Chunqiang Zhang

Chunqiang Zhang Lu Gao1

Lu Gao1 Wenbing Wang

Wenbing Wang Jiapeng An

Jiapeng An

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 04 January 2023

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.1051000

This article is part of the Research TopicSustainable Economic Growth, Green Deal and Macroeconomic Recovery – Most Suitable Pathways to Recovering From the Actual Evolutionary HiatusView all 14 articles

ESG scores are essential information tools in the capital market, but prior study has not fully discussed the effect and internal mechanism of ESG scores on bond investors’ risk pricing in the primary market. The purpose of this study is to investigate the relationship between the ESG scores and risk premium of bond issuance based on the sample of Chinese listed corporations. We find that when ESG scores of the bond issuer are higher, the investors will require a lower risk premium. The result indicates that ESG scores already have positive information effect in Chinese primary bond market. Furthermore, we make mechanism and heterogeneity tests to prove that ESG scores can provide investors with incremental information, which is helpful for bond investors to identify risks and price effectively. Our study in the context of the emerging economy of China examines the incremental information value of ESG scores for bond investors, and provides evidence for the application of sustainable development concepts in global capital markets.

ESG scores, as very important and increasingly concerned principles, have been integrated into all levels of the portfolio allocation process and regarded as a new dimension to redefine bond investment. Previous studies have paid attention to how ESG scores play an information decision-making effect in the secondary circulation market of bonds (Immel et al., 2021; Kanamura, 2021). Actually, for the primary bond issuance market, the basic information of the corporate quality will be more valued by investors, especially the ESG scores that reflects the long-term investment value of the corporation. It is an essential criterion for measuring whether a corporation has enough social responsibility (Hong, 2019) and sustainable business performance (Baker et al., 2021). Therefore, when the corporation has a higher ESG score, it will send a positive signal to investors in the primary bond market, which will alleviate the information asymmetry and reduce the risk premium demanded by investors.

But there has been little discussion about the influence of ESG scores on risk premium in the primary bond issuance market. Especially under the influence of current COVID-19, the concept of sustainable development related to ESG has further become the focus of attention; In addition, as an emerging economy, China already has the world’s second largest bond market. In this context, the purpose of this study is to explore the influence of ESG scores on the risk premium of bond issuance in Chinese market, which will help to understand the extent to which the concept of sustainable development is applied in the global capital market.

Based on information asymmetry theory, we used ESG scores, bond and financial data of corporations which listed on the Shanghai and Shenzhen Stock Exchanges over the period 2016 to 2020, and the pooled regression to study the relationship between the ESG scores and risk premium of bond issuance. Results indicate that ESG scores which are higher, will contribute to significantly lowering the risk premium of issuing bonds, which indicates that ESG scores exert a positive information effect in the Chinese primary bond market. Meanwhile, we used a two-stage least-squares methodology to alleviate the endogeneity problems. Additionally, through the mechanism test and further analysis, we proved that ESG scores can provide investors with incremental information value, which is helpful for bond investors to identify risks and price effectively.

Our study makes several important contributions to the literature and fills the research gap. First, it extends the research on the information effect of ESG scores in capital market. Previous studies tended to focus on the impact of ESG scores on portfolio returns in the stock market, but few studies investigated the information effect of ESG scores in the primary bond issuance market. Second, this paper enriches the researches on the influencing factors of bond issuance cost. There were many literatures that discussed the factors affecting the cost of corporate bond issuance, but few literatures focused on ESG scores issued by financial institutions. Third, this paper contributes to enriching the relevant literature on discussing the incremental information value of ESG scores. Previous literature mainly focused on the stock market, but the primary bond market as an investment and bond issuance market, the basic characteristics and behavior of the bond issuing corporations are crucial to investors, such as ESG scores. Therefore, exploring the impact of ESG scores on China’s primary bond market will help to expand the literature on discussing the incremental information value of ESG scores.

The main potential implication of this paper is to provide strong evidence for the application of the concept of green sustainable development in the global capital market. Unlike other economies, China is an emerging economy with the world’s second-largest bond market, but its capital market is less efficient. In such market, market information cannot be efficiently used as an investment tool, but we have obtained very significant results, indicating that ESG concept has been fully applied in the global capital market.

This paper proceeds as follows. We mainly review related literature on the effect of ESG scores in Section 2. We present the theoretical development and hypothesis in Section 3. And then, we provide the research design in Section 4. Further, we discuss the empirical results in Section 5. We thoroughly examine the incremental information effect of ESG scores from two directions in Section 6. We further explore the heterogeneity of the information effect of ESG scores in Section 7. In Section 8, we conclude.

ESG scores will not only have a significant influence on the corporate financial policy, governance and performance (Aboud and Diab, 2019; Hong, 2019) but also have a significant information effect on the capital market (Baker et al., 2021). First of all, an important component of the information effect study of ESG scores is the impact on investor decisions and earnings in the stock market. As an effective value decision-making tool, ESG concept is widely applied in the practice of stock portfolios, but the results reached by scholars through current study are inconsistent. On the one hand, the market believes that higher ESG scores will have an active influence on the investment portfolio (Czerwińska and Kaźmierkiewicz, 2015). Erragragui and Revelli (2016) found that ESG screening on the stocks that comply with Islamic law has no adverse impact on the stock return, and the portfolio with a good ESG score has better stock performance. Similarly, based on the study of Deng and Cheng (2019), we can conclude that the relationship between ESG indicators and stock market performance was positive. Stotz (2021) found that stocks with higher ESG scores have lower discount rates. In addition, Engelhardt et al. (2021) tested the correlation between ESG scores and stock performance during the COVID-19 pandemic and found that high ESG scores were associated not only with higher abnormal returns but also with lower stock price fluctuations. On the other hand, it is not necessarily for higher ESG scores to exert significant additional value to stock investors. Auer and Schuhmacher (2016) concluded that actively screening stocks with high or low ESG scores cannot provide better risk adjustment performance than a passive investment in the stock market.

Secondly, in recent years, the study issue pertaining to the influence of ESG scores on bond investors has just gotten attention, and the related research scenarios mainly focus on the secondary bond market. In the early stage, Hachenberg and Schiereck (2018) report that the influence of the ESG scores on bond pricing is significant. Subsequently, Badía et al. (2019) found that in terms of the ESG dimension, the performance of government bonds with high scores is better than that of government bonds with low scores at any social responsible investment demand levels. Li et al. (2020) found that ESG scores are closely related to the default probability of corporate bonds. With the deepening of study, scholars began to attach more importance to the studies of internal mechanism of ESG score information effect on the bond market. Research by Bahra and Thukral (2020) has found that ESG scores can boost the result of the portfolio by reducing withdrawal rate, reducing portfolio volatility, and even slightly increasing risk-adjusted return at times. When analyzing the relationship between ESG score and bond return, Jang et al. (2020) also believed that ESG score is an effective supplement to credit rating. In particular, information related to a firm’s downside risk is included in the ESG score, which is specifically significant for understanding small corporations and other corporations with a high degree of information asymmetry. Recently, Kanamura (2021) found that during COVID-19, ESG components have hedging effects on the downward risk of bond prices.

The research about the impact of ESG scores on bond investors in the capital market is in its infancy. ESG score information is also effective incremental information of the capital market, and the prior study has been focusing on the capital market response and other related research. But it is more biased toward the investment portfolio income of the stock market, and in recent years, the research on the bond market had little discussion still. At the same time, few studies investigated the information effect of ESG scores in the primary bond financing market, especially in China, as an emerging economy, the relevant researches are scarce. However, the Chinese bond financing market has developed rapidly. It has become the second largest bond market worldwide, which serves the Chinese economy and attracts investors from all over the world to allocate assets. Especially in recent years, corporate bond defaults have entered a tumultuous period. The quality of issuing corporation development has become a core issue that the market pays attention to, and traditional financial information cannot fully reflect the problems or potential risks in corporate development. Therefore, on the basis of the influence of ESG scores on the risk perception and decision-making of investors in the Chinese primary financing market, our study will have important practical significance and theoretical value.

ESG scores are comprehensive assessment of corporate ESG performance published by financial institutions in the capital market, and it has become an important source of information for investors to make value investments.

On the one hand, ESG scores provided investors with complete risk information (Zopounidis et al., 2020; Yang et al., 2021). ESG scores as critical non-financial information can not only reflect the importance the company attaches to environmental performance, social responsibility and corporate governance in the development process, but also reflect the practical development level of the three aspects. As the ESG criterion is accepted gradually in China, investors attach more importance to corporate ESG behavior and performance. However, it is in its infancy for Chinese corporations to disclose ESG information (Ruan and Liu, 2021). According to statistics, as of mid-2021, 1092 A-share listed corporations have disclosed ESG reports for 2020, accounting for only 25.3% of the total. Due to the small number of disclosed ESG reports and the lack of supervision, the disclosure indicators of ESG report is not uniform, as well as lower comparability and completeness. There is a large gap in investors’ demand for ESG information.

However, unlike ESG behavior information disclosed by the corporation itself, ESG scores are market index evaluated by financial institutions after integrating non-public and public information, so the ESG information provided is more complete. Furthermore, financial institutions obtain ESG related information through multiple channels, such as public and non-public methods (ESG report, research and interview). Meanwhile, the financial institution needs to comprehensively consider the incremental information such as ESG risk exposure, management level and ESG performance to reflect sustainable development potential and the ability to deal with ESG risks of the corporation. MSCI believes that applying ESG scores to investors’ investment decision-making process can help investors capture some risks and opportunities which may not be identified in the traditional financial analysis, thereby helping investors reduce investment risks and improve long-term investment returns. In addition, ESG scores of financial institutions are not just a simple integration of corporate ESG information, but also its quantitative analysis process. This information is expressed in qualitative to quantitative data, which is more helpful for investors to compare and analyze corporations. Therefore, for investors, the information provided by financial institutions on ESG scores has an incremental effect.

On the other hand, practice and prior study show that higher ESG scores help to reduce corporate risk (Zhang et al., 2021), and reduce future development risk perceived by investors. From the corporate perspective, a higher ESG score helps companies to increase environmental, social and governance attention, and help to optimize internal governance procedures and mechanisms and attract more high-quality employees. According to the current ESG performance, the corporation can adjust daily financial and operating policies to reduce ESG risk. From an external environmental perspective, a higher ESG score means that the corporation has more investment in ESG performance (Jang et al., 2020) and lower risk (La Torre et al., 2020), which will lead to the attention and supervision of analysts, media and investors. These effects of the ESG scores will further encourage corporation to restrain their risky behavior. (Brounen et al., 2021). Under the background of emission peak and carbon neutrality, corporations with high ESG scores will receive preferential policy support from the government and pay more attention to the ability of sustainable growth. Therefore, higher ESG scores help to promote the steady and benign development of the corporation, and then decrease the expected risk perceived by investors.

In summary, Higher ESG scores not only provide investors with incremental information on current corporate risk, but also help to reduce investors’ expectations of corporate future development risks, thereby reducing information asymmetry. In practice, ESG scores have been integrated into the process of portfolio allocation in the bond market. ESG scores are becoming a new dimension to redefine bond investment. However, prior study has mainly focused on the secondary bond trading market (Bahra and Thukral, 2020; Kanamura, 2021), and there has been little discussion about the information effect in the primary (issuance) market. In depth, investors of the secondary bond trading market will be affected by market factors, such as liquidity. The primary bond market is not only an investment market, but also a bond financing market for corporations. Investors attach more importance to the basic characteristics and behavior of bond-issuing corporations. Higher ESG scores will help to send a positive signal to investors in the bond financing market, and then reduce the risk premium demanded by investors. Based on the relevant theoretical analysis mentioned above, the following hypothesis are proposed:

To investigate the hypothesis, we selected the sample as follows:

First, we retrieved ESG scores information from the Wind database which provides ESG scores of SynTao Green Finance since 2015 for listed corporations in China. We take the ESG scores lagging 1 year to eliminate endogenous interference, so the sample observation period of this article is 2016–2020. Second, the data on financial, insurance corporations and special treatment (ST) were removed. Finally, accessing firm-level ESG scores data is particularly difficult for non-listed corporations. We selected listed corporations on the Shanghai and Shenzhen Stock Exchanges. In general, our final sample consists of 2,781 observations. We obtain ESG score and bond data from the Wind database and extract financial and corporate data from the China Stock Market and Accounting Research Database (CSMAR).

Following a previous study (Schwert, 2017), we test the relationship between ESG scores and Spreads with the following model:

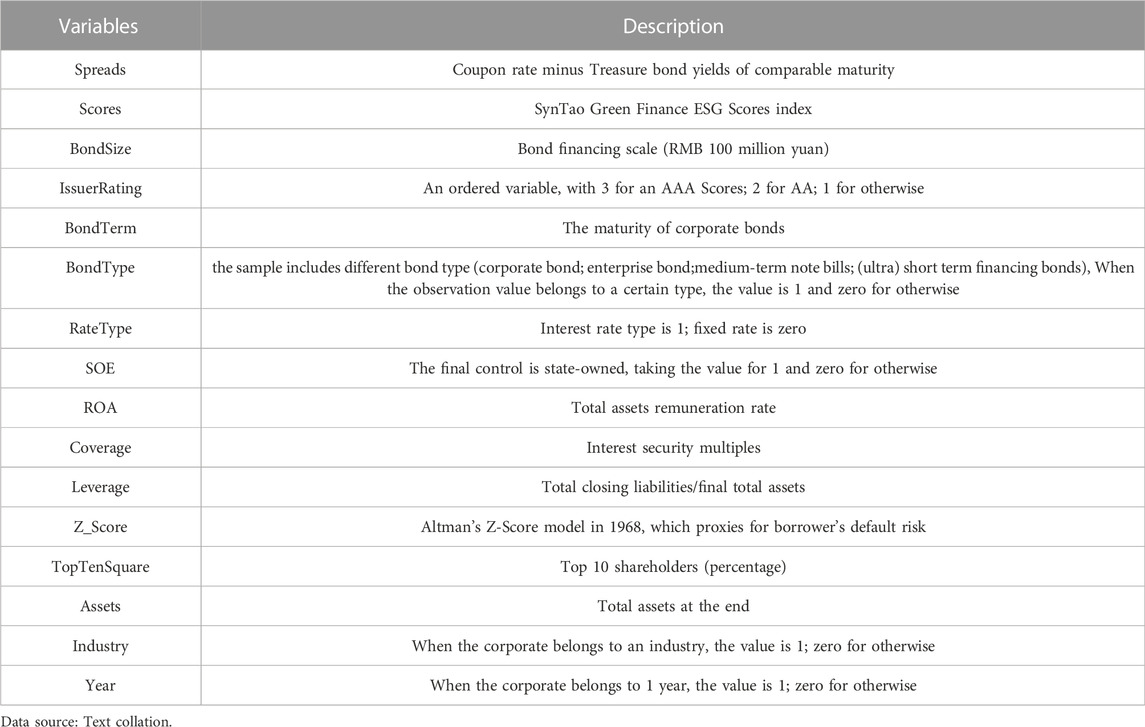

We use Spreads, the initial bond yield spreads, as a proxy for the dependent variable. Scores are independent variable. Following previous analysis (Deng and Cheng, 2019; Broadstock et al., 2021; Xu et al., 2021), we used SynTao Green Finance ESG scores index (ST-ESG), and sorted from low to high based on the sample level, D is the lowest level and is measured 1, and the rank is changed by 1, A+ level is measured 10 (Cornaggia et al., 2017; Ali et al., 2019). Table 1 provides the variables in the regression model.

TABLE 1. Variable definitions.

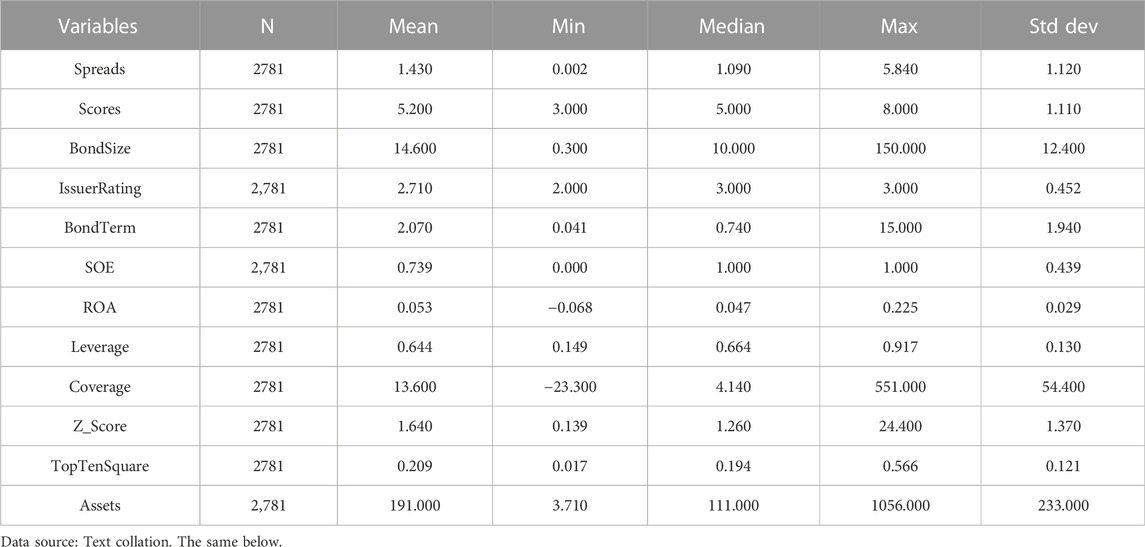

Table 2 lists the summary statistical results of the variables for the entire sample. The average Spreads of bonds are 1.430 and the median Spreads are 1.090, which shows that the interest rate is significantly higher than the treasury bond of the same period, the risk premium is significant. The average ESG scores is 5.200, and the median ESG scores is 5.000, which indicates that the ESG scores of bond issuers are generally low in China. In addition, the statistical results of the control variables also well reflect status of corporate bond issuance. Turning to bond characteristics, the large individual differences in scale and maturity show that companies have significantly different bond issuance capabilities and needs. The solvency and profitability of issuing bond companies are also different. Furthermore, SOEs comprise 74% of the sample, indicating that most bond issuance companies with ESG reporting are state-owned in China.

TABLE 2. Descriptive statistics.

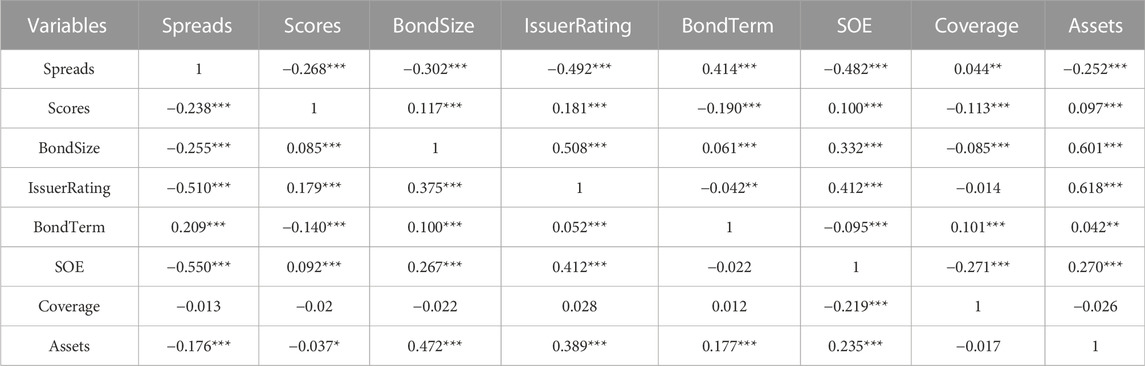

Table 3 reports the correlation matrices for critical variables used in this study. Spearman correlations above diagonal, Pearson correlations below diagonal. Spreads are significantly correlated with scores in the expected direction, and firm characteristics variables with Spreads are consistent with the findings of previous researchers. Such as, the nature of property rights has a significant negative correlation with Spreads, showing that State-owned enterprises possess “priority” in bond financing and the pricing is decreased due to implicit guarantees. The correlation between bond characteristics and Spreads also conforms to reality.

TABLE 3. Correlation analysis.

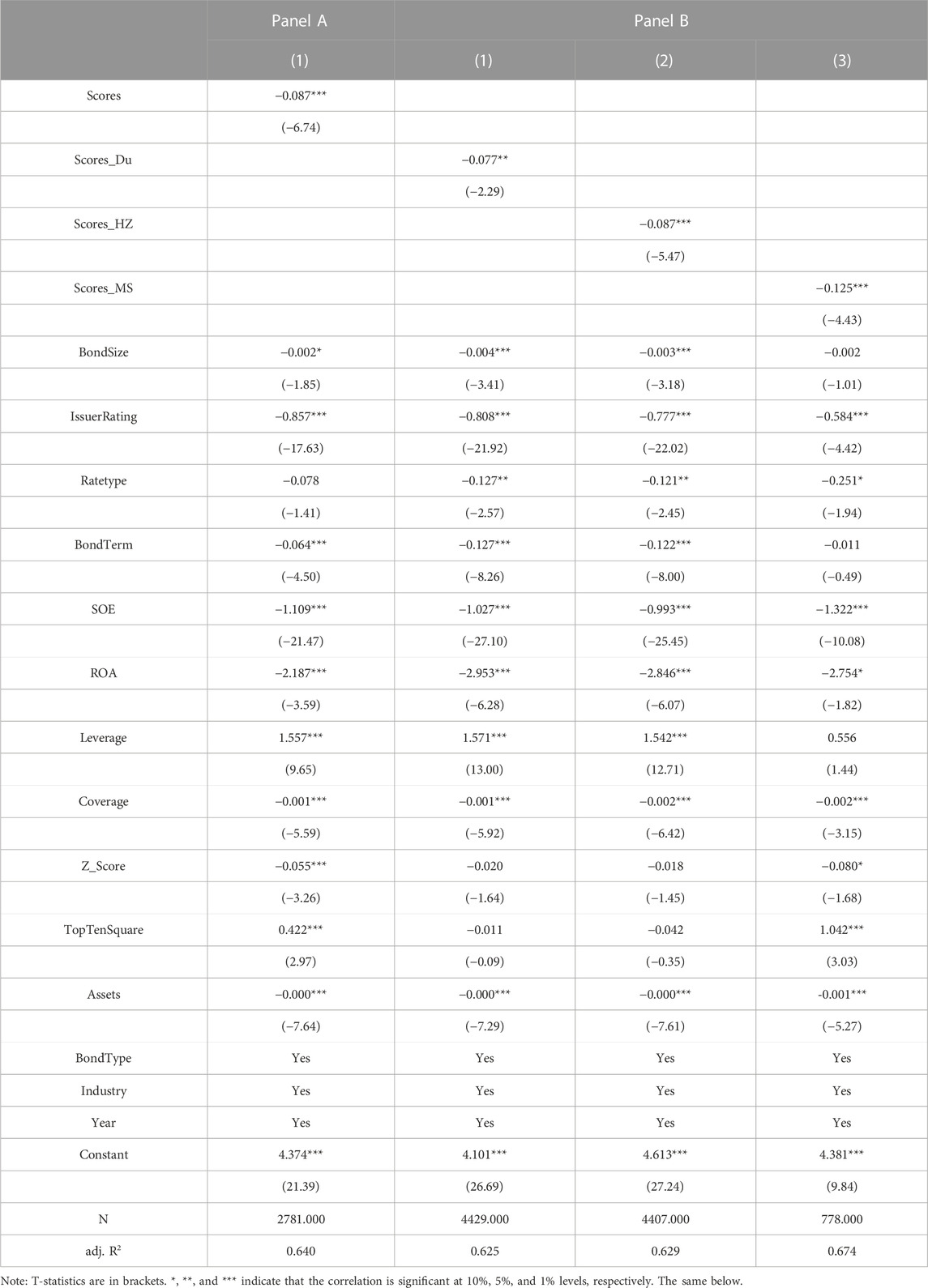

The results of our hypothesis are reported in Table 4 Panel A. The coefficient of ESG scores is -0.087 at 1% significance level, which indicates that ESG scores significantly reduced bond issuance risk premium. Therefore, the main hypothesis is verified.

TABLE 4. Baseline regression and robustness tests.

ESG scores difference test. We set dummy variables according to whether the listed company disclosed ESG scores, and if the corporation had disclosed ESG scores for SynTao Green Finance with one; otherwise, it is zero. As shown by the significantly negative coefficient on scores in the first column of Panel B Table4, it indicates that the risk premium of bonds is reduced significantly when ESG scores are disclosed. Obviously, ESG scores supply incremental information.

Replace explanatory variables. We used the ESG scores of Hua Zheng and MSCI as the explanatory variables to ensure the reliability of explanatory variables. MSCI ESG scores are also authoritative and highly credible, and widely used in investment decision-making. We used Python to request ESG scores for 2016 to 2020 from MSCI’s official website. As shown in columns 2–3 of Panel B Table4, the impact of ESG scores on the risk premium still exists.

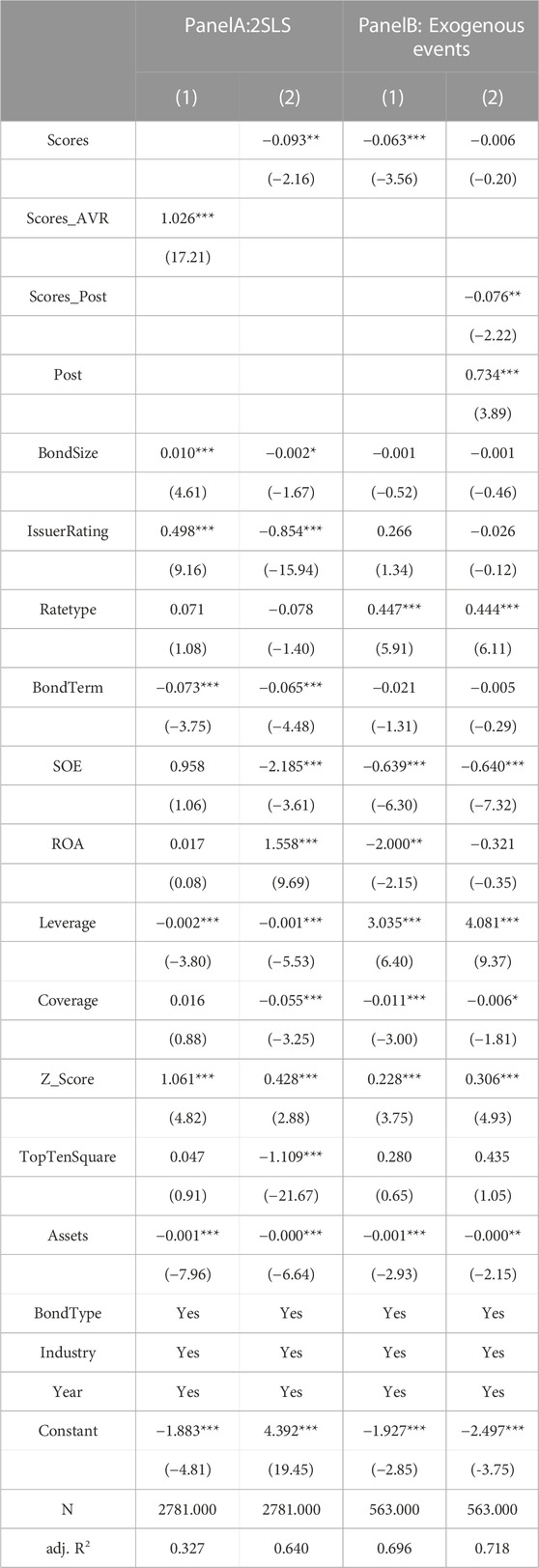

Using 2SLS procedure. We used the 2SLS procedure to alleviate the endogeneity problem. Referring to prior studies (Lin et al., 2012; Liu et al., 2019; Yang et al., 2021), our paper selected the mean values of the ESG scores in the same industry and year as instrumental variables, and carried out the 2SLS procedure. The results indicate that the coefficient of Scores in Table 5 PanelA is -0.093 and significant.

TABLE 5. Endogeneity test.

Using a particular sample and exogenous event. We choose the bond issuers listed in both Chinese mainland and Hong Kong as a particular sample. With the first revision of the Environmental, Social and Governance Reporting Guide completed by the Hong Kong Stock Exchange in 2017, the requirement for ESG information disclosure of Hong Kong-listed companies was raised to the level of “interpretation without disclosure”, which further strengthened the market attention of ESG information. Therefore, we use 2017 as the starting point for exogenous events (Post) to construct the interaction between exogenous events and ESG scores (Scores_Post), and investigate the impact of exogenous events on the ESG scores effect. As reported in Table 5 PanelB, At the significance level of 5%, the coefficient of Scores_Post is -0.076, meaning that the ESG Scores indeed influence the bond premium and will change with the trigger of exogenous events.

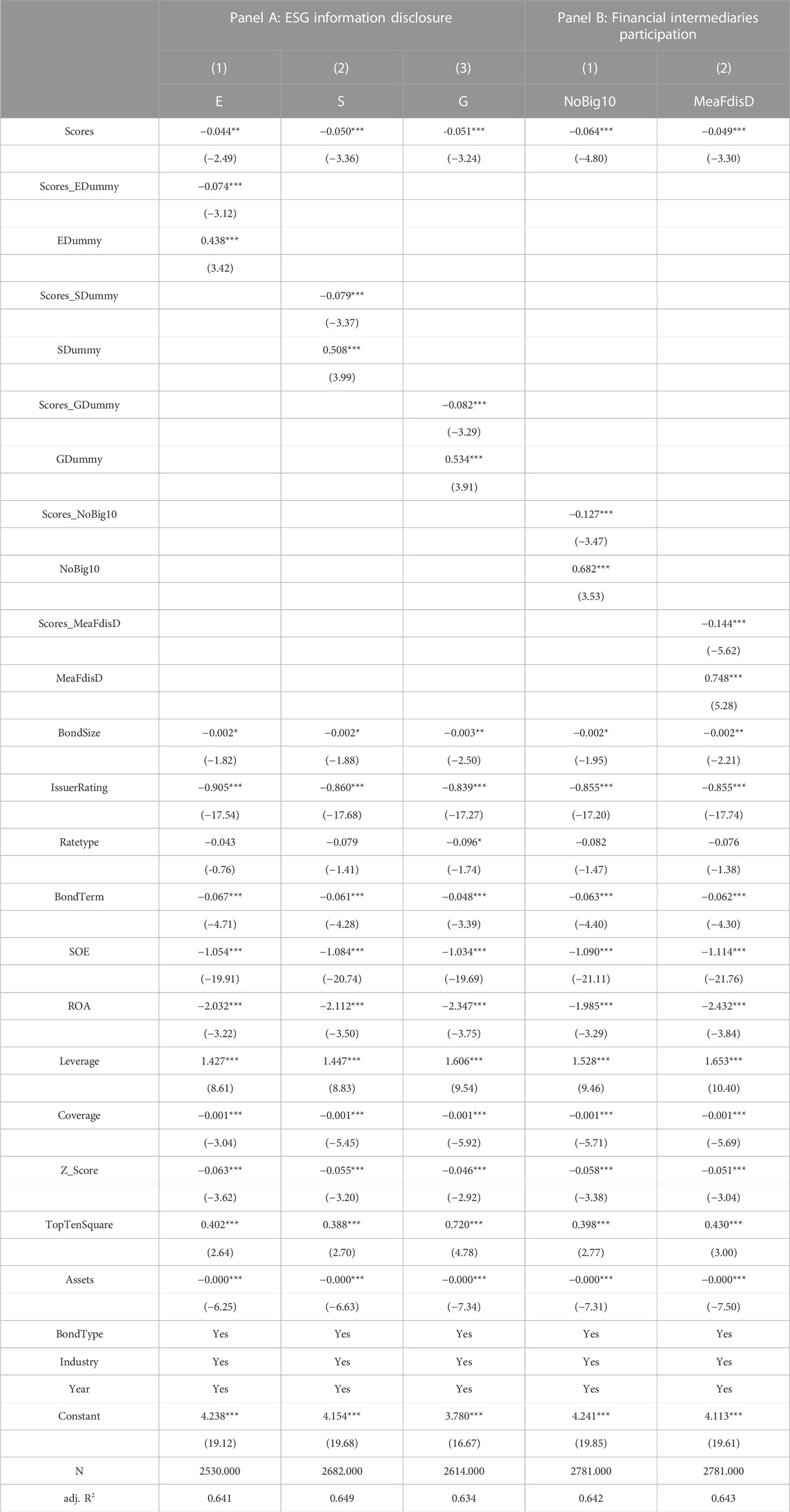

On the basis of information asymmetry perspectives, we examined the incremental information effect of ESG scores from two directions: the information disclosure of ESG behavior and the participation of financial intermediaries.

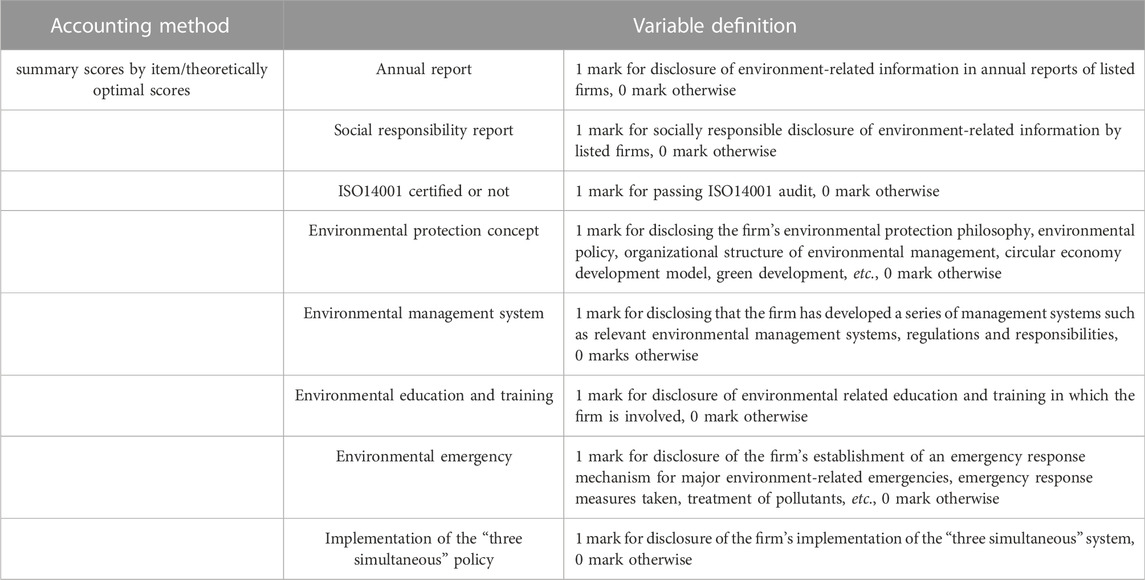

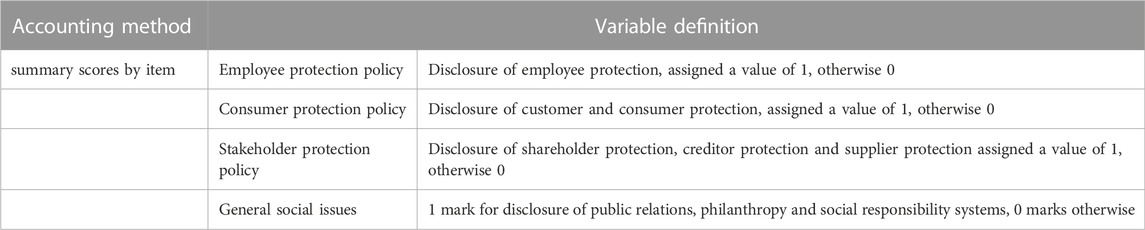

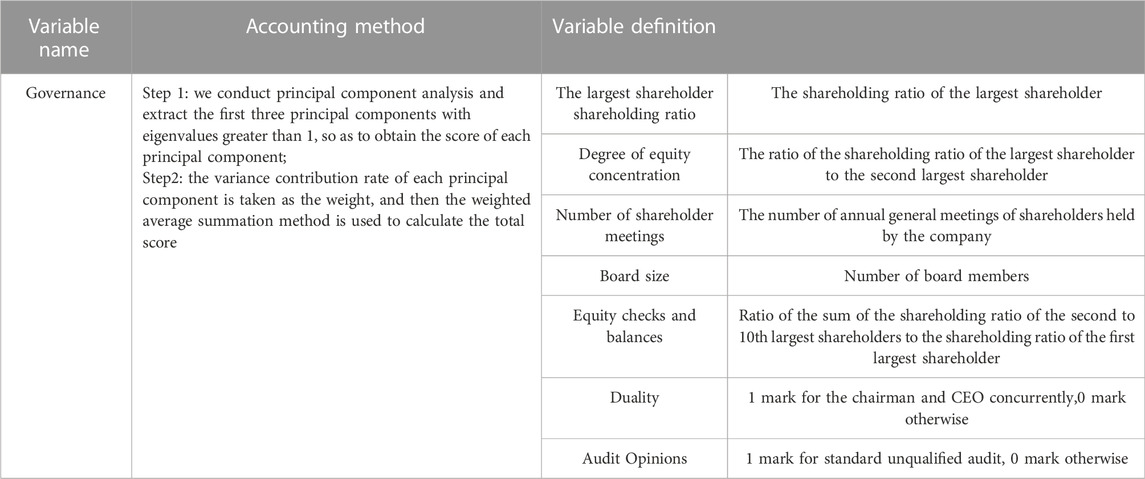

ESG Information Disclosure. We reflected the degree of information asymmetry based on the information disclosure of environmental, social and governance. Following Lanis and Richardson (2012) and Ali et al. (2022), we designed three variables for information disclosure of ESG behavior and reported measures of these three variables in the appendix (Table A1, Table A2, Table A3), then based on the annual industry average of each variable, we set three dummy variables EDummy, SDummy, GDummy (if the Environmental, Social, Governance is lower than the annual industry average respectively, EDummy, SDummy, GDummy with 1, otherwise it is zero). Table 6 Panel A reports that the interaction coefficients between each dummy variable and the explanatory variable are highly significant and negative, indicating that ESG scores’ marginal effect is significant when less information disclosure on the environment, social responsibility, and governance.

TABLE 6. Mechanism analysis.

Financial Intermediaries Participation. We also reflected the degree of information asymmetry from the perspective of financial intermediaries’ characteristics and behavior. According to audit firm and analyst forecast dispersion, set two dummy variables NoBig10 and MeaFdisD (if an audit firm is not Big 10, NoBig10 with 1, otherwise it is zero; if the analyst forecast dispersion is greater than the mean, MeaFdisD with 1, otherwise it is zero). Table 6 Panel B shows that all the coefficients on scores_NoBig10 and scores_MeaFdisD are significantly negative, indicating that ESG scores marginal effect is significant when the audit firm is not Big 10 and higher analyst forecast dispersion. The above results show that ESG scores provide incremental information, thus providing investors with sufficient information on investment risk.

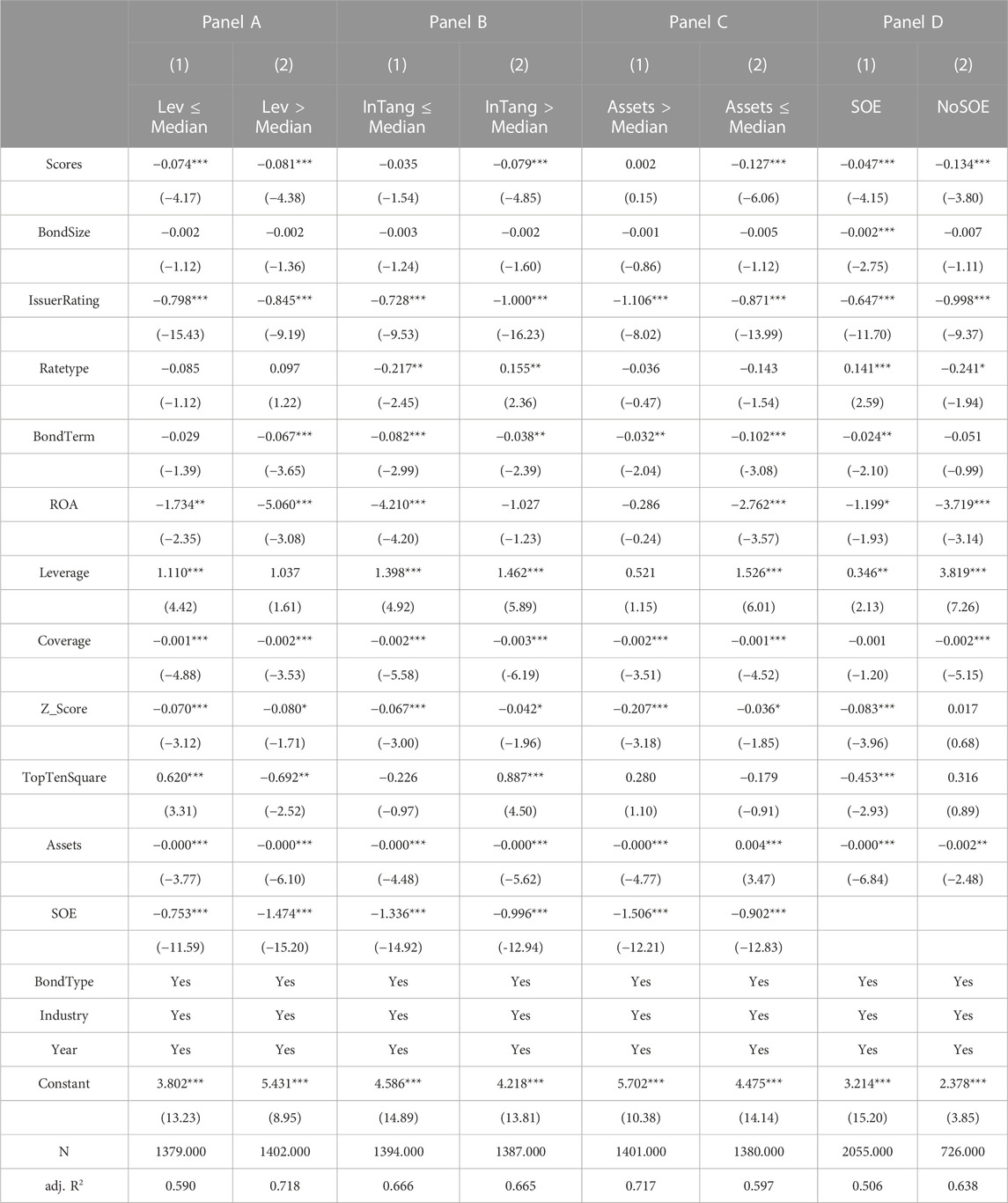

The effect of ESG scores information may be heterogeneous with different debt financing capabilities. Usually, the companies which easier access to financing have low-risk premiums in the bond market, and higher ESG scores are difficult to reduce the risk premium. But other companies with poor debt financing capabilities are at a competitive disadvantage, generally difficult to obtain the recognition of investors. If these companies have excellent performance in non-financial aspects, such as ESG scores, may reduce investors’ valuation of corporate risks to a great extent. We examine ESG scores effect on the companies which have different debt financing capabilities through the following four aspects:

Asset-liability ratio. Asset-liability ratio not only reflects corporate capital allocation, but also reflects the corporate debt risk. The higher debt ratio will increase the risk perceived by investors, which will weaken corporate debt financing ability;

Proportion of intangible assets. The high proportion of intangible assets will increase the risk of investors’ evaluation of the company’s value, thus aggravating the market information asymmetry. Moreover, from the traditional debt financing practice, compared with tangible assets, the mortgage ability of intangible assets is weak;

Firm size. The scale of a company can reflects comprehensive corporate strength. The smaller the scale, the weaker the anti-risk ability and the poorer debt financing capabilities;

Nature of property rights. In practice, non-state-owned holding companies are at a disadvantage in terms of development level, market recognition and trust. Therefore, the debt financing capabilities of non-state-owned holding companies were weaker than state-owned holding companies.

We divided groups by median asset-liability ratio, the proportion of intangible assets, firm size, as well as nature of property rights. The results of Table 7 Panel A to D indicate that ESG scores effect is significant when the company has a higher asset liability-ratio or proportion of intangible assets, smaller size and property rights is non-state-owned holding, The empirical results indicate that when debt financing capabilities are lower, the effect of ESG scores is positive.

TABLE 7. Debt financing capabilities regression.

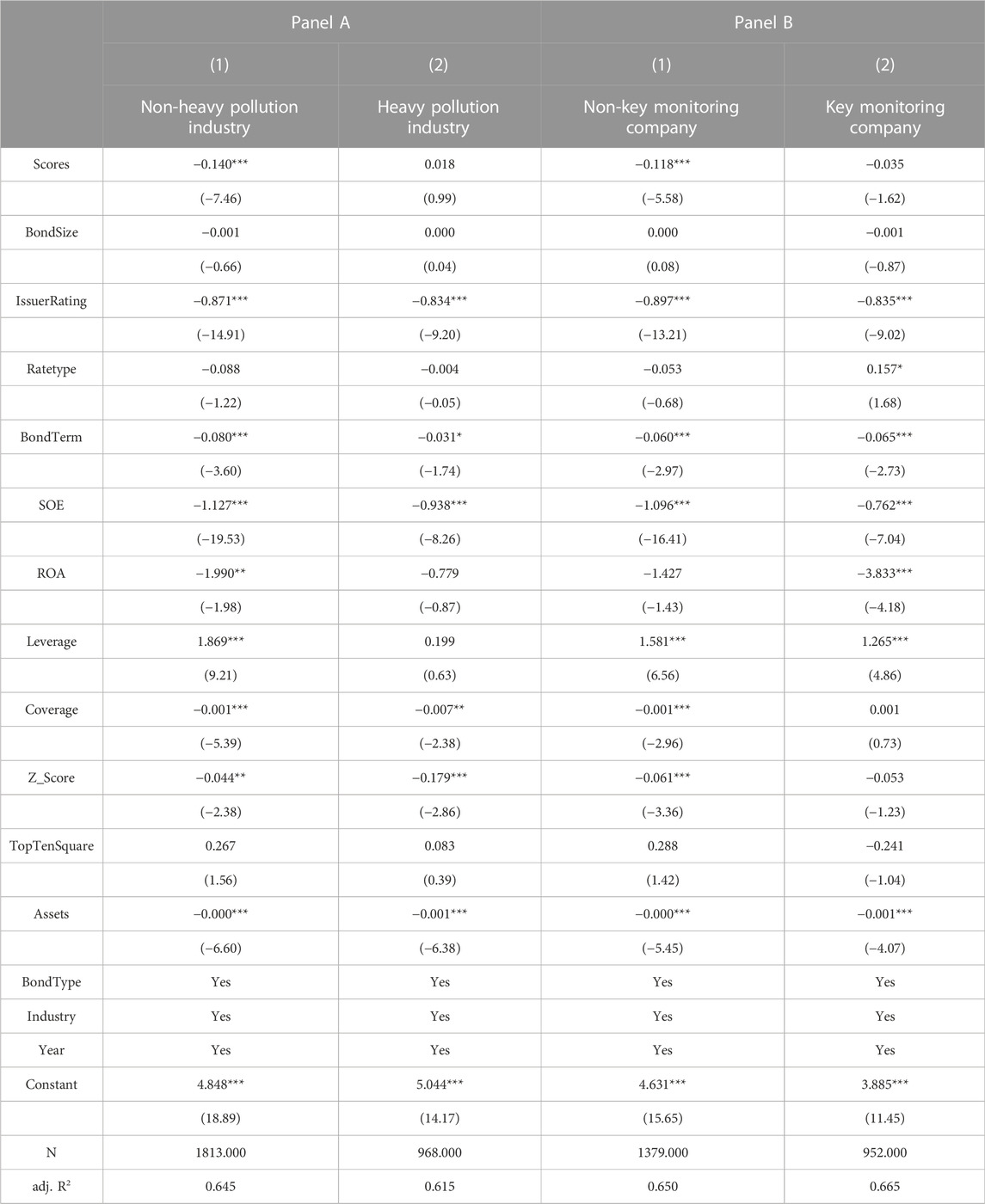

Corporations that are subject to industry supervision and market monitoring disclose a large amount of information to the public, and the incremental information effect of ESG scores is weakened. Heavy pollution industries have always received social attention and government supervision. The Chinese government has issued key monitoring lists for polluting corporations since 2010. From the perspective of information asymmetry, whether heavy pollution or key monitoring corporations, it is necessary to provide market investors with timely and sufficient information on business activities in strict accordance with regulatory regulations. In particular, key monitoring corporations also need to strictly follow relevant policies and regulations for disclosing information on pollution in detail. Investors pay more attention to these corporations and obtain relatively sufficient risk information. Therefore, the incremental information effect of ESG scores may be limited to investors.

Moreover, for heavy pollution or key monitoring corporations, they have had a considerable negative impact on the environment. Market investors believe that the investment of such corporations in environmental and social responsibility is in line with the expected obligatory behavior. However, in light pollution or non-pollution industries, these corporations are not subject to regulatory pressure on environment and social responsibility, if these corporations have positive signals in ESG performance, which will increase the market’s recognition, so the incremental information effect of ESG scores may be greater.

We divided the sample into two groups with whether it was heavy pollution industries, then divide two groups with whether it was key monitoring. Table 8 presents the results and show that in the non-heavy pollution industry (non-key monitoring corporation) ESG scores have reduced the risk premium to a greater extent.

TABLE 8. Industry supervision and market monitoring regression.

When there are massive of defaults in the bond market, the positive effect of ESG scores will be more prominent. Frequent bond defaults cause investors to panic and lose confidence in the market. At that time, investors’demand for positive information increased and they will focus more on corporate quality. ESG scores focus on measuring the values and business paradigms, and evaluating the social value brought by the corporation. Although it is not a financial performance indicator, it has a certain early warning effect on corporate risks (Kanamura, 2021). Especially in the concept of global sustainable development, corporations increasingly consider ESG investment in daily operations, and it will help corporation improve Sustainable Business Performance. ESG scores information also include the behavioral information of corporate investment in green environmental protection, social and governance. Prior study has also shown that corporate social responsibility investment and higher levels of corporate governance can help reduce the default rate of corporate bonds. Therefore, when the market has a large number of bond defaults, ESG scores have a greater impact on bond risk premium.

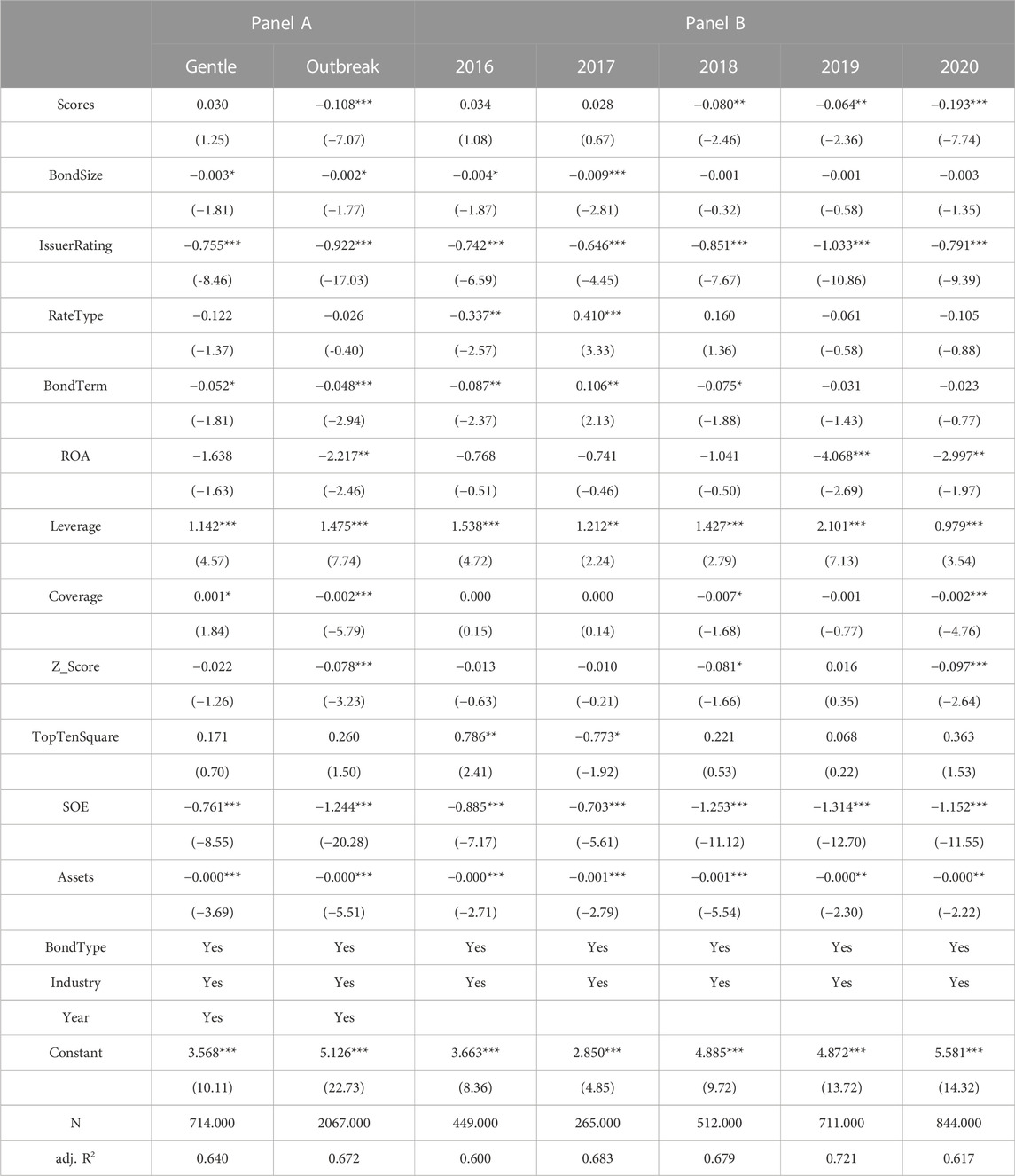

We divided two groups with bond default in the Chinese market, Table 9 Panel A shows that in the gentle period of default, the regression coefficient of scores is 0.030 and not significant, but in the outbreak period of default, the coefficient of scores is −0.108 and highly significant, showing that ESG scores play a greater role in reducing the bond credit risk premium during the outbreak of default.

TABLE 9. Annual trend change regression.

Up to now, the ESG information disclosed by listed corporations still has no unified paradigm and caliber, while the ESG scores of financial institutions have high systematic and quantitative functions, which not only conform to today’s macroeconomic development policies, but also provide timely and comparable information for investors. At the same time, the Chinese government has also attached importance to and issued ESG related green finance policies year by year, so investors have paid more and more attention to ESG scores.

Especially, given that the COVID-19 started in December 2019 in China, it has had a huge impact on the economy of China and the world. In the context of COVID-19 pandemic in 2020, Chinese government has put forward the strategic goal of emission peak and carbon neutrality to face the sustainable development, investors will attach more importance to ESG scores information to help them judge the long-term investment value and potential risks of the corporation.

The five group regression results based on year are presented in Table 9 Panel B. The regression coefficients of scores in 2016 and 2017 are positive but not significant, and the regression coefficients of scores from 2018 to 2020 are negative and significant. Especially the rapid development of COVID-19 in 2020 affects the whole of China. Therefore, investors pay more attention to ESG scores than before, which also showed that investors care more about value investment and also generate more risk aversion needs. The regression coefficient of scores is -0.193 in 2020, and is the most significant, showing that the impact of ESG scores on bond risk premium is prominently reflected in 2020.

1) The purpose of this paper is to explore the relationship between the ESG scores of bond issuers and the risk premium of bond issuance. Based on the ESG scores and bond issuance data of Chinese listed corporations, we empirically tested the relationship between them by referring to Lin et al. (2012) and Schwert (2017), and find that ESG scores can significantly reduce the risk premium of corporate bond issuance. The results of this paper not only help to enrich the research on the economic consequences of ESG scores, but also help to expand the related research on the influencing factors of corporate bond financing cost.

2) This paper further confirms the incremental information value of ESG scores through the bond market. From the perspectives of the disclosure of corporate ESG behavior and the participation of financial intermediaries, this paper carried out the mechanism test, and further proved it through different scenarios of investors’ information needs. Compared with previous studies, this paper based on the bond market can further enrich the research that discusses the incremental information value of ESG scores.

3) This paper may have some limitations. First, as financial institutions only issue ESG scores for listed corporations, the study sample in this paper are only listed corporations, so there is a potential problem of insufficient sample size. Second, the research scenario of this paper is Chinese capital market, so the research results are more applicable to emerging market.

4) In future research, we can not only focus on the study of ESG scores adjustment but also carry out related research from the perspective of E (Environment), S(Society) and G (Government) scores respectively, so as to build a more complete research system.

Using the ESG scores and the bond data of Chinese listed corporations, we empirically investigated the effect and internal mechanism of ESG scores on risk premium of bond issuance. First, we conclude that when the ESG scores of a bond issuer are higher, the investors will require a lower risk premium. Second, the results of the mechanism and further study indicated that the ESG scores can provide incremental information value to investors. Finally, based on the Chinese bond financing market, this study not only promote the expansion of ESG theory, but also proves that ESG scores information contributes to the development of capital market.

First, it provides empirical evidence for the application of ESG concept in global capital markets. As an emerging economy, China has a large bond market, but does not have a higher level of market-oriented pricing. But we have obtained very significant results, indicating that the ESG scores have indeed been widely used in the capital market. Second, corporations need to pay attention to their ESG scores. Based on the impact of ESG scores on financing costs they should establish ESG concept, improve ESG performance, and increase ESG information disclosure, so as to obtain higher ESG Scores from the third-party financial institutions. Finally, ESG scores provide investors with important incremental information about the issuing corporation, therefore ESG scores have important reference significance for investors to allocate investment products.

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding author.

CZ: Conducted funding acquisition and methodology. LG: Conducted formal analysis. WW: Lead the writing and literature review. XC: Lead the data curation and literature review. JA: Leads the writing and the review.

This research was funded by the National Natural Science Foundation of China, grant number 71702001; the National Social Sciences Foundation of China, grant number 21BGL097; Anhui University of Finance and Economics graduate scientific research and innovation foundation, Grant Number ACYC2021470.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Aboud, A., and Diab, A. (2019). The financial and market consequences of environmental, social and governance ratings. Sustain. Account. Manag. Policy J. 10 (3), 498–520. doi:10.1108/SAMPJ-06-2018-0167

Ali, S., Jiang, J., Rehman, R. u., and Khan, M. K. (2022). Tournament incentives and environmental performance: The role of green innovation. Environ. Sci. Pollut. Res. Int. doi:10.1007/s11356-022-23406-w

Ali, S., Zhang, J., Usman, M., Khan, F. U., Ikram, A., and Anwar, B. (2019). Sub-national institutional contingencies and corporate social responsibility performance: Evidence from China. Sustainability 11 (19), 5478. doi:10.3390/su11195478

Auer, B. R., and Schuhmacher, F. (2016). Do socially (ir)responsible investments pay? New evidence from international ESG data. Q. Rev. Econ. Finance 59, 51–62. doi:10.1016/j.qref.2015.07.002

Badía, G., Pina, V., and Torres, L. (2019). Financial performance of government bond portfolios based on environmental, social and governance criteria. Sustainability 11 (9), 2514. doi:10.3390/su11092514

Bahra, B., and Thukral, L. (2020). ESG in global corporate bonds: The analysis behind the hype. J. Portfolio Manag. 46 (8), 133–147. doi:10.3905/jpm.2020.1.171

Baker, E. D., Boulton, T. J., Braga-Alves, M. V., and Morey, M. R. (2021). ESG government risk and international IPO underpricing. J. Corp. Finance 67, 101913. doi:10.1016/j.jcorpfin.2021.101913

Broadstock, D. C., Chan, K., Cheng, L. T. W., and Wang, X. (2021). The role of ESG performance during times of financial crisis: Evidence from COVID-19 in China. Finance Res. Lett. 38, 101716. doi:10.1016/j.frl.2020.101716

Brounen, D., Marcato, G., and Op ’t Veld, H. (2021). Pricing ESG equity ratings and underlying data in listed real estate securities. Sustainability 13 (4), 2037. doi:10.3390/su13042037

Cornaggia, K. J., Krishnan, G. V., and Wang, C. (2017). Managerial ability and credit ratings. Contemp. Acc. Res. 34 (4), 2094–2122. doi:10.1111/1911-3846.12334

Czerwińska, T., and Kaźmierkiewicz, P. (2015). ESG rating in investment risk analysis of companies listed on the public market in Poland. Econ. Notes 44 (2), 211–248. doi:10.1111/ecno.12031

Deng, X., and Cheng, X. (2019). Can ESG indices improve the enterprises’ stock market performance?—An empirical study from China. Sustainability 11 (17), 4765. doi:10.3390/su11174765

Engelhardt, N., Ekkenga, J., and Posch, P. (2021). ESG ratings and stock performance during the COVID-19 crisis. Sustainability 13 (13), 7133. doi:10.3390/su13137133

Erragragui, E., and Revelli, C. (2016). Is it costly to be both shariah compliant and socially responsible? Rev. Financial Econ. 31, 64–74. doi:10.1016/j.rfe.2016.08.003

Hachenberg, B., and Schiereck, D. (2018). Are green bonds priced differently from conventional bonds? J. Asset Manag. 19 (6), 371–383. doi:10.1057/s41260-018-0088-5

Hong, S. (2019). Corporate social responsibility and accounting conservatism. Int. J. Econ. Bus. Res. 19 (1), 1–18. doi:10.1504/IJEBR.2020.103883

Immel, M., Hachenberg, B., Kiesel, F., and Schiereck, D. (2021). Green bonds: Shades of green and Brown. J. Asset Manag. 22 (2), 96–109. doi:10.1057/s41260-020-00192-z

Jang, G.-Y., Kang, H.-G., Lee, J.-Y., and Bae, K. (2020). ESG scores and the credit market. Sustainability 12 (8), 3456. doi:10.3390/su12083456

Kanamura, T. (2021). Risk mitigation and return resilience for high yield bond ETFs with ESG components. Finance Res. Lett. 41, 101866. doi:10.1016/j.frl.2020.101866

La Torre, M., Mango, F., Cafaro, A., and Leo, S. (2020). Does the ESG index affect stock return? Evidence from the Eurostoxx50. Sustainability 12 (16), 6387. doi:10.3390/su12166387

Lanis, R., and Richardson, G. (2012). Corporate social responsibility and tax aggressiveness: An empirical analysis. J. Account. Public Policy 31 (1), 86–108. doi:10.1016/j.jaccpubpol.2011.10.006

Li, P., Zhou, R., and Xiong, Y. (2020). Can ESG performance affect bond default rate? Evidence from China. Sustainability 12 (7), 2954. doi:10.3390/su12072954

Lin, C., Ma, Y., Malatesta, P., and Xuan, Y. (2012). Corporate ownership structure and bank loan syndicate structure. J. Financial Econ. 104 (1), 1–22. doi:10.1016/j.jfineco.2011.10.006

Liu, J.-B., Wang, C., Wang, S., and Wei, B. (2019). Zagreb indices and multiplicative zagreb indices of eulerian graphs. Bull. Malays. Math. Sci. Soc. 42 (1), 67–78. doi:10.1007/s40840-017-0463-2

Ruan, L., and Liu, H. (2021). Environmental, social, governance activities and firm performance: Evidence from China. Sustainability 13 (2), 767. doi:10.3390/su13020767

Schwert, M. (2017). Municipal bond liquidity and default risk. J. Finance 72 (4), 1683–1722. doi:10.1111/jofi.12511

Stotz, O. (2021). Expected and realized returns on stocks with high-and low-ESG exposure. J. Asset Manag. 22 (2), 133–150. doi:10.1057/s41260-020-00203-z

Xu, J., Liu, F., and Shang, Y. (2021). R&D investment, ESG performance and green innovation performance: Evidence from China. K. 50 (3), 737–756. doi:10.1108/K-12-2019-0793

Yang, Y., Du, Z., Zhang, Z., Tong, G., and Zhou, R. (2021). Does ESG disclosure affect corporate-bond credit spreads? Evidence from China. Sustainability 13 (15), 8500. doi:10.3390/su13158500

Zhang, J., De Spiegeleer, J., and Schoutens, W. (2021). Implied tail risk and ESG ratings. Mathematics 9 (14), 1611. doi:10.3390/math9141611

TABLE A1. Definitions of environmental performance variables.

TABLE A2. Definitions of social responsibility performance variables.

TABLE A3. Definitions of corporate governance performance variables.

Keywords: ESG scores, bond risk premium, sustainable business performance, debt financing capacity, incremental information

Citation: Zhang C, Gao L, Wang W, Chen X and An J (2023) Do ESG scores have incremental information value on the primary bond market?——evidence from China. Front. Environ. Sci. 10:1051000. doi: 10.3389/fenvs.2022.1051000

Received: 22 September 2022; Accepted: 07 December 2022;

Published: 04 January 2023.

Edited by:

Alexandru Bodislav, Bucharest Academy of Economic Studies, RomaniaReviewed by:

Mário Nuno Mata, Instituto Politécnico de Lisboa, PortugalCopyright © 2023 Zhang, Gao, Wang, Chen and An. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Jiapeng An, MzIwMTUwMjE4NUBhdWZlLmVkdS5jbg==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.