Xingmin Zhang

Xingmin Zhang Chang’an Wang2

Chang’an Wang2 Xiaoqian Liu

Xiaoqian Liu

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 10 October 2022

Sec. Land Use Dynamics

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.1037248

This article is part of the Research TopicLand Use Management and Carbon Abatement in a Sustainable Development PerspectiveView all 12 articles

Agriculture is the second largest source of carbon emissions in the world. To achieve the strategic goals of “carbon peaking” and “carbon neutrality”, how to effectively control agricultural carbon emissions has become a focus of the Chinese government. As China’s most critical agricultural policy in the early 21st century, assessing the impact of rural tax-and-fees reform (RTFR) on agricultural carbon emissions has vital theoretical and practical implications. Based on panel data of 31 Chinese provinces from 2000 to 2019, this paper constructs a continuous difference-in-differences (CDID) model to identify the effects of RTFR on agricultural carbon emissions, and further tests the mechanisms and heterogeneity of the reform to achieve agricultural carbon emission reduction. The results demonstrate that the reform can effectively reduce the agricultural carbon intensity and improve agricultural carbon efficiency, with the effects of −6.35% and 6.14%, respectively. Moreover, the dynamic effect test shows that the impact of RTFR on agricultural carbon intensity and carbon efficiency is persistent. Furthermore, the mechanism analysis indicates that RTFR achieves the improvement of agricultural operation efficiency and the reduction of agricultural carbon emissions through the expansion of land operation area, the increase of productive investment in agriculture, and the special transfer payment from the central government. However, the impact of RTFR on local government revenue is not conducive to realizing the reform’s carbon reduction effect. The heterogeneity analysis illustrates that the reform policy effects differ in natural climatic conditions, topographical conditions, and crop cultivation structure. The RTFR mostly has a significant negative impact on the carbon emissions generated from material inputs and agricultural production. Therefore, to address the climate change crisis and improve the environmental efficiency of agricultural production, it is necessary to both reduce peasants’ tax burden and implement institutional construction efforts, to further promote the transformation of agricultural production to a low-carbon model.

Since the 1980s, the massive emission of greenhouse gases represented by carbon dioxide has led to a significant acceleration of the global warming trend, and the resulting environmental problems have caused a momentous negative impact on the normal operation of human society, and it has become the consensus of the international community to curb greenhouse gas emissions (Jia et al., 2021; Wang et al., 2021; Wang et al., 2022). Evidence shows that agricultural greenhouse gas emissions account for about 25% of global emissions, ranking second only to energy emissions (Yang et al., 2022). In China, agricultural greenhouse gas emissions account for about 15% of the total national emissions, and are the main source of greenhouse gas emissions (Cui et al., 2021; Kong et al., 2022). Therefore, in the context of Chinese society’s efforts to achieve “carbon peaking” and “carbon neutrality”, it is of great strategic importance to investigate the influencing factors and pathways of agricultural carbon abatement.

To achieve agricultural carbon emission reduction, it is necessary to innovate agricultural development models and enhance the efficiency and level of agricultural production (Jia et al., 2021; Guo et al., 2022; Huang et al., 2022; Xu et al., 2022; Yu et al., 2022). From the international experience, the more successful agricultural modernization models are broadly divided into two kinds. One is the large-scale land management agricultural production model represented by the United States, and the other is the technology-intensive agricultural production model represented by the Netherlands and Israel (Cabral et al., 2022; Chen et al., 2022; Liu and Wang, 2022). Because of the huge geographical differences and uneven population distribution in China, both agricultural modernization models are possible in regions with different comparative advantages (Han and Lin, 2021; Huang and Xiong, 2022). In terms of large-scale operation, a reasonable concentration of land is extremely important. Through the transfer of land, the concentration of land from general farmers to farmers with high productivity and the development of moderate scale operation can effectively improve production efficiency and realize the modernization of agricultural production methods (Carauta et al., 2021; Li et al., 2022). In terms of technologized operation, in addition to continuous innovation in agricultural technology, it is more important that farmers have the capital and ability to apply new technologies to the actual production process, improve new technologies such as mechanical, biological, and environmental protection that are actually used in agricultural production, and complete the technological transformation of agricultural production methods (Chen, 2020; Norton and Alwang, 2020; Zhang et al., 2022).

However, to complete the transformation of agricultural production in large-scale and technology, all cannot be without the corresponding capital investment (Liu et al., 2019; Fei et al., 2021). Generally, China has many people and little land, which is a typical agricultural production mode of the small-scale peasant economy (Liu and Zhuang, 2000). The small-scale peasant economy is the most widely distributed agricultural production mode in East Asia, with many characteristics such as decentralized operation on small plots of land; low productivity level; insufficient specialization and division of labor; low economic returns; and inferior risk resistance (Munroe, 2001; Lahiff and Kay, 2007; Akram-Lodhi and Kay, 2010; Zhang, 2012; Falkowski, 2018). Therefore, the crucial to achieving the modernization and transformation of traditional Chinese agriculture is to address the plight of insufficient agricultural capital and low returns for farmers. For a long time, Chinese farmers not only need to face the difficulties of low agricultural returns, but also have to bear an excessive land burden (Xu et al., 2020). Land burden mainly refers to a series of tax and fee pressures, including agricultural tax, agricultural special tax, and rural public expenditure. Under the heavy pressure of land burden, the comparative return of agricultural operation is low, the contradiction of increasing production without increasing farmers’ income is prominent, and land transfer is difficult (Rymanov, 2017; Gurel, 2019). In some regions, farmers who have transferred their land are not only unable to receive their rightful land rent, but even have to pay unreasonable land transfer management fees. Under such conditions, the double constraints of land burden and agricultural income have suppressed the rational concentration of land and restricted the reasonable investment in agricultural reproduction, which has seriously prevented the modernization and transformation of Chinese agriculture.

Against this background, to maintain social stability, solve the problem of the excessive burden on farmers, and promote the modernization of agriculture and rural areas, the Chinese government gradually implemented the rural tax-and-fees reform (RTFR) in the early 21st century (Li and Sicular, 2014; Wang, 2019). By the end of 2005, the agricultural tax, which had lasted for more than 2,000 years in Chinese society, was officially suspended, marking a fundamental change in the relationship between urban and rural areas as well as agricultural production in China (Chen, 2009). By the end of 2006, the reform directly alleviated the tax-and-fees’ burden on farmers by about 160 billion Yuan, with a per-capita reduction of about 170 Yuan. Therefore, the RTFR objective reduces the pressure on farmers’ land and helps increase agricultural income (Tao and Qin, 2007; Liu et al., 2012; Wang and Shen, 2014). Under the realistic requirement of constructing a low-carbon society, does the RTFR help reduce agricultural carbon emissions? Further, can the impact of RTFR on carbon emissions be realized through the effective utilization of land? In addition, considering the economic and geographical conditions of China, how do the carbon abatement effects of the reform vary in different geographical regions? These are a series of questions that need to be assessed scientifically.

The existing literature demonstrates that government policy intervention is effective in achieving agricultural carbon abatement (Huang et al., 2022; Li and Li, 2022; Yang et al., 2022). Regarding traditional fiscal and monetary policies, rural support-oriented fiscal policies can lead to agricultural emission reduction by promoting agricultural technological progress, increasing farmers’ investment capacity, and improving cultivated land quality (Lin and Huang, 2021; Mamun et al., 2021). The Chinese government’s policy to develop digital and green finance can also decrease agricultural carbon emissions by guiding farmers’ entrepreneurship and agricultural technology innovation (Chang, 2022; Guo et al., 2022; Xu et al., 2022). As for environmental regulation policies, administrative regulation imposed by the central government on local governments and government officials is also conducive to agricultural carbon abatement by stimulating technological innovation inputs and agronomic investments by local governments (Liu et al., 2022). It has also been argued in the literature that enhanced remote regulation of agricultural tractor use by the government is also contributive to improving agricultural production efficiency to achieve carbon curbs (Hou et al., 2022). In addition, carbon trading policies are also considered as an effective measure to achieve carbon mitigation in agriculture (Wu et al., 2022). Carbon trading policies can control agricultural carbon emissions by affecting the technical efficiency of agricultural enterprises, agricultural production efficiency, and consumer preferences (Hua et al., 2022; Yu et al., 2022). In terms of land use policies, long-term rational land planning formulated by local governments is conducive to minimizing the leakage of agricultural carbon emissions through agricultural intensification (Pan et al., 2020). Meanwhile, some scholars argue that carbon emission reduction plans based on market incentives may make policy makers’ emission reduction goals deviate from farmers’ production goals, which in turn is detrimental to the government’s commitment to reduce land use change and agricultural GHG emissions (Carriquiry et al., 2020; Carauta et al., 2021).

In addition, the existing literature provides an extensive discussion on the effects of agriculture-related tax policies. Bawa and Williamson (2020) evaluate the impact of the U.S. Tax Cuts and Jobs Act (TCJA) on income distribution. They find that the TCJA reduces the tax system’s progressivity and has a higher revenue-raising effect on middle- and high-income farm households. By assessing the tax system in Serbia, Milosevic et al. (2020) find that an agricultural tax system based on organic production and tax incentives is conducive to achieving higher levels of sustainable agricultural production. Moreover, Buchholz and Musshoff (2021) find that pesticide taxation in Germany induces farmers to adjust their planting and farming strategies and thus achieve green agriculture. Meanwhile, a study conducted in Denmark came to a similar conclusion that pesticide taxation could promote green technological innovation in agricultural products (Pedersen et al., 2020). Besides, Moberg et al. (2021) argue that the imposition of food excise taxes in Sweden can reduce ecological pollution from agricultural production by restricting the expansion of agricultural land. In China, Shen et al. (2021) find that the progressivity of China’s tax system has increased after the abolition of agricultural taxes, dramatically improving rural residents’ social welfare. However, it is also observed that the abolition of agricultural taxes objectively exacerbated the fiscal pressure on local governments, causing them to turn to distort energy prices to cover fiscal deficits and further worsen energy efficiency (Jiang et al., 2022). Simultaneously caught in the fiscal pressure, local governments intensified their Value Added Tax (VAT) collection efforts after the agricultural tax abolishment, which in turn increases the operating costs of Small and medium-sized enterprises (SMEs) and private firms and negatively affects the welfare effects of workers (Li et al., 2021). Furthermore, Xu et al. (2020) compare the impact of soil N2O emissions on agricultural green total factor productivity (AGTFP) before and after agricultural tax reform and find that the impact of soil N2O emissions on AGTFP is more pronounced after 2006.

The above literature suggests that the current research results on the impact of public policies on agricultural carbon emissions and the effects of tax reform policies are relatively abundant, which helps to correctly understand the basic status, influencing factors, and mechanisms of agricultural carbon emissions, and also provides a solid theoretical foundation for the further development of agricultural carbon abatement mechanisms and institutional arrangements. However, even so, there are still shortcomings in the existing studies, which are mainly reflected in two aspects: first, most of the discussions in the current literature focus on the impact of agriculture-related tax policies on agricultural emissions in developed countries, and there is a lack of analysis on developing countries. Actually, developed countries have fully completed the industrialization and modernization transition, and the amount of agriculture-related tax revenues accounts for a relatively low proportion of the total tax revenue. In contrast, in developing or underdeveloped countries, the industrialization and modernization transition is still a work in progress, and the impact of agricultural tax revenues on the overall national fiscal revenues is conversely larger. Thus, the absence of existing literature on the abatement effect of agricultural tax policies in developing countries is not conducive to an in-depth insight into how developing countries can direct the greening of agriculture and rural development through fiscal policy reforms. Second, when discussing the effects of agriculture-related tax policies, the existing literature mainly analyzes the impact of tax policies on income distribution, enterprise behavior, farm household behavior, and energy efficiency. These studies lack a detailed discussion of agricultural tax reform effects’ on agricultural environmental governance, which ignores the direct policy objectives of agricultural tax reform and is not beneficial to conclude the lessons learned from agricultural tax reform on agricultural and rural environmental governance.

To compensate for the gaps in the existing literature, we construct a quasi-natural experiment with the RTFR implemented by the Chinese government in 2005 to evaluate the impact of RTFR on agricultural carbon emissions, by using a difference-in-differences with a continuous treatment (CDID) approach based on panel data of 31 provincial administrative regions in China from 2000 to 2019. Compared with the previous studies, the possible contributions of this paper include: first, based on the policy practice in China, we use the CDID method to assess the impact of RTFR on agricultural carbon emissions for the first time, which increases the reliability of the conclusions and addresses the gap in the existing literature regarding the impact of agricultural tax policy reform on agricultural environmental pollution in developing countries. Second, we discuss in detail the mechanism behind the effect of RTFR on agricultural carbon abatement in two dimensions: the subject of taxation (farmers) and the object of taxation (governments). This contributes to a deeper understanding of how tax system reform affects the behavior of farmers and governments, and thus provides lessons for developing countries to improve their agricultural carbon abatement mechanisms and institutional arrangements. Third, we provide a relatively comprehensive and systematic measurement framework for agricultural carbon emissions. The framework systematically evaluates China’s agricultural carbon emissions from three aspects: agricultural material inputs, agricultural cultivation, and crop growth. Compared with the lack of carbon emission measurement in tillage and crop growth (Guo et al., 2022; Li et al., 2022; Yang et al., 2022), our framework can reflect the actual situation of agricultural carbon emissions in China more objectively and comprehensively.

The remainder of this paper is organized as follows: Section 2 presents the institutional background and theoretical framework; Section 3 is the methodology, which focuses on this paper’s framework for measuring agricultural carbon emissions and the identification of causal relationships; Section 4 presents the main results, and shows the estimation results of robustness tests after reporting the benchmark regressions; Section 5 is the mechanism identification; Section 6 is the heterogeneity analysis; and Section 7 is the study conclusions, policy implications, and limitations.

The RTFR launched by the Chinese government at the beginning of the 21st century is another major historical event following the 1978 system of responsibility for the joint production of Chinese rural families. The reform completely terminates the exploitation of peasants in China’s traditional agricultural society, and accomplishes a historic institutional change unprecedented in more than 2,000 years. Launched in 2000 and finally completed by the end of 2005, the reform can be roughly divided into two stages according to the process of reform.

The period from 2000 to 2003 was the first phase of the RTFR (the rural fees reform phase), and the primary policy objective of this phase was to regulate the agricultural fees system and curb the rural fundamental government from charging peasants indiscriminately. In March 2000, the RTFR is first piloted in Anhui province. From 2001 to March 2003, the reform is gradually extended to Jiangsu, Shanghai, Zhejiang, Hebei Inner Mongolia, Jilin, Heilongjiang, Jiangxi, Shandong, Henan, Hubei, Hunan, Sichuan, Chongqing, Guizhou, Shaanxi, Gansu, Qinghai, Ningxia, and other 18 provincial administrative regions. The main contents of this phase include: (1) Abolishing public expenditure charges of countryside governments; abolishing rural education and other agricultural-related managerial fees and government funds; and abolishing the slaughter tax. (2) Adjusting the agricultural tax and agricultural special tax, and setting the upper limit of the agricultural tax rate at 7%. (3) Reforming the collection methods of the three public expenditure charges in rural communities, and gradually abolishing the labor accumulation employment and compulsory employment institutions for public affairs. Overall, the RTFR in this phase regulates the phenomenon of unreasonable fees and charges in rural China, leading to a significant decrease in the burden on peasants.

From 2004 to the end of 2005, the second phase of the RTFR, that is, the agricultural tax reform phase, the principal policy objectives of this phase are to gradually reduce the agricultural tax rate until the final abolishment, and to establish the corresponding supporting measures in the post-agricultural tax era. The major reform measures in this phase include: (1) In January 2004, the central government formally aborts the agricultural special tax except for the tobacco leaf tax at the national level. In March 2004, Heilongjiang and Jilin provinces took the lead in abolishing the agricultural tax. Meanwhile, the agricultural tax rate was reduced by three percentage points in 11 grain-producing provinces (districts), including Hebei, Inner Mongolia, Liaoning, Shandong, Jiangsu, Jiangxi, Anhui, Henan, Hubei, Hunan, and Sichuan; the agricultural tax rate is reduced by one percentage point in the remaining provinces. By the beginning of 2005, agricultural taxes are completely abolished in all provinces except for a few counties in Hebei, Shandong, and Yunnan, where agricultural taxes are still levied at a lower rate. On 29 December 2005, the central government announced that the agricultural tax would be officially abolished as of 1 January 2006, which means that the agricultural tax, which has existed in China’s rural areas for more than 2,000 years, has completely bid farewell to the historical stage, and China’s rural areas have ceremoniously entered the post-tax era. (2) In terms of supporting measures: In March 2004, the central government introduced direct production subsidies for grain farmers in 13 major grain-producing regions, and seed subsidies and agricultural machinery purchase subsidies for peasants in other regions. In 2005, the central government launched a nationwide policy of “two reductions and three subsidies”, which directly increased farmers’ income by about 45 billion yuan at the end of 2005. At the same time, since 2004, the central government has arranged special transfer payments for RTFR, mainly for farmland improvement and rural public infrastructure construction, which amounted to 52.4 billion yuan in that year, making up for the shortfall in fiscal expenditures of grassroots governments after the reform. On 1 January 2006, the Regulations of the People’s Republic of China on Agricultural Taxes, which had been in effect since 1958, were officially abolished, and the 6-year rural tax reform is finally completed.

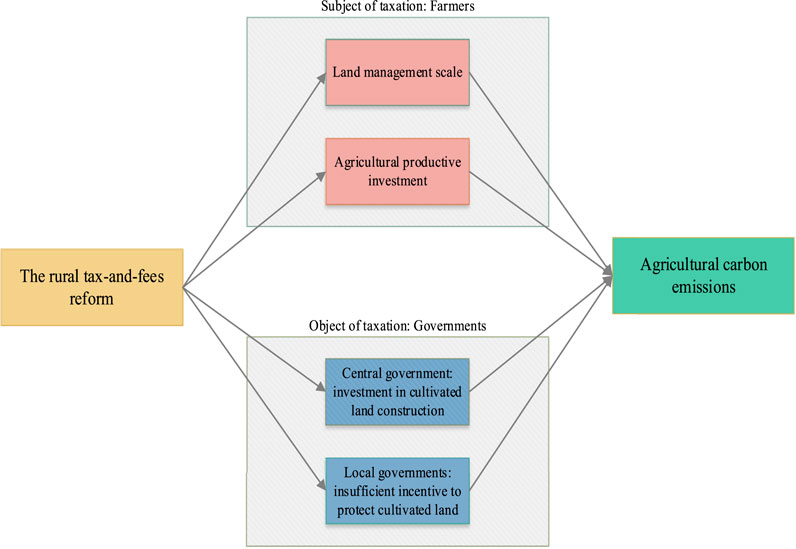

Generally speaking, the tax issue involves two aspects: the object of taxation, which is the taxpayer, is responsible for paying taxes, and the subject of taxation, which is usually the government, is responsible for collecting taxes (Hines and Keen, 2021; Hotak and Kaneko, 2022). Therefore, when studying the mechanism behind the effect of tax reform policy, we need to analyze both the object of taxation (farmers) and the subject of taxation (government). To visualize our analysis, Figure 1 gives the theoretical framework of this paper.

FIGURE 1. Framework for analyzing the agricultural carbon abatement effect of the RTFR in China.

Under the reality of China’s small-scale peasant economy, the inputs of production factors such as land, labor, and cultivated materials are highly fragmented in rural areas. Moderate scale management of agricultural land can obtain scale revenue through the expansion of land production scale, which can solve the problem of land fragmentation, to a certain extent, and promote the scale management of cultivated land (Liu et al., 2018). Meanwhile, it is also conducive to the large-scale use of agricultural machinery, pesticides, and fertilizers, reducing the waste caused by decentralized inputs, promoting agricultural intensification, and thus reducing pollution emissions and improving agricultural operation efficiency (Diao et al., 2018). Moreover, under market economy conditions, the free transfer of land will induce farmers with lower marginal land output to rent out their land to farmers with higher marginal output, which can improve the productivity of farmers in general, and thus achieve more agricultural output with the given factor inputs and realize energy saving and emission reduction (Liu et al., 2019; Chambers and Pieralli, 2020; Li et al., 2021). However, the orderly transfer of land is a prerequisite for the realization of large-scale management (Adamopoulos and Restuccia, 2020). Before the reform of rural tax-and-fees, farmers face burdens from both agricultural taxes and various non-tax forms of fees. In some areas, agricultural taxes are increased at various levels, and taxes are often apportioned according to the area of farmland, which makes the problem of increasing production without increasing income prominent. Under the heavy burden of taxes and fees, the comparative revenue of agriculture is low, and the long-term lack of investment in agriculture hinders the normal transfer of farmland and is not conducive to the expansion of operation scale. In addition, the impact of transaction cost, as a non-productive cost, on agricultural land transfer deserves attention (Gao et al., 2019). In the process of land transfer, the supply and demand sides need to conduct multiple rounds of negotiation on the burden of agricultural taxes and fees, which increases the transaction cost of land transfer and thus discourages the expansion of the land operation scale. Thus, after the rural taxes and fees reform, the burden of peasants is reduced, the transaction cost of farmland transfer is lowered, and the revenue of agricultural operation is relatively higher, which can increase the effective demand for farmland transfer, and then expand the scale of farmland operation, improve the efficiency of agricultural production, and reduce carbon emission. Accordingly, we propose hypothesis 1.

H1: Rural tax reform can achieve improvement in agricultural carbon emission performance by expanding the scale of farmland management.

Compared with traditional agriculture, modern agriculture can enhance agricultural production efficiency through the development of agricultural mechanization, the widespread application of pesticides and fertilizers, and the adoption of new cultivation techniques (Conradie et al., 2009; Guanziroli et al., 2013; McArthur and McCord, 2017). Empirically, traditional agriculture production cannot be achieved without labor input, while the sustainable development of modern agriculture depends on agricultural investment and the advancement of agricultural production technology (Chen, 2020; Mano et al., 2020). For agricultural investment, productive investment of peasant households can increase agricultural production efficiency and improve carbon emission performance by enhancing soil conservation, leveling arable land, and utilization of new technologies and production tools, thereby achieving more agricultural products output with given production inputs (Liu et al., 2020; Norton and Alwang, 2020). However, farmers’ productive investments are often influenced by factors such as returns on agricultural products, government policies, financial market conditions, and land institutions (Zhang and Fan, 2004; Kallas et al., 2012; Lecoutere and Jassogne, 2019; Czubak et al., 2021). Before the RTFR, the burden of taxes and fees, such as agricultural taxes, rural public expenditure fees, and compulsory labor, prevented the improvement of cultivated returns and discouraged farmers from accumulating wealth, which in turn inhibited the growth of productive investment. Meanwhile, before the reform, taxes and fees collection by grassroots governments is more subjective. Due to the pressure of fiscal expenditure, grassroots governments usually mix formal taxes and fees with miscellaneous fees and charges, resulting in strong policy uncertainty and poor predictability. Thus, under the pressure of highly uncertain taxes and fees, peasants are exposed to the risk of tax fluctuations and have to reduce their agricultural investments in order to secure their basic productive livelihood and tax needs, which in turn discourages the development of productive efficiency. After the rural reform, the tax burden disappears, and unreasonable taxes and fees are abolished. Under this condition, agricultural revenues increase and policy uncertainty decreases, which helps to strengthen farmers’ perception of security and increase expected revenues, thus stimulating their agricultural investment and hence increasing their agricultural productivity. In summary, we propose hypothesis 2.

H2: RTFR can improve agricultural carbon performance by increasing agricultural productive investment.

After the RTFR, the central government proceeded to establish a set of supporting reform measures corresponding to the reform. A series of reform initiatives increased transfer payments to counties and townships in financially difficult and impoverished areas, and increased support for infrastructure construction and social development while safeguarding the expenditures required by grassroots governments to perform their functions. Concerning the construction and protection of cultivatable land, the central government arranges special funds for the construction of farmland water conservancy, which improves the agricultural irrigation conditions in rural China. Meanwhile, through a series of institutional arrangements, the central government also implements fertile land projects and farmland standardization construction projects, and increases efforts to reclaim and organize land, improving the quality of arable land in rural China. Considering that irrigation and cultivation activities are essential sources of agricultural carbon emissions in China (Guo et al., 2022; Li et al., 2022; Yang et al., 2022), the treated arable land is more scientifically and rationally equipped with irrigation facilities and has a higher degree of cultivation standardization. As a result, the energy consumed for irrigation and tillage used to produce a unit area of crops is saved, which improves the efficiency of agricultural operations and contributes to the improvement of agricultural carbon performance (Kirmikil and Arici, 2013; Hong et al., 2019; Yuan et al., 2022). For this reason, we propose hypothesis 3.

H3: After the RTFR, the central government’s investment in agricultural cultivation governance can optimize the layout of field roads, irrigation facilities, and cultivated land, which in turn promotes cultivated operation efficiency and contributes to the enhancement of agricultural carbon performance.

As the direct beneficiaries of agricultural taxes, the behavior of local governments deserves special attention; after the 1994 tax-sharing reform, China’s taxes were divided into three categories: central taxes, local taxes, and shared taxes. The implementation of the tax-sharing system causes fiscal revenues to be tilted toward the central government and the share of local revenues to decline, but local governments still need to bear a large amount of public goods expenditures, leading to an increase in the gap between local government revenues and expenditures and an urgent need to find new sources of revenues to make up for the gap (Zhang, 2018; Ding et al., 2019). In addition, the lack of clear property rights of rural land leads to the absence of agricultural land owners, the deficiency of collective economic organizations, and the lack of land contracting rights of farmers, which puts rural land in a disadvantaged position compared to urban land on property rights (Hong and Sun, 2020; Wang and Tan, 2020). Therefore, under the fiscal decentralization system, local governments are more inclined to expropriate peasant collective land in the urban periphery to cover the financial gap (Xu, 2019). By character, agricultural tax is a local tax and shared tax, and is a crucial source of financial revenue for the grassroots government. After the abolition of agricultural tax, the tax revenue of local governments is significantly reduced. In the absence of tax incentives, it intensifies the tendency of local governments to expropriate agricultural land on the outskirts of cities in exchange for fiscal revenue (Li et al., 2010; Zeuthen, 2018). Under the constraints of The Land Management Law of the People’s Republic of China, the Chinese government implements a compensation system for the occupation of arable land. That is, the amount of arable land occupied by construction is to be supplemented by an equivalent amount and quality of arable land. However, in the process of rapid industrialization and urbanization, the preservation of arable land is increasingly regarded as a heavy political and financial burden by local governments. The problem of substandard compensation land for occupied arable land is widespread, which affects the quality of China’s arable land to a certain extent (Zhong et al., 2017; Yang et al., 2018; Shao et al., 2020). Thus, on arable land with relatively worse quality, peasants will adopt intensive farming methods and invest more fertilizers, farm materials, and cultivating labor to increase agricultural output per unit area, which objectively exacerbates agricultural carbon emissions and is not conducive to the improvement of agricultural carbon performance. Accordingly, this paper proposes hypothesis 4.

H4: After the RTFR, the incentive of local governments to protect cultivated land decreases, which affects the quality of arable land in China and is detrimental to the improvement of agricultural carbon performance.

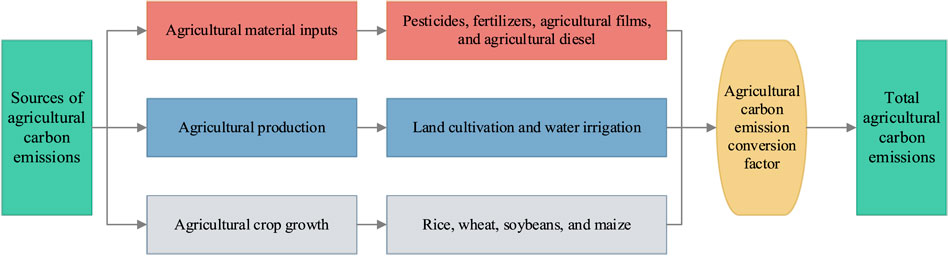

Based on the whole process of agricultural production, this paper measures China’s agricultural carbon emissions from three aspects: agriculture material input, agricultural production, and crop growth, by drawing on relevant studies (Zhang et al., 2019; Cui et al., 2021; Liu et al., 2021). The specific measurement framework is shown in Figure 2.

FIGURE 2. Measurement framework of agricultural carbon emissions in China.

In terms of agricultural material inputs, we specifically investigate the carbon emissions generated by pesticides, fertilizers, agricultural films, and agricultural diesel fuel during the production process of this product and its subsequent application, and the corresponding agricultural carbon emission factors refer to the literature of Liu et al. (2021) and Zhang et al. (2019). For agricultural production, we examine the carbon emissions from cultivation and irrigation activities. Agricultural cultivation disrupts the carbon fixation function of the soil, and organic carbon in the soil is lost to the air, resulting in carbon emissions. The irrigation process indirectly consumes fossil fuels such as oil, which also contributes to carbon emissions. The carbon emissions from these two agricultural production activities are derived from the study by Yang et al. (2022). Finally, there are methane and nitrous oxide emissions induced by the crop growth process. We calculate the carbon emissions formed during the growth of the four major staple grains (rice, wheat, corn, and soybean) in China, with specific carbon emission factors derived from the research of Tian et al. (2014) and Xiong et al. (2016). Based on this measurement framework, we calculate the agricultural carbon emissions of each provincial administrative region in China by employing the following equation.

Where

The difference-in-differences (DID) model is a classic approach to assess policy effects (Wu et al., 2021). The general idea is to consider an exogenous policy shock as a quasi-natural experiment and to divide the sample into treatment and control groups. Then, an economic variable to be analyzed is selected, and two sets of variables are obtained by making the first difference for that economic variable according to the time before and after the policy implementation, and the first difference eliminates individual heterogeneity. Next, a second difference is made between the two sets of variables to eliminate the effect of time variation on the estimation results, and finally, the net effect of policy implementation is obtained (Wang et al., 2022). However, because RTFR is a policy reform conducted at a national level, each individual is subject to policy intervention. Thus, to identify the impact of RTFR on the agricultural carbon performance, drawing on Chen (2017) and Perego (2019), we use the CDID model by dividing the “relative treatment group” and the “relative control group” to estimate the results, and the model is set up as follows.

where

Referring to the existing literature (Zhang et al., 2019; Wu et al., 2020; Liu et al., 2021; Guo et al., 2022), we select agricultural carbon intensity (

In the difference-in-differences model, the sample needs to be divided into treatment and control groups based on whether they are subject to policy intervention. However, in the RTFR, all provinces have been affected by policy shocks, and it is impossible to divide the “complete treatment group” and “complete control group”. For this reason, we draw on the analytical idea of existing studies (Chen, 2017; Perego, 2019; Jiang et al., 2022), and construct a CDID model to divide the “relative treatment group” and “relative control group” for policy assessment by using the output value of agriculture, forestry, animal husbandry, and fishery industries in 2004 as a proxy variable to measure the intensity of exogenous shocks to RTFR. The reason for using the 2004 agricultural, forestry, animal husbandry, and fishery output value as the basis for classification is that, first, the fees reform in 2000–2003 has already affected the agricultural output value in 2004, and therefore, using the 2004 output value as the criteria for measurement reflects the policy effect after the complete abolition of the agricultural tax in 2005, rather than the previous effect caused by the fees reform. Second, because agricultural production is constrained by natural conditions, the impact of economic factors on agricultural production is relatively minor, and the prices of agricultural products generally remain stable in the long run under the policy guidance of the Chinese government (Yu, 2014; Yang et al., 2017; Nigatu and Adjemian, 2020). Thus, expressing the treatment variables in terms of the 2004 agricultural output level can avoid the two-way causality of the treatment variables after the reform, and also avoid the endogeneity of agricultural taxation and economic characteristics variables. On this basis, we standardize the total output value of agriculture, forestry, animal husbandry, and fishery in 2004 to obtain the agricultural output intensity of each province (

Where

Taking reference from previous studies (Xiong et al., 2016; Zhang et al., 2019; Liu et al., 2021), we select the indicators related to economic and social development and agricultural production for each region as the control variables in this paper. The specific variables include regional gross domestic product, the proportion of secondary industry, the proportion of tertiary industry, the intensity of financial support to agriculture, crop cultivation area, agricultural mechanization level per unit area, fertilizer application intensity, disaster rate, and farmers’ per capita disposable income.

The data used in this paper are mainly from the China Statistical Yearbook, the China Rural Statistical Yearbook, the China Financial Yearbook, and the provincial database from the National Bureau of Statistics, as well as the statistical yearbooks and statistical bulletins of each province. The specifics and descriptive statistics of each variable are reported in Table 1.

TABLE 1. Descriptive statistics.

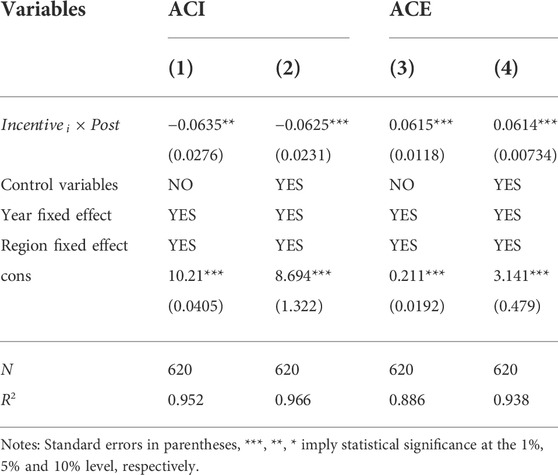

Table 2 reports the regression results of Eq. 2. In column (1), which includes only individual and time fixed effects, the coefficient of

TABLE 2. Baseline regression results.

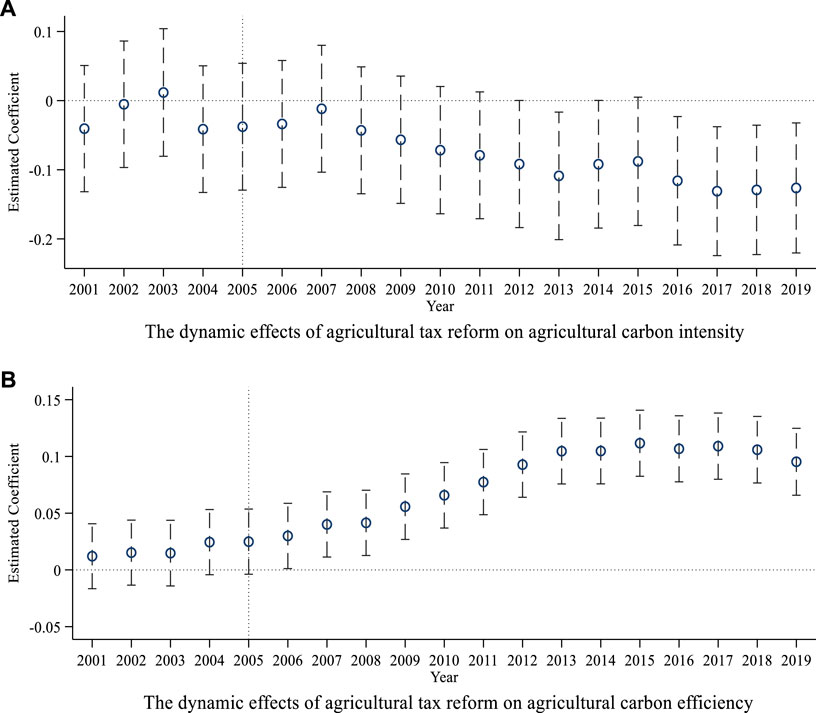

The prerequisite to enabling the validity of DID model estimation results is to satisfy the parallel trend assumption. That is, the dependent variables in the treatment and control groups have a common trend of change before the RTFR. To check the efficiency of the conclusions in this paper and to analyze the differences in the carbon reduction effects of RTFR at different time points, a dynamic effects analysis is conducted in this paper (Chunxiang et al., 2022), with the following model settings.

Where

FIGURE 3. Dynamic effects analysis.

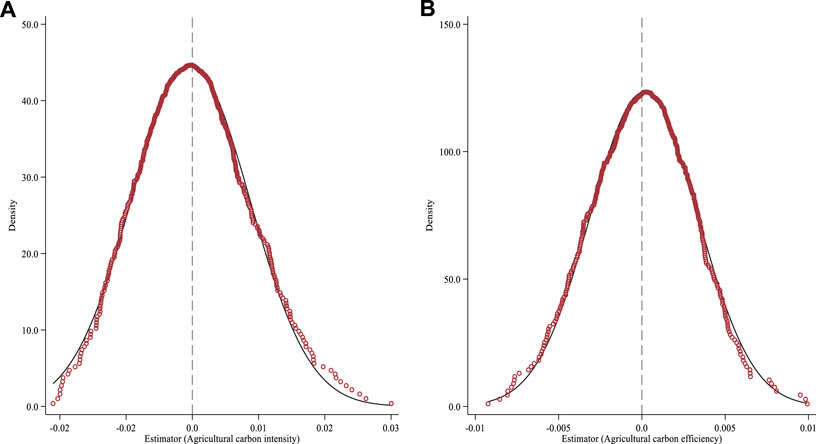

To further test whether the estimation results in this paper are affected by other unobservable factors or omitted variables, this paper refers to the idea of Cai et al. (2016) to randomly select the treatment group for a placebo test. Specifically, the province and the time when the reform started were randomly selected from the sample, and the multiplication of the two items was followed by the regression in Eq. 2, and the above operation is repeated 1,000 times. Figure 4 reports the results based on a placebo test for random selection in the context of agricultural carbon intensity and agricultural carbon efficiency as dependent variables, respectively. We observe that the coefficients of the multiplication terms are mostly concentrated around 0 and symmetrically distributed, indicating that the improvement in agricultural carbon efficiency is due to the RTFR and not due to other unobservable chance factors, and no important explanatory variables are omitted in Eq. 2.

FIGURE 4. Placebo test results.

Considering the endogeneity problem from reverse causality may produce biased estimation results. Hence, we further use the two-stage least squares (2SLS) method with the help of instrumental variables (IV) for robustness checking. Drawing on Nunn and Qian’s (2014) approach, we use the tobacco cultivation area in each province for 1999 as the IV for the RTFR, obtain the fitted value of the agricultural output intensity variable through the first stage in 2SLS, and regress this fitted value on the interaction term after the policy occurs as the independent variable of CDID to test the robustness of the estimated results for the abolition of agricultural tax in this paper.

The reason for selecting the tobacco cultivation area in each province for 1999 as the IV of agricultural output intensity is as follows. (1) The larger the tobacco cultivation area in a province in 1999, the smaller the impact of the agricultural tax abolition policy implemented by the central government on local government revenues (the 2005 rural tax reform did not abolish the tobacco cultivation tax), and the smaller the impact of the agricultural tax reform on local agricultural production, thus satisfying the correlation condition. (2) Since the area sown to tobacco does not account for a large proportion of the agricultural area in most provinces, and the existing literature does not include tobacco cultivation in the measurement system when calculating agricultural carbon emissions, the tobacco cultivation area is not relevant to the agricultural carbon emissions discussed in the vast majority of the literature and satisfies the exclusivity condition. Based on this, we believe that it is reasonable to choose the tobacco cultivation area by the province in 1999 as the IV for agricultural output intensity.

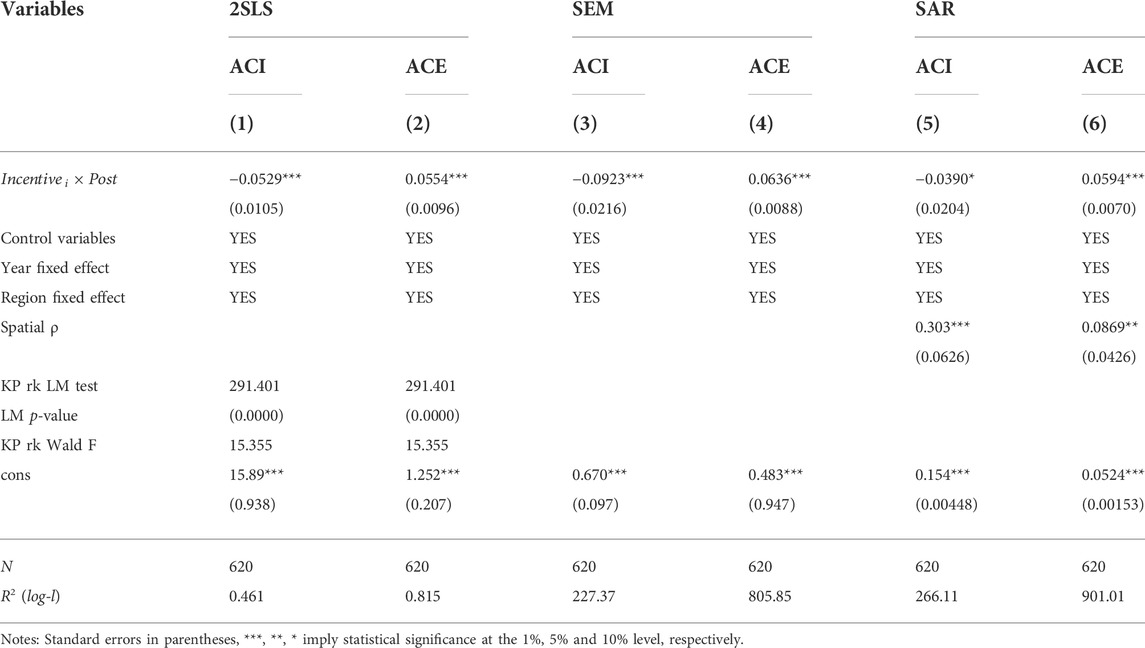

The estimated results of 2SLS are reported in columns (1) and (2) of Table 3. We find that the estimation results are still significant, and although there are changes compared to the results of the baseline regression, they are still in line with expectations. The results of the IV regression still show that there are still significant carbon-reducing effects of abolishing agricultural taxes, indicating that the results of the baseline regression are robust. Meanwhile, the KP rk LM test rejects the null hypothesis, implying that the IV chosen in this paper is reasonable, and the KP rk Wald F-statistic value is greater than 10, suggesting that there are no weak instrumental variables, which also confirms the reasonability of the IV in this paper.

TABLE 3. Robustness tests I.

Another prerequisite for obtaining valid estimation results by using the DID model is to satisfy the Stable Unit Treatment Value Assumption (SUTVA), but it is often infringed because of the existence spatial spillover effect (Delgado and Florax, 2015; Su et al., 2021). Existing studies show that agricultural carbon emissions have a strong spatial spillover effect, and agricultural production affects not only the agricultural carbon emissions in the region, but also those in the neighboring regions (Wu et al., 2019; Wu et al., 2021; Jia et al., 2022; Li and Li, 2022). Thus, any study that does not consider the spatial spillover effect may lead to an inappropriate evaluation of the policy effect (Zhang and Wu, 2022). Accordingly, we draw on Zhang and Wu’s (2022) research method and use a spatial difference-in-differences (SDID) model for robustness testing. Since the spatial correlation of agricultural carbon emissions may be captured by the error term and the auto regressive term relying on the variables (Wu et al., 2021), we use the SDID model based on the spatial error model (SEM) and the spatial auto regressive model (SAR) for robustness testing to overcome the estimation bias arising from ignoring the spatial spillover effect. The estimation results of the SDID model are reported in columns (3) to (6) of Table 3. The estimation results show that under different forms of spatial econometric model settings, the estimation results are still significant, and although there are variations, they are still consistent with the basic conclusions. Consequently, the fundamental findings of this paper still hold after controlling for spatial spillover effects.

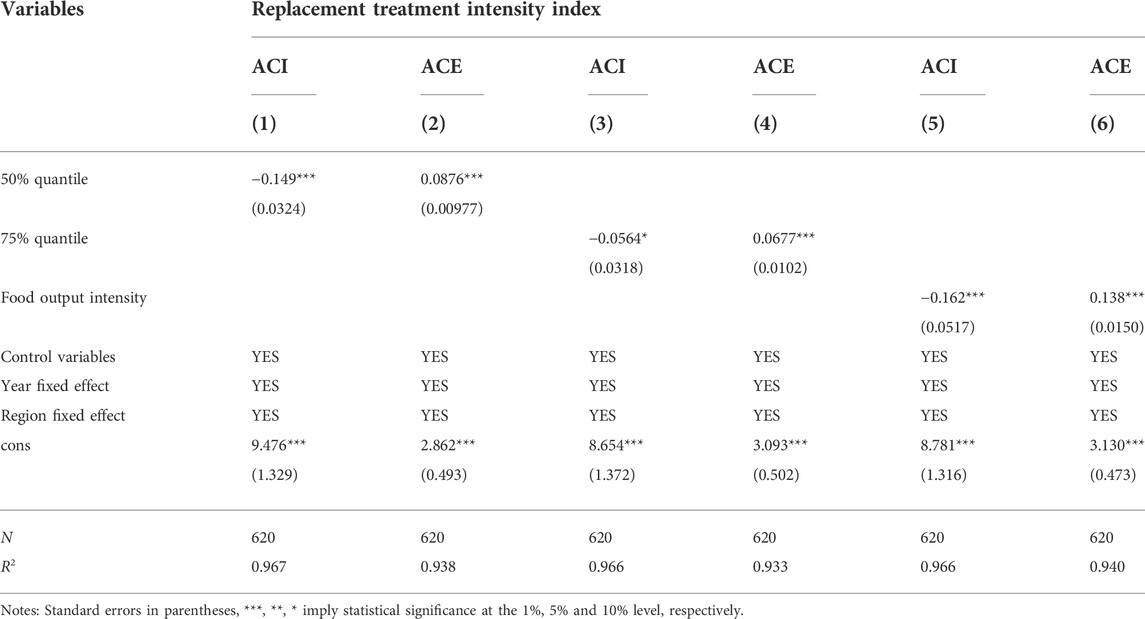

In the baseline regression section, we construct an indicator of agricultural output intensity based on the agricultural output value of each province in 2004, and multiply the agricultural output intensity and the time dummy variable indicating the occurrence of the policy as the independent variable in CDID model. In this section, we adopt two ways to change the independent variable in Eq. 2 and conduct robustness checks. First, the dummy variable

TABLE 4. Robustness tests II.

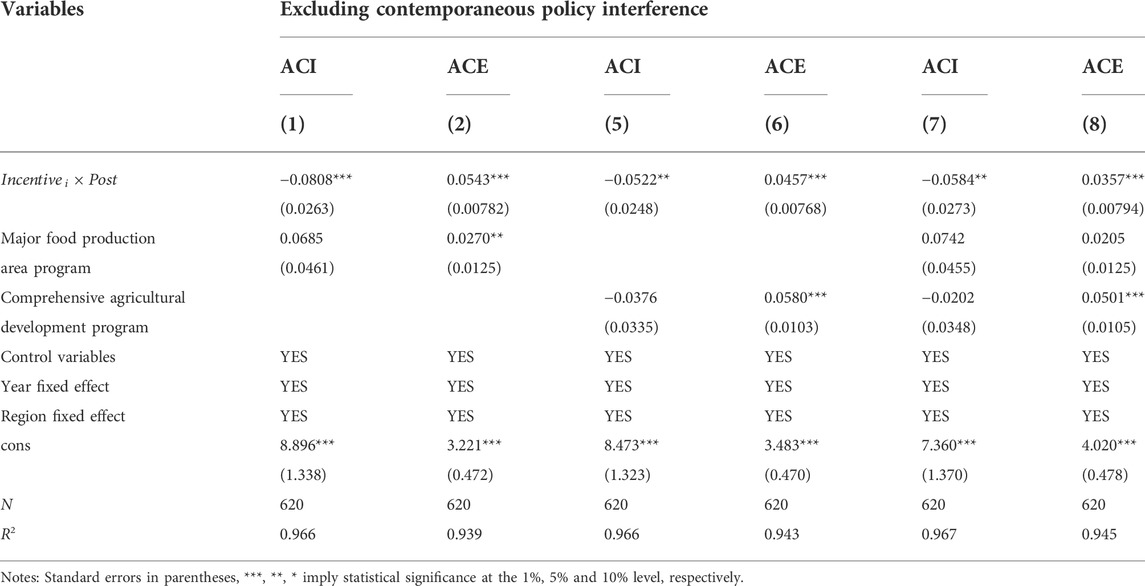

In 2003, the Chinese government began to implement the major food production areas (MFA) policy and designate 13 major food production areas nationwide to promote food production and ensure national food security. The logic of the MFA program’s impact on agricultural carbon emissions is that the MFA program can improve the scale and intensification of agricultural production through the specialized cultivation of large field crops, ameliorate the original scattered operation of small farmers, realize the large-scale application of pesticides, chemical fertilizers, and agricultural machinery, and promote the efficiency of tillage and irrigation, thus achieving the agricultural carbon emission abatement. To exclude the interference of the carbon reduction effect of the MFA project in the baseline regression results, a dummy variable indicating the MFA policy (the policy dummy variable takes the value of 1 for provinces belonging to the major food producing area and after the establishment of the MFA program, and 0 for the other cases) is added to Eq. 2 as a control variable for robustness check. The results in columns (1) and (2) of Table 5 show that the estimated coefficients of rural tax reform change slightly relative to the baseline regression results after controlling for the MFA program, but are still significant at the 5% level, indicating that the MFA program does not influence the conclusions over the same period.

TABLE 5. Excluding contemporaneous policy interference.

In 2011, the Chinese government began to implement the comprehensive agricultural development (CAD) program nationwide, aiming to ensure the quality of farmland and improve crop yields through scientific planning of farmland and construction of farmland infrastructure. On the one hand, the implementation of the CAD program can improve the agricultural scale operation efficiency by optimizing the input of agricultural labor, arable land, and agricultural materials, thus promoting the transformation of farmland into a whole and continuous operation, hence improving the agricultural operation efficiency. On the other hand, the CAD program can help improve land fertility and quality, increase agricultural production with the same agrarian material inputs, further improve cultivated scale management efficiency, and complete the agricultural carbon emission reduction. To exclude the influence of CAD program on the research conclusions, we multiply the investment amount of CAD program in each province as the intensity variable with the policy time dummy variable of the beginning CAD program, and introduce the regression in Eq. 2 again to test the reliability of the estimated results. The results are presented in columns (3) and (4) of Table 5. It can be seen that the estimated coefficients of RTFR are still significant, so the conclusions of this paper are not influenced by the CAD program.

Moreover, we also introduce the policy variables indicating the MFA program and the CAD program simultaneously into Eq. 2 for the regression. The results are presented in columns (5) and (6) of Table 5. We find that the estimated coefficients of RTFR are still significant. Thus, the conclusions of this paper are still very robust after controlling for policy interferences.

The empirical results in the previous section show that the implementation of RTFR has a significant abatement effect on agricultural carbon emissions. In the theoretical analysis section, we conclude that the carbon abatement effect of the reform can be realized through large-scale management, productive investment in agriculture, and financial support from the central government. However, the impact of tax-and-fees reform on local government revenues may reduce the importance of local governments on arable land protection, which in turn affects the carbon reduction effectiveness of the reform. Therefore, after confirming the reduction effect of RTFR on agricultural carbon emissions by using Eq. 2, to explore the transmission effect of the above potential mechanism, we further draw on the test approach proposed by Baron and Kenny (1986), to construct Eqs 5, 6 to perform a stepwise test for whether the mechanism holds (Wu et al., 2021) and to verify the validity of the theoretical hypothesis in this paper.

where

TABLE 6. Mechanism identification: farmer’s perspective.

TABLE 7. Mechanism identification: administration perspective.

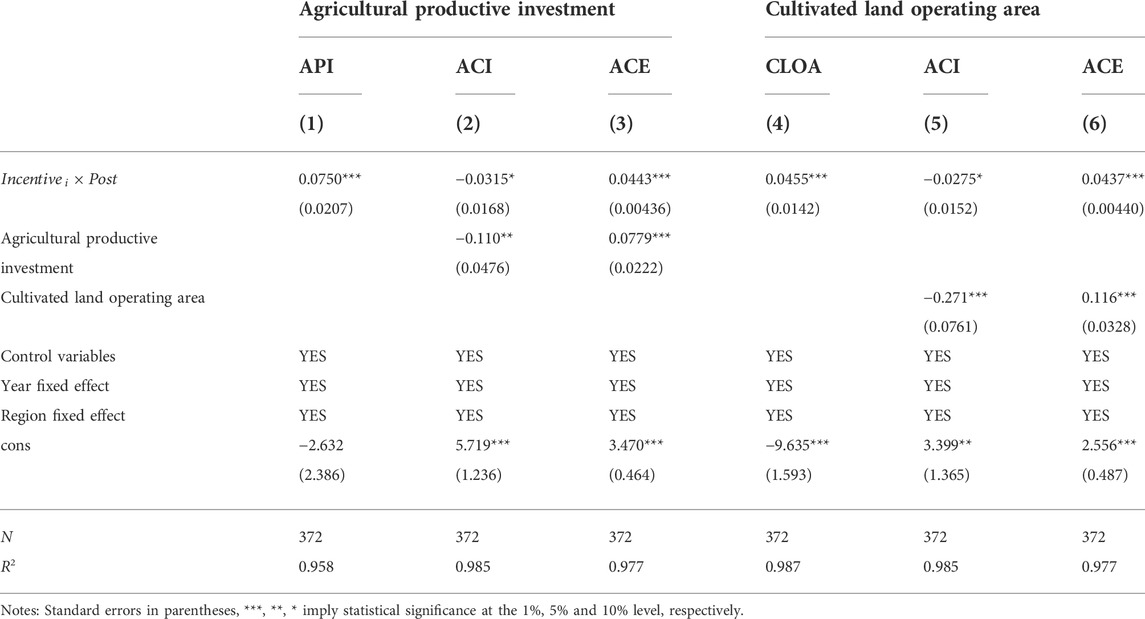

Columns (1) and (4) of Table 6 show the estimated results from the impact of RTFR on the farmers’ productive investment and the farmers’ cultivated operating area, respectively. The results show that the coefficient estimates of

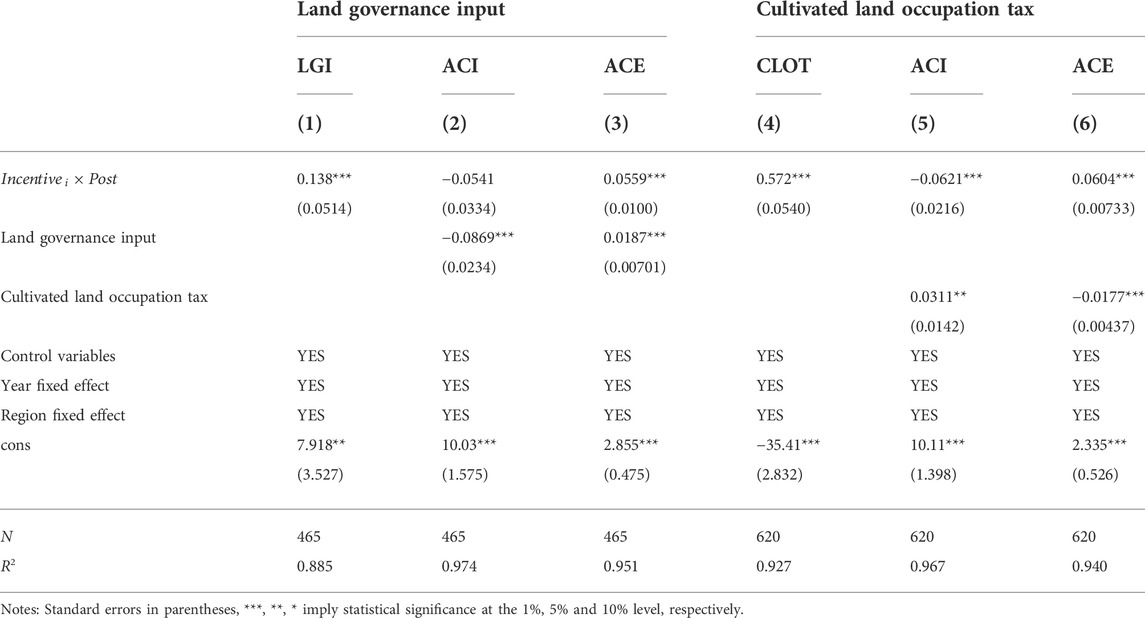

Table 7, columns (1) and (4) show the estimates of the effects for RTFR on central government land management inputs and local government cultivated land protection efforts, respectively. The results show that the coefficient estimates of

To verify the possible heterogeneity in the carbon reduction effect of RTFR in terms of crop type, geographic location, and topographic conditions, we construct a continuous difference-in-difference-differences (CDDD) model for examination. The model is set up as follows.

Where

TABLE 8. Heterogeneity analysis Ⅰ.

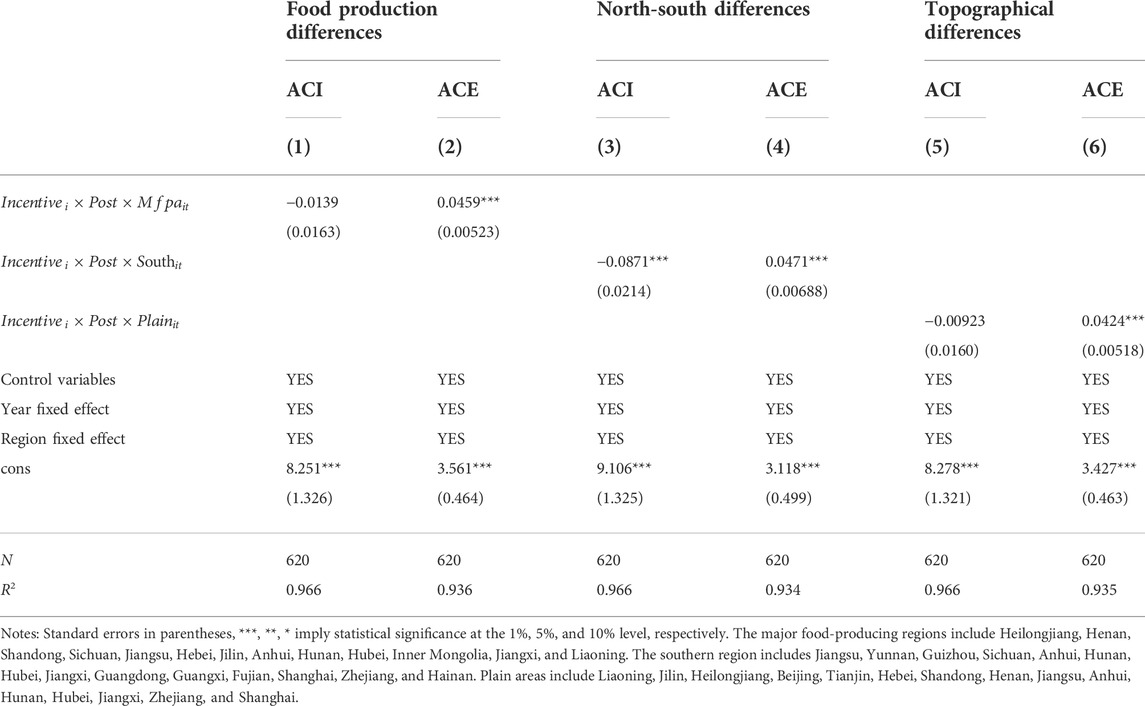

The results in columns (1) and (2) of Table 8 show that the estimated coefficients of the

The estimation results in columns (3) and (4) of Table 8 show that the estimated coefficients of

In terms of topographic conditions, the estimation results in columns (5) and (6) of Table 8 show that the coefficients of the

This paper also examines the possible heterogeneity of agricultural carbon emission sources. Based on the previous process of measuring agricultural carbon emissions, clearly, agricultural carbon emissions originate from three main sources: agricultural production, material inputs, and crop growth. In view of this, we further explore the impact of reform implementation on the agricultural carbon emissions generated from these three emission sources. The heterogeneity results are shown in Table 9. Among them, the RTFR has a significant inhibitory effect on agricultural carbon emissions from both agricultural production and material inputs. And the effects on carbon emissions from crop growth were not significant. Thus, the carbon abatement effect of RTFR is mainly realized through affecting agricultural production and material inputs, and has no significant effect on crop growth.

TABLE 9. Heterogeneity analysis Ⅱ.

In the context of Chinese society’s efforts to achieve the strategic goals of “carbon peaking” and “carbon neutrality”, it is significant to investigate the driving mechanisms and optimization strategies of agricultural carbon emission abatement. On the above basis, this paper treats the RTFR completed in 2005 as a quasi-natural experiment and examines the causal effects, potential mechanisms, and possible heterogeneity of the reform on agricultural carbon performance by employing a continuous difference-in-differences (CDID) model. The following conclusions are drawn.

First, the implementation of RTFR has a significant improvement on agricultural carbon performance, resulting in an average reduction of 6.35% in agricultural carbon intensity and an increase of 6.14% in agricultural carbon efficiency. Meanwhile, the results of the parallel trend test and dynamic effect analysis by event study method not only support the baseline findings but also indicate that the carbon reduction effect of tax and fee reform is persistent. Moreover, after conducting a series of robustness checks such as the placebo test, instrumental variables method, spatial effects analysis, replacing independent variables, and excluding other policy interferences, it is found that the carbon reduction effect of the reform on agriculture still holds. Second, the mechanism analysis indicates that the expansion of farmers’ arable land operation area, the increase in agricultural productive investment, and the rise of central government land governance transfer scale take the role of the channel in the process of agricultural carbon abatement effect of the tax-and-fees reform. However, the decline of local governments’ arable land protection is not conducive to the realization of the reform’s carbon reduction effect. Third, heterogeneity analysis demonstrates that RTFR can produce greater carbon abatement effects in southern regions, and can produce more significant policy effects on agricultural carbon efficiency in the major food-producing regions and plain areas. Meanwhile, the agricultural carbon reduction effect of reform implementation is mainly reflected in two aspects: reducing carbon emissions from agricultural production and agricultural materials.

From the above conclusions, this paper draws the following policy implications: First, agricultural tax is a common tax in developing countries, and the reduction of farmers’ tax burden is an important channel for agricultural carbon emission reduction. The agricultural tax abolition reduces farmers’ burden, promotes the transfer of agricultural land and productive agricultural investments, improves the agricultural operation efficiency, and provides a guarantee for the long-term and stable improvement of agricultural carbon performance. Countries around the world should take into account their national conditions, effectively reduce farmers’ burdens, strive to improve agricultural operation efficiency, and realize agricultural modernization. Second, the impact of the RTFR is heterogeneous in different regions, and countries around the world should formulate appropriate policies according to the climate, ecological environment, topographic conditions, and planting structure of each country when formulating agricultural policies, to avoid the negative consequences arising from unreasonable policy design. Third, the promotion effect of RTFR on agricultural carbon performance is mainly realized through mechanisms such as land transfer and inputs of production materials, so it is necessary to optimize the rural land system and guarantee farmers’ legitimate rights and interests to land, so that those who have constant production will have constant ownership. Fourth, the government is the primary driving force of the tax reform, and governments must have a clean and effective organizational system to complete the reform, dare to benefit the people, and take social responsibility. While maintaining social equity, it also promotes the further improvement of production efficiency. Therefore, in response to the climate change crisis, national governments should continuously optimize the organizational structure and improve organizational efficiency, to establish the institutional foundation for promoting rural agricultural modernization and achieving green and sustainable agriculture.

Lastly, there are some weaknesses in this study that deserve further improvement. First, in terms of data scale, this paper only investigates the impact of RTFR on agricultural carbon emissions at the provincial level, and does not analyze the impact of RTFR on agricultural carbon emissions at the municipal level and the county level. In fact, counties are the most important administrative units for agricultural production in China, and numerous agricultural activities are accomplished within the county. Therefore, in our future study, we will focus on the county level to identify the more elaborate policy effects of RTFR. Second, in terms of mechanism identification, it must be acknowledged that micro-individual data are more applicable to the investigation of land operation scale and agricultural inputs. However, due to the problem of data availability, micro mechanisms are not discussed in this paper. Thus, in the subsequent analytical study, we will conduct a series of field surveys to collect a batch of micro data to further enrich the study of the effect of RTFR on micro individuals.

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

Conceptualization, XZ; methodology, XZ; software, XZ and CW; validation, XZ and TL; formal analysis, XZ and CW; data curation, XZ, CW, and XL; writing—original draft preparation, XZ and XL; writing—review and editing, JW and XL; visualization, XZ, XL, and CW; supervision, CW and XL.

This research is Supported by the National Natural Science Foundation (No. 11701115).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Adamopoulos, T., and Restuccia, D. (2020). Land reform and productivity: A quantitative analysis with micro data. Am. Econ. J. Macroecon. 12, 1–39. doi:10.1257/mac.20150222

Akram-Lodhi, A. H., and Kay, C. (2010). Surveying the agrarian question (part 2): Current debates and beyond. J. Peasant Stud. 37, 255–284. doi:10.1080/03066151003594906

Baron, R. M., and Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. US: American Psychological Association, 1173–1182.

Bawa, S. G., and Williamson, J. M. (2020). Distributional impacts of the tax Cuts and Jobs Act using farm household microdata. Appl. Econ. Perspect. Policy 42, 835–855. doi:10.1093/aepp/ppz012

Buchholz, M., and Musshoff, O. (2021). Tax or green nudge? An experimental analysis of pesticide policies in Germany. Eur. Rev. Agric. Econ. 48, 940–982. doi:10.1093/erae/jbab019

Cabral, L., Pandey, P., and Xu, X. (2022). Epic narratives of the green revolution in Brazil, China, and India. Agric. Hum. Values 39, 249–267. doi:10.1007/s10460-021-10241-x

Cai, X., Lu, Y., Wu, M., and Yu, L. (2016). Does environmental regulation drive away inbound foreign direct investment? Evidence from a quasi-natural experiment in China. J. Dev. Econ. 123, 73–85. doi:10.1016/j.jdeveco.2016.08.003

Carauta, M., Troost, C., Guzman-Bustamante, I., Hampf, A., Libera, A., Meurer, K., et al. (2021). Climate-related land use policies in Brazil: How much has been achieved with economic incentives in agriculture? LAND USE POLICY 109, 105618. doi:10.1016/j.landusepol.2021.105618

Carriquiry, M., Elobeid, A., Dumortier, J., and Goodrich, R. (2020). Incorporating sub-national Brazilian agricultural production and land-use into US biofuel policy evaluation. Appl. Econ. Perspect. Policy 42, 497–523. doi:10.1093/aepp/ppy033

Chambers, R. G., and Pieralli, S. (2020). The sources of measured US agricultural productivity growth: Weather, technological change, and adaptation. Am. J. Agric. Econ. 102, 1198–1226. doi:10.1002/ajae.12090

Chang, J. (2022). The role of digital finance in reducing agricultural carbon emissions: Evidence from China's provincial panel data. Environ. Sci. Pollut. R.

Chen, C. (2020). Technology adoption, capital deepening, and international productivity differences. J. Dev. Econ. 143, 102388. doi:10.1016/j.jdeveco.2019.102388

Chen, K., Tian, G., Tian, Z., Ren, Y., and Liang, W. (2022). Evaluation of the coupled and coordinated relationship between agricultural modernization and regional economic development under the rural revitalization strategy. Agronomy-Basel 12, 990. doi:10.3390/agronomy12050990

Chen, S. X. (2017). The effect of a fiscal squeeze on tax enforcement: Evidence from a natural experiment in China. J. Public Econ. 147, 62–76. doi:10.1016/j.jpubeco.2017.01.001

Chen, X. (2009). Review of China's agricultural and rural development: Policy changes and current issues. China Agric. Econ. Rev. 1, 121–135. doi:10.1108/17561370910927390

Chunxiang, A., Shen, Y., and Zeng, Y. (2022). Dynamic asset-liability management problem in a continuous-time model with delay. Int. J. Control 95, 1315–1336. doi:10.1080/00207179.2020.1849807

Conradie, B., Piesse, J., and Thirtle, C. (2009). District-level total factor productivity in agriculture: Western cape province, south Africa, 1952-2002. Agric. Econ. 40, 265–280. doi:10.1111/j.1574-0862.2009.00381.x

Cui, X., Zhou, F., Ciais, P., Davidson, E. A., Tubiello, F. N., Niu, X., et al. (2021). Global mapping of crop-specific emission factors highlights hotspots of nitrous oxide mitigation. Nat. Food 2, 886–893. doi:10.1038/s43016-021-00384-9

Cui, Y., Khan, S. U., Deng, Y., Zhao, M., and Hou, M. (2021). Environmental improvement value of agricultural carbon reduction and its spatiotemporal dynamic evolution: Evidence from China. Sci. Total Environ. 754, 142170. doi:10.1016/j.scitotenv.2020.142170

Czubak, W., Pawlowski, K. P., and Sadowski, A. (2021). Outcomes of farm investment in Central and Eastern Europe: The role of financial public support and investment scale. LAND USE POLICY 108, 105655. doi:10.1016/j.landusepol.2021.105655

Delgado, M. S., and Florax, R. J. G. M. (2015). Difference-in-differences techniques for spatial data: Local autocorrelation and spatial interaction. Econ. Lett. 137, 123–126. doi:10.1016/j.econlet.2015.10.035

Diao, P., Zhang, Z., and Jin, Z. (2018). Dynamic and static analysis of agricultural productivity in China. CHINA Agr. Econ. Rev. 10, 293–312. doi:10.1108/caer-08-2015-0095

Ding, Y., McQuoid, A., and Karayalcin, C. (2019). Fiscal decentralization, fiscal reform, and economic growth in China. China Econ. Rev. 53, 152–167. doi:10.1016/j.chieco.2018.08.005

Falkowski, J. (2018). Together we stand, divided we fall? Smallholders' access to political power and their place in Poland's agricultural system. J. Agrar. Change 18, 893–903. doi:10.1111/joac.12278

Fei, R., Lin, Z., and Chunga, J. (2021). How land transfer affects agricultural land use efficiency: Evidence from China's agricultural sector. Land Use Policy 103, 105300. doi:10.1016/j.landusepol.2021.105300

Gao, L., Sun, D., and Ma, C. (2019). The impact of farmland transfers on agricultural investment in China: A perspective of transaction cost economics. China & World Econ. 27, 93–109. doi:10.1111/cwe.12269

Guanziroli, C., Buainain, A., and Sabbato, A. (2013). Family farming in Brazil: Evolution between the 1996 and 2006 agricultural censuses. J. Peasant Stud. 40, 817–843. doi:10.1080/03066150.2013.857179

Guo, L., Zhao, S., Song, Y., Tang, M., and Li, H. (2022). Green finance, chemical fertilizer use and carbon emissions from agricultural production. Agriculture-Basel 12, 313. doi:10.3390/agriculture12030313

Gurel, B. (2019). Semi-private landownership and capitalist agriculture in contemporary China. Rev. Radic. Polit. Econ. 51, 650–669. doi:10.1177/0486613419849683

Han, H., and Lin, H. (2021). Patterns of agricultural diversification in china and its policy implications for agricultural modernization. Int. J. Environ. Res. Public Health 18, 4978. doi:10.3390/ijerph18094978

Hines Jr, J. R., and Keen, M. J. (2021). Certain effects of random taxes. J. Public Econ. 203, 104412. doi:10.1016/j.jpubeco.2021.104412

Hong, C., Jin, X., Ren, J., Gu, Z., and Zhou, Y. (2019). Satellite data indicates multidimensional variation of agricultural production in land consolidation area. Sci. Total Environ. 653, 735–747. doi:10.1016/j.scitotenv.2018.10.415

Hong, Z., and Sun, Y. (2020). Power, capital, and the poverty of farmers’ land rights in China. Land Use Policy 92, 104471. doi:10.1016/j.landusepol.2020.104471

Hotak, N., and Kaneko, S. (2022). Fiscal illusion of the stated preferences of government officials regarding interministerial policy packages: A case study on child labor in Afghanistan. Econ. ANALYSIS POLICY 73, 285–298. doi:10.1016/j.eap.2021.11.019

Hou, X., Xu, C., Li, J., Liu, S., and Zhang, X. (2022). Evaluating agricultural tractors emissions using remote monitoring and emission tests in Beijing, China. Biosyst. Eng. 213, 105–118. doi:10.1016/j.biosystemseng.2021.11.017

Hua, J., Zhu, D., and Jia, Y. (2022). Research on the policy effect and mechanism of carbon emission trading on the total factor productivity of agricultural enterprises. Int. J. Environ. Res. Public Health 19, 7581. doi:10.3390/ijerph19137581

Huang, R., Zhang, S., and Wang, P. (2022). Key areas and pathways for carbon emissions reduction in Beijing for the “Dual Carbon” targets. Energy Policy 164, 112873. doi:10.1016/j.enpol.2022.112873

Huang, T., and Xiong, B. (2022). Space comparison of agricultural green growth in agricultural modernization: Scale and quality. Agriculture 12, 1067. AGRICULTURE-BASEL. doi:10.3390/agriculture12071067

Jia, R., Shao, S., and Yang, L. (2021). High-speed rail and CO2 emissions in urban China: A spatial difference-in-differences approach. Energy Econ. 99, 105271. doi:10.1016/j.eneco.2021.105271

Jia, S., Qiu, Y., and Yang, C. (2021). Sustainable development goals, financial inclusion, and grain security efficiency. Agronomy-Basel 11, 2542. doi:10.3390/agronomy11122542

Jia, S., Yang, C., Wang, M., and Failler, P. (2022). Heterogeneous impact of land-use on climate change: Study from a spatial perspective. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.840603

Jiang, W., Li, X., Liu, R., and Song, Y. (2022). Local fiscal pressure, policy distortion and energy efficiency: Micro-evidence from a quasi-natural experiment in China. Energy 254, 124287. doi:10.1016/j.energy.2022.124287

Kallas, Z., Serra, T., and Gil, J. M. (2012). Effects of policy instruments on farm investments and production decisions in the Spanish COP sector. Appl. Econ. 44, 3877–3886. doi:10.1080/00036846.2011.583220

Kirmikil, M., and Arici, I. (2013). The role of land consolidation in the development of rural areas in irrigation areas. J. FOOD Agric. Environ. 11, 1150–1155.

Kong, X., Su, L., Wang, H., and Qiu, H. (2022). Agricultural carbon footprint and food security: An assessment of multiple carbon mitigation strategies in China. China Agric. Econ. Rev. doi:10.1108/CAER-02-2022-0034

Lahiff, E., Borras, S. M., and Kay, C. (2007). Market-led agrarian reform: Policies, performance and prospects. Third World Q. 28, 1417–1436. doi:10.1080/01436590701637318

Lecoutere, E., and Jassogne, L. (2019). Fairness and efficiency in smallholder farming: The relation with intrahousehold decision-making. J. Dev. Stud. 55, 57–82. doi:10.1080/00220388.2017.1400014

Li, J., Wang, W., Li, M., Li, Q., Liu, Z., Chen, W., et al. 2022. Impact of land management scale on the carbon emissions of the planting industry in China. LAND 11.

Li, L., Liu, K. Z., Nie, Z., and Xi, T. (2021). Evading by any means? VAT enforcement and payroll tax evasion in China. J. Econ. Behav. Organ. 185, 770–784. doi:10.1016/j.jebo.2020.10.012

Li, S., and Sicular, T. (2014). The distribution of household income in China: Inequality, poverty and policies. China Q. 217, 1–41. doi:10.1017/s0305741014000290

Li, X., Liu, J., and Huo, X. (2021). Impacts of tenure security and market-oriented allocation of farmland on agricultural productivity: Evidence from China's apple growers. LAND USE POLICY 102, 105233. doi:10.1016/j.landusepol.2020.105233

Li, X., Xu, X., and Li, Z. (2010). Land property rights and urbanization in China. CHINA Rev. 10, 11–37.

Li, Z., and Li, J. (2022). The influence mechanism and spatial effect of carbon emission intensity in the agricultural sustainable supply: Evidence from China's grain production. Environ. Sci. Pollut. Res. 29, 44442–44460. doi:10.1007/s11356-022-18980-y

Lin, W., and Huang, J. (2021). Impacts of agricultural incentive policies on land rental prices: New evidence from China. FOOD POLICY 104, 102125. doi:10.1016/j.foodpol.2021.102125

Liu, D., Zhu, X., and Wang, Y. (2021). China's agricultural green total factor productivity based on carbon emission: An analysis of evolution trend and influencing factors. J. Clean. Prod. 278, 123692. doi:10.1016/j.jclepro.2020.123692

Liu, J., Dong, C., Liu, S., Rahman, S., and Sriboonchitta, S. (2020). Sources of total-factor productivity and efficiency changes in China's agriculture. Agriculture 10, 279. doi:10.3390/agriculture10070279

Liu, M., Xu, Z., Su, F., and Tao, R. (2012). Rural tax reform and the extractive capacity of local state in China. China Econ. Rev. 23, 190–203. doi:10.1016/j.chieco.2011.10.002

Liu, S., and Wang, B. (2022). The decline in agricultural share and agricultural industrialization-some stylized facts and theoretical explanations. CHINA Agr. Econ. Rev. 14, 469–493. doi:10.1108/caer-12-2021-0254

Liu, S., Wang, R., and Shi, G. (2018). Historical transformation of China's agriculture: Productivity changes and other key features. China & World Econ. 26, 42–65. doi:10.1111/cwe.12228

Liu, Y., Yan, B., Wang, Y., and Zhou, Y. (2019). Will land transfer always increase technical efficiency in China?-A land cost perspective. LAND USE POLICY 82, 414–421. doi:10.1016/j.landusepol.2018.12.002

Liu, Y., Ye, D., Liu, S., and Lan, H. (2022). The effect of China's leading officials' accountability audit of natural resources policy on provincial agricultural carbon intensities: The mediating role of technological progress. Environ. Sci. Pollut. R.

Liu, Z. A., and Zhuang, J. Z. (2000). Determinants of technical efficiency in post-collective Chinese agriculture: Evidence from farm-level data. J. Comp. Econ. 28, 545–564. doi:10.1006/jcec.2000.1666

Mamun, A., Martin, W., and Tokgoz, S. (2021). Reforming agricultural support for improved environmental outcomes. Appl. Econ. Perspect. Policy 43, 1520–1549. doi:10.1002/aepp.13141

Mano, Y., Takahashi, K., and Otsuka, K. (2020). Mechanization in land preparation and agricultural intensification: The case of rice farming in the Cote d'Ivoire. Agric. Econ. 51, 899–908. doi:10.1111/agec.12599

McArthur, J. W., and McCord, G. C. (2017). Fertilizing growth: Agricultural inputs and their effects in economic development. J. Dev. Econ. 127, 133–152. doi:10.1016/j.jdeveco.2017.02.007

Milosevic, G., Kulic, M., Duric, Z., and Duric, O. (2020). The taxation of agriculture in the republic of Serbia as a factor of development of organic agriculture. Sustainability 12, 3261. doi:10.3390/su12083261

Moberg, E., Sall, S., Hansson, P., and Roos, E. (2021). Taxing food consumption to reduce environmental impacts-Identification of synergies and goal conflicts. FOOD POLICY 101, 102090. doi:10.1016/j.foodpol.2021.102090

Munroe, D. (2001). Economic efficiency in Polish peasant farming: An international perspective. Reg. Stud. 35, 461–471. doi:10.1080/00343400123499

Nigatu, G., and Adjemian, M. (2020). A wavelet analysis of price integration in major agricultural markets. J. Agric. Appl. Econ. 52, 117–134. doi:10.1017/aae.2019.35

Norton, G. W., and Alwang, J. (2020). Changes in agricultural extension and implications for farmer adoption of new practices. Appl. Econ. Perspect. Policy 42, 8–20. doi:10.1002/aepp.13008

Nunn, N., and Qian, N. (2014). US food aid and civil conflict. Am. Econ. Rev. 104, 1630–1666. doi:10.1257/aer.104.6.1630

Pan, W., Kim, M., Ning, Z., and Yang, H. (2020). Carbon leakage in energy/forest sectors and climate policy implications using meta-analysis. For. Policy Econ. 115, 102161. doi:10.1016/j.forpol.2020.102161

Pedersen, A. B., Nielsen, H. O., and Daugbjerg, C. (2020). Environmental policy mixes and target group heterogeneity: Analysing Danish farmers' responses to the pesticide taxes. J. Environ. Policy & Plan. 22, 608–619. doi:10.1080/1523908x.2020.1806047

Perego, V. M. E. (2019). Crop prices and the demand for titled land: Evidence from Uganda. J. Dev. Econ. 137, 93–109. doi:10.1016/j.jdeveco.2018.11.007

Rymanov, A. (2017). Differential land rent and agricultural taxation. Agric. Econ. 63, 421–429. doi:10.17221/127/2016-agricecon

Shao, Z., Xu, J., Chung, C. K. L., Spit, T., and Wu, Q. (2020). The state as both regulator and player: The politics of transfer of development rights in China. Int. J. Urban Reg. Res. 44, 38–54. doi:10.1111/1468-2427.12843

Shen, Y., Li, S., and Wang, X. (2021). Impacts of two tax reforms on inequality and welfare in China. China & World Econ. 29, 104–134. doi:10.1111/cwe.12377

Su, Y., Li, Z., and Yang, C. (2021). Spatial interaction spillover effects between digital financial technology and urban ecological efficiency in china: An empirical study based on spatial simultaneous equations. Int. J. Environ. Res. Public Health 18, 8535. doi:10.3390/ijerph18168535

Tao, R., and Qin, P. (2007). How has rural tax reform affected farmers and local governance in China? China World Econ. 15, 19–32. doi:10.1111/j.1749-124x.2007.00066.x

Tian, Y., Zhang, J., and He, Y. (2014). Research on spatial-temporal characteristics and driving factor of agricultural carbon emissions in China. J. Integr. Agric. 13, 1393–1403. doi:10.1016/s2095-3119(13)60624-3

Wang, B., Yu, M., Zhu, Y., and Bao, P. (2021). Unveiling the driving factors of carbon emissions from industrial resource allocation in China: A spatial econometric perspective. Energy Policy 158, 112557. doi:10.1016/j.enpol.2021.112557

Wang, C. A., Liu, X. Q., Xi, Q., and Zhang, Y. (2022). The impact of emissions trading program on the labor demand of enterprises: Evidence from China. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.872248

Wang, G. (2019). Principle-guided policy experimentation in China: From rural tax and fee reform to hu and wen's abolition of agricultural tax. China Q. 237, 38–57. doi:10.1017/s0305741018001224

Wang, R., and Tan, R. (2020). Patterns of revenue distribution in rural residential land consolidation in contemporary China: The perspective of property rights delineation. LAND USE POLICY 97, 104742. doi:10.1016/j.landusepol.2020.104742

Wang, X., and Shen, Y. (2014). The effect of China's agricultural tax abolition on rural families' incomes and production. China Econ. Rev. 29, 185–199. doi:10.1016/j.chieco.2014.04.010

Wu, G., Xie, Y., Li, H., and Riaz, N. (2022). Agricultural ecological efficiency under the carbon emissions trading system in China: A spatial difference-in-difference approach. Sustainability 14, 4707. doi:10.3390/su14084707

Wu, H., Hao, Y., and Ren, S. (2020). How do environmental regulation and environmental decentralization affect green total factor energy efficiency: Evidence from China. Energy Econ. 91, 104880. doi:10.1016/j.eneco.2020.104880

Wu, H., Huang, H., Tang, J., Chen, W., and He, Y. (2019). Net greenhouse gas emissions from agriculture in China: Estimation, spatial correlation and convergence. Sustainability 11, 4817. doi:10.3390/su11184817

Wu, H., Sipilainen, T., He, Y., Huang, H., Luo, L., Chen, W., et al. (2021). Performance of cropland low-carbon use in China: Measurement, spatiotemporal characteristics, and driving factors. Sci. Total Environ. 800, 149552. doi:10.1016/j.scitotenv.2021.149552

Wu, H., Xia, Y., Yang, X., Hao, Y., and Ren, S. (2021). Does environmental pollution promote China's crime rate? A new perspective through government official corruption. Struct. Chang. Econ. Dyn. 57, 292–307. doi:10.1016/j.strueco.2021.04.006

Wu, H., Xue, Y., Hao, Y., and Ren, S. (2021). How does internet development affect energy-saving and emission reduction? Evidence from China. Energy Econ. 103, 105577. doi:10.1016/j.eneco.2021.105577

Xiong, C., Yang, D., Xia, F., and Huo, J. (2016). Changes in agricultural carbon emissions and factors that influence agricultural carbon emissions based on different stages in Xinjiang. China. Sci. Rep. 6, 1–10. doi:10.1038/srep36912

Xu, D., Ma, Z., Deng, X., Liu, Y., Huang, K., Zhou, W., et al. 2020. Relationships between land management scale and livelihood strategy selection of rural households in China from the perspective of family life cycle. LAND 9.

Xu, G., Li, J., Schwarz, P. M., Yang, H., and Chang, H. (2022). Rural financial development and achieving an agricultural carbon emissions peak: An empirical analysis of henan province, China. Environ. Dev. Sustain. doi:10.1007/s10668-021-01976-y

Xu, H., Zhu, S., and Shi, H. (2022). Is it possible to reduce agricultural carbon emissions through more efficient irrigation: Empirical evidence from China. Water 14, 1218. doi:10.3390/w14081218

Xu, N. (2019). What gave rise to China's land finance? LAND USE POLICY 87, 104015. doi:10.1016/j.landusepol.2019.05.034

Xu, X., Zhang, L., Chen, L., and Liu, C. (2020). The role of soil N2O emissions in agricultural green total factor productivity: An empirical study from China around 2006 when agricultural tax was abolished. Agriculture 10, 150. doi:10.3390/agriculture10050150