Sun Yat-Sen University, Guangzhou, China

Technological innovation is the core factor for enterprises to maintain competitiveness. This paper aims to investigate how policy uncertainty affect enterprises’ innovation. On the basis of theoretical analysis, this study selects data from 2008–2017- and a share of non-financial listed companies as the research sample. Using patent data of listed companies and China’s economic policy uncertainty (EPU) index, the study examines the impact of EPU on enterprise innovation. In addition, the regulatory effect of enterprise financialization has been investigated. The results show that the EPU can promote the quantity growth of enterprise innovation but inhibit the improvement of enterprise innovation quality. The impact of EPU on enterprise innovation will be affected by enterprise ownership, financing constraint level, life cycle, regional administrative level and regional economic level. Furthermore, enterprise financialization shows a negative regulatory effect in the process of EPU affecting enterprise innovation. This study provides policy enlightenment for reasonably formulating economic policies and promoting enterprise financialization, so as to effectively improve enterprise innovation ability and economic development.

1 Introduction

The COVID-19 pandemic has changed our lives in certain ways (Yang Zhen. et al., 2021; Elavarasan et al., 2021; Ahmad et al., 2022; Huang et al., 2022; Hussain et al., 2022; Wen et al., 2022). In this regard, economic policy is not only an important means for the state to regulate the economy and market, but also an important external condition for enterprises (Yumei et al., 2021; Tang et al., 2022). The frequent adjustment of economic policies by the government can stimulate the investment vitality of enterprises in the short term, but it will also make enterprises to face the uncertainty of the policy environment when making business decisions (Shi et al., 2022; Xiang et al., 2022). According to the global Economic Uncertainty Index data developed by Baker et al. (2016) and jointly released by Stanford University and The University of Chicago, the global EPU Index increased by about 200% from January 2014 to December 2020. The index in December 2020 was much higher than that during the 2008 financial crisis, reaching a record high. China’s EPU index was high during 2008–2009, 2011–2012 and 2016–2020. It is closely related to the changes of global economy, China’s economic development and many intensive economic policies of Chinese government.

At present, China’s economy has shifted from a stage of high-speed growth to a stage of high-quality development (Wu et al., 2021; Irfan and Ahmad 2022; Rauf et al., 2021). The Chinese government emphasizes that adhering to the core position of innovation in the overall modernization, deeply implementing the innovation driven development strategy and improving the technological innovation ability of enterprises (Hao et al., 2020; Hao et al., 2021; Abbasi et al., 2022). How to strengthen the dominant position of enterprises in scientific and technological innovation, improve the independent innovation ability of nation and enterprise, and promote high-quality economic development has become an urgent issue for China. However, finance, real estate and other industries in China have high profit margins compared with the traditional manufacturing industry. The profit seeking characteristics of capital urge enterprises to make a lot of financial investment, while lack enthusiasm for technological innovation and R&D activities. In this context, what impact does financialization have on enterprise innovation in the face of high EPU? Will this impact change with the differences of enterprise ownership, life cycle, financing constraints, regional administrative level and urban economic development? Obviously, the impact of EPU and financialization on enterprise innovation is still an issue worthy of investigation.

2 Literature Review

The existing research on EPU can be divided into two categories. One category of literature studies the impact of EPU on macroeconomic activities. The literatures discussed the impact of EPU on macroeconomic fluctuations, economic recovery, employment, productivity and so on (Caldara et al., 2016). Another category of literature investigates the impact of EPU on micro enterprises’ operation, R&D investment and other decision-making activities. The studies have found that when EPU is enhanced, enterprises’ cash holding level (Wang et al., 2014), commercial credit financing (Zhang et al., 2020), senior management change (Rao and Xu, 2017), R&D investment behavior (Li and Yang, 2015; Gulen and Ion, 2016; Bhattacharya et al., 2017), the level of financialization (Peng et al., 2018) and investment efficiency (Rao and Xu, 2017) will be affected.

For the impact of economic policy uncertainty on enterprise innovation, the existing literature has the opposite conclusion. Some literatures believe that enterprise R&D investment is positively correlated with macro EPU (Meng and Shi, 2017; Irfan et al., 2019; Irfan et al., 2020). EPU has incentive effect and selection effect on enterprise innovation. EPU can affect the enterprise R&D investment and patent application. At the same time, the relationship between EPU and innovation will be affected by the characteristics of enterprises, such as the ownership, government subsidies and financing constraints (Gu et al., 2018). Uncertain policy environment will encourage enterprises to carry out innovation investment as early as possible to obtain future growth options, thus promoting enterprise innovation activities (Liang and Xie, 2019). In addition, Yang C. et al. (2021) explored the internal mechanism between EPU and enterprise innovation from the perspective of corporate social responsibility, and found that EPU had a more significant impact on enterprise invention patent, namely substantive innovation. Yang H. C. et al. (2021) found that EPU has a positive effect on R&D input and innovation output of family business. The literature holds negative views believes that EPU will increase the bank credit risk and make the enterprise have to face strong financing constraints, thus having obvious inhibitory effect on enterprise technological innovation (Zhang and Feng, 2018). The lack of financing capacity caused by macroeconomic uncertainties will limit the improvement of enterprises’ R&D and innovation (Pan and Dong, 2021). In addition, EPU will significantly reduce the product innovation, increase the proportion of service business, promote the transformation of manufacturing enterprises to services (Zhang et al., 2019). Regarding the research question whether economic policy uncertainty can promote enterprise innovation, although there are a lot of research results, there is not a relatively consistent conclusion. When facing the uncertainty of external economic policies, do enterprises with different characteristics have the strategic choice of actively seeking change? Whether there are different innovation behaviors and different innovation outcomes is also the question that this paper considers and tries to answer.

With the continuous attention to financialization in the academic world, scholars at home and abroad have begun to discuss the impact of corporate financial investment on corporate technological innovation. Scholars have not reached a consensus on the impact of financialization on enterprise innovation. Some literatures believe that increasing the investment proportion of financial assets will crowd out the funds for technological innovation, so that enterprises lack sufficient funds for R&D innovation, which will have a restraining effect on enterprise innovation (Wang et al., 2017; Duan and Zhuang, 2021). Other studies show that enterprises can increase the liquidity of assets by using idle funds for short-term financial investment, which can not only realize the maintenance and appreciation of capital, but also bring more investment income, thus alleviating the financing constraints and promoting enterprise innovation (Bonfiglioli, 2008; Yang et al., 2019). In addition, financial investment may also indirectly promote R&D innovation by improving enterprise performance.

Through reviewing the above literature, we find that the existing literature mainly investigates the impact of EPU on enterprise innovation investment, new product sales revenue or the total number of patents. However, there is a lack of analysis from the dual perspective of innovation quantity and innovation quality. Especially, less attention has been paid to the impact of EPU on enterprise innovation with different characteristics. In addition, there is no consensus on the impact of financialization on enterprise innovation.

The marginal contribution of this study lies in three aspects. Firstly, this study investigates the innovation effect of EPU from the dual perspective of innovation quality and innovation quantity, thus enriching the research scope of existing literature and deepening the understanding of EPU. Secondly, this study includes financialization into the analysis of the innovation effect of EPU, and examines the complex relationship between financialization, EPU and enterprise innovation. It not only expands the relevant research perspective, but also provides a reference for enterprises to reasonably allocate financial assets in the face of EPU. Thirdly, this study investigates the differences in the innovation effects of EPU among different types of enterprises. It not only helps to enrich the understanding of the EPU’s innovation effect, but also provides inspiration for different types of enterprises to make scientific innovation strategies in the face of EPU.

The rest of this paper is arranged as follows: The third part contains theoretical analysis and research hypothesis. The fourth part is about research design. The fifth part includes the estimation result and robustness test of the basic model. The sixth part contains further research. The last part is about the conclusion and enlightenment of this paper.

3 Theoretical Analysis and Research Hypothesis

3.1 EPU and Enterprise Innovation

Facing the uncertainty of economic policy, enterprises cannot accurately predict whether, when and how the government will change the current economic policy (Gulen and Ion, 2016). EPU is an important part of economic uncertainty. The objective existence of economic policy uncertainty will have a profound impact on macro-economy and micro enterprise behavior. The continuous adjustment of policies and the differences in the interpretation and implementation of policies by local governments will also bring a certain degree of uncertainty to enterprise operations. Theoretically, if we only rely on the market mechanism to allocate resources, it may lead to problems such as uneven resource distribution and income gap. Therefore, the government needs to adopt corresponding economic policies to overcome or make up for the defects of resource allocation by market mechanism. However, due to the change of market environment and the objective existence of information asymmetry, the government is often unable to make accurate judgment in time. The decision-making and implementation of economic policies often lags behind the changes of the market. Then there is the distortion of resource allocation, which makes enterprises lack of effective incentive mechanism (Lin et al., 2010; Chen et al., 2011).

As a high-risk and high-yield activity, innovation has the characteristics of high R & D cost, long R&D cycle and low success probability. Enterprises are not only the main body of economic activities, but also the main body of innovation activities. They have the demand to transform technical advantages into product advantages, transform innovation achievements into commodities, and get returns through the market. The output of enterprise innovation not only has the form of goods, but also appears in the form of knowledge products such as patents and proprietary technologies. The benefits of technical knowledge and information cannot be fully occupied by individuals alone (Arrow, 1962), but show strong positive externalities through spillover effects. However, it is this spillover effect that makes other enterprises have “free riding” behavior and carry out “imitation innovation” or “follow-up innovation”. This will undoubtedly reduce the motivation of enterprises to carry out independent innovation and breakthrough innovation, and make the innovation activities evolve into a waiting game (Guo, 2018).

When faced with the EPU, the business environment of enterprises will become more complex. Enterprise managers have more difficulty in predicting the changing trend of the market, thus increasing the operating risk and making it more difficult for enterprises to obtain credit resources from banks and other financial institutions. The rise of financing costs increases the uncertainty of corporate profits. Due to financing constraints and risk aversion, enterprises will reduce investment and restrain technological innovation activities (Zhang et al., 2019). However, Bloom (2007) pointed out that although uncertainty brings short-term negative impact on employment, productivity and investment, its impact on enterprise R&D innovation may be different from other economic activities. He also pointed out that the relationship between EPU and firms’ R&D and innovation activities is a very important topic that needs to be further studied theoretically and empirically. Gu et al. (2018) showed that EPU had a positive impact on the enterprise R&D investment and patents. Policy uncertainty will encourage enterprises to implement innovation investment as soon as possible to obtain future growth options, thus promoting enterprises innovation.

The above analysis shows that the impact of EPU on enterprises will vary according to specific behaviors such as enterprise investment, financing behavior or technological innovation. Its impact on enterprise innovation may be different from that on enterprise general investment behavior. Although the increase of EPU inhibits enterprises’ physical capital investment (Li and Yang, 2015), enterprises may transfer part of their investment to R&D input, thus promoting the quantity of enterprises’ innovation output. Innovation is an effective means for enterprises to gain market share and excess profits. When enterprises are faced with market competition and external EPU, they will increase their investment in innovation to strengthen their market power. However, when enterprises face too high EPU, they will weigh the risks and benefits of innovation. Out of caution, enterprises are more willing to carry out “imitation innovation” or “follow-up innovation” and reduce investment in “breakthrough innovation” with high capital demand and high risk. This makes enterprises pay more attention to the quantity growth of innovation rather than the quality improvement of innovation. Therefore, this paper proposes H1:

H1: EPU has a positive effect on the quantity growth of innovation, and a negative effect on quality improvement of innovation.

3.2 EPU, Financial Investment and Enterprise Innovation

In the process of EPU affecting enterprise innovation, enterprise financialization plays a regulatory role. On the one hand, the increase of EPU will make it difficult for enterprises to accurately predict future market demand, thus increasing the uncertainty of corporate cash flow. For the precautionary demand, enterprises will use idle funds for financial investment, increasing the liquidity and revenue of assets. Technological innovation is a process that requires continuous and large investment. Financial investment can create a capital “reservoir” to deal with the capital shortage in the long-term R&D activities (Yang et al., 2019). The rate of return brought by financial investment is generally high. Financial investment can significantly improve the financial performance of enterprises, alleviate the financing constraints of enterprises, and then promote enterprises to pursue the improvement of innovation quality. However, on the other hand, the rise of EPU may lead to a decline in the profits of non-financial industries. As a result, more and more non-financial enterprises choose to invest in financial products, thus crowding out the resources of enterprises for technological innovation (Wang et al., 2017). For enterprise managers, investing in financial products with higher returns can improve business performance in the short term. Therefore, managers have sufficient motivation to reduce investment in R&D activities with long cycle, high cost and high risk, which will eventually inhibit enterprise innovation.

When the uncertainty of economic policies increases, enterprises will choose to hold more financial assets to cope with the uncertainty of cash flow and reduce operational risks (Duchin et al., 2017), which will further enhance the trend of corporate financialization and affect enterprise innovation. On the one hand, the continued to decline in the real economy profit and income under the continuous rise in the overall environment of financial assets, non-financial enterprises to carry out a large number of financial asset investment behavior, will continue to use enterprise resources for technology innovation, crowding out effect on corporate r&d, make enterprises lack enough money for product research and development of innovation and equipment update, Leading to the decline of enterprise innovation output; on the other hand, when enterprises face the uncertainty of external environment and policy, in the face of increasing financial investment, enterprises will be more eager to gain more market share through technical innovation and the excess profit, enterprises under the condition of the limited research and development through compression “strategic innovation” project investment, increasing the financial input in “real innovation” project, In order to increase their core competitiveness, enhance the value of enterprises, and make the innovation quality of enterprises rise. Based on the above analysis, we propose hypothesis H2:

H2: In the process of the impact of economic policy uncertainty on firm innovation, financial investment has a negative moderating effect.

4 Research Design

4.1 Sample Selection and Data Sources

This paper selects A-share listed companies from 2008 to 2017 as research samples. The data mainly come from CSMAR database, Wind database and The National Intellectual Property Office database. The product innovation data comes from the patent database of listed companies and subsidiaries provided by CSMAR and The National Intellectual Property Office database. The data used to measure the EPU comes from the Uncertainty Index of China’s Economic Policy developed by Baker et al. (2016). Considering the availability, validity and quality of data, this paper eliminated the samples as follows: 1) ST and *ST enterprises were eliminated; 2) Exclude financial and insurance enterprises; 3) Eliminate enterprises with missing core variables. In order to reduce the influence of extreme values on regression results, the continuous variables at the enterprise level were treated with 1% bilateral tail shrinking.

4.2 Definition of Variables

4.2.1 Explained Variable: Enterprise Innovation

Existing literature often adopts R&D input, innovation output and innovation efficiency to measure enterprise innovation. Innovation output can be measured by patent output or sales revenue of new products. In this study, patent output is used to measure the enterprise innovation. Patent types include invention patent, utility model patent and design patent. Among them, invention patents have the highest technical content and innovation level. It needs substantive examination. The technical content of utility model patents and design patents is relatively low, and only need to pass the formal examination. Their application authorization rate is close to 100%. The patent data used in this paper comes from the patent database of listed companies and subsidiaries provided by CSMAR. The patent query system of the China National Intellectual Property Database is used to check and verify the patent data of listed companies and subsidiaries. This paper uses the logarithm of “total number of patent applications +1″ to measure the quantity of enterprise innovation (Innovnum), and uses the proportion of invention patent applications in total patent applications to measure the quality of enterprise innovation (Innovqua).

4.2.2 Explanatory Variable: Economic Policy Uncertainty (EPU)

The Economic Policy Uncertainty Index developed by Baker et al. (2016) and published regularly by Stanford University and the University of Chicago covers major economies around the world. The index uses the media’s attention to the uncertainty of economic policy to infer the EPU faced by microeconomic subjects. Baker et al. (2016) used text retrieval and filtering methods to measure China’s EPU index with the Hong Kong South China Morning Post as the retrieval platform for news reports. Referring to Meng and Shi, 2017 and Zhang et al. (2019), this paper uses the geometric mean of monthly EPU index as the annual EPU. In addition, this paper uses the arithmetic mean of monthly EPU index as the explanatory variable in the robustness test.

4.2.3 Moderating Variable: Financialized Investment

At present, there is no unified view on how to measure the level of enterprise financialization. Most of the existing literatures measure it from the perspective of asset allocation and investment return. This paper aims to explore the regulatory effect of financialization on enterprise innovation under the influence of EPU. Therefore, this paper defines the enterprise financialization from the perspective of financial asset allocation. Based on Wang et al. (2017) and Duan and Zhuang, 2021, this paper uses the proportion of enterprise financial assets in total assets to measure enterprise financialization. Enterprise financial assets mainly include monetary capital, trading financial assets, available for sale financial assets, investment real estate, held to maturity investment, dividends receivable and dividends receivable.

4.2.4 Control Variables

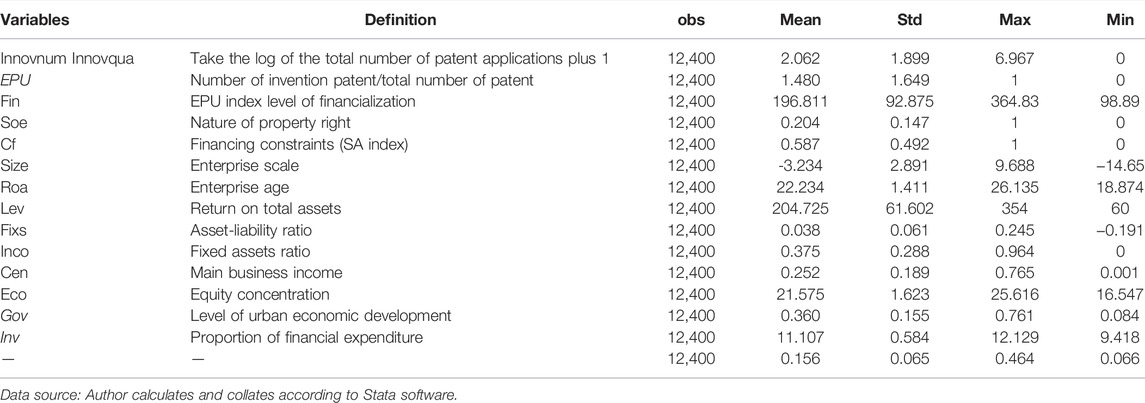

The selection of control variables in this paper mainly refers to the research of Gu et al. (2018) and Zhang et al. (2019). The size, age, return on assets, leverage ratio, fixed assets ratio, main business income and ownership concentration of enterprises are selected as control variables at the enterprise level. The level of economic development, proportion of financial support and proportion of fixed asset investment were used as control variables at the regional level. Where, enterprise Size is measured by the natural logarithm of the company’s total assets. The Age of the enterprise is calculated from the year when the enterprise is established. Return on total assets (ROA) is related to corporate profitability and asset utilization efficiency, and is expressed by net profit/total assets. The leverage ratio (Lev) is related to corporate financial risk, the higher the leverage ratio is, the greater the financial risk is. Fixed assets ratio (Fixs) adopts fixed assets to total assets ratio. Main business income (Inco) is expressed logarithmically. Equity concentration (Cen) is the sum of the previous three shareholders’ shareholding ratio. The level of economic development (Eco) is logarithmic with per capita GDP. Fiscal expenditure ratio (Gov) adopts the ratio of local government fiscal expenditure to GDP. Fixed asset investment ratio (Inv) adopts the ratio of total fixed asset investment to GDP. Table 1 reports the definitions and descriptive statistical results of all variables. It can be seen from Table 1 that the logarithmic mean of total patent applications from 2008 to 2017 is 2.062, the logarithmic mean of invention patents is 1.480 and the logarithmic mean of non-invention patents is 1.623. It shows that there is no obvious quantitative difference between invention patents and non-invention patents among the listed companies in China. The maximum value of the EPU index is 364.83, and the minimum value is 92.875, indicating that the EPU index of China changes greatly from 2008 to 2017, and the degree of uncertainty is relatively obvious.

TABLE 1. Variable definitions and descriptive statistical results.

4.3 Model Construction

In order to test the impact of EPU on enterprise innovation, this paper refers to Zhang et al. (2019) and establishes the following basic regression model:

Among them, Innovnum represents the quantity of enterprise innovation and Innovqua represents the quality of enterprise innovation. EPU represents the uncertainty index of economic policy. εit is the error term. ∑ Controls are a series of enterprise and regional control variables, including: Size, Age, Roa, Lev, Fixs, Cen, Inco, Eco, Gov and Inv. FirmFE and YearFE represent individual fixed effect and time fixed effect, respectively. We mainly focus on the coefficient α1, which reflects the impact of EPU on the quantity and quality of enterprise innovation.

5 Empirical Results Analysis

5.1 Benchmark Regression Results

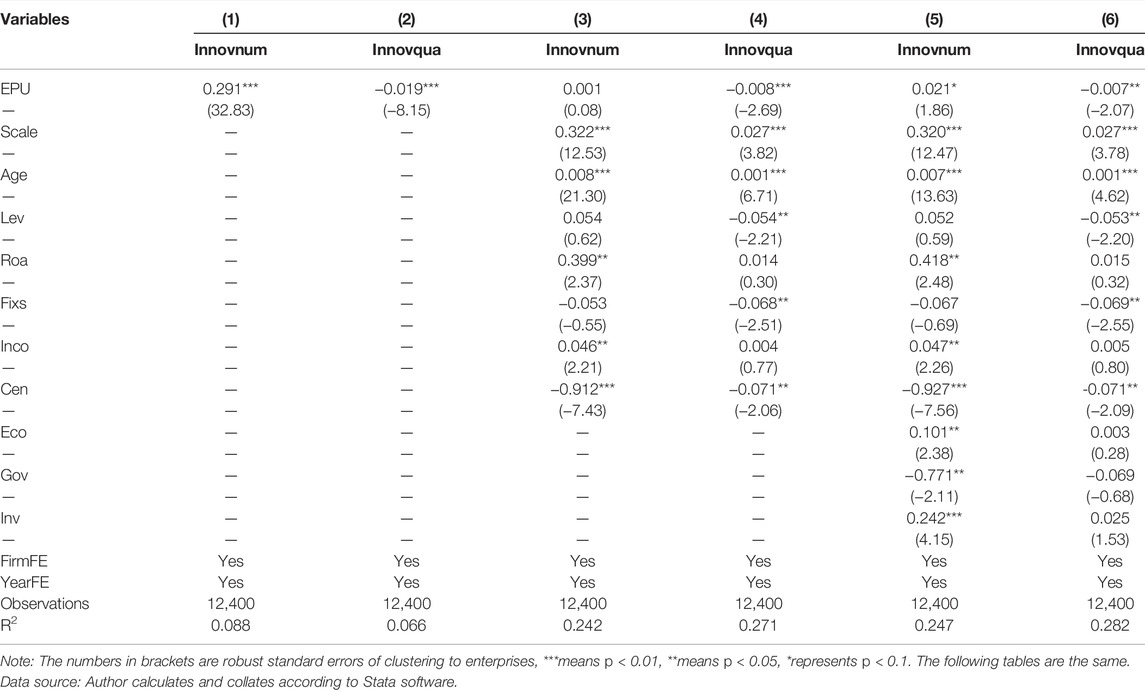

Table 2 reports the regression results of EPU on enterprise innovation. Columns 1) and 2) do not add control variables. Columns 3) and 4) add enterprise-level control variables. Columns 5) and 6) add all control variables. The regression results show that EPU has a significant positive effect on the quantity of enterprises’ innovation and a significant negative effect on the quality of enterprises’ innovation. The regression result verifies H1. As mentioned above, when facing the EPU, enterprises are more willing to enhance their core competitiveness, improve market share and obtain more profits by increasing R&D investment and strengthening the innovation ability of products and technologies. Therefore, the quantity of enterprise innovation will increase. At the same time, with the increase of EPU, the risk and uncertainty of enterprises carrying out innovation activities increase. Motivated by prudence, enterprises are more willing to carry out “follow-up innovation” than breakthrough innovation with high risk, long cycle and high investment, which reduces the innovation quality of enterprises. The coefficients of control variables indicate that the larger the scale of the enterprise, the greater its innovation output. The reason lies in that large companies have resource advantages and stronger technological innovation ability. In addition, the results show that the older the firm, the more innovative it is. The higher the main business income and the higher the rate of return on total assets, the greater the number of innovation output. The more concentrated the equity, the smaller the quantity and quality of innovation. Moreover, regional economic development has positive impact on the quantity of enterprise innovation.

TABLE 2. Regression results of EPU and firm innovation.

5.2 Robustness Test

In order to ensure the reliability of the benchmark regression results, a series of robustness tests were conducted in this paper.

5.2.1 Replace the Explained Variables

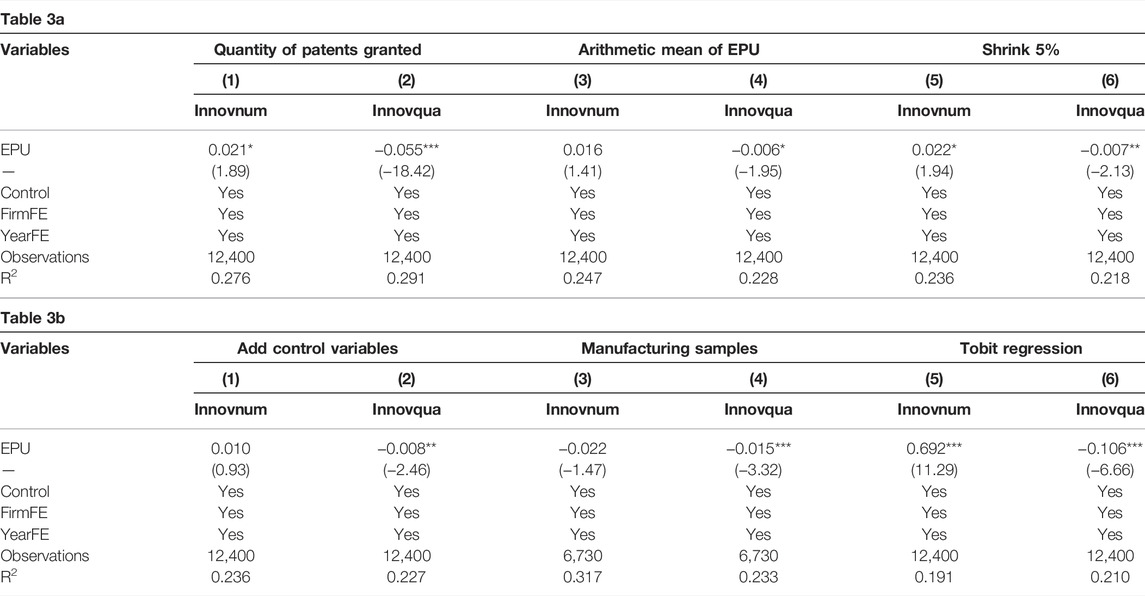

In the benchmark regression, we use the patent applications to calculate the quantity and quality of innovation. In the robustness test, we replace the patent applications with patent authorization, and use the same calculation method to calculate the quantity and quality of enterprise innovation. The regression results are shown in columns 1) and 2) of Table 3a.

5.2.2 Replace Core Explanatory Variables

Referring to Meng and Shi, 2017, the arithmetic mean of monthly EPU index is used as the new explanatory variable in the robustness test. The regression results are shown in columns 3) and 4) of Table 3a.

5.2.3 Further Reduce the Impact of Extreme Values

The core variables were treated with bilateral tail shrinking on the 5% quantile to further reduce the impact of extreme values on the estimated results. The regression results are shown in columns 5) and 6) of Table 3a.

5.2.4 Add Control Variables

Referring to Li and Yang, 2015, this paper further added the regional research support (Scisup) and regional financial development (Finc) into the regression model. The regression results are shown in columns 1) and 2) of Table 3b.

5.2.5 Use Manufacturing Samples

The non-manufacturing enterprises were further removed from the whole samples, and 6,730 manufacturing sample enterprises were retained for robustness test. The regression results are shown in Columns 3) and 4) of Table 3b.

5.2.6 Change Estimation Method

Since the quantity of enterprise patents is non-negative and there is a large number of zero values, this paper chooses Tobit model for robustness test. The regression results are shown in columns 5) and 6) of Table 3.

TABLE 3. Robustness tests.

The results of Table 3a and 3b show that after a series of robustness tests, the regression results of core explanatory variables are consistent with the results of benchmark test. It shows that our benchmark test is reliable. EPU can improve the quantity of enterprise innovation, but it does not improve the quality of enterprise innovation.

5.2.7 Discussion on Endogeneity

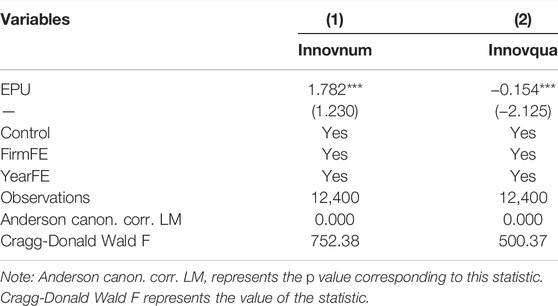

For enterprises, EPU is an exogenous variable. Therefore, a single enterprise cannot affect EPU in reverse. Nevertheless, in order to be robust, this paper refers to Zhang et al. (2019) and selects India’s EPU as the instrumental variable of China’s EPU for analysis. The reason is that India and China have similarities in economic development and policy environment. At the same time, there are close trade ties between China and India. This makes the two countries have similarities in the formulation and implementation of economic policies. We use the two-stage least square method (IV-2SLS) to estimate the parameters. The results are shown in Table 4. It can be seen that the coefficient of EPU has not changed significantly, which also shows that the benchmark conclusion of this paper is still valid after dealing with the endogenous problem.

TABLE 4. Discussion on endogeneity.

6 Further Analysis

6.1 Heterogeneity Analysis

The impact of EPU on enterprise innovation would be heterogeneous due to the differences of enterprises’ characteristics (Zhang et al., 2019). This paper holds that the innovation effect of EPU will be affected not only by the characteristics of the enterprise, but also by the characteristics of the region where the enterprise is located. The following is to study the heterogeneous innovation effect of EPU from the perspective of enterprise characteristics such as ownership, financing constraints and life cycle, as well as regional characteristics such as the regional administrative level and the regional economic development.

6.1.1 From the Perspective of Enterprise Characteristics

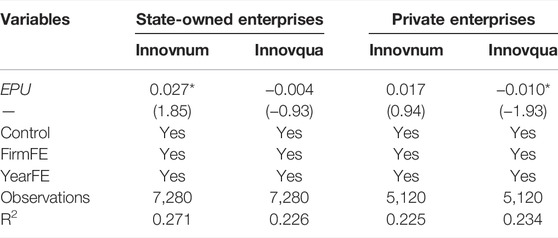

1) Heterogeneity of enterprise ownership. The results of Table 5 show that the EPU has a significant positive effect on the quantity of innovation of State-Owned enterprises, and doesn’t have significant effect on the quality of State-Owned enterprises. when it comes to private enterprises, the impact of EPU on the quantity of innovation is not significant, while the impact on the quality of innovation is significantly negative. The reason for this result is that compared with private enterprises, state-owned enterprises have convenient policy information channels in resource allocation and can obtain the government’s policy guidance in time. At the same time, most of the executives of state-owned enterprises are directly appointed by the government, which makes them think more about being responsible to the government than to the long-term development of enterprises. Therefore, state-owned enterprises are often unwilling to bear the uncertainty and risk of R&D activities (Li and Yu, 2012), and prefer to pursue utility patents and design patents with relatively low risk. When private enterprises are faced with high EPU, they will reduce the capital investment of invention patents due to capital constraints and consideration of financial security. Therefore, the innovation quality of enterprises has declined. The difference of ownership will influence the resource allocation of enterprises, and then lead to different responses to the EPU. China’s private enterprises often face serious “credit discrimination” in the process of financing. Bank credit, government subsidies, land supply and other resources will be allocated more to state-owned enterprises, significantly increasing the R&D input of state-owned enterprises. However, the private enterprises are difficult to obtain the bank credit (Zhang et al., 2012).

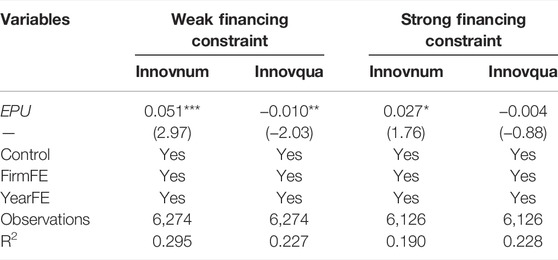

2) Heterogeneity of financing constraint. Enterprise’s internal research and development, technology innovation activities can produce a large number of capital requirements, sustainable, when the enterprise funds nervous, facing serious financing constraints, the enterprise will be limited number of priority funds for daily operation activities and short-term profitability good projects, reduce spending on research and development makes the enterprise technology innovation levels drop. Based on the method of Hadlock & Pierce (2009) [31], this paper uses SA index to measure the degree of financing constraints faced by enterprises. SA index can be calculated as follows: SA = 0.737 Size + 0.043 Size2-0.04 Age. In this formula, Size is the enterprise scale, and Age is the age of the enterprise. The smaller the SA index is, the smaller the financing constraint is. We use SA index to measure the financing constraint of enterprises.

TABLE 5. Heterogeneity of firm ownership.

According to the median of financing constraints, enterprises are divided into strong financing constraint enterprises and weak financing constraint enterprises. The estimated results are shown in Table 6. The results show that, for enterprises with weak financing constraints, EPU has a significant positive impact on the quantity of enterprise innovation and a significant negative impact on the quality of enterprise innovation. For enterprises with strong financing constraints, EPU has a significant positive impact on the quantity of innovation, but not on the quality of innovation. The reason for this result is that when financing constraints are weak, enterprises have cash flow that can be used for R&D investment. However, in the face of higher EPU, enterprises may choose to carry out R&D activities with lower risk and reduce the investment in invention patents. This makes the quantity of enterprise innovation increase, while the quality of innovation decreases. Zhang et al. (2012) found that financing constraints have a negative effect on enterprises’ R&D investment. Pan and Dong (2021) believe that insufficient financing capacity caused by macroeconomic uncertainties would limit the improvement of enterprises’ innovation level. Yu et al. (2019) found that when the degree of macro policy uncertainty is high, enterprises will increase their cash holdings. Therefore, with the rise of EPU, the business risk of enterprises increases and enterprises prefer to invest in financial assets with higher returns. When the financing constraints faced by enterprises are small, enterprises have more funds for financial asset investment. Therefore, enterprises’ investment in financial assets is actually an occupation of innovation resources (Duan and Zhuang, 2021). In addition, the government should focus on overcoming the financing constraints for private enterprises (Ren et al., 2021).

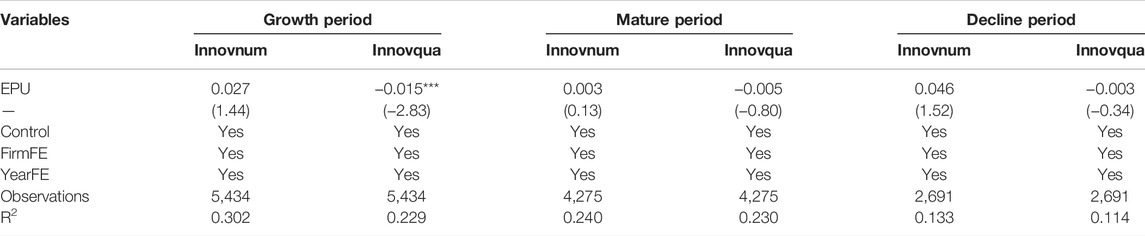

3) Heterogeneity of life cycle. Life cycle theory points out that the scale, investment, financing strategy, profitability, growth and R&D willingness of enterprises will be significantly different at different development stages. There are many methods to define enterprise life cycle in existing literature (Anthony and Ramesh, 1992; Dickinson, 2011). Referring to Dickinson’s method, this paper divides samples into three types: growth stage enterprises, mature stage enterprises and decline stage enterprises. The Dickinson’s method measures the life cycle of enterprise through the combination of the net cash flow of operation, investment and financing activities. It can not only avoid the interference of industry differences, but also avoid the subjective assumption of enterprise life cycle distribution. It has strong objectivity. We conduct grouping regression for enterprises with different life cycles. The results are shown in Table 7. It shows that EPU has a heterogeneous impact on the innovation of enterprises with different life cycles. EPU has no significant impact on the innovation quantity of growth enterprises, but has a significant negative impact on the innovation quality. EPU has no significant impact on the innovation of mature and decline enterprises. The reason may be that compared with the enterprises in the mature and decline periods, the growth enterprises need to make more investment in production and operation, thus crowding out the investment of R&D activities and making the proportion of invention patents relatively low. Enterprises in different development stage have differences in their ability to acquire resources for innovation (Xie and Fang, 2011).

TABLE 6. Heterogeneity of firm financing constraints.

TABLE 7. Heterogeneity of enterprise lifecycle.

6.1.2 Regional Characteristics Perspective

1) Heterogeneity of regional administrative levels. China’s regional administrative level reflects the structure of state power allocation. The essence of many regional development imbalances is the imbalance of resource allocation among regions. Many provinces in China have successively implemented the strategy of developing central cities, which promotes the allocation and agglomeration of resources to the provincial capital and central cities, and then forms a strong squeeze effect and siphon effect on other cities in the province.

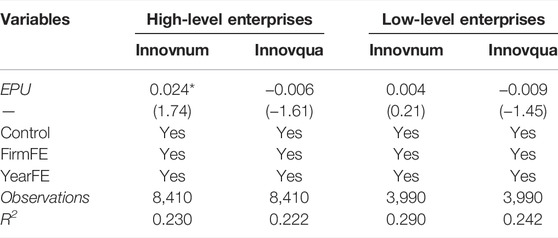

Referring to the national standards of administrative divisions, we define the municipalities directly under the central government, provincial capital cities, sub-provincial cities as high-level cities. The rest of the city is defined as a low-level city. At the same time, according to the administrative level of the city where the enterprise is located, the sample enterprises are further divided into high-level enterprises and low-level enterprises. The estimated results are shown in Table 8. As can be seen, EPU has significant positive impact on the innovation quantity of high-level enterprises, and has negative but insignificant impact on the innovation quality. In addition, EPU has no significant impact on the quantity and quality of innovation of low-level enterprises. It means that the impact of EPU on the innovation of enterprise in cities with different administrative levels is heterogeneous. Jiang et al. (2018) found that compared with lower-level cities, enterprises in high-level cities have more government subsidies, greater talent advantages, more financing facilities and smaller local tax burden.

2) Heterogeneity of regional economic development. Since the Reform and Opening up, China’s economy has been growing at a high speed, but it has also shown a significant regional imbalance. The level of economic development and innovation in the Yangtze River Delta, the Pearl River Delta and the Bohai Rim are significantly higher than those in the central and western regions. This paper refers to Huang et al. (2021), uses the per capita GDP of cities to measure the level of regional economic development. According to the median of per capita GDP of cities, the sample is divided into enterprises with high economic development level and enterprises with low economic development level. Through comparison, it is found that the average of patent applications of enterprises with high economic development level is 128.38, which is significantly higher than 68.98 patents of enterprises with low economic development level. The results of Table 9 show that EPU has no significant impact on the quantity of enterprise innovation, but has a significant negative impact on the quality of innovation. Kou and Liu (2020) shows that there is an obvious regional imbalance in the innovation of Chinese enterprises. The level of industrial agglomeration and innovation in the eastern regions is significantly higher than that in the central and western regions. The eastern regions have three-quarters of the quantity of patent applications in China. Cities with low economic development level have insufficient innovation capacity. Therefore, when facing EPU, these regions are more inclined to carry out innovation activities for accelerating technological progress and promoting economic development.

TABLE 8. Heterogeneity of administrative levels.

TABLE 9. Heterogeneity of the economic development level.

6.2 The Moderating Effect of Financialization

The R&D activities of enterprises need a lot of continuous funds. When an enterprise invests funds in various financial assets, on the one hand, it will make the enterprise’s funds tight and financing limited. The enterprise will reduce the funds for R&D, thus reducing the innovation output of the enterprise. On the other hand, the high return of investing in financial assets can significantly improve the financial performance, alleviate the financing constraints of enterprises, and then promote the innovation of enterprises. Refer to Wu et al. (2020) and Ren et al. (2021), we establish the following regression equation to test whether the financialization shows a moderating effect during the EPU affects enterprise innovation:

In the above formula, Fin represents the financialization of enterprise. The larger Fin is, the higher the enterprise’s financialization level is. The definition of other variables is the same as model (Eq. 1). We mainly focus on the coefficient α3, which reflects the moderating effect of financialization in the process of EPU affecting enterprise innovation.

The results are shown in Table 10. Columns 1) and 2) only control time and individual fixed effect. Columns 3) and 4) further include enterprise and regional control variables. As can be seen, the coefficients of Fin × EPU in Columns 3) and 4) are −0.243 (significant at 1% level) and 0.028 (significant at 10% level) respectively. This means that in the process of EPU affecting enterprise innovation, enterprise financialization has a negative regulatory effect. In the face of EPU, the innovation quantity of enterprises with high degree of financialization is declining, but the innovation quality is rising. Although non-financial enterprises’ investment in financial assets will crowd out resources for R&D activities, thus making enterprises lack sufficient funds for product innovation and equipment upgrading, and resulting in a decline in the quantity of enterprise innovations. However, when facing EPU, enterprises will be more eager to obtain excess profits through innovation. Therefore, on the premise of limited R&D resources, enterprises will focus more on the research of cutting-edge technologies, so as to improve the core competitiveness. This finally makes the innovation quality of enterprises rise. This conclusion also verifies hypothesis 3.

TABLE 10. Regression results of the moderating effect of financialization.

7 Conclusion and Implications

On the basis of theoretical analysis, this paper establishes the relationship between macroeconomic policy and micro enterprise innovation. Taking Chinese A-share listed companies from 2008 to 2017 as research samples, this paper examines the impact of EPU on enterprise innovation by using patent data of listed companies and the Uncertainty index of China’s economic policy constructed by Baker et al. (2016). Meanwhile, the moderating effect of financialization is tested. The results show that the EPU will increase the quantity of enterprise innovation, but inhibit the improvement of enterprise innovation quality. In the process of EPU affecting enterprise innovation, financialization has a negative moderating effect. The impact of EPU on innovation will be affected by enterprise ownership, financing constraint level, life cycle, regional administrative level and regional economic level.

The conclusion of this paper has some policy implications. Firstly, the results of this study show that EPU positively promotes the growth of firm innovation quantity, but inhibits the improvement of firm innovation quality. The increased uncertainty of economic policy will also bring a lot of negative impacts to enterprises. For example, it may cause the rise of enterprise operating costs, inhibit enterprise investment, and lead to the decline of investment efficiency. At the same time, the EPU will also bring negative impacts to the macro economy, such as increasing the volatility of macroeconomic variables and financial assets, affecting employment and output, and hindering economic recovery. Therefore, when relevant government departments frequently adjust economic policies to smooth economic fluctuations, promote economic growth and improve national innovation ability, they should weigh the impact of EPU on different regions, different economic subjects and different economic activities. Secondly, the results of this paper have some inspiration for the adjustment of government innovation policy. Relevant departments should consider the heterogeneous impact of EPU on the innovation of enterprises with different characteristics. We will strive to build a transparent, fair and stable policy environment, promote policy implementation and help enterprises give better play to their innovation vitality. Thirdly, as a big country of patent application, China is not a strong country of patent quality. Patent is an important part of innovation output. The creation of high-quality invention patent and the technology spillover effect of patent itself are the key to promoting technological progress and economic growth. In the face of policy uncertainty and the increasing proportion of financial investment, enterprises should make use of the excess returns brought by financial investment to alleviate the financing constraints, obtain more market shares and excess profits through technological innovation, so as to increase their core competitiveness, enhance corporate value, and improve the quality of innovation. Fourth, in order to further stimulate and protect innovation and promote high-quality development of patents, the State Intellectual Property Office of China (SIPO) has adjusted the funding policy for patent applications. The funding for patent application phase will be completely cancelled by the end of June 2021, and the funding for patent licensing phase will be completely cancelled by 2025. In the face of an application for a patent for aid policy changes, the enterprise should pay attention to regulate the behavior of patent application, improving the quality of patent applications, from a number of one-sided pursuit of innovation to improve the quality of innovation, constantly enhance their innovation through technology innovation level, promote independent innovation ability, promote our country imported from intellectual property powers to create power. Finally, we should recognize that the uncertainty of economic policy has both the causes of policy-making and policy implementation. Local governments should scientifically implement enterprise-related policies and gradually promote the transparent, fair, stable and continuous implementation of various policies.

Data Availability Statement

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding author.

Author Contributions

YZ: Conceptualization, Writing—original draft, and methodology. CZ: supervision. FD: Formal analysis. All authors have read and agreed to the published version of the manuscript.

Funding

This research is funded by National Social Science Foundation of China (18BJL083), Xinjiang Uygur Autonomous Region Natural Science Foundation Project (2017D01C031), Social Science Planning project of Guangdong Province (GD21YYJ17), and Project funded by China Postdoctoral Science Foundation (2021M703772).

Conflict of Interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s Note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Abbasi, K. R., Shahbaz, M., Zhang, J., Irfan, M., and Alvarado, R. (2022). Analyze the Environmental Sustainability Factors of China: The Role of Fossil Fuel Energy and Renewable Energy. Renew. Energy 187, 390–402. doi:10.1016/j.renene.2022.01.066

Aghion, P., Bloom, N., Blundell, R., and Howwit, P. (2005). Competition and Innovation: An Inverted Relationship. Q. J. Econ. 120 (2), 701–728.

Ahmad, B., Irfan, M., Salem, S., and Asif, M. H. (2022). Energy Efficiency in the Post-COVID-19 Era: Exploring the Determinants of Energy-Saving Intentions and Behaviors. Front. Energy Res. 9, 824318. doi:10.3389/fenrg.2021.824318

Anthony, J. H., and Ramesh, K. (1992). Association Between Accounting Performance Measures and Stock.

Arrow, K. J. (1962). The Economic Implications of Learning by Doing. Rev. Econ. Stud. 29, 155–173. doi:10.2307/2295952

Baker, S. R., Bloom, N., and Davis, S. J. (2016). Measuring Economic Policy Uncertainty. Q. J. Econ. 131 (2), 1593–1636. doi:10.1093/qje/qjw024

Bhattacharya, U., Hsu, P., Tian, X., and Xu, Y. (2017). What Affects Innovation More: Policy or Policy Uncertainty. J. Financial Quantitative Analysis 5, 1–33. doi:10.1017/s0022109017000540

Bloom, N., Bond, S., Van Reenen, J., and Reenen, J. V. (2007). Uncertainty and Investment Dynamics. Rev. Econ. Stud. 74, 391–415. doi:10.1111/j.1467-937x.2007.00426.x

Bonfiglioli, A. (2008). Financial Integration, Productivity and Capital Accumulation. J. Int. China Industrial Econ. 9, 1–16. doi:10.1016/j.jinteco.2008.08.001

Caldara, D., Fuentes-Albero, C., Gilchrist, S., and Zakrajšek, E. (2016). The Macroeconomic Impact of Financial and Uncertainty Shocks. Eur. Econ. Rev. 88, 185–207. doi:10.1016/j.euroecorev.2016.02.020

Chen, S., Sun, Z., Tang, S., and Wu, D. (2011). Government Intervention and Investment Efficiency: Evidence from China. J. Corp. Finance 17, 259–271. doi:10.1016/j.jcorpfin.2010.08.004

Dickinson, V. (2011). Cash Flow Patterns as a Proxy for Firm Life Cycle. Account. Rev. 86 (6), 1969–1994. doi:10.2308/accr-10130

Duan, J. S., and Zhuang, X. D. (2021). Financial Investment Behavior and Firm Technological Innovation-Motivation Analysis and Empirical Evidence. Chin. Ind. Econ. 1, 155–173.

Duchin, R., Gilbert, T., Harford, J., and Hrdlicka, C. (2017). Precautionary Savings with Risky Assets : When Cash Is Not Cash[J]. J. Finance 72 (2), 793–852.

Elavarasan, R. M., Pugazhendhi, R., Shafiullah, G. M., Irfan, M., and Anvari-Moghaddam, A. (2021). A Hover View Over Effectual Approaches on Pandemic Management for Sustainable Cities - the Endowment of Prospective Technologies with Revitalization Strategies. Sustain. Cities Soc. 68, 102789. doi:10.1016/j.scs.2021.102789

Fang, V. W., Tian, X., and Tice, S. (2014). Does Stock Liquidity Enhance or Impede Firm Innovation? J. Finance 69 (5), 2085–2125.

Gu, X. M., Chen, Y. M., and Pan, S. Y. (2018). Economic Policy Uncertainty and Innovation: An Empirical Analysis Based on Listed Companies in China. J. Econ. Res. 2, 109–123.

Gulen, H., and Ion, M. (2016). Policy Uncertainty and Corporate Investment. Rev. Financial Stud. 3, 523–564.

Guo, Y. (2018). Signal Transmission Mechanism of Government Innovation Subsidy and Enterprise Innovation.

Hadlock, C. J., and Pierce, J. R. (2010). New Evidence on Measuring Financial Constraints: Moving Beyond the KZ Index. Rev. Financ. Stud. 23 (5), 1909–1940. doi:10.1093/rfs/hhq009

Hall, B. H., Moncada-Paternò-Castello, P., Montresor, S., and Vezzani, A. (2016). Financing Constraints, R&D Investments and Innovative Performances: New Empirical Evidence at the Firm Level for Europe. Econ. Innovation New Technol. 25 (3), 183–196.

Hao, Y., Gai, Z., and Wu, H. (2020). How Do Resource Misallocation and Government Corruption Affect Green Total Factor Energy Efficiency? Evidence from China. Energy Policy 143, 111562. doi:10.1016/j.enpol.2020.111562

Hao, Y., Gai, Z., Yan, G., Wu, H., and Irfan, M. (2021). The Spatial Spillover Effect and Nonlinear Relationship Analysis Between Environmental Decentralization, Government Corruption and Air Pollution: Evidence from China. Sci. Total Environ. 763, 144183. doi:10.1016/j.scitotenv.2020.144183

Hsu, P.-H., Tian, X., and Xu, Y. (2014). Financial Development and Innovation: Cross-Country Evidence. J. Financial Econ. 112 (1), 116–135. doi:10.1016/j.jfineco.2013.12.002

Huang, L. X., Ma, M. H., and Wang, X. B. (2021). Do Economic Growth Targets Affect Corporate Risk-Taking? – an Investigation Based on the Dual Perspectives of Market and Government. Financial Res. 1, 62–77.

Huang, W., Saydaliev, H. B., Iqbal, W., and Irfan, M. (2022). Measuring the Impact of Economic Policies on CO2 Emissions: Ways to Achieve Green Economic Recovery in the Post-COVID-19 Era. Clim. Change Econ., 2240010.

Hussain, A., Yang, H., Zhang, M., Liu, Q., Alotaibi, G., Irfan, M., He, H., Chang, J., Liang, X.-J., Weng, Y., and Huang, Y. (2022). mRNA Vaccines for COVID-19 and Diverse Diseases. J. Control. Release 345, 314–333. doi:10.1016/j.jconrel.2022.03.032

Irfan, M., and Ahmad, M. (2022). Modeling Consumers' Information Acquisition and 5G Technology Utilization: Is Personality Relevant? Personality Individ. Differ. 188, 111450. doi:10.1016/j.paid.2021.111450

Irfan, M., Hao, Y., Panjwani, M. K., Khan, D., Chandio, A. A., and Li, H. (2020). Competitive Assessment of South Asia's Wind Power Industry: SWOT Analysis and Value Chain Combined Model. Energy Strategy Rev. 32, 100540. doi:10.1016/j.esr.2020.100540

Irfan, M., Zhao, Z. Y., Mukeshimana, M. C., and Ahmad, M. (2019). “January. Wind Energy Development in South Asia: Status, Potential and Policies,” in 2019 2nd International Conference on Computing, Mathematics and Engineering Technologies (iCoMET) (IEEE), 1–6.

Jiang, T., Sun, K., and Nie, H. H. (2018). City Level, Total Factor Productivity and Resource Mismatch. Manag. World 3, 8–52.

Kou, Z. L., and Liu, X. Y. (2020). Chinese Firms' Patent Behavior: Characteristic Facts and the Impact from Innovation Policy. Econ. Res. J. 3, 83–99.

Li, F. Y., and Yang, M. Z. (2015). Will Economic Policy Uncertainty Inhibit Corporate Investment? — an Empirical Constraints and Government Subsidies. Sci. Technol. Prog. Countermeas. 6, 1–9.

Li, W. G., and Yu, M. G. (2012). Ownership Nature, Marketization Process and Firm Risk Taking. China Ind.

Liang, Q. X., and Xie, H. J. (2019). Does Policy Uncertainty Hurt China's Long-Term Growth Potential? — Evidence from Firm Innovation Behavior. J. Central Univ. Finance Econ. 7, 79–92.

Lin, Y. F., Wu, H. M., and Xing, Y. Q. (2010). Tidal Surge and the Formation Mechanism of Excess Capacity. Manag. World 10, 4–19.

Meng, Q. B., and Shi, Q. (2017). The Impact of Economic Policy Uncertainty on Firm R&D: Theory and Experience. World Econ. 9, 75–98.

Peng, Y. C., Han, X., and Li, J. J. (2018). Economic Policy Uncertainty and Firm Financialization. Finance Trade Res. 5, 137–155.

Rao, P. G., and Xu, Z. H. (2017). Does Economic Policy Uncertainty Affect Executive Change. Manag. World 1, 145–157.

Rao, P. G., Yue, H., and Jiang, G. H. (2018). Research on Economic Policy Uncertainty and Firm Investment Behavior. World Econ. 2, 27–51.

Ren, S., Hao, Y., and Wu, H. (2021). Government Corruption, Market Segmentation and Renewable Energy Technology Innovation: Evidence from China. J. Environ. Manag. 300, 113686. doi:10.1016/j.jenvman.2021.113686

Shi, R., Irfan, M., Liu, G., Yang, X., and Su, X. (2022). Analysis of the Impact of Livestock Structure on Carbon Emissions of Animal Husbandry: A Sustainable Way to Improving Public Health and Green Environment. Front. Public Health 10, 835210. doi:10.3389/fpubh.2022.835210

Tang, C., Irfan, M., Razzaq, A., and Dagar, V. (2022). Natural Resources and Financial Development: Role of Business Regulations in Testing the Resource-Curse Hypothesis in ASEAN Countries. Resour. Policy 76, 102612. doi:10.1016/j.resourpol.2022.102612

Visnjic, I., Wiengarten, F., and Neely, A. (2016). Only the Brave: Product Innovation, Service Business Model Innovation, and Their Impact on Performance. J. Prod. Innovation Manag. 33 (1), 36–52.

Wang, H. J., Cao, Y. Q., Yang, Q., and Yang, Z. (2017). Financialization of Entity Firms Promotes or Inhibits Firm.

Wang, H. J., Li, Q. Y., and Xing, F. (2014). Economic Policy Uncertainty, the Level of Cash Holdings and Their Market Value. Finance Res. 9, 53–68.

Wen, C., Akram, R., Irfan, M., Iqbal, W., Dagar, V., Acevedo-Duqued, Á., et al. (2022). The Asymmetric Nexus Between Air Pollution and COVID-19: Evidence from a Non-Linear Panel Autoregressive Distributed Lag Model. Environ. Res. 209, 112848. doi:10.1016/j.envres.2022.112848

Wu, H., Ren, S., Yan, G., and Hao, Y. (2020). Does China's Outward Direct Investment Improve Green Total Factor Productivity in the “Belt and Road” Countries? Evidence from Dynamic Threshold Panel Model Analysis. J. Environ. Manag. 275, 111295. doi:10.1016/j.jenvman.2020.111295

Wu, H., Xue, Y., Hao, Y., and Ren, S. (2021). How Does Internet Development Affect Energy-Saving and Emission Reduction? Evidence from China. Energy Econ. 103, 105577. doi:10.1016/j.eneco.2021.105577

Xiang, H., Chau, K. Y., Iqbal, W., Irfan, M., and Dagar, V. (2022). Determinants of Social Commerce Usage and Online Impulse Purchase: Implications for Business and Digital Revolution. Front. Psychol. 13, 837042. doi:10.3389/fpsyg.2022.837042

Xie, W. M., and Fang, H. X. (2011). Financial Development, Financing Constraints and Firm R&D Investment. Financial Res. 5, 171–183.

Yang, C., Hao, Y., and Irfan, M. (2021a). Energy Consumption Structural Adjustment and Carbon Neutrality in the Post-COVID-19 Era. Struct. Change Econ. Dyn. 59, 442–453. doi:10.1016/j.strueco.2021.06.017

Yang, H. C., Wen, J., and Chen, X. Z. (2021b). Economic Policy Uncertainty and Family Firm Innovation: Financing.

Yang, S. L., Niu, D. Y., Liu, T. L., and Wang, Z. H. (2019). Financialization of Entity Firms, Analyst Focus and Internal Innovation Drivers. Manag. Sci. 32 (2), 3–18.

Yang, Zhen., Ling, H. C., and Chen, J. (2021c). Economic Policy Uncertainty, Corporate Social Responsibility and Corporate Technological Innovation. Stud. Sci. Sci. 3, 544–555.

Yu, J. W., Guo, K. M., and Gong, L. T. (2019). Macro Economic Policy Uncertainty and Corporate Cash Holdings.

Yumei, H., Iqbal, W., Irfan, M., and Fatima, A. (2021). The Dynamics of Public Spending on Sustainable Green Economy: Role of Technological Innovation and Industrial Structure Effects. Environ. Sci. Pollut. Res., 1–19. doi:10.1007/s11356-021-17407-4

Zhang, F., Li, X. Y., Wu, L. D., and Yin, X. L. (2019). Product Innovation or Service Transformation: Economic.

Zhang, J., Lu, Z., Zheng, W. P., and Chen, Z. Y. (2012). Financing Constraints, Financing Channels and Firms' R&D Investment. World Econ. 10, 65–90.

Zhang, Q. X., and Feng, L. (2018). Macro EPU and Firm Technological Innovation: Based on Empirical Evidence of Chinese Listed Companies. Contemp. Econ. Sci. 40 (4), 48–59.

Keywords: policy uncertainty, financialization, technological innovation, economic development, China

Citation: Zhang Y, Zhuo C and Deng F (2022) Policy Uncertainty, Financialization and Enterprise Technological Innovation: A Way Forward Towards Economic Development. Front. Environ. Sci. 10:905505. doi: 10.3389/fenvs.2022.905505

Received: 27 March 2022; Accepted: 11 April 2022;

Published: 12 May 2022.

Edited by:

Muhammad Irfan, Beijing Institute of Technology, ChinaReviewed by:

Arifa Tanveer, Beijing University of Technology, ChinaVishal Dagar, Great Lakes Institute of Management, India

Copyright © 2022 Zhang, Zhuo and Deng. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Feng Deng, ZGVuZ2Zlbmd4anVAMTI2LmNvbQ==