Cong Wang1

Cong Wang1 Pengyu Chen

Pengyu Chen Yuanyuan Hao

Yuanyuan Hao Abd Alwahed Dagestani

Abd Alwahed Dagestani

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 10 November 2022

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.1067534

Government intervention is increasingly vital due to the dual externalities of green innovation. We explored the relationship between tax incentives, subsidies, and green innovation. Based on data from Chinese listed companies from 2010 to 2019, we developed an evaluation system for corporate green innovation. First, we find that tax incentives promote corporate green innovation, while subsidies have little effect on green innovation. Second, we find that financing constraints are the main path of influence of tax incentives. Also, subsidies reverse the positive impact of tax incentives. Third, we further explore the heterogeneity of firms. We find that tax incentives and subsidies only impact green innovation by state-owned enterprises, monopolies, and small and medium-sized enterprises. We hope to provide new theoretical insights into intervention policy improvements and corporate green innovation in developing countries such as China.

The industrialization has produced massive pollution emissions while driving economic development. Despite China’s rapid economic development and the improvement in the quality of life of its people, environmental pollution is an increasingly serious problem (Hao et al., 2022a). According to Yale University’s 2022 Global Environmental Performance Report, China ranks only 160th out of 180 countries in terms of environmental performance1. As a major emitter of pollutants, the environmental management of enterprises has received attention (Utomo et al., 2020; Hao et al., 2022c). Green innovation is an essential technological tool to achieve corporate transformation and upgrading, clean production, and sustainable development. In order to promote the development of green innovation in enterprises (Cao et al., 2022). As of 2019, China’s Ministry of Science and Technology noted that China invested around 2.2 trillion yuan in R&D, an increase of 12.5% over the previous year, accounting for 2.23% of GDP, of which enterprises invested 1.69 trillion yuan in R&D, an increase of 11.1% over 2018. In order to reduce the R&D burden on enterprises and encourage them to conduct their own R&D, the government intervenes in their operations through various industrial policies, of which tax incentives and subsidies are used as the main regulatory instruments. However, these two intervention instruments are controversial (Liu et al., 2022), and scholars have explored whether they affect firms’ R&D performance and how strongly they do so.

With the establishment of Keynes’ neoclassical school and government failure theory, scholars began to study the impact of policies on green innovation (Cao et al., 2021; Hao et al., 2022b; Wang J et al., 2021; Zheng et al., 2022). First, Hu et al. (2021) and others explored the impact of subsidies on firms’ green innovation and found that the relationship was positive. Some scholars point out that excessive subsidies may crowd out firms’ original R&D investment (Xu et al., 2021), which inhibits green innovation (Yi et al., 2020). With the controversy over direct cash subsidy instruments (Ren et al., 2021), tax incentives, an indirect fiscal instrument, entered the perspective (Marjanović, 2018). The impact of tax incentives on green innovation is equally varied, either positively (Cao and Chen, 2018) or negatively (Song et al., 2020). While there is a rich literature exploring the impact of a single policy on innovation and based on a single variable measuring green innovation, the impact of both subsidies and tax incentives is rarely considered. Furthermore, external financing forces are an important and integral part of a firm’s R&D investment (Adegboye and Iweriebor, 2018; Feng, 2021). We also consider the role of corporate financing constraints as a mediating variable. Therefore, this paper considers the impact of tax incentives on green innovation under different levels of subsidies and the mechanism of action of tax incentives.

This paper uses data on listed manufacturing companies from 2010 to 2019, measures the intensity of tax incentives policy using the B-index, and establishes an evaluation system for corporate green innovation using the entropy weighting method (EWM). The impact of tax incentives on green innovation of different types of firms is explored, as well as the mediating effect of financing constraints and the moderating effect of subsidies. This paper is innovative in the following ways: 1) Unlike studies that use the DID approach to assess policy effects, this paper uses the B-index (Warda, 1996) to quantify policy effects. The impact between tax incentives and green innovation is explored, broadening the knowledge base of corporate green innovation under the endogenous growth theory. 2) Unlike the existing literature, which mainly uses single variables such as R&D investment and patents to measure corporate innovation (Ren et al., 2021; Zheng et al., 2022), this paper introduces a corporate green innovation evaluation system. It measures the green innovation performance of firms from multiple perspectives. 3) Few articles have considered the role of subsidies as another major instrument of government access. We consider the relationship between subsidies, tax incentives, and green innovation. We attempt to verify the validity of Keynesian theory through empirical analysis, which states that government intervention is needed to balance market supply and demand when firms innovate below the optimal level of the market. We hope to provide new insights for developing countries such as China to improve intervention policies and promote green innovation.

Through this study, we sought to answer the following research questions: RQ1: Do tax incentives promote corporate green innovation? RQ2: Which types of firms are more affected by tax incentives in terms of green innovation? RQ4: Do tax incentives alleviate corporate financing constraints? RQ4: As another direct cash instrument. What is the role of subsidies between tax incentives and green innovation?

The remainder of the paper consists of four sections: theoretical analysis and hypotheses; variables description and methodology; empirical analysis conclusions and discussion; and finally, conclusions, insights, and limitations are presented (see Figure 1).

FIGURE 1. Logic diagram.

Solow (1956) and Solow (1957) clarified the role of physical capital accumulation and suggested the importance of technological innovation as a determinant of sustained economic growth. In other words, most of the economic growth is not directly determined by the increase in the amount of input capital or labor, but with the increase in the amount of capital per unit of labor (Zhu et al., 2022), which is caused by the external factor of technological change (Liu et al., 2021; Wu et al., 2021). And this explains the dramatic growth of the US economy since the Second World War, which is mainly caused by technological change.

However, Solow’s theory (external growth theory) ignores the relationship between technological change and economic growth models, and Romer (1986) proposes a new growth theory (endogenous growth theory) that incorporates technological change such as human capital, R&D investment, and R&D-related equipment into economic growth models (Romer, 1990). However, due to factors such as large R&D investment, long lead time and uncertain output, the level of corporate R&D is often lower than the optimal social R&D investment (Block, 2012). Therefore, according to Keynesian theory, the government actively intervenes in corporate R&D activities to promote the rational allocation and effective use of resources and to ensure efficient output of enterprises. This imbalance can lead to market failure. Based on Keynesian theory, government intervention is necessary when the market failure occurs. It is believed that means can be achieved to promote the rational allocation of resources and improve the efficiency of resource use to ensure the effective output of enterprises.

Existing research on tax incentives and green innovation is still not abundant, with most scholars exploring the relationship between the two separately (Song et al., 2020). Stucki et al. (2018) and Dangelico (2016) point out that tax incentives can drive green product innovation. Tax incentives are more effective and comprehensive than direct R&D subsidies (Carboni, 2011). Firstly, tax incentives increase the net cash flow of enterprises, so that enterprises have enough funds to invest in R&D and improve the efficiency of their innovation output (Pan et al., 2021). Secondly, tax incentives have a good messaging effect. Because it sends a positive signal to financial institutions and private investors, companies can attract more social capital investment (Pénard and Poussing, 2010). Busom et al. (2014) found that neither subsidies nor tax incentives are equivalent instruments for firms, and that tax incentives help solve the problem of allocation difficulties for firms without fiscal constraints, while government subsidies may be a better incentive for firms than tax credits. Griffith et al. (1995) used Canadian innovation incentives as a natural experimental group and find that tax policy has considerable advantages for research and development. Ma et al. (2019) points out that government subsidies are conducive to promoting green innovation in firms due to the “double externality” of green innovation (Yuan et al., 2014). Most scholars have questioned subsidies as a direct cash subsidy instrument. The main reason is that the use of subsidies is unclear, and it is more common for firms to use the subsidies they receive for non-R&D purposes due to low oversight of their use by regulatory bodies (Boeing, 2016). Therefore, based on the above analysis, we propose the following hypothesis.

H1: Tax incentives have a greater impact on green innovation than subsidies.

Signalling theory suggests that under conditions of information asymmetry, the party with the information will selectively disclose favorable information information, and firms that engage in innovation tend to be advantaged in information (Soskice, 1997). Wang M et al. (2021) used industrial firms from 2000 to 2009 as the study population, with value-added tax (VAT) reform as the natural experimental group. The cited authors found that VAT alleviated corporate financing constraints. Firms can not only disclose their financial and R&D status directly to society, but can also indirectly send positive signals to the outside world through information such as government subsidies and tax incentives (Czarnitzki et al., 2011). Fang et al. (2022) explored the impact of the 2002 income tax revenue-sharing reform in China on the financial performance of firms. The cited authors find that the reform policy promotes firm performance through alleviating financing difficulties. Yu et al. (2021) investigated the impact of financing constraints on green innovation using a sample of Chinese listed companies between 2001 and 2017. The cited authors find that firms’ ability to innovate green is impaired when they face higher financing constraints. Therefore, based on the above analysis, we propose the following hypothesis.

H2: Tax incentives can ease corporate financing constraints and thus enhance green innovation.

As direct government support instruments, Subsidies can assist tax incentives in helping to compensate for market failures in R&D activities. However, the subsidies enjoyed by different firms are uneven (González and Pazó, 2008). In order to investigate whether subsidies play a moderating role in the relationship between tax incentives and green innovation. This paper explores the impact of tax incentives on green innovation by using subsidies as a moderating variable.

Yang et al. (2019) show that tax incentives are sustainable and stable, whereas subsidies are only project-specific, which can undermine the green innovation projects that firms are expected to undertake. In addition, subsidized firms are subject to numerous constraints in terms of resource allocation, targeting of innovation activities, and innovation lags. On the other hand, tax incentives have a broader scope and allow firms to undertake green innovation activities that they wish to or are in line with external stakeholders (Zhang et al., 2020). In addition, we consider government failure theory and Keynesian theory. When a firm receives external intervention beyond a certain boundary, this intervention can break the normal operation of the firm. Namely, high-subsidy firms receive large government subsidies and thus exhibit high-output green innovation. The tax incentives are just “icing on the cake”, resulting in a modest contribution to green innovation. Conversely, it is difficult for low-subsidy firms to rely on subsidies to drive autonomous innovation, and tax incentives can more fully compensate for the lack of R&D investment. This is where subsidies become the “unfortunate of all misfortunes”. This statement is supported by numerous scholars’ criticisms of cash subsidies; based on the above analysis, we propose the following hypothesis.

H3: Tax incentives have a greater impact on green innovation in low-subsidy firms than in high-subsidy firms.

In this paper, China A-share listed manufacturing companies from 2010–2019 were used as the research sample, and the following treatments were made to the initial sample: 1) companies with more than 3 years of serious R&D investment data were excluded, 2) companies with continuous losses (ST and *ST companies), and 3) to avoid the effect of data outliers, the sample data were subjected to tail-shrinking (winsorize) at the 1% level. The final screening yielded 517 manufacturing enterprises. The financial data and the number of patents granted were obtained from the China Stock Market & Accounting Research Database.

The dependent variable is green innovation measured through multiple dimensions. Compared to most studies that use R&D input intensity and number of patents as R&D performance, given that individual variables cannot directly measure the actual green innovation (GI), this paper adopts Chen (2022) and Sun et al. (2017) method to measure the green innovation in five dimensions, including green innovation input, technology level, innovation environment, green innovation output and financial environment. The entropy weighting method (EWM) was used to construct a comprehensive evaluation system for R&D and under. In the innovation input dimension, R&D investment is selected; in the technology level dimension, technicians are selected; in the enterprise innovation environment dimension, the weight of the top 10 shareholders, the debt ratio and the average R&D gap between the enterprise and the industry are selected. Shareholder weighting implies that external stakeholders are concerned about corporate sustainability (Sakaki and Jory, 2019). The higher the weight of shareholders, the more stable the corporate board is and the easier it is to implement sustainable development decisions, e.g., green innovation. In the innovation output dimension, the number of green patents granted per capita and the R&D cost investment per unit of green patents are selected. The independent variable is tax incentives, quantified by the B index (1996), which has some assumptions: 1) a company’s R&D expenditure can be divided into recurrent and capital expenditure, accounting for 90% and 10% respectively. 2) the calculation is based on corporate income tax only and does not include other tax rates, and 3) the firm has sufficient revenue to invest in R&D, of which all tax credits, apportioned over the year, can be completed without regard to carryover.

The formula for the B index is as follows (Elschner et al., 2011):

Where ATC is the after-tax cost, namely, the cost of R&D after the enterprise enjoys the tax incentives. t is the corporate income tax rate. B is the actual after-tax cost. When an enterprise enjoys tax incentives, assuming V is the pre-tax deduction rate, ATC = 1 - vt.

The B index implies the change in a firm’s after-tax R&D costs as a result of the tax incentives. 1-B is often used to measure the intensity of the tax incentives, denoted as Tax. If 1-B is higher, the stronger the tax incentive intensity is, the more R&D costs an enterprise can save. High-tech enterprises enjoy an enterprise income tax rate of 15%, while ordinary enterprises enjoy an income tax rate of 25% only. Because the pre-tax deduction ratio was raised from 50% to 75% from 2017, the calculation according to Jun. (2011) method can obtain the intensity of the tax incentives for high-tech enterprises from 2010–2016 as 0.071, for high-tech enterprises from 2017–2019 as 0.115, and for ordinary enterprises from 2010 to 2019 The intensity of the tax incentives for ordinary enterprises from 2010–2019 is 0.133. The mediating variable is the KZ index chosen to measure the firm’s financing constraints (Hadlock and Pierce, 2010). The higher the KZ index, the less access the firm has to external financing. In this paper, the logarithm of the green innovation-related subsidy is used as the moderating variable and denoted as Sub.

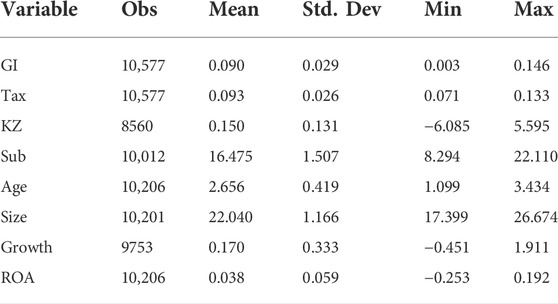

We selected the following control variables based on the literature (Ren et al., 2022; Yu et al., 2021). Operating income growth rate, firm size (logarithm of total assets), firm age and ROA. Table 1 shows the descriptive statistics for all variables, green innovation and tax incentives are significant differences between firms.

TABLE 1. The descriptive statistics.

To explore the impact of tax incentives on corporate green innovation, we developed the following model (Zhai et al., 2022).

We use financing constraints as a mediating variable to explore the relationship between tax incentives and green innovation. The model is as follows:

Considering the moderating effect of subsidies, we introduce a moderating model to test the relationship between tax incentives and innovation under different subsidies

Where Gi is green innovation of firm i in year t. Tax is B index and Sub is the subsidy. We fixed firm-time effects to eliminate the impact of unobserved factors on the regression results.

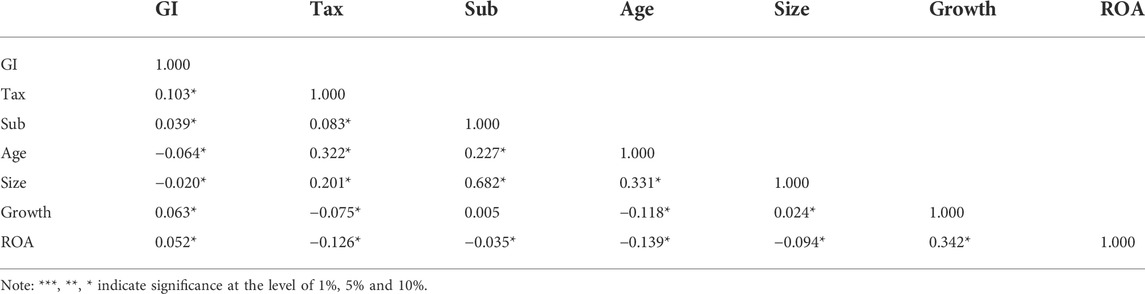

Table 2 shows the results of the correlation tests. We find that tax incentives have a greater impact on green innovation compared to subsidies, tentatively testing hypothesis H1. In addition, the VIF values for our tests of multicollinearity are all 1.23 (1.23 < 10). This indicates that there is no multicollinearity in our model.

TABLE 2. Correlation test.

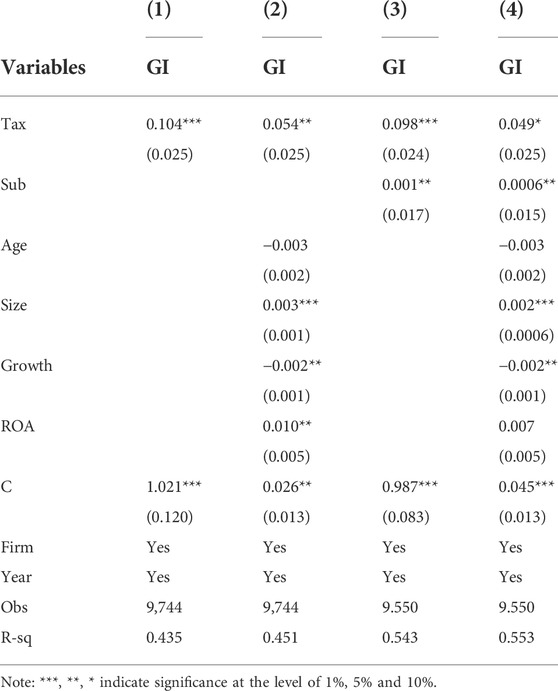

Table 3 shows the regression results before and after adding the subsidy. Take column 4) as an example; the coefficient of tax incentives (Tax) is 0.049 at the 10% significant level; the coefficient of subsidies (Sub) is 0.0006 at the 5% significant level, with the coefficient of tax incentives being much larger than that of subsidies. This suggests that tax incentives promote green innovation compared to subsidies, validating hypothesis H1. This is also supported by Basit et al. (2018), who find that tax incentives have a greater impact on innovation performance. One possible explanation is that although both tax incentives and subsidies stimulate green innovation in firms, the marginal benefits of tax incentives are greater than government subsidies, leading to a preference for tax incentives in firms’ green innovation activities.

TABLE 3. Baseline regression result.

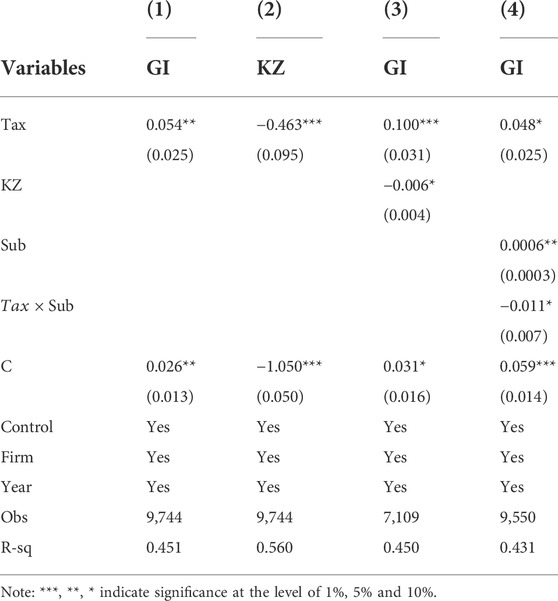

Table 4 tests the mediating effect of financing constraints and the moderating effect of subsidies. In column (1), the coefficient of GI on green innovation is 0.054 at 5% significant level. In column (2), the coefficient of DT on KZ is 0.-0.463 at 1% significant level. In column (3), the coefficient of KZ on GI is -0.006 at 10% significant level, verifying hypothesis H2. This suggests that financing constraints are an important mechanism by which tax incentives affect firms’ green innovation, which is consistent with the findings of Yu et al. (2021). One possible explanation is based on signalling theory, where tax incentives may send positive signals to outsiders, alleviating information asymmetry between firms and external stakeholders and increasing investment confidence. This can also be used to explain in terms of external stakeholder theory (Mainardes et al., 2011). Tax incentives act as a positive signal that will reduce the concerns of external stakeholders of the firm about the firm’s green innovation activities (Acebo et al., 2021), and external stakeholders participate in the firm’s green activities, increasing investors’ confidence. In column (4), the coefficient of the cross term (

TABLE 4. Mediating and moderating effects tests.

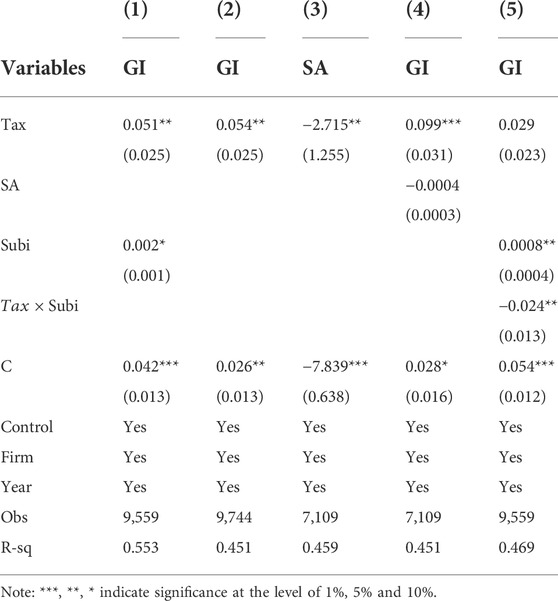

To increase the credibility of the regression results. We replace government subsidies (Sub) with Subi (subsidy/operating income). Moreover, use the SA index to measure financing constraints in Table 5(Huang et al., 2021). The regression results are consistent with Tables 3, 4. This means that our regression results are plausible.

TABLE 5. Robustness tests.

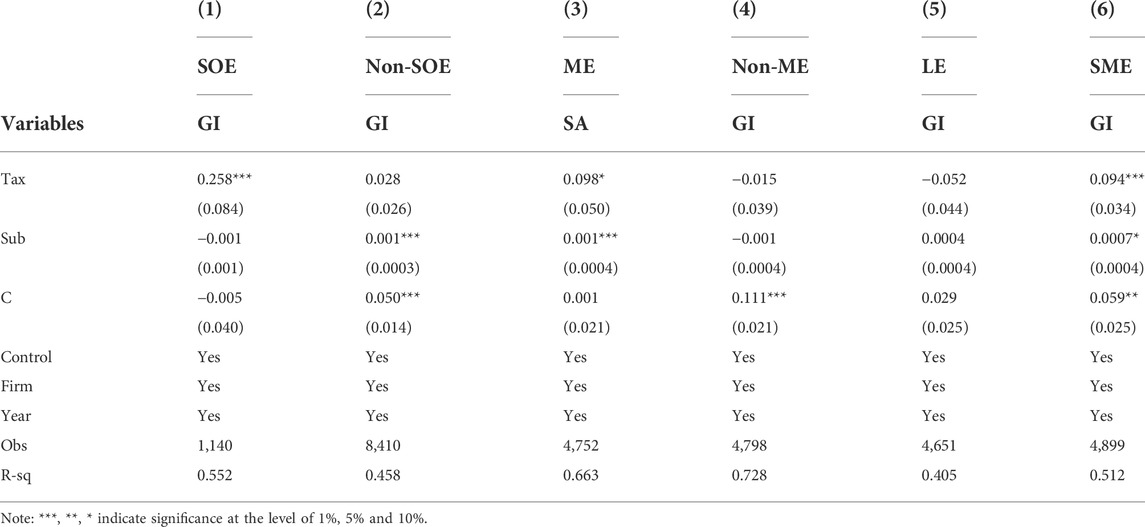

Considering that firm heterogeneity affects the regression results in Table 6, this paper divides the full sample into three subsamples: state-owned enterprises (SOE) and non-state-owned enterprises (Non-SOE), monopolistic enterprises (ME) and non-monopolistic enterprises (Non-ME), and small and medium-sized enterprises (SME) and large enterprises (LE). Specifically, enterprises are classified into SOEs and non-SOEs according to their ownership; enterprises with industry concentration (HHI) less than the median (0.078) are non-monopolistic enterprises, while others are monopolistic enterprises; as it is difficult to identify small, medium and large enterprises, this paper simply uses the total assets of enterprises to define the type of enterprises, and enterprises with total assets less than the median (21.886) are small and medium enterprises, while others are large enterprises.

TABLE 6. Heterogeneity analysis.

The results of the ownership analysis tell us that the coefficient of Tax for SOEs is 0.258 at the 1% significant level, while the impact of Tax for non-SOEs is not significant. In terms of subsidies, subsidies only have an effect on green innovation for non-SOEs. One possible explanation is that SOEs are more likely to receive policy support (Wen and Zhao, 2020), either in the form of tax incentives or subsidies, which is determined by the social role and corporate characteristics of SOEs (Jin et al., 2005). Alternatively, SOEs have a high technological reserve,a long history and a large R&D talent pool, which is conducive to green innovation output (Simon and Cao, 2009). Columns 3) and 4) tell us that tax incentives and subsidies into the team monopolies have an impact on green innovation. This is in line with the findings of Crowley and Jordan (2017). The possible reason is that monopolies monopolise markets for a long time due to their unique products and technologies (Waldman, 2003). The results of the firm size analysis tell us that tax incentives and subsidies have an impact on green innovation in SMEs. One possible explanation is that green innovation is characterized by long lead times, large inputs and uncertain outputs (Zhou et al., 2022). Compared to SMEs, larger enterprises have greater risk resistance and access to more government support (Trianni et al., 2016).

Considering existing research on the incomplete relationship between government intervention instruments and green innovation, we further explored the relationship between tax incentives, subsidies, and green innovation. Based on data from Chinese listed companies from 2010 to 2019, we developed an evaluation system for corporate green innovation. Firstly, based on in-growth and Keynesian theories, tax incentives promote corporate green innovation, while subsidies have little effect on green innovation. Secondly, we find that financing constraints are the main path of influence of tax incentives. As signaling theory explains, tax incentives send positive signals to market investors and mitigate the information dichotomy between firms and market investors. Secondly, subsidies reverse the positive impact of tax incentives. Specifically, when firms that benefit from tax incentives receive large cash subsidies, these subsidies interfere with the expected green innovation activities, thereby creating a ‘crowding out’ effect on the tax incentives. Third, we further explore the heterogeneity of firms. We find that tax incentives and subsidies only have an impact on green innovation of state-owned enterprises, monopolies, small and medium-sized enterprises. We hope to provide new theoretical insights into the improvement of intervention policies and green innovation by firms in developing countries such as China.

We make the following recommendations from the perspective of optimizing intervention policies and promoting green innovation to achieve sustainable development: 1) Appropriately strengthen tax incentives, expand the scope of incentives and increase the pre-tax deduction discount rate to promote green innovation and sustainable development of enterprises. Regarding enterprise heterogeneity, preferential tax policies have a prominent role in promoting green innovation in state-owned, competitive, and large enterprises. The government should formulate targeted policies to promote the green innovation activities of non-state-owned enterprises, monopolistic enterprises, and SMEs. 2) Timely disclosure of policy information and improvement of the disclosure system. Under the strategic transformation of economic globalization, domestic enterprises are all facing greater pressure to invest in R&D. R&D has strong externalities and information asymmetry. Timely disclosure of policy information can not only send timely signals to the outside world, attract social capital and reduce the R&D burden of enterprises but also enable enterprises to carry out R&D tasks in a timely manner and reduce R&D preparation time. Green innovation has the dual externalities of knowledge spillover and environmental governance.3) Modestly reduce direct government cash support to realize the complementary effect of tax incentives. Although subsidies weaken the positive impact of tax incentives on firms’ green innovation enhancement. However, combined with the results of the analysis of enterprise heterogeneity, the government can strengthen tax incentives while targeting increased government subsidies to further realise the complementary effects of tax incentives and government subsidies.

This paper explores the relationship between tax incentives and green innovation from an innovation perspective, but there are some limitations. Firstly, our study years are 2010–2019, making it difficult to explore the long-term effects of tax incentives. Secondly, this paper analyzes firms, nursing geographical, and urban heterogeneity. In addition, both board characteristics and corporate strategies affect the regression results. Therefore, we will take these limitations fully into account in future research.

The original contributions presented in the study are included in the article/Supplementary Materials, further inquiries can be directed to the corresponding author.

PC, AD, YH and CW wrote, edited and revised the text, created and edited figures and tables. PC and AD contributed analysis and figures and edited and revised the manuscript. All authors contributed to the tables, wrote portions of the text, and edited the manuscript.

This work was supported by Research on Optimizing Chinese currency Payment System by Digital RMB [KYH22527] and the 16th social science Research project of Changzhou [CZSKL-2020B038].

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Acebo, E., Miguel‐Dávila, J. Á., and Nieto, M. (2021). External stakeholder engagement: Complementary and substitutive effects on firms' eco‐innovation. Bus. Strategy Environ. 30 (5), 2671–2687. doi:10.1002/bse.2770

Adegboye, A. C., and Iweriebor, S. (2018). Does access to finance enhance SME innovation and productivity in Nigeria? Evidence from the world bank enterprise survey. Afr. Dev. Rev. 30 (4), 449–461. doi:10.1111/1467-8268.12351

Basit, S. A., Kuhn, T., and Ahmed, M. (2018). The effect of government subsidy on non-technological innovation and firm performance in the service sector: Evidence from Germany. Bus. Syst. Res. J. 9 (1), 118–137. doi:10.2478/bsrj-2018-0010

Block, J. H. (2012). R&D investments in family and founder firms: An agency perspective. J. Bus. Ventur. 27 (2), 248–265. doi:10.1016/j.jbusvent.2010.09.003

Boeing, P. (2016). The allocation and effectiveness of China’s R&D subsidies-Evidence from listed firms. Res. policy 45 (9), 1774–1789. doi:10.1016/j.respol.2016.05.007

Busom, I., Corchuelo, B., and Martínez-Ros, E. (2014). Tax incentives or subsidies for business R&D? Small Bus. Econ. 43 (3), 571–596. doi:10.1007/s11187-014-9569-1

Cao, H., and Chen, Z. (2018). The driving effect of internal and external environment on green innovation strategy-The moderating role of top management’s environmental awareness. Nankai Bus. Rev. Int. 10 (3), 342–361. doi:10.1108/nbri-05-2018-0028

Cao, J., Law, S. H., Samad, A. R. B. A., Mohamad, W. N. B. W., Wang, J., and Yang, X. (2022). Effect of financial development and technological innovation on green growth—analysis based on spatial durbin model. J. Clean. Prod. 365, 132865. doi:10.1016/j.jclepro.2022.132865

Cao, J., Law, S. H., Samad, A. R. B. A., Mohamad, W. N. B. W., Wang, J., and Yang, X. (2021). Impact of financial development and technological innovation on the volatility of green growth—Evidence from China. Environ. Sci. Pollut. Res. 28 (35), 48053–48069. doi:10.1007/s11356-021-13828-3

Carboni, O. A. (2011). R&D subsidies and private R&D expenditures: Evidence from Italian manufacturing data. Int. Rev. Appl. Econ. 25 (4), 419–439. doi:10.1080/02692171.2010.529427

Chen, P. (2022). Subsidized or not, the impact of firm internationalization on green innovation—based on a dynamic panel threshold model. Front. Environ. Sci. 303. doi:10.3389/fenvs.2022.806999

Crowley, F., and Jordan, D. (2017). Does more competition increase business-level innovation? Evidence from domestically focused firms in emerging economies. Econ. Innovation New Technol. 26 (5), 477–488. doi:10.1080/10438599.2016.1233627

Czarnitzki, D., Hanel, P., and Rosa, J. M. (2011). Evaluating the impact of R&D tax credits on innovation: A microeconometric study on Canadian firms. Res. policy 40 (2), 217–229. doi:10.1016/j.respol.2010.09.017

Dangelico, R. M. (2016). Green product innovation: Where we are and where we are going. Bus. Strategy Environ. 25 (8), 560–576. doi:10.1002/bse.1886

Elschner, C., Ernst, C., Licht, G., and Spengel, C. (2011). What the design of an R&D tax incentive tells about its effectiveness: A simulation of R&D tax incentives in the European union. J. Technol. Transf. 36 (3), 233–256. doi:10.1007/s10961-009-9146-y

Fang, H., Su, Y., and Lu, W. (2022). Tax incentive and corporate financial performance: Evidence from income tax revenue sharing reform in China. J. Asian Econ. 81, 101505. doi:10.1016/j.asieco.2022.101505

Feng, X. (2021). The role of ESG in acquirers' performance change after M&amp;A deals. Green Finance 3 (3), 287–318. doi:10.3934/gf.2021015

González, X., and Pazó, C. (2008). Do public subsidies stimulate private R&D spending? Res. Policy 37 (3), 371–389. doi:10.1016/j.respol.2007.10.009

Griffith, R., Sandler, D., and Van Reenen, J. (1995). Tax incentives for R&D. Fisc. Stud. 16 (2), 21–44. doi:10.1111/j.1475-5890.1995.tb00220.x

Hadlock, C. J., and Pierce, J. R. (2010). New evidence on measuring financial constraints: Moving beyond the KZ index. Rev. Financ. Stud. 23 (5), 1909–1940. doi:10.1093/rfs/hhq009

Hao, Y., Guo, Y., and Wu, H. (2022b). The role of information and communication technology on green total factor energy efficiency: Does environmental regulation work? Bus. Strategy Environ. 31 (1), 403–424. doi:10.1002/bse.2901

Hao, Y., Huang, J., Guo, Y., Wu, H., and Ren, S. (2022c). “Does the legacy of state planning put pressure on ecological efficiency? Evidence from China,” in Business strategy and the environment (New Jersey, United States: wiley online library).

Hao, Y., Xu, L., Guo, Y., and Wu, H. (2022a). The inducing factors of environmental emergencies: Do environmental decentralization and regional corruption matter? J. Environ. Manag. 302, 114098. doi:10.1016/j.jenvman.2021.114098

Hu, D., Qiu, L., She, M., and Wang, Y. (2021). Sustaining the sustainable development: How do firms turn government green subsidies into financial performance through green innovation? Bus. Strategy Environ. 30 (5), 2271–2292. doi:10.1002/bse.2746

Huang, H., Sun, Y., and Chu, Q. (2021). Can we-media information disclosure drive listed companies' innovation?—from the perspective of financing constraints. China Finance Rev. Int. 12, 477–495. (ahead-of-print). doi:10.1108/CFRI-09-2020-0127

Jin, H., Qian, Y., and Weingast, B. R. (2005). Regional decentralization and fiscal incentives: Federalism, Chinese style. J. public Econ. 89 (9-10), 1719–1742. doi:10.1016/j.jpubeco.2004.11.008

Jun, W. (2011). The measure of government R&D tax incentive intensity and its effect verification in China. Sci. Res. Manag. 32 (9), 157.

Liu, S., Shen, X., Jiang, T., and Failler, P. (2021). Impacts of the financialization of manufacturing enterprises on total factor productivity: Empirical examination from China's listed companies. Green Finance 3 (1), 59–89. doi:10.3934/gf.2021005

Liu, X., Liu, J., Wu, H., and Hao, Y. (2022). Do tax reductions stimulate firm productivity? A quasi-natural experiment from China. Econ. Syst. 2022, 101024. doi:10.1016/j.ecosys.2022.101024

Ma, W., Zhang, R., and Chai, S. (2019). What drives green innovation? A game theoretic analysis of government subsidy and cooperation contract. Sustainability 11 (20), 5584. doi:10.3390/su11205584

Mainardes, E. W., Alves, H., and Raposo, M. (2011). Stakeholder theory: Issues to resolve. Manag. Decis. 49, 226–252. doi:10.1108/00251741111109133

Marjanović, D. (2018). Competitiveness of the Serbian economy through the prism of tax incentives for foreign investors. ea. 51 (3/4), 95–104. doi:10.28934/ea.18.51.34.pp95-104

Pan, X., Guo, S., and Chu, J. (2021). P2P supply chain financing, R&D investment and companies' innovation efficiency. J. Enterp. Inf. Manag. 34, 578–597. doi:10.1108/jeim-07-2020-0258

Pénard, T., and Poussing, N. (2010). Internet use and social capital: The strength of virtual ties. J. Econ. Issues 44 (3), 569–595. doi:10.2753/jei0021-3624440301

Ren, S., Hao, Y., and Wu, H. (2021). Government corruption, market segmentation and renewable energy technology innovation: Evidence from China. J. Environ. Manag. 300, 113686. doi:10.1016/j.jenvman.2021.113686

Ren, S., Yang, X., Hu, Y., and Chevallier, J. (2022). Emission trading, induced innovation and firm performance. Energy Econ. 112, 106157. doi:10.1016/j.eneco.2022.106157

Romer, P. M. (1990). Endogenous technological change. J. political Econ. 98, S71–S102. doi:10.1086/261725

Romer, P. M. (1986). Increasing returns and long-run growth. J. political Econ. 94 (5), 1002–1037. doi:10.1086/261420

Sakaki, H., and Jory, S. R. (2019). Institutional investors' ownership stability and firms' innovation. J. Bus. Res. 103, 10–22. doi:10.1016/j.jbusres.2019.05.032

Simon, D. F., and Cao, C. (2009). China's emerging technological edge: Assessing the role of high-end talent. Cambridge, United Kingdom: Cambridge University Press.

Solow, R. M. (1956). A contribution to the theory of economic growth. Q. J. Econ. 70 (1), 65–94. doi:10.2307/1884513

Solow, R. M. (1957). Technical change and the aggregate production function. Rev. Econ. Statistics 39, 312–320. doi:10.2307/1926047

Song, M., Wang, S., and Zhang, H. (2020). Could environmental regulation and R&D tax incentives affect green product innovation? J. Clean. Prod. 258, 120849. doi:10.1016/j.jclepro.2020.120849

Soskice, D. (1997). German technology policy, innovation, and national institutional frameworks. Industry Innovation 4 (1), 75–96. doi:10.1080/13662719700000005

Stucki, T., Woerter, M., Arvanitis, S., Peneder, M., and Rammer, C. (2018). How different policy instruments affect green product innovation: A differentiated perspective. Energy Policy 114, 245–261. doi:10.1016/j.enpol.2017.11.049

Sun, L. Y., Miao, C. L., and Yang, L. (2017). Ecological-economic efficiency evaluation of green technology innovation in strategic emerging industries based on entropy weighted TOPSIS method. Ecol. Indic. 73, 554–558. doi:10.1016/j.ecolind.2016.10.018

Trianni, A., Cagno, E., and Farné, S. (2016). Barriers, drivers and decision-making process for industrial energy efficiency: A broad study among manufacturing small and medium-sized enterprises. Appl. Energy 162, 1537–1551. doi:10.1016/j.apenergy.2015.02.078

Utomo, M. N., Rahayu, S., Kaujan, K., and Irwandi, S. A. (2020). Environmental performance, environmental disclosure, and firm value: Empirical study of non-financial companies at Indonesia Stock exchange. Green Finance 2 (1), 100–113. doi:10.3934/gf.2020006

Waldman, M. (2003). Durable goods theory for real world markets. J. Econ. Perspect. 17 (1), 131–154. doi:10.1257/089533003321164985

Wang, J., Shen, G., and Tang, D. (2021). Does tax deduction relax financing constraints? Evidence from China's value-added tax reform. China Econ. Rev. 67, 101619. doi:10.1016/j.chieco.2021.101619

Wang, M., Gu, R., Wang, M., Zhang, J., Press, B. C. S., and Branch, B. O. C. S. (2021). Research on the impact of finance on promoting technological innovation based on the state-space model. Green Finance 3 (2), 119–137. doi:10.3934/gf.2021007

Warda, J. (1996). “Measuring the value of R&D tax provisions,” in Fiscal measures to promote R&D and innovation (Paris, France: OECD), 9–22.

Wen, H., and Zhao, Z. (2020). How does China’s industrial policy affect firms’ R&D investment? Evidence from ‘China manufacturing 2025. Appl. Econ. 2020, 1–14.

Wu, H., Hao, Y., Ren, S., Yang, X., and Xie, G. (2021). Does internet development improve green total factor energy efficiency? Evidence from China. Energy Policy 153, 112247. doi:10.1016/j.enpol.2021.112247

Wu, Y. (2005). The effects of state R&D tax credits in stimulating private R&D expenditure: A cross‐state empirical analysis. J. Policy Anal. Manage. 24 (4), 785–802. doi:10.1002/pam.20138

Xu, J., Li, Y., Feng, D., Wu, Z., and He, Y. (2021). Crowding in or crowding out? How local government debt influences corporate innovation for China. PloS one 16 (11), e0259452. doi:10.1371/journal.pone.0259452

Yang, X., He, L., Xia, Y., and Chen, Y. (2019). Effect of government subsidies on renewable energy investments: The threshold effect. Energy Policy 132, 156–166. doi:10.1016/j.enpol.2019.05.039

Yi, M., Wang, Y., Yan, M., Fu, L., and Zhang, Y. (2020). Government R&D subsidies, environmental regulations, and their effect on green innovation efficiency of manufacturing industry: Evidence from the Yangtze River economic belt of China. Int. J. Environ. Res. Public Health 17 (4), 1330. doi:10.3390/ijerph17041330

Yu, C. H., Wu, X., Zhang, D., Chen, S., and Zhao, J. (2021). Demand for green finance: Resolving financing constraints on green innovation in China. Energy Policy 153, 112255. doi:10.1016/j.enpol.2021.112255

Yuan, C., Liu, S., Yang, Y., Chen, D., Fang, Z., and Shui, L. (2014). An analysis on investment policy effect of China’s photovoltaic industry based on feedback model. Appl. energy 135, 423–428. doi:10.1016/j.apenergy.2014.08.103

Zhai, H., Yang, M., and Chan, K. C. (2022). Does digital transformation enhance a firm's performance? Evidence from China. Technol. Soc. 68, 101841. doi:10.1016/j.techsoc.2021.101841

Zhang, Y., Hong, Z., Chen, Z., and Glock, C. H. (2020). Tax or subsidy? Design and selection of regulatory policies for remanufacturing. Eur. J. operational Res. 287 (3), 885–900. doi:10.1016/j.ejor.2020.05.023

Zheng, C., Deng, F., Zhuo, C., and Sun, W. (2022). Green credit policy, institution supply and enterprise green innovation. J. Econ. Analysis 1 (1), 28–51.

Zhou, W., Huang, X., Dai, H., Xi, Y., Wang, Z., and Chen, L. (2022). Research on the impact of economic policy uncertainty on enterprises’ green innovation—based on the perspective of corporate investment and financing decisions. Sustainability 14 (5), 2627. doi:10.3390/su14052627

Keywords: tax incentives, subsidies, green innovation, financing constraints, government intervention

Citation: Wang C, Chen P, Hao Y and Dagestani AA (2022) Tax incentives and green innovation—The mediating role of financing constraints and the moderating role of subsidies. Front. Environ. Sci. 10:1067534. doi: 10.3389/fenvs.2022.1067534

Received: 13 October 2022; Accepted: 28 October 2022;

Published: 10 November 2022.

Edited by:

Haitao Wu, Beijing Institute of Technology, ChinaReviewed by:

Zhongzhu Chu, Shanghai Jiao Tong University, ChinaCopyright © 2022 Wang, Chen, Hao and Dagestani. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Pengyu Chen, Y3B5NzAyMDE4QDE2My5jb20=; Yuanyuan Hao, NTI5NTEzNDA4QHFxLmNvbQ==; Abd Alwahed Dagestani, YS5hLmRhZ2VzdGFuaUBjc3UuZWR1LmNu

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.