Lijun Gao1

Lijun Gao1 Kun Guo

Kun Guo

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 12 January 2023

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.1109796

This article is part of the Research Topic Understanding Carbon Asset Risk under Global Energy Transition View all 6 articles

After the signing of the Paris Agreement, countries around the world paid more attention to climate change and made more efforts to enact policies. Under the dual pressure of policy and environment, each market is affected to different degrees. At the same time, as a new environmental protection tool, the green bond rose to prominence, causing a shock to various markets, but also has a certain hedging role. However, there are few studies on the dynamic co-movement and risk spillover effect between green bonds and stock markets, crude oil and gold in the existing literature. Therefore, it is necessary to explore the changes in the relationship between various markets for the reasonable avoidance of climate risks. Based on the relationship between the three green investment instruments (S&P green Bond, China Green Bond and climate bond) and the three markets, this paper adds the impact analysis on climate risk and policy risk. The conclusions obtained not only have guiding significance for investors interested in environmental protection in asset allocation and hedge selection, but also have reference significance for policymakers who want to realize green investment, which helps smooth the transition to a low-carbon economy.

As an environmentally friendly investment tool, green bonds have emerged after the signing of the Paris Agreement and have become the focus of investors. It has similar characteristics to traditional bonds, except that their proceeds are earmarked for environmental projects. Due to its ability to direct financial resources to environmentally friendly projects, green bonds are becoming increasingly popular in the sustainability-oriented financial markets.

Many countries have committed to transitioning to climate-resilient economies and enacted climate-related policies; At the same time, as green bonds are considered an appropriate tool to finance the transition to a low-carbon economy (OECD, 2017; Monasterolo and Raberto, 2018), and the ability to redistribute the costs of climate change mitigation across generations (Flaherty et al., 2017), so eco-friendly investors are more inclined to invest in green bonds under the influence of climate risk.

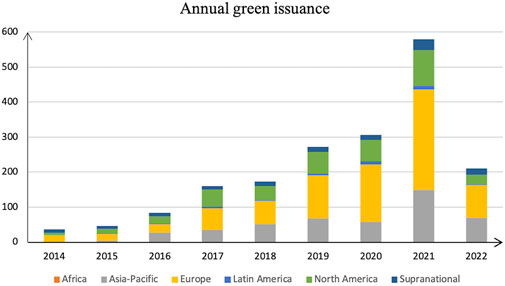

Since the EIB issued its first green bond in 2007, the global green bond market has experienced a “budding period” of 2007–2012, a “growth period” of 2013–2016, and a “maturity period” of 2017 to the present. Global green bond issuance grew from $37 billion in 2014 to $508.8 billion in 2021, with a CAGR of 45%, as shown in Figure 1. In particular, China’s green bond issuance is in a rapid trend. According to data, by the end of 2021, China’s cumulative green bond issuance volume was US$199.2 billion (nearly 1.3 trillion yuan), ranking second in the world, and the issuance volume in the first quarter of 2022 has ranked first in the world. Furthermore, China is also the market with the largest increase in green bond issuance in 2021, with a year-on-year increase of US$44.4 billion, a growth rate of 186%. Even so, the global green bond market still accounts for a relatively small portion of unlabelled climate-related bonds, and its share in bond markets is even smaller. China faces a similar situation, with labeled green bonds accounting for only about 1% of China’s overall bond market, and there is still huge room for growth. It can be seen that the green bond market has broad prospects for the future and is an emerging powerhouse.

FIGURE 1. Annual green bond issuance by region (Unit: US$1 billion).

In the face of such a rapid development of the green bond market, various asset markets have been affected by a certain degree (Gao et al., 2021; Ejaz et al., 2022; Jiang et al., 2022). The linkage between the green bond market and financial markets has become the focus of researchers. First of all, the impact of two-way shocks between emerging assets and traditional assets is necessary and important. For example, the study of whether the emergence of the green bond market will have an impact on other markets, whether the impact is positive or negative, and how other markets will affect the green bond market can lay a theoretical foundation for the further development of the green bond market. Secondly, green bonds have shown certain safe-haven properties in recent years, and whether they can be allocated in the asset portfolio as a hedge asset is also a key area of focus. Third, in the current integration of financial markets, the linkage between markets is enhanced, and the increase or decrease of cross-market correlation is closely related to asset pricing and risk management, and exploring the changes of market linkage in different scenarios is of guiding significance for people’s asset allocation adjustment in the face of emergencies. As a result, such research is also crucial for portfolio risk management for investors in the context of climate change (Reboredo, 2018), as these ultimately influence investors’ motivation to mobilize financial resources for green projects, ultimately in the development of a low-carbon economy (OECD, 2016).

The objective of this paper is to investigate the dynamic time-varying relationship between green bond markets and other major financial markets, which may affect the performance of green bond indices, and to explore the impact of climate change risks and policy uncertainty on the dynamics of markets. In our empirical analyses, various types of financial and commodity markets are considered including the S&P Green Bond Index, China Green Bond Index, Climate Bond Index, Gold Market, Crude Oil Market and US Stock Market. The financial instrument based on the US equity market is used because the S&P 500 is a key indicator of the global economy. In addition, as crude oil and gold often play a crucial role in hedging the downside risk of financial markets, the information on these commodity prices is considered.

This paper aims to study the dynamic time-varying relationship between the green bond market and other major financial markets, which may affect the performance of the green bond index, and explore the impact of climate change risks and policy uncertainty on market dynamics. In our empirical analysis, we included three types of green bond indices (S&P Green Bond, China Green Bond and Climate Bond), mainly to compare whether there are different performances between different green bonds. Various types of financial and commodity markets are also considered, including the gold market, the crude oil market, and the US stock market. Financial instruments based on the US stock market are used because the S&P 500 is a key indicator of the global economy. In addition, since crude oil and gold often play a vital role in hedging downside risks in financial markets, information about the prices of these commodities is considered.

The study not only explores the differences in the linkage relationship between three representative types of green bond indexes and important financial markets, but also explore the influencing factors of across-market linkage in the context of the current era, so that investors can better understand the allocation differences between green bond assets and the financial variables that can affect the risk spillover between green bonds and other assets. The conclusions of this study are not only of reference significance for environmental market participants in their decision-making to hedge climate risks in their investments, but also promote the decarbonization of investment portfolios and the transformation and development of low-carbon society.

For rest of the paper: Section 2 reviews the related literature. Section 3 describes the dataset and methods. Section 4 presents empirical results. Section 5 discuses. Section 6 concludes.

Today, the green bond market is a global market with issuers (large corporations, public entities and supranational institutions) and investors spread across the globe. Given the expanding economic impact of green bonds, different global green bond indices have emerged, including the Barclays MSCI Green Bond Index, the S&P Dow Jones Green Bond Index, the Solactive Green Bond Index, and the Bank of America Merrill Lynch Green Bond Index. Each index reports on the performance of green bonds and uses its own methodology and criteria to incorporate bonds into the components of its index. Since all of these indices exhibit similar dynamics and show correlation coefficients close to one (Reboredo, 2018), in this study we analyzed it by looking at the S&P Dow Jones Green Bond Index (SPG) as a representation of the global green bond market.

Early studies consider the significant presence of green premium, or “greenium”, in green bonds relative to conventional bonds (Ehlers and Packer, 2017). Some researches on green bonds have examined the volatility of the green bond market (Pham, 2016) and the effectiveness of green bonds in addressing the cost of climate change (Flaherty et al., 2017). There are also studies documenting the benefits of issuing green bonds for investors and issuers. For example, some scholars have found that stock prices have a positive reaction to the announcement of green bond issuance, and the liquidity and institutional ownership of stocks have improved after the issuance of green bonds (Tang and Zhang, 2019). Similarly, some studies show that the issuance of green corporate bonds has a positive impact on financial and environmental performance and has increased green innovation and long-term green investment (Flammer, 2020). Regarding green bond pricing, some studies have analyzed the price difference between green bonds and traditional bonds. Such as the yield of a green bond is, on average, two basis points lower than that of a traditional matching bond (Zerbid, 2019). Similarly, other authors (Baker et al., 2018; Hachenberg and Schiereck, 2018; Bachelet et al., 2019; Kapraun and Scheins, 2019) also found that green bonds are yielding lower yields than traditional bonds.

There is also a relatively limited section that studies the relationship between the green bond market and other markets. Specifically, some researches find that correlations are sensitive to financial market conditions, such as volatility, economic policy uncertainty and news sentiment about green bonds (Broadstock and Cheng, 2019; Liu et al., 2021). Similarly, the team of Febi report that market liquidity affects the yield spread of green bonds (Febi et al., 2018). There some researchers analyze the links between green bonds and other traditional assets (Reboredo, 2018; Reboredo et al., 2020; Reboredo and Ugolini, 2020; Dutta et al., 2021; Liu et al., 2021; Saeed et al., 2021). And Dutta et al. studies the time-varying correlations between climate bonds and each of the major financial and commodity market and concluded that they would be affected by COVID-19 outbreak, providing the first evidence of time-variation in the hedging role of climate bonds for different markets and the impact of the COVID-19 pandemic on this role. These findings have implications in terms of portfolio and risk management decisions for environmentally aware investors holding positions in green bonds.

At present, most of the research on the relationship between the green bond market and other markets only discusses a single kind of green bond index, involving market mainly focused on the internal comparison of the bond market and the connection between the stock market, many studies do not include the commodity market. However, commodities such as gold, crude oil, etc. As an important choice for investors’ asset allocation, have an irreplaceable role. At the same time, although the existing research is based on the research background of global warming, it does not discuss whether climate risks and policy risks will really affect the linkage of the market and what kind of impact would be caused, so it is necessary and important to conduct a comprehensive research and comparative analysis of these markets and explore the linkage changes under the severe climate situation.

Due to the global representation of the green bond market, in order to test the linkage between green bonds and other markets, we obtain information about other relevant markets at the global level. These markets include: a) the US. stock market, as the dynamics of the US. dollar correlate with the risk-return profile of green bonds; b) Energy commodity markets, as the evolution of energy prices affects the viability of green projects (Reboredo, 2015), which are financed by green bonds and where we mainly consider crude oil and gold; c) China’s green bond market, to explore whether China’s green bond market has played an important role in the international market, we also include it in the study; d) Climate bonds, as more broadly climate-aligned bonds stocks (Dutta et al., 2021), we try to explore whether there is a difference between climate bonds and green bonds. Table 1 shows the data of green bonds and financial market indices, which range from 2012.6.29 to 2022.7.18.

TABLE 1. Variables selection.

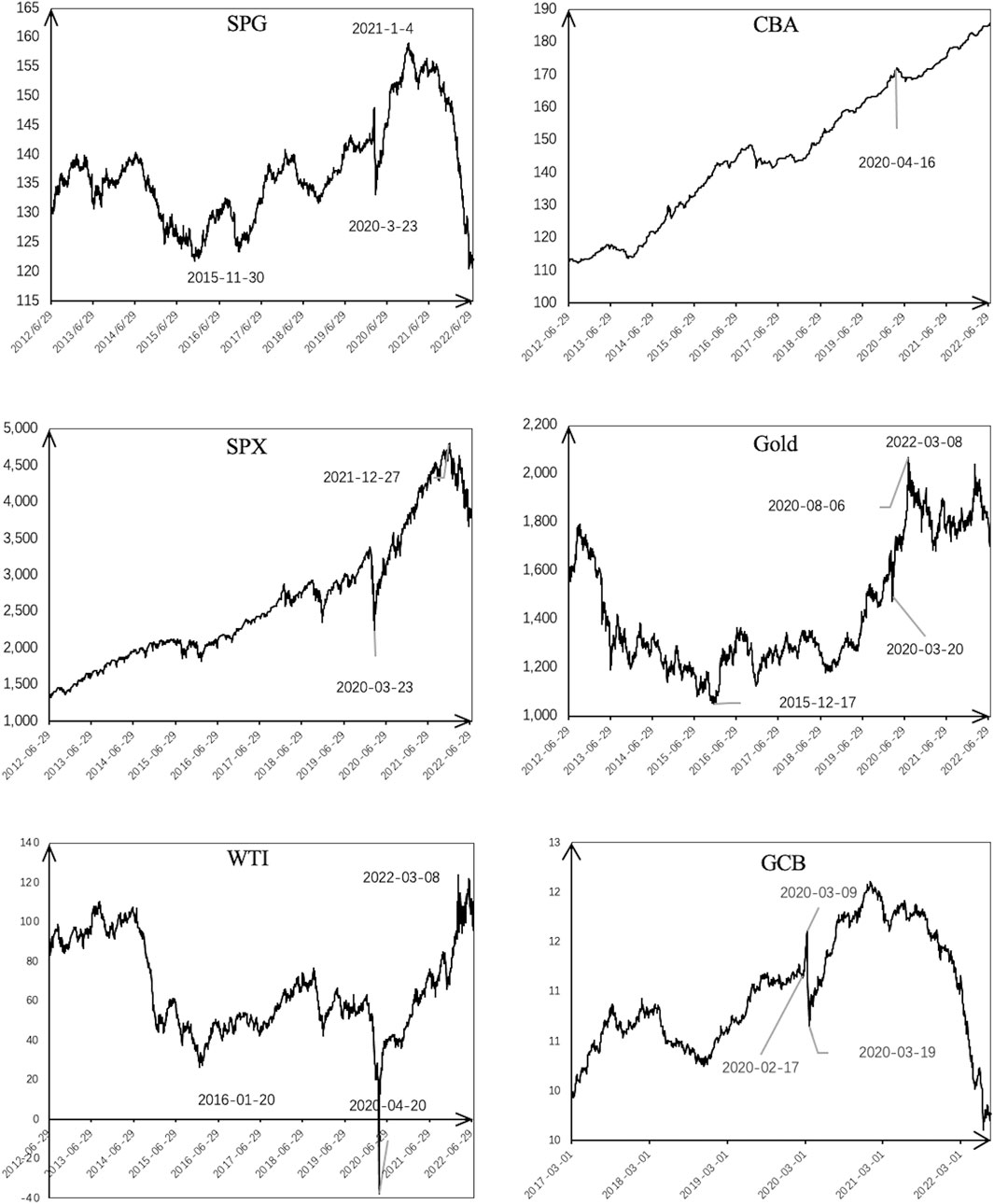

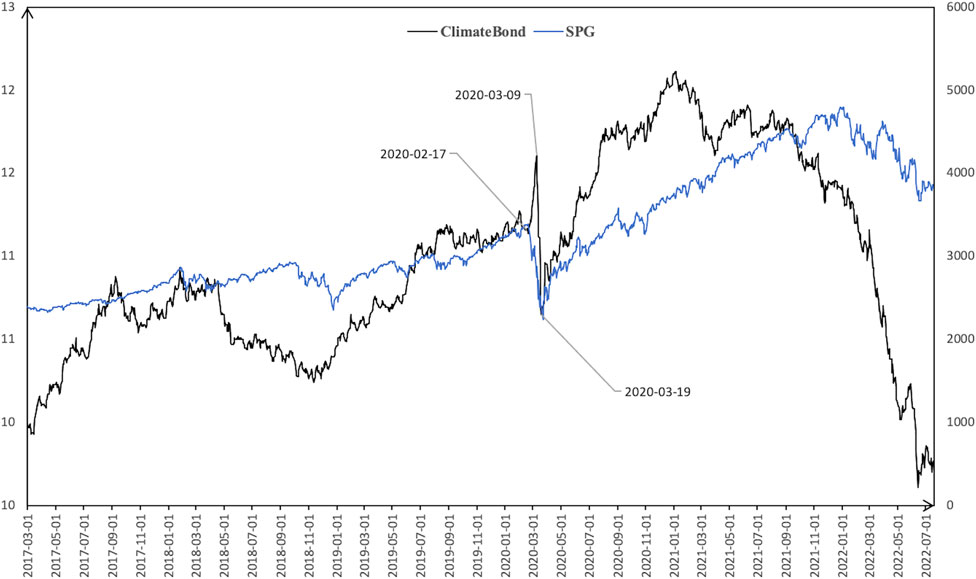

As can be seen from Figure 2, namely, the volatility trend of all asset prices, only China’s green bond index showed a steady upward trend during the sample period, while other markets showed different degrees of coactivity. In periods of stress, gold and oil tend to move in the same direction as US. stocks in the face of larger market shocks, making them less of a safe haven for stocks. In addition, a number of assets suffered sudden price declines at the same time. Specifically, SPG, GCB, SPX, WTI and Gold all fell in February 2020 and reached the lowest point around March 2020, with the maximum declines reaching 10%, 8.3%, 33.8%, 169.8% (crude oil event) and 11% respectively. We believe that the high degree of coherence between different markets has a lot to do with two factors in the same period: first, the severity of COVID-19 peaked in February 2020, and second, the increasing fear of climate risk caused by the record high temperature in Antarctica. Meanwhile, the performance of SPG and climate bonds is similar (Figure 3, correlation coefficient between the two markets is 0.6). Based on the representation of the green bond market, we finally choose Standard & Poor’s green bond as the representative of the green bond in the international market for the following research.

FIGURE 2. Trend chart of each market index.

FIGURE 3. SPG versus GCB price trends.

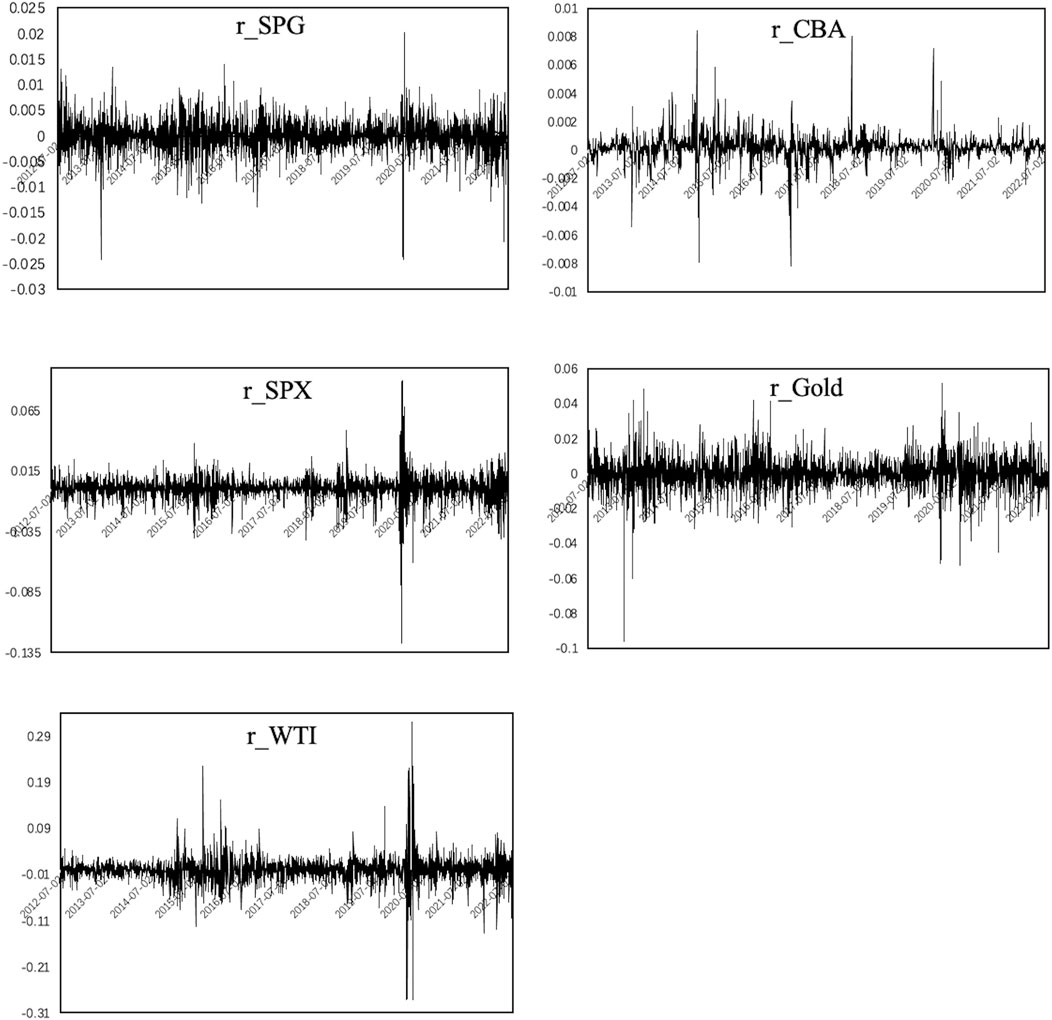

As can be seen from Figure 4, the logarithmic yield series of each asset has obvious heteroscedasticity and a strong fluctuation aggregation effect. This phenomenon indicates that the volatility of each market is time-varying and requires the application of the GARCH model to filter the residuals.

FIGURE 4. Daily logarithmic yield trend chart for each market.

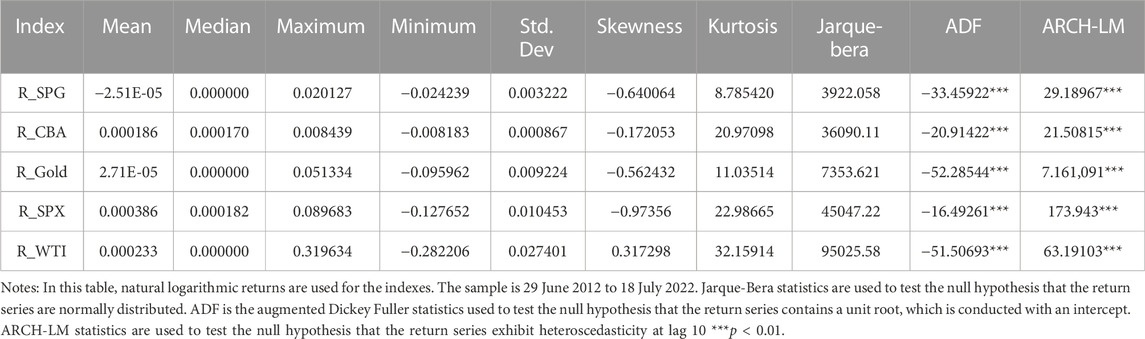

Table 2 shows the descriptive statistical analysis. From the perspective of the average yield, except for the negative SPG green bond, the average yield of the rest is positive. This shows that in recent years, the performance of S&P green bonds has not been satisfactory, which is not conducive to the development of the green bond market. Among them, the SPX S&P 500 has the highest yield and gold has the lowest yield. From the perspective of standard deviation, SPX returns and risks coexist, and the volatility is also the largest, that is, it is greatly affected by the short term, which is related to its market activity and is a yin and yang barometer of economic and financial. All yield series have a kurtosis greater than three and none of the skewness is 0, indicating that all series are spike-thick tails, and the skewness is negative, which belongs to the left trailing tail, which means that the left tail is longer than the right side, and the vast majority of values (including the median) are on the right side of the average; The higher kurtosis of each series indicates that the increase in the variance in the return of each asset is caused by the extreme value of the low frequency greater than or less than the average. The JB statistic for all yield series is well greater than 10, further proving that all sequences do not follow a normal distribution. From the stationarity test-ADF test, it can be seen that all sequences are stationary. And all have the ARCH effect, which is the green signal of the subsequent DCC-GARCH model.

TABLE 2. Descriptive statistical analysis of the daily rate of return of each asset.

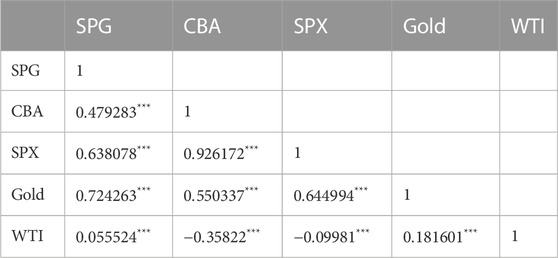

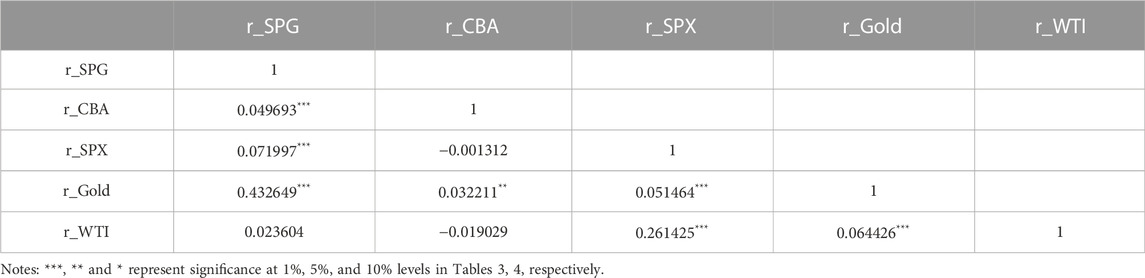

Before modeling DCC-GARCH, this paper calculates an unconditional, simple correlation coefficient for the price of each asset and its rate of return. The unconditional correlation coefficient can be used to preliminarily observe the degree of correlation between each asset, but the static correlation coefficient cannot effectively reflect the dynamic change process of the correlation of the three, which is not enough.

The correlation between the return rate of return and price of each asset can be seen in Tables 3, 4 above. For the S&P Green Bond Index, other markets are positively related, with gold assets having the highest correlation with them, followed by the US equity market. Similarly, the gold market is also positively correlated with the rest of the markets, with the more correlation being S&P green bonds and the US stock market. The relationship between China’s green bond market and other markets is also basically positive, with the highest correlation with the US stock market, except for the crude oil market. Similarly, there is a negative correlation between the US. stock market and the crude oil market.

TABLE 3. Correlation of every asset price.

TABLE 4. Correlation of the rate of return on assets.

Therefore, only the crude oil market has a negative correlation between China’s green bonds, the crude oil market and the US stock market, and there is a certain ability to resist risks. From the perspective of the trend of asset price changes, the remaining assets are in the same direction of change. For S&P Green Bond, Gold and Oil, the yield correlation with each market is nearly significantly positive. The market mix with negative correlation and not significantly coefficients is: Chinese green bonds and US stock markets, Chinese green bonds and crude oil markets. These two combinations can be hedged assets against each other.

There is a slight difference between the correlation of the price of each asset and the correlation of the rate of return. In summary, from the simple correlation coefficient alone, the China Green Bond Index is a relatively stable hedging asset for the crude oil market and the US stock market. For other markets, S&P green bonds are not a good portfolio of asset allocation.

Ordinary models are generally static for the fluctuation analysis of two series, but static methods can only describe the degree of correlation between sample populations in the mean, and cannot be sensitive to the degree of correlation between time series over different time periods.

In order to fully extract the fluctuation aggregation characteristics of the return on assets, Engel first proposed the autoregressive conditional heteroscedasticity (ARCH) model, because it needs to estimate more parameters in the process of use, Bollerslev directly introduces the lag term of the residual squared as the influencing factor of the interpreted variable on the basis of the ARCH model, and proposes a generalized autoregressive conditional heteroscedasticity GARCH model. The GARCH model plays an important role in the modeling of volatility, but its flaw is that it can only describe the volatility characteristics of a single asset and cannot reflect the correlation between the volatility of different assets. To this end, many scholars have explored the expansion of the model, and proposed diagonal VECH, CCC-GARCH, etc., each with advantages and disadvantages. For example, diagonal VECH does not fully characterize volatility, and CCC-GARCH ignores the time-varying characteristics of correlation coefficients between sequences. To further compensate for these deficiencies, Engle proposed the DCC-GARCH (Dynamic Conditional Correlational Autoregressive Conditional Heteroscedasticity Model), also known as the dynamic condition-related multivariate GARCH model, to study the relationship between market volatility. It is a good description of the dynamic correlation between multiple time series. Dynamic correlation between time series fluctuation analysis can be achieved, that is, the fluctuation between series is not a constant, but a coefficient that changes over time. Many scholars have begun to study the linkage between different markets based on this model, from a static perspective to a dynamic perspective.

This paper introduces time-variability between the DCC-GARCH model study and other major market volatility. The DCC-GARCH model of Engle (2002) has gained popularity among the researchers over the past years due to its computational advantages and power over BEKK, CCC, or VAR-GARCH models. Dong et al. analyzed the dynamic correlation between the A and B stocks of CSI and CSI in China by using the DCC-MGARCH model, and found that the overall correlation coefficient between A and B stocks in CSI was positive and had obvious time-varying characteristics (Xiuliang and Renshui, 2008). Based on the VAR-DC-GARCH model, Jia et al. studied the synergy of Chinese mainland stock markets and other Asian stock markets, and found that the Chinese mainland stock market has a significant financial contagion effect and is sustainable with developed Asian economies such as Japan and Hong Kong (Kaiwei et al., 2014). Some scholars have also flexibly applied the DCC-GARCH model to the study of the dynamic relationship between other variables, such as Liu and Li, who studied the dynamic correlation between inflation rates, government spending, consumer confidence indexes and economic growth (Weijiang and Yingqiao, 2017). It can be seen that most of the above literature uses yield data to analyze the dynamic correlation of various financial markets from different angles, and draws similar conclusions that the correlation between financial markets is not a static constant, but has different strengths at different stages of development.

The DCC-GARCH model is usually completed in two steps: first, the univariate GARCH model is estimated on a single time series, and the standardized residuals are obtained by dividing the resulting conditional variance by the residuals; Secondly, the first stage of standardized residuals is used for estimation to obtain the final dynamically related structural parameters. During the fitting process of the entire model, the solution of the parameter

Assuming

where Eq. 1 is the mean equation for a univariate GARCH model,

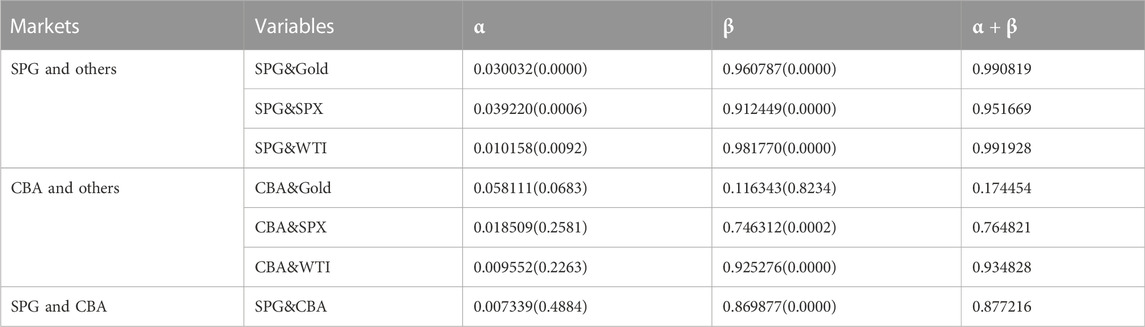

The reason why scholars pay more attention to the study of price fluctuations is that volatility is a measure of future yield uncertainty (risk), the size of price fluctuations, which means the size of the risk, and the volatility coherence can help investors to gain insight or predict the risk contagion mechanism between markets in the future, so as to better grasp the key to asset allocation, while the stock market price itself does not have research value. We obtained the coefficient of coercion between markets by using the DCC-GARCH model. This is shown in Table 5.

TABLE 5. DCC model estimation results.

According to the data in the table, the

Overall, the dynamic correlation between China’s green bonds and the gold market is not significant in the short term or long term, indicating that the fluctuations of the Chinese green bond index will not have a significant impact on gold assets, so it can be used as a hedging option. The dynamic correlation between the remaining markets is around 0.90 (the impact between CBA and SPX is small) and very significant, indicating that the dynamic correlation between other markets has a long-lasting impact on time.

Figure 5 more intuitively shows the trend of dynamic condition correlation coefficient between markets, it can be seen that the dynamic correlation coefficient between markets changes with time, the fluctuation range is large, therefore, the application of unconditional simple correlation coefficient to describe the correlation between the two markets and then hedging and other investment operations will have greater risks. Combined with the performance of the index trend in different markets, the dynamic condition correlation coefficient also changes with the performance of the index in different periods. The specific summary is shown in Table 6.

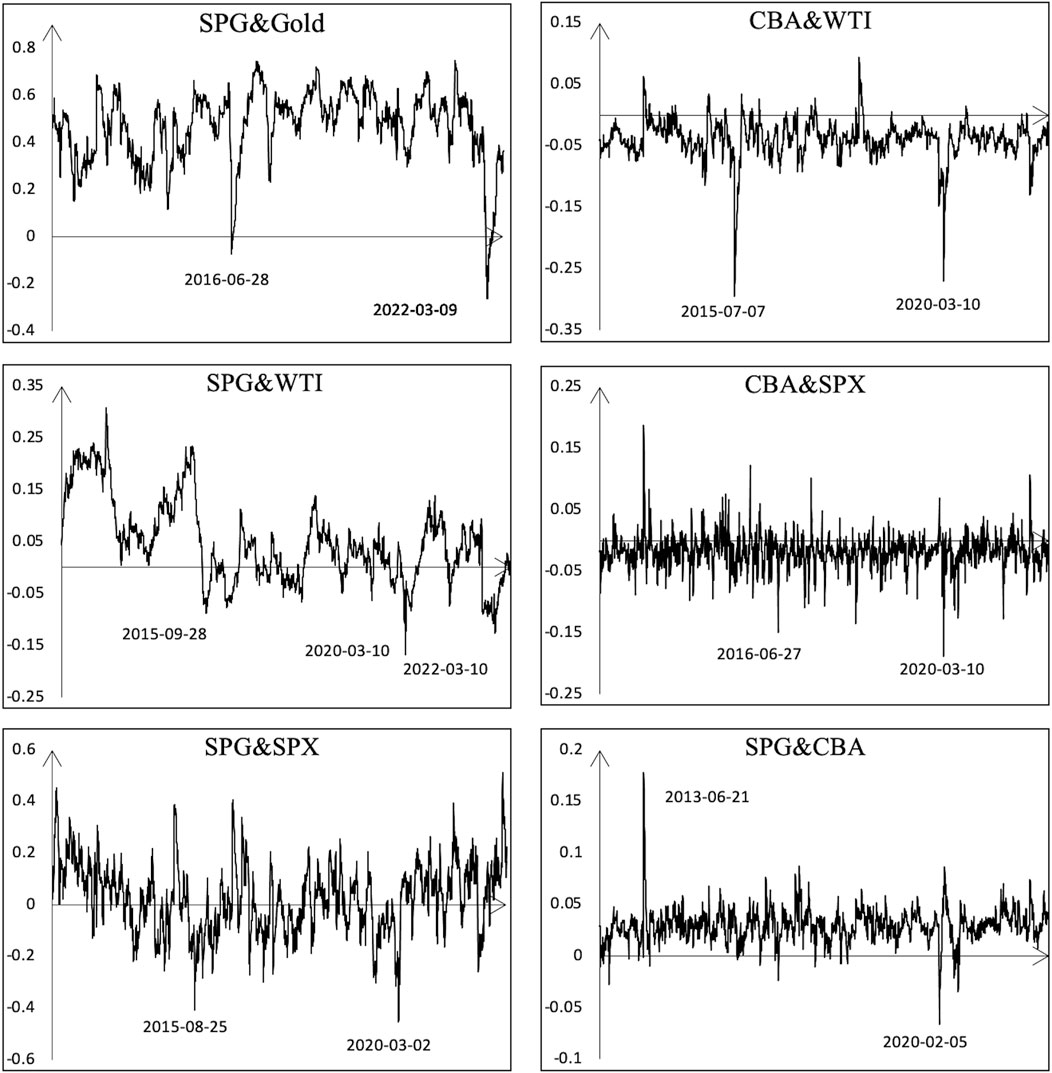

FIGURE 5. Trend graph of correlation coefficients of dynamic conditions between markets.

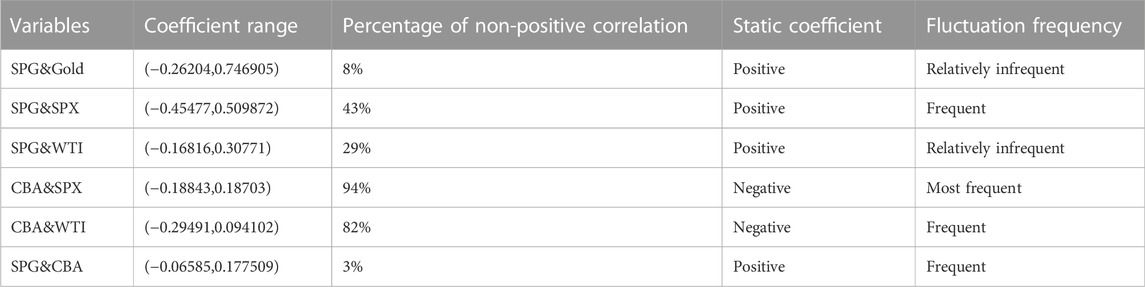

TABLE 6. Statistical analysis of correlation coefficients of dynamic conditions between markets.

As can be seen from Table 6, there are conduction factors between SPG and the other three major markets. From the sign of the dynamic condition correlation coefficient, it can be seen that the correlation between SPG and Gold, SPG and WTI, and SPG and CBA is positive for most of the time, that is, SPG has a significant positive effect on gold, crude oil and China’s green bond market. From Figure 5, it can be seen that the fluctuations between CBA and SPX and SPG and CBA are the most frequent, and small fluctuations in the former will quickly cause the latter to change; SPG and SPX and CBA and WTI are next, SPG and Gold and SPG and WTI are relatively flat. Since the hedging attribute of assets is reflected in the existence of uncorrelated or negative correlation between assets, the proportion of non-positive coefficients in the dynamic correlation between assets is listed in the table, and the stability of the hedging attribute of assets can also be measured from the non-positive proportion of correlation coefficients. The larger the proportion, the stronger the stability of risk avoidance.

The static coefficient relatively correctly expresses the overall relationship between the two assets, however, it is not possible to describe the direction and range of the changes of asset co-movement in different time periods and situations. The relationship between S&P green bonds and the gold market, China’s green bonds and crude oil markets, and the relationship between S&P green bonds and China’s green bond markets has not changed much with time, and the relationship between markets is relatively stable, respectively, positively correlated, negatively correlated and positively correlated. As a result, CBA is the only safe haven for WTI; and S&P green bonds are not a hedge for the gold market. The relationship between S&P green bonds and the crude oil market is relatively stable, and the positive relationship is maintained for more time, but when it encounters a larger shock, from Figure 5, during the worst time of the global COVID-19 pandemic (around March 2020), the correlation coefficient between the two assets reached an all-time low of negative value. So, in general, S&P green bonds cannot normally be used as a hedge against oil market risk, but they can be considered in times of major market shocks. Relatively speaking, the correlation between the US stock market and S&P green bonds and Chinese green bonds is very unstable, the fluctuations are very frequent, and the small fluctuations between the two will soon cause changes in the assets of the other party, so for the US stock market, whether it is the international or Chinese green bond index, the role of hedging risks needs to be further considered.

Faced with the serious problem of global warming, on the one hand, the risk of climate change itself will affect the market; On the other hand, the positive or negative policies promulgated by the governments will directly affect the national economy and thus have an impact on the markets. For example, at the Leaders’ Climate Summit in May 2021, Biden pledged that the United States would reduce greenhouse gas emissions by 50%–52% from 2005 levels by 2030; The European Council and the European Parliament have reached a provisional agreement on the European Climate Act, which commits the EU to reducing net greenhouse gas emissions by 55% from 1990 levels by 2030.; The decree signed by Mr. Putin aims to cut Russia’s greenhouse gas emissions by 70% from 1990 levels by 2030, among other things.

Some researches show that the main drivers of across-market linkage (i.e., the degree of market integration) are various global uncertainty indicators (Febi et al., 2018; Broadstock and Cheng, 2019; Liu et al., 2021). To further explore whether the linkage between assets is affected by climate risk and policy risk, and how these two types of risks affect the relationship between assets, we add climate risk index, climate change index (from Google Index) and Policy Uncertainty Index (EPU) for analysis. We take climate risk index and climate change index as proxy indicators of the uncertainty of climate and environment change respectively to determine whether the impact of climate and environment change will be reflected in the correlation between major markets. We took each dynamic correlation coefficient as the dependent variable and EPU and climate risk as the independent variable to conduct regression analysis. The results are listed in Table 7.

TABLE 7. Analysis of the impact of climate risk and economic risk on the linkage between markets.

As can be seen from Table 7, except for the dynamic relationship between S&P green bonds and Chinese green bonds, which are not affected by climate risks and changes in policy uncertainty, the rest of the market linkages will basically be significantly affected by climate change and policy uncertainty. It can be seen that although the two types of green bonds have certain differences, they are still similar assets, and the changes between the two have always been convergent. So climate risk and policy risk do not have much impact on the linkage between these two assets.

The increase in climate risks can significantly improve the linkage between SPG and Gold. When climate risks intensify, S&P green bond demand increases, while demand for gold increases due to the rise in risk aversion in the market due to climate risk, and S&P green bonds are in line with gold’s trend. Combined with the linkage between the two, the correlation is basically positive, so it is concluded that the two cannot be used as suitable hedging options. At the same time, because both have certain risk-off properties, policy uncertainty has little impact on the dynamic correlation between the two.

Under normal circumstances, the relationship between the stock market and the bond market fluctuates sharply, with a positive correlation mostly, and the increase in policy uncertainty will also intensify the linkage between the two. However, as climate risks increase, the correlation between the two weakens, and it may be that some investors will switch from the stock market to green bonds because of the increased climate risks in order to obtain more stable returns. This means that when climate risks intensify, green bonds may be a safe haven option for the stock market.

As for the linkage between S&P green bonds and crude oil, the correlation between the two will weaken, whether it is affected by policy or climate. Considering the maximum negative correlation between SPG and WTI during the worst of the epidemic mentioned above, people may be inclined to switch to green bonds with more stable yields when hit by risk shocks, but in general, S&P green bonds cannot hedge the risk of crude oil assets.

This paper supplements the research on the linkage between the global green bond market and various markets, by studying the time-varying dynamic correlation between three green investment instruments (S&P Green Bond, China Green Bond, and Climate Bond) and major financial asset markets. Three kinds of uncertainties are added, such as climate risk index, climate change index and policy uncertainty index, to analyze the impact of different risks on the linkage between markets under the background of climate and environmental change. The conclusions are drawn to help people clarify the trend of linkage between markets under climate risk, which is not only of guiding significance for environmental protection investors in investment decision-making, but also has certain reference significance for policymakers and market participants who want to achieve green investment. This is essential for the market to remain robust and transition smoothly to a low-carbon economy in times of stress.

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

LG: Conceptualization, Resources, Data Curation, Methodology, Software, Validation, Formal analysis, Investigation, Writing—Original Draft, Visualization. KG: Conceptualization, Methodology, Investigation, Writing—Review and Editing, Supervision, Project administration, Funding acquisition. XW: Conceptualization, Resources, Visualization.

This research was funded by the Fundamental Research Funds for the Central Universities and MOE Social Science Laboratory of Digital Economic Forecasts and Policy Simulation at UCAS.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Bachelet, M. J., Becchetti, L., and Manfredonia, S. (2019). The green bonds premium puzzle: The role of issuer characteristics and third-party verification. Sustainability 11 (4), 1098. doi:10.3390/su11041098

Baker, M., Bergstresser, D., Serafeim, G., and Wurgler, J. (2018). Financing the response to climate change: The pricing and ownership of us green bonds, (Massachusetts, United States: NBER Working Paper No), 25194.

Broadstock, D. C., and Cheng, L. T. (2019). Time-varying relation between black and green bond price benchmarks: Macroeconomic determinants for the first decade. Financ. Res. Lett. 29, 17–22. doi:10.1016/j.frl.2019.02.006

Dutta, A., Bouri, E., and Noor, M. H. (2021). Climate bond, stock, gold, and oil markets: Dynamic correlations and hedging analyses during the COVID-19 outbreak. Resour. Pol. 74, 102265. doi:10.1016/j.resourpol.2021.102265

Ehlers, T., and Packer, F. (2017). Green bond finance and certification. BIS Quarterly Review September. Available at: https://ssrn.com/abstract=3042378.

Ejaz, R., Ashraf, S., and Gupta, A. (2022). An empirical investigation of market risk, dependence structure, and portfolio management between green bonds and international financial markets. J. Clean. Prod. 365, 132666. doi:10.1016/j.jclepro.2022.132666

Febi, W., Schafer, D., Stephan, A., and Sun, C. (2018). The impact of liquidity risk on the yield spread of green bonds. Financ. Res. Lett. 27, 53–59. doi:10.1016/j.frl.2018.02.025

Flaherty, M., Gevorkyan, A., Radpour, S., and Semmler, W. (2017). Financing climate policies through climate bonds - a three stage model and empirics. Res. Int. Bus. Financ. 42, 468–479. doi:10.1016/j.ribaf.2016.06.001

Flammer, C. (2020). Corporate green bonds. J. Finan. Econ. 142 (2), 499–516. doi:10.1016/j.jfineco.2021.01.010

Gao, Y., Li, Y. Y., and Wang, Y. J. (2021). Risk spillover and network connectedness analysis of China's green bond and financial markets: Evidence from financial events of 2015-2020. N. Am. J. Econ. Financ. 57, 101386. doi:10.1016/j.najef.2021.101386

Hachenberg, B., and Schiereck, D. (2018). Are green bonds priced differently from conventional bonds? J. Asset Manag. 19 (6), 371–383. doi:10.1057/s41260-018-0088-5

Jiang, Y. H., Wang, J. R., Ao, Z. M., and Wang, Y. J. (2022). The relationship between green bonds and conventional financial markets: Evidence from quantile-on-quantile and quantile coherence approaches. Econ. Model. 116, 106038. doi:10.1016/j.econmod.2022.106038

Kaiwei, J., Yang, Y., and Linlin, L. (2014). A co-motion study of stock market timing based on rolling regression and VAR-DC-GARCH models: Is there a financial contagion of developed markets to Chinese mainland stocks? J. Bus. Res. 11, 64–71.

Kapraun, J., and Scheins, C. (2019). (in)-credibly green: Which bonds trade at a green bond premium? Available at: https://ssrn.com/abstract¼3347337.

Liu, X., Bouri, E., and Jalkh, N. (2021). Dynamics and determinants of market integration of green, clean, dirty energy investments and conventional stock indices. Front. Environ. Sci. 9, 786528. doi:10.3389/fenvs.2021.786528

Monasterolo, I., and Raberto, M. (2018). The EIRIN flow-of-funds behavioural model of green fiscal policies and green sovereign bonds. Ecol. Econ. 144, 228–243. doi:10.1016/j.ecolecon.2017.07.029

Pham, L. (2016). Is it risky to go green? A volatility analysis of the green bond market. J. Sustain. Financ. Invest. 6, 263–291. doi:10.1080/20430795.2016.1237244

Reboredo, J. C. (2018). Green bond and financial markets: Co-movement, diversification and price spillover effects. Energy Econ. 74, 38–50. doi:10.1016/j.eneco.2018.05.030

Reboredo, J. C. (2015). Is there dependence and systemic risk between oil and renewable energy stock prices? Energy Econ. 48, 32–45. doi:10.1016/j.eneco.2014.12.009

Reboredo, J. C., Ugolini, A., and Aiube, F. A. L. (2020). Network connectedness of green bonds and asset classes. Energy Econ. 86, 104629. doi:10.1016/j.eneco.2019.104629

Reboredo, J. C., and Ugolini, A. (2020). Price connectedness between green bond and financial markets. Econ. Model. 88, 25–38. doi:10.1016/j.econmod.2019.09.004

Saeed, T., Bouri, E., and Alsulami, H. (2021). Extreme return connectedness and its determinants between clean/green and dirty energy investments. Energy Econ. 96, 105017. doi:10.1016/j.eneco.2020.105017

Saeed, T., Bouri, E., and Tran, D. K. (2020). Hedging strategies of green assets against dirty energy assets. Energies (Basel) 13, 3141. doi:10.3390/en13123141

Tang, D. Y., and Zhang, Y. (2019). Do shareholders benefit from green bonds? J. Corp. Finan. 61, 101427. doi:10.1016/j.jcorpfin.2018.12.001

Weijiang, L., and Yingqiao, L. (2017). A study of the dynamic correlation between online consumer confidence index and economic growth. Financ. Trad. Res. 5, 1–10.

Xiuliang, D., and Renshui, W. (2008). The correlation of A-shares and B-shares in Chinese stock markets and its explanation based on DCC-GARCH model. Chin. Soft Sci. 7, 125–133.

Keywords: green bond, climate change, DCC-GARCH, time-varying dynamic correlation, ethical investors

Citation: Gao L, Guo K and Wei X (2023) Dynamic relationship between green bonds and major financial asset markets from the perspective of climate change. Front. Environ. Sci. 10:1109796. doi: 10.3389/fenvs.2022.1109796

Received: 28 November 2022; Accepted: 15 December 2022;

Published: 12 January 2023.

Edited by:

Pengxiang Zhai, Beihang University, ChinaReviewed by:

Zhenhua Liu, China University of Mining and Technology, ChinaCopyright © 2023 Gao, Guo and Wei. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Kun Guo, Z3Vva3VuQHVjYXMuYWMuY24=

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.