Ling He

Ling He Tingyong Zhong

Tingyong Zhong Shengdao Gan1

Shengdao Gan1 Jiamin Liu

Jiamin Liu Chaoya Xu

Chaoya Xu

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 14 June 2022

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.859591

To reverse the trend of ecological environment deterioration, the government tries to stimulate firms to participate in environmental governance through environmental regulation. Then, which environmental regulation tools can better drive firms to carry out environmental governance activities needs to be corroborated by empirical studies. Using a sample consisting of Chinese A-shares listed firms from 2015 to 2019, this article investigated the effects of two heterogeneous environmental regulation tools (environmental penalties and environmental subsidies) and their interactions on corporate environmental investment. The results showed that environmental penalties have a positive impact on corporate environmental investment. Furthermore, the heavier the penalty or the higher the administrative level of the penalty subject, the more pronounced is the impact of environmental penalties on corporate environmental investment. Firms that receive environmental subsidies do not increase their investment in environmental governance. A series of robustness tests further verify that penalties have a greater impact on the environment than subsidies. In addition, it is found that environmental penalties have an environmental deterrent effect on other firms in the same industry. Our work presents evidence for the economic consequences of environmental regulation and supplements the mechanism of environmental regulation affecting corporate environmental governance. Meanwhile, this article also provides essential guidance for the positive role of environmental penalties in driving corporate environmental governance and has important practical significance for emerging market countries to choose appropriate environmental regulation tools to promote corporate green development.

With the deterioration of the global ecological environment, the contradiction between economic growth and environmental carrying capacity has increased dramatically. Environmental protection has drawn increasing attention from countries around the world. Firms, as the main producer of pollutants, should take the initiative to assume responsibility for environmental governance (Huang and Lei, 2021). However, environmental resources are typically public goods with conspicuous characteristics of high risk, positive externality, and uncertainty of return. In addition, compared with general investment, environmental investment requires more financial support and has a longer payback period. Therefore, in the absence of external pressure, most firms lack the motivation to carry out environmental governance activities (Hartl, 1992; Orsato, 2006; Arouri et al., 2012; Borghesi et al., 2015). The key to encouraging firms to engage in environmental governance is to exert external pressure through government intervention. The government guides and promotes firms to participate in environmental governance through the “visible hand,” which is the key measure of the environmental governance system adopted by various countries (Leiter et al., 2011; Liu et al., 2021).

The government usually plays the role of “two hands” in environmental governance. Using environmental policies to formulate various indicators, the “punishing hand” is used to punish firms that violate or exceed the set indicators, and the “supporting hand” is used to reward firms that meet the standards. By utilizing hard and soft constraint indexes, environmental governance is internalized into the production decisions of firms. In this context, scholars have focused on the impact of the government’s “two hands” on environmental governance. For example, using Chinese data, Dong et al. (2022) and Li et al. (2021) have confirmed that imposing pollution fees or environmental taxes can effectively reduce the regional pollutant discharge. However, this result is not supported by the works of Qu and Sun (2022). They found that higher carbon tax pricing is not necessarily conducive to promoting the implementation of carbon emission reduction. Esen et al. (2021) asserted that there is a non-linear relationship between environment-related taxes and ecological balance by using data from 15 EU countries. Wang and Zhang (2020) emphasized that state subsidies could increase firms’ efforts in green governance.

Although the effects of “two hands” of government penalties and subsidies on corporate environmental responsibility have been studied separately, deficiencies remain. The first problem is that existing studies have focused on government penalties such as environmental taxes and pollution fees (Li and Peng, 2020; Li et al., 2021; Dong et al., 2022), but little attention has been paid to the impact of environmental violation penalties. Wang et al. (2003) indicated that Chinese firms have strong bargaining power with local environmental authorities in paying pollution charges, and such penalties are influenced by political factors. The disciplinary effect of environmental violation penalties on firms is greater than environmental taxes and pollution charges. On the one hand, environmental violation penalties reflect the additional administrative punishment that firms need to receive besides paying pollution charges and environmental taxes. On the other hand, firms’ environmental violations will be publicized to the public, making the firm’s violation information transparent and having a stronger impact on the firm’s economic and reputation penalties. Therefore, it is more meaningful to examine the government’s “punishing hand” from the perspective of environmental violation penalties than pollution charges and environmental taxes. The second problem is that the literature uses government subsidies as the government’s “supporting hand” to examine its impact on environmental governance (Lee et al., 2017; Wang and Zhang, 2020), while ignoring the environmental subsidies that are most relevant to the environment. Environmental subsidies and government subsidies have different incentive effects on corporate environmental investment. Government subsidies can be used for multiple aspects of a firm’s operation, and they might be embezzled or misappropriated, while environmental subsidies are mainly used for environmental governance. So it is significant to investigate the relationship between the government’s “supporting hand” and environmental governance from the perspective of environmental subsidies.

According to our survey, previous studies have not directly used empirical data to compare the impact of two different government regulation tools on corporate environmental governance. Thus, our article attempted to fill this void by using environmental violation penalties as a proxy for the “punishing hand” of the government and using environmental subsidies to measure the “supporting hand” of the government. We empirically tested the effects of two different environmental regulation tools on corporate environmental investment by using the data on Chinese A-shares listed firms from 2015 to 2019. Distinguishing the impact of environmental penalties and environmental subsidies on firms’ environmental investment behavior has important practical implications for emerging market countries to choose reasonably environmental regulation tools.

We have made several contributions to the literature in three aspects. First, we focused on the impact of two kinds of environmental regulation tools—penalties and subsidies—on firms’ environmental investment behavior. The empirical results supported that the environmental regulation tool that promotes firms to increase investment in environmental governance is environmental penalties rather than environmental subsidies. This finding enriches the research on the economic consequences of environmental regulation and provides new ideas for promoting the green development of enterprises. Second, our study broke through the limitations of the previous literature on corporate environmental investment from the perspective of corporate governance and resource constraints (Fryxell and Lo, 2003; Li et al., 2020; Zhang et al., 2022) and found that environmental penalties force firms to engage in environmental governance activities. However, based on the motivation of legitimacy, firms focus on terminal governance by purchasing or modifying environmental equipment rather than increasing investment in green innovation, which is a root governance behavior. Thus, the findings obtained in this study contribute significantly to the relevant research on the instrumental motivation of corporate environmental investment. Finally, from the perspective of environmental penalties, this article supplements the influence mechanism of environmental regulation on corporate environmental governance and also provides theoretical guidance for the government to choose effective environmental regulation tools.

The remainder of this article is organized as follows. Section 2 reviews the prior research on environmental regulation and environmental investment. Section 3 proposes the hypotheses. Section 4 describes the data and variables. Section 5 reports the empirical results. Section 6 summarizes the conclusions of the study and provides policy implications.

With the increasing consumer demand for green products and the strengthening of government environmental supervision, corporate environmental investment has become the focus of stakeholder attention. The concept of corporate environmental investment is divided into two categories: the cost theory and investment theory. According to the cost view, environmental investment is a cost burden of enterprises, that is, the total cost paid by enterprises to control pollution, which will not bring benefits to enterprises (Kim and Statman, 2012). From the perspective of investment, environmental investment has investment properties, and environmental investment subjects use their funds to improve environmental quality, which can bring economic, environmental, and social triple benefits to enterprises (Aksak et al., 2016).

A large volume of the literature has documented different motivations for firms to make environmental investments. One view holds that firms’ environmental investment is a voluntary and proactive behavior because it helps firms gain competitive advantage (Porter and Vanderlinde, 1995) and receive a good social reputation (Lundgren, 2003; Maxwell and Decker, 2006; Aksak et al., 2016). Another view, however, holds that environmental investment is an involuntary and passive action by firms under coercive pressure (Hartl, 1992; Gray and Shadbegian, 1998; Arouri et al., 2012; Maggioni and Santangelo, 2017; Liao, 2018). Environmental investment has become a strategic tool for firms to achieve multiple development goals.

Firms are rule followers and will inevitably be influenced by environmental regulation in order to survive (Gray and Shadbegian, 1998). In this context, prior research has analyzed the impact of environmental regulation on corporate environmental investment. Supporters of the view that environmental regulation inhibits corporate environmental investment believe that environmental regulation increases corporate production costs and crowds out investment in other economic projects, all of which contribute to the lack of enthusiasm and motivation for enterprises to assume environmental responsibility (Orsato, 2006; Arouri et al., 2012). Conversely, arguments in favor of the role of environmental regulation as a catalyst for environmental investment claim that environmental regulation can overcome organizational inertia by exerting external pressures and convert external pressure into incentive mechanisms to promote corporate environmental investment (Leiter et al., 2011; Maggioni and Santangelo, 2017; Liao, 2018; Huang and Lei, 2021).

As can be seen, no consistent conclusion has been reached on the impact of environmental regulation on corporate environmental investment. Existing studies have incorporated all environmental regulation tools into the same research framework and ignored the functional differences of heterogeneous environmental regulation tools, which may lead to different conclusions. In addition to some hard environmental regulations, firms also face some soft regulations. So which environmental regulation tools can better drive firms to carry out environmental governance activities needs to be studied. Also, whether environmental violation penalties and environmental subsidies, as two different environmental regulatory tools, have different impacts on corporate environmental governance should be studied. It remains highly desirable to study the impact of heterogeneous environmental regulatory tools on firms’ strategic decisions related to the environment.

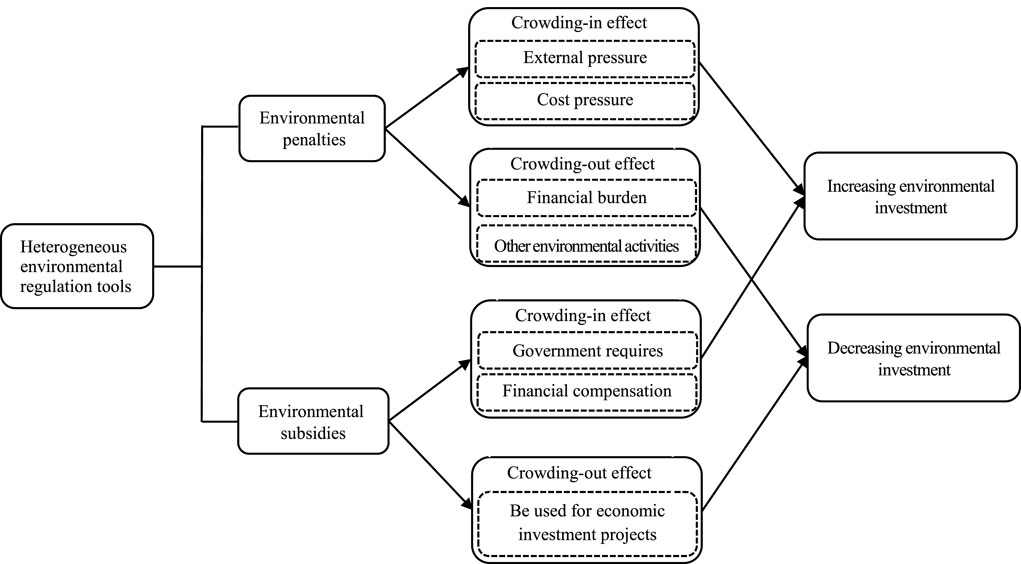

Research evidence suggests that strict supervision and law enforcement are the primary drivers for firms to improve environmental quality (Greenstone and Hanna, 2014). Environmental violation penalties may stimulate firms to increase their investment in environmental governance through external pressures and cost effects. According to the legitimacy theory, organizational legitimacy is one of the reasons for corporate environmental efforts (Thomas and Lamm, 2012; Kuo and Chen, 2013; Berrone et al., 2017). Environmental violations send a signal that the firm has damaged the environment and failed to undertake environmental responsibility, which will provoke public condemnation of the firm. The violating firms not only have to face the government’s supervision and consumers’ doubts but also have to deal with the pressure of public opinion and the trust crisis of employees. Under multiple external pressures, firms cannot avoid their pollution problems. Environmental investment is considered to be an important measure for firms to maintain organizational legitimacy (Maxwell and Decker, 2006). Thus, driven by the motivation of gaining legitimacy, violating firms will increase environmental investment.

In addition to external pressures, environmental violations may also stimulate firms’ environmental investment by increasing the economic cost pressure. China has introduced daily and unlimited penalties for environmental violations and added harsh penalties such as production restriction, production suspension, and administrative detention, which indicates that the cost of violations will increase significantly. Moreover, environmental violations will be disclosed to external stakeholders, which will undoubtedly bring a series of negative consequences to the violating firms, including stock value decline (Dasgupta et al., 2006; Xu et al., 2012), reputation damage (Karpoff et al., 2005; Zou et al., 2015; Lin et al., 2016), restricted financing (Zou et al., 2017), and consumer boycott (Grappi et al., 2013; Long and Liao, 2021). Hence, we can infer that the economic benefits of damaging the environment are far lower than the economic costs of environmental penalties; the illegal cost of firms is higher than the amount of environmental protection investment, thus constructing a mechanism for firms to increase their investment in the environment.

Therefore, our hypothesis is drawn from the aforementioned discussion and is stated formally as follows:

H1-a: Environmental violation penalties are positively associated with corporate environmental investment.

Environmental governance relies on a large amount of capital investment. Environmental investment not only has the characteristics of long cycles and positive externality but also restricts and crowds out corporate investments in other economic projects. In the short term, environmental investment will weaken firms’ profitability and has high opportunity costs (Gray and Shadbegian, 2003). Therefore, most firms do not have the awareness of taking the initiative to invest in environmental protection (Arouri et al., 2012). Violating firms need to pay fines for polluting the environment, which increases their financial burden and further squeezes resources for environmental governance. Currently, environmental penalties in China are imposed on a per-case basis, and the threat is not permanent. This may prompt firms to keep pollution within standards by suspending production and reducing production activities, rather than taking environmental investment actions such as purchasing pollution treatment equipment, improving green production processes, and developing green technologies. It has been documented that environmental violators prefer to increase the number of environmental disclosures to report favorable environmental information to conceal their environmental irresponsibility (Patten, 1992). Empirical evidence from Shevchenko (2021) highlighted that imposing penalties on firms for environmental violations leads to the deterioration of corporate environmental performance. Prechel and Zheng (2012) have also disclosed that environmental penalties cannot induce firms to invest in pollution control technologies. Thus, we proposed the following hypothesis:

H1-b: Environmental violation penalties are negatively correlated with corporate environmental investment.

Resource dependence theory suggests that firms need sufficient financial support to undertake environmental responsibility (Zhang et al., 2022). In recent years, environmental performance has played an increasingly important role in the evaluation of Chinese government officials. Under the pressure of environmental protection, local governments have provided environmental subsidies to firms, requiring them to take responsibility for environmental governance, which prompts firms to use environmental subsidies to directly invest in environmental governance to meet the environmental requirements of local governments (Wang et al., 2021). In addition, environmental subsidies can bridge the gap between environmental benefits and environmental costs, which will diminish firms’ aversion to environmental governance and enhance their willingness to invest in the environment. Specifically, firms engage in a range of environment-related activities, such as purchasing clean manufacturing equipment and researching green technologies, all of which require high capital support. The introduction of environmental subsidies alleviates the shortage of funds required for environmental investment and compensates for the external costs of environmental governance (Lin et al., 2015). Thus, environmental subsidies can motivate firms to invest in environmental governance. Combining these arguments, our hypothesis is formally stated as follows:

H2-a: Environmental subsidies are positively associated with corporate environmental investment.

However, China’s market is still immature, and there are problems such as information asymmetry and ineffective market supervision, which may lead to a crowding-out effect of environmental subsidies on corporate environmental investment. On the one hand, the existence of information asymmetry makes it difficult for the government to obtain accurate information about the environmental conditions of firms. Some firms may disguise green projects in order to obtain environmental subsidies and then transfer these subsidies to other economic investment projects, resulting in a mismatch between environmental subsidies and investment projects (Ren et al., 2021). On the other hand, the Chinese government plays an important role in resource allocation, which has fostered rent-seeking opportunities for firms (Du and Mickiewicz, 2016). Evidence has shown that firms can obtain large amounts of government subsidies by structuring political connections through rent-seeking behavior (Lee et al., 2017; Tao et al., 2017). However, due to the high cost of rent-seeking, subsidies obtained by firms may be used for projects with high economic returns, thus crowding out green investment and ultimately making environmental subsidies fail to achieve the original intention of encouraging firms to participate in environmental governance. Thus, we proposed the following hypothesis:

H2-b: Environmental subsidies are negatively related to corporate environmental investment.

Based on the aforementioned view, the research framework of this study is shown in Figure 1, which integrates the relationships among two heterogeneous environmental regulation tools and corporate environmental investment.

FIGURE 1. Analytical framework for hypothetical relationships.

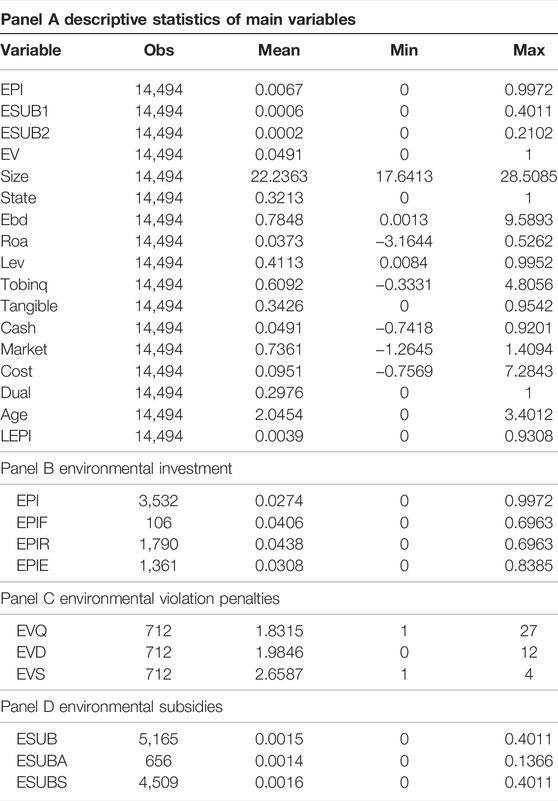

Chinese A-shares listed companies from 2015 to 2019 were selected for this study. Since the new Environmental Protection Law was implemented in China in 2015, the law has adjusted the degree of environmental penalties and the scope of government subsidies (Liu et al., 2021). To ensure the comparability, integrity, and continuity of data, the study interval was chosen to start from 2015. Corporate environmental investment data were collected manually by consulting corporate annual reports, social responsibility reports, and environmental reports. All environmental-related expenditures are included in the firm’s environmental investment, such as investment in renewable technologies and improving pollution treatment equipment. The data on corporate environmental violations came from the website of the China Research Center for Public Environment, and relevant data on environmental violation types, disclosure sources, and penalty information were collected manually. Data on environmental subsidies were obtained from the China Stock Market and Accounting Research (CSMAR) government subsidy database, which was determined by searching keywords such as environmental protection, energy conservation, and emission reduction. To improve data quality, we further screened the sample data. First, the financial and insurance industries were excluded because of its special characteristics. Second, firms with ST (special treatment) and PT (particular transfer) were not included. Third, firms with crucial missing data were also excluded. With the aforementioned screening, our final sample consisted of 14,511 observations from 3,469 listed firms.

Environmental investment (EPI) is the dependent variable in our analysis. The intensity of environmental investment is measured by dividing the amount of environmental investment of the firm in the current year by its total income in the previous period. According to the direction of enterprise investment, environmental investment is divided into three types: environmental governance equipment investment (EPIF), green R&D investment (EPIR), and environmental governance engineering investment (EPIE). To the best of our knowledge, green R&D investment reflects the intensity of environmental governance and is considered to substantially improve the environmental quality. Investment in environmental governance equipment includes the purchase and improvement of environmental pollution control facilities. Environmental governance engineering investment refers to the engineering projects invested by firms in pollution control, ecological protection, and other aspects.

Environmental violation (EV) penalty is the independent variable. The existing literature on environmental penalties includes all types of violations in the same sample, but certain violation penalties (e.g., improperly set pollution signs and non-functional pollution equipment) do not substantially affect corporate environmental investment, and inclusion of these samples may lead to biased results. Therefore, this article selects the violation penalties (e.g., excessive pollution emissions, lack of pollution treatment equipment) that are most likely to affect corporate environmental governance investment, which can supplement the literature on environmental violations. A dummy variable is used to measure whether the firm has been subject to environmental penalties, and EV is assigned to 1 if the firm has received environmental penalties and 0 otherwise. The actual effect of environmental penalties is also affected by the severity, frequency, and subject of the penalty. According to the website of China Public Environment Research Center, the severity of environmental violation penalties (EVD) is divided into 1–12 points, with higher scores indicating heavier penalties. The frequency of environmental violation penalties (EVQ) is the sum of the number of violations that occur in a firm during each year. The subject of environmental penalties (EVS) is divided into four categories: county, city, province, and country. The higher the administrative level of the subject of the penalty, the stronger is the deterrent effect on the firm.

Environmental subsidy (ESUB) is another independent variable. To eliminate the influence of individual characteristics of firms, we used the environmental subsidy standardized by operating income (ESUB1) and the environmental subsidy normalized by total assets (ESUB2) to measure the size of government environmental subsidies received by firms. There are two types of government environmental subsidies. One is the environmental subsidy in the form of bonuses (ESUBA), such as bonuses awarded by the government to firms for their outstanding contributions to the environment, which generally accounts for a relatively small proportion. Another category is special environmental subsidies (ESUBS), such as subsidies given to support firms to develop or build energy-saving and environmental protection technology, which accounts for a relatively large proportion.

Following the conventional practice of the existing literature (Leiter et al., 2011; Huang and Lei, 2021), we included a series of firm-specific characteristics that could influence a firm’s environmental investment activities as follows: firm size (Size), property rights (State), profitability (Roa), leverage ratio (Lev), power balance with a shareholder structure (Ebd), investment opportunities (Tobinq), capital intensity (Tangible), cash flow (Cash), market power (Market), CEO–Chairman duality (Dual), agency cost (Cost), last period environmental investment (LEPI), and firm age (Age). Furthermore, we controlled industry (Industry), year (Year), and province (Province) effects.

In the research sample of this article, not all firms have environmental investments. The value of dependent variables in some samples is 0. Therefore, we developed the following Tobit regression model to capture the effect of environmental penalties on corporate environmental investment:

where EPI represents the environmental investment by firm i in the year t. α0 is a constant. EV denotes the environmental violation penalties. Variable control is a vector of control variables. ut, λj, and δp represent the year fixed effects, the industry fixed effects, and the province fixed effects, respectively. ε is an error term. The standard errors are corrected for heteroskedasticity and clustered at the firm level. To reduce potential endogenous problems in this article, the independent variable is lagged by one period.

We developed the following Tobit regression model to capture the effect of environmental subsidies on corporate environmental investment:

where ESUB is the indicator of environmental subsidies. The other variables are defined in the same way as the model (1). In addition, in the research process, we also put environmental violation penalties and environmental subsidies into the same model for the regression test.

The statistical results of the main variables at the mean, minimum, and maximum values are reported in Table 1.

TABLE 1. Descriptive statistics.

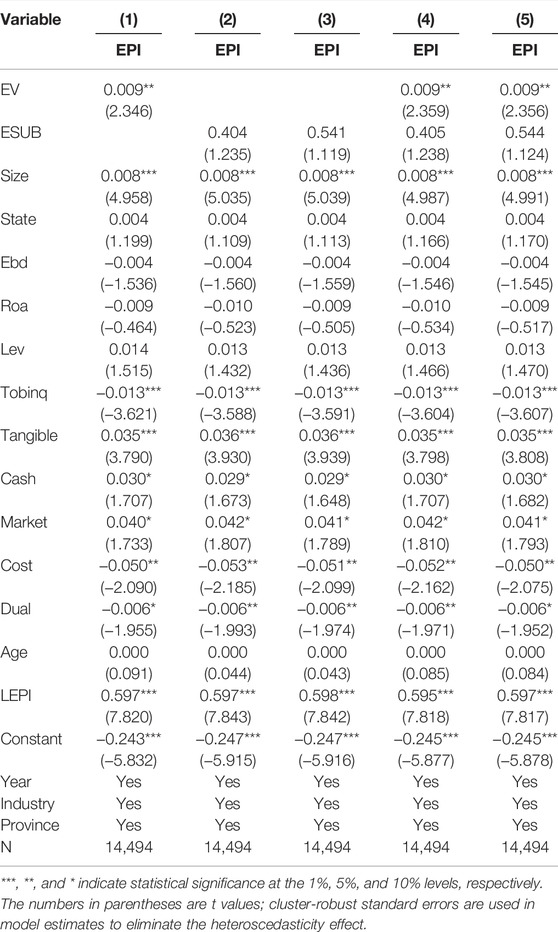

We used the Tobit model to examine the impact of environmental penalties and environmental subsidies on environmental investment, and robust standard deviation is used to overcome heteroscedasticity; the results are shown in Table 2. The results of column (1) show that the coefficient of EV is positive and significant at the level of 5%, which provides strong support for hypothesis 1a, that is, environmental penalties play a positive role in promoting corporate environmental investment. In columns (2) and (3) of Table 2, the coefficient of ESUB fails the significance test, which indicates that environmental subsidies do not have a substantial impact on corporate environmental investment, and the results do not support hypothesis 2a and 2b. Columns (4) and (5) show the results of environmental penalties and environmental subsidies in the same model. The coefficient of EV is positive and significant at the level of 5%, while the coefficient of ESUB is not significant. This suggests that environmental penalties played a “crowding-in” effect rather than a “crowding-out” effect on corporate environmental investment. The environmental subsidies in China do not exhibit a “crowding-out” or “crowding-in” effect.

TABLE 2. Baseline regression results.

In this section, we further broke down the indicators to examine the impact of penalties and subsidies on corporate environmental investment.

Panel A in Table 3 reports the regression results for the segmentation direction of corporate environmental investment. The effect of EV on EPIF is not significant (α = 0.002 and p > 0.1), the effect of EV on EPIR is positive and significant (α = 0.014 and p < 0.001), and the effect of EV on EPIE is positive and significant (α = 0.010 and p < 0.1). The aforementioned results imply that firms receiving environmental penalties do not increase green R&D investments but prefer to increase environmental legitimacy by purchasing environmental equipment and investing in environmental engineering projects.

TABLE 3. Sub-index regression results.

The actual effect of environmental penalties is affected by the severity, frequency, and subject of implementing penalties. Therefore, we re-examined the impact of environmental penalties on corporate environmental investment from three aspects: the frequency of penalties, the subject of penalties, and the severity of penalties, and the results are shown in panel B. In column (1) of panel B, the coefficient of EVQ is not significant (β = 0.001 and p > 0.1). In column (2) of panel B, the effect of EVS on EPI is positive and significant (β = 0.003 and p < 0.1). In column (3) of panel B, the coefficient of EVD is significant and positive at the level of 5% (β = 0.003 and p < 0.05). Our results further showed that the higher the administrative level of the penalty subject and the greater the severity of the penalty, the stronger is the positive incentive for firms to invest in the environment. In contrast, the higher the frequency of violations, the weaker is the incentive for firms to participate in environmental governance.

Panel C in Table 3 reports the regression results of different types of environmental subsidies on corporate environmental investment. Columns (1) and (2) are the regression results for environmental bonus grants, and columns (3) and (4) are the regression results for environmental specific grants, which both do not pass the significance test. The reason may be that, at present, China lacks effective assessment standards and supervision mechanisms for the use of environmental subsidies by firms, resulting in a large amount of environmental subsidy funds that do not produce green effects.

The aforementioned empirical results demonstrated that environmental violation penalties have a significant positive impact on corporate environmental investment. However, the mechanism of the effect remains unexplored. As we speculated in the hypothesis analysis section, internal resource constraints and external pressures caused by environmental penalties would motivate firms to increase environmental investment.

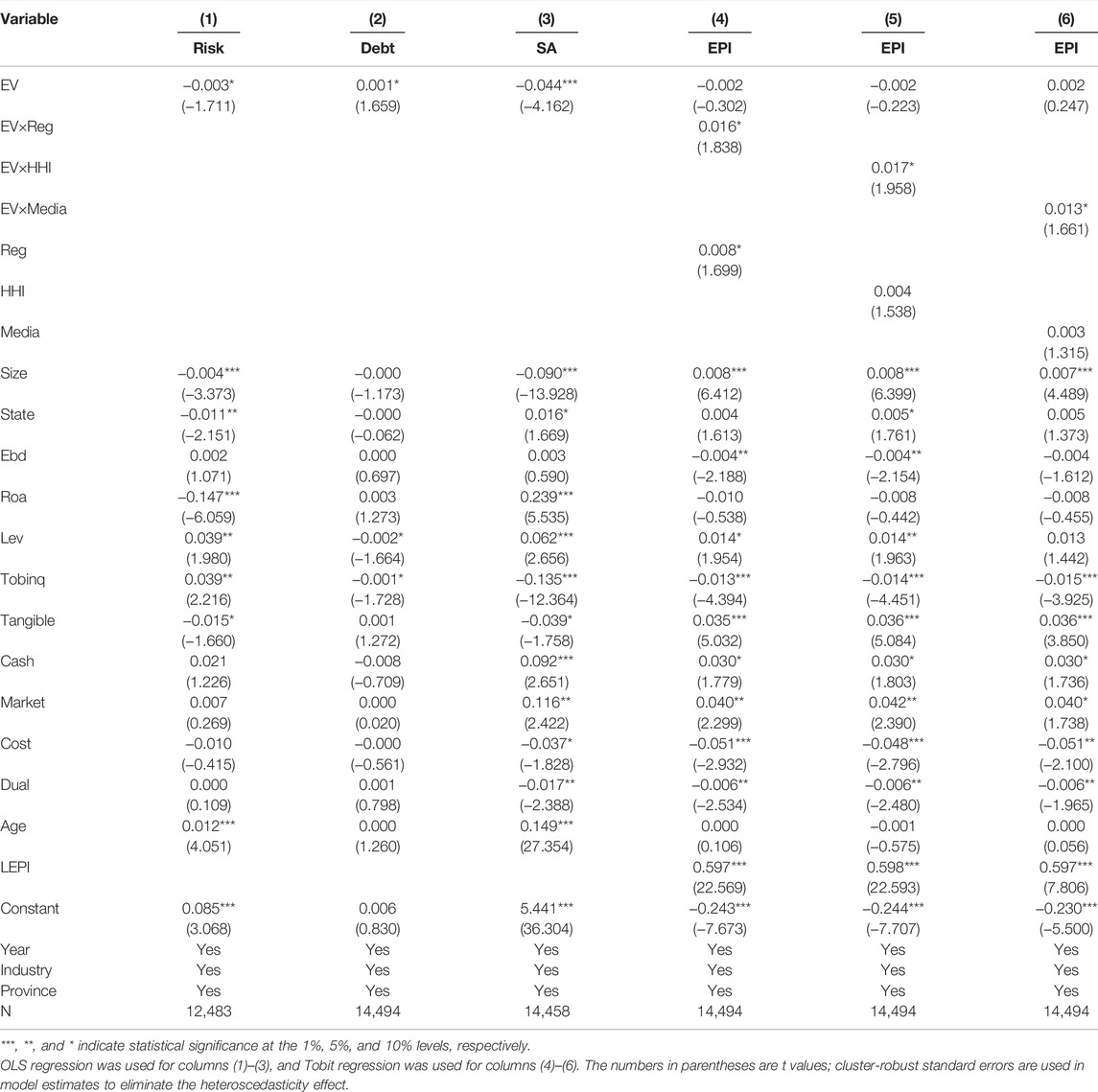

Environmental penalties can only change corporate behavior when it has a significant impact on their production and operation activities. In this section, we aimed to explore the impact of environmental penalties on firms’ risk-taking capacity, debt cost, and financing constraints. Fluctuation of ROA is used to measure the risk-taking level of firms, and a larger value represents a stronger risk-taking ability of firms. Corporate financing cost is measured by dividing its interest expense by total borrowings. The SA index is used as a proxy variable for financing constraint, and the larger the value reflects, the lower is the financing constraint of firms. The results in columns (1)–(3) of Table 4 show that environmental penalties diminish the firms’ risk-taking capacity, increase debt costs, and increase financing constraints, and a series of negative effects will prompt firms to take necessary environmental actions to alleviate the resource constraints caused by penalties, which enhances the motivation of firms to increase investment in environmental governance.

TABLE 4. Motivation test.

In this part, we analyzed how the external environment affects the relationship between environmental penalties and environmental investment from two aspects: the formal institutional environment [regional environmental regulation intensity (Reg)] and the informal institutional environment [market competition (HHI) and media attention (Media)]. The results in columns (4)–(6) of Table 4 show that the cross-product coefficients of EV×Reg, EV×HHI and EV×Media are all significant and positive at the level of 10%. The higher the intensity of regional environmental regulation, the lower is the government’s tolerance for environmental pollution, which will further increase the risk and cost of violating firms. The higher the degree of market competition, the more quickly the negative impact of environmental penalties will be reflected in the product price of the firm, weakening the firm’s market competitiveness. Higher media attention will lead to more negative reports of corporate environmental violations, which will damage firms’ image and reputation. Therefore, it can be seen that environmental penalties significantly increase the external pressure of violating firms and thus have a strong “crowding-in” effect on environmental investment.

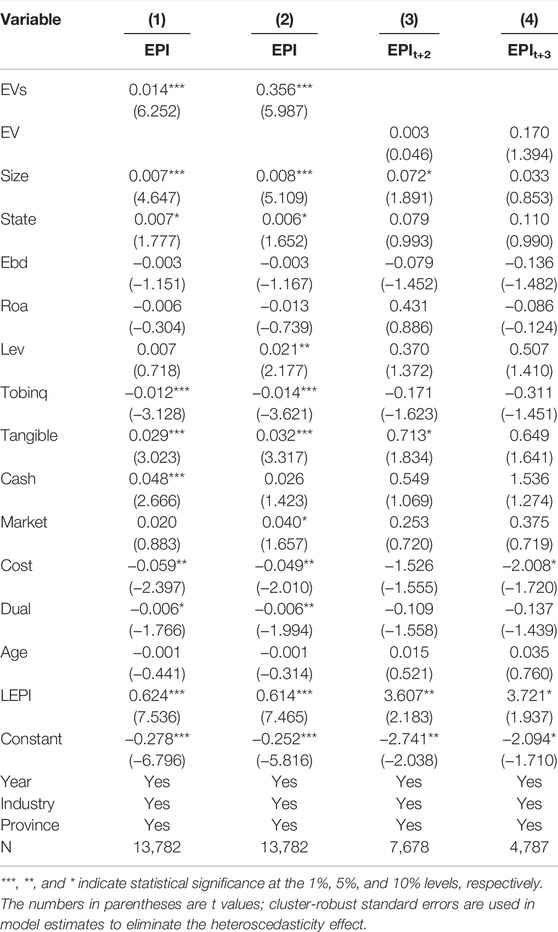

When a firm receives an environmental penalty, does it have a deterrent effect on other firms in the same industry? We used empirical evidence to answer this question. The spillover effect of environmental penalties (EVs) is measured by two methods: the logarithm of violating firms in the industry and the ratio of violating firms to the total number of firms in the industry. The sample of firms that have received environmental penalties is excluded, and only the sample of firms that did not receive penalties is retained. The results in columns (1) and (2) of Table 5 show that the aforementioned two variables have a positive impact on the environmental investment of other firms (α = 0.014, p < 0.001; α = 0.356, p < 0.001). As the number of penalized firms in the industry increases, the more environmental risk information is transmitted to other firms in the same industry and the stronger is the environmental deterrent effect, which in turn motivates other firms to increase their environmental investments for precautionary motives.

TABLE 5. Deterrence effect test.

The environmental investment with a lag of two or three periods is re-introduced into the regression model as a dependent variable to verify whether environmental penalties have a lasting effect on corporate environmental investment, and the results are shown in columns (3) and (4) of Table 5. It is found that the coefficients of EV are not significant, indicating that environmental penalties have an immediate effect on corporate environmental investment but not a long-term lasting effect.

We carried out the robustness test as follows.

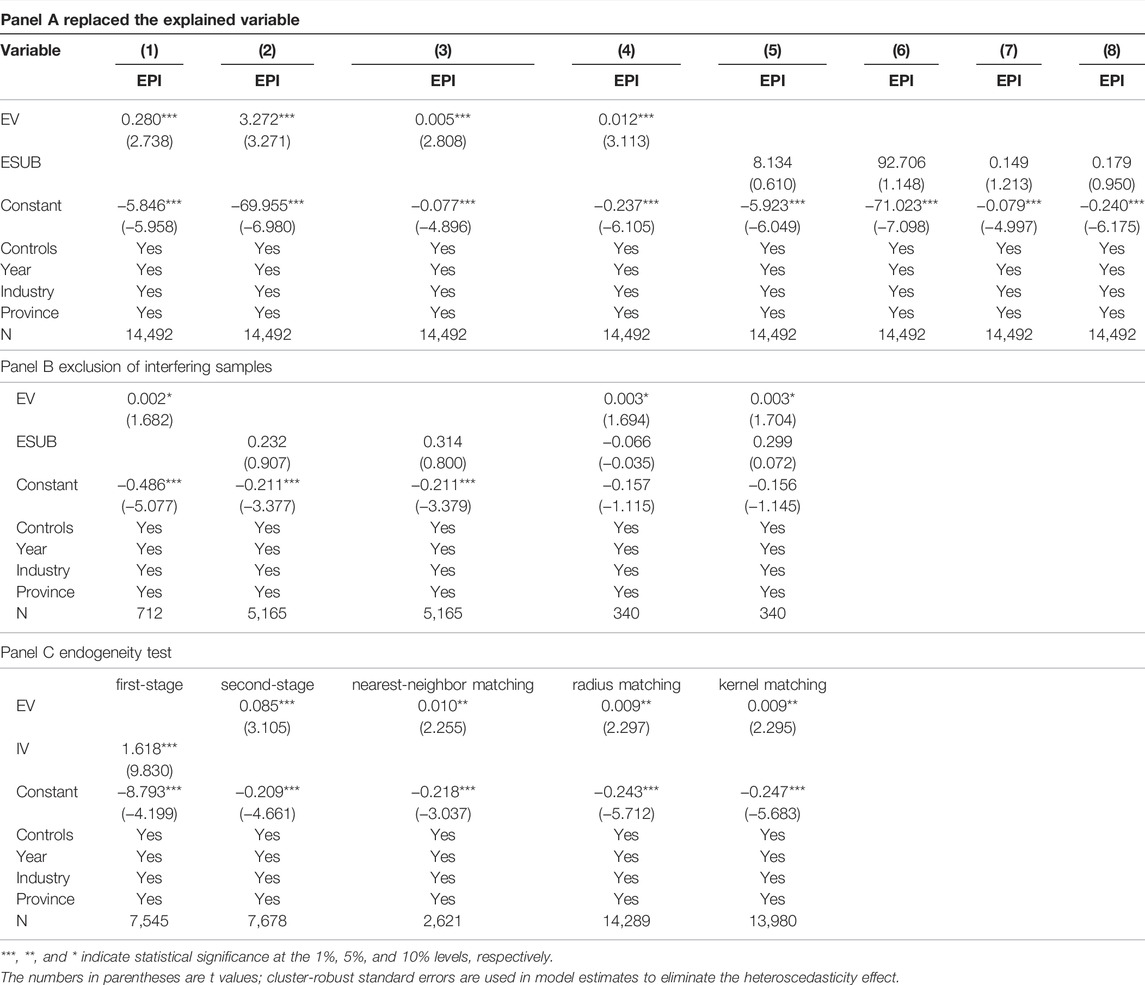

We used additional methods to remeasure environmental investment to strengthen our conclusions. Specifically, we applied four methods that are commonly used in academia to remeasure environmental investment. First, we used dummy variables to remeasure EPI. If the firm has environmental investments, EPI is coded as 1 and 0 otherwise. Second, the logarithm of the total environmental investment was used to measure the environmental investment of listed firms. Third, asset-standardized environmental investment was used to measure the environmental investment level of firms. Fourth, the difference between the next year’s environmental investment and the current year’s environmental investment was used to measure EPI. Eq. 1 is tested by remeasuring environmental investment through the aforementioned four methods. The results of panel A in Table 6 show that even if the measurement method of EPI is changed, the coefficients of EV are always positive and significant, while the coefficients of ESUB still fail the significance test, which proves that our research conclusions have good robustness.

TABLE 6. Robustness test.

When testing the impact of environmental violation penalties on corporate environmental investment, only the samples that are penalized are kept. Similarly, when testing the impact of environmental subsidies on corporate environmental investment, samples not received environmental subsidies are excluded. Column (1) of panel B shows that the regression coefficient of EV is significantly positive at the level of 10% (α = 0.002 and p < 0.1). The regression coefficients of ESUB in columns (2) and (3) still do not pass the significance test (β = 0.232 and p > 0.1; β = 0.314, p > 0.1). Columns (4) and (5) of panel B retain only those samples where both have received penalties and subsidies. The results showed that environmental penalties are still significantly positive, and environmental subsidies are not significant. It can be seen that adopting the policy tool of environmental penalties can better motivate firms to strengthen environmental governance than environmental subsidies.

Considering that sample selection bias may lead to the endogenous problem in this study, we adopted both two-stage least-squares (2SLS) and propensity score matching (PSM) methods to address this problem. For the 2SLS method, whether the firm is subject to environmental penalties with a two-period lag is used as the instrumental variable (IV). The results are shown in columns (1) and (2) of panel C. The results in column (1) of panel C indicate that the instrumental variable is positively correlated with the dependent variable. Column (2) of panel C shows the 2SLS regression results; it can be seen that the test results are consistent with the original regression results, suggesting that our findings are robust. For the PSM method, firms that received environmental penalties are used as the experimental group and other firms as the control group. Three matching methods are adopted: the nearest-neighbor matching method, the radius matching method, and the nuclear matching method. The results are displayed in columns (3)–(5) of panel C. Regardless of which propensity score matching method is chosen, the regression coefficients of environmental penalties have a significant and positive influence on corporate environmental investment, which further verifies the reliability of the conclusion in this article.

Environmental penalties and environmental subsidies are two heterogeneous environmental regulation instruments. Although they both aim to internalize environmental problems, there are significant differences in the mechanisms by which they work. Using a sample of Chinese listed companies from 2015 to 2019, we empirically examined the effects of heterogeneous environmental regulatory instruments on corporate environmental investment by manually collecting data on corporate environmental violations, environmental subsidies, and environmental investments. The findings are as follows: 1) environmental penalties significantly increase corporate environmental investment. At the same time, the motivation of firms to increase environment investment is significantly correlated with the intensity of environmental punishment and the administrative level of the punishment subject. 2) Additional tests reveal that this influence is exerted through internal financial constraints and external environmental pressures. In detail, environmental penalties bring a series of negative resource constraints, such as reduced risk-taking ability, increased capital costs, and increased financing constraints. Meanwhile, external environmental constraints will significantly increase the external pressure on the violating firms. The combination of internal resource constraints and external environmental pressures makes environmental penalties have a strong positive incentive effect on corporate environmental investment. 3) Environmental subsidies do not reflect the green governance effect and have no impact on corporate environmental investment. The reason may be that the government lacks an effective assessment and supervision mechanism for the use of environmental subsidies by firms, thus resulting in a large number of environmental subsidy funds that do not produce green effects. 4) Moreover, our study revealed that environmental penalties have a deterrent effect on other firms in the same industry but do not have a lasting effect.

Based on the aforementioned conclusions, the following suggestions are made. First, this study showed that environmental penalties have a positive effect on corporate environmental investment. This finding affirms the remarkable effectiveness of government environmental enforcement in improving the environmental quality. We recommend that governments, especially the environmental administration department, should continue to enhance the importance of environmental penalty instruments and complete the rigidity of law enforcement to encourage firms to invest more in environmental governance. Second, the higher the administrative level of the penalty subject and the greater the severity of the penalty, the more pronounced is the environmental investment by firms. Therefore, in the process of environmental enforcement, the government needs to improve the execution ability of environmental penalties and increase the cost of violations so as to form an effective deterrent signal of environmental regulations for firms. Third, the results of this article showed that environmental penalties have a deterrent effect on the industry but do not have time persistence. According to our conclusions, we suggest that the government should use multiple platforms and channels to disclose information about corporate environmental violations. This signal transmission mechanism will form a deterrent effect on other firms, leading to firms to reduce violation behaviors and increase environmental governance investment based on precautionary motives and ultimately achieve the goal of environmental protection. More importantly, the government also needs to act jointly with other market institutions to form a long-term supervision mechanism for the violating firms by continuously tracking the follow-up environmental governance actions of firms. Fourth, effective external pressure and resource constraints can prompt enterprises to increase environmental investment. The government should encourage the public, media, and other groups to actively supervise corporate environmental behavior by creating diversified channels for reporting environmental violations, which will increase the reputation cost of violations and promote firms to undertake environmental responsibility. Meanwhile, effective penalty deterrence must be linked with enterprise profits. The government can also force firms to improve their environmental performance by restricting external financing, for example, prohibiting commercial institutions from providing loans to violating firms. Finally, China’s environmental subsidies have not yet produced the green effect, which requires the government to effectively screen the environmental status of firms receiving subsidies, and distinguish whether firms are green or disguised. In addition, the environmental performance assessment of firms receiving environmental subsidies should be strengthened to prevent firms from diverting environmental subsidies for other profit-making purposes.

The limitations of this article mainly include the following aspects. First, we used Chinese firms as the research object. Our conclusion may be applied to other developing countries and emerging economies. However, it may not work in mature markets. Hence, future studies can compare the functional differences of environmental regulatory tools between various economies. Second, this article only studied the environmental investment behavior in the firm environmental behavior. However, the scale of environmental investment only represents the input of enterprise in environmental governance, which cannot include and measure the improvement of enterprise’s overall environmental quality. In the future, systematic research can be conducted from the input to the results of corporate environmental governance. Finally, due to the availability of data, the sample in this article is limited to listed firms, which are usually large firms. Since firms with different sizes differ greatly in resource acquisition and business philosophy, it is also worthwhile to further study whether these two environmental regulation tools have different impacts on the environmental investment of enterprises of different scales.

The original contributions presented in the study are included in the article/supplementary material; further inquiries can be directed to the corresponding author.

LH chose the research ideas, formed the study framework, and wrote the manuscript; TZ collected and analyzed the data; SG and JL reviewed and edited the manuscript; and CX wrote the limitations section and reviewed this manuscript. All authors contributed to the manuscript and approved the submitted version.

This work was supported by the National Social Science Foundation of China (Grant No. 21BJY121).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors, and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

The authors sincerely thank the editor and reviewers for valuable comments and suggestions.

Aksak, E. O., Ferguson, M. A., and Duman, S. A. (2016). Corporate Social Responsibility and CSR Fit as Predictors of Corporate Reputation: A Global Perspective. Public. Relat. Rev. 42, 79–81. doi:10.1016/j.pubrev.2015.11.004

Arouri, M. E. H., Caporale, G. M., Rault, C., Sova, R., and Sova, A. (2012). Environmental Regulation and Competitiveness: Evidence from Romania. Ecol. Econ. 81, 130–139. doi:10.1016/j.ecolecon.2012.07.001

Berrone, P., Fosfuri, A., and Gelabert, L. (2017). Does Greenwashing Pay off? Understanding the Relationship between Environmental Actions and Environmental Legitimacy. J. Bus. Ethics. 144, 363–379. doi:10.1007/s10551-015-2816-9

Borghesi, S., Cainelli, G., and Mazzanti, M. (2015). Linking Emission Trading to Environmental Innovation: Evidence from the Italian Manufacturing Industry. Res. Policy. 44, 669–683. doi:10.1016/j.respol.2014.10.014

Dasgupta, S., Hong, J. H., Laplante, B., and Mamingi, N. (2006). Disclosure of Environmental Violations and Stock Market in the Republic of Korea. Ecol. Econ. 58, 759–777. doi:10.1016/j.ecolecon.2005.09.003

Dong, K., Shahbaz, M., and Zhao, J. (2022). How Do Pollution Fees Affect Environmental Quality in China? Energy Policy 160, 112695. doi:10.1016/j.enpol.2021.112695

Du, J., and Mickiewicz, T. (2016). Subsidies, Rent Seeking and Performance: Being Young, Small or Private in China. J. Bus. Ventur. 31, 22–38. doi:10.1016/j.jbusvent.2015.09.001

Esen, Ö., Yildirim, D. C., and Yildirim, S. (2021). Pollute Less or Tax More? Asymmetries in the EU Environmental Taxes-Ecological Balance Nexus. Environ. Impact Assess. Rev. 91, 106662. doi:10.1016/j.eiar.2021.106662

Fryxell, G. E., and Lo, C. W. H. (2003). The Influence of Environmental Knowledge and Values on Managerial Behaviours on Behalf of the Environment: An Empirical Examination of Managers in China. J. Bus. Ethics. 46, 45–69. doi:10.1023/A:1024773012398

Grappi, S., Romani, S., and Bagozzi, R. P. (2013). Consumer Response to Corporate Irresponsible Behavior: Moral Emotions and Virtues. J. Bus. Res. 66, 1814–1821. doi:10.1016/j.jbusres.2013.02.002

Gray, W. B., and Shadbegian, R. J. (1998). Environmental Regulation, Investment Timing, and Technology Choice. J. Indust. Econ. 46, 235–256. doi:10.1111/1467-6451.00070

Gray, W. B., and Shadbegian, R. J. (2003). Plant Vintage, Technology, and Environmental Regulation. J. Environ. Econ. Manage. 46, 384–402. doi:10.1016/S0095-0696(03)00031-7

Greenstone, M., and Hanna, R. (2014). Environmental Regulations, Air and Water Pollution, and Infant Mortality in India. Am. Econ. Rev. 104, 3038–3072. doi:10.1257/aer.104.10.3038

Hartl, R. F. (1992). Optimal Acquisition of Pollution Control Equipment under Uncertainty. Manage. Sci. 38, 609–622. doi:10.1287/mnsc.38.5.609

Huang, L., and Lei, Z. (2021). How Environmental Regulation Affect Corporate Green Investment: Evidence from China. J. Clean. Prod. 279, 123560. doi:10.1016/j.jclepro.2020.123560

Karpoff, J. M., Lott, Jr., J. R., and Wehrly, E. W. (2005). The Reputational Penalties for Environmental Violations: Empirical Evidence. J. Law Econ. 48, 653–675. doi:10.1086/430806

Kim, Y., and Statman, M. (2012). Do Corporations Invest Enough in Environmental Responsibility? J. Bus. Ethics. 105, 115–129. doi:10.1007/s10551-011-0954-2

Kuo, L., and Chen, V. Y-J. (2013). Is Environmental Disclosure an Effective Strategy on Establishment of Environmental Legitimacy for Organization? Manag. Decis. 51, 1462–1487. doi:10.1108/MD-06-2012-0395

Lee, E., Walker, M., and Zeng, C. (2017). Do Chinese State Subsidies Affect Voluntary Corporate Social Responsibility Disclosure? J. Account. Public Policy 36, 179–200. doi:10.1016/j.jaccpubpol.2017.03.004

Leiter, A. M., Parolini, A., and Winner, H. (2011). Environmental Regulation and Investment: Evidence from European Industry Data. Ecol. Econ. 70, 759–770. doi:10.1016/j.ecolecon.2010.11.013

Li, H., and Peng, W. (2020). Carbon Tax, Subsidy, and Emission Reduction: Analysis Based on DSGE Model. Complexity 2020, 6683482. doi:10.1155/2020/6683482

Li, P., Lin, Z., Du, H., Feng, T., and Zuo, J. (2021). Do environmental Taxes Reduce Air Pollution? Evidence from Fossil-Fuel Power Plants in China. J. Environ. Manage. 295, 113112. doi:10.1016/j.jenvman.2021.113112

Li, Q., Ruan, W., Sun, T., and Xiang, E. (2020). Corporate Governance and Corporate Environmental Investments: Evidence from China. Energy Environ. 31, 923–942. doi:10.1177/0958305X19882372

Liao, Z. (2018). Content Analysis of China's Environmental Policy Instruments on Promoting Firms' Environmental Innovation. Environ. Sci. Policy 88, 46–51. doi:10.1016/j.envsci.2018.06.013

Lin, H., Zeng, S., Ma, H., and Chen, H. (2015). Does Commitment to Environmental Self-Regulation Matter? An Empirical Examination from China. Manag. Decis. 53, 932–956. doi:10.1108/MD-07-2014-0441

Lin, H., Zeng, S., Wang, L., Zou, H., and Ma, H. (2016). How Does Environmental Irresponsibility Impair Corporate Reputation? A Multi-Method Investigation. Corp. Soc. Responsib. Environ. Manag. 23, 413–423. doi:10.1002/csr.1387

Liu, Y., Wang, A., and Wu, Y. (2021). Environmental Regulation and Green Innovation: Evidence from China's New Environmental Protection Law. J. Clean. Prod. 297, 126698. doi:10.1016/j.jclepro.2021.126698

Long, S., and Liao, Z. (2021). Would Consumers Pay for Environmental Innovation? The Moderating Role of Corporate Environmental Violations. Environ. Sci. Pollut. Res. 28, 29075–29084. doi:10.1007/s11356-021-12811-2

Lundgren, T. (2003). A Real Options Approach to Abatement Investments and Green Goodwill. Environ. Resour. Econ. 25, 17–31. doi:10.1023/A:1023602426857

Maggioni, D., and Santangelo, G. D. (2017). Local Environmental Non-Profit Organizations and the Green Investment Strategies of Family Firms. Ecol. Econ. 138, 126–138. doi:10.1016/j.ecolecon.2017.03.026

Maxwell, J. W., and Decker, C. S. (2006). Voluntary Environmental Investment and Responsive Regulation. Environ. Resour. Econ. 33, 425–439. doi:10.1007/s10640-005-4992-z

Orsato, R. J. (2006). Competitive Environmental Strategies: When Does it Pay to Be Green? Calif. Manage. Rev. 48, 127–143. doi:10.2307/41166341

Patten, D. M. (1992). Intra-Industry Environmental Disclosures in Response to the Alaskan Oil Spill: A Note on Legitimacy Theory. Acc. Organ. Soc. 17, 471–475. doi:10.1016/0361-3682(92)90042-Q

Porter, M. E., and Vanderlinde, E. (1995). Toward a New Conception of the Environment-Competitiveness Relationship. J. Econ. Perspect. 9, 97–118. doi:10.1257/jep.9.4.97

Prechel, H., and Zheng, L. (2012). Corporate Characteristics, Political Embeddedness and Environmental Pollution by Large U.S. Corporations. Soc. Forces 90, 947–970. doi:10.1093/sf/sor026

Qu, X., and Sun, X. (2022). How to Improve the Function of Government Carbon Tax in Promoting Enterprise Carbon Emission Reduction: From the Perspective of Three-Stage Dynamic Game. Environ. Sci. Pollut. Res. 29, 31348–31362. doi:10.1007/s11356-021-18236-1

Ren, S., Sun, H., and Zhang, T. (2021). Do environmental Subsidies Spur Environmental Innovation? Empirical Evidence from Chinese Listed Firms. Technol. Forecast. Soc. Chang. 173, 121123. doi:10.1016/j.techfore.2021.121123

Shevchenko, A. (2021). Do financial Penalties for Environmental Violations Facilitate Improvements in Corporate Environmental Performance? An Empirical Investigation. Bus. Strateg. Environ. 30, 1723–1734. doi:10.1002/bse.2711

Tao, Q., Sun, Y., Zhu, Y., and Yang, X. (2017). Political Connections and Government Subsidies: Evidence from Financially Distressed Firms in China. Emerg. Mark. Financ. Trade. 53, 1854–1868. doi:10.1080/1540496X.2017.1332592

Thomas, T. E., and Lamm, E. (2012). Legitimacy and Organizational Sustainability. J. Bus. Ethics. 110, 191–203. doi:10.1007/s10551-012-1421-4

Wang, H., Mamingi, N., Laplante, B., and Dasgupta, S. (2003). Incomplete Enforcement of Pollution Regulation: Bargaining Power of Chinese Factories. Environ. Resour. Econ. 24, 245–262. doi:10.1023/a:1022936506398

Wang, Y., and Zhang, Y. (2020). Do State Subsidies Increase Corporate Environmental Spending? Int. Rev. Financ. Anal. 72, 101592. doi:10.1016/j.irfa.2020.101592

Wang, P., Zhang, Z. J., Zeng, Y. L., Yang, S. C., and Tang, X. (2021). The Effect of Technology Innovation on Corporate Sustainability in Chinese Renewable Energy Companies. Front. Energy Res. 9, 638459. doi:10.3389/fenrg.2021.638459

Xu, X. D., Zeng, S. X., and Tam, C. M. (2012). Stock Market's Reaction to Disclosure of Environmental Violations: Evidence from China. J. Bus. Ethics. 107, 227–237. doi:10.1007/s10551-011-1035-2

Zhang, F., Chen, J., Zhu, L., and Liu, L. (2022). Does Resource Slack Promote or Constrain Firm Environmental Management Investment? Moderating Roles of Technology Sources. Total Qual. Manag. Bus. Excell. 33, 590–613. doi:10.1080/14783363.2021.1882843

Zou, H. L., Zeng, R. C., Zeng, S. X., and Shi, J. J. (2015). How Do Environmental Violation Events Harm Corporate Reputation? Bus. Strat. Env. 24, 836–854. doi:10.1002/bse.1849

Keywords: environmental regulation, environmental penalties, environmental subsidies, environmental governance, deterrent effect

Citation: He L, Zhong T, Gan S, Liu J and Xu C (2022) Penalties vs. Subsidies: A Study on Which Is Better to Promote Corporate Environmental Governance. Front. Environ. Sci. 10:859591. doi: 10.3389/fenvs.2022.859591

Received: 24 January 2022; Accepted: 09 May 2022;

Published: 14 June 2022.

Edited by:

Faik Bilgili, Erciyes University, TurkeyReviewed by:

Luigi Aldieri, University of Salerno, ItalyCopyright © 2022 He, Zhong, Gan, Liu and Xu. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Ling He, MTEyMDgyMTk4MkBxcS5jb20=

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.