Shaoxiang Jiang

Shaoxiang Jiang Yafei Li

Yafei Li Nicole You

Nicole You

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 09 January 2023

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.1103540

This article is part of the Research Topic Sustainable Economic Growth, Green Deal and Macroeconomic Recovery – Most Suitable Pathways to Recovering From the Actual Evolutionary Hiatus View all 14 articles

Digitalization is one of the main ways for enterprise growth in the digital economy era. However, the existing literature on digital technology application models and their impact on corporate green growth is rare. By using the green innovation data of Chinese A-share listed companies from 2008 to 2020, this paper empirically investigates the association between enterprise digitalization and green innovation. The empirical results show that digitalization has significantly improved enterprises’ substantive green innovation level, which is valid after conducting a series of endogenous and robustness tests. Further results show that digital technology application, intelligent manufacturing application, and modern information system application are the three main models of digitalization to promote green innovation of enterprises, while internet business model application cannot significantly promote corporate green innovation. In addition, the mechanism analysis results indicate that the increase in government subsidy and corporate own R&D investment contribute to the incentive effect mentioned above, while the loss of governance efficiency and fluctuation of the external environment offset this effect. This incentive effect is more obvious in non-state-owned, high-tech, and lower-polluted industry enterprises. Our paper reveals the mode and mechanisms for enterprises to realize innovative green growth by applying digital technology in the digital economy era, which is of great significance to relevant theoretical research and policy formulation.

With the increasing development of the global economy, environmental pollution and ecological degradation have become common problems of human beings nowadays (Wang et al., 2020; Lin and Zhou, 2022). As green technology can improve the effective utilization of resources and reduce the pollution emission intensity in the production process (Li and Masui, 2019; Wang et al., 2020), it becomes an inevitable trend for economic and social development to support green development with technological progress (Karmaker et al., 2021; Li and Shen, 2021). However, the technical support for green development is seriously insufficient. Taking China as an example, its overall innovation level shows the characteristics of large quantity but poor quality, and the proportion of green innovation is relatively low. Due to the inherent characteristics of green innovation, such as high investment, high risk, long return cycle, and a high degree of specialization, green innovation projects face problems of insufficient investment and financing constraints (Carrión-Flores and Innes, 2010; Berrone et al., 2013; Amore and Bennedsen, 2016).

With the global economy entering the digital era, the proportion of the digital economy in the economy is increasing yearly. On the one hand, the digital economy can improve the efficiency of resource allocation and reduce the pollution emissions from ineffective production; On the other hand, it can promote green innovation through integration with the real economy and become the key to solving environmental problems. However, the impact of corporate digital transformation on green innovation is poorly studied. This paper aims to analyze the impact of corporate digital transformation and its application models on corporate green innovation and the underlying mechanisms which may contribute to solving the research gap mentioned above.

From the research perspectives of micro and macro levels, there have been many studies on the innovation incentive effect of the digital economy. From the macro perspective, previous researchers have studied the mechanisms of the digital economy promoting industrial ecological integration and innovation, thus achieving the optimization and upgrading of industrial structure and high-quality economic development. For example, Estevez and Janowski (2013), Almeida and Zouain (2016), and Das and Das (2022) study the role of the digital economy in economic development from the perspectives of sustainable development goals, business environment, financial development, international trade, entrepreneurship, respectively. These studies show that digital technology provides opportunities for innovation and promotes the organic integration between green technology innovation and green economic growth.

From the micro perspective, scholars study how digital technology can reduce production factor costs and improve resource allocation efficiency, promote enterprise technology diffusion, increase innovation output and change management mode; Aaron and Jason (2016) point out that the knowledge spillover effect of the digital economy forced the reduction of manufacturing costs within the industrial system, and enhanced the link with the external environment, so as to achieve the goal of ecological environment governance and resource protection in the process of technological innovation. Thompson et al. (2013) argue that the increasingly innovative digital technology creates multidimensional scenarios, effectively reducing inefficiency and unnecessary resource loss. Goldfarb and Tucker. (2019) find that corporate digitalization can reduce information asymmetry by improving the share of enterprise information, which thus promotes corporate green technology innovation. Mubarak et al. (2021) insist that corporate digitalization can promote collaborative innovation and realize the integration and reconstruction of knowledge in different fields, thus encouraging corporate green innovation.

However, few studies explore the digital economy’s green innovation performance from the application types of corporate digitalization. At the same time, the mechanisms behind the association between corporate digitalization and green innovation still need further analysis. This paper conducts an empirical study on the above issues using the financial data of Chinese listed companies from 2008 to 2020. By manually collecting the digital strategic keywords in the annual reports of listed companies to construct the corporate digitalization index, this paper can creatively divide their digital transformation into four types, i.e., digital technology application, intelligent manufacturing application, modern information system application, and internet business model application. Therefore, this paper can make an innovative empirical study on the impact of enterprise digital types on green innovation.

Our empirical results find that corporate digitalization can significantly improve substantive green innovation. We also conduct a series of endogenous and robustness tests, which further prove this conclusion is valid. Further results show that digital technology application, intelligent manufacturing application, and modern information system application are the three main models of digitalization to promote corporate green innovation, while internet business model application cannot. In addition, this paper finds that the incentive effect mentioned above is mainly realized by the increase of government subsidy and corporate own R&D investment, while offset by the loss of governance efficiency and fluctuation of the external environment. This incentive effect is more prominent in non-state-owned, high-tech, and lower-polluted industry enterprises.

This paper has at least three marginal contributions. First, based on the micro perspective, this paper studies the effect of green growth on enterprises under their digital transformation strategy, which deepens the understanding of the digital economy’s low carbon value and green feedback efficiency and provides micro empirical evidence for its innovation incentive effect. Second, using the text recognition method, this paper innovatively constructs the enterprise digital transformation indices by identifying the digital keywords from the annual enterprise reports, which enriches the methodology and ideas for data acquisition of related research. Third, we innovatively classify the types of corporate digital transformation and study the heterogeneous effects of different digital applications to stimulate corporate innovation, further promoting the theoretical depth of digital economy research.

As the driving force of China’s innovative development, the digital economy has become the key factor in promoting high-quality economic development. Digitalization is an inevitable choice for enterprises in the era of the digital economy and plays an important role in China’s economic transformation and development. As a new form of innovation, green innovation can drive rapid economic growth and positively affect the ecological environment. Green innovation has gradually been attached to importance by more and more enterprises and has become an innovation path universally followed by countries worldwide in pursuit of sustainable development goals.

It is generally believed that the influencing factors of enterprise green innovation mainly include environmental regulation pull, government subsidy pull, market push, R&D investment pull, technology push, etc. (Chen et al., 2017; Li et al., 2018; Wang et al., 2019). Existing research has fully proved that the digital economy has achieved technological innovation with high efficiency, low cost, and less resource loss and has become a critical path to promoting high-quality development of green innovation. Corporate digitalization can improve the efficiency of resource allocation, reduce the pollution emissions of ineffective production, and promote green innovation through integration with the real economy (Li and Shen, 2021; Liu et al., 2022). Corporate digitalization will enhance innovation efficiency and reduce innovation costs and become an important grabbing hand to solve environmental problems for substantial, sustainable development.

As an important starting point for China’s high-quality economic development, the digital economy is the government’s key focus. On the one hand, Corporate digitalization can help enterprises obtain more government subsidies and become an important driving force for enterprise development under the regulation of industrial policies and market mechanisms; Moreover, through digitalization, enterprises can optimize their innovative technology resources and increase their R&D investment (Schoenecker and Swanson, 2002), to further enhance their innovation capabilities (Subramaniam and Youndt, 2005), and thus affect their green technology innovation. On the other hand, in the process of digitalization, driven by the digital economy, the supervision, incentive, and decision-making of enterprises may be affected, thus affecting the governance efficiency of enterprises; In the wave of the digital economy, the risks and challenges brought by the new technology revolution will bring more uncertainty to the business environment of enterprises, which may affect the green innovation drive of enterprises. Therefore, this paper conducts empirical research on the relationship between corporate digitalization and green innovation from the micro level and makes research hypotheses from four aspects of resource allocation effect, R&D investment effect, corporate governance effect, and environmental fluctuation effect in mechanism analysis.

First, the digital economy improves the resource allocation effect through the enabling effect, thereby promoting green innovation of enterprises. Green innovation is a technological innovation output that comprehensively considers the environmental burden, uses new concepts and technologies, and reduces environmental pollution and raw materials and energy use. The gradual improvement of digital infrastructure has significantly promoted innovation frequency, technology diffusion, and production link optimization, thus promoting new value creation under low resource consumption conditions in the process of continuous construction and consolidation of green innovation infrastructure. The digital economy can also promote the coordinated development of economic activities, resources, and the environment. For enterprises, in the process of continuously improving the efficiency of resource allocation, the green growth of enterprises has stimulated the green innovation momentum of the digital economy. In addition, through digital construction, the digital economy can also improve the efficiency of resource integration and environmental monitoring capabilities, thus creating greater possibilities for green innovation of enterprises. For the government, the extent enterprises attach importance to green development directly determines whether they will carry out green innovation.

On the one hand, the government enables enterprises to achieve sustainable development through digitalization through industrial policies and optimizes the technological resources to carry out green innovation while enterprises undergo digitalization transformation. On the other hand, the government subsidizes enterprises in the region to carry out green innovation, and the incentive effect generated by the development of green technological innovation for enterprises also urges enterprises to carry out green innovation. Based on this, this paper proposes the first research hypothesis.

Our study sample comprises Chinese A-share companies listed on the Shanghai Stock Exchange and Shenzhen Stock Exchange from 2008 through 2020. We obtain data from at least three primary sources: The China Stock Market and Accounting Research (CSMAR) database, the WIND database, and companies’ financial reports. We drop all financial listed companies, special treatment (S.T.) firms, particular transfer (P.T.) companies, and firms with missing relevant data. We winsorized all continuous variables at 1% at both tails.

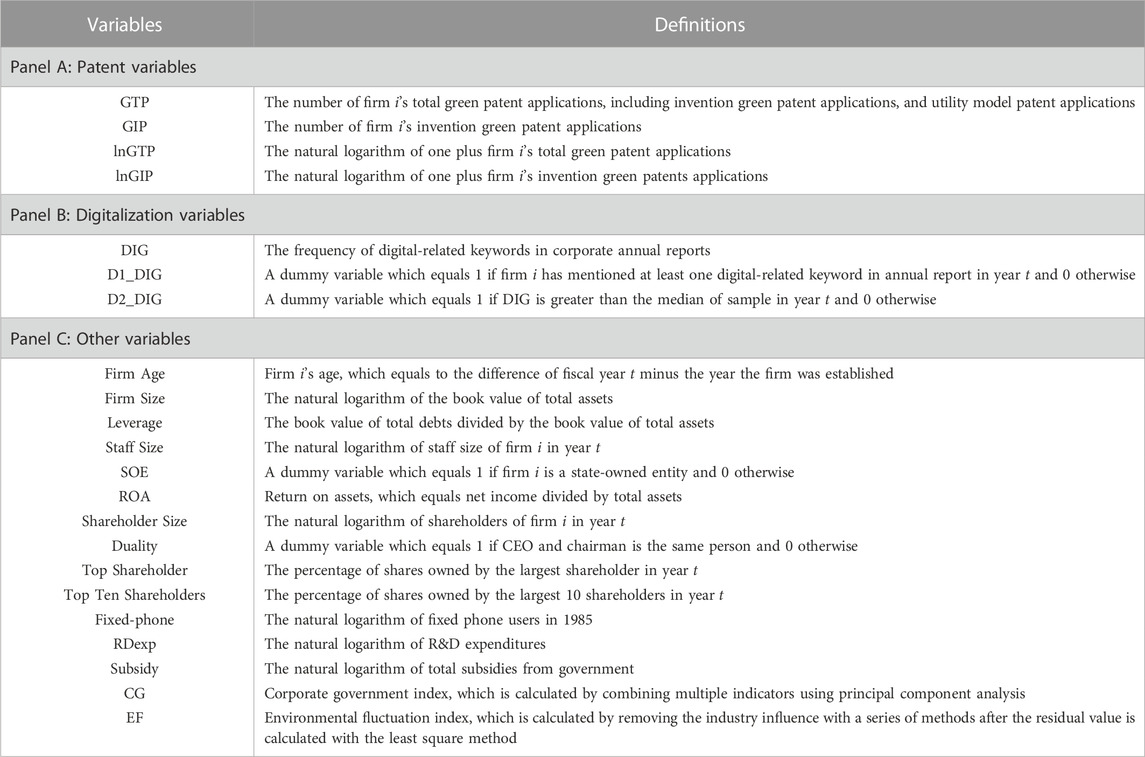

This study uses green patent applications as a proxy measure of corporate eco-innovation output. In China, patents are classified into three classes: invention patents, design patents, and utility model patents. Of the three patent classes, invention patents symbolize quality innovation (Tan et al., 2020). Therefore, in addition to using the total number of green patent applications to measure the quantity of green innovation, we also use the number of green invention patent applications to measure the quality of green inventions. We collect our patent data from the CSMAR database. We use the natural logarithm of one plus the number of green patent applications to reduce skewness bias (Wang et al., 2020).

Corporate digitalization, as our explanatory variable, is measured by the frequency of digital-related keywords that appear in corporate annual reports. Since The enterprise annual report can usually express the company’s operation status and development path (Donovan et al., 2021), we assume the annual report can also tell us about the development of corporate digitalization. We use python to calculate the frequency of digital-related keywords in the annual reports of listed companies and use it to evaluate the implementation of enterprise digital transformation. Keywords that we collected include data, digital, internet, smart, intelligent, integrated, virtual, automatic, precise, online, networking, and portable. We denote the results as

We use the baseline OLS estimation model in our estimations following prior literature. The following basic model is used:

Where

TABLE 1. Variable definitions.

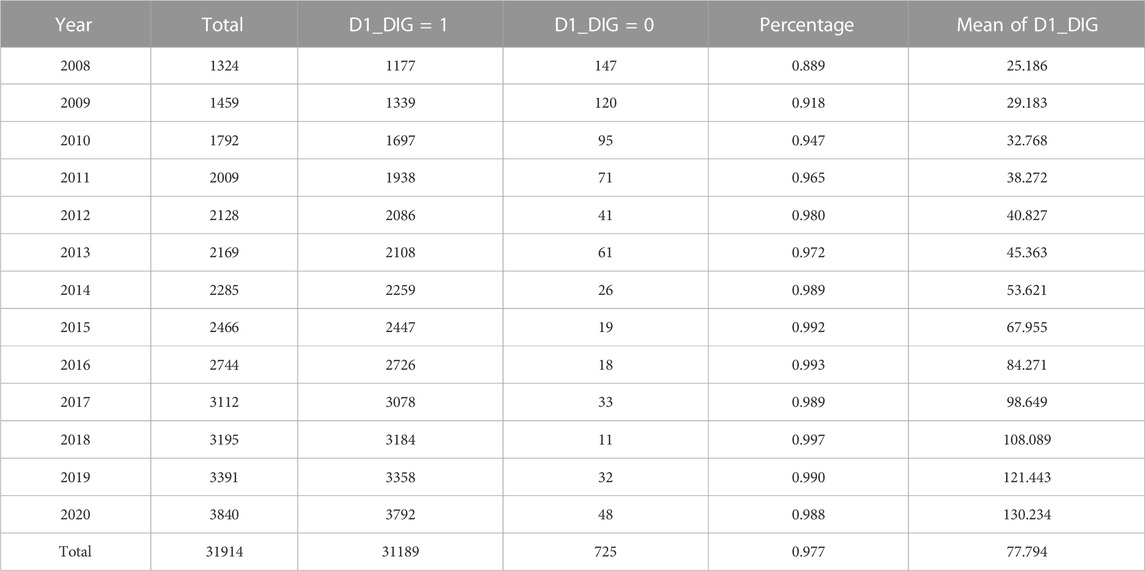

We measure the different degrees of corporate digitalization using a dummy variable D1_DIG, which equals one if the firm has mentioned at least one digital-related keyword in its annual report and zero otherwise. From Table 2, we can see that the percentage of corporate digitalization increased from 88% in 2008% to 98% in 2020, while the mean value also increased from 25.18 to 130.23. It indicates a vast increase in digitalized enterprises and a decrease in non-digitalized enterprises.

TABLE 2. Sample distribution.

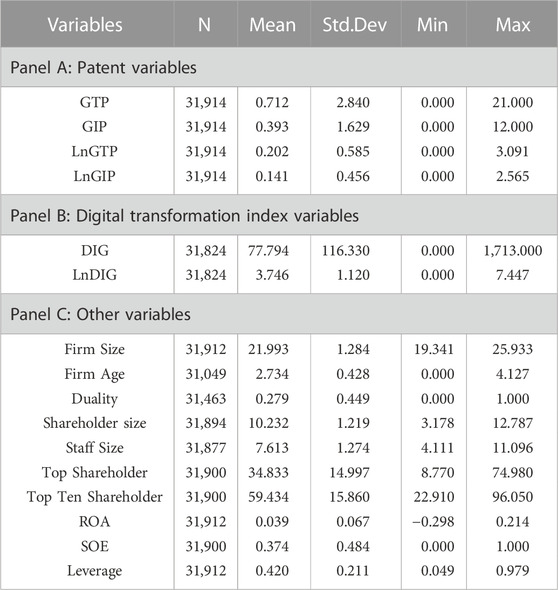

Table 3 reports descriptive statistics for variables. The average value of green invention patents is 0.712, and the average value of total green patents is 0.393, showing that the high-quality green innovation of sample companies generally accounts for about half of the total innovation. The standard deviations of

TABLE 3. Descriptive statistics.

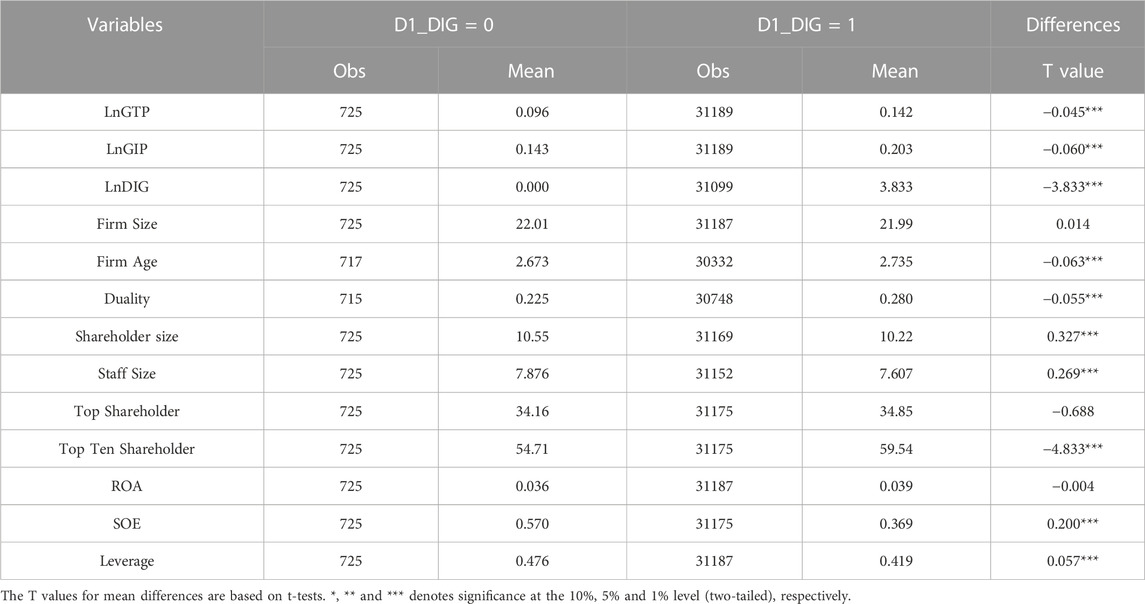

Table 4 presents univariate statistics of the average difference between digitalized and non-digitalized companies. The univariate tests show that the digitalized firms have more green patent applications than the others. Therefore, digitalized companies are more innovative than non-digitalized competitors. Table 4 also shows that digitalized companies are more profitable, less streamlined, and have fewer employees. We also observed that private enterprises are more likely to be digitalized than state-owned enterprises.

TABLE 4. Univariate analysis.

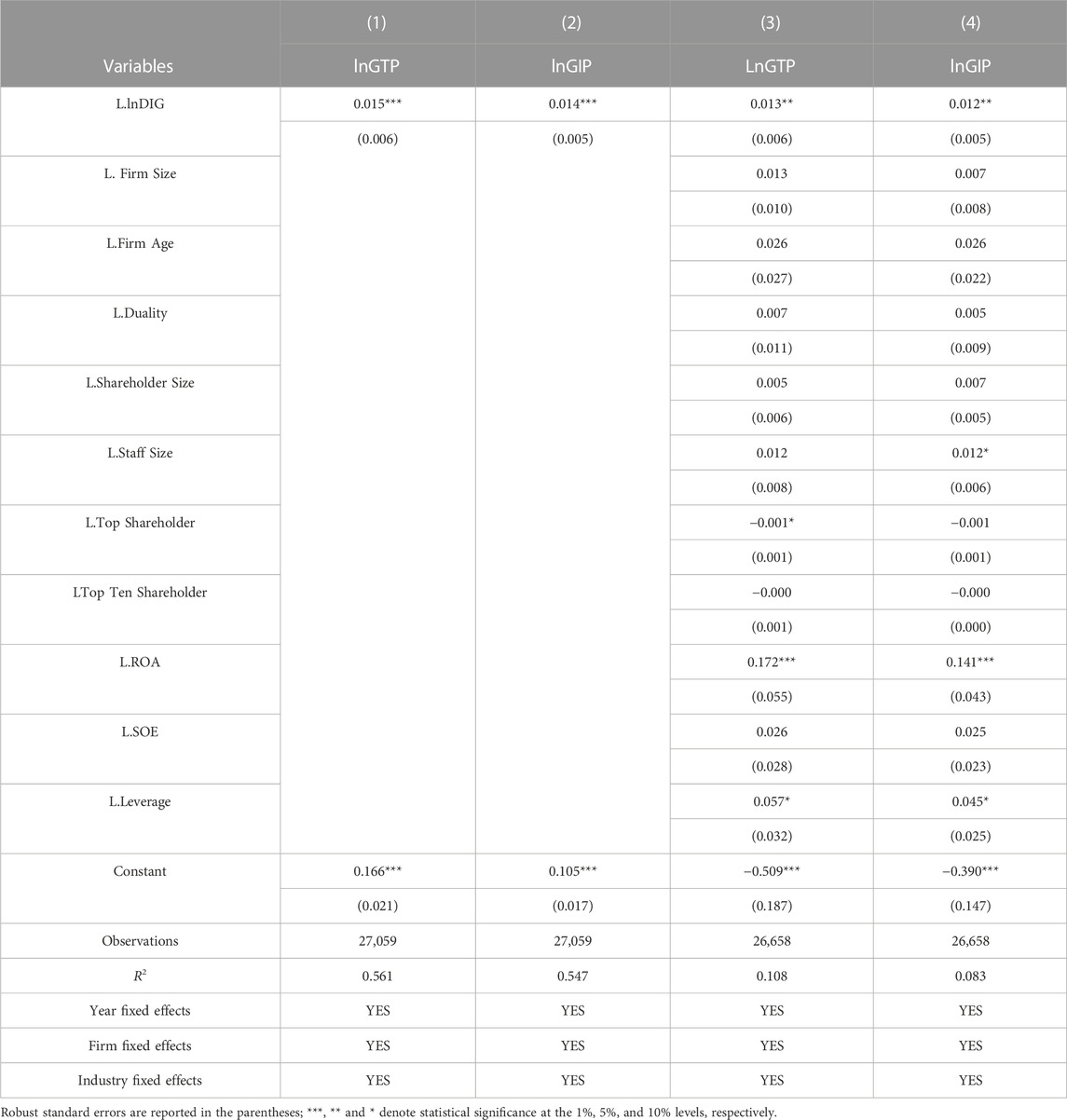

Table 5 reports our baseline results controlling the year fixed effects, firm fixed effects, and industry fixed effects. Columns 1) and 2) show the regression results without control variables, and columns 3) and 4) show the regression results with control variables. Column (3) (4) shows that after adding the control variables into the regression, the coefficients on our explanatory variables DIG to the quantity and the quality of eco-innovation is 0.014 and 0.013, respectively. Both coefficients are positive and significant at a 1% statistical level in columns 1) and 2) and a 5% statistical level in columns 3) and 4). The results show that corporate digitalization could enhance both the quality and quantity of green innovation.

TABLE 5. Baseline result.

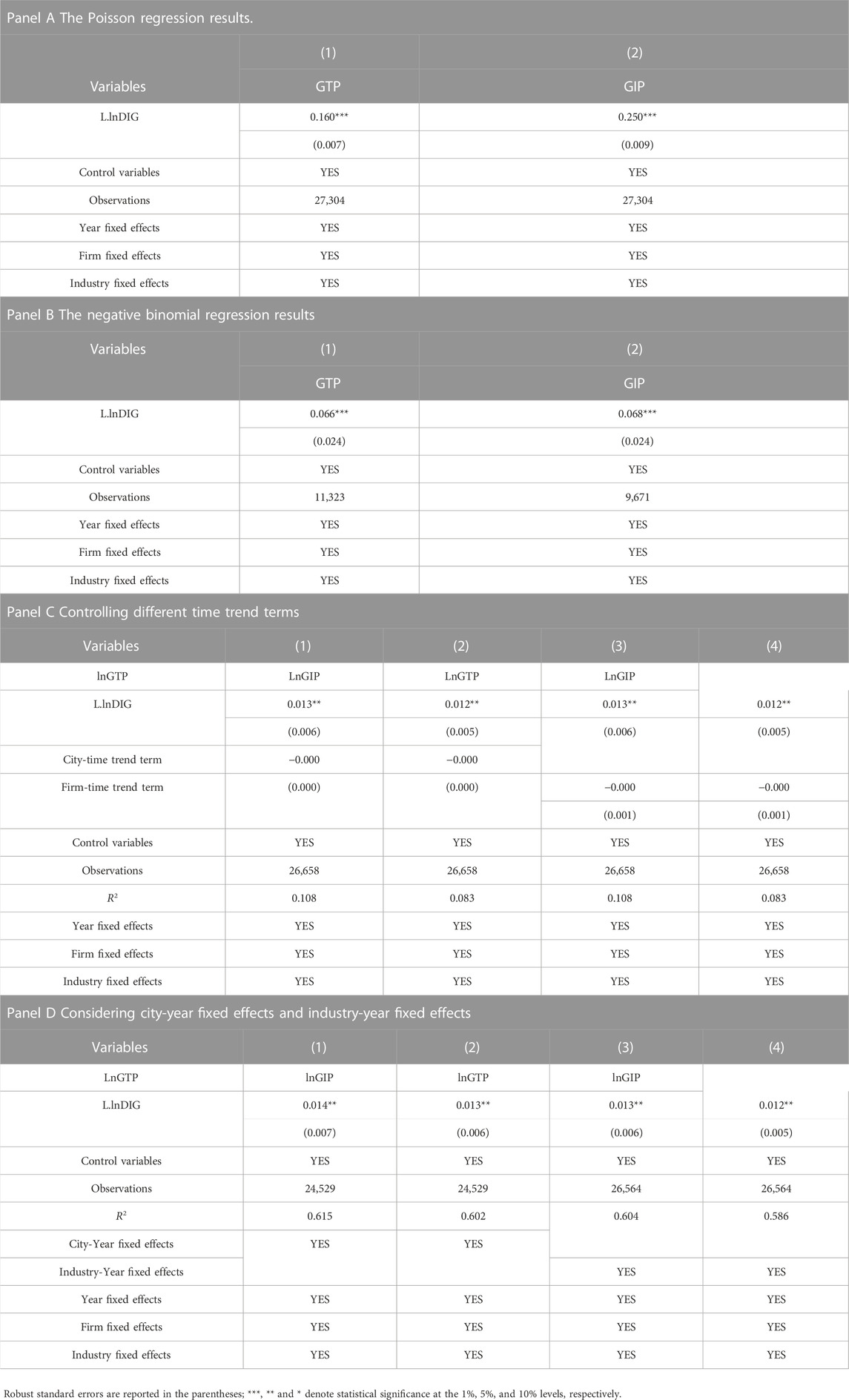

In addition, referring to the previous research, we also do a series of robustness tests to exclude other possible explanations including: 1) considering count dependent variables (Cameron and Trivedi, 2005; Yuan et al., 2015; Zhou and Zhang, 2016); 2) considering different time trends; 3) considering city-time fixed effects and industry-time fixed effects. Table 6 report the corresponding results. All robustness results support our conclusions.

TABLE 6. Considering count dependent variables.

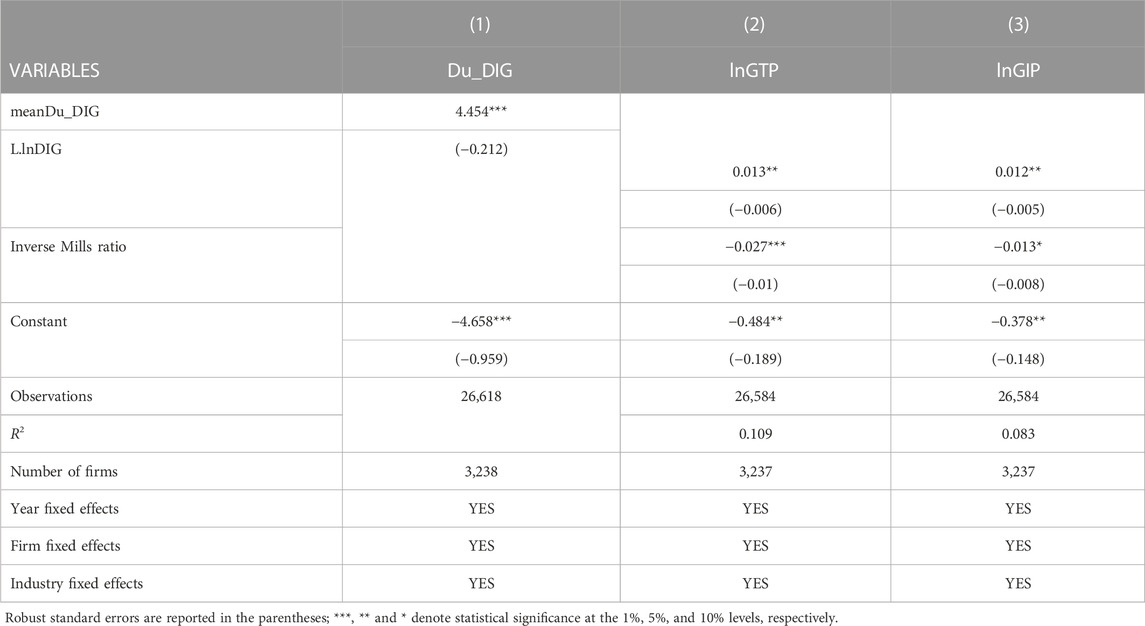

The above findings indicate a positive relationship between corporate digitalization and corporate eco-innovation. However, the results can be spurious due to confounding endogeneity bias. The main endogeneity concerns are reverse causality and omitted variable bias. We address the potential endogeneity issues using various econometric techniques, including the Heckman two-step model and instrumental variable IV) method.

The relationship between digital transformation and corporate eco-innovation may be endogenous due to sample selection bias and reverse causality. On the one hand, digitalization could promote eco-innovation. On the other hand, firms that actively engage in green R&D may also take various digital transformation initiatives to enhance eco-innovation, leading to biased and unreliable estimation results.

We employ the Heckman two-stage correction model to control for any self-selection bias in our sample firms. We use the dummy variable

TABLE 7. Heckman two-stage analysis.

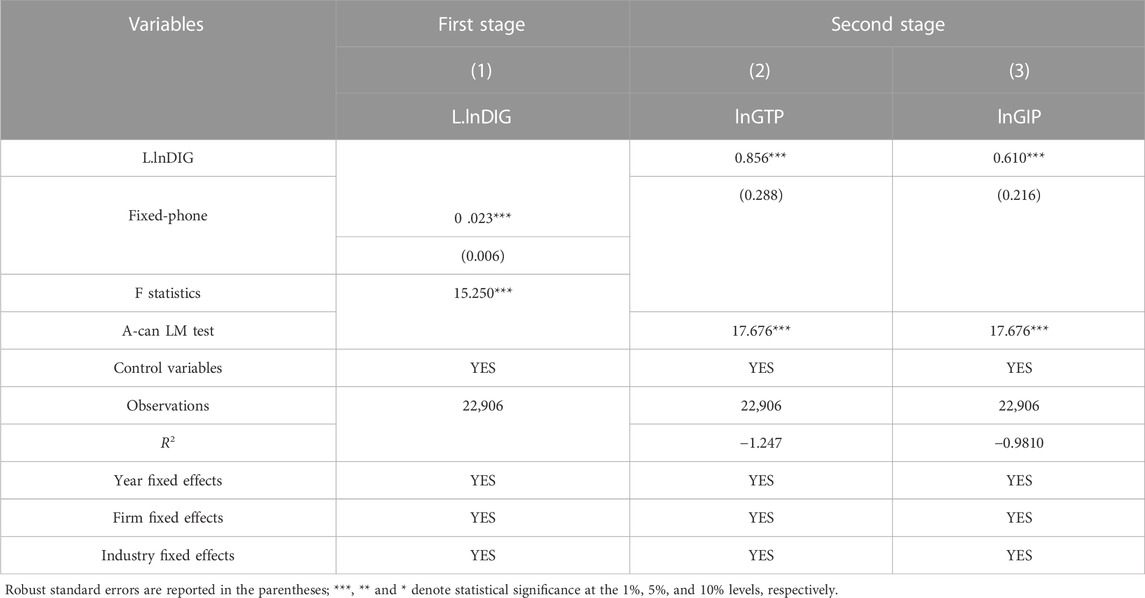

To reduce the endogeneity effect of reverse causality between digital transformation and corporate green innovation, we adopt the instrumental variable IV) approach (two-stage least squares regression method) to deal with endogeneity bias between corporate digitalization and eco-innovation. We use each region’s historical fixed telephone usage in 1985 as an instrumental variable (Fixed-phone) referring to Huang et al. (2019). The infrastructure required for using the fixed telephone is crucial to developing modern digital technology. Therefore, the popularization of fixed telephones can affect the digitalization of local enterprises. However, the use of fixed phones in the past has little to do with the green innovation of enterprises. The number of fixed telephone subscribers is cross-sectional data, which cannot be directly used for the metrological analysis of panel data. Referring to Nunn and Qian (2014), we multiply the number of firm R&D expenditures with a 2-year lag by the number of fixed telephone users in each province in 1985 to construct the interaction terms and use them as an instrumental variable for firm digitization.

We present the first and the second stage results in Table 8. The coefficient of corporate digitalization in the first stage is significant, satisfying the correlation hypothesis between the explanatory and the instrumental variables. The coefficient of corporate digitalization on green innovation is also significant in the second stage. The results support that corporate digitalization is positively related to green innovation of enterprises. In addition, the first-stage F-statistic value is greater than 10, indicating no weak instrumental variable problem. The A-can LM test result is more significant than ten, showing no unidentifiable problem and proving the validity of the instrumental variable selection. Overall, the baseline regression results still hold after considering the possible endogeneity problem in the model.

TABLE 8. Instrumental variable method.

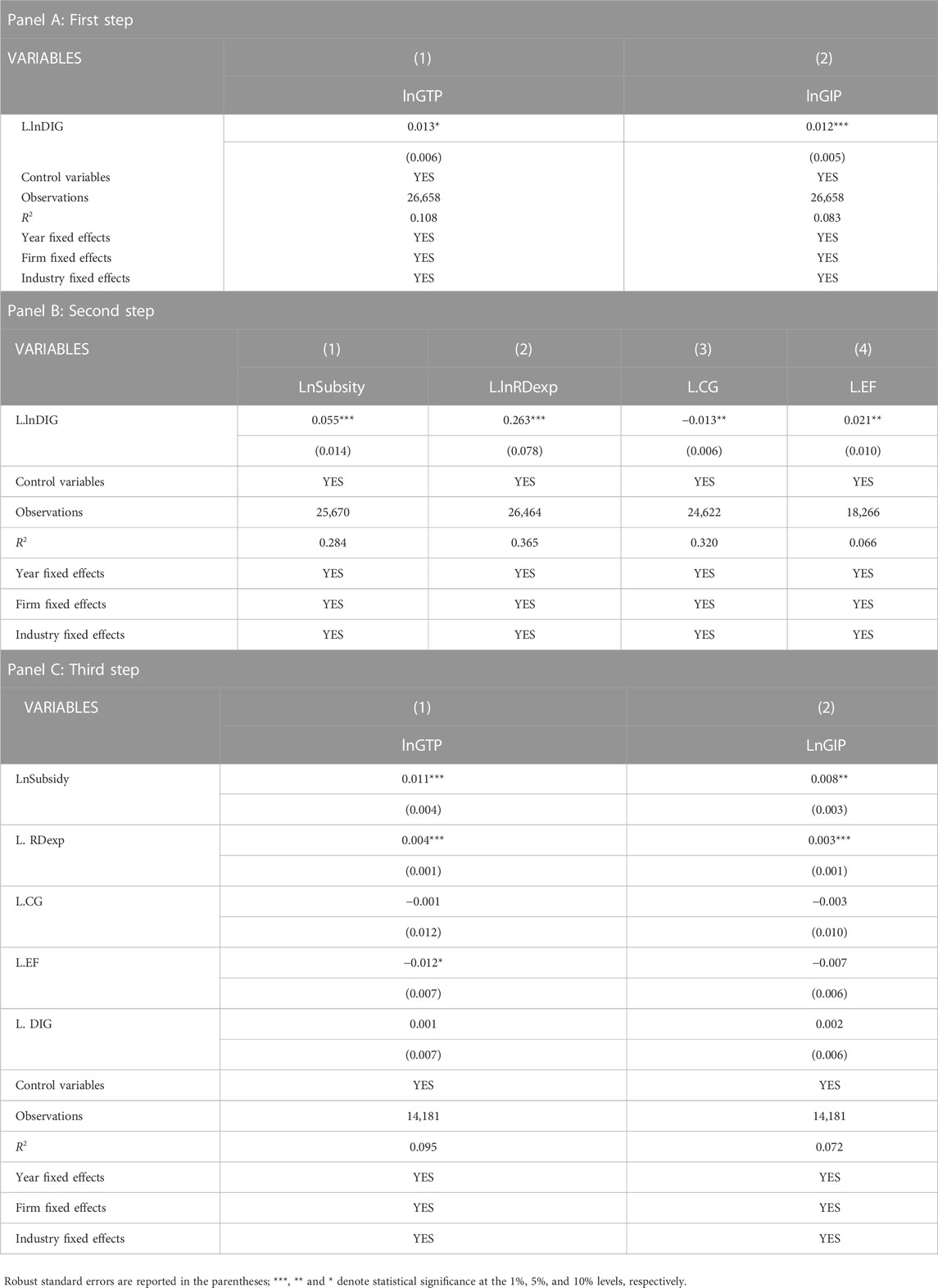

Below we explore the possible mechanisms underlying the effect of digitalization on green innovation. We propose four mechanisms: resource allocation effect, R&D investment effect, corporate governance effect, and environmental fluctuation effect.

Following the approach of Heckman, Pinto, and Savelyev (2013) and Gelbach (2016), we first estimate the effect of digitalization on eco-innovation using Eq. 3, Eq. 4, then we evaluate the effect of digitalization on mechanism variables using Eqs. 5—8, and finally we estimate the effect of digitalization and mechanism variables on green innovation using Eq. 9, Eq. 10. The equations are listed below:

Where ,

TABLE 9. Mechanisms.

To identify how corporate digitization contributes to green innovation, we first examine whether they receive higher subsidies from higher levels of digitalization. If firms could receive more subsidies, we expect them to invest more in green innovation projects. We use government subsidies to firms to examine whether subsidies are associated with corporate green innovation.

The results in Table 9, Panel B, show that the coefficient on total subsidies received by firms is positive and statistically significant at the 1% level. It indicates that firm digitization increases innovation productivity by increasing government subsidies. Next, we control for other mechanism variables in the model and repeat the estimation. The results in Panel C of Table 9 show that the coefficient on subsidy revenue (0.011) is positive and significant at the 1% level. These findings suggest that green innovation output increases with subsidy revenue and reasonably suggest that subsidy revenue is a possible channel through which firm digitization promotes green innovation output.

We then examine whether corporate digitalization enhances R&D expenditures. If corporate digitalization improves the ability to integrate information and managers could use resources more wisely, we expect them to invest more in green innovation. We use firm R&D expenditures to examine whether R&D expenditures are related to green innovation.

The results in Table 10 Panel B show that the coefficient on R&D expenditure is positive and statistically significant at the 1% level. Next, we control for digitization and other mechanical variables in the model and repeat the estimation. The results in Panel C of Table 10 show that the coefficient on R&D expenditure (0.004, 0.003) is positive and significant at the 1% level. These findings show that R&D expenditures increase with digitization and suggest that R&D expenditures contribute to innovation efficiency.

TABLE 10. Heterogeneous effect analysis.

To study this mechanism, we construct an index of corporate governance efficiency in terms of supervision, incentives, and decision-making using principal component analysis. Specifically, we first used executives’ remuneration and shareholding ratios to indicate the incentive mechanism of corporate governance. Secondly, we use the proportion of independent directors and the size of the board of directors to indicate the supervisory role of the board of directors. Thirdly, we use the proportion of institutional shareholding and the degree of equity balances (i.e., from the second to the fifth largest shareholder to the shareholding of the first largest shareholder) to indicate the supervisory role of the equity structure. Finally, we use duality to indicate the decision-making channel. We use principal component analysis to analyze corporate governance efficiency based on the above seven indicators. The first principal component in the principal component analysis reflects the comprehensive corporate governance indicators.

Panel B in Table 9 tests the impact of our enterprise’s digitization on corporate governance. The results indicate a negative correlation between digitalization and the efficiency of corporate governance, and the coefficient is significant at the 1% level. The results indicate that more digitized firms instead reduce corporate governance. We then add other mechanism variables into the regressions and control for

Finally, we study whether digitalization can reduce innovation R&D by improving the uncertainty of the operating environment. The market environment often affects the results of green innovation (Leonidou et al., 2017). The uncertainty of the market environment will bring uncertainty about the effect of green innovation (Ogbeibu et al., 2020). To measure the uncertainty of the market environment, we used the following three steps to measure: 1) Use the company’s revenue data, set them every 5 years, and do the least squares regression. The residual is denoted as the fluctuation of marketing revenue, and the coefficient multiplied by marketing revenue is denoted as the regular marketing revenue. 2) Divide the standard deviation of marketing revenue fluctuation by the regular marketing revenue and calculate the average. 3) Divide the result of the second step by the median marketing revenue of all companies in the same industry in the same year to eliminate the industry’s impact. We take the final calculated results as an index to measure the fluctuation degree of the business environment.

We first test the relationship between firm digitization and environmental uncertainty. The results in column 4) of Panel B of Table 9 show that the coefficient on environmental fluctuation is significantly negative at the 1% level. After observing the negative relationship between environmental uncertainty and R&D subsidies, we examine whether environmental fluctuation affects firms’ green innovation. The results in Table 10 show that the coefficient of environmental fluctuation remains significantly negative in column 1) but insignificant in column 2) after including environmental fluctuation and other mechanical variables in the model. The results show that digitization increases the quantity of green innovation by increasing environmental uncertainty but only significantly improves the quality of green innovation. These results may be because firms face a new digital market environment after choosing digital transformation. While benefiting from the convenience of digital technology, digitalized companies will face new issues such as market monopoly, tax erosion, and data security. These risks and challenges will bring more uncertainty to the business environment and volatility to the marketing revenue of enterprises. At the same time, this will also motivate firms to develop green innovation and establish a green competitive advantage, thus increasing the quantity of green innovation by firms.

In the above sections, we tested the mechanisms related to the digital economy that can affect the green innovation of enterprises through the resource allocation effect, R&D investment effect, corporate governance effect, and environmental fluctuation effect. In order to further test and quantify the above mechanisms, this paper refers to Gelbach (2016) to quantitatively decompose the mechanisms. The contribution of green innovation promoted by the resource allocation effect is 20.70%; the contribution of green innovation promoted by the R&D investment effect is 36.00%; the contribution of green innovation reduced by the environmental uncertainty effect is 8.62%. Although the contribution of the corporate governance effect to green innovation is 0.4%, it is clear from the previous section that this effect does not significantly impact green innovation. The above effects explain 65% of the total impact. This result also shows that the mechanisms above are plausible and indicate that the resource allocation and R&D investment effects strongly influence the digital economy to enhance corporate green innovation.

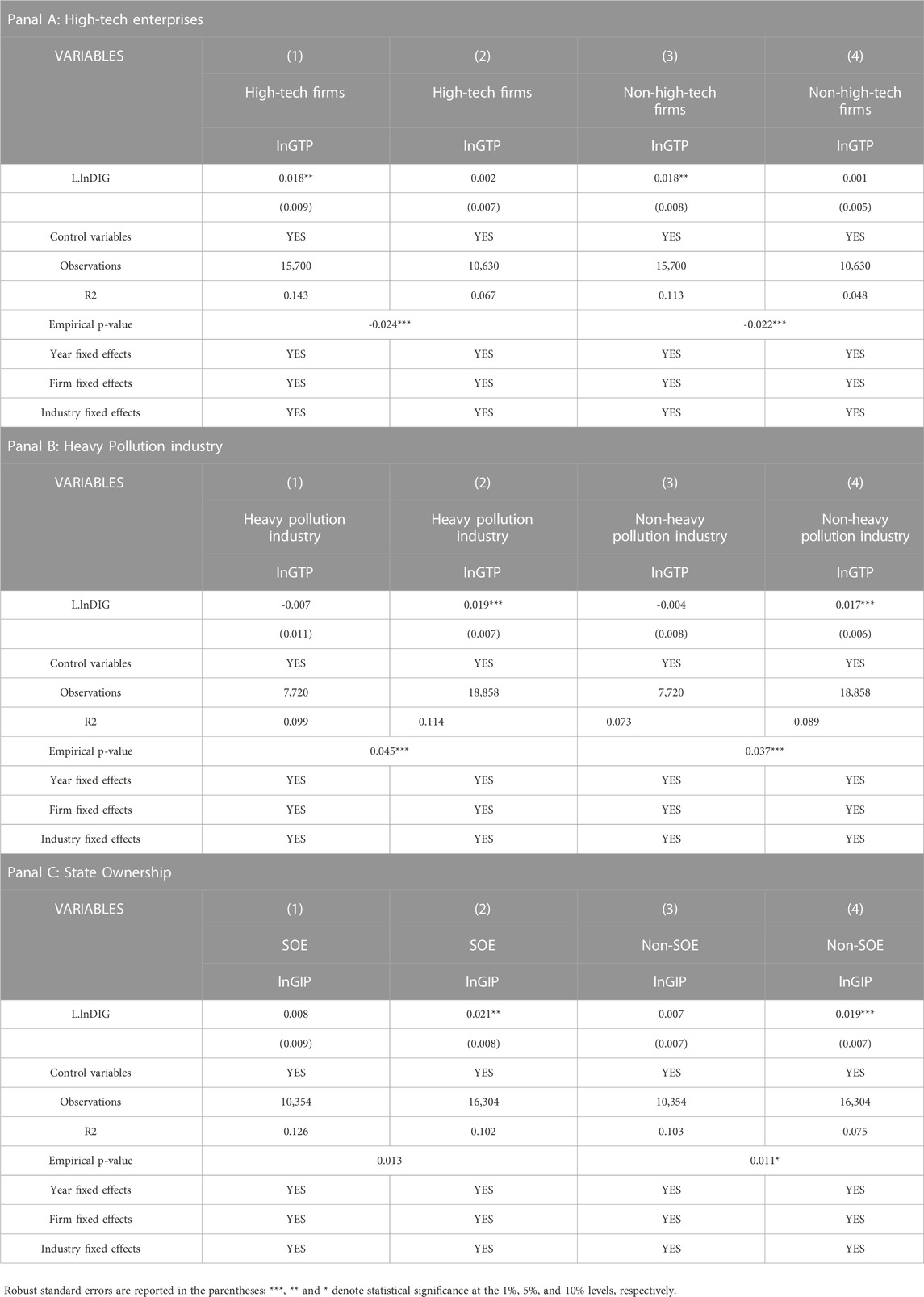

In this section, we examine the impact of digitalization on the green innovation activities of different types of firms by dividing the study sample into three dimensions: technology density, firm pollution, and firm ownership. The results are reported in Table 10.

Under the regulation of market requirements and competition mechanisms, the high-tech industry will focus on developing green products with less pollution and low energy consumption as the focus of the future development of enterprises. It is because most high-tech enterprises are knowledge and technology-intensive, and knowledge integration is an effective way and important mechanism for enterprises to carry out green innovation (Strambach, 2017). Technology can promote open innovation in enterprises, thus encouraging enterprises to engage in green innovation activities (Mubarak et al., 2021). High technology industries are more willing to carry out green innovation and improve the efficiency of resource use in the process of digitalization transformation, and then further enhance the competitiveness of enterprises. Therefore, this paper believes that for high-tech enterprises, digitalization has a greater incentive effect on green technology innovation.

To examine the impact of digitization on firms with different technology densities, we divide the sample firms into groups according to whether they are high-tech firms or not. This paper refers to Peng and Mao (2017) and classifies enterprises in 19 industries as high-tech enterprises in manufacturing, software and information technology services, and scientific research and technology services. Panel A in Table 10 shows the impact of firms on

Driven by the new development concept of the country and guided by the government’s industrial policies, in the process of sustainable development, it is an inevitable choice for enterprises to gradually reduce pollutant emissions, improve resource utilization efficiency, and gradually eliminate industries with heavy pollution and high resource consumption. Considering the business attributes and industry traits of heavy pollution industries, it is difficult for heavy pollution firms to reduce their pollutant emissions through digitalization, and gradually being eliminated by alternative industries seems to be the default path for industry development, while light pollution firms are more motivated to carry out green technology innovation in the process of digitalization to avoid being eliminated by the government. Therefore, this paper believes that for light pollution industries, digitalization has a greater incentive effect on green technology innovation.

We then investigate whether the motivation of enterprises in heavy pollution industries to green innovation may be more assertive. We classified 16 industries, including coal, mining, textile, paper making, pharmaceutical, and chemical, as heavy pollution following the Classified Management Directory of Environmental Protection Verification Industries of Listed Companies formulated by the Ministry of Environmental Protection of China in 2008. The results are presented in panel B of Table 10.

All empirical p-values of the regression are significant, allowing us to compare the coefficients of the two regression groups. Columns 1) and 3) show that the regression coefficient of enterprises belonging to heavy pollution industries is insignificant. In contrast, the coefficient of enterprises belonging to non-heavy pollution industries is positive and significant at a 1% level. The results show that enterprises in non-heavy pollution industries can better promote green innovation through digital transformation.

For industries such as coal mining and paper making, which generate massive pollution, digitalization cannot fundamentally change the fact that these industries need to produce through massive pollution. Therefore, the incentives for such enterprises’ green innovation activities are insignificant.

State-owned enterprises play an important role in China’s economic structure and provide a research perspective for studying the heterogeneous effects of ownership on the digital economy. Compared with non-state-owned enterprises, China’s state-owned enterprises face smaller financing constraints and have more political resources, so state-owned enterprises have a greater ability to make a green investment. In addition, as state-owned enterprises assume more political views, they will actively invest in green innovation projects in the context of the Chinese government’s increasing emphasis on green and innovative development. Therefore, the green innovation activities of state-owned enterprises are less constrained by financing constraints and more pressured by political tasks. On the contrary, the development of the digital economy has less impact on their green innovation strategies. On the contrary, non-state-owned enterprises face greater financing constraints and various resources, and the digital economy can better play the governance effect and resource allocation effect to improve their willingness and ability to invest in green innovation. Therefore, this paper argues that for SOEs, the incentive effect of digitalization on green technology innovation generated by them is greater.

Therefore, we empirically investigate whether the impact of firm digitization on green innovation varies with firm ownership. The results in Table 10 show that the coefficient is significant at the 1% level for non-state-owned firms, while it is not significant for state-owned firms. The results suggest that digital transformation is more critical in achieving better green innovation outcomes for non-state-owned firms than private firms.

These results may be due to the different enterprise structures. Non-SOEs have fewer resources and higher financing constraints, so digital transformation can help non-SOEs achieve green innovation and form the market’s competitiveness of non-SOEs.

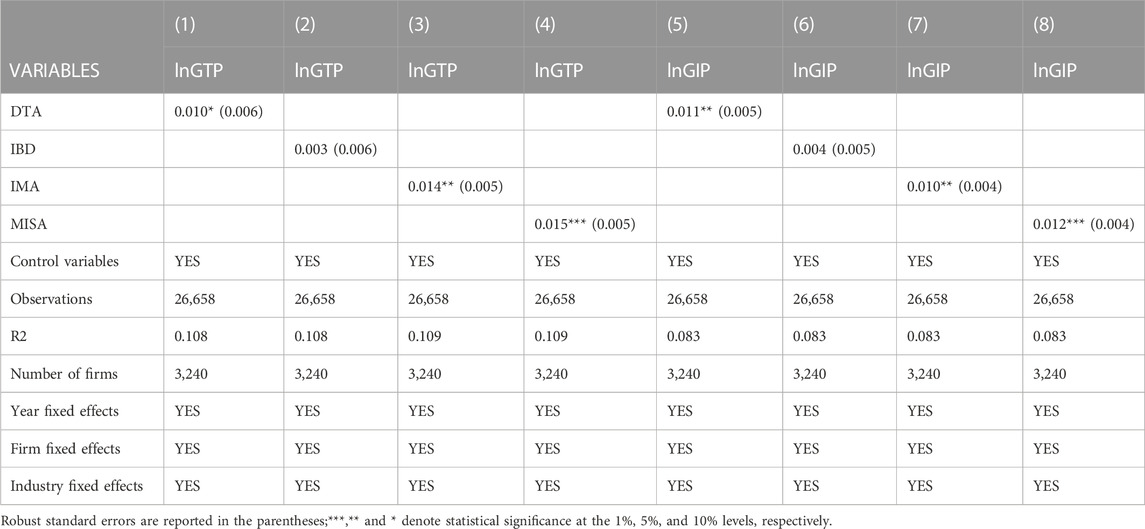

To further investigate which dimensions of digital development have influenced the level of corporate green innovation. We used text analysis referring to Wang et al. (2020), by converting the annual reports of listed companies from 2008 to 2020 into text format. We then filtered the high-frequency words related to digital transformation by python’s crawler function. We divided them into digital technology applications (

The results in Table 11 show that digital technology applications, intelligent manufacturing applications, and modern information system applications are the three main approaches to promoting green innovation. Columns 1) and 5) show that digital technology application has a 5% and 10% significance level, respectively. Columns 3) and 7) show that intelligent manufacturing application has a 5% significance, and columns 4) and 8) show that modern information system application is more likely to promote green innovation in the company at a 1% significant level. In contrast, internet business models of digitalization do not significantly contribute to corporate green innovation. The results show that modern information system application promotes the quantity and quality of green innovation more than other approaches. Therefore, enterprises need to prioritize the development of modern information systems and strengthen information sharing ability. Secondly, consider optimizing the application of digital technology in manufacturing processes and data platforms, which can help improve the level of green innovation in enterprises. Finally, the excessive investment of enterprises in e-commerce development may not benefit corporate green innovation.

TABLE 11. Digitalization in four dimensions.

In the background of global green transformation, green technology innovation is an inevitable requirement for achieving high-quality development. The rapid two-way integration of the digital and real economy has led to the continuous optimization of industrial structure. Based on the annual reports of Chinese listed companies from 2008 to 2020, this paper obtains each company’s annual digital transformation information using the text recognition method and constructs a database of corporate digitalization. By matching the digitalization indices with the green innovation and financial data of enterprises, this paper empirically studies the association between corporate digital transformation and green innovation. Based on the empirical results, this paper draws the following conclusions:

• Corporate digitalization can improve the substantive green innovation of enterprises.

• Digital technology applications, intelligent manufacturing applications, and modern information system applications are the three main models of corporate digitalization to promote green innovation.

• The internet business model application cannot promote corporate green innovation.

• The increase in government subsidy and corporate own R&D investment contribute to the incentive effect mentioned above, while the loss of governance efficiency and fluctuation of the external environment offset this effect.

• Compared to other enterprises, this incentive effect is more prominent in non-state-owned, high-tech, and lower-polluted industry enterprises.

Based on the above research conclusions, to give better play to the incentive role of the digital economy promoting corporate green innovation and realizing corporate green growth, this paper puts forward the following policy recommendations. First, the government should promote the application of digital technology in enterprise production to enable enterprises to achieve sustainable development through digitalization. Our study shows that digitalization can stimulate enterprises to carry out green technology innovation and achieve the integration of enterprise development and sustainable production. Therefore, government departments should encourage enterprises to promote cloud computing, blockchain, digital simulation, big data analysis, and other technologies in production, management, and innovation. In addition, the government can build a sustainable R&D innovation system based on digital technology to enable enterprises to achieve intelligent environmental governance and green production with digitalization.

Second, enterprises should use digital technology to strengthen the construction of internal and external information-sharing platforms to enhance their governance level. This study shows that corporate digitalization can promote enterprise green technology innovation by improving the governance level. Therefore, enterprises should strengthen the application of digital technology in production and manufacturing, energy consumption management and control, supply chain and other processes, rely on digital technology to realize the sharing of internal and external knowledge and information, invest more in green R&D projects, and improve the efficiency of green technology innovation.

Third, in the context of the rapid development of the digital economy, environmental protection departments should use fiscal and tax means to guide green investment in the capital market. This paper finds that external environmental regulation and capital market investment will affect the incentive effect of corporate digitalization promoting green. Enhancing government subsidies is one mechanism behind corporate digitalization that promotes green innovation. Therefore, the government should adopt various policies, such as taxation and financial subsidies, to guide the capital market to invest in corporate green projects to encourage enterprises better to invest in environmental protection and enhance environmental governance capability. In addition, give non-SOEs with higher financing constraints, taxation and financial subsidies are important external financing for them. Therefore, the government can provide more taxation and financial subsidies for the digital projects of non-SOEs to encourage their digitalization.

Forth, the government should adopt different digital development policies for different enterprises. This paper finds that the promotion of corporate digitalization on innovation has a heterogeneous effect. As high-tech enterprises are the main force of digital technology innovation and application, the government should introduce incentive policies to ensure their digital development. For SOEs who have enough financing and resources, the government can encourage their digitalization through administrative guidance rather than financial support. For polluting enterprises, the government can implement constraint policies to guide their digitalization and green development.

However, this paper still has some limitations, which point out the direction for future research. First, corporate digitalization is a more complex and gradually evolving concept. Although this paper obtains enterprise digital transformation by identifying digital keywords in the company’s annual reports, the indices we use still cannot directly reflect the application of digital technology in enterprises. Subsequent research can measure corporate digital transformation by direct evidence of their application of key digital technologies. Second, the research object of this paper is China’s listed companies, which may not represent the digital economy practice of other countries or non-listed companies. On the one hand, due to China’s strong support for digital technology and implementation of a series of digital strategies in recent years, its domestic digital development is fast, so the digital transformation of Chinese enterprises is also fast. On the other hand, listed companies are often the best in their industries, and their digital technology applications have generally reached the frontier of the industry. Future research can provide more empirical evidence by selecting data from other countries or non-listed companies to expand relevant conclusions.

Publicly available datasets were analyzed in this study. This data can be found here: https://www.gtadata.com/.

All authors listed have made a substantial, direct, and intellectual contribution to the work and approved it for publication.

This research was supported by the National Natural Science Foundation of China (Grant number: 72,173,072) and the China Postdoctoral Science Foundation (Grant number: 2022T150022).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Almeida, G. D. O., and Zouain, D. M. (2016). E-Government impact on business and entrepreneurship in high-upper-middle- and lower-income countries from 2008 to 2014: A linear mixed model approach. Glob. Bus. Rev. 17 (4), 743–758. doi:10.1177/0972150916645485

Aaron, P., and Jason, S. (2016). The end of ownership: Personal property in the digital economy. cambridge: The MIT Press.

Amore, M. D., and Bennedsen, M. (2016). Corporate governance and green innovation. J. Environ. Econ. Manage. 75, 54–72. doi:10.1016/J.JEEM.2015.11.003

Berrone, P., Fosfuri, A., Gelabert, L., and Gomez-Mejia, L. R. (2013). Necessity as the mother of ‘green’ inventions: Institutional pressures and environmental innovations. Strateg. Manag. J. 34, 891–909. doi:10.1002/SMJ.2041

Cameron, A. C., and Trivedi, P. K. (2005). Microeconometrics: Methods and applications. New York, NY: Cambridge University Press.

Carr, A. S., and Kaynak, H. (2007). Communication methods, information sharing, supplier development and performance: An empirical study of their relationships. Int. J. Operations Prod. Manag. 27 (4), 346–370. doi:10.1108/01443570710736958

Carrión-Flores, C. E., and Innes, R. (2010). Environmental innovation and environmental performance. J. Environ. Econ. Manag. 59 (1), 27–42. doi:10.1016/j.jeem.2009.05.003

Chen, J., Cheng, J., and Dai, S. (2017). Regional eco-innovation in China: An analysis of eco-innovation levels and influencing factors. J. Clean. Prod. 153, 1–14. doi:10.1016/j.jclepro.2017.03.141

Das, A., and Das, S. S. (2022). E-government and entrepreneurship: Online government services and the ease of starting business. Inf. Syst. Front. 24 (3), 1027–1039. doi:10.1007/s10796-021-10121-z

Donovan, J., Jennings, J., Koharki, K., and Lee, J. (2021). Measuring credit risk using qualitative disclosure. Rev. Account. Stud. 26 (2), 815–863. doi:10.1007/s11142-020-09575-4

Estevez, E., and Janowski, T. (2013). Electronic governance for sustainable development—conceptual framework and state of research. Gov. Inf. Q. 30, S94–S109. doi:10.1016/j.giq.2012.11.001

Gelbach, J. B. (2016). When do covariates matter? And which ones, and how much? J. Labor Econ. 34 (2), 509–543. doi:10.1086/683668

Goldfarb, A., and Tucker, C. (2019). Digital economics. J. Econ. Literature 57 (1), 3–43. doi:10.1257/jel.20171452

Grove, H., Clouse, M., and Schaffner, L. G. (2018). Digitalization impacts on corporate governance. J. Gov. Regul. 7 (7), 51–63. doi:10.22495/jgr_v7_i4_p6

Heckman, J., Pinto, R., and Savelyev, P. (2013). Understanding the mechanisms through which an influential early childhood program boosted adult outcomes. Am. Econ. Rev. 103 (6), 2052–2086. doi:10.1257/aer.103.6.2052

Huang, Q., Yu, Y., and Zhang, S. (2019). Internet development and productivity growth in manufacturing industry: Internal mechanism and China experiences. China Industrial Economics 8, 5–23. doi:10.19581/j.cnki.ciejournal.2019.08.001

Karmaker, S. C., Hosan, S., Chapman, A. J., and Saha, B. B. (2021). The role of environmental taxes on technological innovation. Energy 232, 121052. doi:10.1016/J.ENERGY.2021.121052

Kohli, R., and Melville, N. P. (2019). Digital innovation: A review and synthesis. Inf. Syst. J. 29 (1), 200–223. doi:10.1111/isj.12193

Leonidou, L. C., Christodoulides, P., Kyrgidou, L. P., and Palihawadana, D. (2017). Internal drivers and performance consequences of small firm green business strategy: The moderating role of external forces. J. Bus. ethics 140 (3), 585–606. doi:10.1007/s10551-015-2670-9

Li, G., and Masui, T. (2019). Assessing the impacts of China’s environmental tax using a dynamic computable general equilibrium model. J. Clean. Prod. 208, 316–324. doi:10.1016/J.JCLEPRO.2018.10.016

Li, D., and Shen, W. (2021). Can corporate digitalization promote green innovation? The moderating roles of internal control and institutional ownership. Sustainability 13 (24), 13983. doi:10.3390/su132413983

Li, T., Liang, L., and Han, D. (2018). Research on the efficiency of green technology innovation in China’s provincial high-end manufacturing industry based on the Raga-PP-SFA model. Math. Problems Eng. 2018, 1–13. doi:10.1155/2018/9463707

Lin, B., and Zhou, Y. (2022). Measuring the green economic growth in China: Influencing factors and policy perspectives. Energy 241, 122518. doi:10.1016/J.ENERGY.2021.122518

Liu, J., Jiang, Y., Gan, S., He, L., and Zhang, Q. (2022). Can digital finance promote corporate green innovation? Environ. Sci. Pollut. Res. 29 (24), 35828–35840. doi:10.1007/s11356-022-18667-4

Mubarak, M. F., Tiwari, S., Petraite, M., Mubarik, M., and Rasi, R. Z. R. M. (2021). How Industry 4.0 technologies and open innovation can improve green innovation performance? Manag. Environ. Qual. Int. J. 32 (5), 1007–1022. doi:10.1108/meq-11-2020-0266

Nunn, N., and Qian, N. (2014). US food aid and civil conflict. Am. Econ. Rev. 104 (6), 1630–1666. doi:10.1257/aer.104.6.1630

Ogbeibu, S., Emelifeonwu, J., Senadjki, A., Gaskin, J., and Kaivo-oja, J. (2020). Technological turbulence and greening of team creativity, product innovation, and human resource management: Implications for sustainability. J. Clean. Prod. 244, 118703. doi:10.1016/j.jclepro.2019.118703

Peng, H. X., and Mao, X. S. (2017). Government subsidies for innovation, company executives background and R&D investment: Evidence from the high-tech industry. Finance Trade Econ. 3, 147–161. doi:10.3969/j.issn.1002-8102.2017.03.010

Sama, L. M., Stefanidis, A., and Casselman, R. M. (2022). Rethinking corporate governance in the digital economy: The role of stewardship. Bus. Horizons 65 (5), 535–546. doi:10.1016/j.bushor.2021.08.001

Schoenecker, T., and Swanson, L. (2002). Indicators of firm technological capability: Validity and performance implications. IEEE Trans. Eng. Manag. 49 (1), 36–44. doi:10.1109/17.985746

Strambach, S. (2017). Combining knowledge bases in transnational sustainability innovation: Microdynamics and institutional change. Econ. Geogr. 93 (5), 500–526. doi:10.1080/00130095.2017.1366268

Subramaniam, M., and Youndt, M. A. (2005). The influence of intellectual capital on the types of innovative capabilities. Acad. Manag. J. 48 (3), 450–463. doi:10.5465/amj.2005.17407911

Tan, Y., Tian, X., Zhang, X., and Zhao, H. (2020). The real effect of partial privatization on corporate innovation: Evidence from China's split share structure reform. J. Corp. finance 64, 101661. doi:10.1016/j.jcorpfin.2020.101661

Thompson, P., Williams, R., and Thomas, B. (2013). Are UK SMEs with active web sites more likely to achieve both innovation and growth? J. Small Bus. Enterp. Dev. 20, 934–965. doi:10.1108/jsbed-05-2012-0067

Wang, F., Li, Y., and Sun, J. (2019). The transformation effect of R&D subsidies on firm performance: An empirical study based on signal financing and innovation incentives. Chin. Manag. Stud. 14, 373–390. doi:10.1108/cms-02-2019-0045

Wang, H., Zhang, G., Hu, W., Cao, D., Li, J., Xu, S., et al. (2020a). Artificial intelligence based approach to improve the frequency control in hybrid power system. Energy Rep. 6, 174–181. doi:10.1016/J.EGYR.2020.11.097

Wang, Y., Sun, X., Wang, B., and Liu, X. (2020b). Energy saving, ghg abatement and industrial growth in oecd countries: A green productivity approach. Energy 194, 116833. doi:10.1016/J.ENERGY.2019.116833

Yuan, J., Hou, Q., and Cheng, C. (2015). The curse effect of enterprise political resources: An investigation based on political connections and corporate technological innovations. Manag. World 1, 139–155.

Keywords: corporate digitalization, digital technology application, intelligent manufacturing application, modern information system, internet business model application, corporate green innovation

Citation: Jiang S, Li Y and You N (2023) Corporate digitalization, application modes, and green growth: Evidence from the innovation of Chinese listed companies. Front. Environ. Sci. 10:1103540. doi: 10.3389/fenvs.2022.1103540

Received: 20 November 2022; Accepted: 19 December 2022;

Published: 09 January 2023.

Edited by:

Muhammad Zahid Rafique, Shandong University, ChinaCopyright © 2023 Jiang, Li and You. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Yafei Li, bHlmOTRAcGt1LmVkdS5jbg==

†These authors have contributed equally to this work and share first authorship

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.