Fengjiao Long1,2

Fengjiao Long1,2 Qin Chen

Qin Chen Lu Xu

Lu Xu László Vasa

László Vasa- 1College of Economics and Management, Fujian Agriculture and Forestry University, Fuzhou, China

- 2Department of International Business, Fuzhou Melbourne Polytechnic, Fuzhou, China

- School of Economics, Fujian Normal University, Fuzhou, China

- 4School of Economics, Lanzhou University, Lanzhou, China

- 5School of Economics, Széchenyi István University, Győr, Hungary

For a greener society, good corporate environmental information disclosure is crucial. This study empirically examines the influence of media attention and state-owned equity, and their interaction on corporate environmental information disclosure by A-share heavily polluting firms in the Shanghai and Shenzhen stock markets from 2015 to 2019. The results show that state-owned equity can improve the level of corporate environmental information disclosure; however, it mainly affects financial environmental information disclosure. Media attention also improves the level of corporate environmental information disclosure, but only for non-financial environmental information. Moreover, media attention and state-owned equity have a certain substitution effect on environmental information disclosure: a higher state-owned equity ratio weakens the positive effect of media attention on environmental information disclosure. To improve environmental information disclosure, the government must clarify disclosure standards to improve the comparability of environmental information. In addition, media and shareholders can fully leverage their external and internal supervisory roles to promote the environmental responsibilities of firms. Our findings can be useful for further promoting corporate environmental information disclosure and developing relevant policies.

1 Introduction

In recent years, constructing a greener and ecologically sustainable civilization has become even more important. Given tightening resource constraints, serious environmental pollution, and ecosystem degradation, we must adhere to the basic policy of conserving resources and protecting the ecological environment, and build an environmental governance system in which the government plays the leading role and firms perform the major role with the participation of the public (Yang et al., 2020). As market entities, firms play an important role in the construction of an ecological civilization, and should actively fulfill their environmental responsibilities and disclose their performance on time.

According to the Evaluation Report on Environmental Responsibility Disclosure of Chinese Listed Companies (2020), only 1,135 of the 4,418 companies listed in the Shanghai and Shenzhen stock markets in 2020 had issued social responsibility or environmental reports. Regarding the disclosure level, the average index of environmental disclosure was 36.4 out of 100; this shows that there is still much room for improvement in corporate environmental disclosure. Regarding the disclosure content, it currently includes financial environmental information, such as emission amount and environmental protection expenditures, as well as non-financial environmental information, such as corporate environmental system and environmental management objectives, indicating that the specific content of environmental information varies significantly among different firms (Wu et al., 2015). Regarding the disclosure channels, firms disclose their environmental performance through official websites, environmental responsibility or sustainable development reports, or annual reports.

However, due to the lack of a clear environmental disclosure framework in China, the environmental information disclosed by firms is not comparable. Furthermore, firms’ opportunistic behavior regarding environmental responsibility is not conducive to the acquisition of real information by shareholders, creditors, and potential investors (Radu and Francoeur, 2017). Therefore, effectively improving corporate environmental disclosure is an urgent issue. The extant literature has examined a comprehensive list of factors that influence corporate environmental information disclosure. However, the combined effect of these factors did not receive enough attention. Moreover, the content of the disclosure was not distinguished, leading to biased results. Focusing on heavily polluting firms, this study examines the influence of media attention and state-owned equity on corporate environmental disclosure and their interaction effect. The possible contributions of this study are that we examine: 1) the heterogeneity of the impact of media attention and state-owned equity, as different supervision mechanisms, on corporate environmental information disclosure; and 2) the interaction effect of media attention and state-owned equity on environmental information disclosure.

The remainder of this study is arranged as follows. Section 2 is devoted to the literature review. Section 3 details the theoretical analysis and research hypotheses. Section 4 describes the data source, explains the variable design, and introduces the model. Section 5 outlines the empirical results. Section 6 presents the conclusions, while Section 7 proposes the suggestions.

2 Literature review

Regarding voluntary disclosure of environmental information, an important area of concern is the motivation for corporate environmental information disclosure. These motivations can be divided into internal and external factors. Internal factors include corporate scale, corporate growth, financial leverage, profitability, nature of property rights, corporate governance, and corporate culture, etc. First, let us consider scale and operational factors. Large-scale companies are more active in environmental responsibility efforts and have a higher quality of environmental information disclosure (Lee, 2017). Profitable firms have more environmental governance capital, and thus, are more capable of providing a high level of environmental information disclosure (Qiu et al., 2016). However, some studies find that firms with poor business performance are more inclined to disclose environmental information with no substantive content in order to make up the numbers (Baldini et al., 2018). Firms with high leverage also tend to disclose high-quality environmental information in order to reduce information asymmetry and capital cost (Park and Peng, 2013).

Second, there is the firm’s corporate governance. Firms’ environmental behaviors can differ depending on the nature of their property rights. For example, compared with private firms, state-owned firms may proactively undertake corporate environmental behaviors (Acar et al., 2021). Ownership concentration is negatively correlated with corporate environmental information disclosure, indicating that majority shareholders and management generally lack the enthusiasm to undertake environmental governance (Chen et al., 2021). In addition, under pressure from public shareholders, companies with a higher proportion of institutional investors will tend to disclose high-quality environmental information to meet the needs of shareholders (D'Amico et al., 2016). Other corporate governance factors like board size and proportion of independent directors are also positively correlated with environmental information disclosure, indicating that good internal governance improves corporate transparency (Liu and Zhang, 2017). Finally, experienced managers can make flexible judgments regarding environmental management, and their environmental information disclosures are also of higher quality (Ma et al., 2019).

Next, external factors include regulatory policies, media attention, industry characteristics, and market competitiveness, among others. Regulatory policies tend to pressure firms to comply with regulations; these firms are more inclined to disclose high-quality environmental information (Barbu et al., 2014; Liu et al., 2021). Firms in developed regions are more active in disclosing environmental information due to stricter regulatory measures (Park and Peng, 2013). Media attention will also bring public pressure on firms; under this pressure, firms are more inclined to disclose environmental information to maintain their reputation (Brammer and Pavelin, 2008; Moroney et al., 2012; Rupley et al., 2012; Meng et al., 2019). In addition, disclosures may vary by industry and market competition. For example, firms in environmentally sensitive industries tend to disclose more environmental information to meet investors′ demands (Lu and Abeysekera, 2014); meanwhile, firms experiencing medium competitive intensity disclose more detailed environmental information to distinguish themselves from their competitors (Delgado-Márquez et al., 2017).

In China’s practice, in order to strengthen environmental information disclosure, a series of laws and regulations have been introduced, such as the Guidelines for Environmental Information Disclosure of Listed Companies. These regulations put forward specific requirements for listed companies to accurately, timely, and completely disclose environmental information. Under legal pressure, the number of firms that disclose environmental information has increased, but the quality of their disclosures has not been satisfactory. The disclosures are selective and self-serving: positive and descriptive information that is difficult to verify is quite common, while negative, numerical information is relatively scarce (Xu et al., 2021). When studying the impact of corporate social responsibility (CSR) on corporate performance, Bhattacharyy and Rahman (2019) verified that mandatory laws are an important but not the only determinant of CSR fulfillment (Bhattacharyya and Rahman, 2019). Li (2018) found that environmental information disclosure is widely characterized by “too much expression of strategic planning” and “too little actual practice information”. Those firms are better at self-packaging and exaggerating environmental information disclosure (Li, 2018). Clarkson et al. (2008) pointed out that the research on environmental information disclosure should shift from pure level of disclosure to specific content of disclosure. The empirical research results of Acar and Temiz. (2020) showed that the quality of environmental information disclosed by Chinese enterprises is unsatisfactory. It is impossible to distinguish a firm’s environmental performance simply through general environmental information disclosure. Therefore, it is necessary to distinguish the content of environmental information.

As we can see, the extant literature has examined a comprehensive list of factors that influence environmental information disclosure. Here, we focus on state-owned equity and media attention. Some scholars have analyzed the influence of these two factors on environmental information disclosure. However, these studies failed to consider the combined effect of both factors on environmental information disclosure and did not distinguish the specific content of the disclosed information. On the one hand, as an external supervision mechanism, media plays an important role in the capital market. The media transmits the operational status of firms to the outside world by disseminating information and influences firms’ behavior through the reputation mechanism. Media supervision can promote firms to fulfill their environmental responsibilities better. On the other hand, as government representatives, state-owned firms undertake more environmental responsibilities than non-state-owned ones. The former pay more attention to environmental performance in their operations and tend to promote corporate environmental information disclosure through corporate governance. Thus, media attention and state-owned equity play the roles of external and internal supervision mechanisms, respectively; this can improve the level of corporate environmental information disclosure. Essentially, we ask whether there are differences in the content of environmental information disclosures? Further, what is the interaction effect between media attention and state-owned equity on environmental information disclosure?

To examine these issues, this study distinguished the specific content of environmental information. It tested the impact of media attention, state-owned equity, and their interaction effect on the environmental information disclosure of A-share heavily polluting firms in the Shanghai and Shenzhen stock markets from 2015 to 2019. This study aims to examine: 1) the impact of media attention and state-owned equity, as different supervision mechanisms, on corporate environmental information disclosure; and 2) the interaction effect of media attention and state-owned equity on environmental information disclosure. The results of this paper not only supplement the existing literature but also provide policy support for promoting firms to fulfill their environmental responsibility better.

3 Research hypotheses

While pursuing economic interests, firms also shoulder the social responsibility of protecting the environment. Under information asymmetry, media attention can act as an informal external governance mechanism. Further, it can help in effectively supervising firm behavior and even force firms to fulfill their social responsibilities. As their reputation hinges on it, firms convey good news to the market through the appropriate disclosure of environmental information; this helps establish their positive image as a firm with a good environmental management system.

Indeed, Kuo and chen, (2013) found that the public learned about firms’ environmental systems and their implementation mainly through environmental news. The authors noted that as the primary way of information acquisition, media affected corporate image; consequently, voluntary disclosure of environmental information by firms in social responsibility reports is conducive to improving their social status. Aerts et al. (2008) also showed that firms with high media attention feel pressured by public opinion. Again, the authors found that firms are more proactive in disclosing environmental information to gain social recognition. Notably, the number of ex-post reports on environmental information significantly impacts corporate environmental information disclosures more than prior reports. Using samples of environmentally sensitive industries, Zhou et al. (2022) confirmed that increased community pressure is negatively associated with corporate pollution levels, and thus, positively associated with corporate environmental performance. Kong et al. (2020) reviewed the literature and pointed out that media attention induces firms to exert more effort on environmental protection, especially when there are adverse media reports. Xue et al. (2021) empirically found that both media attention and government regulation were significantly positively correlated with environmental information disclosure; notably, the more adverse the effect of government regulation, the more media attention promotes environmental information disclosure. Based on the above analysis, we propose the following hypothesis:

Hypothesis 1: Media attention has a positive impact on corporate environmental information disclosure.

Shareholders can significantly affect a firm’s behavior. Intuitively, controlling shareholders can positively affect firm performance and operational efficiency commitment to environmental friendliness (Utomo et al., 2018). Interestingly, some studies report that the shareholding ratio of state-owned shareholders is correlated with company performance (Lin et al., 2020). Specifically, compared with non-state-owned firms, state-owned firms must undertake more environmental protection efforts on behalf of their country and society because of their particular political status, and consider political, social, and economic interests.

Furthermore, state-owned enterprises themselves have high social attention. Under the pressure of social supervision, they can play an exemplary role in environmental information disclosure. Zhang et al. (2022) found that CSR activities improve when the proportion of state-owned capital in a private-holding listed company exceeds 5%. Using a sample of 140 countries, Mahjoub and Amara (2020) confirmed a notable positive effect of shareholder governance on environmental sustainability. Calza et al. (2016) found a positive correlation between firms’ performance on environmental activities and their state ownership percentage. Specifically, compared with non-state-owned firms, state-owned firms performed better on environmental responsibility.

Therefore, state-owned equity can have a “governance effect”; the higher the proportion of state-owned equity, the higher the degree of government participation in corporate governance and the higher the level of environmental information disclosure of firms. Data from China Listed Companies′ Environmental Responsibility Information Disclosure Evaluation Report (2020) showed that the level of environmental information disclosure of state-owned firms is much higher than that of non-state-owned firms. Based on the above analysis, we propose our second hypothesis:

Hypothesis 2: State-owned equity has a positive impact on corporate environmental information disclosure.

As argued before, both media attention and state-owned equity can help govern firms’ environmental behavior externally and internally, respectively. However, the effects of these two factors may be substitutable. When the proportion of state-owned equity is low, its internal influence on firm governance will be low, and information asymmetry and agency problems will be prominent; this may trigger other alternative mechanisms to supervise corporate behavior. Then, as an important form of informal governance and extra-legal system, media attention can replace the supervisory function of state-owned equity and address weak corporate governance.

Huang et al. (2020) confirmed that media attention and state-owned equity have a substitution effect on firms’ targeted poverty alleviation behavior. For firms with low degree of state-owned equity, media attention has a more significant impact on firms’ willingness to participate in targeted poverty alleviation efforts. Yang et al. (2020) noted that under media attention, non-state-owned firms are more active in disclosing environmental information. Guo and Lu (2020) observed that the impact of media on corporate environmental performance is more obvious in areas where the government pays less attention to environmental protection; however, in other areas, this impact is not clear.

In summary, compared with firms with high state-owned equity, those with low state-owned equity have less environmental supervision from state-backed shareholders and are more likely to commit environmental violations and attract media attention. Then, under the pressure of public opinion, firms are urged to disclose more environmental information to recover their reputation losses. Meanwhile, for firms with high state-owned equity, government pressure will promote corporate environmental information disclosure and there may be fewer chances for media to exert their external governance function. Based on this, we propose our third and final hypothesis:

Hypothesis 3: There is a substitution relationship between state-owned equity and media attention on the impact of environmental information disclosure.

4 Research design

4.1 Data sources

We use data on A-share listed firms in heavily polluting industries in the Shanghai and Shenzhen stock markets from 2015 to 2019. After excluding listed companies with abnormal financial and missing data, 2,409 sample data were finally collected. The environmental information disclosure index (EDI) is graded manually from annual reports, social responsibility reports, and official websites. Media attention data from China Research Data Service (CNRDS) and other data from the RESSET database. To eliminate the impact of outliers, all continuous variables were winsorized at 1% and 99% levels. Finally, Stata 15.0 was used for data processing and analysis.

4.2 Variable design

4.2.1 Explained variable

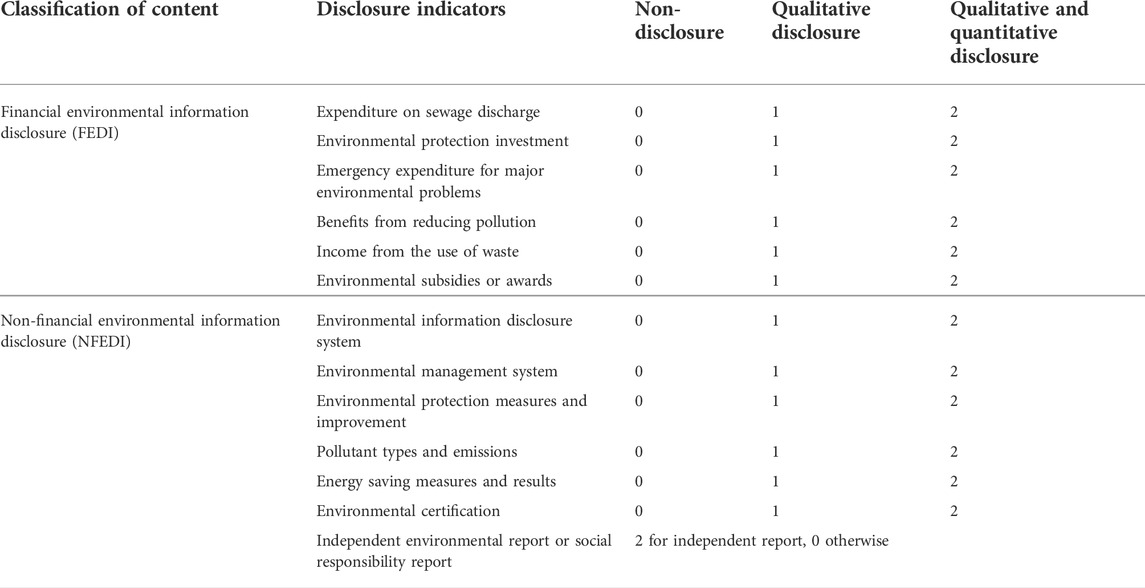

The explained variable is the environmental information disclosure index (EDI). Following Wu et al. (2015), this study uses content analysis, the most common method, to calculate EDI. EDI was calculated from 13 indicators, including 6 financial and 7 non-financial environmental information disclosure indicators. The full score for each indicator is 2 points, with 0 points for non-disclosure, 1 point for qualitative disclosure, and 2 points for both qualitative and quantitative disclosure. Table 1 lists the indicators and scoring rules.

TABLE 1. Environmental information disclosure indicators and scoring rules.

To avoid subjectivity, each item is given the same weight. The formulae of EDI, financial EDI (FEDI), and non-financial EDI (NFEDI) are listed below. A higher index value indicates a higher quality of environmental information disclosure.

where t represents the year, i represents the firm, j represents the disclosure indicator, and SCIDijt represents firm i’s score on indicator j in year t.

4.2.2 Explanatory variables

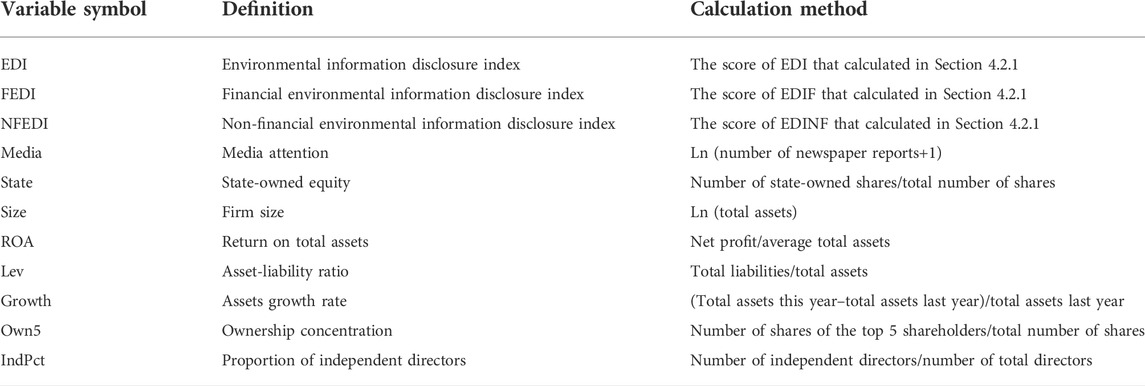

The explanatory variables were media attention and state-owned equity. Media attention can be measured by the number of network or newspaper media reports. This study chooses newspaper media reports because they are highly original, authentic, and authoritative (Zyglidopoulos et al., 2012). The natural logarithm of “number of newspaper reports + 1” is used to express the degree of media attention. The higher the value, the higher the media attention. Regardless of the tendency of the report, media reports will attract stakeholders' attention to the reported firms. Therefore, we do not distinguish the content of media reports further. Next, referring to Song and song (2015), state-owned equity is calculated by dividing the number of state-owned shares by the total number of shares.

4.2.3 Control variables

Following previous research (Lu and Abeysekera, 2014; Kouloukoui et al., 2019; Luo et al., 2019; Wasara and Ganda, 2019), our control variables include firm size, return on total assets, asset-liability ratio, assets growth rate, ownership concentration, and proportion of independent directors. The definition and calculation method of variables are shown in Table 2.

TABLE 2. Variable definition.

4.3 Estimation models and methods

We use the following estimation models for hypothesis testing:

As panel data were used, the Hausman test was conducted on all models; the resulting p values are all less than 0.01, rejecting the hypothesis of random effect. Therefore, this study adopts the fixed effect model to perform regression analysis with the above three models. Although the Hausman test supports the fixed effect model, it has a strict assumption that the explanatory variables do not correlate with the random disturbance term. It will lead to an endogeneity problem if this assumption is not met. Here, we assume that the models in this paper satisfied the assumption that the explanatory variables are exogenous and uncorrelated with the random disturbance term.

5 Empirical results

5.1 Descriptive statistics

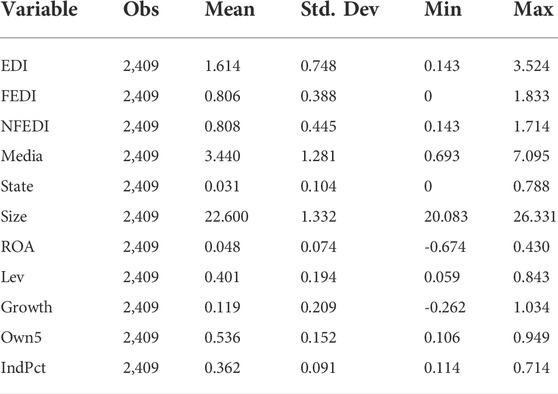

Table 3 shows the descriptive statistics. EDI has mean, maximum, and minimum values of 1.614, 3.524, and 0.143, respectively. This indicates that the level of environmental information disclosure in heavily polluting industries in China is much lower than the total score of 4. The maximum value of FEDI was 1.833 and slightly higher than that of NFEDI at 1.714. Generally, financial environmental information is easier to disclose quantitatively. However, the average FEDI is lower than that of NFEDI at 0.806 versus 0.808. Thus, firms may have a slightly stronger tendency to disclose non-financial environmental information.

TABLE 3. Descriptive statistics of variables.

Next, the mean, maximum, minimum values, and standard deviation of Media are 3.44, 7.095, 0.693, and 1.281, respectively. This indicates that while media pays high attention to firms on average, this attention varies substantially. Finally, the mean, maximum, and minimum values of state-owned equity are 0.031, 0.788, and 0, respectively. Thus, state shareholding in heavily polluting firms is relatively low and most of these firms are private.

5.2 Correlation test

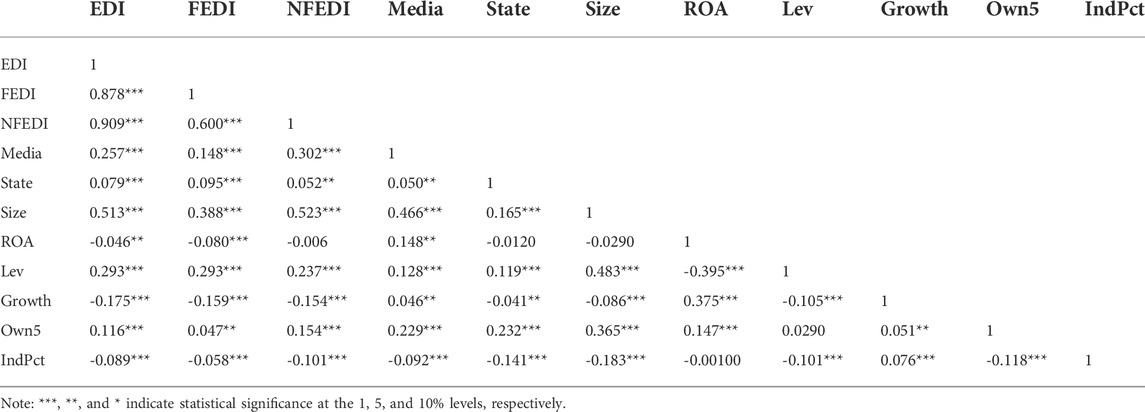

Pearson correlation coefficients of variables are shown in Table 4. Media is positively and significantly correlated with EDI, FEDI, and NFEDI, at the 1% level. This indicates that firms with high media attention have a higher level of environmental information disclosure, which preliminarily supports Hypothesis 1. Next, State has significantly positive correlations with EDI, FEDI, and NFEDI at the 1% level. Thus, firms with a higher proportion of state-owned equity have a higher level of environmental information disclosure, which preliminarily supports Hypothesis 2. Except for the explained variables, the maximum coefficient between all variables is 0.523. This indicates that there is no serious multicollinearity between variables and our model is suitable for further multiple regression analysis.

TABLE 4. Variable correlation coefficients.

5.3 Regression analysis

5.3.1 Media and EDI

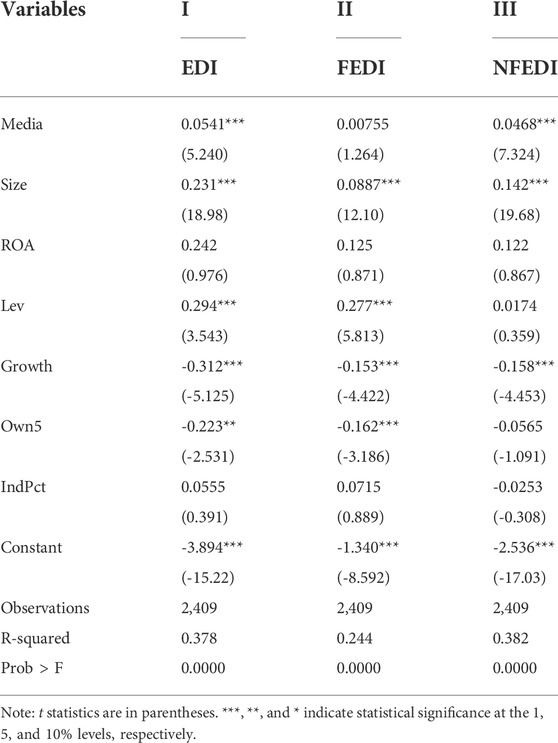

Columns I–III in Table 5 list the regression results of Media with EDI, FEDI, and NFEDI, respectively. The R2 of the three models are 0.378, 0.244, and 0.382, respectively, and the F statistic value is significant at the 1% level, indicating that the model fits well. According to Column I, Media is significantly and positively correlated with EDI at the 1% level. This indicates that media attention has a positive impact on environmental information disclosure. The more media attention a firm receives, the higher the level of its environmental disclosure. Thus, Hypothesis 1 is supported.

TABLE 5. Regression results of Media and EDI.

However, after classifying the content of environmental information, media attention only has a significant impact on NFEDI at the 1% level, but has no significant impact on FEDI. This indicates that the higher the media attention, the more firms are inclined to improve their disclosure of non-financial environmental information. One possible explanation is that firms with high media attention are under high social pressure, which prompts them to disclose more environmental information. However, such disclosure is a passive behavior; its purpose is not to improve the environmental responsibility and rather show off their environmental responsibility. Since financial information is difficult to fabricate in a short time, firms will respond to media attention by disclosing more non-financial information without substance.

5.3.2 State and EDI

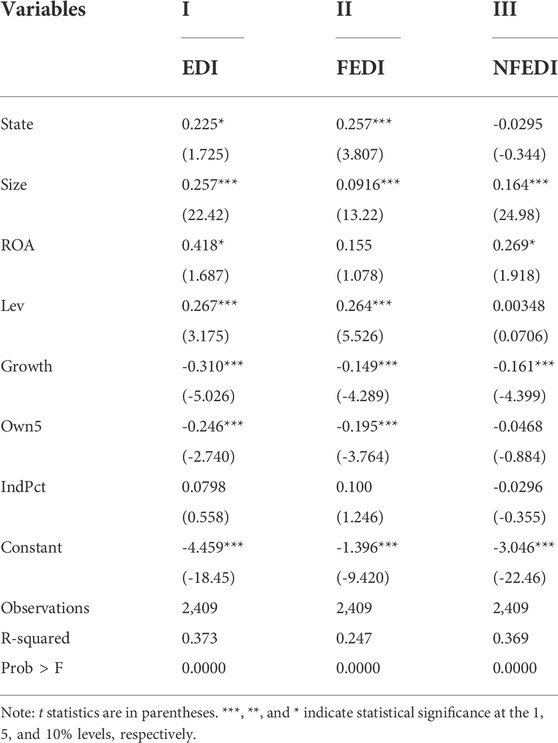

Columns I–III in Table 6 list the regression results of State with EDI, FEDI, and NFEDI, respectively. The R2 of the three models are 0.373, 0.247, and 0.369, respectively, and the F statistic value is significant at the 1% level, indicating that the model fits well. According to Column I, State is positively and significantly correlated with EDI at the 10% level, indicating that state-owned equity has a positive impact on environmental information disclosure. Firms with higher state-owned equity perform better at environmental information disclosure. Thus, Hypothesis 2 is supported.

TABLE 6. Regression results of State and EDI.

Comparing the content of environmental information in columns II and III shows that state-owned equity only has a positive and significant impact on financial environmental information disclosure at the 1% level; the impact on non-financial environmental information disclosure is not significant. This indicates that the higher the proportion of state-owned equity, the higher the disclosure level of financial environmental information. One possible explanation is that state-owned equity has governance effects on firms as the state-backed shareholders’ supervision internally pressures firms to bear social responsibilities, which internally drives firms’ pro-environmental behavior. Therefore, firms are more active in fulfilling their environmental responsibilities. Moreover, rather than just making superficial as under media attention, they will disclose more financial information that cannot be easily manipulated to distinguish themselves from other firms.

5.3.3 Media, state, and EDI

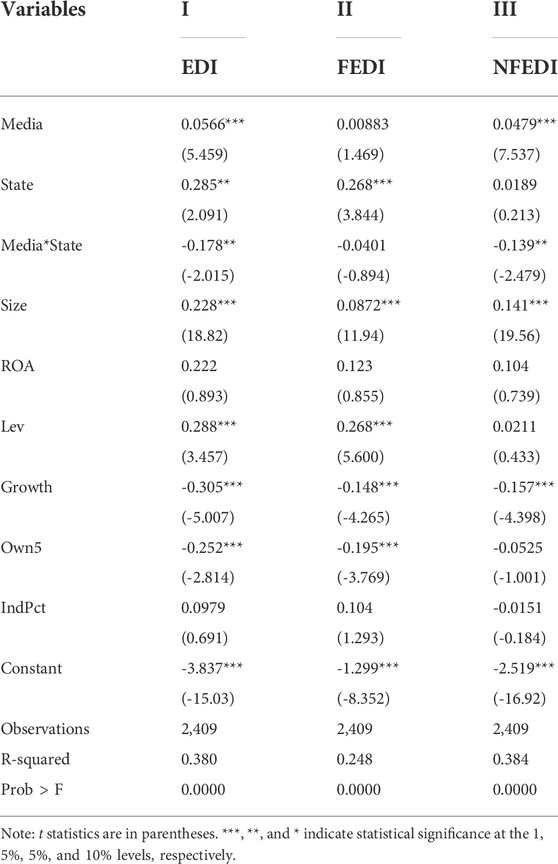

Table 7 incorporates Media, State, and their interaction into the same regression model for testing. To reduce the multicollinearity between State and State*Media as well as between Media and State*Media, Media and State have been centralized before the regression. The R2 of the three models are 0.380, 0.248, and 0.384, respectively, and the F statistic value is significant at 1% level, indicating that the model fits well. According to Column I, the coefficient of Media and State is positive and significant at the 1% and 5% levels, respectively. Meanwhile, the coefficient of State*Media is negative and significant at the level of 5%, implying a substitution effect between Media and State. That is, media attention is more likely to play a supervisory role when the proportion of state-owned equity is low. By contrast, a higher proportion of state-owned equity already plays a sufficient internal supervisory function; then, the additional effect of media attention may not be obvious. That is, high state-owned equity can weaken the positive effect of media attention on corporate environmental information disclosure. Thus, Hypothesis 3 is supported.

TABLE 7. Regression results of Media, State, and EDI.

Again, comparing the indicators of environmental information in columns II and III shows that the substitution effect of media attention and state-owned equity exists only in non-financial environmental information disclosure. This may be because during the measurement, recording, and disclosure of financial information, firms must comply with accounting standards. Consequently, the space for manipulation is limited. Meanwhile, the disclosure of non-financial environmental information is more flexible. This information includes written descriptions, such as policy introductions and system descriptions as well as charts or pictures; these can be easily controlled by firms. When the proportion of state-owned equity is low, firms that receive more media attention will more actively disclose environmental information under public pressure. However, as manipulating financial environmental information is difficult, firms will tend to avoid including monetized data that are difficult to fake. Instead, firms will choose to disclose more non-monetary environmental data that is descriptive, non-substantive, and easily manipulable. Therefore, the substitution effect of state-owned equity and media attention is mainly reflected in non-financial environmental information.

In addition, firm size, ROA, and leverage are positively related to EDI, indicating that firms with large size, strong profitability, and high leverage are more active in environmental disclosure. The empirical results are consistent with the existing literature. Large-scale companies have a higher quality of environmental information disclosure due to their rich experience (Lee, 2017). Profitable firms have more environmental governance capital, and thus, are more capable of providing a high level of environmental information disclosure (Qiu et al., 2016). Firms with high leverage also tend to disclose high-quality environmental information in order to reduce information asymmetry and capital cost (Park and Peng, 2013).

In contrast, growth rate and ownership concentration are negatively related to EDI, indicating that firms with rapid growth and concentrated ownership are more passive in environmental information disclosure. The explanation for the results is that fast-growing firms do not have enough energy for environmental management, and majority shareholders and management generally lack the enthusiasm to undertake environmental governance (Chen et al., 2021). The empirical results are consistent with our expectations.

5.4 Robustness test

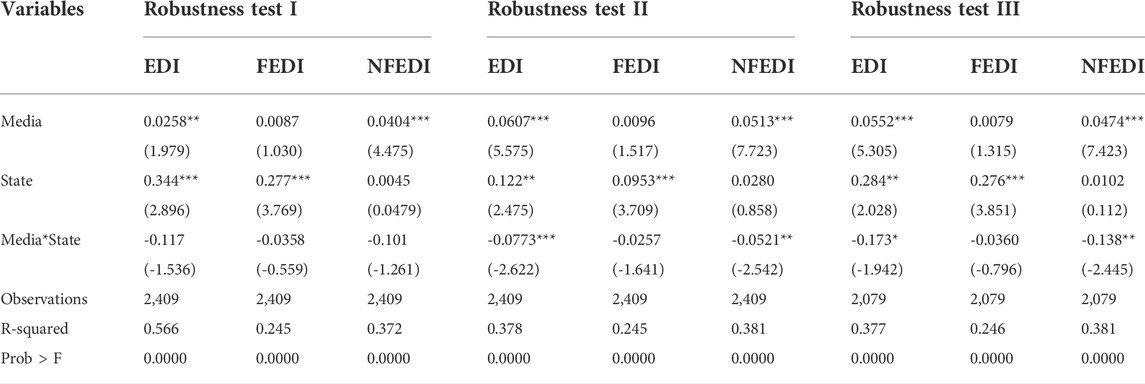

To ensure the reliability of our findings, we conducted the following robustness tests. First, the natural logarithm of “number of network reports + 1” was used to measure the explanatory variable Media Attention. Second, the dummy variable “whether state-owned enterprises” was used to replace the variable State-owned Equity. Finally, we performed repeatability test on the remaining samples after randomly deleting some samples. The results of the above tests showed that our findings qualitatively remained the same, indicating that our research is robust. The results of the robustness test are shown in Table 8.

TABLE 8. Robustness test.

6 Conclusion and limitations

6.1 Conclusion

This study empirically examines the influence of media attention and state-owned equity on environmental information disclosure using data on A-share heavily polluting firms in the Shanghai and Shenzhen stocks markets from 2015 to 2019. Our empirical results are as follows:

First, media attention can play an external supervisory role in corporate environmental information disclosure. However, this supervision only seems effective for non-financial environmental information and the effect on financial environmental information is not obvious. This may be because compared with financial environmental information, which is constrained by accounting standards, the disclosure of non-financial environmental information is more arbitrary, subjective, and manipulatable. Therefore, under external pressure such as media opinion and public pressure, firms will then choose to manipulate non-financial environmental information and disclose more information with no substantive content.

Second, state-owned equity plays an internal governance role in the disclosure of enterprise environmental information. Firms with a high proportion of state-owned equity have a higher level of environmental information disclosure, which is mainly reflected in financial environmental information. This shows that when firms are under the supervision of state shareholders, they will have the internal driving force of environmental responsibility and the urge to take more substantive measures to fulfill their environmental responsibilities, rather than just superficial efforts in text. The results showed the heterogeneity of the impact of media attention and state-owned equity, as different supervision mechanisms, on corporate environmental information disclosure.

Third, media attention and state-owned equity supervise corporate environmental responsibility externally and internally in firms, respectively; importantly, the two have a substitution effect on environmental information disclosure, which is mainly reflected in non-financial information disclosure. When the proportion of state-owned equity is low, supervision from state-owned shareholders is insufficient, and the level of environmental information disclosure is low. Then, when these firms receive high media attention, they will actively disclose environmental information, especially non-financial information, to improve their “green” image. Meanwhile, when the proportion of state-owned shares is high, the supervision from state-owned shareholders induces firms to pay more attention to environmental information and responsibilities. Therefore, greater media scrutiny has no apparent effect on improving the environmental information disclosure and cannot further strengthen the firms’ motivation regarding disclosures. The results imply the substitution effect of media attention and state-owned equity on environmental information disclosure.

6.2 Limitations

There are still some problems worth further discussion in this research, mainly in the following three aspects: Firstly, in terms of the influence mechanism of media attention and state-owned equity on corporate environmental information disclosure, in addition to the moderator factors discussed in this paper, there may be some mediating factors that need further study. Second, in terms of sample selection, the research samples in this paper only include polluting firms. Non-polluting firms should also undertake environmental responsibilities, and the study needs to expand research samples in the future. Third, the fixed effect model has several limitations, and it may not actually be the best method in this paper, which may cause endogeneity problems. Instrumental variables can be considered to deal with endogeneity issues in the future.

7 Suggestions

First, the government should allow media to fully leverage their external supervisory role, and use media to increase the pressure on firms to fulfill their environmental responsibilities. However, media reports should be authentic, reliable, independent, and fair. Furthermore, there should be more attention on firms’ practical and effective environmental responsibility behaviors/efforts to prevent them from greenwashing with empty slogans, and guide investors to pay attention to firms’ substantive environmental performance.

Second, state-owned equity is a suitable supervision mechanism for environmental information disclosure. Firms should give full play to the role of state-owned shareholders in corporate governance. State-owned firms should set an example of environmental responsibility and guide other firms to perform environmental responsibility better.

Third, environmental accounting standards should be further improved and environmental information disclosure standards should be clarified to improve the standardization of environmental information disclosures. Enhancing the comparability of environmental information across firms is vital to reduce discretion and subjectivity in environmental information disclosures.

Last, firms should improve the level of environmental information disclosures according to their own characteristics. Firms with a low level of state-owned equity should focus on improving the construction of environmental protection facilities, increasing R&D and pollution-control investments, and effectively improving their substantive environmental performance. Meanwhile, firms with a high degree of state-owned equity participation should work on publicizing their pro-environmental efforts and actively disclose their environmental management information through their official website or press conferences; this will help enhance the social recognition of their corporate environmental responsibility efforts.

Data availability statement

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding authors.

Author contributions

F L: writing, data collection and review QC: writing draft, conclusion, revision, English corrections, and Discussion L X: Data, analysis, review, improve, concept J W: Introduction, Methods and Data analysis LV: review, editing, discussion, implications.

Funding

This work was funded by the Natural Science Foundation of Fujian Province (No. 2021J01649) and the Social Science Foundation of Fujian Province (No. FJ 2021C085).

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Acar, E., Çalıyurt, K. T., and Zengin-Karaibrahimoglu, Y. (2021). Does ownership type affect environmental disclosure? Int. J. Clim. Chang. Strateg. Manag. 13, 120–141. doi:10.1108/IJCCSM-02-2020-0016

Acar, M., and Temiz, H. (2020). Empirical analysis on corporate environmental performance and environmental disclosure in an emerging market context: Socio-political theories versus economics disclosure theories. Int. J. Emerg. Mark. 15, 1061–1082. doi:10.1108/IJOEM-04-2019-0255

Aerts, W., Cormier, D., and Magnan, M. (2008). Corporate environmental disclosure, financial markets and the media: An international perspective. Ecol. Econ. 64 (3), 643–659. doi:10.1016/j.ecolecon.2007.04.012

Baldini, M., Maso, L. D., Liberatore, G., Mazzi, F., and Terzani, S. (2018). Role of country-and firm-level determinants in environmental, social, and governance disclosure. J. Bus. Ethics 150 (1), 79–98.doi:10.1007/s10551-016-3139-1

Barbu, E. M., Dumontier, P., Feleagă, N., and Feleagă, L. (2014). Mandatory environmental disclosures by companies complying with iass/ifrss: The cases of France, Germany, and the UK. Int. J. Account. 49 (2), 231–247. doi:10.1016/j.intacc.2014.04.003

Bhattacharyya, A., and Rahman, M. L. (2019). Mandatory CSR expenditure and firm performance. J. Contemp. Account. Econ. 15 (3), 100163. doi:10.1016/j.jcae.2019.100163

Brammer, S., and Pavelin, S. (2008). Factors influencing the quality of corporate environmental disclosure. Bus. Strategy Environ. 17 (2), 120–136. doi:10.1002/bse.506

Calza, F., Profumo, G., and Tutore, I. (2016). Corporate ownership and environmental proactivity. Bus. Strategy Environ. 25 (6), 369–389. doi:10.1002/bse.1873

Chen, S., Wang, Y., Albitar, K., and Huang, Z. (2021). Does ownership concentration affect corporate environmental responsibility engagement? The mediating role of corporate leverage. Borsa Istanb. Rev. 21, 13–24. doi:10.1016/j.bir.2021.02.001

Clarkson, P. M., Li, Y., Richardson, G. D., and Vasvari, F. P. (2008). Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Account. Organ. Soc. 33 (4-5), 303–327. doi:10.1016/j.aos.2007.05.003

D'Amico, E., Coluccia, D., Fontana, S., and Solimene, S. (2016). Factors influencing corporate environmental disclosure. Bus. Strategy Environ. 25 (3), 178–192. doi:10.1002/bse.1865

Delgado-Márquez, B. L., Pedauga, L. E., and Cordón-Pozo, E. (2017). Industries regulation and firm environmental disclosure: A stakeholders’ perspective on the importance of legitimation and international activities. Organ. Environ. 30 (2), 103–121. doi:10.1177/1086026615622028

Guo, Z., and Lu, C. (2020). Corporate environmental performance in China: The moderating effects of the media versus the approach of local governments. Int. J. Environ. Res. Public Health 18 (1), 150. doi:10.3390/ijerph18010150

Huang, J., Li, Y., and Duan, Z. X. (2020). Media attention, property rights nature and enterprise targeted poverty alleviation. East China Economic Management. Anhui, 112–120. (In Chinese). doi:10.19629/j.cnki.34-1014/f.200101002

Kong, G., Kong, D., and Wang, M. (2020). Dose media attention affect firms’ environmental protection efforts? Evidence from China. Singap. Econ. Rev. 65 (03), 577–600. doi:10.1142/s021759081741003x

Kouloukoui, D., Sant'Anna, Â. M. O., da Silva Gomes, S. M., de Oliveira Marinho, M. M., de Jong, P., Kiperstok, A., et al. (2019). Factors influencing the level of environmental disclosures in sustainability reports: Case of climate risk disclosure by Brazilian companies. Corp. Soc. Responsib. Environ. Manag. 26 (4), 791–804. doi:10.1002/csr.1721

Kuo, L., and Chen, V. Y. J. (2013). Is environmental disclosure an effective strategy on establishment of environmental legitimacy for organization? Manag. Decis. 51 (7), 1462–1487. doi:10.1108/MD-06-2012-0395

Lee, K. H. (2017). Does size matter? Evaluating corporate environmental disclosure in the Australian mining and metal industry: A combined approach of quantity and quality measurement. Bus. Strategy Environ. 26 (2), 209–223. doi:10.1002/bse.1910

Li, Z. (2018). Will inconsistent environmental disclosure patterns be rejected by information users? World Econ. (12), 167–188. (In Chinese) Available at: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFDLAST2019&filename=SJJJ201812009&uniplatform=NZKPT&v=NxgPt93Va-0cuVRiJ3IhzudV7tRwM2nfqyYOOcrQoPqW3dB1UeNJ6nw9dEBpF0jc.

Lin, S., Chen, F., and Wang, L. (2020). Identity of multiple large shareholders and corporate governance: Are state-owned entities efficient MLS? Rev. Quant. Finan. Acc. 55 (4), 1305–1340. doi:10.1007/s11156-020-00875-z

Liu, X., and Zhang, C. (2017). Corporate governance, social responsibility information disclosure, and enterprise value in China. J. Clean. Prod. 142, 1075–1084. doi:10.1016/j.jclepro.2016.09.102

Liu, Y., Failler, P., and Chen, L. (2021). Can mandatory disclosure policies promote corporate environmental responsibility? Quasi-natural experimental research on China. Int. J. Environ. Res. Public Health 18 (11), 6033. doi:10.3390/ijerph18116033

Lu, Y., and Abeysekera, I. (2014). Stakeholders' power, corporate characteristics, and social and environmental disclosure: Evidence from China. J. Clean. Prod. 64, 426–436. doi:10.1016/j.jclepro.2013.10.005

Luo, W., Guo, X., Zhong, S., and Wang, J. (2019). Environmental information disclosure quality, media attention and debt financing costs: Evidence from Chinese heavy polluting listed companies. J. Clean. Prod. 231, 268–277. doi:10.1016/j.jclepro.2019.05.237

Ma, Y., Zhang, Q., Yin, Q., and Wang, B. (2019). The influence of top managers on environmental information disclosure: The moderating effect of company’s environmental performance. Int. J. Environ. Res. Public Health 16 (7), 1167. doi:10.3390/ijerph16071167

Mahjoub, L. B., and Amara, I. (2020). The impact of cultural factors on shareholder governance and environmental sustainability: An international context. World J. Sci. Technol. Sustain. Dev. 17 (4), 367–385. doi:10.1108/wjstsd-06-2020-0060

Meng, X., Zeng, S., Xie, X., and Zou, H. (2019). Beyond symbolic and substantive: Strategic disclosure of corporate environmental information in China. Bus. Strategy Environ. 28 (2), 403–417. doi:10.1002/bse.2257

Moroney, R., Windsor, C., and Aw, Y. T. (2012). Evidence of assurance enhancing the quality of voluntary environmental disclosures: An empirical analysis. Account. Finance 52 (3), 903–939. doi:10.1111/j.1467-629X.2011.00413.x

Park, S. K., and Peng, W. (2013). Factors affecting corporate environmental disclosure in China. globalbusinessadministrationreview. 10 (3), 111–131. doi:10.17092/jibr.2013.10.3.111

Qiu, Y., Shaukat, A., and Tharyan, R. (2016). Environmental and social disclosures: Link with corporate financial performance. Br. Account. Rev. 48 (1), 102–116. doi:10.1016/j.bar.2014.10.007

Radu, C., and Francoeur, C. (2017). Does innovation drive environmental disclosure? A new insight into sustainable development. Bus. Strategy Environ. 26 (7), 893–911. doi:10.1002/bse.1950

Rupley, K. H., Brown, D., and Marshall, R. S. (2012). Governance, media and the quality of environmental disclosure. J. Account. Public Policy 31 (6), 610–640. doi:10.1016/j.jaccpubpol.2012.09.002

Song, Z. J., and Sang, Q. L. (2015). State-owned equity, social capital and bank financing convenience: Experience evidence from Chinese private holding listed companies. Commer. Res. (06), 138–145. (In Chinese). doi:10.13902/j.cnki.syyj.2015.06.020

Utomo, M. N., Wahyudi, S., Muharam, H., and Taolin, M. L. (2018). Strategy to improve firm performance through operational efficiency commitment to environmental friendliness: Evidence from Indonesia. Organ. Mark. Emerg. Econ. 9 (1), 62–85. doi:10.15388/omee.2018.10.00004

Wasara, T. M., and Ganda, F. (2019). The relationship between corporate sustainability disclosure and firm financial performance in johannesburg stock exchange (JSE) listed mining companies. Sustainability 11 (16), 4496. doi:10.3390/su11164496

Wu, J. F., Ye, C. G., and Liu, M. (2015). Environmental performance, political correlation and environmental information disclosure: Empirical evidence from heavy polluting industries in A-shares in Shanghai. Journal of Shanxi University of Finance and Economics. Shanxi, 99–110. (In Chinese). doi:10.13781/j.cnki.1007-9556.2015.07.009

Xu, F., Ji, Q., and Yang, M. (2021). The pitfall of selective environmental information disclosure on stock price crash risk: Evidence from polluting listed companies in China. Front. Environ. Sci. 178. doi:10.3389/fenvs.2021.622345

Xue, J., He, Y., Liu, M., Tang, Y., and Xu, H. (2021). Incentives for corporate environmental information disclosure in China: Public media pressure, local government supervision and interactive effects. Sustainability 13, 10016. doi:10.3390/su131810016

Yang, G. Q., Du, Y. F., and Liu, Y. Z. (2020). Business performance, media attention and environmental information disclosure. Bus. Manag. J. (03), 55–72. (In Chinese). doi:10.19616/j.cnki.bmj.2020.03.004

Zhang, T., Gu, L., and Wang, J. J. (2022). State-owned capital and corporate social responsibility of private-holding companies: Evidence from China. Account. Finance . (ahead-of-print). doi:10.1111/acfi.12931

Zhou, Y., Luo, L., and Shen, H. (2022). Community pressure, regulatory pressure and corporate environmental performance. Aust. J. Manag. 47 (2), 368–392. doi:10.1177/03128962211017172

Keywords: media attention, sustainable development, state-owned equity, environmental information, green recovery

Citation: Long F, Chen Q, Xu L, Wang J and Vasa L (2022) Sustainable corporate environmental information disclosure: Evidence for green recovery from polluting firms of China. Front. Environ. Sci. 10:1019499. doi: 10.3389/fenvs.2022.1019499

Received: 15 August 2022; Accepted: 07 September 2022;

Published: 29 September 2022.

Edited by:

Muhammad Zahid Rafique, Center for Economic Research, Shandong University, ChinaReviewed by:

Ahmed Samour, Near East University, CyprusMihaela Simionescu, Romanian Academy, Romania

Grzegorz Mentel, Rzeszów University of Technology, Poland

Copyright © 2022 Long, Chen, Xu, Wang and Vasa. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Qin Chen, Y2hlbnFpbjA2MjBAMTI2LmNvbQ==; László Vasa, bGFzemxvLnZhc2FAaWZhdC5odQ==