Jiaqi Liu

Jiaqi Liu Zhan Wang

Zhan Wang Linsen Yin

Linsen Yin Ying Liu

Ying Liu- 1School of Management, Wuhan University of Technology, Wuhan, China

- 2Shanghai Lixin University of Accounting and Finance, Shanghai, China

Water shortage has become a widespread problem worldwide. Preparation of water resource balance sheet forms the basis of regional environmental governance in China and is of great importance for achieving the sustainable development. This study is an attempt of developing a water resource accounting system on an accrual basis by preparing balance sheet and other essential supporting statements for Wuhan within the framework of a parallel reporting system, which is oriented to different objectives. The results show that during 2014–2020 the physical volume of Wuhan’s water resources fluctuated with net precipitation to a large extent. Since 2017, the value of Wuhan’s water has kept increasing even though the water volume of 2017–2019 still declined due to the earlier drought. This demonstrates a relatively better water management performance during the current terms of office, which indicates a positive role of the leadership accountability system based on natural resource balance sheeting that is being implemented in China. This study contributes to the literature on regional water resources accounting and environmental management. The water resource statements prepared for Wuhan, Hubei, China have a good level of generality. They provide a reliable basis for the local government’s performance assessment of water resources management and facilitate the implementation of water resource related policies.

1 Introduction

Water is one of the most widely distributed substance on our planet. It exists almost everywhere (Falkenmark and Widstrand, 1992) and plays a vital role in both the environment and human life (Oki and Kanae, 2006; Lal, 2015). However, with the population growth and economic development, human demand for water resources continues to increase (UN-Water, 2008). Rapid population growth, fast urbanization, increasing economic development, unprecedented technological innovations, drastic land-cover alterations, and climate change have led to a global water supply crisis (Johnson et al., 2001; The World Economic Forum, 2013). At present, nearly half of the global population is already living in areas with potential water scarcity, and this number may increase to between 4.8 thousand million and 5.7 thousand million by 2050 (WWAP, UN-Water, 2018). As a result, the World Economic Forum has declared the water supply crisis as one of the top five crises facing the globe over the next 10 years (The World Economic Forum, 2013). Besides, over two thousand million people have no access to safe drinking water worldwide. Water-borne diseases lead to 250 million illnesses (Gleick, 2016; WWAP, 2019). Water resource utilization sustainability has become a global issue that will eventually pose a serious threat to human health and even survival if not controlled (WWAP, 2019). Therefore, how to evaluate the development and sustainability of regional water resources has become an issue that scientists around the world have relentlessly explored (Richter et al., 2003).

As in many other parts of the world, water resources are increasingly under pressure in China (He et al., 2020). Presently, China is a water-scarce country in terms of water resources per capita (Zhou and Tol, 2004). Among the 663 cities in China, more than 400 cities are short of water all the year round, and 110 cities are seriously short of water (OECD, 2007). In this context, China has made some efforts in water resources management. In 1988, China’s first guiding law on water resources management, the Water Law, was issued. Three laws on water pollution control, water and soil conservation and flood control were also promulgated within 9 years around 1988. After the revision of relevant laws, the water law system tended to be improved. The government began to guide the public to participate in the supervision mechanism of environmental protection, so that citizens’ awareness of environmental protection was gradually increasing. In 2013, the Chinese authorities issued the Measures for the Implementation of the Most Strict Water Resources Management System Assessment, setting specific targets for total water consumption, water use efficiency, and water quality compliance rate of water function zones in various provinces, autonomous regions, and municipalities (Wang and Shi, 2021). In 2016, China Water Resources Bureau proposed the river chief system, which means that the main leaders of the government at all levels serve as the river chief, responsible for organizing and leading the management and protection of corresponding rivers and lakes. This system strengthened the leadership responsibility for water resources. The lifelong responsibility makes leading cadres have to pay more attention to water resource management.

To further clarify the leaders’ responsibilities in management of the natural resource assets, including water resources, the Chinese Authorities proposed to explore the preparation of natural resource balance sheet (CCCPC, 2013). And then it was specified that the government should set up an agency to manage and monitor the state-owned natural resource assets, which highlights the importance of natural resource assets accounting. In fact, the contradiction among economic growth, resource consumption, and environmental pollution in China is the product of policies that focus purely on GDP. Therefore, exploring the preparation of the natural resource balance sheet is an innovative plan proposed by the Chinese authorities to achieve sustainable utilization of resources. It aims to fundamentally resolve the contradictions among economic growth, resource consumption, and ecological destruction from the perspective of reforming the cadre incentive system (Wang, 2019). Preparation of natural resource balance sheet, on one hand, reflects the current conditions of regional natural resources at a certain point in time (Yang et al., 2018) and changes of natural resources during a period. These detailed recordings are conducive for leading cadres to formulate practical strategies and policies (Song et al., 2019). On the other hand, as a basis to promote the ecological civilization construction and sustainable development, preparation of natural resource balance sheet can provide a data support for the off-office audit of leading cadres (Tang et al., 2020).

The purpose of this study is to examine the issue of regional water resources accounting. We attempt to introduce a parallel natural resource reporting system and prepare regional water resource balance sheet, income statement and stock and change statement, based on which we present the regional water resource management results in recent years. This study is an attempt to examine the effectiveness of the natural resource balance sheeting practice and leadership accountability system being promoted in China. It is also expected to provide a reference for water resource accounting in other regions.

2 Literature Review

2.1 System of Environmental-Economic Accounting

To account for the results of human economic activities, the British economists Meade and Stone (1941) built SNA (the System of National Accounts), which was adopted in 1953 by international organizations such as UN (the United Nations) and the World Bank. SNA 2008 issued by the United Nations in 2008 incorporated the national balance sheet into the national economic accounting system. However, The SNA focuses on GDP. Additionally, the accounting system, influenced by resource bias and environmental conditions, tends to generate “false economic prosperity” and “hollow” resources (Hartwick, 1990). This means that SNA does not adequately account for the environment (Nordhaus and Tobin, 1972). As a result, Incorporating resource depletion and environmental pollution into macro-economic accounting has become a hot topic in the field of environmental economics (Costanza et al., 2014). Moreover, scarcities of natural resources and health effects from overloaded sinks for wastes and pollutants had driven extended accounting for improved welfare measurement (Daly and Cobb, 1989; Leipert, 1989). The United Nations (UN) and the World Bank added NR (Natural Resource) and the environment to the national economic accounts in 1993, and then issued the SEEA (System of Environmental-Economic Accounting). This system is coordinated with SNA, using data of physical volume to describe economy-environment interactions in various fields (Eigenraam and Obst, 2018).

After three revisions in 2000, 2003 and 2012, the United Nations SEEA-CF (System of Environmental–Economic Accounting Central Framework) has become an international statistical standard that describes stocks and changes of environmental assets in 2012 (Virto et al., 2018). SEEA 2012 involves multiple disciplines of economics and environment. This system comprehensively expounds the classification, accounting standards and accounting methods of natural resources, etc. As the most widely accepted standard system of environmental economic statistics in the world, SEEA 2012 was used for reference by many countries to explore the construction of their own environmental-economic accounting system. For example, In Australia, SEEA-W (The System of Environmental-Economic Accounting-Water), as the part of SEEA, has been used to support integrating water into economic modelling among others (van Dijk et al., 2014). Additionally, under the guidance of the sustainable development philosophy, accounting and management of their domestic natural resources were conducted on the basis of the SEEA in Namibia, Guatemala and the Netherlands (Morton et al., 2016; Zhang et al., 2017; Vardon et al., 2018). Meanwhile, various regions in China have also begun to conduct extensive explorations on the preparation of natural resource balance sheets.

2.2 Natural Resource Accounting

There is a vast amount of practice on natural resource accounting internationally. Since the 1970s with some initiatives in Canada, Denmark, France, the Netherlands, Norway and Spain, we have witnessed substantial efforts to develop natural capital accounting (Laurans et al., 2013; Weber, 2014). Some researchers have used the SEEA as a guide to explore the construction of a national framework for natural resource asset accounting (Bright et al., 2019; Smith, 2020). Norway has established extensive resource-accounting system to supplement their national income accounts (Costanza et al., 1997). Finland established the framework of natural resources accounting including the detailed forest accounting (Lange, 2004). The Mexican government incorporated oil, land, water, air, soil and forest into the Environmental and Economic Accounting, the stocks and flows of which are measured in physical and monetary unit (Gonzalez-Martinez and Schandl, 2008).

Research on natural resource accounting began late in China but has developed rapidly. In the early 1980s, the Office of the Leading Group for Environmental Protection and the National Bureau of Statistics jointly established an environmental protection statistics system. After a long period of development, September 2006 saw the release of the Research Report on China’s Green National Economic Accounting 2004 (SEPA, 2006). Later, in November 2013, at the third Plenary Session of the 18th CPC Central Committee, the proposition was made to explore preparation of the balance sheet of natural resources and carry out the off-office auditing of leading cadres’ natural resource assets. This resulted in an upsurge in research on natural resource asset accounting. Preparation of natural resources balance sheet is a new concept proposed by Chinese government. Therefore, the current domestic theoretical research related to natural resource balance sheet is still in the exploratory stage. Some scholars adhere to the principle of starting with easy things first, putting forward ideas of the construction of natural resources balance sheet from hot theoretical issues (e.g., the purpose, significance and the main theories). Wu et al. (2020) discussed the concept and classification of natural resources and natural resource assets. Moreover, they put forward suggestions on the formulation of China’s natural resources government accounting standards. Wang et al. (2021) defined precisely each element of natural resource accounting. Based on this, they develop a parallel natural resource reporting system for the purpose of off-office auditing, which is a relatively accepted system of the natural resource balance sheet in China at present.

2.3 Water Resource Accounting

The current international system of water resource accounting mainly includes SEEA-W (the System of Integrated Environmental and Economic Accounting-Water) and AWAS (the Australian Water Accounting Standard) (Danoucaras and Woodley, 2013). SEEA-W provides a conceptual framework for the integration of water resources and economic information (Borrego-Marín et al., 2016), and a series of accounts for water resources accounting, including physical, value, and water quality accounts. As a satellite account of the SNA, SEEA-W aims to include water resources into the national economic accounting and reflect the important role of water resources in economic development (Gan and Gao, 2008). A range of water accounts have been developed based on SEEA-W in different parts of the world (Edens, 2013; Charpleix, 2017). For example, Basic water accounts have been developed in Botswana, Colombia, and Costa Rica (Vardon et al., 2018). Furthermore, accounts that are more detailed are available for Germany, Norway, and Sweden (Smith, 2020). Netherlands’ water accounts provide information on the use and the monetary value of water resources in the country (Edens and Graveland, 2014). AWAS refers to the principle of accounting and introduces the loan relationship into water resources accounting. Based on the water rights system and the annual allocation rules regarding water resources, detailed records of the stock, the income and expenditure of water resources are prepared. This standard adopts the financial accounting theory and system, and takes an accrual basis as the basis. Under the precondition of the water rights being clarified, it takes physical volume as the measurement attribute and adopts the double-entry bookkeeping to prepare statement of water assets and water liabilities, statement of changes in water assets and water liabilities, and statement of water flows. AWAS is one of the few international accounting systems that includes liabilities (Qin et al., 2017).

Some progress has also been made in water resource accounting in China. The NBS (National Bureau of Statistics) began to carry out pilot ecosystem accounting in Guangxi Zhuang Autonomous Region and Guizhou Province in 2017. During this time, the NBS developed close cooperation with the UN Statistics Division, the UN Environment Programme and the European Union on NCAVES (Natural Capital Accounting and Valuation of Ecosystem Services) to strengthen the guidance on national natural resource balance sheets. The natural resource balance sheets they prepared related to the physical and ecological value of land, forest and water ecosystems in Guangxi and Guizhou Province.

To summarize, issues on natural resource balance sheeting are still under exploration. Agreements have hardly been reached on the concepts, principle and presentation of natural resource balance sheet. Besides, researches in the field of environmental accounting have currently been conducted more at the micro-entity level and less at the national or regional government level (Song et al., 2019). Few attempts have been made to account for natural resources based on the accrual basis.

In view of this, we attempt to prepare regional water resource balance sheet, income statement and stock and change statement on an accrual basis, so as to present the data of physical volume and value of regional water resource assets. Based on this, we assess the local government’s water resource management in recent years to find out the impact of China’s ongoing natural resource assets leadership accountability system on local water management.

3 Concept Framework

3.1 Reporting Objectives and Accounting Entity

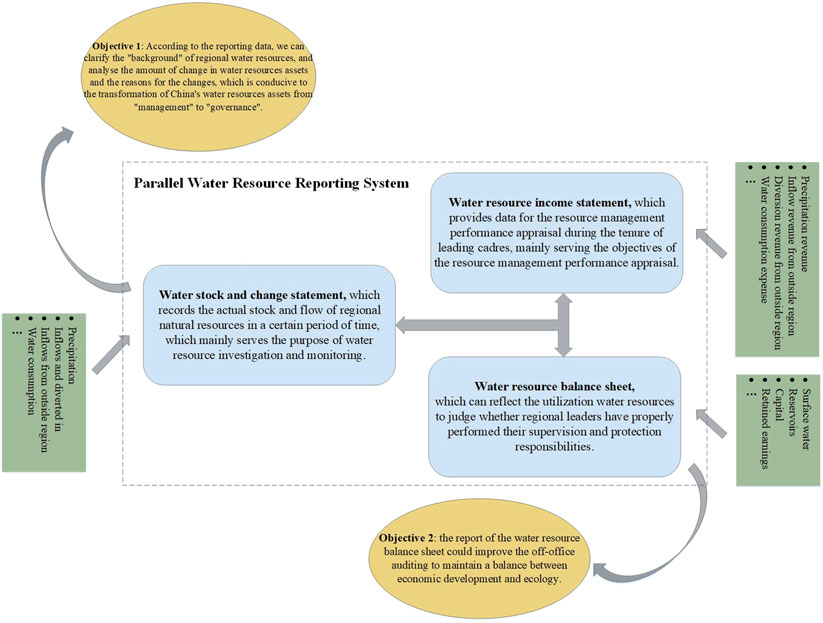

The identification of the purpose is central to the development of a coherent basis for structuring financial reporting (Sutton et al., 2015). The objective and motivation of preparation of the sheet mainly include the following two parts. On the one hand, the purpose of preparation a water resource balance sheet is to investigate the “background” of China’s water resources assets (Yang et al., 2018). According to the reporting data, we can analyze the amount of change in water resources assets and the reasons for the changes, which is conducive to the transformation of China’s water resources assets from “management” to “governance” (Zhang et al., 2010). On the other hand, the report of the water resource balance sheet focuses on improving the off-office auditing to maintain a balance between economic development and ecology (Tang et al., 2020). Preparation of a water resource balance sheet not only can reflect the utilization of water resources in the process of economic development, but also is a prerequisite for incorporating environmental performance into the performance evaluation system.

Preparation of the natural resource balance sheet should focus on the identification of the accounting entity, which is one of prerequisites for asset measurement (Collis et al., 2010). Accounting is possible only when there is an area of economic interest that can be defined (Kurunmaki 1999). In addition, the off-office auditing requires clearly defining the subject of responsibility in the preparation, the purpose of which is to achieve the coordinated development of economy and environment (Ogilvy et al., 2018). Chinese natural resources have the attribute of public property rights. The subject for the protection and use of natural resources is the relevant government departments. Therefore, the preparation subject of the natural resource balance sheet should be the relevant government departments rather than enterprises (Song et al., 2019). The determination of the preparation entity of the relevant resource balance sheet should be different from the determination of the financial accounting entity. Government departments should be the main choice for the preparation subject of natural resource balance sheet. In the water resource balance sheet, the accounting entity is the owner of water resources. According to Law of the People’s Republic of China on Water, the ownership of water resources belongs to the state. However, the state just carry out macroscopic adjustment on water resources. Regional governments have the authority to manage and allocate water resources. Therefore, the accounting entity of water resource balance sheets is the government at all levels.

3.2 Accounting Basis

Preparation of the water resource balance sheet has its accounting basis, which is determined by the preparation principle and logic of the balance sheet.

3.2.1 Double-Entry Bookkeeping System

Financial accounting is based on double-entry bookkeeping, whereby each economic event recorded has equal and opposite effects on at least two related accounts (Trotman and Gibbins, 2003). As component of the financial reports, balance sheet is also based on double-entry bookkeeping. Double-entry accounting applies to the natural resource statement preparation and is used throughout this process. The system takes “asset = liability + owner’s equity” as the accounting balance. It records each transaction or event in equal amounts in two or more accounts that are related to each other (Ker, 1970). Therefore, we can comprehensively reflect the change of each stock and flow of natural resources through the increase or decrease of accounting elements.

3.2.2 Accrual Basis

The accrual method of accounting is commonly accepted as the most scientific and accurate method of handling accounts (Husband, 1926), under which transactions are identified as the underlying economic events occur, regardless of the timing of the related cash receipts and payments (Khan and Mayes, 2009). Following this methodology, revenues are identified when income is earned, and expenses are identified when liabilities are incurred or resources consumed (Khan and Mayes, 2009). For one of the objectives of water resources reporting—the exit audit of leaders—we need to identify whether the entity’s claims/obligations involving the water resource assets are specifically related to the current period. The water resource statements that are based on an accrual-basis allow for a clear delineation of the “payables” or “receivables” from period to period (Husband, 1926), so as to clarify the performance of responsibilities during the term of the leader as well as provide data support for the off-office auditing of leading cadres’ natural resource assets. For events occurring during a leader’s term of office that have a high probability of resulting in a loss of natural resources, even if the outcome of the loss has not yet been seen, a provision should be made for the possible future loss during this term since the related obligation has been incurred. This treatment follows the accrual principle.

3.2.3 Multi-Measurement Attributes

The macroscopic characteristics of natural resource distribution, as well as the uncertainty of environmental impact, complicate the balance sheet accounting (Song et al., 2019). When preparing the water balance sheet, the principle of “calculating the physical volume first, then the value quantity” should be followed. As there has not yet been a standard system for measuring the value of water resource assets, the monetary value measurement is a difficult part of water resources accounting. It is not feasible to require that water assets be measured in monetary units only (Mia, 2005). Physical volume measuring is essential to the water resource valuation. Value accounting is based on physical accounting. The corresponding water resource value data is obtained through the comprehensive accounting of water resource assets such as valuation and recording. Therefore, preparation of the natural resource balance sheet can first calculate the physical volume and then the value quantity, which means that we should give priority to preparing the physical accounting statement of natural resource assets.

3.3 Accounting Elements

3.3.1 Elements of a Balance Sheet

Among the accounting elements of natural resource balance sheets, scholars have unified the definition of assets. According to the SNA2008 and SEEA 2012, the confirmation of the natural resource assets should follow two basic conditions: “the ownership belonging to the authority” and “the inflow of the economic interests.” “The inflow of the economic interests” requires resources to have rarity and value. Thus, combining the SNA 2008, SEEA 2012, and IASB’s definitions of assets, water resources assets can be defined as scarce water resources owned by the state, managed or controlled by the government departments, and from which future economic, ecological, or social benefits are expected to flow to the entity.

The concept of natural resource liabilities has been subject to considerable controversy. Financial Accounting Standards Board (FASB) defines liabilities as “liabilities are probable future sacrifices of economic benefits arising from present obligations of a particular entity to transfer assets or provide services to other entities in the future as a result of past transactions or events.” The present obligation in this context refers to the obligation to discharge the debts. The vast majority of current studies believe that natural resource liabilities are excessive depletion of natural resources as a result of human production and living activities. We compare this definition with the FASB’s definition of “liabilities.” Although excessive depletion of natural resources is a result of past transactions or events of the accounting entity and is likely to result in the future sacrifices of economic benefits, the excessive depletion of natural resources is not a present obligation. Meanwhile, there are neither reasonable creditors nor a specified pay-off date for the natural resources. The liabilities do not meet the IASB’s definition of “liabilities” because they cannot find an object who should perform their obligations. Therefore, it is believed that the so-called natural resource liabilities does not exist.

The natural resource balance sheet must meet the accounting equation of “asset = liability + owner’s equity” (Collis et al., 2010). In the natural resource balance sheet, the natural resource owner’s equity directly reflects occupant and control of natural resources by the state and entities. Some scholars believe that natural resource owner’s equity reflects the government’s total wealth of all natural resources owned by the country or region (Sheng and Yao, 2017). Other studies also generally take this view as the concept of natural resource owner’s equity. The definition of water resource owners’ equity in this study will also follow this view. Since there are no natural resource liabilities, natural resource assets should be attributed to owners’ equity. The natural resource owner’s equity can be divided into two parts: natural resource capital and natural resource retained earnings (Wang et al., 2021). Natural resource capital refers to the region natural resource equity when the current leading cadres take office. Natural resource retained earnings are the cumulative amount of the natural resource net income carried forward in each year during the tenure of the leading cadres. When the leading cadre leaves office, the balance of the natural resource retained earnings can reflect the performance of the leader’s natural resource management during his tenure, so as to meet the needs of natural resource asset off-office audit.

3.3.2 Elements of an Income Statement

Few studies have been conducted to conceptually define the elements of natural resource income statements. However, it can be seen from the double-entry bookkeeping system and the accrual basis that preparation of balance sheets in the field of natural resource accounting cannot avoid the definition of the elements of the income statement.

Revenues are the increase in economic benefits during the accounting period in the form of inflows or enhancements of assets or decreases of liabilities that result in increases in equity, other than those relating to contributions from equity participants (IASB, 2014). Referring to this definition, Wang et al. (2021) defined natural resource revenues as the increases in natural resources formed in natural resource maintenance, maintenance, cultivation, and other activities within a certain period that result in increases in owner’s equity, other than those relating to the newly invested capital. Combined with the characteristics of water resources--circulation and fluidity (Oki and Kanae, 2006), we define water resource revenues as the increases in water resources formed in water resources maintenance and other activities within a certain period that result in increases in owner’s equity, other than those relating to the newly invested capital. Specifically, it includes natural precipitation revenue, inflow revenue from outside region revenue, and industry return revenue, etc. It should be noted that the “revenues” is referred to in a broad sense, which includes not only daily water resource operating revenues, but also incidental revenue caused by resource reclassification.

Expenses refer to the decreases of assets or increases of liabilities that result in decreases in equity, other than those relating to distributions to participants (IASB, 2018). Drawing on accounting elements and basic principles, Tutore (2010) regards the compensation and recovery costs of resources consumption and ecological destruction as environmental costs. Wang et al. (2021) defined natural resource expenses as the decrease of natural resource assets caused by natural resource exploitation, utilization, destruction, and other activities within a certain period that result in decreases in owner’s equity, other than those relating to the profit allocation. Combined with the views of the above scholars, this study defines the water resource expenses as the decreases of water resource assets caused by the utilization and destruction of water resources in a certain period that result in decrease in owner’s equity, other than those relating to income distribution and other activities. Same as income, in addition to normal water resource outflow expenses, the expenses here should also include incidental expenditures such as resource revaluation, impairment, reclassification, and abnormal losses caused by disasters. It should also be noted that the decrease in assets referred to in the expenses not only represents the decrease in the natural resource physical volume, but also includes the decrease in the value due to pollution. If the abnormal losses caused by improper use, disaster damage, etc. can be reasonably predicted before they actually occur, in accordance with the accounting accrual principle and prudence principle, the losses to be incurred should be accrued. The specific recording method is to record an allowance for water assets on the one hand and the occurrence of losses on the other.

Similar to the “profit” defined by the IASB, natural resource profit reflects the results of natural resource development and utilization within a certain period. According to IFRS, profit equals income less expenses (Barker, 2010). In the same view, natural resource profit should be the difference between natural resource income and expenses (Wang et al., 2021). Therefore, this study believes that water resource profit can reflect the results of water resource development and utilization within a certain period, which is the difference between water resource income and expenses. Both income and expenses are both macroscopic, under which water resources profit includes not only recurring items, but also incidental items and abnormal gains and losses. Ultimately, the net water resource benefits will be periodically carried forward to owners’ equity. If the current profit is a net gain, water resource retained earnings will increase; if it is a net loss, water resource retained earnings will decrease.

3.4 Framework of a Parallel Natural Resource Reporting System

With the release of a “multi-purpose, conceptual framework” by the United Nations--SEEA 2012, countries have gradually developed their own systems of environmental-economic accounting under the guidance of the framework. China proposed to “prepare a natural resource balance sheet and implement the off-office audit of leading cadres’ natural resource assets,” which shows that China’s natural resource accounting goals are not only to reflect the natural resources “background,” but also to serve the information needs of the off-office audit of natural resource assets for government and leaders. At this stage, most of the natural resource accounting statements currently are statistical statements. These statements generally only record the actual stock and flow of regional natural resources in a certain period. Moreover, they are mostly physical accounting tables rather than value accounting statements. It is difficult to unify the measurements of various natural resources, which cannot provide direct data for the resource management performance appraisal during the tenure of leading cadres. Therefore, we require a multi-target-oriented parallel reporting system for natural resources.

Taking the government financial accounting system as an example, when facing the users of the government final accounts report, it requires the budget accounting system to provide the information of the reporting entity’s annual budget revenue and expenditure implementation results. When facing the users of government financial reports, the government financial accounting system is needed to provide the financial status and other information of the subject at a certain time. Similarly, the multi-objective orientation of natural resource accounting determines the necessity of a parallel reporting system. As Figure 1 shows, the natural resource statistical reporting system mainly serves the resource investigation and monitoring objectives, thus needs to be based on the cash basis; the accounting statement system mainly serves objectives of the resource management performance appraisal, and therefore needs to be based on the accrual basis. The formation and development of the parallel reporting system in the field of natural resource accounting lies in its dual goal orientation.

FIGURE 1. Framework of parallel water resource reporting system.

4 Form of Water Resource Statements

4.1 Presentation of Water Resource Statements

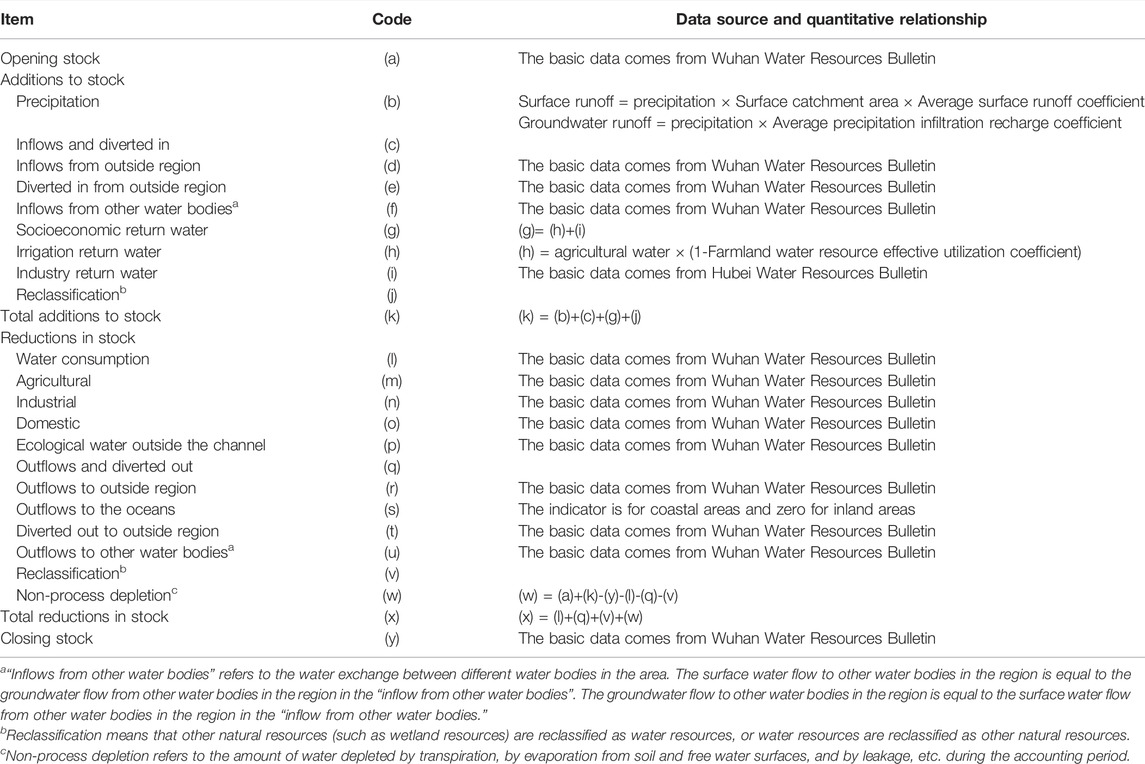

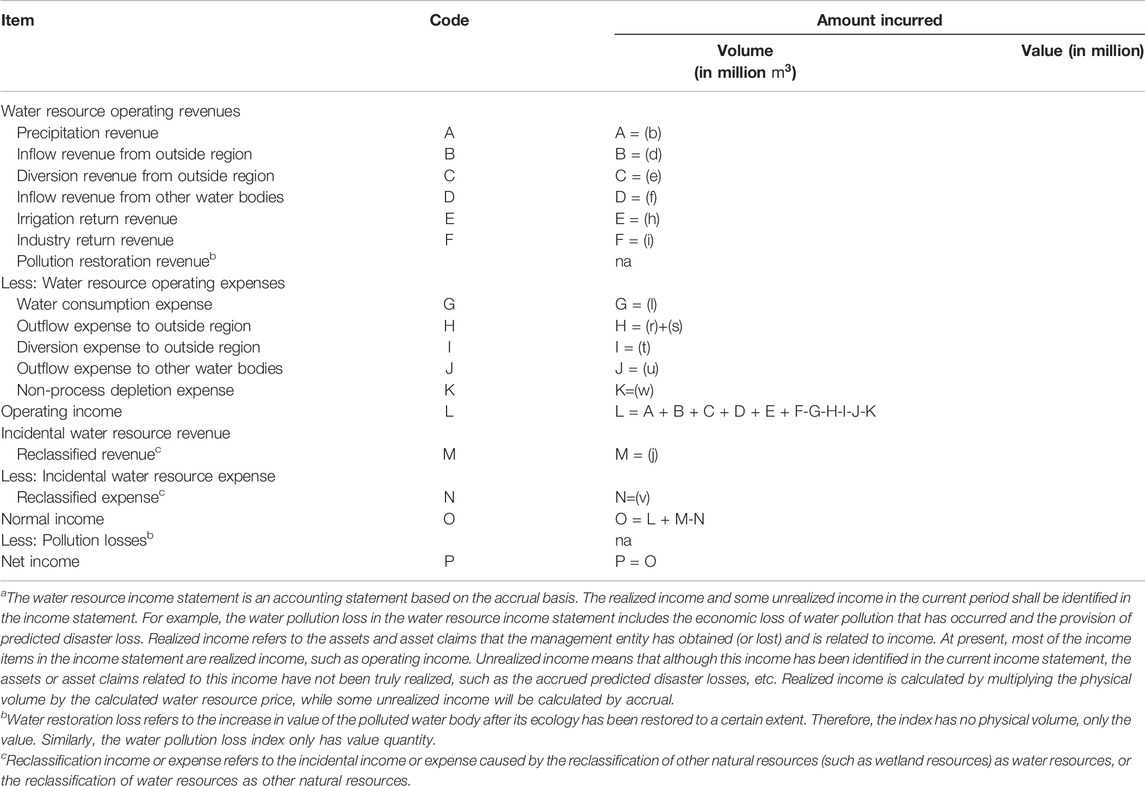

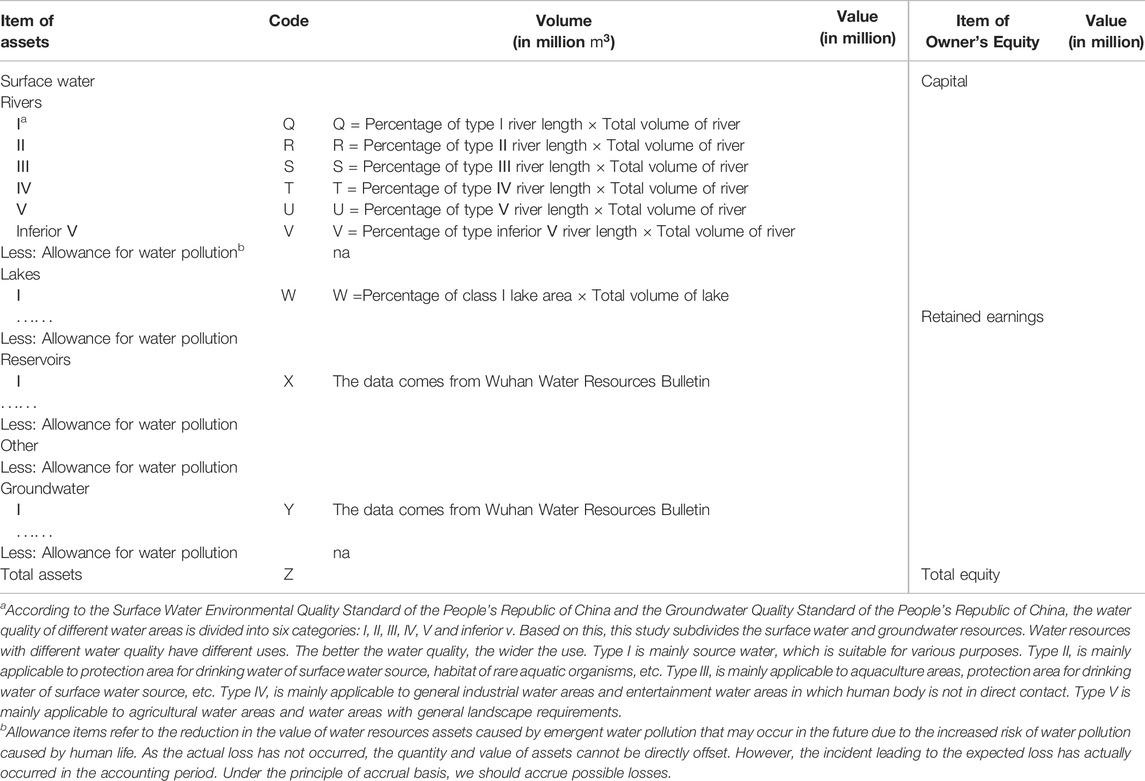

This study referred to the natural resource accounting framework system constructed by Wang et al. (2021). Based on the objectives of preparing the natural resource balance sheet in China, this study proposes the table structure of water resource accounting statements and statistical statements suitable for Chinese conditions, which includes regional water stock and change statement (Table 1), regional water resource income statement (Table 2), and regional water resource balance sheet (Table 3).

TABLE 1. Regional water stock and change statement (in 100 million

TABLE 2. Regional water resource income statementa.

TABLE 3. Regional water resource balance sheet.

4.2 Comparison With Australian Water Statements

The water resource balance sheet and related accounting accounts that China explored and prepared are not the same concept as AWAS. There are many differences between them. The Australian water accounting system has been implemented for many years and is therefore relatively mature. The formation of water rights is the foundation of the Australian water accounting system. In Australia, water rights have a mature online trading system. Therefore, accounting for water resource products and corresponding water rights is the essence of the Australian water accounting system, which is the same as the essence of accounting for intangible assets related to microeconomic entities. In contrast to the Australian water accounting system, the water resource balance sheet explored and prepared in China takes the government as the reporting subject rather than a micro-entity. The accounting object of China’s water resource balance sheet is water resources that are in the state of natural and undistributed utilization, rather than water resources products and corresponding water rights. The reporting objective of the water resource balance sheet is mainly to investigate the local water resource background and serve the off-office audit of natural resource assets. The differences between China’s water resource balance sheet and the Australian water accounting system are:

1) Accounting entity. The origin of Australian water accounting is to meet the needs of the water rights trading market. Therefore, the accounting entities of the Australian water accounting system are mostly single water subjects, such as water supply companies. On the contrary, the accounting of water resource balance sheet and related accounting accounts currently explored in China is from a national (regional) macro perspective. The accounting entities are local government departments that have the right to manage and distribute water resources.

2) Reporting objectives. The purpose of balance sheet reporting under the AWAS is to assist users (such as a single micro entity or a region) in making and evaluating decisions about the allocation of water resources. The report mainly serves the analysis, decision-making, and management of water-related activities by accounting entities. It provides support for the rational allocation of water resources and improves the water resource refined management level. However, the water resource reporting system explored in China not only reflects the value of all the assets owned by the accounting entity, with the aim of finding out the “background” and the utilization of water resources in China, but also meets the needs of the off-office audit of leading cadres’ natural resource assets. The government can judge whether regional leaders have properly performed their supervision and protection responsibilities by reporting the utilization of water resources, so as to promote environmental performance into the political performance appraisal system.

3) Accounting scope. The Australian water accounting system mainly records and reflects the change process and results of water resource products and related water rights owned by certain equity entities. In contrast, the accounting object of the water resource balance sheet and related accounts prepared in China is the natural and unallocated water resources with a government as the equity entity. It records and reflects the stock and changes of water resources under natural conditions, as well as various operating profits and losses, etc.

4) Concept of “liabilities.” As the accounting entity of the Australian water balance sheet is a single micro-enterprise and there is a market for water rights, water liabilities are reflected in debt-claim relationships between water entities. It also includes liabilities to “others” arising from exceeding their own water resources equity limit, mainly referring to present obligations that may lead to the increase in water subject’s obligations or the decrease of water assets of the water reporting entity (WASB, 2009). Australian Water Accounting conducts accounting from the perspective of micro-entities. Water liabilities defined by Australia have definite creditors and debtors, and are the incurred obligations to be performed, which meets the IASB’s definition of liabilities. However, China’s natural resource balance sheet accounting is based on the macro perspective. There is no clear creditor and repayment date for water resources. Therefore, China’s water resource balance sheet should not identify water resources liabilities.

5 Reports of Wuhan’s Water Resources

Located in the middle part of China in the Yangtze River Basin, Wuhan is the core city in the central region. In 2020, Wuhan, the most influential area in the middle reaches of the Yangtze River Basin in terms of socio-economic development, had a permanent population of 12.45 million people and a regional gross domestic product of US$226.43 thousand million. Due to the subtropical monsoon climate, rainfall in Wuhan is abundant all year. As shown in Figure 2, the rivers in the city are longitudinal and horizontal. The lakes and ports are intertwined. The total water area of the whole city is 2,217.6 km2, accounting for 26.1% of the land area (8,494.41 km2) of the whole city (Zhang et al., 2019). Compared with other megacities in China, Wuhan has outstanding advantages in water resources. It is known as the “River City” and “City of Hundreds of Lakes,” with 165 rivers and 166 lakes. Wuhan is rich in fresh water resources as well as possesses the largest water area among large cities in China (Li et al., 2017). The Yangtze River and its largest tributary, the Han River, traverse the center of the city and divide the central city of the Wuhan into three parts, forming the three towns of Wuchang, Hankou, and Hanyang across the river (Zhang et al., 2019). Because of its superior geographical position and convenient waterways, the city has grown rapidly, which has become an integrated transport hub in China.

FIGURE 2. Geographical distribution of Wuhan's water resources (Source: Zhang et al., 2019).

In recent years, Wuhan has improved the management and protection of water resources and the environment. Many relevant regulations have been formulated, such as the Wuhan City Regulations for Water Conservation and the Wuhan Flood Control Ordinance, which led to the gradual legalization of urban water environment management. In 2017, Wuhan carried out the river chief system. A strict assessment and accountability mechanism began to be implemented in Wuhan.

5.1 Data Sources

The corresponding basic data were mainly obtained from Wuhan water resources bulletin and Hubei province water resources bulletin. Based on statistical data, this study took the water resources in Wuhan as an example to prepare water resource stock and change statement, water resource income statement, and water resource balance sheet. Learn from the ideas and sample formats developed by scholars, firstly, we prepared the water resource stock and change statement according to the reserves and utilization of water resources in Wuhan. Secondly, we prepared Wuhan’s water resource income statement according to the completed stock and change statement in Wuhan. Finally, we used the two statements above to prepare a water resource balance sheet for Wuhan. The water accounting process is specifically illustrated for 2019 which is the opening year of the change of government.

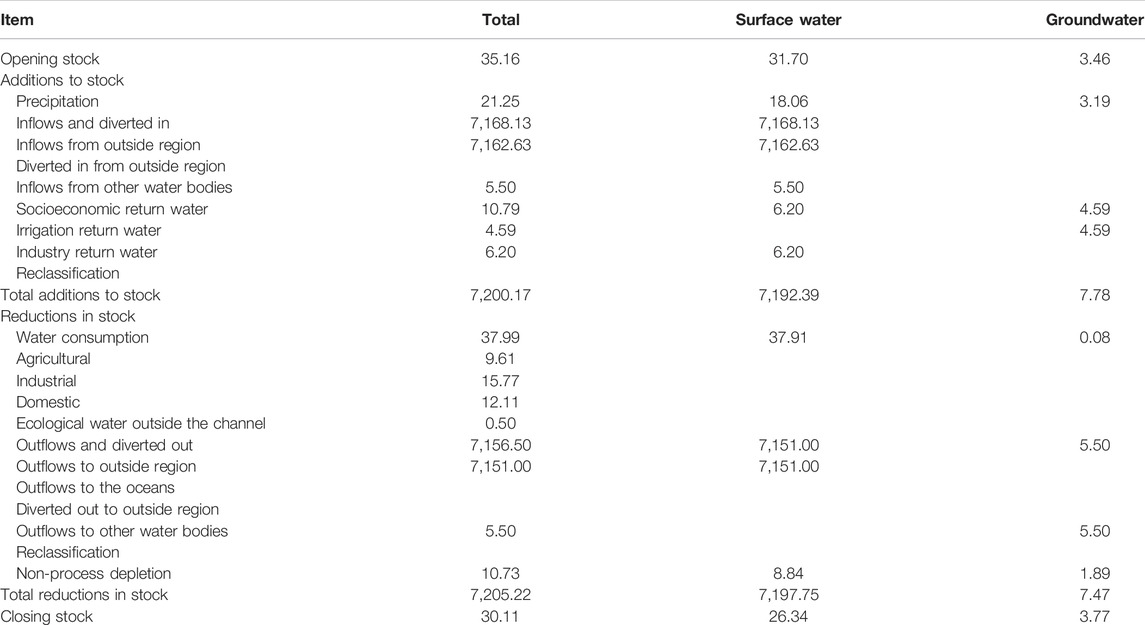

5.2 Notes on Preparation of the Stock and Change Statement

The water resource stock and change statement is a statistical report based on the cash basis. The water resource stock and change statement mainly includes three parts: The first part is the beginning stock balance and the ending stock balance, which means the stock at the beginning and the end of a period. The second part is the increase in stock because of natural reasons (such as water inflow, precipitation) and human activities (such as return flow). The third part is the reduction of stock, which is due to human activities (such as water withdrawal) and natural reasons (such as water outflow, non-process depletion). Especially, the index, average runoff coefficient, required in precipitation is calculated by using the average runoff coefficient 0.85 in Wuhan urban area obtained by Hong et al. (2014) In addition, due to the lack of precipitation infiltration recharge coefficient in Wuhan, this paper adopts the precipitation infiltration recharge coefficient of 0.15 (Wang 2015) in Xiangyang, Hubei Province, which belongs to the same plain area as Wuhan and has a similar environment to Wuhan.

The “non-process depletion” in the stock and change statement is a difficult index to understand and has certain uncertainty. The indicator is interpreted in the National Water Resources Comprehensive Planning Technical Regulations in China as the amount of water depleted by transpiration, by evaporation from soil and free water surfaces, and by leakage, etc. during the accounting period. Specifically, the non-process depletion of surface water mainly consists of the evaporation of surface water such as rivers, lakes, and reservoirs and the drainage evaporation of drainage facilities; the non-process depletion of groundwater mainly includes the evaporation of shallow groundwater. There is a view that the evaporation of this indicator has already been fully considered in the process of obtaining the “precipitation” indicator (Kuczera, 1982; Gabos and Gasparri, 1983). Therefore, this indicator should not be recalculated in the stock and change statement. However, in the practice of water balance analysis and calculation, the basic data required for preparation of water resource stock and change statements have not been fully incorporated into the daily statistical monitoring work of the management department. It is a universal phenomenon that some data is missing in the physical accounting of water resources. In addition, the division of responsibilities of relevant departments and other reasons will also lead to the absence of some crucial data or larger numerical differences in similar data (Song et al., 2019), resulting in poor accuracy of physical accounting, which makes the equation “the ending balance = the beginning balance + change” unbalanced. Therefore, we introduce the “non-process depletion” to keep the balance of the whole statement (Wang et al., 2016), and obtain Wuhan’s water resource stock and change statement in 2019 (Table 4).

TABLE 4. Wuhan’s water resource stock and change statement in 2019 (in 100 million m3).

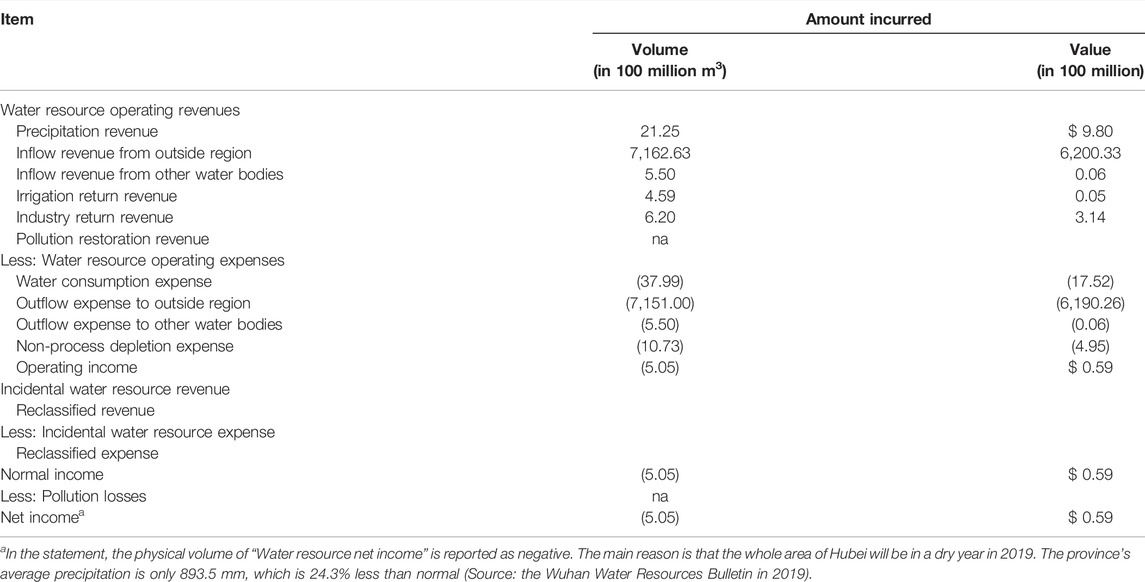

5.3 Notes on Preparation of the Income Statement

The physical accounting in the water resource income statement is based on the accrual basis. The income statement is an accounting statement based on the accrual basis, which reflects the amount of various accrued revenues and expenses of water resources over a period. However, there are few revenues receivable in water resource accounting. Thus, the increase in the stock and change statement corresponds to the physical volume of the water resources operating revenues respectively. Similarly, the decrease in the stock and change statement corresponds to the physical volume of the water resources operating expenses respectively. The water pollution restoration revenues and water pollution losses only involve value, not physical quantities. Therefore, these items cannot correspond to the stock and change statement.

The monetary value accounting of the water resource income statement should be based on the view that there are value differences in water resources of different water quality. In social life, the quality of water resources determines the different uses of water resources, which makes the prices of water resources different as well. Generally speaking, the water quality of the water resources formed by precipitation is affected by many factors. In this study, the precipitation revenues are estimated by using the average price of water grade I, II, III, IV, and V. Industry return revenues, which are the return of industrial water, are calculated by the price of water resources of the IV. Irrigation return water is generally agricultural water discharged or infiltrated from fields and channels into the ground, which eventually becomes a reusable water source. Therefore, the revenue is accounted relied on the price of V water resources. Social water consumption expenses are based on the stage-separated water prices in Wuhan. In particular, in the social water consumption, ecological water consumption, which is mostly the loss caused by evaporation and transpiration, is calculated based on the water resource prices of I, II, and III water quality because of good water quality. Regarding the inflow from the outside regions, the water quality is different when different rivers flow into the area. In principle, we should account for the inflow revenues of each river separately. However, 99% of the water that flows into Wuhan comes from the Yangtze River, Hanjiang River, and the rivers of Daoshui, Sheshui and Jushui. In addition, when the five rivers flow into the area, the water quality of these five rivers is II or III. Thus, based on the principle of materiality, this study takes the price of I, II, and III water resources as the unit inflow revenue from the outside regions. The inflow revenue that should be calculated separately is calculated by multiplying the total inflow by the unit income. For the outflow expense to the outside regions, the calculation method is the same as the above inflow revenue. Therefore, we take the prices of I, II, and III water resources as the unit outflow expense to the outside regions, multiplying the total outflow by the unit expense to obtain the outflow expense. Wuhan’s water resource income statement in 2019 is presented in Table 5.

TABLE 5. Wuhan’s water resource income statement in 2019.

5.4 Notes on Preparation of the Balance Sheet

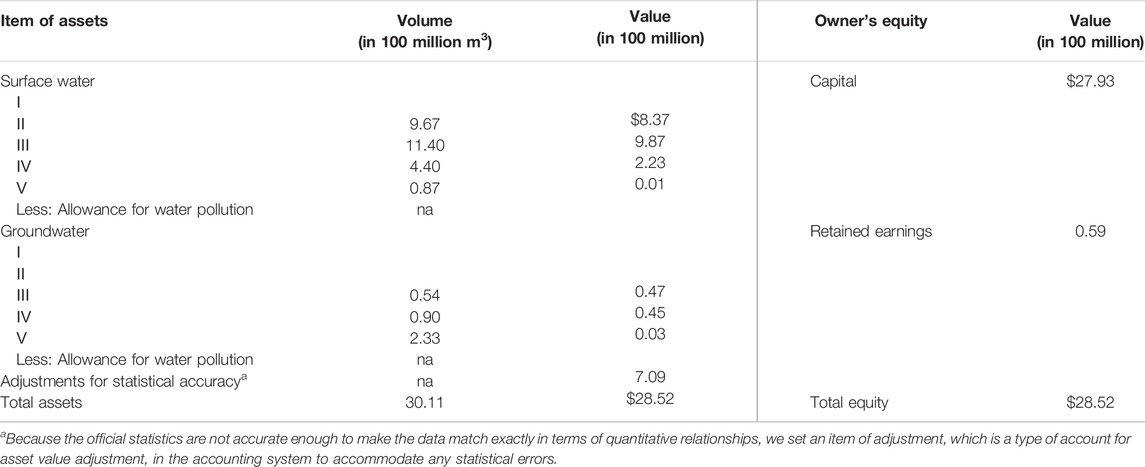

5.4.1 Accounting Based on Physical Volume

As accounting for the physical volume of water resources assets, the differential classification of water resources should be proposed according to the type of water quality. As water resources, different water quality levels directly affect their practical applications. Therefore, it is necessary to classify assets according to water quality types when accounting for water resources assets. In surface water, the total physical volume of water resources, which have different water quality, in rivers and lakes is usually not directly obtained from the Water Bureau. Therefore, the calculation formula for the total physical volume of water resources in rivers or lakes is as follows:

Where

However, the total water resources of rivers and lakes in Wuhan have not been announced separately. It is impossible to account for the water resources of rivers and lakes separately in Wuhan. Moreover, Wuhan has not released the percentage of river length with different water quality. We adopt the total surface water resources and the percentage of river sections with different water quality (the percentage of the number of river sections with different water quality to the total number of sections) to account for the physical volume of surface water. Since people’s production and domestic water mainly comes from rivers, it is reasonable to measure the proportion of total surface water with different water quality by the percentage of river section (Yang, 2016).

5.4.2 Accounting Based on Value

The water resource balance sheet mainly involves two aspects in the value quantity accounting: On the one hand, we need to calculate the book balance of water resource assets. On the other hand, we estimate and accrue the relevant losses.

1) Book value of assets

Due to the limitation of data acquisition, it is currently difficult to calculate the ecological value of water resource assets. The value of water resource assets described in this study in a narrow sense only refers to the economic value. The economic value of water resource assets is calculated as follows:

Where

Water resources with different water quality can meet different needs. According to different purposes, the value of water resources with different water quality is also different, which means that high-quality water resources have higher prices. Due to the absence of unified pricing of water resources, we refer to the stage-separated water price in Wuhan, determining the value of water resources according to the different uses of different water quality. I, II and III water resources are mainly used for drinking and aquaculture. There is no significant difference in functions for I, II and III water resources. Therefore, the price of I, II and III water resources is calculated according to the average price of domestic water and special industry water, which is $0.86565 m−3 (converted to USD at the 2020 exchange rate, 1USD = 6.8974CNY. The prices below are also converted to USD at this same rate). Type IV water resources mainly apply to general industrial purposes. Therefore, the price of such water resources is calculated by the price of non-residential water of $0.50605 m−3. Type V is mainly applicable to agriculture water and general landscape requirements. The price of this kind of water is calculated by the agricultural water price of $0.0116 m−3 (according to the Investigation Report on the Comprehensive Reform of Agricultural Water Price in Hubei Province issued by the Water Conservancy Bureaus of Hubei Province). Inferior V water body basically has no useful function, so the value is $0.

2) Provision for allowances

Based on the accrual and prudent principles, for events that have already occurred and are likely to lead to catastrophic consequences and cause significant losses in the future, the potential losses caused by the events should be estimated. The abnormal losses of water resources are generally caused by pollution, commonly for emergent water pollution accidents. There is no regular discharge mode for unexpected water pollution accidents. These accidents are sudden and fierce, often discharging a large number of harmful pollutants into the river in a short time. When a water pollution accident occurs, the water body with excellent water quality quickly becomes inferior V water quality, so that the water body has no useful function. Thus, the polluted water resources pose a great threat to human health and life safety. Moreover, these threats restrict the ecological balance and socio-economic development (Schwarzenbach et al., 2010; Wang et al., 2018). Because of the unpredictability of environmental pollution accidents, it is difficult to estimate the losses. Therefore, the allowance items for water resource assets involved in the balance sheet lack objective data as a basis, which makes it difficult to recognize the allowance items. In this study, the following formula is used to estimate the accident loss. Based on the historical maximum economic loss caused by similar accidents, the loss provision shall be calculated in a certain proportion, which can be the ratio of the physical amount of pollutants leaked by the two accidents or the ratio of the change of water resource pollutant concentration after the accident.

Where D is the accrued amount of accident loss;

3) Identification of owner’s equity

In the owner’s equity of water resources, the water resource capital is the water resources assets owned by Wuhan when the previous leading cadre left office. The retained earnings of water resources are the sum of the net income of water resources over the years during the tenure of this leading cadre. In September 2018, the leadership of Wuhan was changed. the water resource capital of Wuhan in 2019 is the balance of water resource assets when the last leader left office (at the end of 2018). The retained earnings are only the carry-over of net income of water resources in 2019. The owner’s equity and retained earnings of water resources in 2019 can be determined. However, because the official statistics are not accurate enough to make the data of assets and owner’s equity match exactly in terms of quantitative relationships, we set a type of account for asset value adjustment, “Adjustments for statistical accuracy,” in the accounting system to accommodate any statistical errors and balance the statement.

5.5 Provision for Possible Losses in an Assumed Scenario

At present, there are no significant risk factors for water resources in Wuhan, which makes the risk level of water pollution low, so it is not necessary to accrue the predicted disaster losses of water resources. However, in order to specify the methods and procedures for accruing water pollution loss and water resources allowance, the scenario is set here.

It was assumed that a chemical plant, located near Pinghumen waterworks in Wuchang of Wuhan, was registered and operated in 2008. The industry to which this chemical plant belongs is chemical raw materials and chemical products manufacturing. Their company business scope covers ethylbenzene organic compound products such as m-hydroxybenzoic acid and anisole. In recent years, due to the sluggish production and operation of the chemical enterprise and the obsolete chemical equipment of the enterprise, the storage tank for storing chemical raw material benzene has reached its serovice life but has not been replaced. Moreover, owing to the shortage of funds, the company was forced to lay off a large number of employees, thereby increasing the workload of on-the-job operators. However, the induction training for new employees is shortened. Employees lack targeted training, which leads to employees being unfamiliar with the operational requirements of the operating system, physical and chemical characteristics and production process. To summarize, the safety management of the enterprise is unqualified. In 2019, Wuhan Environmental Protection Bureau conducted a risk assessment on this company. After the assessment, it is considered that this plant has a high risk of water pollution and is prone to occur environmental pollution accidents. In case of explosion or chemical leakage, about 25 tons of benzene raw materials in the plant will flow into the Yangtze River, resulting in serious water pollution. Thus, relevant departments need to accrue the predicted disaster loss of water resources.

This study takes the economic losses caused by the water pollution incident of Songhua River in 2005 as the reference data for this accrual. On 13 November 2005, an explosion occurred in the first workshop of the double benzene plant of Jilin Petrochemical Company. After the explosion, about 100 tons of benzene (nitrobenzene, etc.) flowed into the Songhua River, causing serious pollution of the river water and affecting millions of residents along the coast. Through the accounting of direct or indirect losses of socio-economic activities, residents’ health and ecological environment, the economic loss of Songhua River water pollution incident is $236.03 million (Hou, 2013). Referring to the above loss accrual method, the water resources loss to be accrued in Wuhan in 2019 is $236.03 × 25/100 = $59.01 million.

Therefore, in this scenario, an allowance of $59.01 million for water pollution as well as water pollution losses of $59.01 million is recognized for Wuhan in 2019.

It should be noted that the provision for water pollution losses made here is only the result of accrual-basis book keeping in an assumed scenario. This is only an example of the application of the accrual principle to water resource accounting and is not a real situation. That’s why the related items are not presented in the Wuhan’s water resource income statement or balance sheet in 2019 (presented in Table 6).

TABLE 6. Wuhan’s water resource balance sheet in 2019.

5.6 Discussion

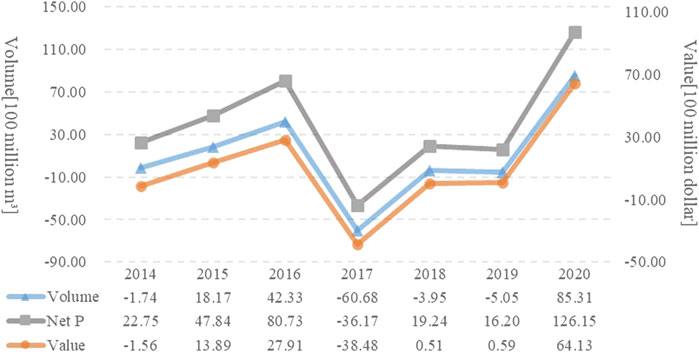

The accounting results show that the closing stock of water resources in Wuhan has decreased compared to the opening stock. The decrease in water stocks was mainly due to the drought that hit Hubei Province in 2019. Precipitation in Hubei Province in 2019 was about 24.3% less than that in a normal year. The decrease in natural precipitation led to the Wuhan’s water stock reduction in 2019. Therefore, relevant departments need to advocate enterprises and individuals to adopt water-saving and water protection measures. In addition, it can be seen from the stock and change statement that surface water is the most important part of water resources in Wuhan, accounting for more than 80%, which shows that Wuhan needs to continue to pay more attention to surface water in the future to ensure its stable supply and water quality. Moreover, there is a special phenomenon in the income statement that needs to be explained. It can be seen from Wuhan’s water resource income statement that the physical volume of net income in 2019 was negative, while its value quantity was positive. This indicates that the physical volume of water resources in 2019 was lower than that in the previous year, but the water value increased because of the improvement of water quality. These data show that the water purification activities in Wuhan have achieved certain effects. The water resource management during this leadership term was successful, which made the water quality of Wuhan better than before.

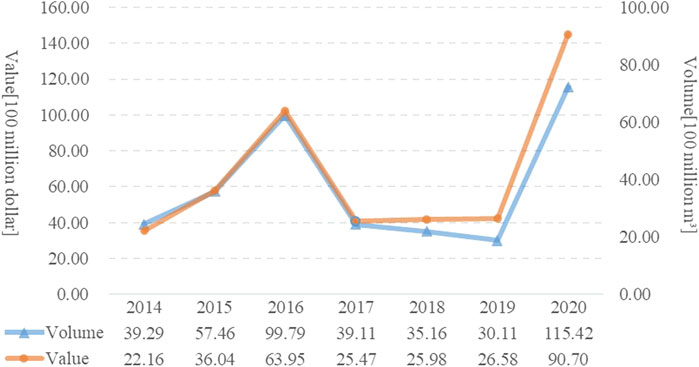

Further, according to Wuhan’s comparative water resource income statement and comparative water resource balance sheet during 2014–2020 (Supplementary Appendix Tables S2A,S2B, S3A,S3B), we obtain the changes of Wuhan’s net water income and net water assets both in volume and value during this period (Figures 3, 4). By comparing the physical volume of Wuhan’s net water income with that of the difference between precipitation and evapotranspiration during 2014–2020, it can be seen that changes of the former are basically synchronized with changes of the latter (as shown in Figure 3). This indicates the changes of Wuhan’s net water income in physical volume depend more on those of precipitation and evapotranspiration than any other human cause.

FIGURE 3. Changes of Wuhan’s net water income both in volume and value during 2014–2020. Note: Net P refers to Net Precipitation, which is obtained from precipitation minus evapotranspiration.

FIGURE 4. Changes of Wuhan's net water assets both in volume and value during 2014–2020.

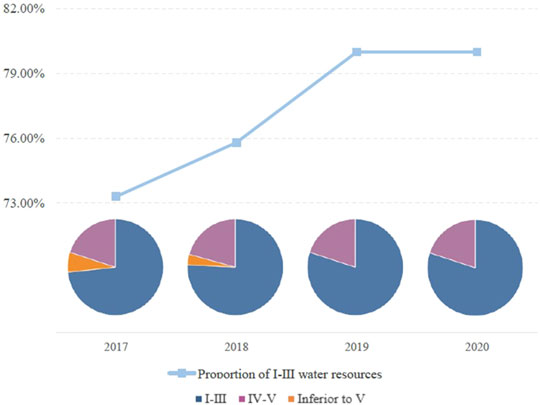

On the other hand, as shown in Figures 3, 4, before 2017, the change curve of the value overlaps exactly that of the physical volume, which means the quality of Wuhan’s water resources remained almost the same during that period. However, both Figures 3, 4 show that there was a marked change after 2017. It can be seen from Figure 3 that in the year of 2017, there was a significant increase in both the value and physical volume of Wuhan’s net water income, with the former maintaining a higher growth rate since then. And according to Figure 4, during 2017–2019, the value of Wuhan’s water has kept increasing despite the declining water volume, which indicates a significantly improved quality of Wuhan’s water resources. This is further confirmed by the fact that after 2019 the value of Wuhan’s water increased at a steadily greater rate than the volume. In addition, as shown in Figure 5, from 2019 to 2020, the inferior to V water resources in Wuhan have disappeared, and the proportion of Ⅰ-Ⅲ water resources in the total surface water has gradually increased. From this, it can be clearly seen that since 2017, the proportion of high-quality water resources in Wuhan has gradually increased.

FIGURE 5. Proportion of surface water with different water quality from 2017 to 2020.

After 2017, the deviation between the value curve and the volume curve either for the net water income or net water assets and the increased proportion of high-quality water resources may result from the efforts the local government has made to protection of water resources since the release of related policies (such as those of natural resource balance sheeting and off-office auditing of natural resource assets) in 2015. After 2 years of implementation, Wuhan has made some progresses in comprehensive water resource supervision and pollution control, which suggests that the off-office auditing of natural resource assets and other leadership accountability system have a positive role on local government’s performance in water resources management.

6 Conclusion

6.1 Summary

Preparation of water resource balance sheet forms the basis of regional environmental governance and is of great importance for achieving the sustainable regional development. This study attempts to collect and process the recent statistics of Wuhan’s water resources within the framework of a parallel reporting system, and to prepare a water resource balance sheet and other essential supporting statements which are for reporting and analyzing Wuhan’s water resources. These construct a water resource accounting system oriented to different objectives. The results show that during 2014–2020 the physical volume of Wuhan’s water resources fluctuated with net precipitation to a large extent. Since 2017, the value of Wuhan’s water has kept increasing even though the water volume of 2017–2019 still declined due to the earlier drought. This demonstrates a relatively better water management performance during the current terms of office, which indicates a positive role of the leadership accountability system based on natural resource balance sheeting that is being implemented in China. This study contributes to the literature on regional water resources accounting and environmental management. The water resource balance sheet, income statement, and stock and change statement prepared for Wuhan, Hubei, China have a good level of generality. They provide a reliable basis for the local government’s performance assessment of water resources management and facilitate the implementation of water resource related policies.

The development of a parallel reporting system for natural resources is not an end in itself, but it is the groundwork for implementing a leadership accountability system and improving regional environmental management. The initial practices so far have suggested that the leadership accountability for natural resource assets has a positive effect on achieving resource and environmental protection and sustainable regional development. It is reasonable to believe that improving the regional natural resource accounting system will help facilitate this process.

6.2 Limitations and Future Work

In the process of research, we also found that there are still some problems in China’s water resource reporting system, which are worth discussing.

Firstly, the preparation method of water resource stock and change statement is not mature. For example, Non-process depletion data are extremely difficult to obtain. Under the existing monitoring technology, this index cannot be obtained through conventional calculation or evaluation, resulting in poor accuracy of stock and change statement. This requires the relevant department staff to strengthen the statistics of water resource monitoring information. It also puts forward new requirements for the professional ability and work content of personnel in relevant water resource management departments.

Secondly, the main body of water resources management is not clear, making the statistical scope of water resources overlap and the statistical caliber is not unified. The jurisdiction of China’s water resources involves multiple government departments. Sometimes, there are situations such as overlapping management objects or functional conflicts, resulting in the lack, error or repeated statistics of some key statistical data, which cannot reflect the real situation of national or regional water resources. Therefore, preparation of the water resource balance sheet should clarify the unified management entity, which can not only ensure the unification of resource classification, data statistics and report format, but also ensure the efficiency and effect of information transmission.

Finally, there is no accounting report on the value of water environment. Water resources integrate resources, environment and ecological attributes. However, due to the complexity of water environmental capacity measurement and lack of measuring means and basic data, only the economic value of Wuhan’s water resources is taken into account. In the future, China needs to issue technical guidelines for water environment value assessment in order to improve the fairness and reliability of water resources valuation. The formulation of a unified value method is conducive to solving the problem that China’s current water environment value cannot be fully reflected.

Data Availability Statement

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding author.

Author Contributions

JL: Investigation, data curation, writing- original draft preparation and editing. ZW: Conceptualization, methodology, writing- reviewing and editing, supervision. LY: Investigation, methodology. YL: Writing- reviewing and editing.

Conflict of Interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s Note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Acknowledgments

The authors would like to express our sincerest gratitude to the Hubei Provincial Statistics Bureau for their kind offering of some essential data that have not been made public.

Supplementary Material

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenvs.2022.902622/full#supplementary-material

References

Barker, R. (2010). On the Definitions of Income, Expenses and Profit in IFRS. Account. Eur. 7 (2), 147–158. doi:10.1080/17449480.2010.511892

Borrego-Marín, M. M., Gutiérrez-Martín, C., and Berbel, J. (2016). Estimation of Cost Recovery Ratio for Water Services Based on the System of Environmental-Economic Accounting for Water. Water Resour. Manage 30, 767–783. doi:10.1007/s11269-015-1189-2

Bright, G., Connors, E., and Grice, J. (2019). Measuring Natural Capital: towards Accounts for the UK and a Basis for Improved Decision-Making. Oxf. Rev. Econ. Policy 35 (1), 88–108. doi:10.1093/oxrep/gry022

Central Committee Communist Party of China (CCCPC) (2013). Decision on Major Issues Concerning Comprehensively Deepening Reforms. Available at: http://politics.people.com.cn/n/2013/1116/c1001-23560979-14.html (Accessed September 24, 2021).

Charpleix, L. (2017). “Accounting for Water,” in Water Policy, Imagination and Innovation. Editors B. Robyn, N. Louise, W. Jacqueline, and H. Stephen (London: Routledge), 84–112. doi:10.4324/9781315189901-6

Collis, J., Holt, A., and Hussey, R. (2010). The Conceptual Framework for Financial Reporting. Cambridge, UK: International Accounting Standards Board.

Costanza, R., d'Arge, R., De Groot, R., Farber, S., Grasso, M., Hannon, B., et al. (1997). The Value of the World's Ecosystem Services and Natural Capital. Nature 387 (6630), 253–260. doi:10.1038/387253a0

Costanza, R., Kubiszewski, I., Giovannini, E., Lovins, H., McGlade, J., Pickett, K. E., et al. (2014). Development: Time to Leave GDP behind. Nature 505, 283–285. doi:10.1038/505283a

Daly, H. E., and Cobb, J. B. (1989). For the Common Good: Redirecting the Economy Towards Community, the Environment, and A Sustainable Future. Boston, MA: Beacon Press.

Danoucaras, A., and Woodley, A. (2013). “Alignment and Differences between the Australian Water Accounting Standard and the Water Accounting Framework for the Minerals Industry,” in Proceedings of the 2013 Water in Mining Conference. Editor C. Moran (Australia: The Australasian Institute of Mining and Metallurgy), 85–90.

Edens, B., and Graveland, C. (2014). Experimental Valuation of Dutch Water Resources According to SNA and SEEA. Water Resour. Econ. 7, 66–81. doi:10.1016/j.wre.2014.10.003

Edens, B. (2013). Reconciling Theory and Practice in Environmental Accounting. The Hague, Netherlands: Statistics Netherlands.

Eigenraam, M., and Obst, C. (2018). Extending the Production Boundary of the System of National Accounts (SNA) to Classify and Account for Ecosystem Services. Ecosyst. Health Sustain. 4 (11), 247–260. doi:10.1080/20964129.2018.1524718

Falkenmark, M., and Widstrand, C. (1992). Population and Water Resources: a Delicate Balance. Popul. Bull. 47 (3), 1–36.

Gabos, A., and Gasparri, L. (1983). Monthly Runoff Model for Regional Planning. Water Int. 8, 42–45. doi:10.1080/02508068308686000

Gan, H., and Gao, M. X. (2008). Basis and Thoughts on Creating the System of Environmental-Economic Accounting for Water (SEEA-W) of China. China Water Resour. 17, 1–5. doi:10.3969/j.issn.1000-1123.2008.17.002

Gleick, P. H. (2016). Water Strategies for the Next Administration. Science 354 (6312), 555–556. doi:10.1126/science.aaj2221

Gonzalez-Martinez, A. C., and Schandl, H. (2008). The Biophysical Perspective of a Middle Income Economy: Material Flows in Mexico. Ecol. Econ. 68 (1-2), 317–327. doi:10.1016/j.ecolecon.2008.03.013

Hartwick, J. M. (1990). Natural Resources, National Accounting and Economic Depreciation. J. Public Econ. 43 (3), 291–304. doi:10.1016/0047-2727(90)90002-y

He, C., Harden, C. P., and Liu, Y. (2020). Comparison of Water Resources Management between China and the United States. Geogr. Sustain. 1 (2), 98–108. doi:10.1016/j.geosus.2020.04.002

Hong, G. P., Liu, J. H., Wan, J., Liu, X. D., Ye, L. M., Li, L., et al. (2014). Risk Regionalization of Waterlogging Easy to Happen in Downtown Wuhan. The 31st Annual Meeting of China Meteorological Society S4 Extreme Climate Events and Disaster Risk managementClimate Change and Low Carbon Development Committee. Beijing, ChinaChina Meteorological Society: National Climate Center.

Hou, Y. (2013). Discussion on Economic and Social Loss Assessment of Water Pollution Accident in Songhua River. Apprais. J. China (04), 38–42. doi:10.3969/j.issn.1007-0265.2013.04.010

Husband, W. H. (1926). The Accrual Principle Applied to Bank Accounting. Acc. Rev. 1 (2), 85–89. doi:10.2307/238823

IASB (International Accounting Standards Board) (2014). “IFRS 15 Revenue from Contracts with Customers,” in International Financial Reporting Standards: A Guide through IFRS Official Pronouncements (London: The IFRS Foundation). A683–A743.

IASB (International Accounting Standards Board) (2018). Conceptual Framework for Financial Reporting. London: International Accounting Standards Board.

Johnson, N., Revenga, C., and Echeverria, J. (2001). Managing Water for People and Nature. Science 292 (5519), 1071–1072. doi:10.1126/science.1058821

Ker, I. R., and Hartley, W. C. F. (1970). An Introduction to Business Accounting for Managers. Operational Res. Q. 21 (2), 294. doi:10.1057/jors.1970.5810.2307/3008167

Khan, A., and Mayes, S. (2009). Transition to Accrual Accounting. Tech. Notes Manuals 2009 (002), 1. doi:10.5089/9781462371730.005

Kuczera, G. (1982). On the Relationship between the Reliability of Parameter Estimates and Hydrologic Time Series Data Used in Calibration. Water Resour. Res. 18 (1), 146–154. doi:10.1029/WR018i001p00146

Kurunmaki, L. (1999). Making an Accounting Entity: the Case of the Hospital in Finnish Health Care Reforms. Eur. Account. Rev. 8 (2), 219–237. doi:10.1080/096381899336005

Lal, R. (2015). World Water Resources and Achieving Water Security. Agron. J. 107 (4), 1526–1532. doi:10.2134/agronj15.0045

Lange, G. M.FAO Forestry Department (2004). Manual for Environmental and Economic Accounts for Forestry: a Tool for Cross-Sectoral Policy Analysis. Available at: https://agris.fao.org/agris-search/search.do?recordID=XF2016041993 (Accessed September 24, 2021).

Laurans, Y., Rankovic, A., Billé, R., Pirard, R., and Mermet, L. (2013). Use of Ecosystem Services Economic Valuation for Decision Making: Questioning a Literature Blindspot. J. Environ. Manag. 119, 208–219. doi:10.1016/j.jenvman.2013.01.008

Leipert, C. (1989). National Income and Economic Growth: the Conceptual Side of Defensive Expenditures. J. Econ. Issues 23 (8), 843–856. doi:10.1080/00213624.1989.11504942

Li, F., Zhang, J., Jiang, W., Liu, C., Zhang, Z., Zhang, C., et al. (2017). Spatial Health Risk Assessment and Hierarchical Risk Management for Mercury in Soils from a Typical Contaminated Site, China. Environ. Geochem. Health 39 (4), 923–934. doi:10.1007/s10653-016-9864-7

Meade, J. E., and Stone, R. (1941). The Construction of Tables of National Income, Expenditure, Savings and Investment. Econ. J. 51 (202/203), 216–233. doi:10.2307/2226254

Mia, A. H. (2005). “The Role of Government in Promoting and Implementing Environmental Management Accounting: the Case of Bangladesh,” in Implementing Environmental Management Accounting: Status and Challenges. Editors P. M. Rikhardsson, M. Bennett, J. Bouma, and S. Schaltegger (Dordrecht: Springer), 297–320. doi:10.1007/1-4020-3373-7_15

Morton, H., Winter, E., and Grote, U. (2016). Assessing Natural Resource Management through Integrated Environmental and Social-Economic Accounting. J. Environ. Dev. 25 (4), 396–425. doi:10.1177/1070496516664385

Nordhaus, W. D., and Tobin, J. (1972). “Is Growth Obsolete?,” in Economic Research: Retrospect and Prospect. Editors W. D. Nordhaus, and J. Tobin (New York: National Bureau of Economic Research).

OECD (Organisation for Economic Co-operation and Development) (2007). OECD Environmental Performance Reviews: China. Paris: OECD Publishing.

Ogilvy, S., Burritt, R., Walsh, D., Obst, C., Meadows, P., Muradzikwa, P., et al. (2018). Accounting for Liabilities Related to Ecosystem Degradation. Ecosyst. Health Sustain. 4 (11), 261–276. doi:10.1080/20964129.2018.1544837

Oki, T., and Kanae, S. (2006). Global Hydrological Cycles and World Water Resources. Science 313 (5790), 1068–1072. doi:10.1126/science.1128845

Qin, C., Gan, H., Wang, L., Jia, L., You, J., and Zhou, P. (2017). Designing the Statement Form of Physical Balance Sheet of Water Resources. J. Nat. Resour. 32, 1819–1831. doi:10.11849/zrzyxb.20161021

Recuero Virto, L., Weber, J.-L., and Jeantil, M. (2018). Natural Capital Accounts and Public Policy Decisions: Findings from a Survey. Ecol. Econ. 144 (feb), 244–259. doi:10.1016/j.ecolecon.2017.08.011

Richter, B. D., Mathews, R., Harrison, D. L., and Wigington, R. (2003). Ecologically Sustainable Water Management: Managing River Flows for Ecological Integrity. Ecol. Appl. 13 (1), 206–224. doi:10.1890/1051-0761(2003)013[0206:eswmmr]2.0.co;2

Schwarzenbach, R. P., Egli, T., Hofstetter, T. B., Von Gunten, U., and Wehrli, B. (2010). Global Water Pollution and Human Health. Annu. Rev. Environ. Resour. 35, 109–136. doi:10.1146/annurev-environ-100809-125342

SEPA (State Environmental Protection Administration of China), NBS(National Bureau of Statistics) (2006). Research Report on China’s Green National Economic Accounting 2004. Environ. Prot. 18, 22–29. doi:10.3969/j.issn.0253-9705.2006.18.007

Sheng, M. Q., and Yao, Z. Y. (2017). Discussion on the Establishment of Natural Resources Balance Sheet Based on the Government. Audit Econ. Res. 32 (01), 59–67.

Smith, R. (2020). Users and Uses of Environmental Accounts: A Review of Select Developed Countries. Washington, DC: World Bank.

Song, M., Zhu, S., Wang, J., and Wang, S. (2019). China's Natural Resources Balance Sheet from the Perspective of Government Oversight: Based on the Analysis of Governance and Accounting Attributes. J. Environ. Manag. 248, 109232. doi:10.1016/j.jenvman.2019.07.003

Sutton, D. B., Cordery, C. J., and van Zijl, T. (2015). The Purpose of Financial Reporting: The Case for Coherence in the Conceptual Framework and Standards. Abacus 51 (1), 116–141. doi:10.1111/abac.12042

Tang, Y., Zhou, Q., and Jiao, J.-L. (2020). Evaluating Water Ecological Achievements of Leading Cadres in Anhui, China: Based on Water Resources Balance Sheet and Pressure-State-Response Model. J. Clean. Prod. 269, 122284. doi:10.1016/j.jclepro.2020.122284

Trotman, K., and Gibbins, M. (2003). Financial Accounting: An Integrated Approach. 2nd edition. Australia: Thomson Nelson.

Tutore, I. (2010). Key Drivers of Corporate Green Strategy. [master’s Thesis]. [Chicago (IL)]: Edamba Summer School.

UN-Water (2008). Transboundary Waters - SharingWaters. Available at: https://www.unwater.org/water-facts/transboundary-waters/ February 24, 2022).